Abstract

Objective

To examine relationships between penalties assessed by Medicare's Hospital Readmission Reduction Program and Value‐Based Purchasing Program and hospital financial condition.

Data Sources/Study Setting

Centers for Medicare and Medicaid Services, American Hospital Association, and Area Health Resource File data for 4,824 hospital‐year observations.

Study Design

Bivariate and multivariate analysis of pooled cross‐sectional data.

Principal Findings

Safety net hospitals have significantly higher HRRP/VBP penalties, but, unlike nonsafety net hospitals, increases in their penalty rate did not significantly affect their total margins.

Conclusions

Safety net hospitals appear to rely on nonpatient care revenues to offset higher penalties for the years studied. While reassuring, these funding streams are volatile and may not be able to compensate for cumulative losses over time.

Keywords: Hospitals, payment policy, financial performance

The Centers for Medicare and Medicaid Services (CMS) implemented the Hospital Readmissions Reduction Program (HRRP) and the Value‐Based Purchasing Program (VBP) in 2013 to incentivize hospitals to improve health outcomes and contain costs for Medicare beneficiaries. The HRRP assesses penalties on hospitals that have higher than expected risk‐adjusted readmission rates for specific patient health conditions and procedures. The HRRP penalties were as high as 1 percent of Medicare base operating inpatient payments in 2013 and 2 percent in 2014. The VBP assesses penalties for poor performance on a broad range of metrics that span patient outcomes, processes of care, patient experience, and costs. The VBP also has opportunities for bonus payments if a hospital exceeds performance thresholds or achieves substantial improvement in metrics relative to baseline. Maximum VBP penalties and bonuses were 1.25 percent of Medicare base operating inpatient payments in both 2013 and 2014.

Several studies have shown that hospitals treating large shares of economically disadvantaged patients have experienced bigger HRRP or VBP penalties when compared to other hospitals (Joynt and Jha 2013; Gilman et al. 2014, 2015; Gu et al. 2014; Sheingold, Zuckerman, and Shartzer 2016; Thompson et al. 2017). This higher penalty burden has raised concern that risk adjustment methods employed by the HRRP and VBP may not adequately account for the complexity and costs of treating socioeconomically vulnerable patients and, thus, lead to excessive financial penalties for hospitals treating these populations (Gilman et al. 2015; Sheingold, Zuckerman, and Shartzer 2016; Thompson et al. 2017). Concern has also been expressed that HRRP and VBP programs might deepen disparities in care as hospitals typically rely on internal resources when implementing strategies to improve patient outcomes and care delivery (Gilman et al. 2015; Woolhandler and Himmelstein 2015).

Our objective was to move beyond earlier studies demonstrating differences in HRRP and VBP penalties across hospitals to assess the combined impact these programs have had on overall hospital financial performance. Specifically, we examined the relationship between changes in combined HRRP and VBP penalties and the operating and total margins for different types of hospitals. Operating margins reflect the extent to which hospitals generate net revenues from their main line of business, direct patient care. Total margins account for additional net revenues from sources such as charitable contributions, public appropriations, government transfers, investment income, and income from subsidiaries or affiliates. While nonpatient revenues may be more accessible to hospitals treating economically disadvantaged patients, these funds may not be sufficient to compensate for losses due to HRRP and VBP penalties.

Study Data and Methods

Several sources of publicly available CMS data were brought together to construct key variables for this study (CMS 2012, 2016, 2017a,b). These include annual CMS files for the HRRP and VBP penalty rates, the CMS hospital cost report that includes financial statements to construct financial ratios, and the CMS Impact File. All CMS data files and the American Hospital Association (AHA) Annual Survey contain the Medicare Provider Identification number and were merged based on this identifier. In some instances, the AHA data lacked Medicare Provider numbers and we used the American Hospital Directory (http://www.ahd.com) to obtain this information. Finally, we used the county FIPs codes in the AHA data to merge county‐level Area Health Resource File data. In total, 4,824 hospital‐year observations with complete data were analyzed, representing 2,720 unique hospitals.

We calculated the combined HRRP and VBP penalty rate assessed on each hospital for the two study years. If hospitals earned a VBP bonus, we treated the bonus as if it were a “negative” penalty. Specifically, if a hospital had a 0.5 percent HRRP penalty and a 0.3 percent VBP bonus, the combined penalty rate would be 0.2 percent for the year. This simple summing of the penalty/bonus rates was appropriate because both are applied to a hospital's Medicare base operating inpatient payments when determining payment adjustments for the two programs. We also estimated the hospital's annual dollar penalty amount given the combined penalty rate and our estimate of Medicare base operating inpatient payments for a hospital. The technical appendix provides details on the calculation of the annual dollar penalty amount.

We identified safety net hospitals treating a disproportionate share of economically disadvantaged patients in two ways. First, following recent studies, we identified hospitals in each study year that had a Medicare DSH index in the top quartile and identified these as High‐DSH (Joynt and Jha 2013; Gilman et al. 2014, 2015; Thompson et al. 2017). Second, AHA data were used to categorize hospitals by ownership type: nonfederal public, voluntary nonprofit, and for‐profit. Public hospitals, which are typically operated by state, county, or local governments, have a legal mandate to treat all individuals regardless of insurance status. Many prior research studies have considered public hospitals to be a critical component of local health care safety nets (Gaskin, Hadley, and Freeman 2001; Hadley and Cunningham 2004; Bazzoli et al. 2012; Needleman and Ko 2012).

To compare our results with those of earlier studies, we first constructed descriptive statistics, comparing HRRP/VBP penalty rates and penalty dollar amounts across various types of hospitals. Next, multivariate analysis of operating and total margins was conducted. Two sets of models were estimated: the first examining High‐DSH versus not and the second focusing on the ownership classification. The basic structure of our multivariate models was as follows:

| (1) |

where Y ht was either operating margin or total margin for hospital h in year t; HRRP/VBP was the combined penalty rate, which enters directly and with interactions by hospital type (namely High‐DSH in the first version of the models and ownership type, with nonprofit status as the reference category, in the second version of the models); H ht was a vector of hospital characteristics, M ht was a vector of market characteristics; Year2014 was a year fixed effect that is entered directly and with interactions by hospital type; ε ht was a random error term; and β and δ were estimated parameters.

A wide range of hospital and market control variables commonly used in analysis of hospital financial performance (Bai and Anderson 2016) was included as control variables in the multivariate analysis. Table 1 reports descriptive statistics on these and other study variables. Most variables are self‐explanatory, but a few require further description. Operating margin was calculated as revenues from operating sources minus operating expenses, divided by operating revenues. Total margin was calculated as total revenues from all operating and nonoperating sources minus all hospital expenses, divided by total revenues. Teaching hospitals were defined as those having one or more approved Accreditation Council for Graduate Medical Education physician residency programs. The tertiary services variable represented a sum of hospital self‐reported AHA Annual survey responses about whether a hospital provided any of 43 services considered to be high tech, as initially identified in Bazzoli et al. (1999) and modified to reflect changes in service questions in the Annual Survey. The Herfindahl‐Hirschman Index of hospital concentration was based on hospital organization market share of admissions in a county, where we combined admissions for those hospitals in a county that belonged to the same multihospital system.

Table 1.

Descriptive Statistics on Hospital Sample: Hospital‐Year Observations (Mean values with standard deviations in parentheses)

| Variable | DSH Status | Ownership Type | |||

|---|---|---|---|---|---|

| High‐DSH | Not High‐DSH | Not‐for‐Profit | For‐Profit | Public | |

| Hospital financial performance | |||||

| Operating margina , b | −6.0% (18.8) | 0.4% (12.8) | −1.11% (12.5) | 4.54% (15.1) | −9.84% (19.9) |

| Total margina , b | 2.89% (11.2) | 5.94% (10.4) | 5.34% (9.8) | 6.73% (13.5) | 2.14% (9.3) |

| Hospital characteristics | |||||

| Proportion teachinga , b | 0.475 (0.50) | 0.322 (0.47) | 0.407 (0.49) | 0.225 (0.42) | 0.316 (0.47) |

| Proportion not‐for profita | 0.544 (0.50) | 0.720 (0.45) | 1 | 0 | 0 |

| Proportion for‐profita | 0.248 (0.43) | 0.172 (0.38) | 0 | 1 | 0 |

| Proportion publica | 0.207 (0.41) | 0.108 (0.31) | 0 | 0 | 1 |

| Proportion high‐DSHb | 1 | 0 | 0.199 (0.40) | 0.322 (0.47) | 0.386 (0.49) |

| No. of staffed/setup bedsa , b | 310.30 (277.7) | 224.84 (192.3) | 261.57 (228.6) | 191.46 (161.4) | 245.19 (233.3) |

| Proportion system memberb | 0.691 (0.46) | 0.711 (0.45) | 0.719 (0.45) | 0.912 (0.28) | 0.339 (0.47) |

| No. of tertiary servicesa , b | 18.93 (9.8) | 18.21 (7.9) | 19.68 (7.8) | 13.59 (8.6) | 18.68 (8.7) |

| % of inpatient days—Medicarea , b | 43.8 (12.8) | 53.5 (12.7) | 51.7 (12.9) | 52.8 (12.5) | 45.7 (15.7) |

| % Occupancy ratea , b | 59.1 (18.5) | 56.3 (16.6) | 59.1 (16.3) | 50.5 (16.8) | 56.0 (18.9) |

| Market characteristics | |||||

| Per capita income ($000)b | 43.1 (14.8) | 43.9 (11.3) | 44.6 (12.1) | 41.8 (10.1) | 41.8 (14.9) |

| % Uninsureda , b | 17.3 (5.8) | 14.2 (5.1) | 13.8 (5.1) | 18.1 (5.6) | 16.5 (5.0) |

| % African Americana , b | 18.1 (16.1) | 10.8 (11.2) | 11.8 (12.3) | 14.1 (13.6) | 14.7 (14.9) |

| % Hispanica , b | 23.3 (22.1) | 11.6 (11.7) | 12.6 (13.3) | 20.5 (20.7) | 15.1 (17.1) |

| % Population 65+a , b | 13.6 (2.8) | 15.3 (4.0) | 15.0 (3.5) | 14.5 (4.5) | 14.9 (3.8) |

| Proportion urban areab | 0.77 (0.42) | 0.75 (0.43) | 0.777 (0.42) | 0.772 (0.42) | 0.620 (0.49) |

| Herfindahl‐Hirschman Indexa , b | 0.474 (0.33) | 0.602 (0.31) | 0.563 (0.31) | 0.515 (0.31) | 0.689 (0.33) |

| No. of observations | 1,194 | 3,630 | 3,262 | 922 | 640 |

Significant difference between High‐DSH and not High‐DSH at p < .05.

Significant difference between ownership categories at p < .05.

DSH, disproportionate share hospital.

Ordinary least squares was used to analyze the pooled 2013 and 2014 hospital data with robust standard errors to account for those hospitals that contributed two observations to the sample. Estimated parameters were then used to simulate how operating and total margins would change for different hospital groups as the HRRP/VBP penalty rate increased from the overall sample average of 0.28 percent to twice this value at 0.56 percent. The simulations created predicted values of the financial margins by treating all hospitals in the sample as if they were of a certain type (i.e., High‐DSH vs. not; public vs. nonprofit vs. for profit) but allowing other model covariates to retain their original values. These predicted values were then averaged over the entire hospital sample to obtain ceteris paribus estimates of the financial measures for the different hospital groups under study. We also conducted sensitivity analysis using the 25th and 75th percentiles of the combined HRRP/VBP penalty rate distribution to assess the sensitivity of our results to baseline assumptions. Bootstrapping with a replication sample of 300 was used to obtain estimates of the standard errors of the differences in predicted values of the financial measures at the lower and higher penalty rate levels, which allowed us to assess the statistical significance of the change in these predictions for each hospital type.

Study Results

Table 2 reports descriptive statistics on the combined penalty rates and estimated annual penalty adjustments for the different hospital types. Consistent with existing studies, we found that High‐DSH and public hospitals had significantly higher average penalty rates (0.43 percent and 0.33 percent, respectively) relative to other hospital types. For High‐DSH hospitals, this translated into significantly higher annual penalty assessments relative to not High‐DSH hospitals, both overall and per hospital bed. Our estimates of the combined penalty amounts for High‐DSH hospitals of $139,212 per year and $429 per staffed bed were consistent with those of Gilman et al. (2015), who found that 2014 average penalty assessments for High‐DSH hospitals were $115,900 per year and $436 per staffed bed.

Table 2.

Combined HRRP and VBP Penalty Statistics by Hospital DSH Status and Ownership Type: Mean Values

| Variable | DSH Status | Ownership Type | |||

|---|---|---|---|---|---|

| High‐DSH | Not High‐DSH | Not‐for‐Profit | For‐Profit | Public | |

| Penalty information | |||||

| HRRP and VBP combined penalty ratea , b (%) | 0.43 | 0.23 | 0.27 | 0.27 | 0.33 |

| Annual dollar amount of combined HRRP and VBP penaltya , b | $139,212 | $76,247 | $104,368 | $54,980 | $81,384 |

| Annual dollar amount of HRRP and VBP penalty per hospital beda , b | $429 | $287 | $345 | $272 | $284 |

Significant difference between High‐DSH and not High‐DSH at p < .05.

Significant difference between ownership categories at p < .05.

DSH, disproportionate share hospital; HRRP, Hospital Readmissions Reduction Program; VBP, Value‐Based Program. Total n = 4,824.

Our multivariate regression models (Table S1 in the technical appendix) yielded negative and highly significant associations between the main HRRP/VBP penalty rate and both operating and total margins. For safety net hospital categories defined as High‐DSH or public, these negative associations were partially offset by significant positive interactions with the HRRP/VBP penalty rate variable in the total margin models.

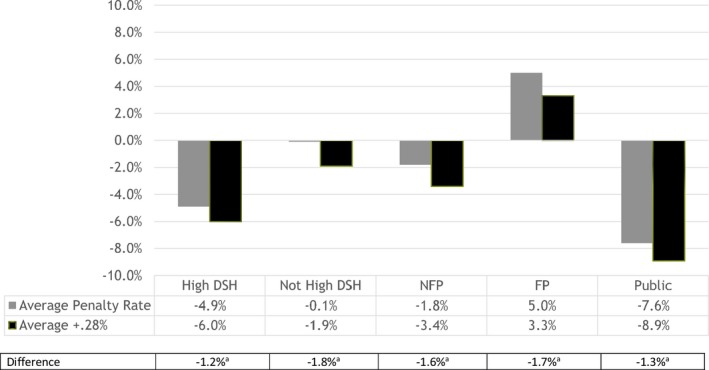

Figure 1 presents predicted operating margins for different hospital groups, first assuming the overall sample average penalty rate of 0.28 percent (grey bars) and then for the rate of 0.56 percent (black bars). As noted above, these estimates hold other factors of the multivariate model constant, including a hospital's Medicare payer share. Predicted operating margins fell by a similar amount (1.2–1.8 percentage points) across the hospital types. These declines were statistically significant at the p < .05 level for each hospital category. The operating margin declines, although similar, differ in actual value across categories because our HRRP/VBP variable is a percent of Medicare base operating revenues rather than a dollar amount or a percent of hospital total revenues.

Figure 1.

- aChange in predicted operating margin is significant at the p < .05 level based on bootstrapped standard errors of estimates.

- DSH, disproportionate share hospital; FP, for‐profit hospital; NFP, voluntary not‐for‐profit hospital; Public, nonfederal government hospital.

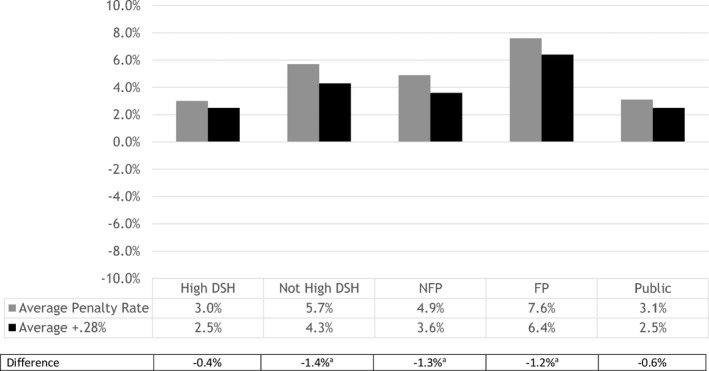

Figure 2 reports predicted total margins for the different hospital groups, again at the average penalty rate for the entire sample (gray bars) and for the rate of 0.56 percent (black bars). In this case, doubling the combined penalty rate led to a statistically significant decline in total margins for the not High‐DSH, not‐for‐profit, and for‐profit hospital categories. These declines were slightly smaller in magnitude compared to declines for operating margins in Figure 1 (i.e., −1.2 to −1.4 vs. −1.6 to −1.8 percentage points, respectively). However, the predicted declines in total margin for the High‐DSH and public hospital categories were small and not statistically significant. Appendix Tables S2 and S3 report our sensitivity analysis results using different base rates from the HRRP/VBP distribution and yielded the same pattern of results and significance for resulting changes in operating and total margins.

Figure 2.

- Notes. DSH, disproportionate share hospital; FP, for‐profit hospital; NFP, voluntary not‐for‐profit hospital; Public, nonfederal government hospital.

- aChange in predicted total margin is significant at the p < .05 level based on bootstrapped standard errors of estimates.

Discussion

Although predicted operating margins declined significantly for all hospital groups with an increase in the HRRP/VBP penalty rate, we did not find statistically significant declines in total margin for hospital categories normally considered safety net hospitals. These discrepant changes between operating margins on the one hand and total margins on the other imply that, at least for the 2 years studied, safety net hospitals relied on nonpatient revenues to fill financial gaps created by higher HRRP/VBP penalties. Forms of nonpatient revenues include charitable contributions, public appropriations, government transfers, investment income, and income from subsidiaries or affiliates. Research has shown that hospitals have historically used nonoperating revenues to offset financial losses from patient care (Singh and Song 2013); our analysis suggests that these sources were likely very important to safety net hospitals when losses arose from the HRRP/VBP programs.

Our results suggest that the HRRP/VBP penalties may not have created the financial hardship for safety net hospitals that so many had feared, at least not in initial program years. As noted by Gilman et al. (2015) and consistent with our findings in Table 2, the overall size of combined HRRP and VBP penalties was small, and from that perspective, it was most likely straightforward to identify other sources of revenues to fill gaps. However, it is important to recognize that funds used to shore up financial performance may have been diverted from important activities that address community needs, such as programs for the uninsured or homeless, local health promotion, and other types of community benefit programs. Additionally, safety net hospitals have faced large negative operating margins over time and consistently high HRRP/VBP penalties (Bazzoli, Fareed, and Waters 2014; Thompson et al. 2017). Thus, short‐term actions taken by these hospitals may not ameliorate potential long‐term financial harm that result from these penalties. This is especially important given the uncertain future of Medicaid reimbursement and DSH funding and also potential growth in the number of uninsured if major parts of the Affordable Care Act are repealed or allowed to fail.

Finally, even if safety net hospitals continue to be able to patch together nonpatient care revenues to fill financial voids from HRRP and VBP, other concerns remain. The primary intent of value‐based programs is to promote better care for patients; their effectiveness may be reduced if hospitals use nonpatient revenue to fill financial gaps from these programs rather than devoting such resources to improving performance on value‐based metrics. These financial workarounds, although helpful to hospitals in sustaining themselves or as a response to the complex design of some pay‐for‐performance programs, may under‐cut the incentives that these performance programs attempt to instill.

Our analysis has certain limitations that must be recognized. First, we used secondary data with well‐acknowledged issues. The hospital financial data we analyzed came from Medicare cost reports and only receive desk reviews by CMS. Thus, they may have data quality problems (Magnus and Smith 2000; Kane and Magnus 2001). We examined several years of financial performance that extended back to 2009 to assess trends and to identify and eliminate observations with extremely low or high margins so they would not distort results. Hospital data reported in the AHA Annual Survey and CMS cost reports are self‐reported and thus subject to measurement error. Our analysis was limited to only 2 years of data (2013 and 2014) given reporting lags for some data sources, especially delays in the reporting of CMS hospital cost report data used to construct financial ratios. A longer time series may be able to shed additional light on whether safety net hospitals rely on nonpatient revenues over time to insulate themselves from accumulating HRRP/VBP penalties.

Our findings add to the growing consensus about the need for better risk adjustment of HRRP and VBP to account for patient socioeconomic factors so that hospitals have meaningful and achievable performance targets. This will be increasingly important as the value‐based purchasing movement continues to grow and, thus, the financial stakes for failing to meet performance targets become higher.

Supporting information

Appendix SA1: Author Matrix.

Appendix SA2:

Table S1. Multivariate Regression Models for Financial Performance Measures (Coefficients and significance levels based on robust standard errors reported).

Table S2. Predicted Operating Margin with Simulated Penalty Increase: Calculated at Overall Average, 25th Percentile, and 75th Percentile Penalty Levels.

Table S3. Predicted Total Margin with Simulated Penalty Increase: Calculated at Overall Average, 25th Percentile, and 75th Percentile Penalty Levels.

Acknowledgments

Joint Acknowledgment/Disclosure Statement: This research was supported by a grant from the Agency for Healthcare Research and Quality R01 HS023783, Teresa M. Waters, Principal Investigator, and Gloria J. Bazzoli and Michael P. Thompson, co‐investigators. No other disclosures.

Disclosures: None.

Disclaimer: None.

References

- Bai, G. , and Anderson G. F.. 2016. “A More Detailed Understanding of Factors Associated with Hospital Profitability.” Health Affairs (Millwood) 35 (5): 889–97. [DOI] [PubMed] [Google Scholar]

- Bazzoli, G. J. , Fareed N., and Waters T. M.. 2014. “Hospital Financial Condition in the Recent Recession and Implications for Institutions That Remain Financially Weak.” Health Affairs (Millwood) 33 (May): 739–44. [DOI] [PubMed] [Google Scholar]

- Bazzoli, G. J. , Shortell S. M., Dubbs N., Chan C., and Kralovec P.. 1999. “A Taxonomy of Healthcare Networks and Systems: Bringing Order out of Chaos.” Health Services Research 33 (1): 1683–717. [PMC free article] [PubMed] [Google Scholar]

- Bazzoli, G. J. , Lee W., Hsieh H. M., and Mobley L. R.. 2012. “The Effects of Safety Net Hospital Closures and Conversions on Patient Travel Distance for Hospital Care.” Health Services Research 47 (February, Part 1): 129–50. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Centers for Medicare and Medicaid Services (CMS) . 2012. “Acute Inpatient PPS. Historical Impact Files for FY1994 through Present” [accessed on July 5, 2017]. Available at https://www.cms.gov/Medicare/Medicare-Fee-for-Service-Payment/AcuteInpatientPPS/Historical-Impact-Files-for-FY-1994-through-Present.html

- Centers for Medicare and Medicaid Services (CMS) . 2016. “Acute Inpatient PPS, Hospital Readmissions Reduction Program” [accessed on cited July 5, 2017]. Available at https://www.cms.gov/medicare/medicare-fee-for-service-payment/acuteinpatientpps/readmissions-reduction-program.html

- Centers for Medicare and Medicaid Services (CMS) . 2017a. “Hospital Value Based Purchasing” [accessed on July 5, 2017]. Available at https://www.cms.gov/Medicare/Quality-Initiatives-Patient-Assessment-Instruments/hospital-value-based-purchasing/index.html?redirect=/hospital-value-based-purchasing

- Centers for Medicare and Medicaid Services (CMS) . 2017b. “Acute Inpatient PPS. FFY2017 IPPS Final Rule Home Page Items” [accessed on July 5, 2017]. Available at https://www.cms.gov/Medicare/Medicare-Fee-for-Service-Payment/AcuteInpatientPPS/FY2017-IPPS-Final-Rule-Home-Page.html

- Gaskin, D. J. , Hadley J., and Freeman V. G.. 2001. “Are Urban Safety Net Hospitals Losing Low‐Risk Medicaid Maternity Patients?” Health Services Research 36 (February, Part I): 25–51. [PMC free article] [PubMed] [Google Scholar]

- Gilman, M. , Adams E. K., Hockenberry J. M., Wilson I. B., Milstein A. S., and Becker E. R.. 2014. “California Safety‐Net Hospitals Likely to Be Penalized by ACA Value, Readmission, and Meaningful Use Programs.” Health Affairs (Millwood) 33 (8): 1314–22. [DOI] [PubMed] [Google Scholar]

- Gilman, M. , Hockenberry J. M., Adams E. K., Milstein A. S., Wilson I. B., and Becker E. R.. 2015. “The Financial Effect of Value‐Based Purchasing and the Hospital Readmissions Reduction Program on Safety‐Net Hospitals in 2014: A Cohort Study.” Annals of Internal Medicine 163 (6): 427–36. [DOI] [PubMed] [Google Scholar]

- Gu, Q. , Koenig L., Faerberg J., Steinberg C. R., Vaz C., and Wheatley M. P.. 2014. “The Medicare Hospital Readmissions Reduction Program: Potential Unintended Consequences for Hospitals Serving Vulnerable Populations.” Health Services Research 49 (3): 818–37. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Hadley, J. , and Cunningham P.. 2004. “Availability of Safety Net Providers and Access to Care of Uninsured Persons.” Health Services Research 39 (October): 1527–46. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Joynt, K. E. , and Jha A. K.. 2013. “Characteristics of Hospitals Receiving Penalties under the Hospital Readmissions Reduction Program.” Journal of the American Medical Association 309 (4): 342–3. [DOI] [PubMed] [Google Scholar]

- Kane, N. M. , and Magnus S. A.. 2001. “The Medicare Cost Report and the Limits of Hospital Accountability: Improving Financial Accounting Data.” Journal of Health Politics, Policy, and Law 26 (February): 81–105. [DOI] [PubMed] [Google Scholar]

- Magnus, S. A. , and Smith D. G.. 2000. “Better Medicare Cost Report Data Are Needed to Help Hospitals Benchmark Costs and Performance.” Health Care Management Review 25 (Fall): 65–76. [DOI] [PubMed] [Google Scholar]

- Needleman, J. , and Ko M.. 2012. “The Declining Public Hospital Sector” In The Health Safety Net in a Post‐Health Care Reform World, edited by Hall M., and Rosenbaum S., pp. 200–16. Piscataway, NJ: Rutgers University Press. [Google Scholar]

- Sheingold, S. H. , Zuckerman R., and Shartzer A.. 2016. “Understanding Medicare Hospital Readmission Rates and Differing Penalties between Safety‐Net and Other Hospitals.” Health Affairs (Millwood) 35 (1): 124–31. [DOI] [PubMed] [Google Scholar]

- Singh, S. R. , Song P. H.. 2013. “Nonoperating Revenue and Hospital Financial Performance: Do Hospitals Rely on Income from Nonpatient Care Activities to Offset Losses on Patient Care?” Health Care Management Review 38 (3): 201–10. [DOI] [PubMed] [Google Scholar]

- Thompson, M. P. , Waters T. M., Kaplan C. M., Cao Y., and Bazzoli G. J.. 2017. “Most Hospitals Received Annual Penalties for Excess Readmissions, But Some Fared Better Than Others.” Health Affairs (Millwood) 36 (5): 893–901. [DOI] [PubMed] [Google Scholar]

- Woolhandler, S. , and Himmelstein D. U.. 2015. “Collateral Damage: Pay‐for‐Performance Initiatives and Safety‐Net Hospitals.” Annals of Internal Medicine 163 (6): 473–4. [DOI] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Appendix SA1: Author Matrix.

Appendix SA2:

Table S1. Multivariate Regression Models for Financial Performance Measures (Coefficients and significance levels based on robust standard errors reported).

Table S2. Predicted Operating Margin with Simulated Penalty Increase: Calculated at Overall Average, 25th Percentile, and 75th Percentile Penalty Levels.

Table S3. Predicted Total Margin with Simulated Penalty Increase: Calculated at Overall Average, 25th Percentile, and 75th Percentile Penalty Levels.