Abstract

Food safety events threaten not only consumers’ health, but also the value of associated firms. While previous studies examined the impact of food safety events on consumer demand for products, little attention has been paid to the impact on the market value of firms. Using the event study method (ESM), this study investigated abnormal returns (ARs) and cumulative abnormal returns (CARs) of firms associated with 40 food safety events over the past 25 years in the U.S. The results of this study demonstrated the magnitude and duration of the impact of food safety events on firm value. Moreover, firm-specific factors (past history and firm size) and situational factor (media attention) were found to influence the magnitude of the impact. This study contributes to the hospitality literature by extending the knowledge of the impact of food safety events and its practical implications for effective crisis management strategies for food-related firms.

Keywords: Food safety event, Firm value, Event study method, Abnormal return, Crisis management

1. Introduction

The past few decades have witnessed several food safety events turn into major national crises. According to recent estimates by the Centers for Disease Control and Prevention (CDC), food safety events cause 48 million illnesses, 128,000 hospitalizations, and 3000 deaths each year in the United States (Scallan et al., 2011). The Foodborne Outbreak Reporting System (FoodNet) noted that 59% of reported foodborne illness outbreaks were associated with food-related firms such as restaurants, food manufacturers, and food distributors (CDC, 2005). The association between food safety events and firms has been recognized in the business and economics literature. The impact of foodborne illnesses on firms has been examined from various perspectives, such as consumer demand (Piggott and Marsh, 2004, Hammit and Haninger, 2007) and changes in purchase intention (Maynard et al., 2008). Despite these efforts, the magnitude and duration of food safety events on firm value has not received sufficient research attention. Further understanding as to what extent food safety events impact the associated firms, how long the impact lasts, and which factors contribute to the impact is of paramount importance for several reasons.

First, understanding the seriousness of food safety events is helpful for designing effective crisis management strategies. The duration of a food safety event impact on firms, which is an indicator of the seriousness of the event, is also of great interest to crisis managers. This lack of understanding regarding the seriousness and duration of food safety events can cause food-related firms to use inappropriate crisis management strategies. Firms that disregard or underestimate the seriousness of an event might face an enormously negative situation due to inappropriate crisis management tactics. On the other hand, this lack of understanding can also cause food-related firms to invest unnecessary resources or to overreact in dealing with food safety event outbreaks.

Second, although there are several ways to measure the impact of a food safety event, the stock market value of the firm provides essential information. In order to investigate the seriousness or duration of food safety events, firms can take actions such as conducting surveys to examine consumer perceptions of the event or gathering information about the number of people affected by the event. While those measures cannot promptly capture the impact of food safety events, stock prices and stock returns show immediate market reactions based on the market's evaluation of the seriousness of potential impacts on a firm's profitability. Acknowledging that many food safety events occur accidentally, the need to examine immediate responses from the stock market is increasing. Thus, examining firm value through stock return movements can provide essential information to understand the impact of food safety events (Hsu and Jang, 2007).

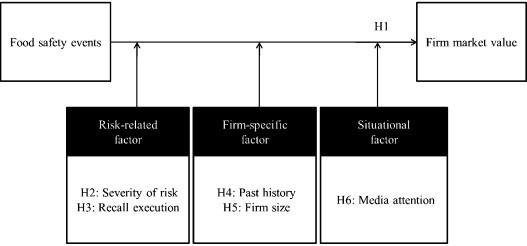

Third, identifying specific factors related to the seriousness and duration of the impact of food safety events may also enable crisis managers to prepare for the necessary reactions to such events. Because every event occurs in different circumstances, there are several factors, risk-related, firm-specific, and situational, that may influence the impact of events. First, risk-related factors are fundamental factors influencing consumers’ perceptions of the food safety event. For example, the severity of risk or the number of people sickened may influence the magnitude of the impact on associated firms. Whether a firm executes a recall of products or not may also affect the duration of the impact. Second, firm-specific factors, such as firm size or past history, also influence the impact of food safety events. For instance, whether a firm has a past history with foodborne illness outbreaks may influence consumers’ perceptions of the food safety event. Finally, situational factors may affect the seriousness and duration of the food safety event's impact on firms. The proliferation of the Internet enables information to be spread quickly and broadly, which can foster crisis communication. However, negative or distorted information can also spread even quicker than positive or correct information. In this sense, the level of media attention may heavily influence consumer responses, which are reflected in the market evaluation of a firm. The more media attention an event garners, the more negative responses are associated with the firm, which can negatively impact firm value. Thus, this study investigates how risk-related, firm-specific, and situational factors contribute to the impact of food safety events on the market value of firms.

As noted earlier, previous studies (e.g., Piggott and Marsh, 2004, Hammit and Haninger, 2007, Maynard et al., 2008) examined the influences of food safety events, but little attention has been paid to the financial impact of such events on the implicated firms. To fill the research gap, this study examines whether food safety events have a significant impact on the stock returns of food-related firms. Specifically, the objectives of this study are (1) to examine the magnitude and duration of impacts of food safety events on the market returns of food-related firms and (2) to identify risk-related factors, firm-specific factors, and situational factors that contribute to stock price movements of food-related firms in response to food safety events. In view of the lack of research on the financial impact of food safety events, this study contributes to the literature by extending our understanding of the consequences of food safety events and by providing empirical evidence of the duration of the impacts for food-related firms. This study also offers important information that may help crisis managers design and implement effective crisis communication strategies. Moreover, this study can help motivate employees in food-related industries to ensure the safety of foods by demonstrating the magnitude of the negative impact and potential harm to the equity of a firm.

2. Related literature and hypotheses

2.1. Impact of food safety events on stock prices of firms

The largest and deadliest food crisis in recent U.S. history was an Escherichia coli (E. coli) scare associated with the Jack in the Box restaurant chain in 1993. The food safety crisis resulted in the deaths of four children and foodborne illnesses of 700 people in multiple states that year. As a result of the crisis, Jack in the Box lost millions of dollars in sales revenue (Braun-latour et al., 2006). In 2000, Chi-Chi's and Sizzler were involved in foodborne illnesses that led to the companies’ eventual bankruptcy. ConAgra, a food manufacturer, was involved in an E. coli outbreak in 2002, which resulted in 19 people falling sick after eating tainted hamburgers. The event forced ConAgra to recall over 19 million pounds of ground beef, the third largest recall in the U.S. history (Becker, 2002). Evidently, food safety events can have a negative impact on the financial performance of food-related firms. However, little attention has been paid to the degree or duration of the impact of food safety events on firms.

The impact of food safety events on firm performance has primarily been examined using metrics such as decreases in consumers’ food purchase intentions (Lobb et al., 2007) and reductions in food consumption (Maynard et al., 2008). While a number of studies were conducted from a consumer demand perspective, the financial impacts of food safety events on firm performances have garnered little attention. For example, an event study by Henson and Mazzocchi (2002) examined the impacts of government announcements regarding a possible link between bovine spongiform encephalopathy (BSE), which is commonly called mad cow disease, and human health on agriculture economies in U.K. The study found that the government announcement caused significantly negative abnormal returns not only for beef processors, but also for processors of dairy products, animal feed, and pet foods as well. The study suggested that abnormal stock returns signal negative impacts of food safety events by reflecting immediate market evaluations of the firm's future value. Moreover, the authors highlighted the need to consider an extended period rather than a single day in assessing the effect of food safety related information on market evaluations. Because the impact of food safety related information on consumer demand can be delayed due to the continuous process of information collection and assimilation in response to uncertainty, examining longer-term cumulative abnormal returns is necessary. In addition, van Ravenswaay and Hoehn (1991) asserted that long term information may generate greater impact on product markets. Accordingly, understanding the financial impacts of food safety events is becoming increasingly important.

2.2. Event study method (ESM) and hypotheses

2.2.1. Abnormal return (AR) and cumulative abnormal return (CAR)

The event study method (ESM) has been widely used to estimate the financial impact of particular events on firms’ stock returns, such as product recall announcements (Chen et al., 2009, Thomsen and McKenzie, 2001), merger and acquisition announcements (Dodd and Warner, 1983, Hsu and Jang, 2007), economic news (Chan, 2003), and a banking crisis (Miyajima and Yafeh, 2007). In essence, unexpected events or crises were found to generate significant negative abnormal stock returns, which reflect the market's negative evaluation of a firm's future value. Previous hospitality research has examined the impacts of negative events, such as terrorism on hospitality stocks (Chang and Zeng, 2011), food recalls on food-related firms (Salin and Hooker, 2001), the Severe Acute Respiratory Syndrome (SARS) outbreak on hotel stocks (Chen et al., 2007), and IT news on hospitality stocks (Lee and Connolly, 2010). The advantage of using ESM is that it identifies stock price movements due to firm-specific events. In addition, ESM captures immediate market reactions that are reflected in daily stock returns. Moreover, ESM makes it possible to examine the cumulative impacts of specific events, indicating the duration of the impact of food safety events on associated firms. Thus, ESM is an appropriate method for examining the impact of food safety events on firm value.

Using ESM, we calculated abnormal return (AR), an indicator of the impact of an event, as the difference between actual returns and expected returns around the time of the event. If the value of AR is positive, the event can be considered desirable and the future profitability of the firm is positive. If the value of AR is negative, the event is unfavorable and leads to the prediction of negative future profitability. Cumulative abnormal returns (CARs) indicate the cumulative impacts of particular events. Previous research suggests that the initial press announcement does not provide sufficient information to investors because investors are not able to accurately gauge the response to the events (Wiles and Danielova, 2009). Extending the event window is suggested in order to judge cumulative impacts and can be applied to the case of food safety events (Wiles and Danielova, 2009). When risk is considered minimal, stock prices may not react to the event after a press announcement of the event. Yet if the risk is viewed as severe, investors may evaluate the value of the firm significantly negatively, resulting in significant abnormal returns. Accordingly, this study used a long-term event window for calculating abnormal returns (ARs) and cumulative abnormal returns (CARs) after the event outbreak date. The prediction is summarized as below:

H1

The outbreak of a food safety event is negatively associated with changes in the market value of the firm in terms of daily abnormal stock returns (ARs) and cumulative abnormal stock returns (CARs).

2.2.2. Risk-related factor

Severity of risk: Protection motivation theory (Rogers, 1975) posits that consumers’ intentions to protect themselves from harm increase as a function of the severity of a risk (seriousness of adverse consequences) and vulnerability to the risk (probability of being exposed to risk). Based on predicted reactions from the public, the market value of a firm is evaluated depending on the severity of the risk. If stakeholders perceive the risk as severe, the value of the firm will be evaluated more negatively. Conversely, if the level of risk is low, the market value of the firm will be less negative.

According to the news archive of Marler Clark (Marler Clark website), a leading law firm in foodborne illness outbreaks, lawsuits have been filed in response to 147 foodborne illness outbreaks in the United States. The lawsuits were in connection with the following illnesses over the past 25 years: E. coli (71), Hepatitis A (13), norovirus (5), Salmonella (47), Shigella (7), Listeria (2), and one incident each of botulism, Campylobacter, and Cryptosporidium. The U.S. Morbidity and Mortality Weekly Report (MMWR) (CDC, 2005) estimated that Salmonella was the most common cause of foodborne illness related hospitalizations, causing 62% of reported hospitalizations, followed by E. coli (17%), and the norovirus (7%). Considering that the market evaluation of firm value is based on the perceived level of risk, the financial impact of each event is expected to vary depending on the severity of risk. The following hypothesis is proposed:

H2

The impact of a food safety event on the market value of a firm varies depending on the severity of risk (high versus low).

Recall execution: Crisis management strategies are important in dealing with unexpected crises that can have a negative impact on a firm. The recall of food products has been considered the most proactive response strategy for food-related firms (Israeli, 2007). In essence, the recall strategy was found to influence consumer perceptions in an affirmative way by reducing perceptions of risk (Siomkos and Kurzbard, 1994). Thus, food safety events may not necessarily lead to significant negative stock returns when proactive recalls are properly executed. However, Salin and Hooker (2001) and Chen et al. (2009) asserted that proactive recall strategies generated more negative abnormal returns than passive recalls because the market tends to evaluate the proactive recall announcement as a signal of a severe crisis. Given the mixed findings of the impact of food recall announcements on stock returns, we hypothesized that recalls would lead to different abnormal return patterns when compared to cases without recalls. Thus, we proposed the following hypothesis:

H3

The impact of a food safety event on the market value of a firm varies depending on the execution of the recall (recall versus no-recall).

2.2.3. Firm-specific factor

Past history: Situational crisis communication theory (SCCT) argues that a past crisis is a critical factor shaping consumers’ perceptions, which determines an organization's reputational threat (Coombs and Schmidt, 2000, Coombs, 2004). SCCT asserted that a history of crises has an indirect effect on the relationship between crisis responsibility and reputational threat to an organization (Coombs, 2004). A past crisis similar to a current crisis indicates that the crisis occurs regularly rather than irregularly, resulting in higher crisis attribution or responsibility. If a firm is perceived as highly responsible for a crisis outbreak, people are more likely to have a negative reaction compared to a firm with no crisis history. Due to the influence of past crisis history on reputational threat, a firm must determine its crisis response strategies accordingly. This notion is used to design theory-based matching systems between response strategy and crisis situation in order to protect an organization's reputation. Different crisis response strategies may have different effects on firm value. Moreover, a consumer's long-term memory system may influence information processing in response to food crises. Resonance theory (Wan, 2008) contends that people process information through an automatic cognitive procedure when they make an association between a stimulus and their long-term memory. People tend to make an association between a firm and an event more readily when the event occurs repeatedly. A firm that has been associated with food safety events in the past may elicit more negative responses because people more easily associate the firm with the negative event. Thus, a past history with food safety events will be associated with more negative abnormal stock returns. The hypothesis is summarized as follows:

H4

The impact of a food safety event on the market value of a firm will be more negative for firms with a past record of food safety events than for those with no past record.

Firm size: Previous studies demonstrated the effect of firm size on stock returns (Grant, 1980, Atiase, 1985). Some studies (e.g., Salin and Hooker, 2001) found that firm size had a positive effect, suggesting that large firms benefit from brand equity and reputation. In particular, the negative effect of a recall strategy was more severe and immediate for smaller firms than larger firms (e.g., Salin and Hooker, 2001). In addition, consumers perceived less risk of failure in highly reputable firms than in less reputable firms (Roehm and Brady, 2007). In contrast, negative effects of firm size were also observed. For example, smaller firms showed larger positive excess stock returns than larger firms in response to earning announcements (Grant, 1980, Atiase, 1985) and dividend increase announcements (Bajaj and Vijh, 1995). In negative situations such as crisis or service failures, consumers had more negative reactions to the failure of large firms (high equity brands) than small firms (low brand equity brands) based on the perceived betrayal of a firm they trusted (Gregoire et al., 2009). Moreover, Borde et al. (1999) argued that more information is available for large firms listed on the New York Stock Exchange (NYSE) than small firms listed on the American Stock Exchange (AMEX). This information asymmetry may also have a negative influence for large firms in a crisis situation. Thus, we hypothesized that larger firms would have more negative abnormal stock returns than smaller firms in response to food safety event outbreaks. The hypothesis is presented as below:

H5

The impact of a food safety event on the market value of a firm is greater on large firms than small firms.

2.2.4. Situational factor

Media attention: There is a little doubt that the media plays an active role in disseminating food-safety related information to the general public. The importance of the media in shaping consumers’ perceptions and behaviors has been studied since the argument of McLuhan (1964, p. 8) “the medium is the message”. McLuhan (1964) asserted that a variety of forms of media such as print media (e.g., newspaper, tabloid magazine), audio media (e.g., radio), and visual media (e.g., television, on-line video clips) are critical factors influencing social discourse. Due to the recent technological developments, the forms of media have become more diverse including social media which is becoming one of the major communication tools (Syed-Ahmad and Murphy, 2010). The user-created nature of social media may increase the danger of disseminating negative information, which limits the controllability of firms under crisis situations (Palen, 2008). Due to the diverse forms of media serving as communication channels, the influence of media on the general public is increasing.

The efficient market assumption is based on the notion that news is immediately incorporated into stock prices and every trader is provided with the same information (Fama, 1970). However, in reality information asymmetry has been detected, resulting in unpredictable stock price movements. In studying the impact of media on stock price movements, there are two types of traders, noise traders who hold random beliefs about future value of firms and rational arbitrageurs who hold systematic (Bayesian) beliefs (Tetlock, 2007). Information delivered by media may contain both noise and factual information. Investors make decisions based on their evaluation of the proportion of fact and noise. In order to investigate the impact of media reporting on stock returns, Tetlock (2007) examined the relationship between the new contents of the Wall Street Journal and daily stock returns, asserting that high media pessimism, such as negative or vague words, predicts temporary decreases in stock returns. Unlike studies focusing on financial crisis news (Swary, 1986, Ellis and Lewis, 2000), the effect of other types of crisis-related information may display different patterns. For example, Chen et al. (2007) examined stock reactions of hotels in Taiwan to the outbreak of Severe Acute Respiratory Syndrome (SARS), an infectious disease caused by a virus resulting in acute respiratory distress. The results of Chen et al.’s (2007) study indicated significant negative abnormal returns persisting over 30 days past the outbreak. Although the study did not examine the role of media in reporting SARS, media may play a critical role in delivering and spreading related information to the public that resulted in the negative influence on hotel stocks. Thus, this study hypothesized the effect of media attention on stock returns of food-related firms as follows:

H6

The impact of a food safety event on the market value of a firm varies depending on the level of media attention (high versus low).

The hypothesized relationships concerning the impact of food safety events on firm value are illustrated in Fig. 1 .

Fig. 1.

A theoretical model of food safety events and firm value.

3. Methodology

3.1. Variables

In order to model potential factors related to firm value and food safety events, five dummy variables were used in the analyses. As shown in Table 1 , severity of risk was determined by whether the number of people sickened/killed was under 50 (low: 0) or over 50 (high: 1) following the guidance of FoodNet released by the Centers for Disease Control and Prevention (CDC, 2005). Recall execution was coded as either a recall was announced (recall: 1) or not (no recall: 0), and past history was categorized as whether the company had been involved in any foodborne illness in the past (with history: 1) or not (no history: 0) based on the archival data provided by the Marler Clark law firm. Firm size was determined by whether the sales revenue was under the mean of sampled firms (small firms: 0) or over the mean (large firms: 1) following the guidance of Chen et al. (2009). Lastly, media attention was determined by the number of news reports covering the outbreak: under 100 (low media attention: 0) or over 100 (high media attention: 1) which divided the sampled firms into two groups. The news reports were retrieved using LexisNexis database by identifying “all news” which contains the search keywords that were combined with restaurant name and foodborne pathogen. For example, ‘Taco Bell and E. coli” was used as a keyword to identify news reports covering the Taco Bell events associated with E. coli. Operationalization of the variables is summarized in Table 1.

Table 1.

Operationalization of variables.

| Factor | Hypothesis/variable | Operationalization |

|---|---|---|

| Risk-related factor | H2: Severity of risk | Whether the number of people sickened/killed is under 50 (low severity: 0), or over 50 (high severity: 1) |

| H3: Recall execution | Whether a recall was announced (recall: 1) or not (no recall: 0) | |

| Firm-specific factor | H4: Past history | Whether the company has been involved in any of foodborne illness events in the past (with history: 1) or not (no history: 0) |

| H5: Firm size | The sales revenue (in billions of U.S. dollars) at the time of event outbreaks is under the mean of sampled firms (small firms: 0), or over (large firms: 1) | |

| Situational factor | H6: Media attention | The number of news reporting covering the outbreak is under 100 (low media attention: 0), or over 100 (high media attention: 1) |

This study determined firm value based on daily stock prices, instead of accounting-based performance measures such as return on assets (ROA) and return of equity (ROE), in order to measure the impact of the food safety events. Accounting data are available on a quarterly basis, which limits the ability to capture the impact of specific events. In contrast, stock prices reflect immediate market reactions to any event, so stock price returns are a good indicator of the market's evaluation of a firm's value (Fama, 1970, Hsu and Jang, 2007). Thus, examining the pattern of stock price returns in response to food safety events would provide evidence of significant short-term negative impacts of food safety events on firm value. Furthermore, identifying risk-specific, firm-specific and situational factors contributing to stock price movements provides valuable insight to the financial impacts of food safety events on food-related firms.

3.2. Event date and data

The event outbreak date is defined as the first date information regarding the food safety event was released via any media. One unique feature of food safety events is the gradual spread of the information. This is due to a typical pattern in news reporting about food safety events concerning victim identification, examination, and confirmation. The reporting is typically initiated by identifying the victims, then examination procedures are conducted by government agencies, and, finally, the cases and risk exposures are confirmed. A restaurant's name can emerge at any stage of news reporting and the impact may vary depending on how many investors view the risk as severe. The involvement of restaurants in food risks at the initial stage might generate less negative response compared to when the restaurant gets highly involved in food risks at the confirmation stage.

First, we obtained information regarding outbreak dates from the case archive on the Marler Clark's website which is the leading law firm in foodborne illness related lawsuits. In order to ensure the accuracy of the information, two researchers independently conducted an extensive search using Google News Archive. If any news release occurred prior to the outbreak date obtained from the Marler Clark's web site, the outbreak date was changed to the news release date.

In order to eliminate external factors, we removed firms associated with other events that might influence abnormal stock price movements, as suggested by McWilliams and Siegal (1997). Using the Factiva database, we eliminated firms associated with earnings, mergers and acquisitions, spin-offs, stock splits, changes in key executives, layoff announcements, restructuring, lawsuits, new product announcements, regulatory announcements, and unexpected dividend changes during the period from 4 days before to 2 days after the identified outbreak date. This procedure follows recommendations by Wiles and Danielova (2009). After the elimination, a total of 40 food-related firms with food safety events remained in the sample. Of the 40 cases of food safety events, 25 cases were associated with E. coli which was the most common cause of food safety events, followed by Salmonella associated with 11 cases, and 4 cases of hepatitis A. There were a variety of foods associated with foodborne illnesses such as ground beef, juice, coleslaw, lettuce, and spinach. In terms of types of operations, 19 cases were associated with restaurants (e.g., Yum! brands, McDonald's), 13 cases with food manufacturers (e.g., ConAgra, Dole), and 8 cases with food retailers (e.g., Wal-mart) (Table 2 ).

Table 2.

Sample of cases included in data analysis.

| Year | Company | FBI | Outbreak date | Operation type | Recall | Number of illness (confirmed cases) | Stock ticker |

|---|---|---|---|---|---|---|---|

| 1993 | Jack in the Box | E. coli | January 18, 1993 | Restaurant | Yes | 700 | JACK |

| 1996 | Odwalla | E. coli | October 30, 1996 | Food manufacture | Yes | 65 | ODWA |

| 2000 | Carl's Jr restaurant | Hepatitis A | February 17, 2000 | Restaurant | No | 29 | CKR |

| 2000 | Sizzler | E. coli | July 24, 2000 | Restaurant | No | 64 | SZ |

| 2002 | ConAgra | E. coli | June 30, 2002 | Food manufacture | Yes | 46 | CAG |

| 2005 | Dole | E. coli | September 30, 2005 | Food manufacture | Yes | 23 | DOLE |

Daily stock returns were obtained from the University of Chicago's Center for Research in Security Prices (CRSP). Following the guidance of Cowan (2003), estimates of the parameters of the market model were calculated over an estimation window of 275 trading days (one calendar year) ending 20 days before the event using the Center for Research in Security Prices equal-weighted index.

3.3. Event study method (ESM)

In order to calculate AR and CAR, we first obtained one-month stock price data after the beginning date of the forty event outbreaks. The 30-day period since the initial date of outbreaks was used for an event window.

The market model (MM) was chosen to measure the expected returns (ERs) of firms’ stocks. First, the firm's stock return was regressed against the return of market index derived from S&P 500 in order to control for the overall market effects (Eqs. (1), (2)).

| (1) |

| (2) |

R j,t, is the return of restaurant firm's stock j on day t; P j,t, is the closing price of stock j on day t; and R m,t, is the return of market on day t.

The expected return (ER) was obtained by conducting ordinary least squares (OLSs) regression analysis (Eq. (3)). Finally, abnormal return (AR) was calculated by subtracting the expected return from the stock return (Eq. (4)). The value of AR indicates how the stock return has changed due to the firm-specific event separately from overall market movements.

| (3) |

| (4) |

The ESM suggests that a post event period that is too long will not be accurate due to the possibility of external factors occurring in the same period. As such, this method allowed us to measure the impact of an event during a relatively short post event period. Accordingly, we examined stock prices within one month after the outbreak of an event. For the data analysis, we performed a series of t-tests using SPSS (Statistical Package for the Social Sciences). In order to examine the seriousness of food safety event impacts, we tested whether AR (or CAR) since the outbreak is significantly different from zero or not. To achieve the goal, the t-test was considered the most appropriate method to determine the significance of difference between AR (or CAR) and zero.

4. Results and discussion

4.1. Impacts of food safety events on food-related firm values

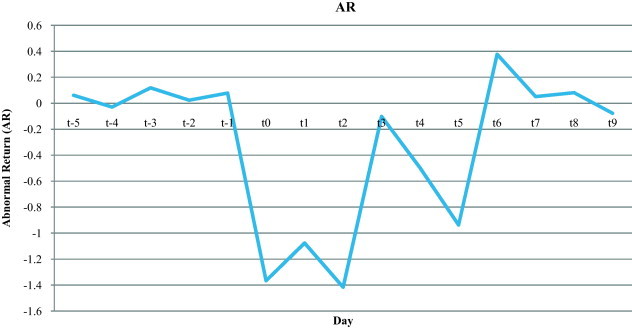

Table 3 presents the results of event study analyses on daily abnormal returns of firms in response to food safety events. Abnormal returns (ARs) were calculated as the difference between expected stock returns and actual stock returns. Cumulative abnormal returns (CARs) were calculated as the sum of ARs. Negative AR or CAR indicates the negative impact of an event on firm value. A t-test was performed to investigate whether AR or CAR is significantly different from zero, since abnormal returns may not be zero if significantly influenced by any events.

Table 3.

Average abnormal returns (ARs) for food safety events.

| Day | Abnormal returns (ARs) |

t-Statistics | p-Value | |

|---|---|---|---|---|

| Mean | SD | |||

| t−5 | .061 | 2.094 | .188 | .852 |

| t−4 | −.029 | 2.236 | −.084 | .934 |

| t−3 | .119 | 2.844 | .268 | .790 |

| t−2 | .133 | 2.051 | .977 | .085 |

| t−1 | .078 | 1.637 | .085 | .400 |

| t0 | −1.366 | 5.711 | −1.532 | .133 |

| t1 | −1.076 | 2.107 | −3.269 | .002** |

| t2 | −1.416 | 3.618 | −2.508 | .016* |

| t3 | −.101 | 3.123 | −.208 | .836 |

| t4 | −.498 | 1.653 | −1.928 | .061 |

| t5 | −.936 | 3.962 | −1.514 | .138 |

| t6 | .376 | 4.640 | .520 | .606 |

| t7 | .051 | 2.539 | .129 | .898 |

| t8 | .081 | 3.184 | .164 | .871 |

| t9 | −.077 | 2.099 | −.237 | .813 |

| t10 | −.351 | 2.166 | −1.038 | .306 |

t0, the day when event outbreaks and tn, nth day since the outbreak day (t0).

p < .05.

p < .01.

***p < .001.

As shown in Fig. 2 , significant negative abnormal returns were found on the days t 1 (t = −3.269, p < .01) and t 2 (t = −2.508, p < .05), suggesting that serious negative impacts on firm value exist once food safety events occur; hence, Hypothesis 1 was supported. The result also indicates that a one-day lag effect exists because there were no significant abnormal returns on the event outbreak date (t 0). As presented in Table 4 and Fig. 3 , cumulative abnormal returns (CARs) showed the overall duration of the impact of food safety events. CARs were found to be significantly negative until the 57th day after the outbreak, and negative CARs were still detected until 254th day. Afterward, positive CARs were consistent, implying that firms fully recovered from the events. Considering that there is an average of 252 stock trading days a year, it takes approximately a year for a firm to fully recover from a food safety event.

Fig. 2.

Abnormal returns (ARs) for food safety event outbreaks.

Table 4.

Cumulative abnormal returns (CARs) for food safety events.

| Event window | Cumulative abnormal returns (CARs) |

t-Statistics | p-Value | |

|---|---|---|---|---|

| Mean | SD | |||

| t0 − t1 | −2.483 | 4.544 | −3.456 | .001** |

| t0 − t2 | −3.929 | 5.821 | −4.269 | .000*** |

| t0 − t3 | −3.957 | 6.508 | −3.846 | .000*** |

| t0 − t4 | −4.408 | 7.029 | −3.966 | .000*** |

| t0 − t5 | −5.291 | 8.931 | −3.747 | .001** |

| ≈ | ||||

| t0 − t10 | −5.170 | 10.514 | −3.110 | .003** |

| ≈ | ||||

| t0 − t20 | −5.392 | 10.784 | −3.162 | .003** |

| ≈ | ||||

| t0 − t30 | −5.508 | 12.494 | −2.788 | .008** |

| ≈ | ||||

| t0 − t57 | −6.812 | 20.386 | −2.060 | .046* |

| t0 − t58 | −6.623 | 20.476 | −1.994 | .054 |

| t0 − t59 | −5.656 | 20.340 | −1.714 | .095 |

| ≈ | ||||

| t0 − t253 | −.827 | 38.293 | −.118 | .907 |

| t0 − t254 | −.405 | 35.532 | −.063 | .951 |

| t0 − t255 | .756 | 34.248 | .121 | .905 |

| t0 − t256 | 1.296 | 33.874 | .210 | .835 |

| ≈ | ||||

| t0 − t370 | 5.008 | 37.437 | .682 | .501 |

| t0 − t371 | 5.568 | 38.135 | .745 | .463 |

p < .05.

p < .01.

p < .001.

Fig. 3.

Cumulative abnormal returns (CARs) for food safety event outbreaks.

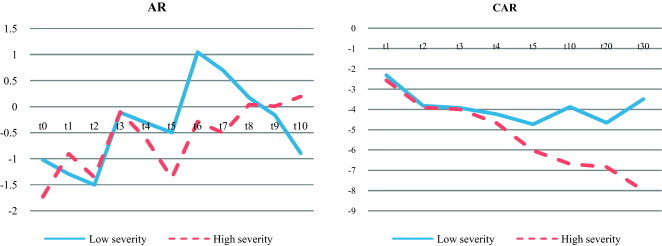

4.2. Severity of risk

To test Hypothesis 2 regarding the severity of risk, the number of people who were ill or died from food safety events was used as an indicator of risk severity (Table 5 ). One-way ANOVA was used to examine the difference in means among the divided two groups. Non-parametric tests were also performed to cross-validate the results of one-way ANOVA because the sample size of each group was relatively small. A Mann–Whitney U test was utilized for the first test since there were two groups to compare.

Table 5.

Impacts of severity of risk (number of people sickened or died) on AR and CAR.

| Descriptive statistics |

Parametric test (high severity risk − low severity risk) |

Non-parametric test (high severity risk − low severity risk) |

||||||

|---|---|---|---|---|---|---|---|---|

| Low severity (n = 20) | High severity (n = 20) | F | Sig. | Mann–Whitney U test | Z | Sig. | ||

| ARn | t0 | −1.020 | −1.729 | .147 | .704 | 166 | −.92 | .358 |

| t1 | −1.293 | −.906 | .324 | .573 | 192 | −.216 | .829 | |

| t2 | −1.502 | −1.355 | .016 | .901 | 199 | −.027 | .978 | |

| t3 | −.110 | −.102 | .000 | .993 | 197 | −.081 | .935 | |

| t4 | −.307 | −.616 | .340 | .563 | 186 | −.379 | .705 | |

| t5 | −.498 | −1.368 | .463 | .500 | 172 | −.757 | .449 | |

| t6 | 1.045 | −.288 | .802 | .376 | 152 | −1.298 | .194 | |

| t7 | .692 | −.506 | 2.269 | .140 | 190 | −.271 | .787 | |

| t8 | .172 | .041 | .016 | .900 | 180 | −.541 | .588 | |

| t9 | −.161 | .007 | .062 | .804 | 189 | −.298 | .766 | |

| t10 | −.892 | .195 | 2.557 | .118 | 160 | −1.082 | .279 | |

| CAR | t0 − t1 | −2.313 | −2.566 | .032 | .860 | 178 | −.835 | .404 |

| t0 − t2 | −3.815 | −3.901 | .002 | .963 | 203 | −.183 | .855 | |

| t0 − t3 | −3.926 | −3.994 | .001 | .973 | 183 | −.704 | .481 | |

| t0 − t4 | −4.234 | −4.673 | .040 | .843 | 197 | −.339 | .735 | |

| t0 − t5 | −4.733 | −6.028 | .215 | .645 | 194 | −.417 | .676 | |

| t0 − t10 | −3.876 | −6.686 | .739 | .395 | 203 | −.183 | .855 | |

| t0 − t20 | −4.659 | −6.838 | .401 | .530 | 210 | .000 | 1.00 | |

| t0 − t30 | −3.491 | −7.989 | 1.344 | .253 | 183 | −.704 | .481 | |

*p < .05.

**p < .01.

***p < .001.

Fig. 4 displays that none of AR or CAR significantly differed from each other, which implies that the impact of food safety events on firm value does not differ depending on the severity of risk. Even though descriptive statistics showed that high severity events showed lower (more negative) CARs than those of low severity events, the differences were not statistically significant. Therefore, results suggest that the severity of risk is not a materialized factor determining the negative impact of food safety events on firm value; hence, Hypothesis 2 was not supported.

Fig. 4.

Impacts of severity of risk (number of people sickened or died) on AR and CAR.

4.3. Recall execution

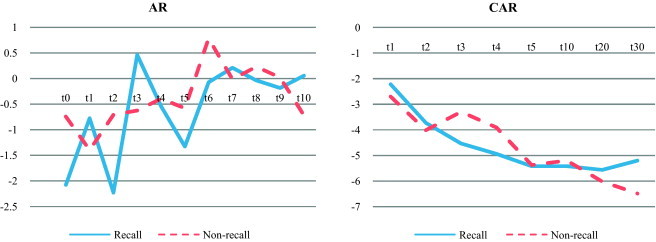

The effect of executing recalls after a food safety event was tested through comparisons of AR and CAR between two groups based on whether events were followed by a recall (recall, n = 19) or not (non-recall, n = 21). Due to the small sample size, a non-parametric test (Mann–Whitney U test) was used to validate the results of one-way ANOVA. The results of Table 6 show no significant difference between recall and non-recall cases. Thus, this result suggests that the impact of food safety events on firm value does not vary depending on whether a recall is executed as shown in Fig. 5 ; therefore, Hypothesis 3 was not supported.

Table 6.

Impacts of recall execution on AR and CAR.

| Descriptive statistics |

Parametric test (recall − non recall) |

Non-parametric test (recall − non recall) |

||||||

|---|---|---|---|---|---|---|---|---|

| Recall (n = 19) | Non-recall (n = 21) | F | Sig. | Mann–Whitney U test | Z | Sig. | ||

| AR | t0 | −2.075 | −.741 | .524 | .474 | 190 | −.257 | .797 |

| t1 | −.773 | −1.395 | .846 | .363 | 172 | −.745 | .456 | |

| t2 | −2.227 | −.706 | 1.755 | .193 | 178 | −.582 | .560 | |

| t3 | .463 | −.622 | 1.181 | .284 | 179 | −.555 | .579 | |

| t4 | −.541 | −.390 | .080 | .779 | 198 | −.041 | .968 | |

| t5 | −1.325 | −.578 | .340 | .563 | 198 | −.041 | .968 | |

| t6 | −.071 | .785 | .325 | .572 | 189 | −.284 | .776 | |

| t7 | .211 | −.014 | .076 | .784 | 197 | −.068 | .946 | |

| t8 | −.034 | .234 | .067 | .797 | 156 | −1.178 | .239 | |

| t9 | −.183 | .020 | .091 | .765 | 188 | −.311 | .755 | |

| t10 | .057 | −.716 | .524 | .474 | 190 | −.257 | .797 | |

| CAR | t0 − t1 | −2.219 | −2.701 | .115 | .737 | 178 | −.811 | .418 |

| t0 − t2 | −3.726 | −4.014 | .025 | .876 | 201 | −.209 | .834 | |

| t0 − t3 | −4.534 | −3.298 | .371 | .546 | 169 | −1.046 | .296 | |

| t0 − t4 | −4.937 | −3.906 | .220 | .642 | 181 | −.732 | .464 | |

| t0 − t5 | −5.416 | −5.373 | .000 | .988 | 181 | −.732 | .464 | |

| t0 − t10 | −5.416 | −5.198 | .004 | .948 | 208 | −.026 | .979 | |

| t0 − t20 | −5.563 | −6.020 | .017 | .896 | 187 | −.575 | .565 | |

| t0 − t30 | −5.199 | −6.485 | .106 | .746 | 204 | −.131 | .896 | |

*p < .05.

**p < .01.

***p < .001.

Fig. 5.

Impacts of recall execution on AR and CAR.

This result supported neither of the two perspectives on the effectiveness of recall announcements: either the positive role of recalls in assuring safety or the negative aspect of magnifying risk perceptions. However, the result does not necessarily suggests that recall strategies are not effective in crisis situations because this study did not examine the effect of other recall-related factors, such as the magnitude of a recall or the type of products recalled. Moreover, the sampled events contain a variety of firms including restaurants, food manufacturers, and food distributors. For example, food safety events associated with food manufacturers are more likely to be accompanied by a recall because they can eliminate the potential risk by removing problematic products; however, restaurant-associated food safety events are primarily caused by mistakes in the process of serving food to people. Thus, restaurants can change their suppliers, sanitize restaurant spaces, and close problematic stores to ensure the safety of foods; recalling products does not apply to the case of restaurants. This inherent difference in the type of operations included in the sample of this study may explain the insignificant effect of recall strategy on stock market returns of firms.

4.4. Past history

The effect of past history, whether or not a firm has been associated with food safety events in the past, on AR and CAR was examined using ANOVA with two groups; “no history” (n = 18) and “history of events” (n = 22). Table 7 and Fig. 6 present that firms with “no history” showed significantly lower CARs than those with a “history of events.” This indicates that first time food safety events caused a dramatically more negative impact than repeated food safety events. In other words, firms with a past history suffered less severe impacts compared to firms that had no prior food safety events.

Table 7.

Impacts of past history on AR and CAR.

| Day | Descriptive statistics |

Parametric test (with history − no history) |

Non-parametric test (with history − no history) |

|||||

|---|---|---|---|---|---|---|---|---|

| No history (n = 18) | With history (n = 22) | F | Sig. | Mann–Whitney U test | Z | Sig. | ||

| AR | t0 | −2.522 | −.436 | 1.297 | .262 | 147 | −1.387 | .166 |

| t1 | −1.454 | −.810 | .903 | .348 | 140 | −1.577 | .115 | |

| t2 | −2.987 | −.154 | 6.800 | .013* | 108 | −2.447 | .014* | |

| t3 | .126 | −.297 | .174 | .679 | 161 | −1.006 | .314 | |

| t4 | −.778 | −.203 | 1.199 | .280 | 142 | −1.523 | .128 | |

| t5 | −1.712 | −.295 | 1.242 | .272 | 182 | −.245 | .807 | |

| t6 | −.032 | .714 | .245 | .624 | 172 | −.707 | .480 | |

| t7 | −.321 | .431 | .855 | .361 | 181 | −.462 | .644 | |

| t8 | .313 | −.062 | .132 | .718 | 189 | −.245 | .807 | |

| t9 | .013 | −.149 | .057 | .812 | 157 | −1.115 | .265 | |

| t10 | .209 | −.805 | 2.186 | .147 | 158 | −1.088 | .277 | |

| CAR | t0 − t1 | −3.976 | −1.242 | 4.015 | .052 | 119 | −2.312 | .021 |

| t0 − t2 | −6.963 | −1.431 | 11.809 | .001*** | 65 | −3.731 | .000*** | |

| t0 − t3 | −6.836 | −1.711 | 7.462 | .009** | 119 | −2.312 | .021* | |

| t0 − t4 | −7.615 | −1.989 | 7.735 | .008** | 115 | −2.417 | .016* | |

| t0 − t5 | −9.328 | −2.319 | 7.347 | .010* | 121 | −2.259 | .024* | |

| t0 − t10 | −9.144 | −2.318 | 4.736 | .036* | 164 | −1.130 | .259 | |

| t0 − t20 | −10.127 | −2.369 | 5.686 | .022* | 161 | −1.208 | .227 | |

| t0 − t30 | −10.809 | −1.871 | 5.808 | .021* | 140 | −1.760 | .078 | |

p < .05.

p < .01.

p < .001.

Fig. 6.

Impacts of past history on AR and CAR.

This result contradicts our expectations; however, this could be partially explained by an incomplete recovery or enhanced communication skills in firms with a “history.” If a firm has not fully recovered from a previous crisis, the change in stock returns (reduction rate) may not be as extreme as that of a first time “offender”. Although a firm may seem to have suffered from less severe impacts, the smaller changes may be simply due to an incomplete recovery from the past crises. Another interpretation is that once a firm experiences food safety events, crisis managers may have learned how to effectively react to events and communicate with the public and the media.

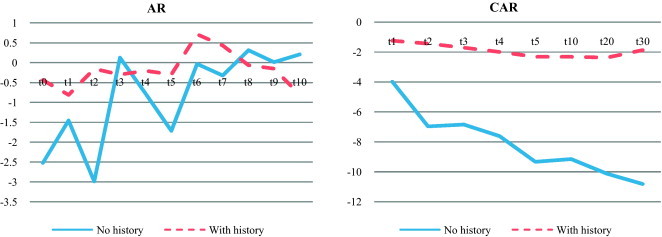

4.5. Firm size

As shown in Table 8 , the effects of firm size, large or small, on AR and CAR were examined using ANOVA. Fig. 7 shows that events associated with small-sized firms had significantly more negative CAR than events associated with large-sized firms. Although ANOVA results indicated that statistically significant differences between the two groups were only found until the second (t 2) or third day (t 3) following the outbreak (until the second day (t 2) supported by Mann–Whitney U test), small firms consistently showed much lower CARs than those of large firms until the 30th day. The result supported the notion that small firms experienced more negative impacts from food safety events than large firms do. Large-sized firms may have more sufficient financial and human resources to utilize for effective crisis communication compared to small-sized firms, which may result in less negative influence for large firms.

Table 8.

Impacts of firm size on AR and CAR.

| Day | Descriptive statistics |

Parametric test (large firms − small firms) |

Non-parametric test (large firms − small firms) |

|||||

|---|---|---|---|---|---|---|---|---|

| Small firms (n = 16) | Large firms (n = 24) | F | Sig. | Mann–Whitney U test | Z | Sig. | ||

| AR | t0 | −2.479 | −.638 | .971 | .331 | 171 | −.580 | .562 |

| t1 | −1.358 | −.927 | .388 | .537 | 136 | −1.546 | .122 | |

| t2 | −2.230 | −.894 | 1.286 | .264 | 150 | −1.160 | .246 | |

| t3 | −.553 | .191 | .526 | .473 | 158 | −.939 | .348 | |

| t4 | −.267 | −.591 | .361 | .551 | 184 | −.221 | .825 | |

| t5 | −.505 | −1.218 | .297 | .589 | 177 | −.414 | .679 | |

| t6 | −1.184 | 1.420 | 3.110 | .086 | 140 | −1.436 | .151 | |

| t7 | −.359 | .3944 | .830 | .368 | 188 | −.110 | .912 | |

| t8 | .945 | −.452 | 1.850 | .182 | 140 | −1.436 | .151 | |

| t9 | .215 | −.2713 | .500 | .484 | 176 | −.442 | .659 | |

| t10 | −.431 | −.294 | .036 | .850 | 175 | −.469 | .639 | |

| CAR | t0 − t1 | −3.838 | −1.550 | 2.631 | .113 | 163 | −0.989 | .323 |

| t0 − t2 | −6.068 | −2.446 | 4.156 | .048* | 122 | −2.085 | .037* | |

| t0 − t3 | −6.622 | −2.258 | 4.941 | .032* | 145 | −1.47 | .142 | |

| t0 − t4 | −6.889 | −2.904 | 3.402 | .073 | 155 | −1.203 | .229 | |

| t0 − t5 | −7.395 | −4.117 | 1.352 | .252 | 147 | −1.417 | .157 | |

| t0 − t10 | −8.209 | −3.464 | 2.076 | .158 | 177 | −0.615 | .539 | |

| t0 − t20 | −8.860 | −3.800 | 2.152 | .150 | 177 | −0.615 | .539 | |

| t0 − t30 | −8.909 | −3.802 | 1.662 | .205 | 164 | −0.962 | .336 | |

p < .05.

**p < .01.

***p < .001.

Fig. 7.

Impacts of firm size on AR and CAR.

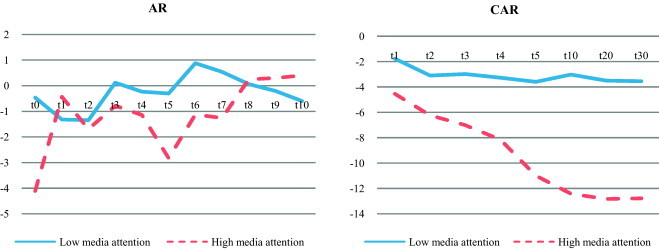

4.6. Media attention

Table 9 presents the results of both ANOVA and Mann–Whitney U test used to examine the impact of media attention (high media attention versus low media attention) on AR and CAR. Consistent with Hypothesis 6, events with high media attention showed greater negative stock returns, which is evidence of the power of media on market responses to food safety events as shown in Fig. 8 .

Table 9.

Impacts of media attention on AR and CAR.

| Day | Descriptive statistics |

Parametric test (high media attention − low media attention) |

Non-parametric test (high media attention − low media attention) |

|||||

|---|---|---|---|---|---|---|---|---|

| Low media attention (n = 30) | High media attention (n = 10) | F | Sig. | Mann–Whitney U test | Z | Sig. | ||

| AR | t0 | −.464 | −4.105 | 3.133 | .085 | 123 | −.828 | .408 |

| t1 | −1.321 | −.435 | 1.308 | .260 | 145 | −.141 | .888 | |

| t2 | −1.342 | −1.689 | .066 | .799 | 137 | −.390 | .696 | |

| t3 | .118 | −.781 | .601 | .443 | 147 | −.078 | .938 | |

| t4 | −.234 | −1.145 | 2.337 | .135 | 123 | −.828 | .408 | |

| t5 | −.301 | −2.828 | 3.136 | .085 | 139 | −.328 | .743 | |

| t6 | .879 | −1.124 | 1.377 | .248 | 100 | −1.546 | .122 | |

| t7 | .543 | −1.258 | 4.007 | .050* | 131 | −.578 | .563 | |

| t8 | .060 | .246 | .025 | .876 | 113 | −1.140 | .254 | |

| t9 | −.202 | .302 | .420 | .521 | 143 | −.203 | .839 | |

| t10 | −.598 | .399 | 1.574 | .217 | 126 | −.734 | .463 | |

| CAR | t0 − t1 | −1.766 | −4.541 | 3.028 | .090 | 113.5 | −1.26 | .208 |

| t0 − t2 | −3.095 | −6.230 | 2.310 | .137 | 110.5 | −1.351 | .177 | |

| t0 − t3 | −2.977 | −7.012 | 3.140 | .084 | 107.5 | −1.442 | .149 | |

| t0 − t4 | −3.266 | −8.157 | 4.029 | .052 | 114.5 | −1.23 | .219 | |

| t0 − t5 | −3.593 | −10.985 | 5.932 | .020* | 125.5 | −0.896 | .370 | |

| t0 − t10 | −3.024 | −12.420 | 7.077 | .011* | 104.5 | −1.533 | .125 | |

| t0 − t20 | −3.500 | −12.826 | 6.226 | .017* | 108 | −1.427 | .154 | |

| t0 − t30 | −3.545 | −12.771 | 4.498 | .040* | 121 | −1.032 | .302 | |

p < .05.

**p < .01.

***p < .001.

Fig. 8.

Impacts of media attention on AR and CAR.

Interestingly, a statistically significant media effect was detected from the 5th day since the outbreak using ANOVA (8th day using Mann–Whitney U-test), implying the presence of an “incubation” time due to the spreading effect of media messages to the public. The difference in CAR between low and high media attention groups increased over time, supporting the gradual spreading effect of the media message. In this respect, media messages may amplify the negative impact of food safety events over time. If a food safety event is repeatedly reported by media for an extended period of time, the negative impact can be amplified regardless of the actual magnitude of the event. Acknowledging the importance of the media in crisis communication, handling media effectively under crisis situations is a critical role for crisis managers.

5. Conclusions and implications

It is clear that food safety events have negative impacts on food-related firms. However, how serious the events are and how long the negative impact usually lasts has not been examined in the hospitality academia. Thus, this study is unique in that it provides empirical evidence of the seriousness and duration of negative impacts of food safety events on associated food-related firms. One significant finding of this study is that daily abnormal returns (ARs) were significantly negative on the first day (t 1) and the second day (t 2) following the outbreak of events. Cumulative abnormal returns (CARs) were found to be significantly negative until the 57th trading day since the outbreak, supporting that discernable negative impacts diminished approximately two working months after the event. Furthermore, negative CARs turned to positive values after 264 trading days, indicating that it took almost one year to fully recover from food safety events. Moreover, the effect of factors contributing to the impact of food safety events on food-related firms was also examined: risk-related, firm-specific, and situational factors. While none of the risk-related factors (severity of risk and recall execution) were significant, both firm-specific factors (past history and firm size) and situational factor (media attention) were significant determinants of the impact of food safety events on the firms. In summary, the significant impact of food safety events on food-related firms (H1), the effect of past history (H4), the effect of firm size (H5), and the effect of media attention (H6) were supported, while the effect of severity of risk (H2) and the effect of recall execution (H3) were not supported in this study. The results are summarized in Table 10 .

Table 10.

Hypotheses testing.

| Hypotheses | Results | Testing | |

|---|---|---|---|

| H1 | The impact of food safety events on food-related firms | Proved the significant negative financial impacts of food safety events | Supported |

| H2 | Severity of risk (high/low) | No difference between low/high severity | Not supported |

| H3 | Recall execution (no/yes) | No difference between recall/non-recall | Not supported |

| H4 | Past history (no/yes) | Negative AR/CAR for non-history firms | Supported |

| H5 | Firm size (small/large) | Negative AR/CAR for small firms | Supported |

| H6 | Media attention (high/low) | Negative AR/CAR for high media attention | Supported |

The insignificant effects of risk factors have important implications to practitioners about the significance of food safety events regardless of the severity of risk and the recall strategy. The perception of risk may be influenced more by how the risk information is delivered to and processed by the public than by the content of the information itself (Kasperson et al., 1988, Frewer et al., 1997). Significant firm-specific and situational factors reinforce this information processing perspective by demonstrating the impact of external factors in shaping risk perception and consumer responses. The effect of recall execution was another insignificant risk-related factor, which supported neither perspective (positive or negative) on the effectiveness of recall announcements. Although the results showed an insignificant effect of recall execution on stock returns, external factors that were not considered in this study, such as type of operations (restaurant, food manufacturer, and food distributor), may have contributed to the results. Although this study could not perform data analysis on the effect of operation type on stock price movements because of the small sample size, future studies can consider the operation type as a factor driving the impact of food safety events on the associated firms.

Firm-specific factors, past history and firm size, were significant factors influencing changes in stock returns due to food safety events. The significant effect of a past history of food safety events implied that a first-time food safety event can cause disastrous results, which is inconsistent with the results of previous research (Coombs, 2004, Coombs, 2007). The previous studies asserted that a past history may intensify the attrition of a firm in the crisis, negatively affecting the reputation of the firm. However, even a one-time event can generate disastrous results, as supported by the case of Chi-Chi's in 2003. Chi-Chi's, a national Mexican chain restaurant, was involved in a hepatitis A outbreak in 2003 and closed its operation in 2004 due to a tainted brand image and negative publicity. Thus, it is difficult to conclude that restaurants that have never experienced food safety events in the past are safe from the risk to the extreme impact of food safety events. Another firm-specific factor, firm size, was found to be significant. This finding suggests that large firms experienced less severe impacts than small firms, which is inconsistent with previous studies asserting the advantages of large firms compared to small firms (Salin and Hooker, 2001, Roehm and Brady, 2007). Large firms can take more effective actions, such as advertisement, campaigns, and promotions, to recover their tainted brand image, whereas small firms may not have sufficient resources to recover from crises. It is suggested that small firm managers should have pre-crisis management plans that recognize the constraints of small firms in handling crisis situations.

The significant effect of the situational factor, media attention, signals the importance of communication channels. The effect of media attention on stock returns provides important evidence of the role of media in shaping risk perception and market evaluations of events. Although the significant relationship between media attention and stock returns has been identified by previous studies (Tetlock, 2007, Ellis and Lewis, 2000), this study contributed to the literature on this topic by demonstrating the amplifying effect of media messages on poor firm value due to the food safety event outbreaks. As the power of media was found to become stronger over time, the importance of effective communication through media is increasing. The amplifying effect of media attention on the magnitude and duration of a food safety event on a firm's market value offers a plausible explanation to the fact that the impact of a SARS outbreak in Taiwan on hotels’ stocks persisted over 30 days, a phenomenon raised but unanswered by Chen et al. (2007). The finding suggests that it is crucial for crisis managers to use media as a communication channel to minimize negative publicity.

The main contributions of this study are (1) broadening the knowledge about the effect of food safety events on food-related firm value and (2) providing practical implications for practitioners to develop effective crisis strategies. More specifically, this study is the first to attempt not only to examine the impacts of food safety events on firm value, but also to investigate how the impact varies depending on several factors, such as risk severity, recall, past history, firm size, and media attention. By initiating research on the impacts of food safety events on stock market evaluations of food-related firms, this study provides opportunities for future studies to use other measurements, such as consumer surveys. Second, the results of this study offer several important implications for practitioners. Having pre-crisis management strategies along with post-crisis communication strategies is important in handling crisis situations in a way that protects a firm's reputation during a crisis. The results regarding a past history with food safety events reinforce the importance of having pre-crisis management strategies for food-related firms. To develop an effective pre-crisis management strategy, training and education of food employees in terms of food safety is of paramount importance. A recent study by Medeiros et al. (2012) suggested that restaurants’ human resource administration should focus on the provisions of food safety information through hiring, evaluating, and training of food-handling employees. The effectiveness of food safety training has also been confirmed by other studies (Murphy et al., 2011, Seaman and Eves, 2006, Soon and Baines, 2012). The findings converge to suggest that proper food safety training contributes to safer food handling practices, which in turn, reduces the possibility of food crises.

This study is not without limitations. First, the actual number of food safety events is limited in order to apply ESM, with only firms that are listed on stock market were included in the study. Future research with a larger sample size may allow researchers to better investigate the effect of food safety events on firm value. Second, since the event study method was designed to measure the short-term impact of events, it was not possible to estimate the long-term impact of food safety events in this study. Future studies can adopt different study methods such as longitudinal analysis to examine long-term financial impacts of food safety events. Lastly, the type of operations may alter the influence of food safety events on financial performance of firms, which can be explored by future studies using a larger sample. By building on the knowledge gained from this study, future studies can further extend our understanding of the impacts of food safety events.

Contributor Information

Soobin Seo, Email: sseo@purdue.edu.

SooCheong (Shawn) Jang, Email: jang12@purdue.edu.

Li Miao, Email: lmiao@purdue.edu.

Barbara Almanza, Email: almanzab@purdue.edu.

Carl Behnke, Email: behnkec@purdue.edu.

References

- Atiase R.K. Predisclosure information, firm capitalization, and security price behavior around earnings announcements. Journal of Accounting Research. 1985;23(1):21–36. [Google Scholar]

- Bajaj M., Vijh A.M. Trading behavior and the unbiasedness of the market reaction to dividend announcements. Journal of Finance. 1995;50(1):255–279. [Google Scholar]

- Becker, E., 2002. 19 million pounds of meat recalled after 19 fall ill. The New York Times. Retrieved May 8, 2010.

- Borde S.F., Byrd A.K., Atkinson S.M. Stock price reaction to dividend increases in the hotel and restaurant sector. Journal of Hospitality & Tourism Research. 1999;23(1):40–52. [Google Scholar]

- Braun-latour K.A., Latour M.S., Loftus E.F. Is that a finger in my chili? Using affective advertising for postcrisis brand repair. Cornell Hospitality Quarterly. 2006;47(2):106–120. [Google Scholar]

- CDC (Centers for Disease Control and Prevention) Preliminary FoodNet data on the incidence of infection with pathogens transmitted commonly through food – 10 states, United States, 2005. MMWR. Morbidity and Mortality Weekly Report. 2006;55(14) Available at: http://www.cdc.gov/mmwr/preview/mmwrhtml/mm5514a2.htm?s_cid=mm5514a2_e (accessed 29.11.06) [PubMed] [Google Scholar]

- Chan W.S. Stock price reaction to news and no-news: drift and reversal after headlines. Journal of Financial Economics. 2003;70(2):223–260. [Google Scholar]

- Chang C., Zeng Y. Impact of terrorism on hospitality stocks and the role of investor sentiment. Cornell Hospitality Quarterly. 2011;52(2):165–175. [Google Scholar]

- Chen Y., Ganesan S., Liu Y. Does a firm's product-recall strategy affect its financial value? An examination of strategic alternatives during product-harm crises. Journal of Marketing. 2009;73(6):214–226. [Google Scholar]

- Chen M.H., Jang S., Kim W.G. The impact of the SARS outbreak on Taiwanese hotel stock performance: an event-study approach. International Journal of Hospitality Management. 2007;26(1):200–212. doi: 10.1016/j.ijhm.2005.11.004. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Coombs W.T. Impact of past crises on current crisis communication: insights from Situational Crisis Communication Theory. Journal of Business Communication. 2004;41(3):265–289. [Google Scholar]

- Coombs W.T., Schmidt L. An empirical analysis of image restoration: Texaco's racism crisis. Journal of Public Relations Research. 2000;12(2):163–178. [Google Scholar]

- Coombs W.T. Protecting organization reputations during a crisis: the development and application of Situational Crisis Communication Theory. Corporate Reputation Review. 2007;10(3):163–176. [Google Scholar]

- Cowan A.R. Cowan Research; Ames, IA: 2003. Eventus 7.6 User's Guide. [Google Scholar]

- Dodd P., Warner J.B. On corporate governance: a study of proxy contests. Journal of Financial Economics. 1983;11(1–4):401–438. [Google Scholar]

- Ellis L., Lewis E. The response of financial markets in Australia and New Zealand to news about the Asian crisis. Bank for International Settlements Conference. 2000;(March (8)):308–348. [Google Scholar]

- Fama E.F. Efficient capital markets: a review of theory and empirical work. Journal of Finance. 1970;25(2):383–417. [Google Scholar]

- Frewer L.J., Howard C., Hedderley D., Shepherd R. The elaboration likelihood model and communication about food risks. Risk Analysis. 1997;17(6):759–770. doi: 10.1111/j.1539-6924.1997.tb01281.x. [DOI] [PubMed] [Google Scholar]

- Grant E.B. Market implications of differential amounts of interim information. Journal of Accounting Research. 1980;18(1):255–268. [Google Scholar]

- Gregoire Y., Tripp T.M., Legoux R. When customer love turns into lasting hate: the effects of relationship strength and time on customer revenge and avoidance. Journal of Marketing. 2009;73(6):18–32. [Google Scholar]

- Hammit J.K., Haninger K. Willingness to pay for food safety: sensitivity to duration and severity of illness. American Journal of Agricultural Economics. 2007;89(5):1170–1175. [Google Scholar]

- Henson S., Mazzocchi M. Impact of bovine spongiform encephalopathy on agribusiness in the United Kingdom: results of an event study of equity prices. American Journal of Agricultural Economics. 2002;84(2):370–386. [Google Scholar]

- Hsu L., Jang S. The post-merger performance of hotel companies. Journal of Hospitality and Tourism Research. 2007;31(4):471–485. [Google Scholar]

- Israeli A.A. Crisis-management practices in the restaurant industry. International Journal of Hospitality Management. 2007;26(4):807–823. [Google Scholar]

- Kasperson R.E., Renn O., Slovic P., Brown S., Emel J., Goble R., Kasperson J.X., Ratick S. The social amplification of risk: a conceptual framework. Risk Analysis. 1988;8(2):177–187. [Google Scholar]

- Lee S., Connolly D.J. The impact of IT news on hospitality firm value using cumulative abnormal returns (CARs) International Journal of Hospitality Management. 2010;29(3):354–362. [Google Scholar]

- Lobb A.E., Mazzocchi M., Traill W.B. Modelling risk perception and trust in food safety information within the theory of planned behavior. Food Quality and Preference. 2007;18(2):384–395. [Google Scholar]

- Marler Clark website. Available at: http://www.marlerclark.com/case_news/C88 (accessed 10.03.11).

- Maynard L.J., Goddard E., Conley J. Impact of BSE on beef consumption in Alberta and Ontario quick-serve restaurants. Canadian Journal of Agricultural Economics. 2008;56(3):337–351. [Google Scholar]

- McLuhan M. McGraw Hill; New York: 1964. Understanding Media: The Extensions of Man. [Google Scholar]

- McWilliams A., Siegal D. Event studies in management research: theoretical and empirical issues. Academy of Management Journal. 1997;40(3):626–657. [Google Scholar]

- Medeiros C.O., Cavalli S.B., da Costa Proenc R.P. Human resources administration processes in commercial restaurants and food safety: the actions of administrators. International Journal of Hospitality Management. 2012;31(3):667–674. [Google Scholar]

- Miyajima H., Yafeh Y. Japan's banking crisis: an event-study perspective. Journal of Banking and Finance. 2007;31(9):2866–2885. [Google Scholar]

- Murphy K.S., DiPietro R.B., Lee J. Does mandatory food safety training and certification for restaurant employees improve inspection outcomes? International Journal of Hospitality Management. 2011;30(1):150–156. [Google Scholar]

- Palen L. Online social media in crisis events. Educause Quarterly. 2008;3:76–78. [Google Scholar]

- Piggott N.E., Marsh T.L. Does food safety information impact US meat demand? American Journal of Agricultural Economics. 2004;86:154–174. [Google Scholar]

- Roehm M.L., Brady M.K. Consumer responses to performance failures by high-equity brands. Journal of Consumer Research. 2007;34(4):537–545. [Google Scholar]

- Rogers R.W. A protection motivation theory of fear appeals and attitude change. The Journal of Psychology. 1975;91(1):93–114. doi: 10.1080/00223980.1975.9915803. [DOI] [PubMed] [Google Scholar]

- Salin V., Hooker N.H. Stock market reaction to food recalls. Review of Agricultural Economics. 2001;23(1):33–46. [Google Scholar]

- Scallan E., Hoekstra R.M., Angulo F.J., Tauxe R.V., Widdowson M.A., Roy S.L. Foodborne illness acquired in the United States-major pathogens. Emerging Infectious Diseases. 2011;17(1):7–15. doi: 10.3201/eid1701.P11101. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Seaman P., Eves A. The management of food safety—the role of food hygiene training in the UK service sector. Hospitality Management. 2006;25(2):278–296. [Google Scholar]

- Siomkos G.J., Kurzbard G. The hidden crisis in product-harm crisis management. European Journal of Marketing. 1994;28(2):30–41. [Google Scholar]

- Soon J.M., Baines R.N. Food safety training and evaluation of handwashing intention among fresh produce farm workers. Food Control. 2012;23(2):437–448. [Google Scholar]

- Swary I. Stock market reaction to regulatory action in the continental Illinois crisis. The Journal of Business. 1986;59(3):451–473. [Google Scholar]

- Syed-Ahmad S.F., Murphy J. Social networking as a marketing tool: the case of a small Australian company. Journal of Hospitality Marketing & Management. 2010;19(7):700–716. [Google Scholar]

- Tetlock P.C. Giving content to investor sentiment: the role of media in the stock market. The Journal of Finance. 2007;62(3):1139–1168. [Google Scholar]

- Thomsen M.R., McKenzie A.M. Market incentives for safe foods: an examination of shareholder losses from meat and poultry recalls. American Journal of Agricultural Economics. 2001;83(3):526–538. [Google Scholar]

- van Ravenswaay E.O., Hoehn J.P. The impact of health risk information on food demand: a case study of alar and apples. In: Caswell J.A., editor. Economics of Food Safety. Elsevier; New York: 1991. [Google Scholar]

- Wan H.H. Resonance as a mediating factor accounting for the message effect in tailored communication: examining crisis communication in a tourism context. Journal of Communication. 2008;58:472–489. [Google Scholar]

- Wiles M.A., Danielova A. The worth of product placement in successful films: an event study analysis. Journal of Marketing. 2009;73(4):44–63. [Google Scholar]