Abstract

Objective

The 340B program allows safety‐net hospitals to acquire discounted outpatient drugs and charge payers full price. We examined whether 340B participation increases safety‐net engagement.

Data Sources

340B participation data, Medicare hospital cost reports, American Hospital Association Survey, and Schedule 990 nonprofit hospital tax returns.

Study Design

Quasi‐experimental difference‐in‐differences design comparing 340B hospitals (the “treatment” group) before and after participating to changes over time to three alternative “control” groups: all other nonprofit and public hospitals, hospitals that are not participating during our study, and hospitals that were not‐yet‐participating but started after 2015. Outcome measures include a range of safety‐net care measures that are alternatives to the standard uncompensated care: charity care, community benefit spending, charity care policies, and low‐profit service‐line provision.

Data Extraction

We extracted data on all nonprofit and public hospitals from 2011 to 2015. We linked 340B participation data to Medicare hospital cost reports and American Hospital Association data using Medicare hospital identifiers. 990 Data was linked on name and address.

Principal Findings

New 340B participation was not associated with a change in uncompensated care, but was associated with a 28.9 percent increase in charity care spending (SE = 8.8), or about $880,000 per hospital. However, total community benefit spending (including charity care) did not change. 340B was associated with an increase in the probability of offering discounted care (4.3 percentage points, SE = 1.6) from 84 to 88 percent and an increase in the income eligibility limit for discounted care (18.9 percentage points, SE = 5.6) from 294 to 313 percent. Participation was not associated with the probability of offering low‐profit medical care services.

Conclusions

Alternative measures show that newly participating hospitals may increase charity care, potentially through offering more patients discounted care. However, increases appear to be fully offset by reductions in other community benefit programs.

Keywords: 340B, community benefit spending, DSH Hospitals, safety‐net care, service provision

What this Study Adds.

The 340B program provides hospitals with large amounts of revenue to be used for safety‐net care provision.

There is no association between uncompensated care, the standard measure of safety‐net care provision, and 340B participation.

Initiating participation in 340B is associated with an increase in some community benefit spending but reductions in other types of community benefit spending.

Initiating participation in 340B is not associated with offering new low‐profit hospital service lines.

1. INTRODUCTION

The 340B program entitles clinics and hospitals that serve low‐income and uninsured (“safety‐net”) patients to substantially discounted outpatient drugs administered in clinics or dispensed through pharmacies. In order to generate revenue that could fund safety‐net care, 340B participants may bill third‐party payers, including Medicare and commercial insurers, 1 for amounts above the discounted price. Although Congress' original intent was that the program support safety‐net care, such as charity care spending or community health improvement programs, there is no explicit requirement that hospitals use 340B revenues in this way. 2 Some worry that the program creates a perverse incentive: the less safety‐net care provided, the more revenues participants may retain as profit. 3 Recent studies have documented the implications of the program's potential unintended consequences: Participating hospitals have acquired oncology practices through which discounted chemotherapies can be dispensed, 4 , 5 and these newly acquired clinics are more likely to be in higher‐income communities. 6 As a result, Medicare spending in 340B oncology clinics is substantially higher than spending in nonregistered clinics. 7 Furthermore, as the program reduces the price of most outpatient drugs by 25‐75 percent, 8 , 9 340B has become an increasingly important profit source for participating hospitals. 6 , 10

Stakeholder concerns have focused on “disproportionate share” (DSH) hospitals, which qualify by providing a minimum fraction of care to low‐income Medicare and Medicaid patients, called the DSH patient percentage. 3 Importantly, free and reduced price care, or “charity care” is not included in the DSH patient percentage. In contrast to safety‐net clinics—such as Federally Qualified Health Centers—which must provide free and reduced price care, DSH hospitals face no such requirement. Participation among DSH hospitals has soared in recent years but recent participants appear to be no more safety‐net engaged than nonparticipating nonprofit and public hospitals. 11

These facts beg the question: “Does new participation in 340B increase hospital safety‐net engagement?” The absence of systematically reported program data and little government oversight presents a challenge to evaluating 340B's effects. On one hand, evaluations by advocates rely on anecdotal and loosely defined measures of safety‐net “activities.” 12 , 13 , 14 On the other, the standard publicly available measure of safety‐net engagement—uncompensated care—may be poorly suited to evaluate 340B participants' engagement in safety‐net efforts. 1 , 15 , 16 , 17

In this paper, we assessed the association of 340B participation with provision of safety‐net care among DSH hospitals using both standard measures of hospital safety‐net engagement and alterative measures that may capture other aspects of safety‐net engagement. We focused on a primary alternative measure most directly related to the program's goal of increasing medical care to safety‐net reliant patients (charity care spending) as well as several other alternative measures not directly related to medical care (spending on noncharity community benefits, eligibility criteria for formal charity care policies, and provision of low‐profit, high community value service lines). We employed a quasi‐experimental research design to identify associations of the 340B program with primary and other alternative measures of safety‐net care provision. Using a difference‐in‐differences design, we compared within‐hospital changes in outcomes before and after hospitals participate in 340B to changes over time in one of two nonparticipating control groups.

1.1. Measuring safety‐net engagement

Uncompensated care is publicly reported by all Medicare‐certified hospitals and is therefore used as the standard measure of safety‐net engagement. 18 , 19 Yet, uncompensated care has limited utility as a standalone measure of hospital safety‐net engagement for several reasons. First, uncompensated care includes both charity care spending and bad debt—care for which the hospital attempted to collect payment. 20 , 21 Because subsidized care through 340B could increase charity care spending while simultaneously reducing patient debts, the opposing effects of the program may cancel each other out. Second, uncompensated care is sensitive to hospital prices, which are often inflated for the purposes of increasing reported uncompensated care. 22 To address the role of differing hospital prices, researchers deflate charges by hospital cost‐to‐charge ratios in order to express charges in terms of costs. However, because cost‐to‐charge ratios are often only available at the hospital level and cost‐to‐charge ratios vary within hospitals across clinical units, the use of cost‐to‐charge ratios can increase measurement error. Third, uncompensated care typically captures only the unreimbursed costs of the hospital's campus and may not reliably include offsite outpatient clinics and contract pharmacies where 340B discounted drugs are administered or dispensed to patients. 23 , 24 Thus, uncompensated care might underestimate safety‐net care in the outpatient and pharmacy setting supported by 340B revenues.

Given some of the drawbacks of the standard measure, an alternative measure of safety‐net engagement is charity care spending. Hospitals are required to report spending on charity care provided through a written charity care policy to the Internal Revenue Service on Form 990, Schedule H. 25 , 26 Importantly, hospitals must report on charity care expenditures not just at the hospital's campus but across all clinics and pharmacies within the hospital's tax filing unit, or organization. Importantly, hospitals must follow a set of common definitions when reporting community benefit spending. Hospitals also report on other types of “community benefit” spending on Schedule H including the public payer shortfall, defined as the difference between revenues and the cost of care for publicly insured patients, and also noncharity care community benefits such as community health improvement activities, cash contributions to community organizations, and research. However, these other forms of community benefit spending may not directly result in increased access for safety‐net reliant patients.

A second measure of safety‐net engagement is hospital charity care policies. Charity care policies are written documents that describe who is eligible for charity care at the hospital and whether free and or discounted medical care is offered to those who are eligible. The eligibility features of these policies are not sensitive to bad debt or differences in charges and are also reported to the IRS on Schedule H. While these eligibility features provide a unique way to assess the generosity of hospitals' charity care spending, an important limitation is that they are a measure of what is “available” rather than what is actually provided. Although one study assessed differences in these policies between Medicaid expansion and nonexpansion states, 25 we know of no other studies that have used these policies as a measure of safety‐net engagement.

A third measure of safety‐net engagement is the provision of low‐profit service lines by hospitals, which does not rely on spending‐based metrics. Using American Hospital Association (AHA) data, Horwitz 27 finds that several low‐profit services lines are less likely to be offered by for‐profit hospitals. These service lines include psychiatric care, substance abuse treatment, burn care, HIV/AIDS care, trauma care, emergency care, and obstetrics. One study tested for cross‐sectional differences in the probability of offering two low‐profit services (psychiatric and burn care) between 340B DSH hospitals. However, this study could not account for selection into 340B nor did it examine a comprehensive list of services. 28

Although none of these alternative measures of safety‐net engagement—charity care spending (our primary alternative measure), charity care policies or low‐profit service‐line provision (our other alternative measures)—provide a single comprehensive metric, taken together, they can address some of the shortcomings inherent to reliance on the single standard measure: uncompensated care.

1.2. Challenges to estimating the causal effect of 340B participation on safety‐net engagement

After 340B was introduced in 1992, DSH hospitals self‐selected into the program over time. Self‐selection presents a clear identification challenge: Simple comparisons between participants and nonparticipants will reflect a mix of both a 340B treatment effect as well as a selection effect. 29 Several identification strategies have been proposed to study the effects of 340B, including safety‐net engagement. Leveraging the fact that eligibility for 340B is based solely on having an adjusted DSH patient percentage >11.75 percent, Desai and McWilliams 4 use regression discontinuity to compare hospitals on either side of the 340B eligibility threshold. They find that hospitals just above the cutoff are more likely to consolidate with physicians who administer expensive 340B‐eligible drugs and spend no more on uncompensated care than hospitals just below the threshold. 4 A challenge with this design is that it assumes hospitals cannot alter their adjusted DSH patient percentage. However, several empirical studies and gray literature sources provide evidence to the contrary. 30 , 31 , 32 , 33 , 34 , 35 , 36 , 37 In fact, hospitals participating since the Affordable Care Act—which dramatically increased the returns to the program by allowing participants to dispense outpatient prescriptions through an unlimited number of contract pharmacies 38 —appear to manipulate the DSH patient percentage to gain eligibility. 39 These post‐2010 participants tend to be smaller and provide little more uncompensated care than nonparticipants. 28 Most importantly, they tend to take efforts to increase their DSH patient percentages to the minimum level to qualify for the program and no further. 39

Other studies have employed difference‐in‐difference methods. Leveraging the Affordable Care Act's expansion of 340B to several types of non‐DSH hospitals—children's hospitals, critical access hospitals, and standalone cancer hospitals—Alpert et al 40 compare vertical integration of oncology practices between counties that contain newly eligible non‐DSH hospitals to those that do not, before and after 2010. Jung et al 5 use a similar identification strategy to estimate the effect of participating in 340B on where cancer patients received chemotherapy and spending in cancer. They compared outpatient hospital‐affiliated clinics where the 340B discounts apply to community clinics where the discounts do not apply. A challenge with this design is that it relies on the 340B program's expansion to non‐DSH hospitals, which represent a minority of hospital participants and are reimbursed differently than DSH hospitals and thus face differing incentives. 41 Results for non‐DSH hospitals may not generalize to DSH hospitals.

To address the challenges above, we employed an alternative approach using difference‐in‐differences to compare within‐hospital variation in safety‐net engagement between DSH hospitals that started participating in the program to several plausible nonparticipating control groups.

2. METHODS

2.1. Data

The data for our study spanned multiple administrative sources, which are described below.

2.2. Charity and other community benefit spending

Data on charity and community benefit spending come from IRS Form 990, Schedule H data. These data are comprised of hospital tax returns filed by all nonprofit and most public hospitals nationwide. These data have been used in numerous studies. 25 , 26 , 42 Schedule H data are reported at multiple levels. Community benefit data are contained in Part 1 of the return and are reported by hospitals at the tax filing, or organization level. Thus, hospitals covered under the same employer identification number report together. From an original sample of 2674 nonprofit and public independent hospitals and hospital systems (11 976 hospital‐year observations), we limited our sample to hospitals, independent or within a system, for which all hospitals in the tax filing unit could be matched to hospital cost reports. We matched hospitals using name and address and a partial text‐matching algorithm that identified close matches between text with a minimum number of insertions, deletions, or substitutions. 43 We further limited our sample to general acute care hospitals and eliminated hospital systems that included hospitals in multiple states. Our final analysis dataset contained 846 independent hospitals and hospital systems, or 4195 hospital‐year observations.

For each hospital in the dataset, we created continuous variables that expressed spending on each type of reported community benefit. Although charity care spending—one component of community benefit—was our primary alternative measure of safety‐net engagement, we also created secondary alternative measures of other types of community benefit that were less directly related to patient care. These secondary alternative measures of safety‐net engagement included Medicaid and other government payer shortfall, which is the loss associated with treating patients on public programs which may reimburse hospitals below costs; other community benefits, including subsidized medical care and community health improvement activities; other types of community benefit, including research, cash contributions, and health professional education; and, finally, a total community benefit spending variable. All values of community benefit were net of off‐setting revenues such as patient payment amounts, program revenues, or government subsidies. We also winsorized each variable at the 1st and 99th percentiles within each year to minimize the influence of outliers. 44 To capture safety‐net engagement on both the intensive margin (spending conditional on any spending) and the extensive margin (any spending), we also created binary variables that expressed whether the hospital system had any spending in each category.

2.3. Charity care policy characteristics

We used 990 Data to create measures describing the characteristics of charity care policies, a secondary alternative measure of this study. Unlike community benefit expenditures, which are reported at the hospital system level, charity care policies are reported at the facility level in Part 5 of Schedule H. We matched the facility‐level data to hospital cost reports to identify general acute care hospitals. Our final sample for these data contained 1410 unique hospitals and 7050 hospital‐year observations. Our measures of hospital charity care policies included binary measures of whether the hospital offered free care or discounted care as part of the charity care policy. We also created continuous measures describing the maximum federal income to poverty level at which patients could receive free or discounted care.

2.4. Low‐profit service‐line provision

Another data source was the AHA annual member survey. These data included responses from nearly all hospitals in the United States (US) and have been used many times over to describe the service‐line offerings of hospitals, an alternative measure of this study. 27 , 45 The survey asked 6242 hospitals about 150 independent service lines between 2011 and 2015, our period of analysis. We limited our analysis sample to 1516 general acute care, nonprofit and public hospitals that could be matched to hospital cost report data, were located in the 50 US states and DC, and contained no missing observations on our service lines of interest (6775 hospital‐year observations). Using information on service lines, we created a set of six binary variables that indicate whether each service line is offered on the facility's campus. We used Horwitz 27 to select low‐profit high community value services, which included inpatient or outpatient drug and alcohol treatment, burn and trauma care, dental care, AIDS‐related care, obstetrical care, and inpatient, outpatient, or emergency psychiatric treatment.

2.5. 340B Participation

All three datasets were merged at the hospital facility level to the 340B provider list, which contains information on all hospitals that have ever participated in the 340B program, including start and end dates of participation for each registered clinic. None of the hospitals in our sample lost eligibility over the 2011‐2015 period. In the AHA data, we matched 340B participation data to 395 (1807 hospital‐year observations) hospitals ever participating in the program, including 211 (964 hospital‐year observations) that began participating between 2012 and 2015. For charity care spending data from schedule H, we matched 340B participation data to 148 (737 hospital‐year observations) hospitals ever participating in the program. For charity care policy data from schedule H, we matched 340B participation data to participants to the community benefit sample and 831 (4155 hospital‐year observations) hospitals ever participating in 340B.

We used the date and participation status to define three nested groups of control hospitals. The first was all other hospitals, which included those hospitals that were already participating, never participated, or would eventually participate after our study period end. The second was nonparticipating hospitals, which included those that never participated in the program or would eventually participate after the study period end. The third was limited to just those hospitals that eventually participate after the study period end. These control groups and their rationale are described in more detail below. Table S1 provides sample sizes and means, including the number of hospitals and observations that comprise our treatment and three control groups, as well as outcome variables from 2011, our baseline year.

2.6. Statistical analysis

2.6.1. Econometric specification

We used a difference‐in‐differences model to estimate the association of 340B participation with safety‐net service provision, comparing DSH hospitals' safety‐net engagement before and after becoming eligible for the program, compared with a control group. By focusing on within‐hospital differences, we compared each hospital to its own baseline and removed comparisons between the level of safety‐net engagement between hospitals with differing levels of effort. By comparing the change to change over time in a nonparticipating control group, we removed market‐wide trends. This approach is summarized in Equation 1:

| (1) |

is a dummy variable indicating if hospital h participated in 340B in time period t. The estimates controlled for time‐invariant differences across hospitals with hospital fixed effects, Fh. To account for any common changes in safety‐net engagement among all hospitals within a state over time, we included state‐by‐year fixed effects. The inclusion of these effects was important because states differentially expanded Medicaid over time, which could affect both 340B participation and safety‐net care provision. For regressions using the community benefit data, in which measures were reported at the system level, we parameterized the 340B participation measure in Equation (1) as a fraction that expressed the fraction of the system's hospitals that participate in 340B. For example, if a system had four hospitals, three of which were participating, the value of this variable was 0.75.

2.6.2. Alternative control groups

There is no one ideal control group for our analysis. Therefore, we present results for Equation (1) estimated comparing new 340B participants to three alternative control groups. We begin by comparing new participants to all other hospitals, including those that are already participating, those that are not‐yet participating at the end of our sample, and hospitals that never participate. Although this approach is the most straightforward, the difference‐in‐difference estimates, , are subject to bias because early participants in the 340B program are substantially different from more recent participants and may have been more likely to use the program as Congress intended. 28 For example, those hospitals that began participating before the ACA tended to be larger and also began participating with higher adjusted DSH patient percentages (see Table S2) than hospitals that qualified after 2010. Earlier participants were also more likely to be academic medical centers and located in urban areas.

To address the challenge posed by including hospitals that already participate in the program, our second control group excludes hospitals that already participate in the program and only includes nonparticipating hospitals. By estimating Equation (1) on only new participants and nonparticipants, we eliminated comparisons between new participants and earlier participants. Because nonparticipants may not serve as a good counterfactual for new 340B participants over our study period, we estimated a propensity score model and created intent‐to‐treat weights of the form . Our propensity score model included continuous measures of hospital beds, total discharges, Medicaid discharges, Medicare discharges, the adjusted DSH patient percentage, and uncompensated care. We then reweighted our estimates for Equation (1) following Abadie. 46 This approach provided more weight to control observations with a higher propensity of treatment in 2011. Because propensity weights could only be estimated for hospitals that were observed in 2011, we excluded some hospitals from each dataset that were not present in the data in 2011. Table S3 presents a balancing test of our propensity score model. After reweighting, we found standardized differences <0.10, indicating no difference. 47

A potential challenge that cannot be addressed by either comparing new participants to either all other hospitals or nonparticipants is nonrandom selection into the program. If hospitals that chose to participate were, for example, more strategic and less safety‐net engaged, then our observed difference‐in‐differences estimate would reflect both a treatment effect and negative selection bias. To reduce selection bias, we re‐estimated Equation (1) focusing on a comparison of two groups: new participants and hospitals that were not participating in the program before the end of our sample period, 2015, but would eventually participate in the following three years (“not‐yet” participants). Hospitals that began participating after the ACA tend to be minimally safety‐net engaged 28 and also display similar behavior in terms of manipulation of the DSH patient percentage to no more than the minimum level to gain eligibility for 340B. Although there may be selection on the timing of manipulation of the DSH patient percentage, comparing new participants to these “not‐yet” participants should reduce the influence of selection bias relative to comparisons between new 340B participants and all other hospitals, or between participants and nonparticipants. Due to small sample size, we included hospital and year fixed effects rather than hospital and state‐by‐year fixed effects. While there were differences in beds and discharges, Medicaid populations, uncompensated care, and region of location between hospitals that began participating between 2011 and 2015 and hospitals that did not participate, there were no differences in these characteristics between new participants and those would‐be participants that started between 2016 and 2018.

2.6.3. Robustness tests

We estimated several robustness tests of our results. These included limiting to a balanced panel of hospitals observed in every year, winsorizing spending data at alternative, more stringent levels (top and bottom 1st and 10th percentiles) and omitting each cohort of new participants between 2012 and 2015.

Additionally, we assessed whether our results for charity care could be explained by factors other than 340B. First, charity care and related measures of spending depend on hospital cost‐to‐charge ratios, which are used to convert hospital charges to the actual cost of services provided. If 340B increases a hospital's costs relative to its charges, charity care and other forms of community benefit spending may rise mechanically. Second, charity care could increase if the DSH patient percentage is correlated with charity care. In the presence of such a relationship, charity care could increase as a result of qualifying for 340B (ie, having a DSH patient percentage above the eligibility limit) rather than 340B participation in itself. Therefore, we also test whether crossing the DSH patient percentage eligibility threshold of 11.75 percent is associated with increased charity care.

Our analysis also considered multiple related outcomes. We therefore compared our results to a Bonferroni‐corrected P‐value. 48

3. RESULTS

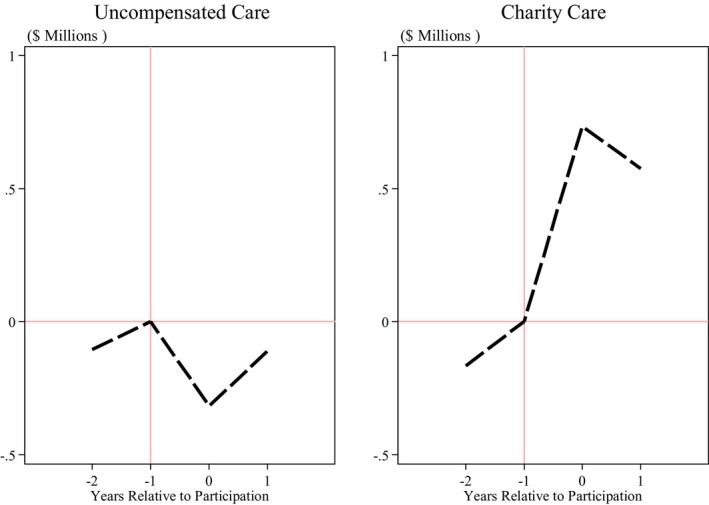

Figure 1 displays average uncompensated care provision in each year before and after each hospital began participating in 340B, net of the average amount of uncompensated care among control group hospitals in each calendar year. The figure is limited to hospitals that began participating between 2012 and 2015. The dark line is the difference relative to two groups of nonparticipant hospitals: hospitals that never participate and the gray line represents the difference between 340B hospitals and not‐yet participating hospitals. Figure 1 shows little difference in uncompensated care before and after participation for either comparison. Figure 1 also presents average charity care spending (the primary alternative measure) in each year before the hospital began participating in 340B, net of the average amount of charity care spending among control group hospitals. Figure 1 suggests that despite a lack of change for uncompensated care, charity care spending increases after 340B participation. This pattern holds whether measured relative to never‐participating hospitals or not‐yet participating hospitals. The difference between participants and nonparticipants continues to increase into the second year of participation when compared to not‐yet participating hospitals.

Figure 1.

Average difference in uncompensated care and charity care spending between 340B hospitals and a control group, before and after participation, 2011‐2015.

Note: The figure presents average spending in uncompensated care (left panel) and charity care (right panel) among hospitals that begin participating in 340B over out study period relative to the average value of spending among nonparticipating hospitals. Each point represents the difference between the average for hospitals that begin participating and control group hospitals in the calendar year of observation, averaged across hospitals with differing start dates, and presented in event time where year −1 is the year before the hospital began participating in the program. The figure adjusts for time‐invariant hospital characteristics and common calendar trends by subtracting the hospital‐specific average and year‐specific average from each observation. The sample is limited to nonprofit and public general acute care hospitals that are observed in all 5 y of our sample. Uncompensated care comes from 2011 to 2015 Medicare Cost Report data and is defined as charity care and bad debt charges net of patient payments, deflated by the cost‐to‐charge ratio. Charity care comes from 2011 to 2015 Schedule H, Part 1 data, and is defined as the cost of providing charity care to patients through a written and publicized charity care policy, net of off‐setting revenues such as patient payments. Nonparticipants include hospitals that never participate in 340B as well as hospitals that eventually participate in 340B but have not yet done so

Table 1 presents the results of difference‐in‐differences models with each outcome as both logged expenditures and an indicator of any expenditures to capture both the intensive and extensive margins of safety‐net engagement. We first consider the intensive margin of spending conditional on any spending, how does such spending change after 340B participation, relative to a control group? Compared to all other hospitals, we find a 21.8 percent (SE = 9.8) increase in charity spending only. Compared to nonparticipating hospitals, we find a 28.9 percent (SE = 8.8) relative increase and compared to not‐yet participating hospitals, we find a 21.3 percent (SE = 9.8) relative increase in charity care expenditures. For other categories, we find a mixed pattern of spending. Compared to nonparticipating hospitals, we find a 21.2 percent (SE = 11.6) relative increase in health professional education spending. However, compared to not‐yet participating hospitals, we find 42.8 percent (SE = 19.5) and 67.3 percent (SE = 29.8) relative decreases in cash donations and research spending. We find no association between newly participating in 340B and total community benefit spending relative to hospitals across all three control groups.

Table 1.

Within‐hospital differences in community benefit spending relative to alternative control groups, 2011‐2015

| Community benefit type | Charity care | Public payer shortfall | Community health activities | Health professions education | Subsidized medical care | Cash donations | Research | Total community benefits |

|---|---|---|---|---|---|---|---|---|

| Panel A: New participants compared to all other hospitals (N = 2719) | ||||||||

| Ln(Expenditures) | 0.218 | 0.211 | 0.153 | 0.229 | 0.006 | −0.236 | −0.367 | 0.008 |

| SE | [0.098] | [0.497] | [0.112] | [0.120] | [0.159] | [0.182] | [0.338] | [0.049] |

| P‐value | 0.026 | 0.671 | 0.171 | 0.056 | 0.971 | 0.195 | 0.278 | 0.870 |

| Pr(Expenditures > 0) | 0.004 | 0.037 | 0.002 | 0.025 | −0.055 | −0.070 | −0.008 | −0.003 |

| SE | [0.006] | [0.030] | [0.026] | [0.024] | [0.030] | [0.038] | [0.030] | [0.010] |

| P‐value | .508 | .217 | .927 | .282 | .068 | .064 | .776 | .786 |

| Panel B: New participants compared to nonparticipants (N = 2704) | ||||||||

| Ln(Expenditures) | 0.289 | 0.141 | 0.150 | 0.212 | 0.111 | −0.287 | −0.293 | 0.004 |

| SE | [0.088] | [0.519] | [.099] | [0.116] | [0.136] | [0.191] | [0.274] | [0.059] |

| P‐value | .001 | .787 | .133 | .067 | .413 | .134 | .287 | .945 |

| Pr(Expenditures > 0) | 0.003 | 0.0184 | 0.018 | 0.014 | −0.063 | −0.074 | −0.038 | 0.003 |

| SE | [0.004] | [0.033] | [0.024] | [0.024] | [0.031] | [0.037] | [0.032] | [0.010] |

| P‐value | .495 | .579 | .446 | .555 | .041 | .044 | .239 | .802 |

| Panel C: New participants compared to not‐yet participants (N = 722) | ||||||||

| Ln(Expenditures) | 0.213 | 0.309 | 0.145 | 0.191 | −0.087 | −0.428 | −0.673 | 0.013 |

| SE | [0.098] | [0.492] | [0.112] | [0.152] | [0.175] | [0.195] | [0.298] | [0.060] |

| P‐value | .031 | .532 | .197 | .212 | .619 | .030 | .030 | .829 |

| Pr(Expenditures > 0) | 0.008 | 0.027 | 0.026 | 0.064 | −0.022 | −0.064 | 0.004 | 0.007 |

| SE | [0.006] | [0.034] | [0.027] | [0.032] | [0.036] | [0.038] | [0.032] | [0.009] |

| P‐value | .162 | .428 | .337 | .043 | .543 | .098 | .891 | .466 |

The table presents estimates from a difference‐in‐differences model as specified in Equation 1. All community benefit outcomes are measured in logs or as indicators of nonzero expenditures. They include the following: charity care, defined as care provided to patients as part of a formal charity care plan; public payer shortfall, defined as the difference between costs of treating Medicaid and other patients covered by state and local programs less revenues for treating those patients; community health improvements, defined as nonmedical community activities to improve health such as health fairs; health professions education, defined as spending on training such as nurse education; subsidized medical care, defined as free or reduced priced medical care provided outside of the hospital's charity care program, such as a patient drug assistance program. Total represents the total across all categories. All expenditures were measured net of off‐setting revenues and were winsorized at the 1st and 99th percentiles. The dependent variable is specified as the fraction of hospitals in the hospital system that are eligible for 340B. Panel A compares hospitals that begin participating in 340B between 2012 and 2015 to all other hospitals. Panel B compares hospitals that begin participating in 340B between 2012 and 2015 to a group of reweighted nonparticipating hospitals using average treatment on the treated propensity scores. Panel C uses not‐yet participating hospitals that begin participating in 340B between 2012 and 2015 to those that are currently not participating but participate eventually after 2015 when our sample ends. All estimates are generated using ordinary least squares. Cluster‐robust standard errors are presented below each estimate and are displayed below in brackets. Panels A and B include hospital and state‐year fixed estimates. Panel C includes only hospital and year fixed estimates.

We used our difference‐in‐differences model to test for changes in uncompensated care after participation in 340B. We find a nonstatistically significant change in uncompensated care after participation relative to either type of nonparticipants: compared to nonparticipants (2.9 percent, SE = 3.7 percent) and compared to not‐yet participants (−1.3 percent, SE = 4 percent). We also found no evidence that cost‐to‐charge ratios increased after participation in 340B, and thus, increases in charity spending likely to do reflect increases in costs associated with 340B.

Next, we consider the extensive margin of spending—whether hospitals spend on particular noncharity community benefits, our secondary alternative measures, after participation. Compared to all other hospitals, we found that 340B participation was associated with a 5.5 and 7 percentage point (PP) (SE = 3.0 PP and SE = 3.8 PP) decrease in the probability of any expenditure on subsidized medical care or cash donations to community organizations. Compared to nonparticipants, we find similar results: Hospitals are 6.3 PP (SE = 3.1 PP) and 7.4 PP (SE = 3.7 PP) less likely to have any spending on subsidized medical care outside of a charity care policy or cash donations to community organizations after participating in 340B. Relative to the fraction of hospitals that spend money on subsidized medical care or make cash donations to community organizations, these estimates represent proportional changes of roughly 10 percent (6.4/58; 7.4/74). Comparing 340B participants to not‐yet participants, we find that hospitals are 6.4 PP (SE = 3.8 PP) less likely to spend on cash donations to community organizations, but also 6.4 PP (SE = 3.2 PP) more likely to spend on health professions education.

Our analysis considers eight related outcomes, and therefore, we also compare our results to a Bonferroni‐corrected P‐value of .00625 (0.05/8). 49 By this stringent standard, we find that 340B participation was only associated with an increase in charity care spending and that estimated decreases in other categories of community benefit spending were no longer statistically significant. Taken together, these results imply that increased charity care spending may be offset by reduced spending in other categories.

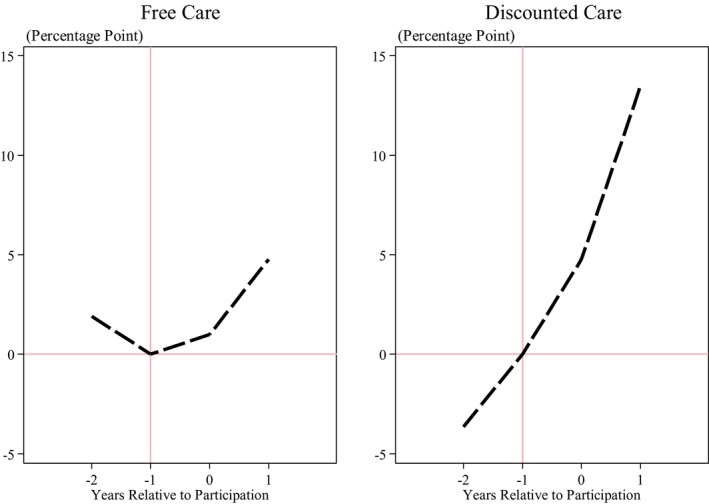

Figure 2 illustrates the difference in features of hospital charity care policies between 340B hospitals and non‐340B hospitals before and after participating relative to each control group. The left‐hand panel shows there is little difference in the probability of offering free care between participants and nonparticipants after participation. However, the right‐hand panel shows that 340B hospitals are more likely to offer discounted care after participating in the program. Table 2 presents the difference‐in‐differences estimates for charity care policy features. We find no change in the probability of offering free care nor the upper income level limit for free care after hospitals begin participating in 340B relative to any of our control groups. In contrast, we find that beginning to participate in 340B is associated with an increased probability of offering discounted care. In our preferred model, hospitals were 4.3 PP (SE = 1.6 PP) more likely to offer discounted care after participating, relative to nonparticipants. Relative to the preperiod mean for hospitals that participate in 340B, this association represents about a 4 percent increase (0.043/0.96). The income level of discounted care increases after program participation by 18.9 PP (SE = 5.6 PP) relative to nonparticipants. Before 340B participation, hospitals offered discounted care to patients with incomes at or below 307 percent of the federal poverty level. Relative to this pre‐340B discounted charity level, the estimated pre‐/postchange represents a 6 percent increase (19/307). The results are similar when comparing new participants to not‐yet participants, although the estimates are less precise. Adjusting for multiple hypothesis testing, the Bonferroni‐corrected P‐value of .0125 (0.05/4) would still judge the estimates compared to nonparticipants to be statistically significant.

Figure 2.

Average difference in charity care policy characteristics between 340B hospitals and control group, before and after participation, 2011‐2015.

Note: The figure presents the upper income limit on free (left panel) and discounted (right panel) care among hospitals that begin participating in 340B over our study period relative to the average value of spending among nonparticipating hospitals. Each point represents the difference between the average for hospitals that begin participating and control group hospitals in the calendar year of observation, averaged across hospitals with differing start dates, and presented in event time where year −1 is the year before the hospital began participating in the program. The figure adjusts for time‐invariant hospital characteristics and common calendar trends by subtracting the hospital‐specific average and year‐specific average from each observation. The sample is limited to nonprofit and public general acute care hospitals that are observed in all 5 y of our sample. Data come from 2011 to 2015 Schedule H 990 sample. Nonparticipants are those that never participate in 340B as well as hospitals that eventually participate in 340B but have not yet done so during our sample

Table 2.

Within‐hospital differences in charity care policy characteristics relative to alternative control groups, 2011‐2015

| Free care | Discounted care | |||

|---|---|---|---|---|

| Offers | FPL Limit | Offers | FPL Limit | |

| Panel A: New participants compared to all other hospitals (N = 7050) | ||||

| Estimate | 0.001 | 1.600 | 0.039 | 16.974 |

| SE | [0.009] | [2.783] | [0.015] | [5.602] |

| P‐value | .911 | .566 | .010 | .002 |

| Panel B: New participants compared to nonparticipant hospitals (N = 4440) | ||||

| Estimate | 0.007 | 3.618 | 0.043 | 18.890 |

| SE | [0.010] | [2.535] | [0.016] | [5.616] |

| P‐value | .499 | .154 | .007 | .001 |

| Panel C: New participants compared to not‐yet participant hospitals (N = 1545) | ||||

| Estimate | 0.008 | 2.901 | 0.040 | 16.497 |

| SE | [0.014] | [3.641] | [0.019] | [7.674] |

| P‐value | .546 | .426 | .035 | .032 |

The table presents estimates from a difference‐in‐differences model as specified in Equation 1. The data come from facility‐level reports from Schedule H, 990 Data. “Offers free care” is defined as offering free care as part of a charity care policy. “Offers discounted care” is defined as offering discounted care, distinct from prompt pay discounts, as part of a charity care policy. Free and discounted FPL thresholds are the maximum federal poverty levels at which individuals may receive charity care under written charity care policies. Panel A compares hospitals that begin participating in 340B between 2012 and 2015 to all other hospitals. Panel B compares hospitals that begin participating in 340B between 2012 and 2015 to a group of reweighted nonparticipating hospitals using average treatment on the treated propensity scores. Panel C uses not‐yet participating hospitals that begin participating in 340B between 2012 and 2015 to those that are currently not participating but participate eventually after 2015 when our sample ends. All estimates were generated using ordinary least squares. Cluster‐robust standard errors are presented below each estimate and are displayed below in brackets. Panels A and B include hospital and state‐year fixed effects. Panel C includes only hospital and year fixed effects.

Table 3 reports the results of difference‐in‐differences models for low‐profit service‐line provision, an alternative measure of this study. Low‐profit service‐line provision does not change after hospitals begin participating in 340B relative to either control group. Although all estimates are no different than zero, the magnitude of the point estimates is mixed in sign across models and the standard errors are quite large. For example, we cannot distinguish between a 9 PP increase in offering trauma and burn care and a 3 PP decrease in the probability of offering this service.

Table 3.

Within‐hospital difference in service‐line provision relative to alternative control groups, 2011‐2015

| Drug and alcohol treatment | Burn and trauma care | Dental care | HIV/AIDS care | Obstetrical care | Psychiatric care | |

|---|---|---|---|---|---|---|

| Panel A: New participants compared to all other hospitals (N = 6775) | ||||||

| Estimate | −0.030 | 0.005 | −0.016 | −0.001 | 0.005 | −0.011 |

| SE | [0.016] | [0.015] | [0.017] | [0.018] | [0.008] | [0.017] |

| P‐value | .058 | .746 | .363 | .978 | .533 | .501 |

| Panel B: New participants compared to nonparticipant hospitals (N = 6662) | ||||||

| Estimate | −0.013 | 0.007 | −0.008 | −0.003 | 0.001 | −0.005 |

| SE | [0.017] | [0.016] | [0.017] | [0.018] | [0.008] | [0.018] |

| P‐value | .454 | .662 | .655 | .873 | .866 | .780 |

| Panel C: New participants compared to not‐yet participant hospitals (N = 1694) | ||||||

| Estimate | −0.018 | 0.005 | −0.018 | −0.021 | 0.005 | −0.009 |

| SE | [0.016] | [0.016] | [0.019] | [0.019] | [0.009] | [0.017] |

| P‐Value | .252 | .768 | .336 | .249 | .566 | .595 |

The table presents estimates from a difference‐in‐differences model as specified in Equation 1. Each dependent variable is an indicator of whether the hospital offers each low‐profit service and comes from the American Hospital Association data from 2011 to 2015. The table presents estimates from a difference‐in‐differences model as specified in Equation 1. Panel A compares hospitals that begin participating in 340B between 2012 and 2015 to all other hospitals. Panel B compares hospitals that begin participating in 340B between 2012 and 2015 to a group of reweighted nonparticipating hospitals using average treatment on the treated propensity scores. Panel C uses not‐yet participating hospitals that begin participating in 340B between 2012 and 2015 to those that are currently not participating but participate eventually after 2015 when our sample ends. Cluster‐robust standard errors are presented below each estimate and are displayed below in brackets. Panels A and B include hospital and state‐year fixed effects. Panel C includes only hospital and year fixed effects. All estimates are generated using ordinary least squares.

We subjected our results to several robustness tests including winsorizing at alternative levels (top and bottom 10th percentiles), limiting to a balanced panel of hospitals observed in every year and omitting each cohort of new participants and found our results were robust to these tests (Table S5A‐C). We found the results were not qualitatively different. We also found no relationship between the DSH patient percentage and charity care around the cut off for eligibility, which suggests that our results for charity care are not a direct result of increases in the DSH patient percentage (Figure S2).

4. DISCUSSION

Although the 340B program has grown to encompass over 40 percent of nonprofit and public hospitals, 28 it is largely an accident of history. The program was created after the introduction of the Medicaid drug rebate program 1990 to extend discounts to a small number of safety‐net hospitals with both low Medicaid populations and large uninsured populations. 50 Congress expected few hospitals would participate in the program, and thus, they were granted wide latitude under the program to use discounts on all patients. 51 Current policy debates about the value of the 340B program hinge upon whether 340B hospitals contribute to the safety net and how much more safety‐net care 340B hospitals provide.

While we did not find that participating in 340B was associated with increased safety‐net engagement as measured by uncompensated care, we did find that hospitals spent more on charity care, offering more discounted care, and at higher‐income eligibility levels through charity care policies. However, the increase in charity care likely did not represent an increase in safety‐net care for two reasons. First, the 21.8 percent increase in charity care identified in this paper translates to a miniscule increase in charity care: about $0.88 M, relative to an average of $4.4 M of charity care spending in the year before participation. Second, the increase in charity care appeared to be offset by reductions in other types of community benefit spending. Our results are partially consistent with anecdotal reports suggesting increased safety‐net engagement, 52 yet we found no support for the claims that 340B results in the offer of high‐value, low‐profit services, at least in the first several years after participation. They are partially consistent with Desai and McWilliams, 4 who found no effect on uncompensated care. Our results also lend support to recent evidence that hospitals may manipulate the DSH patient percentage in order to qualify for 340B. 39

Our paper makes several contributions to the growing literature on the 340B drug discount program. First, stakeholders and academic researchers have struggled to identify a causal effect of hospital participation in 340B. We used a difference‐in‐differences approach that may surmount some existing identification challenges by comparing new participants to hospitals that are not‐yet participating but will eventually participate. 4 This approach may minimize selection bias in estimates of 340B's association with outcomes. Second, our paper considers a broad set of safety‐net engagement measures together rather than just one: uncompensated care. Because charity care spending increases after 340B participation, but bad debt may decrease as individuals are offered more charity care assistance, the two components of uncompensated care move in opposite directions and thus may cancel each other out.

Our paper had several limitations. First, even though we had the best available data, they could not capture all the efforts hospitals may take to contribute to safety‐net care. Detailed information on the number of people receiving safety‐net care or the quality of safety‐net services provided is also unavailable. Our measures only captured whether a service was offered, not whether low‐income and uninsured patients used it. Similarly, we only observed expenditures and not the quality or intensity of care for individual low‐income and uninsured patients. Second, research suggests that hospitals that started participating before 2004 may behave differently than hospitals that participated after 2004. 6 If our estimates could be interpreted as causal, they would represent a local average treatment effect for a specific group of hospitals and may not be generalized to the 198 hospitals that began participating before 2004. Another limitation of these data was that community benefit spending is reported at the hospital tax filing unit level. For multihospital systems, which typically file taxes together, this means we could not separate out community benefit spending for any one hospital. Third, our study considered all new participants as equally affected by the program but it is likely that some hospitals generate more revenue from the program than others. One way to address this heterogeneity would be to estimate the amount of revenue hospitals generated from the program. Unfortunately, such data are not publicly reported and estimates of revenue are beyond the scope of our analysis. Fourth, our analysis took place over a relatively short window, and thus, we were unable to study significantly delayed effects. For example, service lines may take several years to adopt, yet we were unable to analyze association with long‐term outcomes because of the short time span of our data. Fifth, we were unable to consider the association of 340B with safety‐net engagement for non‐DSH hospitals. Critical Access Hospitals, freestanding Cancer, Children's, Medicare‐dependent, Sole Community, and Rural Referral Center hospitals may also participate in the program. However, these hospitals are reimbursed differently and do not report on alternative safety‐net engagement measures, or both. Since their economic incentives might be different and data are not available to assess their safety‐net engagement, we did not include them in the analysis. Sixth, our analysis cannot fully address the possibility that hospitals raise charges after becoming eligible for 340B, thus inflating the value of hospital charity care. We attempted to minimize potential bias by adjusting charity care spending by a cost‐to‐charge ratio; however, if hospitals expand after 340B, their costs could increase and cost‐to‐charge ratios might not change. Finally, and relatedly, there is no clear causal inference design that can be used to estimate one causal effect of the program. We have attempted to advance the literature by minimizing selection bias, yet we do not claim to have estimated a causal effect.

Our paper makes several contributions to the current policy debate on reform of the 340B program. First, our results provide some insight into the likely impacts of 340B‐specific Medicare reimbursement cuts. The Trump administration issued regulations implementing cuts in 2017 that would have reduce physician reimbursements for the administration of 340B‐eligible drugs from the average sales price plus 6 percent to the average sales price minus 22 percent. 13 , 53 340B hospitals successfully blocked the cuts, stating that they would will have been forced to cut back on safety‐net services, lay‐off staff, and even close their emergency rooms. 54 , 55 Although the cuts were not implemented, CMS has since pursued other forms of cuts that would specifically affect 340B hospitals, such as site neutral payments. 56 Our results cast doubt on hospitals' predictions about the effects of such cuts; we did not find that 340B led hospitals to expand the community services provided. Second, our results can put the program's benefit in context to—at least some of—its costs. A recent analysis of Medicare payments for 340B hospitals found that hospitals generated between $550 M and $1.2 B in profit from administering Medicare Part B drugs in 2013. 57 The finding that 340B participation increases hospital charity care by a very small amount (<$1 M) suggests that, even ignoring reductions in other community benefit spending, the associated increase in safety‐net care is small relative to program revenues.

Numerous unanswered questions about the costs and benefits of the 340B program remain. How much of the estimated size of the program in terms of spending ($19.3B in 2018) 58 is borne by taxpayers? Do 340B hospitals benefit even more than other hospitals from the increasing costs of high‐price specialty drugs? 59 How will planned cuts to the safety‐net under the ACA—scheduled to take place October 2019—affect hospital's reliance on 340B and subsequent safety‐net engagement? Does the meager increase in charity care identified in this paper provide a benefit to patients? Our study used the best available data from administrative sources, yet all measures were collected for purposes other than evaluating the 340B program and thus could not directly assess the benefits (safety‐net engagement) nor costs of the program. The National Academies of Science, Engineering, and Medicine, and the Energy and Commerce Committee of the US House of Representatives, the US Senate, the Trump Administration, and several states have proposed increased transparency including reporting program associated savings, revenue, safety‐net engagement activities, and the characteristics of the patient populations served. 60 , 61 , 62 , 63 ,65 These data would also facilitate much‐needed research on the program and foster evidence‐based policymaking.

Supporting information

AuthorMatrix

Appendix

ACKNOWLEDGMENTS

Joint Acknowledgment/Disclosure Statement: This work was supported by the Commonwealth Fund. We wish to thank Gabriela Gracia, Sunita Thapa, and Shiyuan Zhang for excellent research assistance. Nikpay and Buntin are employees of Vanderbilt University Medical Center.

Nikpay SS, Buntin MB, Conti RM. Relationship between initiation of 340B participation and hospital safety‐net engagement. Health Serv Res. 2020;55:157–169. 10.1111/1475-6773.13278

REFERENCES

- 1. MedPAC . Report to congress: overview of the 340B drug pricing program. 2015. http://www.medpac.gov/docs/default-source/reports/may-2015-report-to-the-congress-overview-of-the-340b-drug-pricing-program.pdf?sfvrsn=0. Accessed July 21, 2017.

- 2. Health Resources and Service Administration . Notice regarding section 602 of the Veterans Health Care Act of 1992; Contract Pharmacy Services. 1996. https://www.gpo.gov/fdsys/pkg/FR-1996-08-23/pdf/96-21485.pdf. Accessed October 8, 2018.

- 3. Energy & Commerce Committee . Review of the 340B Drug Pricing Program. Energy & Commerce Committee; 2018:79 https://energycommerce.house.gov/wp-content/uploads/2018/01/20180110Review_of_the_340B_Drug_Pricing_Program.pdf. Accessed January 22, 2018. [Google Scholar]

- 4. Desai S, McWilliams JM. Consequences of the 340B drug pricing program. N Engl J Med. 2018;378(6):539‐548. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5. Jung J, Xu WY, Kalidindi Y. Impact of the 340B drug pricing program on cancer care site and spending in Medicare. Health Serv Res. 2018;53:3528‐3548. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6. Conti RM, Bach PB. The 340B drug discount program: hospitals generate profits by expanding to reach more affluent communities. Health Aff (Millwood). 2014;33(10):1786‐1792. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7. Government Accountability Office . Medicare Part B Drugs: Action Needed to Reduce Financial Incentives to Prescribe 340B Drugs at Participating Hospitals. Government Accountability Office; 2015:1‐40. https://www.gao.gov/assets/680/670676.pdf. Accessed May 17, 2018. [Google Scholar]

- 8. Office of Inspector General . Part B Payments for 340B‐Purchased Drugs. Washington, DC: Office of Inspector General; 2015:32 https://oig.hhs.gov/oei/reports/oei-12-14-00030.pdf. Accessed July 18, 2018. [Google Scholar]

- 9. Vandervelde A, Blalock E. The Oncology Drug Marketplace: Trends in Discounting and Site of Care. Berkeley Research Group; 2017:13 https://www.thinkbrg.com/media/publication/955_955_Vandervelde_COA-2017_WEB_Final.pdf. [Google Scholar]

- 10. Government Accountability Office . Drug Discount Program: Federal Oversight of Compliance at 340B Contract Pharmacies Needs Improvement. Washington, DC: Government Accountability Office; 2018:63 https://www.gao.gov/assets/700/692697.pdf. Accessed July 18, 2018. [Google Scholar]

- 11. Nikpay S, Buntin MB, Conti RM. The 340B program: mandatory reporting, alternative eligibility criteria should be top priorities for congress. Health Aff Blog. October 2017. https://www.healthaffairs.org/do/10.1377/hblog20171021.982593/full/. Accessed May 17, 2018. [Google Scholar]

- 12. 340B Health . 340B Program Helps Hospitals Provide Services to Vulnerable Patients: Results from a Survey of 340B Health Members. 340B Health; 2016:20 https://www.340bhealth.org/files/Savings_Survey_Report.pdf. [Google Scholar]

- 13. American Hospital Association . Hospital groups file lawsuit to stop significant payment cuts for 340B hospitals. https://www.aha.org/presscenter/pressrel/2017/111317-pr-340b-lawsuit.shtml://www.aha.org/presscenter/pressrel/2017/111317-pr-340b-lawsuit.shtml. Accessed August 20, 2018.

- 14. 340B Health . 340B Health strongly opposes proposal to cut 340B hospitals' Medicare part B drug reimbursement – 340B health. Published July 13, 2017. https://www.340bhealth.org/news/340b-health-strongly-opposes-proposal-to-cut-340b-hospitals-medicare-part-b. Accessed August 20, 2018.

- 15. Alliance for Integrity and Reform of 340B (AIR 340B) . The time for strengthening the 340B program is now: patient and policy organizations ask members of congress for increased oversight of the 340B program. March 2017. http://340breform.org/userfiles/FINAL%2520-%2520AIR340B%2520Sign%2520On%2520Letter%2520Release%2520030917%2520(1).pdf. Accessed March 22, 2017.

- 16. Medicaid and CHIP Payment and Access Commission (MACPAC) . March 2017 Report to Congress on Medicaid and CHIP. Washington, DC: MACPAC; 2017. https://www.macpac.gov/wp-content/uploads/2017/03/March-2017-Report-to-Congress-on-Medicaid-and-CHIP.pdf. Accessed January 28, 2018. [Google Scholar]

- 17. Nikpay S, Buchmueller T, Levy HG. Affordable care act Medicaid expansion reduced uninsured hospital stays in 2014. Health Aff (Millwood). 2016;35(1):106‐110. [DOI] [PubMed] [Google Scholar]

- 18. Kenny C, Skaggs J. From here to eternity: the Medicare S‐10 and uncompensated care audits. Presented at the Healthcare Financial Management Association (HFMA); June 24, 2018; Las Vegas, Nevada.

- 19. Medicaid.gov . Medicaid disproportionate share hospital (DSH) payments | Medicaid.gov. U.S. Government. https://www.medicaid.gov/medicaid/finance/dsh/index.html. Accessed March 31, 2019.

- 20. Medicaid and CHIP Payment and Access Commission (MACPAC) . March 2018 Report to Congress on Medicaid and CHIP. Washington, DC: MACPAC; 2018. https://www.macpac.gov/wp-content/uploads/2018/03/Report-to-Congress-on-Medicaid-and-CHIP-March-2018.pdf. [Google Scholar]

- 21. Garthwaite C, Gross T, Notowidigdo MJ. Hospitals as insurers of last resort. Am Econ J Appl Econ. 2018;10(1):1‐39. [Google Scholar]

- 22. Dranove D, Garthwaite C, Ody C. How Do Hospitals Respond to Negative Financial Shocks? The Impact of the 2008 Stock Market Crash. National Bureau of Economic Research; 2013. [Google Scholar]

- 23. Centers for Medicare & Medicaid Services . Hospital form 2552‐10 cost report. https://www.costreportdata.com/instructions/Instr_S100.pdf. Accessed August 20, 2018.

- 24. Department of the Treasury Internal Revenue Service . Instructions for schedule H (Form 990). https://www.irs.gov/pub/irs-pdf/i990sh.pdf. Accessed August 20, 2018.

- 25. Nikpay S, Ayanian JZ. Hospital charity care — effects of new community‐benefit requirements. N Engl J Med. 2015;373(18):1687. [DOI] [PubMed] [Google Scholar]

- 26. Young GJ, Chou C‐H, Alexander J, Daniel Lee S‐Y, Raver E. Provision of community benefits by tax‐exempt U.S. hospitals. N Engl J Med. 2013;368(16):1519. [DOI] [PubMed] [Google Scholar]

- 27. Horwitz JR. Making profits and providing care: comparing nonprofit, for‐profit, and government hospitals. Health Aff (Millwood). 2005;24(3):790‐801. [DOI] [PubMed] [Google Scholar]

- 28. Nikpay S, Buntin M, Conti RM. Diversity of participants in the 340B drug pricing program for US hospitals. JAMA Intern Med. 2018;178:E1‐E3. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 29. Angrist JD, Jorn‐Steffen P. Mostly Harmless Econometrics: An Empiricist's Companion. Princeton, NJ: Princeton University Press; 2009. [Google Scholar]

- 30. Barnes BG, Buchheit S, Parsons LM. Threshold‐based Medicare incentives and aggressive patient reporting in US hospitals. Account Public Interest. 2017;17(1):84‐106. [Google Scholar]

- 31. Barnes BG, Harp NL. The U.S. Medicare Disproportionate Share Hospital Program and Its Effect on Capacity Planning Decisions. Rochester, NY: Social Science Research Network; 2017. https://papers.ssrn.com/abstract=2258695. Accessed May 17, 2018. [Google Scholar]

- 32. Duggan MG. Hospital ownership and public medical spending. Q J Econ. 2000;115(4):1343‐1373. [Google Scholar]

- 33. Office of Inspector General . Wisconsin Physicians Service Insurance Corporation Did Not Properly Settle Indiana Medicare Disproportionate Share Hospital Payments. Washington, DC: Office of Inspector General; 2016:17 https://oig.hhs.gov/oas/reports/region7/71504219.pdf. [Google Scholar]

- 34. Lyons C. Specialty Pharmacy: 5 Ways to Maximize Your 340B Program. Presented at the Virginia Society of Health System Pharmacists; April 7, 2017. Well Partner 5 Ways to Max Your 340B Program.pdf.

- 35. Quality Reimbursement Services . Three things you need to know about disproportionate share (DSH) in 2013. Quality Reimbursement Services: Healthcare Consultants. Published 2013. http://www.qualityreimbursement.com/dsh.html.

- 36. Healthcare Payment Specialists . Solutions: Medicare Disproportionate Share Hospitals. Healthcare Payment Specialists; Published 2017. http://www.healthcarepayment.com/solutions/dsh/#toggle-id-1. [Google Scholar]

- 37. Southwest Consulting Associates . Newborn Assistance Program. Southwest Consulting Associates; Published 2016. https://www.southwestconsulting.net/services/newborn-assistance-program. [Google Scholar]

- 38. Nikpay S, Buntin M, Conti R.Rapid growth in 340B contract pharmacies is unrelated to community level poverty or uninsured rates. October 2018.

- 39. Nikpay S, Conti R, Buntin M. A Prescription for Manipulation? Impact of the 340B Drug Discount Program on Hospitals. Ashecon; 2018. https://ashecon.confex.com/ashecon/2018/webprogram/Paper5891.html. Accessed August 6, 2019. [Google Scholar]

- 40. Alpert A, Hsi H, Jacobson M. Evaluating the role of payment policy in driving vertical integration in the oncology market. Health Aff (Millwood). 2017;36(4):680‐688. [DOI] [PubMed] [Google Scholar]

- 41. Medicare Learning Network . Medicare disproportionate share hospital. September 2017. https://www.cms.gov/Outreach-and-Education/Medicare-Learning-Network-MLN/MLNProducts/downloads/Disproportionate_Share_Hospital.pdf. Accessed April 3, 2019.

- 42. Singh SR, Young GJ, Daniel Lee S‐Y, Song PH, Alexander JA. Analysis of hospital community benefit expenditures' alignment with community health needs: evidence from a national investigation of tax‐exempt hospitals. Am J Public Health. 2015;105(5):914‐921. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 43. Bard GV. Spelling‐error tolerant, order‐independent pass‐phrases via the Damerau‐levenshtein string‐edit distance metric In: Proceedings of the Fifth Australasian Symposium on ACSW Frontiers – Volume 68. ACSW '07. Darlinghurst, Australia: Australian Computer Society, Inc.; 2007:117‐124. http://dl.acm.org/citation.cfm?id=1274531.1274545. Accessed January 19, 2017. [Google Scholar]

- 44. Ghosh D, Vogt A. Outliers: an evaluation of methodologies In: Joint Statistical Meetings. San Diego, CA: American Statistical Association; 2012:3455‐3460. [Google Scholar]

- 45. Horwitz JR, Nichols A. Hospital ownership and medical services: market mix, spillover effects, and nonprofit objectives. J Health Econ. 2009;28(5):924‐937. [DOI] [PubMed] [Google Scholar]

- 46. Abadie A. Semiparametric difference‐in‐differences estimators. Rev Econ Stud. 2005;72(1):1‐19. [Google Scholar]

- 47. Stuart EA, Huskamp HA, Duckworth K, et al. Using propensity scores in difference‐in‐differences models to estimate the effects of a policy change. Health Serv Outcomes Res Methodol. 2014;14(4):166‐182. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 48. Weisstein EW.Bonferroni correction. http://mathworld.wolfram.com/BonferroniCorrection.html. Published 2018. Accessed October 3, 2018.

- 49. Weisstein EW. Bonferroni correction. http://mathworld.wolfram.com/BonferroniCorrection.html. Accessed March 31. 2019.

- 50. Hirsch BR, Balu S, Schulman KA. The impact of specialty pharmaceuticals as drivers of health care costs. Health Aff (Millwood). 2014;33(10):1714‐1720. [DOI] [PubMed] [Google Scholar]

- 51. Mulcahy AW, Armstrong C, Lewis J, Mattke S.The 340B prescription drug discount program. Published 2014. https://www.rand.org/pubs/perspectives/PE121.html. Accessed July 21, 2017.

- 52. 340B Health . Evaluating 340B Hospital Savings and Their Use in Serving Low‐Income and Rural Patients: Results from 340B Health's 2017 Annual Survey. Washington, DC: 340B Health; 2018. https://www.340bhealth.org/files/2017_Annual_Survey_Report_final.pdf. [Google Scholar]

- 53. Federal Register . Medicare Program; Part B Drug Payment Model. Federal Register; Published March 11, 2016. https://www.federalregister.gov/documents/2016/03/11/2016-05459/medicare-program-part-b-drug-payment-model. Accessed March 31, 2019. [Google Scholar]

- 54. Centers for Medicare & Medicaid Services . Medicare Program: Hospital Outpatient Prospective Payment and Ambulatory Surgical Center Payment Systems and Quality Reporting Programs. Federal Register; Published July 20, 2017. https://www.federalregister.gov/documents/2017/07/20/2017-14883/medicare-program-hospital-outpatient-prospective-payment-and-ambulatory-surgical-center-payment. Accessed May 18, 2018. [Google Scholar]

- 55. Nierengarten MB. Policy Change: The Impact of 340B Cuts on Hospitals | Managed Health Care Connect. Managed Health Care Connect; Published January 2018. https://www.managedhealthcareconnect.com/article/policy-change-impact-340b-cuts-hospitals. Accessed January 25, 2018. [Google Scholar]

- 56. Conti RM, Nikpay SS, Buntin MB.Hospital 340B revenues and profits from Medicare patients, 2013‐2016. May 2019. [DOI] [PMC free article] [PubMed]

- 57. Fein AJ.The 340B program reached $19.3 billion in 2017—as hospitals' charity care has dropped. May 2018. https://www.drugchannels.net/2018/05/exclusive-340b-program-reached-193.html. Accessed March 31, 2019.

- 58. Howard DH, Bach PB, Berndt ER, Conti RM. Pricing in the market for anticancer drugs. J Econ Perspect. 2015;29(1):139‐162. [DOI] [PubMed] [Google Scholar]

- 59. Bucshon L.Text – H.R.4710 – 115th Congress (2017‐2018): 340B PAUSE Act. 2017. https://www.congress.gov/bill/115th-congress/house-bill/4710/text.

- 60. National Academies of Sciences, Engineering, and Medicine . Making Medicines Affordable: A National Imperative. Washington, DC: The National Academies Press; 2017. [PubMed] [Google Scholar]

- 61. United States, Executive Office of the President, United States, Office of Management and Budget . A Budget for a Better America: Fiscal Year 2020 Budget of the U.S. Government. 2019.

- 62. 340B In the spotlight – key program developments. The National Law Review; https://www.natlawreview.com/article/340b-spotlight-key-program-developments. Accessed September 5, 2019. [Google Scholar]

- 63. Grassley introduces bill to bring transparency to the 340B prescription drug program | Chuck Grassley. https://www.grassley.senate.gov/news/news-releases/grassley-introduces-bill-bring-transparency-340b-prescription-drug-program. Accessed September 5, 2019.

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

AuthorMatrix

Appendix