Abstract

Purpose

High-deductible health plans (HDHPs) require substantial out-of-pocket spending and might delay crucial health services. Breast cancer treatment delays of as little as 2 months are associated with adverse outcomes.

Methods

We used a controlled prepost design with survival analysis to assess timing of breast cancer care events among 273,499 women age 25 to 64 years without evidence of breast cancer before inclusion. Women were included if continuously enrolled for 1 year in a low-deductible ($0 to $500) plan followed by up to 4 years in a HDHP (at least $1,000 deductible) after an employer-mandated switch. Study inclusion was on a rolling basis, and members were followed between 2003 and 2012. The comparison group comprised 2.4 million contemporaneously matched women whose employers offered only low-deductible plans. Measures were times to first diagnostic breast imaging (diagnostic mammogram, breast ultrasound, or breast magnetic resonance imaging), breast biopsy, incident early-stage breast cancer diagnosis, and breast cancer chemotherapy. Outcomes were analyzed by using Cox models and adjusted for age-group, morbidity score, poverty level, US region, index date, and employer size.

Results

After the index date, HDHP members experienced delays in receipt of diagnostic imaging (adjusted hazard ratio [aHR], 0.95; 95% CI, 0.94 to 0.96), biopsy (aHR, 0.92; 95% CI, 0.89 to 0.95), early-stage breast cancer diagnosis (aHR, 0.83; 0.78 to 0.90), and chemotherapy initiation (aHR, 0.79; 95% CI, 0.72 to 0.86) compared with the control group.

Conclusion

Women switched to HDHPs experienced delays in diagnostic breast imaging, breast biopsy, early-stage breast cancer diagnosis, and chemotherapy initiation. Additional research should determine whether such delays cause adverse health outcomes, and policymakers should consider selectively reducing out-of-pocket costs for key breast cancer services.

INTRODUCTION

Breast cancer is the most common nonskin malignancy among US women and the second-leading cause of cancer death.1 The diagnosis and treatment of breast cancer require a series of expensive services, such as diagnostic breast imaging, specialist visits, breast biopsy, mastectomy, lumpectomy, and chemotherapy.2,3 Women who face high out-of-pocket costs might delay receipt of these services.

High-deductible health plans (HDHPs) have become the predominant commercial health insurance arrangement in the United States.4 This insurance type requires potential annual out-of-pocket spending of between $1,000 and $6,000 per person for most nonpreventive care, including services for cancer diagnosis and treatment. In 2016, 51% of covered workers had deductibles of ≥ $1,000.4

Experts have voiced concerns that the increasing out-of-pocket burden of cancer5,6 is causing financial toxicity that could harm the health of patients with cancer,7,8 but research that has quantified such harm is limited. Neugut et al9 studied the association of copayments and aromatase inhibitor nonpersistence among patients with breast cancer and found that copayments > $90 were associated with lower persistence. Dusetzina et al10 found that patients with chronic myeloid leukemia with higher out-of-pocket payments had a greater likelihood of imatinib discontinuation or nonadherence than matched patients with lower out-of-pocket payments.

The effects of cost sharing on other key services along the spectrum from cancer diagnostic testing to treatment are unknown. Whether women in HDHPs will generally accept high out-of-pocket payments to receive potentially life-saving breast cancer care or will delay services and risk adverse health consequences is unclear. Breast cancer treatment delays of as few as 2 months are associated with adverse outcomes.11-13 We hypothesized that breast cancer diagnostic testing, diagnosis, and treatment would be delayed among women after they transition to HDHPs.

METHODS

Population

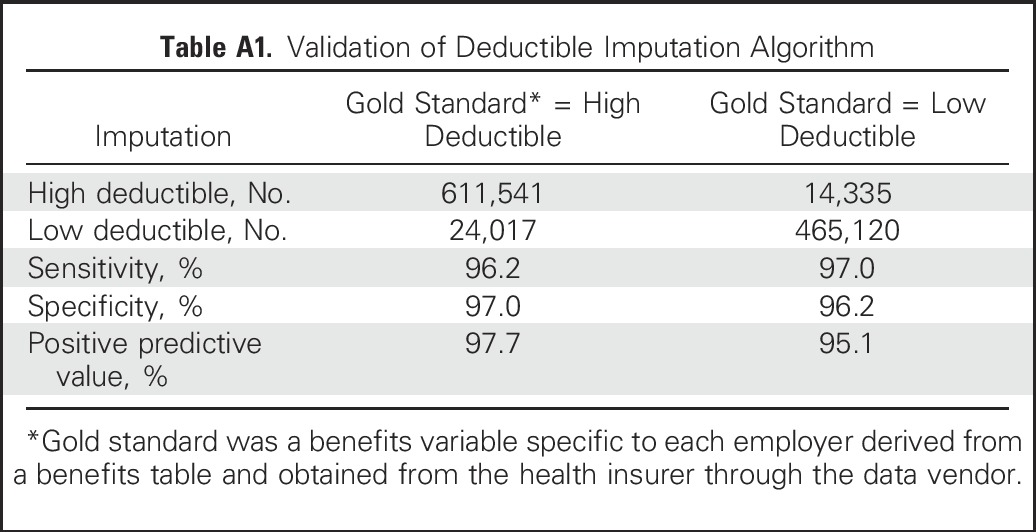

We drew our study population from commercially insured members in the deidentified Optum database (Eden Prairie, MN) enrolled between January 2003 and December 2012. Data comprised all medical, pharmacy, and hospitalization claims from members of a large national health plan. We included members on the basis of their employers’ health insurance offerings. We defined employers with low- and high-deductible coverage as those that offer exclusively annual deductibles of $0 to $500 and ≥ $1,000, respectively (Appendix, online only). To determine employer annual deductibles, we used a benefits variable available for most smaller employers (approximately ≤ 100 employees). For larger employers, we imputed deductible levels by using out-of-pocket spending among employees who used health services, an algorithm that had 96.2% sensitivity and 97.0% specificity (Appendix Table A1, online only).

Both high- and low-deductible plans generally cover breast cancer screening and preventive primary care visits at low or no out-of-pocket cost. However, HDHP members on average must pay substantially higher amounts than low-deductible members for specialist care, diagnostic tests, and surgical procedures.4

Our population of interest was composed of generally healthy women without breast cancer at the beginning of the study period so that we could observe their progression along the pathway from breast cancer work-up (ie, screening mammography, diagnostic imaging, biopsy) to diagnosis and treatment. Study members were drawn from employers who were present for at least 1 year before and after either a mandated HDHP switch or a mandated continuation in low-deductible plans (n = 18,258,838 members), which minimized self-selection. We excluded 26,066 women who had at least one breast cancer diagnosis (International Classification of Diseases, 9th Revision, codes 174.xx, 233.0) before the baseline year. From a subset of women age 25 to 64 years at baseline (n = 5,853,802), we selected 3,594,311 with 12 potential baseline months of enrollment in a low-deductible plan followed by ≥ 1 month in a high-deductible or low-deductible plan. We included women age 25 to 39 years because initial work-ups for breast lumps are common in this population,14 and delayed evaluation could cause substantial anxiety irrespective of cancer risk. Furthermore, although rare, women in this group do develop breast cancer.15

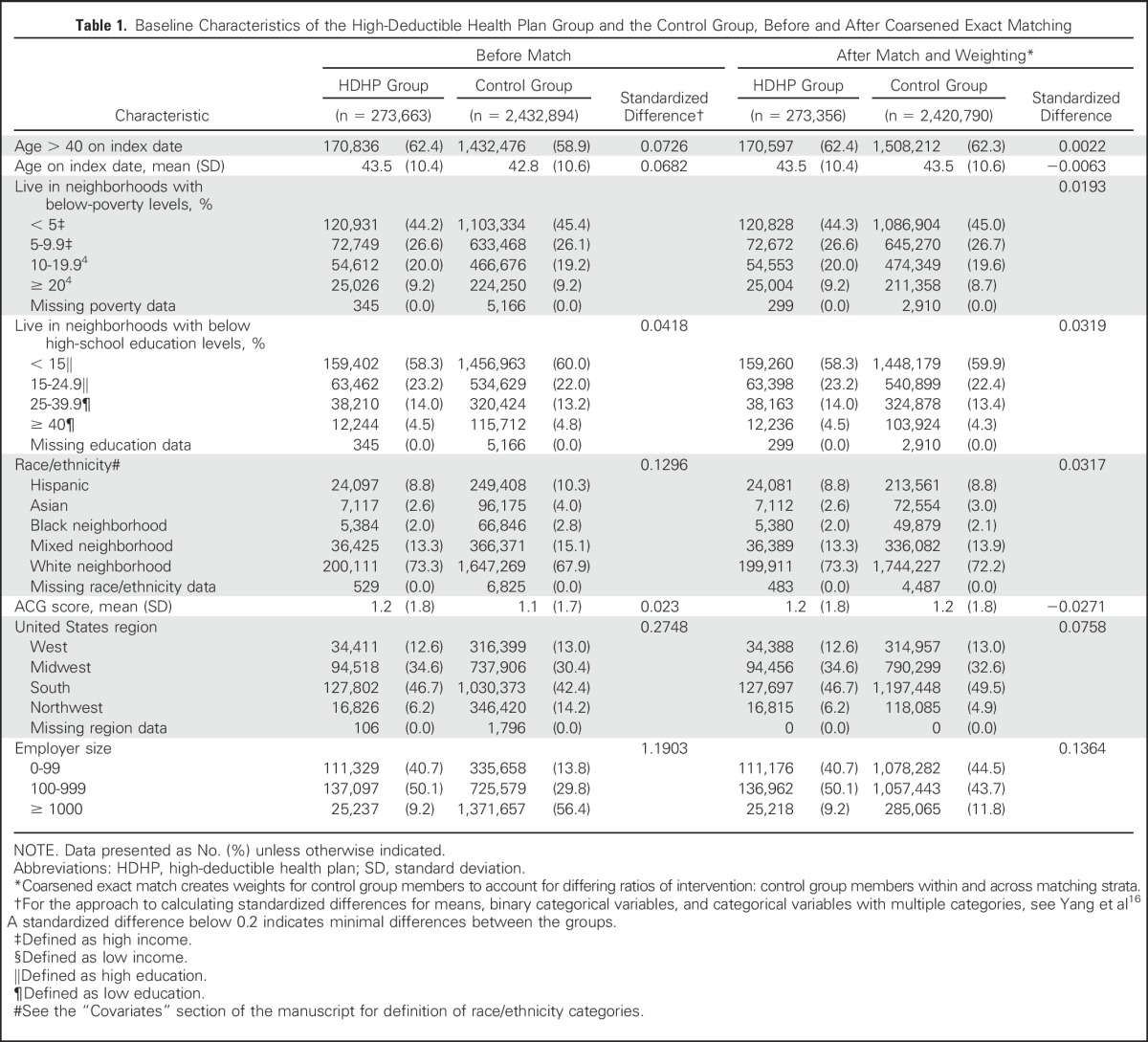

Because a subset of women could have multiple eligible 12-month low-deductible baseline periods, we randomly selected one per woman, leaving 273,663 high-deductible and 2,432,894 control pool members (Table 1). We defined the beginning of the month of the low- to high-deductible transition as the index date.

Table 1.

Baseline Characteristics of the High-Deductible Health Plan Group and the Control Group, Before and After Coarsened Exact Matching

To further minimize potential selection effects, especially at the employer level, we used a coarsened exact match17-19 on employer- and member-level propensity20,21 to join HDHPs (Appendix); baseline annual out-of-pocket spending category (< $100, $100 to 999, $1,000 to $9,999, ≥ $10,000); whether members had a baseline breast diagnostic image, breast biopsy, early-stage breast cancer diagnosis, or breast cancer chemotherapy treatment (Appendix Table A2, online only); and follow-up duration divided into 6-month categories (to minimize differential dropout). We included baseline indicators of outcome measures (eg, breast imaging, biopsy) to balance the future population-level need for breast cancer services during the follow-up period.

Compared with the unmatched sample, the coarsened exact match (after applying match-generated weights) increased the similarity of the HDHP and control groups across all baseline characteristics (Table 1). The final groups included 273,356 women in HDHPs and 2,420,790 women in the matched control group.

Design

We first displayed weighted and marginally adjusted Kaplan-Meier plots of outcomes in the high-deductible and control groups and then compared times to events in the groups before and after the index date. Controlled survival designs test the null hypothesis that the hazard ratios of the intervention and control groups are the same.

Measures

We defined time zerob as the beginning of the 12-month baseline period and time zerof as the beginning of the follow-up period. In the baseline and follow-up periods, we measured months from time zerob and zerof, respectively, until the first observed breast cancer diagnostic imaging (diagnostic mammogram, breast ultrasound, or breast MRI [Appendix]),22 first breast biopsy (Appendix),23-25 first incident early-stage cancer diagnosis (by using an algorithm validated by Nattinger et al23), and first breast cancer chemotherapy treatment (defined herein). At the patient level, the breast cancer diagnostic imaging and biopsy measures could occur in both the baseline and the follow-up periods (once per woman per period) given that repeat diagnostic testing occurs. For the incident early-stage breast cancer diagnosis and chemotherapy initiation measures, we allowed a given woman to have only a single first event over the entire study period. The Nattinger incident early-stage breast cancer diagnosis algorithm is based on evidence of both breast cancer diagnosis and early-stage breast cancer treatment (mastectomy or combined lumpectomy and radiotherapy), so this measure describes timing of both early-stage diagnosis and treatment.23 We measured first chemotherapy initiation to assess the timing of treatment of more-advanced breast cancers (ie, those that spread at least to local lymph nodes).26 This outcome required evidence of first chemotherapy administration preceded (at most 3 months before) by a breast cancer diagnosis. We derived chemotherapy codes on the basis of the SEER-Medicare claims-based algorithm27 and then restricted to agents used for breast cancer3,28 or codes specific to chemotherapy administration (Appendix).

Because screening mammography (Appendix) has low out-of-pocket costs in HDHPs, we measured this as a control outcome that we hypothesized would be less affected by the HDHP switch in contrast to the previously described expensive breast cancer services. To generate more clinically intuitive measures of potential delays among HDHP members, we measured intervals (in months) between time zerof and any subsequent first diagnostic breast imaging, breast biopsy, incident early-stage breast cancer diagnosis, or breast cancer chemotherapy. We conducted sensitivity analyses to determine whether estimates differed if we restricted to women age 40 to 64 years or restricted to women with at least 6 months follow-up after the index date.

Covariates

Using 2000 US Census block group data and validated methods,29,30 we defined four neighborhood income and education levels (Table 1).29-31 We applied the ACG comorbidity algorithm, a validated measure that predicts mortality,32,33 to members’ baseline year to estimate comorbidity. We classified members as white, black, Hispanic, Asian, or mixed race/ethnicity neighborhood on the basis of a combination of geocoding and surname analysis (Appendix).34,35 Other covariates included age category (25 to 39 and 40 to 64 years), employer size (10 to 99, 100 to 999, and ≥ 1,000 enrollees), and US region (West, Midwest, South, Northeast).

Analysis

We compared baseline characteristics of our study groups by using a standardized differences approach.16 We analyzed time to the four primary outcomes independently by using Cox proportional hazards regression models adjusted for baseline age-group, ACG score, employer size, poverty level, US region, and index date. We analyzed time to event in the baseline and time to event in the follow-up periods in separate models. Women were censored if they dropped from the sample (eg, as a result of disenrollment), reached age 65 years (when Medicare coverage begins), or reached the end of follow-up (1 year for the baseline model and 4 years for the follow-up model). The key term of interest from the baseline and follow-up period regression models was a binary indicator of membership in the high-deductible group. This term generated an adjusted hazard ratio (aHR) of the high-deductible group compared with the control group. For example, a follow-up period aHR with CI bounds < 1.0 is interpreted as indicating that the high-deductible group experienced a delay in the outcome of interest during follow-up relative to the control group.

To develop insights about the clinical significance of any statistically significant aHRs at follow-up, we predicted the interval in months between time zerof and the month that the control group reached half of its final follow-up period rate (derived from the Cox models) and the corresponding time for the high-deductible group to reach this same percentage (half of the control group’s final follow-up rate), which assumed that event time followed a Weibull distribution and used an accelerated failure time model.36

RESULTS

After matching and applying match-generated weights, all standardized differences between HDHP and control group characteristics were well below 0.2 (Table 1), which indicates minimal differences.16 The mean age of HDHP and control members was 43.5 years (standard deviation, 10.4 to 10.6; Table 1). Twenty-eight percent to 29% lived in low-income neighborhoods, 18% to 19% lived in low-education neighborhoods, and 9% were of Hispanic ethnicity. The HDHP and control groups were well balanced with respect to morbidity at baseline, with ACG scores (standard deviation) of 1.2 (1.8) and a standardized difference of −0.027.

From baseline to follow-up, HDHP members experienced increases in total out-of-pocket medical spending (ie, nonpharmacy deductible, copayment, coinsurance amounts) relative to control group members of between 39.0% (37.5% to 40.4%) to 50.2% (47.4% to 52.9%) across the follow-up years (Fig 1).

Fig 1.

Mean total out-of-pocket medical spending (ie, nonpharmacy deductible, copayment, coinsurance amounts) per month in the high-deductible health plan (HDHP) and control groups before and after the HDHP switch, which indicates the extent of the cost-sharing exposure in the HDHP group.

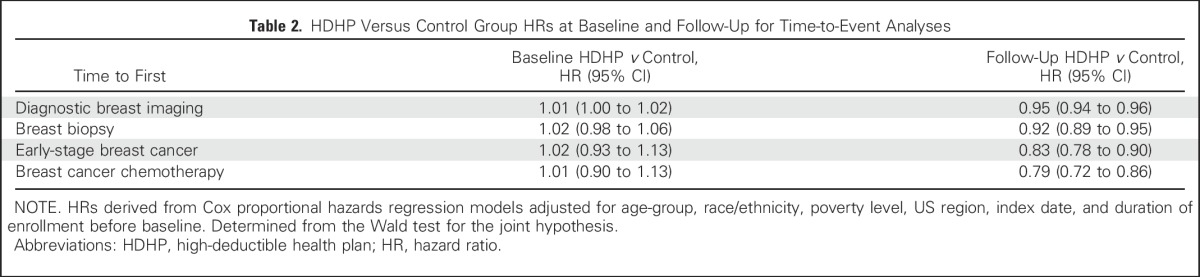

At baseline (before the index date), no evidence of delay in times to first breast diagnostic imaging, breast biopsy, incident early-stage breast cancer, and breast cancer chemotherapy initiation were found in the matched high-deductible group relative to the control group (Table 2; Fig 2). Over the follow-up period, women in HDHPs experienced delays in receipt of first observed breast diagnostic imaging (aHR, 0.95; 95% CI, 0.94 to 0.96), breast biopsy (aHR, 0.92; 95% CI, 0.89 to 0.95), incident early-stage breast cancer diagnosis (aHR, 0.83; 95% CI, 0.78 to 0.90), and breast cancer chemotherapy initiation (aHR, 0.79; 95% CI, 0.72 to 0.86) compared with control group members. The baseline aHR for time to first breast cancer screening was 1.00 (95% CI, 1.00 to 1.01; data not shown), and the follow-up period aHR was 0.97 (95% CI, 0.96 to 0.98).

Table 2.

HDHP Versus Control Group HRs at Baseline and Follow-Up for Time-to-Event Analyses

Fig 2.

Adjusted plots show the time to first breast cancer–related services in a population of women age 25 to 64 years at 12 months before and up to 48 months after a mandated high-deductible health plan (HDHP) switch compared with a contemporaneous control group that remained in low-deductible plans.

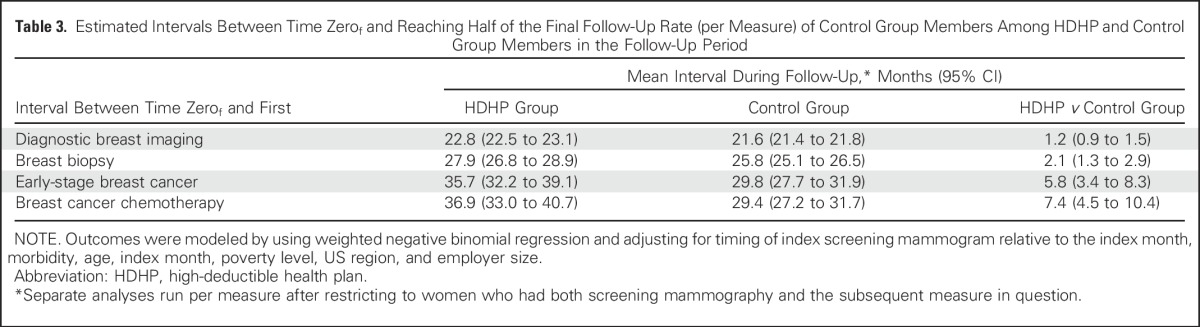

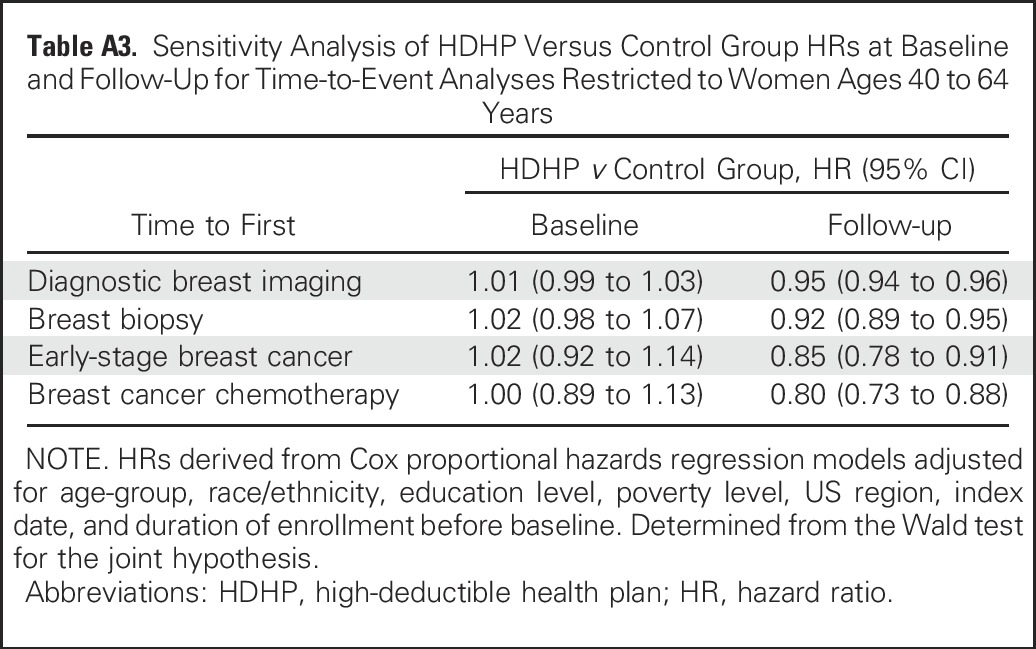

The estimated interval between time zerof and reaching half of the final follow-up breast diagnostic imaging rate of the control group was 22.8 months (95% CI, 22.5 to 23.1 months) among HDHP members and 21.6 months (95% CI, 21.4 to 21.8 months) among control group members for a relative high-deductible group delay of 1.2 months (95% CI, 0.9 to 1.5 months; Table 3). Corresponding delays in time to first breast biopsy, early-stage breast cancer diagnosis, and chemotherapy initiation were 2.1 months (95% CI, 1.3 to 2.9 months), 5.8 months (95% CI, 3.4 to 8.3 months), and 7.4 months (95% CI, 4.5 to 10.4 months), respectively, among HDHP members relative to control group members. Sensitivity analyses that restricted the population to women age 40 to 64 years or to women with at least 6 months follow-up after the index date (Appendix Tables A3 and A4, online only) demonstrated nearly identical effect estimates compared with the overall analyses.

Table 3.

Estimated Intervals Between Time Zerof and Reaching Half of the Final Follow-Up Rate (per Measure) of Control Group Members Among HDHP and Control Group Members in the Follow-Up Period

DISCUSSION

Women experienced delays in breast cancer diagnostic testing, early-stage diagnosis, and chemotherapy initiation after an employer-mandated switch to HDHPs. The findings imply that the high out-of-pocket obligations under HDHPs might be a barrier to timely receipt of essential breast cancer services. Women in HDHPs might either delay presenting for concerning symptoms or, if proceeding along the pathway from breast cancer screening to diagnostic testing to treatment, be hesitant to undergo subsequent (and generally more-expensive) care. In the current sample, it seems that small to moderate delays between earlier stages of care (ie, diagnostic imaging, biopsy, breast cancer diagnosis), including those we did not capture (eg, oncology visits), accumulated to a substantial delay from the point of HDHP enrollment to chemotherapy initiation.

The study cohorts began as generally healthy women without breast cancer, and we observed for progression along the path from breast cancer work-up to diagnosis and treatment. Thus, the majority of HDHP members would have faced sizeable financial barriers to obtaining the services we examined. The small subset of HDHP members who were ultimately diagnosed with breast cancer likely exceeded their deductible and, therefore, subsequently faced lower out-of-pocket burden until their deductibles reset in the next benefit year. Such lower cost sharing, in combination with fear of a life-threatening diagnosis, might lead to lessened delays among HDHPs from the point of breast cancer diagnosis to initiation of treatment (eg, surgery, radiotherapy, chemotherapy).

During follow-up, the high-deductible group compared with the control group experienced relative delays of 1.2, 2.1, 5.8, and 7.4 months in reaching comparable rates of diagnostic mammography, breast biopsy, early-stage breast cancer diagnosis, and chemotherapy initiation, respectively. Although these population-level delays cannot be directly translated to the person level, results suggest that HDHP members might experience adverse breast cancer outcomes. Small delays of 2 to 3 months between breast cancer diagnosis and surgery,11 surgery and adjuvant chemotherapy initiation,12 or lumpectomy and radiotherapy13 are associated with adverse outcomes. Women in HDHPs who undergo breast cancer work-ups might also experience anxiety related to their cost-sharing burden and delayed care,37-39 although the current study was not designed to assess such outcomes. Such delays could have other adverse effects on quality of life that should be addressed by subsequent studies of women in HDHPs.

Previous research has not addressed the effects of HDHPs on cancer diagnosis and treatment. Two studies investigated effects of high out-of-pocket costs on adherence to oral anticancer therapies and found an association between higher cost sharing and suboptimal medication use.9,10 The current study adds a comprehensive assessment of the effect of high cost sharing on key events along the pathway from breast cancer diagnostic testing to treatment, which demonstrates delays at all stages of care that might have adverse long-term effects. In addition, previous HDHP research generally has not examined expensive services, and no studies have addressed rare, life-threatening conditions, such as cancers that include major out-of-pocket expenses.

HDHP enrollment is expected to increase dramatically over the decade, and our findings raise concerns about the effects on patients who face expensive, potentially life-threatening diseases. In the short-term, providers and payers should identify, monitor, and educate HDHP members at risk for expensive cancer work-ups who might forgo needed care. In the longer term, policymakers, health insurers, and employers should consider designing or incentivizing health insurance benefits that facilitate transitions through key steps along the cancer care pathway. This could take the form of population-targeted exclusions of essential care (ie, low or no out-of-pocket obligations for certain services, such as diagnostic breast cancer testing).40,41 For example, value-based design features for cancer screening generally have been successful in maintaining rates among HDHP populations21,42-46 and are now mandated by the Affordable Care Act. Such cost-sharing exemptions could be applied across entire populations or more selectively41 if future research identifies key subgroups at risk for delayed cancer care under HDHPs.

Future studies should assess HDHP effects on cancer stage at diagnosis, adherence to oral cancer medications, survival, and breast cancer expenditures. Larger studies also should assess potentially at-risk HDHP subgroups, such as low-income and vulnerable minority patients, and effects of generously funded health savings accounts on outcomes.

This study has several limitations. Women were not randomly assigned to study groups, but we included only members who did not have a choice of a low- or high-deductible plan, which reduced selection bias. HDHP and control members possibly differed on unmeasured characteristics that influence the likelihood of breast cancer occurrence or aggressiveness, but this seems unlikely given the substantial balance between groups across multiple important baseline characteristics (Table 1). Similar to many long-term studies, attrition occurred over the study period, but our approach of matching on follow-up duration and adjusting time-to-event estimates should minimize the effects of differential attrition. We were unable to determine whether HDHP enrollment delayed care long enough to shift the stage of presentation from earlier to later stages because of the lack of validated algorithms to measure incident later-stage breast cancer. Because the events we studied are rare, the study was not powered to determine effects among key HDHP subgroups, such as low-income or vulnerable minority populations. We also were unable to analyze HDHP members with especially high deductibles (eg, ≥ $2,000) because of very low prevalence during our 2003 to 2012 study period.4 The results, therefore, do not necessarily generalize to women with such benefit arrangements. Given constraints of the data environment, we were unable to determine precise reasons for why women experienced delays in care. For example, delays could be related to general apprehension about facing high out-of-pocket costs and to women who put off care until they have exceeded their annual deductible level. Finally, the study does not represent state health insurance exchange members or people whose first exposure to insurance is under HDHPs.

In conclusion, women who were switched to HDHPs experienced delays in breast cancer diagnostic testing, early-stage diagnosis, and chemotherapy initiation. Such delays might lead to adverse long-term breast cancer outcomes. Policymakers, health insurers, and employers should consider designing or incentivizing health insurance benefits that facilitate transitions through key steps along the cancer care pathway. This could take the form of population-targeted exclusions of essential care41 so that women would pay minimal amounts for services such as breast diagnostic imaging and biopsy.

ACKNOWLEDGMENT

J.F.W. and F.Z. primarily analyzed the data. We thank Xin Xu, MS, for data management programming support; Jamie Wallace and Katherine Callaway, MS, for manuscript revision support; and Matthew Callahan, MS, for project management.

Appendix

Study Group Construction and Deductible Imputation Algorithm

To determine employer deductible levels, we used a benefits type variable that we had for most smaller employers (with approximately ≤ 100 employees). For larger employers, we took advantage of the fact that health insurance claims data are the most accurate source for assessing out-of-pocket obligations among patients who use health services. The claims data contained an in-network/out-of-network deductible payment field. For patients who use expensive or frequent services, the sum of their yearly deductible payments add up to clearly identifiable exact amounts, such as $500.00, $1,000.00, and $2,000.00. When even several members have these same amounts, it provides strong evidence that the employer offered such an annual deductible level. It is also possible to detect that employers offer choices of deductible levels when multiple employees have deductibles at two or more levels, such as 20 employees with an exact annual amount of $1,000.00 and 12 employees with $500.00. For employers with at least 10 workers, we therefore summed each member’s in-network deductible payments and number of claims over the enrollment year and assessed other key characteristics, such as percentage with health savings accounts. We randomly selected half of the employer data set that contained both our calculated employer characteristics (independent variables) and actual annual deductible levels from the benefits table (dependent variable, after categorization). We then used a logistic model that predicted the three-level outcome of deductible (≤ $500, $500 to $999, and > $1,000 [again, dependent variable]) on the basis of multiple aggregate employer characteristics (independent variables), such as the first and second most common whole-number deductible value; percentage with health savings accounts or health reimbursement arrangements; median deductible payment; percentage of employees who use services; employer size; and percentage of employees with summed annual deductible amounts (from claims data) between $100 and ≤ $500, > $500 and < $1,000, ≥ $1,000 and ≤ $2,500, and > $2,500. This predictive model output the probability that employers had deductibles in the three categories (which summed to 1), and we assigned the employer to the level that had the highest probability. If we detected employers that had ≥ 10 employees with whole-number deductible levels both > and < $500 (eg, $250.00 and $1,500.00), we assigned the employers’ category as choice. If 100% of employees had health savings accounts, we also overwrote any previous assignment to classify the employer as a high-deductible employer. We tested the predictive model on the other half of the sample for which we had actual deductible levels from the benefits table (Table A1). For employers with 75 to 100 enrollees, we found sensitivity and a specificity of > 96%. The sensitivity and specificity would be expected to be even higher for employers with > 100 enrollees (because more claims data would be available to provide evidence of deductible levels), but we were unable to test this because the data set for which we had actual deductibles included employers with generally ≤ 100 enrollees.

Rationale for Low- and High-Deductible Cutoff Values.

When health savings account–eligible high-deductible health plans (HDHPs) came to market in 2006, the Internal Revenue Service set the minimum deductible level for qualifying HDHPs at $1,050 (which could be adjusted upward for inflation annually). The range of this minimum deductible during our study period was $1,050 to $1,200. For these reasons, we defined HDHPs as annual individual deductibles of at least $1,000 (otherwise, health savings account plans would be excluded). In addition, this cutoff (eg, as opposed to $2,000) also improves the sensitivity and specificity of the imputation because this deductible level is common, and more enrollees per employer meet this threshold. This cutoff is also a real-world deductible minimum that allows the most generalizable results. We did not create a separate imputation algorithm for deductible levels of, for example, ≥ $2,000 because of concerns that a less-sensitive and -specific algorithm would lead to biased effect estimates and a smaller HDHP sample size. Note that $1,000 was the minimum annual deductible level, not the mean deductible level. We cannot calculate the mean deductible level of the HDHP group directly, but we would expect it to be in the range of approximately $1,500 to $2,000. We defined traditional plans as having deductible levels of ≤ $500 after determining that a threshold of ≤ $250 would lead to an inadequate sample size for the control group. Again, the mean deductible level of the control group members would be < $500.

After assigning deductible levels at the employer plan-year level, we began with 1,830,665 employer plan-years. We excluded 201,230 plan-years (11%) that included deductible levels other than only low or only high. Among the remaining 1,629,435 plan-years, we excluded 191,519 plan-years (12%) that did not have 2 years of continuous enrollment. Finally, from the remaining 1,437,916 employer plan-years, we excluded 549,638 plan-years (38%) that were not transitions of low deductible to low deductible or low deductible to high deductible. Most of these exclusions were a result of employers having high deductibles at their initial appearance in our data set and remaining with HDHPs.

Our HDHP group, therefore, comprised the enrollment years of employers that had a year-on-year transition from low- to high-deductible coverage (from ≤ $500 to ≥ $1,000). Some employers had multiple eligible index dates (eg, multiple low- to low-deductible years or both low- to low- and low- to high-deductible years). In these cases, we randomly assigned employers to the HDHP or control pool and then randomly selected one of their index dates (and their corresponding before-after enrollment years). We then identified women age 25 to 64 years and made further exclusions as described in the article.

Coarsened Exact Matching Approach

Coarsened exact matching helps to control for the confounding influence of baseline study group differences by reducing the imbalance on matching variables between the intervention (eg, HDHP) and control groups.1,2 We used a coarsened exact match11,12 on employer- and member-level propensity13,14 to join HDHPs; baseline annual out-of-pocket spending category (< $100, $100 to $999, $1,000 to $9,999, and ≥ $10,000); and whether at baseline members had a first observed breast diagnostic image, breast biopsy, early-stage breast cancer diagnosis, or breast cancer chemotherapy treatment. The logistic model for calculating employer propensity6-9 to join an HDHP predicted this likelihood on the basis of calendar index month (ie, anniversary month when employers and/or enrollees can change benefits each year); employer size (< 50, 50 to 99, 100 to 249, 250 to 499, ≥ 500 employees); percentage of women, members in income strata, education strata, age strata, race strata, and region strata; employer baseline cost level and trend; average employer ACG score; and outpatient copay. We constructed the corresponding member-level propensity model to ensure contemporaneous study groups as well as to balance key characteristics that had substantial prematch imbalance (high prematch standardized differences); thus, this model included age category, employer size category, US region, and calendar year of the index date. Evidence suggests that matching on baseline levels or trends of outcome measures in quasi-experimental studies closely approximates the effect estimates of randomized controlled trials.10 We therefore included the key outcomes of whether at baseline, members had a first-observed breast diagnostic image, breast biopsy, early-stage breast cancer diagnosis, or breast cancer chemotherapy treatment as binary measures per 4-month period. Our final group included 273,499 women in HDHPs and 2,424,868 matched control members.

Covariates

To derive proxy demographic measures, the data vendor linked members’ most recent residential street addresses to their 2000 US Census block group.19 Census-based measures of socioeconomic status have been validated17,18 and used in multiple studies to examine the effect of policy changes on disadvantaged populations.20-22

We classified members as from predominantly white, black, or Hispanic neighborhoods if they lived in a census block group (geocoding) with at least 75% of members of the respective race/ethnicity. We then applied a superseding ethnicity assignment if members had an Asian or Hispanic surname23 and classified remaining members as from mixed race/ethnicity neighborhoods. This validated approach of combining surname analysis and census data has positive and negative predictive values of approximately 80% and 90%, respectively.24

Table A1.

Validation of Deductible Imputation Algorithm

Table A2.

Codes Used to Create Breast Cancer Chemotherapy Measures

Table A3.

Sensitivity Analysis of HDHP Versus Control Group HRs at Baseline and Follow-Up for Time-to-Event Analyses Restricted to Women Ages 40 to 64 Years

Table A4.

Sensitivity Analysis of HDHP Versus Control Group HRs at Baseline and Follow-Up for Time-to-Event Analyses Restricted to Women With at Least 6 Months of Follow-Up Time

Footnotes

Supported by the National Cancer Institute and the Office of the Director, National Institutes of Health under Grant No. R01CA172639 (principal investigator J.F.W.).

Presented at the 8th Biennial Cancer Survivorship Research Conference, Washington, DC, June 16-18, 2016; AcademyHealth Annual Research Meeting, Boston, MA, June 26-28, 2016; Society of General Internal Medicine Annual Meeting, Washington, DC, April 19-22, 2017; and Cancer and Primary Care Research International Network, Edinburgh, UK, April 18-20, 2017.

AUTHOR CONTRIBUTIONS

Conception and design: J. Frank Wharam, Christine Y. Lu, Larissa Nekhlyudov, Stephen B. Soumerai, Dennis Ross-Degnan

Collection and assembly of data: J. Frank Wharam, Dennis Ross-Degnan

Data analysis and interpretation: All authors

Manuscript writing: All authors

Final approval of manuscript: All authors

Accountable for all aspects of the work: All authors

AUTHORS' DISCLOSURES OF POTENTIAL CONFLICTS OF INTEREST

Breast Cancer Diagnosis and Treatment After High-Deductible Insurance Enrollment

The following represents disclosure information provided by authors of this manuscript. All relationships are considered compensated. Relationships are self-held unless noted. I = Immediate Family Member, Inst = My Institution. Relationships may not relate to the subject matter of this manuscript. For more information about ASCO's conflict of interest policy, please refer to www.asco.org/rwc or ascopubs.org/jco/site/ifc.

J. Frank Wharam

No relationship to disclose

Fang Zhang

No relationship to disclose

Christine Y. Lu

No relationship to disclose

Anita K. Wagner

Patents, Royalties, Other Intellectual Property: Tufts New England Medical Center, held license with Johnson & Johnson

Larissa Nekhlyudov

Honoraria: Pri-Med, UpToDate

Travel, Accommodations, Expenses: Pri-Med

Craig C. Earle

Patents, Royalties, Other Intellectual Property: UpToDate

Stephen B. Soumerai

No relationship to disclose

Dennis Ross-Degnan

Consulting or Advisory Role: Quintiles IMS Holdings

REFERENCES

- 1. American Cancer Society: Breast Cancer Facts & Figures 2015-2016, 2016 http://www.cancer.org/acs/groups/content/@research/documents/document/acspc-046381.pdf.

- 2. National Comprehensive Cancer Network: Breast Cancer Screening and Diagnosis: NCCN Clinical Practice Guidelines in Oncology, 2015. http://www.nccn.org/professionals/physician_gls/pdf/breast-screening.pdf.

- 3. National Comprehensive Cancer Network: Breast Cancer. NCCN Clinical Practice Guidelines in Oncology, 2015. http://www.nccn.org/professionals/physician_gls/pdf/breast.pdf.

- 4. The Henry J. Kaiser Family Foundation: 2016 Employer Health Benefits Survey. http://kff.org/health-costs/report/2016-employer-health-benefits-survey.

- 5.Finkelstein EA, Tangka FK, Trogdon JG, et al. : The personal financial burden of cancer for the working-aged population. Am J Manag Care 15:801-806, 2009 [PubMed] [Google Scholar]

- 6.Davidoff AJ, Erten M, Shaffer T, et al. : Out-of-pocket health care expenditure burden for Medicare beneficiaries with cancer. Cancer 119:1257-1265, 2013 [DOI] [PubMed] [Google Scholar]

- 7.Ubel PA, Abernethy AP, Zafar SY: Full disclosure—out-of-pocket costs as side effects. N Engl J Med 369:1484-1486, 2013 [DOI] [PubMed] [Google Scholar]

- 8.Zafar SY: Financial toxicity of cancer care: It’s time to intervene. J Natl Cancer Inst 108:djv370, 2015 [DOI] [PubMed] [Google Scholar]

- 9.Neugut AI, Subar M, Wilde ET, et al. : Association between prescription co-payment amount and compliance with adjuvant hormonal therapy in women with early-stage breast cancer. J Clin Oncol 29:2534-2542, 2011 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10.Dusetzina SB, Winn AN, Abel GA, et al. : Cost sharing and adherence to tyrosine kinase inhibitors for patients with chronic myeloid leukemia. J Clin Oncol 32:306-311, 2014 [DOI] [PubMed] [Google Scholar]

- 11.Bleicher RJ, Ruth K, Sigurdson ER, et al. : Time to surgery and breast cancer survival in the United States. JAMA Oncol 2:330-339, 2016 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12.Gagliato DM, Gonzalez-Angulo AM, Lei X, et al. : Clinical impact of delaying initiation of adjuvant chemotherapy in patients with breast cancer. J Clin Oncol 32:735-744, 2014 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Punglia RS, Saito AM, Neville BA, et al. : Impact of interval from breast conserving surgery to radiotherapy on local recurrence in older women with breast cancer: Retrospective cohort analysis. BMJ 340:c845, 2010 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 14.Miller AC: Breast abscesses and masses, 2017. https://emedicine.medscape.com/article/781116-overview

- 15.Foxcroft LM, Evans EB, Porter AJ: The diagnosis of breast cancer in women younger than 40. Breast 13:297-306, 2004 [DOI] [PubMed] [Google Scholar]

- 16. Yang D, Dalton JE: A unified approach to measuring the effect size between two groups using SAS®. https://www.lerner.ccf.org/qhs/software/lib/stddiff.pdf.

- 17.Iacus SM, King G, Porro G: Multivariate matching methods that are monotonic imbalance bounding. J Am Stat Assoc 106:345-361, 2011 [Google Scholar]

- 18. Iacus SM, King G, Porro G: Causal inference without balance checking: Coarsened exact matching. Polit Anal, 20:1-24, 2011. [Google Scholar]

- 19. Iacus S, King G, Porro G: CEM: Coarsened exact matching software. https://gking.harvard.edu/cem.

- 20.Schreyögg J, Stargardt T, Tiemann O: Costs and quality of hospitals in different health care systems: A multi-level approach with propensity score matching. Health Econ 20:85-100, 2011 [DOI] [PubMed] [Google Scholar]

- 21.Wharam JF, Zhang F, Landon BE, et al. : Colorectal cancer screening in a nationwide high-deductible health plan before and after the Affordable Care Act. Med Care 54:466-473, 2016 [DOI] [PubMed] [Google Scholar]

- 22.Stout NK, Nekhlyudov L, Li L, et al. : Rapid increase in breast magnetic resonance imaging use: Trends from 2000 to 2011. JAMA Intern Med 174:114-121, 2014 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23.Nattinger AB, Laud PW, Bajorunaite R, et al. : An algorithm for the use of Medicare claims data to identify women with incident breast cancer. Health Serv Res 39:1733-1749, 2004 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 24. doi: 10.1097/MLR.0b013e3182a303d7. Fenton JJ, Onega T, Zhu W, et al: Validation of a Medicare claims-based algorithm for identifying breast cancers detected at screening mammography. Med Care, 54:e15-e22, 2016. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 25.Solin LJ, MacPherson S, Schultz DJ, et al. : Evaluation of an algorithm to identify women with carcinoma of the breast. J Med Syst 21:189-199, 1997 [DOI] [PubMed] [Google Scholar]

- 26. National Comprehensive Cancer Network: Breast Cancer. NCCN Clinical Practice Guidelines (NCCN Guidelines), Version 2.2017, 2017. https://www.nccn.org/professionals/physician_gls/pdf/breast.pdf.

- 27. National Cancer Institute Division of Cancer Control & Population Sciences: Procedure Codes for SEER-Medicare Analyses. https://healthcaredelivery.cancer.gov/seermedicare/considerations/procedure_codes.html.

- 28. National Cancer Institute: Breast Cancer Treatment (PDQ®)–Health Professional Version. https://www.cancer.gov/types/breast/hp/breast-treatment-pdq#section/all.

- 29.Krieger N: Overcoming the absence of socioeconomic data in medical records: Validation and application of a census-based methodology. Am J Public Health 82:703-710, 1992 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 30.Krieger N, Chen JT, Waterman PD, et al. : Race/ethnicity, gender, and monitoring socioeconomic gradients in health: A comparison of area-based socioeconomic measures—the public health disparities geocoding project. Am J Public Health 93:1655-1671, 2003 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31.US Bureau of the Census Geographical Areas Reference Manual. Washington, DC, US Bureau of the Census, 1994 [Google Scholar]

- 32.The Johns Hopkins ACG Case-Mix System Reference Manual, Version 7.0. Baltimore, MD, The Johns Hopkins University, 2005 [Google Scholar]

- 33.Reid RJ, Roos NP, MacWilliam L, et al. : Assessing population health care need using a claims-based ACG morbidity measure: A validation analysis in the Province of Manitoba. Health Serv Res 37:1345-1364, 2002 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 34.Ethnic Technologies : http://www.ethnictechnologies.com/product/e-tech/

- 35.Fiscella K, Fremont AM: Use of geocoding and surname analysis to estimate race and ethnicity. Health Serv Res 41:1482-1500, 2006 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 36.Kalbfleisch JD, Prentice RL: The Statistical Analysis of Failure Time Data (ed 2). Hoboken, NJ, Wiley, 2002 [Google Scholar]

- 37.Fentiman IS: Pensive women, painful vigils: Consequences of delay in assessment of mammographic abnormalities. Lancet 331:1041-1042, 1988 [DOI] [PubMed] [Google Scholar]

- 38.Ellman R, Angeli N, Christians A, et al. : Psychiatric morbidity associated with screening for breast cancer. Br J Cancer 60:781-784, 1989 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 39.Brett J, Austoker J, Ong G: Do women who undergo further investigation for breast screening suffer adverse psychological consequences? A multi-centre follow-up study comparing different breast screening result groups five months after their last breast screening appointment. J Public Health Med 20:396-403, 1998 [DOI] [PubMed] [Google Scholar]

- 40.Fendrick AM, Chernew ME: Value-based insurance design: A “clinically sensitive” approach to preserve quality of care and contain costs. Am J Manag Care 12:18-20, 2006 [PubMed] [Google Scholar]

- 41.Wharam JF, Ross-Degnan D, Rosenthal MB: The ACA and high-deductible insurance—strategies for sharpening a blunt instrument. N Engl J Med 369:1481-1484, 2013 [DOI] [PubMed] [Google Scholar]

- 42.Rowe JW, Brown-Stevenson T, Downey RL, et al. : The effect of consumer-directed health plans on the use of preventive and chronic illness services. Health Aff (Millwood) 27:113-120, 2008 [DOI] [PubMed] [Google Scholar]

- 43.Busch SH, Barry CL, Vegso SJ, et al. : Effects of a cost-sharing exemption on use of preventive services at one large employer. Health Aff (Millwood) 25:1529-1536, 2006 [DOI] [PubMed] [Google Scholar]

- 44.Wharam JF, Galbraith AA, Kleinman KP, et al. : Cancer screening before and after switching to a high-deductible health plan. Ann Intern Med 148:647-655, 2008 [DOI] [PubMed] [Google Scholar]

- 45.Wharam JF, Graves AJ, Zhang F, et al. : Two-year trends in cancer screening among low socioeconomic status women in an HMO-based high-deductible health plan. J Gen Intern Med 27:1112-1119, 2012 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 46.Beeuwkes Buntin M, Haviland AM, McDevitt R, et al. : Healthcare spending and preventive care in high-deductible and consumer-directed health plans. Am J Manag Care 17:222-230, 2011 [PubMed] [Google Scholar]