Abstract

Objective

To test the hypothesis that the earned income tax credit (EITC)—the largest US poverty alleviation program—affects short‐term health care expenditures among US adults.

Data Sources

Adult participants in the 1997‐2012 waves of the US Medical Expenditure Panel Survey (MEPS) (N = 1 282 080).

Study Design

We conducted difference‐in‐differences analyses, comparing health care expenditures among EITC‐eligible adults in February (immediately following EITC refund receipt) with expenditures during other months, using non‐EITC‐eligible individuals to difference out seasonal variation in health care expenditures. Outcomes included total out‐of‐pocket expenditures as well as spending on specific categories such as outpatient visits and inpatient hospitalizations. We conducted subgroup analyses to examine heterogeneity by insurance status.

Principal Findings

EITC refund receipt was not associated with short‐term changes in total expenditures, nor any expenditure subcategories. Results were similar by insurance status and robust to numerous alternative specifications.

Conclusions

EITC refunds are not associated with short‐term changes in health care expenditures among US adults. This may be because the refund is spent on other expenses, because of income smoothing, or because of similar refund‐related variation in health care expenditures among noneligible adults. Future studies should examine whether other types of income supplementation affect health care expenditures, particularly among individuals in poverty.

Keywords: determinants of health, observational data, population health, quasi‐experiments, social determinants of health, socioeconomic causes of health

1. INTRODUCTION

Poverty has been hypothesized to lead to foregone care among low‐income households in the United States and other high‐income countries.1, 2, 3 This may be mediated by the inability to afford insurance coverage, out‐of‐pocket costs like co‐pays and deductibles, or transportation, and it may result in worsened health, for example, if individuals do not seek care related to chronic conditions.4, 5 Alternately, poverty is also associated with a higher burden of disease and chronic stress, potentially resulting in greater utilization of specific types of services such as emergency care, depending on insurance coverage.6 For example, prior studies that exploit the discrete shock created by the Great Recession have found that financial and job insecurity may have resulted in foregone outpatient care, as well as increased utilization of and expenditures on emergency and mental health services.7, 8

Despite this evidence, little is known about the ways in which US social welfare policies that target poverty may influence health care utilization and expenditures. The largest US poverty alleviation program is the earned income tax credit (EITC), with over 25 million beneficiaries receiving almost US$63 billion in 2018.9 The EITC is a federal program that provides tax refunds to low‐income families contingent upon employment, with the size of the refund calculated by the Internal Revenue Service (IRS) based on income, number of children, marital status, age, and tax year.10, 11, 12 More than half of states also provide additional state‐level supplements to the federal EITC of varying generosity.13

The EITC has been shown to reduce poverty and increase the labor supply,14, 15 particularly for single mothers,16 with generally positive (but mixed) effects on the health of adult recipients and their children.17, 18, 19, 20, 21, 22, 23, 24 Prior work has also shown that the EITC is associated with increased household expenditures more generally,25 and qualitative work suggests that the EITC refund is spent differently from typical employment income, perhaps because it is distributed annually as a lump sum in the form of a tax refund.26, 27

No studies to our knowledge have examined the EITC's effects on health care expenditures, although several have examined effects on insurance coverage. For example, one found that the EITC increased private insurance coverage,28 likely due to increased employment and subsequent coverage through employers. Another found that state‐level EITC programs resulted in a shift away from public insurance among children under 14, with no net change in the percent of children uninsured29; this study also found no effect of state EITC programs on health care utilization among children.

A handful of studies have examined the effects on health care utilization of other US welfare policies. For example, the Personal Responsibility and Work Opportunity and Reconciliation Act (PRWORA) of 1996, which limited the amount of welfare receipt and mandated work requirements, was found to have either no effect on or reduced health care utilization, perhaps due to changes in insurance coverage.30, 31, 32, 33, 34 Others have found an increase in health care utilization in response to the 2008 Economic Stimulus Payments, with the increased demand potentially driven by worsened health due to increased substance use.35

In this study, we tested the hypothesis that EITC refund receipt leads to changes in short‐term health care expenditures, including multiple categories of provider visits, and that there are differential effects by insurance status. We used a large diverse sample drawn from a nationally representative survey and employed a quasi‐experimental difference‐in‐differences (DID) approach. This study is among the first to assess the effects of social welfare policy on health care expenditures, examining whether income supplementation to alleviate poverty influences health care spending in the short run.

2. METHODS

2.1. Dataset

This study was conducted using the 1997‐2012 waves of the Medical Expenditure Panel Survey (MEPS), a nationally representative survey of multiple overlapping two‐year panels. MEPS provides detailed data on health care expenditures, income, and sociodemographic characteristics. Each year, MEPS interviewed a sample of 20 000‐30 000 individuals. Each cohort was interviewed five times over a two‐year period, roughly once every 4‐5 months. At each interview, participants gave information on health care encounters that took place during the 4‐5 months preceding their interview. Importantly, episode‐level detail was collected, including the month and year when the medical event occurred, enabling us to match health care spending to the time period when the EITC is typically received.

Because taxes are filed each year based on earnings from the prior calendar year, and because the EITC is received shortly thereafter, we used income and family structure data for each individual from year 1 of his/her interview to calculate the size of the EITC refund received in year 2. We then estimated the effect of the EITC refund received in year 2 on health care expenditures in year 2, as described below. All variables that were reported in dollar values—including expenditures, income, and (imputed) EITC refund size—were inflation‐adjusted to 2011 US dollars.

Finally, we restricted our sample to individuals with family incomes below US$100 000, since individuals with higher incomes are unlikely to be an appropriate control group for EITC recipients.

2.2. Exposure

The primary exposure was the size of the federal EITC refund for which an individual was eligible in a given year. We imputed refund size using the TAXSIM package for Stata, based on IRS tax tables36; inputs included pretax household income, number of children, marital status, age, and tax year. MEPS queries subjects about whether they received an EITC refund but not the amount, and numerous prior studies have shown that self‐reported receipt of EITC and other welfare benefits is neither sensitive nor specific and may bias results.37, 38, 39, 40 We therefore assumed that all individuals received the refund for which they were eligible, which is analogous to an intent‐to‐treat approach in a randomized controlled trial. Prior work has shown that approximately 80 percent of eligible individuals during this time period received their refunds,41 which means that this technique suffers from a degree of misclassification. Moreover, most publicly available datasets do not include questions about welfare receipt, so this method is one that is commonly used in the EITC literature.21, 22, 42, 43, 44

2.3. Outcomes

We examined individual health care expenditures across several domains. We included only expenditures reported in the second year of the survey, since the EITC refund that we imputed was received at the beginning of year 2. For each person, outcomes included total monthly out‐of‐pocket (OOP) spending, OOP spending for all office‐based visits, and OOP spending for the following subcategories of office‐based visits: general checkups, mental health, follow‐up appointments, diagnosis, and others. We also examined dental visits, emergency department visits, and inpatient and outpatient hospital services. For each of these, we were able to identify the month in which the expenditure took place. We included multiple outcome domains, as they may capture different mechanisms through which the EITC may affect health expenditures. For example, there may be an increase in more discretionary health care spending, for example, preventive visits, or there may be decreased spending on visits for exacerbations of acute conditions due to increased medication adherence and reduced (financial) stress.

For prescription drugs, MEPS does not query about the exact month of purchase, but rather about purchases within the entire 4‐ to 5‐month reference period. Given the coarseness of this measure relative to the more narrow window of EITC refund receipt, we did not examine prescription drug utilization as an outcome.

2.4. Covariates

Covariates included gender, race, marital status, a third‐degree polynomial for age (ie, age, age‐squared, age‐cubed), a fifth‐degree polynomial for family income, number of children in the household, number of adults in the household, and insurance status. We used values of these covariates that were reported for year 1 of a given individual's survey participation.

2.5. Data analysis

Prior work has demonstrated that roughly 60 percent of EITC refunds are received in February.18, 45 Thus, we first calculated descriptive characteristics for individuals in our sample separately by EITC eligibility and month in which the expenditure occurred (February versus other months).

We then estimated the EITC's effects on health care expenditures using difference‐in‐differences (DID) analysis, a quasi‐experimental econometric method that estimates the effects of discrete events while accounting for secular trends.46 We took advantage of the fact that most EITC beneficiaries received their refunds in February. We therefore compared expenditures among EITC‐eligible participants in February with expenditures during other times of the year. To factor out possible secular changes, DID analysis then “differences out” the change observed for February expenditures among non‐EITC‐eligible individuals relative to expenditures in other months, such that individuals who are not eligible for the EITC serve as a control group. This enabled us to estimate short‐term effects that were not confounded by individual or household factors that might bias an observational study of the association between EITC refund receipt and health care expenditures. The primary assumption underlying DID is that the differences in these outcomes across the year would be similar for EITC‐eligible and noneligible individuals in the absence of the EITC. While this assumption is not empirically testable, we validated the related assumption that there are no differences in the trends in the outcomes during nonexposure months (see Appendix S1 and Figure S1). This seasonal DID strategy has been used in prior work examining the health effects of the EITC.18, 44

DID analyses were carried out by including an interaction term between a binary variable for whether the expenditure occurred in February (Feb) and a continuous variable representing EITC refund size (EITC). Analyses involved multivariable linear regressions. The equation for a given outcome Y was specified as:

The coefficient β 1 represents the short‐term effects of the EITC on the outcome of interest. Subscript i denotes individuals, and subscript t denotes time. We included a vector of individual covariates described above (Covar) and fixed effects for year (Year) to account for secular trends. Survey weights were used to account for the MEPS sampling design. Robust standard errors were clustered at the family level to account for heteroskedasticity (ie, correlated observations within the same family and individual).

2.6. Alternative specifications

We carried out numerous sensitivity analyses to test the robustness of our results to alternative specifications. First, we tested the hypothesis that the EITC's effects may be different based on the ability to access and afford health care. To do so, we conducted a subgroup analysis in which we stratified our analyses by insurance status (uninsured, Medicaid, and private).

Second, we considered the “treatment” period of the EITC to include both February and March, instead of just February, since an additional 30 percent of EITC beneficiaries receive their refunds in March.18, 45 Similarly, we conducted an alternative specification in which the treatment period included February, March, and April; this enabled us to capture virtually all months in which EITC‐eligible individuals received their refunds. These specifications therefore included individuals up to three months after receipt of their refund (eg, those who received their refunds in late January and but reported expenditures in late April). This allowed for a lag between refund receipt and health care expenditures, although it may have also resulted in the inclusion of individuals more remote from refund receipt and therefore less likely to be affected by the income boost.

Third, we carried out the primary analysis without controlling for income, marital status, or the number of adults/children in the household, since these are inputs that determine EITC refund size, and adjusting for them may reduce variation in our exposure.

Additional sensitivity analyses are described in the Appendix S1 and included: (a) dichotomizing the outcome variables (ie, any expenditure), (b) testing for heterogeneous effects of the EITC over time, (c) restricting the sample to individuals with less than $50 000 in household income, (d) stratifying the results by gender, and (e) modeling the number of family members as indicator rather than continuous variables.

2.7. Ethics approval

This study involved public use data with no personal identifiers. No ethics approval was required.

3. RESULTS

3.1. Sample characteristics

Roughly 30 percent of individuals were eligible for any EITC payment during the study period, with a mean refund size of US$1739. EITC‐eligible individuals were more likely to be younger, female, nonwhite, and uninsured or covered by Medicaid as opposed to private insurance (Table 1). Average OOP health expenditures were lower among EITC‐eligible individuals for all outpatient categories, but higher for emergency visits and inpatient hospital services. Note that MEPS is a panel study, with repeated measurements of the same individuals over time; this is why the distribution of demographic variables was nearly identical for observations representing expenditures in February versus other months.

Table 1.

Sample characteristics

| Variable | Full sample | EITC‐eligible | Not EITC‐eligible | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| February | Other months | February | Other months | |||||||

| Mean/% | SE | Mean/% | SE | Mean/% | SE | Mean/% | SE | Mean/% | SE | |

| Age (y) | 37.7 | 0.01 | 35.2 | 0.06 | 35.2 | 0.02 | 38.9 | 0.04 | 38.9 | 0.01 |

| Male | 46.7 | 41.5 | 41.5 | 49.1 | 49.1 | |||||

| White | 58.4 | 52.7 | 52.7 | 61.1 | 61.1 | |||||

| Black | 11.2 | 13.6 | 13.6 | 10.1 | 10.1 | |||||

| Hispanic | 27.6 | 38.9 | 38.9 | 22.4 | 22.4 | |||||

| Asian | 2.7 | 2.1 | 2.1 | 3.0 | 3.0 | |||||

| Number of children in family | 0.9 | 0.00 | 1.4 | 0.01 | 1.4 | 0.00 | 0.7 | 0.00 | 0.7 | 0.00 |

| Numbers of adults in family | 1.7 | 0.00 | 1.8 | 0.00 | 1.8 | 0.00 | 1.7 | 0.00 | 1.7 | 0.00 |

| Medicaid coverage | 10.2 | 17 | 16.8 | 7.2 | 7.2 | |||||

| Private insurance coverage | 59.9 | 39.1 | 39.3 | 69.6 | 69.3 | |||||

| Uninsured | 30.1 | 44.4 | 44.5 | 23.3 | 23.6 | |||||

| Family income, year 1 (US$) | 36 781 | 22.3 | 22 761 | 97.6 | 22 757 | 29.4 | 43 187 | 94.1 | 43 188 | 28.4 |

| Any EITC receipt | 31.4 | 100 | 100 | 0 | 0 | |||||

| EITC receipt (US$) | 0.55 | 0.00 | 1739 | 8.9 | 1739 | 2.7 | 0 | 0 | 0 | 0 |

| Monthly OOP health expenditures (US$) | ||||||||||

| Total spending | 22.5 | 0.22 | 19.0 | 2.59 | 16.1 | 0.36 | 25.1 | 0.78 | 25.3 | 0.28 |

| Total office‐based visits | 8.9 | 0.09 | 6.1 | 0.34 | 5.9 | 0.13 | 11.0 | 0.45 | 10.2 | 0.12 |

| Office‐based general checkup | 1.2 | 0.02 | 0.80 | 0.05 | 0.87 | 0.03 | 1.3 | 0.06 | 1.4 | 0.03 |

| Office‐based mental health | 0.5 | 0.01 | 0.3 | 0.04 | 0.2 | 0.02 | 0.6 | 0.05 | 0.6 | 0.02 |

| Office‐based follow‐up | 0.6 | 0.02 | 0.4 | 0.07 | 0.4 | 0.03 | 0.8 | 0.10 | 0.7 | 0.03 |

| Office‐based diagnosis/treatment | 3.9 | 0.05 | 3.1 | 0.28 | 2.7 | 0.10 | 5.0 | 0.30 | 4.4 | 0.06 |

| Dental care | 7.6 | 0.10 | 4.9 | 0.44 | 4.8 | 0.14 | 8.9 | 0.43 | 8.9 | 0.13 |

| Emergency department services | 1.6 | 0.05 | 2.4 | 0.35 | 2.1 | 0.13 | 1.5 | 0.22 | 1.4 | 0.05 |

| Inpatient hospital services | 2.6 | 0.15 | 4.0 | 2.5 | 2.2 | 0.25 | 2.1 | 0.30 | 2.7 | 0.18 |

| Outpatient hospital services | 1.8 | 0.06 | 1.6 | 0.42 | 1.1 | 0.08 | 1.7 | 0.16 | 2.1 | 0.09 |

| Monthly OOP health expenditures (any) | ||||||||||

| Total spending | 14.2 | 10.6 | 9.7 | 16.9 | 16.2 | |||||

| Total office‐based visits | 11.2 | 8.2 | 7.4 | 13.6 | 12.8 | |||||

| Office‐based general checkup | 2.9 | 2.0 | 1.9 | 3.4 | 3.4 | |||||

| Office‐based mental health | 0.5 | 0.4 | 0.3 | 0.7 | 0.7 | |||||

| Office‐based follow‐up | 1.3 | 0.8 | 0.8 | 1.4 | 1.5 | |||||

| Office‐based diagnosis/treatment | 6.1 | 4.5 | 3.9 | 7.8 | 7.0 | |||||

| Dental care | 2.9 | 1.9 | 1.8 | 3.4 | 3.3 | |||||

| Emergency department services | 0.5 | 0.6 | 0.6 | 0.5 | 0.5 | |||||

| Inpatient hospital services | 0.3 | 0.2 | 0.2 | 0.3 | 0.3 | |||||

| Outpatient hospital services | 0.7 | 0.6 | 0.5 | 0.8 | 0.8 | |||||

| Number of individuals | 1 282 080 | 33 517 | 368 530 | 73 359 | 806 674 | |||||

Sample includes adults surveyed in the 1997‐2012 waves of the Medical Expenditure Panel Survey.

Abbreviations: EITC, earned income tax credit; OOP, out‐of‐pocket.

3.2. EITC effects on health care expenditures

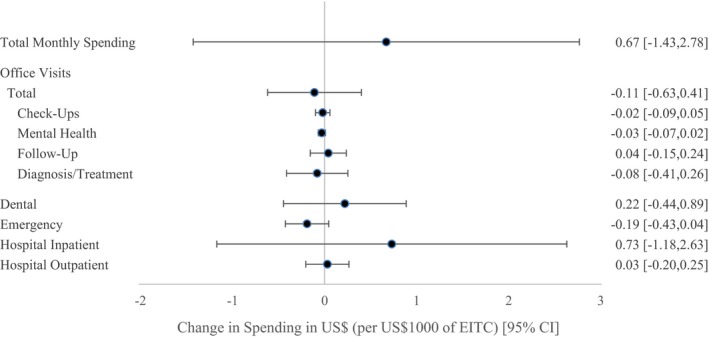

We first examined whether the EITC was associated with a change in short‐term health expenditures, differencing out secular trends among the control group of non‐EITC‐eligible individuals. In our primary models (Figure 1), we were unable to reject the null hypothesis that there was no short‐term effect of EITC receipt in February on any of the outcomes of interest, including out‐of‐pocket expenditures overall and the subcategories that we examined.

Figure 1.

Effects of the earned income tax credit on short‐term out‐of‐pocket health care expenditures [Color figure can be viewed at wileyonlinelibrary.com]

Note: N = 1 282 080 adults surveyed in the 1997‐2012 waves of the Medical Expenditure Panel Survey. EITC: earned income tax credit. Estimates derived from multivariable linear regressions using difference‐in‐differences analyses, adjusting for gender, race, marital status, a third‐degree polynomial for age (ie, age, age‐squared, age‐cubed), a fifth‐degree polynomial for family income, number of children in the household, number of adults in the household, insurance status, and year. Observations during the months of February were considered to fall in the “treatment” window. Expenditures on provider visits were reported on a monthly basis for each individual in the family. Robust standard errors clustered at the family level.

3.3. Alternative specifications

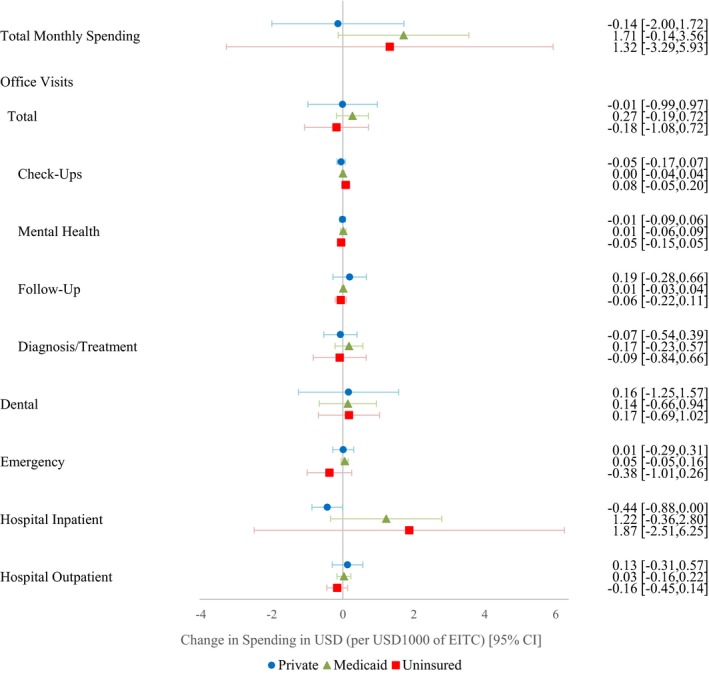

We next tested whether there was heterogeneity in the EITC's effects by insurance status, comparing individuals with no insurance, Medicaid, and private insurance (Figure 2). There were no statistically significant differences by insurance status. For each of these groups, we were unable to reject the null hypothesis that there was no short‐term effect of EITC refund receipt in February on any outcome.

Figure 2.

Effects of the earned income tax credit on short‐term out‐of‐pocket health care expenditures, by insurance status [Color figure can be viewed at wileyonlinelibrary.com]

Note: N = 1 282 080 adults surveyed in the 1997‐2012 waves of the Medical Expenditure Panel Survey. EITC: earned income tax credit. Estimates derived from multivariable linear regressions using difference‐in‐differences analyses, adjusting for gender, race, marital status, a third‐degree polynomial for age (ie, age, age‐squared, age‐cubed), a fifth‐degree polynomial for family income, number of children in the household, number of adults in the household, and year, stratified by insurance status. Observations during the months of February were considered to fall in the “treatment” window. Expenditures on provider visits were reported on a monthly basis for each individual in the family. Robust standard errors clustered at the family level.

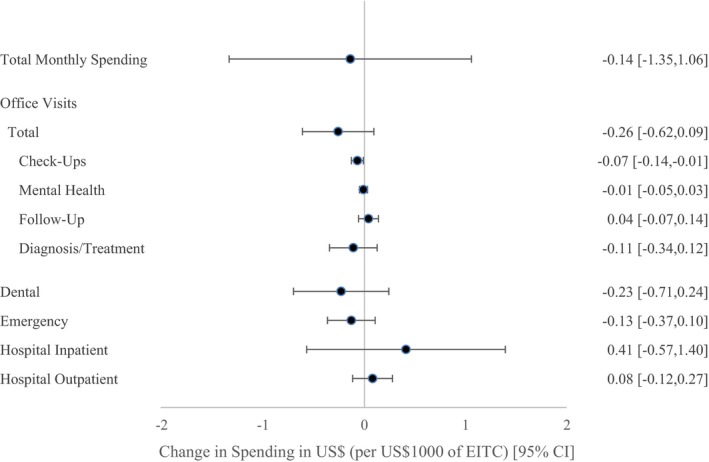

When expanding the EITC exposure window to include both February and March, which would capture a larger percent of EITC recipients after they had received their refunds, we were again unable to reject the null hypothesis that there was no short‐term effect of the EITC on expenditures in any category (Figure 3). The sole exception was a small reduction in expenditures on checkup visits (−0.07 per $1000 in EITC, 95% CI −0.14, −0.01) that was not statistically significant when correcting for multiple hypothesis testing. Results were similarly null when expanding the exposure window to include February, March, and April (Table S1).

Figure 3.

Effects of the earned income tax credit on short‐term out‐of‐pocket health care expenditures, February‐March specification [Color figure can be viewed at wileyonlinelibrary.com]

Note: N = 1 282 080 adults surveyed in the 1997‐2012 waves of the Medical Expenditure Panel Survey. EITC: earned income tax credit. Estimates derived from multivariable linear regressions using difference‐in‐differences analyses, adjusting for gender, race, marital status, a third‐degree polynomial for age (ie, age, age‐squared, age‐cubed), a fifth‐degree polynomial for family income, number of children in the household, number of adults in the household, insurance status, and year. Observations during the months of February and March were considered to fall in the “treatment” window. Expenditures on provider visits were reported on a monthly basis for each individual in the family. Robust standard errors clustered at the family level.

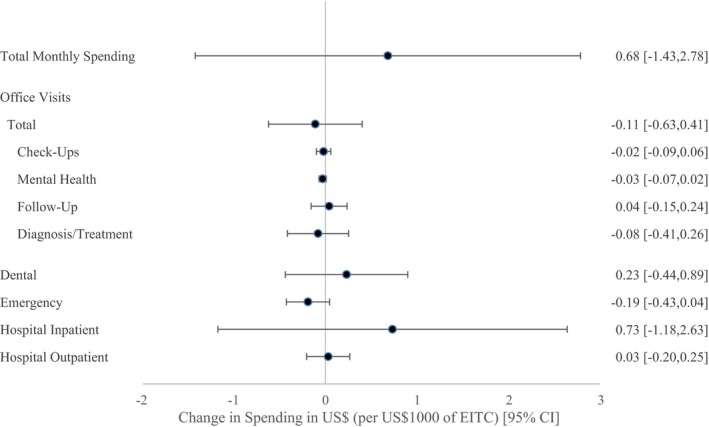

Because adjusting for inputs into the EITC might reduce variation in our exposure, we next carried out our models without adjusting for income, marital status, and number of adults/children in the household. In these models, we again failed to reject the null hypothesis that EITC receipt had no short‐term effect on the outcomes of interest (Figure 4).

Figure 4.

Effects of the earned income tax credit on short‐term out‐of‐pocket health care expenditures, limited covariates [Color figure can be viewed at wileyonlinelibrary.com]

Note: N = 1 282 080 adults surveyed in the 1997‐2012 waves of the Medical Expenditure Panel Survey. EITC: earned income tax credit. Estimates derived from multivariable linear regressions using difference‐in‐differences analyses, adjusting for gender, race, marital status, a third‐degree polynomial for age (ie, age, age‐squared, age‐cubed), insurance status, and year. As compared with the main specification, we have excluded controls for family income, number of children in the household, and number of adults in the household. Observations during the months of February were considered to fall in the “treatment” window. Expenditures on provider visits were reported on a monthly basis for each individual in the family. Robust standard errors clustered at the family level.

We also carried out a number of additional sensitivity analyses (Tables S1 and S2): (a) dichotomizing the outcome variables (ie, any expenditure), (b) testing for heterogeneous effects of the EITC over time, (c) restricting the sample to individuals with less than $50 000 in household income, (d) stratifying the results by gender, and (e) modeling the number of family members as indicator rather than continuous variables. For the gender‐stratified analysis, we found reduced emergency department expenditures among men (−0.50 per $1000 in EITC, 95% CI: −0.88, −0.11). This effect estimate was statistically significantly different from the estimate for women's expenditures on emergency department services (0.04 per $1000 in EITC, 95% CI: −0.24, 0.32), although it was not robust to adjustment of the p‐value for multiple hypothesis testing. For every other analysis, we were again unable to reject the null hypothesis that there was no short‐term effect of the EITC on any category of health care expenditures.

4. DISCUSSION

This study examined the short‐term effects of the EITC on health care expenditures in a large longitudinal diverse sample drawn from nationally representative MEPS data. We examined multiple types of health care expenditures using several model specifications. This included subgroup analyses to examine heterogeneity by insurance status. In each of these, we found that EITC refund receipt was not associated with a change in OOP health care expenditures in the short term across a variety of expenditure types and model specifications. The sole exception was a small decrease in expenditures on checkup visits, US$0.07 per US$1000 in EITC refund size. This finding was not statistically significant when correcting for multiple hypothesis testing and not large enough to represent a clinically significant change in expenditure. This effect was only detected in the February‐March model specification, and there was otherwise no consistent direction or magnitude of effect sizes for other outcomes, suggesting that this result may be an artifact of multiple hypothesis testing.

Prior work has shown that the EITC is associated with increased household expenditures more generally25 and with a range of short‐ and long‐term health outcomes.18, 20, 21, 22, 44, 47 It may be that the EITC is spent differently from other types of income because it is received as a lump‐sum payment. For example, previous work has shown that the EITC refund is more likely to be spent on big‐ticket items such as cars or appliances or on debt payments,26, 27, 48, 49 so that recipients may be less likely to use this income to pay for health care expenses. In economic terms, it may be that liquidity constraints may not be an important factor, in that individuals are able or willing to borrow or delay paying bills long enough to purchase health care when it is necessary, more so than they are able or willing to do for other types of expenses.

One prior study has shown that tax refunds are associated with a 60 percent increase in health care spending in the weeks after tax refund receipt,50 although that study did not focus specifically on EITC refunds. It may be that certain types of health care expenses are more sensitive to an income boost among higher‐income families, for example, elective procedures. Alternately, it may be that the receipt of tax refunds in general is less predictable than receipt of the EITC, so that noneligible families are not able to anticipate their tax refund size and smooth their income accordingly over the course of the year. Notably, this prior study did not include a control group as we do here. That is, our study “differences out” secular changes that occur in non‐EITC‐eligible individuals to tease out the effects of the EITC itself, one of the strengths of a DID design. In fact, it may be that EITC‐eligible and noneligible families similarly increase health expenditures immediately after refund receipt, such that our null findings are due to the fact that EITC‐eligible individuals do so at similar rates as the control group of noneligible individuals.

In terms of the concern that low‐income individuals may be foregoing necessary care, our findings suggest that providing an annual lump‐sum income boost may not be a remedy for this particular issue in the short term. Of note, we found that EITC‐eligible individuals were more likely to have lower expenditures overall but higher expenditures on emergency department care, consistent with a pattern of foregoing necessary preventive care. Future studies should examine the effects of other types of interventions intended to address foregone care. For example, differences in the structure of health insurance plans may be important for low‐income individuals, as was demonstrated by the Rand Health Insurance Experiment of the 1970s.51 Although we find that EITC refund receipt did not result in differential effects by insurance status, it may be that changes to health insurance coverage itself may be more meaningful determinants of health care expenditures. Alternately, more regular and reliable income distributed throughout the year—for example, changes to the minimum wage—may be more effective than an annual lump‐sum refund. Other potential barriers to timely and appropriate care that might be investigated in future interventional work include health care access, transportation difficulties, perceived or actual racial discrimination, awareness of when to seek care, and social or cultural norms around health care utilization.52, 53, 54

Our study has several strengths. First, we used over 15 years of data from a large diverse sample of over 1 million individuals drawn from a nationally representative dataset, ensuring that we were well powered to detect small effects. These data also included detailed information on both the inputs into the EITC—that is, income and demographic characteristics—and the health outcomes of interest. We applied a quasi‐experimental DID approach, which allowed us to adjust for seasonal trends in health care spending through the use of a contemporaneous control group of non‐EITC‐eligible individuals.

Our study also has several limitations. First, self‐reported variables such as income may suffer from measurement error and result in misclassification, which could bias our results toward or away from the null. Second, as participants did not specifically report their EITC refund amount, we imputed refund size based on self‐reported demographic characteristics. Since roughly 80 percent of individuals during this time period actually received EITC refunds for which they were eligible,41 this is likely to result in misclassification, although these estimates are analogous to intent‐to‐treat estimates in an RCT. Moreover, this is an improvement upon prior studies that impute EITC eligibility solely using an individual's educational attainment.47, 55 Relatedly, MEPS does not collect information on the exact month of EITC refund receipt, so in our primary analyses we assumed that EITC‐eligible individuals received their refunds in February. This may also result in misclassification, although 60 percent of individuals are known to receive their EITC refunds during February; we also conducted sensitivity testing to expand the treatment window to also include March and April, resulting in similar findings. Of note, several other studies have employed this seasonal DID technique and found statistically significant effects using smaller samples,18, 44 suggesting that this misclassification is unlikely to be the primary cause of the null results of this study. Finally, DID analyses assume that the differences in outcomes between February and the rest of the year would be the same in treatment and control groups in the absence of the intervention, a counterfactual scenario that is fundamentally untestable.

In summary, our study is among the first to examine the effects of an income boost on health care expenditures, providing important evidence on the effects of the largest US poverty alleviation program on the health care spending of low‐income individuals. We were unable to reject the null hypothesis that there is no effect of EITC refunds on short‐term out‐of‐pocket health care spending compared with spending among noneligible individuals, suggesting that the refund is spent on other types of household expenses or that liquidity constraints are not a limiting factor for health care expenditures in this population relative to the control group. Future studies should examine whether other types of income supplementation affect health care expenditures, particular among individuals in poverty.

Supporting information

ACKNOWLEDGMENTS

Joint Acknowledgment/Disclosure Statement: This work was supported by the National Heart, Lung, and Blood Institute (grant K08HL132106 to R.H.). The funders had no role in study design, data collection and analysis, decision to publish, or preparation of the manuscript. No other disclosures.

Hamad R, Niedzwiecki MJ. The short‐term effects of the earned income tax credit on health care expenditures among US adults. Health Serv Res. 2019;54:1295–1304. 10.1111/1475-6773.13204

REFERENCES

- 1. Mielck A, Kiess R, Ovd K, Stirbu I, Kunst AE. Association between forgone care and household income among the elderly in five Western European countries – analyses based on survey data from the SHARE‐study. BMC Health Serv Res. 2009;9(1):52. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2. Newacheck PW, Hughes DC, Hung Y‐Y, Wong S, Stoddard JJ. The unmet health needs of America's children. Pediatrics. 2000;105(Suppl. 3):989‐997. [PubMed] [Google Scholar]

- 3. Centers for Disease Control . QuickStats: Delayed or forgone medical care because of cost concerns among adults aged 18–64 years, by disability and health insurance coverage status–National Health Interview Survey, United States, 2009. MMWR Morb Mortal Wkly Rep. 2010;59(44):1456. [Google Scholar]

- 4. Mojtabai R, Olfson M. Medication costs, adherence, and health outcomes among Medicare beneficiaries. Health Aff. 2003;22(4):220‐229. [DOI] [PubMed] [Google Scholar]

- 5. Sarmiento OL, Miller WC, Ford CA, et al. Routine physical examination and forgone health care among Latino adolescent immigrants in the United States. J Immigr Minor Health. 2005;7(4):305‐316. [DOI] [PubMed] [Google Scholar]

- 6. Cooper RA, Cooper MA, McGinley EL, Fan X, Rosenthal JT. Poverty, wealth, and health care utilization: a geographic assessment. J Urban Health. 2012;89(5):828‐847. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7. Hamad R, Modrek S, Cullen MR. The impact of job insecurity on healthcare utilization: findings from a panel of U.S. workers. Health Serv Res. 2015;51(3):1052‐1073. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8. Modrek S, Hamad R, Cullen MR. Psychological well‐being during the great recession: changes in mental health care utilization in an occupational cohort. Am J Public Health. 2015;105(2):304‐310. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9. U.S. Internal Revenue Service . Statistics for tax returns with EITC. 2019. https://www.eitc.irs.gov/eitc-central/statistics-for-tax-returns-with-eitc/statistics-for-tax-returns-with-eitc. Accessed June 6, 2019.

- 10. Friedman P. The earned income tax credit. Welfare Inform Netw. 2000;4(4):Issue Notes. [Google Scholar]

- 11. Nichols A, Rothstein J. The earned income tax credit In: Moffitt RA, ed. Economics of Means‐Tested Transfer Programs in the United States. Vol 1 Chicago, IL: University of Chicago Press; 2016:137‐218. [Google Scholar]

- 12. Committee on Ways and Means . Green Book. Washington, DC: U.S. House of Representatives; 2004. [Google Scholar]

- 13. Davison G, Roll SP, Taylor SH, Grinstein‐Weiss M. The state of state EITCs: an overview and their implications for low‐ and moderate‐income households In: CSD Research Brief 18–04. St. Louis, MO: Center for Social Development, Washington University in St. Louis; 2018. [Google Scholar]

- 14. Chetty R, Friedman JN, Saez E. Using differences in knowledge across neighborhoods to uncover the impacts of the EITC on earnings. Am Econ Rev. 2013;103(7):2683‐2721. [Google Scholar]

- 15. Dahl M, DeLeire T, Schwabish J. Stepping stone or dead end? The effect of the EITC on earnings growth. Natl Tax J. 2009;62(2):329‐346. [Google Scholar]

- 16. Eissa N, Liebman JB. Labor supply response to the earned income tax credit. Q J Econ. 1996;111(2):605‐637. [Google Scholar]

- 17. Cowan B, Tefft N. Education, maternal smoking, and the earned income tax credit. BE J Econ Anal Policy. 2012;12(1):Article 45. [Google Scholar]

- 18. Rehkopf DH, Strully KW, Dow WH. The short‐term impacts of earned income tax credit disbursement on health. Int J Epidemiol. 2014;43(6):1884‐1894. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19. Schmeiser MD. Expanding wallets and waistlines: the impact of family income on the BMI of women and men eligible for the earned income tax credit. Health Econ. 2009;18(11):1277‐1294. [DOI] [PubMed] [Google Scholar]

- 20. Hoynes HW, Miller DL, Simon D. Income, the earned income tax credit, and infant health. Am Econ J Econ Policy. 2015;7(1):172‐211. [Google Scholar]

- 21. Hamad R, Rehkopf DH. Poverty, pregnancy, and birth outcomes: a study of the earned income tax credit. Paediatr Perinat Epidemiol. 2015;29(5):444‐452. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 22. Hamad R, Rehkopf DH. Poverty and child development: a longitudinal study of the impact of the earned income tax credit. Am J Epidemiol. 2016;183(9):775‐784. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23. Rehkopf DH, Strully KW, Dow WH. The Effects of Anti‐Poverty Tax Policy on Child and Adolescent BMI and Obesity. Working Paper. Washington, DC: Strong Foundations, The Economic Futures of Kids and Communities, Federal Reserve Bank of San Francisco; 2017. [Google Scholar]

- 24. Averett S, Wang Y. The effects of earned income tax credit payment expansion on maternal smoking. Health Econ. 2013;22(11):1344‐1359. [DOI] [PubMed] [Google Scholar]

- 25. Barrow L, McGranahan L. The effects of the earned income credit on the seasonality of household expenditures. Natl Tax J. 2000;53(4):1211‐1244. [Google Scholar]

- 26. Romich JL, Weisner T. How families view and use the EITC: advance payment versus lump sum delivery. Natl Tax J. 2000;53(4, Part 2):1245‐1262. [Google Scholar]

- 27. Goodman‐Bacon A, McGranahan L. How do EITC recipients spend their refunds? Econ Perspect. 2008;32(2):17‐32. [Google Scholar]

- 28. Baughman RA. Evaluating the impact of the earned income tax credit on health insurance coverage. Natl Tax J. 2005;58(4):665‐684. [Google Scholar]

- 29. Baughman RA, Duchovny N. State earned income tax credits and the production of child health: insurance coverage, utilization, and health status. Natl Tax J. 2016;69(1):103. [Google Scholar]

- 30. DeLeire T, Levine JA, Levy H. Is welfare reform responsible for low‐skilled women's declining health insurance coverage in the 1990s? J Human Resour. 1990s;41(3):495‐528. [Google Scholar]

- 31. Bitler MP, Gelbach JB, Hoynes HW. Welfare reform and health. J Human Resour. 2005;40(2):309‐334. [Google Scholar]

- 32. Danziger S, Corcoran M, Danziger S, Heflin CM. Work, income, and material hardship after welfare reform. J Consumer Affairs. 2000;34(1):6‐30. [Google Scholar]

- 33. Narain K, Bitler M, Ponce N, Kominski G, Ettner S. The impact of welfare reform on the health insurance coverage, utilization and health of low education single mothers. Soc Sci Med. 2017;180:28‐35. [DOI] [PubMed] [Google Scholar]

- 34. Cawley J, Schroeder M, Simon KI. How did welfare reform affect the health insurance coverage of women and children? Health Serv Res. 2006;41(2):486‐506. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 35. Gross T, Tobacman J. Dangerous liquidity and the demand for health care evidence from the 2008 stimulus payments. J Human Resour. 2014;49(2):424‐445. [Google Scholar]

- 36. Feenberg D, Coutts E. An introduction to the TAXSIM model. J Policy Anal Manag. 1993;12(1):189‐194. [Google Scholar]

- 37. Meyer BD, Mok WK, Sullivan JX. Household surveys in crisis. J Econ Perspect. 2015;29(4):199‐226. [Google Scholar]

- 38. Marquis KH, Moore JC. Measurement errors in SIPP program reports. Washington, DC: U.S. Census Bureau; 2010. [Google Scholar]

- 39. Courtemanche CJ, Denteh A, Tchernis R. Estimating the Associations between SNAP and Food Insecurity, Obesity, and Food Purchases with Imperfect Administrative Measures of Participation. Working Paper 24412. Cambridge, MA: National Bureau of Economic Research; 2018. [Google Scholar]

- 40. Meyer BD, Mittag N. Using linked survey and administrative data to better measure income: implications for poverty, program effectiveness and holes in the safety net. Am Econ J Appl Econ. 2019;11(2):176‐204. [Google Scholar]

- 41. Hotz VJ, Scholz JK. The earned income tax credit In: Moffitt RA, ed. Means‐Tested Transfer Programs in the United States. Chicago, IL: University of Chicago Press; 2003:141‐197. [Google Scholar]

- 42. Dahl GB, Lochner L. The impact of family income on child achievement: evidence from the earned income tax credit. Am Econ Rev. 2012;102(5):1927‐1956. [Google Scholar]

- 43. Eissa N, Hoynes HW. Taxes and the labor market participation of married couples: the earned income tax credit. J Pub Econ. 2004;88(9‐10):1931‐1958. [Google Scholar]

- 44. Hamad R, Collin DF, Rehkopf DH. Estimating the short‐term effects of the earned income tax credit on child health. Am J Epidemiol. 2018;187(12):2633‐2641. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 45. LaLumia S. The EITC, tax refunds, and unemployment spells. Am Econ J Econ Policy. 2013;5(2):188‐221. [Google Scholar]

- 46. Dimick JB, Ryan AM. Methods for evaluating changes in health care policy: the difference‐in‐differences approach. JAMA. 2014;312(22):2401‐2402. [DOI] [PubMed] [Google Scholar]

- 47. Evans WN, Garthwaite CL. Giving mom a break: the impact of higher EITC payments on maternal health. Am Econ J Economic Policy. 2014;6(2):258‐290. [Google Scholar]

- 48. Shaefer HL, Song X, Williams Shanks TR. Do single mothers in the United States use the earned income tax credit to reduce unsecured debt? Rev Econ Household. 2013;11(4):659‐680. [Google Scholar]

- 49. Mendenhall R, Edin K, Crowley S, et al. The role of earned income tax credit in the budgets of low‐income households. Soc Serv Rev. 2012;86(3):367‐400. [Google Scholar]

- 50. Farrell D, Greig F, Hamoudi A. Deferred Care: How Tax Refunds Enable Healthcare Spending. Washington, DC: J.P. Morgan Chase Institute; 2018. [Google Scholar]

- 51. Aron‐Dine A, Einav L, Finkelstein A. The RAND health insurance experiment, three decades later. J Econ Perspect. 2013;27(1):197‐222. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 52. Ford CA, Bearman PS, Moody J. Foregone health care among adolescents. JAMA. 1999;282(23):2227‐2234. [DOI] [PubMed] [Google Scholar]

- 53. Documét PI, Sharma RK. Latinos' health care access: financial and cultural barriers. J Immigr Health. 2004;6(1):5‐13. [DOI] [PubMed] [Google Scholar]

- 54. Allen EM, Call KT, Beebe TJ, McAlpine DD, Johnson PJ. Barriers to care and health care utilization among the publicly insured. Med Care. 2017;55(3):207‐214. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 55. Markowitz S, Komro KA, Livingston MD, Lenhart O, Wagenaar AC. Effects of state‐level earned income tax credit laws in the U.S. on maternal health behaviors and infant health outcomes. Soc Sci Med. 2017;194(Suppl. C):67‐75. [DOI] [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials