Abstract

We study choice over prescription insurance plans by the elderly using government administrative data to evaluate how these choices evolve over time. We find large “foregone savings” from not choosing the lowest cost plan that has grown over time. We develop a structural framework to decompose the changes in “foregone welfare” from inconsistent choices into choice set changes and choice function changes from a fixed choice set. We find that foregone welfare increases over time due primarily to changes in plan characteristics such as premiums and out-of-pocket costs; we estimate little learning at either the individual or cohort level.

The past five years has seen a sea change in the way that publicly provided health insurance benefits are delivered to the U.S. population. From the introduction of the Medicare and Medicaid programs in 1965, expansions in public health insurance entitlements came through the extension of these monopoly government-run insurance plans. But beginning with the introduction of the Medicare Part D Prescription drug program in 2006, and continuing through the exchanges that are at the center of the Affordable Care Act that was passed in 2010, the U.S. has been moving to a different model: insurance exchanges where the publicly insured choose from a host of subsidized private insurance options.

This privatization of the delivery of public insurance raises a host of interesting policy and research questions. Primary among these is the ability of individuals to make consistent choices across a potentially large array of choices with meaningful differences. In Abaluck and Gruber (2011), we explored this issue in the context of the Part D program. We considered in particular whether elders appeared to be properly weighing the premium and out of pocket spending implications of their plan choices. We concluded that they were not, with the typical elder able to save about 30 percent of total costs (premiums plus out of pocket costs) through a more appropriate choice of plan.

A subsequent paper by Ketcham et al. (2012), however, argues that these choice inconsistencies are largely initial errors made by those newly enrolling in Part D and that they are mostly corrected through plan switching from 2006 to 2007. This is an important contention. If in fact choice inconsistency was simply a feature of the initial year of the program, it suggests that this is not a major issue for the long run welfare evaluation of this new insurance model.

In this paper we revisit the question of evolving choice inconsistencies over time. We do so using newly available data on a 20% sample of Part D claims data recently made available by the Centers for Medicare and Medicaid Services (CMS). These data have information on the full set of prescription drug claims under Part D for every senior enrolled in the program, as well as information on the characteristics of the plans that they chose.

Using these improved data, we continue to find that seniors are making inconsistent plan choices in the first year of Part D (2006). We find a similar level of foregone savings and overweighting of premiums relative to expected out of pocket costs as in our previous work. However, in contrast to Ketcham et al., we find that choices do not improve over time in aggregate. Rather, the amount of “foregone savings” available to consumers choosing Part D plans grows over time, and is larger by 2009 than it was at the start of the Part D program in 2006.

This fact motivates us to develop a structural framework in which to study plan choices over time. This framework allows us to mathematically decompose the “foregone welfare” from inconsistent plan choices into components due to changes in the choice set and product characteristics, changes in the choice function from a fixed choice set, and changes in preferences over time.1 On the choice function side, we can use data on choices by movers and stayers, as well as by new cohorts over time, to separately identify the effects of inertia, learning from experience, and calendar year or “cohort” learning effects on the quality of choices. On the choice set side, we can use the structural parameters of our model to decompose the total choice set effect into factors such as the change in premiums, the change in out of pocket costs, and the set of plan choices available.

Overall, we find that the welfare cost of choice inconsistencies increases over time. These net changes reflect a number of moving pieces and different factors appear to be driving the changes in different years. But the key general conclusion of our analysis is that there is little improvement in the ability of consumers to choose plans over time; we identify and estimate little learning at either the individual or cohort level over the years of our analysis. Inertia does reduce welfare, but even in a world with no inertia we estimate that substantial welfare losses would remain. We conclude that the increased choice inconsistencies over time are driven by changes in plan characteristics that are not offset by substitution both because of inertia and because non-inertial consumers still make inconsistent choices.

Our welfare analyses are sensitive to the assumptions we make about brand preferences; should we regard these as reflecting omitted but desirable features of brands (meaning only within brand errors are possible) or should we regard preferences for particular brands as heuristics which have no actual value to consumers after conditioning on coverage characteristics and quality? In the extreme case in which we assume that only within brand errors are possible because all across brand choices are rationalized by non-parametric brand effects, foregone welfare is on average 60% lower. To help assess which normative model is most appropriate, we estimate several random coefficients models to better understand the structure of brand preferences. These models allow brand preferences to rationalize across brand choices but do not require that they do. We find little correlation in preferences for particular brands over time (after conditioning on inertia), but we do find evidence that some beneficiaries consistently prefer more popular brands. We also find that across brand choices are better explained by a large variance in the idiosyncratic error term “ε” than by substantial heterogeneity in brand random effects. These results could be interpreted as evidence against the hypothesis that brand choices are rationalized by persistent unobserved quality, although it does not conclusively settle the question of whether estimated brand effects should matter normatively.

Our paper proceeds as follows. In Part I, we review the Medicare Part D program and related previous literature. In Part II, we discuss at length the new CMS Part D data. Part III presents the basic facts on plan choice and plan switching. Part IV describes our empirical strategy for more rigorously modeling choice inconsistencies as well as the reasons for changes in welfare over time, and Part V presents the results of our analysis. Part VI concludes.

I: Background2

A. The Medicare Part D Program

Medicare, which provides universal health insurance coverage to those over age 65 and to those on the disability insurance program, did not include coverage of outpatient prescription drugs when it was established in 1965; this coverage was added through the Part D program that passed in 2003 and became active in 2006. The most noticeable innovation of the Part D plan is that this new Medicare benefit is not delivered by the government, but rather by private insurers under contract with the government. Beneficiaries can choose from stand-alone plans called Medicare Prescription Drug Plans (PDP) (a plan that just offers prescription drug benefits), Medicare Advantage (MA) plans that provide all Medicare benefits, or existing employer/union plans, so long as coverage is “creditable” or at least as generous (i.e. actuarially equivalent) as the standard Part D plan, for which they would receive a subsidy from the government.

Under Part D, recipients are entitled to basic coverage of prescription drugs by a plan with a structure actuarially equivalent to a standard plan. In 2006 the standard plan offered the following coverage: none of the first $250 in drug costs each year; 75 percent of costs for the next $2,250 of drug spending (up to $2,500 total); 0 percent of costs for the next $3,600 of drug spending (up to $5,100 total, the “donut hole”); and 95 percent of costs above $5,100 of drug spending (McClellan, 2006). Over 90 percent of beneficiaries in 2006, however, were not enrolled in the standard benefit design, but rather are in plans with low or no deductibles, flat payments for covered drugs following a tiered system, or some form of coverage in the donut hole (McClellan, 2006). The main requirement for plans is that they must have equal or greater actuarial value than the standard benefit.

Enrollment in Part D plans was voluntary for Medicare eligible citizens, although Medicare recipients not signing up by May 15, 2006 were subject to a financial penalty if they eventually joined the program (to mitigate adverse selection in the choice of joining the program). One group, however, was automatically enrolled: low income elders who had been receiving their prescription drug coverage through state Medicaid programs (the “dual eligibles”). These dual eligible were enrolled in Part D plans by default if they did not choose one on their own, and copayments were lowered. There were also special subsidies for lower income elders slightly above Medicaid eligibility.

Despite reluctance voiced before the legislation passed, there was enormous interest from insurers in participating in the Part D program. By November 2006, 3,032 plans were being offered to potential Part D enrollees. Every county in the nation had at least 27 plans available; the typical county had 48 plans, while some counties featured more than 70 choices, primarily due to high number of MA plans.3 As of June 2006, there were 10.4 million people enrolled in stand-alone PDP plans, 5.5 million people enrolled in MA plans and about 6 million dual eligibles.4 Yet 73 percent of people over 65 felt that the Medicare prescription drug benefit was too complicated, while 91 percent of pharmacists and 92 percent of doctors expressed this concern. When asked if they agree with the statement “Medicare should select a handful of plans that meet certain standards so seniors have an easier time choosing,” 60 percent of seniors answered “Yes.”5

Despite these reservations, there were no signs of diminished plan choice in subsequent years. The number of PDPs increased by about 30 percent in 2007, from 1,429 to 1,875 and remained at this level in 2008.6 By 2012, there were 1603 PDPs available.

The presentation of options for Part D depends very much on the context in which individuals choose plans. Medicare.gov lays out plan choices in a very clear way and includes a calculator on which our simulator is based. Unfortunately, data in Kling et al. (2012) suggests that only a very small share of enrollees, at least at the time of their survey, use this resource. There is no default plan for initial enrollment, but individuals are auto-reenrolled in their existing plan each year unless they make an affirmative change.

B. Issues of Elder Choice in Part D

Standard economic theory would suggest that Medicare beneficiaries are better off choosing from a wide variety of plans that meet their needs, rather than constraining them to a limited set of choices being made by the government. But, as reviewed in detail in Iyengar and Kamenica (2010), and summarized in AG, there are a large number of behavioral economics models which suggest that in fact agents may be better off with more restrictive choice sets. Other recent literature has shown that the nature of how choices are presented can have important impacts on choice. And work by Agarwal et al. (2007) shows that issues may be magnified for the elderly.

Our work builds on a small existing literature on elder choice in Part D. Most relevant for the current paper is our previous paper (AG) and the work of Ketcham et al. (KLMR, 2012).7 In AG, we use data from Wolters Kluwer (WK), the largest “switch” operator in the prescription drug market that collects the electronic claims from pharmacies and pass them on to the Pharmacy Benefit Managers (PBMs) and insurance companies that will pay the claims. We find in that paper that only about 12 percent of elders choose the cost minimizing plan (the plan which minimizes the sum of premiums plus expected out of pocket costs), and that the average elder could save about 30 percent by choosing the cost minimizing plan. We also estimate plan choice models that document key choice inconsistencies. We conclude with a partial equilibrium welfare analysis which implies that welfare would have been 27 percent higher if patients had all chosen rationally.

KLMR focus on plan switching decisions, highlighting the fact that a number of studies document the amelioration of choice biases through repeated market interactions. They turn to data from CVS Caremark, a Pharmacy Benefit Manager (PBM) for a number of PDPs (9 in 2006 and 18 in 2007). KLMR find large choice inconsistencies in 2006, with most individuals in their sample choosing plans that were significantly more expensive than the cost minimizing option. But they find that these inconsistencies are substantially reduced by plan switching in 2007, with the median amount of “Foregone Savings” relative to the cost minimizing choice falling by more than $200, and the number of individuals foregoing savings by less than $100 rises from zero to one-third of the sample.

Our work significantly improves on both of these studies along two dimensions. First, we use administrative data sampled from the full universe of Part D enrollees and claims. AG’s data captured by the WK system represent only 31 percent of all 3rd party prescription claims filled in the U.S, and there is a sizeable rate of attrition from the data (about one-third of the sample per year), which potentially arises from individuals using pharmacies outside of the WK network. KLMR are only able to follow individuals who stay within their small set of PDPs, and their limited set of plans do not include any plans with donut hole coverage (which AG highlight as a major source of choice inconsistency) so that they may as a result understate inconsistencies.

Our results confirm the findings of both AG and KLMR that there are sizeable choice inconsistencies in 2006. But unlike KLMR, we find that choice inconsistencies worsen over time, with a large growth in foregone savings from 2006 to 2009. We are unable to replicate KLMR’s results in our data so we cannot say for sure what drives this inconsistency. But we suspect that it arises from the limited nature of the plans in their subsample. In particular, they find that most of this reduction comes from switchers moving to more cost effective plans, but their estimated switching rate of 54% is much higher than is reported in virtually every other health insurance study.8,9 Further, while we do replicate the finding that foregone savings declined from 2006 to 2007, we find that in fact, this is explained by consumers choosing cheaper plans with lower quality ratings and our more comprehensive measure which includes these quality ratings suggests that choices did not improve from 2006 to 2007 and grew substantially worse thereafter. We also find that the large foregone savings in 2006 are driven largely by a single low-cost plan; if we compute foregone savings relative to the 2nd lowest cost plan, we see a monotonic increase over time.

The second major contribution of our approach is the use of a structural model which decomposes the reasons for changes in the nature of choice over time. This allows us to not only document these growing choice inconsistencies, but to explain their sources – and in particular to contrast the (limited) role of learning against the (significant) role of choice set changes.

II: Data

The main source of data for our analysis is a 20% sample of the newly released universe of claims for Medicare Part D enrollees; we study the subset of claims for beneficiaries enrolled in stand-alone prescription drug plans not receiving any low income subsidies. These claims are linked to encrypted plan IDs which are linked to a plan characteristics file containing information on premiums, deductibles, and donut hole coverage. Information on plan formularies is inferred from copayment costs.

A. Construction of Out of Pocket Cost Variables

The total enrollee costs of Part D can be decomposed into premiums, which are known for certain at the time of plan choice, and the distribution of out of pocket costs given the information available at the time when plans are chosen. Our focus is on estimating the distribution of costs given all of the information potentially available to individuals at the time when they make their choice. However, we only observe realized out of pocket costs for the plan in which an individual is enrolled. We therefore assume that the set of claims is fixed and would remain constant had the individual in question chosen a different plan.10

We consider two alternative models of out of pocket costs: the first is a “realized cost” model in which we construct out of pocket costs using the claims incurred by individuals during that year. This amounts to assuming that individuals chose their Part D plans with perfect foresight as to what their claims would be, which is clearly not fully accurate. The second model we consider is a “rational expectations” model in which we compute expected spending in that year based on either prior year claims or claims in the first month of enrollment. We use this model in our regression analysis because it allows us to quantify in a natural way the riskiness of alternative plans. In AG, we show that our main conclusions regarding choice inconsistencies are not sensitive to the choice of model, and are further robust to allowing consumers to have private information so that they know more than we would predict using the previous year’s claims but have less than perfect foresight.

Both models rely on the calculator we construct to determine what out of pocket costs would be for a fixed set of claims in each of the plans in a beneficiary’s choice set. We can check the accuracy of our calculator by comparing simulated out of pocket costs using the calculator to actual out of pocket costs in the plan in which beneficiaries were actually enrolled. We find a very high correlation of 0.992. The mean difference is $11.6 with a mean absolute deviation of $33 on a mean of $890 (using our baseline sample of full year enrollees). This is an order of magnitude smaller than the cost savings we find, so we do not believe these errors could be driving our results.

Another issue that must be addressed is that we observe only a single realization of out of pocket costs for each individual, so we do not observe the variance in spending across choices. We construct this variance in our rational expectation measure based on the distribution of realized costs among individuals who look ex ante identical. In AG, we defined 1000 cells based on deciles of total expenditure, days supply of branded drugs and days supply of generic drugs in the prior year and called individuals ex ante identical if they were in the same cell. Because we do not observe prior year spending in 2006, in our main specifications we define 10 cells based on expenditures in the first month of enrollment and construct the distribution of realized costs among individuals who enrolled in the same month and were in the same cell. We show in Appendix Table 1 that our results do not depend on whether we use the 10 cell or 1000 cell model in 2007 when both models are feasible.11

B. Sample Selection

We begin with a 20 percent sample of all Medicare Part D beneficiaries in 2006, 2007, 2008 and 2009. This includes 7,213,755 beneficiaries. We then drop all beneficiaries with employer coverage or who are eligible to receive low income subsidies; in the former case, we lack sufficient information to characterize their plans and in the latter case, there is little variation in cost-sharing given available subsidies. The omission of those with low income subsidies does not much limit the broader application of our results, say to ACA exchanges, since everyone in this market is receiving some subsidies; the low income population simply receives extra subsidies.

We additionally drop beneficiaries who change location during the year, who have claims from multiple plans or are enrolled in plans with brands with fewer than 100 enrollees in a state (this last has little impact on the sample but reduces the number of fixed effects in our model). In the primary sample considered in the text, we also restrict to individuals who were enrolled in a Part D plan for the full year. This restriction makes costs more comparable across years (since more consumers enrolled late in 2006) and leaves 1,762,059 beneficiaries. We show in Appendix Table 2 that the trends we observe in foregone savings over time are not sensitive to this restriction.

In our structural models, we consider two samples. The first, which we refer to as the “Full Sample”, includes a 20 percent sample of our data in all years, or a 4% sample of Part D enrollees because our data is itself a 20% sample (we impose this further restriction because it is computationally more convenient and more than adequate for statistical significance in all of our analysis). The second, which we refer to as the “Panel Sample”, restricts to a 20 percent sample of beneficiaries who are present in our data in 2006, 2007, 2008 and 2009, or a 4% sample of all such Part D beneficiaries. Our structural model is estimated using the full sample (new enrollees entering in each year help identify several parameters), but we report simulation results using the panel sample so that changes over time are not confounded by individuals entering and leaving the sample.

Appendix Tables 3 and 4 analyze the reasons why beneficiaries enter and exit the sample in each year for our “full sample”. The most common reasons for entering the sample are having enrolled after January in the previous year, having claims from multiple plans in the previous year, or being enrolled in a non-PDP plan the previous year (either an MA plan or a plan through one’s employer). The most common reasons for exiting are switching from a non-PDP plan, death or having claims from multiple plans, or - in 2009 – simply disappearing from the data entirely. Some identification in our analysis below comes from comparing new entrants with returning beneficiaries; new entrants are defined based on their first appearance in the beneficiary file, not based on their year of entry into our sample. For example, a beneficiary who turned 65 in 2007 would count as a new entrant; a beneficiary who entered our final sample in 2007 because they enrolled in a month after January in 2006 would count as a returning beneficiary.

III: Plan Choices and Switching: The Facts

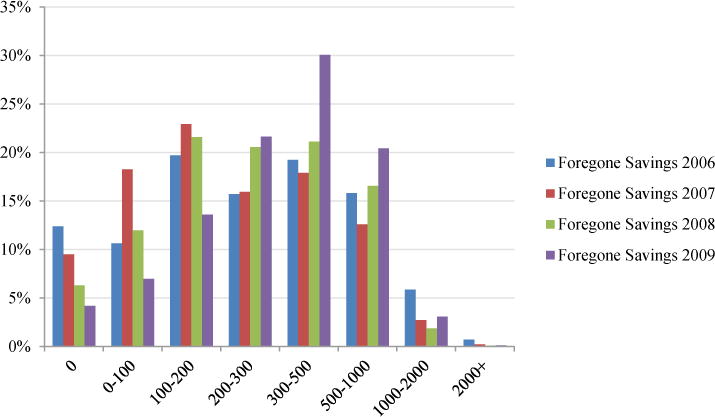

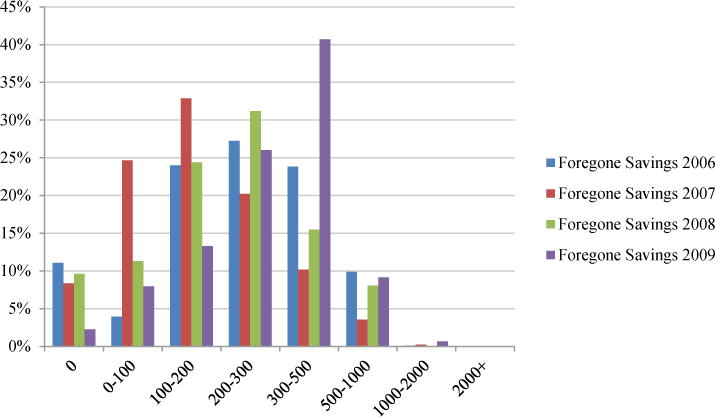

We begin our analysis by presenting the basic facts on plan choice in Figure 1. For each individual in the data, we estimate the total cost of enrolling in each PDP plan in their county, adding both premiums and expected out of pocket costs. We then estimate the difference in total costs between the plan chosen by that individual and the lowest cost plan in their county, which we call “foregone savings”. This corresponds to KLMR’s concept of “overspending”. Figure 1 conducts this exercise using the perfect foresight model of expectations, while Figure 2 reports the results with our rational expectations model.

FIGURE 1.

PERFECT FORESIGHT FOREGONE SAVINGS

FIGURE 2.

RATIONAL EXPECTATIONS PREDICTED FOREGONE SAVINGS

Notes: Figure 1 shows the distribution of foregone savings per year in the Full Sample using our perfect foresight measure while Figure 2 gives the distribution using our predicted costs measure. The x-axis gives dollars of foregone savings, the y-axis the fraction of the total population in that bin.

As Figure 1 shows, fewer than 15% percent of individuals choose the lowest realized cost plan in their choice set in 2006. On average, individuals could save 26–33 percent of their total Part D spending by choosing the lowest cost plan rather than the plan they chose. We find that half of beneficiaries could have saved more than $330 by enrolling in a different plan. These findings are very similar to those in AG, although they appear smaller than for KLMR for 2006, where mean foregone savings is $550. Figure 2 replicates Figure 1 using our “ex ante” predicted cost measure. Potential savings are smaller according to this measure (as one would expect, since this measure mechanically reduces the variation in out of pocket cost across plans) but nonetheless remain substantial with more than half having foregone savings of $230 or more.

The first major difference between our findings and those of KLMR is in the degree of inertia. In KLMR’s sample, 54% of returning beneficiaries switch plans in each year. We find that fewer than 10% of returning consumers switch plans in each year, and the rate of switching remains remarkably stable, between 9.61% and 9.69% in all years. This suggests that KLMR’s sample – focusing on a limited subset of plans – is not representative of the larger Part D population.

Unlike KLMR, the CMS data show that the share of individuals making cost minimizing choices does not improve over time. We further find that an ever-falling share of individuals choose the cost minimizing plan. On net, we find that 11 percent of individuals in 2006, 8 percent in 2007, 9 percent in 2008 and just 2 percent in 2009 chose the low-cost plan according to our predicted costs measure.

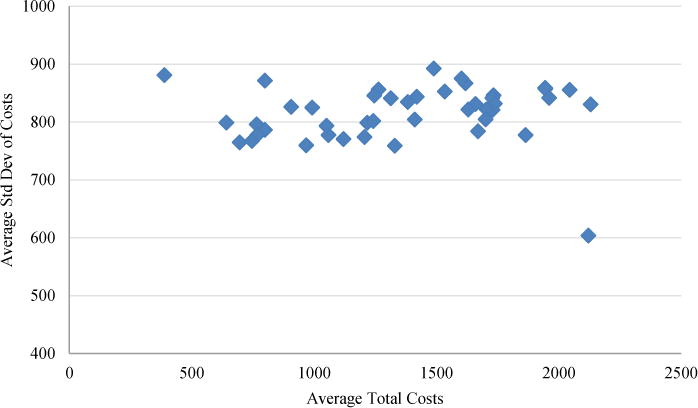

One reason consumers might not choose the cost minimizing plan is because they are willing to pay more for plans with better risk protection. To deal with this issue, we use an “efficient frontier” measure: we ask what cost savings are possible if consumers are restricted to choosing a plan with weakly better risk protection, as measured by a weakly lower variance of costs. If a plan lies on the efficient frontier, it implies that no alternative plan is both lower in expected costs and better in terms of the risk protection it provides. While plans are required to be actuarially equivalent to the standard plan, for any given individual, a plan might lie off the efficient frontier because it offers financial characteristics which are not valuable to that individual. For healthy individuals, a plan with poor coverage in the initial coverage range and high premiums due to donut hole coverage may be dominated in an efficient frontier sense by a plan with lower premiums, no donut hole coverage, but more generous coverage prior to the donut hole. This point is depicted graphically in Figure 3 where we show the average mean and standard deviation of costs for each plan in the CA choice set. Because we are averaging across all consumers, this does not literally show the efficient frontier for any given beneficiary. Nonetheless, one can see that the majority of plans lie off the frontier demarcated by the lower-left envelope of the scatter plot.

FIGURE 3.

CALIFORNIA CHOICE SET, 2006

Notes: CA Choice Set in 2006. Each point represents a single plan. Average total costs are the average of perfect foresight total costs (premiums plus realized out of pocket costs).

The results from this efficient frontier measure are summarized in Table 1. We report these results using our predicted cost measure because the variance of costs as a measure of risk only makes sense in that model (in the perfect foresight model, there is no uncertainty and thus no risk). Because we are restricting the set of plans to which one can move to save money, efficient frontier savings are smaller but most beneficiaries could still have saved several hundred dollars in all years without sacrificing risk protection.

TABLE 1.

REALIZED OVERSPENDING, PREDICTED OVERSPENDING, AND EFFICIENT FRONTIER OVERSPENDING

| 2006 | 2007 | 2008 | 2009 | |

|---|---|---|---|---|

| Foregone Savings PF ($) | 351 | 277 | 308 | 373 |

| Foregone Savings PF (%) | 26.6 | 24.9 | 29.3 | 32.9 |

| Foregone Savings Pred ($) | 262 | 176 | 231 | 313 |

| Foregone Savings Pred (%) | 18.8 | 14.7 | 19.4 | 24.7 |

| Efficient Frontier Pred ($) | 213 | 130 | 174 | 250 |

| Efficient Frontier Pred (%) | 15.1 | 10.3 | 14.6 | 20.6 |

| Foregone Savings – 2nd Best Plan ($) | 173 | 198 | 245 | 314 |

| Foregone Savings Pred – 2nd Best Plan ($) | 128 | 147 | 184 | 269 |

| # of Beneficiaries | 538,807 | 1,344,636 | 1,316,396 | 1,179,665 |

Notes: Table shows various measures of choice quality from 2006 through 2009, both in absolute terms and as a percentage of total costs (computed as the sum of premiums paid and out of pocket costs) in the “Full Sample” described in the text (as opposed to the full panel). “Foregone Savings PF” gives our “perfect foresight” measure: realized total costs relative to the plan which minimizes realized total costs (ex post). “Foregone Savings Pred” compares predicted costs in the chosen plan to predicted costs in the cost minimizing plan, where predicted costs are computed as average costs among all individual in the same decile of costs in January of that year. “Efficient Frontier Pred” gives the same measure, but compares the chosen plan only with plans which have weakly lower variance (computed as the variance in simulated out of pocket costs for that plan among 200 beneficiaries in the same decile of January expenditure). Percentages are percentages of total costs in the chosen plan. Savings from the bottom quartile are average savings from choosing a plan in the bottom quartile of total costs. The number of beneficiaries is lower in 2006 because we restrict to beneficiaries enrolled for the entire year and this restriction excludes a larger share of the sample in 2006 when open enrollment stretched from January to June.

Table 1 also reports foregone savings and the efficient frontier measure as a percentage of total costs. The change in this measure overtime is confounded by the fact that better choices reduce both the numerator (foregone savings) and denominator (realized costs). Nonetheless, the magnitude gives a sense of the stakes involved, between 10 percent and 21 percent of total costs for the efficient frontier measure and between 25 and 33 percent for the perfect foresight measure. It is therefore clear that choices did not materially improve over the first three years of the Part D program, and clearly worsened substantially in 2008 and 2009.

We also investigate whether the apparent foregone savings arise because individuals are failing to find a single best plan by comparing choices to the cost of the second least cost plan. We find that in 2006, the foregone savings from the single best plan are almost twice as large as the foregone savings from the 2nd best plan. In subsequent years, savings from the 2nd best plan are 70–85% as large as the best plan. These results suggest that there are substantial returns to choosing the best available plan, but also that the results are not driven by a particular low cost plan.12 Measured relative to the 2nd best plan, foregone savings is monotonically increasing over time and nearly doubling from 2006 to 2009. The drop in foregone savings relative to the best plan is due to a single very low cost plan which was available in 2006 but exited the market in 2007.

These reduced form facts are compelling – but limited. In particular, we have no way of accounting for strong brand preferences. What appear to be choices off the “efficient frontier” could just be preferences for other aspects of brands that are incorporated into premiums or out of pocket costs. This motivates our move toward structural estimation in the next section.

IV: Modeling Plan Choice and Switching

A. Restrictions on Preferences

To move from foregone savings to a more comprehensive welfare metric, we consider a structural model of plan choice. We begin by specifying a CARA utility model with a normally distributed cost distribution:

| (1) |

We show in our earlier paper that this specification leads to a conditional logit model of plan choice where the utility of individual i from choosing plan j in year t is given by:

| (2) |

In this equation, πjt gives the annual premium of plan j, gives expected out of pocket costs, gives the variance of costs, xjt represents any financial plan characteristics which impact choice, ξb(j)t represents brand fixed effects, is a dummy variable which is 1 if and only if plan j was chosen by consumer i during the previous year, and εijt are i.i.d. type I extreme value random variables. We allow the inertia dummy to depend on plan characteristics xi in two ways: first, the dummy is interacted with the change in characteristics of the previously chosen plan and second, the dummy is interacted with the change in characteristics of the minimum cost plan.

The financial plan characteristics include the deductible of the plan; a dummy for whether the plan covers all donut hole expenditures; a dummy for whether the plan covers generic expenditures in the donut hole only; and a cost-sharing index. The cost sharing index is calculated for each plan as the average percentage of expenditures covered by the plan between the deductible and the donut hole. This variable differs from expected out of pocket costs in that it has the same value for everyone in the sample for each plan, and because it is not directly impacted by whether plans have deductibles or donut hole coverage. To control for other aspects of plan quality, we include a full set of brand dummies. This will capture the many features of plans that are common within brand, such as consumer support and pharmacy access.

Identification is a natural concern in this context. All of the plan characteristics included in our model may be endogenous due to unobserved demand factors, and they may be biased by correlation with unobserved plan characteristics. To address this concern, we observe and include in our model much of the publicly available information that might be used by individuals to make their choices – premiums, deductible information, donut hole coverage dummies, as well as variables capturing formulary completeness and cost sharing. We also control for a full set of brand dummies, so that we are only comparing choices of plans with different cost-sharing structure within a given insurer.

Including brand dummies also raises a normative question regarding whether these reflect additional value that consumers receive from plans. One way of interpreting these coefficients is to assume that the brand dummies represent heuristic shortcuts taken by boundedly rational individuals who cannot properly evaluate financial comparisons across plans. In this case, given that we (the econometrician) can directly evaluate the financial consequences, brand dummies should not count in the normative welfare function. Alternatively, one might interpret the brand dummies as capturing some omitted feature of brands which consumers do value, such as familiarity with the logistics of plans from an earlier experience with a given brand. In this case, brand dummies should count normatively in our appraisal of plans. We consider both possibilities in our analysis below. In our baseline model, we do not count brand dummies in the normative welfare function but we do include a quality rating (which summarizes features such as customer service) whose normative weight is recovered by an OLS regression of the brand dummies on the quality variable (that is, we assume that ξb(j)t = qb(j)tδ + vjt where only the qb(j)tδ term counts in the normative welfare function). In an alternative model, we do count brand dummies as part of normative welfare.

A similar normative question arises regarding the inclusion of the inertia term in our normative welfare function. Our measured inertia term may reflect several different underlying phenomena. Actively choosing a plan may be costly, leading individuals to prefer (all else equal) to just remain in the same plan. Alternatively, our inertia term could represent an adjustment cost that is incurred by consumers if they switch plans in order to learn how the new plan functions. In the adjustment cost story, everything else held equal, consumers may be made worse off if they are forced to enroll in a new plan. In the setting of prescription drug insurance we believe that adjustment costs are small (unlike the setting of health insurance where they might include needing to switch doctors) and so we omit the inertia term from welfare. Once again we consider an alternative treatment of the inertia term in the welfare analysis below.

The model laid out above suggests three natural restrictions on preferences which extend the efficient frontier concept to the discrete choice setting.

Restriction 1: β0 = β1

This restriction states that the coefficient on premiums should equal the coefficient on expected out of pocket costs. Controlling for the risk characteristics of plans, individuals should be willing to pay exactly one dollar in additional premiums for coverage which reduces expected out of pocket costs by one dollar. If this restriction fails to hold, individuals may choose off the efficient frontier: they could switch to alternative plans with comparable risk characteristics but lower total costs.13

Restriction 2: γ = 0

This restriction states that financial plan characteristics other than premiums, expected out of pocket costs and the variance of out of pocket costs do not impact choices. Individuals should not care about deductibles, donut hole coverage or copays per se; they should only care about these factors to the extent that they impact the distribution of out of pocket costs. Once we control for this distribution, these factors should be redundant.

Restriction 3: β2 < 0

This restriction states that individuals should be risk averse.

In this paper, we remain agnostic about the reasons we might observe violations of these restrictions. Consumers might underweight out of pocket costs relative to premiums because they construct a mistaken forecast of what their claims will be in the coming year, because they fail to adequately price these claims given each plan’s formularies and cost-sharing features, or because they simply do not consider anything beyond the nominal characteristics of alternative plans (such as whether a plan has donut hole coverage). In any of these cases, it may be that consumers are simply erring (for example, not understanding what a deductible is) or it may be that they are behaving rationally given high search costs. All of these cases imply that consumers could be made better off were they enrolled in different plans, and this is the normative judgment we seek to make. There is a legitimate concern that some of these stories might imply structural specifications different from the one we estimate. In Abaluck and Gruber (2009) we consider a model in which out of pocket costs receive less weight than premiums because there is a component of out of pocket costs which is observable to the econometrician but not observable to consumers. This leads to a model quite close to the one we estimate here, but with some additional random coefficients; in that paper, we find that omitting those random coefficients has little impact on our results.

Appendix D of AG shows how to evaluate welfare in conditional logit models when positive and normative utility functions fail to coincide. Unlike the money metric of foregone savings, the welfare metric we compute takes into account risk aversion and plan quality. That is, for each plan, we compute:

| (3) |

This is the welfare measure taking into account total costs, risk protection, and plan quality variables and scaling by the marginal utility of income so that it is expressed in a money-metric. This metric omits from welfare other plan financial characteristics, non-financial brand characteristics, the inertia dummy and the error term. This is the appropriate metric if one believes that the financial characteristics of plans and the plan quality rating capture everything of importance about plans and that – if they matter at all – other factors matter only heuristically because consumers are unable to calculate, or unwilling to spend the time to calculate, the welfare metric above. As noted above, omitting the inertia term from our welfare evaluation is consistent with a story in which the true adjustment costs of switching plans are small. We also consider below models in which brand characteristics matter for welfare.

Let , welfare for the best plan. We define foregone welfare for individual i at time t in plan j as:

| (4) |

This is the welfare analogue of our foregone savings measure.

B. Modeling the Dynamics of Foregone Welfare

Conceptually, changes in foregone welfare can be driven by changes in how consumers choose from a fixed choice set, choice set factors such as changing plan characteristics, changes in the underlying claims (which determine the welfare consequences of choosing a given plan) or changes in the normative parameters (i.e. how consumers value risk protection and plan quality ratings).

We can further decompose the choice function factors into three effects, which we label inertia, individual learning, and cohort learning. Inertia is the tendency of consumers to remain in the same plan regardless of changes in the plan choice environment. Learning is the tendency for consumer choices to change as they gain experience in the market, individually or collectively. Individual learning concerns whether individuals with experience in the market choose differently conditional on choosing a new plan than individuals with less experience, while cohort learning reflects “calendar year” effects – given a fixed choice set, do we see differences in the choice function of each cohort of individuals over time? (controlling for their individual experience in the market – so we are comparing across years beneficiaries with a given amount of experience).We allow nearly all the structural parameters in our model to vary both by year (cohort learning) and with experience (individual learning) – thus, our model is capable of capturing a large range of ways in which choice functions might change as consumers learn. We seek to understand specifically whether these changes lead consumers to make better choices, so we summarize the impact of each type of learning by evaluating how the estimated changes in structural parameters with experience impact foregone welfare given a fixed choice set.

It is important to note that given our definition, individuals could save money by switching plans in every year but this is not necessarily evidence of learning; that is, learning is not just the complement of inertia. If, for example, all consumers switched whenever foregone welfare exceeded $400 and chose plans with foregone welfare of $300 conditional on switching, this would suggest that they saved money by switching and it would suggest that inertia is making consumers worse off (assuming that inertial consumers would choose as well as switchers were they to switch). It would not suggest that consumers who switched plans were learning – because in every year their behavior is the same – they switch plans and choose plans averaging $300 in foregone welfare if their current plan becomes sufficiently unsuitable. It would be evidence of learning if either a) Consumers with more experience in the market systematically chose better plans so switchers did better than new enrollees (individual learning), or b) Controlling for choice set differences, consumers in 2007 chose systematically better than consumers in 2006 (cohort learning).

Even if there is no change in consumers’ ability to choose over time from a given choice set, plan characteristics may change and choice sets might become more “dangerous”; for example, suppliers may learn to better conceal costs and otherwise take advantage of consumers’ biases. We can decompose choice set changes into changes in which plans are available in different years (which we separate into the impact of plans exiting and entering), changes in plan premiums and changes in plan characteristics which impact out of pocket costs.

Formally, we can define each of these effects in terms of changes in the parameters of our structural model (equation 1). Above, we allowed the structural coefficients β, γ, δ and ξ to vary flexibly from year-to-year for each individual. We will now place additional structure on this variation. Let and where Eit denotes individual i’s years of experience in the market in calendar year t. Cohort learning can then be identified with changes in the α1 coefficients or brand fixed effects, individual learning with changes in the α2 coefficients, and inertia with the inertial dummy ξ. Choice set changes can be straightforwardly equated with changes in , and xjt and qb(j)t over time.14 Out of pocket costs in a given year are a function both of an individual’s claims and of the characteristics of the plan in which they are enrolled. To separately identify the impact of changes in plan characteristics holding fixed an individual’s claims data, we use our calculator to simulate how out of pocket costs would have changed if the characteristics of plans changed from year t to year t+1 but the underlying claims remained fixed at their year t level. The changes in welfare we attribute to the choice set all hold fixed these underlying claims.

We will consider decomposing the change in welfare over time for the panel sample so that all individuals are present in all years; this is not substantively important but it simplifies the exposition. Individuals not in this sample – such as beneficiaries who appear for the first time in 2007 – will nonetheless be of use in identifying the structural parameters as we describe below.

Formally, denote foregone welfare for individual i, evaluated from the standpoint of the normative preference parameters estimated in year n using that individual’s claims in year m. The subscript gives the year from which choice set characteristics are taken, including the plans in the choice set and the premium and cost-sharing features of those plans. The superscript gives the year in which choice function factors are evaluated (i.e. which structural parameters of the choice function are used); these include cohort effects, experience terms and the inertial tendency.15 The change in foregone welfare from year t to year t+1 is given by:

| (5) |

We can decompose this into choice set (CS), choice function (CF), underlying changes in claims and normative terms.

| (6) |

We further decompose the choice function factors into the welfare impacts of cohort learning, inertia and individual learning. We decompose choice set welfare effects into the change in welfare induced by changes in premiums, changes in out of pocket costs and plan characteristics for a fixed set of claims, and changes in the choice set itself. The “claims” change in welfare describes how welfare changes due to changes in the underlying claims observed. This term is not completely independent of choice set effects – it may for example be driven by utilization responses to changes in plan characteristics. Nonetheless, we find it useful to separate out the changes in welfare due to changes in plan characteristics which impact premiums and out of pocket costs for a fixed set of claims and changes in the observed claims. The normative change in welfare - Nit – asks how welfare changes due to the fact that preferences may change overtime (e.g. individuals may become more risk averse or the revealed preference value placed on plan quality may change).

In order to estimate each of the above effects, we need to identify the associated coefficients in the structural model. We now discuss the intuition for the identification of each of these effects.

Consider first “individual learning” effects, α2. Individual learning is identified by comparing the choices of returning consumers conditional on choosing a new plan with the choices of new consumers in a given year. A confounding factor is that returning consumers who choose a new plan may be a selected sample of the broader pool of returning consumers – in other words, those consumers who choose to switch might do so in part because they are better at choosing plans. To control for this, we also attempt to identify individual learning by comparing the choices of new beneficiaries and “forced switchers”, consumers whose choice in the prior year is no longer available meaning they had no choice but to choose a new plan. This solution is not perfect, however, as “forced switchers” are not randomly chosen: consumers who choose plans in year t-1 which are no longer available in year t tend to perform worse than average in year t−1. The comparison between new beneficiaries and active switchers should provide an upper bound on the change in foregone welfare from learning (because active switchers are better than average choosers) and the comparison between new beneficiaries and forced switchers should provide a lower bound on this learning effect (because forced switchers are worse than average choosers).

Consider next inertia, the ξij=Cij(t−1) dummies. These are identified by asking how much more likely beneficiaries are to choose the plan they were enrolled in last year than we would expect given the characteristics of that plan. The welfare impact of inertia is identified by comparing the choices of switchers and non-switchers; it depends on whether non-switchers would have been better off had they actively chosen a plan. This is not necessarily the case even if they are not already enrolled in the best plan: the choice set might become “more dangerous” and active choices might lead them to choose even more poorly than if they just remained in the same plan. We can assess whether they would be made better off by switching by assuming that had they switched, they would have chosen as well as switchers (either active or forced).

Consider finally the “cohort learning” effects, α1. Cohort learning is the impact of market experience on choice functions controlling for any direct individual experience with the market. Some channels for this type of learning might be a greater abundance of tools which help consumers choose better or increasing knowledge on the part of healthcare providers such as pharmacists and doctors who consumers turn to for advice. These effects can be identified by comparing beneficiaries in different years with the same amount of experience: for example, new beneficiaries in 2006 and 2007 or beneficiaries with a single year of experience in 2007 and 2008. In the estimates we report here, the model uses both sources of variation to identify cohort learning.16

Identification of the choice set factors is straightforward. Given the estimated structural parameters, we can use the model to simulate how choices (and ultimately welfare) differ when premiums, out of pocket costs or the available plans change.17 Intuitively, one can think of the choice set estimates as analogous to the usual “area under the demand curve” welfare measures. If premiums of Plan A increase by $100, welfare does not fall by $100 because consumers can substitute towards alternative plans: the amount by which welfare falls depends on the degree of substitution via the price elasticity.

V: Structural Results

We begin by reporting the estimated coefficients in the structural model. Table 2 reports our baseline specification as described above. The first column shows our results for 2006, the year studied in AG. The coefficients are the structural coefficients in a conditional logit model and not marginal effects. They can be roughly interpreted as the impact of a one unit increase in the variable of interest on the probability that a plan is chosen; a premium coefficient of −0.68 implies that a $100 increase in premiums decreases the probability that a plan is chosen by 68 percent (this interpretation holds exactly for plans which are a negligible share of the overall market).

TABLE 2.

CONDITIONAL LOGIT MODEL COEFFICIENTS WITH BRAND FIXED EFFECTS

| Brand Dummies | 2006 | 2007 | 2008 | 2009 |

|---|---|---|---|---|

| Premium (hundreds) |

−0.68*** (0.03) |

−0.69*** (0.06) |

−0.96*** (0.07) |

−0.80*** (0.06) |

| OOP (hundreds) |

−0.20*** (0.03) |

−0.38*** (0.04) |

−0.35*** (0.04) |

−0.58*** (0.09) |

| Variance (times 106) | 0.41 (0.52) |

0.44 (0.29) |

−0.34 (0.52) |

−2.70*** (0.74) |

| Inertia | X | 3.90*** (0.43) |

6.48*** (0.07) |

7.07*** (0.11) |

| Deductible (hundreds) |

−0.96*** (0.09) |

−0.25*** (0.04) |

−0.81*** (0.03) |

−0.40*** (0.05) |

| Full Donut Hole Coverage | 2.39 (0.17) |

5.11*** (0.41) |

X | X |

| Generic Coverage | 0.69*** (0.04) |

0.71*** (0.07) |

1.28*** (0.08) |

1.60*** (0.10) |

| Cost Sharing | −7.88*** (0.88) |

0.79** (0.35) |

−0.63 (0.33) |

−1.41*** (0.42) |

| Number of top 100 on form | 0.08*** (0.01) |

0.33*** (0.02) |

0.44*** (0.02) |

−0.03*** (0.01) |

| Quality Rating | 0.63*** (0.02) |

0.27*** (0.01) |

0.76*** (0.02) |

0.60*** (0.03) |

Notes: Table shows conditional logit results from estimating equation (2) by maximum likelihood. Standard errors are in parentheses. In addition to the coefficients reported here, all specifications include brand fixed effects, separate coefficients for active and forced switchers (only those for active switchers are reported), interactions between all the reported coefficients and experience variables, and interactions between the inertia coefficient and (demeaned) values of the plan characteristics for the minimum cost plan, deciles of expenditure in the previous year, and characteristics of the chosen plan in the previous year. In later years, separate inertia dummies are included for the plan one was enrolled in during each preceding year. The average quality variable is a normalized version of the “average rating” index provided by CMS, recovered by auxiliary regression of estimated brand fixed effects on the quality rating variable.

Significant at the 1 percent level.

Significant at the 5 percent level.

Significant at the 10 percent level.

We find that even with this improved data, the choice inconsistencies described above and documented in AG persist. First, there is a sizeable gap between the estimated premium and out of pocket cost coefficients, with the former often 2–3 times as large as the latter. That is, consumers are substantially overweighting premiums relative to out of pocket cost exposure in choosing their insurance plans.

We also find that there are significant coefficients on several plan characteristics: the deductible, donut hole coverage variables and formulary variables all matter even after controlling for out of pocket cost variables. The magnitude of these coefficients is substantial: we observe that, controlling for out of pocket cost consequences, individuals are willing to pay $350 to obtain donut hole coverage in 2006 and substantially more in 2007 (the ratio of the donut hole coefficient to the premium coefficient).

The coefficient on the variance is insignificant in most specifications, and even where significant it is close to zero in magnitude: foregone welfare changes by less than $6 relative to a world where the variance coefficient is identically zero. As we saw in our efficient frontier analysis, we cannot rationalize consumers’ foregone savings as arising because consumers prefer plans with superior risk protection.

While these restrictions follow naturally from utility maximization with full information and standard preferences, the model from which they are derived makes several important functional form assumptions. Even in models which considerably loosened these assumptions, however, we would still not expect to see these rejections of consistency. Appendix Table 5 carries out simulations where we assume that consumers maximize expected utility given CARA or CRRA utility, the empirically estimated distribution of costs, and different levels of risk aversion. We then take the simulated choices and estimate our conditional logit model as if the simulated choices were the true choices observed in the data. In these simulations, we sometimes see significant coefficients on plan characteristics, but they are several orders of magnitude smaller. This suggests that the significant coefficients we find in the data are not due to the linearization or normality assumptions we make in our theoretical model, but rather due to the fact that consumers attach special weight to these characteristics beyond their personalized out of pocket cost consequences.

Importantly, our findings do not imply that consumers err primarily by choosing plans with low premiums but poor coverage. When we omit plan characteristics entirely from our model (Table 3), we find that the resulting coefficients on out of pocket costs are substantially larger than the coefficients on premiums. This suggests that if anything, beneficiaries may be choosing plans whose coverage is too generous (in other words, they are paying higher premiums to choose plans which provide more generous coverage on average, but not for their particular mix of drugs). Taken together, the results with and without plan characteristics imply that enrollees are making two sets of “mistakes”: overweighting plan characteristics that do not apply to them, while underweighting relative to premiums more subtle coverage characteristics that do reduce the cost of the particular drugs they consume.

TABLE 3.

CONDITIONAL LOGIT MODEL COEFFICIENTS WITH BRAND FIXED EFFECTS, OTHER PLAN CHARACTERISTICS OMITTED

| Brand Dummies | 2006 | 2007 | 2008 | 2009 |

|---|---|---|---|---|

| Premium (hundreds) |

−0.21*** (0.04) |

−0.39*** (0.05) |

−0.58*** (0.04) |

−0.52*** (0.07) |

| OOP (hundreds) |

−0.31*** (0.06) |

−0.50*** (0.06) |

−0.93*** (0.09) |

−0.93*** (0.09) |

| Variance (times 106) |

1.12*** (0.30) |

−1.03* (0.55) |

1.72 (1.30) |

−2.91*** (0.69) |

| Inertia | X | 3.64*** (0.10) |

5.63*** (0.04) |

6.66*** (0.14) |

| Quality | 0.59*** (0.02) |

0.25*** (0.01) |

0.55*** (0.03) |

0.61*** (0.03) |

Notes: Table shows conditional logit results from estimating equation (2) by maximum likelihood; the specification is identical to Table 2, but all financial plan characteristics are omitted.

Significant at the 1 percent level.

Significant at the 5 percent level.

Significant at the 10 percent level.

Of course, this means that our finding of choice inconsistency in this respect is generated by the joint finding of a premium-OOP gap in tandem with the fact that plan characteristics enter the model conditional on OOP costs. This raises the question of whether our model with plan characteristics included is really separately identified from the simpler model that excludes these (theoretically irrelevant) broader plan characteristics. Indeed, we do find that the two models make very different predictions. In Appendix B, we show that 12% of choices are predicted to change if we drop plan characteristics from our model and the average change in the probability that a plan is chosen is 20%.

The remaining columns of Table 2 show that the stylized facts from the 2006 results persist in 2007, 2008 and 2009. We observe that the premium and out of pocket cost coefficients move closer together. The specifications include a flexible set of interactions between the inertia dummy and plan characteristics both in the present year and in the previous year. These interactions allow the decision of whether to switch to depend flexibly both on the current year choice set and specifically on changes to the plan in which the consumer was previously enrolled. With these interactions included, the reported coefficients are identified only by the choices of switchers conditional on switching. The fact that the premium-OOP coefficient gap narrows in later years relative to 2006 reflects the fact that these coefficients are identified only by the 10 percent of individuals who switched plans.

Despite the fact that we are focusing on switchers, however, the premium and out of pocket cost coefficients remain significantly different. Moreover, the other choice inconsistencies persist: other plan characteristics are highly significant and the variance term is insignificant or small in magnitude. The inertia term is extremely large in magnitude, reflecting the fact that the vast majority of consumers remain in the same plan they chose in the previous year. The inertia term can be interpreted to mean that consumers are 500–700% more likely to choose a plan if it is the plan they chose last year; comparing the inertia term to the premium coefficient, we find that consumers are willing to give up more than $600 worth of premiums to remain in the same plan.

Table 4 considers the results when we condition on forced switchers. In this case we obtain slightly higher coefficients on out of pocket costs but the sizeable gap between the premium and out of pocket cost coefficients remains, as does the significance of the coefficients on other plan characteristics (note that forced switchers only exist from 2007 onward because they are defined as Part D enrollees whose choice in the previous year was discontinued). The similarities between the choices of switchers and forced switchers suggest that it is not unreasonable to use the observed choices of switchers to model how inertial consumers would choose were they forced to switch.

TABLE 4.

CONDITIONAL LOGIT MODEL COEFFICIENTS WITH BRAND FIXED EFFECTS AND FORCED SWITCHERS

| Brand Dummies and Forced Switchers | 2007 | 2008 | 2009 |

|---|---|---|---|

| Premium (hundreds) |

−0.70*** (0.07) |

−0.90*** (0.04) |

−0.87*** (0.06) |

| OOP (hundreds) |

−0.41*** (0.08) |

−0.62*** (0.06) |

−0.60*** (0.05) |

| Variance (times 106) |

1.05** (0.52) |

−0.56 (0.62) |

−0.87** (0.41) |

| Inertia | X | X | X |

| Deductible (hundreds) |

−0.06 (0.10) |

−0.67*** (0.04) |

−0.30*** (0.03) |

| Full Donut Hole Coverage | 5.01*** (0.59) |

X | X |

| Generic Coverage | 1.82*** (0.08) |

1.78** (0.19) |

1.41*** (0.09) |

| Cost Sharing | 2.35** (0.96) |

−3.26*** (0.72) |

1.16** (0.58) |

| Number of top 100 on form | 0.96*** (0.11) |

0.81*** (0.05) |

0.06*** (0.01) |

| Quality Rating | 0.72** (.04) |

.03 (.07) |

.61** (.02) |

Notes: Table shows conditional logit results from estimating equation (2) by maximum likelihood. Standard errors are in parentheses. This Table differs from Table 2 in that we report the coefficients on each variable interacted with whether you were a forced switcher (meaning that the plan in which you were enrolled the previous year is no longer available). In addition to the coefficients reported here, all specifications include brand fixed effects, interactions between all the reported coefficients and experience variables, and interactions between the inertia coefficient and (demeaned) values of the plan characteristics for the minimum cost plan, deciles of expenditure in the previous year, and characteristics of the chosen plan in the previous year. In later years, separate inertia dummies are included for the plan one was enrolled in during each preceding year. The average quality variable is a normalized version of the “average rating” index provided by CMS, recovered by auxiliary regression of estimated brand fixed effects on the quality rating variable.

Significant at the 1 percent level.

Significant at the 5 percent level.

Significant at the 10 percent level.

A. Heterogeneous Preferences

An additional implication of our model is that beneficiaries sacrifice a great deal of money to choose particular brand names. The range of brand fixed effects (expressed in dollars of premiums) is more than $1,100. The panel nature of our data allows us to investigate in some detail the structure of these preferences – are they persistent over time or are they idiosyncratic, and are they correlated across similar types of plans? Additionally, by allowing for persistent brand preferences, we prevent these factors from loading onto our estimated inertial term.

To address these issues, we estimate an extension of our baseline model in which brand fixed effects are heterogeneous and normally distributed and can be decomposed into brand and time components: where we allow for arbitrary correlations between and and between it and . Estimation of this model is described in more detail in Appendix C. Because it is much more computationally demanding than our baseline model, we use a 2.5% random sample and restrict to beneficiaries who chose amongst the 11 most popular brands; this yields 9,127 beneficiaries. In addition to our usual plan-level inertial terms, we add inertial terms at the brand level to aid in separate identification of brand preferences. In the appendix we show the results of estimating our baseline model on this more restricted sample; the results are very similar to the full sample.

Table 5 shows the results from estimating this richer model that incorporates heterogeneity. The stylized facts regarding choice inconsistencies reported in the previous section continue to hold (in this case, the inertial coefficients from our original model can be compared to the sum of the plan and brand coefficients in the more flexible specification). Firstly, we note that – comparing the inertial coefficients in Table 5 with Appendix Table 6 - the inertial coefficients are hardly impacted; this suggests that rather than reflecting persistent unobserved factors of chosen plans, they reflect either adjustment costs or inattention.

TABLE 5.

RESTRICTED SAMPLE RANDOM COEFFICIENT MODEL COEFFICIENTS

| Brand Dummies | 2006 | 2007 | 2008 | 2009 |

|---|---|---|---|---|

| Premium (hundreds) |

−0.97*** (0.05) |

−0.92*** (0.06) |

−0.86*** (0.05) |

−1.03*** (0.07) |

| OOP (hundreds) |

−0.20*** (0.03) |

−0.51*** (0.07) |

−0.26*** (0.08) |

−0.64*** (0.11) |

| Variance (times 106) |

−0.16 (0.45) |

−0.26 (0.73) |

−0.59 (0.84) |

−2.33** (1.10) |

| Inertia (plan) | X X |

1.78 (2.28) |

3.96*** (0.32) |

5.85*** (0.42) |

| Inertia (brand) | X X |

2.07** (0.13) |

2.69*** (0.15) |

1.82*** (0.14) |

| Deductible (hundreds) |

−1.35*** (0.09) |

−0.37*** (0.08) |

−0.73*** (0.07) |

−0.62*** (0.09) |

| Full Donut Hole Coverage | 3.55*** (0.33) |

5.88*** (0.58) |

X X |

X X |

| Generic Coverage | 1.27*** (0.18) |

1.52*** (0.17) |

1.35*** (0.22) |

3.06*** (0.34) |

| Cost Sharing | −10.66*** (0.84) |

0.96 (0.99) |

0.54 (0.89) |

−3.70*** (1.07) |

| Number of top 100 on form | 0.09*** (0.01) |

0.48*** (0.14) |

0.37*** (0.09) |

−0.19*** (0.07) |

Notes: Table shows coefficients results from estimating equation (2) by simulated maximum likelihood given the correlational structure specified in Appendix C. Standard errors are in parentheses. In addition to the coefficients reported here, all specifications include brand random effects, separate coefficients for active and forced switchers (only those for active switchers are reported), interactions between all the reported coefficients and experience variables, and interactions between the inertia coefficient and (demeaned) values of the plan characteristics for the minimum cost plan, deciles of expenditure in the previous year, and characteristics of the chosen plan in the previous year. In 2007–2009, separate inertia dummies are included for the plan one was enrolled in during each preceding year as well as separately for the brand one was enrolled in.

Significant at the 1 percent level.

Significant at the 5 percent level.

Significant at the 10 percent level.

Table 6A reports the estimation correlation matrix for the time and brand components of the estimated random effects. In each case, the random effects are identified relative to an omitted brand (the most popular brand) and an omitted time (2006). The time random effects show little evidence of either heterogeneity (the diagonal terms) or persistence (the off-diagonal terms). In other words, any changes across time in brand preferences are well-captured by shifts in means. This does not conclusively tell us whether these brand preferences should count normatively – uncorrelated brand fixed effects could represent some changing aspect of customer service not captured by our quality rating, or they could represent changes in advertising that increase demand in some years but not others. Nonetheless, the lack of correlation across beneficiaries over time does weigh against the possibility that brands which look bad on observable dimensions have some persistent compensating factor.

TABLE 6A.

BRAND RANDOM COEFFICIENT COVARIANCE STRUCTURE

| Panel 1: Covariance Matrix of (in units of premiums) | |||||

|---|---|---|---|---|---|

| 2007 | 2008 | 2009 | |||

| 2007 | 13.72 (134.79) |

−6.53 (32.15) |

−2.98 (18.45) |

||

| 2008 | −6.53 (32.15) |

9.57 (27.64) |

−7.09 (42.78) |

||

| 2009 | −2.98 (18.45) |

−7.09 (42.78) |

21.37 (118.38) |

||

| Panel 2: Covariance Matrix of (in units of premiums) | |||||

| Brand 2 | Brand 3 | Brand 4 | Brand 5 | Brand 6 | |

| Brand 2 | 159.40 (42.47) |

75.74 (37.37) |

93.31 (52.36) |

100.74 (180.34) |

80.68 (94.58) |

| Brand 3 | 75.74 (37.37) |

316.67 (61.26) |

73.41 (70.75) |

140.66 (452.23) |

109.01 (75.13) |

| Brand 4 | 93.31 (52.36) |

73.41 (70.75) |

151.74 (85.86) |

107.34 (51.09) |

129.55 (52.06) |

| Brand 5 | 100.74 (180.34) |

140.66 (452.23) |

107.34 (51.09) |

138.52 (285.31) |

130.95 (264.54) |

| Brand 6 | 80.68 (94.58) |

109.01 (75.13) |

129.55 (52.06) |

130.95 (264.54) |

187.55 (169.85) |

| Brand 7 | 75.61 (72.52) |

195.83 (93.92) |

104.50 (63.49) |

132.95 (102.41) |

155.66 (120.46) |

| Brand 8 | 82.03 (59.56) |

60.97 (51.24) |

155.33 (89.52) |

116.93 (190.84) |

170.06 (87.28) |

| Brand 9 | 149.90 (39.44) |

70.59 (73.06) |

99.89 (102.20) |

96.77 (120.50) |

89.41 (64.14) |

| Brand 10 | 139.84 (44.67) |

123.86 (73.84) |

91.02 (88.34) |

116.70 (85.85) |

81.24 (69.44) |

| Brand 11 | 84.68 (46.88) |

137.76 (137.35) |

124.47 (119.16) |

144.11 (133.59) |

145.79 (92.91) |

| Brand 7 | Brand 8 | Brand 9 | Brand 10 | Brand 11 | |

| Brand 2 | 75.61 (72.52) |

82.03 (59.56) |

149.90 (39.44) |

139.84 (44.67) |

84.68 (46.88) |

| Brand 3 | 195.83 (93.92) |

60.97 (51.24) |

70.59 (73.06) |

123.86 (73.84) |

137.76 (137.35) |

| Brand 4 | 104.50 (63.49) |

155.33 (89.52) |

99.89 (102.20) |

91.02 (88.34) |

124.47 (119.16) |

| Brand 5 | 132.95 (102.41) |

116.93 (190.84) |

96.77 (120.50) |

116.70 (85.85) |

144.11 (133.59) |

| Brand 6 | 155.66 (120.46) |

170.06 (87.28) |

89.41 (64.14) |

81.24 (69.44) |

145.79 (92.91) |

| Brand 7 | 199.41 (125.04) |

116.96 (76.89) |

87.16 (82.16) |

94.33 (43.35) |

129.94 (78.51) |

| Brand 8 | 116.96 (76.89) |

193.88 (70.32) |

92.66 (63.02) |

70.96 (89.22) |

138.40 (123.68) |

| Brand 9 | 87.16 (82.16) |

92.66 (63.02) |

163.15 (44.21) |

132.57 (43.73) |

74.14 (87.11) |

| Brand 10 | 94.33 (43.35) |

70.96 (89.22) |

132.57 (43.73) |

161.03 (42.89) |

114.09 (62.96) |

| Brand 11 | 129.94 (78.51) |

138.40 (123.68) |

74.14 (87.11) |

114.09 (62.96) |

186.01 (108.98) |

Notes: Panel 1 reports the estimated covariance matrix for the time random effects and Panel 2 reports the estimated covariance matrix for brand random effects, as specified in Appendix C. The time random effects are defined relative to 2006 – the diagonal terms are the variance of the difference between time component of the random effect in the specified year and the time component in 2006. The off-diagonal terms are the correlation between these time components. The brand random effects are defined relative to the omitted brand (which is chosen to be the most popular brand). All coefficients are expressed in dollar terms by dividing the estimated covariance parameters by the premium coefficient in 2006.

The across brand random effects show more evidence of both heterogeneity and correlation. The standard deviation of the brand random effects ranges from $125 to $181 (this is the square root of the non-normalized covariance coefficient divided by the premium coefficient); this suggests that beneficiaries vary in the weight they attribute to different plans, but the range of the variation is substantially less than the $1,100 difference in average valuation between the most and least desirable plan. We also find some evidence of correlation amongst brand preferences; while only a few of the off-diagonal terms are significant, all are positive, implying that beneficiaries are correlated in their preference for the most popular plan (which is normalized to 0).

To investigate this correlation further, we estimate a version of the model which classifies all brands into terciles based on overall popularity across all years (table 6B). This model suggests both that preferences for popular plans are correlated (so beneficiaries who prefer brands in the most popular tercile are also more likely to prefer the 2nd tercile to the least popular brands) and that preferences for popular brands are persistent, at least in 2008 and 2009. Thus, while there is little tendency for beneficiaries who idiosyncratically preferred a given brand to prefer that same brand in later years, we do find that beneficiaries who idiosyncratically preferred popular brands have a consistent preference for popular brands over time.

TABLE 6B.

TERCILE OF BRAND POPULARITY RANDOM COEFFICIENT COVARIANCE STRUCTURE

| Panel 1: Covariance Matrix of Time Tercile Random Effects | |||

|---|---|---|---|

| 2007 | 2008 | 2009 | |

| 2007 | 0.08 (0.12) |

−0.25 (0.19) |

−0.37 (0.23) |

| 2008 | −0.25 (0.19) |

1.08 (0.30) |

1.23 (0.33) |

| 2009 | −0.37 (0.23) |

1.23 (0.33) |

1.84 (0.65) |

| Panel 2: Covariance Matrix of Brand Tercile Random Effects | |||

| Tercile 2 | Tercile 3 | ||

| Tercile 2 | 81.99 (45.23) |

76.17 (40.28) |

|

| Tercile 3 | 76.17 (40.28) |

78.74 (39.30) |

|

Notes: Table 6B is identical to 6A, but for the model where brand random effects are replaced with random effects for terciles of brand popularity. Panel 1 reports the estimated covariance matrix for the time component of these random effects and Panel 2 reports the estimated covariance matrix for the brand component of these random effects, as specified in Appendix C. The brand random effects are defined relative to the omitted tercile (which is chosen to be the least popular brands). All coefficients are expressed in dollar terms by dividing the estimated covariance parameters by the premium coefficient in 2006.

B. Welfare Implications

We next use our structural model to move from the results for foregone savings presented above to a welfare metric which includes not only expected spending but also risk protection and plan quality based on the revealed preference weights estimated by the model.

Table 7 shows the results of this welfare analysis in our baseline model. For comparison purposes, the first two rows replicate in the panel sample our earlier results using the predicted spending measure, with foregone savings falling from 2006 to 2007 but then rising from 2007–2009, even relative to plans with similar or lower variance (Table 1 reports the analogous results in the full sample). The third row shows the welfare equivalent in our baseline model: foregone welfare increases overtime, rising from about $161 in 2006 to $251 in 2009. This occurs despite the fact that mean expenditures in our final sample are lower in 2009 than in 2006 ($2150 in 2006 compared to $2100 in 2009). In contrast to foregone savings, welfare is increasing monotonically over time because the one “low cost” plan in 2006 is rated poorly according to the plan quality measure. Thus, while we find as in Ketcham et al. (2012) that foregone savings fall from 2006 to 2007, our more comprehensive welfare measure suggests that this arises mainly because some consumers in 2007 enrolled in cheap, low quality plans.

TABLE 7.

FOREGONE SAVINGS, EFFICIENT FRONTIER SAVINGS, AND FOREGONE WELFARE

| Foregone Welfare | 2006 | 2007 | 2008 | 2009 |

|---|---|---|---|---|

| Foregone Savings PF ($) | 351 | 277 | 308 | 373 |

| Efficient Frontier Pred ($) | 213 | 130 | 174 | 250 |

| Welfare (baseline) | 161 | 170 | 211 | 251 |

| # of Beneficiaries: Baseline | 55585 | 55585 | 55585 | 55585 |

| Inertia Welfare Loss | 2006–2007 | 2007–2008 | 2008–2009 | |

| Baseline Model | 12 | 66 | 60 |