Supplemental Digital Content is available in the text.

Abstract

Purpose

To understand the long-term economic implications of key pathways for financing a medical school education.

Method

The authors calculated the net present value (NPV) of cash flow over a 30-year career for a 2013 matriculant associated with (1) self-financing, (2) federally guaranteed loans, (3) the Public Service Loan Forgiveness program, (4) the National Health Service Corps, (5) the Armed Forces Health Professions Scholarship Program, and (6) matriculation at the Uniformed Services University of the Health Sciences. They calculated the NPV for students pursuing one of four specialties in two cities with divergent tax policies. Borrowers were assumed to have a median level of debt ($180,000), and conservative projections of inflation, discount rates, and income growth were employed. Sensitivity analyses examined different discount and income growth rates, alternative repayment strategies, and various lengths of public-sector service by scholarship recipients.

Results

For those wealthy enough to pay cash or fortunate enough to secure a no-strings scholarship, self-financing produced the highest NPV in almost every scenario. Borrowers start practice $300,000 to $400,000 behind their peers who secure a national service scholarship, but those who enter a highly paid specialty, such as orthopedic surgery, overtake their national service counterparts 4 to 11 years after residency. Those in lower-paid specialties take much longer. Borrowers who enter primary care never close the gap.

Conclusions

Over time, the value of a medical degree offsets the high up-front cost. Debt avoidance confers substantial economic benefits, particularly for students interested in primary care.

Medical education in the United States is expensive.1 According to the Association of American Medical Colleges (AAMC), the median four-year cost of attending a public medical school for the class of 2017 is $240,351. A private medical education costs a median of $314,203.2 Institutional scholarships can reduce this burden, but the median four-year award is only $18,000. Less than one in five students receives $100,000 or more in financial assistance from any source.3 In addition, only about 5% of matriculating students secure a federally funded national service scholarship. Because few of the remaining students are wealthy enough to self-finance, most borrow to pay part or all of the cost of their education. As a result, more than 80% of U.S. medical students graduate with substantial debt of $100,000 or more.2

To understand the long-term economic consequences of borrowing versus other options of covering the cost of medical school, we analyzed several major pathways for financing a medical school education in the United States. We hypothesized that although avoiding debt through national service confers substantial up-front economic benefits, borrowers do better in the long run because of the higher incomes available through nonprofit or for-profit practice in the private sector.

Method

Pathways for financing a medical school education

We examined the six major options for financing a medical school education in the United States.

First, federally guaranteed loans (FGLs) are largely authorized under Title IV of the Higher Education Act. Unsubsidized Stafford loans, widely used by medical students, offer terms more favorable than those generally available from commercial lenders. In the 2014–2015 academic year, the interest rate for an unsubsidized Stafford loan was 6.21%; in the 2015–2016 academic year, it was 5.84%.4 Students are not required to start repaying their loans during medical school, but interest accrues. Borrowing is limited to $40,500 annually for a nine-month academic year and slightly more for a longer academic year; these amounts are insufficient to fully cover the expenses at many medical schools.5 Other options exist, but most require the student to commit to a particular career path. For example, the Primary Care Loan program offers long-term, low-interest loans to “full-time, financially needy students” who agree to complete a primary care residency within four years of graduation and practice primary care for either 10 years or until the loan is repaid, whichever comes first.6

Second, the Public Service Loan Forgiveness (PSLF) program was established to encourage newly graduated professionals to work for a public service organization. After making 120 monthly payments while employed full-time by a qualifying organization, any remaining debt is forgiven. The PSLF program is only available for loans made under the William D. Ford Federal Direct Loan Program. Forgiven debt is not taxable. All federal, state, and local government agencies, as well as most nonprofit organizations, qualify as public service organizations.7

Third, the National Health Service Corps (NHSC) was created to place primary care providers in federally designated health professional shortage areas.8 The small number of new students sponsored each year (196 in 2015) receive tax-free payments sufficient to cover their tuition and fees, plus a taxable monthly stipend.9 In return, the students owe a year of practice in a shortage area for each year they are sponsored in school.

Fourth, the Armed Forces’ Health Professions Scholarship Program (HPSP) is sponsored by the U.S. Army, Navy, and Air Force. Each service pays students’ tuition and fees and provides a signing bonus and a taxable stipend of more than $2,000 per month. The 700 to 750 HPSP students recruited annually are commissioned as junior officers in their sponsoring service and placed on inactive (reserve) status for the duration of medical school. They are transferred to active duty upon graduation. After completing residency training in a military or civilian hospital, one year of service is owed for each year of medical school they are sponsored. Additional years of service may be required for those who undertake a lengthy residency or subspecialty fellowship.10–12

Fifth, the Uniformed Services University of the Health Sciences (USU) serves as the leadership academy for military medicine. It charges no tuition or fees.13 Because matriculating students are placed on active duty, they receive the salary, benefits, and housing allowance of a junior officer in their sponsoring service. After completing residency training in a military or civilian hospital, graduates owe a minimum of seven years of service. Most willingly serve longer.14,15

Finally, students wealthy enough to pay cash or fortunate enough to secure a no-strings institutional scholarship can graduate debt-free without incurring a service obligation by self-financing their education.

Data analysis

To analyze the financial implications of each of these six pathways, we calculated the net present value (NPV) of the predicted cash flows over 30 years for unmarried students who enrolled in medical school in 2013, plan to pursue one of four specialties with different annual incomes, and intend to enter private-sector practice as soon as possible. To estimate their subsequent income, we looked at practicing in two cities with substantial numbers of public- and private-sector physicians and divergent tax policies—San Antonio, Texas, and Washington, DC. We assumed that students take four years to graduate medical school and complete their residency training in the prescribed length of time—three years for general internal medicine, four for ophthalmology, and five for general and orthopedic surgery.

For students who borrowed money, we examined six repayment options. For national service scholarship recipients, we modeled transitioning from the public sector to the private sector at three different time points. We assumed that all students matriculate debt-free with no prior service obligations. Table 1 lists the main parameters of our analysis.

Table 1.

Main Parameters Used in a Net Present Value Analysis of Six Options for Financing a Medical School Educationa

FGLs.

To estimate the NPV for this option, we first projected forward the median salary for the student’s first year of residency training ($50,214 according to the AAMC’s 2013 Debt Fact Card16) using a 2% nominal growth rate. We increased the pay for each subsequent year of residency training at a 6% nominal rate. Next, to estimate the starting salary of a physician’s first year of practice in each of the four specialties, we used the 2013 median starting salaries for assistant professors from the AAMC (see Table 1) projected forward using a 2% nominal growth rate. We conservatively assumed that practice income grows with increasing experience at a real rate of 1% above inflation, which would result in a 3% annual growth rate. Third, we computed the amount borrowed annually by proportionally allocating the median 2013 debt of a medical school graduate ($180,000 according to the AAMC’s Debt Fact Card16) to the length of the academic year (9 months for the first two years and 11 months for the last two years of medical school). Then, we computed the amount of principal, accrued interest, loan payments, and end-of-year loan balances associated with six repayment scenarios: (1) a standard repayment plan over 10 years, (2) a pay-as-you-earn (PAYE) repayment plan, or (3) an income-based repayment (IBR) plan using the 2014–2015 Stafford loan interest rate of 6.21%, assuming either (a) forbearance or (b) initiation of debt repayment during residency for each of the three plans listed above. We used 2013 U.S. dollars (USD) to express all estimates of future earnings and repayment amounts, taking into account inflation. To estimate Federal Insurance Contribution Act (FICA), federal, and state income taxes, we used gross taxable amounts, expressed in 2013 USD, as inputs in TAXSIM, the National Bureau of Economic Research’s tax simulator.17 To estimate net pay amounts in 2013 USD, we subtracted total taxes and loan payments from the physician’s gross pay. Finally, to obtain the estimated NPV in 2013 USD, we discounted the net future values using the U.S. Panel on Cost-effectiveness in Health and Medicine’s recommended 3% annual real discount rate.18

Self-financing.

To model the impact of paying cash or obtaining a no-strings scholarship, we employed the same assumptions regarding physician income that we used for borrowers. However, this scenario assumes that students graduate without debt and have no service obligation, so we discounted future gross pay to 2013 USD, then subtracted the resulting taxes.

NHSC.

The NHSC pays the student’s tuition, fees, and other educational expenses directly to the medical school and provides a monthly stipend ($1,330 in 2016). Because the NHSC places primary care providers in health professional shortage areas, it is not open to students pursuing all specialties.8 We assumed that a student receives NHSC support for all four years of medical school and honors his or her service obligation. Because NHSC physicians work in low-income communities, we modeled a somewhat lower starting salary—$140,000 in 2013 USD—compared with what other primary care physicians receive. Then, we assumed that their earnings grow at the same rate as other private-sector physicians. With the exception of loan repayment computations, which are moot if the service obligation is met, we employed the same assumptions used for recipients of FGLs to calculate the NPV for this pathway.

PSLF program.

To maximize the fiscal impact of the PSLF program, we assumed that a physician would start repaying his or her debt during residency to qualify for the PAYE plan, minimize monthly payments, and maximize debt forgiveness. As a proxy for the earnings of physicians at public service organizations, we interpolated the 2013 average age-group earnings of physicians employed by the Department of Veterans Affairs from FedScope.19 Because this average spans all specialties, it does not differentiate pay by specialty. We projected gross pay into the future, conservatively assuming a nominal growth rate of 1% (the approved increase for federal employees in 2013) and accounting for inflation (2%, which is the current Federal Reserve target inflation rate). To maximize the NPV of this option, we modeled transitioning to private-sector practice shortly after completing 10 years of public service, the point at which loan forgiveness occurs. Because physicians transitioning to the private sector lack seniority and established referral relationships, we assumed that they would earn 90% of the salary of their colleagues who entered private-sector practice immediately after residency.

Armed Forces’ HPSP and USU.

To estimate the NPV associated with these military programs, we first added the various types of taxable and nontaxable compensation that military physicians receive throughout their careers, using the 2013 military pay tables. These include basic pay, basic allowance for housing, basic allowance for subsistence, variable special pay, board-certified pay, additional special pay, incentive special pay, and multiyear special pay. Next, we projected gross pay into the future, assuming periodic promotions in rank and a nominal growth rate of 1%, which is the approved military pay increase for 2013. We accounted for inflation (2%) to express future estimated gross pay in 2013 USD. To estimate FICA, federal, and state income taxes, we input total taxable gross pay, expressed in 2013 USD, into TAXSIM.17 We then subtracted total taxes from gross pay to generate net pay estimates. Finally, to obtain the estimated NPV in 2013 USD, we discounted the net future value using the U.S. Panel on Cost-effectiveness in Health and Medicine’s recommended 3% annual real discount rate.18

Hybrid careers.

HPSP physicians may transition to private-sector practice after four years of postresidency military service. USU graduates must serve at least seven years in the military.20 Those who separate shortly after fulfilling their service obligation forego several retention incentives, including incentive special pay and multiyear special pay. Conversely, those who serve 20 or more years secure these incentives and qualify for a lifetime pension that is equal to 2.5% of the average of their three highest basic pay years for every year of service.21 Any income generated after retiring from the military can be added to their military pensions.

To model transitioning to the private sector at different time points, we calculated the NPV associated with separating from the military: (a) shortly after one’s service obligation is met, (b) at the end of the multiyear specialty pay period that falls closest to the 20-year mark, or (c) serving until the end of our 30-year study period. Our main model conservatively assumed that when military physicians transition to the private sector, their starting salary is 90% of that of their colleagues who entered the private sector immediately after residency.

To assess the impact of different economic assumptions, we performed sensitivity analyses.

Because our study is based on national data and used no individual identifiers, institutional review board review was not applicable.

Results

In nearly every comparison, self-financing produces the highest 30-year NPV because students avoid taking on debt and can immediately enter private-sector practice (see Figures 1–4 and Table 2). Because recipients of national service scholarships receive a stipend or salary during medical school, they do even better than self-financers for the first decade or so. In contrast, borrowers quickly fall behind because of their lack of income, the need to take on debt, and interest accrual. However, once they complete residency training, those who enter high-paying specialties, like orthopedic surgery, overtake their national service scholarship counterparts. How quickly this happens depends on the magnitude of the initial gap in NPV ($300,000–$400,000 in most of our models), how much more a particular specialty is paid in the private sector relative to the public sector, and the tax rate in the community where the physician resides.

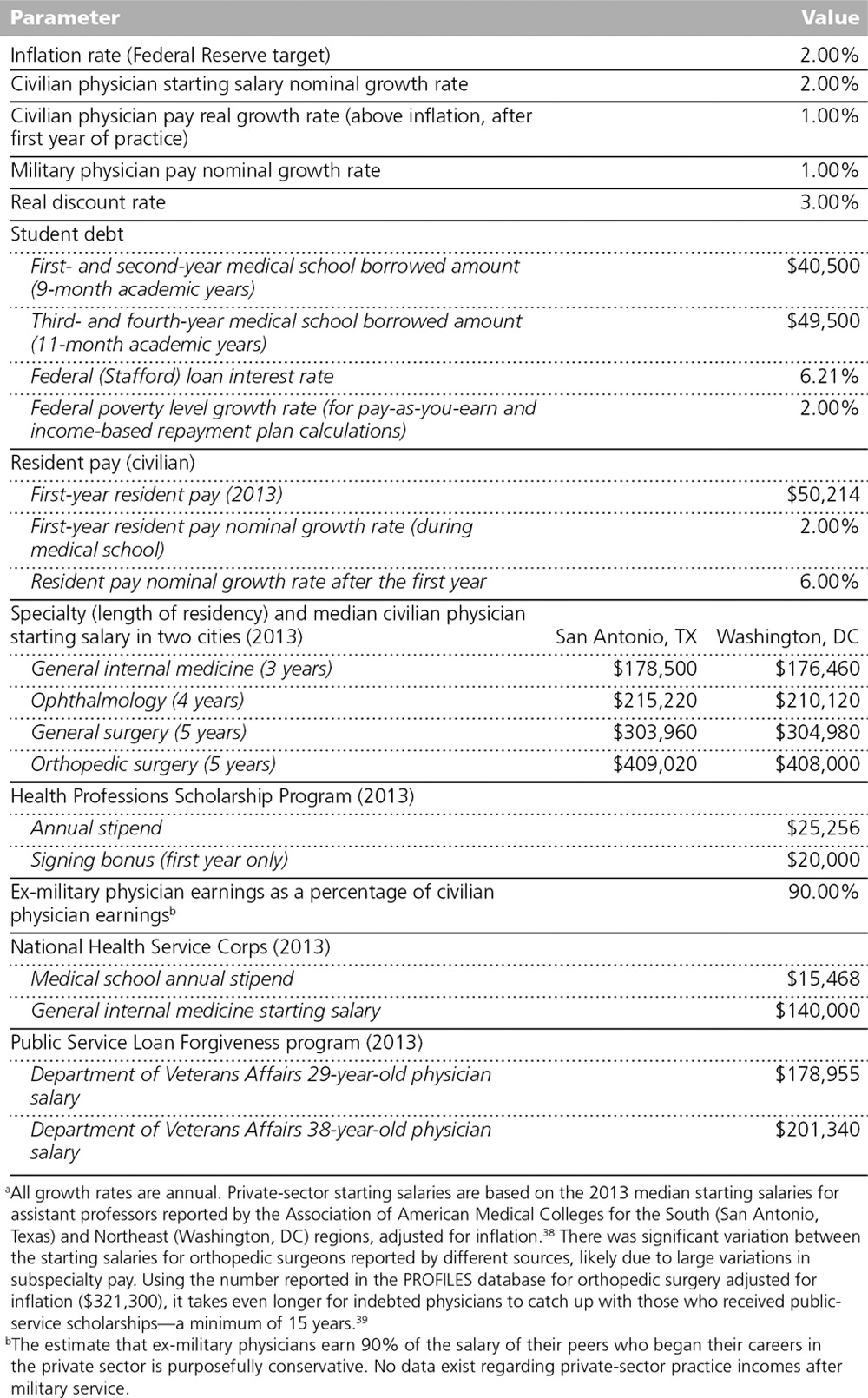

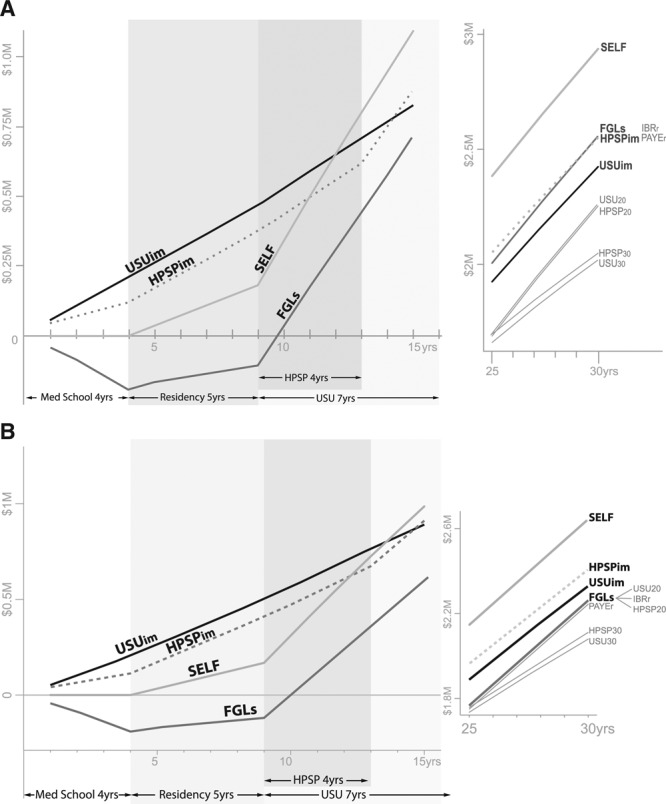

Figure 1.

The results of a 30-year net present value analysis of different pathways for financing a medical school education starting in 2013, then practicing orthopedic surgery in San Antonio, Texas (Panel A) and in Washington, DC (Panel B). Abbreviations: FGLs, federally guaranteed loans, including pay-as-you-earn repayment (PAYEr) starting in residency and income-based repayment (IBRr) starting in residency; HPSP, Health Professions Scholarship Program, including transitioning to the private sector immediately after the 4-year service obligation (HPSPim), transitioning to the private sector after 20+ years of military service (HPSP20), remaining in the military until the end of the 30-year analysis (HPSP30); USU, Uniformed Services University of the Health Sciences, including transitioning to the private sector immediately after the 7-year service obligation (USUim), transitioning to the private sector after 20+ years of military service (USU20), remaining in the military until the end of the 30-year analysis (USU30); and SELF, self-financing the degree or obtaining a full institutional scholarship. Numerical values for these pathways are listed in Table 2.

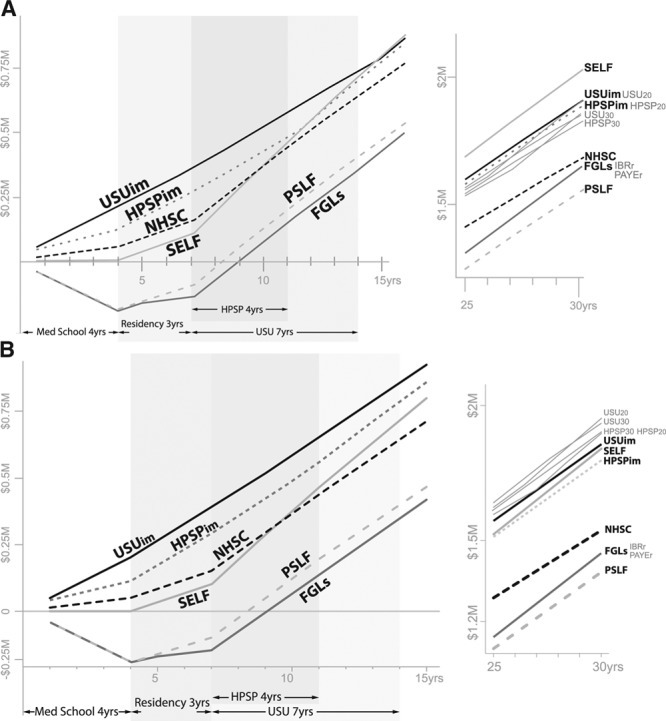

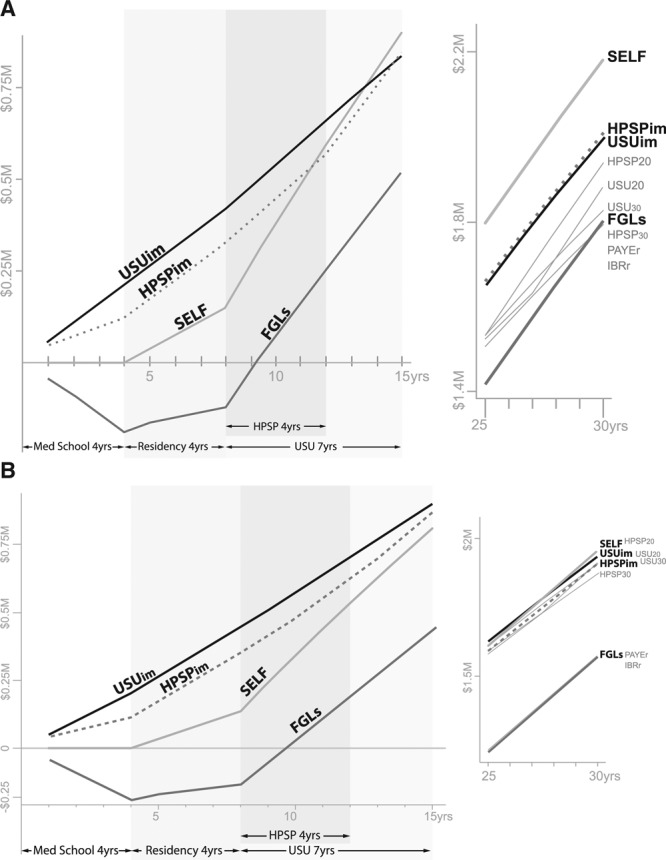

Figure 4.

The results of a net present value analysis of different pathways for financing a medical school education starting in 2013, then practicing general internal medicine in San Antonio, Texas (Panel A) and in Washington, DC (Panel B). Abbreviations: FGLs, federally guaranteed loans, including pay-as-you-earn repayment (PAYEr) starting in residency and income-based repayment (IBRr) starting in residency; NHSC, National Health Service Corps; PSLF, Public Service Loan Forgiveness program; HPSP, Health Professions Scholarship Program, including transitioning to the private sector immediately after the 4-year service obligation (HPSPim), transitioning to the private sector after 20+ years of military service (HPSP20), remaining in the military until the end of the 30-year analysis (HPSP30); USU, Uniformed Services University of the Health Sciences, including transitioning to the private sector immediately after the 7-year service obligation (USUim), transitioning to the private sector after 20+ years of military service (USU20), remaining in the military until the end of the 30-year analysis (USU30); and SELF, self-financing the degree or obtaining a full institutional scholarship. Numerical values for these pathways are listed in Table 2.

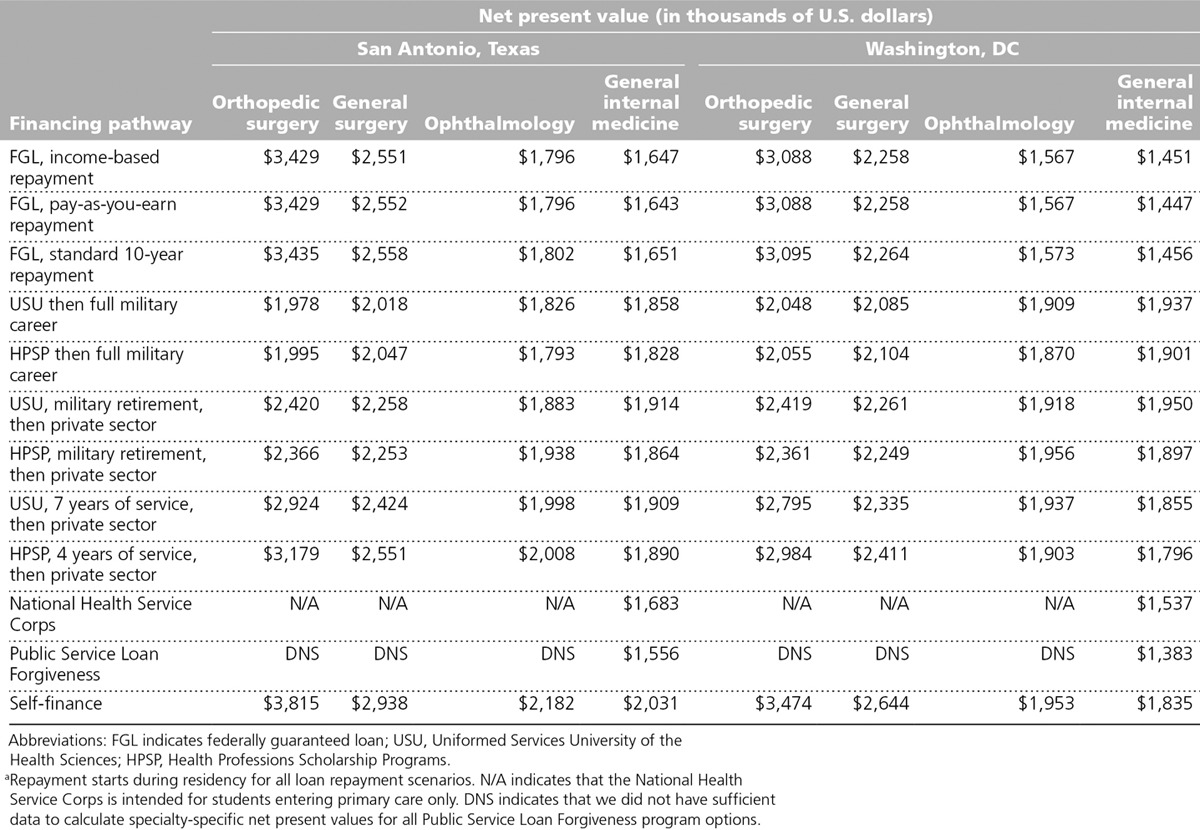

Table 2.

Results of a 30-Year Net Present Value Analysis of Different Pathways for Financing a U.S. Medical School Educationa

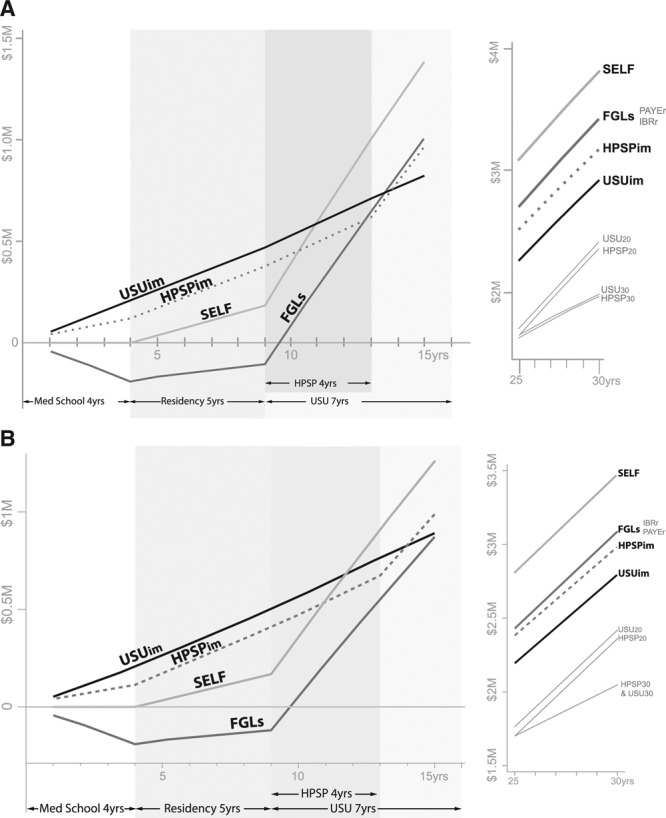

For example, in San Antonio, Texas, a city with no state income tax, borrowers who enter orthopedic surgery overtake their national service scholarship counterparts roughly four years after completing residency training (see Figure 1, Panel A). In Washington, DC, which has a high tax rate, it takes two additional years (see Figure 1, Panel B). Because the gap between what public- and private-sector general surgeons are paid is smaller than that between what public- and private-sector orthopedic surgeons are paid, borrowers require more than 20 postresidency years to match recipients of national service scholarships who turn to private-sector practice as soon as they fulfill their service obligation (see Figures 2 and 1, respectively). In ophthalmology, where the gap is smaller still, borrowing lags behind nearly all other options throughout our three-decade study interval (see Figure 3). Because public-service primary care physicians are paid as well as their counterparts in the private sector, borrowers who choose general internal medicine never catch up with their counterparts who secured a national service scholarship (see Figure 4).

Figure 2.

The results of a net present value analysis of different pathways for financing a medical school education starting in 2013, then practicing general surgery in San Antonio, Texas (Panel A) and in Washington, DC (Panel B). Abbreviations: FGLs, federally guaranteed loans, including pay-as-you-earn repayment (PAYEr) starting in residency and income-based repayment (IBRr) starting in residency; HPSP, Health Professions Scholarship Program, including transitioning to the private sector immediately after the 4-year service obligation (HPSPim), transitioning to the private sector after 20+ years of military service (HPSP20), remaining in the military until the end of the 30-year analysis (HPSP30); USU, Uniformed Services University of the Health Sciences, including transitioning to the private sector immediately after the 7-year service obligation (USUim), transitioning to the private sector after 20+ years of military service (USU20), remaining in the military until the end of the 30-year analysis (USU30); and SELF, self-financing the degree or obtaining a full institutional scholarship. Numerical values for these pathways are listed in Table 2.

Figure 3.

The results of a net present value analysis of different pathways for financing a medical school education starting in 2013, then practicing ophthalmology in San Antonio, Texas (Panel A) and in Washington, DC (Panel B). Abbreviations: FGLs, federally guaranteed loans, including pay-as-you-earn repayment (PAYEr) starting in residency and income-based repayment (IBRr) starting in residency; HPSP, Health Professions Scholarship Program, including transitioning to the private sector immediately after the 4-year service obligation (HPSPim), transitioning to the private sector after 20+ years of military service (HPSP20), remaining in the military until the end of the 30-year analysis (HPSP30); USU, Uniformed Services University of the Health Sciences, including transitioning to the private sector immediately after the 7-year service obligation (USUim), transitioning to the private sector after 20+ years of military service (USU20), remaining in the military until the end of the 30-year analysis (USU30); and SELF, self-financing the degree or obtaining a full institutional scholarship. Numerical values for these pathways are listed in Table 2.

Varying loan repayment terms made little difference in our models, because private-sector physicians earn enough to make IBR and PAYE repayments similar to standard 10-year loan repayments. Although a substantial amount of the debt accrued by PSLF program physicians is forgiven after 10 years of repayment, military physicians who serve 20 years before transitioning to the private sector do even better because any subsequent earnings can be added to their military pension.

For recipients of military scholarships (i.e., HPSP and USU), transitioning to private-sector practice has different effects, depending on timing and specialty. For orthopedic surgeons, separating from the military at the first available opportunity generates a substantially higher NPV than serving until eligible for a military pension (see Figure 1). For general internists, serving 20-plus years produces similar or higher NPVs than quickly transitioning to private-sector practice (see Figure 4).

Alternative assumptions were tested using sensitivity analyses. For example, if one assumes that the salaries of private-sector general internists will grow 3% faster than inflation rather than 1%, which is the base estimate, borrowers catch up with their military counterparts at the end of three decades. A similar salary growth rate among orthopedic surgeons shortens the time required for borrowers to overtake recipients of national service scholarships. If the Stafford loan rate was reduced from 6.21% to 3.5% (the current rate of a 30-year fixed mortgage), the NPV for borrowers would increase by $45,000 with a standard 10-year repayment term and by $53,000 to $61,000 in scenarios involving IBR or PAYE repayment plans. Conversely, modeling a real discount rate of 5% instead of 3% makes borrowing much less attractive, regardless of specialty. If military physicians who transition to the private sector reach salary parity with their specialty peers who went straight into private practice within two years, national service scholarships become more attractive. But if they are never paid more than 80% of the salary earned by these same peers, the value of this option decreases. Substituting Medical Group Management Association starting salaries or employing the slightly lower 2015–2016 Stafford loan rate of 5.84% did not appreciably alter our findings.

Discussion

Since 1987, approximately half of U.S. medical students have come from the richest quintile of household incomes; the proportion of students from the poorest quintile has not exceeded 5.5%.22 Even so, more than 80% of students finance part or all of their medical school education with loans. For the class of 2016, the median debt owed by new graduates was $190,000. Thirteen percent owed $300,000 or more.2 Although physicians are paid more than most Americans,23 their adjusted earnings have not kept pace with other health professionals.24 As a result, the debt-to-income ratios of new physicians have increased substantially over the past 20 years.25

To project the long-term consequences of borrowing versus other options for financing a medical school education, we conducted an NPV analysis, which is a standard economic approach that sums the present values of incoming and outgoing cash flows over time. Businesses use NPV analysis to project the profitability of different investment and financing options. NPV is not the same as retirement savings, because it does not take into account cost of living (e.g., family spending on food, clothing, shelter, child care, and other expenses) and discretionary purchases. Spending can vary dramatically from one household to the next, based on family size, circumstances, lifestyle, and the local cost of goods and services. We calculated the NPV of various financing pathways at the time a student matriculates to medical school and every year thereafter for three decades.

The results of our main model confirm that, for the first decade or more, students who avoid taking on debt are financially better off than those who borrow because the NPV of borrowing is sharply negative in medical school and does not cross zero until residency training is complete. At that point, it climbs steadily. In high-paying specialties, such as orthopedic surgery, where the pay gap between public-sector service and private-sector practice is large, borrowers overtake national service scholarship recipients as quickly as four years after residency. But, when the pay gap is narrow or nonexistent, as in primary care, borrowers never catch up with national service scholarship recipients (see Table 2).

Our study is limited by the uncertainty that surrounds long-term economic projections. Our main model assumed that existing differences in specialist pay, loan repayment options, and interest rates will remain stable over time. Because it is probable that one or more of these parameters will change in future years, we performed sensitivity analyses to examine different discount and income growth rates, alternative repayment strategies, and various lengths of service by scholarship recipients. Varying assumptions about income growth rates made the biggest difference over our study’s three-decade time span. To enable readers to assess alternative assumptions, we built an interactive tool that includes detailed calculations for each medical school education financing scenario (see Supplemental Digital Appendix 1 at http://links.lww.com/ACADMED/A419).

Our main model assumed that, when recipients of national service scholarships transition to private-sector practice, they earn 10% less than their peers who started in the private sector immediately after residency. Yet, there are no data to support this assumption. Alternative assumptions, including the equalization of pay within two years or, conversely, large and persisting disparities, substantially alter the projected NPV of national service scholarship recipients.

Our projections of the NPV of PSLF program participants are limited because specialty-specific figures on physician pay in PSLF facilities are not available. Thus, we could not analyze the difference in earnings between a general internist working in a public health department and an orthopedic surgeon working at a major academic medical center. Moreover, all of our models are based on aggregate data. An individual medical student’s tuition, fees, financial aid, monthly spending, family support, and future earnings may be higher or lower than the values incorporated into our models.

Career choices are based on more than economics. Students who are intent on becoming specialists and those who are reluctant to practice in a health professional shortage area are unlikely to pursue an NHSC scholarship. Likewise, students averse to military service will have no interest in USU or an HPSP scholarship, regardless of the financial benefits they confer. Conversely, debt-averse students and those drawn to the ideals of national service may find these programs attractive, even if they end up making less money in the long run.

Previous studies of medical student debt focused on the affordability of loan repayment, particularly for physicians who enter primary care. In 2010, Palmeri and colleagues26 modeled the probable income and expenses of a new primary care physician and determined that, during the first three to five years following residency, expenses exceed earnings. They concluded, “This reality greatly increases the financial disincentive for pursuing a career in [primary care].” In 2013, a team led by a senior AAMC analyst examined how a hypothetical physician might handle different levels of education debt. They analyzed 3 specialties and 16 repayment plans, including standard and extended repayment schedules, and 3 debt-reduction programs. The authors concluded that “a primary care career remains financially viable for medical school graduates with median levels of education debt.” However, some of the scenarios modeled left the primary care physician with as little as $200 to $600 per month in discretionary income.27

In the United States, most medical students are responsible for their own tuition, whereas, in many other countries, the bulk of medical education costs are borne by the public sector. Over time, the higher earnings of U.S. physicians more than offset this initial expense, particularly in highly remunerated specialties such as orthopedic surgery.28

Do medical school debt and the prospect of relatively low pay discourage graduates from choosing primary care?29–31 The evidence is mixed. One study found that students with high debt are less likely to pursue primary care, but the effect was modest when gender, race, and other demographic characteristics were taken into account.32 Other studies have suggested that economic considerations are less important than specialty content, the student’s personality, and the culture of the medical school.33–35

An even more fundamental concern is whether the cost of medical school deters disadvantaged students, particularly underrepresented minority (URM) students, from pursuing a career in medicine.22 If so, we must consider whether our nation’s current approach to financing medical education is in the best interest of students and the public. More than a decade ago, in a report entitled “In the Nation’s Compelling Interest: Ensuring Diversity in the Health-Care Workforce,” the Institute of Medicine (IOM) determined that “The costs associated with health professions training pose a significant barrier for many URM students, whose economic resources are lower, on average, than non-URM students.”36 To address this problem, the IOM recommended that “Congress should increase funding for Public Health Service Act Titles VII and VIII programs shown to be effective in increasing diversity, and should develop other financial mechanisms to enhance the diversity of the health-care workforce.” The IOM also recommended that “State and local entities … should increase support for diversity efforts through programs such as loan forgiveness, tuition reimbursement, loan repayment, GME, and supportive affiliations with community-based providers.”36

Conclusions

The economic value of a degree from a U.S. medical school eventually offsets the high up-front cost. However, avoiding debt through any of several options confers substantial economic benefits, particularly for medical students who are intent on practicing primary care or a relatively low-paying specialty. Our findings suggest that national service scholarships are an attractive option for students who aspire to become physicians but cannot afford a large education debt. If our nation wants to attract a more diverse health care workforce to meet its needs,37 policy makers should consider a range of options36 to make medical school more affordable.

Acknowledgments: The authors are deeply grateful to Anne Altemus, Donald Bliss, Bona Kim, John Harrington, and Kara Lukasiewicz of the Audiovisual Program Development Branch, Lister Hill National Center for Biomedical Communications, National Library of Medicine, for their expert assistance in producing the figures used to present these findings.

Supplementary Material

Footnotes

Editor’s Note: Invited Commentaries by U.E. Reinhardt and by J.E. Prescott, J.A. Fresne, and J.A. Youngclaus appear on pages 907–911 and 912–913, respectively.

Supplemental digital content for this article is available at http://links.lww.com/ACADMED/A419.

Funding/Support: Open access funding to make this report freely available to the public was provided by Defense Health Horizons, a policy analysis group sponsored by the U.S. Department of Defense.

Other disclosures: The views expressed are those of the authors and may not necessarily represent those of the U.S. Office of Personnel Management, the U.S. Department of Defense, or the U.S. Government.

Ethical approval: Reported as not applicable.

References

- 1.Association of American Medical Colleges. Tuition and student fees for first-year students. Summary statistics for academic years 2012–2013 through 2016–2017. AAMC Tuition and Student Fees Questionnaire. November 2016. https://www.aamc.org/data/tuitionandstudentfees/. Accessed December 6, 2016. [Google Scholar]

- 2.Association of American Medical Colleges. Medical student education: Debt, costs, and loan repayment fact card. http://members.aamc.org/eweb/upload/2016_Debt_Fact_Card.pdf. Published October 2016. Accessed December 6, 2016.

- 3.Association of American Medical Colleges. Physician Education Debt and the Cost to Attend Medical School. 2012 Update. February 2013Washington, DC: Association of American Medical Colleges. [Google Scholar]

- 4.U.S. Department of Education. Federal student aid. Interest rates for new direct loans. https://studentaid.ed.gov/About/announcements/interest-rate. Accessed December 6, 2016.

- 5.Edvisors. Federal student loans for graduate students. https://www.edvisors.com/college-loans/federal/stafford/graduate/?utm_source=staffordloan. Published 2016. Accessed December 6, 2016.

- 6.U.S. Department of Health and Human Services. Health Resources and Services Administration. Primary care loans. http://www.hrsa.gov/loanscholarships/loans/primarycare.html. Accessed December 6, 2016.

- 7.Federal Student Aid. Public Service Loan Forgiveness program. https://studentaid.ed.gov/sites/default/files/public-service-loan-forgiveness.pdf. Published 2015. Accessed December 6, 2016.

- 8.U.S. Department of Health and Human Services. Health Resources and Services Administration. National Health Service Corps. Scholarships. http://nhsc.hrsa.gov/scholarships/. Accessed December 6, 2016.

- 9.National Health Service Corps. National Health Service Corps Scholarship Program. School Year 2016–2017 Application & Program Guidance. March 2016. Rockville, MD: Bureau of Health Workforce, Health Resources and Services Administration, U.S. Department of Health and Human Services; https://nhsc.hrsa.gov/downloads/spapplicationguide.pdf. Accessed December 6, 2016. [Google Scholar]

- 10.U.S. Army. Army medicine: Health professions scholarship program. http://www.goarmy.com/amedd/education/hpsp.html. Accessed December 6, 2016.

- 11.Navy Medicine Professional Development Center. Health professions scholarship program. http://www.med.navy.mil/sites/navmedmpte/accessions/pages/healthprofessionsscholarshipprogram_prospective.aspx. Accessed December 6, 2016.

- 12.U.S. Air Force. Healthcare Professionals. Education and training: Health professions scholarship program. https://www.airforce.com/careers/specialty-careers/healthcare/training-and-education. Accessed December 6, 2016.

- 13.Uniformed Services University of the Health Sciences. School of Medicine. https://www.usuhs.edu/medschool. Accessed December 6, 2016.

- 14.Kinnamon KE. The Uniformed Services University of the Health Sciences: First Generation Reflections. 2004Bethesda, MD: Uniformed Services University of the Health Sciences. [Google Scholar]

- 15.DeZee KJ, Durning SJ, Dong T, et al. Where are they now? USU School of Medicine graduates after their military obligation is complete. Mil Med. 2012;177(9 suppl):68–71.. [DOI] [PubMed] [Google Scholar]

- 16.Association of American Medical Colleges. Medical Student Education: Debt, Costs, and Loan Repayment Fact Card. October 2013Washington, DC: Association of American Medical Colleges. [Google Scholar]

- 17.National Bureau of Economic Research. Internet TAXSIM Version 9.2 With ATRA. 2013. Cambridge, MA: National Bureau of Economic Research;http://users.nber.org/~taxsim/taxsim9/. Accessed December 6, 2016. [Google Scholar]

- 18.Weinstein MC, Siegel JE, Gold MR, Kamlet MS, Russell LB. Recommendations of the Panel on Cost-effectiveness in Health and Medicine. JAMA. 1996;276:1253–1258.. [PubMed] [Google Scholar]

- 19.U.S. Office of Personnel Management. Federal human resources data. http://www.fedscope.opm.gov/. Accessed December 6, 2016.

- 20.Uniformed Services University of the Health Sciences. Graduate medical education. https://www.usuhs.edu/gme/. Accessed December 6, 2016.

- 21.U.S. Department of Defense. Military compensation. http://militarypay.defense.gov/Pay/Retirement/. Accessed December 6, 2016.

- 22.Jolly P. Diversity of U.S. medical students by parental income. AAMC Analysis in Brief. 2008;8(1):1–2.. [Google Scholar]

- 23.Leigh JP, Tancredi D, Jerant A, Romano PS, Kravitz RL. Lifetime earnings for physicians across specialties. Med Care. 2012;50:1093–1101.. [DOI] [PubMed] [Google Scholar]

- 24.Seabury SA, Jena AB, Chandra A. Trends in the earnings of health care professionals in the United States, 1987–2010. JAMA. 2012;308:2083–2085.. [DOI] [PubMed] [Google Scholar]

- 25.Asch DA, Nicholson S, Vujicic M. Are we in a medical education bubble market? N Engl J Med. 2013;369:1973–1975.. [DOI] [PubMed] [Google Scholar]

- 26.Palmeri M, Pipas C, Wadsworth E, Zubkoff M. Economic impact of a primary care career: A harsh reality for medical students and the nation. Acad Med. 2010;85:1692–1697.. [DOI] [PubMed] [Google Scholar]

- 27.Youngclaus JA, Koehler PA, Kotlikoff LJ, Wiecha JM. Can medical students afford to choose primary care? An economic analysis of physician education debt repayment. Acad Med. 2013;88:16–25.. [DOI] [PubMed] [Google Scholar]

- 28.Laugesen MJ, Glied SA. Higher fees paid to US physicians drive higher spending for physician services compared to other countries. Health Aff (Millwood). 2011;30:1647–1656.. [DOI] [PubMed] [Google Scholar]

- 29.Bach PB, Kocher R. Why medical school should be free. N Y Times. May 28 2011. http://www.nytimes.com/2011/05/29/opinion/29bach.html. Accessed December 6, 2016. [Google Scholar]

- 30.Dower C. Health policy brief. Graduate medical education. Health Aff (Millwood). August 16 2012. http://healthaffairs.org/healthpolicybriefs/brief_pdfs/healthpolicybrief_73.pdf. Accessed December 6, 2016. [Google Scholar]

- 31.Brook RH, Young RT. The primary care physician and health care reform. JAMA. 2010;303:1535–1536.. [DOI] [PubMed] [Google Scholar]

- 32.Vaughn BT, DeVrieze SR, Reed SD, Schulman KA. Can we close the income and wealth gap between specialists and primary care physicians? Health Aff (Millwood). 2010;29:933–940.. [DOI] [PubMed] [Google Scholar]

- 33.Rosenblatt RA, Andrilla CH. The impact of U.S. medical students’ debt on their choice of primary care careers: An analysis of data from the 2002 medical school graduation questionnaire. Acad Med. 2005;80:815–819.. [DOI] [PubMed] [Google Scholar]

- 34.McDonald FS, West CP, Popkave C, Kolars JC. Educational debt and reported career plans among internal medicine residents. Ann Intern Med. 2008;149:416–420.. [DOI] [PubMed] [Google Scholar]

- 35.Kahn MJ, Markert RJ, Lopez FA, Specter S, Randall H, Krane NK. Is medical student choice of a primary care residency influenced by debt? MedGenMed. 2006;8:18. [PMC free article] [PubMed] [Google Scholar]

- 36.Institute of Medicine Committee on Institutional and Policy-Level Strategies for Increasing the Diversity of the U.S. Healthcare Workforce. In the Nation’s Compelling Interest: Ensuring Diversity in the Health-Care Workforce. 2004Washington, DC: National Academies Press. [PubMed] [Google Scholar]

- 37.Lipstein SH, Kellermann AL. Workforce for 21st-century health and health care. JAMA. 2016;316:1665–1666.. [DOI] [PubMed] [Google Scholar]

References cited in Table 1 only

- 38.Association of American Medical Colleges. Report on Medical School Faculty Salaries, 2012–2013. 2014Washington, DC: Association of American Medical Colleges. [Google Scholar]

- 39.2011–2012 Physician Salary Survey. PROFILES database. http://www.profilesdatabase.com/resources/2011-2012-physician-salary-survey. Published 2011. Accessed July 8, 2014. [No longer available.]