Abstract

Several previous studies have evaluated the potential greenhouse gas (GHG) benefits of forest biomass energy relative to fossil fuel equivalents over different spatial scales and time frames and applying a variety of methodologies. This paper contributes to this literature through an analysis of multiple projected sources of biomass demand growth in different regions of the world using a detailed intertemporal optimization model of the global forest sector. Given the range of current policies incentivizing bioenergy expansion globally, evaluating the combined global implications of regional bioenergy expansion efforts is critical for understanding the extent to which renewable energy supplied from forest biomass can contribute to various policy goals (including GHG emissions mitigation). Unlike previous studies that have been more regionally focused, this study provides a global perspective, illustrating how large potential demand increases for forest biomass in one or multiple regions can alter future forest management trends, markets, and forest carbon sequestration in key timber supply regions. Results show that potential near term (2015–2030) biomass demand growth in the U.S., Europe, and elsewhere can drive forest resource investment at the intensive and extensive margins, resulting in a net increase in forest carbon stocks for most regions of the world. When the reallocation of biomass away from traditional pulp and sawtimber markets is accounted for, net forest carbon sequestration increases (that stored on the land and in wood products) by 9.4 billion tons CO2 over the near term and 15.4 billion tons CO2 by 2095. Even if most of the increased forest biomass demand arises from one region (e.g., Europe) due to a particularly strong promotion of forest bioenergy expansion, changes in forest management globally in anticipation of this demand increase could result in carbon beneficial outcomes that can be shared by most regions.

Keywords: Bioenergy, Carbon sequestration, Forest management

1. Introduction and background

Global energy consumption projections over the near term (by 2030) suggest that biomass utilization for energy generation could rise substantially. This expected increase will likely be driven by policies implemented to increase energy security or to reduce greenhouse gas (GHG) emissions relative to fossil energy sources. Such policies range from renewable energy directives in the United Kingdom and European Union (EU) to state- or national-scale renewable energy initiatives in the United States. There is lengthy literature that elaborates on these policy efforts and potential role of biomass energy in increasingly renewable-dependent energy systems at regional, national, and global scales (Faaij, 2001; Galik and Abt, 2015; Gurgel et al., 2007; Galik et al., 2009; Rose et al., 2012). Furthermore, recent literature suggests that large-scale adoption of negative emissions technologies such as biomass energy with carbon capture and sequestration could play an important role for reaching climate stabilization targets of 2°C or less (Kriegler et al., 2013; Smith et al., 2016).

It is important to evaluate policies or technology changes that stimulate forest biomass demand to determine the extent to which such expansion could alter terrestrial carbon stocks and to ascertain whether the sourcing of this feedstock results in increased or decreased emissions from the land use sectors. Forest biomass can be used as a feedstock to produce liquid biofuels or burned for electric power generation through various sources (including wood pellets or direct cofiring of residual biomass). Following the implementation of several biofuel policies in the United States, Brazil, and other regions, a lengthy literature has emerged that has assessed the global GHG implications of various biofuel policies, including corn ethanol or cellulosic ethanol expansion (e.g., Hertel et al., 2010; Keeney and Hertel, 2009; Mosnier et al., 2013), though these studies have typically focused on biofuel production from agricultural feedstocks. More recently, however, there is a focused debate in the literature regarding the use of forest biomass for energy production and whether the use of woody biomass results in net GHG emissions when consumed. Searchinger et al. (2009) argue that assuming all biomass is carbon neutral is an inappropriate GHG accounting procedure because it ignores the implication of decreased terrestrial storage once biomass is removed from the landscape. Several recent papers have illustrated this point by projecting the potential forest harvest, net emissions, and required carbon payback period of biomass removals from single-forest resource systems (e.g., Walker et al., 2013; Zanchi et al., 2012). These studies, however, do not assess forest biomass expansion as part of an economic system and often evaluate removals on single-forest stands modeled in isolation.

Recent studies have used integrated assessment models (IAMs) to evaluate bioenergy pathways and more broadly GHG abatement potential from the land use sectors (e.g., Calvin et al., 2014; Favero et al., 2017; Favero and Mendelsohn, 2017; Humpenöder et al., 2014; Riahi et al., 2017). IAMs offer the advantage of treating forest and land-based mitigation strategies (including bioenergy) as a contributing to broader GHG mitigation portfolios established through the IAM scenario design. However, IAMs typically do not capture forest resource management possibilities or product markets in sufficient detail. Furthermore, as most recent IAM studies have addressed the role of forestry in contributing to system-wide GHG mitigation policies, it is important to evaluate potential GHG implications of policies designed in the absence of specific GHG abatement price incentives or net emissions reduction targets. That is, while more detailed forest sector or land use models require exogenous assumptions to drive bioenergy policy analysis (e.g., hypothetical mandates), conducting such analyses in the assumed absence of broader GHG policies can result in an unbiased projection of the potential GHG implications of a policy designed specifically to increase the utilization of forest biomass for energy generation.

Furthermore, forest sector models depict spatial heterogeneity in the forest resource base, temporal heterogeneity through the course of a simulation horizon as forests age or are managed/harvested, and forest product market differentiation. These are important considerations for bioenergy policy analysis. Regardless of whether policies encourage use of forest biomass for electricity generation or liquid transportation fuels, it is critical to evaluate policy-induced forest biomass demand expansion systematically, accounting for market feedbacks (e.g., higher prices) that can influence carbon stocks globally. In forested systems, this is particularly important for several reasons. First, forests are long-term investments, and if bioenergy is expected to increase future prices, investments will increase (e.g., Daigneault et al., 2012). Second, price changes may differ for sawtimber and pulpwood commodities. For example, although pulpwood prices are likely to rise, because pulp material is the closest substitute for biomass energy inputs, sawtimber harvests may increase as well if bioenergy policies increase overall harvesting levels. These increased harvests could potentially reduce pulpwood and sawtimber prices in the long run as forest inventories increase and land managers invest in increasing productivity of the forest resource base. Third, forests are managed differently across the world, so the effects of changes in demand will have different implications for carbon. For instance, in places where forests grow relatively rapidly or plantations are more widely used, higher prices will invite more investments. Alternatively, in places where forests grow slowly or old growth extraction occurs, higher prices could increase old growth extraction and reduce (increase) carbon stocks.

Several existing studies, such as Nepal et al. (2012), suggest that large-scale forest biomass energy programs would convert U.S. forests from a net sink to a source of carbon emissions over the next half century. Similarly, Frank et al. (2016) find that biomass energy policies in Europe lead to positive net emissions from forests if biomass material is sourced from forests rather than agriculture. Other static partial equilibrium studies have also evaluated the implications of woody biomass expansion. Raunikar et al. (2010) and Buongiorno et al. (2011) both project the market implications of long-term increases in forest bioenergy using the GFPM. Raunikar et al. (2010) evaluate two Intergovernmental Panel on Climate Change (IPCC) scenarios (A1B and A2). Raunikar et al. (2010) uses macroeconomic growth and bioenergy demand assumptions from the IPCC scenarios to drive forest product market changes, finding a 600% increase in total forest product demand by 2060 and consequentially a substantial increase in prices and harvests. Buongiorno et al. (2011) considers a doubling of global forest bioenergy generation relative to a baseline, and find a long-term convergence between industrial roundwood and fuelwood prices.

However, these studies project equilibrium outcomes via static simulations, which ignore dynamic considerations of harvesting now relative to future periods when prices may rise under the influence of policy changes. Static approaches typically assume that forest management will respond to market stimuli in the future as it has in the past and that landowners do not explicitly consider expected future market and policy changes when making harvest and management decisions. Such methods can result in higher harvest levels in any given period from an increase in prices or some exogenous policy stimuli relative to dynamic approaches that account for the marginal user costs of harvesting today on future forest values.

As discussed in Miner et al. (2014), forestry is a long-term proposition, and landowners involved in forestry production are forward-looking when making management decisions. If future forest bioenergy demand increases substantially, foresters will expand the productive forestry land base to increase output. Dynamic forest management models that examine bioenergy scenarios have found that the global stock of forest carbon increases as foresters respond to the increased demand for forest products by increasing inventories (and thus accumulating additional carbon) to meet future demand (Daigneault et al., 2012; Sedjo and Tian, 2012). Latta et al. (2013) and Wang et al. (2015) apply dynamic methods to assess land use and market outcomes of biomass energy expansion (with a U.S. regional focus), finding relatively modest land use and regional GHG implications of forest bioenergy expansion. Tian et al. (2018) offers additional insight into potential differences between static and structural dynamic approaches when projecting forest carbon outcomes, and illustrates how forest product demand growth can result in increased terrestrial carbon fluxes. This result is not specific to intertemporal modeling frameworks, however, as recent studies using regional simulation and partial equilibrium frameworks have also shown that bioenergy demand shocks can result in forest management expansion on the intensive and extensive margins and increased terrestrial C uptake (e.g., Abt et al., 2012; Galik and Abt, 2012, 2015).

One of the issues with the current literature is that most authors focus on relatively modest, regional bioenergy programs. Many studies consider changes in demand due to local changes in bioenergy policy incentives (e.g., Daigneault et al., 2012; Galik et al. 2009), although some studies are considering the local effects of increased demands from specific (outside) regions, such as the effects of EU policies on demand for pellets in the Southeastern United States (Galik and Abt, 2015). Countries, however, are not exploring bioenergy expansion policies in isolation. The EU, the United Kingdom, the United States, Canada, Brazil, and China, for instance, have policies in place that promote biomass energy expansion. Wood product markets are global, and shifts in demand in one region will have an impact elsewhere; thus, it is important to account for the impacts globally. To understand how bioenergy expansion efforts will affect forests, one needs to aggregate the demand shocks for all regions and conduct global analysis that accounts for interactions across regions.

This study makes two unique contributions. First, we evaluate the combined global effects of forest bioenergy expansion policies across several regions simultaneously instead of focusing on the effects of a single regional policy. While these sources represent near-term projections, our scenario design couples projected demand growth from pellets and other forest bioenergy sources over the near term with a modest demand growth assumption to reflect long-term demand potential. This scenario design focuses exclusively on the utilization of forest biomass for energy production and thus does not capture the potential role of agricultural feedstocks in supplying requisite biomass as a fuel input into various bioenergy pathways. This allows for a more focused analysis on the interactions between sustained bioenergy expansion, forest product markets, and forest management.

The modeling framework applied in this analysis, the Global Timber Model (GTM), is agnostic about the final energy source that the biomass will be used to generate because GTM does not differentiate between bioenergy end uses. Scenarios are designed to represent the cumulative projected demand of several regional (and hypothetical) policy targets as a new demand source that directly competes for forest resources with traditional pulpwood and sawtimber markets. We do not attempt to distinguish between alternative bioenergy demand sources, instead converting specific policy targets into biomass input requirements, as distinguishing between final bioenergy end uses would not materially change the analysis of upstream forest-sector impacts.1 We compare aggregate market, land management, and carbon implications of a single region bioenergy policy shock that is also agnostic to final energy use of the biomass.

The second contribution that this paper makes is that we conduct our analysis with an intertemporal model of the global forestry sector with heterogenous forest product demand that allows for intensive and extensive margin forest management responses to policy stimuli. Other studies have applied similar modeling frameworks to address forest bioenergy expansion, but this study is unique in that we apply intertemporal optimization techniques to evaluate near-term, simultaneous forest biomass expansion in the United States, EU, and other regions to project the implications for global forest carbon stocks while also capturing potential interactions between pulpwood and sawtimber markets globally.

To analyze the aggregate effects of bioenergy expansion policies on forest carbon sequestration, we use the Global Timber Model (GTM) as discussed in Sohngen et al. (1999), Daigneault et al. (2012), and Favero and Mendelsohn (2014). The model is a dynamic optimization model that accounts for the dynamic response of over 200 global forest types to demand or ecosystem perturbations. The demand structure includes separate demand for both pulpwood and sawtimber. An additional demand component is included that specifically relates to forest biomass for energy generation purposes. This bioenergy demand component competes directly with traditional pulpwood and sawtimber and can be sourced from roundwood, residual biomass (logging residues), or short rotation plantations.

This study advances the current literature in part by conducting a dynamic analysis that allows investments in forest resources in response to forest biomass demand increases driven by renewable energy policy. The intertemporal dynamic optimization approach applied in this analysis offers insight into how anticipated policy shocks can influence demand for specific commodity groups, and how this can result in forest management changes and ultimately changes in terrestrial carbon storage. While we do not assess simultaneous expansion of forestry and agricultural feedstocks, our results offer important insight into the interactions between forest bioenergy expansion, markets for pulpwood and sawtimber, and potential resource management changes at the intensive and extensive margins. Furthermore, while recent literature has linked GTM to an existing IAM framework (Favero and Mendelsohn, 2017; Favero et al., 2017), these studies applied a version of the model with homogenous forest product demand and thus do not explicitly capture interactions between pulpwood and sawtimber markets.

This study also advances the literature by examing the implications of a number of drivers of forest bioenergy demand expansion that have emerged around the world. The aggregate effect of these policies turns out to be quite large, potentially increasing global demand for wood by 5–12% per year over the next 20–25 years. The only similar study is that of Favero and Mendelsohn (2014), who consider a very aggressive biomass energy expansion program. The Favero and Mendelsohn (2014) study, however, considers the very long run because most biomass energy consumption occurs in the second half of the coming century in their study. This study, in contrast, examines a large set of programs around the world that are implemented in the near term. By focusing on hypothetical policy scenarios that mimic large near-term policy efforts documented in various literature sources coupled with an assumed growth rate for biomass energy in the future, our study considers short-term (2025), medium-term (2055), and long-term (2095) effects of bioenergy expansion scenarios.

The paper is organized as follows. The next section describes our model in general. We then present our baseline and scenarios. We then discuss the results of the scenario analysis, provide conclusions, and discuss limitations of this analysis (including parametric uncertainty, limitations of not direclty representing agricultural sector production possibilities and markets, and the inability to isolate GHG impacts of specific forest biomass sources due to the aggregate nature of our scenario design).

2. Model and analysis

The GTM is a dynamic optimization model of the global forestry sector. The basic structure of the model and the data are described in Daigneault et al. (2012). This model is updated from that earlier version to include heterogeneous products in demand. Daigneault et al. (2012) and other previous versions of the model assumed a single global demand for all wood, implying that wood is a homogeneous product. For this application, we improve on that assumption and allow heterogeneous products by incorporating separate demand functions for sawtimber and pulpwood. Each log harvested in the model will be used proportionally in the supply of wood to sawtimber or pulpwood markets, though this proportion changes endogenously over time, by region, by forest type, and based on the age of a stand at harvest (e.g., older stands yield a higher proportion of sawtimber).

Capturing heterogeneous product demand in a forest bioenergy policy context is important as anticipated policy and/or market changes that favor a greater level of pulpwood or sawtimber production can shift forest management profiles over time. For example, a policy mechanism that incentivizes near-term expansion in forest biomass can increase pulpwood harvests and new investment in plantation systems to meet increased demand for lower-valued pulpwood utilized for energy generation.

Furthermore, incorporating heterogeneous products allows us to more carefully model the substitution between traditional timber markets and forest biomass energy markets. Forest biomass energy can be sourced from residual biomass, traditional pulpwood sources, traditional sawtimber sources, and short rotation woody coppice plantations. Although we technically allow bioenergy feedstocks to substitute for either sawtimber or pulpwood in the model, pulpwood has lower prices; thus, most biomass for bioenergy will be drawn from traditional pulpwood markets. In turn, some sawtimber will then be used in pulpwood markets. As in past versions of the model, the global demand for sawtimber and pulpwood is aggregated from regional demand functions. Since regional demands are aggregated to a single global demand function for pulpwood and sawtimber, respectively, the modeling framework assumes that biomass can be traded across regions for alternative end uses (given various cost considerations).

Holding baseline demand growth rates for pulpwood and sawtimber, we incorporate constraints into the model to account for bioenergy demand. Specifically, we require a fixed amount of wood to be used by the global electricity, industrial, and transportation sectors for energy generation, which is functionally equivalent to a separate and generic demand function for forest biomass bioenergy that is perfectly inelastic and exogenously defined. Constraints like this can be imposed on specific timber supply regions, such as Southern pine plantations in the Southeastern states of the United States, they can be imposed in aggregate for an entire region or country or they can be imposed in aggregate for the entire world. For this analysis, two scenarios are developed to project the effect of an increase in the demand for biomass on the global timber market. One scenario implements a global increase in demand for biomass energy with the ability to source the wood from anywhere in the world. Although the data for all countries are not available, the hypothetical projected biomass demand in this scenario includes assumed increases from major countries in Europe, North and South America, and East Asia. The second scenario focuses on Europe alone, examining the implications of an increase in biomass energy demand in that region only. For this scenario, there is no increase in demand for biomass in the rest of the world.

To set the constraints for biomass demand for our analysis, we rely on estimates from the literature. Biomass feedstock demand is likely to be affected by a number of renewable energy goals in the future, including to increase total energy consumption from renewable resources, to reduce GHG emissions, or for other policy goals such as energy independence and rural income generation (Abt, 2014; Cocchi et al., 2011; European Commission, 2010; Joudrey et al., 2012;). Projections of demand for wood pellets, a type of solid biomass, and other bioenergy sources by 2020 based on various studies are shown in Table 1.

Table 1.

Biomass Demand Projections for Bioenergy, Including Pellet and Nonpellet Sources (Million Short Tons) by 2020.

| Regions | Current demand (year) | Projected Demand (by 2020) | Source | Notes |

|---|---|---|---|---|

| Western and Eastern Europe | 12.3 2010 |

27.1 | Pöyry (2011) | |

| 11.5 2011 |

38.6 | Cocchi et al. (2011) | EU only, BAU scenario: based on past and current trends, industry expectations, press releases, existing studies, etc. | |

| 10.8 2009 |

126.5 | Sikkema et al. (2011) | EU only, Reference scenario: Growth projections based on current growth rates, competition with forestry sector | |

| n/a | 88.2 | European Commission (2010) | EU only | |

| n/a | 212.7 | Atanasiu (2010) | EU only | |

| 164.2 2010 |

241.4 | Beurskens et al. (2011) | EU only, from National renewable energy policies: Solid biomass for electricity and heating | |

| Russia | 0.0 2010 |

0.1 | Pöyry, 2011 | |

| North and South America | 3.8 (2010) |

6.6 | Pöyry (2011) | |

| 8.3 2011 |

20.5 | Conti et al. (2014) | U.S. only, including demand for nonpellet biomass | |

| 15–34 2015 |

29–57 | Abt (2014) | U.S. only, including demand for nonpellet biomass | |

| 2.3 2011 |

6.4 | Cocchi et al. (2011) | Canada only | |

| Oceania | 0.03 2010 |

0.1 | Pöyry (2011) | |

| South Korea and Japan | 0.2 2010 |

6.1 | Pöyry (2011) | |

| 0.4 2011 |

5.5 | Cocchi et al. (2011) | South Korea only | |

| China | 0.7 2010 |

11.0 | Pöyry (2011) |

Europe2 is the largest solid biomass consumer in the world and is expected to increase its biomass demand. Pöyry (2011) estimates the percentage increase in demand for wood pellet biomass in Europe between 2010 and 2020 to be about 120%. For EU countries specifically, various studies show a different estimate, with the percentage increase by 2020 varying from 47% to 1000%.

The second largest consumer of forest biomass energy (including wood pellets) is the United States, and it is possible that consumption of forest biomass for energy generation through pellets and/or production of cellulosic liquid fuels could increase significantly in the coming decades. The Annual Energy Outlook 2014 (Conti et al., 2014) suggests that U.S. biomass consumption for energy generation (excluding municipal waste) is expected to increase from 8.3 million short tons in 2011 to 20.5 million short tons in 2020.3 The demand in East Asia will depend strongly on developments in Japan, South Korea, and China but can be estimated to be in the range of 5–11 million tons by 2020 (Pöyry, 2011).

With regard to supply, major suppliers of forest biomass for energy production are the United States, Canada, and Europe (WRI, 2014; Abt, 2014). As seen in Table 1, the estimates of demand projection from other authors vary widely. For this analysis, the median projected quantity for each region from Table 1 is used to develop the future demand projection, which is shown in Table 2. Changes in demand for bioenergy will drive the changes in wood pellet production and consumption of woody biomass generally and, in turn, will affect existing forests, forest management, and land use, as well as carbon sequestration in the forestry sector (Abt, 2014; European Commission, 2010).

Table 2.

Hypothetical Global Solid Biomass Demand Constraints (Million Short Tons).

| Regions | Current Demand | Projected Demand (by 2020) | Source |

|---|---|---|---|

| EU | 11.90 | 107.36 | Median value from studies in Table 1 |

| Russia | 0.03 | 0.06 | Pöyry (2011) |

| North and South America | 6.05 | 13.56 | Take median from previous studies in Table 1 |

| Oceania | 0.03 | 0.14 | Pöyry (2011 |

| South Korea and Japan | 0.33 | 5.79 | Take median from previous studies in Table 1 |

| China | 0.66 | 11.02 | Pöyry (2011) |

| Sum of Demands | |||

| Scenario (1): World biomass demand | 19.01 | 137.94 | |

| Scenario (2): Europe biomass demand only | 11.90 | 107.36 | |

The first scenario assumes that timber from all over the world is allowed to be a source of feedstock to meet the global biomass demand projections constructed in Table 1. The second scenario is constructed to examine the effect of European biomass demand alone. Given that Europe is currently the world’s largest market for wood pellets and will likely remain the largest consumer of pellets in the near future, this analysis assumes that woody biomass energy demand growth in Europe will have a larger impact on the wood biomass market, timber products market, and consequently on carbon storage in forests relative to bioenergy policies in other regions modeled. In this second scenario, we constrain biomass used in Europe to be sourced from Europe. Europe can still import wood to meet demand for typical industrial wood production.4 Fig. 1 illustrates two demand shocks for biomass energy converted into million cubic meters per year of timber, which is the output measure used in the model relative to a no-bioenergy policy baseline with status quo demand growth in pulpwood and sawtimber markets. The 2010 and 2020 global biomass demand projections are obtained directly from previous studies shown in Table 1. Beyond 2020, we assume that the annual percentage change in biomass demand follows the annual percentage increase in demand for timber production, which averages 0.3% per year over the century. Although this is a modest increase in forest biomass for energy demand post-2020, it represents a large change in total demand around mid-century and later. The hypothetical growth rate in demand is an important component of our scenario design and does not explicitly reflect existing policies. However, this growth rate assumes the possibility of continued policy-induced expansion in forest-based energy (including biopower and liquid transportation fuels) that could be supported by mid-century or long-term climate stabilization efforts in different regions of the world. This perspective is consistent with recent economy-wide modeling projections that show large-scale expansion in bioenergy as a mitigation strategy (Riahi et al., 2017). After 2110, demand for biomass energy is held constant through the simulation horizon.

Fig. 1.

Woody Biomass Demand Growth under Europe and World Bioenergy Expansion Scenarios.

3. Results

3.1. Baseline

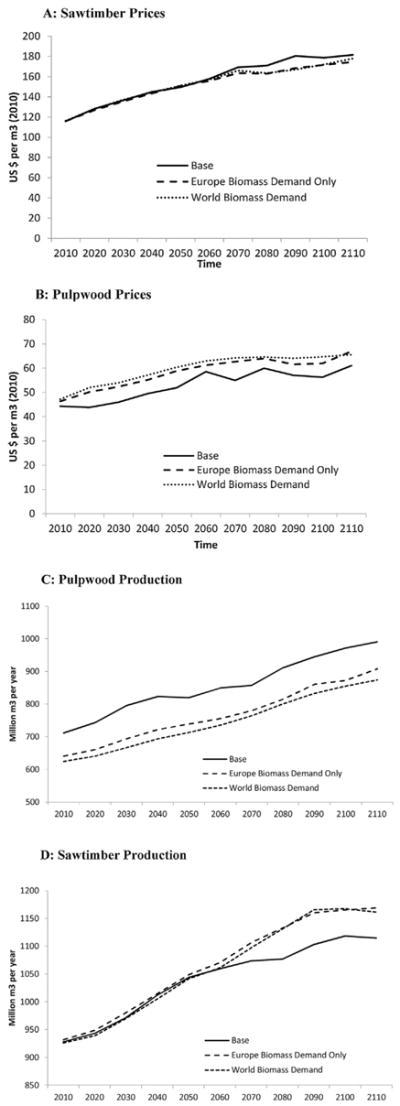

A base case for the model is solved first assuming that there is no demand for biomass energy. In the base case, timber is allocated either to sawtimber or pulpwood. Prices are resolved at the global level, although they are indexed to the price of wood in the southern United States. Prices in other regions will follow these price trends but will differ depending on local costs of production and quality differences among species. Sawtimber prices are projected to be about 3 times higher than pulpwood prices (Fig. 2), which is consistent with historic price ratios. Sawtimber provides the higher-value end use and thus commands a higher price. From 2010 to 2060, sawtimber and pulpwood prices rise about 0.6% and 0.4% per year, respectively. It is not surprising that pulpwood prices rise more slowly given that pulpwood is fairly homogeneous and can be easily substituted across regions and types.

Fig. 2.

Timber Prices under the Baseline.

Global timber outputs are projected to increase by relatively modest amounts, 0.25% per year, over the next century, and this growth is driven by projected changes in global income over time. Gross domestic product growth shifts the demand for pulpwood and sawtimber over time and results in this modest growth in timber outputs. Northern regions like Europe and Canada are projected to have little to no growth in output, while the United States and Latin America experience a fairly substantial increase (Fig. 3). The large increase in these regions is due to historical and continued expansion of fast-growing plantations in subtropical regions, such as the U.S. South.

Fig. 3.

Total Forest Output over Time for the Baseline Case.

Total forestland area globally is projected to decline by 186 million hectares over the next century. This reduction is largely driven by deforestation in tropical regions. This is less deforestation on average than is shown historically by the Food and Agricultural Organization (FAO) for the period 1990–2010 for similar regions. The FAO (2015) suggests that around 6.7 million hectares of tropical forest have been lost per year over that time period, and our estimates suggest a reduction to only about 0.3 million hectares per year over the next century. However, that rate of forest loss has dropped precipitously from 0.18% of forest area per year in the 1990s to 0.08% from 2010 to 2015 (FAO, 2015). Part of this reversal is due to policy intervention and concerted forest conservation efforts, while some is driven by increased agricultural intensification and productivity growth that has been land sparing in countries like Brazil (Barretto et al., 2013). Our projection shows less deforestation, assuming a continuation of policy trends and agricultural productivity improvements that offset the need for more land in agriculture.

3.2. Forest biomass energy demand scenarios

The bioenergy demand scenarios increase demand for woody biomass and raise prices (Fig. 4) and reduces production of pulpwood globally as a portion of traditional pulpwood harvests is allocated to bioenergy use. The overall market impact is consistent for the Europe and World bioenergy expansion scenarios. Therefore, we focus most of the following discussion on comparing projected outcomes from the World bioenergy expansion case to the baseline.

Fig. 4.

Global Sawtimber and Pulpwood Prices and Production under Three Scenarios.

The demand scenarios have a much stronger impact on pulpwood prices than on sawtimber prices. Pulpwood prices increase by up to 18% initially under the World demand scenario. Over the longer run, pulpwood prices increase 10–12%. For sawtimber, the price change is negligible initially, with a long-term reduction in prices. This reduction in prices is perhaps surprising, but it results from the global investments in timber growing that occur in response to the biomass energy stimulus. The reduction in prices for sawtimber is caused by the overall increase in wood material harvested in the near-term, of which some of the higher value timber enters sawtimber markets, thus increasing supply and reducing prices. Over the long run, supply increases due to investments, which increases supply of all three wood uses (biomass, pulpwood, and sawtimber). The economic forces that drive higher demand for biomass material drive more investments in forests that ultimately increases the output of sawtimber.

Although pulpwood prices increase due to the large increase in demand for wood in the biomass energy sector and the ease of substitution between pulpwood and biomass material, the increase in demand spurs greater overall harvesting globally. Wood products output (sawtimber, pulpwood, and biomass material) increases by 3.7% globally in the first decade, rising to 7.0% by mid-century and 11% by the end of the century. One of the key issues with biomass energy policies is that effects could vary over time. Some studies argue that the use of woody biomass to meet renewable energy policy goals could drive forest harvests in the near term, resulting in a carbon debt that would be repaid over many decades, although these analyses often rely on stand-level frameworks as opposed to systematic assessments of forest biomass energy expansion in the context of a fully integrated market system (McKechnie et al., 2010). Thus, the carbon debt result ignores the potential for product substitution or forest-related investments made in anticipation of future demand growth, both of which can ameliorate near-term emissions relative to stand-level analyses. In the short term, most of the material used to produce biomass is derived from substituting other timber uses (Fig. 5). Over time, as higher prices drive new investments in forestry, the increase in biomass for energy is derived largely from an increase in overall harvesting.

Fig. 5.

Proportion of Biomass Energy Sourced from Timber Product Substitution and Increased Harvests (World Bioenergy Expansion Scenario).

The increase in harvesting is shared broadly across the world but not evenly (Fig. 6). By 2025, the harvesting in the United States declines modestly as a result of the policy, while China, Canada, the EU, and Latin America experience the bulk of the increase in total harvesting. By 2055, the benefits are shared by most regions, although China experiences a decline in timber harvesting. This decline is temporary, however, because the long-term implications of the policy in China suggest that timber harvests increase there by the end of the century. Most regions, in fact, appear to increase harvesting over the century, except Canada. Canada achieves short-term gains, but in the longer run, these gains are limited, and indeed harvesting is projected to decline there.

Fig. 6.

Change in Regional Total Wood Output between the World Biomass Scenario and the Baseline for Selected Regions (2025, 2055, 2095).

These changes in timber production result from a number of adjustments that occur in markets. First, higher demand for wood materials causes prices to increase. These higher prices cause harvesting ages in productive forests to change across the world. In general, forests that are managed for timber are harvested at an age that is lower than the biologically optimal harvesting age, so more wood can be supplied from these forests by shifting to older rotation ages (Faustman, 1849). A second way to increase timber harvesting is to increase harvesting in old growth forests. Old growth forests exist in many regions around the world and can be accessed to increase wood production in periods of demand growth. A third way to increase timber harvesting is to expand productive forests, such as fast-growing timber plantations in regions like the Southern United States, Latin America, or China. A final way to increase timber harvesting is to increase management in existing stands or to increase management of newly established stands. The first two options above will mainly increase the supply of wood in the short term, while the last two options can increase supply over the longer run.

In the United States, for example, total harvesting declines initially in response to the bioenergy policies, as foresters begin to adjust the forest to a long-term increase in demand. Foresters anticipate higher prices in the future, so they withhold some wood from markets initially; as a result, the supply of wood increases in the future. The long-term increase in U.S. output is driven by an increase in forestland of 0.57 million ha by 2025 and around 5 million ha by 2055 (Fig. 7). U.S. extensive margin expansion is consistent between the Europe and World biomass scenarios. Around 20% of this expansion is due to an increase in the area of Southern pine or Douglas fir plantations. Overall forest management expenditures also increase. In the baseline, on managed land in the United States, foresters spend about $120 per ha regenerating and managing forestland. With the policy-driven increase in demand, management expenditures increase by around $26 per ha. The increase in management continues, and by mid-century, foresters are spending around 40% more per ha establishing stands in managed forests than they would have spent in the baseline. This increase in management has long-term implications for wood products supply as well as terrestrial carbon.

Fig. 7.

Change in Forestland, World Biomass Scenario Relative to the Baseline.

Canada is a contrast to the United States. For both biomass expansion scenarios, results suggest that total timber harvests increase initially in Canada and then decline over the century. This trend is perhaps surprising, but it results from the global market response that limits any price increases for sawtimber and, in fact, increases global output of sawtimber in the long run. With the global biomass scenario, Canada responds initially by harvesting more extensively in old growth forests because sawtimber prices increase initially. Over time, as sawtimber prices remain similar to their baseline level and even fall in the long run relative to the baseline, Canada harvests less old growth forest relative to the baseline. This results entirely from the global productivity response to the biomass energy scenarios that drive down sawtimber prices and reduce incentives to access old growth forests in Canada. Because Canadian forests are relatively slow growing, there is no offsetting investment response like that which occurs in the United States or Latin America. The baseline scenario projects cumulative global deforestation to exceed 100 Mha through the 2095 simulation period, though net deforestation changes over time under the influence of the bioenergy policy incentives. In the near term, global deforestation rises slightly as harvests increase. Over the medium- and long-term and under the influence of continued price growth, total forest area increases for the bioenergy expansion scenarios relative to the baseline. This change is particularly strong in regions such as Latin America, where deforestation rates decrease by approximately 20% through 2095 under the bioenergy scenarios. Such a change can be interpreted as a contraction in the future agriculture sector extensive margin, though GTM does not explicitly model what types of agricultural land would contract in future periods with lower deforestation. In some regions (such as the U.S.), total forest area increases slightly in the baseline and we see further extensive margin expansion in the bioenergy scenarios. The bulk of the U.S. afforestation is planted pine systems in the Southeast, though there is a small additional area devoted to short rotation woody coppice stands for bioenergy (less than 0.1 Mha).

In addition to shifting harvest levels of industrial roundwood for pulpwood and sawtimber markets, the bioenergy policies greatly expand collection and utilization of forest residues for pulpwood and bioenergy. In the U.S., cumulative residue supply from the 2010 to 2050 simulation periods more than doubles under the EU policy case relative to the baseline (from approximately 40 million m3 to 84 million m3) and nearly triples under the World bioenergy scenario (108 million m3). Cumulative consumption of forest residues globally also expands during the same time frame from approximately 312 million m3 under the baseline to 517 million m3 and 637 million m3, respectively, for the EU and World policy scenarios. Forest residues are fungible with pulpwood and biomass for energy use, and face the same marginal price as pulpwood. As the pulp price increases over time under the influence of demand growth and the bioenergy policy shocks, this expands residue collection and utilization globally.

One interesting question is what happens to imports and exports. There is significant concern about whether the material used for biomass energy would dramatically change the pattern of trade globally. Although our model is not a trade model, because global demand is the aggregation of regional demand for wood, we can calculate consumption by region and the net trade balance with all other regions. For the biomass energy scenarios, we include demand for biomass energy inputs following the scenario. Thus, while we cannot determine specifically which regions trade with which other regions, the model captures net trade flows on a global scale and results indicate whether each of our regions is projected to be a net importer or exporter of industrial roundwood, including biomass for energy. For this analysis of trade flows, we consider only the United States, Europe, and Canada separately and then include the rest of the world (ROW) in an ROW region (Table 3). The United States is assumed to purchase 10% of the total forest biomass material for all products over time, Europe 78%, and Canada 2%.

Table 3.

Net Imports (+) or Net Exports (−) vis-à-vis All Other Regions (Million m3/yr).

| U.S. | Europe | Canada | ROW | |||||

|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

|||||

| Baseline | World Scenario | Baseline | World Scenario | Baseline | World Scenario | Baseline | World Scenario | |

| 2015 | 60.4 | 25.8 | 26.2 | 78.1 | −18.3 | −28.1 | −795.8 | −1156.5 |

| 2025 | −23.8 | 22.4 | 21.8 | 107.9 | 12.6 | −2.4 | −569.4 | −685.4 |

| 2035 | 36.7 | 38.7 | 25.0 | 116.7 | 31.9 | 22.1 | 356.1 | −1497.3 |

| 2045 | 120.9 | 11.4 | −12.9 | 92.9 | 36.9 | 34.9 | −2227.3 | −1955.9 |

| 2055 | 100.0 | 15.1 | −54.6 | 51.2 | 30.0 | 33.9 | −672.8 | −829.3 |

| 2065 | 2.5 | −12.2 | −26.7 | 96.1 | 54.6 | 44.6 | −834.2 | −1173.0 |

| 2075 | −5.9 | −39.3 | −17.1 | 110.0 | 35.5 | 41.6 | 226.7 | −1398.3 |

| 2085 | 16.9 | −38.0 | −12.3 | 124.6 | 2.2 | 23.1 | −475.4 | −847.3 |

| 2095 | −99.2 | −139.5 | −12.9 | 134.5 | 8.3 | 8.4 | 341.2 | −1346.3 |

The United States is a modest net importer in the few decades of the simulation horizon. Over the longer run, production in the United States largely keeps up with demand, so we see increased exports from the United States. In the biomass energy scenario, U.S. net imports decline in the first half of the century, and the United States becomes a net supplier of wood to the ROW. In contrast, Europe is a net importer initially and then also becomes a net exporter over time in the baseline. With the large expansion in biomass energy demands, Europe becomes a larger net importer of wood material. Canada is initially a net exporter but becomes a net importer over time in the baseline. This result is perhaps surprising, but given the growth in more competitive timber production in other regions, Canadian timber output remains fairly stable over time, while demand grows. Even though prices are higher for pulpwood, investments are relatively modest in Canada, and long-run output does not increase substantially. The large response to the biomass energy scenario occurs in the ROW, which becomes a stronger net exporter over time.

Although there are only minor differences in market and land use outcomes when comparing the Europe and World biomass demand scenarios, the differences in the global carbon stock changes are relatively small but consequential (Fig. 8). The key result from these bioenergy expansion policies is that they increase net carbon storage in global forests, and the sign and overall magnitude of this effect is consistent across the bioenergy policy scenarios. For the Europe biomass demand scenario, forest carbon increases by 9.2 billion tons CO2 by 2025, 23.4 billion tons CO2 by 2055, and 21.4 billion tons CO2 by 2095. For the World biomass scenario, total carbon stocks grow 9.5 billion tons CO2 by 2025, 21.3 billion tons CO2 by 2055 and 15.4 billion tons CO2 by 2095.

Fig. 8.

Cumulative Change in Carbon Storage Relative to the Baseline in Land-Based and Wood Product Components (i.e., Including Market Carbon).

Investments and changes in harvesting patterns that increase the supply of timber are complementary with carbon storage, and the amount of carbon sequestered in forests increases globally with longer-term growth in bioenergy demand under the hypothetical scenarios developed for this analysis. This is true for most regions (Fig. 8). Although carbon increases on the landscape, with the aboveground, soil, and slash components increasing overall, the amount of carbon stored in durable wood products (“market carbon”) declines because some timber is shifted into biomass energy consumption. The long-term decline in carbon stocks for the World biomass scenario relative to the Europe-only case is driven by harvest trends in Europe and the ROW regions. While initial land use investments and land management changes are consistent across the two bioenergy expansion scenarios, total biomass removals and the reallocation of forest biomass from traditional markets increase under the World bioenergy expansion case. Overall, this results in less total carbon sequestration for the World bioenergy expansion scenario relative to the Europe-only scenario, although the net effect remains a large increase in total carbon storage relative to the baseline.

For the purposes of our accounting, we do not consider any fossil fuel emissions displacement that could potentially occur with the use of forest biomass for bioenergy applications, although this increased biomass energy supply could displace a portion of the emissions that otherwise would occur from fossil fuel consumption in the transportation or power sector.

Interestingly, the largest relative increases in carbon occur in the United States and Europe. The ROW increase is fairly large but is aggregated over a large area of the world’s forests. Despite the modest reduction in forestland area in Europe, the increase in carbon storage there results from shifts in harvesting patterns and age classes among managed stands. In general, the age class distribution increases in Europe, albeit modestly, and this allows for an increase in total harvest by 2025 and in the future, as well as an increase in carbon storage. The harvest increase is about 40 to 50 million m3 per year and the carbon increase is about 5.3 billion tons CO2 by 2095 under the World biomass expansion scenario, or 6.9 billion tons CO2 by 2095 for the Europe-only scenario.

4. Conclusions

This paper analyzes the forest carbon implications of large-scale increases in biomass harvesting to meet national-level energy policy scenarios over the next century. We start by reviewing the literature to project hypothetical biomass demand scenarios based on published projections of pellet and nonpellet woody biomass energy demand in various regions given current and expected policy and market conditions. We then incorporate this demand for woody biomass material into the GTM and assess the implications for woody biomass harvesting, forest investments, forest area, and carbon sequestration relative to a baseline that does not assume increased demand for woody biomass for energy production. Given that some of these policies would create a market incentive to increase in harvesting in the near term and because longer-term demands are less clear, we assume that increased demand for woody biomass energy follows the existing projections in the near term, and over the longer run, we assume that demand for woody biomass increases similarly to the demand for other wood products.

The dynamic global model of timber markets and carbon consequences used in this analysis has been updated from earlier versions to include heterogeneous products, namely sawtimber, pulpwood, and wood used for biomass energy. Wood used for biomass energy can be drawn from either type but likely will be drawn mainly from pulpwood because pulpwood prices are significantly lower.

The baseline scenario assumes that no wood is used for biomass energy aside from amounts already used as by-products of milling activities or currently drawn from markets. Thus, all demands for pellet and nonpellet biomass energy presented in Table 1 are additional to the baseline. Timber prices for both sawtimber and pulpwood are projected to increase in the future, albeit modestly. Timber outputs for both types also increase in the future, also modestly. The area of forests declines in the baseline by about 186 million ha over the next 100 years, but this rate of decline is significantly slower than the rate of reduction that has occurred in the last century.

The world biomass energy demand scenario assumes that the demand for woody-based biomass energy is around 19 million short tons per year currently, rising to 138 million short tons within a decade. About 78% of this demand occurs in Europe, with another 10% in the United States, and the rest in Canada, Russia, China, and other parts of Asia. The additional demand for biomass material amounts to about 4% of the total global timber harvest initially, rising to slightly more than 12% by 2030, and remaining approximately the same proportion of total harvest through the remainder of the simulation horizon.

Higher demand for biomass material drives pulpwood prices up by 7% initially, and by around 18% over the next 30 years. In contrast, sawtimber prices decline modestly over the next 30 years (less than 2%), and then more substantively by the end of the century, approximately 8%. Rather than devoting large areas of land to short-rotation forests that supply only biomass for final energy use, our projections suggest that the highest value on the landscape lies in producing a range of product values from traditional harvesting sites, including sawtimber. This result follows from the projected price changes from the model simulations relative to the baseline—with higher pulpwood and sawtimber prices, a large bioenergy demand shock focuses new forest resource investments on systems that produce biomass sources that are fungible across a range of commodities (traditional forest products and bioenergy). To increase production of biomass material for all end uses, foresters also increase production of sawtimber, which drives down prices. To increase timber harvests under the bioenergy scenarios, total forest area increases globally by around 6 million hectares by the end of century through reduced net deforestation in some regions (e.g., Latin America) and extensive margin expansion in others (e.g., afforestation in the U.S. region). Perhaps more importantly, total forest investments increase, particularly in regions with faster-growing forest types. In other locations, such as Europe, outputs increase with changes in the age of harvesting typical stands.

The increase in timber harvesting is shared by most regions, although in the long run Canada experiences a reduction in timber harvests as a result of the policy. This reduction results directly from the global decline in sawtimber prices, which reduce incentives for increased harvesting in inaccessible crown forests of Canada. This is perhaps surprising, but it suggests that regions like Canada with slow-growing forests will have a harder time cost-effectively increasing output to increase biomass energy production.

Our model illustrates potential carbon benefits of large-scale forest biomass demand for energy production, evaluated using hypothetical scenarios of forest biomass demand growth based on published projections of pellet and nonpellet biomass energy over the near term and adopting an assumed annual growth reflecting expected future demand growth. For the World bioenergy expansion scenarios, total carbon storage increases globally.

Even if the reallocation of biomass away from traditional pulp and sawtimber markets is counted (that is, less carbon is stored in wood product pools), the resulting carbon benefits are consistent, as net forest carbon sequestration increases (that stored on the land and in wood products) by 9.4 billion tons CO2 over the near term and 15.4 billion tons CO2 by 2095. The increases in carbon stocks are shared by most regions. Thus, even if most of the demand arises from Europe due to a particularly strong promotion of biomass energy production there, both Europe and other regions could experience increases in total carbon storage.

There are a few limitations of this analysis worth noting, however. First, as with any global economic modeling analysis, there is uncertainty in the physical and economic parameters underlying the GTM, including regional forest yield growth functions, elasticities, and other cost parameters. Uncertainty in parameters arises from measurement error or biases in variable estimation, the simplified representation of natural variability (within forest systems and across economic actors), and the inherent unknowability of future economic and physical conditions that are common to all predictive analyses.5 Previous analysis has shown that parametric uncertainty has only a modest effect on year-to-year carbon fluxes, but the cumulative effect of these flux changes could imply large uncertainty bounds for stock variables over the long term (and hence large uncertainty regarding net emissions differences between baseline and bioenergy policy scenarios). Results presented in this analysis are based on a deterministic analysis with the GTM using set parameter assumptions and thus do not capture the inherent uncertainty in physical and economic parameters. Subsequent analysis is needed to test the impact of parameter uncertainty on net carbon stock changes across different hypothetical bioenergy policy scenarios.

Second, the GTM models the forest sector only, so certain interactions with the agricultural sector, including leakage effects, are not explicitly captured. The value of agricultural land is represented in that rental functions represent the opportunity cost of maintaining an acre in forests rather than converting it to agricultural land. Additionally, rental costs increase as more land is added to the forestry area, simulating increasing pressure on forestlands the more forest acres expand. However, depending on the specific crop or region that may be affected by forestland change, leakage could be underestimated. Higher leakage impacts could mitigate forestland cover and thus the carbon stored in them.

Third, without a fully functioning agricultural sector, this analysis does not explicitly address the potential role of agricultural-derived feedstocks, including dedicated energy feedstocks like switchgrass, in competing with forestry feed-stocks to meet long-term bioenergy demand. If dedicated energy crops account for a dominant share of the global bioenergy feedstock supply, land competition between traditional and bioenergy crop cultivation and more generally between agriculture and forestry will be important to evaluate using similar dynamic economic modeling methods. Second, we apply demand shocks broadly and do not exogenously target specific feedstock groups or forest types within a particular region.

Fourth, this study does not explicitly account for projected climate change impacts and the effect that changes in temperature, precipitation, and atmospheric CO2 concentrations may have on future forest yields and hence management. Recent applications of the GTM have found similar differences across a common set of scenarios run with and without climate change impacts, although it could be important still to consider the interactions among climate change, forest bioenergy expansion scenarios, and land management.

Finally, this analysis employs a hypothetical policy design that assumes regional bioenergy expansion efforts that result in large demand perturbations in the global forestry sector. While useful for the purposes of this exercise, the analysis is not consistent with previous studies that have focused on specific policies within a country or region, specific feedstock groups, and individual supply regions. Evaluating policy-mandated changes in the consumption of particular biomass sources supplied from a given region could yield different net results than the generic global demand increases applied here in which all sources of forest biomass (including residual biomass) can contribute to the additional demand. Also, this policy design does not assume any additional GHG mitigation policies in the forest sector in conjunction with the bioenergy expansion scenarios. Reduced Emissions from Deforestation and Degradation (REDD+) and other global policy efforts to conserve forest resources for various purposes could interact directly and indirectly with the bioenergy policy scenarios considered in this analysis.

Nonetheless, this study offers an assessment of global forest carbon implications of near term bioenergy expansion efforts in multiple regions simultaneously using dynamic economic optimization of the global forest sector. Furthermore, it is possible that additional bioenergy-related activities will be implemented by countries pursuing near- and long-term climate action strategies and other efforts to support rural economic growth. Thus, evaluating the combined global implications of multiple regional bioenergy expansion efforts is critical for understanding the extent to which forest biomass energy can contribute to long-term energy security, rural economic development, and climate stabilization goals. This analysis shows that near term investments in forest resources at the intensive and extensive margins can have a lasting effect on maintaining and increasing forest carbon stocks globally.

Acknowledgments

This paper was supported by the US Environmental Protection Agency (EPA) (Contract EP-C-11-045). The views and opinions expressed in this paper are those of the authors alone and do not necessarily state or reflect those of the EPA, and no official endorsement should be inferred.

Appendix A. Global Timber Model Description

The model used in this analysis is a dynamic optimization model of the global forestry sector. It is based on the earlier global timber model described in Sohngen et al. (1999), Sohngen and Sedjo (2006), and Sohngen and Mendelsohn (2007). As such, the model maximizes the net present value of consumers’ and producers’ surplus in the forestry sector. By maximizing the net present value, the model optimizes the age of harvesting timber and the intensity of regenerating and managing forests.

The model relies on forward-looking behavior and solves all time periods at the same time. This “dynamic optimization” approach means that when land owners make decisions today about forest management, they do so by considering the implications of their actions today on forests in the future. For example, when forests are regenerated, the amount of money spent regenerating forests is determined consistent with future expectations about timber prices. In addition, when forests are harvested, forestland owners consider the marginal benefits and costs of waiting additional periods to harvest their trees. This supplemental appendix provides a general algebraic form of the model, including recent model updates such as the inclusion of heterogeneous forest product demand. In this model, sawtimber and pulpwood are drawn from the same forest resource base, which is allocated to either product after harvest. Forest resources are differentiated in several different ways, either by ecological productivity or by management and cost characteristics. To account for differences in ecological productivity, different land classes in different regions of the world will have different yield functions for timber. Data inputs used to differentiate forests by productivity are discussed below.

Furthermore, forests are broken into different types of management classes. One type is moderately valued forests (denoted by the subscript “i” below). These forests are managed in rotations and located primarily in temperate regions. A second type of management is inaccessible forest, located in regions that are costly to access. These types are denoted by the subscript “j” below. A third type is low-value forests that are lightly managed, if they are managed at all. These types are denoted by the subscript “k” in the temperate and boreal zones. These low-value lands in temperate and boreal zones are linked to inaccessible types directly, such that when inaccessible forests are harvested in boreal and temperate zones they are converted to semi-accessible forests, that is, when harvested, types in “j” convert to “k.” Inaccessible forests are harvested only when the value of accessing the land exceeds the marginal access costs.

A fourth type of forests includes low-value timberland in inaccessible (“l”) and semi-accessible (“m”) regions of the tropical zones. Inaccessible forests in this class are harvested only when the value of accessing the land exceeds the marginal access costs. They may be converted to agriculture or returned to forestry after harvesting, depending on the opportunity costs of land and the value of future timber harvests. If the lands return to forestry, they do so in a type in m that corresponds to a similar ecological productivity level in l. The key difference between the conversions of land from inaccessible to accessible but low-value land in the temperate/boreal zones and the tropics is that lands in the temperate/boreal regions are assumed to have no opportunity costs so they remain in forestry. In contrast, opportunity costs may be greater than 0 in the tropics and inaccessible or low-value accessible lands may convert to agriculture now or in the future.

A final type is the high-valued timber plantation (“n”) type that is managed intensively. These high-value forest types can be located anywhere in the world, but at present they are principally found in subtropical regions of the United States (e.g., loblolly pine plantations), South America, southern Africa, the Iberian Peninsula, Indonesia, and Oceania including Australia and New Zealand. There are numerous types of fast-growing plantations globally with various rotation ages. Southern pines in the United States have rotation ages of approximately 30 years, while pines in other parts of the world (South America, Central America, Australia, South Africa) have rotation ages of 20 years. Eucalypts have rotation ages of around 10 years. Douglas fir has a longer rotation age, of 40 years, and teak plantations have rotations of 50 or so years. The new dedicated bioenergy plantation types in the United States are placed in this category because they are assumed to be managed similarly in 10-year rotation ages.

Within the United States, we do not specifically break out land by land ownership type. The global forestry and agricultural model is a long-term modeling framework. Over the last 100 years, federal lands have been managed similarly as private lands, with timber harvests as a predominant use of the land. While these lands now are managed more for environmental purposes, their uses could change in the future, particularly as they continue to accumulate stock. Federal forestlands in this model currently are maintained in the inaccessible and semi-accessible types, which allows them to be drawn into use in the timber industry should prices rise enough to warrant such utilization.

The forestry model maximizes the present value of net welfare in the forestry sector. Net welfare is defined as the sum of consumers’ and producers’ surplus for timber markets that are derived from inverse timber demand functions and costs of managing and holding timberland. The costs of managing timberland include the costs of replanting timber and the costs of harvesting, accessing, and transporting timber. There is an opportunity cost of maintaining land in forests rather than switching to agriculture for crop cultivation and livestock grazing.

This objective function of this optimization model can be written formally as:

| (1) |

Where Table A1 describes indexes, variables, functions, and parameters in the social planner’s problem (1). The maximization problem (1) is constrained by the following (2) through (9), with details of each equation provided below:

| (2i) |

| (2j) |

| (2k) |

| (2l) |

| (2m) |

| (2n) |

| (3) |

Table A1.

Indexes, Variables, Functions, and Parameters in the Social Planner Problem.

| Category | Label | Description |

|---|---|---|

| Index | i | Moderate-value forest types in accessible regions |

| j | Low-value forest types (inaccessible regions) in temperate and boreal zones | |

| k | Low-value forest types (semi-accessible type) in temperate and boreal zones | |

| l | Low-value forest types(inaccessible regions)in tropical zones | |

| m | Low-value forest types (semi-accessible regions) in tropical zones | |

| n | High-value forest type | |

| t | Time | |

| a | Age class | |

| P | Pulpwood | |

| S | Sawtimber | |

| b | Biomass | |

| res | Residues | |

| Variable | H | The area of timber harvested (hectares) |

| N | Brand new area planted (hectares) | |

| G | The area of timber regenerated (hectares) | |

| X | Total timber area | |

| Za,t | Stock of management intensity for age class a at time t | |

| Za = 1,t | Management intensity determined at time of planting (a = 1) | |

| q or Q | Timber harvested (cubic meter) | |

| Y | The quantity of other good consumed (measured by gross domestic product (GDP) per capita) | |

| λ | The proportion of timbers for each wood product | |

| Function | V(.) | Yield function |

| D(.) | Inverse demand function | |

| C(.) | Cost of harvesting, accessing, and transporting timberland | |

| MC(.) | Marginal cost function of harvesting, accessing, and transporting timberland | |

| PLANTC(.) | Total cost function of regenerating forests including new plantation | |

| RENT(.) | The opportunity cost of holding timberland by maintaining forests rather than agricultural land use | |

| Δ . | The hectares of area changed when converted from inaccessible into semi-accessible type | |

| RESCOST(.) | Cost of collecting residues on accessible lands | |

| Parameter | φ, τ, δ, π | Parameter in yield function |

| ∅ | Constant in inverse demand functions | |

| θ | Income elasticity of demand functions | |

| ω | Price elasticity of demand functions | |

| α, β | Constant in marginal cost functions for type i, k, m, n | |

| ξ | Constant in marginal cost functions for type n (associated with transportation cost for biomass) | |

| μ, ε | Constant in marginal cost for types j, l | |

| ca, cb, cc | Constant in cost of collecting residues function | |

| e | Establishment cost for new plantation in type n | |

| r | Constant price for a unit of management intensity (Sedjo and Lyon, 1990) | |

| A, η, z | Constant in rental function | |

| d | Decadal discount factor | |

| ρ | Discounting factor |

| (4) |

| (5) |

| (6) |

| (7) |

| (8) |

| (9) |

The model solution determines how much to harvest in each age class (a) and time period (t), ; how many hectares to regenerate in each type in time period t, ; how intensively to regenerate the hectares when they are planted, ; and now many new hectares of high-value plantations to establish, Nnt.

Total timber area in each age class a and type, , is a stock variable and adjusts over time according to Eqs. (2i) through (2n). Initial stocks must be given (Eq. (3)), and all choice variables are constrained to be greater than or equal to zero (Eq. (4)). The area of timber harvesting does not exceed the total timber area (Eq. (5)).

Eq. (6) shows that each inaccessible type in temperate and boreal zones is linked to a semi-accessible type. The semi-accessible types start with no forest area. When inaccessible forests are accessed, the hectares are converted to a similar semi-accessible type. Thus, the total area of inaccessible and semi-accessible forest area in each i remains constant over the scenario time horizon. Thus, we are making an implicit assumption in temperate and boreal regions that the opportunity costs of converting land in inaccessible/semi-accessible regions is 0 and thus that the rental costs are 0.

Fig A1.

Yield for Representative Species in the Model.

In addition, Eq. (7) implies that each inaccessible type in the tropics also has a similar semi-accessible type associated with it; however as noted above, forestland is allowed to exit and enter forestry in this region. Therefore, the area regenerated in these regions may be less than or more than the area harvested or removed in any period. There are two reasons why forests may be accessed in tropical regions, either due to timber demand or demand for land conversion. The demand for land conversion is driven by the rental functions, which generally are shifting inward and upward in tropical regions (representing increasing demand for land use in agriculture). Eqs. (8) and (9) are the equations of motion for management in forest type “i” and “n” in which forests are moderately and intensively managed.

Table A1 provides a brief description of each set index, variable, function, and parameter in the model.

Forest yields (volume per hectare) are given as . The yield function measures the volume in each age class a and type i at time t. The functional form for the yield function is:

| (10) |

The functional forms for other types (j, k, l, m, n) are the same, although the parameters will differ. is the management intensity for type i at time time t. Per equation , h is the stocking density, which can be adjusted depending on the intensity of management, . We restrict stocking elasticity, τ, to be positive and less than 1. The τi affects the elasticity of management inputs in forestry to account for technology change. Initial stocking is denoted by φi. Increase in will increase h, e.g., dh/dZ>0, but the increase diminishes as rises, e.g., d2h/dZ2 <0. The model chooses management intensity by optimally choosing . Increases in management intensity will increase yield and shift the entire yield function upward. Forests are assumed to grow according to . Fig. A1 shows a representative yield function assuming h = 1.32, δ = 5.2, and π = 30

Total harvested trees are valued for either pulpwood or sawtimber in markets. Biomass energy can then be derived either from sawtimber harvests or pulpwood harvests. Let be the proportion of timber harvested for pulpwood for type i, j, k, l, m; be the proportion of timbers harvested for saw timber; and be the proportion of timbers used for bioenergy where for each i, j, k, l, m. Also, the total quantity of timber harvested in each type i is the sum of the area harvested, , times the yield per hectare, , over age class:

| (11) |

The form of Eq. (11) is also applicable for types j, k, l, m, n. Then the quantity of timber harvested for sawtimber, , for pulpwood, , for bioenergy, , and for total Qt are the following:

| (12) |

| (13) |

| (14) |

| (15) |

As noted above, the model has two types of market-valued wood: sawtimber and pulpwood, each with its own downward-sloping demand function. The inverse demand functions are shown in Eq. (16), where Yi is the quantity of other goods consumed (e.g., GDP), are constants, θis income elasticity, and ω is price elasticity:

| (16) |

The model includes many costs of managing forests and land use, including a) costs of harvesting, accessing, and transporting timbers to mills; b) costs of collecting residues to be used for bioenergy; c) costs of regenerating forests including new plantation; and d) (opportunity) costs of holding timberland. First, Eqs. (17) through (19) show that costs of harvesting, accessing, and transporting for sawtimber, pulpwood, and biomass are the following functional forms, respectively, where MCs, p, b (.) are the marginal cost functions in Eqs. (20) through (22). The forms of Eqs. (20) and (21) are also applicable for type k and m:

| (17) |

| (18) |

| (19) |

| (20) |

| (21) |

| (22) |

Second, in addition to using pulpwood and sawtimber for bioenergy, the model allows the use of forest residues for pulpwood. These residues are set to be collected from accessible timberlands. They are material that is left on the forest floor after timber is harvested. Typically this material is called slash and it is left on site. Sometimes it is collected into piles and burned. At other times, it is just left to decompose. We have assumed that some of this material can be collected and used for pulpwood, where the costs of collecting this material are modeled as:

| (23) |

where

| (24) |

In Eq. (24), 0.3 is the proportion of total forest yield that is forest residues, and 0.5 is the proportion of forest residues that can be removed from the stand.

Third, the costs of regenerating forests (including new plantation) are given as:

| (25) |

Where is the value of initial management intensity at age class one only, which is calculated by a unit of management intensity at only age class one times constant price r (Sedjo and Lyon, 1990); en is the marginal cost of establishing new hectares of plantation. The costs of establishing new plantations in fast-growing types are assumed to be fairly high because these forests are highly valuable, and they require substantial site preparation efforts to obtain such high growth rates.

Table A2.

Variables, Functions, and Parameters in the Carbon Calculations.

| Category | Label | Description |

|---|---|---|

| Variable | Carb | Carbon in age class a and time period t for timber type i |

|

|

Proportion of total wood harvest allocated to sawtimber | |

| Parameters | WD | Wood density |

| BEF | Biomass expansion factor (tons biomass per m3 wood material) | |

| R | Root-shoot ratio | |

| CF | Proportion of biomass that is carbon | |

| dr | Decomposition rate | |

| carm | Tons of carbon per m3 wood used in markets | |

|

|

Initial emission from the sawtimber or pulpwood pool | |

|

|

Wood products pool turnover (or decomposition) rate | |

| rri | Growth rate | |

| Ki | The steady state soil carbon potential for each timber type. |

For the accessible/semi-accessible type of forests (type i, k, m), it is assumed to have only regenerating trees, , and new plantation area is assumed to be only in type n. For inaccessible types j and l, which are low-value trees, both and are assumed to be zero.

Fourth, the opportunity costs of holding timberland rather than using it as agricultural land to grow crops or livestock are represented by a rental cost function, RENTt(Xa,ti,l,m,n). Inaccessible and semi-accessible lands in the temperate and boreal regions are assumed to have zero rental costs. This assumption is consistent with the internally generated bare land value returns calculated by the model for forest types in these regions. Rental costs are given as functions that increase as more land is added to the forestry area:

| (26) |

Where d is a decadal discount factor and the parameters η and A are calibrated parameters.

Carbon modeling

This section describes how carbon is calculated in the model. The methods for calculating carbon follow the Intergovernmental Panel on Climate Change (IPCC) Good Practice Guidance (Penman et al., 2003). We track carbon in four basic pools: aboveground carbon, slash, marketed products, and soils. For aboveground carbon, we calculate carbon on any given hectare in the model as:

| (27) |

The variables shown in Eq. (27) are described in Table A2. The parameters are obtained from various sources, including Penman et al. (2003) and shown in the appendix. To determine total carbon for a given timber type, we sum over the hectares in each age class as follows:

| (28) |

Total carbon for all timber types, of course, can be determined by further summing across timber types, i.