Abstract

Background

The Affordable Care Act established policy mechanisms to increase health insurance coverage in the United States. While insurance coverage has increased, 10 to 15% of the U.S. population remains uninsured.

Objectives

To assess whether health insurance literacy and financial literacy predict being uninsured, covered by Medicaid, or covered by Marketplace insurance, holding demographic characteristics, attitudes toward risk, and political affiliation constant.

Research Design

Analysis of longitudinal data from fall 2013 and spring 2015 including financial and health insurance literacy and key covariates collected in 2013.

Subjects

2,742 U.S. residents ages 18-64, 525 uninsured in fall 2013, participating in the RAND American Life Panel, a nationally representative internet panel.

Measures

Self-reported health insurance status and type as of spring 2015.

Results

Among the uninsured in 2013, higher financial and health insurance literacy were associated with greater probability of being insured in 2015. For a typical uninsured individual in 2013, the probability of being insured in 2015 was 8.3 percentage points higher with high compared to low financial literacy, and 9.2 percentage points higher with high compared to low health insurance literacy. For the general population, those with high financial and health insurance literacy were more likely to obtain insurance via Medicaid or the Marketplaces compared to being uninsured. The magnitude of coefficients for these predictors was similar to that of commonly used demographic covariates.

Conclusions

A lack of understanding about health insurance concepts and financial illiteracy predict who remains uninsured. Outreach and consumer-education programs should consider these characteristics.

Keywords: Affordable Care Act, Health Insurance, Health Policy, Demand for Insurance

Introduction

The Affordable Care Act (ACA) of 2010 introduced multiple policy mechanisms designed to increase health insurance coverage in the United States. First, it offered incentives for states to expand Medicaid to low-income groups. Second, it introduced health insurance Marketplaces to facilitate enrollment and create competition across insurers. Third, it subsidized the purchase of insurance in the Marketplaces for those with incomes between 100% (effectively 138% in Medicaid expansion states) and 400% of the Federal Poverty Level (FPL). Finally, it established a penalty for those who opt to remain uninsured, with some exemptions. While surveys estimate that the rate of insurance coverage among adults age 18-64 increased by 4 to 8 percentage points since 2013, they also estimate that 10 to 15% of the U.S. population remains uninsured.1-8 This lingering gap suggests that important impediments to further increasing insurance enrollment may persist.

Previous research on insurance choices following the first ACA open enrollment has focused on socio-demographic characteristics, finding, for example, that lower educational and income levels and being Hispanic are associated with being uninsured, and that people who live in states that did not expand Medicaid are also likely to remain uninsured.1-3,5-8 Perceptions that premiums for insurance in the Marketplace are too high may also limit the total impact that the ACA has on uninsurance rates. However, there are potentially other unrecognized factors that may influence choices about health insurance. Financial literacy (defined as knowledge about financial concepts) and attitudes towards risk, for instance, have been found to play an important role in other financial decisions.9-12 It seems likely that they would influence decisions about health insurance as well. Similarly, limits in knowledge about health insurance concepts, such as deductibles or copayments, may limit some consumers' ability to evaluate whether the benefits of health insurance exceed its costs.

In this paper, we turn the lens onto these potential impediments to further decreasing the number who are uninsured and to enrollment in Medicaid and Marketplace insurance, investigating whether health insurance transitions are associated with health insurance literacy (defined as knowledge of health insurance concepts) and financial literacy. Furthermore, our data allow us to control for levels of risk aversion and political leanings, which may also predict uptake of insurance but are not typically available in surveys about health insurance. Unlike most previous research on this topic, we made use of rich longitudinal data, acquired from the nationally representative RAND American Life Panel (ALP), that offer information on more of the potential impediments to enrollment than datasets used in earlier studies. In particular, we made use of a new measure of health insurance literacy documented in previous work13 and assessed whether knowledge is associated with health insurance coverage. With access to these data, we could analyze the role of these variables, along with those of traditional socio-demographic insurance predictors. A key strength of this research design is the use of longitudinal data enabling us to investigate how these factors were related to individual-level changes in insurance coverage over time. Notably, the data allowed us to measure these characteristics prior to the ACA Marketplace's first open enrollment period in 2013, ensuring that enrollment decisions made after the rollout of the Marketplaces did not impact our measures of knowledge. Furthermore, by collecting data about respondents' current insurance status, we avoided recall bias. Other studies assessing these effects used cross sectional data, lacked the rich set of covariates, or focused on samples not representative of the general population.14

Methods

Data Sources and Study Sample

The American Life Panel is a nationally representative internet panel of respondents who participate in occasional online surveys. Panel members without internet access are provided with a computer and an internet connection, eliminating the bias found in many internet surveys, which include only existing computer users.15 We calculated sample weights to make the distributions of age, gender, ethnicity, education, income, and household size approximate the distributions in the Census Bureau's Current Population Survey.16 Panel members have been recruited over time, via several different mechanisms. The cumulative response rate across all recruitment waves is approximately 9%. While this is low, it is similar to other nationally representative surveys conducted by non-governmental organizations. Furthermore, American Life Panel estimates of the uninsured rate among working-age adults in 2013 and 2014 (2013: 20.3%; 2014: 13.7%)17 are similar to those from the Current Population Survey (2013: 18.5%; 2014 14.3%).7 The American Life Panel has produced accurate predictions in other settings as well, notably the 2012 Presidential Election.18

Our analyses focused on 2,742 respondents age 18-64 who completed surveys in fall 2013 (baseline) and spring 2015 (follow-up). We conducted our baseline survey from August 23 to September 30, 2013, just before the first open-enrollment period for the Marketplaces. We fielded our follow-up survey from March 1 to May 26, 2015. 84 % of those answering the baseline survey also responded to the follow-up. Both surveys included questions about health insurance literacy and coverage. Measures of risk aversion and financial literacy were collected between September 20, 2013 and March 5, 2014. Information about political affiliation was collected in earlier American Life Panel surveys fielded by other researchers before our baseline survey. This information was missing for approximately 28% of respondents who were not previously asked about their political affiliation. We focused on respondents who answered all questions included in our analysis constituting 92% of those who completed both surveys (except those about political affiliation where we included an indicator if this information was missing).

Outcome Measures

At both baseline and follow-up, we collected data about whether the respondent currently had health insurance, and if so, what type—Employer Sponsored Insurance (ESI), Medicaid, insurance through a Marketplace, or insurance through other sources (e.g., privately purchased non-group insurance, Medicare, Military or Veterans insurance, insurance from other small state programs). Employer sponsored insurance includes coverage obtained through COBRA, the survey respondent's employer, or the employer of the respondent's spouse or parent. The rates of uninsurance, enrollment in Medicaid, and enrollment via the Marketplaces that we estimated from these data were similar to rates measured in other studies,1-4 as well as to estimates from the Centers for Medicare and Medicaid Services (CMS), the Department of Health and Human Services (HHS), and the Census Bureau.19,20,7

Independent Variables of Interest

We focused on two predictors of insurance coverage, both measured at baseline. First, we collected standard measures of financial literacy covering fundamental concepts of economics and finance which have been shown to affect complex financial decisions, including retirement planning and stock market participation.9,10 The questions measure basic knowledge of interest rates (numeracy), inflation, and the safety of stocks versus bonds (risk). We classified individuals as having high financial literacy if they correctly answered all three questions.10,11 Previously research has found that financially literate individuals are better at making financial decisions and avoiding negative financial consequences.9,10 Individuals who are less financially literate may have more difficulties or feel less confident making decisions about health insurance, which aims to shield individuals from uncertain, potentially large financial consequences related to medical expenditures.

Second, we measured health insurance literacy (7 questions about deductibles, co-pays, coinsurance, networks, and prescription drug pricing (generic versus brand name)).21 These questions reflect individual knowledge of health insurance concepts, which are the factors that distinguish health insurance plans. These factors are likely to be important to anyone who has a choice in health insurance plans, especially those who have many plans to compare in the Marketplaces. Knowledge of these concepts is thus likely to be important for choosing health insurance22 – and making good choices.23 We classified individuals as having low health insurance literacy if they correctly answered fewer than 3 out of the 7 questions. This presents a rather low bar and captures individuals with potentially limited experience with health plans which is likely to be the case for the previously uninsured. Individuals with lower health insurance or financial literacy may be less likely to purchase insurance, because of difficulties in fully considering costs and benefits of different products when comparing insurance products in the complex environment.24,25 More information on these variables is provided in an online appendix.

Covariates

We controlled for demographic characteristics collected at baseline, including gender, age, race and ethnicity, education, household income, employment status, family status, and health. We also included an indicator for whether or not the respondent's state of residence expanded Medicaid. We obtained similar results from alternative specifications controlling for whether the states had state-based Marketplaces, the states' leaning in the 2012 presidential election, or using state-fixed effects.

In addition to these more commonly used demographic variables, we also controlled for risk aversion and political preference. We measured risk aversion, defined as one's willingness to take risks (measured on a 0 to 10 scale). We classified individuals as having either a high (less willing to take risks) or low (more willing to take risks) aversion to risk by splitting them at the median. Prior research has shown the behavioral validity of this measure using paid lottery choices.26 Those who are more risk averse may be more likely to demand health insurance.27 Finally, we included political affiliation prior to baseline. Public opinion of the ACA is divided strongly along party lines, with Republicans often opposing the ACA28,29,30 and showing lower intentions to comply with the individual mandate.31 Republicans may consequently be less likely to take advantage of Medicaid or the Marketplaces, leading to lower levels of insurance coverage. Previous research has been inconclusive on this issue.32

Statistical Analysis

We analyzed two populations in two separate sets of analyses: respondents uninsured at baseline and all respondents, regardless of initial insurance status. For those uninsured at baseline, we calculated the fraction who obtained insurance by spring 2015 by various demographic characteristics. For both populations, we separately estimated logit regressions to model the predicted probability of having insurance at follow up (i.e., the choice to become insured), and multinomial logit regressions to model the predicted probability of selecting different types of insurance (i.e., Medicaid, the Marketplaces, or through their employers) in comparison to being uninsured. To account for possible correlation between different factors that influence insurance take-up or choice of type of insurance, we include the above-mentioned control variables. The results can thus be interpreted as changes in insurance status or type related to levels of knowledge when holding the other factors constant. We report odds ratios (OR) for logit regressions and relative risk ratios (RRR) for multinomial logit regressions. We also interpret the results in terms of marginal effects. We used heteroscedasticity-adjusted standard errors clustered at the state of residence. We conducted our analyses using Stata 14.33 In the multinomial regressions for the full sample, we controlled for the type of insurance individuals had at baseline, as individuals who had insurance in 2013 were likely to have the same type of insurance at follow-up.

Results

Descriptive Statistics

Columns 1, 3, and 5 of Table 1 provide summary statistics for the full sample and those uninsured and insured at baseline while columns 2, 4 and 6 provide them for the March 2013 Current Population Survey. Our weighted American Life Panel survey sample tracks the distribution of key covariates in the broader, nationally representative CPS sample, including for variables that were not used to construct the statistical weights. 54% of our sample had low financial literacy; 12%, low health insurance literacy. Both numbers were higher among those uninsured compared to those insured at baseline. The correlation between the two variables is 0.271 among the general population and 0.268 among the uninsured (both p<0.001). Table 1 in the online appendix shows summary statistics by source of insurance.

Table 1. Descriptive statistics.

| Characteristics | Full sample | Uninsured | Insured | |||

|---|---|---|---|---|---|---|

| American Life Panel [n=2,742] | Current Population Survey [n=122,316] | American Life Panel [n=525] | Current Population Survey [n=24,523] | American Life Panel [n=2,217] | Current Population Survey [n=97,793] | |

| Health insurance in fall 2013 | ||||||

| Uninsured, % | 18 | 21 | 100 | 100 | 0 | 0 |

| Medicaid, % | 6 | 9 | 0 | 0 | 7 | 11 |

| ESI, % | 60 | 58 | 0 | 0 | 73 | 74 |

| All other, % | 17 | 12 | 0 | 0 | 20 | 15 |

| Literacy | ||||||

| Low financial literacy, % | 54 | a | 74 | a | 50 | a |

| High financial literacy, % | 46 | a | 26 | a | 50 | a |

| Low health insurance literacy, % | 12 | a | 26 | a | 9 | a |

| High health insurance literacy, % | 88 | a | 74 | a | 91 | a |

| Risk attitude | ||||||

| Low risk aversion, % | 52 | a | 57 | a | 50 | a |

| High risk aversion, % | 48 | a | 43 | a | 50 | a |

| Political affiliation | ||||||

| Democrat, % | 29b | a | 29 b | a | 29 | a |

| Republican, % | 21b | a | 15 b | a | 22 | a |

| Other party/Independent, % | 23 b | a | 22 b | a | 23 | a |

| Missing party affiliation, % | 28 b | a | 35 b | a | 26 | a |

| Gender | ||||||

| Male, % | 49 | 49 | 49 | 54 | 49 | 48 |

| Female, % | 51 | 51 | 51 | 46 | 51 | 52 |

| Age | ||||||

| Younger than 26, % | 15 | 18 | 26 | 22 | 12 | 17 |

| 26-44, % | 36 | 40 | 39 | 46 | 36 | 38 |

| 45 and older, % | 49 | 42 | 35 | 33 | 52 | 45 |

| Race and ethnicity | ||||||

| Non-Hispanic White, % | 66 | 63 | 46 | 46 | 71 | 68 |

| Non-Hispanic non-White, % | 15 | 20 | 23 | 22 | 13 | 20 |

| Hispanic, % | 19 | 17 | 31 | 31 | 16 | 13 |

| Education | ||||||

| No degree, % | 9 | 11 | 21 | 22 | 7 | 9 |

| High school or equivalent, % | 28 | 28 | 37 | 36 | 26 | 26 |

| Some college, % | 20 | 21 | 23 | 20 | 20 | 21 |

| Associate degree, % | 10 | 10 | 8 | 8 | 11 | 10 |

| Bachelor's degree and more, % | 32 | 30 | 12 | 14 | 37 | 34 |

| Income | ||||||

| Income lower than 138 of FPL, % | 21 | 23 | 46 | 45 | 15 | 17 |

| Income 138-250 of FPL, % | 22 | 19 | 29 | 26 | 20 | 17 |

| Income 251-400 of FPL, % | 20 | 21 | 17 | 16 | 21 | 22 |

| Income higher than 400 of FPL, % | 37 | 38 | 9 | 13 | 44 | 44 |

| Employment | ||||||

| Employed 2013/2015, % | 64 | a | 46 | a | 68 | a |

| Unemployed 2013/2015, % | 24 | a | 30 | a | 23 | a |

| Employed 2013/Unemployed 2015, % | 6 | a | 9 | a | 5 | a |

| Unemployed 2013/Employed 2015, % | 6 | a | 15 | a | 4 | a |

| Family status | ||||||

| Single, % | 36 | 39 | 52 | 51 | 32 | 36 |

| Married, % | 64 | 61 | 48 | 49 | 68 | 64 |

| 3 and less other household members, % | 84 | 83 | 80 | 80 | 85 | 84 |

| More than 3 other household members, % | 16 | 17 | 20 | 20 | 15 | 16 |

| Health | ||||||

| Excellent/very good/good health, % | 87 | 89 | 80 | 88 | 89 | 89 |

| Fair/poor health, % | 13 | 11 | 20 | 12 | 11 | 11 |

| Health expenditures (last 4 months): ≤$100, % | 67 | a | 74 | a | 65 | a |

| Health expenditures (last 4 months): >$100, % | 33 | a | 26 | a | 35 | a |

| State characteristics | ||||||

| No Medicaid expansion, % | 44 | 50 | 48 | 55 | 43 | 49 |

| Medicaid expansion, % | 56 | 50 | 52 | 45 | 57 | 51 |

Data sources: Fall 2013 RAND American Life Panel and March 2013 Current Population Survey, individuals aged 18-64. Notes: Tables displays weighted averages for individuals younger than 65 with non-missing values in the baseline dimensions. The ALP samples were constructed for those individuals participating prior to October 2013 with valid health insurance information in fall 2013 and spring 2015.

No comparable information available in CPS.

Most recent indicated political affiliation in ALP, missing for some participants.

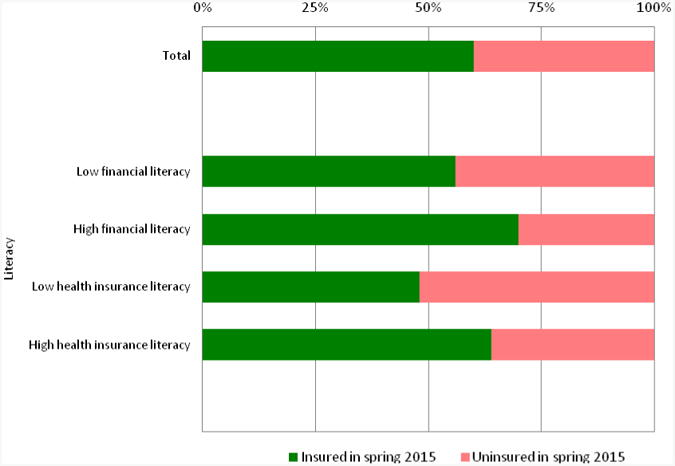

Insurance Coverage among the Previously Uninsured

In this section we investigate who gained insurance, focusing on enrollment in Medicaid and Marketplace insurance among the previously uninsured. Figure 1 displays the insurance status of respondents uninsured at baseline, by our key variables of interest. Overall, 60.2% of this group had obtained insurance by spring 2015. Those with lower levels of financial and health insurance literacy were less likely to have obtained coverage. Figure 1 in the online appendix shows that in the bivariate analysis the more risk averse, Republicans, Hispanics, the less educated, larger households, those with lower health expenditures, and those living in states that opted not to expand Medicaid were less likely to have obtained insurance by spring 2015 (all p<0.05).

Figure 1. Insurance status in spring 2015 for individuals uninsured in fall 2013 by knowledge and preferences.

Data source: RAND American Life Panel, individuals aged 18-64. Notes: Figure displays the share of prior uninsured individuals obtaining health insurance between fall 2013 and spring 2015 by literacy, risk attitude and political affiliation (n=525).

Table 2, Column 1 presents the results from the logit regression modeling the predicted probability that those uninsured at baseline have insurance at follow-up. We found significant associations with the probability of obtaining insurance for our key independent variables: Those with high financial (OR=1.429; 95% CI, 0.934 to 2.185) or health insurance literacy (OR=1.464; 95% CI, 1.025 to 2.093) were more likely to gain insurance than those with low literacy.

Table 2. Characteristics associated with coverage and selection of health insurance for individuals uninsured in fall 2013.

| Any coverage | Type of coverage selected | ||||

|---|---|---|---|---|---|

| Logit (95% CI) | Multinomial logit (95% CI) [n=525] | ||||

| [n=525] | Medicaid | Marketplace | ESI | All other | |

| [n=71] | [n=56] | [n=100] | [n=89] | ||

| Literacy | |||||

| High financial literacy | 1.429* | 1.793 | 1.862* | 1.355 | 1.332 |

| (0.934, 2.185) | (0.794, 4.049) | (0.963, 3.603) | (0.812, 2.262) | (0.648, 2.738) | |

| High health insurance literacy | 1.464** | 1.404 | 1.543 | 1.277 | 1.803*** |

| (1.025, 2.093) | (0.713, 2.766) | (0.658, 3.617) | (0.651, 2.504) | (1.160, 2.801) | |

| Pseudo-R2 | 0.1101 | 0.1724 | |||

Data source: RAND American Life Panel, individuals aged 18-64. Notes: Table displays odds ratios (95% CIs) from logistic regression (column 1) and relative risk ratios (95% CIs) from multinomial logistic regression (columns 2-5) using heteroscedasticity-adjusted standard errors clustered at the state of residence level. Regressions further include controls for gender, age, race and ethnicity, education, income, employment and family status, health and state characteristics, risk aversion, and political affiliation. Results in these dimensions are presented in online appendix table 2. Significance levels:

p < 0.01,

p < 0.05,

p < 0.10.

The magnitude of the effects of financial and health insurance are large relative to key covariates. Take a typical individual without health insurance in 2013. The probability they had health insurance in 2015 was 8.3 percentage points higher if this individual had high instead of low financial literacy. Moreover, it was an additional 9.2 percentage points higher if this individual had high instead of low health insurance literacy. In comparison, having attended at least some college (or more) in comparison to having no degree was associated with a 20-22 percentage point increase in the probability to have insurance in 2015. This shows that a large fraction of this college advantage can be offset by having high financial and health insurance literacy (together 17.5 percentage points) and that financial and health insurance literacy matter for insurance choice above and beyond formal education. Furthermore, the probability of having health insurance in 2015 decreases by 13.1 percentage points for those losing employment between 2013 and 2015 in comparison to those staying employed during that period.

Columns 2-5 in Table 2 report the results of the multinomial logit regression investigating in what types of insurance respondents enrolled in, compared with being uninsured. The uninsured with high financial literacy were more likely to obtain insurance from the Marketplaces compared to staying uninsured (RRR=1.862, 95% CI 0.963 to 3.603). Those with high health insurance literacy tended to obtain insurance from other sources, besides Medicaid, the Marketplace, or employer insurance (RRR=1.803, 95 % CI, 1.160 to 2.801).

Table 2 in the online appendix presents the findings for the demographic controls in the regressions including gender, age, race and ethnicity, education, income, employment and family status, health and state characteristics. The coefficients for these predictors are in line with earlier studies. In addition, it presents results for risk aversion and political leaning. Among the previously uninsured, risk averse individuals are more likely to obtain insurance and Republicans are less likely to obtain insurance.

Insurance Coverage among the General Population

In this section we investigate how insurance coverage changed following the introduction of the ACA Marketplaces, focusing on enrollment in Medicaid and Marketplace insurance among both the previously uninsured and the previously insured. Table 3, Column 1 shows who among our full sample had insurance coverage at follow-up. Those with high financial and health insurance literacy were each more likely (OR=1.598; 95% CI, 1.142 to 2.234 and OR=1.537; 95% CI, 1.221 to 1.933, respectively) to have insurance in 2015 than those with low literacy.

Table 3. Characteristics associated with coverage and selection of health insurance for full sample.

| Any coverage | Type of coverage selected | ||||

|---|---|---|---|---|---|

| Logit (95% CI) | Multinomial logit (95% CI) [n=2,742] | ||||

| [n=2,742] | Medicaid | Marketplace | ESI | All other | |

| [n=274] | [n=148] | [n=1,582] | [n=460] | ||

| Literacy | |||||

| High financial literacy | 1.598*** | 1.697** | 2.140*** | 1.382* | 1.599* |

| (1.142, 2.234) | (1.056, 2.725) | (1.381, 3.316) | (0.940, 2.032) | (0.997, 2.564) | |

| High health insurance literacy | 1.537*** | 1.853*** | 1.987** | 1.407 | 1.420** |

| (1.221, 1.933) | (1.352, 2.540) | (1.146, 3.447) | (0.760, 2.603) | (1.020, 1.976) | |

| Pseudo-R2 | 0.3488 | 0.4008 | |||

Data source: RAND American Life Panel, individuals aged 18-64. Notes: Table displays odds ratios (95% CIs) from logistic regression (column 1) and relative risk ratios (95% CIs) from multinomial logistic regression (columns 2-5) using heteroscedasticity-adjusted standard errors clustered at the state of residence level. Regressions further include controls for prior health insurance coverage type, gender, age, race and ethnicity, education, income, employment and family status, health, state characteristics, risk aversion and political affiliation. Results in these dimensions are presented in online appendix table 3. Significance levels:

p < 0.01,

p < 0.05,

p < 0.10.

Take a typical individual regardless of insurance status in 2013. The probability they had health insurance in 2015 is 1.6 percentage points higher for individuals with high instead of low financial literacy and by 1.7 percentage points for those with high instead of low health insurance literacy. Those with high financial and high health insurance literacy are thus 3.3percentage points more likely to have insurance, which is similar to the calculated marginal effect of having a bachelor's degree (or more) relative to no degree, 3.3 percentage points, or living in a Medicaid expansion state, 3.1 percentage points higher.

In the multinomial logit (Table 3, Columns 2-5), those with high levels of financial or health insurance literacy were more likely (RRR=2.140; 95% CI, 1.381 to 3.316 and RRR=1.987, 95% CI, 1.146 to 3.447, respectively) to be covered via the Marketplaces. Those who in 2015 were covered through employers and the Marketplaces had the highest levels of financial and health insurance literacy in 2013 (Figure 2).

Figure 2. Financial and health insurance literacy by type of health insurance coverage in spring 2015.

Panel A: Financial literacy Panel B: Health insurance literacy

Data source: RAND American Life Panel, individuals aged 18-64. Notes: Figure displays the share of individuals having low or high levels of literacy by type of health insurance coverage in spring 2015 (n=2,742).

Table 3 in the online appendix presents the findings for the demographic controls, risk aversion, and political leaning in the regressions, which are consistent with other studies.

Conclusions

When looking at the decisions of Americans about health insurance in the context of the ACA, it is important to consider not just individuals who were uninsured before 2014, when key provisions of the legislation rolled out, but also the general population, as a number of those who chose to enroll in Medicaid and through the Marketplaces already had coverage in 2013.4 In this study, we were able to look at each of these populations and our dataset enabled us to investigate a wider set of characteristics than other research has done to date. We found that knowledge variables that until now have been unrecognized—health insurance literacy and financial literacy—did, indeed, appear to play a role in the health-insurance choices of our sample between 2013 and 2015. Furthermore, these effects hold even after controlling for other important determinants of insurance coverage such as income and employment, as well as less commonly used but important variables of risk aversion and political affiliation.

As we have demonstrated, it is remarkable that the association of these variables with people's insurance decisions are of the same order of magnitude as standard demographic determinants, such as education and employment status.

The fact that both financial and health insurance literacy were associated with having insurance seems likely to stem from the greater comfort level that more knowledgeable individuals probably have with making health insurance decisions. Those with low health insurance literacy, who answered fewer than 3 of 7 questions correctly, were especially unlikely to have insurance coverage, potentially because they lack experience with the health care system. Because the ACA relies on consumer choice, those who are uninsured and have low health insurance literacy represent a particularly vulnerable population; for them obtaining coverage may be especially difficult. Our findings are robust to alternative specifications using different health measures. It is thus unlikely that our findings for health insurance literacy solely reflect differences in health that are correlated with both the literacy measures and health insurance choices (online Appendix Table 4). Interestingly, the correlation between financial and health insurance literacy is low, suggesting that they may contribute to insurance coverage through slightly different mechanisms.

Our study has several limitations. First, our sample size was relatively small. Despite this, we find significant results. Second, our survey had a low cumulative response rate. The rate was on par, however, with other nationally representative surveys conducted by non-governmental organizations that have provided early pictures of the impact of the ACA including others reported in this journal,8 and estimates from the American Life Panel closely track administrative data.4 The trade-off for the small sample size and low response rate was access to data on financial and health insurance literacy—variables that are usually lacking in data from federal surveys with larger sample sizes and higher cumulative response rates. Third, we relied on survey data, which may be biased due to sample selection or self-reporting. But this does not necessarily distort the accuracy of findings: The American Life Panel provided highly accurate predictions in the 2012 presidential elections, for example.18

We focus on two points in time and thus in this work did not distinguish between those who experienced one or multiple health insurance transitions. Health insurance and financial literacy might also contribute to maintaining consistent insurance coverage over this period.

Understanding which factors affect an individual's decision to get health insurance and to enroll via Medicaid versus the Marketplaces versus other channels can help to inform health policy and better target and design outreach and consumer-education programs. Our findings suggest that the impediments to obtaining coverage go beyond the primarily socio-demographic ones which have been established as contributing to gaps in coverage. In that light, policies and programs designed to further reduce the numbers of uninsured—especially through Medicaid and the Marketplaces—should take into account not just ethnicity, employment status, and income, but levels of financial literacy and health insurance literacy. While we cannot exclude that our results on the literacy measures may be – at least partly – capturing the influence of third factors which we cannot observe, the results still suggest that low financial and health insurance literacy predict remaining uninsured. Limited health insurance and financial literacy may make it difficult for consumers to assess whether insurance premiums are “worth it”. Any programs designed to further decrease the number of uninsured adults should take into account that these individuals may have low health insurance and financial literacy. Whether changes to the federal healthcare.gov Marketplace designed to simplify decision making during the 2016 open enrollment period will be enough to help these groups gain coverage remains an open question.

Supplementary Material

Acknowledgments

This research was supported by grants R21-AG044737 and 5P30AG024962 from the National Institute on Aging and by the Bing Center for Health Economics at the RAND Corporation. The authors have no conflicts of interest. We thank Susan Bohandy Ph.D. for her comments on our manuscript and the ALP Technical Team. Part of this research was conducted while Hoerl was visiting the University of Southern California.

Footnotes

The authors have no conflicts of interest.

Contributor Information

Maximiliane Hoerl, Department of Economics, University of Munich, Ludwigstr. 33, D-80539 Munich, Germany, Phone: +49 89 2180 5377, Fax: +4989 2180 992459

Amelie Wuppermann, Department of Economics, University of Munich, Ludwigstr. 33, D-80539 Munich, Germany, Phone: +49 89 2180 6291, Fax: +4989 2180 3954

Silvia H. Barcellos, Center for Economic and Social Research, University of Southern California, 635 Downey Way, Los Angeles, CA 90089-3332, Phone: +1 213 821 2732, Fax: +1 213 821 2716

Sebastian Bauhoff, Center for Global Development, 2055 L Street NW, Washington, DC 20036, Phone: +1 202 416 4000, Fax: +1 202 416 4050

Joachim K. Winter, Department of Economics, University of Munich, Ludwigstr. 33, D-80539 Munich, Germany, Phone: +49 89 2180 2459, Fax: +4989 2180 992459

Katherine G Carman, The RAND Corporation, 1776 Main Street, P.O. Box 2138, Santa Monica, CA 90407-2138, Phone: +1 310 393 0411 x6187, Fax: +1 310 260 8176

References

- 1.Sommers BD, Musco T, Finegold K, et al. Health reform and changes in health insurance coverage in 2014. N Engl J Med. 2014;371(9):867–74. doi: 10.1056/NEJMsr1406753. [DOI] [PubMed] [Google Scholar]

- 2.Collins SR, Rasmussen PW, Doty MM. Gaining ground: Americans' health insurance coverage and access to care after the Affordable Care Act's first open enrollment period. New York, NY: Commonwealth Fund; 2014. http://www.commonwealthfund.org/publications/issue-briefs/2014/jul/health-coverage-access-aca. [PubMed] [Google Scholar]

- 3.Long SK, Karpman M, Shartzer A, et al. Taking stock: Health insurance coverage under the ACA as of September 2014. Washington, DC: Urban Institute; 2014. http://hrms.urban.org/briefs/health-insurance-coverage-under-the-aca-as-of-september-2014.html. [Google Scholar]

- 4.Carman KG, Eibner C, Paddock SM. Trends in health insurance enrollment, 2013-15. Health Aff. 2015;34(6) doi: 10.1377/hlthaff.2015.0266. [DOI] [PubMed] [Google Scholar]

- 5.Vistnes J, Cohen SB. Transitions in health insurance coverage over time, 2012-2014 (selected intervals): Estimates for the US civilian noninstitutionalized adult population under the age 65. Rockville, MD: Agency for Healthcare Research and Quality; 2015. Statistical brief no. 467. [PubMed] [Google Scholar]

- 6.Witters D. In U.S., uninsured rates continue to drop in most states. Gallup. 2015 Aug 10; http://www.gallup.com/poll/184514/uninsured-rates-continue-drop-states.aspx.

- 7.Smith JC, Medalia C. Health insurance coverage in the United States: 2014. 2015 Sep; U.S. Census Bureau Report P60-253. https://www.census.gov/content/dam/Census/library/publications/2015/demo/p60-253.pdf.

- 8.Sommers BD, Gunja MZ, Finegold K, et al. Changes in Self-reported Insurance Coverage, Access to Care, and Health Under the Affordable Care Act. JAMA. 2015;314(4):366–374. doi: 10.1001/jama.2015.8421. [DOI] [PubMed] [Google Scholar]

- 9.Van Rooij M, Lusardi A, Alessie R. Financial literacy and stock market participation. J Financ Econ. 2011;101(2):449–472. [Google Scholar]

- 10.Lusardi A, Mitchell OS. Financial literacy and retirement planning in the United States. J Pension Econ Financ 2011. 2011;10(4):509–25. doi: 10.1017/S1474747211000448. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11.Lusardi A, de Bassa Scheresberg C. Financial literacy and high-cost borrowing in the United States. National Bureau of Economic Research; 2013. Working Paper 18969. [Google Scholar]

- 12.Cutler DM, Finkelstein A, McGarry K. Preference heterogeneity and insurance markets: Explaining a puzzle of insurance. Am Econ Rev Pap Proc. 2008;98(2):157–162. doi: 10.1257/aer.98.2.157. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Barcellos SH, Wuppermann AC, Carman KG, et al. Preparedness of Americans for the Affordable Care Act. Proc Natl Acad Sci U S A. 2014;111(15):5497–5502. doi: 10.1073/pnas.1320488111. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 14.California's Previously Uninsured After The ACA's Second Open Enrollment Period. Washington, DC: Kaiser Family Foundation; 2015. http://kff.org/health-reform/report/californias-previously-uninsured-after-the-acas-second-open-enrollment-period/ [Google Scholar]

- 15.More information is available at https://alpdata.rand.org/.

- 16.King M, Ruggles S, Alexander JT, et al. Integrated Public Use Microdata Series, Current Population Survey: Version 3.0. Minneapolis, MN: Minnesota Population Center; 2010. Machine-readable database. [Google Scholar]

- 17.Carman KG, Eibner C. Insurance transitions following the first ACA Open Enrollment Period. 2015 RAND Research Report RR-948-RC. http://www.rand.org/pubs/research_reports/RR948.html. [PMC free article] [PubMed]

- 18.Gutsche TL, Kapteyn A, Meijer E, et al. The RAND Continuous 2012 Presidential Election Poll. Public Opin Q. 2014;78(S1):233–254. [Google Scholar]

- 19.Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation. Health insurance Marketplaces 2015 open enrollment period: March enrollment report. Washington, DC: HHS; 2015. http://aspe.hhs.gov/health/reports/2015/MarketPlaceEnrollment/Mar2015/ib_2015mar_enrollment.pdf. [Google Scholar]

- 20.Centers for Medicare and Medicaid Services. Medicaid and CHIP: December 2014 monthly applications, eligibility determinations and enrollment report. Baltimore, MD: CMS; 2015. http://medicaid.gov/medicaid-chip-program-information/program-information/downloads/december-2014-enrollment-report.pdf. [Google Scholar]

- 21.Barcellos SH, Wuppermann AC, Carman KG, et al. Preparedness of Americans for the Affordable Care Act. Proc Natl Acad Sci U S A. 2014;111(15):5497–5502. doi: 10.1073/pnas.1320488111. for a description of the health insurance literacy questions. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 22.Heiss F, McFadden D, Winter J. Who failed to enroll in Medicare Part D, and why? Early results. Health Aff (Project Hope) 2006;25(5) doi: 10.1377/hlthaff.25.w344. [DOI] [PubMed] [Google Scholar]

- 23.Bhargava S, Loewenstein G, Sydnor J. Do individuals make sensible health insurance decisions? Evidence from a menu with dominated options. Q J Econ. forthcoming. [Google Scholar]

- 24.Baicker K, Congdon WJ, Mullainathan S. Health insurance coverage and take-up: Lessons from behavioral economics. Milbank Q. 2012;9(1):107–134. doi: 10.1111/j.1468-0009.2011.00656.x. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 25.Liebmann J, Zeckhauser R. Simple humans, complex insurance, subtle subsidies. 2008 NBER Working Paper 14330. [Google Scholar]

- 26.Dohmen T, Falk A, Huffman D, et al. Individual risk attitudes: Measurement, determinants, and behavioral consequences. J Eur Econ Assoc. 2011;9(3):522–550. [Google Scholar]

- 27.De Meza D, Webb D. Advantageous selection in insurance markets. RJE. 2001;32(2):249–262. [Google Scholar]

- 28.Kaiser Health Tracking Poll: April 2015. Washington, DC: Kaiser Family Foundation; 2015. http://kff.org/health-reform/poll-finding/kaiser-health-tracking-poll-april-2015/ [Google Scholar]

- 29.Data note: Predictors of positive and negative attitudes towards the ACA among non-group insurance enrollees. Washington, DC: Kaiser Family Foundation; 2015. http://kff.org/health-reform/poll-finding/data-note-predictors-of-positive-and-negative-attitudes-towards-the-aca-among-non-group-insurance-enrollees/ [Google Scholar]

- 30.Blendon RJ, Benson JM. Voters and the Affordable Care Act in the 2014 Election. N Engl J Med. 2014;371(20):e(31)1–e(31)7. doi: 10.1056/NEJMsr1412118. [DOI] [PubMed] [Google Scholar]

- 31.Newport F. Politics Affect Uninsured Americans' Insurance Intentions. Gallup. 2014 Mar 28; http://www.gallup.com/poll/168143/politics-affect-uninsured-americans-insurance-intentions.aspx.

- 32.Sommers BD, Maylone B, Nguyen KH, Blendon RJ, Epstein AM. The Impact Of State Policies On ACA Applications And Enrollment Among Low-Income Adults In Arkansas, Kentucky, And Texas. Health Aff. 2015;34(6):1010–1018. doi: 10.1377/hlthaff.2015.0215. [DOI] [PubMed] [Google Scholar]

- 33.StataCorp. Stata Statistical Software: Release 14. College Station, TX: StataCorp LP; 2015. [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.