ABSTRACT

The debate on drug prices has reached new heights with the controversy around the role of prices in promoting innovation. Critics claim that prices of innovative drugs are excessive and argue that lowering prices will not harm the flourishing innovation. On the opposite end, the pharmaceutical industry insists that restrictive pricing policies will have a detrimental impact on their ability to generate innovation. Amid these two divergent positions, this manuscript presents a conceptual framework to better understand the role played by drug prices to influence the ability of pharmaceutical firms to raise money in capital markets and hence finance pharmaceutical innovation. We argue that deviations from established value-based pricing principles, by either firms or payers, will distort access by firms to capital and lead to an undesirable level of innovation in the long term. We hope that this framework helps policy-makers anticipate the impact of their proposals, and ultimately guide policies towards setting optimal drug prices as a means to maximise social welfare.

KEYWORDS: Innovation, pharmaceutical industry, health technology assessment (HTA), finance, value–based pricing

Introduction

Policy-makers start from the premise that innovation is socially desirable, and as such deserves to be incentivised and rewarded. Multiple types of incentives already exist for basic and applied research because both have important implications for the rate of innovation [1]. For applied pharmaceutical research, multiple forms of incentives exist (incl. patent and data protection, market exclusivity, tax credits and drug prices), which can be viewed as a reward for bringing valuable innovation to patients. This manuscript will focus on drug pricing to shed light on the role it plays in promoting pharmaceutical innovation.

The appropriate level of incentives/rewards needs to be balanced against the sustainability of the healthcare system, a principle that has come to be known as value-based pricing (VBP). VBP lies on the principle that prices should on the one hand reflect the added drug’s benefit to patients, healthcare systems and, in some cases, broader society, and on the other hand reward successful innovation and create incentives for further R&D [2,3]. VBP leads to a win-win outcome because it gives payers a transparent mechanism to signal their priorities to the market, and incentivises the pharmaceutical industry to engage in purposeful R&D that aims to produce the kind of innovations that meet this demand. It necessarily requires both sides to take a long view. This more collaborative approach is particularly critical for a topic rarely discussed in the literature; specifically, the need of pharmaceutical firms to secure the finance to fund R&D activities, generally lasting several years before a product reaches the market and becomes profitable.

However, these principles are not always applied in practice. The pharmaceutical industry is sometimes criticised for taking advantage of their market power by charging prices above what is justifiable, particularly in the absence of therapeutic alternatives. Likewise, payers are also criticised for taking advantage of their monopsonistic purchasing power by extracting unilateral discounts from the industry. This opportunistic approach to pricing negotiation can distort VBP signals, erode trust between payers and manufacturers, and eventually patients and society will lose out.

The aim of this paper is to describe how the pharmaceutical industry finances innovation, and how deviations from the principles of value-based pricing, either by industry or by payers, can distort access to capital markets and lead to undesirable outcomes for patients, healthcare systems and ultimately society at large. We propose a conceptual framework describing the mechanism that links investors in capital markets to pharmaceutical innovation. The framework describes, from a financial perspective, the role played by key features along the lifecycle of pharmaceutical innovation. We anticipate that this conceptual framework will help policy-makers appreciate the lifecycle of innovation from a financial perspective and inform future policy proposals in the area of drug pricing.

Value-based pricing, innovation and sustainability of healthcare systems

The first step of VBP is to define and quantify the drug’s therapeutic value. For this purpose, the clinical and economic evidence is generated, collected, synthesised, analysed and appraised by organizations typically partnering with the local reimbursement authority (hereafter named ‘payer’ for brevity). Nowadays, most countries undertake some form of Health Technology Assessment (HTA); In most countries, the HTA findings are used to inform pricing negotiations rather than directly set the prices of medicines [4]. The two main VBP schools differ with regard to whether the focus of HTA is primarily on establishing the level of added clinical benefit (as in Germany) [5,6] or go beyond by also taking into consideration the economic evidence using cost-effectiveness analysis (as in Sweden or England) [7,8].

An important feature of VBP is that the implementation is adaptable to the payer’s definition of value [9,10]. This flexibility is intended to reflect relevant contextual factors when establishing the drug’s value in a specific jurisdiction (over and above the local standard of care). The generalizability of the VBP principle to different jurisdictions (including low- and middle-income countries) is possible thanks to its adaptability to the local definition of value, noting that the willingness and ability to pay may differ across jurisdictions. Altogether, it is not surprising that countries negotiate different (value-based) prices for the same innovative drug. When entering into Pricing and Reimbursement (P&R) negotiations, the first objective is to define and measure the drug’s added value. Next, the objective is to establish the willingness to pay for the drug’s added value, as well as the ability to pay. The latter helps payers address any concerns about affordability given the local budget constraints or a large prevalent patient population. Multiple payment models are available to ease concerns on affordability as well as the performance of innovative products in the real world. This manuscript will focus on drug pricing. Questions about affordability are outside the scope of this manuscript because the payment models are already described in the literature, comprising sophisticated performance-based commercial arrangements and the more traditional volume-price agreements, where higher utilization is compensated with a lower drug price [11–13].

Despite the adaptability of the VBP principle to the local setting, some policy-makers still view VBP as a threat to the sustainability of healthcare systems because it does not take into account the unmet medical need and disease prevalence, and thus encourage payers to focus on affordability, rather than value, as the driving criterion for pricing negotiations [14,15]. Implicitly, this recommendation advocates for drug prices below the VBP, disregarding any implications for future innovation. And by doing so, the assumption is made that future waves of innovation will not be delayed (or prevented) since the industry’s capacity to develop new treatments will remain unchanged. In this article, we investigate the plausibility of this assumption by exploring the causal relationship between the firm’s profitability and the generation of innovation; to then consider whether uncertainty on the industry’s profitability (e.g., induced by increasingly restrictive pricing policies) could influence its capacity to mobilise sufficient capital to fund R&D activities.

The conceptual framework

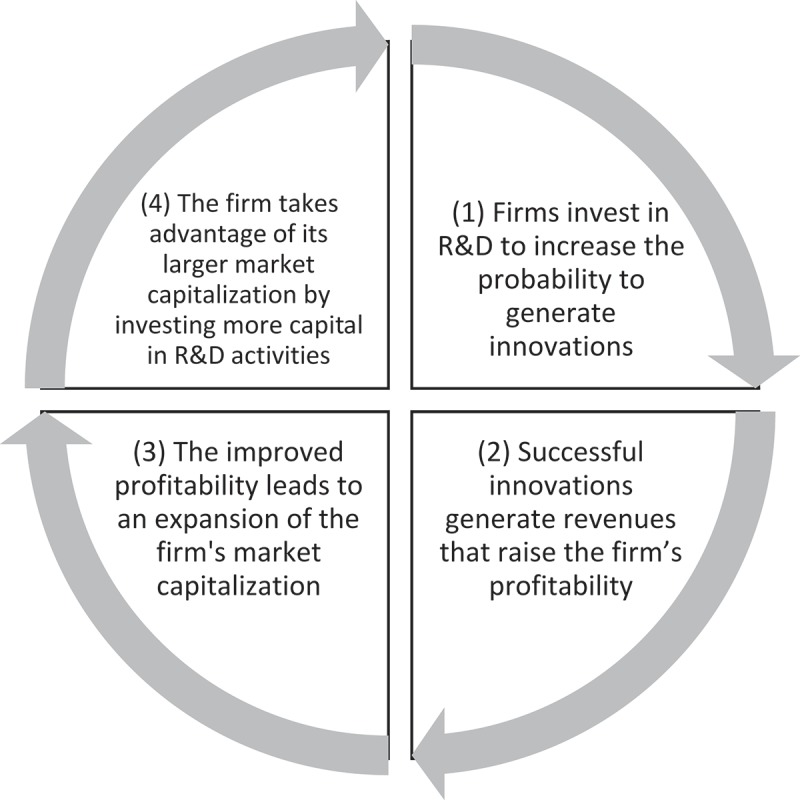

To the best of our knowledge, there is no robust empirical evidence supporting a direct causal relationship between (higher) firms’ profitability and the generation of (more) innovation. Given the lack of this direct evidence, we have developed a conceptual framework representing the lifecycle of pharmaceutical innovation from a financial perspective. The framework breaks up the mechanism leading to innovation in a loop of four causal associations (some of which are based on axioms rather than data) (Figure 1). The four-step loop rotates around the need for companies to remain profitable in order to raise capital and continue funding R&D activities [16,17]. The firm’s ability to develop innovative products and generate profits from marketing them will determine its long-term sustainability. The next three sections describe how profitability determines the market value of a firm, as defined in terms of return on investment from the company and shareholder perspectives.

Figure 1.

Financing of innovation in the pharmaceutical industry.

Market capitalization of innovation-driven companies

The optimal mix of sources and size of capital needed to finance innovation will depend on the firm characteristics and its environment, and no single rule applies to all [18]. Little is known about the relative importance of the different sources of funding used by the pharmaceutical industry. The sparse literature indicates a distinction between larger well-established companies and smaller new start-ups [18], where younger publically-traded companies tend to finance their R&D mainly from equity markets and internal cash flows. In contrast, debt financing is a more important source of finance for larger firms with tangible assets to pledge as collateral [19] Multiple sources of capital are available to a firm, including: 1) selling its own stock or issuing new shares without diluting their price when there is an upwards buying pressure of the company’s stock, 2) taking on more debt (e.g., through corporate bonds) without turning overleveraged, and 3) retaining a larger portion of past earnings (internal cash flows) in detriment of dividends. The latter is welcome by shareholders who believe that the firm will offer a better long term return than could be obtained by investing the dividend elsewhere. For the purpose of this manuscript, we focus on raising capital in the stock markets, although the general principles apply in all these cases. Empirical evidence indicates that the level of access to funding influences the aggregate R&D. For example, Brown et al. 2009 [19] present the boom and bust in the 1990s [in both cash flow and stock market) as a good example of a finance-driven cycle in US R&D. The authors analysed longitudinal data from 1,347 US firms from 1990–2004 and conclude that supply shifts in finance have an aggregate effect on R&D investment. Additional studies supporting similar conclusions can be found in Kerr and Nanda [18].

One possible approach to valuing a firm is given by its market capitalization. It shows how the stock market is valuing the company and is calculated by multiplying the total number of outstanding shares by their price in the stock market. A firm’s market capitalization changes with fluctuations in the quantity of outstanding shares or their price [20]. In the pharmaceutical industry, the share price is known to fluctuate over time depending on the expected profitability of the portfolio (i.e., products already marketed) [21] and pipeline (i.e., products under development) [22]. Besides drug prices, R&D efficiency is a factor where the industry is making major efforts because of its potential to enhance future profitability [23]. Of course, profitability also depends on external factors, such as the entry of competitors, either of marketed products (portfolio competition) or under development (pipeline competition). Another key factor is the loss of market exclusivity and the arrival of generics, making market capitalization partially depend on the firm’s ability to bring new products to the market and generate profits; and more so when the company is close to losing market exclusivity on highly profitable products [24]. Indeed, fluctuations of share prices can be partly interpreted as an indicator of (shareholders’ belief on) the firm’s ability to innovate [25]. This is particularly true for innovation-driven industries, where the dynamics of the stock market are closely related to the dynamics of innovation [26,27,28]. All else being equal, we can anticipate that a firm’s market capitalization will expand with growing outlooks of a commercially successful pipeline [29,30] particularly if supported by a long and solid record of R&D accomplishments [31].

It is interesting to notice the insatiable appetite of the big fish in the pharmaceutical industry, as shown by the fact that big pharma increasingly feeds its pipeline with innovation from very small companies (often with a single relevant product in the pipeline), and less from in-house discoveries [30,32,33]. These small companies can be viewed as a source of innovation intended to nourish the portfolios of other companies with well-established capabilities in manufacturing and commercialization [32]. We also acknowledge that these smaller companies experience a different lifecycle of innovation and financial dynamics because they do not intend to generate revenues from the commercialization of their compounds. Hence, this manuscript focuses on pharmaceutical companies of any size able to commercialise innovative products regardless of their R&D origin.

Return on investment from the company perspective

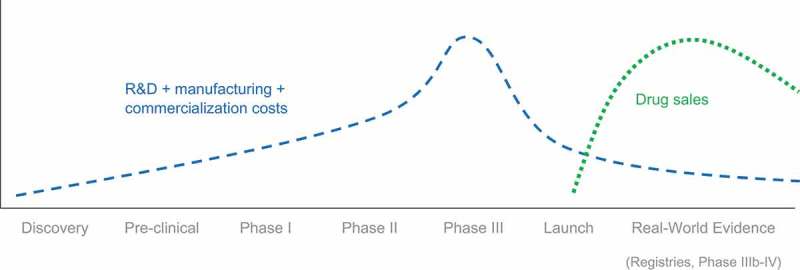

Due to the arduous path from drug discovery to commercialization, only a handful of pipeline compounds become ultimately available to patients (following approval of marketing authorization and price negotiation with payers) [34]. Pharmaceutical companies have long relied on few ‘successful’ products to generate enough revenues to boost the underlying firm’s profitability and sustain its long-term growth [35,36]. For innovation-driven companies, the long-term growth is expected to come from the return on investment (RoI) in pharmaceutical innovation. This RoI is predicted by subtracting all the capital being invested on R&D, manufacturing and commercialization from the future revenues to be generated from the products’ sales. Figure 2 depicts the basic dynamics of spend and revenues for an archetypal pharmaceutical product going through all three clinical development phases until its approval by a regulatory agency. As soon as the regulatory agency grants the marketing authorization, P&R negotiations take place between the manufacturer and the local payer.

Figure 2.

Costs and revenues over the lifecycle of a drug.

In order to pursue a R&D project, the compound must show consistent clinical benefit in every development phase and be commercially viable. The decision to keep funding the development of a compound is revisited at the end of each development phase, with the projected profitability having a heavier weight on the decision in latter phases. From the financial standpoint, the RoI must be positive and expected to achieve a minimum pre-specified size using the valuation method of choice. The net present value (NPV) calculation underlying this estimate is adjusted to account for the multiple risks associated to R&D activities [37,38], such as high cost of failure along the product’s clinical development process, and risks associated to manufacturing and commercialization (e.g., arrival of new competitors). The consideration of such risks tends to diminish the NPV and thus the expected RoI for the specific R&D project. This is clearly manifested at the time of allocating the company’s R&D budget because all R&D projects are competing for a portion of this same limited budget. It is not surprising therefore that many deliberations tend to center on the identification and quantification of specific opportunities (upsides) and risks (downsides) impacting future sales; and in the case of downsides, diminishing the NPV to the point where the R&D project is no longer competitive or commercially viable.

Return on investment from the perspective of private investors

Pharmaceutical companies compete for investors by offering the greatest returns possible (in the form of dividends and gains in share price) [16]. With this objective in mind, companies release profitability metrics regularly like the Return On Invested Capital (ROIC), which indicates how efficient a company is at generating returns (given the available resources/capital). Prospective shareholders scrutinise the portfolios and pipelines of multiple firms, to then purchase shares from the firm/s that maximise the RoI on their capital, given their appetite for risk [39]. The assessment of risk, and hence the cost of capital, can vary widely across different R&D projects and portfolios, and therefore, also across pharmaceutical companies and industries [39].

In view of the risk and high cost of failure along the entire process leading to pharmaceutical innovation (i.e., discovery, development, manufacturing and commercialization) [41], the pharmaceutical industry is compelled to offer a RoI (for any given level of risk) that compensates investors for the competitive disadvantage against other industries with no R&D component and more stable market conditions. Without a competitive RoI, prospective shareholders would prioritise other more lucrative industries, drying out the inflow of capital needed to fund R&D activities in detriment of future pharmaceutical innovations. Therefore, the sustainability of the pharmaceutical industry, and that of individual companies, depends on their ability to keep profitability levels attractive in the eyes of investors. Indeed, according to a time-series analysis of US data from 1930 to 2015 [32], and despite the considerable variability between individual companies, the average pharmaceutical RoI has generally outperformed the overall market. The more favourable RoI levels offered by the pharmaceutical industry can be attributed to the risks inherent to this industry, with special emphasis in those relating to drug development and commercialization [42].

Approaches to reduce uncertainty around the return on investment

Volatility in the RoI is generally higher in the pharmaceutical industry than for the overall market, with an upward trend, providing evidence that the risk sustained by this industry has been increasing over the years [32]. To retain shareholders and attract new ones, the pharmaceutical industry has to offset the increasing risk by offering a higher RoI. This can have undesirable implications for drug prices because the higher RoI can only be achieved by boosting profitability [43]. When the objective is to maximise short-term profitability prospects, companies might achieve this through two complementary channels: 1) lessening operating expenses [44], or 2) in cases where they have market power, deviating from VBP principles by raising prices of marketed products [45] or price outlooks of pipeline compounds.

Firms raise capital in diverse ways and for diverse purposes, not all of which will be directed at R&D or innovation [42]. In a context of expanding market capitalization, the tendency is to spend more capital on upscaling operations through different channels, such as reinforcing marketing/branding, extending manufacturing capacity, in-licensing/acquisitions of compounds under development elsewhere and funding R&D activities in-house. However, within a diverse pharmaceutical firm, to a large extent these projects compete for a given pool of capital. Our central point is that where there is great uncertainty about the profitability prospects for new innovation, firms may see greater benefit from being passive in R&D [46] and concentrate their effort and resources on maximizing profits from existing products, whether through unilateral price increases for drugs where patients have limited alternatives or boosting promotion of existing brands following the arrival of generics.

One way to reverse this pervasive pattern is by improving the predictability of the profitability of future innovation. In other words, the more confident that investors become on their future RoI, the less need for companies to maximise profits in ways that deviate from VBP principles. With this in mind, investors would welcome long-term predictability on the company’s ability to generate and commercialise innovation. That is, removing uncertainty around R&D efficiency and future sales will make the company more attractive for investors, which automatically translates into a stronger demand for shares. This buying pressure lifts the share price, expanding the firm’s market capitalization. Firms benefit from this by gaining more freedom on defining their capital structure to grow the company while minimizing its cost of capital [46].

Specifically in R&D, the average global spend by the top 20 pharmaceutical companies in 2017 was 21.5% of their total sales [47]. We anticipate that in a scenario with higher levels of RoI volatility, firms will lose competitiveness in the stock market. This will negatively impact their ability to meet the high capital requirements to fund R&D activities, resulting in a contraction of the investment made towards the generation of innovation. With the objective to improve long-term profitability and remain competitive in the stock market, the pharmaceutical industry is undergoing a transformation in the way it generates innovation, which will ultimately increase certainty on the company’s ability to generate innovation and strengthen the value proposition of the innovative products:

To increase R&D efficiency by means of lowering R&D costs without sacrificing the success rate. This can be achieved by moving into the digital era and the application of artificial intelligence. [48]

To place patients and healthcare systems at the center of the R&D decisions in order to generate more socially valuable innovations. This can be achieved by redefining success, and placing patient access to innovative treatments as the ultimate goal (with regulatory approval as an intermediate goal).

To ensure that the industry develops valuable innovations, it is fundamental to remove any ambiguity around the ‘value framework’ used by payers to appraise the value of pharmaceutical products and then set value-based prices [9] [49]. Clarification is important because value frameworks signal the type of innovation preferred (whether that be expressed as gain in quality-adjusted life years (QALY), or prioritizing specific areas of high unmet medical need such as vaccines [50], antibiotics [51], end of life treatments [52], etc.); and so, it encourages the generation of socially valuable innovations as opposed to just innovation per se [53,54].

Value frameworks offer some degree of certainty to the industry that innovations that generate added therapeutic value to patients will be able to gain a price premium over existing therapies. Hence clarification of pricing criteria is an important element of VBP. Moreover, payers and HTA agencies can also encourage appropriate innovation by providing clarity over other market or reimbursement conditions, such as estimates of disease burden; epidemiology of the disease; insurance coverage; and patient and healthcare provider belief in the value of the product. While VBP allows flexibility for local payers to set prices according to their chosen criteria, there is currently a proliferation of HTA and value frameworks across and, in some cases, within countries. Some degree of international coordination may be desirable, especially in areas of global health such as antibiotic resistance [51]. Indeed, HTA agencies are already working towards the harmonization of methods and the definition of value by forming regional and global networks and alliances (e.g., EUnetHTA [European network for HTA], HTA Asia Link, RedETSA [HTA Network of the Americas], HTA international, INAHTA [International Network of Agencies for HTA]).

Practices that increase uncertainty and deviate from VBP principles would include arbitrary periodic cuts eroding prices or capping profits, restrictions in the level of patient coverage and market penetration, as well as the length and depth of legal protection, which all have a direct impact on the firm’s revenues (via drug prices or sales volume). Naturally, there will always be factors influencing revenues outside the control of the firm, such as the entry of competitors or generics, which are a normal part of the commercial risk taken on by private companies. Payers and policy-makers would be justified in strengthening measures that promote rational prescribing, fair competition and a level playing field [55,56].

Setting optimal drug prices

The question of what constitutes an ‘optimal’ value-based price demands an understanding of the extent of surplus that society is willing to forgo in order to incentivise an appropriate degree of innovation. A few countries have operationalised a VBP system, and of these, the most common approach is to accept new drugs with a cost-per-QALY below a threshold (either implicit or explicit) [9]. A disadvantage of this approach is that is does not fully take into account the overall ‘budget impact’ of an intervention, that is, the additional costs that will be accrued by health services over the entire lifecycle of the drug. An alternative approach to determining the value of innovation was described by Moreno et al. [57]. Conveniently, this approach allows payers to conceive the new health technology as an investment and work out its present monetary value in a similar fashion as the NPV function does. The present value is estimated by summing up the discounted incremental costs and quality-adjusted life-years (QALYs) generated along the entire lifespan of the technology (in the same way that the NPV function sums up future cash inflows and outflows). QALY gains are converted into money to compute the total value in monetary terms. To do so, each QALY gained is priced in line with the local cost-effectiveness threshold (for example, each QALY is priced at £30,000), and so reflecting ‘good value for money’. Then, the total ‘monetary’ value is split between the manufacturer and the payer in line with society’s preferences. Society’s preferences can be elicited in terms of opportunity cost [58] to learn the value placed in health-related innovation (compared to saving or spending in other goods and services). Last, the drug price is derived to enable manufacturers collect the agreed sum of ‘money’ during the legal protection period.

The distinctive elements of the proposed pricing approach (compared to the conventional cost-effectiveness analysis) is the consideration of future (incidence) patients and the price drop following the loss of exclusivity. Accounting for the entire (prevalent and incident) patient population offers the advantage of internal consistency between the cost-effectiveness and budget impact analyses, and therefore is ideal for investigating affordability. Under the conventional approach, the price drop is materialised by switching all prescribing to generics/biosimilars (assuming that the market is competitive) [59]. The proposed approach allows negotiating the launch price together with the future off-patent price of the originator. We anticipate that manufactures will be open to negotiate marginal off-patent prices in exchange for a premium during the legal protection period. This will ensure uninterrupted access to the originator drugs at affordable prices. Moreover, the widespread adoption of this negotiation tactic promotes further innovation because there will be limited revenues to be generated from off-patent products, particularly as off-patent prices are negotiated downwards.

Discussion

This article contributes to the much-needed debate about the role of drug prices in incentivizing innovation [60]. To unveil the role played by drug prices in the complex dynamics leading to pharmaceutical innovation, a conceptual framework is put forward. From an investment perspective, the framework is intended to provide a conceptual structure describing the many inter-dependencies among key economic aspects (such a drug pricing) mediating in the lifecycle of innovation. The framework suggests that the long-term sustainability of pharmaceutical companies lies with profitability forecasts, which are partly driven by price expectations. Positive profitability forecasts attract investors, expanding the firm’s market capitalization and ultimately allowing companies meet the high capital requirements to fund R&D activities. The strong competition among companies for attracting investors largely explains why successful companies (either thanks to R&D efficiency or strong sales) have no incentive to pass on their profits in the form of lower drug prices. Instead, the incentive is for companies to direct profits towards activities enhancing their long-term profitability prospects with special emphasis on R&D activities [17].

We anticipate that volatility in the expected firm’s profitability will negatively impact its market capitalization, and hence limit its capacity to fund R&D activities in detriment of future innovations [61]. Long-term stability on price regulations will ultimately promote innovation (ceteris paribus). Greater certainty in the firm’s future profitability may partially reverse the industry’s need to persistently maximise drug prices as a means to outperform the profitability of other companies, leading to an escalation of drug prices [44]. In conclusion, this manuscript argues that predictable market conditions together with a more efficient R&D process are key for fostering innovation in the fight against cancer and other deadly and health-impairing diseases. Furthermore, it has the potential to minimise price escalations caused by the profitability race between companies.

Funding Statement

This publication is independent research of the authors. This paper was conceived and originally drafted by SM in discussion with DE. SM worked for Novartis Pharma AG at the time of writing and submitting the manuscript for publication, but received no funding to prepare this article that is attributable to the manuscript.

Disclaimer

The views expressed in this article are solely the authors’ and are not intended to reflect those of their professional affiliations.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- [1].Cockburn IM, Henderson RM, School MS, et al. Balancing incentives in pharmaceutical research; 2004. Available from: http://www.mit.edu/people/rhenders/WorkingPapers/CHS_Balance_01_04_V4.pdf

- [2].EFPIA EFPIA response to draft opinion on innovative payment models for high-cost innovative medicines; 2017a. Available from: https://www.efpia.eu/media/288630/final_efpia-response-to-exph-draft-opinion-7_12_2017_wir.pdf

- [3].EFPIA Healthier future the case for outcomes-based, sustainable healthcare; 2017b. Available from: https://www.efpia.eu/media/412313/the-case-for-outcomes-document-17102018.pdf

- [4].Hill S, Velazquez A, Tay-Teo K, et al. 2015 Global survey on health technology assessment by national authorities. Geneva; 2015. Available from: www.who.int

- [5].Wenzl M, Paris V.. Phamaceutical reimbursement and pricing in Germany; 2018. Available from: http://www.oecd.org/els/health-systems/Pharmaceutical-Reimbursement-and-Pricing-in-Germany.pdf

- [6].HAS Pricing and reimbursement of drugs and HTA policies in France. Online. 2014March Available from: http://www.has-sante.fr/portail/upload/docs/application/pdf/2014-03/pricing_reimbursement_of_drugs_and_hta_policies_in_france.pdf [Google Scholar]

- [7].Claxton K, Longo R, Longworth L, et al. The value of innovation. NICE decision support unit. National Institute for Health and Care Excellence (NICE); 2009. Available from: http://www.ncbi.nlm.nih.gov/pubmed/28481490 [PubMed] [Google Scholar]

- [8].TLV Pharmaceutical pricing and reimbursement policies Sweden; 2015. Available from: http://whocc.goeg.at/Publications/CountryReports

- [9].Angelis A, Lange A, Kanavos P. Using health technology assessment to assess the value of new medicines: results of a systematic review and expert consultation across eight European countries. Eur J Health Econ. 2017;19(1):123–9. [DOI] [PMC free article] [PubMed] [Google Scholar]

- [10].Value Frameworks: Hampson, G.Value in health special issue. Available from: https://www.ohe.org/news/value-frameworks-value-health-special-issue

- [11].EXPH Innovative payment models for high-cost innovative medicines. Paris: Expert Panel on Effective Ways of Investing in Health (EXPH); 2018. [Google Scholar]

- [12].Garrison LP, Towse A, Briggs A, et al. Performance-based risk-sharing arrangements—good practices for design, implementation, and evaluation: report of the ISPOR good practices for performance-based risk-sharing arrangements task force. Value Health. 2013;16(5):703–719. [DOI] [PubMed] [Google Scholar]

- [13].Vogler S, Paris V, Ferrario A, et al. How can pricing and reimbursement policies improve affordable access to medicines? Lessons learned from European countries. Appl Health Econ Health Policy. 2017;15(3):307–321. [DOI] [PubMed] [Google Scholar]

- [14].Garner S, Rintoul A, Hill SR. Value-based pricing: L’Enfant terrible? PharmacoEconomics. 2018;36(1):5–6. [DOI] [PMC free article] [PubMed] [Google Scholar]

- [15].WHO Pricing of cancer medicines and its impacts. Available from: https://apps.who.int/iris/bitstream/handle/10665/277190/9789241515115-eng.pdf?ua=1

- [16].US Congress Office of Technology Assessment Pharmaceutical R&D: costs, risks, and rewards. Washington (DC); 1993Available from: https://www.princeton.edu/~ota/disk1/1993/9336/9336.PDF [Google Scholar]

- [17].Scherer FM. The link between gross profitability and pharmaceutical R&D spending. Health Affairs. 2001;20(5):216–220. [DOI] [PubMed] [Google Scholar]

- [18].Kerr W, Nanda R. Financing innovation. MA; 2014. DOI: 10.3386/w20676 [DOI] [Google Scholar]

- [19].Brown JR, Fazzari SM, Petersen BC. Financing Innovation and Growth: Cash Flow, External Equity, and the 1990s. R&D Boom. Available from: https://onlinelibrary.wiley.com/doi/full/10.1111/j.1540-6261.2008.01431.x

- [20].INVESTOPEDIA How can I use market capitalization to evaluate a stock? Available from: https://www.investopedia.com/ask/answers/042415/how-can-i-use-market-capitalization-evaluate-stock.asp

- [21].Mishra M, Grover N. AbbVie to remain cautious on drug pricing, shares fall. Available from: https://www.reuters.com/article/us-abbvie-results/abbvie-to-remain-cautious-on-drug-pricing-shares-fall-idUSKBN1AD1G7

- [22].Zacks Equity Research Here's Why Lilly (LLY) Stock is Up 15% Since Q2 Earnings. Available from: https://www.zacks.com/stock/news/317659/heres-why-lilly-lly-stock-is-up-15-since-q2-earnings

- [23].Digital R&D Transforming the future of clinical development. Available from: https://www2.deloitte.com/insights/us/en/industry/life-sciences/digital-research-and-development-clinical-strategy.html

- [24].Times Financial. Make informed decisions with the ft. Available from: https://www.ft.com/content/8c2eab30-e5a4-11e7-97e2-916d4fbac0da

- [25].Rothenstein JM, Tomlinson G, Tannock IF, et al. Company stock prices before and after public announcements related to oncology drugs. JNCI. 2011;103(20):1507–1512. [DOI] [PubMed] [Google Scholar]

- [26].Mazzucato M.Innovation and stock prices: a review of some recent work. Milton Keynes; 2006. Available from: https://www.ofce.sciences-po.fr/pdf/revue/10-97bis.pdf.

- [27].Mazzucato M, Tancioni M. R&D, Patents and Stock Return Volatility. In: Pyka A., Andersen E. (eds) Long Term Economic Development. Economic Complexity and Evolution. Springer, Berlin, Heidelberg [Google Scholar]

- [28].Chun H, Kim J.-W Productivity Growth Morck R. and Stock returns: firm- and aggregate-level analyses. Available from: https://www.nber.org/papers/w19462

- [29].Ghent University Analysis of stock market reactions to fda and emea announcements. Available from: https://lib.ugent.be/fulltxt/RUG01/002/062/116/RUG01-002062116_2013_0001_AC.pdf

- [30].Nord LJ https://digitalcommons.iwu.edu/uer/vol8/iss1/6/ R&D Investment Link to Profitability: A Pharmaceutical Industry Evaluation. Available from:

- [31].Cohen L, Diether K Malloy C.. Misvaluing innovation. Rev Financ Stud. 2013;26(3):635–666. [Google Scholar]

- [32].Thakor RT, Anaya N, Zhang Y, et al. Just how good an investment is the biopharmaceutical sector? Nat Biotechnol. 2017;35(12):1149–1157. [DOI] [PubMed] [Google Scholar]

- [33].Madsen ES, Wu Y. Low R&D efficiency in large pharmaceutical companies. Available from: https://pure.au.dk/ws/files/103275100/7_MadsenWu.pdf

- [34].DiMasi JA, Grabowski HG, Hansen RW. Innovation in the pharmaceutical industry: new estimates of R&D costs. Available from: https://www.sciencedirect.com/science/article/abs/pii/S0167629616000291 [DOI] [PubMed]

- [35].Grabowski H, Vernon J. A new look at the returns and risks to pharmaceutical R&D. Manage Sci. 1990;36:804–821. [Google Scholar]

- [36].Schuhmacher A, Gassmann O, Hinder M. Changing R&D models in research-based pharmaceutical companies. Available from: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4847363/ [DOI] [PMC free article] [PubMed]

- [37].Deloitte Measuring the return from pharmaceutical innovation; 2017. Available from: https://www2.deloitte.com/us/en/pages/life-sciences-and-health-care/articles/measuring-return-from-pharmaceutical-innovation.html#

- [38].Svennebring AM, Wikberg JE. Net present value approaches for drug discovery. SpringerPlus. 2013;2(1):140. [DOI] [PMC free article] [PubMed] [Google Scholar]

- [39].EvaluatePharma®. World Preview 2018, Outlook to 2024. Available from: http://info.evaluategroup.com/rs/607-YGS-364/images/WP2018.pdf

- [40].Sussex J, Marchant N. Risk and return in the pharmaceutical industry. OHE; 1996Available from: https://www.ohe.org/publications/risk-and-return-pharmaceutical-industry [Google Scholar]

- [41].DiMasi JA, Grabowski HG, Hansen RW. Innovation in the pharmaceutical industry: new estimates of R&D costs. Available from: https://www.sciencedirect.com/science/article/abs/pii/S0167629616000291 [DOI] [PubMed]

- [42].Scherer FM. Pharmaceutical innovation In: Handbook of the economics of innovation. Vol. 1 North-Holland; 2010. p. 539–574. DOI: 10.1016/S0169-7218(10)01012-9 [DOI] [Google Scholar]

- [43].Tay-Teo K, Ilbawi A Hill SR.. Comparison of sales income and research and development costs for fda-approved cancer drugs sold by originator drug companies. Available from: https://jamanetwork.com/journals/jamanetworkopen/fullarticle/2720075 [DOI] [PMC free article] [PubMed]

- [44].Miller J. Novartis to cut 2,550 jobs in Switzerland UK in profit push. Available from: https://uk.reuters.com/article/us-novartis-workers/novartis-to-cut-2550-jobs-in-switzerland-uk-in-profit-push-idUKKCN1M50HD

- [45].Gordon N, Stemmer SM, Greenberg D, et al. Trajectories of injectable cancer drug costs after launch in the USA. J Clin Oncol. 2018;36(4):319–325. [DOI] [PubMed] [Google Scholar]

- [46].Lee M, Choi M.. The determinants of research and development investment in the pharmaceutical industry: focus on financial structures. Available from: https://www.sciencedirect.com/science/article/pii/S2210909915300187 [DOI] [PMC free article] [PubMed]

- [47].EvaluatePharma World preview 2018, outlook to 2024; 2018. Available from: www.evaluate.com/PharmaWorldPreview2018

- [48].Digital R&D.Transforming the future of clinical development. Available from: https://www2.deloitte.com/insights/us/en/industry/life-sciences/digital-research-and-development-clinical-strategy.html

- [49]. Hampson G. Value frameworks: value in health special issue. Available from: https://www.ohe.org/news/value-frameworks-value-health-special-issue

- [50].US Department of Health and Human Services Encouraging vaccine innovation: promoting the development of vaccines that minimize the burden of infectious diseases in the 21 st century report to congress; 2017. Available from: https://www.gpo.gov/fdsys/pkg/PLAW-114publ255/pdf/PLAW-114publ255.pdf

- [51].Simpkin VL, Renwick MJ, Kelly R, et al. Incentivising innovation in antibiotic drug discovery and development: progress, challenges and next steps. J Antibiot (Tokyo). 2017;70(12):1087–1096. [DOI] [PMC free article] [PubMed] [Google Scholar]

- [52].Collins M, Latimer N. NICE’ s end of life criteria: who gains, who loses? BMJ. 2013;346 Available from: https://www.bmj.com/bmj/section-pdf/187873?path=/bmj/346/7905/Analysis.full.pdf [DOI] [PubMed] [Google Scholar]

- [53].Light D, Lexchin J. Pharmaceutical R&D: what do we get for all that money? BMJ. 2012;345:e4348-e4348. [DOI] [PubMed] [Google Scholar]

- [54].Slomiany M, Madhavan P, Kuehn M, Richardson S., Value frameworks in oncology: comparative analysis and implications to the pharmaceutical industry. Am Health Drug Benefits. 2017July;10(5):253–260. [PMC free article] [PubMed] [Google Scholar]

- [55].United Nations Seventh united nations conference to review all aspects of the set of multilaterally agreed equitable principles and rules for the control of restrictive business practices; 2015. Available from: http://unctad.org/meetings/en/SessionalDocuments/tdrbpconf8d3_en.pdf

- [56].Morton FS, Boller LT. Enabling competition in pharmaceutical markets Hutchins center working paper #30; 2017. Available from: https://www.brookings.edu/wp-content/uploads/2017/05/wp30_scottmorton_competitioninpharma1.pdf

- [57].Moreno SG, Ray JA. The value of innovation under value-based pricing. J Mark Access Health Policy. 2016;4(1):30754. [DOI] [PMC free article] [PubMed] [Google Scholar]

- [58].Fritzell G, Strand L. The opportunity cost neglect of money and time – the role of mental budgeting. Available from: http://www.diva-portal.org/smash/get/diva2:1219163/FULLTEXT01.pdf

- [59].Cole AL, Dusetzina SB. Generic price competition for specialty drugs: too little, too late? Health Affairs. 2018;37(5):738–742. [DOI] [PubMed] [Google Scholar]

- [60].Cutler DM, McClellan. M. Is technological change in medicine worth it? Health Affairs. 2001;20(5):11–29. [DOI] [PubMed] [Google Scholar]

- [61].Warusawitharana M. Research and development, profits, and firm value: a structural estimation. Quant Econ. 2015;6:531–565. [Google Scholar]