ABSTRACT

Background

Residents graduate from medical school with increasing levels of debt and also may possess poor financial knowledge and practices. Prior studies have assessed resident financial knowledge and interest in financial education, yet additional information regarding their attitudes about personal finance and financial planning could be essential for the development of relevant curricula.

Objective

We assessed baseline financial attitudes and planning behaviors of internal medicine and internal medicine–pediatrics residents in 3 geographically diverse academic programs.

Methods

A modified version of the Financial Industry Regulatory Authority National Financial Capability survey was administered anonymously to residents in 3 programs in spring 2017. Outcomes included levels of educational debt, positive financial planning behaviors, perception of finances and debt, and education about personal finance.

Results

Response rate was 62% (184 of 298). Rates of educational debt were high, with 81% (149 of 184) of respondents reporting educational debt, and the majority owing more than $100,000. Residents' financial practices were variable, and residents could be grouped into 1 of 3 categories—concerned-engaged, concerned-unengaged, and unconcerned-unengaged—based on their engagement with debt and financial management. Residents with high debt (> $250,000) had a bimodal distribution of respondents who strongly agreed and those who strongly disagreed they were concerned about debt.

Conclusions

Resident financial attitudes and practices are variable, ranging from highly engaged residents actively managing their financial wellness to unengaged residents who have low concern, despite high educational debt.

What was known and gap

Resident debt load and financial knowledge are areas of concern, yet relatively little information has been collected about residents' attitudes regarding their financial situation.

What is new

A study assessed financial attitudes and planning behaviors of internal medicine and internal medicine–pediatrics residents.

Limitations

Limited specialty and geographic representation; survey instrument lacked validity evidence.

Bottom line

Residents' financial attitudes and behaviors fit into various profiles, which may facilitate the creation of tailored financial curricula.

Introduction

Graduate medical education programs need to support residents, including promoting their well-being.1 One area that may threaten well-being is resident finances. Financial well-being is a state where an individual has achieved minimal financial stress, established a strong financial foundation, and created an ongoing plan to reach future financial goals.2 Compared with other college-educated peers, residents often face significant educational debt and delay in accumulating income and savings. Residents also often have little guidance on financial planning.3 Surveys of residents reported low rates of financial knowledge, high levels of debt, and deficits in financial preparedness.4–6 High levels of educational debt among internal medicine residents have been associated with high burnout and low quality of life.7

Lack of financial planning during residency can have long-term effects. Previous studies have shown low rates of saving for emergency funds, financial planning, and contingency planning (disability or life insurance).7–9 Education on financial planning and debt management is important in residency programs, according to surveys of program directors10 and residents.11 However, there are few published studies on the effects of financial curricula in residency programs.3,12–14 Even brief interventions on financial topics were well received by trainees and could change long-term investment behavior.3,13,14 The literature has largely focused on financial knowledge and behaviors, and assessment of single institution, one-size-fits-all interventions. As programs develop interventions to promote financial well-being, it is important to understand residents' attitudes, including level of concern and satisfaction with their personal finances and their current financial behaviors.

The objective of this study was to assess baseline financial attitudes and behaviors—debt management, personal finance, investing for retirement, and employer-based resources—of a multiprogram sample of internal medicine (IM) and internal medicine–pediatrics (MP) residents.

Methods

A cross-sectional survey was administered to IM and MP residents at the State University of New York (SUNY) at Stony Brook, the University of Pittsburgh, and the University of Kansas. The Financial Industry Regulatory Authority (FINRA) Investor Education Foundation commissioned the National Financial Capability Study in 2009 (updated in 2012 and 2015) to assess the baseline financial capability of adults in the United States.15,16 With permission from FINRA, we administered a modified version of the survey to assess residents' satisfaction with their personal finances, ability to pay monthly expenses, emergency savings, and retirement planning. We included 12 questions from the original 125-question FINRA survey, and we changed the answer key from a 10-point to a 5-point scale for 4 questions on level of satisfaction with personal finances and concern about paying student loans. Twelve questions were developed by the study investigators to collect information about type of medical school education, level of training, student loan amount, importance of financial education during residency, role of debt in career choice, disability and life insurance, and sources of prior financial advice (provided as online supplemental material).17 The modified survey was not tested prior to use.

The survey was administered at educational conferences between January and April 2017. Surveys were completed anonymously online via the Qualtrics platform at SUNY Stony Brook and in paper format at the 2 other sites. Paper surveys were collected by faculty not involved in the study or were placed directly into a collection folder. For sites with block scheduling, survey administration was repeated for each block. Paper surveys were entered into a database by 1 author (A.E.M.) and double-checked for accuracy.

The study was approved as exempt by the Institutional Review Boards at SUNY at Stony Brook and the University of Pittsburgh, and as quality improvement at the University of Kansas.

Outcomes of interest included resident levels of educational debt, positive financial planning behaviors (box), perception of finances and debt, and experience with education in personal finance. Analysis was conducted using STATA version 14 (StataCorp LLP, College Station, TX). Descriptive statistics were used for baseline demographic data. Chi-square and Fisher's exact tests were used to analyze categorical variables. Ordinal variables were assessed with analysis of variance as appropriate. Residents were grouped by assessing aggregate variables relating to concern and engagement in positive financial behaviors. Regression analysis was performed to determine what factors might predict a resident's satisfaction with his or her current personal financial situation. Significance was set at P value of .05.

Box Study Definition of Positive Financial Behaviors.

Savings Behaviors18,19

Have a savings account, money market account, or CD

Aware employer offered retirement account

Have a previous employment retirement account

Have a nonemployment retirement account

Regularly contribute to retirement account

Have estimated savings needed for retirement

Have not taken a hardship withdrawal within the last year

Debt Management18

Consolidated loans for loan forgiveness program

Catastrophic Planning18,19

Have rainy day funds

Have a life insurance policy

Have a disability policy

Results

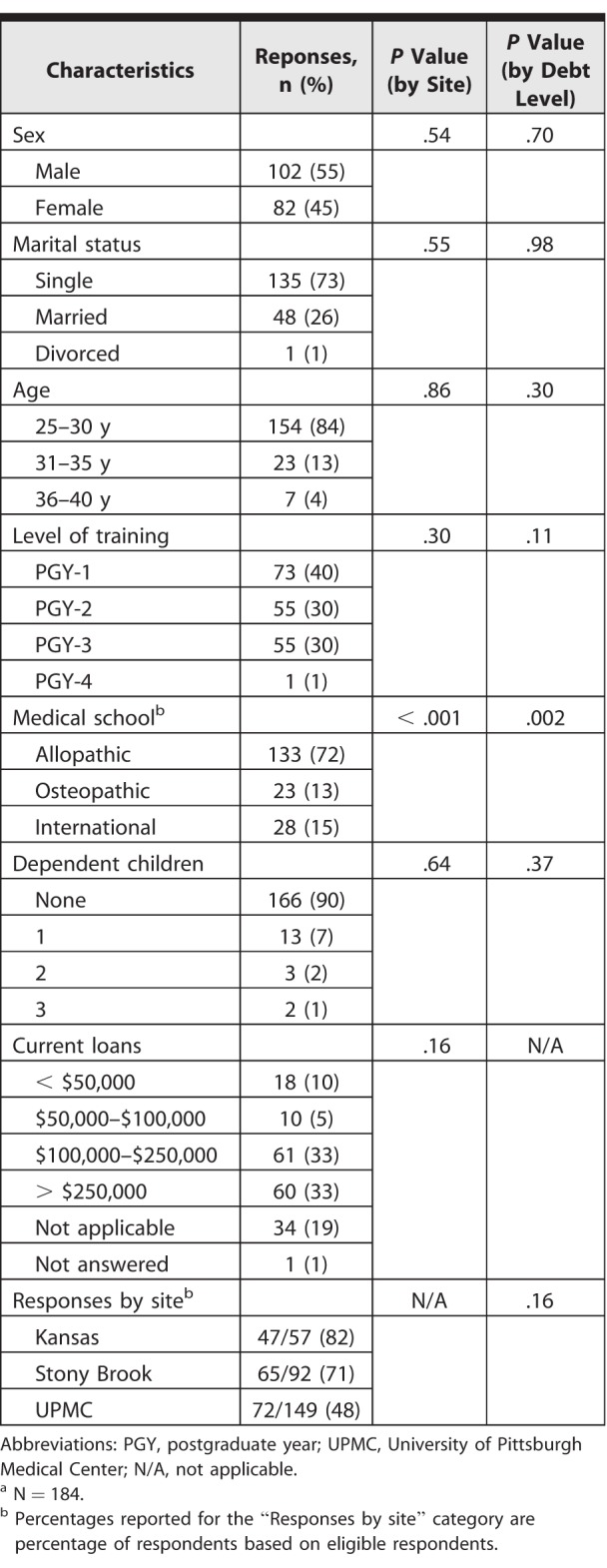

Our response rate was 184 of 298 (62%). Table 1 provides characteristics of respondents, with the majority between ages 25 and 30 years and unmarried with no children. Educational debt levels were high, with 81% (149 of 184) reporting educational debt and 66% (121 of 184) reporting owing more than $100,000.

Table 1.

Demographics of Survey Participantsa

Savings, Debt, and Catastrophic Planning

Participants' financial planning status by level of debt is shown in Table 3. One resident did not report an educational debt level. A total of 77% (141 of 183) responded that employers offered a retirement account. A total of 26% (47 of 183) reported previous employment retirement accounts, 24% (44 of 183) reported nonemployment retirement accounts, and 42% (76 of 183) contributed regularly to a retirement account. However, 67% of respondents (123 of 183) had never estimated retirement savings needs. Residents who engaged in 1 positive financial wellness behavior (eg, having estimated retirement savings needs) were more likely to engage in other positive financial behaviors (such as regularly contributing to a retirement account; 32 of 53 versus 44 of 123; P < .001). A total of 41% (75 of 184) reported consolidating their loans into the Public Service Loan Forgiveness program. Regarding planning for catastrophic events, 61% (112 of 184) reported having a rainy day fund, 45% (83 of 184) had life insurance, and 37% (68 of 184) had disability insurance.

Table 3.

Savings, Debt, and Catastrophic Planning by Level of Debta

Resident Perceptions of Finances and Debt

Among respondents, 46% (85 of 183) reported satisfaction and 34% (63 of 183) reported dissatisfaction with their current financial situation. Two respondents did not respond further to this area of questioning, resulting in 182 respondents. A total of 40% (73 of 182) agreed or strongly agreed they were concerned with their financial situation, 24% (43 of 182) disagreed, and 19% (35 of 182) strongly disagreed. The distribution of responses regarding perception of debt was bimodal, with 36% (65 of 183) strongly agreeing, 15% (28 of 183) agreeing, 10% (19 of 183) neither agreeing nor disagreeing, 15% (27 of 183) disagreeing, and 24% (44 of 183) strongly disagreeing that they had “too much debt right now.” This finding was driven by responses from residents with more than $250,000 in loans, as more residents than expected strongly disagreed that they had too much debt (23 observed versus 14.3 expected, P < .001) and strongly disagreed that they were concerned with paying it off (15 observed versus 11.4 expected, P < .001). Residents with the greatest levels of debt were also less likely than their peers to exhibit behaviors such as obtaining advice about debt management (2 of 34 versus 50 of 149, P < .001) or holding an Individual Retirement Account (4 of 34 versus 40 of 149, P = .007). The amount of loan debt did not correlate with resident agreement that debt had a substantial role in final career choice.

Regression analysis was performed to determine what factors in Table 3 might be associated with a resident's satisfaction with his or her current personal financial situation (adjusted R2 0.190, P < .001). The factors most predictive of satisfaction were whether residents had consolidated in anticipation of Public Service Loan Forgiveness and their perception of having too much debt.

Financial Resources and Educational Curricula

A total of 43% (79 of 184) of residents reported they were the most financially knowledgeable individual in their household, 23% (42 of 184) reported that someone else was most knowledgeable, and 15% (28 of 184) reported no one was knowledgeable. A total of 61% of residents (112 of 184) had sought any financial advice, with 31% seeking advice about savings/investment (57 of 184), 28% about debt (52 of 184), and 26% about insurance (48 of 184). A total of 54% (99 of 184) had participated in financial education offered in college, medical school, or through employment, and 24% (44 of 184) had never been offered financial education. A total of 92% (170 of 184) agreed that personal finance education should be taught during residency, with no differences noted by level of debt or perception of financial situation.

These findings indicate that residents may fit 3 profiles (Table 2): (1) residents concerned about financial wellness and debt and engaged in positive financial practices (concerned, engaged); (2) residents concerned about financial wellness and debt but not engaged in positive financial practices (concerned, unengaged); and (3) residents with high debt, low concern, and maybe not engaged in financial planning (unconcerned, unengaged). Although our study was not designed to define what interventions can help each group, these resident profiles may be useful for developing future financial curricula.

Table 2.

Summary of Resident Profilesa

Discussion

In this study, we found that IM and MP residents have high debt burden, limited engagement in positive financial planning behaviors, and variable concern about their financial well-being. They believe that financial education should be taught during residency, which opens up opportunities to develop targeted financial curricula for this group. Unexpectedly, residents with the highest debt reported both high and low levels of concern about their debt.

Our findings were similar to those of previous educational studies, where residents from various specialties were mostly described to have high educational debt and limited financial preparedness.5,6,8,9,11 In our study, we were able to categorize residents' financial behaviors and attitudes in relation to their concern over educational debt. Our data showed that while a significant portion of residents engage in positive financial behaviors, a subset have high debt, lower levels of concern, and fewer positive financial practices compared with their peers.

To date, most resident financial education interventions have taken a one-size-fits all approach,2,12 and the optimal type and timing for this education are unknown (eg, mandatory versus elective workshops, 1 session versus multiple sessions, etc). Educators may consider focusing future curricula on the most concerning profile (unconcerned, unengaged). This group may be difficult to motivate to exhibit positive financial behaviors due to lack of concern. Given that high educational debt has been associated with lower quality of life,7 and medical education is focusing on resident well-being,1 medical educators may consider including financial education in overall wellness programs.

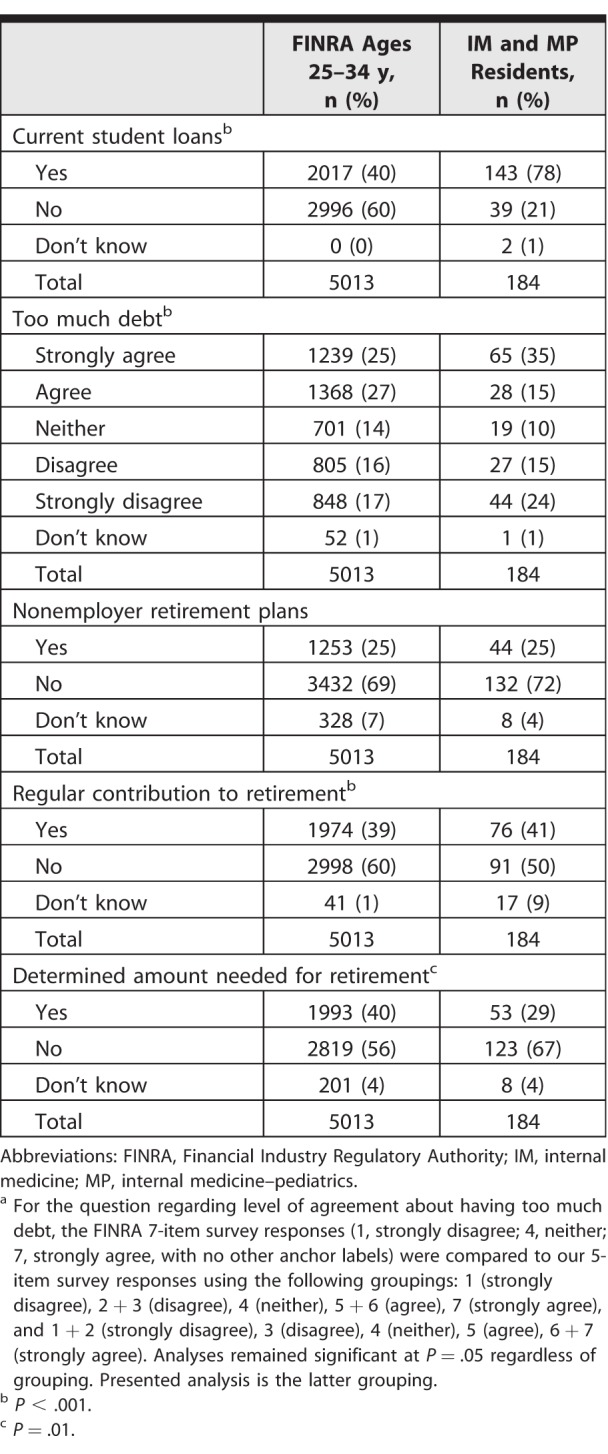

Compared with 25- to 34-year-old respondents of FINRA's 2016 Financial Capability report, residents are more likely to agree that they have too much current loan debt (Table 4). Residents with more than $250,000 of debt were sorted into individuals who disagreed that they had too much debt and were satisfied with their financial position, and those reporting they had too much debt and were dissatisfied with their financial position. Differences disappeared when this group was removed from analysis (P = .46). Compared with age-matched peers, IM and MP residents are less likely to know if they regularly contribute to a retirement account or to figure out how much savings is needed for retirement.17 Residents with high debt loads may be less financially fit compared with peers and may need personal finance education.

Table 4.

Residents' Financial Wellness Behaviors Relative to US Peersa

Limitations of our study include that the questionnaire did not ask about participation in all loan repayment programs, along with self-reporting and inability to corroborate reported financial behaviors. The modified survey was not tested prior to use, and respondents may not have interpreted questions as intended. Answers may also have been affected by social desirability biases. Generalizability is limited by the exclusion of a broad range of specialties, community-based programs, and programs in the western United States.

Residency programs could use the suggested resident profiles to develop and study the effectiveness of tailored financial curricula. Future work could include stratifying residents by profile type, and assessing interventions specific to self-identified resident reports of financial concern.

Conclusion

In a cross-sectional study of 3 university-based IM and MP residency programs, we found residents have high educational debt, variable levels of financial engagement and concern, and strong interest in financial planning education during residency. Residents' financial attitudes and behaviors fit into various profiles, which may facilitate the creation of tailored financial curricula.

Supplementary Material

References

- 1.Accreditation Council for Graduate Medical Education. ACGME tools and resources for resident and faculty member well-being. 2018 http://www.acgme.org/What-We-Do/Initiatives/Physician-Well-Being/Resources Accessed September 27.

- 2.Spann S. Does financial wellness at work really work? Forbes. 2018 January 28, 2016. https://www.forbes.com/sites/financialfinesse/2016/01/28/does-financial-wellness-at-work-really-work/#34a2140967f7 Accessed September 27.

- 3.Dhaliwal G, Chou CL. A brief educational intervention in personal finance for medical residents. J Gen Intern Med. 2007;22(3):374–377. doi: 10.1007/s11606-006-0078-z. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.AMA Insurance Agency Inc. 2017 Report on U.S. physicians' financial preparedness. 2018 https://www.amainsure.com/research-reports/2017-financial-preparedness-medical-students/index.html?page=1 Accessed September 27.

- 5.Ahmad FA, White AJ, Hiller KM, et al. An assessment of residents' and fellows' personal finance literacy: an unmet medical education need. Int J Med Educ. 2017;8:192–204. doi: 10.5116/ijme.5918.ad11. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Teichman JM, Cecconi PP, Bernheim BD, et al. How do residents manage personal finances? Am J Surg. 2005;189(2):134–139. doi: 10.1016/j.amjsurg.2004.11.007. [DOI] [PubMed] [Google Scholar]

- 7.West CP, Shanafelt TD, Kolars JC. Quality of life, burnout, educational debt, and medical knowledge among internal medicine residents. JAMA. 2011;306(9):952–960. doi: 10.1001/jama.2011.1247. [DOI] [PubMed] [Google Scholar]

- 8.Yoo PS, Tackett JJ, Maxfield MW, et al. Personal and professional well-being of surgical residents in New England. J Am Coll Surg. 2017;224(6):1015–1019. doi: 10.1016/j.jamcollsurg.2016.12.024. [DOI] [PubMed] [Google Scholar]

- 9.Teichman JM, Bernheim BD, Espinosa EA, et al. How do urology residents manage personal finances? Urology. 2001;57(5):866–871. doi: 10.1016/s0090-4295(00)01128-6. [DOI] [PubMed] [Google Scholar]

- 10.Lusco VC, Martinez SA, Holk HC., Jr Program directors in surgery agree that residents should be formally trained in business and practice management. Am J Surg. 2005;189(1):11–13. doi: 10.1016/j.amjsurg.2004.05.002. [DOI] [PubMed] [Google Scholar]

- 11.Glaspy JN, Ma OJ, Steele MT, et al. Survey of emergency medicine resident debt status and financial planning preparedness. Acad Emerg Med. 2005;12(1):52–56. doi: 10.1197/j.aem.2004.02.532. [DOI] [PubMed] [Google Scholar]

- 12.Mizell JS, Berry KS, Kimbrough MK, et al. Money matters: as resident curriculum for financial management. J Surg Res. 2014;192(2):348–355. doi: 10.1016/j.jss.2014.06.004. [DOI] [PubMed] [Google Scholar]

- 13.Bar-Or YD, Fessler HE, Desai DA, et al. Implementation of a comprehensive curriculum in personal finance for medical fellows. Cureus. 2018;10(1):e2013. doi: 10.7759/cureus.2013. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 14.Witek M, Siglin J, Malatesta T, et al. Is financial literacy necessary for radiation oncology residents? Int J Radiat Oncol Biol Phys. 2014;90(5):986–987. doi: 10.1016/j.ijrobp.2014.08.010. [DOI] [PubMed] [Google Scholar]

- 15.FINRA Investor Education Foundation. 2015 national financial capability study. State-by-state survey instrument. 2018 http://www.usfinancialcapability.org/downloads/NFCS_2015_State_by_State_Qre.pdf Accessed August 15.

- 16.FINRA Investor Education Foundation. Financial capability in the United States 2016. 2018 July 2016. http://www.usfinancialcapability.org/downloads/NFCS_2015_Report_Natl_Findings.pdf Accessed August 15.

- 17.Marcu MI, Kellerman AL, Hunter C, et al. Borrow or serve? An economic analysis of options for financing a medical school education. Acad Med. 2017;92(7):966–975. doi: 10.1097/ACM.0000000000001572. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 18.Clancy M. Financial planning for medical residents. [PowerPoint slides] 20162018 https://students-residents.aamc.org/video/financial-planning-medical-residents Accessed September 27.

- 19.Weis M. Personal financial planning for physicians. Basics to financial wellness [PowerPoint slides] 20172018 https://www.acponline.org/system/files/documents/meetings/personal_financial_planning_for_physicians_feb_2017_final.pptx Accessed September 27.

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.