Abstract

The Open Payments Program (OPP) was recently implemented to publicly disclose industry payments to physicians, with the goal of enabling patient awareness of potential conflicts-of-interests. Awareness of OPP, its data, and its implications for transplantation are critical. We used the first wave of OPP data to describe industry payments made to transplant surgeons. Transplant surgeons (N=297) received a total of $759,654. The median (IQR) payment to a transplant surgeon was $125 ($39–1018), and the highest payment to an individual surgeon was $83,520; 122 surgeons received <$100, and 17 received >$10,000. A higher h-index was associated with 30% higher chance of receiving >$1000 (RR/10 unit h-index increase= 1.181.301.44, p<0.001). The highest payment category was consulting fees, with a total of $314,448 paid in this reported category. Recipients of consulting fees had higher h-indices, median (IQR) of 20 (10–35) vs. 9 (3–17) (p<0.001). Ten of 122 companies accounted for 62% of all payments. Kidney transplant (KT) and liver transplant (LT) centers that received >$1,000 had higher center volumes (p<0.001). LT centers that received payments of >$1,000 had a higher percentage of private-insurance/self-pay patients (p<0.01). Continued surveillance of industry payments may further elucidate the relationship between industry payments and physician practices.

INTRODUCTION

The Open Payments Program (OPP), also known as the Physician Payment Sunshine Act, was implemented by the Centers for Medicare and Medicaid Services (CMS) to create transparency regarding the financial relationships between physicians and the biomedical industry. Manufacturers of drugs, medical devices and supplies have been mandated to submit their payment records and any “transfers of value” (greater than $10) paid to physicians to the CMS. The data from August 1, 2013 to December 31, 2013 were made available to the general public on September 30, 2014, and moving forward, will be publicized annually (1). The stated rationale is to allow patients to identify potential conflicts-of-interest, and to enable them to make more informed decisions when choosing a health care provider (2). Recognizing the importance of industry support for research, CMS has designated separate databases for disclosing research funding and non-research payments (3). Research funding is a different domain of potential industry influence on physician behavior, and the majority of public concern is in direct payments and gifts to individual physicians (4, 5).

Patients believe that industry relationships influence physician behavior and should be disclosed (5). However, national statistics have never been reported, and reports to date have been disputed by both physicians and industry. In 2007, a national survey documented that 94% of U.S. physicians reported some form of relationship with industry (6). Data from market research companies in 2004, reported that U.S. pharmaceutical companies spent $57.5 billion, or 24.4% of their revenue, on product promotion (7). The OPP represents the first nationwide report of financial relationships that have been confirmed by both industry and physician. The data were reported directly by industry and, prior to the data release, health care providers were given the opportunity to dispute a reported payment.

In solid organ transplantation, the pharmaceutical industry has played a significant role in improving patient outcomes, particularly through the development of novel immunosuppression agents and the subsequent funding of large multicenter randomized trials (8–12). Given the central role of our field in organ donation, both deceased and live, the success of transplantation dependents almost entirely on public trust, altruism and good will. The financial relationships between industry and our field, other than research payments, both perceived and documented, could substantially affect this public trust. However, the specifics of these financial relationships, while postulated in the media, have never been formally studied at a national level.

To better understand the relationship between industry and transplantation, the goals of this study of the first wave of non-research OPP data were to: 1) characterize the distribution of industry payments to transplant surgeons; 2) examine whether industry payments were associated with a transplant center’s operative volume and insurance case-mix; and 3) evaluate whether industry payments were associated with a transplant surgeon’s academic contribution, quantified by the h-index.

METHODS

Study Population

All physicians who reported themselves as “Transplant Surgeons” to the OPP were included in the study population (N=176). In addition, we included surgeons who self-reported in the following categories and were also members of the American Society of Transplant Surgeons (ASTS), as matched by last name, first name, and zip code when necessary (N=121): Surgery, Urology, Pediatric Urology, and Pediatric Surgery. A total of 297 individuals identified as transplant surgeons in the OPP dataset were included in the study.

Data Sources and Linkages

Payments made to transplant surgeons between August 1, 2013 and December 31, 2013 were obtained from the OPP datasets available on the CMS website (http://www.cms.gov/openpayments) and accessed on September 30, 2014. Physician-level payments were aggregated using the unique physician identification number. In the data published by the OPP, zip codes were identified from each transplant surgeon’s postal address. Using their zip codes, surgeons were linked at a state level. A surgeons’ transplant center affiliation was determined by linking them to the transplant center’s zip code. Transplant center zip codes were ascertained using data from the Scientific Registry of Transplant Recipients (SRTR). Where zip codes were not linkable, they were linked by the institution they reported in ASTS. Non-unique matches were resolved through internet search. 100% of the surgeons were successfully linked by state.

Transplant center operative volume and insurance case mix from January 1, 2012 to December 31, 2013 was obtained from SRTR data. The SRTR data system includes data on all donor, wait-listed candidates, and transplant recipients in the US, submitted by the members of the Organ Procurement and Transplantation Network (OPTN), and has been described elsewhere (13). The Health Resources and Services Administration (HRSA), U.S. Department of Health and Human Services provides oversight to the activities of the OPTN and SRTR contractors. Center level characteristics were explored separately for kidney transplants (KT), liver transplants (LT), as well as the combination of KT and LT. When studying either KT or LT, only data from centers that performed that specific organ transplant were included.

Payments Made to All Health Care Providers and Transplant Surgeons

The OPP data were used to ascertain the total amount of payments made by industry to all Health Care Providers (HCP). HCP consisted of physicians, dentists, podiatrist and nurse practitioners. This was then compared to the total amount of payments made to transplant surgeons.

Distributions of Payments made to Transplant Surgeons

The total amount that each transplant surgeon received was studied and presented as a box and whiskers plot. The amount received was also categorized as follows: less than $100, $100-$999, $1,000-$9,999, and greater than $10,000 and presented as bar graphs. All companies and the amount of payments they made to transplant surgeons were identified (Appendix 1). Payments of the ten highest paying companies and their distribution by categories were shown. Heat maps were used to show the geographic distribution of industry payments collectively by state, as well as the average payments per transplant surgeon in each state.

Payments Categories

OPP payments were reported under the following categories: consulting fees; food and beverage; honoraria; education; travel and lodging; entertainment; gifts; services other than consulting, including serving as faculty or as a speaker at a venue other than a continuing education program (abbreviated as ‘speaker non-CEP’); and serving as faculty or as a speaker for a non-accredited and non-certified, continuing education program (abbreviated as ‘speaker CEP’). The number of transplant surgeons that received payments for each payment category was quantified.

Distribution of Payments by Transplant Center Characteristics

Transplant surgeons were linked to their affiliated transplant centers. 96% of transplant surgeons were successfully linked to 126 transplant centers. The sum of all payments made by industry to individual transplant surgeons at their affiliated center was calculated; these were described as center-payments, but the term center-payment does not mean industry payments made directly to a transplant center. Center-payments were then divided into payment categories of less than $1,000 or $1,000 or more. Based on these center-payment categories, we explored whether center-payments were associated with center volume or insurance case mix. Centers were further differentiated based upon the transplant organ of interest: KT, LT, and collectively for both KT and LT.

Payments Based on Transplant Surgeons’ h-index

To explore if transplant surgeons’ academic productivity was associated with the amount of payments that they received, we ascertained each individual transplant surgeon’s h-index from Scopus as of October 20, 2014. Initially introduced by Hirsh in 2005, the h-index is calculated by determining the number of papers, h, from a researcher with citation counts of h or greater for each paper (14). H-indices were identified for 261 (88%) surgeons. We calculated the total number of payments received by each physician and modeled the relative risk of a physician’s receiving $1,000 or more in total payments using Poisson regression with a robust variance estimator (15). We studied the association between h-index and receipt of payments in each category.

Statistical Analysis

Analyses were performed with R 3.1.1 (the R Foundation for Statistical Computing, Vienna, Austria). For all analyses, p < 0.05 was considered statistically significant. To compare center volumes and insurance case mix, we used the Wilcoxon rank sum test. 95% confidence intervals are reported as per the methods of Louis and Zeger (16).

RESULTS

Payments Made to All Physicians

During this first OPP reporting period, industry made payments totaling $508,215,270 to 359,402 HCPs. Total payments per HCP were: median (IQR) of $95 ($29–258) and a mean of $1,414; the top 5 received $7,356,000, $3,994,022, $3,921,410, $3,849,711 and $2,413,281 during the 5 month OPP study period.

Payments to Transplant Surgeons

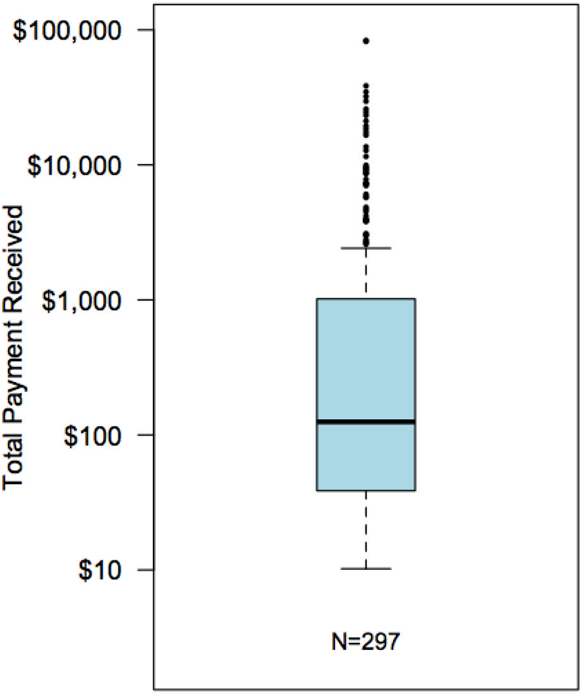

Transplant surgeons received a total of $759,654, or 0.15% of total payments made to all providers. Individual transplant surgeons received payments from one (59%), two (19%), three (11%), or greater than three (15%) companies. The largest number of companies from which a single transplant surgeon received payments was 17. Total payments per transplant surgeon had a median (IQR) of $125 ($39–1,018) and a mean of $2,558; the 5 highest transplant surgeons received $83,520, $38,484, $34,744, $32,100, and $29,603 (Figure 1A). Of transplant surgeons who received industry payments, 41% received payments below $100, 33% received payments between $100 and $999, 20% received payments between $1,000 and $9,999, and 6% received payments in excess of $10,000 (Figure 1B).

Figure 1A: Distribution of Payments Received by Transplant Surgeons from Industry.

Transplant surgeons received a total of $759,654, payments per transplant surgeon were of a median (IQR) of $125 ($39–1018) and a mean of $2,558; the 5 highest transplant surgeons received $83,520, $38,484, $34,744, $32,100, and $29,603. Data are shown on a log scale.

Figure 1B: Payments Received per Transplant Surgeon by Amount Category.

Of the 297 transplant surgeons were reported to OPP, 122 (41%) received payments below $100; 99 (33%) received payments between $100 and $999; 59 (20%) received payments between $1,000 and $9,999, and 17 (6%) received payments greater than $10,000.

Payments Categories

The $759,654 total payments made to transplant surgeons were categorized by the OPP as follows: $314,448 (41%) for consulting fees; $131,641 (17%) for travel and lodging; $118,264 (15%) for speaker non-CEP; $54,995 (7%) for food and beverage; $53,124 (7%) for speaker CEP; $38,400 (5%) for honoraria; $33,776 (4%) for education; $216 (<0.5%) for entertainment; and $94 (<0.5%) for gifts (Table 1).

Table 1: Industry Payments by Category.

This table describes the amount paid to all transplant surgeons by payment category, the median (IQR) of individual payments, the number of surgeons that received payments in each category, the h-indices median (IQR) of surgeons that were paid versus not paid in that particular category. The last column compares the h-indices of paid versus unpaid transplant surgeon. H-indices were higher among transplant surgeons who were paid for: consulting, travel and lodging, and food and speaker-CEP.

|

Payment Category |

Total Payment (%) |

Median (IQR) of Payments |

Number of Surgeons Paid (%) |

H-index of Paid Surgeons |

H-index of un-paid Surgeons |

H-index paid vs. unpaid p-value |

|---|---|---|---|---|---|---|

| Consulting | $314,448 (41%) | $2,000 ($1,500-$3,563) | 36 (12%) | 20 (10–35) | 9 (3–17) | < 0.001 |

| Travel & lodging | $131,641 (17%) | $222 ($79-$470) | 24 (23%) | 15 (7–33) | 8 (3–17) | < 0.001 |

| Speaker non-CEP | $118,264 (15%) | $562 ($36-$2075) | 27(9%) | 12 (5–26) | 9 (3–19) | 0.28 |

| Food & beverage | $54,995 (7%) | $24 ($13-$88) | 269(90%) | 9 (3–18) | 15.0 (6–23) | 0.2 |

| Speaker-CEP | $53,124 (7%) | $2,500 ($1,500-$2500) | 11 (4%) | 25 (11–36) | 9 (3–18) | 0.02 |

| Honorarium | $38,400 (5%) | $2,000 ($2,000-$2,400) | 7 (2%) | 20 (6–32) | 10 (3–19) | 0.28 |

| Education | $33,776 (4%) | $85 ($24-$750) | 40 (13%) | 8 (3– 20) | 10 (3–20) | 0.69 |

| Entertainment | $216 (<0.5%) | $68 ($39-$103) | 3 (0.1%) | 15 (12–24) | 10 (3–20) | 0.30 |

| Gifts | $94 (<0.5%) | $28 ($23-$28) | 3 (0.1%) | 2 (1–3) | 10 (4–20) | 0.13 |

The median (IQR) for each payment and the percentage of transplant surgeons paid by expense category were: consulting fees $2,000 ($1,500-$3,563) to 12% (N=36); travel and lodging $222 ($79-$470) to 23% (N=24); speaker non-CEP $562 ($36-$2075) to 9% (N=27); food and beverage $24 ($13-$88) to 90% (N=269); speaker CEP $2,500 ($1,500-$2500) to 4% (N=11); honoraria $2,000 ($2,000-$2,400) to 2% (N=7); education $85 ($24-$750) to 13% (N=40); entertainment $68 ($39-$103) to 0.1% (N=3); and gifts $28 ($23-$28) to 0.1% (N=3, Table 1).

Distributions of Payments made by Companies

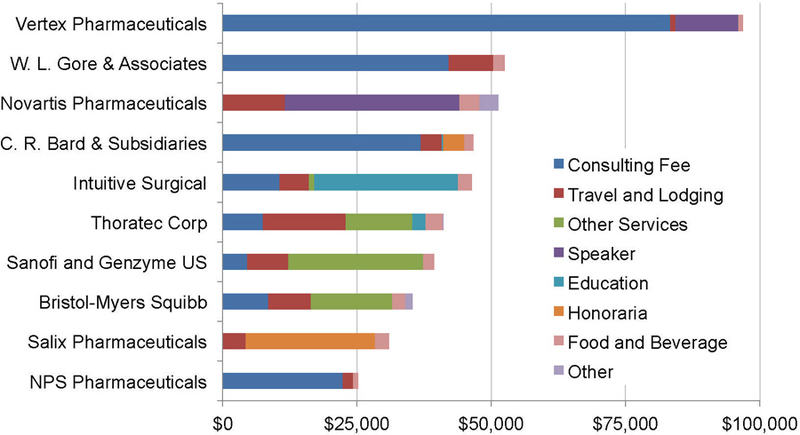

The average total payment made by a single company was $6227 (ranging from $3.47-$96,864). Of 122 companies that made payments to transplant surgeons (Appendix 1), the 10 highest paying companies accounted for $465,585 (62%) of the total payments. The distribution of payments by category from these 10 companies is shown in Figure 2.

Figure 2: Category Payments of the Top 10 Companies.

These are the 10 companies that were identified to have the highest total amount payments made to transplant surgeons.

Geographic Distribution

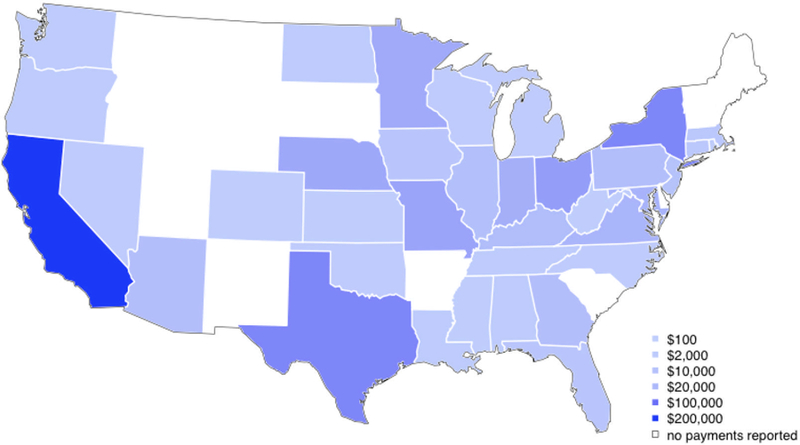

In terms of total payments to transplant surgeons in a given state, the highest 5 states were California ($213,122), Texas ($76,033), New York ($75,150), Ohio ($49,427), and Missouri ($42,685), and the 5 lowest states (Delaware, West Virginia, Kansas, Rhode Island, and Colorado) had total payments ranging from $13 to $151. In terms of average payment-per-surgeon, the highest 5 states were Nebraska ($9,555/surgeon), California ($7,349/surgeon), Missouri ($6,098/surgeon), Indiana ($5,221/surgeon), and DC ($5,008/surgeon) and the lowest 5 states (Delaware, West Virginia, Kansas, Colorado, and North Carolina) had per-surgeon average payments ranging from $13–107 (Figures 3A and 3B).

Figure 3A: Total Payments made to Transplant Surgeons by State.

In terms of total payments to all providers in a given state, the highest 5 states were California with $213,122, Texas with $76,033, New York with $75,150, Ohio with $49,427, and Missouri with $42,685.

Figure 3B: Average Payments/Surgeon by State.

In terms of payment-per-surgeon, the highest 5 states were Nebraska $9,555/surgeon, California $7,349/surgeon, Missouri $6,098/surgeon, Indiana $5,221/surgeon, and DC $5,008/surgeon.

Payments by Affiliated Transplant Center

In terms of the sum of payments to surgeons at a given transplant center, the 6 highest paid transplant centers accounted for a total $375,078 (49%) of the total payments, with amounts of $189,313, $45,861, $38,268, $35,838, $33,550, and $32,248. Surgeons at the remaining centers (N=121) received payments with a median of $614 per center (IQR $94 - $2259). The 5 transplant centers with the lowest industry payments ranged from $11 to $14.

In terms of average payment-per-surgeon, the highest 5 centers had $27,045/surgeon, $19,134/surgeon, $16,593/surgeon, $16,124/surgeon, and $13,624/surgeon, and the lowest 5 centers had per-surgeon average payments ranging from $11 to $14.

Payments by Transplant Center Volume

For all transplants centers (combining KT and LT) the median (IQR) transplant volume was 34 (14–64) at centers that received no center-payments, 66 (35–138) at centers that received center-payments totaling less than $1000, and 130 (61–279) at centers that received center-payments of $1,000 or more. The difference in volume between centers receiving payments of less than $1,000 versus centers receiving no payments was statistically significant (p<0.001), as was the difference between centers receiving payments of $1,000 or more versus centers receiving no payments (p<0.001). The median (IQR) KT volume was 29 (11–57) at centers that received no center-payments, 64 (35–106) at centers that received center-payments totaling less than $1000, and 74 (50–173) at centers that received center-payments of $1,000 or more. The difference in KT volumes between centers receiving payments of less than $1,000 versus centers receiving no payments was statistically significant (p<0.001), as was the difference between centers receiving payments of $1,000 or more versus centers receiving no payments (p<0.001). The median (IQR) LT volume was 23 (10–48) at centers that received no center-payments, 29 (10–63) at centers which received center-payments totaling less than $1000, and 59 (30–96) at centers which received center-payments of $1,000 or more. The difference in volume between LT centers receiving payments of less than $1,000 versus centers receiving no payments was not statistically significant (p=0.07); however, the difference between centers receiving payments of $1,000 or more versus centers receiving no payments was statistically significant (p<0.001, Table 2).

Table 2: Industry Payments and Transplant Centers that Performed Kidney or Liver Transplants.

This table shows center volumes and center insurance case mix compared to transplant centers affiliated with transplant surgeons that received no industry payments. The Wilcoxon rank sum test was used to compare centers that received payments of less than $1,000 versus no payments, and centers with payments of $1000 or more to centers that received no center-payments.

| No Industry Payment $0 |

Industry Payments <$1000 |

Industry Payments >=$1000 |

p-value ($0 vs <$1,000) |

p-value ($0 vs $1000+) |

|

|---|---|---|---|---|---|

| All Centers that Performed Liver or Kidney Transplants | |||||

| Number of centers | 116 | 73 | 53 | ||

| Med (IQR) volume | 34 (14–64) | 66 (35–138) | 130 (61–279) | <0.001 | <0.001 |

| % private insurance | 36% (24%-43%) | 35% (25%-45%) | 43% (39%-49%) | 0.52 | <0.001 |

|

Centers that Perform Kidney Transplants | |||||

| Number of centers | 115 | 67 | 53 | ||

| Med (IQR) volume | 29 (11–57) | 64 (32–106) | 74 (50–173) | <0.001 | <0.001 |

| % private insurance | 33% (25%-42%) | 31% (22%-38%) | 38% (27%-43%) | 0.34 | 0.22 |

|

Centers that Perform Liver Transplants | |||||

| Number of centers | 48 | 44 | 44 | ||

| Med (IQR) volume | 23 (10–48) | 29 (19–63) | 59 (30–96) | 0.072 | <0.001 |

| % private insurance | 46% (39%-57%) | 53% (44%-60%) | 56% (48%-64%) | 0.127 | 0.01 |

Payments by Insurance Case mix

For all transplants centers (combining KT and LT) the median (IQR) percentage of private insurance/self-pay transplant recipients was 36% (24%−43%) at centers which received no center-payments, 35% (25%−45%) at centers which received center-payments totaling less than $1000, and 43% (39%−49%) at centers which received center-payments of $1,000 or more. The difference in the percentage of private insurance/self-pay patients between centers receiving payments of less than $1,000 versus centers receiving no payments was not statistically significant (p=0.52), however, the difference between centers receiving payments of $1,000 or more versus centers receiving no payments was statistically significant (p<0.001). For KT, the median (IQR) percentage of private insurance/self-pay recipients was 33% (25%−42%) at centers that received no center-payments, 31% (22%−38%) at centers which received center-payments totaling less than $1000, and 38% (27%−43%) at centers which received center-payments of $1,000 or more. The difference in the percentage private insurance/self-pay recipients at KT centers between centers receiving payments of less than $1,000 versus centers receiving no payments was statistically significant (p=0.34), as was the difference between centers receiving payments of $1,000 or more versus centers receiving no payments (p=0.22). For LT, the median (IQR) percentage of private insurance/self-pay was 46% (39%−57%) at centers which received no center-payments, 53% (44%−60%) at centers which received center-payments totaling less than $1000, and 56% (48%−64%) at centers which received center-payments of $1000 or more. The difference in the percentage of private insurance/self-pay patients at LT centers between centers receiving payments of less than $1,000 vs. centers receiving no payments was not statistically significant (p=0.13); however, the difference between centers receiving payments of $1,000 or more vs. centers receiving no payments was statistically significant (p=0.01, Table 2).

Non-Research Payments by H-index

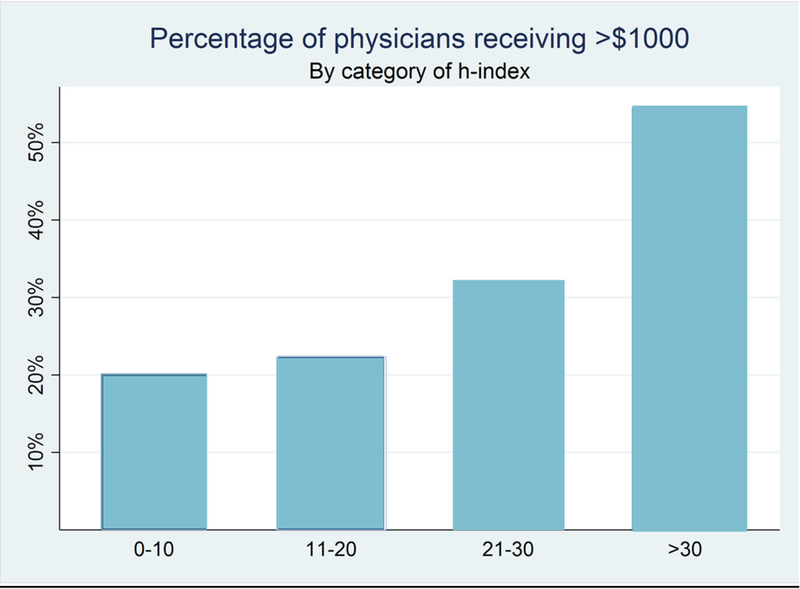

The Median (IQR) of h-indices among the 261 transplant surgeons was 10 (3–20). Those paid for consulting had a median (IQR) H-index of 20 (10–35) while those not paid for consulting, but who received payments for under other categories had an h-index of 9 (3–17, p<0.001); similar differences were seen only for the categories of travel and lodging (15 [7–33] versus 9 [3–17], p<0.001) and speaking CEP (25 [11–36] versus 9 [3–18], p=0.02, Table 1). Of the 261 transplant surgeons, 69 (26.4%) received total payments of $1,000 or more. Median (IQR) h-index for transplant surgeons receiving $1,000 or more was 15 (6–32), compared to 9 (3–16) for transplant surgeons receiving less than $1,000. An increase of ten units of h-index was associated with 30% higher chance of a physician’s receiving at least $1000 in total payments (RR=1.18 1.301.44, p<0.001, Figure 4). In other words, a transplant surgeon with an h-index of 17 had a 30% higher chance of receiving at least $1,000 compared to a transplant surgeon with an h-index of 7.

Figure 4: Association of Payments made to Transplant Surgeons and their h-index.

The Median (IQR) h-index among the 261 physicians whose h-index we obtained was 10 (3–20). Of these, 69 (26.4%) received total payments of at least $1000. An increase of ten units of h-index was associated with 30% higher chance of a physician’s receiving at least $1000 in total payments (RR=1.18 1.30 1.44, p<0.001)

DISCUSSION

Before the implementation of the Sunshine Act, there was much debate and speculation about the potential implications and patient perceptions of the forthcoming OPP data (1, 2, 17, 18). In this national study, we used the newly available OPP data to describe how industry paid $759,654 directly to 297 transplant surgeons. Of all surgeons, 41% received less than $100, and 6% received $10,000 or more. The highest payment to an individual surgeon was $83,520. The median payment of $125 to a transplant surgeon was within the range compared to other medical specialties in the OPP: $102 to dermatologists; $88 to neurosurgeons; and $173 to urologists (18). Centers at which transplant surgeons received $1,000 or more had higher transplant volumes (median 130 versus median 34, p<0.001). An increase of ten units of h-index was associated with 30% higher chance of a transplant surgeons receiving at least $1000 in total payments (RR=1.18 1.301.44, p<0.001).

Collaboration between physician scientists and the pharmaceutical industry has significantly improved immunosuppressive therapies and improved outcomes in transplant recipients (8–12). To quantify a transplant surgeon’s scientific contributions, we used their h-index. The h-index has been well accepted and used by other specialties to study academic productivity. A greater H-index has been associated with a higher academic rank among US academic programs in various surgical specialties (14, 19). The analysis of transplant surgeons showed that greater academic productivity was associated with higher industry payments, suggesting that the pharmaceutical industry tends to seek scientific leaders in the field for consulting and speaking. One would hope that the research findings of scientific leaders in the field would not be biased by pharmaceutical support, but one is also reminded of the importance of the current practice of reporting potential conflicts of interest in scientific manuscripts and presentations.

The highest payment category was consulting fees, with a total of $314,448 (41%) of all payments paid to 36 (12%) transplant surgeons. Transplant surgeons who received consulting payments tended to have a higher h-index than surgeons who did not receive them. Drug companies may seek out physician-researchers with a higher h-index because their greater knowledge and experience is more likely to lead to advances in therapy. On the other hand, companies may select these researchers as a marketing effort, to gain prestige by associating themselves with opinion leaders in medicine (18). However, it is important to note that our study was not intended to address motivations behind industry payments, but rather to report payment patterns and associations.

Several limitations of our study merit consideration. First, the CMS has designated a different database for disclosures of research funding. In the research database, recipients of payments are both hospitals as well as individuals, thus the payments made to a particular medical specialty for research cannot be comprehensively studied (3). Second, the OPP data withhold identifying payments that were disputed by either physicians or industry, so some of the details might change as the dispute process evolves. Third, since the OPP is intended merely to report the financial data, we cannot make inferences about whether the financial impact affects behavior or is beneficial or harmful to patient care and the field of surgical transplantation. Fourth, the industry is responsible for reporting the data. There is a possibility that payments are reported or categorized incorrectly, and therefore physicians are given an opportunity to review the data before its release. However, inaccurate reporting is considered a crime and the CMS has the right to review accounts of either party. Fifth, there is a possibility that institutions may limit the payment amount made to an individual, in such cases the remaining amount goes to the institution or department. Finally, although the OPP database and ASTS membership were combined to identify transplant surgeons, it is possible that some transplant surgeons did not report themselves as such to OPP and were not ASTS members, excluding them from this study.

In transplantation, physicians and industry have clearly worked together to substantially improve immunosuppression, ultimately leading to better patient outcomes (8–12). Although intended to provide greater transparency to patients, the payment data by itself are open to speculation (1, 2, 17). In a survey of 2,086 patients, most were unaware of how their physicians are paid (4). Regarding the OPP, Santhakumar states, “with reputations at stake, more detailed explanation is called for if misperceptions are to be minimized” (20). The transplant community needs a better understanding of the OPP data to prevent potential misinterpretation and misunderstanding. In this first national study of transplant surgeons, we found that payments were mostly made for consulting and were associated with academic productivity. Moving forward, it will be interesting to see how the OPP data will impact our field and the public perception of our field.

ACKNOWLEDGMENTS

This work was supported by grant number 1-R01-DK-098431–01-A1 from the National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK).The analyses described here are the responsibility of the authors alone and do not necessarily reflect the views or policies of the Department of Health and Human Services, nor does mention of trade names, commercial products or organizations imply endorsement by the U.S. Government. The data reported here have been supplied by the Minneapolis Medical Research Foundation (MMRF) as the contractor for the Scientific Registry of Transplant Recipients (SRTR). The interpretation and reporting of these data are the responsibility of the author(s) and in no way should be seen as an official policy of or interpretation by the SRTR or the U.S. Government. The authors wish to thank: Saad Anjum, Maurice Dunn, Sumukh Shetty and Arnaldo Mercado-Perez for Scopus H-index search.

Abbreviations:

- ASTS

American Society of Transplant Surgery

- CEP

Continuing Education Program

- CME

Continuing Medical Education

- CMS

Centers for Medicare and Medicaid Services

- HCP

Health Care Provider

- HRSA

Health Resources and Services Administration

- IQR

Interquartile Range

- KT

Kidney Transplant

- LT

Liver Transplant

- OPP

Open Payments Program

- OPTN

Organ Procurement and Transplantation

- SRTR

Scientific Registry of Transplant Recipients

Payments Made to Transplant Surgeons by Company

| Company | Amount ($) |

|---|---|

| Penumbra, Inc. | 3.47 |

| ZOLL Lifecor Corporation | 8.60 |

| Endocare, Inc. | 10.59 |

| Flowonix Medical Incorporated | 10.97 |

| Dendreon Corporation | 11.33 |

| Terumo Cardiovascular Systems Corporation | 11.84 |

| CareFusion Corporation | 12.12 |

| Medtronic Vascular, Inc. | 12.28 |

| Lantheus Medical Imaging, Inc. | 12.68 |

| Alcon Laboratories Inc | 13.49 |

| Mallinckrodt LLC | 14.49 |

| CSL Behring | 17.01 |

| Forest Laboratories, Inc. | 18.18 |

| Takeda Pharmaceuticals U.S.A., Inc. | 23.09 |

| Shionogi Inc | 23.52 |

| Valeant Pharmaceuticals International | 24.62 |

| The Medicines Company | 25.10 |

| MAQUET Cardiovascular U.S. Sales, L.L.C. | 27.43 |

| Eli Lilly and Company | 30.82 |

| DENTSPLY IH Inc. | 31.7 |

| Amgen Inc. | 32.15 |

| Warner Chilcott LLC | 34.91 |

| Daiichi Sankyo Inc. | 35.97 |

| DePuy Synthes Sales Inc. | 36.50 |

| American Medical Systems Inc. | 38.28 |

| ArjoHuntleigh, Inc. | 38.80 |

| The Spectranetics Corporation | 40.61 |

| Par Pharmaceutical, Inc. | 50.67 |

| Aesculap, Inc. | 57.01 |

| Optimer Parmaceuticals Inc | 57.06 |

| Ellman International | 67.67 |

| Teva Pharmaceuticals USA, Inc. | 68.20 |

| Astellas Scientific and Medical Affairs | 74.52 |

| AstraZeneca Pharmaceuticals LP | 83.22 |

| Ferring Pharmaceuticals Inc. | 84.03 |

| Eisai Inc. | 84.49 |

| Wilson Cook Medical Incorporated | 91.46 |

| Stryker Corporation | 92.89 |

| Hollister Incorporated | 98.93 |

| Atrium Medical Corporation | 109.16 |

| Medivation Inc. | 112.49 |

| Ozark Cryosurgery, LLC | 115.68 |

| United Therapeutics Corporation | 119.64 |

| Medistim USA, Inc. | 137.52 |

| Sorin Group USA, Inc | 143.66 |

| Galil Medical Inc. | 144.5 |

| KCI USA, Inc | 156.11 |

| Biotronik Inc. | 164.64 |

| GAMBRO AAB | 165.11 |

| Smith & Nephew, Inc. | 168.62 |

| Coloplast Corp | 189.53 |

| AbbVie, Inc. | 195.01 |

| Abbott Laboratories | 197.77 |

| Kadmon Pharmaceuticals LLC | 206.46 |

| Baxter Healthcare | 217.52 |

| Actavis Pharma Inc | 218.25 |

| Endo Pharmaceuticals Inc. | 229.93 |

| Alpha Orthopedic Systems | 258.00 |

| CONMED Corporation | 342.00 |

| Questcor Pharmaceuticals | 348.16 |

| Auxilium Pharmaceuticals, Inc. | 366.20 |

| Roanoke Area Surgical Lasers, LLC | 379.28 |

| Allergan Inc. | 386.28 |

| ABIOMED | 488.33 |

| Cubist Pharmaceuticals Inc | 563.88 |

| Innovative Lasers, LLC | 597.27 |

| Great Lakes Medical Services, LLC | 744.74 |

| AngioDynamics, Inc. | 784.42 |

| Cook Incorporated | 800.64 |

| Cryo Specialty Medical, LLC | 843.85 |

| Laser Specialty Medical, LLC | 881.13 |

| Innovative Cryosurgery, LLC | 1045.70 |

| Pacira Pharmaceuticals Incorporated | 1161.48 |

| Actelion Pharmaceuticals US, Inc. | 1241.46 |

| Hansen Medical, Inc. | 1270.43 |

| CorMatrix Cardiovascular Inc. | 1411.38 |

| 3M Company | 1500.00 |

| LeMaitre Vascular, Inc. | 1535.10 |

| Astellas Pharma Inc | 1639.28 |

| Covidien LP | 1768.10 |

| Medtronic USA, Inc. | 2115.38 |

| LifeCell Corporation | 2245.83 |

| Merit Medical Systems Inc | 2250.00 |

| Wako Life Sciences, Inc. | 2266.02 |

| Seattle Genetics, Inc. | 2613.51 |

| Alexion Pharmaceuticals, Inc. | 2656.11 |

| Pfizer Inc. | 2951.36 |

| Covidien Sales LLC | 3459.46 |

| St. Jude Medical, Inc. | 3536.86 |

| NeuWave Medical, Inc. | 3694.19 |

| GlaxoSmithKline, LLC. | 3908.20 |

| BTG International, Inc. | 4065.98 |

| Roche Health Solutions Inc. | 5200.00 |

| Millennium Pharmaceuticals, Inc. | 5215.80 |

| Onyx Pharmaceuticals, Inc., an Amgen subsidiary | 5566.41 |

| Janssen Pharmaceuticals, Inc | 5690.08 |

| Boston Scientific Corporation | 6601.98 |

| Astellas Pharma US Inc | 8188.29 |

| Novartis Pharma AG | 8799.82 |

| LifeNet Health Inc. | 9023.66 |

| Genentech, Inc. | 9041.54 |

| CryoLife, Inc. | 9663.29 |

| Gilead Sciences Inc | 11178.88 |

| Merck Sharp & Dohme Corporation | 11762.55 |

| Ethicon Inc. | 12662.54 |

| Syncardia Systems, Inc | 13151.74 |

| Boehringer Ingelheim Pharmaceuticals, Inc. | 15066.91 |

| Bayer HealthCare LLC | 15420.13 |

| Astellas Pharma Global Development | 16120.14 |

| Celgene Corporation | 19896.77 |

| Thoratec Europe Limited | 20384.25 |

| Otsuka America Pharmaceutical, Inc. | 24811.26 |

| NPS Pharmaceuticals, Inc. | 25256.44 |

| Salix Pharmaceuticals, Ltd | 30958.41 |

| Bristol-Myers Squibb Company | 35348.81 |

| Sanofi and Genzyme US Companies | 39339.85 |

| Thoratec Corporation | 41080.17 |

| Intuitive Surgical, Inc. | 46322.45 |

| C. R. Bard, Inc. & Subsidiaries | 46643.27 |

| Novartis Pharmaceuticals Corporation | 51289.47 |

| W. L. Gore & Associates, Inc. | 52482.09 |

| Vertex Pharmaceutical Incorporated | 96863.57 |

Footnotes

DISCLOSURE

The authors of this manuscript have no conflicts of interest to disclose as described by the American Journal of Transplantation.

REFERENCES

- 1.Agrawal S, Brennan N, Budetti P. The Sunshine Act—effects on physicians. N Engl J Med 2013;368:2054–2057. [DOI] [PubMed] [Google Scholar]

- 2.Centers for Medicare and Medicaid Services. Medicare, Medicaid, Children’s Health Insurance Programs: transparency reports and reporting of physician ownership or investment interests. Fed Regist 2013;78:9457–9528. [PubMed] [Google Scholar]

- 3.Gorlach I, Pham-Kanter G. Brightening up: the effect of the Physician Payment Sunshine Act on existing regulation of pharmaceutical marketing. J Law Med Ethics 2013. Spring;41(1):315–22. [DOI] [PubMed] [Google Scholar]

- 4.Kao AC, Zaslavsky AM, Green DC, Koplan JP, Cleary PD. Physician incentives and disclosure of payment methods to patients. J Gen Intern Med 2001. March;16(3):181–8. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5.Licurse A, Barber E, Joffe S, Cross C The impact of disclosing financial ties in research and clinical care: a systematic review. Arch Intern Med, 170 (2010), pp. 675–68. [DOI] [PubMed] [Google Scholar]

- 6.Campbell EG, Gruen RL, Mountford J, Miller LG, Cleary PD, Blumenthal D. A national survey of physician-industry relationships. N Engl J Med 2007;356:1742–1750 [DOI] [PubMed] [Google Scholar]

- 7.Gagnon MA, Lexchin J. The cost of pushing pills: a new estimate of pharmaceutical promotion expenditures in the United States. PLoS med 2008;5:e1. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.Brennan DC, Daller JA, Lake KD, Cibrik D, Del Castillo D; Thymoglobulin Induction Study Group. Rabbit antithymocyte globulin versus basiliximab in renal transplantation. N Engl J Med 2006. November 9;355(19):1967–77 [DOI] [PubMed] [Google Scholar]

- 9.Ekberg H, Tedesco-Silva H, Demirbas A, Vítko S, Nashan B, Gürkan A, Margreiter R, Hugo C, Grinyó JM, Frei U, Vanrenterghem Y, Daloze P, Halloran PF; ELITE-Symphony Study. Reduced exposure to calcineurin inhibitors in renal transplantation. N Engl J Med 2007. December 20;357(25):2562–75. [DOI] [PubMed] [Google Scholar]

- 10.Budde K, Bunnapradist S, Grinyo JM, Ciechanowski K, Denny JE, Silva HT, Rostaing L; on behalf of the Envarsus study group. Novel Once-Daily Extended-Release Tacrolimus (LCPT) Versus Twice-Daily Tacrolimus in De Novo Kidney Transplants: One-Year Results of Phase III, Double-Blind, Randomized Trial. Am J Transplant 2014. December;14(12):2796–806. [DOI] [PubMed] [Google Scholar]

- 11.Vo AA, Lukovsky M, Toyoda M, Wang J, Reinsmoen NL, Lai CH, Peng A, Villicana R, Jordan SC. Rituximab and intravenous immune globulin for desensitization during renal transplantation. N Engl J Med 2008. July 17;359(3):242–51. [DOI] [PubMed] [Google Scholar]

- 12.Hershberger RE, Starling RC, Eisen HJ, Bergh CH, Kormos RL, Love RB, Van Bakel A, Gordon RD, Popat R, Cockey L, Mamelok RD. Daclizumab to prevent rejection after cardiac transplantation. N Engl J Med 2005. June 30;352(26):2705–13 [DOI] [PubMed] [Google Scholar]

- 13.OPTN / SRTR 2010 Annual Data Report Rockville, MD; 2011. [Google Scholar]

- 14.Hirsch JE. An index to quantify an indivdual’s scientific research output. PNAS 2005; 102: 16569–16572. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15.Zou G A modified poisson regression approach to prospective studies with binary data. Am J Epidemiol 2004; 159: 702– 706. [DOI] [PubMed] [Google Scholar]

- 16.Louis TA, Zeger SL. Effective communication of standard errors and confidence intervals. Biostatistics 2009(1):1–2. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 17.McCarthy M US intends to publish drug company payments to doctors from October despite calls for delay. BMJ2014;349:g5693. [DOI] [PubMed] [Google Scholar]

- 18.Chang JS. The Physician Payments Sunshine Act: Data Evaluation Regarding Payments to Ophthalmologists. Ophthalmology 2015. January 8 pii: S0161–6420(14)01049–5. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19.Khan NR, Thompson CJ, Taylor DR, Venable GT, Wham RM, Michael LM 2nd, Klimo P Jr. An analysis of publication productivity for 1225 academic neurosurgeons and 99 departments in the United States. J Neurosurg 2014. March;120(3):746–55. [DOI] [PubMed] [Google Scholar]

- 20.Santhakumar S, Adashi EY. The Physician Payment Sunshine Act: testing the value of transparency. JAMA 2015. January 6;313(1):23–4. [DOI] [PubMed] [Google Scholar]