Abstract

Southeast Asia accounts for nearly 86 per cent of the smokeless tobacco (SLT) consumers in the world. The heterogeneous nature of SLT is a major impediment to using taxation as a tool to regulate SLT. This study was aimed to review issues around fiscal policies on SLT with the objective of providing clarity on the use of taxation as an effective policy instrument to regulate SLT use. Descriptive statistics and graphical representations were used to analyze published data from different sources. An analysis of prices and tax between smoke and SLT products was done to understand the impact of tax policies on SLT consumption. India, Bangladesh and Myanmar together account for 71 per cent of the world SLT users. The retail prices (PPP$) and tax were lower for SLT in low- and lower-middle-income countries and higher in high-income countries, on an average, suggesting a direct relationship between the two. Evidence from India and Bangladesh suggested that taxation had significantly reduced SLT use among adults. The compounded levy scheme used in India to tax SLT was found effective after incorporating speed of packing machines into the assessment of deemed production and tax on SLT products. The current analysis shows that taxation can be an effective instrument to regulate SLT consumption if tax rates are harmonized across SLT products and in a manner not to encourage substitution with other tobacco products. It is also imperative to set a minimum floor price on all tobacco products including SLT.

Keywords: Bangladesh, chewing tobacco, India, lower middle-income countries, low-income countries, smokeless tobacco, taxation

The health effects of smokeless tobacco (SLT) are well documented and SLT is known to cause a variety of cancers including oral cancers, oesophageal cancer and pancreatic cancer in humans1,2. SLT also imposes an enormous economic burden on countries. In India, for example, the total economic costs attributable to SLT use alone from all diseases in the year 2011 for persons aged 35-69 yr was ₹ 233.6 billion3. In comparison, the excise tax revenue collected from SLT in that year amounted to only ₹ 12.6 billion.

SLT consists of a wide range of heterogeneous products such as chewing tobacco, betel quid with tobacco, gutka, snuff, snus and others whose product characteristics as well as methods of use are different and are packed in different sizes and shapes. Apart from the traditional forms of SLT use found in Regions such as South and Central Asia, South America and Sub-Saharan Africa, the markets for which are largely dominated by informal cottage type production, there is also a new generation of SLT products largely found in North America, Western Europe and Australia supplied by multinational corporations and are commercially manufactured. However, the available estimates indicate that, by volume, 91.3 per cent of the SLT products sold worldwide are sold in traditional markets2.

A substantial body of research shows that significantly increasing the excise tax and price of tobacco products is the single most consistently effective tool for reducing tobacco use4. This is also recognized by the Parties to the World Health Organization - Framework Convention on Tobacco Control (WHO FCTC)5 and is expressed as such under Article 6 of the Treaty. While the literature on taxing cigarettes and similar smoked tobacco products is fairly well established4, the same is not true in case of taxation of SLT products owing to their heterogeneous nature. Although the provisions of Article 6 apply to both smoking and SLT and the guidelines to implement the Article recommend measures to specifically address all tobacco products, in particular, to prevent product substitution within and across categories, yet, little is known about the nature of taxes on SLT products or the extent to which higher SLT taxes translate into higher SLT prices and how these prices affect the consumption and affordability of SLT products. Data from the Global Youth Tobacco Survey (GYTS) - as reported in a 2014 report by The National Cancer Institute (NCI)2 - show that students aged 13-15 yr surveyed in 132 countries were more likely to report using non-cigarette tobacco products including SLT products (11.2%) than to report smoking cigarettes (8.9%).

Price and tax measures on SLT are often confusing, and it is important to provide more clarity on this so that tax policies on SLT can be made more effective. A systematic review of tobacco control policies relating to SLT use in the USA concluded that price elasticities of SLT products lie mostly in the inelastic range and SLT tax is an effective tool in reducing tobacco use6. Estimates of price elasticities of SLT products are rarely available from Southeast Asian countries. Available studies in India7,8,9,10 show the price elasticity of SLT products is in the range −0.1 to −0.9 and those from Bangladesh11 show the elasticity to be in the range −0.39 to −0.64. If price elasticity lies within the range of 0 to 1 such products are relatively insensitive to price increase. A given percentage increase in prices of such product through taxation would result in reducing consumption - to a proportion less than the increase in price - and increase tax revenue.

The heterogeneous nature of SLT makes quantification and enforcement of tax and price policies administratively difficult. Consequently, regulating SLT use through fiscal policy has been a major challenge. Hence, it is important to understand the best practices for SLT taxation used in countries so that this knowledge may inform other countries where similar products are consumed. This study was aimed to review issues around fiscal policies on SLT with the objective of providing clarity on the use of taxation as an effective fiscal policy instrument to regulate the use of SLT.

Published data from different sources such as the WHO report on the global tobacco epidemic12,13 in different years, National Cancer Institute (NCI) Tobacco Control Monograph 21: The Economics of Tobacco and Tobacco Control (NCI and WHO, 2016)4, Global Adult Tobacco Surveys (GATSs)14,15, official government sources and other published literature were used for the analysis. Since the Southeast Asia Region alone accounts for nearly 86 per cent of the total SLT users worldwide4, the analysis was largely restricted to countries in this Region although other countries were included when comparable data were available.

Descriptive statistics and graphical representations were used to understand the prevalence and trends in SLT use across different countries. An analysis of prices and tax between cigarettes and SLT was also done to understand how tax policies on SLT compare to that of cigarettes. As much as possible the analysis was performed by different World Bank country income groups - High-income Countries (HICs), Upper-Middle-Income Countries (UMICs), Lower Middle-Income Countries (LMICs) and Low-Income Countries (LICs) - and the WHO Regions.

Prevalence of smokeless tobacco

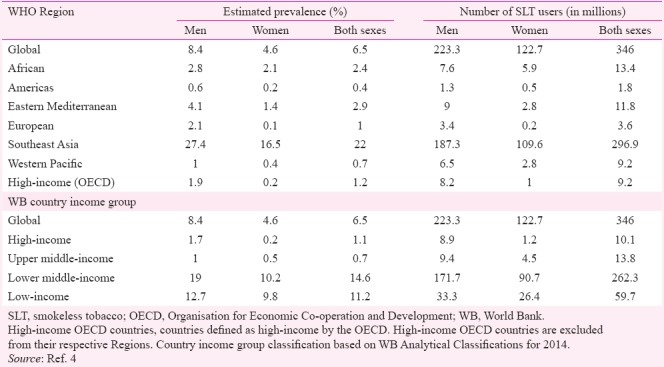

There was substantial variation in both the prevalence and the number of users of SLT across regions as shown in Table I. While the prevalence of SLT use was as high as 22 per cent in Southeast Asia, it was <1 per cent in the Western Pacific region. There were approximately 346 million adult SLT users in the world dominated by the Southeast Asian Region accounting for nearly 86 per cent of the total SLT users worldwide4. India alone accounted for 60 per cent of the SLT users in the world in 2010 with approximately 206 million users4. Bangladesh (28 million) and Myanmar (11.1 million) were two other countries where the number of SLT users exceeded 10 million4. Together, India, Bangladesh and Myanmar contributed about 71 per cent of the world SLT user base. Both the prevalence and the number of SLT users were much higher in LICs and LMICs.

Table I.

Prevalence and number of smokeless tobacco users by World Health Organization Region and country income groups, 2010

According to the second GATS in India14, the prevalence of SLT use among adults decreased from 25.9 per cent in 2010 to 21.4 per cent in 2017 which was a relative decline of more than 17 per cent. This translated to 199 million adults SLT users in 201714 which was a decrease of 7 million SLT users since 2010. If the number of SLT users remained the same elsewhere in the world, this meant a global total of 339 million SLT users in 2017 and India contributing 59 per cent of it. Khaini, an SLT product, was the most commonly used tobacco product in India used by 104 million adults (males and females) and gutka, another SLT product, was the third most commonly used product being used by 51 million adult males14. Among adult women, all three most commonly used tobacco products were smokeless varieties, namely, betel quid with tobacco (20 million), tobacco for oral applications (20 million), and Khaini (19 million) according to the same survey14.

The most prevalent forms of SLT use in Bangladesh were betel quid with zarda, gul, khoini (similar to Khaini in India), and sadapata (powdered or dried tobacco leaves)4. Data from international tobacco control (ITC) study in Bangladesh also showed a relative decline of 23.1 per cent in the prevalence of SLT use in three years. Prevalence of SLT use went down from 28.6 per cent in 2009 to 22 per cent in 201216. This effectively reduced the number of SLT users by about 4 million. Bangladesh is also unique for higher SLT prevalence among women (24.5%) than in men (19.5%) unlike in most other countries16. If we account for the reduction in the user base of SLT experienced in India and Bangladesh in recent surveys14,16, the global user base of SLT may be revised down to 335 million.

Taxation of smokeless tobacco

Experience in both India and Bangladesh showed that tax increases were effective in reducing SLT use. Successive GATS surveys14,15 done in 2010 and 2017 in India and ITC surveys16 done in 2009 and 2012 in Bangladesh showed significant reductions in the prevalence of SLT use in the general adult population. Significant tax increases on SLT products occurred during this period in both countries. In India, it was found that increasing the price of SLT products discouraged SLT use among men9 and youth10. The impact of an increase in prices of the two most popular varieties of SLT products (khaini and zarda) on consumption were examined in India17. It was found that 58 per cent rise in the prices of Khaini resulted in a 51 per cent decline in the consumption during the period 2008-2013 and a 28 per cent rise in the price of zarda led to a 24 per cent decline in the consumption during the same period17. In Bangladesh, it was observed that ‘the negative effect of the increase in tax that was presumably passed on to the price increase was at work in inducing SLT users to quit’17. An earlier study from Bangladesh11 also confirmed the inverse relationship between tax increases and SLT use.

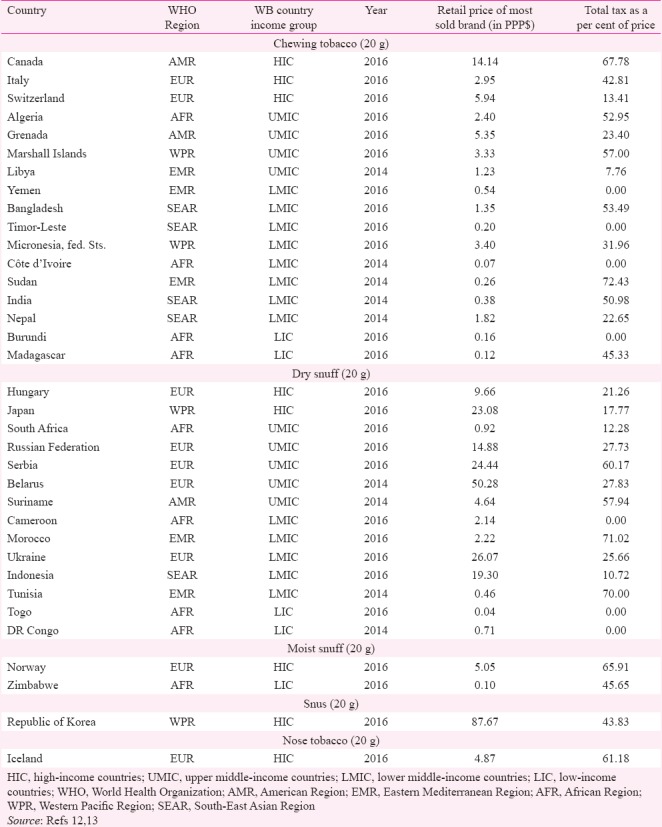

The WHO report on the global tobacco epidemic in 2015 and 2017 reported the tax burden - the proportion of overall taxes in retail prices - of SLT products along with their prices (in international dollars at purchasing power parity) for the most common type of SLT products, as reported by 35 countries12,13. There was huge variation in both prices and tax incidence on SLT products across countries from an absolute 0 per cent (i.e., no tax of any kind on SLT products in seven countries) to as high as 72.4 per cent in Sudan (Table II). Only three countries (Morocco, Sudan, and Tunisia) of the 35 had total tax incidence at or above 70 per cent. The WHO's Technical Manual on Tobacco Tax Administration16 recommends tobacco excise taxes alone should account for at least 70 per cent of the retail prices of tobacco products. In the Southeast Asia Region, although Indonesia had the highest price for SLT products, it showed the lowest tax at 10.72 per cent (Table II). On the other hand, India had one of the lowest prices per unit of SLT and second highest tax on SLT in Southeast Asia.

Table II.

Price and tax burden of smokeless tobacco by country

Of the 28 countries imposing some taxes on SLT products, 15 including Nepal and Indonesia from the SEAR, levy specific excise on SLT. Singapore levies the highest specific excise at 70 per cent. Twelve countries including India and Bangladesh from the SEAR impose ad valorem excise on SLT. In addition to specific excise or ad valorem excise most countries impose VAT on sale of SLT, while Algeria, Tunisia and Morocco were the only countries that imposed a mix of all the three kinds of taxes on SLT products. It was clear that most countries where SLT products were sold underutilized taxation as a tool to regulate consumption of SLT products12,13.

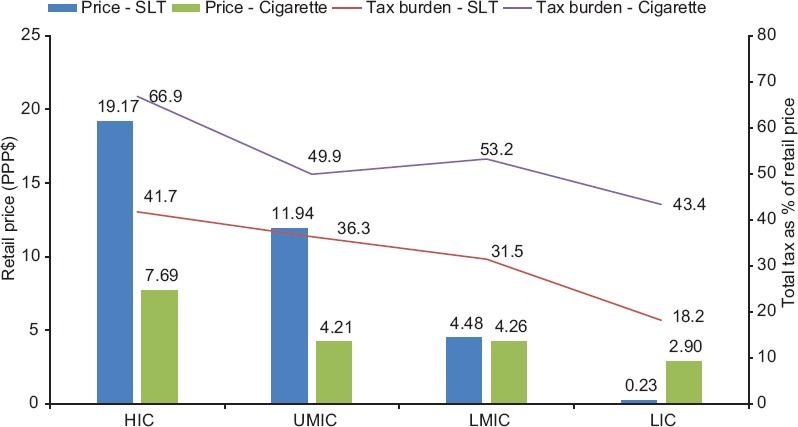

Examining price variation of SLT products across countries also revealed interesting insights. Some countries such as Morocco, Sudan and Tunisia although have relatively high tax, their unit price of SLT products was relatively cheaper than several other countries where tax was low. Republic of Korea, Belarus, Ukraine, Indonesia and Japan, for example, have a relatively high price for SLT products although the tax was relatively low. On the other hand, there were countries where both tax and price were high (e.g., Serbia, Canada, Norway, Iceland and Suriname). To examine the relationship between tax burden and retail price of SLT, the countries were grouped into different income groups and average prices of SLT (20 g pouch of most sold SLT brand in each country) were mapped. The average tax burden on SLT in these country income groups is shown in the Figure. It showed a direct relationship between the retail price of SLT products and tax burden. Two observations became immediately clear: One, the tax burden of STLs was relatively larger in HICs compared to LICs and LMICs. Two, the retail prices (international PPP $), in general, were lower for SLT products in LICs and LMICs and higher in HICs.

Figure.

Comparison of retail price and tax incidence between smokeless tobacco (SLT) and cigarettes by country income groups. Note: Retail Price (PPP$) shows the retail price in international purchasing power parity dollars for a 20 cigarettes pack of the most sold brand and 20 g pouch of the most sold SLT brand in each country. HIC, high-income countries; UMIC, upper middle-income countries; LMIC, lower middle-income countries; LIC, low-income countries. Source: Refs 12, 13

The figure also presents a comparison of retail prices (international PPP $) and tax burden for a 20 cigarette pack of the most sold brand of cigarette and that of a 20 g pouch of SLT, assuming they are comparable units. The per unit price of SLT products was larger than that of cigarettes in all country income groups except LICs. However, in four of the five LICs and nine of the 13 LMICs, unit prices of cigarettes were at least two PPP $ larger than that of SLT. These were the countries with relatively low tax burden on SLT compared to cigarettes. Such differences in prices between two tobacco products within a single country may not be good from a tobacco control perspective as tax increases on either or both products can affect the relative price and tax burden and induce people to switch from higher priced products to lower priced products.

Smokeless tobacco taxation in India and Bangladesh

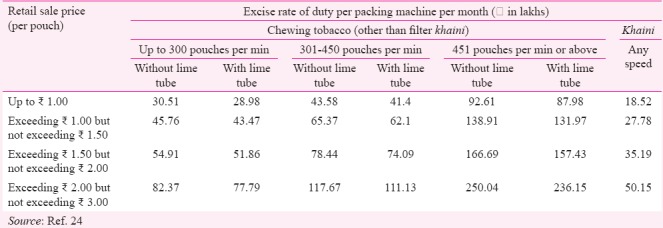

SLT taxation in India and Bangladesh needs special attention as these two countries, together account for roughly 68 per cent of the total SLT users in the world. India follows a compounded levy scheme (or presumptive taxation) to tax SLT products. This is because most SLT products in India such as chewing tobacco, pan masala and gutka are packed in pouches with the aid of packing machines. Under this system, a manufacturer is required to pay a lump sum amount of duty per packing machine installed in the production facility. The amount of duty would depend on the retail price of the pouch/pack that is produced using that packing machine. In other words, the manufacturer would pay duty on the basis of a normative assessment of production and not on the actually declared production18. This often incentivises manufactures to under-report the capacity of their machines or produce beyond the declared capacity.

Due to several limitations of this scheme and its inability to check the evasion of excise payable on SLT products, the Government of India, in its budget for FY 2015-2016, made maximum speed of packing machine as a factor for determining both the deemed production and excise duty payable under the Compounded Levy Scheme and it was applied to pan masala, gutka and chewing tobacco. Packing speed would be typically determined by a Government approved Chartered Engineer. Both deemed production and duty payable per machine per month were notified in respect of these SLT products with reference to the speed range in which the maximum speed of a packing machine for packages of various retail sale prices falls. Table III provides a sample snapshot of a compounded levy scheme in India as taken from the FY 2016-17 budget documents. It shows the different rates of excise taxes charged on SLT products based on the speed/capacity of the machine and the retail price in which each pouch is sold which ranges from < ₹ 1 to > ₹ 50 per pouch.

Table III.

Example of a compounded levy scheme in India (financial year 2016-2017)

An examination of excise data from SLT products19 shows that following the amendments that made the speed of packing machines as a determining factor for deemed production as well as excise duty payable, the excise tax revenue from pan masala and chewing tobacco increased by 66 and 48 per cent, respectively, in the FY 2015-2016. In comparison, in FY 2014-15, the excise revenue showed a decline of 0.4 and 7.8 per cent, respectively, for pan masala and chewing tobacco compared to the previous financial year. It indicates effective tax administration will positively impact tax revenue. According to data obtained from the Ministry of Finance, Government of India, of the total excise tax of ₹ 217.2 billion on all tobacco products collected in the FY 2016-17, only ₹ 21.5 billion (9.9%) came from SLT products alone19. However, the share of excise of SLT products in all tobacco excises has been consistently growing in the past several years - increased from about 6.8 per cent in the FY 2010-11 to 9.9 per cent in FY 2016-17- despite the decrease in SLT use indicating a possible improvement in the tax administration itself.

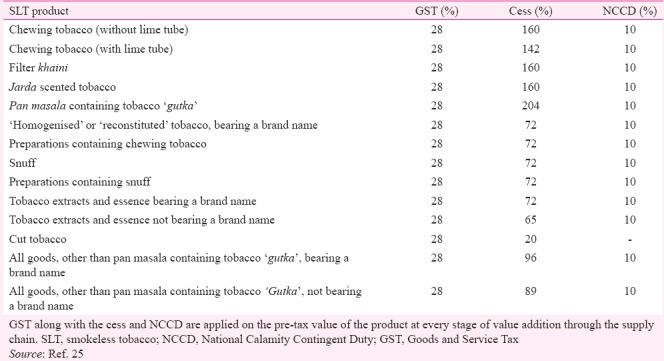

After the most recent Goods and Service Tax (GST) reform in India which was implemented on July 1, 2017, the SLT products are categorized under demerit product category and are imposed the highest GST rate of 28 per cent20. There is also an additional cess that varies by different SLT product varieties as shown in Table IV20. A simple average of cess across all SLT products is about 104 per cent. There is also a National Calamity Contingent duty (NCCD) of 10 per cent imposed on all SLT products apart from the taxes detailed above. With all these rates, however, the effective tax of SLT products in India is estimated to be around 60 per cent (this was estimated using a 28% GST, an average of 104% cess, and 10% NCCD that are applied on most SLT products under GST as well as assuming a 10% retail margin and a retail price of about ₹ 11.4 for a 10 g SLT pouch) prior to GST20. The tax burden of 60 per cent is still below the recommended rate of 75 per cent by the WHO and the World Bank13.

Table IV.

Tax rate on various smokeless products in India under goods and service tax (GST), 2017

Bangladesh, on the other hand, historically chose not to tax SLT products, unlike cigarettes. Only in 2008-2009, the government of Bangladesh recognized SLT as a manufacturing industry rather than a cottage industry2. SLT was brought under the tobacco control mechanism for the first time in 2008 with the imposition of 15 per cent value-added tax (VAT) on zarda (chewing tobacco) and gul (oral powder) which are the most common forms of SLT products in the country16. A 10 per cent supplementary duty on the ex-factory price of zarda and gul was also introduced in 2009. In the years 2010-2011 and 2011-2012, the supplementary duty was further revised to 20 and 30 per cent, respectively16. These supplementary duties were again revised to 60 per cent and later to 100 per cent in the years 2015-2016 and 2016-2017, respectively21. The tax base was however, shifted from ex-factory prices to a pre-determined tariff value from the year 2017-1822.

Affordability of smokeless tobacco

Available data12 suggest cigarettes are becoming less affordable in developed countries and much more affordable in developing countries. Data on the affordability of SLT across countries is, however, limited. Earlier studies7 in India showed that SLT products became more affordable over the period 2001 to 2007. Studies17 using data for 2006-2012 also suggested that SLT products were becoming more affordable in India. The study observed that despite a higher increase in the price of SLT compared to general prices, the SLT products became more affordable due to a higher increase in the per capita GDP. Using data from 2009 to 2015, a recent study23 from Bangladesh showed that the affordability of SLT products remained unchanged between 2011-2012 and 2014-2015. The study also observed that ‘despite the increase in price in real terms, affordability did not change due to offsetting income growth of SLT users’18. It also suggested the ‘growth in affordability of cigarettes relative to SLT may have induced switching from SLT use to cigarette smoking resulting in the higher prevalence of cigarette smoking and lower prevalence of SLT use in recent years in Bangladesh’18.

Affordability studies on SLT products from both India and Bangladesh underlined the need to increase taxes on tobacco products regularly to keep up with growth in income and purchasing power to make tax measures for SLT control more meaningful and effective. It is also important to decrease the affordability of all tobacco products in a country to discourage switching from relatively unaffordable products to more affordable products.

Conclusions

There are approximately 346 million adult SLT users in the world and the Southeast Asian region accounts for nearly 86 per cent of them4. India and Bangladesh are the two major countries that constitute much of the SLT user base. The literature on price and tax measures to control SLT use has not been well developed unlike the case of cigarettes. This is primarily because SLT consists of a wide range of heterogeneous products and finding a standard unit for quantification is challenging. It was found that, by volume, 91.3 per cent of the SLT products sold worldwide are sold in traditional markets dominated by Southeast Asia4.

In this study it was found that in both India and Bangladesh, the prevalence of SLT use declined by 17 per cent from 2010 to 2016-2017 and 23 per cent from 2009 to 2012, respectively. The global user base of SLT may be revised down to 335 million as a result. However, together, India and Bangladesh continue to contribute about 68 per cent of the total SLT user base in the world and about 79 per cent of the SLT users in the Southeast Asian Region4. The prevalence as well as the number of SLT users are relatively much higher in low and lower-middle-income countries. More than 93 per cent of the SLT users live in either LICs or LMICs.

Available studies on price elasticities of SLTs from India and Bangladesh concluded that the elasticity of SLT products fell in the inelastic range of <1 and, as a result, taxation can be used as an effective tool to reduce the consumption of SLT products as well as a tool to generate more tax revenue. A review of price and tax incidence of SLT products across 35 countries revealed that in general, prices were higher where high tax rates on SLT prevailed and vice versa, although there were individual countries with exceptions. The retail prices (international PPP dollars) as well as tax burden, were lower for SLT products in LICs and LMICs and higher in HICs and UMICs, on an average. In four of the five LICs and nine of the 13 LMICs, the unit prices of cigarettes was at least two PPP $ larger than that of SLT leading to possible substitution opportunities to lower priced SLTs in the event of tax increases on cigarettes. Special examination of SLT taxation system in India revealed that the introduction of compounded levy scheme and the amendments introduced in 2015-2016 saw tax revenue from SLT products going up substantially compared to previous year. The share of excise of SLT products in all tobacco excises has been consistently growing in the past several years and was 9.9 per cent in FY 2016-2017. The tax burden of SLT under GST, however, still remains at 60 per cent which is below the recommended rate by the WHO20. In Bangladesh, it was learnt that SLT was brought under the tobacco control mechanism for the first time only in 2008 with the imposition of 15 per cent value-added tax (VAT) on zarda (chewing tobacco) and gul (oral powder), two most common forms of SLT use in the country11. A supplementary duty on the ex-factory price was also introduced in 2009 which was at 100 per cent as of FY 2017-2018 and the tax base was shifted to a predetermined tariff value instead of ex-factory prices22.

Available studies indicated that SLT products in India have become increasingly affordable largely because per capita GDP has increased more than the increase in the price of SLT products during the period 2006-2012. Data from Bangladesh, on the other hand, suggest that the affordability has remained the same during the period 2011-2012 to 2015.

While data on prevalence of SLT use are available through different rounds of GATS, GYTS, Demographic and Health Survey and other generic health and household surveys in several countries and readily available to assess the trends on prevalence and number of users in a given country, similar data either on the price of these products or the quantity consumed in each country are hardly available. Based on an unpublished report in 2017 compiled by a team of experts at the WHO FCTC Global Knowledge Hub on SLT located in the National Institute of Cancer Prevention and Research, Noida, India, of the 179 Parties in the Conference of the Parties, 33 Parties had either not defined SLT or provided no definition of tobacco products and 11 Parties’ laws were not available in English language. According to the WHO report on the global tobacco epidemic in 201512 and 201713, only about 28 countries were imposing some kind of taxes on SLT products. Most countries do not report either the price or the quantity consumed of various SLTs. In a 2014 report by the NCI and Centers for Disease Control and Prevention4, the volume of total SLT available globally was quoted as 710.2 billion tonnes, about 91.3 per cent (648.2 billion tons) of which was in the traditional market4. However, this volume information appeared to be highly overstated, was sourced from the Euromonitor, a global market information database, and could not be verified as the methods used by Euromonitor were not transparent. It is of critical importance to know that there are no data at the country level on the volume of production, sales or consumption which are necessary to carry out meaningful analysis of the impact of tax and prices on SLTs. Parties should make reporting such data on SLT mandatory to facilitate meaningful economic research on SLT in future.

It is evident that taxation is an effective tool to reduce the use of SLT products. However, how tax is implemented is crucial to make the best use of this tool. Taxation should be as simple as possible, and it should be efficient to meet both public health and fiscal needs. Determining a standard unit for taxation can be challenging for SLT products due to its heterogeneous nature. Unit for taxation of SLT can be either the retail price of pouch/pack in which the product is sold, the weight of the pack/pouch, or weight of dry tobacco leaf used in the product. The experience in India shows that taxation based on the pre-notified capacity of packing machine that takes into account the speed of these machines can be effective. Continuous monitoring of the supply chain (from manufacturing to retail distribution) of SLT products should be in place to make taxation effective.

Taxation of SLT products should follow the following principles: (i) tax should be revised upwards frequently (at least once a year) to keep the affordability of SLT products low taking into account both the inflation and income growth for that year; (ii) tax should not make the SLT products cheaper than the alternative tobacco products such as cigarettes, bidis or other smoked tobacco products available in a country. This should be of particular concern in countries where risk of substitution with other tobacco products exist; (iii) tax should be such that the minimum price per pouch/pack of SLT will be at least as high as a pack of alternative smoked tobacco products available in the same market; (iv) given that SLT products are already much cheaper than cigarettes in most LICs and LMICs where SLT is sold, the incremental changes in SLT tax need to be much larger than that of cigarettes to bring about parity in taxation and retail price across tobacco products; and (v) it is important to set a minimum floor price on all tobacco products including SLT that are sold in a country. The minimum floor price per the lowest unit of the tobacco product sold should be harmonized across all tobacco product categories. To harmonize the minimum floor price, first, loose sale of all tobacco products should be prohibited and second, manufacturing/production of all tobacco products should be standardized at a unit level based on its weight, size and/or dimensions.

Acknowledgment:

Authors thank Dr Nigar Nargis at the American Cancer Society for her valuable suggestions.

Footnotes

Financial support & sponsorship: None.

Conflicts of Interest: None.

References

- 1.Lyon, France: World Health Organization, International Agency for Research on Cancer; 2004. International Agency for Research on Cancer. Betel-quid and areca-nut chewing and some areca-nut-derived nitrosamines. [Google Scholar]

- 2.Smokeless tobacco and public health: A global perspective. Bethesda, MD: U.S. Department of Health and Human Services, Centers for Disease Control and Prevention and National Institutes of Health, National Cancer Institute; 2014. National Cancer Institute and Centers for Disease Control and Prevention. [Google Scholar]

- 3.John RM, Rout SK, Kumar RB, Arora M. Economic burden of tobacco related diseases in India. New Delhi: Ministry of Health & Family Welfare, Government of India; 2014. [accessed on July 30, 2018]. Available from: https://mohfw.gov.in/node/3236 . [Google Scholar]

- 4.U.S. National Cancer Institute and World Health Organization. The economics of tobacco and tobacco control. Bethesda, MD, Geneva, CH: U.S. Department of Health and Human Services, National Institutes of Health, National Cancer Institute, World Health Organization; 2016. [accessed on February 19, 2017]. Available from: http://www.cancercontrol.cancer.gov/brp/tcrb/monographs/21/index.html . [Google Scholar]

- 5.World Health Organization. WHO Framework Convention on Tobacco Control. 2013. [accessed on February 19, 2017]. Available from: http://www.who.int/tobacco/global_report/2013/who_fctc.pdf .

- 6.Levy DT, Mays D, Boyle RG, Tam J, Chaloupka FJ. The effect of tobacco control policies on US smokeless tobacco use: A structured review. Nicotine Tob Res. 2017;20:3–11. doi: 10.1093/ntr/ntw291. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.John RM, Rao RK, Rao MG, Deshpande RS, Sengupta J, Selvaraj S, et al. Paris: International Union against Tuberculosis and Lung Disease; 2010. The economics of tobacco and tobacco taxation in India. [Google Scholar]

- 8.Selvaraj S, Srivastava S, Karan A. Price elasticity of tobacco products among economic classes in India, 2011-2012. BMJ Open. 2015;5:e008180. doi: 10.1136/bmjopen-2015-008180. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9.Kostova D, Dave D. Smokeless tobacco use in India: Role of prices and advertising. Soc Sci Med. 2015;138:82–90. doi: 10.1016/j.socscimed.2015.05.036. [DOI] [PubMed] [Google Scholar]

- 10.Joseph RA, Chaloupka FJ. The influence of prices on youth tobacco use in India. Nicotine Tob Res. 2014;16(Suppl 1):S24–9. doi: 10.1093/ntr/ntt041. [DOI] [PubMed] [Google Scholar]

- 11.Nargis N, Hussain AKMG, Fong GT. Smokeless tobacco product prices and taxation in Bangladesh: Findings from the international tobacco control survey. Indian J Cancer. 2014;51(Suppl 1):S33–8. doi: 10.4103/0019-509X.147452. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12.World Health Organization. WHO report on the global tobacco epidemic, 2015: Raising taxes on tobacco. Geneva, Switzerland: World Health Organization; 2015. [accessed on January 1, 2016]. Available from: http://www.who.int/tobacco/global_report/2015/report/en/ [Google Scholar]

- 13.World Health Organization. WHO report on the global tobacco epidemic, 2017: Monitoring tobacco use and prevention policies. Geneva, Switzerland: World Health Organization; 2017. [accessed on August 4, 2017]. Available from: http://www.apps.who.int/iris/bitstream/10665/255874/1/9789241512824-eng.pdf?ua=1 . [Google Scholar]

- 14.Global adult tobacco survey (GATS India report) 2016-2017. New Delhi, India: Tata Institute of Social Sciences; 2017. Ministry of Health and Family Welfare, Government of India. [Google Scholar]

- 15.International Institute for Population Sciences. Global Adult Tobacco Survey (GATS India Report) 2009-2010. Mumbai: IIPS, Ministry of Health and Family Welfare, Government of India; 2010. [Google Scholar]

- 16.Nargis N, Thompson ME, Fong GT, Driezen P, Hussain AK, Ruthbah UH, et al. Prevalence and patterns of tobacco use in Bangladesh from 2009 to 2012: Evidence from international tobacco control (ITC) study. PLoS One. 2015;10:e0141135. doi: 10.1371/journal.pone.0141135. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 17.Rout SK, Arora M. Taxation of smokeless tobacco in India. Indian J Cancer. 2014;51(Suppl 1):S8–12. doi: 10.4103/0019-509X.147420. [DOI] [PubMed] [Google Scholar]

- 18.Sangwan S. New Delhi: Government of India Perspective; 2012. Tobacco taxation structure in India. [Google Scholar]

- 19.Directorate General of Systems & Data Management, Customs & Central Excise. Historical data on excise taxes. (Ministry of Finance, Government of India, 2017) [Google Scholar]

- 20.John RM, Dauchy E, Goodchild M. Goods and service tax reform and estimated impact on tobacco products in India. [accessed on June 30, 2018];Tob Induc Dis. 2018 16(Suppl 1):A121. Available from: https://doi.org/10.18332/tid/83781 . [Google Scholar]

- 21.Government of Bangladesh. Tariff schedule. National board of revenue, Ministry of finance. Bangladesh: Government of Bangladesh; 2017. [Google Scholar]

- 22.Rijo M John. Noida: WHO FCTC Global Knowledge Hub on Smokeless Tobacco, National Institute of Cancer Prevention and Research; 2018. [accessed June 30, 2018]. Taxation and pricing of smokeless tobacco products. Smokeless Tobacco Webinar Series 2018. Available from: http://untobaccocontrol.org/kh/smokelesstobacco/details-second-webinar/ [Google Scholar]

- 23.Nargis N, Stoklosa M, Drope J, Fong GT, Quah ACK, Driezen P, et al. Waterloo, Ontario, Canada: University of Waterloo, Waterloo, Ontario, Canada; 2016. [accessed on July 31, 2017]. The trend in affordability of tobacco products in Bangladesh 2009-2015: Evidence from ITC Bangladesh surveys. Available from: http://www.canceratlas.cancer.org/assets/uploads/2016/05/ITCBDTobacco-Affordability-in-Bangladesh.pdf . [Google Scholar]

- 24.Central board of Excise and Customs, Ministry of Finance. Chapter 24: Central excise tariff 2016-17. 2017. [accessed on July 31, 2017]. Available from: http://www.cbic.gov.in/htdocs-cbec/excise/cxt-2016-17-new/cxt-1617-june16-idx .

- 25.Central board of Excise and Customs, Ministry of Finance. GST Rates. 2018. [accessed on June 20, 2018]. Available from: http://www.cbic.gov.in/htdocs-cbec/gst/index .