Abstract

Aims

To perform an economic evaluation of a work‐place smoking cessation group training programme with incentives compared with a training programme without incentives.

Design

A trial‐based cost‐effectiveness analysis (CEA) and cost–utility analysis (CUA) from a societal perspective and an employer's perspective.

Setting

Sixty‐one companies in the Netherlands.

Participants

A total of 604 tobacco‐smoking employees.

Intervention and comparator

A 7‐week work‐place smoking cessation group training programme. The intervention group earned gift vouchers of €350 for 12 months’ continuous abstinence. The comparator group received no incentives.

Measurements

Online questionnaires were administered to assess quality of life (EQ‐5D‐5 L) and resource use during the 14‐month follow‐up period (2‐month training period plus 12‐month abstinence period). For the CEA the primary outcome measure was carbon monoxide (CO)‐validated continuous abstinence; for the CUA the primary outcome was quality‐adjusted life years (QALY). Bootstrapping and sensitivity analyses were performed to account for uncertainty. Incremental cost‐effectiveness ratio (ICER) tables were used to determine cost‐effectiveness from a life‐time perspective.

Findings

Of the participants in the intervention group, 41.1% had quit smoking compared with 26.4% in the control group. From a societal perspective with a 14‐month follow‐up period, the ICER per quitter for an intervention with financial incentives compared with no incentives was €11 546. From an employer's perspective, the ICER was €5686. There was no significant difference in QALYs between the intervention and control group within the 14‐month follow‐up period. The intervention was dominated by the comparator in the primary analysis at a threshold of €20 000 per QALY. In the sensitivity analysis, these results were uncertain. A life‐time perspective showed an ICER of €1249 (95% confidence interval = €850–2387) per QALY.

Conclusions

Financial incentives may be cost‐effective in increasing quitting smoking, particularly from a life‐time perspective.

Keywords: Cost‐effectiveness, cost–utility, economic evaluation, employees, financial incentives, QALY, RCT, smoking cessation, work‐place

Introduction

Smoking is the most preventable cause of illness and premature death, and smoking‐related illnesses lead to large health‐care costs and loss of productivity 1, 2, 3, 4, 5, 6. A meta‐analysis focusing on working populations found that smoking was associated with a 31% increase in risk of absenteeism and 2.9 more sickness absence days per year compared to non‐smoking 7. While many different types of intervention have been used to decrease smoking in society 8, 9, 10, 11, stimulating individual smokers to quit still proves difficult, especially among smokers from lower socio‐economic groups 12, 13, 14.

Smoking cessation interventions at the work‐place have been shown to be an effective approach to reach smokers and stimulate quitting smoking 11. In a work‐place setting, successful interventions are group smoking cessation counselling and financial incentives for quit success 11, 15, 16, 17. Stimulating smoking cessation at the work‐place has benefits for both the employee and the employer. For the employee, apart from health benefits, smoking cessation counselling at the work‐place is convenient, does not require a personal financial investment and offers peer support from colleagues 11, 18, 19, 20. For employers, investing in smoking cessation leads to healthier employees and can reduce costs that are associated with smoking, such as absenteeism 4, 21 and reduced performance 22, 23, which were estimated to be $5816 per smoker per year 6.

Inspired by these results, we designed a cluster‐randomized controlled trial (RCT) to investigate the effectiveness of financial incentives for smoking cessation, which was conducted within Dutch companies. Participants of this trial were adult employees who smoked, and who voluntarily signed up for a smoking cessation group training programme at the work‐place. Employees in companies who were randomized into the intervention condition additionally earned financial incentives totalling €350 if they quit smoking for 12 months 24. The results of this trial showed that significantly more participants had quit smoking in the intervention group with incentives (41.1 versus 26.4%, P < 0.001) than in the control group with the cessation programme alone 25.

Apart from establishing the effectiveness of financial incentives for smoking cessation at the work‐place, it is important to evaluate the broader costs and benefits of such an intervention and to assess its cost‐effectiveness from a societal perspective, as well as from an employer's viewpoint. An economic evaluation of the costs and benefits of using financial incentives at the work‐place to reduce smoking can improve the acceptability of incentives to society 26, and could convince employers to offer a smoking cessation programme with incentives to their employees 27.

However, evidence on the cost‐effectiveness of incentives for smoking cessation is sparse. To our knowledge, no study has yet performed a full economic evaluation of financial incentives alongside a trial with a population of employees who smoke. Additionally, to our knowledge, no economic evaluation from an employer's viewpoint has been performed in this research field. One study that involved financial incentives worth £400 for smoking cessation during pregnancy found an incremental cost per quitter of £1127 (US $1716) compared to routine care, but measured only costs directly related to the smoking cessation treatment and the incentives, but no other health‐care consumption, nor did the study assess quality of life during the trial 28. However, the benefits of quitting smoking expressed in QALYs were estimated using a Markov model, and the authors estimated incremental costs of £482 (€541) per QALY 28. Another study that performed a cost–benefit analysis for a large cohort of Medicaid enrollees found that providing quitline callers with modest financial incentives was a cost‐effective method to increase cessation rates over a 10‐year horizon with a benefit–cost ratio of 1.30 29.

Research has shown that health improvements among employees who quit smoking can substantially reduce employers’ costs related to productivity losses and absenteeism, and can decrease societal costs as a whole 6, 21, 30. When financial incentives are added to a smoking cessation programme, they will inevitably increase the costs of the intervention at first. However, if adding a reward to a smoking cessation programme increases the number of quitters, the cost‐effectiveness of the programme could be improved, making financial incentives a short‐term investment that pays off in the future.

The aim of the present study was to assess from both a societal and an employer's perspective the cost‐effectiveness (CEA) and cost–utility (CUA) of a work‐place smoking cessation group training programme with incentives compared to a training programme without incentives in Dutch employees who smoke. It is hypothesized that providing financial incentives for quit success is associated with improved effects and health‐related quality of life and decreased costs.

Methods

Reporting guidelines

This study follows the Consolidated Health Economic Evaluation Reporting Standards (CHEERS) Statement. 31

Design

A trial‐based economic evaluation was performed alongside a cluster RCT, which has previously been described in detail in another publication 24. The RCT was conducted within 61 companies in the Netherlands. Employees in both the intervention group and control groups participated in a smoking cessation training organized at the work‐place, provided by the Dutch company SineFuma. SineFuma's smoking cessation programme is registered in the Dutch Stop Smoking Quality Register for proven effective interventions. The training consisted of seven sessions of 90 minutes each, distributed over a period of 2 months. As part of the smoking cessation training, participants were informed about smoking cessation medication and encouraged to consider using medication during their quit attempt. Employees were recruited by the companies themselves. The aim of the RCT was to organize a single group training within each company, and it was not intended to reach all smokers within a company. Participants in the intervention group additionally earned gift vouchers with a total amount of €350 if they quit smoking. Participants received a digital voucher via e‐mail, which was sent by a research assistant if they were abstinent from smoking directly after finishing the smoking cessation programme (€50), after 3 months (€50) and after 6 months (€50); the last voucher of €200 was earned 12 months after finishing the programme. The main outcome was successfully quitting smoking, defined as CO‐validated and continuous smoking abstinence, from the moment that the participant had finished the training programme up to 12 months later. Companies and participants were enrolled between March 2016 and March 2017.

Participants

All participants who had participated in the RCT were included into the current study. Participants were male and female employees who were current tobacco smokers at the start of the trial, aged at least 18 years and who did not have a life‐threatening disease at the start of the trial.

Identification of costs

The relevant costs that were identified were: intervention costs, health‐care costs, patient and family costs and costs in other sectors 32, 33. Intervention costs consisted of costs of the smoking cessation group training, costs of the incentives and time costs. Health‐care costs use included visits to health‐care providers, costs of medical treatments, costs of overnight stay in hospitals, costs of home care and costs of (smoking cessation) medications. Participant and family costs included travel costs for visits to health‐care services and cost representing time spent by family members providing informal care (such as domestic work or taking care of the children). Costs in other sectors consisted of costs related to productivity, and will be referred to as ‘productivity costs’ in the remainder of this paper. Productivity costs included absenteeism from work, costs related to presenteeism and costs for work breaks.

Measurement and valuation of costs

To measure all relevant resource use costs, a questionnaire was designed for this study based on existing questionnaires 34, 35, 36, 37. Participants were asked to report the data from their resource use questionnaire relating to the previous 3 months at baseline and at 2, 5, 8 and 14 months follow‐up, with a recall period of 2, 3, 3 and 6 months, respectively. Online questionnaires were sent by e‐mail, and if participants preferred a paper version of the questionnaire it was sent to them by post. Multiple e‐mail reminders were sent, and participants were called by telephone to remind them to complete the questionnaire. Participants were awarded a gift voucher of €25 if they had completed the final questionnaire. The valuation of costs was based on Dutch guidelines 32, 38. Cost prices were expressed in 2017 euros, based on the consumer price index (http://www.statline.cbs.nl). Due to the short time horizon of 14 months, costs were not discounted. Health‐care costs were estimated using a bottom‐up (or micro‐costing) approach. A detailed description of the cost valuation is presented in Supporting information, File S1.

Effects

Smoking abstinence was measured by self‐report and validated using expired air carbon monoxide (CO) measurement. The research assistant visited the participants who claimed to be abstinent from smoking at the work‐place to perform the CO measurement, or offered to travel to an alternative location that was suggested by the participant. If CO measurements were higher than the cut‐off point of 9 parts per million (p.p.m.), or if CO measurement could not be performed, participants were considered to be smokers (Russell's Standard) 39. The primary outcome for the CEA was cost per CO‐validated continuously abstinent participant (cost per successful quitter). The primary outcome of the CUA was cost per quality‐adjusted life year (QALYs). The utility value derived from the standard health‐related quality of life questionnaire, EuroQol‐5D‐5 L 40, using Dutch tariff 41, was used to compute QALYs. The utilities at the various time‐points were used to compute QALYs over the 14‐month time horizon by means of the area under the curve method, where the utility of a particular health state is multiplied by the time in this state 33, 42. Costs (the use of resources) were measured continuously; outcomes for the economic evaluation study were measured at baseline (T0), directly after finishing the smoking cessation training programme (2 months after baseline, T1) and 5 (T2), 8 (T3) and 14 months (T4) after baseline.

Statistical analyses

The analyses of the effect measure continuous abstinence from smoking were performed according to an intention‐to‐treat (ITT) protocol, where all withdrawals were considered to be smokers. For the cost analysis, only participants who provided cost data for at least one follow‐up measurement point (T1–T4) were included 43. Data were analyzed using IBM SPSS Statistics version 25 and Microsoft Excel 2010. Differences between participants lost to follow‐up were tested using independent t‐tests and χ2 tests. Two‐sided P‐values ≤ 0.05 were considered statistically significant. Individual mean imputation was used to impute missing cost data 43. Mean costs and 95% confidence intervals (CI), as well as baseline differences in costs and utilities between the intervention and control group, were assessed using bootstrapping (1000 replications). The incremental cost‐effectiveness ratio (ICER) was calculated by dividing the incremental costs by the incremental effects/QALYs. Bootstrap simulations (5000 replications) were conducted in order to quantify the uncertainty around the ICER 44. The bootstrapped cost‐effectiveness ratios were subsequently plotted on a cost‐effectiveness plane, which is divided into four quadrants by a vertical line that reflects the difference in costs and the horizontal line reflects the difference in effectiveness. The choice of treatment depends upon the willingness to pay (WTP), which is the maximum amount of money that society is prepared to pay for a gain in effectiveness. Based on a report of the Dutch National Health Institute, a WTP of €20 000 for an additional QALY was used in this study 45. There are no guidelines on the WTP for an additional quitter. The bootstrapped ICERs were also depicted in a cost‐effectiveness acceptability curve (CEAC) showing the probability that the use of incentives for smoking cessation in a business setting is cost‐effective over a range of ceiling ratios. Additionally, to demonstrate the robustness of the base case findings, sensitivity analyses were performed. A sensitivity analysis was performed where respondents with extremely high total costs (based on the 95th percentile) were excluded, a complete case analysis was performed where only participants who had completed all follow‐up questionnaires were included, an analysis from a societal perspective was performed where self‐reported smoking abstinence was used as outcome measure instead of CO‐validated smoking abstinence and an analysis was performed where only intervention costs were included.

Ethics approval, registration and data access

The current study was pre‐registered in the Netherlands Trial Register (NL5537) The study protocol was approved by the Medical Research Ethics Committee METC Z in Heerlen, the Netherlands (no. 16‐N‐13). Data access requests can be made to the corresponding author. The full study protocol can be accessed via Van den Brand et al. 24.

Life‐time perspective analysis

To provide an additional estimation of the cost‐effectiveness of the current intervention from a life‐time perspective we used the current intervention's cost and effect data as input, and used standardized tables from Stapleton & West to determine the ICER 46. The tables offer estimates of life years gained by quitting smoking attributable to interventions with different effect sizes. The life years gained are adjusted for future life‐time cessation (proportion of smokers who are expected to quit smoking in their life‐time without an intervention: 2.5% per annum) and are adjusted for relapse after the final follow‐up (12‐month follow‐up). The ICER was corrected for the proportion of study participants within the age groups < 35, 35–54 and > 54 years. A discount rate of 3.5% was used. The results in life years can also be interpreted as QALYs, where the years are weighted according to the quality of life that is experienced during these years 46. Because there are no verified utility weights for ex‐smokers and smokers for the Dutch population, we followed the recommendations of Stapleton et al. and assumed that 1 life year was equal to 1 QALY 46. We contacted the authors 46 and they checked our calculations.

Results

Loss to follow‐up

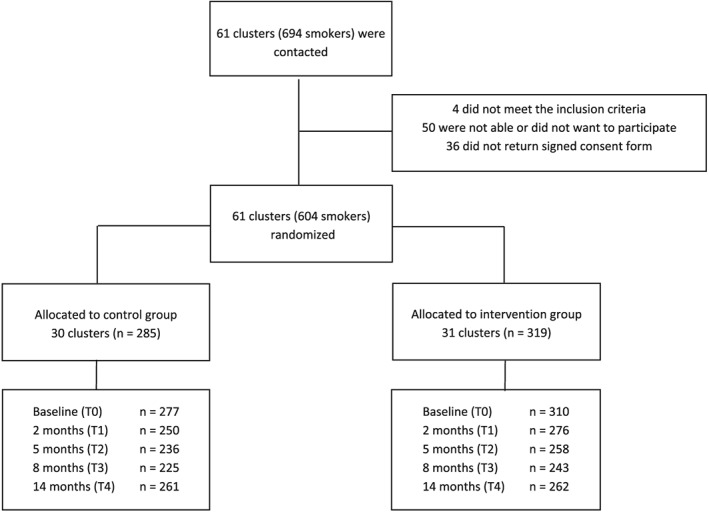

All 604 employees within 61 companies who had participated in the RCT were included in the current study (Fig. 1); 406 participants (67%) completed all five cost questionnaires, including baseline measurement (T0–T4); 41 participants (7%) did not provide cost data in any of the follow‐up questionnaires (T1–T4). Within these 41 participants, there were 10 individuals from whom cost data of follow‐up questionnaires were missing because they completed a shortened version of the questionnaire. After imputing missing values, cost data were available for 563 participants (93%). Validated smoking cessation data were available for 603 employees; one employee was excluded from the analysis due to unavoidable loss to follow‐up according to Russell's Standard 39. The participants who did not provide any cost data were more likely to be in the intervention group (9.4 versus 3.9%, P = 0.007), had a higher mean Fagerström score (5.5 versus 4.3, P > 0.001), had on average more pack years (mean 29.2 versus 22.1, P = 0.046), were more often lower‐educated (45.7 versus 26.3%, P = 0.037) and more often had a lower income (66.7 versus 31.5%, P < 0.001), but did not differ significantly in age or sex.

Figure 1.

Flow‐diagram of the study showing number of participants (n) who provided cost data at each measuring point

Participant characteristics

Participant characteristics and mean costs 3 months prior to baseline are presented in Table 1. There were no baseline differences between groups for total overall costs. Total health‐care costs were higher in the control group (P = 0.03); there were no differences between groups for patient and family costs or productivity costs.

Table 1.

Baseline participant characteristics of control group and intervention group and health‐care costs and absenteeism costs of 3 months prior to baseline (n = 604)

| Variable | Intervention group (n = 319) | Control group (n = 285) |

|---|---|---|

| Age, mean (SD) | 43.9 (10.4) | 46.6 (9.7) |

| Gender, n (%) | ||

| Women | 102 (32.0) | 121 (42.5) |

| Men | 217 (68.0) | 164 (57.5) |

| Educational level, n (%) | ||

| Low | 97 (30.4) | 62 (21.8) |

| Moderate | 136 (42.6) | 119 (41.8) |

| High | 75 (23.5) | 90 (31.6) |

| Missing | 11 (3.4) | 14 (4.9) |

| Income level, n (%) | ||

| Low | 111 (34.8) | 68 (23.9) |

| Moderate | 91 (28.5) | 84 (29.5) |

| High | 76 (23.8) | 105 (36.8) |

| Missing | 41 (12.9) | 28 (12.5) |

| FTNDa (range = 0–10), mean (SD) | 4.4 (1.9) | 4.5 (2.0) |

| Pack years, mean (SD) | 21.6 (13.2) | 23.5 (13.0) |

| QALYb, mean (SD) | 0.90 (0.13) | 0.91 (0.13) |

| Health‐care costs (€), mean (SD) | ||

| General practitioner | 21 (35) | 22 (41) |

| Occupational doctor | 10 (43) | 11 (42) |

| Hospital | 76 (334) | 134 (624) |

| Other care | 54 (103) | 72 (148) |

| Home care | 0 (4) | 4 (63) |

| Medication | 21 (81) | 73 (528) |

| Smoking cessation medication | 1 (13) | 1 (6) |

| Smoking cessation coach | 7 (19) | 5 (17) |

| Total health‐care costs | 189 (399) | 318 (912) |

| Participant and family costs | ||

| Travel and parking costs | 13 (15) | 15 (21) |

| Informal care | 115 (475) | 61 (236) |

| Total participant and family costs | 127 (477) | 76 (246) |

| Productivity costs (€), mean (SD) | ||

| Absenteeism | 456 (1320) | 364 (1061) |

| Presenteeism | 289 (1198) | 210 (674) |

| Work breaks | 1655 (848) | 1640 (913) |

| Total productivity costs | 2356 (2137) | 2165 (1647) |

| Total costs | 2623 (2534) | 2551 (2096) |

Fagerström Test for Nicotine Dependence; bquality‐adjusted life years. SD = standard deviation.

Costs and effects

Mean 14‐month resource use is displayed in Table 2. The largest costs for both groups were those related to productivity in general, and within this subcategory the costs of work breaks were the highest. Mean total health‐care costs, participant and family costs and productivity costs did not differ significantly between intervention and control groups. The cost of the subcategory absenteeism was significantly higher in the intervention group than in the control group. The effect analyses showed that significantly more participants quit smoking in the intervention group (131 of 319 = 41.1%) than in the control group (75 of 284 = 26.4%). Of the 206 participants who were validated abstinent from smoking, 205 (99.5%) had a CO score < 6 p.p.m. at the final follow‐up measurement (the single remaining participant had a CO score of 9). The 14‐month QALY scores were not significantly different between the intervention and the control group. Comparing 14‐month QALY scores between participants who were continuously abstinent [QALY = 1.071, standard deviation (SD) = 0.125] to unsuccessful quitters (QALY = 1.057, SD = 0.153) showed no significant difference (t (560) = 1.14, P = 0.256). Total volumes and costs during the entire 14‐month follow‐up period are presented in Supporting information, Table S1.

Table 2.

Mean 14‐month costs of intervention and control group (1000 bootstrap replications)

| Cost type | Costs per group (€), mean (SD) | Difference (95% CI) | |

|---|---|---|---|

| Societal perspective | Intervention group | Control group | Intervention–control group |

| Intervention costs (n = 319/285) | |||

| Incentives | 189 (9) | – | 189 (171 to 206) |

| Smoking cessation group training | 421 | 421 | 0 |

| Time attending training (within working hours) | 389 | 389 | 0 |

| Total intervention costs | 998 (9) | 809 | 189 (173 to 205) |

| Health‐care costs (n = 289/274) | |||

| General practitioner | 103 (8) | 89 (7) | 14 (−5 to 36) |

| Occupational doctor | 95 (15) | 49 (9) | 45 (12 to 78) |

| Hospitala | 919 (200) | 600 (93) | 319 (−67 to 781) |

| Other careb | 353 (40) | 282 (26) | 71 (−19 to 166) |

| Home care | 175 (144) | 15 (13) | 160 (−26 to 474) |

| Medication | 158 (61) | 268 (101) | −110 (−381 to 97) |

| Smoking cessation medication | 76 (9) | 50 (10) | 26 (−2 to 52) |

| Smoking cessation coach | 59 (6) | 72 (6) | −13 (−32 to 4) |

| Total health‐care costs | 1942 (318) | 1423 (167) | 519 (−122 to 1274) |

| Participant and family costs (n = 289/274) | |||

| Travel and parking costs | 62 (5) | 58 (4) | 5 (−7 to 17) |

| Informal carec | 761 (122) | 484 (137) | 278 (−119 to 644) |

| Total patient and family costs | 833 (122) | 557(141) | 276 (−103 to 615) |

| Productivity costs (n = 289/274) | |||

| Absenteeism | 3436 (370) | 2458 (292) | 978 (52 to 1932) |

| Presenteeism | 1486 (207) | 1292 (211) | 194 (−387 to 823) |

| Work breaks | 7135 (195) | 7318 (227) | −183 (−747 to 403) |

| Total productivity costs | 12 079 (529) | 11 091 (486) | 988 (−427 to 2417) |

| Employer's perspective | Intervention group | Control group | Intervention–control group |

|---|---|---|---|

| Intervention costs (n = 319/285) | |||

| Incentives | 189 (9) | – | 189 (171 to 206) |

| Smoking cessation group training | 421 | 421 | 0 |

| Time attending training (within working hours) | 389 | 389 | 0 |

| Total intervention costs | 998 (9) | 809 | 189 (173 to 205) |

| Productivity costs (n = 289/274) | |||

| Absenteeism | 3436 (370) | 2458 (292) | 978 (52 to 1932) |

| Presenteeism | 1486 (207) | 1292 (211) | 194 (−387 to 823) |

| Work breaks | 7135 (195) | 7318 (227) | −183 (−747 to 403) |

| Total productivity costs | 12 079 (529) | 11 091 (486) | 988 (−427 to 2417) |

This includes the costs of: visits to a medical specialist, day care treatment, days hospitalized, visits to the emergency department and ambulance rides.

This includes the costs of: visits to a medical assistant, occupational therapist, dietitian, speech therapist, physical therapist, psychologist, skin therapist, dentist, dental hygienist, pedicure, social worker and alternative medicine.

Informal care includes unpaid work such as domestic work; for example, taking care of the children, grocery shopping or volunteer work. CI = confidence interval; SD = standard deviation.

Cost‐effectiveness analyses at 14 months

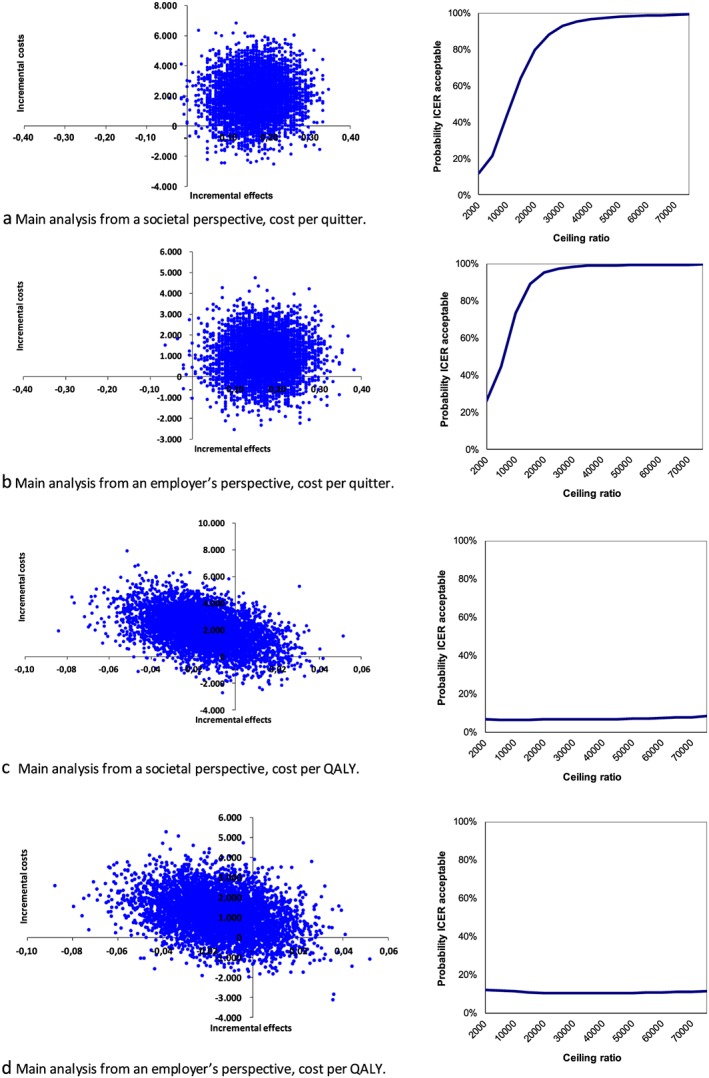

The intervention condition with incentives resulted in higher costs and in higher effects compared to the control group (Table 3). The incremental costs or costs for an additional quitter from a societal perspective were €11 546. The cost‐effectiveness plane for the main analysis from the societal perspective shows that most (92%) of the bootstrapping results lie in the north‐east quadrant (Fig. 2a). The corresponding cost‐effectiveness acceptability curve shows that the probability that the intervention is cost‐effective is 80% (at €20 000 per abstinent smoker) up to 97% (at €40 000 per abstinent smoker).

Table 3.

Incremental costs per quitter and per QALY gained for the incentive versus control group, societal perspectives

| Total costs | Total effects | |||||||

|---|---|---|---|---|---|---|---|---|

| Analysisd | Effect measure | Intervention group | Control group | Δ costs | Intervention group | Control group | Δ effects | ICERa |

| Cost‐effectivenesse | Quit smokinga | €15 869 | €13 928 | €1942 | 0.44 | 0.27 | 0.17 | €11 546 |

| Cost–‐utilityg | QALYb | €15 869 | €13 889 | €1980 | 1.055 | 1.070 | −0.02 | Dominatedc |

Calculated based on the formula for ICER or ICUR, i.e. (Ci – Cc) / (Ei – Ec).

Coded as 1 = abstinent and 0 = not abstinent.

Based on the Dutch tariff of the EQ‐5D‐5 L.

ICUR = €128 280.

Only participants were included in the cost‐effectiveness analyses who completed at least one cost questionnaire, therefore the data in this table differ from the RCT data.

Intervention group n = 289, control group n = 273. gIntervention group n = 289, control group n = 274. QALY = quality‐adjusted life years; RCT = randomized controlled trial; ICUR = incremental cost–utility ratio; ICER = incremental cost‐effectiveness ratio.

Figure 2.

Cost‐effectiveness planes (left) and corresponding cost‐effectiveness acceptability curves (right) for the main analyses from societal and an employer's perspectives for the outcomes quitting smoking and quality of life. QALY = quality of life years [Colour figure can be viewed at http://wileyonlinelibrary.com]

The sensitivity analysis from a societal perspective where participants with the highest costs (above the 95th percentile) were removed showed an ICER of €3432, and the complete case analysis showed an ICER of €17 610. The CEA from an employer's perspective showed ICERs varying between €1124 and €12 117 (see Table 4 for all sensitivity analyses). The bootstrapped results are mainly presented in the north‐east quadrant of the cost‐effectiveness plane (Fig. 2b). This indicates that the intervention was more effective although more costly, but also reveals that there was large uncertainty surrounding the ICER.

Table 4.

Results from cost‐effectiveness analyses for the outcome quitting smoking for intervention and control group based on 5000 bootstrap replications: ICERS and distributions on the cost‐effectiveness plane

| Sensitivity analysesa | ICERb | North East | South East (dominant) | South west | North West (inferior) |

|---|---|---|---|---|---|

| Society main analysis | €11 546 | 0.92 | 0.08 | 0.00 | 0.00 |

| Society 95th percentile | €3432 | 0.78 | 0.22 | 0.00 | 0.00 |

| Society complete case | €17 610 | 1.00 | 0.00 | 0.00 | 0.00 |

| Society self‐reported abstinence | €12 826 | 0.93 | 0.07 | 0.00 | 0.00 |

| Employer main analysis | €5686 | 0.83 | 0.16 | 0.00 | 0.00 |

| Employer 95th percentile | €2638 | 0.73 | 0.26 | 0.00 | 0.00 |

| Employer complete case | €12 117 | 0.99 | 0.01 | 0.00 | 0.00 |

| Intervention costs only | €1124 | 1.00 | 0.00 | 0.00 | 0.00 |

Society = analysis based on a societal perspective where all costs are included; employer = analysis based on an employer's perspective where only intervention costs and productivity costs are included.

Calculated based on the formula ICER = (Ci – Cc) / (Ei – Ec). ICER = incremental cost‐effectiveness ratio.

Cost–utility analyses at 14 months

Mean QALY scores were comparable between intervention and control group (1.05 versus 1.07, P = 0.205), while the costs were higher in the intervention group from both societal and the employer's perspectives (Table 3). In the study, 172 of 563 participants (31%) reported the maximum score of QALYs during the entire 14‐month period (not shown in Table 3). The cost‐effectiveness planes of the main and sensitivity analyses show that the bootstrapped replications were distributed around the origin, and therefore no effect for QALYs could be detected (Fig. 2c,d). The ICUR from the main analysis from a societal perspective was €128 280 and the ICUR from an employer's perspective was €76 810. With a ceiling ratio of €20 000 per QALY, this means that the intervention was dominated by the control condition for both societal and the employer's perspectives.

The sensitivity analyses showed that the ICURs from a societal perspective varied between €41 217 and €211 411; the ICURS from an employer's perspective varied between € 12 249 and €145 921 (not shown in Table 3).

Cost‐effectiveness estimates from a life‐time perspective

The estimation of costs from a life‐time perspective was based on the ICER tables of Stapleton & West 46, using an incremental intervention cost of €189, an incremental cessation percentage of 17.0 and a discount rate of 3.5%. Adjusting the results for the proportion of participants within the age categories < 35 (18.0%), 35–54 (61.8%) and > 54 years (20.2%) showed an incremental cost per (quality‐adjusted) life year of €1249 (95% CI = €850–2387). A more detailed overview of the calculations is presented in Supporting information, File S2.

Discussion

In the current study a cost‐effectiveness and cost–utility analysis were performed alongside a randomized controlled trial involving financial incentives for smoking cessation. From a societal perspective, the results of the main cost‐effectiveness analyses using a 14‐month follow‐up period showed that the intervention condition with incentives is cost‐effective if society is willing to pay €11 546 for an additional quitter or if the employer is willing to pay €5686 per quitter. The cost‐effectiveness acceptability curves demonstrate that provided that the ceiling ratio is high enough (approximately €20 000), there is a high probability that the intervention will be cost‐effective.

The cost–utility analyses did not find an improvement in QALYs within the 14‐month follow‐up period. Given a WTP of €20 000 per QALY, the intervention condition was dominated by the control condition from both societal and the employer's perspectives. The corresponding cost‐effectiveness acceptability curves demonstrated that, within the trial's follow‐up period, the probability that the intervention was cost‐effective was less than 10% at the €20 000 ceiling ratio. The estimates from a life‐time perspective, where ICER tables were used with input from the trial's cost and effect data, showed an incremental cost per QALY of €1249. This amount is far below the WTP threshold of €20 000 per QALY 45.

The current study is the first full economic evaluation, to our knowledge, of a trial with incentives for smoking cessation at the work‐place. Therefore, results cannot be compared to previous work. Because there is no accepted monetary cut‐off point for smoking abstinence, it is difficult to conclude when a smoking cessation intervention is cost‐effective. A study with pregnant women found incremental costs per additional quitter of £1127 (€1265) 28 and three internet‐based smoking cessation interventions conducted in the Netherlands showed ICERs between €1500 and €50 400 (amounts uncorrected for inflation and time preferences) 47, 48, 49. From the perspective of an employer, WTP for incentives for smoking cessation will form an important part, depending on whether or not it eventually saves costs. In a study conducted in the United States 6, the annual excess cost of an employee who smokes was estimated to be $5816 (€5141, uncorrected amount). Although costs in the Netherlands may differ, and this amount needs to be interpreted as a general indication, it shows that an employer can benefit within a relatively short period of time by offering incentives, and that it therefore may be a good investment.

Estimation of the incremental costs per life year, which we calculated using ICER tables that were developed to provide estimates of cost‐effectiveness from a life‐time perspective 46, showed an ICER of €1249. This result gives an indication that financial incentives may be a very cost‐effective intervention from a long‐term perspective.

Contrary to our hypothesis, we could not detect an improvement in quality of life within the 14‐month follow‐up period of the trial. An explanation for the lack of improvement of QALYs in the intervention group may be the withdrawal symptoms 50 and anhedonia 51 associated with smoking cessation, which would have been more prevalent in the intervention group with more successful quitters. Additionally, the time horizon of 14 months in the current trial may be too short to detect long‐term improvements in health‐related quality of life, as previous research found higher quality of life scores in smokers who had quit for 1–3 years and longer compared to current smokers 52, 53, 54. Of course, although quitting smoking can lead to short‐term health improvements, such as a decrease in coughing and shortness of breath 55, the time‐frame of this study was too short to fully assess the most important health benefits of quitting smoking; namely, the reduced risk of life‐threatening disease and mortality 2. In the pregnancy study by Boyd et al. 28, the life‐time benefits of quitting smoking expressed in QALYs were estimated using modelling techniques to estimate long‐term cost‐effectiveness and cost–utility, and based on these results concluded that financial incentives were a cost‐effective method to stimulate smoking cessation.

As may be expected from a general population of healthy employees 41, the QALY scores in both groups were extremely high, with an average baseline score of 0.90 and almost one‐third of participants reporting the maximum utility score in the follow‐up period. Therefore, there may have been a ceiling effect in a large proportion of the study population which prevented us from finding improvements in QALY scores 56. As was suggested in previous research, the Euroqol‐5D‐5 L may not have the discriminative power to detect changes in a healthy population 57. Changes in health‐related quality of life have been detected within 1 year in studies using alternative measures such as positive affect, craving and frequency of stressful events 54, 58. Therefore, a measuring instrument more specific to healthy employees should be developed that is sensitive enough to assess changes in health‐related quality of life within the relatively short follow‐up time of trial‐based economic evaluation studies.

Strengths and limitations

To the best of our knowledge, this is the first study evaluating the cost‐effectiveness and cost–utility of incentives for success in quitting in combination with a smoking cessation programme at the work‐place. A strength of this trial‐based economic evaluation is that there is a direct link between the cost and effect data because these were measured within the same study population. Additionally, this study measured a broad array of health‐care costs, and included productivity losses and patient and family costs. The economic evaluation was performed from both societal and the employer's perspectives, which increases the relevance and applicability of the results. Another strength of this study is that the outcome smoking abstinence was not based merely on self‐report, but was biochemically validated by an independent research assistant. The current study also has some limitations. The follow‐up period of 14 months may have been too short to measure important health benefits related to smoking cessation, which should be addressed in future studies. Nevertheless, the cost‐effectiveness estimates from a life‐time perspective based on ICER tables 46 provide an indication that financial incentives may be a very cost‐effective intervention in the long term. However, a limitation of the ICER tables is that they only consider the costs of the intervention and not costs and benefits from a broader perspective, such as employer's or societal perspectives 46. Another limitation of the current study was that the incentives were still in place at the final follow‐up moment. However, previous studies and a meta‐analysis of financial incentives for smoking cessation have provided evidence for a sustained effect of financial incentives after the incentives were removed 15, 16, 59. Because a proportion of the participants did not complete all questionnaires, some cost data had to be imputed. However, the complete case analysis showed comparable results, which strengthens confidence in the data. Furthermore, cost data were based on self‐report, which may be prone to bias, and the retrospective nature of the questionnaires may have led to recall bias, which may have caused an over‐ or underestimation of costs 60. A systematic review comparing self‐reports and administrative data to measure health‐care resource use for cost estimation found that although patients may report lower resource use, self‐reported data may provide adequate estimates when administrative data are not available 61. Regarding the reliability and validity of self‐reports to measure absenteeism from work a meta‐analysis found, compared to employer records, a tendency to under‐report absenteeism, which was reduced if the self‐report was focused specifically on absence due to sickness, as was performed in the current study 62. Moreover, in the current study, a potential bias in the reporting of resource use is expected to be comparable for both the intervention and control group. A final limitation is that the current study was designed to include a limited number of employees within each company. To maximize the impact of financial incentives, it should be further investigated how the reach of the intervention among employees can be increased.

Conclusion

Financial incentives were cost‐effective in increasing the number of successful quitters from both societal and an employer's perspectives within a 14‐month time‐frame, depending on how much society or the employer is willing to pay for an additional quitter. The results of the cost–utility analysis within the 14‐month time‐frame were inconclusive, due probably to the relatively short observation period. The results from a life‐time perspective showed that financial incentives were far below the WTP threshold of €20.000 per QALY.

The current study demonstrates that providing financial incentives for smoking cessation may be cost‐effective within a short time‐period, and may help policymakers and employers to decide on implementing incentives to stimulate smoking cessation.

Clinical Trial registration

Netherlands Trial Register (NL5537).

Declaration of interests

None.

Supporting information

File S1 Valuation of costs.

File S2 Calculation of ICER from a lifetime perspective based on ICER tables.

Acknowledgements

This study was funded by the Dutch Cancer Society (KWF Kankerbestrijding), grant number UM 2015‐7943. The authors would like to thank Lotte De Haan‐Bouma for assisting with the data collection, Mascha Twellaar and Karin Aretz for assisting with the data cleaning, and would like to thank the companies and their employees who participated in this study. We are grateful to John Stapleton and Robert West for checking our life‐time calculations.

van den Brand, F. A. , Nagelhout, G. E. , Winkens, B. , Chavannes, N. H. , van Schayck, O. C. P. , and Evers, S. M. A. A. (2020) Cost‐effectiveness and cost–utility analysis of a work‐place smoking cessation intervention with and without financial incentives. Addiction, 115: 534–545. 10.1111/add.14861.

References

- 1. World Health Organization (WHO) . WHO Report on the Global Tobacco Epidemic, 2008: the MPOWER package. Geneva, Switzerland: WHO; 2008.

- 2. National Center for Chronic Disease Prevention and Health Promotion (US) Office on Smoking and Health . The health consequences of smoking—50 years of progress. a report of the Surgeon General. Atlanta, GA: US Department of Health and Human Services, Centers for Disease Control and Prevention, National Center for Chronic Disease Prevention and Health Promotion, Office on Smoking and Health; 2014.

- 3. Jha P., Ramasundarahettige C., Landsman V., Rostron B., Thun M., Anderson R. N., et al 21st‐century hazards of smoking and benefits of cessation in the United States. N Engl J Med 2013; 368: 341–350. [DOI] [PubMed] [Google Scholar]

- 4. Halpern M. T., Shikiar R., Rentz A. M., Khan Z. M. Impact of smoking status on workplace absenteeism and productivity. Tob Control 2001; 10: 233–238. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5. Tsai S., Wen C., Hu S., Cheng T., Huang S. Workplace smoking related absenteeism and productivity costs in Taiwan. Tob Control 2005; 14: i33–i37. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6. Berman M., Crane R., Seiber E., Munur M. Estimating the cost of a smoking employee. Tob Control 2014; 23: 428–433. [DOI] [PubMed] [Google Scholar]

- 7. Troelstra S. A., Coenen P., Boot C. R., Harting J., Kunst A. E., van der Beek A. J. Smoking and sickness absence: a systematic review and meta‐analysis. Scand J Work Environ Health 2019; 10.5271/sjweh.384. [DOI] [PubMed] [Google Scholar]

- 8. Hartmann‐Boyce J., Stead L. F., Cahill K., Lancaster T. Efficacy of interventions to combat tobacco addiction: Cochrane update of 2012 reviews. Addiction 2013; 108: 1711–1721. [DOI] [PubMed] [Google Scholar]

- 9. Cahill K., Stevens S., Perera R., Lancaster T. Pharmacological interventions for smoking cessation: an overview and network meta‐analysis. Cochrane Database Syst Rev 2013. CD009329. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10. Stead L. F., Koilpillai P., Fanshawe T. R., Lancaster T. Combined pharmacotherapy and behavioural interventions for smoking cessation. Cochrane Database Syst Rev 2016. CD008286. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11. Cahill K., Lancaster T. Workplace interventions for smoking cessation. Cochrane Database Syst Rev 2014; 2: CD003440. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12. Hiscock R., Dobbie F., Bauld L. Smoking cessation and socioeconomic status: an update of existing evidence from a National Evaluation of English stop smoking services. Biomed Res Int 2015; 2015: 274056. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13. Huisman M., Kunst A. E., Mackenbach J. P. Inequalities in the prevalence of smoking in the European Union: comparing education and income. Prev Med 2005; 40: 756–764. [DOI] [PubMed] [Google Scholar]

- 14. Hill S., Amos A., Clifford D., Platt S. Impact of tobacco control interventions on socioeconomic inequalities in smoking: review of the evidence. Tob Control 2014; 23: e89–e97. [DOI] [PubMed] [Google Scholar]

- 15. Halpern S. D., Harhay M. O., Saulsgiver K., Brophy C., Troxel A. B., Volpp K. G. A pragmatic trial of E‐cigarettes, incentives, and drugs for smoking cessation. N Engl J Med 2018; 378: 2302–2310. [DOI] [PubMed] [Google Scholar]

- 16. Volpp K. G., Troxel A. B., Pauly M. V., Glick H. A., Puig A., Asch D. A., et al A randomized, controlled trial of financial incentives for smoking cessation. N Engl J Med 2009; 360: 699–709. [DOI] [PubMed] [Google Scholar]

- 17. van den Brand F. A., Nagelhout G. E., Winkens B., Chavannes N. H., van Schayck O. C. P. Effect of a workplace‐based group training programme combined with financial incentives on smoking cessation: a cluster‐randomised controlled trial. Lancet Public Health 2018; 3: e536–e544. [DOI] [PubMed] [Google Scholar]

- 18. Smith A. L., Carter S. M., Chapman S., Dunlop S. M., Freeman B. Why do smokers try to quit without medication or counselling? A qualitative study with ex‐smokers. BMJ Open 2015; 5: e007301. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19. Carroll C., Rick J., Leaviss J., Fishwick D., Booth A. A qualitative evidence synthesis of employees’ views of workplace smoking reduction or cessation interventions. BMC Public Health 2013; 13: 1095. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20. Van den Brand F. A. Dohmen, LME , Van Schayck C. P., Nagehout G. E. ‘Secretly, it's a competition’: a qualitative study investigating what helped employees quit smoking during a workplace smoking cessation group training programme with incentives. BMC Open 2018;8(11). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21. Weng S. F., Ali S., Leonardi‐Bee J. Smoking and absence from work: systematic review and meta‐analysis of occupational studies. Addiction 2013; 108: 307–319. [DOI] [PubMed] [Google Scholar]

- 22. Eriksen M. P., Gottlieb N. H. A review of the health impact of smoking control at the workplace. Am J Health Promot 1998; 13: 83–104. [DOI] [PubMed] [Google Scholar]

- 23. Osinubi O. Y., Slade J. Tobacco in the workplace. Occup Med 2002; 17: 137–158; vi. [PubMed] [Google Scholar]

- 24. Van den Brand F. A., Nagelhout G. E., Winkens B., Evers S. M. A. A., Kotz D., Chavannes N. H., et al The effect of financial incentives on top of behavioral support on quit rates in tobacco smoking employees: study protocol of a cluster‐randomized trial. BMC Public Health 2016; 16: 1056. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 25. Van den Brand F. A., Nagelhout G. E., Winkens B., Chavannes N. H., Van Schayck C. P. Effect of a workplace-based group training programme combined with financial incentives on smoking cessation: a cluster‐randomised controlled trial. The Lancet. Public health 2018. 10.1016/s2468-2667(18)30185-3 [DOI] [PubMed] [Google Scholar]

- 26. Promberger M., Dolan P., Marteau T. M. ‘Pay them if it works’: discrete choice experiments on the acceptability of financial incentives to change health related behaviour. Soc Sci Med 2012; 75: 2509–2514. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 27. Giles E. L., Robalino S., Sniehotta F. F., Adams J., McColl E. Acceptability of financial incentives for encouraging uptake of healthy behaviours: a critical review using systematic methods. Prev Med 2015; 73: 145–158. [DOI] [PubMed] [Google Scholar]

- 28. Boyd K. A., Briggs A. H., Bauld L., Sinclair L., Tappin D. Are financial incentives cost‐effective to support smoking cessation during pregnancy? Addiction 2016; 111: 360–370. [DOI] [PubMed] [Google Scholar]

- 29. Sung H.‐Y., Penko J., Cummins S. E., Max W., Zhu S.‐H., Bibbins‐Domingo K., et al Economic impact of financial incentives and mailing nicotine patches to help Medicaid smokers quit smoking: a cost–benefit analysis. Am J Prev Med 2018; 55: S148–S158. [DOI] [PubMed] [Google Scholar]

- 30. Max W. The financial impact of smoking on health‐related costs: a review of the literature. Am J Health Promot 2001; 15: 321–331. [DOI] [PubMed] [Google Scholar]

- 31. Husereau D., Drummond M., Petrou S., Carswell C., Moher D., Greenberg D., et al Consolidated health economic evaluation reporting standards (CHEERS) statement. Cost Eff Resour Alloc 2013; 11(6): f1049 10.1186/1478-7547-11-6 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32. Hakkaart‐van Roijen L, Van der Linden N, Bouwmans C, Kanters T, Swan Tan SK. Costing manual: Methodology of costing research and reference prices for economic evaluations in healthcare. Rotterdam: Institute for Medical Technology Assessment Erasmus Universiteit Rotterdam; 2015.

- 33. Drummond M. F., Sculpher M. J., Claxton K., Stoddart G. L., Torrance G. W. Methods for the economic evaluation of health care programmes. Oxford: Oxford University Press; 2015. [Google Scholar]

- 34. Thorn J., Coast J., Cohen D., Hollingworth W., Knapp M., Noble S., et al Resource‐use measurement based on patient recall: issues and challenges for economic evaluation. Appl Health Econ Health Policy 2013; 11: 155–161. [DOI] [PubMed] [Google Scholar]

- 35. Bouwmans C., Krol M., Severens H., Koopmanschap M., Brouwer W., Roijen L. H.‐V. The iMTA productivity cost questionnaire: a standardized instrument for measuring and valuing health‐related productivity losses. Value Health 2015; 18: 753–758. [DOI] [PubMed] [Google Scholar]

- 36. Bouwmans C., Hakkaart‐van Roijen L., Koopmanschap M., Krol M., Severens H., Brouwer W. Medical Cost Questionnaire (iMCQ). Rotterdam: iMTA, Erasmus Universiteit Rotterdam; 2013. [Google Scholar]

- 37. Dirum . Database of instruments for resource use management 2016. Available at: http://www.dirum.org, accessed on 15 July 2016.

- 38. Tan S. S., Bouwmans C. A. M., Rutten F. F. H., Hakkaart‐van R. L. Update of the Dutch manual for costing in economic evaluations. Int J Technol Assess Health Care 2012; 28: 152–158. [DOI] [PubMed] [Google Scholar]

- 39. West R., Hajek P., Stead L., Stapleton J. Outcome criteria in smoking cessation trials: proposal for a common standard. Addiction 2005; 100: 299–303. [DOI] [PubMed] [Google Scholar]

- 40. Group TE EuroQol‐a new facility for the measurement of health‐related quality of life. Health Policy 1990; 16: 199–208. [DOI] [PubMed] [Google Scholar]

- 41. Versteegh M. M., Vermeulen K. M., Evers S. M., de Wit G. A., Prenger R., Stolk E. A. Dutch tariff for the five‐level version of EQ‐5D. Value Health 2016; 19: 343–352. [DOI] [PubMed] [Google Scholar]

- 42. Manca A., Hawkins N., Sculpher M. J. Estimating mean QALYs in trial‐based cost‐effectiveness analysis: the importance of controlling for baseline utility. Health Econ 2005; 14: 487–496. [DOI] [PubMed] [Google Scholar]

- 43. Faria R., Gomes M., Epstein D., White I. R. A guide to handling missing data in cost‐effectiveness analysis conducted within randomised controlled trials. Pharmacoeconomics 2014; 32: 1157–1170. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 44. Briggs A. H., Wonderling D. E., Mooney C. Z. Pulling cost‐effectiveness analysis up by its bootstraps: a non‐parametric approach to confidence interval estimation. Health Econ 1997; 6: 327–340. [DOI] [PubMed] [Google Scholar]

- 45. Zwaap J KS, van der Meijden C, Staal P, van der Heiden L. Cost-effectiveness in practice, Diemen, the Netherlands: National Health Care Institute, 2015.

- 46. Stapleton J. A., West R. A direct method and ICER tables for the estimation of the cost‐effectiveness of smoking cessation interventions in general populations: application to a new cytisine trial and other examples. Nicotine Tob Res 2012; 14: 463–471. [DOI] [PubMed] [Google Scholar]

- 47. Schulz D. N., Smit E. S., Stanczyk N. E., Kremers S. P., de Vries H., Evers S. M. Economic evaluation of a web‐based tailored lifestyle intervention for adults: findings regarding cost‐effectiveness and cost‐utility from a randomized controlled trial. J Med Internet Res 2014; 16: e91. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 48. Smit E. S., Evers S. M. A. A., de Vries H., Hoving C. Cost‐effectiveness and cost‐utility of internet‐based computer tailoring for smoking cessation. J Med Internet Res 2013; 15: e57. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 49. Stanczyk N. E., Smit E. S., Schulz D. N., de Vries H., Bolman C., Muris J. W., et al An economic evaluation of a video‐ and text‐based computer‐tailored intervention for smoking cessation: a cost‐effectiveness and cost‐utility analysis of a randomized controlled trial. PLOS ONE 2014; 9: e110117. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 50. Shiffman S., Patten C., Gwaltney C., Paty J., Gnys M., Kassel J., et al Natural history of nicotine withdrawal. Addiction 2006; 101: 1822–1832. [DOI] [PubMed] [Google Scholar]

- 51. Cook J. W., Piper M. E., Leventhal A. M., Schlam T. R., Fiore M. C., Baker T. B. Anhedonia as a component of the tobacco withdrawal syndrome. J Abnorm Psychol 2015; 124: 215–225. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 52. Mulder I., Tijhuis M., Smit H. A., Kromhout D. Smoking cessation and quality of life: the effect of amount of smoking and time since quitting. Prev Med 2001; 33: 653–660. [DOI] [PubMed] [Google Scholar]

- 53. Heikkinen H., Jallinoja P., Saarni S. I., Patja K. The impact of smoking on health‐related and overall quality of life: a general population survey in Finland. Nicotine Tob Res 2008; 10: 1199–1207. [DOI] [PubMed] [Google Scholar]

- 54. Piper M. E., Kenford S., Fiore M. C., Baker T. B. Smoking cessation and quality of life: changes in life satisfaction over 3 years following a quit attempt. Ann Behav Med 2012; 43: 262–270. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 55. US Department of Health and Human Services (USDHHS) The health benefits of smoking cessation. Center for Chronic Disease Prevention and Health Promotion, Office on Smoking and Health. Atlanta, GA: USDHHS; 1990. [Google Scholar]

- 56. Ferreira L. N., Ferreira P. L., Ribeiro F. P., Pereira L. N. Comparing the performance of the EQ‐5D‐3L and the EQ‐5D‐5L in young Portuguese adults. Health Qual Life Outcomes 2016; 14: 89. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 57. Konnopka A., Koenig H.‐H. The ‘no problems’‐problem: an empirical analysis of ceiling effects on the EQ‐5D 5L. Qual Life Res 2017; 26: 2079–2084. [DOI] [PubMed] [Google Scholar]

- 58. Schlam T. R., Piper M. E., Cook J. W., Fiore M. C., Baker T. B. Life 1 year after a quit attempt: real‐time reports of quitters and continuing smokers. Ann Behav Med 2012; 44: 309–319. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 59. Notley C., Gentry S., Livingstone‐Banks J., Bauld L., Perera R., Hartmann‐Boyce J. Incentives for smoking cessation. Cochrane Database Syst Rev 2019; 7: CD004307. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 60. Brusco N. K., Watts J. J. Empirical evidence of recall bias for primary health care visits. BMC Health Serv Res 2015; 15: 381. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 61. Noben C. Y., de Rijk A., Nijhuis F., Kottner J., Evers S. The exchangeability of self‐reports and administrative health care resource use measurements: assessment of the methodological reporting quality. J Clin Epidemiol 2016; 74: 93–106.e2. [DOI] [PubMed] [Google Scholar]

- 62. Johns G., Miraglia M. The reliability, validity, and accuracy of self‐reported absenteeism from work: a meta‐analysis. J Occup Health Psychol 2015; 20: 1–14. [DOI] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

File S1 Valuation of costs.

File S2 Calculation of ICER from a lifetime perspective based on ICER tables.