Abstract

Critics of me-too innovation often argue that follow-on drugs offer little incremental clinical value over existing pioneer products, while at the same time increasing health care costs. We examine whether consumers view follow-on and pioneer drugs as close substitutes or distinct clinical therapies. For five major classes of drugs, we find that large reductions in the price of pioneer molecules after patent expiration—which would typically lead to decreased consumption of strong substitutes—have no effect on the trend in demand for follow-on drugs. Our findings are likely unaffected by health insurance, competitive pricing of me-toos, marketing, and switching costs.

Keywords: innovation, pharmaceuticals, “me-too” drugs

1. Introduction

The creation of a successful new therapeutic class of pharmaceuticals, based on a previously unknown or unexploited biological mechanism, typically motivates the development of similar drugs employing the same mechanism but with a different molecule and therefore a different patent. Depending on the speed with which competing molecules can be discovered and tested, and the projected profitability of the therapeutic area, the result can be a gradually expanding therapeutic class. Among the most notable examples of this dynamic are the penicillin and cephalosporin classes of antibiotics, beta-blockers for heart disease, H2-blockers and proton pump inhibitors for peptic ulcers and acid reflux disease, HMG-COA reductase inhibitors (statins) for hypercholesteremia, and the SSRI and SNRI classes of antidepressants. Although this process was once seen as taking place more or less sequentially, in recent years most follow-on drugs have been developed in parallel, almost simultaneously (DiMasi and Paquette, 2004).

The development of follow-on or “me-too” drugs has long been the subject of much controversy (US Department of Health, 1968). Critics charge that follow-on drugs provide little or no therapeutic improvements while increasing health care costs through increased marketing and R&D and by diverting sales to newer drugs before patents of pioneer brands expire, thus maintaining or increasing class revenues despite the introduction of inexpensive generic versions of pioneers (Angell, 2004; Goozner, 2004; Kessler, 1994).

A number of analysts have argued, however, that follow-on drugs benefit patients and the health care system in several ways. They can reduce health care costs by providing price competition and limiting the length of pioneer market exclusivity and, perhaps, offering new ways to offset costs elsewhere in the health care system (DiMasi and Paquette, 2004; Lee 2004). Follow-ons typically provide therapeutic improvements for some patients, especially as the emerging science of pharmacogenomics reveals with greater clarity the groups of patients who respond poorly to existing drugs (Lee, 2004; Wertheimer, 2001). Follow-ons can also provide superior or more flexible dosage and administration, which in turn, may reduce treatment costs. Marketing for follow-on drugs can reduce the under-treatment associated with even some of the most crowded therapeutic classes as well. These findings are consistent with simple economic reasoning—-the fact that a substantial fraction of individuals purchase follow-on drugs when similarly priced pioneer drugs exist, suggests that there is likely some value added by these medicines. Finally, and perhaps most important, follow-on drugs, which typically have a longer remaining patent life than pioneers, motivate and support research that applies to an entire therapeutic class. This has been especially notable in connection with the statins (Langreth, 1998; Shepherd et al., 1995; Topol, 2004; Nissen et al., 2006) and SSRI antidepressants (Holden, 2003). This in turn can increase usage, much of it coming from marketing for drugs with expanded FDA-approved indications that are never approved for pioneer drugs.

Empirical research on these effects is remarkably scarce. One of us has estimated that follow-on drug competition, rather than patent expirations, is the strongest force in reducing the capital value of pioneer brands in competitive therapeutic classes (Lichtenberg and Philipson, 2005). DiMasi (2000) and Lee (2004) document that the earliest follow-on drugs often enter at prices below those of the dominant existing therapies, thus putting pressure on the pioneer company to reduce price in order to maintain share.

We are aware of no empirical attempt, however, to assess whether follow-on drugs tend to provide sufficiently improved therapeutic outcomes so that patients, physicians and health care payers would prefer to use them even when cheaper generic versions of pioneer drugs appear. To address this question, we examine the extent to which patients, providers, and health plans actually substitute between pioneer and follow-on drugs in real markets.

In economic terms, determining whether follow-on drugs provide sufficiently improved therapeutic outcomes or value to patients, providers, and payers is akin to determining whether pioneer and follow-on drugs are weak or strong substitutes. By definition, two goods are substitutes if an increase in the price of one leads individuals to consume more of the other, as might be the case with comparable TVs, comparable cars, or other goods. Much like two identical TVs sold by different quality stores, branded drugs and their generics are naturally strong substitutes—an increase in the price of one significantly increases demand for the other. When individuals find two drugs (or TVs) less comparable, however, an increase in the price of one may lead only a few consumers to substitute towards the other. In fact, the extent to which the demand for follow-on drugs rises as the price of pioneers falls can inform us about their substitutability. In particular, large reductions in the price of pioneer molecules that are accompanied by small (large) changes in the demand for follow-on drugs would indicate that the two are less (more) substitutable than often argued.

Our reasoning implies that if follow-on drugs provide negligible therapeutic advantages, physicians will rapidly switch to prescribing generic versions of pioneer drugs in the wake of dramatic price reductions after patents expire. That physicians quickly abandon pioneer brands in favor of less expensive generic versions is well established, so it is clear that price reductions do have dramatic effects on prescribing when only insignificant therapeutic losses are involved. In particular, for a group of 21 innovator drugs facing generic competition between 1991 and 1993, a 1998 Congressional Budget Office Report found that generics accounted for nearly 40% of the market share within one year of branded patent expiration. It seems reasonable, then, to expect similar, if less pronounced, switching behavior away from me-too drugs if, in fact, those drugs provide little therapeutic advantage over the pioneer. Conversely, a lack of such switching in the face of large price advantages for the generic pioneer would strongly suggest that patients and physicians see follow-ons as providing therapeutic advantages worth the premium in price.

To explore these questions, we obtain national sales data on five important and best-selling therapeutic classes in which the pioneer drug went off-patent during the years 1992 through 2004: statins, H-2 receptor antagonists (H2RAs), proton pump inhibitors (PPIs), ACE inhibitors, and SSRIs. Focusing on a window of time around patent expiration offers us a unique natural experiment with which to trace out the effects of exogenous changes in the price of pioneer molecules on the demand for follow-on drugs.1 Prior to patent expiration, the price of the pioneer molecule is simply the price of the branded version. After patent expiration, however, the average price individuals pay for the molecule is significantly lower, reflecting the introduction of cheaper generics.

Our data indicate the well known pattern that the fall in the price of a pioneer molecule following patent expiration is large. For the classes considered, the average price paid prior to patent expiration is nearly 3 to 5 times higher than 3 years after expiration. As is also well known, this price decrease is accompanied by a large substitution from the branded version of the pioneer molecule to its generic form, consistent with strong substitutability between the two. Absent, however, is any observed change in the trend of follow-on drug demand, suggesting that for many patients and physicians, follow-on drugs may be perceived as imperfect substitutes for their predecessors. Importantly, for 3 of the 5 classes considered, follow-on drugs command a premium in price compared to the branded pioneer in the years prior to its patent expiration. This suggests that follow-on drugs in at least some classes are perceived to offer clinical benefits worth the extra premium.

After presenting our results, we will discuss several possible alternative explanations for our findings. One is that the presence of insurance and/or physicians acting on behalf of their patients makes individuals less responsive to changes in price. However, this view is, of course, inconsistent with the observed substitution towards generics after patents expire. A second explanation for this lack of response is a concomitant reduction in the price of follow-on drugs that causes individuals who would otherwise switch to continue consuming. We find no evidence of this. Relative prices of pioneer drugs (i.e. price of the pioneer divided by the average price of follow-ons) are stable prior to patent expiration and exhibit sharp declines thereafter, consistent with little or no offsetting decreases in the price of follow-on drugs. A third alternative explanation is that a surge of marketing for follow-on drugs prevented diversion to generic versions of the pioneer molecule. A final alternative explanation is that non-financial costs of switching brands dissuaded physicians and patients from moving to generics. Our sub-analysis of new prescriptions, as opposed to refills, suggests, however, that new prescriptions for follow-ons are still unresponsive to the generic availability of the pioneer drug.

2. Data

We analyzed national-level revenue and quantity data estimated by IMS Health on individual drugs in five leading therapeutic classes from 1992 through 2004: statins for hypercholesterolemia, H-2 receptor antagonists and proton pump inhibitors for peptic ulcers and acid reflux disease, ACE inhibitors for hypertension, and SSRIs for depression. In each of these classes, the pioneer drug went off patent during this period. These classes represent a significant portion of total US sales revenue. In 2005, for example, statins, PPIs, and SSRIs were the top three classes in terms of sales revenue with ACE inhibitors coming in tenth. Together, revenue for these four classes amounted to nearly $44 billion or 17% of total US sales (IMS Health). As would be expected, the individual drugs within these classes were also important in terms of total sales. Lipitor, Zocor, Prevacid, Nexium, and Zoloft were among the top six selling drugs in 2005 and are included in our data.

To isolate the effect of reductions in the price of pioneer molecules on the demand for follow-on drugs, we restricted our attention to a six-year window surrounding patent expiration (3 years before and after). Focusing on patent expiration allowed us to capture the effect of a supply-induced change in pioneer price, one that is presumably uncorrelated with unobserved factors affecting the demand for follow-on drugs.

For each class, national-level sales data (quantity and revenues) were available for both the first-in-class drug (in both its branded and generic form), as well as all other follow-on drugs marketed and sold during our roughly six-year timeframe. To avoid an artificial expansion in follow-on market share after patent expiration of the pioneer product, we restricted the follow-on drugs in our sample to only those that were introduced prior to patent expiration of the pioneer. Exhibit 1 displays the specific years considered for each class as well as the individual drugs included.2

EXHIBIT 1.

Pioneer and follow-on drugs in our sample

| Class | Pioneer Drug | Date of Generic Entry | Dates Considered | Follow-On Drugs |

|---|---|---|---|---|

| H-2 Receptor Antagonists | Tagamet (Cimetedine) |

5/94 | 1/92 to 5/97 | Axid, Pepcid, Tritec, Zantac |

| ACE Inhibitors | Capoten (Captopril) |

12/95 | 3/92 to 3/98 | Accupril, Altace, Lotensin, Monopril, Prinivil, Univasc, Vasotec, Zestril |

| SSRIs | Prozac (Fluoxetine) |

8/01 | 8/98 to 8/04 | Celexa, Lexapro, Paxil, Zoloft |

| Statins | Mevacor (Lovastatin) |

12/01 | 8/98 to 8/04 | Baycol, Lescol, Lipitor, Pravachol, Zocor |

| Proton Pump Inhibitors | Prilosec (Omeprazole) |

12/02 | 11/98 to 11/04 | Aciphex, Nexium, Prevacid, Prevpac, Protonix, Zegerid |

Notes: ‘Prozac’ includes prescription form Prozac Weekly, ‘Tagamet’ includes Tagamet HB, and ‘Prilosec’ includes Prilosec OTC.

In the IMS data, quantity is defined as the total number of units purchased—individual tablets, capsules, etc. for solids and the number of grams or millimeters for liquid forms.3 Sales (or purchase dollars) are defined as the total amount of money retail pharmacies, mail service pharmacies, non-federal hospitals, federal facilities, long-term care facilities, clinics, HMOs, home health care facilities, and miscellaneous facilities spent on a given product. Although this measure does not account for off-invoice discounts such as rebates, it does include on-invoice discounts (e.g. to hospitals).4

We used these measures of sales revenue and purchase quantity to construct the per-unit price for each drug, defined as sales divided by the total number of units purchased. For the pioneer molecule, per-unit price is equal to the per-unit brand price prior to patent expiration and to a quantity-weighted average of the generic and brand price afterwards. The average price of follow-on drugs is calculated similarly—sales divided by quantity purchased. The average price across all me-too drugs in a class is a quantity-weighted average of the individual prices.

3. Results

3.1 Substitution between Follow-On and Pioneer Drugs after Patent Expiration

This section presents our findings for each of the five classes considered. In each case, we are interested in three questions. How does the price of a pioneer molecule change after its patent expires? What is the impact of this supply-induced price change on the demand for pioneer molecules? And most importantly, what is the impact on the demand for follow-on drugs?

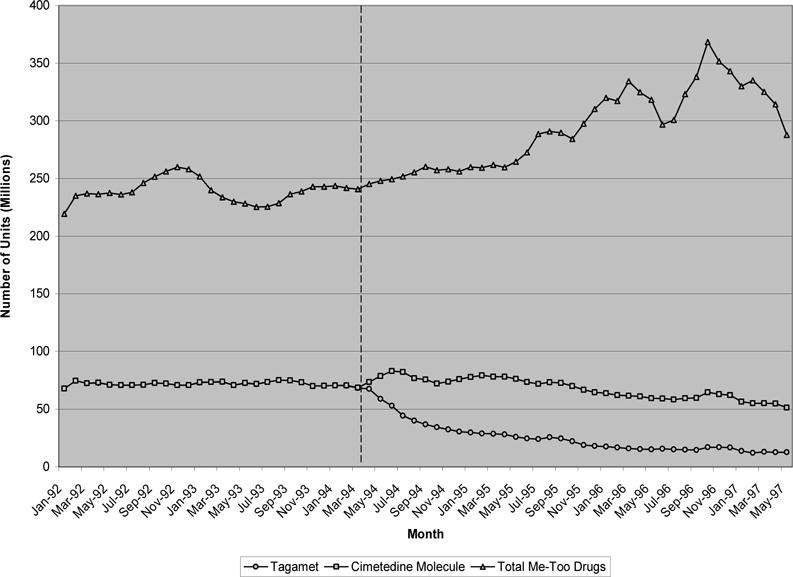

Exhibit 2 considers the earliest therapeutic class in our data set, H-2 receptor antagonists (H2RAs). The pioneer molecule of this class, Tagamet (cimetedine), lost patent protection in May 1994. Prior to patent expiration, nearly 70 million units of Tagamet were purchased monthly, compared to 250 million units for its follow-on counterparts. Immediately after patent expiration, however, Tagamet experienced a sharp decline in quantity. However, sales of generic replacements nearly fully offset that reduction, leaving the total quantity of the molecule purchased relatively unchanged. This transition was associated with a 67% reduction in the price of the pioneer molecule, from 75 cents for the branded version to 25 cents per unit for the generic versions. At the same time, the purchase quantity of the follow-on brands remained stable and then increased, despite the dramatic reduction in the price of the pioneer molecule. Put together, these findings suggest a relatively inelastic demand for the pioneer molecule among those consuming it. It appears that the main effect of generic introduction was to induce switching away from branded Tagamet to generic versions, with little or no switching away from the follow-on drugs.

EXHIBIT 2.

Monthly quantity of H-2 Receptor antagonists

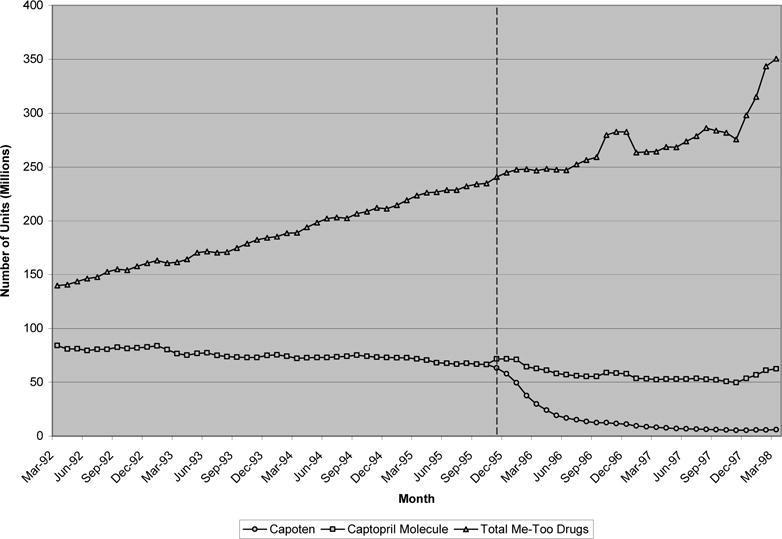

Exhibit 3 presents similar results for ACE inhibitors, a class characterized by a great deal of me-too competition—nearly 10 molecules were available in this class in the six year time period considered. Capoten (captopril), the pioneer drug in this class, went off patent in December 1995. In the two years prior to patent expiration, roughly 70 millions unit of branded captopril were purchased monthly compared to close to 250 millions units of me-too ACE inhibitors. After generic entry, the average price of the captopril molecule fell 78% from 55 cents per unit to 12 cents. This reduction in price was accompanied by little or no change in the total quantity of the captopril molecule purchased, but instead a large substitution from Capoten to generic versions of the drug. Similar to the H2RAs, little or no change in the demand trend was observed for “me-too” ACE inhibitors in the 12 months after Capoten’s patent expired. By the end of two years, the quantity of follow-on drugs purchased was actually higher than before.

EXHIBIT 3.

Monthly quantity of ACE inhibitors

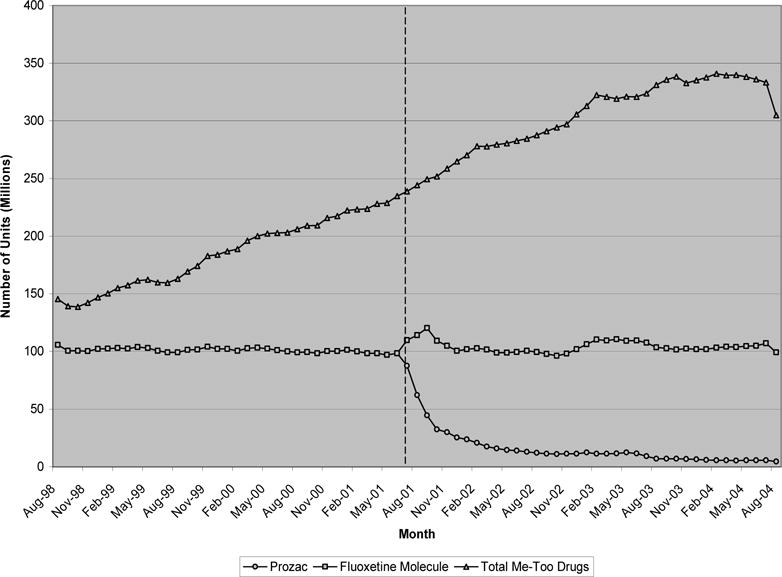

Exhibit 4 presents the quantity data for SSRIs. Prozac (fluoxetine), the first and most widely prescribed molecule in this class, went off patent in August 2001. Its early dominance in this class is clear—three years prior to patent expiration, nearly 100 million units of the 250 million units of SSRIs purchased monthly were due to prescriptions for Prozac. Over the course of the next six years, purchases of the fluoxetine molecule remained nearly constant at 100 million units monthly. While the quantity of the pioneer molecule purchased was unchanged after patent expiration, there was again significant substitution away from the brand towards generic versions of the medicine. In this case, substitution was particularly large with nearly 95% of fluoxetine purchases coming from generic sales three years after patent expiration. This was associated with an 80% reduction in the average price of the pioneer molecule, from $2 per unit to 40 cents. Consistent with our results so far, there again appeared to be no change in the trend of follow-on drug purchases within the same class, Celexa, Lexapro, Paxil, and Zoloft. After August 1998, sales of these products followed a roughly linear trend over the next six years, with no observable decline in the trend following expiration of Prozac’s patent.

EXHIBIT 4.

Monthly quantity of SSRIs

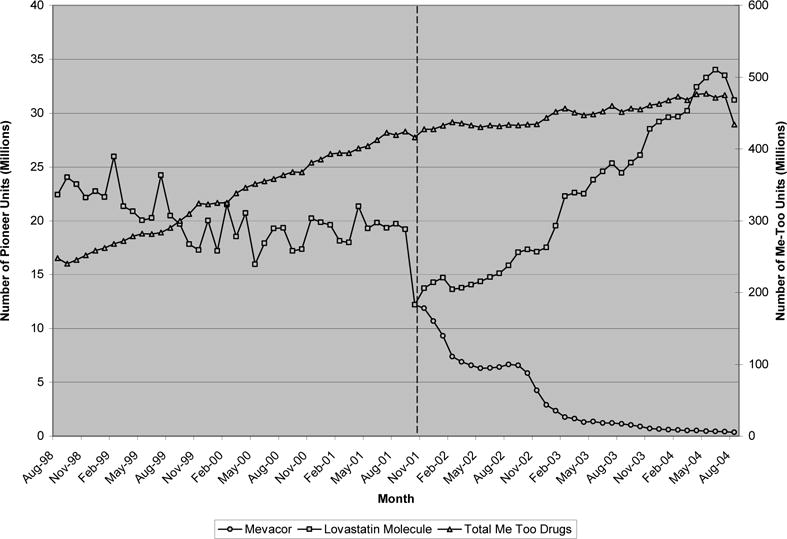

The next leading class of therapeutics considered, statins, displays a pattern similar to the earlier classes. Since 2003, the statins have been the highest revenue class of medicines. Exhibit 5 illustrates that by August 2004, just over 500 million units of statins were purchased monthly.5 This compares to slightly more than 200 million units six years earlier. Compared to the previous classes, however, the first drug in this class, Mevacor (lovastatin), experienced substantially lower market share in the face of me-too competition. In the six years considered, this share hovered between 5 and 10 percent of all statin purchases. Interestingly, and unlike the other drugs classes considered, Mevacor faced me-too competition from not only other manufacturers’ drugs, but from its own as well—Merck introduced Mevacor in August of 1987 and Zocor in December of 1991. In the 3 years following Mevacor’s December 2001 patent expiration, the price of the pioneer molecule fell 74% from $1.90 per unit to 50 cents. Associated with this was a large increase in (generic) purchases of the lovastatin molecule This suggests that the introduction of generic lovastatin not only shifted purchases away from its branded form, but also expanded the lovastatin market to include new purchases as well. Despite the price reduction, however, there appeared to be little or no substitution away from Lipitor, Zocor, and other me-too competitors after generic lovastatin was introduced.

EXHIBIT 5.

Monthly quantity of statins

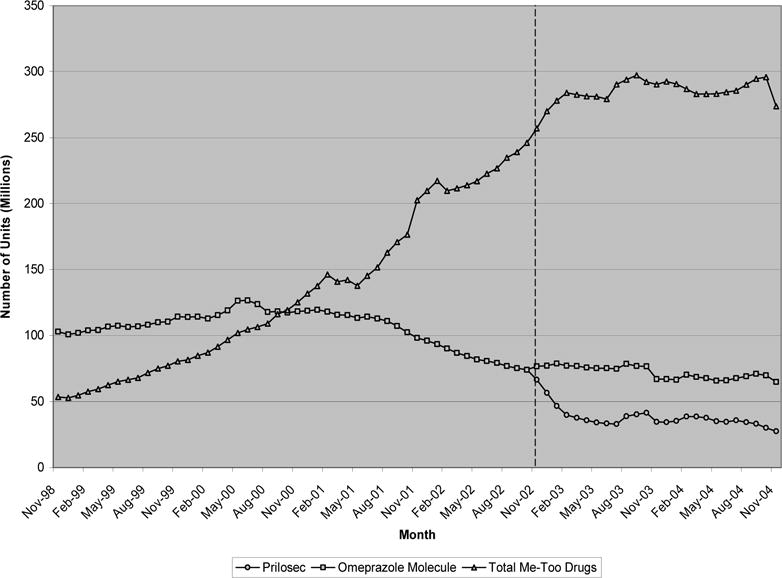

Exhibit 6 presents the trend in purchase quantity for our last class of therapeutics, proton pump inhibitors, used for preventing peptic ulcers and treating acid reflux disease. In 2005, US sales of PPIs generated nearly $12.5 billion in revenue (5% of total US pharmaceutical sales revenue). From November 1998 to October 2000, Prilosec (omeprazole) purchases outnumbered purchases of all other me-too drugs in this class. Continuing their upward trend, however, me-toos in this class reached nearly 250 million purchases monthly by the date Prilosec’s patent expired in December 2002. Much of this increase was fueled by increases in purchases of Prevacid and the introduction of Nexium in March 2001. Similar to Mevacor, Prilosec purchases declined slowly in the years prior to patent expiration leveling off at 75 million units purchased monthly prior to December 2002. After patent expiration, the average price of the omeprazole molecule declined by more than 50%, from $3.2 per unit just prior to $1.4 two years later. Similar to the other classes, total purchases of the omeprazole molecule remained nearly constant, with sales of generic versions of the drug almost completely offsetting the reduction in purchases of the branded version— note that our estimates of branded Prilosec quantity account for its over-the-counter form, Prilosec OTC, introduced nine months after patent expiration in September 2003. Again, as with the other classes considered, there was no apparent reduction in the trend of all other me-too purchases after Prilosec’s patent expired.

EXHIBIT 6.

Monthly quantity of proton pump inhibitors

3.2 Alternative Explanations

The above figures suggest a clear relationship between patent expiration of a pioneer molecule and the introduction of generic formulations that substitute for existing brand purchases, leaving the total quantity purchased relatively unchanged. These figures also suggest the lack of any clear substitution away from follow-on drugs in the wake of such generic entry. While this may imply that pioneer molecules were perceived to be poor substitutes for follow-on drugs, several alternative explanations are plausible.

Prices don’t matter

In most situations, neither patients nor their physicians have strong reasons to choose lower priced drugs because drug costs are covered by third parties. But payers, operating mainly through pharmacy benefit managers, are price-sensitive. This is reflected in the observed substitution towards generics after patents expire. This substitution may be due to mandates by plans (who presumably due to a lack of perceived substitution, do not mandate switching away from me-toos) or result from differences in co-pays between branded and generic drugs. In the latter case, instances in which co-pay differences are small (or absent as in one-tiered plans) relative to the actual price differential between me-toos and pioneer molecules and on par with the price differential between branded and generic pioneer molecules would lead us to underestimate the degree of substitutability between the two.

Pricing Response

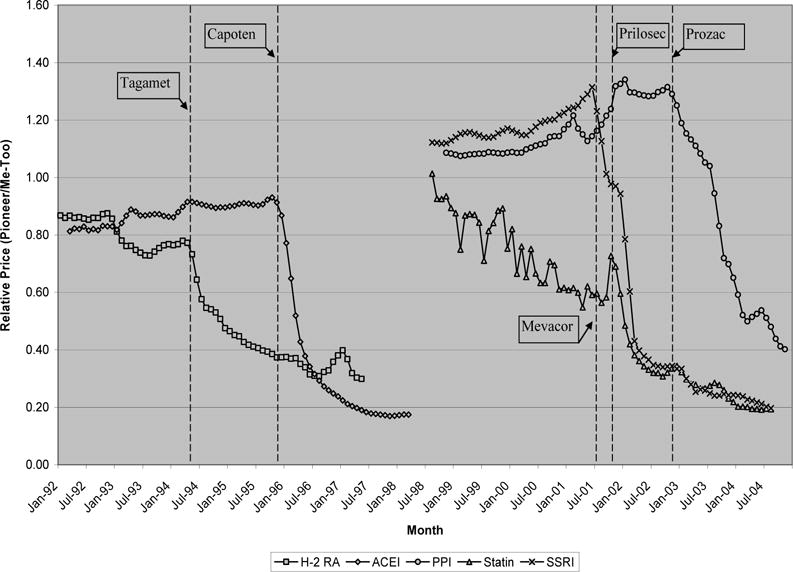

First, manufacturers of follow-on drugs may reduce their prices to remain competitive, thereby leaving quantity or the trend in quantity unchanged. Exhibit 7 explores this possibility by plotting the relative per-unit price of pioneer molecules over time (i.e., the price of a pioneer molecule divided by the average price of its follow-on competitors).

EXHIBIT 7.

Relative price changes of pioneer drugs post patent expiration

The dotted lines represent the date of patent expiration for a particular pioneer molecule. For example, in the 3 years prior to its patent expiration in December 1995, Capoten’s per-unit price increased from 55 cents to 64 cents. During the same period, the average per-unit price of all other follow-ons in this class increased from 68 cents to 70 cents. The relative price of Capoten therefore increased from 80 cents to 90 cents in this period. Three years after patent expiration, the average price of the captopril molecule fell to 13 cents per unit, while the average per-unit price of follow-on ACE inhibitors was slightly higher at 73 cents. The relative price of captopril therefore fell from 90 cents to 17 cents per unit after patent expiration.

Several points stand out in this figure. First, except for statins, the price of pioneer molecules relative to follow-on drugs was fairly stable in the years prior to patent expiration. For H2RAs, statins, and ACE inhibitors, it appears that follow-on drugs were significantly more expensive (indicated by a ratio > 1.0), while the opposite was true for PPIs and SSRIs.6 Importantly, this implies that for 3 of the 5 classes considered, follow-on drugs were perceived to offer clinical benefits worth at least the additional premium. This is not surprising considering the top sellers in these classes—Zantac, Pepcid, Lipitor, Zocor, Vasotec, and so on—many of which were therapeutically superior to the pioneers.7

Second, following patent expiration, the relative price of pioneer molecules fell sharply, usually by 60–80% over the course of 3 years. If price reductions for follow-on drugs were responsible for the unresponsive demands observed, then we would expect to see large declines in follow-on prices, leaving little change in the relative price of pioneer molecules after patent expiration. That relative prices fell so sharply, with little or no offsetting from follow-on price reductions, suggests that other factors are responsible for the unresponsive demand. In fact, though relative prices are displayed in Exhibit 7, we find that (absolute) follow-on drug prices did not decline noticeably in the wake of pioneer patent expirations either.

That said, one potential critique of our pricing data is that it does not include off-invoice rebates, which are common in pharmaceutical purchases. It is still possible that large rebates for follow-on drugs were offered around the time of pioneer patent expiry, causing follow-on demand to remain unchanged. However, if pioneer and follow-on drugs were perceived as perfect or close substitutes, patients and physicians would presumably always select the cheaper alternative. Hence, for relative prices to remain the same after accounting for rebates, the reduction in the price of pioneer molecules after patent expiration would have to be matched by equally large rebates for follow-on drugs. Given the tremendous magnitude of the reduction in price of pioneer molecules (56% to 80% decline), it is highly unlikely that such large rebates would have been offered. Rebates of that size are simply beyond the levels that sources suggest are likely (US Department of Health, 2004).

Marketing Response

An alternative non-price mechanism by which follow-on drugs may compete after pioneer patent expiration is marketing. For example, if price reductions in pioneers were met with substantial increases in marketing among follow-on drugs around the point of patent expiration, one might expect the subsequent level or trend in follow-on purchases to be unchanged. Without product level data on marketing, it is difficult to test this claim, though it is unlikely for at least two reasons. First, the consistency of our results across diverse therapeutic categories and time-spans, along with relative stability among follow-on brand shares, seems to weaken a marketing based claim. Second, if increases in follow-on marketing at the point of pioneer patent expiration were large enough to leave the trend in follow-on demand precisely unchanged, why then stop there? Since additional marketing efforts could presumably raise demand further, it seems coincidental that firms would advertise up to the point where demand remained unchanged and no further. More generally, if follow-on marketing were sufficiently powerful to compete with the large price reductions in pioneer molecules, it should also be powerful enough to generate substantial fluctuations in follow-on demand both before and after pioneer generic entry. We observe neither in our data.

A potentially important limitation of this reasoning is that for 3 of the 5 classes we considered, the firm manufacturing the pioneer molecule also owned and marketed several of the important follow-on drugs.8 In this setting, it is more plausible that manufacturers would ramp up advertising of the follow-on drug immediately after patent expiration of the pioneer. While this effect may exist, two points are worth noting. First, in each these 3 classes, a large share of the follow-on drugs were still not owned by the manufacturer of the pioneer molecule. Second, and most important, follow-on drugs still did not respond to pioneer patent expiration in the 2 other classes we considered.

Switching Costs

A final alternative explanation of the unresponsiveness of follow-on demand to pioneer price reductions is the cost of switching. Since health plans and pharmacy benefits managers (PBMs) are typically aggressive in making generics available, the main ‘cost’ of switching falls on patients who must request new prescriptions for newly available generic pioneers rather than continue consumption of the follow-on drug. For those follow-on patients who are at the end of a prescription and seeking new scripts, or for first time users, requesting the generic pioneer may require less time and effort than for someone in the middle of their prescription cycle. If this is true, those follow-on patients with higher costs of switching may be reluctant to switch, despite the substantial cost savings associated with the generic pioneer.9 More generally, if patients and physicians are reluctant to switch from a therapy that clearly works to one that is cheaper and potentially equally or more effective, a similar result may hold.

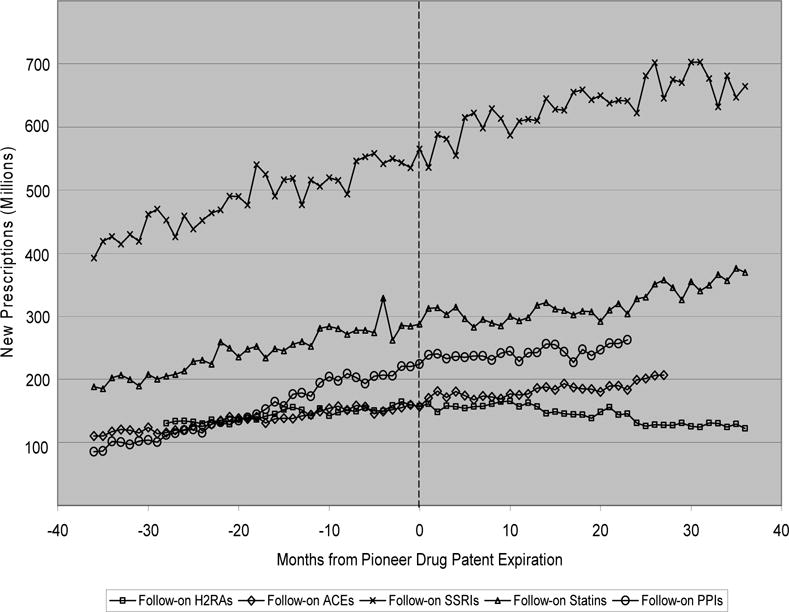

In order to assess the importance of switching costs in explaining our findings, we analyzed data on new prescriptions for the follow-on drugs in our sample. Since switching costs can implicitly be thought of as lowering substitutability among those already consuming follow-on drugs, an analysis of new prescriptions allows us to focus on those individuals for whom the costs of switching are by definition virtually zero. Exhibit 8, therefore, plots the number of new monthly prescriptions (as opposed to units purchased) in the 3 years before and after pioneer patent expiration, here depicted by the dotted line.

EXHIBIT 8.

New prescriptions for follow-on drugs

As can be seen in Exhibit 8, there does not appear to be a break in trend for any of the five classes considered, at least up to a year after patent expiration. At roughly 12 months post-expiration, the trend of new scripts for H2RAs appears to change somewhat. However, this change is not very pronounced and is not true of the other four classes for which a steady upwards trend continues. Also, the slight downward shift for H2RAs might very well be due to the new over-the-counter (OTC) availability of these drugs that occurred during this time. For example, over-the-counter Tagamet HB was introduced in August 1995, roughly 14 months after Tagamet’s patent expiration. This time frame is consistent with the mild change in trend seen in Exhibit 8. OTC purchases are not included in these data, and shifts to such purchases would be expected to put downward pressure on the trend in new prescriptions.

4. Discussion

Critics of me-too innovation in pharmaceutical markets often argue that follow-on or “me-too” drugs offer little incremental clinical value over existing pioneer products, while at the same time increasing health care costs through increased marketing and R&D. The basic merit of this argument relies on an assessment of whether patients, physicians, and health plans view follow-on and pioneer drugs as close substitutes or distinct clinical therapies. This is particularly important given extensive clinical trial evidence of therapeutic value from more powerful follow-on statins (Topol, 2004) plus anecdotal evidence of the benefits of other me-too drugs—differential efficacy and tolerability among SSRIs, variable safety and cardio-selectivity profiles among beta-blockers, etc.— and the fact that a large share of within-class purchases are towards me-too drugs in the first place, even when those drugs are priced above pioneers.

Our economic approach suggests that me-too innovation may, in fact, provide distinct benefits from the perspective of patients and physicians. First, for 3 of the 5 classes considered, follow-on drugs command a significant premium in prices, presumably reflecting a perception of clinical benefits worth at least the additional cost. Second, large reductions in the price of pioneer molecules, which would typically lead to decreased consumption of strong substitutes, appear to have no effect on the trend in demand for follow-on drugs. Given the observed substitution from pioneer brands towards generics after patents expire, this lack of response cannot be explained by the presence of insurance or physicians acting as agents on behalf of their patients, both of which presumably make individuals less responsive to changes in price. As shown, our results can also not be explained by reductions in the price of follow-on drugs to compete with generic entry of the pioneer molecule. Still further, our examination of the trends in new prescriptions suggests that our findings cannot be explained by switching costs.

Thus, we are left with the possibility that me-too drugs are perceived to be different than pioneer drugs, at least from the perspective of patients and physicians. Importantly, our analysis does not address whether me-too drugs are perceived to be close substitutes to one another. This would certainly be true if each subsequent me-too drug offered incrementally less benefit than the prior. In fact, anecdotal evidence from the market for statins suggests one instance in which substitutability may be closer than predicted by our results. For example, patent expiration of Zocor in June 2006 was met with significant substitution away from Pfizer’s product Lipitor towards generic Zocor—in the 18 months after Zocor’s patent expired, Lipitor’s share of the cholesterol market fell nearly 10 percent.10 Thus, while our analysis suggests the possibility that me-too drugs are perceived to be poor substitutes of pioneer products, within-me-too substitution may be less stark. Whether that perception is consistent with clinical differences in effectiveness, safety, side effects, dosing convenience, etc., is beyond the scope of our analysis. At any rate, it probably depends greatly on the therapeutic category being considered.

Footnotes

We thank Dana Goldman, Steven Teutsch, and Marc Berger for their helpful comments and suggestions, as well as Jamie Busza, Lisa Klein, and Steven Geisel for their assistance with respect to the IMS data. We also thank seminar participants at the Frontiers in Health Policy Research meeting and, in particular, David Cutler for suggesting the inclusion of Zocor’s patent expiration into our analysis. Jena acknowledges fellowship support from the National Institute of General Medical Sciences through Medical Scientist National Research Service Award 5 T32 GM07281 and from the Agency for Health Care Research and Quality through UCLA/RAND Training Grant T32 HS 000046.

Patent expiration is an “exogenous” force in the sense that the associated change in price is due to a change in supply conditions that are unrelated to factors affecting pioneer and follow-on demand.

Note that for several classes, variations of the pioneer product were introduced by the pioneer firm after patent expiration of the initial product. This includes Prozac Weekly following Prozac patent expiration, Tagamet HB following Tagamet expiration, and Prilosec OTC following Prilosec expiration. We include each of these formulations in our definition of the pioneer molecule.

Although all of the drugs we consider are solid forms, a natural limitation of our data is that we cannot account for the fact that drugs often vary in strengths; an ideal comparison across classes might therefore involve 30-day prescription equivalents instead.

Omitting rebates induces measurement error in price that may be correlated with patent expiration if the relative size of rebates differs between generics and branded drugs. We later demonstrate, however, that rebates are simply too small to disturb our basic results.

Note that Exhibit 5 contains two y-axes, one for the total quantity of follow-on drugs and one for the lovastatin molecule (i.e. Mevacor and generic lovastatin).

Lee (2004) argues that follow-on drugs provide price competition by entering at prices below their pioneer counterparts. This is only true for 2 of the 5 classes we consider, though our results are not at odds with Lee’s. For example, Lee finds that Capoten was more expensive than the early me-too Mavik (trandolapril), which is true in our sample as well. Expanding this analysis to the later and more heavily prescribed me-too ACE inhibitors reveals, however, that follow-on drugs in this class were generally more expensive.

For example, compared to Tagamet (cimetedine), Zantac (ranitidine) demonstrated improved tolerability, longer lasting action, and nearly ten times the activity, while Pepcid (ranitidine) demonstrated nearly 30 times the activity.

For example, in the H2RA class, Glaxo Smith Kline invented Tagamet but also owned the follow-on drugs Tritec and Zantac. In the statin class, Merck owned both Mevacor and the follow-on drug Zocor. Finally, among PPIs, Astrazeneca owned both Prilosec as well as the follow-on drug Nexium.

Cost-savings may be substantial. Drugs given first-tier status (such as generics) may save individuals anywhere from $145 to $354 in annual co-pays compared to second or third-tier branded drugs (Pharmacy Benefit Management Institute, LP. Prescription Drug Benefit Cost and Plan Design Survey Report. Available at no charge (through order) at: http://www.pbmi.com/.)

See, e.g., Stephanie Saul and Alex Berenson’s New York Times article published online November 3, 2007 entitled “Maker of Lipitor Digs in to Fight Generic Rival.” Available online at: http://www.nytimes.com/2007/11/03/business/03generic.html.

References

- Angell M. The Truth About the Drug Companies: How They Deceive Us and What to Do About It. New York: Random House; 2004. [Google Scholar]

- DiMasi JA. Price Trends for Prescription Pharmaceuticals: 1995–1999. Background report prepared for the U.S. Department of Health and Human Services’ Conference on Pharmaceutical Pricing Practices, Utilization and Costs; Washington, D.C.. August 8–9, 2000. [Google Scholar]

- Dimasi JA, Paquette C. The Economics of Follow-on Drug Research and Development: Trends in Entry Rates and the Timing of Development. Pharmacoeconomics. 2004;22(s2):1–14. doi: 10.2165/00019053-200422002-00002. [DOI] [PubMed] [Google Scholar]

- Goozner M. The $800 Million Pill: The Truth Behind the Cost of New Drugs. Berkeley, California: University of California Press; 2004. [Google Scholar]

- Holden C. Future Brightening for Depression Treatments. Science. 2003;302(5646):810–3. doi: 10.1126/science.302.5646.810. [DOI] [PubMed] [Google Scholar]

- IMS Health. IMS Health, Plymouth Meeting. PA: National Sales Perspectives™ 1992–2005. [Google Scholar]

- Kessler DA, Rose JL, Temple RJ, Schapiro R, Griffin JP. Therapeutic-Class Wars–Drug Promotion in a Competitive Marketplace. New England Journal of Medicine. 1994;331(20):1350–3. doi: 10.1056/NEJM199411173312007. [DOI] [PubMed] [Google Scholar]

- Langreth R. Drug Marketing Drives Many Clinical Trials. The Wall Street Journal. 1998 [Google Scholar]

- Lee TH. “Me-Too” Products–Friend or Foe? New England Journal of Medicine. 2004;350(3):211–2. doi: 10.1056/NEJMp038215. [DOI] [PubMed] [Google Scholar]

- Lichtenberg FR, Philipson TJ. The Dual Effects of Intellectual Property Regulations: Within- and between-Patent Competition in the U.S. Pharmaceuticals Industry. Journal of Law and Economics. 2002;45:643–672. [Google Scholar]

- Nissen SE, et al. Effect of Very High-Intensity Statin Therapy on Regression of Coronary Atherosclerosis: The Asteroid Trial. Journal of the American Medical Association. 2006;295(13):1556–65. doi: 10.1001/jama.295.13.jpc60002. [DOI] [PubMed] [Google Scholar]

- Pharmacy Benefit Management Institute, LP. Prescription Drug Benefit Cost and Plan Design Survey Report. Available at no charge (through order) at: http://www.pbmi.com/

- Shepherd J, et al. Prevention of Coronary Heart Disease with Pravastatin in Men with Hypercholesterolemia. West of Scotland Coronary Prevention Study Group. New England Journal of Medicine. 1995;333(20):1301–7. doi: 10.1056/NEJM199511163332001. [DOI] [PubMed] [Google Scholar]

- Topol EJ. Intensive Statin Therapy–a Sea Change in Cardiovascular Prevention. New England Journal of Medicine. 2004;350(15):1562–4. doi: 10.1056/NEJMe048061. [DOI] [PubMed] [Google Scholar]

- U.S. Department of Health, Education and Welfare. The Drugs Makers and the Drug Distributors. Task Force on Prescription Drugs, Background Papers. 1968 [Google Scholar]

- U.S. Department of Health and Human Services. Report on Prescription Drug Importation. 2004 http://www.hhs.gov/importtaskforce/Report1220.pdf.

- Wertheimer A, O’Connor TW, Jr, Levy R. The Value of Incremental Pharmaceutical Innovation for Older Americans. Philadelphia: Temple University Center for Pharmaceutical Health Services Research; 2001. [Google Scholar]