Abstract

Objective

To assess the effects of longitudinal patterns of health insurance and poverty on out‐of‐pocket expenditures among low‐income late middle‐aged adults.

Data Sources/Study Setting

Six waves (2002–2012) of the Health and Retirement Study, in combination with RAND Center for the Study of Aging data, were used.

Study Design

A random coefficient regression analysis was conducted in a multilevel growth curve framework to estimate the impact of health insurance and poverty on out‐of‐pocket expenditures.

Principal Findings

At baseline, individuals with private insurance or unstable coverage were more likely to have out‐of‐pocket expenditures and financial burdens than public insurance holders. Over time, the poor who had no insurance, unstable coverage, or insurance type change had higher out‐of‐pocket expenditures; private coverage holders had higher odds of financial burden.

Conclusions

Unstable insurance coverage had a discernible effect on the long‐term, out‐of‐pocket expenditures among low‐income adults. Findings have an important policy implication to protect poor late middle‐aged population; as this population enters old age, the high financial burden it faces may exacerbate persistent socioeconomic health disparity among older people with unstable insurance coverage.

Keywords: Health insurance coverage change, poverty, out‐of‐pocket expenditure change, out‐of‐pocket burden, late middle age

Along with rising health care costs and sustained disparities in health care access and health outcomes, out‐of‐pocket expenditure (OOPE), the amount typically spent for health care service use (Chen et al. 2014), has been a key concern among researchers and policy makers. High health care OOPE often contributes to families’ financial difficulties (Cunningham 2009). High OOPE has also been linked to reduced use of health care and has the potential to aggravate socioeconomic inequality in health care access and health outcomes (Eaddy et al. 2012). In 2010, more than 40 percent of low‐income Americans spent more than 5 percent of their incomes on OOPE, a percentage that increased by 1.4 percentage points between 2010 and 2013—the largest increase occurring among the poor (Baird 2016).

This study aimed to extend the OOPE literature by addressing three concerns. First, current knowledge about OOPE comes largely from the population aged 18 to 64; few studies have focused on the late middle‐aged. Unmet health care needs among the late middle‐aged due to high OOPE have important implications for future health spending; demand for health care workers; and continued labor force participation (Martin et al. 2010), as individuals in this life stage are generally at greater risk of serious health problems (Johnson and Crystal 2000). As life circumstances change rapidly in late middle age, individuals may alternate between Medicaid and private insurance, or between no coverage and coverage (Smolka, Multack, and Figueiredo 2012). Their insurance status tends to be more affected by their employment status than does their younger counterparts’ (Blumberg, Garrett, and Holahan 2016) because they transition in and out of the labor force—moving, for example, from full‐ to part‐time employment before retiring (Banerjee and Blau 2016). Also, late middle‐aged adults with no or intermittent insurance coverage reported greater difficulty affording care than those with continuous coverage (Skopec et al. 2016). Those with long periods of no insurance may be at risk of higher barriers to health care access and high OOPE burden (Zimmer 2012).

Second, focusing on the low‐income late middle‐aged, we examine two OOPE drivers: health insurance coverage types and poverty (Banthin, Cunningham, and Bernard 2008). Studies typically examine these two factors separately; they rarely explore the extent to which insurance type, poverty, and OOPE are related. To better understand the variation in OOPE, it is important to consider both insurance status and poverty level. The challenges that OOPEs pose for the economically vulnerable are well known (Baird 2016). For example, Magge et al. (2013) compared OOPE burden among four insurance types and showed that 91.4 percent of low‐income adults had high OOPE burden, regardless of insurance type. In the United States, the poor had the highest uninsured rate (Smith and Medalia 2014) and a significant increase in OOPE, or financial burden due to OOPE, occurred when insurance coverage was absent (Sommers and Oellerich 2013). The poor appeared to have longer periods without insurance than the nonpoor (Rhoades and Cohen 2013). The near‐poor are more likely to fall in a coverage gap, reflecting public insurance eligibility rules and unstable employer‐sponsored coverage (Martinez, Cohen, and Zammitti 2016). People living in extreme poverty tend to be less healthy, and they are likely not to obtain medical care because meeting OOPEs is a burden (Frohlich et al. 2015). Despite the importance of extreme poverty, to our knowledge, no studies have analyzed the association among deep poverty, insurance status, and OOPE.

Third, prior OOPE studies have focused on a single or short time period, so the extent to which OOPE changes over time is largely unknown. Using two‐wave data, Cunningham (2009) showed that individuals without high burdens in either year were less likely to be continuously insured. Another study explored changes in high OOPE burden between 2001 and 2011 (Li et al. 2014). At the beginning, there was a substantial difference in high OOPE burden between the privately insured, publicly insured, and uninsured. This was also true when comparing poor and low‐income groups to high‐income groups. By the end of the study period, these differences disappeared or diminished. Banthin, Cunningham, and Bernard (2008) also found that financial burdens were highest among the poor with private insurance, about twice that of those with middle incomes and four times that of those with high incomes. Moreover, financial burdens increased for the poor, which indicates that private coverage was becoming less affordable for this group. Focusing on late middle‐aged adults, Johnson and Crystal (2000) investigated how OOPE changes over time varied with three baseline insurance coverage types using two‐wave data. OOPEs were significantly higher for the uninsured than for those with private insurance. The uninsured used relatively few health services unless they were seriously ill, in which case they were likely to acquire public insurance. Most of these studies tend to be descriptive and/or cross‐sectional, which undermines the ability to understand the extent to which stability or instability in insurance type is associated with OOPE changes.

To address these three primary concerns, this study had two aims. First, we examined to what extent changes in insurance types and poverty level were associated with changes in OOPEs and OOPE burden over a 10‐year period. Second, we investigated to what extent the associations between insurance types and OOPEs/OOPE burden varied by poverty level.

Data and Methods

We used six waves of panel data from the 2002–2012 Health and Retirement Study (HRS), in combination with RAND Center for the Study of Aging data. Conducted by the University of Michigan with support from the National Institute of Aging, HRS is a nationally representative panel of noninstitutionalized adults aged 51 and older in the United States and reinterviews respondents biennially (HRS 2008).

We used four criteria to draw our sample: First, we restricted our sample to late middle‐aged adults between ages 51 and 64 (observations = 37,964). Second, we excluded those who responded to biennial surveys in fewer than three of six waves (observations = 15,544) to analyze changes in insurance status associated with changes in OOPEs. Third, we excluded respondents who were institutionalized or unable to independently answer survey questions (observations = 724). Fourth, we excluded adults with incomes higher than 250 percent of the federal poverty level (FPL) (observations = 15,221). We focused on people with incomes below 250 percent of FPL, because these people would most likely benefit from Medicaid expansions and cost‐sharing subsidies under the Affordable Care Act (ACA). Finally, listwise deletion for missing information on either the dependent or the explanatory variables led to further reductions, resulting in a total sample size of 1,866 adults (observations = 5,260).

To control for bias in follow‐up waves, introduced by missing data resulting from death or refusal to participate, we included attrition as a covariate. A few died (N = 23; Observations = 66; 1.25 percent) during the study period. Including death information as a separate control variable during sensitivity tests introduced little change in effect sizes for the other variables, so attrition including death information was included in the models.

Dependent Variables

To achieve our research aims, we used two dependent variables: one continuous variable (out‐of‐pocket expenditures) and one dichotomous variable (financial burden due to high out‐of‐pocket expenditures). The HRS asked respondents a series of questions about the amount and cost of health care services they had used for the last two years. Out‐of‐pocket expenditures (OOPEs) were defined as the amount paid by the family for medical provider visits, hospital inpatient stays, outpatient services, and prescription medications during the period. Despite the two‐year recall period and self‐reported measures, the quality of the health care use and cost data in the HRS has proven acceptable and has been widely used in research (Chen et al., 2014). Moreover, HRS OOPE estimates are similar to those from other datasets (Johnson and Crystal 2000).

For the OOPEs analysis, we explored OOPEs directly related to health care use that includes deductibles, copayments, and all other health expenses not covered by insurance. Following previous studies, health insurance premiums were not included, enabling us to focus on the amount spent at the point of health care use (Chen et al., 2014; Baird 2016). To reduce skewness in the OOPE distribution, the logarithmic‐transformed OOPE was used in analyses (Johnson and Crystal 2000).

For the burden analysis, we measured the financial burden resulting from high OOPEs by calculating a household's medical expenses as a percentage of disposable income. If this ratio exceeded 5 percent for individuals with household incomes below 200 percent FPL and 10 percent for those with higher incomes (Baird 2016), individuals in the household were regarded as having financial burdens resulting from high medical OOPEs.

Independent Variables

Respondents indicated the type of insurance coverage they had at each wave of interviews and were grouped into five mutually exclusive categories: (1) those not covered by private insurance at any time during the study period and who were constantly covered by Medicaid, Medicare, or other public coverage (constantly public); (2) respondents who constantly had only private insurance coverage (constantly private); (3) respondents who were constantly uninsured; (4) respondents whose insurance coverage changed between private and public with no uninsured periods (insurance type changed); and (5) respondents with partial or intermittent insurance coverage or those who were uninsured at any time (unstable coverage). Respondents who reported having both Medicaid and private insurance at the same time were excluded (0.77 percent) to isolate the effect of each insurance type (Li et al. 2014). The constantly public group is treated as the reference group for the growth curve models as public insurance has been proved effective in reducing OOPEs (Finkelstein and McKnight 2008).

Poverty level was divided into four categories: nonpoor (150–250 percent FPL); near‐poor (100–150 percent FPL); poor (50–100 percent FPL); and extremely poor (below 50 percent FPL).

Covariates

A dummy variable for gender (female = 1) was created. Race/ethnicity was coded into three categories: Caucasians (reference; 0), non‐Hispanic African Americans (1), and others (2). Educational attainment was measured: high school graduates (0), less than high school (1), and some college education or more (2). Residential area was assessed: city areas (1) and rural areas (0). For marital status, respondents who were married during the whole study period formed the reference group; constantly unmarried (1); and changed marital status (2). Work status was measured in the same manner: constantly worked (0); constantly not worked (1); and work status changed (2) during the study period. Multiple chronic conditions (MCCs) were defined as suffering from two or more chronic health conditions (high blood pressure, diabetes, cancer, lung disease, heart disease, stroke, psychiatric problems, and arthritis) ever diagnosed by a doctor. A binary indicator was used to measure presence of MCCs (0/1). We identified disabled adults by their work‐related disability.

Analysis Strategy

We began with a descriptive analysis exploring baseline characteristics of individuals within each insurance subgroup. Overall differences in percentages and standard errors were examined using chi‐square tests, and overall differences in means were tested using Wald F‐tests. We applied sample weights for cross‐sectional analyses (Table 1) to reflect the sampling design of the HRS. However, we did not apply weights to the regression models. Proper application of survey weights to survey data remains unclear as survey weights depend on the actual data and the design of the survey. It becomes particularly challenging in complex analyses. In a complicated multilevel regression model, it becomes difficult to interpret or use the result (Gelman 2007).

Table 1.

Baseline Characteristics of Each Insurance Status Group (Mean or Median [standard error] or %)

| Total Sample | Constantly Public (N = 909; 48.71%) | Constantly Private (N = 337; 18.06%) | Constantly Uninsured (N = 149; 7.98%) | Insurance Type Changed (N = 263; 14.09%) | Unstable Coverage (N = 208; 11.25% | |

|---|---|---|---|---|---|---|

| Age** | 59.42 (3.19) | 59.32 (3.21) | 59.87 (2.90) | 59.48 (3.29) | 59.61 (3.13) | 58.85 (3.43) |

| Race*** | ||||||

| Caucasian | 67.43 | 59.82 | 80.56 | 63.49 | 74.05 | 76.34 |

| African American | 20.79 | 25.79 | 14.42 | 14.28 | 17.57 | 15.59 |

| Others | 11.78 | 14.39 | 5.02 | 22.23 | 8.38 | 8.07 |

| Gender (female) | 68.99 | 67.63 | 74.32 | 71.07 | 67.66 | 65.48 |

| City residence** | 74.27 | 77.27 | 73.66 | 56.34 | 73.64 | 73.65 |

| Marital status *** | ||||||

| Constantly married | 35.03 | 27.33 | 39.81 | 46.03 | 43.93 | 45.69 |

| Constantly unmarried | 54.59 | 61.69 | 54.54 | 44.44 | 41.84 | 43.01 |

| Status changed | 10.38 | 10.98 | 5.32 | 9.53 | 14.23 | 11.30 |

| Education*** | ||||||

| Less than high school | 49.88 | 57.73 | 28.21 | 51.58 | 49.37 | 47.84 |

| High school graduates | 28.13 | 21.73 | 32.28 | 41.26 | 34.30 | 34.94 |

| Some college or higher | 21.99 | 20.54 | 39.51 | 7.14 | 15.89 | 17.22 |

| Employment*** | ||||||

| Constantly employed | 11.32 | 5.15 | 29.78 | 14.28 | 11.29 | 6.98 |

| Constantly unemployed | 54.37 | 68.27 | 33.22 | 25.39 | 52.71 | 44.08 |

| Status changed | 34.31 | 26.58 | 37.00 | 60.33 | 36.00 | 48.94 |

| Health | ||||||

| Work‐related disability *** | 39.68 | 58.39 | 11.91 | 2.38 | 40.58 | 19.35 |

| Multiple chronic conditions *** | 67.88 | 75.52 | 54.54 | 44.44 | 73.22 | 62.36 |

| Poverty status*** | ||||||

| Nonpoor (above 150%) | 35.98 | 28.97 | 56.42 | 33.33 | 38.49 | 32.79 |

| Near‐poor (100–150%) | 21.18 | 21.84 | 21.00 | 19.04 | 21.75 | 18.27 |

| Poor (50–99%) | 27.41 | 34.24 | 8.15 | 26.19 | 26.35 | 29.03 |

| Extremely poor (<50%) | 15.43 | 14.95 | 14.43 | 21.44 | 13.41 | 19.91 |

| Household income*** (median, $) | 13092.00 (10458.98) | 11160.00 (9011.44) | 18075.00 (12321.97) | 12887.00 (13609.44) | 14400.00 (9635.5) | 12500 (10393.96) |

| Out‐of‐pocket expenditure*** (median, $) | 288.00 (6212.66) | 250.00 (4729.60) | 318.00 (3370.76) | 300.00 (4823.43) | 200.00 (7438.89) | 400.00 (15443.05) |

| Logged OOPE*** (median) | 4.39 (3.04) | 3.25 (3.15) | 5.44 (2.38) | 3.93 (3.06) | 3.93 (2.89) | 4.52 (3.19) |

| OOPE burden | ||||||

| 5% of household income | 21.80 | 20.52 | 27.27 | 16.66 | 16.73 | 27.95 |

| 10% of household income* | 15.75 | 14.59 | 21.00 | 9.52 | 11.71 | 20.96 |

Statistically significance differences between insurance status groups are denoted by *(p < .05), **(p < .01), and ***(p < .001); N = 1,866.

Second, for the OOPE analysis, we used a random coefficient regression analysis to assess OOPE trajectories in relation to insurance and poverty level. Here, the OOPE trajectories are characterized in the context of between‐individual variation in initial levels of and the rate of change in OOPE over time (Neelon, O'Malley, and Normand 2011). This approach is specifically designed to analyze changes in repeated measures of longitudinal or panel data (Bollen, Christ, and Hipp 2004). It accounts for within‐individual changes over time as well as between‐individual differences in change patterns by dividing the model into two levels, meaning the data are treated as repeated measures (level‐1) nested within individuals (level‐2) (Singer and Willett 2003). The linear mixed models are based on person‐specific initial values (intercepts) and rates of change (slope) that indicate intraindividual patterns of change in OOPE as a function of age. We centered age at the grand mean for the intercept (age 58) to represent an individual of average age at baseline, in order to determine changes in OOPE based on the age difference between individual and group.

We conducted preliminary analyses to determine the specification of fixed and random effects for OOPE change and respondent's age (results not shown). As the starting point for longitudinal analysis, we estimated the total constant correlation across occasions and assessed the relative magnitude of each source of variation via an intraclass correlation (ICC). The results showed that 47 percent of OOPE was due to the variability between persons, while 53 percent was due to the remaining variation within a person as a result of repeated observations. Comparisons of model fit between models of increasing complexity indicated that a random linear model provided the best fit for describing age‐related outcome change. The repeated observation equation that captured OOPE change associated with age is defined as follows:

| (1) |

Y it represents the OOPE for respondent i at time t; α i represents the mean number of OOPE at age 58 for a respondent i; β i is the mean linear component of the trajectory indicating the linear rate of change in OOPE for respondent i with each additional year of AGE; and ε it is an error term which is the deviation of each respondent i at time t from his or her average level of OOPE. Our data involve equal time intervals between observations (2 years), which could be easily incorporated into the random coefficient growth curve model involving random effects (age) to examine intraindividual differences in initial status and rates of change. The estimation of the fixed and random effects for a specific individual can be expressed as follows:

| (2) |

Here, αi can be interpreted as OOPE at time t = 0 for a respondent who has an average trajectory (u 1i = 0); β i is the expected amount of change in OOPE per year for a respondent who has an average trajectory (u 2i = 0). The error terms, u 1i and u 2i , reflect the amount of variation that exists among individuals in relation to their growth parameters. Combining the equations (1) and (2), the mixed model of fixed and random effects can be expressed as (3). Here, the former parenthesis is interpreted as the fixed effects (level‐1) that estimate repeated observations capturing changes in OOPE associated with age. The latter parenthesis is the random effects (level‐2) that capture intraindividual differences in the initial level and rates of change.

| (3) |

Third, we conducted burden analysis. As the OOPE burden was a dichotomized variable, we conducted preliminary analyses to determine the specification of fixed and random effects for change in OOPE burden over time using random logistic regression in a multilevel growth curve framework (xtmelogit in STATA [StataCorp LLC, College Station, TX, USA]) (results not shown). Coefficients for age were not allowed to vary at the individual level (a random slope model); that is, there was no evidence of variation in individual‐level changes (a random slope model). Therefore, we used random‐effects logistic regression models (xtlogit in STATA). These models accounted for the correlation of repeated observations from each individual resulting from the longitudinal design and included an individual‐specific random intercept, allowing us an individual‐specific interpretation.

In preliminary analyses, we included possible confounders (e.g., health care utilization) and the results were not notably different from those that emerged from analyses conducted without confounders. But we could not present these results in this study because the model fit of the hierarchical models did not significantly improve. For both the random coefficient growth curve model and the random intercept logistic regression model, Model 1 examined the effects of insurance and poverty level and Model 2 tested the effect of interactions between insurance and poverty level. For all analyses, STATA (version SE 13.1) was used.

Results

Table 1 presents baseline characteristics of the sample and their bivariate associations with insurance coverage status groups measured over a 10‐year period. Of 1,866 late middle‐aged adults at baseline, almost half belonged to the constantly public group. Individuals in this group had lower socioeconomic status (SES) relative to those in other groups. They spent relatively low OOPEs, but about 20 percent of the group spent 5 percent of household income for medical out‐of‐pocket spending. Individuals in constantly private spent much higher OOPEs, and larger proportions of people who experienced OOPE burdens than those in constantly public. Individuals in constantly uninsured had the smaller proportion of people with OOPE burdens than those in constantly private. The insurance type changed group spent the lowest OOPEs and relatively small proportions of people who experienced OOPE burdens. The unstable coverage group spent the highest OOPEs. Its proportion of people who experienced OOPE burdens was similar to that found in the constantly private group.

Table 2 presents estimates from random coefficient growth curve models of low‐income late middle‐aged adults’ logged OOPEs. Model 1 contains estimates for the effects of insurance and poverty level on the initial level and changes in logged OOPEs controlling for sociodemographic and health factors and panel attrition. The initial level of logged OOPEs varied significantly in two insurance groups, constantly private and unstable coverage. Late middle‐aged adults who constantly had private insurance had logged OOPEs that were 1.21 higher, and those whose insurance coverage was unstable had logged OOPEs that were 0.39 more than those constantly public. The initial level of logged OOPEs varied significantly by the poverty level, and all poverty groups spent significantly less on logged OOPEs than the nonpoor: The poor spent 0.50 less; the extremely poor 0.36 less; and the near‐poor 0.26 less logged OOPEs at baseline than the nonpoor. But, the age‐associated rate of change in logged OOPEs generally did not significantly vary by the insurance status and poverty level. That is, the five insurance groups had statistically similar rates of change in logged OOPEs with age.

Table 2.

Effects of Insurance and Poverty on Trajectories of Out‐of‐Pocket Expenditures among Late Middle‐Aged Adults

| Fixed Effects | Model 1 | Model 2 |

|---|---|---|

| Intercept (baseline level)† | 3.85 (0.26)*** | 4.02 (0.27)*** |

| Insurance status (ref: constantly public) | ||

| Constantly private | 1.21 (0.18)*** | 0.95 (0.21)*** |

| Constantly uninsured | 0.12 (0.19) | −0.19 (0.26) |

| Insurance type changed | 0.06 (0.15) | −0.00 (0.22) |

| Unstable coverage | 0.39 (0.16)* | 0.41 (0.23) |

| Poverty level (ref: nonpoor) | ||

| Near‐poor | −0.26 (0.09)** | −0.29 (0.15) |

| Poor | −0.50 (0.10)*** | −0.62 (0.14)*** |

| Extremely poor | −0.36 (0.11)** | −0.75 (0.18)*** |

| Interaction terms | ||

| Constantly private × near‐poor | 0.14 (0.26) | |

| Constantly private × poor | 0.49 (0.36) | |

| Constantly private × extremely poor | 1.04 (0.33)** | |

| Constantly uninsured × near‐poor | 0.06 (0.31) | |

| Constantly uninsured × poor | 0.69 (0.32)* | |

| Constantly uninsured × extremely poor | 0.81 (0.35)* | |

| Insurance type changed × near‐poor | 0.05 (0.28) | |

| Insurance type changed × poor | −0.24 (0.29) | |

| Insurance type changed × extremely poor | 0.49 (0.34) | |

| Unstable coverage × near‐poor | −0.08 (0.29) | |

| Unstable coverage × poor | 0.00 (0.30) | |

| Unstable coverage × extremely poor | 0.03 (0.34) | |

| Linear slope (rate of change; ageC)‡ | 0.08 (0.04)* | 0.14 (0.05)** |

| Insurance status (ref: constantly public) | ||

| Constantly private | −0.05 (0.06) | −0.10 (0.08) |

| Constantly uninsured | −0.00 (0.07) | −0.15 (0.10) |

| Insurance type changed | −0.10 (0.06) | −0.23 (0.09)* |

| Unstable coverage | −0.00 (0.06) | −0.13 (0.09) |

| Poverty level (ref: nonpoor) | ||

| Near‐poor | 0.01 (0.04) | −0.06 (0.06) |

| Poor | 0.03 (0.04) | −0.10 (0.06) |

| Extremely poor | −0.02 (0.04) | −0.09 (0.08) |

| Interaction terms | ||

| Constantly private × near‐poor | −0.00 (0.11) | |

| Constantly private × poor | 0.16 (0.16) | |

| Constantly private × extremely poor | 0.01 (0.15) | |

| Constantly uninsured × near‐poor | 0.22 (0.13) | |

| Constantly uninsured × poor | 0.29 (0.13)* | |

| Constantly uninsured × extremely poor | 0.19 (0.15) | |

| Insurance type changed × near‐poor | 0.14 (0.12) | |

| Insurance type changed × poor | 0.27 (0.12)* | |

| Insurance type changed × extremely poor | 0.12 (0.14) | |

| Unstable coverage × near‐poor | 0.14 (0.12) | |

| Unstable coverage × poor | 0.29 (0.13)* | |

| Unstable coverage × extremely poor | 0.06 (0.15) | |

| Random effects | ||

| Variance (ageC) | 1.16 (1.37)*** | 1.35 (1.56)*** |

| Variance (Intercept) | 3.24 (0.17)*** | 3.21 (0.17)*** |

| Variance (residual) | 4.77 (0.10)*** | 4.75 (0.10)*** |

| Log likelihood chi2 (df) | −12452.36 (28)*** | −12436.52 (52)*** |

| Likelihood ratio test (∆χ 2) | 32.24 (24)*** | |

The coefficients are based on random coefficient growth curve models controlling for panel attrition, gender, race/ethnicity, city residence, education, employment status, marital status, and health status.

*p < .05; **p < .01; ***p < .001; observations = 5,260; N = 1,866.

†Intercepts indicate person‐specific baseline level (initial values) of out‐of‐pocket expenditures.

‡Linear slopes (rates of change) describe intraindividual patterns of change in out‐of‐pocket expenditures as a function of age (ageC).

In Model 2, we added interaction terms between insurance and poverty groups to examine the extent to which poverty level moderates the main effect of insurance status on logged OOPEs. At baseline, the constantly private group still reported significantly more (0.95) logged OOPEs than the constantly public group. Over time, those in insurance type changed spent 0.23 less logged OOPEs than the constantly public group. At baseline, only the poor and extremely poor spent significantly less logged OOPEs than the nonpoor, but the changes in logged OOPEs did not vary significantly by poverty groups. Of interaction terms significantly associated with logged OOPEs, the extremely poor spent 1.04 more logged OOPEs when they had private insurance. The poor spent 0.69 more logged OOPEs and the extremely poor spent 0.81 more logged OOPEs when they were without insurance. Over time, only the poor spent more logged OOPEs than the nonpoor if they were constantly uninsured (0.29 more), had changed insurance type (0.27 more), or had unstable coverage (0.29 more).

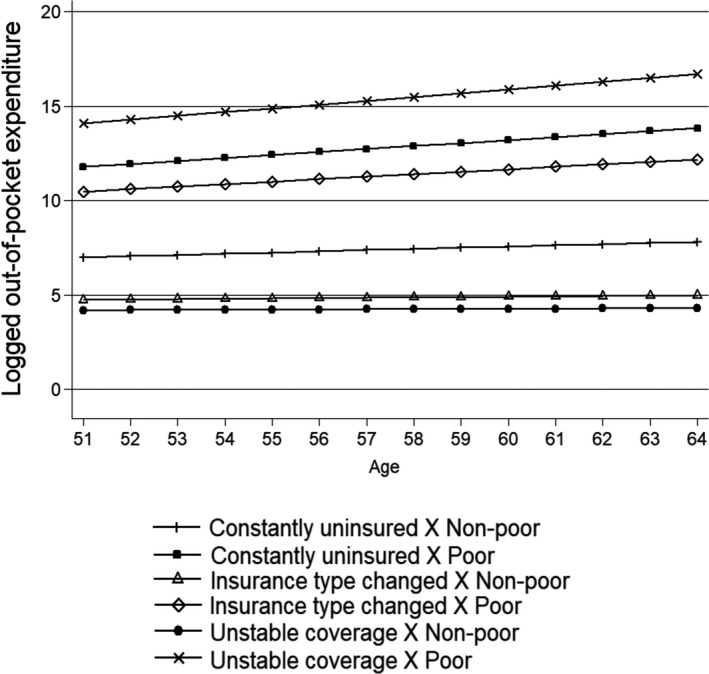

To depict these trajectories of logged OOPEs, we present only the logged OOPE trajectories significantly varied by insurance/poverty groups over time in Figure 1. Only the poor appeared to moderate the effects of insurance status on logged OOPEs. That is, over time, compared to the nonpoor, the poor who had no insurance, those who had unstable insurance coverage, or those who changed insurance type spent more logged OOPEs over time, starting from significantly higher initial levels of OOPEs (ranging from about $20,000 to $100,000) than the nonpoor (ranging from about $54 to $148).

Figure 1.

Age‐Trajectories of Logged OOPE by Interactions between Insurance Status and Poverty Level from Random Coefficient Growth Curve Model

Table 3 presents estimates from random intercept logistic regression models for financial burden due to high OOPEs. Model 1 shows the effects of insurance and poverty level on OOPE burden, with sociodemographic and health factors and panel attrition controlled. Individuals in constantly private had 2.01 higher odds ratio of experiencing OOPE burden than those in constantly public, and unstable coverage had 1.64 higher odds ratio than those in constantly public. Compared to nonpoor individuals, all poor groups had higher odds ratio of facing OOPE burden. Notably, the extremely poor had 7.64 higher odds ratio than the nonpoor.

Table 3.

Effects of Insurance and Poverty on Odds Ratio of Out‐of‐Pocket Expenditure Burden

| Model 1 | Model 2 + Interaction Terms | |

|---|---|---|

| Odds Ratio (Standard Error) | Odds Ratio (Standard Error) | |

| Insurance status (ref: constantly public) | ||

| Constantly private | 2.01 (0.37)*** | 0.78 (0.19) |

| Constantly uninsured | 1.19 (0.24) | 0.83 (0.26) |

| Insurance type changed | 0.96 (0.16) | 0.64 (0.18) |

| Unstable coverage | 1.64 (0.28)** | 1.33 (0.37) |

| Poverty level (ref: nonpoor) | ||

| Near‐poor | 1.41 (0.18)** | 1.08 (0.21) |

| Poor | 1.91 (0.25)*** | 1.21 (0.23) |

| Extremely poor | 7.64 (1.09)*** | 3.06 (0.68)*** |

| Interaction terms | ||

| Constantly private × near‐poor | 2.32 (0.80)* | |

| Constantly private × poor | 3.67 (1.59)** | |

| Constantly private × extremely poor | 17.81 (7.26)*** | |

| Constantly uninsured × near‐poor | 1.07 (0.44) | |

| Constantly uninsured × poor | 2.36 (0.95)* | |

| Constantly uninsured × extremely poor | 1.96 (0.81) | |

| Insurance type changed × near‐poor | 1.21 (0.48) | |

| Insurance type changed × poor | 1.21 (0.48) | |

| Insurance type changed × extremely poor | 3.71 (1.52)** | |

| Unstable coverage × near‐poor | 1.04 (0.40) | |

| Unstable coverage × poor | 1.27 (0.48) | |

| Unstable coverage × extremely poor | 1.86 (0.74) | |

| Cons | 0.10 (0.08)** | 0.14 (0.12)* |

| Log likelihood | −2366.32 (21)*** | −2333.92 (33)*** |

| Likelihood ratio test (∆χ 2) | 64.78 (12)*** | |

The odds ratios are based on random‐effects logistic models controlling for panel attrition, age, gender, race/ethnicity, city residence, education, employment status, marital status, and health status.

*p < .05; **p < .01; ***p < .001; observations = 5,260; N = 1,866.

In Model 2, the addition of interaction terms made significant associations of constantly private and constantly uninsured with OOPE burden disappear; only the extremely poor remained significantly associated with OOPE burden. That is, the extremely poor had 3.06 higher odds of facing OOPE burden than the nonpoor. Of interaction terms significantly associated with OOPE burden, all poor subgroups in the constantly private group had higher odds of OOPE burden. Notably, the extremely poor had 17.8 higher odds of facing OOPE burden if they had constantly private insurance. The poor had 2.36 higher odds of having OOPE burden if they had no insurance. The extremely poor whose insurance type changed had 3.71 higher odds of experiencing OOPE burden.

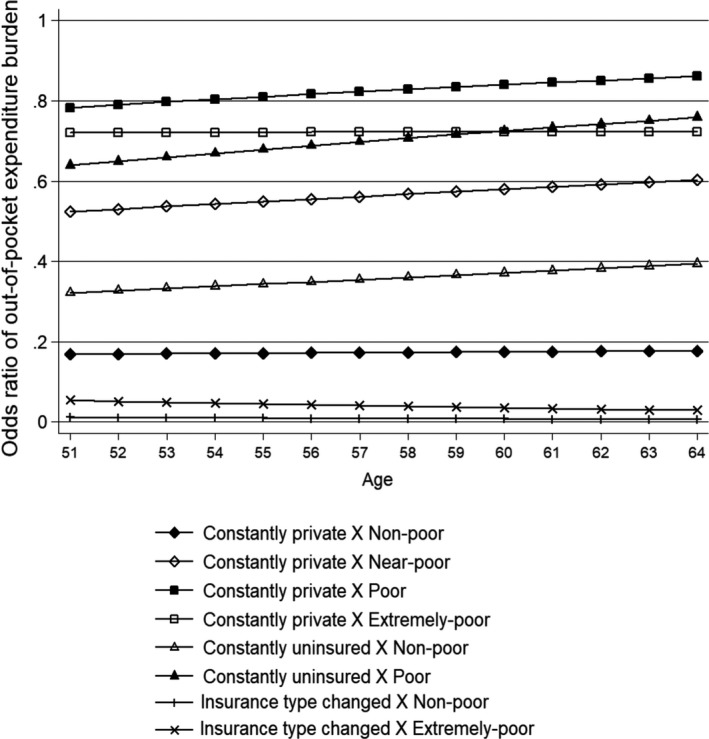

Although in preliminary analysis (random intercept logistic regression model) we found no evidence of variation in change over time in likelihood of OOPE burden, we tried to depict the odds ratios of OOPE burden over time, which varied significantly by insurance/poverty groups (Figure 2). This depiction shows the extent to which the odds ratio of OOPE burden differs between poor and nonpoor within the same insurance group.

Figure 2.

Log Odds of OOPE Burden by Interactions between Insurance Status and Poverty Level from Random Intercept Logistic Regression Model

Discussion

By focusing on the needs of high‐risk populations, particularly the socioeconomically vulnerable, health care reform initiatives aim to reduce disparities in health care access as one way of controlling rising health care costs. This study focused on the low‐income late middle‐aged population, examining relationships among insurance type, poverty, and OOPEs. Specifically, we examined five longitudinal patterns of insurance coverage; whether poverty level is associated with changes in OOPEs and OOPE burden; and the extent to which insurance status and poverty level interact to affect the changes. Our study contributes to the literature on health care spending by providing empirical evidence for the role that changes in health insurance coverage play among low‐income adults. The findings have three major implications.

First, there was a substantial difference in OOPEs and OOPE burden between constantly public and other subgroups. Consistent with prior findings, individuals in constantly private were more likely to spend OOPEs and face financial burden than those in constantly public (Shen and McFeeters 2006). Differences in spending and financial burden between people with private and public coverage may reflect differences in health care needs and sociodemographic characteristics, which affect health care use behavior (Hadley and Holahan 2003). In supplementary analyses, we rotated the reference group to see how the constantly public group compared to other groups and found they were likely to have lower OOPEs. This finding demonstrates that public insurance coverage provides a safety net for low‐income people relative to private insurance (Golberstein and Gonzales 2015). Health insurance coverage may play a protective role for people facing medical needs, but OOPEs vary greatly across public and private insurance products (Shen and McFeeters 2006).

In this study, we intended to provide empirical evidence of how insurance status transitions affect OOPEs under the ACA by restricting our study sample to those with incomes below 250 percent FPL—the population that will be most affected by the ACA's outreach. In our sample, individuals with changes in insurance type made up about 15 percent of the total sample. Of these, about 83 percent had been privately insured but became publicly insured, mostly Medicaid. The remaining 17 percent experienced change in the opposite direction (results not shown). The latter group spent more than twice the OOPEs as the former group. This may help predict the extent to which those late middle‐aged who will be newly eligible for Medicaid under the ACA would experience changes in OOPEs. However, we cautiously suggest that most of the difference in expenditures could be due to differences in provider payment rates. That is, the Medicaid program, which places severe financial strain on states, may have limited access to health care (i.e., specialists and intensive care) for beneficiaries, resulting in their reduced use of health care services (Hadley and Holahan 2003). As policy makers debate the future of the ACA and states consider whether to expand Medicaid, future research should lay a solid foundation of knowledge regarding the benefits associated with Medicaid expansion for low‐income adults.

Notable differences in OOPE between public insurance holders and the uninsured have also been studied. It is important to note that financial constraints on obtaining health care are more likely among those without insurance or with unstable insurance coverage (Clemans‐Cope et al. 2013). In our sample, among adults whose coverage was unstable, about 40 percent who were without insurance at baseline gained public insurance and 16.23 percent gained private insurance. The rest had coverage at baseline but became uninsured. This dynamic pattern of insurance status and its relationship to OOPE changes is an important direction for future inquiry. There also was a substantial difference in OOPEs and OOPE burden between nonpoor and poor adults. Compared to the nonpoor, poor adults were less likely to spend OOPEs but more likely to experience financial burden. However, the association between poverty level and OOPEs or OOPE burden was not significant over time, which may reflect lower use of health care services among the poor, to avoid medical expenses.

Second, insurance status and poverty level were found to be associated with OOPEs and odds for OOPE burden. The poor with private coverage spent higher OOPEs and had much higher odds of facing OOPE burden than the nonpoor with private coverage, which may reflect disparities in private insurance policies. Higher‐income beneficiaries were more likely to have benefits that covered a wider range of health care services or provided better cost‐sharing. In contrast, low‐income adults were less likely to have jobs that offered employer‐sponsored coverage with similar benefits (Rowland and Lyons 1996). Among low‐income adults with private insurance, 19 percent rated their coverage as poor in terms of financial protection (i.e., high medical bills) (Long 2014). It may be that the privately insured poor are not in a more secure position when compared to the uninsured poor. Further work is required to understand the source of the high OOPE burdens among the poor with private insurance, so that the higher medical costs can be prevented. Our study results also contribute to the policy conversation regarding the ACA's cost‐sharing assistance measures for the low‐income individuals who are privately insured. Further study will help achieve an effective financial protection strategy for these individuals.

Third, our analyses confirm that low‐income late middle‐aged adults’ health care spending will continue to increase as they age, but the rate of change will vary depending on insurance types and poverty level. These findings add to current literature on OOPEs and insurance by emphasizing the need to identify the most vulnerable population exposed to significant OOPE increases until they enter old age. Over time, compared to the nonpoor, the poor who had no insurance, unstable coverage, or a change in insurance type were more likely to spend OOPEs. OOPE burden was more likely among the poor without insurance and the extremely poor whose insurance type changed. These groups may be in a coverage gap. For example, due to a financial inability to secure medical services, they might forego necessary health care services or use less health care than needed, particularly preventive care services (Almeida, Dubay, and Ko 2001). In fact, 17 percent of late middle‐aged adults in our sample were in a coverage gap because they were ineligible for public coverage in their state or lacked income to purchase coverage in a private marketplace. Most were in low‐income working families and could not afford their share of insurance costs even if they had employment‐based coverage (Garfield and Damico 2016). Further work is needed to better understand the adults who still hold unstable insurance status or remain uninsured post‐ACA. In fact, it has been reported that a large share of these people still perceives coverage costs as a barrier (Zuckerman et al., 2014). This perception may be particularly correct for poor adults, as even Marketplace subsidies may not make insurance costs affordable.

It would have been helpful if we had considered the Great Recession of 2008 when examining associations among insurance coverage, poverty, and OOPEs. The Great Recession may have affected the sharp decline in employer‐sponsored insurance, especially among low‐wage workers and the increase in the rate of uninsured. Many observe that the economy is now in recovery and cite reduced poverty and unemployment rates as reasons for increased private insurance coverage rates (Holahan 2011). However, our findings will help estimate long‐term patterns of insurance status among low‐income late middle‐aged adults in the context of insurance stability and type. They may also inform policy‐level predictions of characteristics of those at risk of entering old age with high OOPE and the role of insurance in reducing health care burdens.

Supporting information

Appendix SA1: Author Matrix.

Acknowledgments

Joint Acknowledgment/Disclosure Statement: Support for this project came from Center for Social Science of Seoul National University and George Warren Brown School of Washington University in St. Louis.

Disclosures: None.

Disclaimer: None.

References

- Almeida, R. A. , Dubay L., and Ko G.. 2001. “Access to Care and Use of Health Services by Low‐Income Women.” Health Care Financing Review 22 (4): 27–47. [PMC free article] [PubMed] [Google Scholar]

- Baird, K. 2016. “Recent Trends in the Probability of High Out‐of‐Pocket Medical Expenses in the United States.” SAGE Open Medicine 4: 1–8. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Banerjee, S. , and Blau D.. 2016. “Employment Trends by age in the United States: Why Are Older Workers Different?” Journal of Human Resources 2016 (51): 163–99. [Google Scholar]

- Banthin, J. S. , Cunningham P., and Bernard D. M.. 2008. “Financial Burden of Health Care, 2001–2004.” Health Affairs 27 (1): 188–95. [DOI] [PubMed] [Google Scholar]

- Blumberg, L. J. , Garrett B., and Holahan J.. 2016. “Estimating the Counterfactual: How Many Uninsured Adults Would There Be Today without the ACA?” Inquiry 53: 1–13. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Bollen, K. A. , Christ S. L., and Hipp J. R.. 2004. “Growth Curve Model” In The Sage Encyclopedia of Social Science Research Methods, edited by Bryman A., Lewis‐Beck M. S., and Liao T. F. Thousand Oaks, CA: Sage Publishing. [Google Scholar]

- Chen, L. M. , Norton E. C., Langa K. M., Le S., and Epstein A. M.. 2014. “Geographic Variation in Out‐of‐Pocket Expenditures of Elderly Medicare Beneficiaries.” Journal of the American Geriatrics Society 62 (6): 1097–104. [DOI] [PubMed] [Google Scholar]

- Clemans‐Cope, L. , Long S. K., Coughlin T. A., Yemane A., and Resnick D.. 2013. “The Expansion of Medicaid Coverage Under the ACA: Implications for Health Care Access, use, and Spending for Vulnerable Low‐Income Adults.” Inquiry 50 (2): 135–49. [DOI] [PubMed] [Google Scholar]

- Cunningham, P. J. 2009. “Chronic Burdens: The Persistently High Out‐of‐Pocket Health Care Expenses Faced by Many Americans with Chronic Conditions” [accessed on September 27, 2016]. Available at http://www.commonwealthfund.org/~/media/Files/Publications/Issue%20Brief/2009/Jul/Chronic%20Burdens/1303_Cunningham_chronic_burdens_high_OOP_expenses_chronic_conditions_ib.pdf [PubMed]

- Eaddy, M. T. , Cook C. L., O'Day K., Burch K. P., and Cantrell C. R.. 2012. “How Patient Cost‐Sharing Trends Affect Adherence and Outcomes.” P and T 37 (1): 45–55. [PMC free article] [PubMed] [Google Scholar]

- Finkelstein, A. , and McKnight R.. 2008. “What did Medicare do? The Initial Impact of Medicare on Mortality and Out of Pocket Medical Spending.” Journal of Public Economics 92 (7): 1644–68. [Google Scholar]

- Frohlich, L. , Swenson K., Wolf S., Mccartney S., and Hauan S.. 2015. “Financial Condition and Health Care Burdens of People in Deep Poverty.” ASPE Issue Brief, July.

- Garfield, R. , and Damico A.. 2016. “The Coverage Gap: Uninsured Poor Adults in States That Do Not Expand Medicaid – An Update.” Kaiser Family Foundation.

- Gelman, A. 2007. “Struggles with Survey Weights and Regression Modeling.” Statistical Science 22: 153–64. [Google Scholar]

- Golberstein, E. , and Gonzales G.. 2015. “The Effects of Medicaid Eligibility on Mental Health Services and Out‐of‐Pocket Spending for Mental Health Services.” Health Services Research 50 (6): 1734–50. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Hadley, J. , and Holahan J.. 2003. “How Much Medical Care do the Uninsured Use, and Who Pays for It?” Health Affairs W3: 66–81. [DOI] [PubMed] [Google Scholar]

- Holahan, J. 2011. “The 2007–2009 Recession and Health Insurance Coverage.” Health Affairs 30 (1): 145–52. [DOI] [PubMed] [Google Scholar]

- Johnson, R. W. , and Crystal S.. 2000. “Uninsured Status and Out‐of‐Pocket Costs at Midlife.” Health Services Research 33 (5): 911–32. [PMC free article] [PubMed] [Google Scholar]

- Li, R. , Barker L. E., Shrestha S., Zhang P., Duru O. K., Pearson‐Clarke T., and Gregg E. W.. 2014. “Changes over Time in High Out‐of‐Pocket Health Care Burden in U.S. Adults with Diabetes, 2001–2011.” Diabetes Care 37:1629–35. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Long, S. K. 2014. Beyond Coverage: The High Burden of Health Care Costs on Insured Adults in Massachusetts. Boston, MA: Blue Cross Blue Shield Foundation of Massachusetts. [Google Scholar]

- Magge, H. , Cabral H. J., Kazis L. E., and Sommers B. D.. 2013. “Prevalence and Predictors of Underinsurance among Low‐Income Adults.” Journal of General Internal Medicine 28 (9): 1136–42. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Martin, L. G. , Freedman V. A., Schoeni R. F., and Andreski P. M.. 2010. “Trends in Disability and Related Chronic Conditions among People Ages Fifty to Sixty‐Four.” Health Affairs 29 (4): 725–31. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Martinez, M. E. , Cohen R. A., and Zammitti E. P.. 2016. “Health Insurance Coverage: Early Release of Estimates From the National Health Interview Survey, January–September 2015.” National Center for Health Statistics.

- Neelon, B. , O'Malley J. A., and Normand S. T.. 2011. “A Bayesian Two‐Part Latent Class Model for Longitudinal Medical Expenditure Data: Assessing the Impact of Mental Health and Substance Abuse Parity.” Biometrics 67 (1): 280–9. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Rand HRS . 2008. RAND HRS Data. Santa Monica, CA: National Institute on Aging and the Social Security Administration. [Google Scholar]

- Rhoades, J. A. , and Cohen S. B.. 2013. The Long‐Term Uninsured in America, 2008–2011: Estimates for the U.S. Civilian Noninstitutionalized Population Under Age 65. Statistical Brief 424 Rockville, MD: Agency for Healthcare Research and Quality. [PubMed] [Google Scholar]

- Rowland, D. , and Lyons B.. 1996. “Medicare, Medicaid, and the Elderly Poor.” Health Care Financing Review 18 (2): 61–85. [PMC free article] [PubMed] [Google Scholar]

- Shen, Y. , and McFeeters J.. 2006. “Out‐of‐Pocket Health Spending between Low‐ and Higher‐Income Populations: Who Is at Risk of Having High Expenses and High Burdens?” Medical Care 44 (3): 200–9. [DOI] [PubMed] [Google Scholar]

- Singer, J. D. , and Willett J. B.. 2003. Applied Longitudinal Data Analysis: Modeling Change and Event Occurrence. New York: Oxford University Press. [Google Scholar]

- Skopec, L. , Sung J., Waidmann T. A., and Dean O.. 2016. Monitoring the Impact of Health Reform on Americans Ages 50–64, p. 110. AARP Insight on the Issues. [Google Scholar]

- Smith, J. C. , and Medalia C.. 2014. “Health Insurance Coverage in the United States.” U.S. Census Bureau, P60–250, Current Population Reports. Washington, DC: U.S. Government Printing Office. [Google Scholar]

- Smolka, G. , Multack M., and Figueiredo C.. 2012. Health Insurance Coverage for 50‐ to 64‐year‐olds, p. 159. AARP Insight on the Issues. [Google Scholar]

- Sommers, B. D. , and Oellerich D.. 2013. “The Poverty‐Reducing Effect of Medicaid.” Journal of Health Economics 32 (5): 816–32. [DOI] [PubMed] [Google Scholar]

- Zimmer, D. M . 2012. “Inequality in Durations of Insurance Loss Following Employment Disruption” Working paper. Available at http://people.wku.edu/david.zimmer/index_files/surv.pdf

- Zuckerman, S. , Karpman M., Blavin F., and Shartzer A.. 2014. “Navigating the Marketplace: How Uninsured Adults Have Been Looking for Coverage“ [accessed on February 14, 2016]. Available at http://hrms.urban.org/briefs/navigating-the-marketplace.html

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Appendix SA1: Author Matrix.