Abstract

The use of health insurance schemes in financing healthcare delivery and to minimize the poverty gap is gaining considerable recognition among the least developed and resource challenged countries around the world. With the implementation of the socialized health insurance scheme, Ghana has taken the lead in Sub-Saharan Africa and now working out further strategies to gain universal coverage among her citizenry. The primary goal of this study is to explore the spatial relationship between the residential homes and demographic features of the people in the Barekese subdistrict in Ghana on the probability to enroll the entire household unit in the National Health Insurance Scheme (NHIS). Household level data were gathered from 20 communities on the enrollment status into the NHIS alongside demographic and socioeconomic indicators and the spatial location of every household that participated in the study. Kulldorff’s purely spatial scan statistic was used to detect geographic clusters of areas with participatory households that have either higher or lower enrollment patterns in the insurance program. Logistic regression models on selected demographic and socioeconomic indicators were built to predict the effect on the odds of enrolling an entire household membership in the NHIS.

Three clusters significantly stood out to have either high or low enrollment patterns in the health insurance program taking into accounts the number of households in those sub-zones of the study region. Households in the Cluster 1 insurance group have very high travel expenses compared to their counterparts in the other idenfied clusters. Travel cost and time to the NHIS registration center to enroll in the program were both significant predictors to participation in the program when controlling for cluster effect. Residents in the High socioeconomic group have about 1.66 [95% CI: 1.27-2.17] times the odds to enroll complete households in the insurance program compared to their counterparts in the Low socioeconomic group.

The study demonstrated the use of spatial analytical tools to identify clusters of household enrollment pattern in the NHIS among residents in rural Ghana. In the face of limited resources, policy makers can therefore use the findings as guideline to strategically channel interventions to areas of most need. Furthermore, these analyses can be repeated annually to assess progress on improving insurance coverage.

Key words: Spatial scan statistic, Bernoulli model, National Health Insurance Scheme, Barekuma Collaborative Community Development Project, Ghana

Introduction

Access to healthcare remains very difficult and debatable in the developing world due to limited economic resources, modest economic growth, constraints on the public sector and low institutional capacity.1 In an attempt to address these challenges, Ghana adopted several strategies immediately after gaining independence in 1957, including making service delivery free at all government-owned health facilities.2 However, by the late 1990, the nation could not sustain this free healthcare policy and introduced the pay-per-service model commonly referred to as the cash-and-carry system, where patients and their families were made to pay the full cost out-of-pocket for all services offered them.3,4

In an effort to address the negative effects associated with the out-of-pocket payment mode5-8 and also align the nation’s long term healthcare goals to the World Health Organization (WHO) call in its 58th World Health Assembly resolution (WHA58.33) for all member states to plan the transition to universal coverage of their citizens so as to contribute to meeting the healthcare needs of the population with improved quality,9,10 Ghana’s 2003 Parliament promulgated the National Health Insurance Act 650 (HI Act).11-13 This legislative instrument led to the implementation of the National Health Insurance Scheme (NHIS) with the policy objective of extending health insurance coverage to all residents in the country.13

To help understand the utilization trends of health services among patients, several empirical studies have been conducted globally to assess how factors like time, distance, economic status and users perception levels of health facilities has impacted attendance.14,15 For example, Feikin et al. (2009) in a study assessing the impact of distance on pediatric healthcare utilization in rural Kenya concluded the rate of clinic visits decreases by 34 percent for every kilometer increase in distance travelled from the home to the clinic.16 In a cross-sectional study conducted by Bour (2003) in the Ahafo-Ano district in Ghana, he alluded to the fact that the average travel cost from the rural areas to the nearest health facility is very high, thereby playing a very significant role in accessing health care.17 Hounton et al. (2008) also concluded that distance to health facility is a major determinant in seeking of delivery health care among women in rural Burkina Faso.18

However, despite the commitment to pursuing a universal healthcare delivery system in Ghana, there has been no known study that measured how time, cost or distance to get to the designated registration centers for enrolling into the NHIS are impacting the probabilities of subscription into the program, especially among those in the rural and peri-rural settings.

Spatial analytical techniques and geography information systems (GIS) have been used in recent times to help explain the variability in events in epidemiology and health research19 and have helped in directing limited resources efficiently to solve health related issues.20 The location of residential homes is a key indicator for the likelihood of enrollment or participation in any health program as it affects the time, distance or cost one needs to commit to in order to utilize services provided. Adopting spatial analytical methodologies will therefore help visualize, manage and evaluate the impact of location on access.21

This research thus seeks to explore the spatial relationship between locations of residential homes and the likelihood of having either no or partial versus complete enrollment of an entire household into the newly introduced health insurance program among residents in the study area.

Materials and Methods

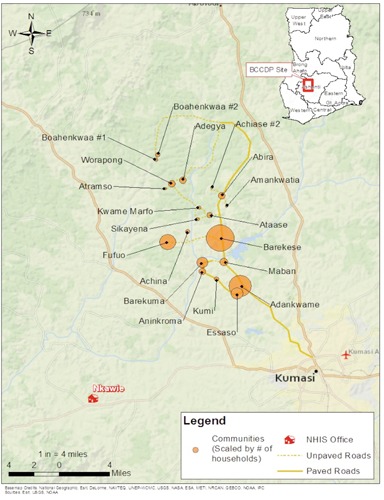

The study participants included all heads of households enrolled in a cross-sectional study conducted in 20 rural and peri-rural communities in the Barekese subdistrict of the Atwima-Nwabiagya district of Ghana (Figure 1). The communities constitute the Barekuma Collaborative Community Development Project site; a collaborative partnership between the community leadership and researchers from Komfo Anokye Teaching Hospital, Kwame Nkrumah University of Science and Technology (KNUST) both in Kumasi, Ghana, and the University of Utah (UofU) in Salt Lake City, USA.

Figure 1.

Location of the Barekuma Collaborative Community Development Project (BCCDP) study site and the National Health Insurance Scheme Office at Nkawie.

A total of 3228 heads of household were interviewed using a survey instrument adopted from the Ghana Demographic and Health Survey with minimal modifications. The questionnaire has items related to household subscription to the NHIS, socioeconomic variables (such as ownership of farmland, home, household items, etc.) and demographic variables (such as gender, age, marital status, level of education, religious beliefs, occupation, etc.). The research team used hand held global positioning system units to determine the location of each home and the designated registration center (at Nkawie) for enrollment in the study. The study received ethical approval from the UofU Institutional Review Board and Committees on Human Research Publications and Ethics of the KNUST College of Health Sciences, School of Medical Sciences.

The outcome variable of the study is a binary response to the question on whether all members of a participating household were fully enrolled in the health insurance program versus partial or no enrollment. Using the household as unit for analysis in Kulldorff’s purely spatial scan statistic,22,23 a Bernoulli model was then developed to identify possible local geographic clusters of either complete versus partial or no households enrollment in the NHIS.24-26 The method uses circular window of varying radius centered at each household and moves across the map so that at any given position the window includes different sets of neighboring households. The radius of the circular window varies repeatedly from zero up to a maximum radius set such that not more than 50 percent of the total study population was within the circle. This method allows the scanning window to continuously vary in both location and size, thereby creating a large number of distinct potential clusters. The test determines the location and statistical significance of clusters without prior assumptions about the factors affecting enrollment to the program in the study region.25

A bivariate analysis was then conducted to assess the association of selected demographic and socioeconomic household indicators within the cluster grouping. Since all variables from the bivariate analysis came out to be statistically significant, several multivariate logistic regression models were built to assess which variable retain its significance in predicting the odds of a household enrolling the entire membership in the health insurance program and also to evaluate the effect of the detected geographic clusters on enrollment.

The socioeconomic status (SES) for the households was computed using factor scores generated from principal component analysis as weights on ownership of fourteen selected household assets (such as furniture, television, fan, cell phone, sewing machine, etc.). Households were assigned aggregate scores based on the possession of these assets. The ranked scores were then classified into SES three groups such as Low, Middle and High.27 This approach was adopted due to the challenge of getting actual household income data in deprived settings as this and the fact that acquired household assets are good indicators to long term wealth.28

Travel-related time and cost for reaching the NHIS registration center were computed as the total duration and expense incurred, respectively, to make a round trip from a home to a centralized location within the respective communities on foot and then continue with a public commercial transport. These were generated based on travel cost and duration estimates gathered from selected leaders in the communities. Travel time on foot was also estimated as the time it takes an average healthy person to travel a distance of one mile by using a stopwatch to time this out. Distance measuring tools in ArcGIS and Google Earth were used to estimate the distances from the homes to the registration center. Cut-off points used in creating categories for total travel time and cost to make a round trip to register into the insurance scheme were selected based on the observed distribution patterns of the variables. All data analyses were performed using SaTScan 9.1.1 Sun Microsystems Inc., ArcGIS 10.1 [Environmental Systems Research Institute (ESRI), Redlands, California and STATA statistical software package StataCorp. 2007. Stata Statistical Software: Release 12. College Station, TX: StataCorp LP].

Results

Of the 3228 total heads of households that participated in the cross-sectional study, 1952 (60%) indicated having health insurance coverage for their entire family units with the remaining 40 percent reported having partial or no coverage. Out of the total respondents, 1141 (35%) were females and 65 percent were males. Seventy two percent reported being married, while 231 (7%) were single at the time of participation. Just over half the households were classified under low economic status. A significant proportion of the respondents (46%), reported farming as the the main occupation. About a third of the reported not having any form of formal education, while 2548 (79%) professed faith in the Christian religion (Table 1).

Table 1.

Demographic characteristics of households.

| Variables | Categories | No. (%) |

|---|---|---|

| Gender | Female | 1141 (35.35) |

| Male | 2087 (64.65) | |

| Age (years) | ≤35 | 796 (25.56) |

| 36-45 | 800 (25.69) | |

| 46-60 | 817 (26.24) | |

| ≥61 | 701 (22.51) | |

| Marital status | Married | 2340 (72.49) |

| Single | 231 (7.16) | |

| Divorced | 263 (8.15) | |

| Widowed | 394 (12.21) | |

| Occupation | Farming | 1489 (46.13) |

| Teachers/Students | 111 (3.44) | |

| Trading | 596 (18.46) | |

| Others | 1032 (31.97) | |

| Educational level | None | 1085 (33.61) |

| Primary | 425 (13.17) | |

| Middle/ Junior High | 1,353 (41.91) | |

| Senior High | 200 (6.20) | |

| Tertiary | 165 (5.11) | |

| Religious beliefs | Christianity | 2548 (78.93) |

| Moslem | 576 (17.84) | |

| Others | 104 (3.22) | |

| Household size | ≤4 | 1309 (40.55) |

| 5-8 | 1394 (43.18) | |

| 9-11 | 277 (8.58) | |

| ≥12 | 248 (7.68) | |

| SES | Low | 1874 (58.05) |

| Middle | 938 (28.97) | |

| High | 419 (12.98) | |

| NHIS | Yes | 1952 (60.47) |

| Enrollment | No | 1276 (39.53) |

| Cluster | Outside | 2108 (65.30) |

| Cluster 1 | 320 (9.91) | |

| Cluster 2 | 611(18.93) | |

| Cluster 3 | 189 (5.86) |

SES, socioeconomic status; NHIS, National Health Insurance Scheme.

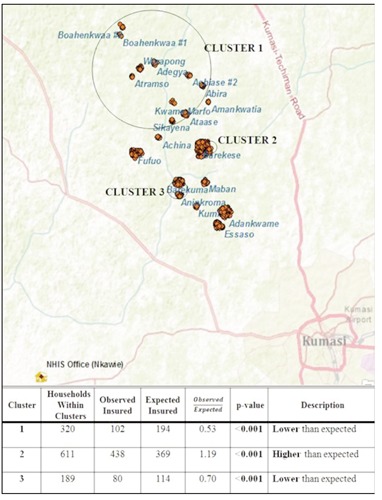

The spatial scan statistic test identified three statistical significant clusters (Cluster 1, 2 and 3) of households with either high or low enrollment rates in the health insurance program. All households outside the three significant clusters were grouped as Outside Cluster. The largest cluster area (Cluster 1) of lower than expected complete household enrollment rate into the insurance program covered 10 out of the 20 communities in the study region (Figure 2). This cluster consisted of a total of 320 (10%) households.

Figure 2.

Map of the identified clusters in enrollment patterns and the National Health Insurance Scheme (NHIS) Office.

Cluster 2 and 3 had a total of 611 (19%) and 189 (6%) households, respectively. All other households outside the significantly detected clustered zones of residences with high and low enrollment clusters accounting to about 2108 (65%) were grouped as the Outside cluster or houses in the region with no or random enrollment pattern.

The enrollment rate into the NHIS spanned from about 25 percent to 91 percent across the communities. The travel time and cost to the registration center varies by community and within clusters. The highest average cost to commute from the farthest community to and from the registration center with a public commercial transport was about 10 GH¢. Based on the location of the community, it takes approximately of 143 to 330 minutes in travel time for a head of a household to register his or her dependents into the insurance program. The average family size ranges from about 5 to 8 persons per household within the communities (Table 2).

Table 2.

Distribution of community and cluster features.

| Category | Variable | Enrollment rate | Mean household size | Mean distance (miles) | Mean time (min) | Mean cost (gh¢) |

|---|---|---|---|---|---|---|

| Community | Sikayena | 0.11 | 5.28 | 81.73 | 261.04 | 4.80 |

| Atramso | 0.25 | 5.25 | 103.24 | 304.84 | 7.60 | |

| Ataase | 0.29 | 6.11 | 79.01 | 218.79 | 4.80 | |

| Boahenkwaa #1 | 0.32 | 6.04 | 111.58 | 330.58 | 10.00 | |

| Boahenkwaa #2 | 0.32 | 5.63 | 110.57 | 311.94 | 10.00 | |

| Adegya | 0.32 | 7.19 | 97.56 | 226.95 | 9.00 | |

| Kwame Marfo | 0.33 | 5.11 | 81.83 | 262.80 | 4.80 | |

| Achiase #2 | 0.36 | 4.55 | 82.06 | 254.29 | 4.80 | |

| Worapong | 0.40 | 7.46 | 100.81 | 241.21 | 10.00 | |

| Barekuma | 0.44 | 8.07 | 72.18 | 199.05 | 4.20 | |

| Aninkroma | 0.50 | 8.00 | 71.17 | 176.42 | 4.00 | |

| Marban | 0.54 | 6.42 | 65.40 | 161.83 | 3.40 | |

| Kumi | 0.55 | 7.24 | 67.54 | 165.27 | 4.00 | |

| Abira | 0.58 | 7.85 | 77.72 | 194.92 | 4.80 | |

| Essaso | 0.60 | 5.90 | 63.31 | 149.10 | 3.80 | |

| Fufuo | 0.61 | 5.88 | 77.82 | 196.02 | 4.80 | |

| Barekese | 0.66 | 5.11 | 69.36 | 170.20 | 3.80 | |

| Adankwame | 0.68 | 5.47 | 61.15 | 142.61 | 3.20 | |

| Achina | 0.77 | 5.46 | 80.47 | 240.73 | 4.60 | |

| Amankwatia | 0.91 | 4.91 | 79.63 | 223.92 | 4.80 | |

| Cluster | Cluster 1 | 0.32 | 6.43 | 93.79 | 249.83 | 7.69 |

| Cluster 2 | 0.71 | 5.04 | 69.34 | 169.66 | 3.80 | |

| Cluster 3 | 0.42 | 8.27 | 71.78 | 190.28 | 4.12 | |

| Outside | 0.63 | 5.68 | 67.81 | 165.80 | 3.81 |

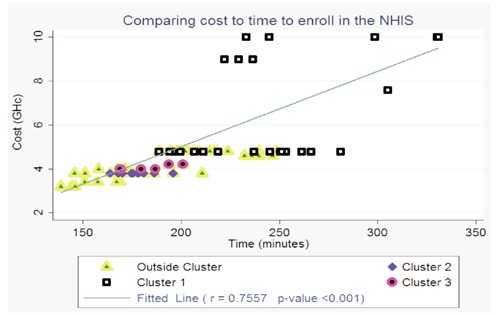

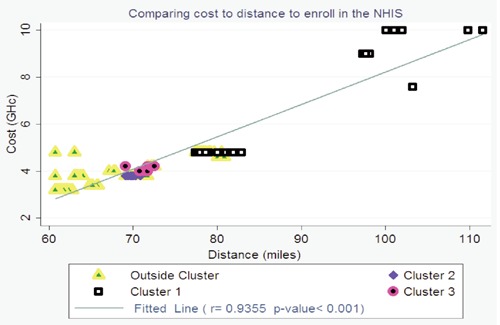

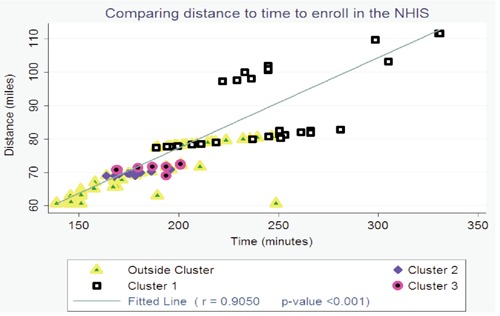

There is a positive linear correlation between travel time and cost, distance and cost and finally between time and distance to get to the enrollment center to subscribe in the program. Thus, a one unit rise in one indicator leads to a corresponding increase in the other. However, there was a wide variability in the three indicators among clusters. Households on average experience more in total travel time, distance and cost to make a round trip to and from the registration center compared to their counterparts in the other clusters. Conversely, households in the Cluster 2 households tend to spend much lower when comparing all significantly detected clusters thereby confirming the identification of such group (Figures 3-5).

Figure 3.

Plot comparing total travel cost to time for enrolling in the insurance program. NHIS, National Health Insurance Scheme.

Figure 4.

Plot comparing travel cost to distance for enrolling in the insurance program. NHIS, National Health Insurance Scheme.

Figure 5.

Plot comparing total travel distance to time for enrolling in the insurance program. NHIS, National Health Insurance Scheme.

Bivariate analysis to evaluate the relationship between selected household demographic indicators and complete household enrollment in the NHIS within each identified cluster showed highly significant statistical associations with all selected variables at an α=0.05 level of significance. An evaluation of the distribution pattern of the respondents by marital status and occupation across clusters revealed relatively similar trends with a very significant proportion of them either married or farmers. Larger proportion also reported Middle/Junior High as their highest attained level of formal education across all detected clusters. However, the greatest proportional differences were in travel cost and time where almost all respondents in the Cluster 1 fell in the high ends of those variables while the other clusters did not (Table 3).

Table 3.

Bivariate analysis of selected indicators.

| Variable | Category | All households No. (%) | Association within clusters | ||||

|---|---|---|---|---|---|---|---|

| Cluster 1 No. (%) | Cluster 2 No. (%) | Cluster 3 No. (%) | Outside No. (%) | P-value | |||

| Gender | Female | 1141 (35.35) | 87 (27.19) | 258 (42.23) | 71 (37.57) | 725 (34.39) | <0.001 |

| Male | 2087 (64.65) | 233 (72.81) | 353 (57.77) | 118 (62.43) | 1383 (65.61) | ||

| Age (years) | ≤35 | 796 (25.56) | 61 (20.54) | 152 (25.63) | 24 (13.26) | 559 (27.36) | <0.001 |

| 36-45 | 800 (25.69) | 72 (24.24) | 146 (24.62) | 38 (20.99) | 544 (26.63) | ||

| 46-60 | 817 (26.24) | 94 (31.65) | 163 (27.49) | 56 (30.94) | 504 (24.67) | ||

| ≥61 | 701 (22.51) | 70 (23.57) | 132 (22.26) | 63 (34.81) | 436 (21.34) | ||

| Marital status | Married | 2340 (72.49) | 238 (74.38) | 430 (70.38) | 139 (73.54) | 1533 (72.72) | 0.040 |

| Single | 231 (7.16) | 13 (4.06) | 55 (9.00) | 6 (3.17) | 157 (7.45) | ||

| Divorced | 263 (8.15) | 30 (9.38) | 49 (8.02) | 12 (6.35) | 172 (8.16) | ||

| Widowed | 394 (12.21) | 39 (12.19) | 77 (12.60) | 32 (16.93) | 246 (11.67) | ||

| Occupation | Farming | 1489 (46.13) | 277 (86.56) | 199 (32.57) | 136 (71.96) | 877 (41.60) | <0.001 |

| Teachers/Students | 111 (3.44) | 5 (1.56) | 22 (3.60) | 4 (2.12) | 80 (3.80) | ||

| Trading | 596 (18.46) | 11 (3.44) | 138 (22.59) | 17 (8.99) | 430 (20.40) | ||

| Others | 1032 (31.97) | 27 (8.44) | 252 (41.24) | 32 (16.93) | 721 (34.20) | ||

| Educational level | None | 1085 (33.61) | 139 (43.44) | 149 (24.39) | 69 (36.51) | 728 (34.54) | <0.001 |

| Primary | 425 (13.17) | 43 (13.44) | 71 (11.62) | 36 (19.05) | 275 (13.05) | ||

| Middle/Junior High | 1353 (41.91) | 110 (34.38) | 314 (51.39) | 71 (37.57) | 858 (40.70) | ||

| Senior High | 200 (6.20) | 21 (6.56) | 35 (5.73) | 9 (4.76) | 135 (6.40) | ||

| Tertiary Education | 165 (5.11) | 7 (2.19) | 42 (6.87) | 4 (2.12) | 112 (5.31) | ||

| Religious belief | Christianity | 2548 (78.93) | 235 (73.44) | 493 (80.69) | 158 (83.60) | 1662 (78.84) | <0.001 |

| Moslem | 576 (17.84) | 59 (18.44) | 97 (15.88) | 30 (15.87) | 390 (18.50) | ||

| Others | 104 (3.22) | 26 (8.13) | 21 (3.44) | 1 (0.53) | 56 (2.66) | ||

| Household size | ≤4 | 1309 (40.55) | 102 (31.87) | 296 (48.45) | 55 (29.10) | 856 (40.61) | <0.001 |

| 5-8 | 1394 (43.18) | 144 (45.00) | 256 (41.90) | 62 (32.80) | 932 (44.21) | ||

| 9-11 | 277 (8.58) | 34 (10.63) | 27 (4.42) | 28 (14.81) | 188 (8.92) | ||

| ≥12 | 248 (7.68) | 40 (12.50) | 32 (2.24) | 44 (23.28) | 132 (6.26) | ||

| Travel time (min) | ≤ 163 | 1635 (50.65) | 0 (0.00) | 366 (59.90) | 0 (0.00) | 1269 (60.20) | <0.001 |

| 164-245 | 1420 (43.99) | 161 (50.31) | 245 (40.10) | 189 (100.00) | 825 (39.14) | ||

| ≥ 246 | 173 (5.36) | 159 (49.69) | 0 (0.00) | 0 (0.00) | 14 (0.66) | ||

| Travel cost (gh¢) | ≤3.90 | 2151 (66.64) | 0 (0.00) | 611 (100.00) | 0 (0.00) | 1540 (73.06) | <0.001 |

| 4.00-7.50 | 894 (27.70) | 137 (42.81) | 0 (0.00) | 189 (100.00) | 568 (26.94) | ||

| ≥7.60 | 183 (5.67) | 183 (57.19) | 0 (0.00) | 0 (0.00) | 0 (0.00) | ||

| SES | Low | 1874 (58.05) | 295 (92.19) | 263 (43.04) | 165 (87.30) | 1151(54.60) | <0.001 |

| Middle | 938 (28.97) | 24 (7.50) | 242 (39.61) | 24 (12.70) | 645 (30.60) | ||

| High | 419 (12.98) | 1 (0.31) | 106 (17.35) | 0 (0.00) | 312 (14.80) | ||

| NHIS enrollment | No | 1276 (39.53) | 218 (68.13) | 177 (28.97) | 109 (57.67) | 772 (36.62) | <0.001 |

| Yes | 1925 (60.47) | 102 (31.87) | 434 (71.03) | 80 (42.33) | 1336 (63.38) | ||

A comparison of the odds of enrollment appeared relative similar between the four models. For example, there was a statistically significant increase in the odds of enrollment regardless of the model with an increase in age, the level of education attained and higher socio-economic level of the respondents. Thus, heads of households with tertiary level of education have 2.1 [95% CI: 1.29-3.53] times the odds of enrolling their entire dependents in the insurance program comapared to their counterparts who had no formal education. Residents in the Cluster 2 region had about 1.5 [95% CI: 1.19-1.86] times the odds of enrolling compared to the counterparts in the outside sub-zone. The odds to enroll, however, reduces with an increase in both travel time and cost when predicting enrollment rates without assessing for cluster effect.

There was a significant reduced odds of enrolling with an increase in the size of the household unit. For example, households with more than 12 members have about 0.67 [95% CI: 0.25-0.47] times the odds to enroll comapred to those with less than 4 members across all predictive models. The occupational background of the heads of households seemed not to have any effect on the likelihood of enrolling their dependents. However, those who reported to be teachers or students in school tend to have much higher odds compared to their farming counterparts (Table 4).

Table 4.

Logistic regression assessing for cluster effect on subscription odds to the National Health Insurance Scheme.

| Variable | Category | All households | All households | All households | All households | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (without cost and cluster effect) | (without time and cluster effect) | (without cluster effect) | (with cluster effect) | ||||||||||

| (N=3228) | (N=3228) | (N=3228) | (N=3228) | ||||||||||

| Odds ratio | P-value | [95% CI] | Odds ratio | P-value | [95% CI] | Odds ratio | P-value | [95% CI] | Odds ratio | P-value | [95% CI] | ||

| Gender | Female (R) | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - |

| Male | 0.766 | 0.012 | 0.62-0.94 | 0.754 | 0.008 | 0.61-0.93 | 0.761 | 0.010 | 0.62-0.93 | 0.817 | 0.060 | 0.66-1.01 | |

| Age (years) | ≤35 (R) | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - | - | ||

| 36-45 | 1.303 | 0.019 | 1.04-1.63 | 1.307 | 0.017 | 1.05-1.53 | 1.304 | 0.019 | 1.04-1.63 | 1.297 | 0.023 | 1.04-1.62 | |

| 46-60 | 1.400 | 0.004 | 1.11-1.76 | 1.410 | 0.003 | 1.12-1.77 | 1.407 | 0.003 | 1.12-1.77 | 1.391 | 0.005 | 1.01-1.75 | |

| ≥61 | 1.822 | 0.000 | 1.41-2.36 | 1.866 | 0.000 | 1.44-2.41 | 1.834 | 0.000 | 1.41-2.38 | 1.791 | 0.000 | 1.38-2.33 | |

| Marital status | Married (R) | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - |

| Single | 0.682 | 0.016 | 0.50-0.93 | 0.686 | 0.017 | 0.50-0.93 | 0.680 | 0.015 | 0.50-0.93 | 0.679 | 0.015 | 0.50-0.93 | |

| Divorced | 0.734 | 0.140 | 0.58-1.08 | 0.807 | 0.170 | 0.59-1.10 | 0.801 | 0.156 | 0.59-1.09 | 0.807 | 0.173 | 0.59-1.10 | |

| Widowed | 0.909 | 0.521 | 0.68-1.22 | 0.912 | 0.536 | 0.68-1.22 | 0.913 | 0.539 | 0.68-1.22 | 0.913 | 0.544 | 0.68-1.22 | |

| Occupation | Farming (R) | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - |

| Teachers/Students | 1.623 | 0.100 | 0.91-2.89 | 1.659 | 0.085 | 0.93-2.95 | 1.629 | 0.098 | 0.91-2.90 | 1.568 | 0.130 | 0.87-2.80 | |

| Trading | 1.042 | 0.715 | 0.83-1.30 | 1.046 | 0.698 | 0.83-1.32 | 1.040 | 0.736 | 0.83-1.31 | 1.043 | 0.723 | 0.83-1.31 | |

| Others | 1.098 | 0.339 | 0.91-1.33 | 1.110 | 0.297 | 0.91-1.35 | 1.097 | 0.356 | 0.90-1.34 | 1.063 | 0.549 | 0.87-1.30 | |

| Educational level | None (R) | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - |

| Primary | 0.968 | 0.800 | 0.75-1.24 | 0.991 | 0.941 | 0.77-1.27 | 0.981 | 0.885 | 0.76-1.26 | 0.970 | 0.812 | 0.75-1.25 | |

| Middle/ JHS | 1.265 | 0.018 | 1.04-1.54 | 1.295 | 0.010 | 1.06-1.57 | 1.284 | 0.013 | 1.06-1.56 | 1.219 | 0.052 | 1.00-1.49 | |

| SHS | 1.469 | 0.032 | 1.03-2.09 | 1.501 | 0.024 | 1.06-2.13 | 1.504 | 0.024 | 1.06-2.14 | 1.471 | 0.034 | 1.03-2.10 | |

| Tertiary | 2.122 | 0.003 | 1.29-3.49 | 2.142 | 0.003 | 1.31-3.51 | 2.159 | 0.002 | 1.31-3.55 | 2.138 | 0.003 | 1.29-3. 53 | |

| Religious beliefs | Christianity (R) | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - |

| Moslem | 1.058 | 0.589 | 0.86-1.30 | 1.068 | 0.532 | 0.87-1.31 | 1.067 | 0.540 | 0.87-1.31 | 1.082 | 0.458 | 0.88-1.33 | |

| Others | 0.550 | 0.005 | 0.36-0.84 | 0.574 | 0.010 | 0.38-0.87 | 0.566 | 0.008 | 0.37-0.86 | 0.559 | 0.008 | 0.38-0.86 | |

| Household size | ≤4 (R) | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - |

| 5-8 | 0.934 | 0.448 | 0.78-1.11 | 0.945 | 0.526 | 0.79-1.13 | 0.939 | 0.486 | 0.79-1.12 | 0.950 | 0.577 | 0.80-1.14 | |

| 9-11 | 0.596 | 0.000 | 0.45-0.80 | 0.605 | 0.001 | 0.45-0.81 | 0.597 | 0.000 | 0.45-0.80 | 0.625 | 0.002 | 0.47-0.84 | |

| ≤12 | 0.324 | 0.000 | 0.24-0.44 | 0.333 | 0.000 | 0.24-0.45 | 0.326 | 0.000 | 0.24-0.45 | 0.346 | 0.000 | 0.25-0.47 | |

| SES | Low (R) | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - |

| Middle | 1.443 | 0.000 | 1.20-1.74 | 1.467 | 0.000 | 1.21-1.77 | 1.444 | 0.000 | 1.19-1.75 | 1.474 | 0.000 | 1.22-1.79 | |

| High | 1.639 | 0.000 | 1.27-2.12 | 1.656 | 0.000 | 1.27-2.16 | 1.637 | 0.000 | 1.26-2.13 | 1.662 | 0.000 | 1.27-2.17 | |

| Travel time(min) | ≤163 (R) | 1.000 | - | - | - | - | - | 1.000 | - | - | 1.000 | - | - |

| 164-245 | 0.800 | 0.009 | 0.68-0.95 | - | - | - | 0.795 | 0.033 | 0.64-0.98 | 0.731 | 0.005 | 0.58-0.91 | |

| ≥246 | 0.316 | 0.000 | 0.22-0.46 | - | - | - | 0.376 | 0.000 | 0.24-0.60 | 0.556 | 0.027 | 0.33-0.93 | |

| Travel cost(gh¢) | ≤3.90 (R) | - | - | - | 1.000 | - | - | 1.000 | - | - | 1.000 | - | - |

| 4.00-7.50 | - | - | - | 0.841 | 0.087 | 0.69-1.03 | 1.047 | 0.720 | 0.81-1.35 | 1.700 | 0.002 | 1.27-2.27 | |

| ≥7.60 | - | - | - | 0.407 | 0.000 | 0.28-0.58 | 0.702 | 0.120 | 0.45-1.10 | 2.513 | 0.000 | 1.38-4.56 | |

| Cluster | Outside (R) | - | - | - | - | - | - | - | - | - | 1.000 | - | - |

| Cluster 1 | - | - | - | - | - | - | - | - | - | 0.260 | 0.000 | 0.16-0.42 | |

| Cluster 2 | - | - | - | - | - | - | - | - | - | 1.488 | 0.000 | 1.19-1.86 | |

| Cluster 3 | - | - | - | - | - | - | - | - | - | 0.477 | 0.000 | 0.34-0. 68 | |

CI, confidence interval; R, reference group; SES, socioeconomic status.

There was some level of statistical significance detected for travel cost in predicting the probability of enrollment in the second model without the time component. However, this level of significance completely disappeared when time was added to the third model. A further evaluation to assess the effect of clustering in the forth model revealed that travel time and cost played very significant role in predicting the odds of enrolling in the program given the location of the cluster. This finding therfore offers more credence to the existence of great variability in the detected clusters and should be the prominent factor in the allocation of resources when designing intervention programs for the study region.

Discussion

Despite the progress made with the introduction of the nationalized health insurance scheme for helping Ghanaians access health care, some groups of the populace still lack the access anticipated in the policy objective that ushered in the NHIS. Studies of this kind, taking into consideration the effect of spatial factors on the subscription to the program, are therefore of high importance.

Using a Bernoulli-based spatial scan statistic, we have identified the existence of potential clustering in the enrollment pattern of households into the health insurance program. We found three significant clusters of households in the study region with either high or low participatory rates in the program. Interestingly, the largest geographic cluster with very low enrollment rate (Cluster 1) appeared in the most difficult communities to access by road in the subdistrict. The implication of this in relationship to the NHIS policy objective will be the urgent call for setting further administrative strategies that will include locating registration centers much closer to such areas or using mobile registration centers that visit outlying regions. From the study, we have identified SES, travel cost and time to the registration center as factors that are strongly associated with enrollment of entire household membership in the health insurance program. Additionally, efforts should be made to target the poor in educative programs that will help woo their interest and understanding of the benefits in enrolling in a program that will help alleviate the heavy cost associated in accessing health care. Given that the inhabitants are predominantly farmers earning seasonal income from crop harvest, further strategies like premium payment in installment fashion could be set in place to offer some reliefs during the between-harvest periods.

The use of Spatial Scan test for locating potential clusters as done in this study has some limitations including the choice of perceived enrollment percentage of the study population one needs to use to effectively pick significant cluster groups. However, we think findings from this study are important to help identify areas for which more outreach is needed to increase enrollment in the insurance scheme.

Conclusions

Notwithstanding the positive impact of the nationalized health insurance program in Ghana in getting the citizenry access to healthcare, some residents in the research area are still not participating in the program. Even though it is designed to help lessen the health shock and associated financial expenses to a household in times of need. Using spatial scan analysis, we have detected clusters of households with either low or high enrollment rates in the NHIS among residents in the study region with travel time and cost to the designated registration center from the research communities being the most significant predictors influencing those enrollment patterns. It is also worth noting that, the higher than expected cluster of households was detected around the only government-owned health facility (Barekese Community Health Post) in the entire subdistrict while the lower than expected clusters are in locations where access to health facilities is restricted.

To help improve equity in accessing healthcare and promote the NHIS’s primary goal of achieving universal health insurance coverage, policy and decision makers need to understand factors beyond socioeconomic indicators that are associated with enrollment in the program. This could help direct strategies that might inform how registrations centers are to be located to ease the cost and time element in order to motivate participation in the insurance program in the face of limited resource availability.

Acknowledgements

We want to acknowledge the Staff of the Research and Development Unit of the Komfo Anokye Teaching Hospital in Kumasi (Ghana) and the BCCDP fieldworkers who helped in the data collection process. Nick Faust helped in the plotting of the maps.

References

- 1.Carrin Guy. Social health insurance in developing countries: a continuing challenge. Int Social Security Rev. 2002;55:57-69. [Google Scholar]

- 2.Sulzbach S, Garshong B. Evaluating the effects of the National Health Insurance Act in Ghana: baseline report. Bethesda, MD: The Partners for Health Reformplus Project, Abt. Associate; 2005. [Google Scholar]

- 3.Schieber G, Cashin C, Karima S. Health financing in Ghana. Washington, DC: International Bank for Reconstruction and Development / The World Bank; 2012. Available from: http://uhcforward.org/sites/uhcforward.org/files/718940PUB0PUBL067869B09780821395660.pdf [Google Scholar]

- 4.Yogesh R. The political development of the Ghanaian National health Insurance System: lessons in health. Bethesda, MD: USAID; 2007. Available from: http://www.healthsystems2020.org/content/resource/detail/2046/ [Google Scholar]

- 5.Nyonator F, Kutzin J. Health for some? The effects of user fees in the Volta Region of Ghana. Health Policy and Planning. 1999;14:329-41. [DOI] [PubMed] [Google Scholar]

- 6.Dalinjong PA, Laar AS. The national health insurance scheme: perceptions and experiences of health care providers and clients in two districts of Ghana. Health Econ Rev. 2012;2:13. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Leive A, Xu K. Coping with out-of-pocket health payments: empirical evidence from 15 African countries. Bull World Health Organ. 2008;86:849-56. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.Seddoh A, Adjei S, Nazzar A. Ghana’s National Health Insurance Scheme: views on progress, observations and commentary; 2011. Available from: http://www.chghana.org/documents/Publication/Report on observations and commentary on NHIS.pdf [Google Scholar]

- 9.Yates R. Universal health care and the removal of user fees. Lancet. 2009;373:2078-81. [DOI] [PubMed] [Google Scholar]

- 10.Fusheini A, Marnoch G, Gray AM. The implementation of the National Health Insurance Programme in Ghana – an institutional approach; 2012. Available from: http://www.psa.ac.uk/journals/pdf/5/2012/873_495.pdf [Google Scholar]

- 11.Akazili J, Gyapong J, McIntyre D. Who pays for health care in Ghana? Int J Equity Health. 2011;10:26. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12.Dixon J, Tenkorang EY, Luginaah I. Ghana’s National Health Insurance Scheme: helping the poor or leaving them behind? Environ Plan C Govern Policy. 2011;29:1102-15. [Google Scholar]

- 13.Sarpong N, Loag W, Fobil J, et al. National health insurance coverage and socio-economic status in a rural district of Ghana. Tropical Med Int Health. 2010;15:191-7. [DOI] [PubMed] [Google Scholar]

- 14.Comber AJ, Brunsdon C, Radburn R. A spatial analysis of variations in health access: linking geography, socio-economic status and access perceptions. Int J Health Geograph. 2011;10:44. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15.Connelly JE, Philbrick JT, Smith GR, et al. Health perceptions of primary care patients and the influence on health care utilization. Medical Care. 1989;27:S99-109. [DOI] [PubMed] [Google Scholar]

- 16.Feikin DR, Nguyen LM, Adazu K, et al. The impact of distance of residence from a peripheral health facility on pediatric health utilisation in rural western Kenya. Tropical Med Int Health. 2009;14:54-61. [DOI] [PubMed] [Google Scholar]

- 17.Buor D. Analysing the primacy of distance in the utilization of health services in the Ahafo-Ano South district, Ghana. Int J Health Plan Manage. 2003;18:293-311. [DOI] [PubMed] [Google Scholar]

- 18.Hounton S, Chapman G, Menten J, et al. Accessibility and utilisation of delivery care within a Skilled Care Initiative in rural Burkina Faso. Tropical Med Int Health. 2008;13 Suppl 1:44-52. [DOI] [PubMed] [Google Scholar]

- 19.Higgs G, Gould M. Is there a role for GIS in the “new NHS”? Health Place. 2001;7:247-59. [DOI] [PubMed] [Google Scholar]

- 20.Delamater PL, Messina JP, Shortridge AM, et al. Measuring geographic access to health care: raster and network-based methods. Int J Health Geograph. 2012;11:15. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21.Moore D, Carpenter TE. Spatial analytical methods and geographic information systems: use in health research and epidemiology. Epidemiol Rev. 1999;21:143-61. [DOI] [PubMed] [Google Scholar]

- 22.Huang L, Pickle LW, Stinchcomb D, et al. Detection of spatial clusters: application to cancer survival as a continuous outcome. Epidemiology (Cambridge, Mass). 2007;18:73-87. [DOI] [PubMed] [Google Scholar]

- 23.Kulldorff M. Spatial Scan Statistics. Commun Stat Theor Method. 1997;26:1481-96. [Google Scholar]

- 24.Westercamp N, Moses S, Agot K, et al. Spatial distribution and cluster analysis of sexual risk behaviors reported by young men in Kisumu, Kenya. Int J Health Geograph. 2010;9:24. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 25.Kulldorff M. Prospective time periodic geographical disease surveillance using a scan statistic. J R Stat Soc A. 2001;164:61-72. [Google Scholar]

- 26.Huang L, Kulldorff M, Gregorio D. A spatial scan statistic for survival data. Biometrics. 2007;63:109-18. [DOI] [PubMed] [Google Scholar]

- 27.Vyas S, Kumaranayake L. Constructing socio-economic status indices: how to use principal components analysis. Health Policy Plan. 2006;21:459-68. [DOI] [PubMed] [Google Scholar]

- 28.Houweling TAJ, Kunst AE, Mackenbach JP. Measuring health inequality among children in developing countries: does the choice of the indicator of economic status matter? Int J Equity Health. 2003;12:1-12. [DOI] [PMC free article] [PubMed] [Google Scholar]