Abstract

Objective

To examine whether market competition is associated with improved health outcomes in hemodialysis.

Data Sources

Secondary analysis of data from a national dialysis registry between 2001 and 2011.

Study Design

We conducted one‐ and two‐part linear regression models, using each hospital service area (HSA) as its own control, to examine the independent associations among market concentration and health outcomes.

Data Collection

We selected cohorts of patients receiving in‐center hemodialysis in the United States at the start of each calendar year. We used information about dialysis facility ownership and the location where patients received dialysis to measure an index of market concentration—the Hirschman‐Herfindahl Index (HHI)—for HSA and year, which ranges from near zero (perfect competition) to one (monopoly).

Principal Findings

An average reduction in HHI by 0.2 (one standard deviation in 2011) was associated with 2.9 fewer hospitalizations per 100 patient‐years (95 percent CI, 0.4 to 5.4). If these findings were generalized to the entire in‐center hemodialysis population, this would translate to 8,100 (95 percent CI 1,200 to 15,000) fewer hospitalizations in 2011. There was no association between change in market competition and mortality.

Conclusions

Market competition in dialysis may lead to improved health outcomes.

Keywords: Competition, dialysis, health outcomes

Due to federal law, nearly every patient with end‐stage renal disease (ESRD) in the United States qualifies for and receives Medicare, regardless of age or disability status (USRDS 2013). Over the past three decades, Medicare reimbursement policy has emphasized provision of low‐cost outpatient dialysis care, contributing to industry consolidation (Hirth et al. 1999; Himmelfarb et al. 2007). Currently, two corporations provide care for more than 70 percent of patients receiving dialysis in the United States (Medicare Payment Advisory Commission 2015). Prior to the enactment in 2011 of the ESRD Prospective Payment System (PPS), or payment “bundle,” local dialysis markets were highly concentrated by conventional standards (Erickson et al. 2016). Additional financial pressures faced by dialysis facilities since enactment of the PPS and its associated pay‐for‐performance quality initiatives may further industry consolidation (Sedor et al. 2010; Johnson, Meyer, and Johnson 2011).

While consolidation in the dialysis industry has been occurring for several decades, it has recently occurred in other health care markets as well. Passage of the Affordable Care Act coincided with a series of recent hospital mergers and concern that integration in other areas of health care delivery (such as physician services) may lead to more widespread consolidation (Dafny 2014; Tsai and Jha 2014). It is unknown whether—and in what circumstances—market competition affects the quality of care provided and health outcomes. Evidence from selected health care markets in the United States and abroad where government regulation “fixes” prices, thereby forcing providers to compete on quality, suggests that competition leads to higher‐quality care and better health outcomes (Gaynor 2006; Gaynor and Town 2012). Because prices for 85 percent of patients receiving dialysis in the United States are fixed by Medicare reimbursement policy, a similar relation between competition, quality, and health outcomes may exist in dialysis care.

In this study, we examined associations among competition in U.S. dialysis markets and major health outcomes—mortality and hospitalization—in patients receiving in‐center hemodialysis. Understanding whether market competition has a role in preserving quality of care and health outcomes in hemodialysis can guide future reimbursement policies and quality initiatives directed at dialysis providers and may inform policy in other areas of medicine, particularly those dominated by fixed prices.

Methods

Data and Patient Selection

We identified patients receiving in‐center hemodialysis in the United States on January 1 of each year from 2001 through 2011 from the U.S. Renal Data System, a national registry of nearly every patient with ESRD. The registry contains patient health, demographic, socioeconomic, and insurance information, eligible patients’ Medicare claims, and annual dialysis facility surveys. We obtained information about dialysis facility addresses and ownership from the Centers for Medicare and Medicaid Services Dialysis Facility Compare. We linked patient zip codes to census‐based rural–urban commuting area codes (WWAMI 2005) and data from the Dartmouth Atlas Project (Fisher et al. 2009) to identify population density and assign patients to hospital service areas (HSAs). Because we selected a new patient cohort each calendar year, patients could appear in our dataset more than once if they received in‐center hemodialysis in multiple years. On January 1 of each year, we used the prior six months of Medicare claims to ascertain and update patients’ medical comorbidities and dialysis locations.

We focused on markets for in‐center hemodialysis, which is the predominant method of dialysis therapy in the United States. Fewer than 10 percent of patients at any time in the study period received dialysis at home (USRDS 2013). While home dialysis (e.g., home hemodialysis and peritoneal dialysis) may, in some instances, be a substitute for in‐center hemodialysis, patients receiving home‐based therapies are often different in important ways from those receiving in‐center hemodialysis. Decisions about whether to receive home versus in‐center hemodialysis reflect patient health, socioeconomics, and demographics (Xue et al. 2002), along with individual preferences and differences in access to pre‐ESRD nephrology care (Wilson and Nissenson 2002; Bass et al. 2004; Mehrotra et al. 2005). Due to these differences, we considered home dialysis to represent a different market.

We also excluded patients receiving dialysis at Veterans Affairs facilities, prisons, and military facilities, who were less likely to have a choice about where they received dialysis. When calculating indices of market concentration, we examined dialysis facility choices among all other patients receiving in‐center hemodialysis. In the analytic cohort, we examined the relation between market competition and health outcomes among patients with primary Medicare Parts A and B coverage and ESRD for at least six months prior to the start of each calendar year, for whom we could ascertain comorbidities and hospitalizations using Medicare claims.

Study Exposure

The study exposure was the Hirschman‐Herfindahl Index (HHI), an index of market concentration commonly used in industrial organization economics and by regulatory agencies (Church and Ware 2000; Federal Trade Commission 2013). The HHI is the sum of squares of market share and can range from near zero to one. A market for dialysis would have an HHI near zero if there were many competing dialysis facilities available from which patients can (and do) choose to receive dialysis, while an HHI equals one if there were only one dialysis facility or service organization. An HHI of 0.5 represents a duopoly, where two facilities of equal size share the market.

We assigned an HHI to each HSA annually, based on where patients receiving in‐center hemodialysis lived and the facilities where they received dialysis at the start of each calendar year. We used a method for calculating HHI that avoids bias associated with defining discrete market boundaries, has been used previously to study competition in hospital, dialysis, and physician markets (Kessler and McClellan 2000; Lee, Chertow, and Zenios 2010; Baker et al. 2014), and is closely linked to the number of dialysis facility choices available to patients (Erickson et al. 2016). Because we calculated an HHI for each HSA on January 1 of each calendar year, our competition metric did not account for patients moving to other facilities during the year (Exhibit 1 in Appendix SA2).

Study Outcomes and Comorbidities

The primary study outcomes were the number of all‐cause hospitalizations per year and the annual probability of death (reported as hospitalizations and deaths per 100 patient‐years). Each year, we followed patients from January 1 through December 31 to ascertain outcomes. Secondary outcomes were the probability of at least one hospitalization for infection, dialysis vascular access complication, or cardiovascular disease (CVD). We used the primary International Classification of Diseases, Ninth Revision, codes from hospitalization claims to identify hospitalization cause.

When examining the number of all‐cause hospitalizations per year, we censored patients for death, kidney transplantation, change from in‐center hemodialysis to home dialysis, or change to a non‐Medicare insurance provider. Due to differences in length of follow‐up, we standardized hospitalizations per year by multiplying the number of hospitalizations per follow‐up day by 365. We did not include hospitalizations in the week prior to kidney transplantation, as these were likely related to the transplant procedure. We did not censor patients when examining the annual probabilities of death or cause‐specific hospitalization. In all analyses, we controlled for the calendar year, time on dialysis prior to January 1 of each year, patient health status, demographic and socioeconomic characteristics, and dialysis facility characteristics listed in Table 1, as well as population density.

Table 1.

Baseline Characteristics Stratified by Level and Change in Market Concentration

| More Competitive (Lower 1/2 of HHI) | Less Competitive (Upper 1/2 of HHI) | p‐Value for Difference | Competition Increaseda | Competition Decreaseda | p‐Value for Difference | |

|---|---|---|---|---|---|---|

| (%) | (%) | (pp Change) | (pp Change) | |||

| Patient‐years (years) | 969,742 | 969,718 | 899,106 | 839,306 | ||

| Demographic characteristics | ||||||

| Mean age—years | 61.5 | 62.6 | <.001 | 0.08 | 0.16 | .10 |

| Male | 53.8 | 52.9 | <.001 | 0.11 | −0.02 | .43 |

| Black | 48.2 | 34.7 | <.001 | 0.07 | 0.00 | .35 |

| Native American | 0.8 | 2.5 | <.001 | 0.05 | 0.00 | .31 |

| White | 46.1 | 59.7 | <.001 | −0.16 | −0.04 | .21 |

| Other race | 4.9 | 3.1 | <.001 | 0.04 | 0.04 | .88 |

| Hispanic ethnicity | 13.4 | 8.8 | <.001 | 0.04 | 0.15 | .12 |

| Medical comorbidities | ||||||

| Cerebrovascular disease | 11.0 | 10.0 | <.001 | 0.12 | 0.01 | .45 |

| Peptic ulcer disease | 7.5 | 6.7 | <.001 | −0.08 | −0.11 | .80 |

| Coronary heart disease | 14.0 | 13.1 | <.001 | −0.10 | 0.00 | .57 |

| Heart failure | 31.3 | 30.6 | <.001 | 0.55 | 0.57 | .94 |

| Lung disease | 17.4 | 19.1 | <.001 | 0.71 | 1.02 | .10 |

| HIV positive | 1.8 | 0.7 | <.001 | 0.04 | 0.01 | .15 |

| Malignancy | 5.2 | 5.1 | <.001 | 0.15 | 0.09 | .55 |

| Dementia | 3.5 | 2.9 | <.001 | 0.17 | 0.08 | .26 |

| Diabetes | 50.1 | 51.8 | <.001 | 1.05 | 1.11 | .77 |

| Liver disease | 7.3 | 5.3 | <.001 | 0.32 | 0.17 | .16 |

| Paralysis | 1.8 | 1.5 | <.001 | 0.01 | −0.04 | .36 |

| PVD | 19.1 | 17.8 | <.001 | 0.20 | 0.08 | .53 |

| Rheumatologic disease | 2.5 | 2.3 | <.001 | 0.01 | −0.02 | .61 |

| Failed transplant | 8.8 | 7.8 | <.001 | −0.66 | −0.72 | .49 |

| Time on dialysis—months | 48.5 | 45.3 | <.001 | 1.04 | 1.14 | .31 |

| Nursing home | 8.0 | 8.3 | <.001 | 0.34 | 0.36 | .91 |

| Drug or alcohol abuse | 2.3 | 2.0 | <.001 | 0.08 | −0.07 | .01 |

| Smokes | 3.5 | 4.0 | <.001 | 0.25 | 0.14 | .25 |

| Geographic, facility, and socioeconomic | ||||||

| Medicaid eligible | 48.5 | 46.4 | <.001 | 0.05 | 0.35 | .07 |

| For‐profit facility | 79.5 | 81.2 | <.001 | 0.54 | 0.35 | .24 |

| Free‐standing facility | 88.1 | 89.9 | <.001 | 0.92 | 0.66 | .03 |

| Facility size—no. of patients | 110.6 | 91.6 | <.001 | −0.88 | 0.54 | <.001 |

| Rural or small town | 2.4 | 18.8 | <.001 | −0.1 | 0.7 | .01 |

Notes: The complete analytic cohort includes 632,734 patients and 1,939,460 patient‐years. Distribution of patient‐years over time was as follows: 7.3% in 2001, 7.8% in 2002, 8.4% in 2003, 8.7% in 2004, 9.1% in 2005, 9.3% in 2006, 9.5% in 2007, 9.6% in 2008, 9.9% in 2009, 10.0% in 2010, and 10.4% in 2011. Baseline characteristics assessed after pooling all HSA‐years. “pp” is percentage point. PVD is peripheral vascular disease. HHI is Hirschman‐Herfindahl index. Mean HHI in more competitive regions is 0.30; mean HHI in less competitive regions is 0.65. p‐Values represent statistical significance of differences in each characteristic between high versus low HHI areas and between areas where HHI increased versus decreased in one year.

The second panel only includes hospital service areas (HSAs) when patients received dialysis in two consecutive years. Patients dialyzed in 2011 (the final year of analysis) were excluded from comparison of characteristics by change in HHI.

Study Design and Statistical Analysis

We used separate multivariable linear probability models to examine the associations between market competition, probability of death, and probability of each cause‐specific hospitalization. We used cluster‐robust standard errors to account for heteroscedasticity and repeated measures involving the same patient (Huber 1967). We identified indices of market competition and examined outcomes of interest for all patient‐years between 2001 and 2011.

We used a two‐part “hurdle” model to examine the association between market competition and the number of all‐cause hospitalizations in a given year. A major advantage of the two‐part model is that it allows model covariates (including HHI) to have a different association with the likelihood of at least one hospitalization and repeat hospitalizations. This additional flexibility is important considering evidence in dialysis and other areas of health care indicating a potentially unique link between repeat hospital admissions and the quality of care delivered (Bradley et al. 2014; Erickson et al. 2014; Ryan et al. 2017).

In the first part of the two‐part model, we included all patient‐years in a linear probability model to estimate the probability of a hospitalization in a year as a function of market concentration and model covariates. In the second part of the model, we restricted the population to those hospitalized at least once in a given year and used linear regression to estimate the (log‐transformed) number of hospitalizations per year as a function of market concentration and the same covariates. We used linear regression due to its computational feasibility and previously demonstrated accuracy in predicting health care use in two‐part models (Eichner, McClellan, and Wise 1997). For each patient in our cohort, we used estimates from the two‐part model to predict the marginal effect of a one‐unit change in HHI on the number of hospitalizations per year (Mullahy 1998). We took the average of predicted marginal effects across all patients and obtained block‐bootstrap standard errors from 200 simulations to account for repeated observations within patients (Exhibit 2 in Appendix SA2).

To present our findings in the way most relevant to clinicians and policy makers, we used our mortality and all‐cause hospitalization model results to predict the change in outcomes per 100 patient‐years that would occur if dialysis markets were more competitive by one standard deviation in 2011, equal to a change in HHI of 0.2. We applied our primary regression results to data on the number of patients receiving in‐center hemodialysis in the United States to predict the expected change in hospitalizations per year in the United States from a decline in HHI of 0.2 in all HSAs. We described the expected change in outcomes in hypothetical market scenarios where the entry of a new dialysis facility into markets equally shared among competing organizations gives patients one additional choice among competing facilities. Finally, we used the average amount paid by Medicare for hospitalizations ($16,000 USD) among patients receiving in‐center hemodialysis in 2010 (USRDS 2013) to estimate potential cost savings associated with each hypothetical market scenario (Exhibit 3 in Appendix SA2).

Addressing Geographic Differences in Health and Health Care Use

It is possible that HHI partially reflects differences in health status across regions that are not fully captured by control variables. For example, while there are fewer competing dialysis providers in less densely populated areas (Erickson et al. 2016), evidence suggests that health outcomes and quality of care are worse among patients with kidney disease who live in more remote areas (Rucker et al. 2011; Thompson et al. 2012). If worse health outcomes and quality of care in remote areas are merely associated with (and not caused by) differences in the numbers of competing dialysis providers, our study could be biased toward concluding that less market competition is bad for patient health.

To address this potential source of bias, we included in our analyses geographic “fixed effects.” Fixed effects have been used to study competition in health care markets (Jung and Polsky 2014) in order to account for observed—and unobserved—differences among geographic areas that do not change over time. We included fixed effects at the level of each HSA, effectively focusing our analyses on changes in market competition and health outcomes within HSAs. Due to persistent financial pressures faced by some dialysis facilities and growth in the dialysis population, we expected that changes in market concentration over time within HSAs are more likely a consequence of economic constraints and opportunities than changes in patient health. To verify this, we described changes in observable patient characteristics within HSAs after stratifying by change over time in HHI (Table 1).

Additional Analyses

We examined several alternative model specifications (Exhibit 4a in Appendix SA2). First, we conducted a “stacked cross‐sectional” model to examine the associations between HHI and each outcome while controlling for all model covariates except for HSA fixed effects. Because this model did not include HSA fixed effects, we included additional socioeconomic characteristics at the HSA‐level obtained from the U.S. Census. We examined a model with an index of market competition based on the zip codes where patients lived rather than HSA and using zip‐code fixed effects. Finally, we aggregated all patient characteristics within dialysis facilities in each year and examined a dialysis facility‐level model, where each facility‐year represented one observation. In this model, we used a measure of HHI calculated at the dialysis facility‐level (step 2 in the calculation of HHI; Exhibit 1 in Appendix SA2) and linear regression with HSA fixed effects to examine the associations between market competition and health outcomes.

A commonly cited concern in studies of competition in health care is that the quality of care provided may simultaneously influence health outcomes and indices of market competition. This could happen, for example, if patients choose to travel farther to receive higher‐quality care (Kessler and McClellan 2000). We examined our model's sensitivity to this potential “endogeneity” of HHI by creating a modeled index of market competition that uses distances between patients’ homes and dialysis facilities to predict where patients would choose to receive dialysis. This method was originally developed to address bias in studies of hospital markets and has since been adapted to the study of dialysis and home health markets (Exhibit 5 in Appendix SA2; Kessler and McClellan 2000; Brooks et al. 2006; Lee, Chertow, and Zenios 2010; Jung and Polsky 2014) We also examined the sensitivity of our findings to geographic differences in Medicare Advantage penetration, controlling for specific dialysis facility chains and changes in the number of dialysis facilities within HSAs, and nonlinearity in the associations between HHI and health outcomes (Exhibit 4b in Appendix SA2).

Results

Our analytic cohort included 632,734 patients (1,939,460 patient‐years) with Medicare Parts A and B receiving in‐center hemodialysis between 2001 and 2011 living in 3,379 HSAs. Calculations of market concentration were based on all patients receiving in‐center hemodialysis and included 3,228,376 patient‐years. In all results, unless otherwise noted, we report HHIs calculated at the HSA level from the method described in Exhibit 1 in Appendix SA2. The mean HHI was 0.48 (SD 0.21). Although on average market concentration did not change within HSAs between 2001 and 2011 (mean change 0.002), the change in HHI within HSAs varied substantially (SD of change was 0.15) and approximately one‐half of markets became more concentrated over the decade. To describe trends in HHI over time, we stratified HSAs based on the magnitude of the overall change in HHI between 2001 and 2011. The median changes in HHI per HSA between 2001 and 2011 for the first, second, and third tertiles of HHI change were −0.12, 0.001, and +0.13, respectively. Areas that became more competitive over the decade were slightly less competitive, on average, at the start of the decade (Exhibit 6 in Appendix SA2).

After pooling all patient‐years, we stratified each HSA‐year by both the level of HHI and magnitude of year‐to‐year change in HHI. We compared patient, geographic, and facility characteristics within HHI strata and year‐to‐year HHI change (Table 1). When comparing patients living in areas in the upper versus lower half of HHI, we observed significant differences in every patient, geographic, and facility characteristic. In contrast, changes in nearly every observable characteristic were similar across strata of HHI change. Of 30 characteristics compared across year‐to‐year HHI change per HSA, only four differed more in years with increases in HHI compared to years when the HHI decreased or remained the same.

Market Concentration and Mortality

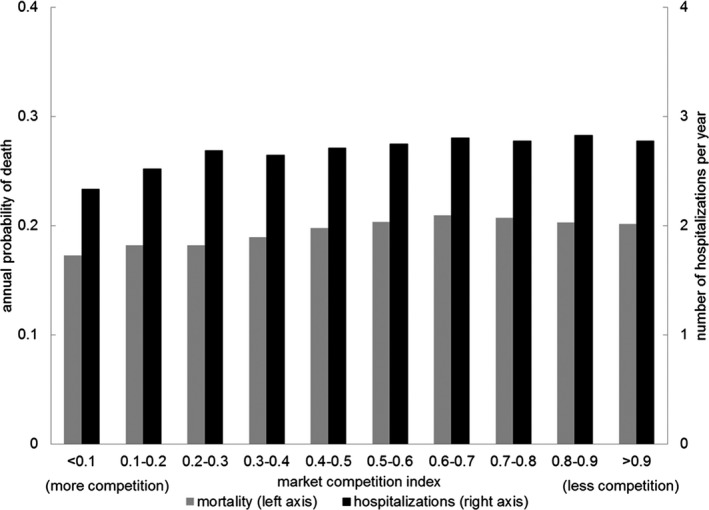

The annual probability of death was 20 percent during the study period and ranged from 21 percent before 2004 to 17 percent in 2010. There was a slight unadjusted trend toward increased probability of death in areas that were less competitive (Figure 1). After adjusting for patient and dialysis facility characteristics and HSA fixed effects, there was no association between market concentration and mortality (Tables 2a and 3).

Figure 1.

- Note: Market competition index is the Hirschman‐Herfindahl Index (HHI). Mortality and hospitalizations were positively associated with increasing category of HHI (i.e., less competition was associated with more hospitalizations and higher probability of death) in a univariate model. p‐Value for HHI in both models was <.01. The average annual probability of death throughout the entire study period was 0.2. The average number of hospitalizations per year throughout the study period was 2.7.

Table 2.

Regression Results Evaluating the Associations between Changes in Market Competition (a 0.2 Point Increase in Hirschman‐Herfindahl Index) and Health Outcomes. (a) Dependent Variable: Estimated Increase in Deaths per 100 Person‐years. (b) Dependent Variable: Estimated Increase in Hospitalizations per 100 Person‐years

| Primary Model (HSA Fixed Effects) | Zip‐Code HHI Model (Zip‐Code Fixed Effects) | Dialysis Facility‐Level Model (HSA Fixed Effects) | Stacked Cross‐Sectional Model (No Fixed Effects) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Unit of Market Competition Based on Hospital Service Area | Unit of Market Competition Based on Zip Code | Unit of Market Competition Based on Dialysis Facility | Unit of Market Competition Based on Hospital Service Area | ||||||||

| (a) | |||||||||||

| No. of deaths | LCI | UCI | No. of deaths | LCI | UCI | No. of deaths | LCI | UCI | No. of deaths | LCI | UCI |

| 0.0 | −0.2 | 0.1 | 0.0 | −0.2 | 0.2 | 0.2 | −0.1 | 0.5 | 0.4 | 0.3 | 0.5 |

| (b) | |||||||||||

| No. of hospitalizationsa | LCI | UCI | No. of hospitalizationsa | LCI | UCI | No. of hospitalizationsa | LCI | UCI | No. of hospitalizationsa | LCI | UCI |

| 2.9 | 0.4 | 5.4 | 2.3 | −0.3 | 4.9 | 8.8 | 2.3 | 15.3 | 8.6 | 6.3 | 10.9 |

Notes: HSA is hospital service area. HHI is Hirschman‐Herfindahl Index. LCI and UCI are lower and upper 95% confidence intervals, respectively. See Table 3 for full model results involving the primary regression analyses, and Exhibit 4 in Appendix SA2 for results involving additional model specifications.

Results from the initial two‐part regression models examining the association between HHI and number of hospitalizations are described in Table S3. These were transformed to predicted change in hospitalizations per 100 patient‐years associated with a change in HHI of 0.2 as described in Exhibit 3a in Appendix SA2. Results from each part of the two‐part Zip Code, Dialysis Facility‐Level, and Stacked Cross‐sectional Models are included Exhibits 4a, 4b, and 4c in Appendix SA2, respectively.

Table 3.

Detailed Regression Results from Primary Models Examining Hospitalization and Mortality

| Two‐part Model (First Stage) a | Two‐part Model (Second Stage) a | Mortality Model | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Dependent Variable | (Probability of at Least One Hosp.) | (log No. of Hosp. Given at Least One) | (No. of Deaths per 100 Patient‐years) | ||||||

| Coef. | LCI | UCI | Coef. | LCI | UCI | Coef. | LCI | UCI | |

| Herfindahl index (0.2 change) | 0.001 | −0.001 | 0.003 | 0.006 | 0.002 | 0.011 | 0.0 | −0.2 | 0.1 |

| Male | −0.040 | −0.041 | −0.039 | −0.045 | −0.048 | −0.041 | 1.3 | 1.2 | 1.4 |

| Race (White reference) | |||||||||

| Black | 0.005 | 0.003 | 0.007 | −0.012 | −0.017 | −0.008 | −5.1 | −5.3 | −5.0 |

| Native American | 0.000 | −0.007 | 0.007 | −0.018 | −0.035 | −0.002 | −2.5 | −3.1 | −2.0 |

| Other | −0.057 | −0.061 | −0.052 | −0.102 | −0.112 | −0.093 | −3.7 | −4.0 | −3.5 |

| Documented Hispanic | 0.000 | −0.003 | 0.003 | 0.002 | −0.004 | 0.008 | −2.3 | −2.5 | −2.1 |

| Age (<50 reference) | |||||||||

| 50–65 | −0.005 | −0.007 | −0.003 | −0.092 | −0.097 | −0.087 | 3.2 | 3.1 | 3.4 |

| 65–75 | 0.010 | 0.008 | 0.013 | −0.087 | −0.092 | −0.082 | 7.7 | 7.6 | 7.9 |

| >75 | 0.049 | 0.046 | 0.051 | −0.016 | −0.022 | −0.011 | 15.7 | 15.5 | 15.9 |

| Dialysis duration (>3 years reference) | |||||||||

| <90 days | −0.031 | −0.040 | −0.023 | 0.099 | 0.079 | 0.119 | −1.9 | −2.7 | −1.2 |

| 90–365 days | −0.015 | −0.017 | −0.013 | −0.018 | −0.023 | −0.014 | −4.2 | −4.4 | −4.1 |

| 1–2 years | −0.014 | −0.016 | −0.013 | −0.019 | −0.022 | −0.015 | −3.6 | −3.8 | −3.5 |

| 2–3 years | −0.008 | −0.010 | −0.007 | −0.012 | −0.016 | −0.008 | −2.5 | −2.7 | −2.4 |

| Nursing home | −0.005 | −0.007 | −0.003 | 0.146 | 0.141 | 0.151 | 13.2 | 13.0 | 13.5 |

| Drug or alcohol use | 0.070 | 0.067 | 0.074 | 0.339 | 0.328 | 0.350 | 3.0 | 2.6 | 3.4 |

| Cerebrovascular disease | 0.033 | 0.031 | 0.034 | 0.108 | 0.104 | 0.113 | 4.1 | 3.9 | 4.3 |

| Peptic ulcer disease | 0.032 | 0.030 | 0.034 | 0.175 | 0.170 | 0.181 | 5.1 | 4.9 | 5.4 |

| Coronary artery disease | 0.040 | 0.038 | 0.041 | 0.132 | 0.128 | 0.136 | 2.0 | 1.8 | 2.2 |

| Heart failure | 0.074 | 0.073 | 0.076 | 0.240 | 0.236 | 0.243 | 7.9 | 7.8 | 8.1 |

| Pulmonary disease | 0.056 | 0.054 | 0.057 | 0.187 | 0.183 | 0.191 | 6.3 | 6.1 | 6.5 |

| HIV | 0.067 | 0.061 | 0.073 | 0.174 | 0.159 | 0.190 | 5.5 | 5.1 | 6.0 |

| Cancer | 0.031 | 0.028 | 0.033 | 0.138 | 0.131 | 0.144 | 8.8 | 8.5 | 9.1 |

| Dementia | 0.011 | 0.008 | 0.014 | 0.144 | 0.136 | 0.152 | 10.6 | 10.2 | 11.0 |

| Diabetes | 0.067 | 0.066 | 0.069 | 0.124 | 0.121 | 0.128 | 2.7 | 2.6 | 2.8 |

| Liver disease | 0.034 | 0.031 | 0.036 | 0.139 | 0.133 | 0.146 | 4.3 | 4.1 | 4.6 |

| Paralysis | 0.019 | 0.014 | 0.023 | 0.085 | 0.074 | 0.096 | 4.4 | 3.9 | 5.0 |

| PVD | 0.040 | 0.039 | 0.042 | 0.124 | 0.120 | 0.128 | 6.4 | 6.2 | 6.6 |

| Rheum. disease | 0.061 | 0.057 | 0.064 | 0.156 | 0.146 | 0.167 | 2.8 | 2.5 | 3.2 |

| Smokes | 0.062 | 0.059 | 0.065 | 0.234 | 0.226 | 0.242 | 1.3 | 0.9 | 1.6 |

| Previous failed transplant | −0.041 | −0.044 | −0.037 | −0.048 | −0.055 | −0.041 | −3.1 | −3.3 | −2.9 |

| Medicaid eligible | 0.055 | 0.053 | 0.056 | 0.104 | 0.100 | 0.107 | 0.2 | 0.1 | 0.3 |

| Facility size (per 25 patients) | −0.001 | −0.001 | −0.001 | −0.004 | −0.004 | −0.003 | −0.1 | −0.1 | 0.0 |

| For profit | 0.009 | 0.006 | 0.012 | 0.023 | 0.017 | 0.029 | 0.3 | 0.1 | 0.5 |

| Free‐standing | 0.008 | 0.004 | 0.012 | −0.021 | −0.029 | −0.013 | −1.3 | −1.6 | −1.0 |

| Rural or small town | −0.011 | −0.014 | −0.007 | −0.014 | −0.023 | −0.005 | −0.3 | −0.6 | 0.0 |

Notes: Models include dummy variables for each calendar year and account for hospital service area fixed effects. PVD is peripheral vascular disease. LCI and UCI are lower and upper 95% confidence intervals, respectively. First part of hospitalization model and mortality model includes 632,734 patients and 1,939,460 patient‐months. Second part of hospitalization model includes 571,883 patients and 1,464,995 patient‐months, which is 76% of the total patient‐months.

The estimates of hospitalizations from both stages were combined in a two‐part model as described in Exhibit 2 in Appendix SA2 and were transformed into an estimate of change in hospitalization per 100 patient‐years as described in Exhibit 3a in Appendix SA2. Results from the initial two‐part model are described in Table S3, while results from the transformed model are described in Table 2.

Market Concentration and Hospitalization

Patients had a 76 percent probability of at least one hospitalization per year, with an average of 2.7 hospitalizations per year (SD 3.5). The number of hospitalizations per patient‐year was 2.7 throughout the decade. Similar to mortality, there was an unadjusted trend toward more hospitalizations in less competitive areas, ranging from 2.3 hospitalizations per patient‐year in areas with an HHI <0.1 to 2.8 hospitalizations per patient‐year in areas with an HHI >0.6 (Figure 1). In our multivariable model with HSA fixed effects, a 0.2‐unit increase in HHI was independently associated with an increase in 2.9 hospitalizations per 100 patient‐years (95 percent CI, 0.4 to 5.4) (Table 2b; Exhibit 3a in Appendix SA2). The first part of the two‐part model of all‐cause hospitalizations did not demonstrate a significant association between market concentration and the probability of at least one hospitalization, while the second part of the model indicated that 0.2‐unit change in HHI was independently associated with an approximate 0.6 percent (95 percent CI, 0.2 percent to 1.1 percent) increase in the annual number of repeat hospitalizations among patients hospitalized at least once in a given year (Table 3, panel 2).

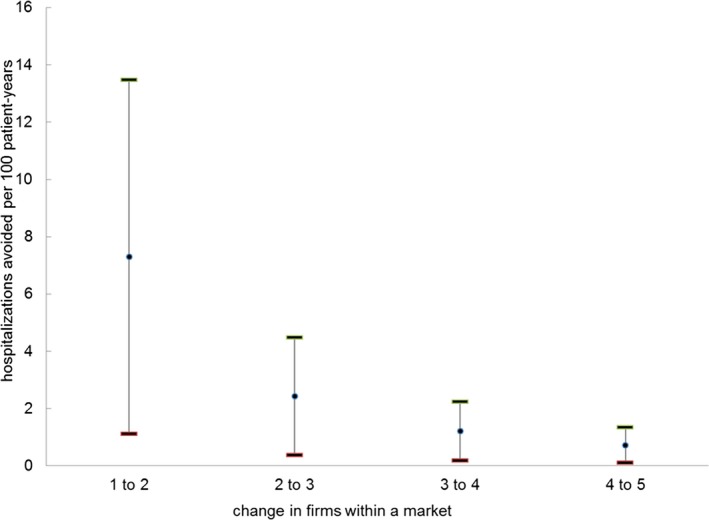

In 2011, there were 396,000 patients receiving in‐center hemodialysis in the United States (USRDS 2013). If our findings were generalizable to all patients receiving in‐center hemodialysis, and if all markets were more competitive by one standard deviation of HHI (0.2), our model predicts 8,100 fewer hospitalizations (95 percent CI, 1,200 to 15,000) in 2011 (Exhibit 3b in Appendix SA2). The estimated change in number of hospitalizations that would occur if patients had one additional choice among competing providers equally sharing a market varies according to the existing degree of market concentration. Our model predicts that a new dialysis facility equally splitting a monopolistic market would yield 7.3 fewer hospitalizations and save approximately $120,000 per 100 patient‐years, while the addition of one competing provider equally sharing markets previously split by two competing facilities would yield 2.4 fewer hospitalizations and save approximately $40,000 per 100 patient‐years (Figure 2; Exhibit 3c in Appendix SA2).

Figure 2.

- Note: Estimates were obtained from the initial model results as described in Table S3 and were transformed into estimated reductions in hospitalizations and cost per 100 patient‐years as described in Exhibit 3c in Appendix SA1. The changes in HHI and associated reductions in number of hospitalizations and hospital costs for each scenario illustrated above are as follows: one to two firms equally sharing a market: HHI decrease in 0.5 with 7.3 fewer hospitalizations and $120,000 savings per 100 patient‐years; two to three firms equally sharing a market: HHI decrease in 0.17 with 2.4 fewer hospitalizations and $40,000 savings per 100 patient‐years; three to four firms equally sharing a market: HHI decrease in 0.08 with 1.2 fewer hospitalizations and $20,000 savings per 100 patient‐years; four to five firms equally sharing a market: HHI decrease in 0.05 with 0.7 fewer hospitalizations and $12,000 savings per 100 patient‐years.

Results of Additional Analyses

Market competition was associated with all‐cause hospitalizations in each of our alternative model specifications. The magnitude of the association and statistical significance varied due to different assumptions and uncertainties associated with each specification. Less competition was significantly associated with an increased risk of death and hospitalization in the stacked cross‐sectional models, and consolidation (measured at the dialysis facility level) was associated with more hospitalizations at the dialysis facility level. When examining zip‐code‐level HHIs, there was a positive association between HHI and hospitalizations that was of marginal statistical significance (Table 2; Exhibit 4a in Appendix SA2).

The results from our analysis of all‐cause hospitalizations were not sensitive to controlling for the five largest dialysis chains, temporal changes in the number of dialysis facilities in an HSA, and adjustment for Medicare Advantage penetration (Exhibit 4b in Appendix SA2). Models using an alternative index of HHI designed to address potential bias from endogeneity of market concentration did not indicate evidence of this bias (Exhibit 5 in Appendix SA2). Our findings were not sensitive to the use of linear regression to analyze binary outcomes (Exhibit 7 in Appendix SA2).

Cause‐Specific Hospitalization

On average during the study period, patients had a 26 percent unadjusted probability of hospitalization for CVD in a given year, a 24 percent probability of hospitalization for vascular access complication, and a 15 percent probability of hospitalization for infection. Hospitalization for infection, vascular access complication, and CVD accounted for 8 percent, 12 percent, and 15 percent of overall hospitalizations, respectively. In fully adjusted regression models, the annual probability of at least one hospitalization for an infection was slightly higher in more concentrated markets (a 0.2 change in HHI was associated with an absolute increase in the probability of at least one hospitalization for infection of 0.24 percent; 95 percent CI, 0.07 to 0.41 pp; p = .01; Exhibit 8 in Appendix SA2). There was no significant association between market concentration and hospitalization for CVD or vascular access complication.

Discussion

We found that patients receiving in‐center hemodialysis in the decade prior to the ESRD PPS were hospitalized less frequently if they lived in areas with more competition among dialysis providers. Nearly all of the decrease in hospitalizations from additional market competition was due to reduced repeat hospitalizations, suggesting that dialysis providers in more competitive areas may more effectively manage patients who experience multiple hospitalizations.

Economic models conclude that lower competition between firms allows them to raise prices and earn higher profits. In cases where the government sets prices, firms in less competitive markets are unable to increase prices; but firms may still be able to increase profits by lowering costs through provision of lower‐quality products. Studies of hospital market consolidation in the 1990s and early 2000s found that less competition led to higher prices in many markets (Town and Vogt 2006) and was more closely associated with lower quality of care and worse health outcomes in markets with fixed prices (Gaynor 2006; Gaynor and Town 2012). Medicare is the primary payer for most patients receiving hemodialysis and administers primarily fixed prices through its payment policies. Consequently, dialysis providers must find nonprice mechanisms to attract many patients and physician referrals. Our findings suggest that nonprice competition in dialysis markets may influence the quality of care and patient health outcomes.

Although the magnitude of the observed association between competition and hospitalizations in this study was relatively modest, there are several reasons why changes in hospitalizations resulting from increased dialysis market competition could substantially affect patients receiving dialysis. First, because many dialysis markets are highly concentrated, the entry of as few as one new competitor in many areas could generate a meaningful increase in competition and associated reductions in hospitalizations. Approximately 40 percent of patients receiving hemodialysis live in areas where the HHI is greater than 0.5. For these patients, having one additional choice among competing facilities could lead to three‐to‐seven fewer hospitalizations per 100 patient‐years. Second, because competition can affect the care delivered to all patients in a geographic market, increases in competition persisting over time could lead to large aggregate and cumulative reductions in hospitalizations. Our model predicted that a one standard deviation decline in HHI across all regions in 2011 would yield 8,100 fewer hospitalizations in that year. If this annual reduction persisted, the cumulative change in hospitalizations, and corresponding cost savings, would be large.

The quality of dialysis care can vary in many domains and for many different reasons. One example where competition could influence the quality of care delivered is through an effect on strategic decisions about facility capacity (i.e., dialysis stations per patient). Previous studies of market competition in dialysis have found a positive association between the amount of competition and dialysis facility capacity (Held and Pauly 1983; Hirth, Chernew, and Orzol 2000). Market competition could influence facility capacity if providers in more competitive markets are willing to open up a new facility or to continue operating an existing facility in order to attract patients despite insufficient numbers of patients to fill all stations during all dialysis shifts. Dialysis facilities with more capacity may have more time and resources available for facility staff to take necessary antiseptic precautions and address patients’ needs. An economic analysis of the trade‐off between quality and quantity in dialysis care found that, when facilities choose to dialyze more patients for a given amount of fixed inputs (including dialysis stations), patients are more likely to develop serious infections (Grieco and McDevitt 2014). An association between market competition, dialysis facility capacity, and infections is consistent with our finding that the probability of hospitalization for infection was slightly higher in less competitive markets.

Another example of how more competition may influence the quality of dialysis care involves dialysis facilities’ staffing decisions. More competition for patients and physician referrals may encourage facilities to improve the quality (e.g., level of education, training, and experience) of their staff, hire additional staff, or devote additional resources to better equip staff to improve care for patients. Staffing ratios vary across dialysis facilities (Yoder et al. 2013), and evidence suggests that facilities with more nurses per patient provide higher‐quality care in some domains (Thomas‐Hawkins, Flynn, and Clarke 2010). An analysis in 1990 found an association between competition in certain dialysis markets and staffing decisions (Farley 1996). The presence of more (and higher‐quality) staff may improve a facility's ability to prevent recurrent hospitalizations, particularly hospitalizations related to infection.

Although the entry of competing facilities into dialysis markets with limited competition could reduce hospitalization rates, dialysis market competition remained limited during the study period; acquisitions by large for‐profit chains largely offset potential increases in competition with new market entrants and a growing dialysis population (Businesswire 2004a,b; PRNewswire 2004; Erickson et al. 2016). Meanwhile, firms considering entering new markets face barriers to entry, including difficulties finding a physician group to partner with for referrals, state and local certificate of need laws, and unfavorable labor costs and payer mixes in some areas (Federal Trade Commission 2011). By rewarding economies of scale and penalizing facilities treating sicker patient populations, Medicare's current bundled payment system for dialysis reimbursement (ESRD PPS) and pay‐for‐performance system (ESRD Quality Incentive Program (QIP)) may create additional entry barriers for smaller providers (Sedor et al. 2010; Johnson, Meyer, and Johnson 2011). Policies that regulate acquisitions and lower barriers to entry could encourage competition and improve health outcomes. Examples of such policies include stricter regulation by the Federal Trade Commission of proposed acquisitions, reforming certificate of need laws, creating economic incentives within Medicare's ESRD PPS and QIP programs for competing dialysis providers to enter markets, and regulating contracts between physician groups and dialysis facilities to promote competition.

A commonly cited concern regarding studies of market competition and quality of care relates to potential endogeneity of market concentration indexes. In particular, areas with higher quality of care may attract patients from farther away, increasing the size of these markets and the proportion of patients concentrated at one facility. In that setting, the magnitude of a competition index may be a consequence of the quality of care, rather than a determinant of quality. This issue has been proposed as an explanation of discrepant findings related to hospital competition and patient health outcomes (Town and Vogt 2006). We did not find evidence of this bias in our analysis. The absence of bias may be due to patients’ strong preferences to receive dialysis close to where they live. Unlike the decision about where to receive hospital care for surgery or another major acute health condition, patients receiving in‐center hemodialysis typically travel to their facility three to four times per week. Almost half of dialysis patients choose to receive dialysis at the facility closest to where they live (Lee, Chertow, and Zenios 2010), and the average distance traveled to dialysis decreased between 2001 and 2011 (Erickson et al. 2016). While patients receiving in‐center hemodialysis may prefer to receive care at a higher‐quality facility when choosing among facilities similarly close to their homes, they may be unlikely to travel significantly farther, even to a facility of higher real or perceived quality. Alternatively, our use of geographic fixed effects may have sufficiently addressed this potential issue, as changes in competition within a geographic region over time are more likely to reflect entry and exit of firms and mergers than patient choices about where to receive dialysis.

Our study has several limitations. We examined only the association between market concentration and two major health outcomes (death and hospitalization) and did not examine specific ways that market competition may affect health care quality, or whether market competition affects physical or mental health, health‐related quality of life, patient satisfaction, or costs. We did not distinguish between different underlying causes of changes in competition. The effect of a change in market competition on quality of care may differ following mergers and acquisitions, facility openings and closures, and reallocation of patients among existing facilities. It will be important for future analyses to investigate: 1) potential links between market competition and specific measures of dialysis care quality and 2) whether the underlying reasons for changes in competition influence associated effects on the quality of care. Our measure of HHI based on HSAs only approximates market competition. HSA fixed effects may have limited our power to detect an effect of competition on mortality, as any effect on mortality would likely be small. Because of computational limitations associated with our study design, it was necessary to use linear regression models, despite theoretical limitations associated with their use to examine discrete outcomes. However, evidence suggests that the difference in estimated average marginal effects from linear models compared with nonlinear models for discrete outcomes may be small (Angrist and Pischke 2009), and our results did not materially change in a sensitivity analysis using nonlinear models. Our examination of health outcomes was limited to patients with Medicare coverage and did not consider ways in which the availability of other forms of kidney replacement therapy (e.g., home dialysis and kidney transplantation) may have influenced in‐center hemodialysis market competition.

In summary, we found that patients receiving in‐center hemodialysis in areas with more competition among dialysis providers experienced fewer hospitalizations. More competition among providers in highly concentrated dialysis markets could lead to meaningful reductions in hospitalizations, particularly among patients with multiple hospitalizations per year. The association between market competition and number of hospitalizations highlights the importance of considering how policies and regulations affecting dialysis care might influence market competition. Our findings in dialysis care also suggest that market competition may be associated with health outcomes in other areas of health care where providers have a limited ability to compete on prices.

Supporting information

Appendix SA1: Author Matrix.

Appendix SA2: Supplementary Materials.

Exhibit 1: Calculating Market Concentration Index.

Figure S1: Stylized Example of Calculating Herfindahl‐Hirschman Index with Two Hospital Service Areas and Three Dialysis Facilities.

Exhibit 2: Two‐Part Model to Estimate the Marginal Effect of All‐Cause Hospitalization.

Exhibit 3: Methods Used to Represent Findings from the Two‐Part Regression Model.

Table S3: Two‐Part Regression Model Results Prior to Transformation.

Exhibit 3a: Transforming Two‐Part Regression Model Estimates to Hospitalizations per 100 Patient‐Years from a 0.2 Change in HHI.

Exhibit 3b: Calculating the Change in Overall Hospitalizations in 2011.

Exhibit 3c: Estimating the Change in Hospitalizations and Hospital Costs Associated with Hypothetical Scenarios Where a Competitor Enters Markets.

Exhibit 4: Additional Models.

Table S4a: Results from Zip Code–Level Model.

Table S4b: Results from Dialysis Facility‐Level Model.

Table S4c: Results from “Stacked Cross‐Sectional” Model.

Table S4d: Linear Regression Model Results on Number of Hospitalizations.

Exhibit 5: Modeling HHI.

Figure S5a: Predicted Probability of Choosing a Dialysis Facility by Distance in 2001.

Figure S5b: Predicted Probability of Choosing a Dialysis Facility by Distance in 2011.

Figure S5c: Difference between Modeled and Observed HHI in 2001, by Observed HHI.

Figure S5d: Difference between Modeled and Observed HHI in 2011, by Observed HHI.

Table S5: Coefficients for Observed and Modeled HHI When Included Together in Two‐Part Model of All‐Cause Hospitalizations.

Exhibit 6: Examination of Distribution of and Changes in Hirschman‐Herfindahl Index over Time.

Figure S6a: Distribution of Hirschman‐Herfindahl Index in Each Calendar Year.

Figure S6b: Change in Hirschman‐Herfindahl Index over Time, Stratified by Category of Change between 2001 and 2011.

Table S6: Population Included in Each Calculation of Hirschman‐Herfindahl Index.

Exhibit 7: Sensitivity to Use of Linear Models.

Exhibit 8: Association between Market Competition and the Probability of Hospitalization for Infection.

Acknowledgments

Joint Acknowledgment/Disclosure Statement: The authors thank Liran Einav, PhD, for guidance in developing a model of market competition, and Phillip Held, PhD, for assistance in interpreting preliminary study findings.

Author Access to Data: This work was conducted under a data use agreement between Dr. Winkelmayer and the National Institutes for Diabetes and Digestive and Kidney Diseases (NIKKD). An NIDDK officer reviewed the manuscript and approved it for submission. The data reported here have been supplied by the U.S. Renal Data System. The interpretation and reporting of these data are the responsibility of the author(s) and in no way should be seen as an official policy or interpretation of the U.S. government.

Funding: K23 1K23DK101693‐01 from NIDDK (Dr. Erickson); DK085446 (Dr. Chertow); Dr. Bhattacharya would like to thank the National Institute on Aging for support for his work on this paper (R37 150127‐5054662‐0002). This material was also supported by the use of facilities and resources of the Houston VA HSR&D Center for Innovations in Quality, Effectiveness, and Safety (CIN13‐413). The opinions expressed are those of the authors and not necessarily those of the Department of Veterans Affairs, the U.S. government or Baylor College of Medicine.

Disclosures: Dr. Chertow serves as a Chair on the Board of Directors at Satellite Healthcare. The authors report no other financial conflict of interest.

Disclaimer: None.

References

- Angrist, J. D. , and Pischke J. S.. 2009. Mostly Harmless Econometrics: An Empiricist's Companion. Princeton, NJ: Princeton University Press. [Google Scholar]

- Baker, L. C. , Bundorf M. K., Royalty A. B., and Levin Z.. 2014. “Physician Practice Competition and Prices Paid by Private Insurers for Office Visits.” Journal of the American Medical Association 312 (16): 1653–62. [DOI] [PubMed] [Google Scholar]

- Bass, E. B. , Wills S., Fink N. E., Jenckes M. W., Sadler J. H., Levey A. S., Meyer K., and Powe N. R.. 2004. “How Strong Are Patients’ Preferences in Choices between Dialysis Modalities and Doses?” American Journal of Kidney Diseases 44 (4): 695–705. [PubMed] [Google Scholar]

- Bradley, E. H. , Sipsma H., Horwitz L. I., Curry L., and Krumholz H. M.. 2014. “Contemporary Data About Hospital Strategies to Reduce Unplanned Readmissions: What Has Changed?” Journal of the American Medical Association Internal Medicine 174 (1): 154–6. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Brooks, J. M. , Irwin C. P., Hunsicker L. G., Flanigan M. J., Chrischilles E. A., and Pendergast J. F.. 2006. “Effect of Dialysis Center Profit‐Status on Patient Survival: A Comparison of Risk‐Adjustment and Instrumental Variable Approaches.” Health Services Research 41 (6): 2267–89. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Businesswire . 2004a. “Fresenius Medical Care to Acquire Renal Care Group, Inc.”

- Businesswire . 2004b. “Renal Care Group to Acquire National Nephrology Associates in Transaction Valued at $345 Million.”

- Church, J. , and Ware R.. 2000. Industrial Organization, A Strategic Approach. Boston, MA: Irwin McGraw‐Hill. [Google Scholar]

- Dafny, L. 2014. “Hospital Industry Consolidation–Still More to Come?” New England Journal of Medicine 370 (3): 198–9. [DOI] [PubMed] [Google Scholar]

- Eichner, M. J. , McClellan M. B., and Wise D. A.. 1997. “Health Expenditure Persistence and the Feasibility of Medical Savings Accounts.” Tax Policy and the Economy 11: 91–128. [Google Scholar]

- Erickson, K. F. , Winkelmayer W. C., Chertow G. M., and Bhattacharya J.. 2014. “Physician Visits and 30‐Day Hospital Readmissions in Patients Receiving Hemodialysis.” Journal of the American Society of Nephrology 25 (9): 2079–87. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Erickson, K. F. , Zheng Y., Ho V., Winkelmayer W. C., Bhattacharya J., and Chertow G. M.. 2016. “Consolidation in the Dialysis Industry, Patient Choice, and Local Market Competition.” Clinical Journal of the American Society of Nephrology 12 (3): 536–45. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Farley, D. O. 1996. “Competition under Fixed Prices: Effects on Patient Selection and Service Strategies by Hemodialysis Providers.” Medical Care Research & Review 53 (3): 330–49. [DOI] [PubMed] [Google Scholar]

- Federal Trade Commission . 2011. United States of America before Federal Trade Commission: In the Matter of DAVITA, INC., a Corporation. Washington, DC: United States Department of Justice. [Google Scholar]

- Federal Trade Commission . 2013. Horizontal Merger Investigation Data: Fiscal Years 1996–2011. Washington, DC: Federal Trade Commission: 34. [Google Scholar]

- Fisher, E. S. , Goodman D., Skinner J., and Bronner K.. 2009. Health Care Spending, Quality, and Outcomes. Hannover, NH: The Dartmouth Institute for Health Policy and Clinical Practice. [PubMed] [Google Scholar]

- Gaynor, M. 2006. What Do We Know about Competition and Quality in Health Care Markets? NBER Working Paper Series. National Bureau of Economic Research.

- Gaynor, M. , and Town R.. 2012. The Impact of Hospital Consolidation: Update. Princeton, NJ: The Robert Wood Johnson Foundation. [Google Scholar]

- Grieco, P. , and McDevitt R.. 2014. “Productivity and Quality in Health Care: Evidence from the Dialysis Industry.” Journal of Economic Literature 24 (1): 40. [Google Scholar]

- Held, P. J. , and Pauly M. V.. 1983. “Competition and Efficiency in the End Stage Renal Disease Program.” Journal of Health Economics 2 (2): 95–118. [DOI] [PubMed] [Google Scholar]

- Himmelfarb, J. , Berns A., Szczech L., and Wesson D.. 2007. “Cost, Quality, and Value: The Changing Political Economy of Dialysis Care.” Journal of the American Society of Nephrology 18 (7): 2021–7. [DOI] [PubMed] [Google Scholar]

- Hirth, R. A. , Chernew M. E., and Orzol S. M.. 2000. “Ownership, Competition, and the Adoption of New Technologies and Cost‐Saving Practices in a Fixed‐Price Environment.” Inquiry 37 (3): 282–94. [PubMed] [Google Scholar]

- Hirth, R. A. , Held P. J., Orzol S. M., and Dor A.. 1999. “Practice Patterns, Case Mix, Medicare Payment Policy, and Dialysis Facility Costs.” Health Services Research 33 (6): 1567–92. [PMC free article] [PubMed] [Google Scholar]

- Huber, P. J. 1967. “The Behavior of Maximum Likelihood Estimates under Nonstandard Conditions.” Proceedings of the Fifth Berkeley Symposium on Mathematical Statistics and Probability 1: 221–33. [Google Scholar]

- Johnson, D. S. , Meyer K. B., and Johnson H. K.. 2011. “The 2011 ESRD Prospective Payment System and the Survival of an Endangered Species: The Perspective of a Not‐for‐Profit Medium‐Sized Dialysis Organization.” American Journal of Kidney Diseases 57 (4): 553–5. [DOI] [PubMed] [Google Scholar]

- Jung, K. , and Polsky D.. 2014. “Competition and Quality in Home Health Care Markets.” Health Economics 23 (3): 298–313. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Kessler, D. P. , and McClellan M. B.. 2000. “Is Hospital Competition Socially Wasteful?” Quarterly Journal of Economics 115 (2): 577–615. [Google Scholar]

- Lee, D. K. K. , Chertow G. M., and Zenios S. A.. 2010. “Reexploring Differences among for‐Profit and Nonprofit Dialysis Providers.” Health Services Research 45 (3): 633–46. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Medicare Payment Advisory Commission . 2015. March 2015 Report to Congress: Medicare Payment Policy. Washington, DC: Medicare Payment Advisory Commission. [Google Scholar]

- Mehrotra, R. , Marsh D., Vonesh E., Peters V., and Nissenson A.. 2005. “Patient Education and Access of ESRD Patients to Renal Replacement Therapies beyond In‐Center Hemodialysis.” Kidney International 68 (1): 378–90. [DOI] [PubMed] [Google Scholar]

- Mullahy, J. 1998. “Much Ado about Two: Reconsidering Retransformation and the Two‐Part Model in Health Econometrics.” Journal of Health Economics 17 (3): 247–81. [DOI] [PubMed] [Google Scholar]

- PRNewswire . 2004. “DaVita to Acquire Gambro Healthcare, a Renal Dialysis Services Company.”

- Rucker, D. , Hemmelgarn B. R., Lin M., Manns B. J., Klarenbach S. W., Ayyalasomayajula B., James M. T., Bello A., Gordon D., Jindal K. K., and Tonelli M.. 2011. “Quality of Care and Mortality Are Worse in Chronic Kidney Disease Patients Living in Remote Areas.” Kidney International 79 (2): 210–7. [DOI] [PubMed] [Google Scholar]

- Ryan, A. M. , Krinsky S., Adler‐Milstein J., Damberg C. L., Maurer K. A., and Hollingsworth J. M.. 2017. “Association between Hospitals’ Engagement in Value‐Based Reforms and Readmission Reduction in the Hospital Readmission Reduction Program.” Journal of the American Medical Association Internal Medicine 177 (6): 862–8. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Sedor, J. R. , Watnick S., Patel U. D., Cheung A., Harmon W., Himmelfarb J., Hostetter T. H., Inrig J. K., Mehrotra R., Robinson E., Smedberg P. C., Shaffer R. N., and American Society of Nephrology ESRD Task Force . 2010. “ASN End‐Stage Renal Disease Task Force: Perspective on Prospective Payments for Renal Dialysis Facilities.” Journal of the American Society of Nephrology 21 (8): 1235–7. [DOI] [PubMed] [Google Scholar]

- Thomas‐Hawkins, C. , Flynn L., and Clarke S. P.. 2010. “Relationships between Registered Nurse Staffing, Processes of Nursing Care, and Nurse‐Reported Patient Outcomes in Chronic Hemodialysis Units.” Nephrology Nursing Journal 35 (2): 123–30, 45; quiz 31. [PMC free article] [PubMed] [Google Scholar]

- Thompson, S. , Gill J., Wang X., Padwal R., Pelletier R., Bello A., Klarenbach S., and Tonelli M.. 2012. “Higher Mortality Among Remote Compared to Rural or Urban Dwelling Hemodialysis Patients in the United States.” Kidney International 82 (3): 352–9. [DOI] [PubMed] [Google Scholar]

- Town, R. J. , and Vogt W.. 2006. How has Hospital Consolidation Affected the Price and Quality of Hospital Care? [Internet]. Research Synthesis Report. Princeton, NJ: Robert Wood Johnson Foundation. [PubMed]

- Tsai, T. C. , and Jha A. K.. 2014. “Hospital Consolidation, Competition, and Quality: Is Bigger Necessarily Better?” Journal of the American Medical Association 312 (1): 29–30. [DOI] [PubMed] [Google Scholar]

- USRDS . 2013. “Annual Data Report: Atlas of Chronic Kidney Disease and End‐Stage Renal Disease in the United States.” United States Renal Data System. Bethesda, MD: National Institutes of Health, National Institute of Diabetes and Digestive and Kidney Diseases.

- Wilson, J. , and Nissenson A. R.. 2002. “Determinants in APD Selection.” Seminars in Dialysis 15 (6): 388–92. [DOI] [PubMed] [Google Scholar]

- WWAMI . 2005. “Rural‐Urban Commuting Area Codes (RUCA).” WWAMI Rural Health Research Center.

- Xue, J. L. , Chen S. C., Ebben J. P., Constantini E. G., Everson S. E., Frazier E. T., Agodoa L. Y., and Collins A. J.. 2002. “Peritoneal and Hemodialysis: I. Differences in Patient Characteristics at Initiation.” Kidney International 61 (2): 734–40. [DOI] [PubMed] [Google Scholar]

- Yoder, L. A. G. , Xin W., Norris K. C., and Yan G.. 2013. “Patient Care Staffing Levels and Facility Characteristics in U.S. Hemodialysis Facilities.” American Journal of Kidney Diseases 62 (6): 1130–40. [DOI] [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Appendix SA1: Author Matrix.

Appendix SA2: Supplementary Materials.

Exhibit 1: Calculating Market Concentration Index.

Figure S1: Stylized Example of Calculating Herfindahl‐Hirschman Index with Two Hospital Service Areas and Three Dialysis Facilities.

Exhibit 2: Two‐Part Model to Estimate the Marginal Effect of All‐Cause Hospitalization.

Exhibit 3: Methods Used to Represent Findings from the Two‐Part Regression Model.

Table S3: Two‐Part Regression Model Results Prior to Transformation.

Exhibit 3a: Transforming Two‐Part Regression Model Estimates to Hospitalizations per 100 Patient‐Years from a 0.2 Change in HHI.

Exhibit 3b: Calculating the Change in Overall Hospitalizations in 2011.

Exhibit 3c: Estimating the Change in Hospitalizations and Hospital Costs Associated with Hypothetical Scenarios Where a Competitor Enters Markets.

Exhibit 4: Additional Models.

Table S4a: Results from Zip Code–Level Model.

Table S4b: Results from Dialysis Facility‐Level Model.

Table S4c: Results from “Stacked Cross‐Sectional” Model.

Table S4d: Linear Regression Model Results on Number of Hospitalizations.

Exhibit 5: Modeling HHI.

Figure S5a: Predicted Probability of Choosing a Dialysis Facility by Distance in 2001.

Figure S5b: Predicted Probability of Choosing a Dialysis Facility by Distance in 2011.

Figure S5c: Difference between Modeled and Observed HHI in 2001, by Observed HHI.

Figure S5d: Difference between Modeled and Observed HHI in 2011, by Observed HHI.

Table S5: Coefficients for Observed and Modeled HHI When Included Together in Two‐Part Model of All‐Cause Hospitalizations.

Exhibit 6: Examination of Distribution of and Changes in Hirschman‐Herfindahl Index over Time.

Figure S6a: Distribution of Hirschman‐Herfindahl Index in Each Calendar Year.

Figure S6b: Change in Hirschman‐Herfindahl Index over Time, Stratified by Category of Change between 2001 and 2011.

Table S6: Population Included in Each Calculation of Hirschman‐Herfindahl Index.

Exhibit 7: Sensitivity to Use of Linear Models.

Exhibit 8: Association between Market Competition and the Probability of Hospitalization for Infection.