Abstract

25 years is a relatively short period of time for a medical technology to become a standard of care impacting the treatment of millions of people every year. Yet 25 years ago there were no OCT companies, no OCT products, no OCT markets, and only one journal article published using the term OCT (optical coherence tomography). OCT has had a tremendous scientific, clinical, and economic impact on society. Today, it is estimated that there are ~30 Million OCT imaging procedures performed worldwide every year and the OCT system market is approaching $1B per year. OCT has helped diagnose patients with retinal disease at early treatable stages, preventing or greatly reducing irreversible vision loss. The technology has facilitated pharmaceutical development and contributed to fundamental understanding of disease mechanisms in multiple fields. The invention and translation of OCT from fundamental research to daily clinical practice would not have been possible without a complex ecosystem involving interaction among physics, engineering, and clinical medicine; government funding of fundamental and clinical research; collaborative and competitive research in the academic sector; entrepreneurship and industry; addressing real clinical needs; harnessing the innovation that occurs at the boundaries of disciplines; and economic and societal impact. This invited review paper discusses the translation of OCT from fundamental research to clinical practice and commercial impact, as well as describes the ecosystem that helped power OCT to where it is today and will continue to drive future advances. While OCT is an example of a technology that has had a powerful impact, there are many biomedical technologies which are poised for translation to clinical practice, and it is our hope that highlighting this ecosystem will help accelerate their translation and clinical impact.

OCIS codes: (170.3880) Medical and biological imaging, (170.4500) Optical coherence tomography

1. Introduction

25 years is a relatively short period of time for a medical technology to become a standard of care impacting the treatment of millions of people every year. Yet 25 years ago there were no OCT companies, no OCT products, no OCT markets, and only one journal article published using the term OCT (optical coherence tomography) [1]. Today there are 100’s of companies supplying OCT systems and components; 1,000’s of researchers at leading international universities advancing the frontiers of OCT; over 10,000 OCT journal articles on clinical, fundamental scientific, and materials applications; tens of thousands of workers employed designing, manufacturing, or operating ~50,000 installed OCT systems; over $500M of venture capital and corporate R&D investment developing OCT related products; over $500M of government funding towards OCT research; and an OCT system market approaching $1B/year [2–6]. OCT played, and continues to play, a key role in the development of vision saving pharmaceutical treatments [7–9] as well as in reducing healthcare costs, including ~$10B in estimated Medicare savings in the US [9]. Most importantly, every year, tens of millions of OCT procedures are performed, nearly one every few seconds, to make important clinical decisions for patients suffering potentially blinding ophthalmic disease [5–9]. In addition OCT is being used to advance clinical understanding and treatments in cardiovascular disease and cancer, leading causes of death in the industrialized world.

Biomedical technologies which impact patient care face unique challenges that differ from technologies in the research or consumer market. Adoption in clinical medicine is evidence-based, requiring demonstration of diagnostic sensitivity and specificity, therapeutic effectiveness and cost effectiveness. Clinical medicine involves complex regulatory and reimbursement requirements. At the same time, the societal and quality of life impact of improvements in clinical medicine is a primary goal and motivation for all who work in the biomedical community. The translation of OCT from fundamental research to daily clinical practice would not have been possible without a complex ecosystem that involves the interaction between: physics, engineering and clinical medicine; government funding of fundamental and clinical research; collaborative and competitive research in the academic sector; entrepreneurship and industry; addressing real clinical needs; harnessing the innovation that occurs at the boundaries of disciplines; and having economic and societal impact. This invited review paper will discuss the translation of OCT from fundamental research to clinical practice and commercial impact as well as describe the ecosystem that helped power OCT to where it is today and will continue to drive advances in the future. While OCT is an example of a technology that has had a powerful impact, there are many biomedical technologies which are poised for translation to clinical practice, and it is our hope that highlighting this ecosystem will help accelerate their translation and clinical impact.

2. The physics of OCT

Figure 1 illustrates some of the key system concepts of OCT including: time domain OCT (TD-OCT), spectral domain OCT (SD-OCT), and swept source OCT (SS-OCT) detection; axial and lateral image resolution and depth of field; and how 2D images (B-scans) and 3D volumetric images are generated from 1D axial scans (A-scans). There are many closely related embodiments of OCT including: optical coherence microscopy (OCM), full-field OCT (FF-OCT), optical coherence elastography (OCE), optical coherence tomography angiography (OCT-A), anatomical OCT (aOCT), optical coherence photoacoustic microscopy (OC-PAM), micro optical coherence tomography (μOCT), and others. One of the reasons OCT has been so successful is because underlying physics of the interferometric detection process that enables near quantum-limited sensitivity, achieving detection of less than 1:1010 of the sample incident power (due to the heterodyne optical gain), high dynamic range (since signal electric field is detected instead of intensity), and high lateral and axial resolution (where coherence gating rejects unwanted scattered light orders of magnitude more than confocal gating). This article will not discuss the details OCT systems, which are described in many existing references [10], except to note that these impressive specifications can be achieved in a system that is relatively low-cost and compact and which can image at depths and resolutions that are relevant to many diseases and industrial applications.

Fig. 1.

Key concepts of OCT including: TD-OCT, SD-OCT, and SS-OCT detection; axial and lateral image resolution and depth of field; and how 2D images (B-scan) and 3D volumetric images are generated from 1D axial scans (A-scans).

3. Government funding

It is unlikely that OCT would be where it is today if it wasn’t for government funding of fundamental and clinical research. OCT grew out of fundamental research in ultrafast optics which was initially funded by the Air Force Office of Scientific Research (AFOSR) [3, 11]. The AFOSR Medical Free Electron Laser (MFEL) program also supported early technology development and translation. The National Institutes of Health supported a multitude of OCT clinical studies as well as fundamental investigations in disease pathogenesis [2].

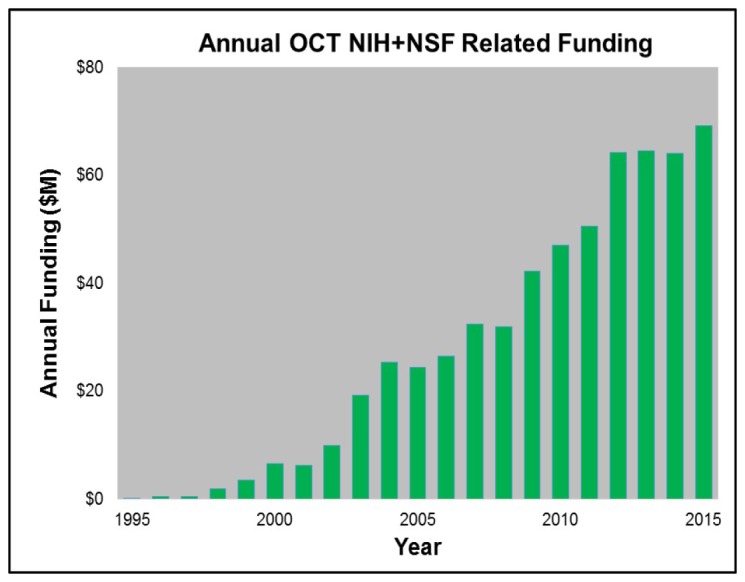

It is difficult to accurately survey the historical worldwide government funding of OCT research dating back to 1990 [2]. There are many countries to consider including: United States, Europe, China, Japan, Russia, and Canada, and there are few reliable databases that are accessible. The funding of OCT in the US can be used as a proxy for the increase in worldwide funding. The NIH and NSF have good databases and also the US historically is a significant component of worldwide research funding. Figure 2 shows early NIH and NSF funding, determined by searching the NIH RePORTER and NSF Award databases using the term “optical coherence tomography” in the title and abstract. The funding totals ~$600M with the vast majority (over 90%) from the NIH. It should be noted that this is an upper bound since many of these programs utilize OCT, rather than developing OCT technology or clinical applications. If OCT in the “title only” is used as the only search criterion, the number drops to about $90M, which is probably more indicative of the NIH and NSF funding for OCT technology. Of course, governments from all over the world have invested in OCT research over the past decade and total funding has likely exceeded $500M [2]. Although small compared to total healthcare costs or entitlement programs, this is a large investment of tax-payer supported research dollars. Government funding was, and remains, essential for the advancement of OCT and biomedicine in general. And today, more than ever, as the discretionary portion of the US budget is under pressure [12], there are increasing demands on those dollars and even calls to cut government research budgets. This places a responsibility on all to make sure that tax payer funds are being invested wisely. As we describe later, it is our opinion that the return on this government investment of taxpayer funds has been outstanding from an economic perspective, from the perspective of advancing science and clinical understanding, and from the perspective of improving patient care and quality of life.

Fig. 2.

Yearly NIH and NSF funding of OCT related research which cumulatively totals ~$600M.

4. Collaborative and competitive researchers

Government funding enables teams of researchers to pursue creative ideas. The dual competitive and collaborative nature of academic scientific research creates a tension between competing for research funding, while sharing results in conferences and publications. This duality contributed to rapid advancement in the field of OCT. As mentioned earlier, the first paper published using the term “OCT” appeared in Science in 1991 and arose from a collaboration among investigators at MIT, MIT Lincoln Laboratory, and Harvard Medical School [1].

Figure 3A shows that by 1998, only 7 years later, there was a significant jump, to an estimated 123 “OCT” publications. This timepoint was 2 years after the release of the first commercial ophthalmic OCT product and also coincides with the early studies which investigated OCT in cardiology, pathology, oncology, surgical guidance and other applications. This figure was obtained by searching the PubMed database for journal articles with the term “OCT” in the title or abstract and graphically plotting the results with the node size depending on the number of publications of a particular institution and the link size depending on the joint publications between two or more institutions [3]. We note that the search term “Optical Coherence Tomography” which was used to generate the data shown in Fig. 2, Fig. 3, and Fig. 4 could be broadened to include terms such as “optical tomography”, “time domain optical ranging”, “low coherence interferometry”, “low coherence ocular biometry”, “optical coherence domain reflectometry” or even “white light interferometry”. This is a limitation in the search and may result in bias, however broadening the search results in an ambiguous scope and starting point. We used the term OCT because it had a well-defined starting point and is the standard well understood term in research and industry for this technology. However it is important to note OCT developed from many fields including femtosecond optics, low coherence interferometry and telecommunications. The figures illustrate how collaborations expanded and the number of independent groups working on OCT increased. A budding global network of researchers publishing and sharing their creative ideas is clearly evident. Figure 3B shows a similar graph of the world-wide footprint of OCT in 2015 as estimated by a combination of manual and automated machine learning from the website www.octnews.org. There are currently ~20,000 scientific publications and there is worldwide collaboration with innovative scientists, engineers, and clinicians from ~500 organizations. This demonstrates the highly collaborative, rapidly moving, and global nature of science.

Fig. 3.

(A, top) In 1998 there were 123 cumulative scientific publications with the term “OCT” in the title or abstract in as estimated from the PubMed database. (B, bottom) Currently there are ~20,000 cumulative scientific, business, product publications with the term “OCT” as estimated from the website: www.octnews.org. In the figures shown above and as noted below, if terms the search terms were broadened the relative sizes of the circles and links would change.

Fig. 4.

Annual PubMed publications with the term OCT in the title or abstract, along with a categorization of topic / clinical specialty. Dates where the first commercial clinical products were introduced are indicated. Note in some cases there were earlier commercial releases of products, but some companies did not achieve positive revenues and left the market. Since scientific and clinical publications are a bellwether for scientific and clinical knowledge as well as clinical adoption, this data shows the key role of industry. There are ~20,000 publications in a wide range of clinical specialties as well as other applications.

Figure 4 shows an estimate of the number of scientific publications with the term “OCT” in the title or abstract as determined from the PubMed database with a manual categorization of the topic or clinical specialty [3]. Cumulatively there are ~20,000 scientific publications and there is a clear trend with the number of publications continuing to grow by ~3,500 each year. While it is sometimes difficult to precisely categorize the publications, the legend shows categories with the largest publication volume. Ophthalmology is the dominant category, followed by cardiology, general OCT technology, dermatology, and gastroenterology. Not coincidently, these four clinical specialties coincide with markets where OCT has been commercialized. It is clear that the release of commercial instruments is a catalyst for clinical research and publications, since it puts this technology into the hands of clinician-scientists who explore and develop clinical applications, perform large scale studies that evaluate accuracy and efficacy. This provides clinical and economic evidence that is needed for adoption and routine use by clinicians on the front lines of patient care.

5. Innovation at the boundaries

Innovation often occurs at the boundaries of fields and disciplines. Leveraging ideas, knowledge, and technology from one field into another is one of the richest sources of innovation. The clearest example of this in OCT is the adoption and leveraging of technology and ideas from fiber optic telecommunications. The lasers, detectors, many of the system concepts, and the fiber optic components used in OCT largely came from telecom. The heart of an OCT system looks very much like coherent fiber optical data communication systems which have been deployed worldwide and power global telecommunications. Without the billions of dollars of development in the fiber optical communications and other industries, OCT would not be where it is today and could not advance to the exciting places that it will reach in the future. Today’s OCT systems are more than 1,000 times faster than they were 25 years ago. These high speeds present challenges for high speed electronics engineers who adapt the latest ideas from the electronics industry. High speeds also create unique mechanical challenges for the scanning optics used in many OCT endoscopic probes and microscope systems, fostering the advancement of MEMs-based µ-motors and other technologies. OCT produces some of the largest image data sets in medicine, which challenge signal processing and software engineers to collect and visualize this data using technology derived from gaming and other medical market sectors. Many OCT applications involve miniature optical imaging probes that have to fit into torturous channels such as the coronary arteries or biopsy ports of endoscopes while performing high speed scanning, which challenge mechanical and medical device designers. OCT is a rich combination of laser technology, photonics, electronics, software, mechanical design, medical devices, and clinical medicine. The multidisciplinary nature of OCT, as it crosses so many boundaries, is also one of the reasons there has been so much innovation, and more innovation is still to come.

6. Clinical needs

Although it was impossible to predict 25 years ago that OCT would be where it is today, there was a clear unmet clinical need in ophthalmology. In the 1990s an ophthalmologist had excellent views of the surface of the retina from ophthalmic examination, fundus photography or scanning laser ophthalmoscopy, but there was limited information about depth and cross sectional structure. The possibility of generating cross sectional images of retinal architecture, similar to histology, but non-invasively and in real-time, was unprecedented at that time. OCT could perform cross sectional imaging at resolutions that were previously impossible to obtain in-vivo, enabling diagnosis of eye disease at early stages before irreversible loss of vision occurred. The ability to repeatedly image retinal pathology to assess disease progression and response to therapy contributed to the understanding of disease mechanisms and accelerated the development of new sight-preserving pharmaceutical therapies [7–9].

Figure 5 shows a reprint of the first OCT images in the 1991 Science paper entitled “Optical Coherence Tomography” [1]. It is interesting to note that the first OCT images were in ophthalmology and cardiology which have become the two largest and most important clinical applications and economic drivers of OCT. Figure 6 shows a photograph of a prototype instrument similar to the one used for the first in vivo ophthalmic human OCT studies at MIT and Tufts University School of Medicine. The images in Fig. 5 were performed using a laboratory benchtop instrument and required several minutes to acquire a single image. The prototype in Fig. 6, developed at MIT Lincoln Laboratory, was portable, had a patient interface for retinal scanning and could acquire an image in a few seconds, enabling studies in patients. Despite the simplicity of this system by today’s standards, it enabled the first clinical studies in glaucoma, diabetic retinopathy, and macular degeneration, imaging over 5,000 patients at the New England Eye Center. This illustrates the important role of engineering in advancing fundamental research to the first steps of clinical translation.

Fig. 5.

The first OCT images published in the journal Science in 1991 [1]. (A) Optical coherence tomography of the human retina ex vivo and corresponding histology. (B) Optical coherence tomography of human artery ex vivo and corresponding histology. Ophthalmology and cardiology have become the two largest clinical applications on OCT.

Fig. 6.

The first clinical ophthalmic imaging OCT prototype designed at MIT Lincoln Laboratories and used at the New England Eye Center. Left OCT imaging engine, Right: slit lamp modified to support in vivo OCT (picture from August 1992). Image courtesy MIT Lincoln Laboratory.

By 1996 the first clinical atlas of OCT in ophthalmology was published and became an important milestone in the clinical translation process [13]. It provided a guide for clinicians to interpret this new imaging modality, pointing out the important role of education which is required for clinical adoption. Although commercialization, regulatory and reimbursement hurdles remained to be addressed, at this point it seemed clear that OCT had a very bright future. One of the reasons OCT has been so successful is because it addressed clinical needs and did so in a cost effective way. OCT promises to continue to grow in economic and healthcare impact because there are a multitude of remaining clinical applications and challenges in detecting, treating and understanding major diseases where the imaging capabilities of OCT may play an important role.

7. Entrepreneurship and industry

No technology can advance to impact patient care without industry playing a major role. It requires tremendous effort, money, and time to transform a research prototype into a robust clinical product. This process requires a major multidisciplinary effort and the ‘silent’ innovation which occurs along the way is often under appreciated. Figure 7 shows an estimate of the growing number of system companies that have entered the OCT space over the past 25 years. There are many more OCT subsystem and component companies that are not listed. It is noteworthy that ~40% of these companies are associated with institutions receiving government funding for OCT research [2]. This is evidence that taxpayer dollars are having a positive translational impact on society. Approximately 75% of the OCT companies today are, or originated as, startups (as indicated by the blue dots). This is a clear testament to entrepreneurial spirit and the positive impact entrepreneurship can have on expediting the translation of important research into clinical care. The first OCT startup in 1992, Advanced Ophthalmic Devices, was in ophthalmology and grew out of an MIT and Tufts University collaboration. It was founded by Eric Swanson, James Fujimoto, and Carmen Puliafito and was acquired two years later by Zeiss, which invested substantial financial, engineering and marketing resources to bring OCT to the clinical ophthalmology market. The second startup, Coherent Diagnostic Technologies (later renamed LightLab Imaging), founded in 1998 by Eric Swanson, James Fujimoto, and Mark Brezinski, was in cardiology and grew out of an MIT and Harvard collaboration. LightLab Imaging was acquired by Goodman Corporation in 2002, by St. Jude Medical in 2009, and then by Abbot Medical in 2016. Today, Zeiss and St. Jude Medical remain the leaders in their respective OCT markets and together dominate a large fraction of the total worldwide OCT system revenue. In both cases, the risk taken by these startups and the businesses that acquired them dramatically accelerated the development and clinical adoption of OCT, by perhaps nearly a decade. This, in turn, benefited the diagnosis and treatment of patients, accelerated pharmaceutical development, and the understanding of disease pathogenesis.

Fig. 7.

Estimate of the growing number of OCT system companies over the past 25 years. There are many more subsystem and component companies not listed. Blue dots represent companies that began or still are startups and red dots are existing companies that started OCT programs internally. A few of these companies have been acquired or gone out of business.

Each of the companies shown in Fig. 7 has a slightly different history and perspective on the challenges and rewards of their entry and progress in the OCT market. However one commonality is that it requires a great deal of time, money, and effort to develop a product and bring a research prototype (such as that shown in Fig. 6) to clinical acceptance and economic success. In many cases companies required 3-5 years to get to their first product release or first customer shipment (version 1.0). After that there can still be many more years working with physicians and regulatory bodies, performing clinical studies to develop clinical indications, assess efficacy and demonstrate economic benefit before a product achieves success. Typically this phase requires multiple product iterations to move beyond the early adopter, clinician scientist community, to be used in routine practice and become a successful product. Figure 8 shows a qualitative view of the typical product, clinical/regulatory, and business milestones. As shown, it can take well over 10 years for a new technology to become a clinically and economically viable product, which has been the case for OCT in ophthalmology and cardiology. Additional metrics are discussed in the next section.

Fig. 8.

A qualitative view of the phases and milestones of medical device products. Compared to other technologies, medical products face a longer path to market because of the need to gather clinical evidence and obtain regulatory and reimbursement approval. Pioneering firms which introduce new technologies usually have a more difficult path than later entrants who are following established clinical applications.

Ironically, these timetables can be much shorter for competitors who enter an established market where clinical evidence already exists, and regulatory and reimbursement pathways have been paved by the first company to develop the market. In this sense, being a pioneer is much more challenging and risky than being second or third in the market. At the same time entering a market later, results in a battle to gain market share against an established incumbent. Both scenarios point to the importance of intellectual property (IP).

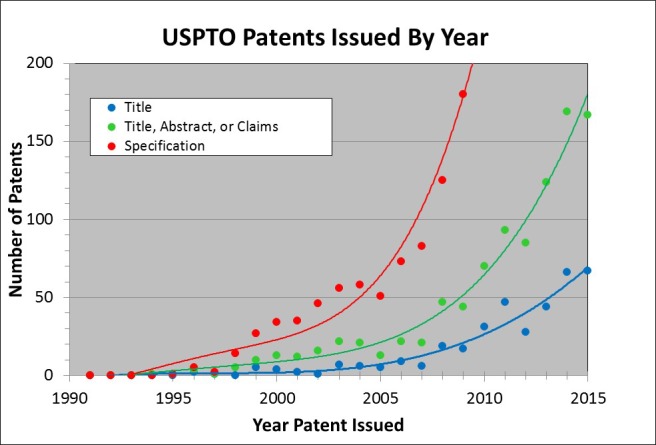

Patents / intellectual property (IP) are an important component of the translational ecosystem. There are multiple reasons for filing patents and developing an IP portfolio including generating licensing revenue for academic institutions, protecting a company’s investment in product and market development by creating barriers to competitors, as well as ensuring freedom for businesses to operate when competitors have related IP. Figure 9 shows US patents issued by year with the term “Optical Coherence Tomography” in the Title (blue), Title, Abstract, or Claims (green), and Specification (Red) [14]. There are similar trends on issued patents in other countries and there are many additional patents that are explicitly or incidentally related to OCT that do not mention the word “Optical Coherence Tomography” in the title or abstract. Cumulatively there are ~1,000 US issued patents since 1990 with the term “Optical Coherence Tomography” in the title, abstract, or claims. It is very difficult to have a new fundamental patent (one that is broad and difficult for competitors to overcome) issue given that OCT is nearly 25 years old. In fact, many of the fundamental patents from MIT and elsewhere filed in early years covering time-domain OCT, swept source OCT, OCT probes (e.g. endoscopes, catheters, and guidewires), and full field OCT have expired [15–21]. Patents play a particularly prominent role in startup companies as a barrier to market entry by competitors, protecting the investment required to develop new technology, address regulatory and reimbursement hurdles, and create the clinical market. It is clear that the number of OCT patents generated in academics and industry is increasing. This is due to many factors, including the fact that the underlying commercial OCT market is growing, the importance funding agencies are placing on translation and IP, as well as the general high-tech industry-wide increase in the importance of patents.

Fig. 9.

US Patents issued by year with the term “Optical Coherence Tomography” in the Title (blue), Title, Abstract, or Claims (green), and Specification (Red). Cumulatively there are ~1,000 US Issued patents since 1990 with the term “Optical Coherence Tomography” in the title, abstract, or claims.

The lengthy timescale, high costs, uncertain and challenging route to regulatory and reimbursement approval and ultimate growth, represent a barrier to medical technology start-ups attracting investment funding from the Venture Capital industry. There has been well over $500M in cumulative venture and corporate R&D investment in OCT companies. Today there are increased challenges facing OCT entrepreneurs competing for VC investment compared with start-ups developing software based products such as smart-phone apps, which potentially offer VCs rapid growth, lower initial investment costs, and more exit opportunities. In spite of these challenges, OCT offers powerful long-term positive global societal impact through improved patient outcomes and research into disease mechanisms, diagnosis and therapy. Therefore, government funding in early translational stages, alongside Venture Capital is of critical importance. The impact of government investment is discussed in the next section.

8. Impact

In order to retain innovative people working in a field, to continue government investment of tax payer dollars, and to keep entrepreneurs and industry engaged, there must be an important mission and there must be impact. OCT has an important mission, to improve patient care and advance scientific and clinical knowledge, while also having economic, scientific and clinical impact. Figures 10, Fig. 14, Fig. 16, and Fig. 18 below show examples of this impact in the form of metrics for ophthalmology, cardiology, dermatology, and gastroenterology - four representative OCT markets which have commercial regulatory cleared products. For each example, the estimated number of OCT publications is shown in the upper left, the estimated number of OCT procedures is lower left, the estimated number of companies making system OCT products is upper right, and the estimated OCT system market is lower right. In Fig. 10, Fig. 14, Fig. 16, and Fig. 18 publications were estimated by manual sorting and categorization of PubMed articles that mention “Optical Coherence Tomography” in the title or abstract. Numbers of procedures were estimated using Medicare data for ophthalmology [5,6] and for the other fields procedure numbers were estimated using information from executives at the leading OCT system companies. System revenue was estimated using similar methods.

Fig. 10.

Ophthalmic OCT metrics illustrating: the estimated number of OCT publications, yearly US OCT procedures, growing number of OCT companies, and OCT system revenue. The commercial introduction of SD-OCT occurred after substantial growth of TD-OCT. The revenue plot does not include technology associated with the ocular biometry which has technological commonality with OCT. Ophthalmic OCT procedures were normalized to account for the CPT code change in 2010 (discussed below).

Fig. 14.

Cardiovascular OCT metrics illustrating: the estimated number of OCT publications, yearly WW OCT procedures, growing number of OCT companies, and OCT system and disposable revenue. Note the commercial introduction of SS-OCT after substantial success of TD-OCT. Note CardioSpectra/Volcano entered the market in ~2005 but ended their effort around 2013.

Fig. 16.

Dermatology OCT metrics illustrating: the estimated number of OCT publications, yearly WW OCT procedures, growing number of OCT companies, and growing OCT system revenue (y-axis intentionally left blank). Note ISIS entered the market in ~1999 but ended their effort around 2004. Note: the numerical axis is missing on the annual revenue due to its confidential nature being dominated by only one company.

Fig. 18.

Gastroenterology OCT metrics illustrating: the estimated number of OCT publications, yearly WW OCT procedures, growing number of OCT companies, and growing OCT system and disposable revenue (y-axis intentionally left blank). Note both Lightlab and Imalux entered the market but left as described above. Note that the annual revenue is not labelled because it is attributed predominantly to one company and is confidential.

Figure 10 shows examples of ophthalmic OCT metrics. In ophthalmology, the first market to have a commercial OCT product release in 1996, strong growth in publications, procedures, revenues and competition can be seen. The number of yearly OCT procedures in the US is estimated to be ~15M/year and ~30M/year worldwide, which equates to one procedure every few seconds [5,6]. It is noteworthy that TD-OCT had already grown to become a standard of care with more than ~$50M/year in revenue and more than ~10M procedures per year worldwide by 2006 when SD-OCT was first introduced commercially by Optovue. Multiple ophthalmic OCT companies entered the market about the same time as Optovue, as can been seen from Fig. 10. The substantial existing market, established clinical evidence, regulatory approvals, and standard of care that were developed over the ten year period from 1996 to 2006 using TD-OCT, combined with the improved performance offered by SD-OCT and the desire by new companies to enter the marketplace facilitated the rapid adoption of SD-OCT. Multiple companies eventually released SD-OCT products and growth continued. SD-OCT offered dramatically increased sensitivity (10X to 50X more than previous TD-OCT). The sensitivity advantage afforded increased imaging speed, higher pixel density images, and improved area coverage. This further improved the ability to detect, monitor, and manage eye disease, accelerating the adoption of OCT in ophthalmology. More recently the revenue growth of ophthalmic OCT has flattened, likely due to saturation of the ophthalmology market and increased healthcare cost pressures. However, the introduction of OCT angiography (OCT-A) has generated intense interest in the ophthalmic research community. This and other advances promise to increase growth as well as further improve understand of disease mechanisms and benefit patient care.

Carl Zeiss Meditec was first to release a commercial ophthalmic TD-OCT product in 1996 and has released many follow-on ophthalmic TD-OCT and SD-OCT products. In Q4 2016, Zeiss was first to receive US FDA clearance for an SS-OCT system for advanced retina research. The Zeiss SS-OCT operates at 1050 nm wavelength, with 100 kHz A-scan rates to perform structural and angiography imaging. Figure 11 shows a wide field B-Scan of a normal human eye. A comparison of Fig. 5 and Fig. 11 shows how dramatically ophthalmic OCT image quality and capability has improved over the past 25 years.

Fig. 11.

OCT image of the normal retinal from the Carl Zeiss Meditec commercial PLEX Elite 9000 ophthalmic SS-OCT instrument. Imaging was at 1050 nm wavelength, at 100 kHz A-scan rate with 6.3 μm axial resolution. In addition to retinal structure, the full choroidal thickness and vasculature can be visualized in this widefield image. Image courtesy of Zeiss.

Optovue was the first to release a US FDA cleared ophthalmic SD-OCT in 2006 as well as to commercially develop optical coherence tomography angiography (OCT-A) which was released outside the US in 2014. OCT-A provides three dimensional visualization of retinal vasculature without requiring injected contrast agents. Figure 12 shows an example of the Optovue software which can quantify and map vessel density. Three dimensional structural data is available from the same acquisition and can characterize retinal features including retina thickness. Clinicians can assess retinal pathology by examining both functional (flow) and structural images side by side.

Fig. 12.

Screen shot of one view of the Optovue commercial AngioVue ophthalmic SD-OCT product. The top left shows the OCT-A en-face view of micro-capillary network of blood flow. The upper right shows an OCT en-face with a retinal thickness map. The lower right shows a cross sectional B-scan with automated segmentation of a layer shown in green. The lower left shows a cross sectional view of both structural and OCT-A flow information. Image courtesy of Optovue.

Figure 13 illustrates how OCT ophthalmic services have grown compared with two other common imaging modalities, fundus photography and fluorescein angiography. This data was obtained from US Medicare databases for CPT Codes which are used to describe and track services of physicians, hospitals, and other healthcare providers. Obtaining a CPT code is a milestone in the success of medical products since it can be an important step in determining the reimbursement to clinicians and hospitals for both public and private payers, affecting the economics of the product use. Ophthalmic OCT is currently reimbursed at a rate of ~$45 per procedure. CPT code 92235 is used for fluorescein angiography, 92250 is used for fundus photography, and 92132/3/4/5 are used for OCT (and other diagnostic imaging, but is dominated by OCT). It is clear the rate of growth of OCT has dramatically outpaced these other imaging modalities. The reimbursement payments associated with these services had a dramatic growth and in 2010 had reached nearly $1B/year [5, 6]. In that year the Medicare reimbursement was reduced to allow one reimbursement irrespective of whether one or both eyes were scanned. This illustrates how important CPT codes can be. The change in CPT code reimbursement accounts for the dramatic drop in CPT code 92132/3/4/5 services between 2010 and 2011. Note that this drop is not indicative of a reduction in OCT use but is a manifestation of accounting (how services were defined) and the fact that most ophthalmologists were scanning, and billing for, both eyes. Growth in ophthalmic OCT use was only minimally impacted (see Fig. 10), which is particularly interestingly in light of the change in the reimbursement. Despite a factor of ~2X reduction in reimbursement which removed over $300M in payments, OCT services continue to grow based on clinical utility.

Fig. 13.

Allowed Medicare services per year for three CPT code categories: CPT code 92235 is used for fluorescein angiography, 92250 is used for fundus photography, and 92132/3/4/5 is used for OCT (including other diagnostic imaging, but dominated by OCT). In 2010 Medicare accounting was changed to only allow one service to be credited whether one eye or both eyes were scanned. This caused an adjustment in the Medicare service count, but the overall growth of OCT is apparent.

Many ophthalmologists have said that OCT transformed the way that they practice ophthalmology. The introduction of new ophthalmic OCT technologies such SS-OCT, OCT angiography (OCT-A), and polarization sensitivity OCT as well as the development of lower cost instruments which can enter optometry and other markets promises to further increase the penetration of OCT into ophthalmic practice and patient care.

Figure 14 shows examples of cardiovascular OCT metrics. Cardiology was the second market to have a commercial clinical OCT product. Intravascular OCT was released in 2004 by LightLab Imaging and there is a continued strong growth in publications, procedures, and revenue. The number of OCT procedures worldwide is estimated to be ~100,000/year, one procedure every few minutes. As with ophthalmology, TD-OCT technology was first to the market. Procedures had passed ~10,000/year and revenue had passed ~$10M/year when in 2009 Lightlab introduced SS-OCT (EU and Japan approval very early in 2009 and FDA clearance in 2010). This was also the first introduction of SS-OCT technology for any clinical market. SS-OCT had a powerful impact on product uptake since it offered much faster data acquisition times and eliminated the need for an occlusion balloon to remove blood from the imaging area, thereby reducing ischemia as imaging times were shortened from 30 seconds or longer to approximately 2 seconds. The speed increase provided by SS-OCT also changed the procedure from a two device (imaging plus occlusion balloon catheter) procedure to a single device, single-step procedure [22]. Cardiovascular OCT revenue has grown rapidly in recent years and there are three companies shipping cardiovascular OCT products (Terumo released its IV-OCT product in 2012 and Avinger released its FDA cleared peripheral OCT imaging product in 2012). It is noteworthy that it took ~12 years after the first cardiovascular OCT startup for the market to cross ~$50M/year – the approximate return often cited for a medical device company to thrive, due to the combination of regulatory, clinical, manufacturing, quality, sales, marketing, and R&D burdens they face.

Figure 15 shows a screen shot from the St. Jude Medical cardiovascular SS-OCT imaging system user interface. The upper left corner shows a 3D rendering with a virtual perspective inside a human coronary artery with a stent, color coded to show strut apposition that is keeping the artery open. The guidewire used to deploy the OCT catheter is also visible in gray. The upper right corner shows a cross sectional image and the bottom centered image shows a longitudinal pullback image also showing the artery, stent and guidewire. Intravascular OCT has become a very important clinical research tool for understanding the role of plaque morphology in heart disease and evaluating new therapies and interventional devices. It is increasingly being used to make clinical decisions and there have been over 400,000 cumulative procedures. The long-term outlook on the role of OCT imaging in routine interventional decisions remains an important open question and additional clinical studies are needed [23–28].

Fig. 15.

Screen shot of one view from the St. Jude medical cardiovascular SS-OCT imaging system user interface. The upper left shows a 3D rendering of the inside of a human coronary artery. The upper right shows a cross sectional 2D image and the bottom image shows a longitudinal pullback 2D image also showing the artery, stent, and guidewire. Image courtesy St. Jude Medical.

Figure 16 shows some examples of dermatology OCT metrics. Skin cancer is the most common form of cancer worldwide and Medicare costs for diagnosing and treating skin cancer are in excess of $1B/year in the US alone. Michelson Diagnostics is the dominant company supplying dermatological OCT products. Michelson released their first CE-marked and FDA cleared product in 2010 and the number of procedures has grown to over 10,000 per year in Germany, where reimbursement is available for OCT scanning of lesions clinically suspicious for skin cancer. Commercial growth in US may follow when a CPT code is approved in the near future. OCT imaging enables both early detection of non-melanoma skin cancer and follow-up monitoring of treatment response to non-invasive topical chemotherapy, thereby avoiding scarring caused by biopsy and/or excisional surgery. This combination of a non- or minimally-invasive diagnostic with a non- or minimally-invasive treatment for better overall healthcare outcome is a key theme in the adoption of OCT into routine clinical practice. Figure 17 shows an en-face structural OCT and OCT-A images of a basal cell carcinoma skin cancer in a human taken with the Michelson Diagnostics commercial instrument [29]. Dermatological OCT is an emerging research and clinical tool that used alone, or in combination with other imaging technology, promises to improve patient care and reduce healthcare costs [29–35].

Fig. 17.

Screen shot of a one view of the Michelson Diagnostics Vivosight Scanner user interface showing basal cell carcinoma, structural OCT (top left en-face, top right cross-sectional views) and dynamic OCT with OCT-A overlaid on structural OCT (bottom left side en-face, right cross-sectional views). The bascal cell carcinoma exhibits several oval areas with homogenous signal, surrounded by a dark rim. The tumor vessels are arranged around the tumor islands. Image courtesy Julia Welzel Head of Department of Dermatology, General Hospital, Ausburg, Germany and Michelson Diagnostics [29].

Figure 18 shows examples of gastroenterology (GI) OCT metrics. There is a clinical need to improve diagnostics for screening, surveillance, and treatment of esophageal adenocarcinoma as it is one of the fastest growing cancers and has a poor five-year survival rate. Lightlab Imaging (in partnership with Pentax) and Imalux initially explored commercial products in the gastroenterology space but Lightlab pivoted into cardiology and Imalux eventually went out of business. NinePoint Medical entered the gastroenterology field in 2010 and licensed substantial IP and other technology from the Massachusetts General Hospital [36] a leading OCT research institution and recipient of US OCT government research funding [2]. Three years later, in 2013, NinePoint released its first commercial product for GI OCT, focused on the early detection of esophageal cancer. Other documented uses of OCT in the GI tract include imaging the biliary and pancreatic system, stomach and colon for the early identification of various diseases, including cancer. A promising future embodiment of OCT technology uses a tethered, swallow-able capsule to enable screening for esophageal disease without using an endoscope or anesthesia [37, 38]. Figure 19 shows a screen shot of the NinePoint Medical commercial GI VLE imaging system user interface along with a comparison of an OCT image and histology (VLE stands for “volume laser endomicroscopy”). There have been over 7,000 cumulative procedures to date. OCT in gastroenterology is an emerging research and clinical tool that offers tremendous promise to improve patient care and reduce healthcare costs. Clinical studies assessing the sensitivity and specificity of OCT for identifying dysplasia in patients with Barrett’s esophagus, an important initial market opportunity are currently underway [39–43]. Recently, esophageal OCT has had a substantial increase in the Medicare reimbursement rate (CPT Code 43252), which is a very positive step for OCT in GI [44].

Fig. 19.

Screen shot of one view of the NinePoint Medical Nvision VLE Imaging System user interface (left side) showing in in vivo structural OCT images of human esophagus along with a 3D rendering (upper right corner) and a zoomed region compared with a histological section (lower right corner). Image courtesy NinePoint Medical.

There are many other exciting commercial OCT efforts in varying stages of maturity. In addition to clinical applications, research systems and subsystems are a substantial market, valued in excess of ~$30M/year. Another exciting market is OCT for surgical guidance, where there are several companies making surgical ophthalmic microscopes or attachments which integrate a normal microscope view along with real-time 2D or volumetric OCT images to provide enhanced depth resolution or virtual perspectives to augment the standard microscopic view in surgical procedures. LLTech is a start-up company which is utilizing full field OCT (FF-OCT) in digital pathology of ex-vivo surgical tissues specimens to confirm core biopsy or assess surgical margin status. Figure 20 shows a FF-OCT image of a human pancreas biopsy obtained using the commercial LLTech instrument in comparison to conventional histology [45]. FF-OCT could be used in the endoscopy suite workflow as a rapid aid tool for the endosonographer during the EUS biopsy to increase the number of satisfactory specimens and reduce the number of repeat procedures. Photonicare is a startup company developing a handheld OCT product for otolaryngology which could potentially be used as a general purpose tool in primary care physician offices. There are three startup companies which are developing OCT for real-time breast cancer lumpectomy margin assessment in order to reduce the rates of second surgeries from positive or close margins. If successful, this application promises to not only reduce patient morbidity from second surgeries, but could potentially save ~$1B of additional healthcare costs in the US which result from repeat lumpectomy surgeries [46–52].

Fig. 20.

FF-OCT image of a human pancreas biopsy taken using the commercial Light-CT Scanner (a, b) in comparison to conventional histology (c, d). Image courtesy LLTech.

Employment is another important metric to assess the economic impact of OCT [3,4]. Figure 21 shows an estimate of OCT related employment with four components of employment shown in different colors. Shown in red are jobs associated with “Research” which consists of professors, postdocs, and other university staff at the numerous OCT research groups around the world. This employment is estimated to be ~1,000 full-time-equivalent jobs in 2015 and was obtained using estimates from www.octnews.org and PubMed publications. Shown in green are “Direct OCT Industry” jobs. This data was obtained by contacting 64 of the world’s leading OCT system, subsystem, and component companies who generously cooperated with a survey estimating their employment in engineering, marketing, sales, manufacturing, management or other areas that are directly attributed to their OCT products [4, 53]. In 2015 there were over 2,500 high quality yearly jobs or ~18,000 person-years of direct cumulative employment. This figure does not include an additional 2-4X number of jobs related to other employment in the OCT supply chain such as for computers, displays, power supplies, chassis, optical beam scanners, fiber optic components, and the many other components that make up commercial OCT systems. These estimated “Indirect Industry” jobs are shown in blue (assumed 2X). Another major source of employment is all the jobs associated with operating and supporting the roughly 50,000 installed OCT systems around the world that require nurses, medical technicians, and administrators. Although this is challenging to estimate, one approach recommended by ophthalmology administrators is to assume ~20% of a staff member’s time is required for support, operation and maintenance of one instrument. This implies about ~10,000 additional jobs per year in 2015. These “Hospital and Clinic” jobs are shown in yellow. In summary, there are over 2,500 direct high-quality jobs in OCT system and component companies and perhaps 5-10X that number indirectly. Cumulatively as of 2016, this represents ~125,000 person-years of employment.

Fig. 21.

Estimated OCT related employment. “Research” employment consists of professors, postdocs, and other university staff. “Direct OCT Industry” jobs are from a survey of 64 leading OCT system, subsystem, and component companies showing employment in engineering, marketing, sales, manufacturing, management that are directly attributed to OCT products. “Indirect Industry” shows additional ~2X number of jobs related to other employment in the OCT supply chain. “Hospital / Clinic” shows estimate of clinical jobs related to OCT.

Figure 22 shows the estimated annual OCT system market along with estimated NIH and NSF funding as shown earlier in Fig. 2. The yearly market size was estimated by data provided by executives at the major OCT companies and from other sources such as market analyst reports. It can be seen that the OCT market is approaching $1B per year or over $5B cumulatively. This is ~10X the sum of NIH and NSF funding investment which was estimated between $90-$600M. As mentioned earlier, the OCT NSF and NIH cumulative funding is estimated between $90-$600M, with $90M probably being a more representative number and $600M being an upper bound. Of course, the revenue shown is a worldwide number and there are many other governments around the world investing in OCT research. Assuming worldwide government funding at ~$500M [2], the worldwide cumulative system revenue of $5.2B is ~10X the worldwide government investment. The system revenue in a single year exceeds the cumulative research investment over 25 years, indicating a large return on investment of tax-payer dollars. Another way to assess the financial return to the tax payers is to estimate tax receipts from corporations and employees working in the OCT market. There are multiple taxing agencies and the types of taxes and tax rates vary across countries. However it is estimated that tax receipts to governments are well in excess of ~$500M from direct corporate and payroll taxes from the system companies alone [3, 4]. Substantial additional tax receipts are collected through OCT component companies, indirect employment in the supply chain and at clinics around the world operating installed OCT systems.

Fig. 22.

Estimated OCT yearly system revenue (green) in comparison to yearly NIH and NSF OCT funding. The yearly revenue includes the biometry market.

Another example of the economic impact of OCT is the savings in healthcare costs. Although challenging to quantify, as one example, it is estimated that using OCT to assess treatment response and the need to re-treat age-related macular degeneration patients with anti-VEGF therapy has saved Medicare ~$10B dollars [9]. This savings dwarfs the government tax-payer sponsored research investment over 25 years. However, another, more important economic impact of OCT is the most difficult to quantify. In ophthalmology, clinicians have said the OCT enables the non-specialist to detect disease with a sensitivity approaching that of a specialist. This means that comprehensive ophthalmologists or optometrists can use OCT to detect retinal disease and refer patients to specialists at early, treatable stages, reducing or preventing irreversible loss of vision. This has a profound economic as well as quality of life impact. Government investment in research is under increasing pressure, with increasing costs in entitlement programs and a decrease in the discretionary part of the US budget. However, it is our belief that the examples that we present here show that the economic return to taxpayers can be outstanding and justify government investment in research, not only in OCT but across a wide range of biomedical technologies.

9. Summary

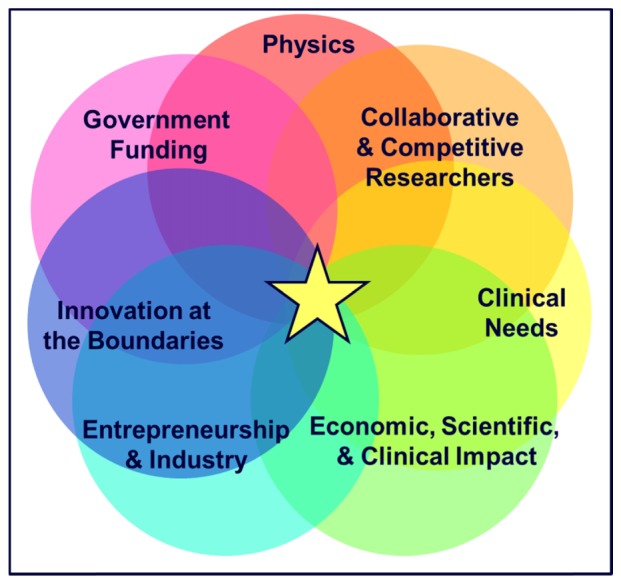

In 25 years OCT has grown to have a tremendous positive impact on society. This growth was due in large part to a worldwide ecosystem (Fig. 23) that consisted of: 1. Underlying physical principles which enabled high performance and scalability; 2. Sustained government funding for fundamental and clinical research; 3. The academic scientific research infrastructure and process which involves competition and collaboration, where researchers compete for funding, but also share results in journals and at conferences; 4. Innovation at the boundaries, leveraging ideas and concepts from related industries such as fiber optical telecommunications, software, and computers to accelerate advances in medical technology; 5. Addressing real clinical needs to improve patient care and simultaneously lower costs; 6. The role of entrepreneurism and venture capital investment which can facilitate high risk commercial advances along with industry engagement which can provide the large scale investment, engineering, and marketing necessary to develop a clinical technology; 7. The ultimate clinical, economic, and scientific impact which is needed to reinforce, justify, and continue all of the aforementioned components and investments.

Fig. 23.

The Ecosystem for medical technology translation and clinical impact. Although this manuscript focused on OCT, other medical instrumentation / device technologies would require a similar ecosystem for translation and clinical impact.

This paper has reviewed some of the quantitative and qualitative data associated with the commercialization of OCT and its economic impact, as well as described the exceptional return on government investment. However, the most important impact of OCT or medical technology in general is the improvement in healthcare for millions of patients where it is used to increase diagnostic performance and make therapeutic decisions, as well as to advance clinical and scientific knowledge for the benefit of future patients and society at large.

The future of the OCT ecosystem to foster innovation and provide societal benefits looks as bright as ever. On the technology side, there are numerous frontiers with new imaging devices, system concepts, integrated optics, light sources, and multimodality that will to power the technology far into the future. There is continuing funding from governments to explore these new ideas as well as a substantial OCT industrial base of R&D funding. On the application side, OCT will continue to expand in the clinical and non-medical markets where it is used today and there remain numerous untapped clinical markets both in developed and developing economies. These markets will require continued risk taking, clever engineering, clinical validation studies, and regulatory and reimbursement approval on a specialty by specialty basis. However some of these markets offer billion dollar revenues and promise to benefit the health and wellbeing of millions of people around the world as well as help contribute to their economies.

Although this paper focused on OCT and was written for the 25th Anniversary of OCT special issue of Biomedical Optics Express, it is important to emphasize that there are many biomedical technologies which are being developed and are poised for translation into clinical practice. Optics is a powerful modality for biomedicine because it can have low to moderate costs and enables non-invasive or minimally invasive assessment. Imaging, structured illumination, fluorescence and nonlinear microscopy, diffuse photon techniques, spectroscopy, photoacoustics and many other techniques are all making major advances which promise to have a powerful impact on fundamental understanding of disease as well as clinical care. Outside of optics, computational methods including neural networks, deep learning, CMOS fabrication techniques, robotics, and medical devices are examples of medical instrumentation/device based technologies which would all require similar ecosystems in order to be translated to clinical care. It is our hope that elucidating this ecosystem will help to support the important role that government funding, the academic sector, entrepreneurship, and industry play in advancing healthcare and reducing suffering caused by disease.

Financial Disclosures

Eric Swanson receives patent royalties from MIT owned OCT patents which are licensed to several companies and is on the board of directors and has financial interest in NinePoint Medical Incorporated. James Fujimoto receives patent royalties from MIT owned OCT patents which are licensed to several companies and is an advisor and has financial interest in Optovue.

Acknowledgements

The authors would like to thank past and present generations of trainees, clinical collaborators, and industrial partners for their countless scientific, engineering, clinical and business contributions. We thank Dr. Ben Potsaid for his assistance in preparing Fig. 3 showing OCT publications and collaboration. We would also like to thank Carl Zeiss Meditec Corporation, Jay Wei from Optovue, Jon Holmes from Michelson Diagnostics, Julia Welzel from General Hospital, Ausburg, Germany, Joel Friedman from St. Jude Medical, Betrand Le Conte from LLTech, and the 64 OCT related companies that participated in our survey for help in supplying material for this manuscript.

Funding

We gratefully acknowledge continuing support from the National Institutes of Health and the Air Force Office of Scientific Research. We acknowledge current sponsorship by the National Institutes of Health R01-EY11289, R01-CA75289, R01-CA178636 and the Air Force Office of Scientific Research FA9550-10-1-0551 and FA9550-12-1-0499 and support from the Champalimaud Foundation.

References and links

- 1.Huang D., Swanson E. A., Lin C. P., Schuman J. S., Stinson W. G., Chang W., Hee M. R., Flotte T., Gregory K., Puliafito C. A., Fujimoto J. G., “Optical coherence tomography,” Science 254(5035), 1178–1181 (1991). 10.1126/science.1957169 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2.Swanson E. A., “One Decade and $500M: The Impact of Federal Funding on OCT Parts I & II,” BioOptics World (2011). [Google Scholar]

- 3.Fujimoto J., Swanson E., “The Development, Commercialization, and Impact of Optical Coherence Tomography,” Invest. Ophthalmol. Vis. Sci. 57(9), OCT1–OCT13 (2016), doi:. 10.1167/iovs.16-19963 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Swanson E., “Beyond Better Clinical Care: OCT’s Economic Impact,” BioOptics World (2016). [Google Scholar]

- 5.Swanson E. A., Huang D., “Ophthalmic OCT Reaches $1 Billion per Year: But Reimbursement Clampdown Clouds Future Innovation,” Retinal Physician 45, 58–59 (2011). [Google Scholar]

- 6.Swanson E. A., “Estimates of Ophthalmic OCT Market Size and the Dramatic Reduction in Reimbursement Payments,” http://www.octnews.org/articles/4176266/estimates-of-ophthalmic-oct-market-size-and-the-dr/, (2012).

- 7.Fung A. E., Lalwani G. A., Rosenfeld P. J., Dubovy S. R., Michels S., Feuer W. J., Puliafito C. A., Davis J. L., Flynn H. W., Jr, Esquiabro M., “An optical coherence tomography-guided, variable dosing regimen with intravitreal ranibizumab (Lucentis) for neovascular age-related macular degeneration,” Am. J. Ophthalmol. 143(4), 566–583 (2007). 10.1016/j.ajo.2007.01.028 [DOI] [PubMed] [Google Scholar]

- 8.G. A. Lalwani, P. J. Rosenfeld, A. E. Fung, S. R. Dubovy, S. Michels, W. Feuer, J. L. Davis, H. W. Flynn Jr., M. Esquiabro, “A variable-dosing regimen with intravitreal ranibizumab for neovascular age-related macular degeneration: year 2 of the PrONTO Study,” American Journal of Ophthalmology, 148:43–58 e41 (2009). 10.1016/j.ajo.2009.01.024 [DOI] [PubMed]

- 9.M. A. Windsor, J. J. Sun, E. A. Swanson, P. J. Rosenfeld, K. Frick, and D. Huang, manuscript under preparation.

- 10.Drexler W., Fujimoto J. G., Optical coherence tomography: technology and applications 2nd Edition. Springer Science & Business Media; (2015). [Google Scholar]

- 11.Wills S., “OSA Centennial Snapshots: OCT and the Flowering of Biopotonics,” Opt. Photonics News 27(9), 42 (2016). 10.1364/OPN.27.9.000042 [DOI] [Google Scholar]

- 12.M. Hourihan and D. Parks, “Guide to the President’s Budget, Research & Development FY2017,” American Association for the Advancement of Science (AAAS), September 20th, 2016.

- 13.Puliafito C. A., Hee M. R., Schuman J. S., Fujimoto J. G., “Optical Coherence Tomography of Ocular Diseases,” Thorofare, NJ: Slack, Inc., (1995). [Google Scholar]

- 14.Swanson E. A., “Some Historical Statistics of USPTO Patents in the Field of Optical Coherence Tomography”, http://www.octnews.org/articles/4099230/some-historical-statistics-of-uspto-patents-in-the/, (2012).

- 15.N. Tanno, T. Ichimura, and A. Saeki, inventors. “Device for measuring the light wave of a reflected image”, Japanese Patent 6–35946. Issued May 11, 1994.

- 16.E. A. Swanson, D. Huang, J. G. Fujimoto, C. A. Puliafito, C. P. Lin, and J. S. Schuman, inventors, Massachusetts Institute of Technology, assignee, “Method and apparatus for optical imaging with means for controlling the longitudinal range of the sample”, United States Patent 5,321,501, Filed April 29, 1991, Issued June 14, 1994.

- 17.E. A. Swanson, D. Huang, J. G. Fujimoto, C. A. Puliafito, C. P. Lin, and J. S. Schuman, inventors, Massachusetts Institute of Technology, assignee, “Method and apparatus for performing optical measurements” United States Patent 5,459,570, Filed March 16th, 1993, Issued October 17, 1995.

- 18.E. A. Swanson, inventors, Massachusetts Institute of Technology, assignee, “Method and Apparatus for Acquiring Images using a CCD Detector Array and No Transverse Scanner”, US Patent Number 5,465,147, Filed June 2, 1994, Issued November 7, 1995.

- 19.E. A. Swanson and S. R. Chinn, inventors, Massachusetts Institute of Technology, assignee, “Method and apparatus for performing optical measurement using a rapidly frequency -tuned Laser”, United States Patent 5,956,355, Filed February 7, 1997, Issued September 21, 1999.

- 20.G. Tearney, S. A. Boppart, B. Bouma, M. E. Brezinski, E. A. Swanson, and J. G. Fujimoto, inventors; Massachusetts Institute of Technology, assignee. “Method and apparatus for performing optical measurements using a fiber optical imaging guidewire, catheter, or endoscope” United States Patent 6,134,003, Filed February 27, 1996, Issued October 17, 2000.

- 21.S. A. Boppart, G. J. Tearney, B. E. Bouma, M. E. Brezinski, J. G. Fujimoto, and E. A. Swanson, inventors, Massachusetts Institute of Technology, assignee, “Methods and Apparatus for Forward-Directed Optical Scanning Instruments”, US Patent Number 6,485,413, Filed March 6, 1998, Issued November 26, 2002.

- 22.Yamaguchi T., Terashima M., Akasaka T., Hayashi T., Mizuno K., Muramatsu T., Nakamura M., Nakamura S., Saito S., Takano M., Takayama T., Yoshikawa J., Suzuki T., “Safety and Feasibility of an Intravascular Optical Coherence Tomography Image Wire System in the Clinical Setting,” Eur. Heart J. 31, 401–415 (2010), doi:. 10.1093/eurheartj/ehp433 [DOI] [PubMed] [Google Scholar]

- 23.Ong D. S., Jang I. K., “Causes, assessment, and treatment of stent thrombosis--intravascular imaging insights,” Nat. Rev. Cardiol. 12(6), 325–336 (2015). 10.1038/nrcardio.2015.32 [DOI] [PubMed] [Google Scholar]

- 24.Prati F., Regar E., Mintz G. S., Arbustini E., Di Mario C., Jang I. K., Akasaka T., Costa M., Guagliumi G., Grube E., Ozaki Y., Pinto F., Serruys P. W. J., Expert’s OCT Review Document , “Expert review document on methodology, terminology, and clinical applications of optical coherence tomography: physical principles, methodology of image acquisition, and clinical application for assessment of coronary arteries and atherosclerosis,” Eur. Heart J. 31(4), 401–415 (2010), doi:. 10.1093/eurheartj/ehp433 [DOI] [PubMed] [Google Scholar]

- 25.Yonetsu T., Bouma B. E., Kato K., Fujimoto J. G., Jang I. K., “Optical coherence tomography– 15 years in cardiology,” Circ. J. 77(8), 1933–1940 (2013). 10.1253/circj.CJ-13-0643.1 [DOI] [PubMed] [Google Scholar]

- 26.Z. A Ali, A. Maehara, P. Généreux, R. A Shlofmitz, F. Fabbiocchi, T. M. Nazif, G. Guagliumi, P. M. Meraj, F. Alfonso, H. Samady, T. Akasaka, E. B. Carlson, M. A Leesar, M. Matsumura, M. O. Ozan, G. S Mintz, O. Ben-Yehuda, G. W Stone, “Optical coherence tomography compared with intravascular ultrasound and with angiography to guide coronary stent implantation (ILUMIEN III: OPTIMIZE PCI): a randomized controlled trial,” The Lanclet. (2016). 10.1016/S0140-6736(16)31922-5 [DOI] [PubMed]

- 27.H. Bezzera, “Intravascular OCT in PCI”, Part 1 and Part 2, American College of Cardiology, June 2016.

- 28.G. Mintz, “IVUS in PCI guidance”, American College of Cardiology, June 2016.

- 29.Ulrich M., Themstrup L., de Carvalho N., Manfredi M., Grana C., Ciardo S., Kästle R., Holmes J., Whitehead R., Jemec G. B., Pellacani G., Welzel J., “Dynamic Optical Coherence Tomography in Dermatology,” Dermatology (Basel) 232(3), 298–311 (2016), doi:. 10.1159/000444706 [DOI] [PubMed] [Google Scholar]

- 30.Cheng H. M., Guitera P., “Systematic review of optical coherence tomography usage in the diagnosis and management of basal cell carcinoma,” Br. J. Dermatol. 173(6), 1371–1380 (2015). 10.1111/bjd.14042 [DOI] [PubMed] [Google Scholar]

- 31.Ulrich M., von Braunmuehl T., Kurzen H., Dirschka T., Kellner C., Sattler E., Berking C., Welzel J., Reinhold U., “The sensitivity and specificity of optical coherence tomography for the assisted diagnosis of nonpigmented basal cell carcinoma: an observational study,” Br. J. Dermatol. 173(2), 428–435 (2015). 10.1111/bjd.13853 [DOI] [PubMed] [Google Scholar]

- 32.Gambichler T., Jaedicke V., Terras S., “Optical coherence tomography in dermatology: technical and clinical aspects,” Arch. Dermatol. Res. 303(7), 457–473 (2011). 10.1007/s00403-011-1152-x [DOI] [PubMed] [Google Scholar]

- 33.Hussain A. A., Themstrup L., Jemec G. B. E., “Optical coherence tomography in the diagnosis of basal cell carcinoma,” Arch. Dermatol. Res. 307(1), 1–10 (2015). 10.1007/s00403-014-1498-y [DOI] [PubMed] [Google Scholar]

- 34.Markowitz O., Schwartz M., Feldman E., Bienenfeld A., Bieber A. K., Ellis J., Alapati U., Lebwohl M., Siegel D. M., “Evaluation of optical coherence tomography as a means of identifying earlier stage basal cell carcinomas while reducing the use of diagnostic biopsy,” J. Clin. Aesthet. Dermatol. 8(10), 14–20 (2015). [PMC free article] [PubMed] [Google Scholar]

- 35.Schmitz L., Reinhold U., Bierhoff E., Dirschka T., “Optical coherence tomography: its role in daily dermatological practice,” J. Dtsch. Dermatol. Ges. 11(6), 499–507 (2013). [DOI] [PubMed] [Google Scholar]

- 36.“NinePoint Medical Licenses 188 Patents and Patent Applications; Patents Support NinePoint’s Broad-Based Platform Technology for Development of in vivo Pathology Devices”, NinePoint Medical Press Release, December 13th, 2010.

- 37.Ughi G. J., Gora M. J., Swager A.-F., Soomro A., Grant C., Tiernan A., Rosenberg M., Sauk J. S., Nishioka N. S., Tearney G. J., “Automated segmentation and characterization of esophageal wall in vivo by tethered capsule optical coherence tomography endomicroscopy,” Biomed. Opt. Express 7(2), 409–419 (2016), doi:. 10.1364/BOE.7.000409 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 38.Lee H.-C., Ahsen O. O., Liang K., Wang Z., Cleveland C., Booth L., Potsaid B., Jayaraman V., Cable A. E., Mashimo H., Langer R., Traverso G., Fujimoto J. G., “Circumferential optical coherence tomography angiography imaging of the swine esophagus using a micromotor balloon catheter,” Biomed. Opt. Express 7(8), 2927–2942 (2016), doi:. 10.1364/BOE.7.002927 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 39.Sharma P., Savides T. J., Canto M. I., Corley D. A., Falk G. W., Goldblum J. R., Wang K. K., Wallace M. B., Wolfsen H. C., ASGE Technology and Standards of Practice Committee , “The American Society for Gastrointestinal Endoscopy PIVI (Preservation and Incorporation of Valuable Endoscopic Innovations) on imaging in Barrett’s Esophagus,” Gastrointest. Endosc. 76(2), 252–254 (2012). 10.1016/j.gie.2012.05.007 [DOI] [PubMed] [Google Scholar]

- 40.Robles L. Y., Singh S., Fisichella P. M., “Emerging enhanced imaging technologies of the esophagus: spectroscopy, confocal laser endomicroscopy, and optical coherence tomography,” J. Surg. Res. 195(2), 502–514 (2015). 10.1016/j.jss.2015.02.045 [DOI] [PubMed] [Google Scholar]

- 41.Coda S., Siersema P. D., Stamp G. W. H., Thillainayagam A. V., “Biophotonic endoscopy: a review of clinical research techniques for optical imaging and sensing of early gastrointestinal cancer,” Endosc Int Open 3(5), E380–E392 (2015). 10.1055/s-0034-1392513 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 42.Leggett C. L., Chan D. K., Wang K. K., “Optical Coherence Tomography: Clinical Applications in Gastrointestinal Endoscopy,” in Endoscopic Imaging Techniques and Tools, Konda Vani J. A., Waxman Irving, eds. (Springer International Publishing, 2016), pp. 115–128.. [Google Scholar]

- 43.Trindade A. J., Smith Michael S., Pleskow D. K., “The new kid on the block for advanced imaging in Barrett’s esophagus: a review of volumetric laser endomicroscopy,” Therapeutic Advances in Gastroenterology, pp 408–416. (2016). [DOI] [PMC free article] [PubMed]

- 44.“NinePoint Medical Announces Substantial Hospital Reimbursement Increase for Procedures Using the NvisionVLE Imaging System with Real-time Targeting”, NinePoint Medical Press Release, November 2015.

- 45.Grieve K., Palazzo L., Dalimier E., Vielh P., Fabre M., “A feasibility study of full-field optical coherence tomography for rapid evaluation of EUS-guided microbiopsy specimens,” Gastrointest. Endosc. 81(2), 342–350 (2015). 10.1016/j.gie.2014.06.037 [DOI] [PubMed] [Google Scholar]

- 46.Blumen H., Fitch K., Polkus V., “Comparison of Treatment Costs for Breast Cancer, by Tumor Stage and Type of Service,” Am. Health Drug Benefits 9(1), 23–32 (2016). [PMC free article] [PubMed] [Google Scholar]

- 47.McCahill L. E., Single R. M., Aiello Bowles E. J., Feigelson H. S., James T. A., Barney T., Engel J. M., Onitilo A. A., “Variability in reexcision following breast conservation surgery,” JAMA 307(5), 467–475 (2012). 10.1001/jama.2012.43 [DOI] [PubMed] [Google Scholar]

- 48.Dillon M. F., Hill A. D. K., Quinn C. M., McDermott E. W., O’Higgins N., “A pathologic assessment of adequate margin status in breast-conserving therapy,” Ann. Surg. Oncol. 13(3), 333–339 (2006), doi:. 10.1245/ASO.2006.03.098 [DOI] [PubMed] [Google Scholar]

- 49.Breast Cancer Facts & Figures, American Cancer Society, 2015–2016.

- 50.Kummerow K. L., Du L., Penson D. F., Shyr Y., Hooks M. A., “Nationwide trends in mastectomy for early-stage breast cancer,” JAMA Surg. 150(1), 9–16 (2015), doi:. 10.1001/jamasurg.2014.2895 [DOI] [PubMed] [Google Scholar]

- 51.Wilke L. G., Czechura T., Wang C., Lapin B., Liederbach E., Winchester D. P., Yao K., “Repeat surgery after breast conservation for the treatment of stage 0 to II breast carcinoma: a report from the National Cancer Data Base, 2004-2010,” JAMA Surg. 149(12), 1296–1305 (2014). 10.1001/jamasurg.2014.926 [DOI] [PubMed] [Google Scholar]

- 52.Metcalfe L. N., “Beyond the margins: Economic costs and complication rates associated with repeated breast-conserving surgeries,” J. Clin. Oncol. 34(15S), 1050 (2016). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 53.The following companies participated in the OCT employment survey: Agfa, Alazartech, Avinger, Axsun, Bausch + Lomb / TPV, Bioptigen/Leica, Canon, Cambridge Technology, Colibri, Compact Imaging, Corning, CyLite Optics, DermaLumics, Damae Medical, Diagnostic Photonics, Exalos, Gooch & Housego, Haag Streit, Heidelberg Engineering, Imalux, Innoluce, Innolume GmbH, Insight Photonics, Jenoptik, Keysight Technologies, LLTech, Mabri.Vision, MedLumics, Michelson Diagnostics, Micron Optics, MicroTech, Shenzhen Moptim Imag. Tech. Co, NinePoint Medical, NKT Photonics, Novacam, OCTLight ApS, OCT Medical Imaging, OFS/Furukawa, OPMedT, Optores, Optos, Optovue, Perimeter Medical, PhotoniCare, Physical Sciences Incorporated, Praevium, Santec, Schwind Eye-Tech Solutions, Sensors Unlimited/UTC, St. Jude Medical, Superlum, Terumo, Thorlabs, Tomey, Tomophase, Topcon, Tornado Spectral Systems, Unnamed Company, Unnamed Company, VivoLight, Voxeleron, Wasatch Photonics, WiO Technology Limited, Zeiss Meditec.