Abstract

Introduction:

Pakistan spends 0.7% of its gross domestic product on health. The public sector health-care system provides services to 22% of population thus paving the way for a dominant private sector. Patients in Pakistan mostly pay their medical expenses directly, and 64% of the health expenditures are borne by the household. Expenditure on medicine constitutes 43% of the total household expenditure.

Methods:

A quantitative cross-sectional study was conducted in Karachi, Pakistan, for a month. It was aimed at gathering response from different pharmacies to understand the brand versus generic dispensing trend of ciprofloxacin 500 mg, levofloxacin 500 mg, and moxifloxacin 400 mg oral dosage forms. The study employed convenience sampling and used a survey checklist. The data gathered was entered in SPSS version 22.

Results:

The mean price per tablet for ciprofloxacin brand and generic was reported at Pakistani Rupees (PKR) 48.44 and PKR 26.85, respectively. The trend for dispensing ciprofloxacin highlighted a split in the market between brand (51%) and generic (49%). For levofloxacin brand and generic, the price per tablet was reported at PKR 36.50 and PKR 36.15 respectively, and despite same price, the market was dominated by generic levofloxacin (92%). Due to a price difference between brand and generic moxifloxacin, i.e., PKR 129.44 and PKR 71.91, respectively, the market was mostly occupied by the generic form (75%).

Conclusion:

Pricing mechanism must be revisited, and the authorities should take stern actions against any illegitimate price hike. The surging burden of drug expenditure on poorer sections of the society must be addressed by the government on an urgent basis.

Keywords: Antibiotics, brand-generic substitution, ciprofloxacin, fluoroquinolone, generic drug, levofloxacin, moxifloxacin, Pakistan

INTRODUCTION

Inadequate access to affordable health care and medicines is one of the vital concerns in the developing countries.[1] United Nation's set of sustainable development goals place huge emphasis on the issue of health and well-being of people, particularly from developing countries. Goal 3 is of particular importance since it highlights the issue of providing access to effective and affordable treatment and medicines for everyone.[2]

Pakistan is one of the developing countries in South Asia. It spends 0.7% of its gross domestic product on health care. The public health-care system is not adequate to meet the demands of the masses. It provides services to merely 22% of the population thus paving way for a dominant private sector.[3] Moreover, in the absence of a national medical insurance; patients in Pakistan mostly pay their medical expenses directly out of their own pockets. 64% of the health expenditures are borne by the household themselves. Expenditure on medicine constitutes 43% of the total household expenditure in the country.[4] In this context, generic prescribing is advantageous in Pakistan as it lowers the price of medications thereby becoming less burdening on patient's pocket.[5]

A brand drug is a drug molecule which is developed by the parent pharmaceutical firm after years of research and investing huge finances. It is patented legally which stays in effect for a number of years. The generic drugs become available after the expiry of the patent of brand drug. Generic drugs are same as brand drugs and contain same active ingredient. Since they are the copies of brand drugs and do not require hefty amounts of finances to be invested in researching the molecule, they are less expensive and thus affordable for the poorer patients.[5,6,7]

However, generic prescribing has certain drawbacks in Pakistan where generic medicines can be registered in the country without bioequivalence studies.[8,9] This can lead to large number of generic drugs acquiring registration in the country. In addition, it can lead to competition among pharmaceutical companies and in the absence of vigilance on marketing and sales promotion activities, it can lead to unethical practices.[10]

According to the research literature and latest reports pertaining to pharmaceutical sector of Pakistan, the therapeutic category of systemic anti-infectives has a 24.7% market share which currently accounts for largest market share by any therapeutic category in the country and has a second highest growth rate, i.e., 13%. Further to this, a category of systemic anti-infectives, i.e., fluoroquinolone (FQL) antibiotic, namely, ciprofloxacin is the 3rd leading drug molecule in Pakistan with a sales volume over 6 billion Pakistani Rupees i.e., (PKR 6,004,295,567).

In this context, we designed a study targeting the above-mentioned therapeutic group which included antibiotics, namely, ciprofloxacin 500 mg, levofloxacin 500 mg, and moxifloxacin 400 mg, and documented the brand versus generic dispensing trend among the three drug molecules in the city of Karachi, Pakistan.[11,12,13]

METHODS

A quantitative cross-sectional study of 1-month duration was conducted among pharmacies located in different areas of the city of Karachi, Pakistan. The data collection began in April 2015 and was completed in May 2015. It was aimed at gathering response from different pharmacies regarding the brand versus generic dispensing trend for oral dosage forms of 3rd generation FQL antibiotics, namely, ciprofloxacin 500 mg, levofloxacin 500 mg, and moxifloxacin 400 mg. The scope of the study was to report the brand versus generic dispensing trend regardless of the prescribing patterns and patient demands for the said drugs. The study adhered to STROBE guidelines.

Operational definition

The study identified the following definitions for the terminologies used in the methodology:

Brand drug

A brand drug is a drug molecule developed a pharmaceutical firm after research and is patented for a number of years depending on the country's drug regulations.[5,7]

Generic/me-too drugs

Generic or me-too drugs are copies of the brand drug molecule and contain same active ingredient. They are available after the expiry of the patent period and are less expensive thus affordable for the poorer patients.[5]

Fast-moving and slow-moving drugs

Fast-moving drugs were those which according to the pharmacy's sale data had a relatively higher inventory turnover rate (ITOR) as compared to the other drugs and vice versa. ITOR is the number of times a particular drug stock is completely sold in the pharmacy.[14]

Participants and eligibility criteria

Community and hospital pharmacies were included in the study. Each pharmacy was represented by a pharmacy manager or owner. All medical and drug stores, marts, general stores, and pharmacies without a pharmacist were excluded from the study. In addition, pharmacies which did not consent to participate in the study were also excluded from the study. One response was gathered from each pharmacy.

Sampling technique

The study employed convenience sampling and gathered data from tertiary care hospital pharmacies and large community-based pharmacies in four districts of Karachi, namely, Central, East, Malir, and West. The reason to conduct a field survey in these districts was the presence of tertiary care hospitals and a large number of community pharmacies. Pharmacies were approached in their off-peak hours.

Research instrument and piloting

The study employed a checklist termed as FQL checklist for gathering the data which was exclusively developed by a team of experts comprising of a health economist and pharmacists with clinical, pharmaceutical, and regulatory knowledge. It was subjected to physical piloting and reliability analysis. The research instrument was piloted among 12 pharmacies and was validated. The reliability analysis reported Cronbach alpha value of 0.7.

The FQL checklist contained 6 items out of which 3 items, namely, location in districts, name of drug, price of drug were open-ended, and other 3 items i.e., type of pharmacy, type of drug, category of drug were close ended. The variables identified were demographics of the pharmacy such as the location in the city which was identified by city districts. Second, the type of the store, i.e., community-based or hospital-based was also identified as a variable. The other set of variables was the information about the drugs. Type of drug, i.e., fast- and slow-moving, category of the drug such as brand or generic and price of the drug were recognized as variables.

Data analysis and presentation

The data gathered was entered in Statistical Package for Social Sciences IBM SPSS version 22 (Statistical Package for Social Sciences) SPSS Inc., Chicago USA. software and was analyzed using frequency descriptive statistics, Chi-square (χ2) test, and cross tabulation. A significance level alpha (α) was noted at 0.05. The results were expressed as sample counts (N), percentages (%), and mean values (X). Statistical significance was reported in terms of significant P < 0.05.

Informed consent and ethical approval

Before data collection, informed consent was obtained from pharmacy representative. The participation in the study was voluntary. The representatives of the pharmacies were neither pressurized nor incentivized to participate. The study was subjected for ethical approval and was deemed exempted by the Department of Pharmacy Practice, Faculty of Pharmacy, Hamdard University Karachi, Pakistan, in April 2015. In addition, the study was also subjected to the ethical review and was granted exemption by the Institutional Review Board, Clifton Central Hospital, Karachi 75600, Pakistan (Letter #CHC234-1e-415).

RESULTS

A survey was conducted in the city of Karachi, Pakistan, which incorporated various districts of the city. The result of the study is divided in the following subsections.

Demographic information

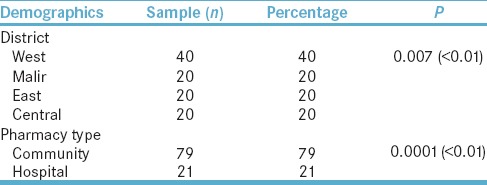

A total of 100 pharmacies were surveyed in the city of Karachi. The highest number of responses gathered (N = 40, 40%) were from the district West of Karachi; significant P < 0.01 were obtained. Furthermore, the survey also included responses from both community (N = 79, 79%) and hospital pharmacies (N = 21, 21%); significant P < 0.01 were reported. The summary is presented in Table 1.

Table 1.

Demographics of pharmacies

Description of drugs

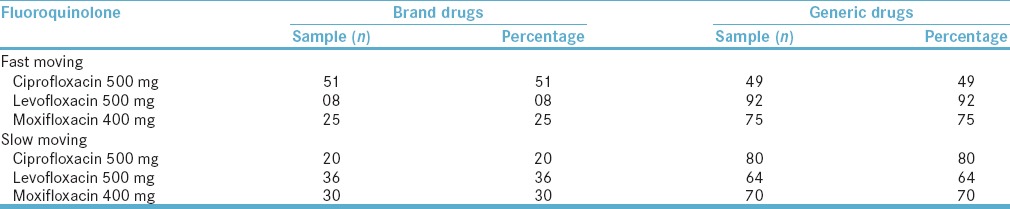

Furthermore, the trend reported that for fast-moving ciprofloxacin 500 mg, the market was split between brands (51%) and generics (49%) drugs. Contrastingly, generic levofloxacin dominated the market (92%). Similar figures were obtained for fast-moving moxifloxacin. The summary of FQL drugs with respect to brand and generic is reported in Table 2.

Table 2.

Fast-moving and slow-moving fluoroquinolone

Price per tablet

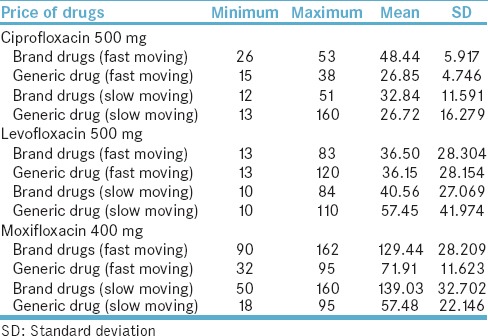

Regarding the prices of drug in fast-moving category, the mean price per tablet for ciprofloxacin 500 mg brand and generic was reported at PKR 48.44 and PKR 26.85, respectively. The slow-moving ciprofloxacin 500 mg brand and generic price were PKR 32.84 and PKR 26.72, respectively. The mean price of levofloxacin 500 mg brand and generic was reported at PKR 36.50 and PKR 36.15, respectively. The pricing information is tabulated in Table 3.

Table 3.

Pricing information

Cross tabulation of districts with drug category

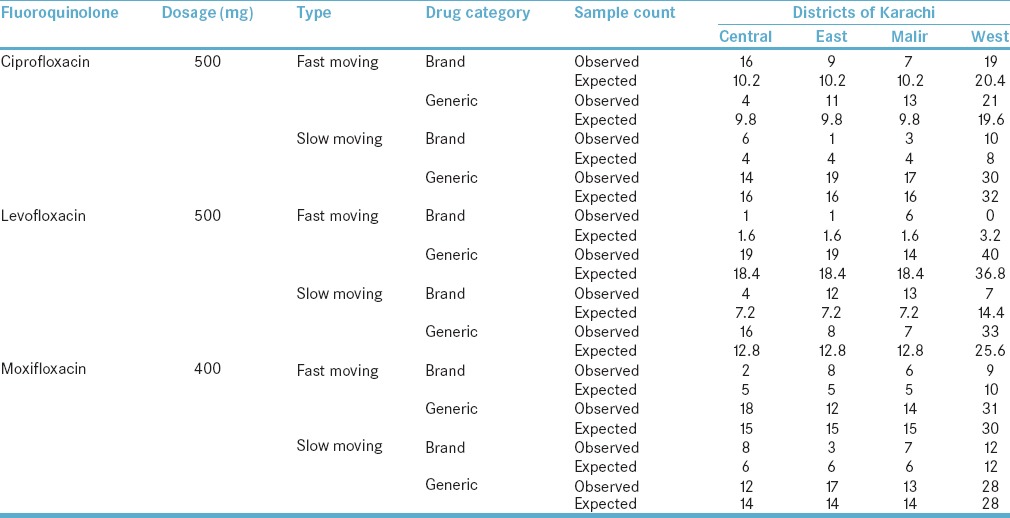

The association of districts of Karachi with the use of ciprofloxacin 500 mg fast-moving drug was statistically significant with Chi-square value reported at 9.264 and P = 0.026, i.e., <0.05. The strength of phi was strong, i.e., 0.304 effect size. However, in the case of slow moving, no statistical significance was observed, i.e., P = 0.172. The association of districts with levofloxacin 500 mg fast-moving drug was statistically significant as Chi-square value reported was 17.120 and P = 0.001, i.e., <0.05. The strength of phi for this association was strong, i.e., 0.414 effect size. Similarly, the association of districts with slow-moving levofloxacin 500 mg drug was also statistically significant with high value reported for Chi-square, i.e., 20.464, P = 0.0001, i.e., <0.01 and strong effect size with phi = 0.452. There was no statistical significance for the use of fast- and slow-moving moxifloxacin 400 mg with districts of Karachi with P value reported at 0.158 and 0.343, respectively. The summary of cross tabulation is presented in Table 4.

Table 4.

Cross-tabulation of districts with medications

DISCUSSION

This cross-sectional observational study was designed in the form of a survey using a checklist coined by the term FQL. The survey was conducted in the city of Karachi and gathered response from the pharmacies. The majority of the pharmacies surveyed were community-based (79%) and were located in the district West of Karachi (40%). The survey observed that the drugs under investigation were fast moving and slow moving. This was established by a predefined criterion based on ITOR which has been explained previously in methodology. There could be no figure which defines this phenomenon as stocking of drugs depends on the size and work load of a pharmacy.

The survey reports that for ciprofloxacin 500 mg, the pharmaceutical market is split between brand (51%) and generic drugs (49%); however, the market is dominated by generic drugs (92%) for levofloxacin 500 mg and moxifloxacin 400 mg (75%). The category of slow-moving drugs largely comprises generic form, i.e., ciprofloxacin 500 mg (80%), levofloxacin 500 mg (64%), and moxifloxacin 400 mg (70%). In Pakistan, there is no restriction on the number of generic medicines registration, and no bioequivalence tests are required as a prerequisite to new drug registration. As a result, it is very easy to register a generic drug against a patented drug molecule or a brand drug. This results in the market being flooded with too many average quality generic drugs.[8,15]

The issue of price of drugs is of paramount importance keeping in view the health-care system of Pakistan where in most cases, patients have to pay out of their own pocket for treatments and drugs.[7,16] Regarding the price per tablet for ciprofloxacin 500 mg, the mean price of a fast-moving brand is PKR 48.44 with least expensive brand available for PKR 26 and most expensive for PKR 53. Similarly, the mean price per tablet for fast-moving generic ciprofloxacin is PKR 26.85 giving a price difference of PKR 21.59 between brand and generic form. Despite this price difference, the market is almost split between the two categories. Generic prescribing and dispensing are desired in developing countries where share of expenditure on drugs in the total out of pocket medical expenses account for almost 80% in most of the cases.[17] This is because generic medicines are generally less costly than brand; however, perceptions regarding generic medicines may not be positive, and this may lead to an increased preference for brand drug.[18]

In a study conducted in Pakistan, it was reported that the perceptions of health-care professionals toward generic medicines were negative.[5] Hence, they preferred prescribing the brand which was expensive. Moreover, there is a lack of technical expertise for the detection of substandard and counterfeit products at various levels of pharmaceutical supply chain.[19] It contributes to the apprehensions about generic prescribing in the country, and thus, it is observed that brand drugs are preferred despite being high-priced.

For levofloxacin 500 mg, the mean price per tablet for fast-moving brand is PKR 36.50 while the price for generic is PKR 36.15. The least expensive generic available costs PKR 13 and most expensive is available for PKR 120 which is far greater than the most expensive levofloxacin brand available, i.e., PKR 83. Despite same mean price per tablet for brand and generic levofloxacin drugs, the market is dominated by generic levofloxacin which presents an opposite picture when compared to the scenario of ciprofloxacin. This is contrary to the purpose generic drugs were introduced, i.e., to safely reduce the overall expenditure on drugs a patient had to make. In theory, the average cost of a generic drug is far lower than the brand; however, this case highlights an escalating price of generic instead of brand.[7]

The preference of a generic medicine normally results due to its economical price which is not observed in this case. However, it is still prescribed and dispensed largely; hence, highlighting the marketing and sales promotion activities of local pharmaceutical manufacturers. A number of studies have been conducted in Pakistan, especially in Karachi, that draw attention to the mal prescribing and unethical sales promotion activities of local pharmaceuticals in Pakistan.[5,10] Apart from this, the surging prices for generic drugs, in this case, highlight the issue of supply shortages. For many drugs, there are only few generic manufacturers that are responsible for the supply of the particular drug. These companies thrive on their market position and enjoy the little competition friction, thereby posing risks for creating drug shortage as well as exploitation of pricing power.[20]

For moxifloxacin 400 mg, the mean price per tablet for fast-moving brand is PKR 129.44 while generic is available for PKR 71.91. Our data reported that the generic form was dispensed mostly. This is logical in the context of Pakistani environment as poor economic conditions compel the patients to opt to cheaper alternatives. The important role of generic drugs in helping reduce the overall expenditure on health care can be observed in this particular case of moxifloxacin.

The results of cross-tabulation revealed that the location of pharmacies in the city were statistically associated with the dispensing trends. For fast-moving ciprofloxacin 500 mg, there is a high-dispensing trend of brand drug in the district central while generic form is routinely dispensed in more numbers in districts East, Malir, and West. For levofloxacin 500 mg and moxifloxacin 400 mg, fast-moving generic form dominates the market.

Generic drugs, in essence, can play a significant role in the development of a sustainable health-care system through their lower costs. However, in case of Pakistan, certain policy measures must be taken to fully realize the benefits of it. First, the Drug Regulatory Authority of Pakistan (DRAP) needs to take measures and devise plans for inclusion of bioequivalence tests as a prerequisite to new registrations for generic medicines. This may help in limiting the number of generics being registered and at the same time improving the quality of registered generics in the country. It must keep a vigilant eye on the unethical sales and promotion practices of pharmaceutical firms in the country. Steps must be taken for the detection of counterfeit and substandard drugs.

The surging burden of drug expenditure on poorer sections of the society must be addressed by the authorities on an urgent basis, and pricing mechanism must also be revisited. It should be structured after discussion with the various drug suppliers. The authorities should take stern actions against any illegitimate price hike or drug shortages which adversely affect the well-being of patients.

Efforts must be taken to improve the perceptions about generic drugs among all important stakeholders including physicians, pharmacists, and patients. Discussions must be held to address the misconceptions of all stakeholders. Literature highlights that apprehensions exist among physicians and patients regarding generic drugs which results in refusal of brand-generic substitution for various medicines.

CONCLUSION

Generic drugs are usually preferred in those countries where patients have to pay for the health-care expenditures out of their own pocket. The surging cost of the pharmaceuticals is a vital factor that impedes the access to medicines in the developing countries. The drug registration procedure of Pakistan lacks important steps such as bioequivalence testing. This makes the process easier for a new generic drug to obtain registration and enter the market without upholding quality standards. As a result, the market is filled with average-quality me-too drugs. In some cases, despite price of generic drug being much lower than the brand, a high dispensing trend for the brand is observed which highlights the negative perceptions of health-care professionals regarding generic prescribing. In another case where there is no gap between brand and generic in terms of price, dispensing of generic versus brand indicates the intensive marketing and sales activities of pharmaceutical firms.

Financial support and sponsorship

Nil.

Conflicts of interest

There are no conflicts of interest.

Supporting information

This research paper is based on a student research project undertaken by Sumbul Tasneem, Adnan Zia Shamsi, Naqiya Ali Asghar and Ghufran Ullah Khan of Doctor of Pharmacy (Pharm D) program at Faculty of Pharmacy, Hamdard University Karachi, Pakistan, during March 2015 to September 2015. The research project was a part of Evidence-Based Improvement Initiative.[21] It was aimed at inciting a research culture among undergraduate pharmacy students of Pakistan.[22]

REFERENCES

- 1.Improving Access to Health Care for the Poor, Especially in Developing Countries. Global Economic Symposium. 2008. [Last cited on 2017 Jan 12]. Available from: http://www.global-economic-symposiumorg/knowledgebase/the-global-society/financing-health-care-for-the-poor/proposals/improving-access-to-health-care-for-the-poor-especially-in-developing-countries .

- 2.Ensure Healthy Lives and Promote Well-being for All at All Ages. Sustainable Development Goal 3. Progress Towards the Sustainable Development Goals, E/2016/75. United Nation Sustainable Development Knowledge Platform. 2016. [Last cited on 2017 Jan 12]. Available from: https://www.sustainabledevelopment.un.org/sdg3 .

- 3.Zaidi S, Bigdeli M, Aleem N, Rashidian A. Access to essential medicines in Pakistan: Policy and health systems research concerns. PLoS One. 2013;8:e63515. doi: 10.1371/journal.pone.0063515. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Zaidi S, Nishtar NA. Access to Medicines: Identifying Policy Concerns and Policy Research Questions, Research Report, Aga Khan University Karachi and the Alliance for Health Policy & Systems Research. Geneva: WHO; 2011. [Google Scholar]

- 5.Jamshed SQ, Hassali MA, Ibrahim MI, Babar ZU. Knowledge attitude and perception of dispensing doctors regarding generic medicines in Karachi, Pakistan: A qualitative study. J Pak Med Assoc. 2011;61:80–3. [PubMed] [Google Scholar]

- 6.Das N, Khan AN, Badini ZA, Baloch H, Parkash J. Prescribing practices of consultants at Karachi, Pakistan. J Pak Med Assoc. 2001;51:74–7. [PubMed] [Google Scholar]

- 7.Aijaz T. Generic Drugs: A Better Alternative for Low Income Countries. JPMS 2015. [Last cited on 2017 Jan 14]. Available from: http://blogs.jpmsonline.com/2015/09/19/generic-drugs-a-better-alternative-for-low-income-countries/

- 8.Hasan SK. Prospects of drug bioequivalence studies in Pakistan. J Dow Univ Health Sci Karachi. 2012;6:39–41. [Google Scholar]

- 9.Generic Medicines Flooding Market Sans Tests, Research. The News. 2012. [Last cited on 2017 Jan 14]. Available from: https://www.thenews.com.pk/archive/print/343372-generic-medicines-flooding-market-sans--tests-research .

- 10.Khan N, Naqvi AA, Ahmad R, Ahmed FR, McGarry K, Fazlani RY, et al. Perceptions and attitudes of medical sales representatives (MSRs) and prescribers regarding pharmaceutical sales promotion and prescribing practices in Pakistan. J Young Pharm. 2016;8:244–50. [Google Scholar]

- 11.Aamir M, Zaman K. Review of Pakistan pharmaceutical industry: SWOT analysis. Int J Bus Inf Technol. 2011;1:114–7. [Google Scholar]

- 12.A Comparative Study of Pharmaceutical Industry of Pakistan and China. Industrial Notes: Pharmaceutical Industry. Institute of Business Administration (IBA) 2016. [Last cited on 2017 Feb 5]. Available from: https://www.iba.edu.pk/News/industrial-note-pharmaceutical-sector.pdf .

- 13.Sfetcu N. Health and Drugs: Disease, Prescription and Medication. 1st ed. ebook (ePub.) 2014 Feb 22; ISBN 9781312039995. [Google Scholar]

- 14.Ingersoll K. Inventory Management for the Pharmacy Technician. Educational Review Systems. Accreditation Council of Pharmacy Education (ACPE). Ch. 6. [Last cited on 2017 Feb 5]. Available from: https://www.s3.amazonaws.com/EliteCME_WebSite_2013/f/pdf/RPTFL04IMI14.pdf .

- 15.Ahmed SI. Global Pharma Companies See Battle for Survival in Pakistan. Intellectual Property Watch. 2013. [Last cited on 2017 Jan 28]. Available from: http://www.ip-watchorg/2013/03/21/global-pharma-companies-see-battle-for-survival-in-non-ipr-compliant-pakistan/

- 16.Naqvi AA, Naqvi SB, Zehra F, Ahmad R, Ahmad N. The cost of poliomyelitis: Lack of cost of illness studies on poliomyelitis rehabilitation in Pakistan. Arch Pharma Pract. 2016;7:182–4. [Google Scholar]

- 17.WHO. WHO/EDM/PAR/20045. Geneva: World Health Organization; 2017. [Last cited on 2017 Jan 29]. The World Medicines Situation. Available from: http://www.who.int/medicines/areas/policy/world_medicines_situation/en/ [Google Scholar]

- 18.Mathew P. Generic drugs: Review and experiences from South India. J Family Med Prim Care. 2015;4:319–23. doi: 10.4103/2249-4863.161305. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19.Robles YR, Casauay JF, Bulatao BP. Addressing the Barriers to Effective Monitoring, Reporting and Containment of Spurious/Substandard/Falsely-labelled/Falsified/Counterfeit Medical Products through Sustainable Multi-stakeholder Collaboration and Community/Consumer-based Interventions. Medicines Transparency Alliance, Philippines. 2016. [Last cited on 2017 Jan 31]. Available from: http://www.who.int/medicines/areas/coordination/SSFFC_Report.pdf .

- 20.Financing and Sustainability. Pharmaceutical Pricing Policy. 2012. [Last cited on 2017 Jan 31]. Available from: http://www.apps.who.int/medicinedocs/documents/s19585en/s19585en.pdf .

- 21.Abbas A. Evidence based improvements in clinical pharmacy clerkship program in undergraduate pharmacy education: The Evidence Based Improvement (EBI) initiative. Pharmacy. 2014;2:270–5. [Google Scholar]

- 22.Naqvi AA. Evolution of clinical pharmacy teaching practices in Pakistan. Arch Pharma Pract. 2016;7:26–7. [Google Scholar]