Abstract

Purpose

To assess the financial outcomes and associated social and economic effects on cancer survivors and their families. Methods We assessed the responses of 1656 cancer survivors to a survey with both closed- and open-ended questions about cancer-related financial sacrifices they and their family experienced and evaluated differences in financial sacrifice by reported levels of cancer-related debt.

Results

The most commonly reported financial sacrifices included cutbacks on household budgets, challenges with health care insurance and costs, career/self-advancement constraints, reduction/depletion of assets, and inability to pay bills. Survivors who incurred $10,000 or more in debt were significantly more likely to report social and economic impacts, including housing concerns and strained relationships.

Conclusions

Our analysis demonstrates both the frequency with which cancer survivors and families must make financial sacrifices as a result of their cancer, and the variety of forms that this sacrifice can take, even for individuals who have health insurance. The many types of financial hardship create challenges that are unique to each survivor and family.

Implications for Cancer Survivors

Interventions that allow for personalized assistance with the specific financial and social needs of cancer survivors and their families have the potential to address a critical aspect of the long-term wellbeing of this important population.

Keywords: Financial hardship, Medical debt, Access to care, Cancer survivors, Social and economic needs

Introduction

In 2016, over 15.5 million individuals with a history of cancer were alive in the United States (U.S.), and this population is projected to surpass 20 million by 2026 [1]. As the costs of cancer therapies have increased over time, [2–5] so too has patient cost-sharing (e.g., deductibles, copayments, coinsurance) [6, 7]. Together, these factors can pose a large burden on the finances of individuals diagnosed with cancer and their families. Estimates from U.S. studies indicate that between 9 and 53% of cancer survivors experience material financial hardship (e.g., inability to cover their share of medical care costs, incurring debt, filing for bankruptcy) and many cancer survivors continue to suffer financial consequences of the disease for years following treatment [8–15]. Yet, financial hardship from cancer is not entirely a U.S. phenomenon. Findings from the limited international studies report material financial hardship ranging from approximately 20–49%, as well as high out-of-pocket costs among patients with cancer [16–23]. Younger patients and survivors may face unique challenges associated with their age, as they are less likely to have accumulated wealth, less likely to be insured, more likely to have children at home, and more likely to encounter employment interruptions and work productivity loss that could negatively impact income and health insurance coverage [16, 22, 24–29]. Prior research has demonstrated that financial hardship can lead to worse physical and mental health and wellbeing, and can have negative effects on family relationships and parenting outcomes [30–34].

Given the extent to which financial hardship may uniquely affect younger cancer patients and survivors, providing additional support to mitigate negative financial consequences among cancer patients and survivors could have lasting consequences [35, 36]. In order to determine how best to provide this support, a broad understanding is needed of the ways that financial hardship is experienced by this population of cancer survivors, and how their day-to-day lives are affected [37]. The primary goal of this study was to elucidate the specific financial sacrifices made in the lives of cancer survivors less than 65 years of age in their own words. To understand how severity of financial hardship was related to survivor experiences, reported financial sacrifices were compared between those with high and low levels of medical debt.

Methods

Study population

We examined data from adults ages 18–64 years who participated in the 2012 LIVESTRONG Survey for People Affected by Cancer [38]. This online survey was designed to assess the experiences and needs of individuals diagnosed with cancer, both during and after their cancer treatment, including the different kinds of financial burden cancer survivors or their family may have experienced because of cancer, its treatment, or the lasting effects of that treatment. Survey participants were recruited through outreach efforts of the LIVESTRONG Foundation constituency (e.g., donors, participants at events or programs, advocates, and community members), social media, and partnering national and community-based organizations. Of the 4484 survey participants aged 18–64 years, approximately 37% (n = 1656) responded to the open-ended survey item about financial sacrifices and were included in the study. We excluded participants who did not respond to the open-ended item about financial sacrifices (Supplemental Table).

Measures

The questions used to assess financial hardship on the LIVESTRONG survey were the same questions used by the 2011 Medical Expenditure Panel Survey (MEPS) Experiences with Cancer Supplement [39]. More details about the MEPS survey design, cognitive testing of questions contained in the Cancer Supplement, and content are available elsewhere [39, 40].

The present study focuses on answers to a series of questions about the financial hardships participants experienced as a consequence of their cancer, its treatment, or the lasting effects of that treatment. This included five questions asking about borrowing money or going into debt, amount of debt incurred, filing for bankruptcy, inability to cover their share of medical care costs, and spending down assets. Following this series of questions, participants were asked to report on their financial hardship experiences in their own words by responding to the open-ended question: Have you or your family had to make any other kinds of financial sacrifices because of your cancer, its treatment, or the lasting effects of that treatment?

We also assessed sociodemographic characteristics of participants, measured at the time of the survey, including age (18–39, 40–54, 55–64 years), sex (female, male), race/ethnicity (non-Hispanic white, non-white, unknown/missing), marital status (married/domestic partner, single/separated/divorced/widowed, unknown/missing), insurance status (private, government, uninsured, other, unknown/missing), and annual household income ($0–$40,000, $41,000–$80,000, $81,000–$120,000, > $120,000, unknown/missing).

Data analysis

Descriptive statistics

Descriptive statistics including frequencies and percentages were calculated for all measures included in the analysis, including sociodemographic and financial hardship characteristics.

Content analysis process

Responses to the open-ended financial sacrifices question were coded by study staff trained (JLS, AJF) and experienced in qualitative content analysis [41–43]. A codebook was developed based on multiple reviews of the open-ended responses. The codebook consisted of a list of overarching domains, each containing sub-codes to differentiate among specific sacrifices within individual domains. For example, the domain “career and self-advancement impact” had eight sub-codes, including “reduced earnings” and “altered career trajectory”. The codebook was shared with the study team and feedback was incorporated. The resulting list of 18 overarching domains, each with between three and eight sub-codes, was then used for formal coding of the open-ended responses. The full codebook is available upon request.

Formal coding consisted of each coder independently categorizing responses into domains and sub-codes using codebook criteria. Coding responsibility for each response was randomly assigned to one of the two coders. Approximately 10% of responses were randomly selected for review by both coders to compare application and interpretation of codes. Coders met weekly to review their coding, discuss questions, refine the codebook as needed, and re-code responses as necessary. Responses often applied to more than one domain or sub-code. To retain the descriptive richness of participant comments, responses were given codes for as many domains and sub-codes as applicable. Because data were collected from open-ended survey responses and not from face-to-face interviews, clarifying the true meaning of very brief or difficult-to-interpret responses was not possible. Responses that were uninterpretable were labeled as “unable to code” rather than as missing data. Once all responses were coded and reviewed, the individual coding sheets were merged into a single data set for interpretation.

Interpretation of data

To explore the range and types of financial sacrifices participants described, we first explored the frequency of each overarching domain mentioned by participants (referred to as an instance). An overarching domain (i.e., reduction/depletion of assets) could have more than one instance coded for each participant response when reflecting specific sub-codes within that domain (i.e., “sold major asset like house or car” or “depleted savings account”). Second, for each of the nine overarching domains that were represented in over 100 instances, we report in-depth descriptions of the sub-codes within the domain and the frequencies with which they occurred.

Experience of financial sacrifice by medical debt level

Chi square tests for independence were used to examine potential associations between participants’ reported level of treatment-related debt incurred (< $10,000 vs. ≥ $10,000) and each of the nine most common domains of financial sacrifice for the 1656 participants who answered both the open-ended and level-of-debt questions. All statistical tests were conducted with a two-sided alpha of 0.05. Analyses were conducted using a Stata 13.1 (StataCorp LLC, College Station, TX).

Results

Descriptive statistics

Table 1 shows the sociodemographic and financial hardship characteristics of the 1656 cancer survivors included in this study who responded to the open-ended item about making other financial sacrifices. The majority of participants were female (71%), non-Hispanic white (87%), between the ages of 40–54 years (50%), and married (68%). Approximately 82% of participants had private insurance and approximately 53% reported an annual household income of less than $80,000. Those participants who were included in our analysis were more likely to be female, non-White, non-married, uninsured, have low income, and have experienced financial hardship from cancer compared to the larger population of survey respondents aged 18–64 (Supplemental Table).

Table 1.

Descriptive characteristics of respondents

| Characteristic | Total (n = 1656) n | % | |

|---|---|---|---|

| Sociodemographic | |||

| Age (years) | |||

| 18–39 | 293 | 17.7 | |

| 40–54 | 833 | 50.3 | |

| 55–64 | 518 | 31.3 | |

| Sex | |||

| Female | 1176 | 71.0 | |

| Male | 472 | 28.5 | |

| Race/ethnicitya | |||

| White, Non-Hispanic | 1444 | 87.2 | |

| Other | 205 | 12.4 | |

| Marital status | |||

| Married/domestic partner | 1125 | 67.9 | |

| Single, separated, divorced, widowed | 513 | 31.0 | |

| Insurance type | |||

| None | 71 | 4.3 | |

| Private or employer | 1361 | 82.2 | |

| Government or military | 149 | 9.0 | |

| Other | 62 | 3.7 | |

| Annual household income, dollarsb | |||

| $0–$40,000 | 403 | 24.3 | |

| $41,000–$80,000 | 473 | 28.6 | |

| $81,000–$120,000 | 338 | 20.4 | |

| > $120,000 | 239 | 14.4 | |

| Financial hardship | |||

| Ever borrow money or go into debt | |||

| Yes | 928 | 56.0 | |

| No | 721 | 43.5 | |

| Amount borrowed or debt incurredc | |||

| < $10,000 | 3641085 | 4065.5 | |

| ≥ $10,000 | 551 | 33.3 | |

| Ever file bankruptcy | |||

| Yes | 87 | 5.3 | |

| No | 1550 | 93.6 | |

| Ever unable to cover share of medical care costs | |||

| Yes | 712 | 43.0 | |

| No | 940 | 56.8 | |

| Ever spent down assets to qualify for Medicaid/other cancer-related program | |||

| Yes | 153 | 9.2 | |

| No | 1489 | 89.9 | |

| Ever worried about paying large medical bills related to cancer | |||

| Yes | 1400 | 84.5 | |

| No | 253 | 15.3 | |

Frequencies and percentages are based on respondents with non-missing values and, thus, category frequencies and percentages may not add to 100%

Other includes non-Hispanic Black, Hispanic, non-Hispanic American Indian/Alaskan Native, non-Hispanic Asian/Pacific Islander, other non-Hispanic

Income categories are based on the original categories as presented in the 2012 LIVESTRONG Survey.

Respondents who reported “No” to the item “Ever borrow money or go into debt” were classified as having “Amount borrowed or debt incurred” equal to $0 and included in the “< $10,000” group

Among this sample of cancer survivors who reported making other financial sacrifices, over half (56%) of participants reported borrowing money or going into debt as a result of their cancer, with 33% borrowing or incurring debt of $10,000 or more. More than 5% of participants filed for bankruptcy because of cancer, its treatment, or the lasting effects of treatment, and 43% reported inability to cover their share of cancer care costs. Over 9% spent down assets to qualify for Medicaid or another cancer-related program. Most (85%) participants worried about paying large cancer-related medical bills.

Financial sacrifices

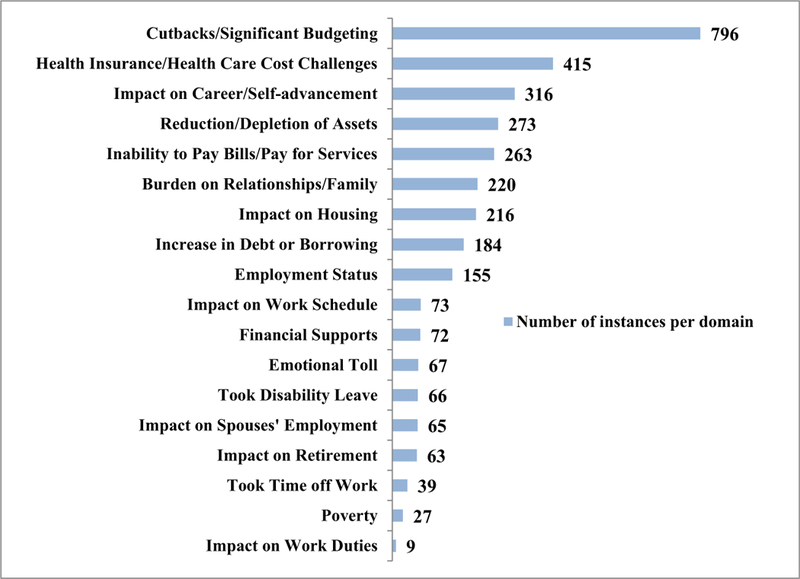

Figure 1 shows the 18 financial sacrifice domains coded from the data, and the number of times each financial sacrifice was mentioned (i.e., instances) in participant responses. Among these 18 domains, nine financial sacrifices were mentioned in at least 100 instances: Cutbacks/Significant Budgeting (n = 796), Health Insurance/Health Care Cost Challenges (n = 415), Impact on Career/Self-advancement (n = 316), Reduction/Depletion of Assets (n = 273), Inability to Pay for Bills/Pay for Services (n = 263), Burden of Family/Relationships (n = 220), Impact on Housing (n = 216), Increase in Debt or Borrowing (n = 184), and Employment Status (n = 155).

Fig. 1.

Frequency of qualitative domains for financial sacrifice open-ended responses (n = 1656). Notes: Information presented includes the 18 financial sacrifice domains coded from the open-ended qualitative data of the 1656 respondents, and the number of times each financial sacrifice was mentioned (e.g., instances) in participant responses. A domain (i.e., reduction/depletion of assets) could have more than one instance coded for each participant when reflecting specific sub-codes within that domain (i.e., “sold major asset like house or car” or “depleted savings account”)

Below, we present a summary of the nine most common financial sacrifice domains, including the number of total instances for each domain and related sub-codes. Illustrative quotes from each of these domains as well as for examples of multiple financial sacrifices are provided in Table 2.

Table 2.

Illustrative quotes representing experiences within the top 9 financial sacrifice domains and those with multiple financial sacrifices

| Cutbacks/significant budgeting (796 instances) |

| Cut back on many normal expenses - did not spend money for entertainment or going out to eat, saved money any way I could. |

| Total reduction in expenditures...no cable TV, internet, vacations, going out to dinner, fast foods, and anything else we could think of to save money. |

| Extreme cuts to household budget. And I mean everything! |

| Much tighter budget, buy necessities only. |

| Live paycheck to paycheck now, no emergency fund. |

| Health insurance/health care cost challenges (415 instances) |

| The insurance still does not cover my scans 100%. So once a year, I go get my scans done & we just have to watch what we spend that month, so we can pay off the remaining balance of that bill. |

| Pay exorbitant rates for insurance in the high-risk pool because I cannot get regular insurance. My medical bills including insurance are more than my income now. |

| Co-insurance and out of pocket expenses were a hit to the family budget, so we had to cut back on spending to cover these expenses. |

| My health insurance is very expensive and does not pay for office visits. I have to see my oncologist every 4 months for the next 5 years. |

| My insurance provider rescinded my coverage. I paid most of my costs out of pocket. My savings were wiped out. I was comfortable, now I struggle and am ashamed and isolated by my lack of funds. I do not know that I will ever recover financially. It is a considerable stress; I am currently without insurance… |

| Impact on career/self-advancement (316 instances) |

| I transferred out of a very lucrative position to less paying position. |

| As I did not take advancement or increase my hours, my salary is less than it might have become. |

| I stayed with a company that provides excellent health benefits rather than seek higher paying jobs where health insurance might not be as good. |

| I changed jobs because I was declared physically unfit for my job. So I went from a great career line of work that I went to school for, to a part time retail job. |

| I was pressured to resign from my job and have not been able to secure another since my cancer diagnosis. |

| Reduction/depletion of assets (273 instances) |

| We used up all of our savings and had to dip into retirement funds to pay co-insurance, deductible, copays, etc. |

| My husband and I, as well as our parents have all had to dig into our savings accounts to cover the insurance copays for my treatment. We have currently totaled approximately $12,000 over the last 2 years. |

| Oh my ... have spent thousands and thousands and thousands from retirement accounts and have done without. |

| I had to cash out my 401 K to pay off the medical bills |

| Sold most of our valuables - jewelry, motorcycles, and the like. |

| Inability to pay bills/pay for services (263 instances) |

| [I] choose which bills to let lapse to pay hospital co-pay. |

| Bills went into collection because I could not afford all the copays. |

| Can no longer afford dance lessons for my daughter, and cannot afford |

| preschool for my son. Cannot pay bills. |

| Could barely afford the basics during this time. I was lucky to eat and keep a roof over my head. |

| [I was] not able to buy groceries or pay some of my medical bills. |

| Burden on relationships/family (220 instances) |

| [I] got a divorce because of my being sick. |

| My husband became depressed due to my withdrawal from intimacy after my cancer. He stopped working. |

| My thirty-year-old daughter and my 24-year-old daughter have stayed with me to help pay rent and expenses instead of the oldest marrying her boyfriend and moving out, or the younger getting a place of her own. They should have lives of their own, but they are “stuck” taking care of me. |

| My family could not do or have as much because of the medical bills. |

| My daughter had to come home from college. |

| Impact on housing (216 instances) |

| We had to let our home go back to the bank…After 20 years of home ownership, we had to file bankruptcy and now rent. |

| I had to sell my house at a loss to have money to survive. |

| Unable to refinance our home due to medical debt and cannot afford current mortgage due to all of the medical debt. |

| Home maintenance and repairs were neglected. |

| We had to let our home go and move in with my son and his wife, so I can continue treatment. |

| Increase in debt or borrowing (184 instances) |

| I put my cancer expenses on credit cards and eventually could no longer make payments on them - settled some [credit cards] for less and got sued by one card company. |

| I am still paying for debts accrued from co-payments or hospital bills not covered by my insurance…and paying credit card debt that was accrued during my time out of work. |

| I delayed paying my student loans and ran up my credit cards. |

| [I] ran up credit card debt and borrowed money from family members. |

| I delayed paying my student loans and ran up my credit cards. |

| Employment status (155 instances) |

| I have not been able to return to work. I was between jobs, about to start a new one, when diagnosed. Now I experience chronic issues which preclude meaningful employment. |

| I lost the ability to do my job because it is brain cancer - I cannot drive and because of my treatment I have tremors…I was a hair stylist and I can no longer do my job. |

| I cannot work but I try to. I want to die I have so much pain. |

| I lost my job and believe that it could have been partially due to long term aftereffects of cancer treatment. |

| I sold my business and was unemployed for several years while I regained my health. |

| Multiple financial sacrifices |

| We have cut back having almost no vacations in the past 10 years, no entertainment except dollar rental on movies. The house is in disrepair and cannot fix to sell. [We] shop only for needs and look for best deal with less snacks and “fun food” in house for kids, less food in house, [and] cannot help daughter with college. [We] have very little discretionary income and most of that goes to gas to be able to drive to work; defaulting on school loans; pets do not go to vet except when emergency; and [we] shop at thrift stores for clothes and bread… |

| We had to sell our home after three years (had bone cancer), and child left college had to take out student loan. [We] sold nice car bought old one, had to lose my life insurance, could not afford dental care the lack of income combined with the large co-pays, deductibles, limits of my very expensive insurance destroyed financial stability and there was no way to rebuild once my health was okay. [I] lost time and a huge resume gap with no explanation that would be positive for an employer. Although I have a master’s degree, I used money for classes to get re-employed. |

| [I] owned my business, and lost everything due to [pancreatic cancer] no insurance at the time of cancer. [I] sold all life policies, gold, and anything of value trying to stay ahead of bills did not make it. Now [I am] losing my home as well, in foreclosure, and cannot work full time as I do not have stamina or endurance. I have no help. I was the one everyone counted on and now I feel I’ve let all down…nowhere to turn. |

Information presented includes select qualitative responses for the top 9 financial sacrifice domains from the open-ended qualitative data of the 1656 respondents to the 2012 LIVESTRONG survey, as well as select qualitative responses from respondents who reported experiencing multiple financial sacrifice domains

Cutbacks/significant budgeting (796 instances, 48% of total participants)

The most commonly mentioned aspect of financial sacrifice involved a combination of cutting back on spending and changing priorities about where participants spent their money. Some responses were general in nature (n = 341 instances) such as brief descriptions of making “cutbacks”; however, the majority of participants provided more detailed descriptions of budgeting and reductions in spending. Participants expressed “living off a very tight budget” (n = 196 instances), describing living paycheck-to-paycheck on budgets that mostly focused on daily essentials (e.g., food, gas, and home costs) and, when possible, health care expenses. Others noted decreasing or no longer taking vacations (n = 259 instances), with many participants reporting lack of funds for leisure or entertainment of any kind.

Health insurance/health care cost challenges (415 instances, 25% of total participants)

Many participants identified specific challenges they faced regarding health insurance coverage of their cancer care and related health care costs. Nearly half (n = 197 instances) of the responses in this category identified costly out-of-pocket expenses related to their health insurance, including co-payments, co-insurance, and deductibles for cancer-related treatments and medications as a hardship that led to financial sacrifice. Participants also described cost challenges due to treatments, care, or medications that were not covered by their health plan (n = 93 instances), as well as experiencing higher insurance premiums (n = 54 instances) or loss of health insurance (n = 25 instances) after their cancer diagnosis. Less frequent responses included no longer being able to afford medication or treatment for other (non-cancer) medical conditions (n = 18), using costly COBRA insurance from their employer (n = 14 instances), and health insurance benefits as a larger consideration in job choice than position or income (n = 14 instances).

Impact on career/self-advancement (316 instances, 19% of total participants)

Responses in this category described effects of cancer symptoms, treatment, or medical costs on participants’ careers and self-advancement. Participants described receiving a lower salary or making less money following their cancer treatment (n = 187 instances) or an alteration or stagnation in the trajectory of their career that was inconsistent with their career goals prior to cancer diagnosis (n = 129 instances). Participants described promotions that were jeopardized, inability to proceed with their careers due to cancer (e.g., postponing higher degree plans or becoming unable to travel for work), changing careers or positions to facilitate coping with treatments, or to obtain or maintain better health care benefits. Some participants experienced employment discrimination after being diagnosed with cancer.

Reduction/depletion of assets (273 instances, 16% of total participants)

Participants described a variety of ways in which they experienced a reduction or overall depletion of their assets. Over one-third of these participants (n = 104 instances) reported accessing their savings accounts, with some spending most or all their savings on cancer care and/or daily living expenses. Others described cashing out or depleting retirement accounts (n = 79 instances). Participants also mentioned selling both major and minor assets including their home or car (n = 46 instances) or other valuables such as jewelry or home goods (n = 26 instances). Less frequent were descriptions of participants cashing out or depleting other assets such as stocks or life insurance policies (n = 12 instances) or reports of extended family members selling major assets to help pay for cancer care and other life expenses (n = 6 instances).

Inability to pay bills/pay for services (263 instances, 16% of total participants)

Some participants reported that the high costs of their cancer care left them unable to pay for other expenses. Most such participants had unpaid bills, primarily for credit cards and non-cancer-related health care such as dental services (n = 133 instances). Others (n = 67 instances) reported inability to pay for their children’s expenses (e.g., child care, school fees). In some instances, participants articulated more extreme financial hardships, such as difficulty paying for daily living costs like food or utility bills (n = 45 instances) or having to file bankruptcy (n = 18 instances).

Burden on relationships/family (220 instances, 13% of total participants)

Participants described a variety of ways that their family and social relationships were affected by their cancer-related financial hardships. Some participants reported that this financial strain led to separation or divorce from their partner (n = 47 instances). Participants reported having extended family members cover expenses such as mortgages (n = 52 instances) and changing children’s college plans (e.g., postponed or delayed college, taking out loans for school or to pay for their own college, deciding to attend a less expensive college) (n = 45 instances). Additionally, increased financial stress or strain on the family unit resulting from the need to tighten budgets created an inability to afford family activities (n = 40 instances) was disclosed. Some participants described moving in with family members or family members living with them to help reduce expenses (n = 30 instances). A few participants said they delayed or decided against starting a family due to the costs associated with infertility treatments or adoption (e.g., due to cancer side effects) or the costs of raising children (n = 6 instances).

Impact on housing (216 instances, 13% of total participants)

The most commonly articulated financial sacrifice pertaining to housing was selling one’s home and/or downsizing to a smaller/more affordable home (n = 105 instances). This included moving from a house to an apartment, moving in with others, being forced to sell a home, or losing a home to foreclosure. Other common challenges related to housing included difficulties paying rent or mortgage (n = 35 instances), not being able to afford planned or needed home repairs (n = 33 instances), inability to buy or sell a home as planned (n = 18 instances), refinancing of home mortgages (n = 12 instances), and general concerns about home stability (n = 13 instances).

Increase in debt or borrowing (184 instances, 11% of total participants)

Many of the responses in this category were general comments about increased borrowing or debt (n = 60 instances). Participants described experiencing increases in credit card use and related debt (n = 47) and borrowing money from family or friends (n = 44 instances). Some participants reported taking out loans (n = 20 instances), such as bank or student loans. Others described borrowing money from their child’s college savings plan or account (n = 13 instances).

Employment status (155 instances, 9% of total participants)

The most commonly reported employment sacrifice was discontinuation of work (n = 91 instances). Participants described never being able to return to work because of their cancer or related treatments. Some participants lost jobs due to their cancer treatments or related side effects (n = 34 instances), including statements of being laid off or fired after cancer treatment. Additionally, participants described struggling to find a job due to their cancer treatment schedule or effects of treatment (n = 22 instances), and some reported selling or closing their own business (n = 8 instances).

Other domains reflected various impacts on the work lives of participants and spouses. Participants noted that they had to change their work schedule to accommodate treatment or symptoms (n = 73 instances), taking disability leave (n = 66 instances), changing their retirement plans as a result of their illness and/or its costs (n = 63 instances), taking non-disability time off work (n = 39 instances), and other impacts on their work duties (n = 9 instances). Additionally, participants mentioned the impact of their cancer on their spouse’s employment (n = 65 instances).

Support (72 instances, 4% of total participants)

Some participants used this open-ended question to highlight support that they experienced which they perceived to have eased their financial hardship. Participants most often reported support from family and friends with paying bills or financing other medical treatments not covered by health insurance (e.g., infertility — egg harvesting), as well as fundraising efforts to help cover the patient’s living and medical expenses. Participants also described the benefits of payment plans to manage existing medical debt, and access to financial support through charity organizations, including reduced or free medications (e.g., provided by pharmaceutical companies), or having their debts forgiven. Participants noted the high emotional toll of financial hardship (n = 67 instances), as well as mentioning that the costs of cancer had left them in poverty (n = 27 instances).

Toll of multiple financial sacrifices

The majority of participants who answered the open-ended question (61%) described more than one overarching domain of financial sacrifice (Table 2). Many participants described multiple financial sacrifices that built upon each other, forming complex and interrelated burdens with a heavy financial and emotional toll. The last row of Table 2 includes quotes from three different participants that show how multiple financial impacts can interact to exert compounding influence on a cancer survivor’s financial health and quality of life.

Experience of financial sacrifice by medical debt level

To explore whether the type and magnitude of financial sacrifice experienced by participants differed by level of medical debt, we compared the prevalence and frequency of financial sacrifices coded among the open-ended responses according to participants’ reported medical debt level, categorized as either under $10,000 or $10,000 or more in debt (Table 3).

Table 3.

Frequency of codes and domains by reported debt level

| Debt < $10,000 |

Debt ≥ $10,000 |

p value | |||

|---|---|---|---|---|---|

| n = 1085 | % within debt category | n = 551 | % within debt category | ||

| Top nine financial sacrifice domainsb | |||||

| Cutbacks/significant budgeting | 411 | 37.9 | 182 | 33.0 | 0.054 |

| Health insurance/health care cost challenges | 245 | 22.6 | 86 | 15.6 | 0.001 |

| Impact on career/self-advancement | 168 | 15.5 | 74 | 13.4 | 0.269 |

| Reduction/depletion of assets | 147 | 13.6 | 101 | 18.3 | 0.011 |

| Inability to pay bills/pay for services | 113 | 10.4 | 121 | 22.0 | < 0.001 |

| Burden on relationships/family | 114 | 10.5 | 94 | 17.1 | < 0.001 |

| Impact on housing | 87 | 8.0 | 113 | 20.5 | < 0.001 |

| Increase in debt or borrowing | 86 | 7.9 | 89 | 16.2 | < 0.001 |

| Employment status | 89 | 8.2 | 57 | 10.3 | 0.151 |

| Total number of uniquely applied codesa | |||||

| Applied 1–2 unique codes | 853 | 78.6 | 360 | 65.3 | < 0.001 |

| Applied 3 or more unique codes | 232 | 21.4 | 191 | 34.7 | < 0.001 |

Frequencies and percentages based on the number of unique codes, for the 18 identified financial sacrifice domains, applied to each participant response. Only those participants who had non-missing information on the medical debt question were included in the analysis

Frequencies and percentages based on the number of the nine most commonly coded financial sacrifice domains

p value for Chi-square test

Across the top nine financial sacrifice domains, cutbacks/significant budgeting was the most commonly reported sacrifice among participants in both debt level groups, 38% among participants with debt under $10,000 and 33% among participants with debt of $10,000 or more (Table 3). However, differences emerged between the high- and low-debt groups with respect to the frequency of other reported financial sacrifice domains. The prevalence rates for the second and third most common financial sacrifices among those with debt of ≥ $10,000 were significantly greater compared to those with under $10,000 of debt; specifically, among participants with debt ≥ $10,000, approximately 22% reported Inability to Pay Bills/Pay for Services and 21% reported Impact on Housing compared to 10% (p < 0.001) and 8% (p < 0.001), respectively, among those participants with debt under $10,000. Participants with ≥ $10,000 of debt were also significantly more likely to experience financial sacrifices of Reduction/Depletion of Assets (18% compared 14% of those with < $10,000 of debt, p = 0.011), Burden on Family/Relationships (17% compared to 11% of those with < $10,000 of debt, p < 0.001), and Increase in Debt of Borrowing (16% compared to 8% of those with < $10,000 of debt, p < 0.001). More than one in three (35%) participants with debt of ≥ $10,000 had three or more unique financial sacrifice domain codes applied to their open-ended responses compared to about one in five (21%) participants with debt under $10,000 (p < 0.001).

Discussion

In this study, we demonstrate the considerable social and economic burden from cancer experienced among a predominately insured, middle-aged population of survivors. Among the study sample of cancer survivors who responded to the open-ended question on financial sacrifices, half reported to have borrowed money or gone into debt (56%) and approximately 43% were unable to cover medical care costs. More than eight in every ten survivors (85%) worried about paying the large medical bills associated with their cancer. Our study reveals the wide range of financial sacrifices experienced by cancer survivors aged ≤ 65 years, and their families, and the various aspects of life impacted by cancer and its treatment. We found significant differences in the types of financial sacrifices reported by cancer survivors’ level of debt and identified financial sacrifices that were common among cancer survivors aged 18–64 years. Significant budgeting and financial cutbacks were the most commonly reported sacrifices that, when taken into consideration with other described financial sacrifices such as increased debt and inability to pay bills, suggests an important trend with respect to reduced or eliminated discretionary income and, in some cases, an inability to pay for even the most basic needs. The financial sacrifices reported by cancer survivors also highlight the degree to which social needs, including employment, housing, and social relationships, are affected by cancer, and suggest that some cancer survivors may represent socially at-risk populations. [44]

The study findings highlight interrelationships among cancer, financial hardship, and the social consequences among cancer survivors. When asked about the financial sacrifices they made, many survivors described the short- and long-term effects that cancer had on employment and career opportunities. Several survivors reported the impact of financial hardship from cancer on interpersonal relationships, including the burden on their children and withdrawal or divorce from their spouses. Other survivors experienced issues with their housing stability, such as being forced to sell their homes, to move in with family, or allowing their homes to fall into disrepair. The financial sacrifices reported by the study population support a growing body of literature that underscores heterogeneity in experiences across the different domains of financial hardship from cancer [8], including the material conditions that arise as individuals face medical expenses and depletion of financial resources [9, 19, 24, 26, 28, 45–47], psychological responses to cancer cost-related distress [11, 18, 48–50], and coping behaviors used while experiencing a potential reduction in financial resources [12, 13, 51–55].

These sacrifices reveal the type and significance of negative interpersonal and life events that can result from financial hardship [56], and illustrate the complexity of problems that can arise after a cancer diagnosis. Since cancer is not an acute event, but rather occurs across phases from diagnosis and treatment through survivorship or end-of-life, our findings reflect the sacrifices that survivors must make within their socioeconomic contexts alongside everyday life and family obligations. The various experiences of cancer survivors emphasize a range of potential avenues for intervention, which may be critical for improving the overall well-being of cancer survivors aged 18–64 years. For instance, the financial effects on cancer survivors could potentially be mitigated by provision of additional resources (e.g.,, financial counseling, medical financial assistance programs, community-based organizations), such as financial navigation interventions that aim to improve patient knowledge about medical costs, provide financial resources, and help manage out-of-pocket expenses [57–59]. Notably, though, cancer survivors may also require connections or referrals to other members of the health care team (e.g., social workers, mental health specialists) and to other community resources (e.g., legal assistance, employment resource centers) to manage the various social and economic consequences of financial hardship on themselves and their families. Further research, using standardized measures that specifically target the financial impact of cancer, is needed to better understand both the most common effects experienced by cancer survivors with financial hardship and the downstream consequences on these survivors’ financial, emotional, physical, and mental wellbeing.

Noteworthy, cancer survivors with more than $10,000 in debt reported experiencing a broader range of financial sacrifice issues than those with under $10,000 of debt. Perhaps unsurprisingly, the types of financial sacrifices made by survivors with higher debt were also different than those with lower debt. Specifically, a significantly higher proportion of survivors with higher debt reported reduction/depletion of assets, inability to pay for bills or services, and an impact on housing. These findings suggest that financial hardships experienced by individuals differ based on socioeconomic characteristics and financial capability as costs increase across the cancer care continuum. Further, as noted by Tucker-Seeley and Yabroff [60], financial well-being may differ for families based on their characteristics at diagnosis, as they experience rising health care expenses and declining income. For example, a family with high annual household income cutting back on vacation spending is much different than a family with low annual household income exhausting their credit card accounts and taking out a second mortgage on their house to pay for their cancer care. Importantly, this underscores the need for comprehensive data collection on financial well-being over time, as well as evidence on interventions designed to prevent catastrophic financial outcomes and the associated social consequences among individuals diagnosed with cancer.

Though our study provides important information about financial sacrifices experienced by cancer survivors aged 18–64 years, certain limitations need to be considered. First, the study population consisted of U.S. respondents to an internet-based survey, recruited from multiple sources, who responded to an open-ended item about having made other financial sacrifices and, thus, was not population-based. Compared to the larger population of survey respondents aged 18–64 (Supplemental Table), those included in our analysis were more likely to be female, non-White, non-married, uninsured, have low income, and have experienced financial hardship from cancer. Thus, it is likely that our study sample may have been at greater risk for financial hardship and experience more financial sacrifices than the general population of cancer patients and survivors. Additionally, given that this study is based on self-reported data, the results may be subject to desirability bias. More work is needed to assess the categories of financial sacrifice most commonly experienced across cancer survivor populations, including those that may be most vulnerable (i.e., uninsured, low-income patients and non-English speakers), as well as those that are insured and employed. The categories of sacrifice identified in our analysis could provide a basis for exploring financial sacrifice quantitatively using a more representative sample.

In summary, our analysis demonstrates both the frequency with which cancer patients and survivors must make financial sacrifices as a result of their condition, and the variety of forms that this sacrifice can take, even for individuals who have health insurance. Future mixed-methods research on the financial challenges faced by individuals diagnosed with cancer, their families, and caregivers, from both U.S. and international populations is needed to further demonstrate that financial hardship can be expressed in a variety of ways, resulting in unique challenges from one patient to the next. Interventions that allow for personalized assistance depending on a person’s specific financial situation have the potential to address a critical aspect of the long-term wellbeing of cancer survivors.

Supplementary Material

Acknowledgments

This study was funded, in part, by the Kaiser Permanente Center for Health Research. The article is based on a secondary data analysis performed by the authors.

Informed consent was obtained from all individual participants included in the study as part of the 2012 LIVESTRONG Survey for People Affected by Cancer. MPB has received a research grant from AstraZeneca for a project outside of this work.

Disclaimer The findings and conclusions in this paper are those of authors and do not necessarily represent the official position of the American Cancer Society, Centers for Disease Control and Prevention, Emory University, Kaiser Permanente, LIVESTRONG Foundation, National Cancer Institute, or University of Texas.

Footnotes

Electronic supplementary material The online version of this article (https://doi.org/10.1007/s11764–019-00761–1) contains supplementary material, which is available to authorized users.

Conflict of interest The authors declare that they have no conflict of interest.

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

References

- 1.American Cancer Society. Cancer treatment & survivorship facts & figures 2016–2017 Atlanta: American Cancer Society; 2016. [Google Scholar]

- 2.Shih YC, Smieliauskas F, Geynisman DM, Kelly RJ, Smith TJ. Trends in the cost and use of targeted cancer therapies for the privately insured nonelderly: 2001 to 2011. J Clin Oncol 2015;33(19):2190–6. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 3.Shih YT, Xu Y, Liu L, Smieliauskas F. Rising prices of targeted oral anticancer medications and associated financial burden on Medicare beneficiaries. J Clin Oncol 2017. August 1;35(22):2482–2489. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Bennette CS, Richards C, Sullivan SD, Ramsey SD. Steady increase in prices for oral anticancer drugs after market launch suggests a lack of competitive pressure. Health Aff (Millwood) 2016;35(5):805–12. [DOI] [PubMed] [Google Scholar]

- 5.Dusetzina SB. Drug pricing trends for orally administered anticancer medications reimbursed by commercial health plans, 2000–2014. JAMA Oncol 2016;2(7):960–1. [DOI] [PubMed] [Google Scholar]

- 6.Claxton G, Levitt L, Long M. Payments for cost sharing increasing rapidly over time: Kaiser Family Foundation; 2016. October 5, 2017. [Available from: https://www.kff.org/health-costs/issue-brief/paymentsfor-cost-sharing-increasing-rapidly-over-time/. [Google Scholar]

- 7.Peppercorn J Financial toxicity and societal costs of cancer care: distinct problems require distinct solutions. Oncologist 2017;22(2): 123–5. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.Altice CK, Banegas MP, Tucker-Seeley RD, Yabroff KR. Financial hardships experienced by cancer survivors: a systematic review. J Natl Cancer Inst 2017;109(2):djw205. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9.Yabroff KR, Dowling EC, Guy GP Jr, Banegas MP, Davidoff A, Han X, et al. Financial hardship associated with cancer in the United States: findings from a population-based sample of adult cancer survivors. J Clin Oncol 2016;34(3):259–67. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10.Pisu M, Kenzik KM, Oster RA, Drentea P, Ashing KT, Fouad M, et al. Economic hardship of minority and non-minority cancer survivors 1 year after diagnosis: another long-term effect of cancer? Cancer 2015;121(8):1257–64. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11.Regenbogen SE, Veenstra CM, Hawley ST, Banerjee M, Ward KC, Kato I, et al. The personal financial burden of complications after colorectal cancer surgery. Cancer 2014;120(19):3074–81. [DOI] [PubMed] [Google Scholar]

- 12.Zafar SY, Peppercorn JM, Schrag D, Taylor DH, Goetzinger AM, Zhong X, et al. The financial toxicity of cancer treatment: a pilot study assessing out-of-pocket expenses and the insured cancer patient’s experience. Oncologist 2013;18(4):381–90. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Bestvina CM, Zullig LL, Rushing C, Chino F, Samsa GP, Altomare I, et al. Patient-oncologist cost communication, financial distress, and medication adherence. J Oncol Pract 2014;10(3):162–7. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 14.Kent EE, Forsythe LP, Yabroff KR, Weaver KE, de Moor JS, Rodriguez JL, et al. Are survivors who report cancer-related financial problems more likely to forgo or delay medical care? Cancer 2013;119(20):3710–7. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15.Davidoff AJ, Hill SC, Bernard D, Yabroff KR. The affordable care act and expanded insurance eligibility among nonelderly adult cancer survivors. J Natl Cancer Inst 2015;107(9):djv181. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 16.Sharp L, Timmons A. Pre-diagnosis employment status and financial circumstances predict cancer-related financial stress and strain among breast and prostate cancer survivors. Support Care Cancer 2016;24(2):699–709. [DOI] [PubMed] [Google Scholar]

- 17.Sharp L, O’Leary E, O’Ceilleachair A, Skally M, Hanly P. Financial impact of colorectal cancer and its consequences: associations between cancer-related financial stress and strain and health-related quality of life. Dis Colon Rectum 2018;61(1):27–35. [DOI] [PubMed] [Google Scholar]

- 18.Sharp L, Carsin AE, Timmons A. Associations between cancer-related financial stress and strain and psychological well-being among individuals living with cancer. Psychooncology 2013;22(4):745–55. [DOI] [PubMed] [Google Scholar]

- 19.Group AS, Kimman M, Jan S, Yip CH, Thabrany H, Peters SA, et al. Catastrophic health expenditure and 12-month mortality associated with cancer in Southeast Asia: results from a longitudinal study in eight countries. BMC Med 2015;13:190. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.Group AS, Jan S, Kimman M, Peters SA, Woodward M. Financial catastrophe, treatment discontinuation and death associated with surgically operable cancer in South-East Asia: results from the ACTION study. Surgery 2015;157(6):971–82. [DOI] [PubMed] [Google Scholar]

- 21.Chan A, Chiang YY, Low XH, Yap KY, Ng R. Affordability of cancer treatment for aging cancer patients in Singapore: an analysis of health, lifestyle, and financial burden. Support Care Cancer 2013;21(12):3509–17. [DOI] [PubMed] [Google Scholar]

- 22.Lauzier S, Levesque P, Mondor M, Drolet M, Coyle D, Brisson J, et al. Out-of-pocket costs in the year after early breast cancer among Canadian women and spouses. J Natl Cancer Inst 2013;105(4): 280–92. [DOI] [PubMed] [Google Scholar]

- 23.de Oliveira C, Bremner KE, Ni A, Alibhai SM, Laporte A, Krahn MD. Patient time and out-of-pocket costs for long-term prostate cancer survivors in Ontario, Canada. J Cancer Surviv 2014;8(1): 9–20. [DOI] [PubMed] [Google Scholar]

- 24.Ekwueme DU, Yabroff KR, Guy GP Jr, Banegas MP, de Moor JS, Li C, et al. Medical costs and productivity losses of cancer survivors–United States, 2008–2011. MMWR Morb Mortal Wkly Rep 2014;63(23):505–10. [PMC free article] [PubMed] [Google Scholar]

- 25.LIVESTRONG Foundation. Survivors’ experiences with employment Austin: LIVESTRONG Foundation; 2013. [Google Scholar]

- 26.Zheng Z, Yabroff KR, Guy GP Jr, Han X, Li C, Banegas MP, et al. Annual medical expenditure and productivity loss among colorectal, female breast, and prostate cancer survivors in the United States. J Natl Cancer Inst 2016;108(5):djv382. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 27.Parsons HM, Schmidt S, Harlan LC, Kent EE, Lynch CF, Smith AW, et al. Young and uninsured: insurance patterns of recently diagnosed adolescent and young adult cancer survivors in the AYA HOPE study. Cancer 2014;120(15):2352–60. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 28.Gordon LG, Walker SM, Mervin MC, Lowe A, Smith DP, Gardiner RA, et al. Financial toxicity: a potential side effect of prostate cancer treatment among Australian men. Eur J Cancer Care (Engl) 2017;26(1):e12392. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 29.Mahal A, Karan A, Fan VY, Engelgau M. The economic burden of cancers on Indian households. PLoS One 2013;8(8):e71853. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 30.Bradley SE, Sherwood PR, Kuo J, et al. Perceptions of economic hardship and emotional health in a pilot sample of family caregivers. J Neurooncol 2009;93(3):333–342. 10.1007/s11060-008-9778-z [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31.Advani PS, Reitzel LR, Nguyen NT, Fisher FD, Savoy EJ, Cuevas AG, et al. Financial strain and cancer risk behaviors among African Americans. Cancer Epidemiol Biomark Prev 2014;23(6):967–75. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32.Meeker CR, Geynisman DM, Egleston BL, Hall MJ, Mechanic KY, Bilusic M, et al. Relationships among financial distress, emotional distress, and overall distress in insured patients with cancer. J Oncol Pract 2016;12(7):e755–64. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 33.Ceilleachair AO, Costello L, Finn C, Timmons A, Fitzpatrick P, Kapur K, et al. Inter-relationships between the economic and emotional consequences of colorectal cancer for patients and their families: a qualitative study. BMC Gastroenterol 2012;12:62. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 34.Ponnet K Financial stress, parent functioning and adolescent problem behavior: an actor-partner interdependence approach to family stress processes in low-, middle-, and high-income families. J Youth Adolesc 2014;43(10):1752–69. [DOI] [PubMed] [Google Scholar]

- 35.Stepanikova I, Powroznik K, Cook KS, Tierney DK, Laport GG. Exploring long-term cancer survivors’ experiences in the career and financial domains: interviews with hematopoietic stem cell transplantation recipients. J Psychosoc Oncol 2016;34(1–2):2–27. [DOI] [PubMed] [Google Scholar]

- 36.Moffatt S, Noble E, White M. Addressing the financial consequences of cancer: qualitative evaluation of a welfare rights advice service. PLoS One 2012;7(8):e42979. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 37.de Souza JA, Wong YN. Financial distress in cancer patients. J Med Person 2013;11(2):73–7. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 38.LIVESTRONG Foundation. LIVESTRONG surveys 2016. [Available from: https://www.livestrong.org/what-we-do/livestrong-surveys.

- 39.Yabroff KR, Dowling E, Rodriguez J, Ekwueme DU, Meissner H, Soni A, et al. The medical expenditure panel survey (MEPS) experiences with cancer survivorship supplement. J Cancer Surviv 2012;6(4):407–19. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 40.Agency for Healthcare Research and Quality. Summary of recommendations from round 1 cognitive testing of the MEPS cancer SAQ Rockville: AHRQ; n.d. [Available from: http://meps.ahrq.gov/mepsweb/survey_comp/hc_survey/2011/MEPS_Cancer_SAQ_R1_Results.htm [Google Scholar]

- 41.Corbin J, Strauss A, editors. Basics of qualitative research: techniques and procedures for developing grounded theory 3rd ed. Thousand Oaks: Sage Publication, Inc.; 2008. [Google Scholar]

- 42.Patton MQ, editor. Qualitative research & evaluation methods 3rd ed. Thousand Oaks: Sage Publications, Inc.; 2002. [Google Scholar]

- 43.Bernard HR, Wutich AY, Ryan GW, editors. Analyzing qualitative data: systematic approaches 2nd ed. Thousand Oaks: Sage Publications, Inc.; 2017. [Google Scholar]

- 44.Office of the Assistant Secretary for Planning and Evaluation. Report to congress: social risk factors and performance under Medicare’s value-based payment programs Washington, D.C.: U.S. Department of Health and Human Services December; 2016. p. 21. [Google Scholar]

- 45.Banegas MP, Guy GP Jr, de Moor JS, Ekwueme DU, Virgo KS, Kent EE, et al. For working-age cancer survivors, medical debt and bankruptcy create financial hardships. Health Aff (Millwood) 2016;35(1):54–61. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 46.Kent EE, Davidoff A, de Moor JS, McNeel TS, Virgo KS, Coughlan D, et al. Impact of sociodemographic characteristics on underemployment in a longitudinal, nationally representative study of cancer survivors: evidence for the importance of gender and marital status. J Psychosoc Oncol 2018;36(3):287–303. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 47.Kirchhoff AC, Nipp R, Warner EL, Kuhlthau K, Leisenring WM, Donelan K, et al. “Job lock” among long-term survivors of childhood cancer: a report from the Childhood Cancer Survivor Study. JAMA Oncol 2018;4(5):707–11. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 48.Chino F, Peppercorn J, Taylor DH Jr, Lu Y, Samsa G, Abernethy AP, et al. Self-reported financial burden and satisfaction with care among patients with cancer. Oncologist 2014;19(4):414–20. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 49.Ell K, Xie B, Wells A, Nedjat-Haiem F, Lee PJ, Vourlekis B. Economic stress among low-income women with cancer: effects on quality of life. Cancer 2008;112(3):616–25. [DOI] [PubMed] [Google Scholar]

- 50.Stump TK, Eghan N, Egleston BL, Hamilton O, Pirollo M, Schwartz SJ, et al. Cost concerns of patients with cancer. J Oncol Pract 2013;9(5):251–7. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 51.Banegas MP, Dickerson JF, Kent EE, de Moor JS, Virgo KS, Guy GP Jr, et al. Exploring barriers to the receipt of necessary medical care among cancer survivors under age 65 years. J Cancer Surviv 2018;12(1):28–37. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 52.Zheng Z, Han X, Guy GP Jr, Davidoff AJ, Li C, Banegas MP, et al. Do cancer survivors change their prescription drug use for financial reasons? Findings from a nationally representative sample in the United States. Cancer 2017;123(8):1453–63. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 53.Zullig LL, Peppercorn JM, Schrag D, Taylor DH, Lu Y, Samsa G. Financial distress, use of cost-coping strategies, and adherence to prescription medication among patients with Cancer. J Oncol Pract 2013;9(6 SUPPL):60s–3s. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 54.Chino F, Peppercorn JM, Rushing C, Kamal AH, Altomare I, Samsa G, et al. Out-of-pocket costs, financial distress, and underinsurance in cancer care. JAMA Oncol 2017;3(11):1582–4. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 55.Shankaran V, Ramsey S. Addressing the financial burden of cancer treatment; From Copay to Can’t Pay. JAMA Oncol 2015;1(3):273–4. [DOI] [PubMed] [Google Scholar]

- 56.Sturgeon JA, Arewasikporn A, Okun MA, Davis MC, Ong AD, Zautra AJ. The psychosocial context of financial stress: implications for inflammation and psychological health. Psychosom Med 2016;78(2):134–43. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 57.Banegas MP, Dickerson JF, Friedman NL, Mosen DM, Ender AX, Chang TR, et al. Evaluation of a novel financial navigator pilot to address patient concerns about medical care costs. Perm J 2019;23: 18–084. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 58.Shankaran V, Leahy T, Steelquist J, Watabayashi K, Linden H, Ramsey S, et al. Pilot feasibility study of an oncology financial navigation program. J Oncol Pract 2018;14(2):e122–e9. [DOI] [PubMed] [Google Scholar]

- 59.Yezefski T, Steelquist J, Watabayashi K, Sherman D, Shankaran V. Impact of trained oncology financial navigators on patient out-of-pocket spending. Am J Manag Care 2018;24(5 Suppl):S74–S9. [PubMed] [Google Scholar]

- 60.Tucker-Seeley RD, Yabroff KR. Minimizing the “financial toxicity” associated with cancer care: advancing the research agenda. J Natl Cancer Inst 2016;108(5):djv410. [DOI] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.