Abstract

Hospital capital investment is important for acquiring and maintaining technology and equipment needed to provide health care. Reduction in capital investment by a hospital has negative implications for patient outcomes. Most hospitals rely on debt and internal cash flow to fund capital investment. The great recession may have made it difficult for hospitals to borrow, thus reducing their capital investment. I investigated the impact of the great recession on capital investment made by California hospitals. Modeling how hospital capital investment may have been liquidity constrained during the recession is a novel contribution to the literature. I estimated the model with California Office of Statewide Health Planning and Development data and system generalized method of moments. Findings suggest that not-for-profit and public hospitals were liquidity constrained during the recession. Comparing the changes in hospital capital investment between 2006 and 2009 showed that hospitals used cash flow to increase capital investment by $2.45 million, other things equal.

Keywords: hospital capital investment, recession, liquidity constraint

Introduction

Capital investment by a firm is the acquisition and maintenance of plant, property, and equipment needed for its operations. Hospital capital investment is important for purchasing technology and equipment necessary to serve patient needs, such as beds, magnetic resonance imaging, and health information technology. Cutbacks in capital investment by a hospital have negative implications for patient outcomes.

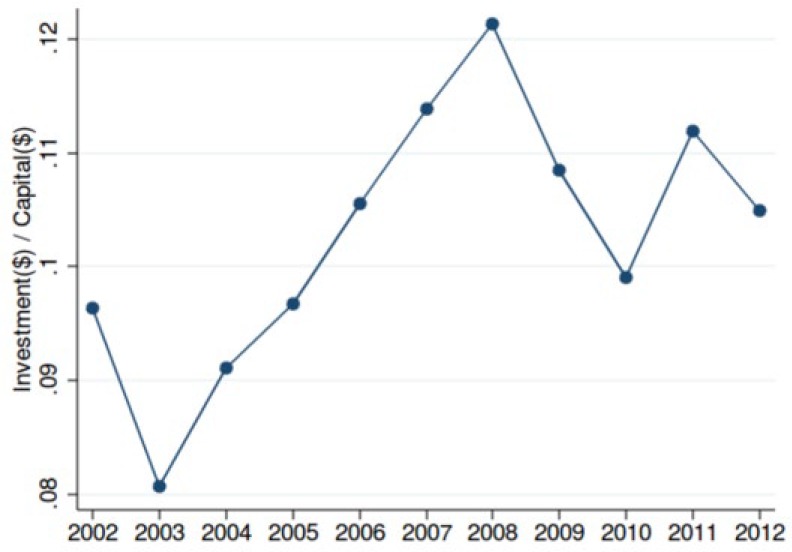

The great recession in the United States began in December 2007 and ended in June 2009.1 Not-for-profit hospitals, which comprise about 58% of US community hospitals,2 rely on debt in the form of bonds and bank loans as the main source of capital to fund capital investment. Investor-owned hospitals (21% of US community hospitals) have more flexibility in financing capital investment because in addition to debt, they can raise equity by selling stocks. In 2008, nearly half of all non-federal hospitals had put capital projects, including facilities, clinical technology, and information technology, on hold or stopped projects in progress.3 Also, the recession deteriorated the value of marketable securities held by hospitals. Endowment loss due to the recession led hospitals to delay purchase of health IT and cut unprofitable services.4 I focused on California hospitals because their financial data were readily available in detail through the California Office of Statewide Health Planning and Development (OSHPD). In California, hospital capital investment per dollar of capital decreased from 2008 to 2010, reversing the increasing trend from 2003 to 2008 (Figure 1).

Figure 1.

Mean capital investment per dollar of capital (OSHPD).

Note. OSHPD = Office of Statewide Health Planning and Development.

A firm is liquidity constrained when lenders limit how much a firm can borrow to fund capital investment. Liquidity-constrained firms may fund capital investment using internal cash as an alternative. The recession was a powerful disruption to the national economy and hospitals may have been liquidity constrained during the recession. My study examined whether hospital capital investment was affected by liquidity constraints in the following periods: pre-recession, during the recession, and during the recovery. Furthermore, hospital ownership differences in liquidity constraint were addressed. Ownership differences allow for different financing mechanisms. Not-for-profit and public hospitals do not have access to equity capital while investor-owned hospital do, and hence investor-owned hospitals are less likely to be liquidity constrained. If the effects of the recession on capital investment were driven by a liquidity constraint, policy changes that mitigate the information asymmetry between hospitals and lenders may facilitate hospitals to make timely capital investments even when market conditions are turbulent.

Previous Literature

The capital structure of a firm is defined as how much of its capital is composed of debt versus equity. The seminal Modigliani-Miller5 theorem showed that in a perfect capital market, the value of a firm is independent of its capital structure. In such a case, the value of a firm only depends on the present value of the expected profits from its assets. Therefore, a firm is indifferent between using debt or equity to finance its investment.

Furthermore, in a perfect capital market, the cost of debt and the opportunity cost of internal cash are equal; this makes them perfect substitutes and makes the investment decision of a firm independent of its ability to generate cash flow.6-8 A perfectly functioning capital market allows a firm with low current cash flow, such as a startup company, to invest by raising equity and debt capital if a firm is expected to generate high future profits.

Departing from the perfect capital market model, the literature on capital market imperfections has explored how information problems in the capital market constrain the investment decision of a firm.9-12 Investment models with a liquidity constraint hypothesize that when lenders have less information than a firm regarding the financial performance of a firm, the cost of borrowing of a firm may be drastically higher than its opportunity cost of using internal funds. If a firm is liquidity constrained, then its investment should be related to its cash flow because a firm must rely more on its internal cash to fund investment.

Theoretical mechanisms through which the recession affected hospital capital investment have not been investigated in the health economics literature. A liquidity constraint may be a mechanism through which the recession affected hospital capital investment. The presence of a liquidity constraint among firms can be empirically tested using the following method: first, stratify the study population by the predictor of liquidity constraint; second, for each stratum estimate the effect of a liquidity variable (such as cash flow) on investment controlling for the theoretical determinant of investment (Tobin’s Q or marginal product of capital).13 A significant relationship between the liquidity variable and investment suggests that firms are liquidity constrained.

Poor hospital cash flow led to cutbacks in hospital investments in plant and equipment among community hospitals between 1995 and 2000.14 However, it is unclear whether liquidity constraints were driving the relationship. Medicare payment cuts resulting from the Balance Budget Act of 1997 and the growth of Health Maintenance Organizations during that time period may have increased the risk of lending to hospitals but the study did not address whether hospitals were liquidity constrained.

Liquidity was strongly related to investment among small non-system hospitals.15 System hospitals are less likely to face financing constraints because they can diversify risk by earning revenue from a wider range of services. Having diverse revenue sources also means that system hospitals are less likely to be affected by the disruptions in service lines or fluctuations in the demand for services. Health information technology systems can lower information asymmetries, but at a high fixed cost, which system hospitals can spread out over their affiliated hospitals. Also, system hospitals may have greater negotiating power against payers and vendors to generate higher profit.

Not-for-profit hospitals often carry large cash reserves to smooth out fluctuations in revenues and expenses and to improve their bond rating from credit rating agencies.16 In response to a liquidity constraint, a not-for-profit hospital may compensate for its low borrowing limit by using its cash reserves in addition to cash flow to internally fund capital investment or to improve access to debt from the capital market. Although cash reserves may improve access to debt, holding large cash reserves also has negative welfare implications for patients as those funds are tied up in reserves instead of being used for hospital operations.

Methods

Theoretical Model

In a perfect capital market, the neoclassical model of investment specifies the capital investment decision of a hospital manager as a dynamic utility maximization problem.6,7 The hospital manager maximizes her profits over an infinite time horizon by equating the marginal cost of capital investment of today to the expected discounted marginal benefit of capital investment in the future. The optimal level of investment measured in dollars, which is normalized by capital stock measured in dollars, is a function of interest rate (%) and marginal product of capital (equation 1). Normalizing investment to investment per dollar of capital is done by dividing the investment by capital stock for hospital at time . Marginal product of capital is the change in hospital output in dollars from a unit change in capital stock :

When lenders do not have full information regarding the ability of a hospital to service its debt, lenders may place a liquidity constraint on the hospital by limiting the amount it can borrow, raising the cost of borrowing, or requiring cash reserves as collateral. A liquidity-constrained hospital, unable to borrow debt, may fund capital investments internally with cash. Hence, the capital investment decision by a liquidity-constrained hospital should be related to its cash flow .12,17 Cash flow measures the net cash inflows and outflows from hospital operations. Cash inflows include payments from payers and donations, and cash outflows include cash expensed to pay for labor and supplies. In addition to cash flow, liquid asset can be used to fund investment directly or used as a collateral to lower the cost of debt. Liquid asset includes cash reserves and marketable securities separate from cash flow. Liquid asset should also be linked to investment in the presence of liquidity constraint (equation 2):

Empirical Model

I specified the empirical model based on the investment model with liquidity constraint. Investment normalized by capital is a function of cash flow , liquid asset , interest rate , and average product of capital . and are normalized by for hospital at time . is the year fixed effects. is the hospital fixed effects. is the idiosyncratic error (equation 3):

The marginal product of capital captures the effect of the marginal product of capital on investment derived from the neoclassical model. However, the marginal product of capital was unobserved in the data, thus substituted with the average product of capital , which was specified as operating revenue per capital. The substitution of marginal product of capital with average product of capital is consistent with the literature.17

I hypothesized that (1) hospitals were not liquidity constrained before the recession, (2) hospitals were liquidity constrained during the recession, and (3) hospitals were not liquidity constrained during the recovery. The recession may have contributed to the information asymmetry between hospitals and lenders because lenders expected the demand for hospital services to fall like the rest of the economy, whereas the demand for hospital services may actually have been less affected. The Medicare population was probably not affected by the weak labor market and the loss of private insurance might have been partially offset by the Consolidated Omnibus Budget Reconciliation Act (COBRA).

Information problem during the recession may have discouraged capital investment by hospitals because lenders limited how much hospitals can borrow, placing a liquidity constraint. When unable to borrow debt due to liquidity constraint, hospitals may respond by using their own internal cash to fund investment.

Alternatively, finding a significant relationship between cash flow and investment in the pre-recession or recovery period suggests that hospitals were chronically liquidity constrained, rather than the recession having an effect. Such finding should raise further concerns about the inefficiencies in the capital market that are preventing hospitals from investing. Furthermore, finding a null relationship between cash flow and investment during the recession suggests that hospitals had access to a well-functioning capital market. Government stimulus during the recession may have encouraged lending to hospitals. The American Recovery and Reinvestment Act of 2009 (ARRA) promoted banks to lend to the not-for-profit and public sectors by expanding the definition of bank-qualified bonds. Bank-qualified bonds allow issuers to sell bonds directly to banks that reduce issuance costs. The banks who purchase bank-qualified bonds benefit from tax incentives. From 2009 to 2011, hospitals have taken advantage of bank-qualified bonds to fund new capital projects.18,19

I anticipated average product of capital to have a significant positive effect because increasing profitability of capital should be related to higher capital investment. The coefficient on average product of capital captures the profit-seeking behavior of hospitals. The investment model describes how hospital investment decision is motivated solely by its profit-maximizing objective. This gross simplification ignores how hospitals may seek to provide high-quality care for their patients. The omission of quality and the resulting endogeneity problem is further discussed in the identification strategy section.

I tested the 3 hypotheses by stratifying the study population into pre-recession, during-recession, and during-recovery periods, then for each period estimating the empirical model. Significant and positive beta coefficients for either or both cash flow and liquid asset are evidence of liquidity constraint in the given period.

Although the recession was dated between 2007 and 2009 nationally, the effect of the recession may have lagged for the hospital industry. A drop in employer-sponsored insurance would have lagged behind the recession because COBRA allows people who lost their jobs to continue their coverage. To account for the lag, years 2008 to 2010 were set as the recession period and 2002 to 2006 were set as the pre-recession period. Year 2007 was excluded because it was a transition period with 11 months out of the year not in recession. Ownership differences may contribute to liquidity constraint. Not-for-profit hospitals and public hospitals are more likely to be liquidity constrained than investor-owned hospitals because they cannot raise equity. During the recession, I further stratified hospitals by ownership and tested for liquidity constraint.

Identification Strategy

The estimation model (equation 3) contains endogenous regressors and unobserved hospital effects that bias the ordinary least squares (OLS) estimates. The regressors cash flow, liquid asset, average product of capital, and interest rate are endogenous to unobserved shocks related to capital investment and the direction of bias can be positive or negative. For example, the service mission of a hospital to improve the health of the community exerts a negative bias on the effect of cash flow. A service activity with a quality objective rather than a profit objective is negatively correlated with cash flow. At the same time, investment is positively correlated with service activity because equipment and facilities are needed to carry out the service activity. In contrast, the reputation of a hospital exerts a positive bias on the effect of cash flow. Hospitals with a good reputation will attract patients; thus, reputation is positively correlated with cash flow. Simultaneously, hospitals invest more to maintain a good reputation and thus reputation is positively correlated with investment. Unobserved hospital effects, such as the performance of the hospital manager, may affect both cash flow and investment. OSHPD provides facility-level financial data. System-level financial information and change in system affiliation were not observed. System affiliation is likely correlated with capital investment and other regressors. Hospital fixed effects absorb the time invariant system effects. Omitted time-varying system effects may bias the OLS estimates. The system generalized method of moments (system GMM) estimator was used to address the fixed effects and endogeneity issues in the estimation model.

Exogeneity of instruments

System GMM estimates a system of levels and differenced equations using the lags and lag differences of the endogenous regressors as instruments for the endogenous regressors. When the endogenous regressor is persistent, lags and lag differences of the endogenous regressors sufficiently removed from the contemporaneous error term are exogenous. If the error term is Autoregressive(p) in the levels equation, is used to instrument for the endogenous regressors . In the differenced equation, is used to instrument for the endogenous regressors ∆.20 System GMM combines the moment conditions for the differenced equation with the moment conditions for the levels equation.21 Compared with estimating the differenced equation alone, system GMM improves the finite sample properties regarding the bias and root mean squared error.

System GMM requires strong assumptions regarding the lags and lag differences of the endogenous regressors. Validity of the assumptions is rigorously tested in an appendix which is available on request. A previous study using system GMM identification strategy for estimating hospital productivity yielded similar results to alternative identification strategies for estimating production functions.22 System GMM producing similar results to alternative identification strategies provides support for the validity of using system GMM with hospital financial data.

Decomposition

The Blinder-Oaxaca decomposition technique was used to decompose the change in hospital capital investment between the pre-recession and during-recession periods.23,24 Hospital observations from 2006 were selected as the pre-recession group. Observations from 2009 were selected as the recession group. Using the GMM coefficient estimates from the pre-recession period and during-recession periods, capital investment was predicted in term of dollars and then separated into the following components.

The effect of the recession due to the change in the estimated coefficients was captured by the coefficient effect . Difference in investment due to the change in the explanatory variables was captured by the change in the variable effect . The effect of the recession due to the difference in the intercepts was captured by the residual effect. Standard errors for the decomposition were estimated by block bootstrapping the hospitals.

Data

OSHPD collects financial data from about 450 not-for-profit and investor-owned hospitals in California each year.25 Participating hospitals report detailed financial information from balance sheets and income statements. OSHPD data include all non-federal California hospitals. The study panel was limited to short-term general acute-care hospitals observed in years 2002 to 2012. Kaiser Permanente hospitals were excluded because they do not report comparable financial data. Hospitals with reporting days less or greater than 365 (less or greater than 366 for leap years) were excluded. A total of 311 hospitals (3168 observations) remained. Then missing and out-of-range values (negative numbers in capital stock or investment) were excluded because they are likely to be data entry errors. The remaining 298 hospitals with an unbalanced panel of 2557 hospital-year observations were analyzed. Dollar amounts were adjusted to 2011 dollars using the GDP deflator.26

Measures

Cash flow measures the net cash inflows and outflows from hospital operations at the end of the reporting period. Liquid asset includes cash reserves and marketable securities measured at the beginning of the reporting period, which excludes cash flow earned in the current reporting period. Liquid asset includes cash and marketable securities reported as current assets; it excludes cash and marketable securities whose use is limited. Interest rate for hospital at time was not observed in the data. Instead, interest rate on outstanding long-term debt was observed. The average interest rate on long-term debt was used a proxy for interest rate. Average product of capital was measured as operating revenue divided by capital at the end of the reporting period.

Results

The study data are summarized in Table 1. Pooling across ownership types, hospitals had a mean annual capital investment of 12.5 million dollars, capital stock of 139.7 million dollars, and investment per capital ratio of 0.098. Ownership differences showed that investor-owned hospital invested relatively more than others with a higher investment per capital ratio. Investor-owned hospitals also generated greater returns from a dollar of capital with a higher average product of capital than others. Investor-owned hospitals had the smallest capital stock, about a third of the size of not-for-profit hospitals and two thirds of the size of public hospitals. The study hospitals comprised 1549 not-for-profit hospitals, 453 investor-owned hospitals, and 555 public hospitals.

Table 1.

Summary Statistics of CA Short-Term General Hospitals.

| All |

Not-for-profit |

Investor-owned |

Public |

|

|---|---|---|---|---|

| Mean (SD) | Mean (SD) | Mean (SD) | Mean (SD) | |

| Investment per Capital I/K | 0.098 | 0.097 | 0.105 | 0.093 |

| (0.114) | (0.098) | (0.163) | (0.109) | |

| Investments I ($ Million) | 12.521 | 16.091 | 5.168 | 8.558 |

| (18.477) | (20.940) | (8.043) | (14.199) | |

| Capital K ($ Million) | 139.695 | 176.819 | 61.740 | 99.707 |

| (144.645) | (157.854) | (64.092) | (114.573) | |

| Cash Flow CF ($ Million) | 14.042 | 17.425 | 8.495 | 9.130 |

| (25.675) | (27.196) | (19.314) | (24.271) | |

| Liquid Assets LA ($ Million) | 14.419 | 17.878 | 2.181 | 14.754 |

| (31.471) | (35.590) | (5.574) | (29.133) | |

| Average Product of Capital APK(Operating Rev/K) | 1.602 | 1.427 | 2.536 | 1.328 |

| (1.017) | (0.798) | (1.380) | (0.750) | |

| Interest Rate on Long Term Debt r (%) | 5.783 | 5.456 | 8.035 | 5.638 |

| (1.958) | (1.761) | (2.557) | (1.402) | |

| N obs | 2557 | 1549 | 453 | 555 |

Source. OSHPD 28th Year (2002-2003) to 38th Year (2012-2013), CA Short-Term General Hospitals, 2002-2012. In millions of 2011 dollars. OSHPD = Office of Statewide Health Planning and Development.

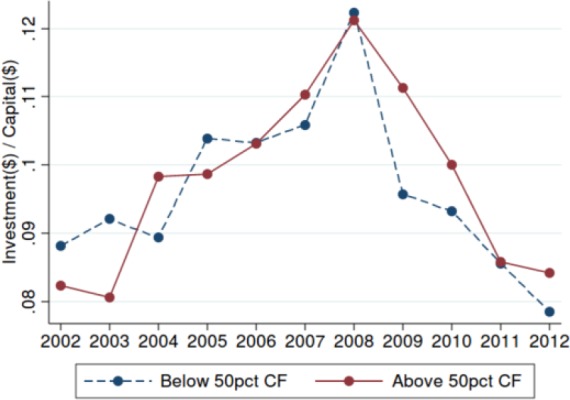

Figure 2 shows the investment time trend separately plotted for hospitals with high cash flow and low cash flow. For each hospital, I calculated its mean cash flow in the pre-recession period. Then I classified the hospitals into high– or low–cash flow group based on whether their pre-recession mean cash flow was above or below the median. Assuming the lack of liquidity constraint, trends in investment prior to the recession should not vary by cash flow status. During the recession, I expected hospitals to be liquidity constrained. When liquidity constrained, high–cash flow hospitals should invest more than low–cash flow hospitals because hospitals are limited in how much they can borrow and must use their own cash flow to fund investment. Time trend in Figure 2 shows that up to 2008, trends in investment between the 2 groups track closely; then the low–cash flow hospitals experienced a sharper drop in investment between 2008 and 2009 compared with the high–cash flow hospitals. The time trend is consistent with the expectation, showing that high–cash flow hospitals invested more than low–cash flow hospitals during the recession.

Figure 2.

Mean capital investment per dollar of capital by cash flow.

I estimated the empirical model (equation) using system GMM. Estimates are stratified by pre-recession (2002-2006), during recession (2008-2010), and recovery (2011-2012). In addition to the GMM estimates, fixed effects regression estimates are reported for comparison. Pre-recession period estimates are presented in Table 2. Cash flow and liquid asset were not significantly related to investment per capital for all hospitals, suggesting that hospitals were not liquidity constrained in the pre-recession period. The GMM estimate for average product of capital at 0.0331*** (P < .001) was significant and positive, and thus investment per capital was significantly related to the profitability of capital. The GMM estimate for average product of capital was smaller than the fixed effects estimate 0.1155*** (P < .001), which implies that managerial performance was positively biasing .

Table 2.

Pre-recession 2002-2006 Estimates.

| All | Fixed Effects | GMM |

|---|---|---|

| I/Kit | (1) | (2) |

| Cash Flowit | −0.0168 | 0.0061 |

| (0.0143) | (0.0372) | |

| Liquid Assetit | 0.0625 | 0.2315 |

| (0.0705) | (0.1184) | |

| Average Product of Capitalit+1 | 0.1155*** | 0.0331*** |

| (0.0341) | (0.0076) | |

| rit +1 | −0.0021*** | −0.0022 |

| (0.0007) | (0.0061) | |

| 2003 | −0.0143** | −0.0149 |

| (0.0065) | (0.0092) | |

| 2004 | −0.0117 | −0.0013 |

| (0.0096) | (0.0109) | |

| 2005 | 0.0078 | −0.0072 |

| (0.0146) | (0.0119) | |

| 2006 | −0.0046 | −0.0114 |

| (0.0092) | (0.0123) | |

| Constant | −0.0721 | 0.0387 |

| (0.0547) | (0.0394) | |

| Arellano-Bond test for Autoregressive(2) P-value | 0.388 | |

| Hansen P-value | .120 | |

| N instruments | 37 | |

| N obs | 1333 | 1091 |

| N hospitals | 263 | 250 |

Note. GMM = generalized method of moments.

P < .05. **P < .01. ***P < .001.

Recession period estimates are presented in Table 3. Cash flow was significantly related to investment per capital, suggesting that hospitals were liquidity constrained during the recession. Increasing cash flow increased investment per capital. The GMM estimate for cash flow at 0.1309** (P < .01) was larger than the fixed effects estimate 0.0932*** (P < .001), which implies that quality was negatively biasing cash flow.

Table 3.

During-Recession 2008-2010 Estimates.

| All | Fixed Effects | GMM |

|---|---|---|

| I/Kit | (1) | (2) |

| Cash Flowit | 0.0932*** | 0.1309** |

| (0.0217) | (0.0454) | |

| Liquid Asset it | −0.0435 | −0.0450 |

| (0.0531) | (0.0724) | |

| Average Product of Capital it+1 | 0.0527** | 0.0307** |

| (0.0192) | (0.0107) | |

| rit +1 | −0.0003 | −0.0014 |

| (0.0005) | (0.0114) | |

| 2009 | 0.0174* | −0.0227** |

| (0.0072) | (0.0085) | |

| 2010 | 0.0032 | −0.0115 |

| (0.0077) | (0.0096) | |

| Constant | 0.0164 | 0.0712 |

| (0.0328) | (0.0610) | |

| Arellano-Bond test for Autoregressive (2) P-value | 0.104 | |

| Hansen P-value | 0.215 | |

| N instruments | 81 | |

| N obs | 669 | 664 |

| N hospitals | 247 | 236 |

Note. GMM = generalized method of moments.

P < .05. **P < .01. ***P < .001.

The coefficient estimate for average product of capital was significant and positive at 0.0307** (P < .01). Again, the GMM estimate for average product of capital was smaller than the fixed effects estimate. The average product of capital coefficient during the recession was smaller than the pre-recession estimate, suggesting that investment decision was less sensitive to the profitability of capital during the recession. Liquidity-constrained hospitals would be limited in their borrowing, thus unable to invest even when there are profitable investment opportunities.

Recovery period estimates are presented in Table 4. Cash flow and liquid asset were not significantly related to investment per capital, suggesting that hospitals were not liquidity constrained. The coefficient estimate for average product of capital was significant and positive at 0.0457** (P < .01). The average product of capital coefficient during the recovery was larger than the recession estimate, suggesting that hospitals were able to finance profitable investments by borrowing.

Table 4.

Recovery 2011-2012 Estimates.

| All | Fixed Effects | GMM |

|---|---|---|

| I/Kit | (1) | (2) |

| Cash Flowit | 0.0810 | 0.0807 |

| (0.1102) | (0.0767) | |

| Liquid Asset it | −0.0461 | −0.0488 |

| (0.0571) | (0.0694) | |

| Average Product of Capital it+1 | 0.0166 | 0.0457** |

| (0.0437) | (0.0171) | |

| rit +1 | −0.0089** | 0.0215 |

| (0.0033) | (0.0301) | |

| 2012 | 0.0422 | 0.0244* |

| (0.0297) | (0.0118) | |

| Constant | 0.1270 | −0.0961 |

| (0.0882) | (0.1467) | |

| Arellano-Bond test for Autoregressive (2) P-value | ||

| Hansen P-value | .463 | |

| N instruments | 56 | |

| N obs | 890 | 445 |

| N hospitals | 253 | 237 |

Note. GMM = generalized method of moments.

P < .05. **P < .01. ***P < .001.

Table 5 shows the during-recession GMM estimates by ownership. Not-for-profit hospital investment was sensitive to cash flow at 0.1878* (P < .05). Public hospital investment was sensitive to liquid asset at 0.0871* (P < .05). Investor-owned hospital investment was not related to cash flow or liquid asset. These results suggest that during the recession, not-for-profit and public hospitals were liquidity constrained. Estimates for investor-owned hospitals were imprecise due to smaller sample size, and did not show statistically significant evidence of liquidity constraint.

Table 5.

During-Recession 2008-2010 Estimates by Ownership.

| GMM | Not-for-profit | Investor-owned | Public |

|---|---|---|---|

| I/Kit | (1) | (2) | (3) |

| Cash Flowit | 0.1878* | 0.2123 | −0.0668 |

| (0.0866) | (0.1365) | (0.0745) | |

| Liquid Asset it | −0.1949 | −0.3568 | 0.0871* |

| (0.1073) | (0.5883) | (0.0406) | |

| Average Product of Capital it+1 | 0.0830* | 0.0619* | −0.0078 |

| (0.0396) | (0.0293) | (0.0109) | |

| rit +1 | 0.0110 | −0.0950 | 0.0048 |

| (0.0153) | (0.0962) | (0.0165) | |

| 2009 | 0.0011 | −0.0506 | 0.0015 |

| (0.0094) | (0.0554) | (0.0166) | |

| 2010 | −0.0033 | 0.1371 | 0.0093 |

| (0.0141) | (0.1714) | (0.0220) | |

| Constant | −0.0626 | 0.6670 | 0.0788 |

| (0.0951) | (0.6955) | (0.0933) | |

| Arellano-Bond test for Autoregressive (2) P-value | 0.280 | 0.470 | 0.997 |

| Hansen P-value | .217 | .441 | .481 |

| N instruments | 51 | 27 | 60 |

| N obs | 429 | 75 | 160 |

| N hospitals | 150 | 30 | 57 |

Note. GMM = generalized method of moments.

P < .05. **P < .01. ***P < .001.

Diagnostic tests supported the validity of the system GMM estimates. In each of the tables presented, the Hansen test of joint validity of the instruments failed to reject the null, showing no evidence that the instruments were not exogenous. Also, over-instrumenting did not appear to be a problem, as the Hansen test statistic was reasonably far from 1.00.27 The Arellano-Bond test for Autoregressive (2) in first differences failed to reject the null, showing no evidence of Autoregressive (1) auto-correlation in the levels equation.

Table 6 summarizes the decomposed change in hospital capital investment between pre-recession and during recession. The residual recession effect is the change in baseline capital investment between the 2 periods. The residual recession effect absorbs the change in capital investment unexplained by the predictors in the empirical model. The residual recession effect was not significant.

Table 6.

All Hospitals Decomposition of Change in Expected Investment due to the Recession.

| E (Investment 2009) − E (Investment 2006) | estimate | [Bootstrap 95% CI] | |

|---|---|---|---|

| I. Cash Flow Effect | 2.45* | 0.51 | 4.38 |

| II. Change in Cash Flow | −0.27 | −0.65 | 0.12 |

| III. Liquid Asset Effect | −2.35 | −6.69 | 1.99 |

| IV. Change in Liquid Assets | 0.54 | −0.31 | 1.39 |

| V. Average Product of Capital Effect | −1.79 | −7.84 | 4.26 |

| VI. Change in Average Product of Capital | 0.48 | −0.17 | 1.12 |

| VII. Interest Rate Effect | 12.52 | −10.84 | 35.87 |

| VIII. Change in Interest Rate Effect | −0.04 | −1.11 | 1.03 |

| IX. Residual Recession Effect | −9.88 | −34.52 | 14.76 |

| Net effect | 1.65 | −1.83 | 5.12 |

Note. Millions of 2011 dollars. CI = confidence interval.

P < .05. **P < .01. ***P < .001.

During the recession, hospital investment was related to cash flow, whereas in pre-recession it was not. The cash flow coefficient effect increased capital investment by $2.45*(P < .05) million. Change in cash flow between the pre-recession group and the recession group was not statistically different. The average product of capital coefficient effect, change in average product of capital, interest rate coefficient effect, and change in interest rate were not statistically different between the pre-recession and the recession groups.

Alternative Specifications

I investigated the robustness of my results against alternative specifications of the empirical model. The effect of cash flow may vary by the level of liquid asset. The interaction term for cash flow and liquid asset captures the substitution effect between the two. System GMM estimates for the pre-recession, recession, and recovery periods including the interaction term showed consistent results with hospitals being sensitive to cash flow only during the recession period. The interaction term was not significant in the 3 periods.

Investment may be persistent over time. A dynamic specification included the lagged dependent and independent variables to test for the presence of an autoregressive (1) error component. The coefficient on the lagged dependent variable was not significant, thus failing to reject the absence of serial correlation in the error term.

The theoretical model and the subsequent empirical model do not explicitly include debt as a predictor of capital investment. However, debt may be correlated with interest rate, because lenders may evaluate existing debt and interest expense. Debt is likely to be correlated with capital investment because it is a funding source for capital investment. Including debt as a predictor in the empirical model did not change the coefficient estimates for cash flow and average product of capital. Also, debt was not a significant predictor.

Interest rate in the empirical model was defined as the average interest rate on long-term debt. Long-term debt took about 5 to 10 years to mature and it did not vary greatly from year to year, which may explain why interest rate was never a significant predictor. Alternatively, I tested the average interest expense per debt as a proxy for interest rate and it was not a significant predictor. The limitation with using average interest expense per debt was that some hospitals had interest expenses greater than debt, which made the ratio implausible.

OSHPD data capture limited use cash and limited use securities. Limited use securities, specifically stocks and bonds, are mainly invested in mutual funds or exchange-traded funds, which can be liquidated within a week. The restrictions on limited use assets may be set internally by the board rather than an external agency; hence, hospitals may have discretion over its limited use asset to fund investment. However, only about 30% of the study hospitals reported having limited use assets, most of them being not-for-profits. Adding limited use cash and limited use securities to the liquid asset variable did not change the estimation results for the pre-recession, during, and recovery periods.

Conclusion

During the recession, capital investment of California not-for-profit and public hospitals was linked to their cash flow. My findings suggest that these hospitals were liquidity constrained during the recession. The fixed effect estimates that suffer from an endogeneity problem underestimated the relationship between cash flow and investment compared with the system GMM estimates. The negative bias on cash flow may be due to the unobserved quality objective of the hospital. Cash flow and liquid asset (cash reserves and marketable securities) measure unrestricted assets that are not limited by external restrictions. These variables should capture the decision of hospital managers, rather than external influences, on how to allocate their cash flow and liquid asset to fund capital investment under liquidity constraint.

The California hospital market is unique because it has a high managed care penetration and dominant multi-hospital systems, specifically Hospital Corporation of America (HCA), Sutter, and Dignity. Therefore, findings from my study may not be reflective of other state markets. My study excluded Kaiser Permanente hospitals, which are a major competitor in California, and this exclusion thereby limits the generalizability of my findings within California. For multi-hospital systems, system-level financial data were not available; thus, my findings are limited to describing hospital-level investment behavior.

A liquidity constraint arises when lenders are uncertain about the ability of hospitals to service their debt and consequently limit how much hospitals can borrow. If there had been a perfectly functioning capital market, cash flow would not have been related to investment. A liquidity constraint drives hospitals to generate large cash flows to fund capital investment rather than spending on expenses related to the provision of health care. Hospital management can reduce expenses by cutting hospital staff, delaying wage payments, and closing service lines. Trading off operating expenses for capital investment may have adverse short-run consequences. A reduction in hospital staff may worsen patient outcomes by increasing provider error.

Not-for-profit hospitals hold a significantly greater proportion of asset as unrestricted cash and marketable securities than investor-owned hospitals.28 Not-for-profit hospitals cannot raise equity capital, which gives them less flexibility when raising capital compared with investor-owned hospitals. Because of this limitation, credit rating agencies emphasize days-cash-on-hand, which is the amount of cash on hand to meet operating expenses, when rating not-for-profit hospitals.29,30 Having more cash and marketable securities help not-for-profit hospitals improve their bond ratings and lower the cost of debt. In contrast, investor-owned hospitals are less concerned about using internal cash to fund investments or improving their credit rating because of their broader access to external funds. It is important to note that agency problems associated with excess cash may influence investment behavior of hospitals, which would obscure the relationship between cash and investment. Among not-for-profit firms, excess cash was not associated with increased investment, but with higher manager compensation.31

The effect of cash flow on investment varied by hospital ownership. During the recession, capital investment of not-for-profit hospitals was sensitive to cash flow; capital investment of public hospitals was sensitive to liquid asset. But capital investment of investor-owned hospitals was not related to either. These findings suggest that during the recession, not-for-profit and public hospitals were liquidity constrained. For investor-owned hospitals, cash flow and liquid asset were not significantly linked to capital investment, suggesting no evidence of liquidity constraint. Investor-owned hospitals can raise equity to fund capital investments, whereas not-for-profit and public hospitals cannot. This institutional difference makes investor-owned hospitals less susceptible to liquidity constraint.

Decomposing the change in hospital capital investment between pre-recession and during recession did not reveal a significant drop in capital investment. The average decrease in capital investment is the change in capital investment while holding constant the effects of cash flow and other predictors in the empirical model. This change in capital investment unexplained by the model, or the residual effect, includes the net of the pre-recession year fixed effect and the during-recession fixed effect. Thus, any policy changes affecting capital investment is captured by the residual effect. However, the large uncertainty around the estimated residual effect makes it unclear how policy changes, such as the government stimulus funds going to hospitals through ARRA, affected hospital capital investment.

Hospitals responded to the recession by using cash flow to offset the effect of restricted borrowing. Capital investment was more sensitive to cash flow during the recession, which increased capital investment by $2.45* (P < .05) million, other things equal. The cash flow effect isolates the change in capital investment due to the change in coefficient estimate for the pre-recession group and the recession group.

The interval estimates in Table 6 reflect two sources of uncertainty: (1) uncertainty around the coefficient estimates and (2) uncertainty around the variables. Using bootstrap sampling, for each sample drawn I estimated the empirical model coefficients and then inserted them into the Blinder-Oaxaca equation for decomposition. Low precision in the coefficient effect is likely due to large variations in the beta coefficient among the bootstrap samples. Stratifying the population by ownership did not improve the precision of the bootstrap confidence intervals. In Tables 2 and 3, the coefficient on liquid asset was significantly positive in the pre-recession period, and then negative but not significant during the recession. I suspect that the relationship between liquid asset and investment was mixed because hospitals may be holding it as a collateral for debt rather than using it to directly fund investment. Average product of capital was significantly positive in the pre-recession period and significantly positive during the recession; the coefficient did not change much in size (0.0331 to 0.0307). Hence, the small change between periods would yield an estimate close to zero. Interest rate suffered from measurement noise, which may explain the wide uncertainty around its coefficient effect.

The unexpected estimation results for liquid asset challenge the hypothesized relationship between liquid asset and capital investment. During the recession, the coefficient on liquid asset was negative and not significant. The negative estimate for liquid asset, where a positive estimate was expected, raises the question of multi-collinearity due to the correlation between cash flow and liquid asset. In the pooled data, the Pearson correlation coefficient between cash flow and liquid asset was 0.11; during the recession it was .24. Both coefficients suggest a low correlation between the 2 variables. Removing 1 of the 2 variables from the estimation model did not change the result for the other. For the recession period, estimating the investment model without liquid asset resulted in a positive and significant cash flow coefficient; estimating the investment model without cash flow resulted in a negative but not significant liquid asset coefficient. Overall, the robustness checks did not provide strong evidence of multi-collinearity.

If the imprecise coefficient estimate for liquid asset is unbiased and truly negative, a negative relationship between liquid asset and capital investment is nonetheless counterintuitive. Fluctuations in operating revenue and costs during the recession may have prompted hospitals to build its liquid assets at the expense of cutting investments. But it is not obvious why increasing liquid asset decreases investment when increasing cash flow increases investment, given that they are both internal funds that can be used at discretion by hospitals.

Because the negative coefficient on liquid asset was not significant, I am more comfortable interpreting the coefficient as a null instead of a negative. A null relationship between liquid asset and capital investment is also inconsistent with expectation. Among not-for-profit hospitals, holding more liquid asset should improve their bond rating, which facilitates the debt financing of capital investment. Because a certain level of liquid asset is needed to meet the days-cash-on-hand requirement by credit rating agencies, not-for-profit hospitals may not have been able to use liquid asset to directly fund investment. Another motive for hospitals to hold liquid asset is to engage in indirect arbitrage by borrowing funds at the tax-exempt interest rate while using the liquid asset to generate returns in the taxable market.

For some hospitals, shift in financing strategy to bank direct placements in response to the collapse of the auction rate bond market in 2008 may have diminished the role of liquid asset in financing capital investment. Hospitals can directly sell their bond to banks through a direct placement, which eliminates the need for a credit rating agency. In addition, a direct placement does not require a debt service reserve fund, which is cash set aside to service debt. Hence, a bank direct placement uncouples liquid asset from access to debt.

A liquidity-constrained hospital with poor cash flow is likely to fall behind on making the capital investment necessary for its operations and face the risk of closure. Hospitals with low cash flow tend to be small rural hospitals that provide care to underserved populations. During an economic recession when poor financial performance is due to the external environment rather than the hospital management, access to debt is critical for hospitals to endure the recession. Policy changes that reduce payments to hospitals may discourage liquidity-constrained hospitals from investing in capital.

The relationship between average product of capital and capital investment diminished during the recession, although the change in coefficient was not statistically significant. Capital investment may have been forgone during the recession because of greater uncertainty regarding the return on investment, even though the investment may have been profitable. The implications of the forgone profitable investment for patient welfare depend on who is the residual claimant of hospital profits. Profits from investment may be returned to the community, which in theory defines not-for-profit organizations, or may be used to improve the quality of hospital services. Decreased profits from investment would decrease patient welfare because less residual surplus is returned to patients. However, forgoing profitable investment that provides no medical benefit to patients but only generates profits for the hospital manager would be beneficial to patient welfare.

Prior to the great recession, auction rate bonds and variable rate demand bonds were financing strategies available to hospitals that offered short-term interest rates on long-term maturities. Auction rate bonds were especially attractive to issuers because of low financing costs. During the subprime mortgage crisis in 2008, the auction rate bond market collapsed and the variable rate demand bond market was volatile. Facing spikes in interest rates, many hospitals that held these variable rate bonds refinanced into long-term bonds.32-35 Hospitals moving into fixed rate long-term bonds during the recession may explain why interest rate did not vary year to year in the data. Also, direct placements between hospitals and banks steadily grew between 2008 and 2011. In a direct placement, hospitals directly issue bonds to banks instead of public offerings. Regulation and accounting guidelines surrounding direct placements were unclear during the time,36-37 and hence direct placements may not have been captured in the OSHPD financial data.

My study provides evidence of liquidity constraint among California not-for-profit and public hospitals during the recession. The theoretical cause of this liquidity constraint is asymmetric information, a market failure that warrants policy intervention. Leading up to the recession, municipal bond market disclosures had shortcomings regarding their timeliness, frequency, and completeness compared with the private bond market.38 These issues may have exacerbated the volatility in the municipal bond market in 2008. Securities and Exchange Commission made rule changes in 2010 aimed to provide more information to investors in a timely manner.39 The rule changes made certain information, including official statements, continuing disclosure, and real-time trade price, available online to the public.40 The lack of transparency in the financial disclosures of not-for-profit hospitals may have disastrous consequences such as the failure of the Allegheny Health Education and Research Foundation. Policy interventions that mitigate the problem of asymmetric information between hospitals and lenders may alleviate liquidity constraints during economic downturns. Improving hospital access to debt for investing in new equipment and facilities is critical for maintaining and improving the quality of hospital services.

Acknowledgments

I acknowledge my committee members Roger Feldman, Jeffrey McCullough, Stephen Parente, Santiago Bazdresch, and Pinar Karaca-Mandic for their guidance and support.

Footnotes

Author’s Note: The author is now at Owen Graduate School of Management, Vanderbilt University, Nashville, Tennessee. This research article was prepared by the author’s personal capacity. The opinions expressed in this article are the author’s own and do not reflect the view of the University of Minnesota.

Declaration of Conflicting Interests: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding: The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the University of Minnesota Doctoral Dissertation Fellowship.

References

- 1. National Bureau of Economic Research. The NBER’s Business Cycle Dating Committee. 2010. http://www.nber.org/cycles/recessions.html. Accessed May 12, 2017.

- 2. American Hospital Association. AHA annual survey. 2013. http://www.ahadataviewer.com/book-cd-products/aha-survey/. Accessed May 12, 2017.

- 3. American Hospital Association. Report on the capital crisis: impact on hospitals. Washington, DC; 2009. http://www.aha.org/content/00-10/090122capitalcrisisreport.pdf. Accessed May 12, 2017. [PubMed] [Google Scholar]

- 4. Dranove D, Garthwaite C, Ody C. How do hospitals respond to negative financial shocks? The impact of the 2008 stock market crash. http://www.nber.org/papers/w18853. National Bureau of Economic Research working paper series 18853. Published February 2013. Accessed May 12, 2017.

- 5. Modigliani F, Miller MH. The cost of capital, corporation finance and the theory of investment. Am Econ Rev. 1958;48(3):261-297. [Google Scholar]

- 6. Jorgenson D. Capital theory and investment behavior. Am Econ Rev. 1963;53(2):247-259. http://www.jstor.org/stable/10.2307/1823868. Accessed May 12, 2017. [Google Scholar]

- 7. Hall R, Jorgenson D. Tax policy and investment behavior. Am Econ Rev. 1967;57(3):391-414. http://www.jstor.org/stable/10.2307/1812110. Accessed May 12, 2017. [Google Scholar]

- 8. Jorgenson DW, Siebert CD. Optimal capital accumulation and corporate investment behavior. J Polit Econ. 1968;76(6):1123-1151. doi: 10.1086/259478. [DOI] [Google Scholar]

- 9. Fazzari S, Athey M. Asymmetric information, financing constraints, and investment. Rev Econ Stat. 1987;69(3):481-487. doi: 10.2307/1925536. [DOI] [Google Scholar]

- 10. Fazzari S, Hubbard G, Petersen BC. Financing constraints and corporate investment. Brookings Pap Eco Ac. 1988;1988(1):141-195. doi: 10.1016/j.jfineco.2007.11.005. [DOI] [Google Scholar]

- 11. Hoshi T, Kashyap A, Scharfstein D. Corporate structure, liquidity, and investment: evidence from Japanese industrial groups. Q J Econ. 1991;106(1):33-60. doi: 10.2307/2937905. [DOI] [Google Scholar]

- 12. Whited TM. Debt, liquidity constraints, and corporate investment: evidence from panel data. J Financ. 1992;47(4):1425-1460. http://onlinelibrary.wiley.com/doi/10.1111/j.1540-6261.1992.tb04664.x/abstract. Accessed May 12, 2017. [Google Scholar]

- 13. Hubbard R. Capital-market imperfections and investment. http://www.nber.org/papers/w5996. National Bureau of Economic Research working paper series 5996. Published April 1997. Accessed May 12, 2017.

- 14. Bazzoli GGJ, Clement JPJ, Lindrooth RC, et al. Hospital financial condition and operational decisions related to the quality of hospital care. Med Care Res Rev. 2007;64(2):148-168. doi: 10.1177/1077558706298289. [DOI] [PubMed] [Google Scholar]

- 15. Calem PS, Rizzo JA. Financing constraints and investment: new evidence from hospital industry data. J Money Credit Bank. 1995;27(4):1002-1014. doi: 10.2307/2077785. [DOI] [Google Scholar]

- 16. Robinson JC. Bond-market skepticism and stock-market exuberance in the hospital industry. Health Aff. 2002;21(1):104-117. doi: 10.1377/hlthaff.21.1.104. [DOI] [PubMed] [Google Scholar]

- 17. Gilchrist S, Himmelberg C. Investment: fundamentals and finance. NBER working paper 6652. 1998. doi: 10.3386/w6652. [DOI] [Google Scholar]

- 18. Ostlund G, Cheney JE. Tax-exempt bank loans still an option for providers. Healthc Financ Manage. 2011;65(7):70-73. [PubMed] [Google Scholar]

- 19. Fallor E. Bill to raise issuer limit for bank qualified bonds offered in senate. Bond Buyer. July 20 2016. https://www.bondbuyer.com/news/bill-to-raise-issuer-limit-for-bank-qualified-bonds-offered-in-senate Accessed May 12, 2017.

- 20. Arellano M, Bond S. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Rev Econ Stud. 1991;58(2):277-297. doi: 10.2307/2297968. [DOI] [Google Scholar]

- 21. Blundell R, Bond S. Initial conditions and moment restrictions in dynamic panel data models. J Econometrics. 1998;87(1):115-143. doi: 10.1016/S0304-4076(98)00009-8. [DOI] [Google Scholar]

- 22. Lee J, McCullough JS, Town RJ. The impact of health information technology on hospital productivity. RAND J Econ. 2013;44(3):545-568. doi: 10.1111/1756-2171.12030. [DOI] [Google Scholar]

- 23. Blinder AS. Wage discrimination: reduced form and structural estimates. J Hum Resour. 1973;8(4):436-455. http://econpapers.repec.org/RePEc:uwp:jhriss:v:8:y:1973:i:4:p:436-455. Accessed May 12, 2017. [Google Scholar]

- 24. Oaxaca R. Male-female wage differentials in urban labor markets. Int Econ Rev. 1973;14(3):693-709. http://ideas.repec.org/a/ier/iecrev/v14y1973i3p693-709.html. Accessed May 12, 2017. [Google Scholar]

- 25. Office of Statewide Health Planning and Development (OSHPD). Hospital annual financial data. 2012. https://www.oshpd.ca.gov/HID/Find-Hospital-Data.html Accessed May 12, 2017.

- 26. Federal Reserve Bank of St. Louis. Gross domestic product: implicit price deflator. 2015. https://fred.stlouisfed.org/series/GDPDEF. Accessed May 12, 2017.

- 27. Roodman D. A note on the theme of too many instruments. Oxford B Econ Stat. 2009;71(1):135-158. doi: 10.1111/j.1468-0084.2008.00542.x. [DOI] [Google Scholar]

- 28. Song PH, Reiter KL. Trends in asset structure between not-for-profit and investor owned hospitals. Med Care Res Rev. 2010;67(6):694-706. doi: 10.1177/1077558710368807. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 29. Moody’s Investor Service. Rating Methodology: For-Profit Hospitals Versus Not-for-Profit Hospitals: Explaining the Gap. New York, NY: Moody’s Investor Service; 1999. [Google Scholar]

- 30. Moody’s Investor Service. Not-for-Profit Healthcare Rating Methodology. New York, NY: Moody’s Investor Service; 2012. [Google Scholar]

- 31. Core JE, Guay WR, Verdi RS. Agency problems of excess endowment holdings in not-for-profit firms. J Account Econ. 2006;41(3):307-333. doi: 10.1016/j.jacceco.2006.02.001. [DOI] [Google Scholar]

- 32. Blanda CM, Gould KA. Financing Options for Large Nonprofit Hospitals and Multi-Hospital Systems. Columbus, OH: Lancaster Pollard; 2013. [Google Scholar]

- 33. D’Silva A, Gregg H, Marshall D. Explaining the Decline in the Auction Rate Securities Market. Chicago, IL: Federal Reserve Bank of Chicago; 2008. [Google Scholar]

- 34. Evans M. Auction-rate endgame. Modern Healthcare. December 1, 2008. http://www.modernhealthcare.com/article/20081201/MAGAZINE/811269983. Accessed May 12, 2017. [PubMed]

- 35. Evans M. Hospitals turn to banks for direct loans. Modern Healthcare. March 3, 2012. http://www.modernhealthcare.com/article/20120303/MAGAZINE/303039961. Accessed May 12, 2017. [PubMed]

- 36. Municipal Securities Rulemaking Board. Municipal Auction Rate Securities and Variable Rate Demand Obligations. 2010. http://www.msrb.org/~/media/Files/Special-Publications/MSRBARSandVRDOReportSeptember2010.ashx?la=en Accessed May 12, 2017.

- 37. Municipal Securities Rulemaking Board. Potential applicability of MSRB rules to certain “direct purchases” and “bank loans.” MSRB 2011-52. 2011. http://msrb.org/Rules-and-Interpretations/Regulatory-Notices/2011/2011-52.aspx. Accessed January 24, 2017.

- 38. Government Accountability Office. Municipal Securities: Options for Improving Continuing Disclosure. GAO-12-698. 2012. http://www.gao.gov/assets/600/592669.pdf Accessed May 12, 2017.

- 39. Securities and Exchange Commission. New rules improving municipal disclosure. 2010. https://www.sec.gov/investor/alerts/investorbulletin-munis.htm. Accessed January 24, 2017.

- 40. Municipal Securities Rulemaking Board. Electronic municipal market access. 2017. http://emma.msrb.org/. Accessed January 24, 2017.