Abstract

Introduction:

For the Commonwealth Games 2010, Jai Prakash Narayan Apex Trauma Centre (JPNATC) of India had been directed by the Director General Health Services and Ministry of Health and Family Welfare, Government of India, to set up a specialized unit for the definitive management of the injured/unwell athletes, officials, and related personnel coming for the Commonwealth Games in October 2010. The facility included a 20-bedded fully equipped ward, six ICU beds with ventilator capacity, one very very important person observation area, one perioperative management cubicle, and one fully modular and integrated operating room.

Objective:

The objective of this study was to calculate the cost of disaster facility at JPNATC, All India Institute of Medical Sciences, New Delhi.

Methodology:

Traditional (average or gross) costing methodology was used to arrive at the cost for the provisioning of these services by this facility.

Results:

The annual cost of providing services at disaster facility at JPNATC, New Delhi, was calculated to be INR 61,007,334.08 (US$ 983,989.258) while the per hour cost was calculated to be INR 7061.03 of the total cost toward the provisioning of services by disaster facility where 26% was the capital cost and 74% was the operating cost. Human resource caters to maximum chunk of the expenditures (47%).

Conclusion:

The results of this costing study will help in the future planning of resource allocation within the financial constraints (US$ 1 = INR 62 in the year 2013).

Keywords: Cost centers, costing, disaster, support services, trauma care

INTRODUCTION

Disasters have inflicted a heavy cost on human, material, and physical resources. A comprehensive review of the literature has revealed that the development of disaster management strategies such as preparedness must be undertaken before the event strikes.[1]

Hospital preparedness is crucial to any disaster response system.[2] Each hospital should have an emergency preparedness plan to deal with mass casualties and should be manned by trained health managers.

In some developing countries with middle-income economies where there has not been a reference unit cost and/or standard hospital costing system for medical services, individual hospitals conduct unit cost analysis employing different methods. Different methods result in different calculation outcomes.[3]

The cost of operating disaster facility depends on the resources being consumed. Concept of having disaster facility in a hospital is unique, and other hospitals can also prepare themselves to handle disaster at any point of time. Therefore, it is important to understand the various cost centers and costs involved in having disaster facility so that limited resources in a developing country such as India can be efficiently utilized.

Determining the actual cost of care in trauma centers has remained difficult. Trauma services are especially vulnerable to cost pressures because their payer mix is often marginal and the care provided is extremely resource intensive.[4] By calculating the cost of disaster facility at an apex trauma center, this study will give an insight into the amount of resources needed to provide services by such facility.

Cost centers in the study are as follows:

-

Capital cost

- Building cost

- Cost of equipment.

-

Operating cost

- Workforce

- Material and supplies

- Support services (Central Sterile Supply Department [CSSD], laundry, manifold, laboratory, and blood bank)

- Engineering maintenance cost

- Biomedical waste management cost.

METHODOLOGY

This study was observational and descriptive in nature. The methodology used to arrive at the cost of the disaster facility from April 2012 to March 2013 was traditional (syn-average or gross) costing. Cost was calculated under two heads as capital and operating costs. Major cost centers included in the study are detailed above. This study was carried out in the disaster facility of Jai Prakash Narayan Apex Trauma Centre (JPNATC), All India Institute of Medical Sciences, New Delhi, from April 2012 to March 2013 after getting approval from the concerned authorities.

Capital assets

For capital assets, the first replacement cost was calculated by multiplying procurement cost with cost inflation multiplication factor (cost inflation index for 2012–2013/cost inflation index of procurement year). Consequently, the annualized method of depreciation (suggested by the World Health Organization)[5] was used to calculate the annual cost by dividing replacement cost of the asset in the years 2012–2013 by the annualization factor.

Using the given methodology, annualized building (per m2) and equipment cost for disaster facility was calculated. Following that, building cost of support services was calculated and apportioned to disaster facility.

Records of the Expenditure Finance Committee were reviewed for building cost. Similarly, annualized equipment cost was calculated for support services. Indent books of user department were reviewed for consumables and nonconsumables. Cost of the same was retrieved from the stores department. Apportioning for equipment of disaster facility was not done since all the equipment were dedicated for disaster facility. Annualized building and equipment cost of support services was apportioned to disaster facility on the basis of workload.

The formula[5] for calculating the annualization factor is (1/r) × [1 − 1/(1 + r) × n].[5] (Equation 1)

Where, r is the real interest rate, which is calculated by the following formula:

([1 + nominal interest rate)/(1 + annual inflation) −1]

Nominal interest rate is the prevailing national bank savings rate for the year 2011

n is the number of years of life (100 years and 10 years [15 years] for building, machinery, and equipment (fixed), respectively) Equation-1.

Operating cost

Records of disaster facility were studied to understand its functioning and the support services utilized there. Information pertaining to floor area of disaster facility and support services was obtained from records of the engineering department. An unstructured interview was held with staff working in the disaster facility.

Maintenance cost for engineering services was calculated by multiplying the floor area of the disaster ward with engineering maintenance cost per square meter of the building. Support services engineering maintenance cost was calculated and apportioned to disaster unit on the basis of workload. Building maintenance cost was taken from the accounts department. To calculate the time devoted by various categories of hospital staff for providing services in disaster facility, an unstructured interview was carried out to apportion their salary. The salary of employees was taken from the accounts section.

To take into account the oscillation in consumption of consumables in relation to seasonal variation, cost of consumables for whole 1 year was taken. It was assumed that consumables indented by the staff in the year of study were consumed in that particular year. The actual quantity as per indent book was considered, and cost of the same was taken from rate contracts of All India Institute of Medical Sciences.

Average monthly CSSD load and disaster facility load (sets, drums, and linen processed) for CSSD were calculated by taking the average of the values for the 12-month period. The average number of drums, sets, and linen processed in one cycle was calculated from the CSSD records and through an interview with the CSSD manager. Thereafter, the total number of steam and ethylene oxide sterilization cycles run for disaster facility was calculated. Average monthly laundry load and disaster facility load (in kg) for laundry were calculated by taking the average for 12-month period.

The proportion of disaster facility terminal manifold units to the total terminal units of medical gases, compressed air, and vacuum was used as an apportioning criterion for various costs (capital and operating costs). Average monthly blood bags produced by blood bank and disaster facility load (number of blood bags consumed per month) were calculated by taking the average of the values for 12-month period. Average monthly laboratory investigation load on JPNATC laboratory and disaster facility load (number of laboratory investigations done) were calculated by taking the average of the values for 12-month period.

With regard to biomedical waste (BMW)/m2, the cost of biomedical waste management was calculated and then apportioned to disaster facility. Operating cost for different support services was taken as per the contract agreement executed between All India Institute of Medical Sciences and an outsourced agency. Microsoft Excel software was used for analysis.

RESULTS AND ANALYSIS

For the Commonwealth Games 2010, JPNATC was directed by the Director General Health Service and Ministry of Health and Family Welfare, Government of India, to set up a specialized facility for the definitive management of the injured/unwell athletes, officials, and related personnel who came for the Commonwealth Games in October 2010. The facility included a 20-bedded fully equipped ward, six ICU beds with ventilator capacity, one very very important person observation area, one perioperative management cubicle, and one fully modular and integrated operating room. JPNATC spreads over an area of 20,600 m2 and has more than 200 beds to provide emergency trauma care. All the cost estimates were calculated for the financial year April 2012–March 2013. The annualization factor for capital assets was calculated to be 38.5, 8.82, and 12.53 for building, machinery, and equipment (fixed), respectively. Annualized building and engineering maintenance cost of JPNATC was calculated to be INR 1761 and 3784.94/m2, respectively.

Cost of disaster facility

Total capital cost

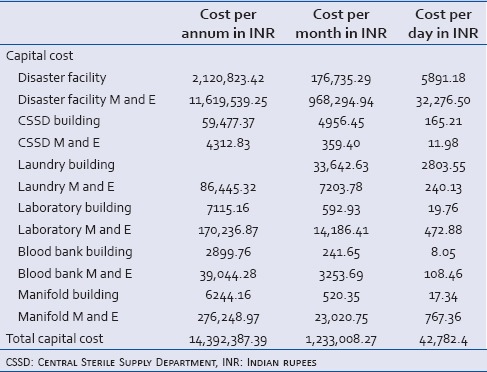

Annualized total capital cost of a disaster facility for 2012–2013 was calculated to be INR 14,392,387.39 [Table 1].

Table 1.

Capital costing of a disaster facility at Jai Prakash Narayan Apex Trauma Centre from April 2012 to March 2013

Cost of support services

Cost of Central Sterile Supply Department

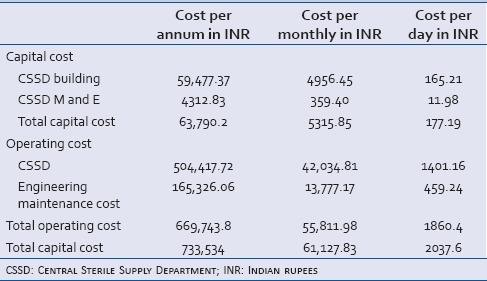

Total annualized cost of CSSD building and equipment apportioned to disaster facility for 2012–2013 was calculated to be INR 59,477.37 and INR 4312.2, respectively. Operating cost of CSSD for 2012–2013 apportioned to disaster facility was found to be INR 504,417.72.

Disaster facility load formed 14.28% of the total CSSD load. CSSD maintenance cost apportioned to the disaster facility was calculated to be INR 165,326.06. Annualized total cost of CSSD was INR 733,534.00 [Table 2].

Table 2.

Total cost of Central Sterile Supply Department in Indian rupees

Cost of blood bank

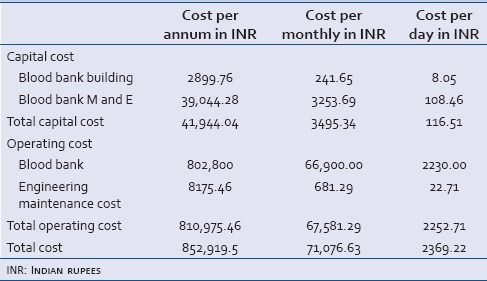

Total annualized cost of blood bank and equipment apportioned to disaster facility for 2012–2013 was calculated to be INR 2900 and INR 39,044.28, respectively. Operating cost of blood bank for 2012–2013 was found to be INR 802,800.

Disaster facility load on blood bank amounts to 1% of the total blood bank load. Annualized capital and operating cost apportioned to the disaster facility for 2012–2013 was calculated to be INR 41,944.04 and INR 802,800, respectively. Blood bank maintenance cost apportioned to the disaster facility was calculated to be INR 8175.46. Annualized total cost of blood bank was INR 852,919.5 [Table 3].

Table 3.

Total cost of blood bank

Cost of laboratory

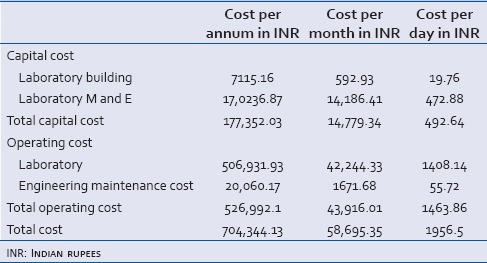

Total annualized cost of laboratory building and equipment apportioned to disaster facility for 2012–2013 was calculated to be INR 7115.16 and INR 170,236.87, respectively. Operating cost for 2012–2013 was found to be INR 506,931.93.

Disaster facility formed 2% of the total laboratory load. Annualized capital and operating cost apportioned to the disaster facility for 2012–2013 was calculated to be INR 177,352.03 and INR 506,931.93, respectively. Laboratory maintenance cost apportioned to the disaster facility was calculated to be INR 20,060.17. Annualized total cost of laboratory was INR 704,344.13 [Table 4].

Table 4.

Total cost of laboratory in Indian rupees

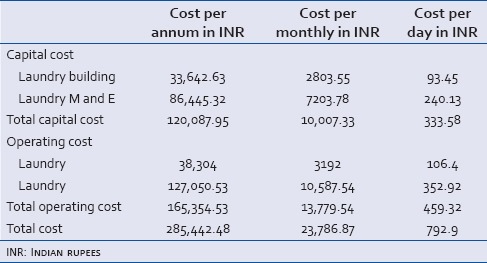

Cost of laundry

Total annualized cost of laundry building and equipment apportioned to disaster facility for 2012–2013 was calculated to be INR 33,642.63 and INR 86,445.32, respectively. Disaster facility load formed 7% of the total laundry load; therefore, 7% of the total laundry cost was apportioned to disaster facility. Annualized capital and operating cost apportioned to the disaster facility for 2012–2013 was calculated to be INR 120,087.95 and INR 38,304, respectively. Laundry engineering maintenance cost apportioned to the disaster facility was calculated to be INR 127,050.53. Annualized total cost of laundry was INR 285,442.48 [Table 5].

Table 5.

Total cost of laundry in Indian rupees

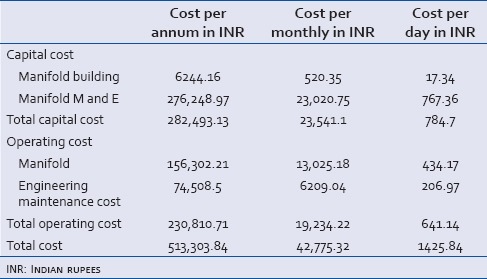

Cost of manifold

Disaster facility manifold terminal units formed only 6% of the total manifold terminal units installed at JPNATC. Total annualized cost of manifold building and equipment apportioned to the disaster facility for 2012–2013 was calculated to be INR 6244.16 and INR 276,248.97, respectively. Annualized capital and operating cost apportioned to the facility was found to be INR 156,302.21. Manifold engineering maintenance cost apportioned to the disaster facility was calculated to be INR 74,508.50. Annualized total cost of manifold was INR 513,303.84 [Table 6].

Table 6.

Total cost of manifold in Indian rupees

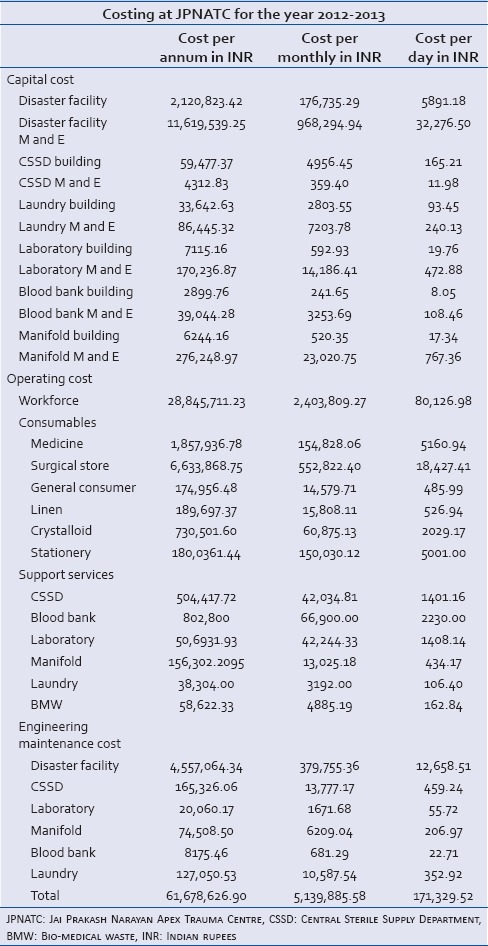

Total cost of disaster unit

The detailed information on the capital and operating costs of the disaster unit is shown in Table 7. Annual and monthly cost of providing disaster facility services at JPNATC, New Delhi, was calculated to be INR 61,678,626.92 and INR 5,139,885.58, respectively. The total cost per day was calculated to be INR 171,329.52.

Table 7.

Costing of a disaster facility at Jai Prakash Narayan Apex Trauma Centre

This study at JPNATC was conducted to gain an insight regarding the quantity of resources being dedicated toward the provisioning of services at disaster facility at the apex tertiary care trauma center in the country. The results of this costing will act as rough estimates for planning such similar services. Of the total cost, 24% was the capital cost while 76% was the operating cost. The disaster unit expenditure mainly comprised three major components contributing to more than 90% of the cost, i.e., workforce, capital cost, and cost of consumables

Activity-based costing and microcosting are required for identifying and costing of every resource consumed in providing a “unit of care.” It is challenging to determine the accurate cost of an activity in health care setup because of the complexity of health-care delivery itself. Existing costing systems, which measure the costs of individual departments, services, or support activities, often encourage the shifting of costs from one type of service or provider to another, or to the payer or consumer. The micromanagement of costs at the individual organizational unit level does little to reduce the total cost or improve value.[6]

It is evident from literature that spending more on early detection and better diagnosis of disease spares patients from suffering and often leads to less complex and less expensive care later. If diagnostics and treatment are provided to patients in a required time, health of patient can be prevented from deteriorating and also will lower the costs by reducing the resources required for the care. Health-care providers can utilize medical staff, equipment, facilities, and administrative resources far more efficiently, streamlining the path of patients through the health system, and selecting treatment that improve outcomes and eliminating services that are not required.[7]

It is obvious from literature that indirect costs are rising in health-care management. One of the solutions is to share such services to cut down the costs. The setting up of a facility of such magnitude will help in sharing costs among health-care providers within the public sector ambit.[8]

DISCUSSION

The study was carried out at the disaster facility of JPNATC, All India Institute of Medical Sciences, from 2012 to 2013 after obtaining approval from the concerned authorities. This study was observational and descriptive in nature.

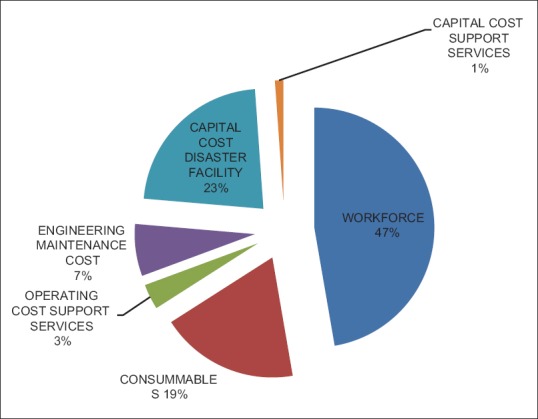

The study at JPNATC was conducted to have an idea regarding the amount of resources being devoted toward the provisioning of services for disaster facility at the apex tertiary care trauma center in the country. The results of this costing can be used for planning a similar disaster facility in the near future by any other trauma center in our country and it would act as rough estimates for planning. The study gives an insight into various costs involved in setting up and operating a disaster facility of such magnitude. The knowledge regarding costs involved in various cost centers help to apportion the budget allocated. It is evident from this study that cost for human resources is maximum at 47% and utilization of the same needs to be evaluated. Capital cost of the disaster facility amounts to 23% capital cost of support services that take 1% of the total cost. Consumables accounts for 19% share of the cost. Engineering maintenance cost averages to 7% and operating cost for support averages to 3%. Since the disasters occur in an unpredictable frequency at irregular intervals and to optimally utilize the services (infrastructure, equipment, and human resource), it is necessary that these resources are utilized for patient care services at times other than disasters. This has to be planned in association with the clinicians. The facility has to be functional at all times and be ready with staff and equipment to run the facility irrespective of the number of disasters that may be catered to on any day. This exercise will require standard budgetary allocation apart from variations that may occur at times. One way of optimizing human resource is to train them who will subsequently train others. This will lead to capacity building. Moreover, developing standard operating procedures for various procedures can help in reducing costs, as variations in procedures consume time and money [Figure 1].

Figure 1.

Cost breakdown for disaster facility

In one of the studies conducted in the year 2011 in New Delhi, it was found that human resource caters to a maximum chunk of the expenditure.[9]

At present, there is no similar facility in the country at the tertiary level that caters to disasters in such a way. Emergency care centers/trauma centers are being established, but, currently, no data are available for disaster facilities.

One of the major weaknesses of the study was nonavailability of records. With regard to workforce, only directly involved workforce was included. Administrative workforce and human resource indirectly involved were not considered. The reason for not considering indirectly involved workforce was lack of data to keep the log of activity done by them. In the study, major cost centers were included, as time and resources were the constraints. Land cost was excluded from the study since the land where the trauma center is located was donated by the New Delhi government.

The cost of the departments which were excluded from the study would have an insignificant impact on the final outcome of this study. However, this costing of disaster facility is an underestimation of the real cost. An additional drawback of the study was allied to the traditional or average costing methodology used. However, it is not an easy task to do costing using activity-based methodology as for that, data and activity incurred need to be recorded.

This disaster facility is now well recognized within New Delhi and NCR region as the premier disaster care facility. Disasters are now directed to this facility. That apart, cases which may not fall under the definition of disasters are also at times provided admission in one of these beds in case of providing emergency treatment and are subsequently transferred to the regular beds of the unit concerned. This facility not only caters to New Delhi and NCR but also to various other states of North India. Moreover, trained human resource are also sent to other places at times of disaster. This center provides distance training and training of trainers for hospitals all over the country.

The study highlights the need for a management approach to emergency care infrastructure development. Often, there is neither ownership nor demand from clinical departments for facilities to tackle disasters. In addition, the structural and process requirements for disaster preparedness are better handled by hospital administrators as this requires a holistic view and coordination of multiple departments. It is crucial that the hospital administrators address this lacuna in their planning. It would be appropriate for the management to proactively take a lead in co-coordinating the requirements from various departments such as anesthesia, critical care, emergency medicine, orthopedics, and neurosurgery for both structural and human resource requirements. The budgetary requirements could also be better projected by the hospital management and also in terms of justifying a facility that is required only occasionally, but with all resources to be made available optimally when the need arises. This would also require further planning to keep the staff engaged and prepared during the other days of the year. Through this paper, the costing aspects of such a facility have been deliberated upon to assist planning any similar such facility in hospitals.

Financial support and sponsorship

Nil.

Conflicts of interest

There are no conflicts of interest.

REFERENCES

- 1.Ngcamu ND, Dorasamy N. Disaster preparedness by local government: A case study of foreman and Kennedy road informal settlements in the Ethekwini municipality. Corp Ownership Control. 2011;8:352–65. [Google Scholar]

- 2.Guidelines for Hospital Emergency Preparedness Planning. GOI-UNDP DRM Programme. National Disaster Management Division. Ministry of Home Affairs. Government of India. 2002-2008 [Google Scholar]

- 3.Riewpaiboon A, Malaroje S, Kongsawatt S. Effect of costing methods on unit cost of hospital medical services. Trop Med Int Health. 2007;12:554–63. doi: 10.1111/j.1365-3156.2007.01815.x. [DOI] [PubMed] [Google Scholar]

- 4.Taheri PA, Wahl WL, Butz DA, Iteld LH, Michaels AJ, Griffes LC, et al. Trauma service cost: The real story. Ann Surg. 1998;227:720–4. doi: 10.1097/00000658-199805000-00012. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5.Shepard DS, Hodgkin D, Anthony Y. Analysis of Hospital Costs: A Manual for Managers. Geneva: World Health Organization; 1998. pp. 1–74. [Google Scholar]

- 6.Youell N, Catalli S, Papparotto R, Bachini P, Schmidt PJ, Alle C. Profitability and Cost Management in Healthcare. Oracle White Paper. 2015. [Last accessed on 2016 Oct 09]. Available on http://www.oracle.com/us/industries/healthcare/042343.pdf .

- 7.Berger SH. 10 ways to improve healthcare cost management. Healthc Financ Manage. 2004;58:76–80. [PubMed] [Google Scholar]

- 8.Christianson JB, Trude S. Managing costs, managing benefits: Employer decisions in local health care markets. Health Serv Res. 2003;38(1 Pt 2):357–73. doi: 10.1111/1475-6773.00120. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9.Siddharth V, Kumar S, Vij A, Gupta SK. Cost analysis of operation theatre services at an apex tertiary care trauma centre of India. Indian J Surg. 2015;77(Suppl 2):530–5. doi: 10.1007/s12262-013-0908-2. [DOI] [PMC free article] [PubMed] [Google Scholar]