Abstract

Generally, there are three levels to define construction within the literature (Dang and Low in Infrastructure Investments in Developing Economies. Springer, 2015). At one extreme, construction is referred to as an economic activity that involves the entire construction process from producing raw and manufactured building materials and components, and providing professional services such as design and project management, to executing the physical work on site.

Some Basic Concepts of the Construction Industry

Construction as an Economic Activity

Generally, there are three levels to define construction within the literature (Dang & Low, 2015). At one extreme, construction is referred to as an economic activity that involves the entire construction process from producing raw and manufactured building materials and components, and providing professional services such as design and project management, to executing the physical work on site. In this view, construction is an economic activity that crosses over all three economic sectors: primary sector that involves the extraction of natural resources; secondary sector that involves the manufacture of building materials and components, and the transformation of these materials into finished buildings; and tertiary sector that involves the provision of consultancy services such as project management, design and structural engineering (Gruneberg, 1997). From this angle of approach, the construction process actually starts long before the physical work on site that transforms materials and design into the complete buildings, structures and facilities.

At the other extreme, construction is conceived as an economic activity that focuses only on the last stage of the construction process which is the physical work carried out on the production site. From this perspective, all services such as project management, planning and design as well as the offsite manufacture and supply of building materials are excluded. One typical example of this kind of definition is the one provided in the International Standard Industrial Classification of all Economic Activities (United Nations, 1990). According to this classification, project management for construction, architectural and engineering activities, and the manufacture of building materials are listed under different categories other than construction. This manner of classification is considered convenient for statistical purposes (Ofori, 1990). Following this classification, construction is perceived as an economic activity directed to the new work, renovation, repair or extension of buildings, structures and other heavy constructions such as roads, bridges, dams and so forth (United Nations, 1990). Accordingly, only the work force working on the construction site is defined as the labour force of the construction industry (Ive & Gruneberg, 2000).

There is one more way of defining the construction industry, which is somewhat in between the two above mentioned extremes. In this context, construction is referred to as the production process of the built environment including various activities from conception through design to execution. The objects of the built environment include buildings and other fixed structures (Ive & Gruneberg, 2000). In other words, the construction industry is “a sector of the economy which, through planning, design, construction, maintenance and repair, and operation, transforms various resources into constructed facilities” (Moavenzadeh, 1978, p. 98). As such, the construction industry encompasses all firms or organizations, who professionally engage in the construction process, from those providing consultancy services in the planning, design, supervisory and managerial services to those carrying out execution work on site such as the general contractors and builders (Colean & Newcomb, 1952; Ofori, 1990). These firms or organizations, in turn, often have a close relationship with clients and financers (Hillebrandt, 2000). This phenomenon is directly derived from the characteristics of the industry’s products, which are described below.

All the three levels of definition of the construction industry are useful. In order to obtain a full picture of the industry, it is reasonable to use the broadest definition mentioned above. However, the other two narrower definitions are more relevant to this study. It is important to know whether the final products, which is defined by the narrowest definition of the construction industry is increasing or decreasing. This type of information is often of great importance for economic planning purposes (Ofori, 1990). There have also been views arguing that construction should be considered as a project-based level economic activity (Groak, 1994), or views that questioned if construction is one industry (Ball, 1988; National Economic Development Office, 1978) or several industries (Ive & Gruneberg, 2000). However, for the purpose of this study, which analyzes construction in relation to other economic activities, the concept of one industry would be more appropriate.

Construction Products

This section looks at the classification of the construction industry’s products and their characteristics. The classification of products is necessary as each type of output represents different kinds of supply and demand, which will be affected by different factors in the market (Ofori, 1990). According to the International Standard Industrial Classification of all Economic Activities (United Nations, 1990), complete products of the construction industry consists of dwellings, office buildings, stores and other public and utility buildings, farm buildings, etc., or heavy constructions such as highways, streets, bridges, tunnels, railways, airfields, harbors and other water projects, irrigation systems, sewerage systems, industrial facilities, pipelines and electric lines, sports facilities, etc. More generally, outputs of the construction industry are grouped into housing, infrastructure, industrial and commercial buildings, and repair and maintenance (Gruneberg, 1997; Wells, 1986). Another way to classify construction outputs is to group them into civil engineering work, buildings, and repairs and maintenance. Civil engineering work includes transport facilities, telecommunication and power networks, water supplies, etc. Buildings include housing and the remainder (hospitals, schools, offices, factories, hotels and agricultural buildings) (Wells, 1985).

Construction’s final outputs share certain common characteristics with each other, such as their custom-built nature, immobility, complexity, durability and costliness (Colean & Newcomb, 1952; Moavenzadeh, 1978). These products are also often distinguished from others in terms of time lag, labour intensive operations, site production and temporary organizations (Ofori, 1990; Koskela, 2003). It is not difficult to envisage products of the construction industry in these terms. Construction products are not mass produced commonly. Each construction product is only constructed after the client decides to procure it. Custom-built nature or the one-of-a-kind nature of construction outputs is featured by different clients with different needs and priorities, by different sites, and by different views of designers (Ofori, 1990). Products of the construction industry are immobile; they are fixed to the site where they will be used (Colean & Newcomb, 1952). The products are constructed on site as well. As a result, the construction process depends not only on the natural conditions of the site but also on the local resources such as the local labour force, local subcontractors, local building materials suppliers, local regulations, etc. Complexity of construction products follows from their custom-built nature and site production. The high diversity of customers’ requirements and site conditions result in a wide range of materials, technological requirements, design solutions and construction methods of varying degrees of complexity. Another reason for the complexity is the number of different teams from different parties involved in the construction works (Ofori, 1990). Each team with different professional practices, specializing in different operations often leads to a complicated organization in the construction process. The organization is obviously only temporary for a particular product.

Construction products are extremely durable. They are built to generate a flow of services for a very long time. Civil engineering works and buildings thus often last for generations. Except for catastrophes caused by human or nature, a construction product is only demolished when it becomes obsolete and no one wants to use it, which means it is no longer economical to maintain (Colean & Newcomb, 1952; Gruneberge, 1997). Durability and complexity are the main reasons why the construction of civil engineering works and buildings is capital-intensive, involves a large number of labour, and takes a long time to complete. Delays are also often unavoidable. Delays can be caused by unexpected natural events, technical, financial, procedural, and contractual problems (Ofori, 1990).

Infrastructure

Infrastructure in the construction industry is generally related to economic infrastructure. Economic infrastructure is constructed to facilitate other economic activities of the national economy. Development economists often refer to infrastructure as “social overhead capital” or public infrastructure capital since it has traditionally been owned and managed by the public sector (Howes & Robinson, 2005). Some other broader definitions of economic infrastructure also include offices, shops, housing, factories, warehouses, industrial parks, schools, hospitals, etc. (Miller, 2000; Howes & Robinson, 2005). The economic infrastructure as defined by the World Bank (1994) is the most suitable one adopted for this study. According to the definition, there are three main groups in economic infrastructure:

Public utilities—power, telecommunications, piped water supply, sanitation and sewerage, solid waste collection and disposal, and piped gas.

Public works—roads and major dam and canal works for irrigation and drainage.

Other transport sectors—urban and inter-urban railways, urban transport, ports and waterways, and airports (World Bank, 1994, p. 2).

The concept of infrastructure by the World Bank (1994) has been widely adopted in many national, regional as well as international economic studies and reports (Parkin & Sharma, 1999; ESCAP, 1994; Kohsaka, 2006; Mody, 1997).

Structure of the Construction Industry

By nature of the work, the structure of the construction industry can be characterized by type of product, size of contract, complexity and geographical location of finished products (World Bank, 1984). By type of product, the construction industry consists of construction firms specializing in residential, industrial and commercial buildings, and infrastructure or civil engineering works. The construction industry can also be structured by size of contract and degree of complexity. Large construction firms usually undertake large contracts with high degree of complexity. The technical as well as managerial skills are the two major advantages that large construction firms have over the small firms. This explains that the potential competitors for large civil engineering works are often large construction firms. Geographical location is also an important determinant of the structure of the construction industry. Construction firms are usually market-located (Gruneberg, 1997). Because construction product is characterized by site-production, most construction firms need to consider the transportation costs of materials, equipment and labour to the production site. Beyond a certain geographical area, these costs become excessive in relation to other costs, thus rendering the project’s profitability unattractive. Only for large contracts would the proportion of transportation costs in total costs become small enough, so that it is still profitable for firms to undertake the jobs farther afield. For very large projects, firms might set up a local office to reduce transportation costs, but then these firms will need to consider the attendant overheads associated (Hillebrandt, 2000).

By pattern of production organization, this study focuses on the formal sector rather than the informal one. Within the formal sector, the structure of the construction industry can be classified into public and private firms, and domestic and foreign firms. Public firms are state-owned enterprises, which are often protected by the government. The establishment of these public enterprises is essential to take on works which are unattractive to private firms or as required by the government, or perform as a source of providing the necessary trained labour for the development of the construction industry. Meanwhile, private contractors contribute to the development of the construction industry by their competitiveness, efficiency and flexibility. One more noticeable point in the structure of the construction industry is the participation of international contractors. Their presence can make the competition more difficult for domestic firms. However domestic firms will become stronger in the process. The structure of the construction industry can be quite different among countries depending on the social and economic environments such as the development state of the economy, government policies, and the traditions of doing business (World Bank, 1984).

Major Economic Factors Influencing Construction Activity

Instability of Demand

Construction demand is inherently volatile. Wide fluctuations in construction outputs are common. Studying a number of countries with different income from various parts of the world, the World Bank (1984) indicated that the fluctuation of construction outputs was more than half of the manufacturing sector and the economy as a whole. A study of the European region by the United Nations (1976) came to the same conclusion that the construction industry experienced stronger movements of business cycle than other economic sectors. These fluctuations are partly due to the nature of construction demand and partly due to the nature of construction products. Demand for construction outputs is considered derived demand from other economic activities (United Nations, 1976; Hillebrandt, 2000). Outputs of the construction industry are investment-goods, which are produced to facilitate the creation of other consumption-goods and services. In other words, the construction industry itself cannot create the demand for its outputs (Nam & Tatum, 1988). Demand for construction is therefore largely dependent on the business activities of other goods and services that the construction products help create. Following the ups and downs of the economy, the demand for construction can go through the movement of a business cycle earlier and more strongly than other sectors because of the nature of its products (Riggleman, 1933; United Nations, 1976). A construction product is immobile and is often constructed only after the client realizes the demand. This nature of construction products makes the industry unable to stock up products for sale. Hence, when there is a sudden increase in demand, the industry cannot respond to the demand quickly (United Nations, 1976; Nam & Tatum, 1988). The fluctuations of construction demand can be very large, thus affecting the economy considerably. The immobility and the durability properties also make construction demand geographically dependent. Demand for construction within a geographical area will at some time in the future experience a substantial fall and suffer saturation when much of the demand in the area is met and the existing facilities are still economical to maintain (Colean & Newcomb, 1952; Hillebrandt, 2000).

Apart from the above mentioned factors, the stages of economic development as well as the structural changes also have significant influences on the growth rate of demand for construction as well as the compositions of demand for construction over time. A study by the United Nations (1976) pointed out that the fluctuations in construction activity, with reference to those of other economic sectors, tend to be greater in developing than in developed countries. In developing countries, the demand for infrastructural facilities is of the greatest proportion compared with other construction demands. Since in the initial stages of development, infrastructure is of great importance in creating the framework for the economy, spending on building new infrastructure in these stages is relatively heavy (Lewis, 1955). As a result, the share of construction expenditure on public works and public utilities such as harbours, railways, roads, electricity, etc., in the less developed countries are often higher than that in the more developed countries (Lewis, 1955). Structural changes such as changes in development goals, priorities of economic growth among sectors, and changes in demographics can also impact the demand for construction (United Nations, 1976). The World Bank (1994) observed that as countries develop, infrastructure must adapt to support changing patterns of demand.

Main Construction Inputs

Main inputs in construction include labour, materials and equipment. The characteristics of each component are discussed further below.

Labour

Since construction products are frequently labour-intensive, labour is one of the major cost components in construction (Ive & Gruneberg, 2000). The construction labour force can be divided into the major categories of: administrative, managerial, professional and technical staff, and workers. Demand for labour is directly affected by the characteristics of demand for construction. In line with the cyclical fluctuations in construction outputs, the level of employment in the industry can vary noticeably (United Nations, 1976). As a result, a large proportion of construction labour force is paid on a project-by-project basis, rather than on a permanent basis, except for a small number of administrative and managerial staff. Furthermore, outsourcing labour through subcontractors also make the employment in construction increasingly temporary and insecure (International Labour Office, 2001). At the bottom of the supply chain, construction workers have low job security and need for mobility (Moavenzadeh, 1978). Careers in construction are also less attractive because of the high rate of accidents (Jensen, 1983). The industry therefore has to compete with other sectors of the economy for manpower by increasing wage level (Ofori, 1990). Labour can also be imported if the wages of the imported labour plus transport costs can be less than the local wages (Gruneberg, 1997). In addition, the price of construction labour is affected by minimum wage laws and union agreements, which would raise the costs of hiring unskilled labour substantially (World Bank, 1984).

The labour market of the construction industry is characterized by the shortage of skilled labour, especially in the developing countries. In the developed countries, the skilled workers account for about 50% of the total labour force (Moavenzadeh, 1978). However, the construction industry in these countries has apparently been experiencing a shrinking workforce, thus a reduction in the number of the skilled labour (Ofori, 1990). Meanwhile in the developing countries, the shortage of skilled labour is more serious. The labour markets in these countries are largely unstructured and relatively unorganized, which rely heavily on a relatively untrained workforce (Gruneberg, 1997). In public works construction, the shortage of skilled labour occurs at both levels, the supervisory personnel and skilled workers (Moavenzadeh, 1978). The inability of the industry to attract workers and to invest in training them has seriously affected the productivity and quality of construction products and hence the ability of contractors to satisfy the clients’ needs (International Labour Office, 2001). One of the solutions to the problem is to improve vocational training in the domestic construction industry. While this solution has proved to be successful in the developed countries, the non-availability or inadequacy of educational and training facilities is still a problem in the developing countries (Rao, 1983; Edmonds & Miles, 1984). Another way to reduce the dependence on labour is through the use of labour-saving construction technology such as prefabrication. However, this solution has proved to be inappropriate in the developing countries as will be illustrated below.

Equipment and Construction Technology

The intensity of equipment used in construction projects depends on construction technology. Construction technology reflects the level of mechanization used in the method of construction. The use of construction technology can vary across projects. This is because there is a certain degree of technological flexibility for the same construction work. For the same construction work, designers and contractors can choose between the two construction methods: one that is highly mechanized; and the other that is fully manual (Moavenzadeh, 1978). The choice of the contractor depends on the constraints of time and budget. If time is of the essence, then the highly mechanized method may be used. However, if the total cost of using plant and equipment plus wages for technical personnel and semi-skilled workers is much higher than the total labour cost of minimally-trained unskilled workers used in the fully manual method, the latter may be used when the budget is limited (Ofori, 1990). In developed countries where labour has become more costly compared to other inputs, the use of equipment-intensive technology has been more common than in developing countries where the cost of plant and equipment is high and labour is still cheap and abundant (International Labour Office, 2001). In other words, the choice of technology is predominately affected by the prevailing prices of labour and equipment (World Bank, 1984).

In a research study by the World Bank (1984), the role of labour-intensive technology in the development of infrastructure in developing countries has proved to be important. The results of the study showed that labour-intensive technology in capital-scarce, labour-abundant economies were technically and economically feasible for government-run labour-intensive civil construction programs. With improvements at the managerial and technical level, labour-intensive methods could be fully competitive with equipment-intensive methods in terms of quality and productivity (World Bank, 1984). Since labour continues to be abundant in developing countries, more serious efforts from the government would be essential to make the labour-intensive option more attractive for a wide range of construction activities.

Building Materials

Building materials make up a major component of total construction costs (Ive & Gruneberg, 2000). The price level of building materials thus directly affects the construction output value. The price of a particular type of materials depends on the market forces, demand and supply of that building material. Demand for a particular building material in turn depends on client’s tastes and preferences, and level of income; local building standards and codes; and the choices made by designers and contractors. The choices made by designers and contractors vary according to the experience of the designers, the familiarity of contractors with the technology involved in the use of the materials and the availability of human resource with the required skills (Ofori, 1990).

The supply of a particular building material is affected by: the availability of raw materials; the technology for extracting and processing raw materials; the environmental impacts related to the production process; and the government policy. The availability of raw materials directly determines the supply level of building materials. Some countries that lack raw materials have to import them. Apart from the lack of raw materials, building materials supply may be unable to meet local demand because of the low production capacity and low quality, especially in the developing countries. Production capacity and quality of building materials in turn depends on the technology of extracting and processing the raw materials used (Ofori, 1990). The technology used in the developing countries is generally older than in the developed countries. In line with older technology, environmental impacts in the developing countries are also more serious than that in the developed countries. A growing awareness of these environmental impacts has made governments in the developing countries restrict the production of low-grade materials that uses the old technology, and support the import of more modern technology from the developed countries (ICR Research, 2007, 2008).

Apart from market forces, the price of building materials may also be controlled by the government. To facilitate the local construction industry, the government can fix the price levels, and provide subsidies for some materials, especially for the materials that are used in public sector projects. The government can encourage or discourage the import of some building materials by changing import duties, and taxes, or quotas on them (World Bank, 1984; ICR Research, 2007, 2008).

Sources of Finance

Financing production in construction is quite different from that in manufacturing. The production in construction is financed largely by clients, rather than the contractors, the producers of construction products. At the top of the payment chain in the construction industry are the contractors and at the bottom are the subcontractors and the suppliers. Contractors receive advance payments and periodic payments to mobilize resources (labour, equipment and materials) necessary for the construction projects. Cash flow of subcontractors and suppliers are therefore also affected by the payment procedure. The source of client’s finance is often in the form of bank loans backed by the constructed facility itself. Although the major source of finance come from clients, the contractors in some countries can obtain bank loans from special banks, which are established to assist the financing of construction works and investments in the construction industry. Other forms of financial assistance that help contractors get started in heavy construction works can include supplier credit, direct loans from commercial banks, and the establishment of companies that lease and hire equipment (World Bank, 1984).

Contractors’ financial concerns can be different across the construction phases and the technology employed. The initial stages of mobilization require a large amount of cash, especially for contractors using the equipment-intensive construction technology to purchase the equipment. Meanwhile, cash flow at the later stages of an uneventful construction operation is generally more stable. Delayed payments and uncertainty of cash flow are common in the construction industry (World Bank, 1984). The problem has continually raised concerns in construction industries throughout the world, although the problem can be more serious in the developing countries. Payment problems were considered a factor that can hamper the healthy development of the construction industry (Wu et al., 2008).

In the developing countries, financial aids for the major construction projects largely come from the government or international agencies. This is because an infrastructural construction project is often capital-intensive, and due to its public good characteristics, is not directly seen to be feasible from the viewpoint of individual private investors. For example, a new transportation facility could bring about improvement in the performance of all individual firms. However, it is not in the interests of an individual firm to address such issues. Moreover, the high cost of investment may render the returns from the project unenviable. Meanwhile, the external effects of the consumption of such goods by the whole community can go beyond the benefits to individual investors. In other words, the social rate of returns from such investments is higher than the purely private rate of return. In that case, it is the responsibility of the government to provide the investment-goods for the economy as a whole. Consequently, public investments form the major source of demand for construction in these countries. In such a situation, the government and these international agencies can exert great influence on the level of construction activity through their loan conditions (Moavenzadeh, 1978). Therefore, investments in the construction industry can be used as a government tool to introduce desired changes in the economy (Lea, 1973; Ofori, 1988; Lange & Mills, 1979; United Nations, 1976; Hillebrandt, 2000; Howes & Robinson, 2005). This would be examined further below.

However, some infrastructural facilities are quasi-public goods. That is, infrastructure displays public good properties up to a certain point. When the infrastructure gets overly congested, it diminishes the benefits of other users. At this point, there is rivalry in the consumption of infrastructure services, and positive marginal cost. The private good characteristics of some infrastructural facilities make it more productive for the private sector to provide (Howes & Robinson, 2005). As a result, there has been a shift away from public demand to private demand for infrastructural construction in more developed countries (Colean & Newcomb, 1952; Hillebrandt, 2000). Only a small part of the demand is public demand in these countries because of national security issues. Although infrastructure in some developing countries has started to be privatized, governments of most developing countries still own and finance nearly all infrastructure (Colean & Newcomb, 1952; World Bank, 1994). Recently, the development of new arrangements of both private and public financing (i.e. public-private partnership or PPP) has broadened the provision capacity of infrastructural construction (Hillebrandt, 2000; Howes & Robinson, 2005).

Construction and Aggregate Output

Capital Formation

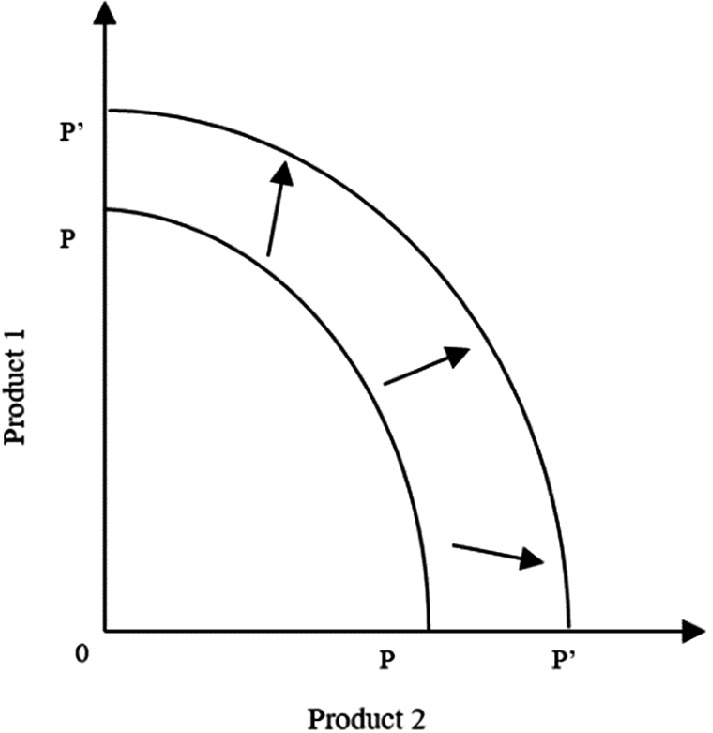

The productive capacity of an economy is usually described in terms of the complete utilization of factors of production; that is the full employment of the factors of production (labour and capital). Hence, the productive capacity determines the aggregate supply or national output of an economy in the long run. If there are changes in the total capital stock, the fixed amount of national output will change accordingly. One way for an economy to expand production or grow is to invest in capital stocks (human and physical resources). The relationship has long been recognized in economic theory. According to the Harrod-Domar model of economic growth, net investment (I), which is defined as the change in the capital stock (ΔK), is necessary for the economy to grow. Besides investments in new factories, machinery, equipment, and materials, investments in economic infrastructure—roads, electricity, communication and the like—also increase the physical capital stock of a nation, thus expanding national output level. Investments in economic infrastructure are considered a supplement to other physical capital. For example, a farmer may increase the total output of the crops by an investment in a new tractor, but without adequate transport facilities, this extra product cannot be available in local commercial markets, and thus his investment may not add anything to national food production. As a result, assuming there were only two products, product 1 and product 2, produced by the economy at a given technology level, increases in capital stock (human and physical resources) would make it possible to shift the production possibility curve outward uniformly from PP to P’P’ as shown in Fig. 2.1 (Todaro & Smith, 2003).

Fig. 2.1.

Effect of increases in capital stock on the production possibility frontier

Infrastructure can also raise productivity of other factors of production. For example, an installation of a new irrigation system can improve the quality of farm land, thus raising productivity per hectare and shifting the production possibility curve outward (Todaro & Smith, 2003). The higher productivity in turn attracts more resources (private investments) into production, which further contribute to higher levels of output, profitability of production, income and employment in these sectors. The process of investing in the physical capital stocks of an economy, including infrastructure is measured by the gross fixed capital formation (GFCF).

There has been a huge amount of literature analyzing the positive correlation between aggregate output growth and investments in infrastructure. In the end 1980s and early 1990s, many empirical studies on the returns on total infrastructure investments indicated high rates of returns in developed countries such as the US (Aschauer, 1989; Munnell, 1990), Sweden (Berndt & Hansson, 1992), and Canada (Wylie, 1996). There have also been studies focusing on a specific type of infrastructure. In the European Conference of Ministers of Transport (ECMT) (2002), transport was demonstrated to foster economic development by enhancing the efficiency of the economic system in both the goods and employment markets. Easterly and Rebelo (1993) studied historical time series and cross-country data of 28 developed countries. The study showed a highly and consistently positive correlation between transport and communication investments, and economic growth rate. Studies aimed at the developing countries have also been conducted by Canning and Fay (1993), and Canning (1998). Throughout these studies, transportation and telephone systems appears to promote economic growth. For example, Canning and Fay (1993) examined the rates of returns of the transportation (road and rail) infrastructure and telephone systems from 1960 to 1980 in 104 countries at different income levels. The cross section analysis showed that both transportation and telephone systems had large effects on growth rates, with high rates of returns; especially for countries with lower ratios of infrastructure to output, the rates of returns were higher than 40%. Many studies addressed the impacts of inadequate infrastructure on economic development as well. For example, in a study of economic development in Africa by Mountjoy and Hilling (1988), low rate of capital formation was argued to have a clear link with poverty in this continent. The study by the United Nations (1990) indicated that infrastructural development was an essential part of economic development in Asia and the Pacific region. As a result, this has been interpreted as a causal linkage, suggesting that infrastructure investment does appear to lead economic growth by improving the capacity as well as the efficiency of the economy.

As an industry supplying the physical infrastructure facilities, construction thus has a profound impact on economic development. GFCF by construction is the total value of all additions within a year, including new construction and all capital alterations or extensions, which significantly improve upon the utility or extend the life of the building or works to fixed capital. Repair and maintenance are not included in the indicator (Turin, 1969; Ofori, 1990). Many studies have emphasized that about half of the investments in GFCF in most developing countries comes from construction (Turin, 1978; Ofori, 1988; Lewis, 1955; World Bank, 1984; Wells, 1985; Gruneberg, 1997; Hillebrandt, 2000; Ruddock & Lopes, 2006). It is thus understandable that the construction industry plays a dominant role in a country’s rate of GFCF (Lewis, 1955; Gruneberg, 1997). The cross-section analysis of 87 countries at different per capita GDP levels during the period of 1955–65 by Turin (1969) showed a strong linear correlation between the logarithms of per capita formation by construction and per capita GDP. The share of capital formation in construction in GDP also increased with per capita GDP (Turin, 1969). Further studies by Strassmann (1970), Turin (1973) and Wells (1986) all argued that during the periods of accelerating economic growth, the construction industry needs to grow faster than the economy as a whole. A study by the World Bank (1994) also confirmed that infrastructure has to expand fast enough to create adequate infrastructure and productive facilities for economic growth (World Bank, 1994). Inadequate construction capacity is therefore a constraint on capital investment programs (Wells, 1986).

National Income

Construction like any other economic activities can contribute to national income by creating income or value adds. Based on the definition by the United Nations, Ofori (1990) explained that value added in construction is the gross output value at producer’s prices less the value of all industry’s current purchases from other enterprises. It is important to note that according to the narrowly defined scope of the construction industry, all industry’s current purchases from other enterprises are excluded, which are the value of input materials and components, costs of hiring plant, costs of goods sold in the same conditions as purchased, legal and other professional fees, and payments made for repair and maintenance undertaken by others on the construction firm’s own assets. Value added therefore is actually the sum of salaries and wages of employees, interest on borrowed capital, net rent, profit and allowance for depreciation (Ofori, 1990). According to data provided by the World Bank (1984), the value added-to-output ratios of the construction industry in most developing countries were higher than that of manufacturing over the period of 1970–1980. In some countries, the ratios of the construction industry could be as high as 60% (World Bank, 1984).

The linkage between the value added of construction as a share in GDP and per capita GDP has long been recognized. According to Turin (1969) and Strassmann (1970), there is a strong linear correlation between the logarithms of per capita value added by construction and per capita GDP. The share of value added in construction as a percentage in GDP also increases as per capita GDP increases. The share of the valued added in construction as a percentage to GDP was found to be around 3–5% for developing countries and 5–8% for more developed countries over the period of 1955–1965 (Turin, 1969). The results were later confirmed by many other studies such as those completed by Edmonds and Miles (1984), Wells (1985, 1986), Ofori (1988), Low and Leong (1992), and Chen (1998). Although these studies focused more on the static view of the close relationship between construction activity and economic growth, these studies do note that construction’s role in the economy would decline when the economy reaches the middle income stage (Strassmann, 1970) or when the volume of construction products was sufficient to raise the productive capacity of the economy at a steady growth rate (Wells, 1986). The contribution of the construction industry required for a steady economic growth as suggested by Edmonds (1979) should be 5% of GDP. Lopes, Ruddock, and Ribeiro (2002) also demonstrated that when the share of construction value added in GDP was around 4–5%, the economy would enter a period of sustained growth. The level should be interpreted within the long term trend rather than the annual fluctuation (Lopes et al. 2002).

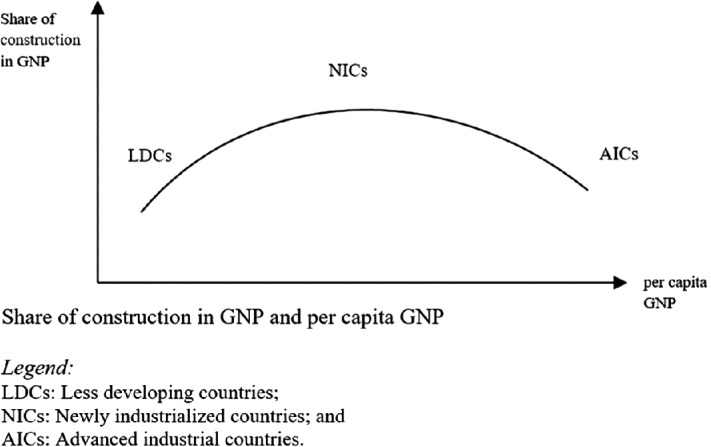

The dynamic views of construction in the national economy have been further examined by Bon (1992, 2000). Analyzing the data over different development stages in the more developed countries, the US, UK, Japan, Italy, Finland and Ireland, Bon (1992, 2000) argued that as a country develops, the share of construction in total GNP as well as the total construction output actually follows an inverted U-shape. That is, in the initial development stages, the share of construction output in GNP increases, but starts to decline in the more mature stages. Thus in the long run, the volume of construction output will decline accordingly. The contribution of the construction industry to economic growth is therefore not indefinite (non-linear relationship). Bon (1992, 2000) observed that there is a point at which the basic major infrastructure is put in place and the need for new construction gradually becomes less. However, Ruddock and Lopes (2006) and Lopes (2009) argued that in the more mature stages of development, construction output declines only in relative terms, not in absolute terms. That is, in the more developed countries, construction still grow but at slower rates than the economy. The inverted U-shaped relationship between the share of construction in GNP and GNP per capita proposed by Bon (1992, 2000) (as shown in Fig. 2.2) was further confirmed by Maddison (1987), Crosthwaite (2000) and Yiu, Lu, Leung, and Jin (2004). These observations implied that capacity expansion in construction is more important for the developing countries than for the developed countries. The feature of the activity in the industry is also different between the developing and developed countries. Repair and maintenance capacity become important in the developed countries, whereas the industry’s capacity for new build as well as the development of capacity for repair and maintenance is a major focus of the developing countries (Bon & Crosthwaite, 2000).

Fig. 2.2.

Share of construction in GNP and per capita GNP

As a result, policy implications within the literature have focused on the measures to expand the capacity of the construction industry in the developing countries. The development strategies for the construction industry are consequently centered on the schemes to remove the constraints of the industry’s production factors such as labour, materials, capital and technology. By building up an adequate domestic capacity, the construction industry is expected to drive economic growth. The policy recommendations also include creating an institutional environment that facilitates a competitive business environment for an efficient construction industry. At the macroeconomic level, monetary and interest rate policies are expected to deal with the distortions in factor prices, the limits to the availability of foreign exchange for the purchase of imported inputs and related issues such as foreign exchange rates and import tariffs. Meanwhile, fiscal policies related to government spendings and taxes on public construction works are expected to encourage employment, and to stabilize construction activities. Throughout these studies, the role of governments has been demonstrated by using these policies to directly or indirectly influence construction activities to stimulate economic growth.

Other Observations

Further empirical studies have shown that the contribution of construction in the economy as suggested by Turin (1969) as well as Bon (1992, 2000) is not consistent across countries, especially in the developing countries. The data provided by the World Bank (1984) indicated that construction value added in most developing countries over the period of 1970–1980 varied between 3 and 8% of GDP. Studying the data of 75 countries in 2003, Ruddock and Lopes (2006) found that the share of gross value added in construction varied considerably from over 2% to over 10% across countries in the same category of GDP per capita. Meanwhile, a study of the share of construction in GFCF by Lewis (2009) found that the figure was much lower than 50% as suggested by previous studies. The average proportion of construction in GFCF from 1970 to 2006 for developed countries was around 26% and for the developing countries was around 23%. There was also a trend of divergence among the developing countries. The divergence trend was explained by the fact that most infrastructure in the developing countries was financed by the government; and thus was directly affected by different government-expenditure policies (Lewis, 2009).

The problem of the direction of the causality between construction and GDP has also been analyzed. However, the results of these empirical studies were inconclusive. On the one hand, the study using data from Hong Kong by Tse and Ganesan (1997) indicated that the causality ran from GDP to construction activity. On the other hand, the study using data from Western Europe by Wilhelmsson and Wigren (2009) showed that the causality effect was weak in the case of infrastructural construction in the long run. Meanwhile, Chan (2001), in studying the linkage between construction and other economic sectors in Singapore, found a bi-directional causal relationship between construction activities and GDP. In the case of China, the study by Zheng and Liu (2004) also indicated a bi-directional casual relationship; construction investment had a strong short-run effect on economic growth, whereas economic growth had a long-term effect on construction. Lewis (2009) indicated that the relationship between construction and the national economy of Trinidad and Tobago changed over time under different circumstances. During the economic upturn, the economy led construction; and during the economic downturn, construction drove the economy.

In striking contrast to a number of the above studies, there have been studies concerning the negative impacts of the construction industry in the economy. The concern was first raised by Drewer (1980). Analyzing the data of the United Nations Economic Commission for Europe (ECE) region between 1970 and 1976, Drewer (1980) observed that more construction works do not necessarily result in higher economic growth when resources are misallocated. Drewer (1997) found that the relationships between construction and the economy are unstable and the uncontrolled expansion of the construction industry could negatively impact the economy. A number of other studies found a negative relationship between public expenditure and economic growth. Analyzing data from 69 developing countries over a 20-year time series, Devarajan, Swaroop, and Zou (1996) noticed a statistically significant negative relationship between the share of central government investments on transport and communications, and per capita GDP. The study explained that the negative relation was possibly caused by political factors in decision-making. The study of the US data by Kocherlakota and Yi (1996) illustrated that infrastructure does not permanently raise economic growth rate. Furthermore, the study of infrastructure in developing countries by Devarajan et al. (1996) indicated that infrastructure actually had negative impacts on economic growth if infrastructure is over-supplied relative to the economic scale. The empirical analysis of 210 transportation infrastructure projects completed between 1969 and 1998 around the world by Flyvbjerg (2008) also confirmed the problem of an over-estimation of demand for infrastructure. The economic recessions in Southeast Asia in 1997, in Singapore in 1985 and in Trinidad and Tobago around the same time (Lewis, 1984; Ganesan, 2000) were caused by excessive supply of construction outputs. The pressures generated by the expansion of the construction industry may push up the costs of inputs (such as labour and materials), affect the availability of financial capital for other uses, and intensify environmental stress. As a result, the over-expansion of construction activities may affect macroeconomic stability by generating inflationary pressures, and misallocating as well as wasting resources. The negative impacts of over-expansion of construction activities may considerably offset the real growth of the economy.

Construction and Sectoral Output

The ability of the construction industry to stimulate economic growth also comes from the strong linkages between construction and other sectors in the economy. The construction industry is one of the top four out of twenty economic sectors in terms of inter-sectoral linkages, backward and forward linkages (Riedel & Schultz, 1978). The important role of construction through a complex set of inter-relationships was also highlighted by Ofori (1990).

Backward Linkages

Since large quantities of building materials and components are purchased from a large number of supply industries, an expansion of the construction industry can stimulate the expansion of these industries through backward linkages. The impact can be significantly large because much of the building materials can be provided by relatively unsophisticated labour-intensive domestic resources and by basic industries such as cement and steel manufacturing (World Bank, 1984). Many input-output analyses (Park, 1989; Pietroforte & Bon, 1995; Bon & Yashiro, 1996; Bon, Birgonul, & Ozdogan, 1999) have demonstrated the strong backward linkages. Consequently, should the value added by construction takes into consideration the backward linkages such as the manufacture of building materials and components, the value added can account for a considerable proportion in GDP. The value added through backward linkages could be up to 55% of the value of construction purchases of materials and services from other industries (Kirmani, 1988). However, it is important to note that the value add will be high when locally produced inputs are used. Hence, while imported materials may be necessary in the short run, an economy needs to develop its local supply industries in the long run if it aims to increase value add. These issues have been addressed in many studies (Drewers, 1980; Wells, 1986).

Forward Linkages

The indexes of forward linkages of the construction industry are relatively less extensive than that of the industry’s backward linkages (Bon & Minami, 1986; Bon & Pietroforte, 1990; Pietroforte & Bon, 1995; Bon & Yashiro, 1996; Bon et al., 1999). Nevertheless, the magnitude of the forward linkages can be more significant since the demand for construction outputs is derived demand from all other sectors of the economy. As a result, how these sectors react to the change in the level of construction activity, and vice versa, ultimately affect the economy.

Within the literature of infrastructure, how infrastructure impacts on other sectors is somewhat clear. Many studies have shown the strong linkages between infrastructure investments and sectoral outputs. The strong linkages stem from the fact that all other sectors of the economy use the flow of services generated by infrastructure, which in turn can lead to growth in the production of other economic sectors in two ways: through the reduction in costs of intermediate inputs from infrastructure services such as transport, water and electricity; and through the increase in the productivity of other factors of production. As a result, the supply of infrastructure services can raise the profitability of production, level of returns, output, income and employment of other sectors. In studies by Binswanger et al. (1987, 1993), roads and electricity supply were found to have a strong positive effect on aggregate agricultural output, as well as the growth of farm investments. Antle (1983) found that spending on transport and communication services was a significant determinant of differences in aggregate agricultural productivity across countries. The study by Chhibber (1988) concluded that public goods and services, including infrastructure, were the determinant of agricultural outputs in the developing countries; meanwhile, in the more developed countries which had better basic infrastructure, the determinant was price. Elhance and Lakshmanan (1988), Kranton (1991) and Lee and Anas (1992) examined the contribution of infrastructure to growth through reductions in costs and found that infrastructure could be a major share of business expenses. The unreliable delivery of infrastructure services and lack of access to infrastructure services could result in multiple economic costs such as direct costs of production delays, loss of perishable raw materials or outputs, costs of under-utilization of productive capacity, etc. In addition, several studies of the U.S. (Bartik, 1985; Carlton, 1979; Fox & Murray, 1990) indicated the impacts of infrastructure on attracting private capital. Among other infrastructure components, transportation was found to be the most important factor to locational decisions of business investments. Public investments in infrastructure was credited to have a positive effect on private investments in several studies of developing countries as reviewed by Chhibber and Dailami (1990) and Serven and Solimano (1992). Infrastructure has also become one of the determinants of international competitiveness, which directly impact the ability of countries to engage in international trade, and to compete for direct foreign investments. A number of studies on the relationship between infrastructure, especially transport and communication, and trade found that an adequate and reliable infrastructure system can promote trade, expand market through cost and time savings in transportation and telecommunications (Peters, 1992; Hulten, 1996; ECMT, 2002). The remarkable growth of a number of developing countries in Asia in recent decades has been attributable much to the expansion of international trade, which in turn has been supported by the development of infrastructure systems (Hukill & Jussawalla, 1989; Brooks & Menon, 2008). All these important contributions of infrastructure on other sectors of the economy highlight the crucial role of construction’s supply capacity in raising other sectoral outputs. However, little is known about the reverse flow of influence, which is how the adaptive capacities of other economic sectors can affect the construction sector. The influence is equally important since over-expansion of the construction sector and misallocation of resources in the economy might stem from the lack of understanding of this effect.

Construction and Macro-economic Stabilization

The contribution of construction in the economy has also been measured by construction employment as a share of total employment (Strassmann, 1970; Turin, 1978; Wells, 1985). Turin (1978) suggested that since employment in construction correlated positively with economic growth, there is a potential use of construction to generate sustained employment. Turin (1978) also argued that the misuse of construction by the government as a cheap way to absorb unskilled unemployment through ill-planned public work programs would only damage the healthy development of the construction industry.

Numerous data has shown that there have been dramatic increases in construction employment in most developing countries (International Labour Office, 2001). The fact that the construction industry is more labour intensive than many other industries, especially relative to manufacturing (Hillebrandt, 2000), makes the industry a traditional focus of employment-generation policy in many countries through labour-intensive public works projects. The labour created in these projects in turn spends the income from the employment on other locally produced goods and services, thereby stimulating demand in the rest of the economy through the multiplier effect. The employment multiplier effect also makes public works a more promising instrument for moderating the business cycle over others such as credit or tax incentives offered to the private sector. As a result, during periods of slack demand and high unemployment rate, infrastructural construction projects funded by the government are often implemented as a counter-cyclical instrument (Gruneberg, 1997; Hillebrandt, 2000). Similarly, the government can stabilize the economy by postponing these projects during boom periods (Burns & Grebler, 1984). Through fiscal policy such as changing the amount of public expenditure or interest rates of loans financing these infrastructure projects, the government can generate desired changes in the economy, which has been the subject of many studies (Lea, 1973; Ofori, 1988; Lange & Mills, 1979; United Nations, 1976; Hillebrandt, 2000; Howes & Robinson, 2005). The 2008–2009 economic crisis has witnessed many countries relying considerably on construction spendings to jumpstart the economy and spur employment. Many countries around the world have included construction of infrastructure such as railways, highways, airports and power grids into their fiscal stimulus packages (Donnges, 2009).

However, there are several difficulties in realizing the expected results. One of the difficulties is the time lag between government action and the actual construction works from the project start to completion. As a result, “unless the government can foresee problems far in advance, the effect will be too slow to be useful at the beginning of the period and the major effect will come much later, perhaps at a time when the contrary effect is clearly required” (Hillebrandt, 2000, p. 188). Other difficulties might come from technical considerations when the government wants to postpone infrastructural construction. Technical problems make it difficult and costly to cancel infrastructural construction in mid-stream (Burns & Grebler, 1984). An empirical study of the regional data of the U.S. by Duffy-Deno and Eberts (1991) indicated that these difficulties caused infrastructure to only have short-run multiplier effects.

In many poor countries, the objective of public programs is usually a combination of poverty alleviation, employment generation and the provision of infrastructure. These public programs have been carried out for decades in South Asia and Africa (World Bank, 1994). However, the results of these programs were varied. On the one hand, as reviewed by Kessides (1992), the emphasis of traditional public work programs on short-term benefits (through quick creation of employment and assets) have dampened the long term economic benefits, which could be derived from more careful project selection, creation of higher-quality assets, and more emphasis on the training of workers. On the other hand, as reviewed by McCutcheon (2001), large scale programs for employment-intensive construction and maintenance have successfully created employment without compromising cost, quality or time. The experience suggests that these programs should be integrated into other long term development programs to generate the greatest benefits.

Government Institutions for Construction Industry Development

The role of the construction industry in the economy recognized by academics has led to the recommendation of creating a government agency which specifically deals with the development of the construction industry. Having observed the critical role of construction in the developing economies, Turin (1978) suggested the establishment of such a government department. The roles and functions of such an agency were furthered analyzed by Ofori (1985). Several countries have realized the constraints of the domestic construction industry and have established sophisticated agencies to guide the industry towards development. The Construction Industry Development Board of South Africa was established in 2000 after the 1997 Green Paper identified some of the challenges facing the industry (Construction Industry Development Board, 2000). In Australia, after a report prepared by the Joint Working Party (consisting of the major contractors, the Australian Federation of Construction Contractors, the National Building and Construction Council and the National Public Works Committee) to provide a report on the difficulties facing the industry in the late 1980s, the government outlined the Construction Industry Reform Strategy, which led to the establishment of the Construction Industry Development Agency and Construction Industry Development Council in 1992 (Commonwealth of Australia Law, 1992; Royal Commission into the Building and Construction Industry, 2002). The Construction Industry Development Board of Singapore was formed in 1984 to deal with the then pressing issues of the industry (Ofori, 1993) which has now been renamed the Building and Construction Authority (BCA). Some other example of countries that have established the bureau or boards to respond to problems in the construction industry include Indonesia, India and Malaysia. The government agencies are often under ministerial control. Members of these agencies are usually appointed by the Ministry and compose of government officials, academics and private consultants to monitor and manage the sector. Generally, the creation of these agencies is to address the issues concerning the weaknesses of the local construction industry. The common functions of the agencies relate to formulating, monitoring, managing policies, standards, programs and initiatives to deal with the shortage of local skilled labour, materials, low output productivity and quality, or the low competitiveness of the local construction industry. Other focus might be the issues relating to sustainability, regulatory reforms, new procurement procedures and measurement of the industry’s performance. To fulfill these functions, these agencies formed divisions or departments, and advisory boards or committees for specific purposes. For example, the Construction Industry Development Board of Singapore, when established in 1984, consisted of the Manpower Division (to deal with manpower development), Technology Development Division (to deal with technology development) and Industrial Development Division (to deal with commercial aspects of construction industry) (Ofori, 1993).

Other government agencies, professional bodies and trade associations, and academic institutions can also impact construction industry development (Ofori, 1994; Miles & Neale, 1991; Tan, 2002). Construction activities can be influenced by other government bodies such as the Ministry of Finance (through public spending and fiscal policies, etc.), the Ministry of Trade and Industry (through raw materials, manufacturing regulations, prices, tariff, taxes, etc.), and the Ministry of Labour (employment regulations, site safety, wage policies, etc.). The roles of professional bodies and trade associations were also emphasized (Ofori, 1994; Miles & Neale, 1991). These institutions can enhance the competitivenessl of the construction industry by preparing their members necessary skills “through accreditation of courses, continuing professional development and dissemination of relevant state-of-the-art information and facilities through central data services, computerized libraries and similar” (Ofori, 1994, p. 208). In this context, academic institutions implement research programs, providing the industry with pertinent views about shortcomings in construction, and new techniques or approaches to overcome these shortcomings.

By establishing these institutions to attend to pressing issues in the construction industry, governments have demonstrated an active commitment to construction industry development. The agency that is specifically concerned with construction industry development can be considered the core agency for this purpose. To function effectively, the core agency needs to co-ordinate with other government bodies and organizations in connection with the performance of its tasks.

Key Concepts

The key concepts relating to the role of the construction industry in economic development over the past 40 years were reviewed above. Much of the existing empirical literature on the linkage between construction and economic growth seeks to capture this effect through observation of the relationship between increases in the construction outputs (measured by the share of construction in GFCF or value added) and some measures of aggregate output (GDP or GNP). Many of the findings from these studies over the past 40 years have demonstrated the positive and statistical significant relationship between the construction industry and economic growth in the developing countries. However, the conclusions have been questioned when further studies on this relationship were conducted for more developed countries. The results of these studies indicate that the relationship between economic development and the construction industry appears to be more complicated. Moreover, whether growth in the share of the value of construction activities in total GDP is a cause or a consequence of economic growth is not clear. However, there exists a general consensus on the underlying pattern of the relationship between GDP per capita and the share of construction in total GDP. This means that in the initial development stages of an economy, the share of the construction industry in GDP increases at a faster rate, then levels off and finally declines at higher levels of economic development. This suggests that in developing countries, construction is still a crucial factor for consideration when economic policies in these countries are being formulated.

Since construction involves high stakes in the developing economies, most of the policy implications recommended within the literature focus on stimulating construction outputs, and expand the domestic construction capacity. However, the preceding discussion also suggests that there are high potential costs from over-expansion in the sector, especially in infrastructural construction. Consequently, construction might contribute to the economy in the short run, but offset the real growth of the economy in the long run. Since demand for construction is derived demand from other sectors of the economy, construction can only contribute to the economy when there is sufficient complement and basic productive level of other sectors to absorb the construction outputs. Further expansion of the construction industry beyond the adaptive capacity of the economy will only waste national resources (Dang & Low, 2015).

When placed within the institutional framework described above, the relationship between the construction industry and the national economy is strategically an important one. This is because beyond this, there are also other implications relating to market competitiveness that can affect allied issues such as construction quality delivered during boom and bust times in the national economy. In this context, construction quality may be compromised when contracting firms try to cut corners in order to survive during a recession. It is therefore of interest to understand how construction quality pans out correspondingly with national economic performance. The national economy and construction industry of Singapore, where this study was based, will be examined for this purpose.

Economic Recessions in Singapore

The economic cycle is the natural fluctuation of the economy. An economic cycle, also referred to as the business cycle, has four stages: recovery, peak, recession and trough. As the terminology suggests, economic cycles are recurring and the economy revisits each phase of the cycle.

In the United Kingdom, recessions are measured by the adjusted quarter-on-quarter figures for real GDP; commonly defined as two consecutive quarters of negative economic growth (BBC NEWS, 2018; “Glossary of Treasury terms”, 2018). Similarly, Singapore defines a technical recession as two consecutive quarters of decline in economic output (Chia, 2016). Figure 2.3 illustrates the quarterly GDP of Singapore spanning the first quarter of 1993 to the third quarter of 2017. Table 2.1 specifies the economic recessions experienced in Singapore since the country gained independence in 1965.

Fig. 2.3.

Quarterly GDP of Singapore

(Source SingStat, 2018)

Table 2.1.

Timeline of recessionary periods in Singapore post-1965

| No. | Recessions | Remarks |

|---|---|---|

| 1 | 1985–1986 | In 1985, the Singapore economy went into a recession (Menon, 2015). Nonetheless, a swift recovery was made in mid-1986. By the second quarter of that year, Singapore posted a growth of 1.2%, which increased to 3.8% in the third quarter (NLB, 2018) |

| 2 | 1998–1999 | The Asian financial crisis in 1997 (Menon, 2015) |

| 3 | 2001–2003 | The global IT industry meltdown in 2001 (Menon, 2015) |

| The SARS virus in 2003 (Menon, 2015) | ||

| 4 | 2008–2009 | The Global financial crisis in 2008 (Menon, 2015) |

As observed from Fig. 2.3, there are two consecutive falls in GDP from 1998 Q1 to 1998 Q2, two consecutive falls from 1998 Q4 to 1999 Q1, three consecutive falls from 2001 Q1 to 2001 Q3, two consecutive falls from 2003 Q1 to 2003 Q2, two consecutive falls from 2008 Q1 to 2008 Q2 and two consecutive fall from 2008 Q4 to 2009 Q1. These periods are the periods of recession in Singapore since 1993. There were no data for the quarterly GDP between 1965 and 1992. Nonetheless, with archival sources, Table 2.1 shows the timeline of recessions in Singapore post-1965.

Economic Recessions and the Impact on Construction Firms

Firms in the construction industry have always had to confront economic cycles and developing strategies to address the resulting effects on them. In fact, economic recessions have huge effects on the construction industry, more so than most other industries (Ruddock, Kheir, & Ruddock, 2014). However, the cycles are rarely analyzed and management often cannot react correctly to the economic cycles because the firm is usually still reacting to the last cycle the company experienced, while simultaneously attempting to anticipate the actions needed to address the next cycle (Schleife, Sullivan, Murdough, & Wallace, 2014).

In Singapore, it was reported that approximately 97% of contractors suffered heavy losses as a result of the 1997 Asian financial crisis (The Contractor, 1998). Consequently, the number of construction firm cessations recorded rose by 49%; from 205 cases in 1997 to 306 cases in 1998 (Lim, Oo, & Ling, 2010). Many established contractors (such as Econ Corporation, Neo Corporation and Wan Soon Construction) applied for cessations during the 1997–2005 recessionary period (Teh, Sua, & Nadarajan, 2006). Table 2.2 identifies the impacts of economic recessions on the construction industry in further detail.

Table 2.2.

A review of existing literature on the impacts of economic recessions on the construction industry

| No. | Impacts of economic recessions on the construction industry | References |

|---|---|---|

| 1 | Fall in construction demand and volume of work | Grogan (2010), Ruddock, Kheir, and Ruddock (2014), Tansey (2014) |

| 2 | Construction firms feel pressure to get work | Lim et al. (2010) |

| 3 | Aggressive assumptions made for bidding | Lim et al. (2010) |

| 4 | Higher contractor to projects ratio | Alaka, Oyedele, Owolabi, Bilal, Ajayi, and Akinade (2017) |

| 5 | Bidding competition increases | Alaka et al. (2017), Ruddock et al. (2014), Tansey (2014), Yoo and Kim (2015) |

| 6 | More changes to the agreed scope of works and/or requests for increase in speed of project | Treacy, Spillane, and Tansey (2016) |

| 7 | Fall in prices of property | Grogan (2010), Yoo and Kim (2015) |

| 8 | Poorly motivated people resulting in declining performance in all areas | Schleife et al. (2014), Albattah, Shun, Goodrum, and Taylor (2017) |

| 9 | Risk of failure in the supply chain which includes subcontractors and suppliers | Ruddock et al. (2014) |

| 10 | Overhead costs rises | Lim et al. (2010) |

| 11 | Clients defaulting on their payment | Ruddock et al. (2014) |

| 12 | Sources of fund are affected and firms see a reduction in lenders | Lim et al. (2010), Ling and Lin (2013), Tansey (2014), Thach and Oanh (2018) |

| 13 | Higher interest rates charged for lending i.e. higher costs of borrowing | Deereper, Lobez, and Statnik (2017) |

| 14 | Fluctuations in prices of materials, manpower and machinery | BCA (2018b) |

Table 2.2 details the impacts of economic recessions on the construction industry as suggested by existing literature. However, it is important to understand firms’ perceived impacts (for they can be exaggerated, reduced or even absent) in order to better capture firms’ considerations and the subsequent decisions they make. As such, Hypotheses 1a–1p are formulated; following the analysis of trends such as construction contracts awarded annually as shown in Fig. 2.4 and the prices of construction resources discussed later.

Fig. 2.4.

Construction contracts awarded annually in Singapore

(Source BCA, 2018b)

Keeping in mind the periods of economic recession detailed in Table 2.1, one can observe from Fig. 2.4 that the contracts awarded by the private sector falls in 1998 following the Asian financial crisis in 1997, in 2001 following the global IT meltdown in 2000 and in 2009, following the global financial crisis in 2008.

One observation from these dips is that there is a gestation period between economic recessions and the impacts on the construction industry. This is because, taking the 2008 recession (which Singapore was hit with in 2008 Q2) as a case in point, the contract value awarded in the private sector was $6.1 billion in 2008 Q1, $7.1 billion in 2008 Q2, $5.2 billion in 2008 Q3, $1.8 billion in 2008 Q4, less than $1 billion in 2009 Q1 and $1.5 billion in 2009 Q2. Keeping in mind that it takes on average three to six months for the tendering process before contracts are awarded, the statistics presented suggest that construction demand may have reacted instantly to periods of economic recessions. Hence, the reflection of the lower volume of contracts awarded in 2009 Q1 and 2009 Q2 is a result of lesser construction demand two to three quarters prior to these contract award periods. However, one should note that at the point of recession, firms in Singapore are still preoccupied with jobs. The impacts are only felt two to three quarters after the onset of an economic recession. In fact, even at the point where the total value of building commencement falls, contractors may not have been affected yet because sufficient works are still around to keep their resources occupied. It is only upon substantial completion of construction work and when the same resources are left idle that the impacts would set in (Low & Tan, 1996b). This would suggest that the total time lag for certain effects of economic recessions to affect firms would be beyond two to three quarters. Having said that, Hypotheses 1a–1l are set out as follows.

Hypothesis 1a: When an economy falls towards a recession, the construction demand in Singapore falls.

Hypothesis 1b: When an economy falls towards a recession, firms’ pressure to secure new projects rises.

Hypothesis 1c: When an economy falls towards a recession, the more aggressive the assumptions made by firms in deriving the bid price.

Hypothesis 1d: When an economy falls towards a recession, the number of bidders per project generally rises.

Hypothesis 1e: When an economy falls towards a recession, bidding competition rises.

Hypothesis 1f: When an economy falls towards a recession, the changes to the agreed scope of work rises.

Hypothesis 1g: When an economy falls towards a recession, employee productivity falls.

Hypothesis 1h: When an economy falls towards a recession, supply chain reliability (which includes subcontractors and suppliers) falls.

Hypothesis 1i: When an economy falls towards a recession, overhead costs rises.

Hypothesis 1j : When an economy falls towards a recession, defaults in payment rises.

Hypothesis 1k: When an economy falls towards a recession, sources of fund decreases.

Hypothesis 1l: When an economy falls towards a recession, lending/interest rates rises.

With reference to the fall in property prices, the research team studied the “Singapore residential property price index” and “Singapore office space in central region price index” from 1975 to 2018 in Figs. 2.5 and 2.6.

Fig. 2.5.

Singapore residential property price index

(Source Trading Economics, 2018)

Fig. 2.6.

Singapore office space in central region price index

(Source Trading Economics, 2018)

With reference to Figs. 2.5 and 2.6, one observes an instant fall in the prices of property (for both residential and commercial) following recessions with sharp declines of property prices in 1997 Q1 and 2008 Q1. Hence, it can be concluded that there is a positive correlation between economic recessions and property prices and there is little to no gestation period between the downturn of an economy and the fall in property prices. Hypothesis 1m is established to test the perceived impact of this phenomenon on main contractors and subcontractors in times of economic recession.

Hypothesis 1m: When an economy falls towards a recession, property prices fall.

In relation to the fluctuations in the prices of materials, manpower and machinery, examining the trends with the aid of time series statistics from government archives would shed light on the effects of economic recessions on the prices of materials, manpower and machinery. One useful indicator would be the tender price index as it reflects prices of major construction resources such as construction materials, manpower and machinery. The tender price index for Singapore’ Housing and Development Board (HDB) per se reflects the price movements in construction materials, equipment, manpower and elements of competition, risk and profit allowance by contractors (SISV, 2018). Figure 2.7 examines the tender price index in Singapore from 1987 to 2016.

Fig. 2.7.

Tender price index in Singapore

(Source BCA, 2018b)

From Fig. 2.7, the tender price index starts at a low point in 1987, falls in 1992 and falls relatively largely in 1998 and 1999, remained as a low in what some touted as an 8-year long recessionary period from 1997 to 2004 and falls in 2009 following the global financial crisis in 2008. The sharp decline in tender price index in 1998 and 2009 seems to suggest that prices of materials, manpower and machinery fall in times of economic recession. In addition to the tender price index, statistics on the price of steel, concrete, labour costs and wholesale trade index (for construction machinery) shall be studied as well. Figure 2.8 shows the trend in the prices of concrete and steel in Singapore from 1999 to 2017.

Fig. 2.8.

Price of concrete and steel in Singapore

(Source BCA, 2018b)