Abstract

The United States has recently set ambitious national goals for greenhouse gas (GHG) reductions over the coming decades. A portion of these reductions are based on expected sequestration and storage contributions from land use, land use change, and forestry (LULUCF). Significant uncertainty exists in future forest markets and thus the potential LULUCF contribution to US GHG reduction goals. This study seeks to inform the discussion by modeling US forest GHG accounts per different simulated demand scenarios across a grid of over 130,000 USDA Forest Service Forest Inventory and Analysis (FIA) forestland plots over the conterminous United States. This spatially disaggregated future supply is based on empirical yield functions for log volume, biomass and carbon. Demand data is based on a spatial database of over 2300 forest product manufacturing facilities representing 11 intermediate and 13 final solid and pulpwood products. Transportation costs are derived from fuel prices and the locations of FIA plot from which a log is harvested and mill or port destination. Trade between mills in intermediate products such as sawmill residues or planer shavings is also captured within the model formulation. The resulting partial spatial equilibrium model of the US forest sector is solved annually for the period 2015–2035 with demand shifted by energy prices and macroeconomic indicators from the US EIA’s Annual Energy Outlook for a Reference, Low Economic Growth, and High Economic Growth case. For each macroeconomic scenario simulated, figures showing historic and scenario-specific live tree carnon emissions and sequestration are generated. Maps of the spatial allocation of both forest harvesting and related carbon fluxes are presented at the National level and detail is given for both regions and ownerships.

1. Introduction

Increasing emissions of greenhouse gases globally, largely due to anthropogenic activities, have caused a substantial increase in atmospheric concentrations of these gases, contributing to climate change and related impacts, such as higher temperatures, on the planet’s natural systems (IPCC 2014; USEPA 2016a). As a result, many countries, U.S. states and cities have committed to pursue actions to reduce greenhouse gas (GHG) emissions. As part of international efforts to mitigate the expected long-term impacts of climate change, many nations have pledged specific GHG emissions reduction targets. Prior to and following the United Nations Framework Convention on Climate Change (UNFCCC) 2015 Conference of the Parties (COP 21) in Paris, 187 parties (single nations or coalitions of multiple nations) provided intended nationally determined contributions (INDCs), which represent each party’s anticipated individual post-2020 policy commitments to combat climate change via targeted mitigation actions to reduce emissions over time1 and accounts for a significant portion of current anthropogenic GHG emissions globally. In November 2016, the threshold for the Paris Agreement to enter into force - after at least 55 Parties to the Convention accounting for at least 55% of the total global GHGs emissions formally signed onto the Agreement – was passed, with 112 Parties of 197 Parties to the UNFCCC ratifying it, and signatories also submitted their final nationally determined contributions (NDCs).2 The U.S. 2015 INDC target calls for a 26–28% emissions reduction relative to 2005 levels and any future commitment could also consider a net emissions reduction relative to a historic period. In addition to previous national U.S. commitments made in the international arena, individual U.S. states and state coalitions have also made commitments to pursue climate action, including, for example, California, Washington, and Northeastern U.S. states (via the Regional Greenhouse Gas Initiative).

To meet these policy goals, however requires a projection of future emissions levels across all or specific sectors of the economy (pending on the policy scope) as well as a methodology to include possible mitigation actions within those projections. While projecting emissions from any sector of the economy can be difficult given uncertainty in future economic conditions, policy, and technological advancement, estimates of future land use, land use change, and forestry (LULUCF) activities and related GHG emissions and carbon sequestration present an especially unique challenge. In particular, projecting emissions from LULUCF sectors requires capturing complex carbon dynamics of different terrestrial ecosystems, the related interactions between terrestrial ecosystems and markets, and the potential extent and location of land use change between sectors.

This uncertainty in future potential emissions from U.S. forestry is also reflected in the 2016 Second Biennial Report (2016 BR2) submission by the U.S. under the UNFCCC (U.S. Dept. of State 2016), which presented high and low potential future net sequestration estimates rates rather than one single projection for the land use sectors. Net projected sequestration in 2030 ranges −689 to −1118 TgCO2e under the “Current Measures” (business as usual) scenario. The higher end of this range (−689 TgCO2e) is referred to as the “low sequestration” scenario, while the greater negative value (−1118 TgCO2e) represents “high sequestration.” The projected 2030 net annual GHG emissions flux for all sectors in the U.S. reported in the 2016 BR2, including the high and low sequestration scenarios (respectively), ranges 5274 to −5703 TgCO2e. The difference between these two scenarios (429 TgCO2e) is due to the high and low sequestration range given for LULUCF and represents approximately 6.6% of total net emissions in the U.S. for 2005 (which is the reference period the U.S. refers to in its 2015 INDC).

As the U.S. 2015 INDC target calls for a 26–28% emissions reduction relative to 2005 levels, this uncertainty range in the LULUCF sector represents a significant part of the overall U.S. strategy to reduce GHG emissions. Moreover, as mitigation commitments are set across all sectors, uncertainty in projected emissions of any individual sector makes comprehensive mitigation target setting and achieving difficult. Therefore, improving analytical tools for projecting future LULUCF emissions that capture the complex interactions between terrestrial and economic systems can improve future LULUCF net sequestration estimates, as well as overall U.S. economy-wide net emissions estimates, and mitigate risks of any future NDC non-compliance. Since the U.S. formally announced its intentions to withdraw from the Paris Agreement and renegotiate re-entry, it is likely that individual cities, states, or state coalition efforts on climate action will continue. Either way, as climate policy action continues at the state level, then a spatially disaggregated forest sector model tied to national markets would be necessary for projecting forest-related GHG emissions at a state or regional level. Such projections can be used to establish LULUCF emissions baselines or to develop climate mitigation strategies in the land use sectors.

Furthermore, if national or state obligations are formed based on expectations of relatively high sequestration from LULUCF and the opposite trend emerges, then additional mitigation actions would be needed to stabilize the emissions trajectory. Projections tools should be able to provide insights about different emissions trajectories and mitigation options, related GHG emissions reduction potential, and optimal locations and timing to invest in future mitigation actions to help inform the formation of policies needed to achieve the U.S. NDC and other regional or state climate goals.

While the modeling framework has broad application potential, this analysis focuses purely on variations in future macroeconomic conditions and the impact that these changes could have on localized CO2 emissions from forest management and biomass removals. Results from this analysis show that with no additional forest management intervention incentivized by policy or anticipated market changes (e.g., management intensification or afforestation), the U.S. forest carbon sink could diminish in the coming decades under status quo economic conditions. With exceptionally high housing starts or other policy factors that could drive regional harvest rates beyond recently observed levels (e.g., trade disputes and imposed lumber tariffs), it is possible the aboveground forest carbon sink could approach a positive emissions source in the coming decades. This result is consistent with the findings in Wear and Coulston (2015) but diverge from other recent research that focuses on the role of forest management and investment in projecting future forest carbon stocks in the U.S. (Tian et al. 2017). Regardless of how forest management is treated, results from this manuscript highlight the potential sensitivity of a key environmental attribute of the forest resource base to changing economic and policy conditions. We argue that this sensitivity deserves more analysis and that spatial allocation optimization modeling offers unique insight into potential changes in disaggregated regional biomass utilization trends and emissions outputs not offered by traditional structural and reduced form economic models.

2. Background

In terms of historic land use sector emissions and sequestration levels, recent estimates show that forests continue to be an important carbon sink globally (Pan et al. 2011), and that the size of that annual sink grew between 1990 and 2007 for some regions (including the U.S.). The 2016 U.S. GHG Inventory shows a net annual LULUCF emissions flux of −787 TgCO2e in 2014, including approximately −742 TgCO2e from forests remaining forests (USEPA 2016b). Furthermore, the United Nations Food and Agricultural Organization FAO 2015 Global Forest Resources Assessment (FAO 2015) notes that the growing stock of U.S. forests has grown more than 22% since 1990, and the annual growth rate increased from 0.8% per year (1990–2015) to 1.1% per year from 2010 to 2015. Thus, literature indicates that the U.S. has increased its forest carbon sink capacity in recent years.

Nonetheless, the future trajectory of U.S. forest carbon is less certain. As U.S. forests age, forest product demand grows, and urbanization and other factors like climate change alter forest size and attributes, it is possible that this sink could decline in the future. Nepal et al. (2012) show a wide range of projected U.S. forest carbon fluxes using a statistical simulation approach across a range of scenarios from the fourth IPCC special report on emissions (A1B, etc.). These projections range from a relatively stable U.S. forestry sink to a rapid decline, resulting in a switch from emissions sink to source within two decades. The 2010 Resource Planning Act Assessment (USFS 2012) also estimated future potential net forest carbon fluxes associated with different IPCC climate scenarios, with three scenarios showing the U.S. LULUCF carbon flux becoming a net GHG source and one scenario trending close to zero net sequestration over the next 15–35 years. A more recent study by Wear and Coulston (2015) show a decline in annual net sequestration in the U.S. of approximately 45% over the next 25 years. This includes some regions (such as the Southeastern U.S.) which transition from net sink to source.

Tian et al. (In Press) used applies an intertemporal optimization model of the global forest sector to project baseline emissions in the U.S., and show a stable sequestration rate that even rises slightly over the next 20–30 years as trends in forest management intensification and extensive margin expansion continue in the U.S. Tian et al. (In Press) also develop scenarios that limit the model’s ability to expand or intensify forest management in response to anticipated market conditions. Incorporating these restrictions has a meaningful effect on projected sequestration levels, as the most restrictive case (no land use change and no additional management) results in a declining sink similar to the projections from Wear and Coulston (2015).

3. Contributions of this study

While policies can help mitigate against loss of forest carbon and can further increase sequestration in the LULUCF sector and projections are an important component of both reporting and crafting such policy, it is important to better understand how economic drivers and model choice can influence LULUCF emissions fluxes in such projections. As discussed, some previous projections of U.S. forest carbon were developed using statistical simulation models (e.g., Nepal et al. 2012; Wear and Coulston 2015), or optimal control models of the forest resource system (Tian et al. In Press). To our knowledge, however, none have directly incorporated the spatial relationship between supply points (Forest Inventory and Analysis (FIA) plots) and demand points (forest product mills and ports) within an optimization framework for the entire conterminous U.S. This study attempts to fill this void by developing a Land Use and Resource Allocation (LURA) model of the U.S. forest resource and forest products markets that utilizes a spatial optimization methodology. This approach can offer additional insight into regional variation in forest emissions based on spatial dependencies in forest product markets and into how the extent of such variation may change over time. A spatial allocation model linked to underlying macroeconomic inputs can also be used to project a range in emissions outcomes to reflect a range in LULUCF emissions driven by uncertainty in potential future market conditions. Finally, these methods can be used to estimate the economic costs of targeted mitigation potential of various management options should future mitigation be needed in the forest sector to maintain or enhance net LULUCF sequestration.

The empirical approach offered by this paper is a departure from the econometric or reduced form models that have typically been used to project forest resource use and emissions. In this paper, we use a spatially explicit economic optimization model of the U.S. forestry sector to project near- and medium-term LULUCF emissions attributable to forest growth and harvest levels across private and public timberland. We illustrate how forest carbon flux projections can vary greatly with underlying macroeconomic drivers, including Gross Domestic Product (GDP) housing starts, and expected demand increases in bioenergy and forest products.

For the latter, the LURA modeling framework efficiently allocates forest resources to satisfy projected forest product demand targets over time. We adjust the projected demand for specific forest products based on key macroeconomic and energy market drivers from the 2015 Annual Energy Outlook (EIA, 2015), including GDP, housing starts, and diesel prices, to illustrate how changes in economic drivers can lead to large differences in forest carbon outcomes. Results indicate that the U.S. is likely to remain a strong forest carbon sink, but that annual sequestration levels decline over time as forests are harvested to meet increasing forest product demand, existing stands age, and new stands are planted. The rate of decline increases with higher economic growth, which drives housing starts, forest product demand, and bioenergy expansion.

Beyond climate mitigation action, the spatial allocation optimization methods presented in this manuscript have broad applicability to several relevant forest policy and market contexts. This includes regional (and national) assessments of forest biomass utilization for electricity generation in the U.S., and projections of alternative wood pellet production expansion scenarios to meet EU demand, which will build on an existing and growing literature base (e.g., Galik and Abt 2016; Wang et al. 2015; Latta et al. 2013). Furthermore, evaluating the impact of emerging policy topics such as changes to existing trade agreements (e.g. Canadian softwood lumber tariffs) on U.S. forest harvests, product supply, and prices would also benefit from a national and spatially explicit analysis. Finally, projections from this framework can be combined with spatially explicit representations of ecosystem services indicators to identify “hot-spots” where high levels of future economic output from forest management could collide with at-risk species and other ecosystem services.

Regional forest policy and related bioenergy policies vary substantially across the U.S., which can require more detailed regional frameworks to assess. However, there are major structural differences between existing national and regional forest sector models in the U.S. which makes consistent integration between national (or global) market models and regional frameworks cumbersome, as discussed in several recent papers (Galik et al. 2015; Galik et al. 2016). LURA is designed to bridge the gap between structural models developed at national scale with regional models that offer improved regional and geospatial detail.

3.1. Data

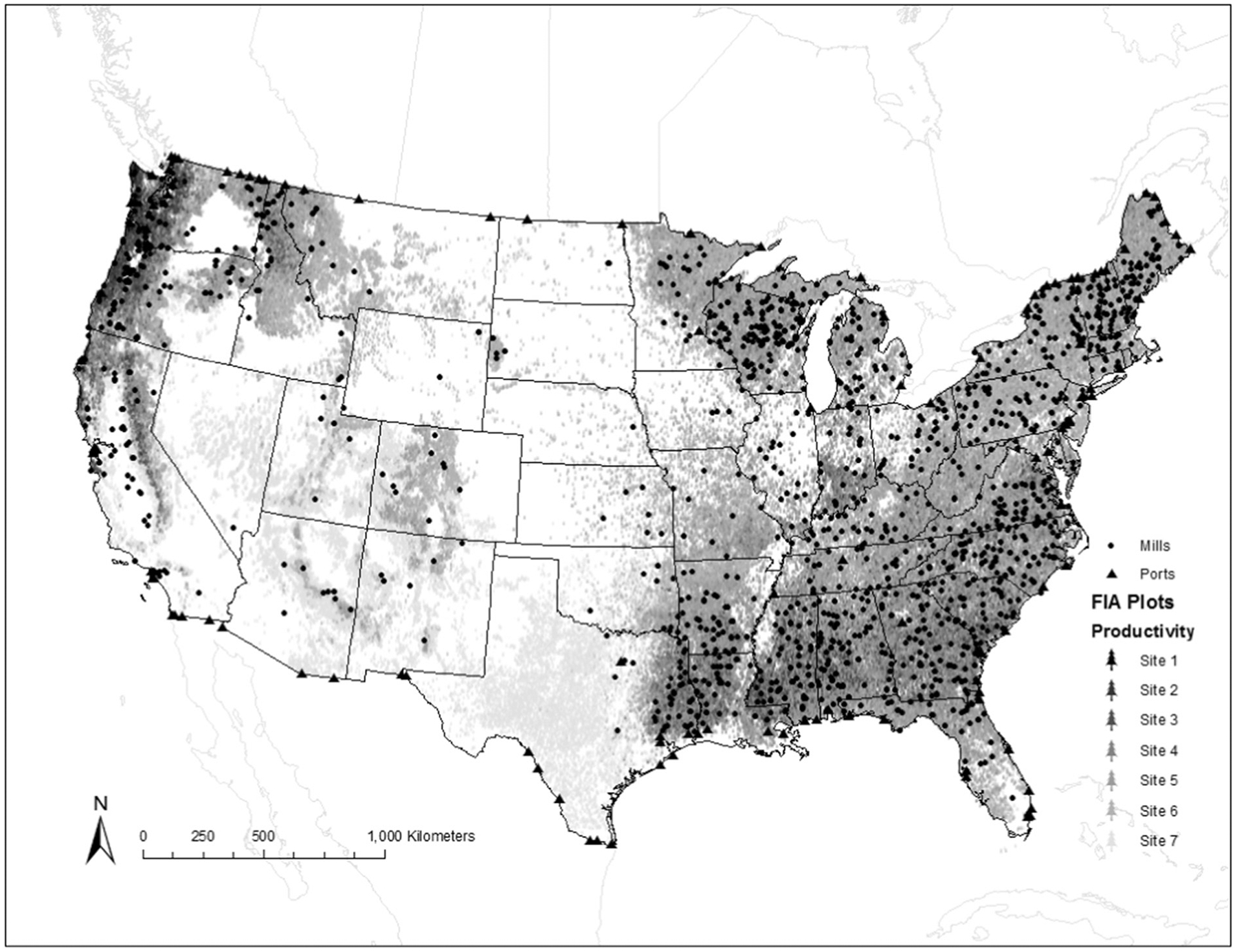

LURA is unique in its ability to represent supply-side logistical considerations throughout the forest product sector. Linking specific locations of forest biomass supply points (FIA plots) and demand locations (mills, ports) allows for improved modeling of the hauling costs associated with transporting tree biomass from forest to mill/port, or from mill to mill/port. Furthermore, because LURA has detailed representation of forest growth rates, model results show the change in forest composition (age class distribution and species mix) and supply-chain logistics (hauling distance and capacity utilization by mill) over time as forests age, are harvested, and regenerate after harvest. All mills contribute to the overall national supply of processed forest products, and total demand is exogenously determined. Fig. 1 shows the spatial allocation of the FIA plots that form the basis for LURA forest biomass supply, the full portfolio of LURA forest products manufacturing facilities that form the basis of LURA demand, and the ports which are the linkage between local markets and global supply and demand. For this study, we calibrate demand using three scenarios from the 2015 Annual Energy Outlook. Key macroeconomic information (such as energy prices and housing starts) lead to different levels of demand project the U.S. forest carbon flux over time.

Fig. 1.

FIA plots, forest product mills, and ports represented in the LURA framework.

3.1.1. Supply side data components

To represent the resource base we used data collected from 130,283 FIA plots for which forest site productivity was recorded. The FIA plots, each consisting of four subplots totaling 0.07 ha in size, are part of the national inventory of forests for the United States (Roesch and Reams 1999). A tessellation of hexagons, each approximately 2400 ha in size, is superimposed across the nation, with one field plot randomly located within each hexagon. In the western states, approximately one tenth of the plots are measured annually, while in the eastern states the re-measurement period is five years (Roesch and Reams 1999). LURA employs information from 150,350 condition classes, or homogenous components, of the full conterminous U.S.3 FIA plot system as seen in Fig. 1. Measurement of just under 5 million trees on that plot system provide the basis for calculation of timber volume as well as biomass and carbon which are aggregated across ownership and site class in Table 1. This 50.6 Gt CO2 of recently measured aboveground live tree carbon forms the starting point for the static and dynamic LURA procedures.

Table 1.

Area, aboveground biomass, and carbon stocks by ownership class and site class.

| Forest | Biomass | Tree carbon | ||||

|---|---|---|---|---|---|---|

| Area | Bole | Top | Stump | Sapling | Above ground | |

| Million hectares | Million dry tonnes | Mt CO2 | ||||

| By owner | ||||||

| BLM | 13 | 297 | 259 | 14 | 10 | 1063 |

| Ofederal | 8 | 707 | 149 | 36 | 40 | 1706 |

| Private | 173 | 9429 | 2458 | 556 | 1057 | 24,732 |

| State | 23 | 1653 | 400 | 91 | 144 | 4193 |

| USFS | 55 | 4882 | 1044 | 240 | 222 | 11,704 |

| By site class | ||||||

| 1 | 1 | 161 | 27 | 8 | 4 | 367 |

| 2 | 7 | 895 | 158 | 46 | 37 | 2081 |

| 3 | 20 | 2285 | 419 | 116 | 116 | 5380 |

| 4 | 44 | 3553 | 729 | 194 | 296 | 8745 |

| 5 | 77 | 5615 | 1225 | 317 | 536 | 14,094 |

| 6 | 65 | 3979 | 892 | 226 | 415 | 10,099 |

| 7 | 57 | 479 | 859 | 29 | 68 | 2631 |

| Total | 271 | 16,968 | 4311 | 937 | 1473 | 43,398 |

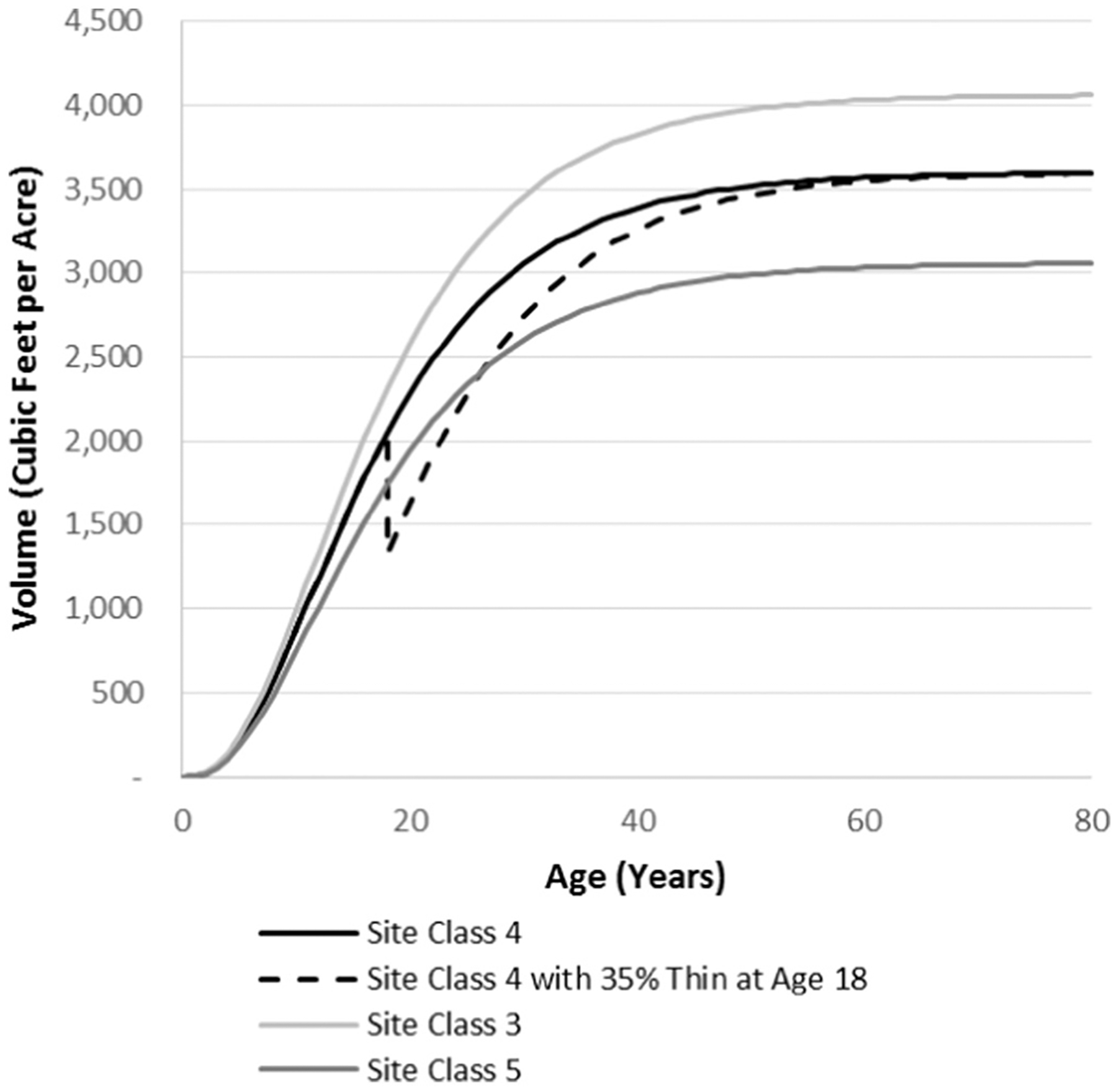

To determine biomass growth rates for FIA plots, we first aggregate plots across 36 forested ecoprovinces e (Cleland et al. 2007), seven site class codes s (following the FIA classification), and distinguish between 14 forest types u. Unlike political boundaries, ecoprovinces were chosen to aggregate plot-level data as each province represents an area with relatively consistent climate, geography, soils and potential natural communities. Yield curves were estimated using measured volume and ages from all FIA condition classes f within each of the 676 unique ecoprovince, site class, and forest type combinations. A yield curve is fit using a two parameter von Bertalanffy growth equation such that volume is a nonlinear function of stand age (Von Bertalanffy 1938). At each age volume is a cubic function of the stand of age n, a βeus slope controlling growth rate, and an asymptote parameter αeus limiting total volume, or maximum stocking potential. This approach allows for explicit FIA condition class level biomass growth rates representing the heterogeneity in forest yields within an ecoprovince and across forest types and site classes. Fig. 2 shows an example of growth curves across a range of three site classes for the planted pine forest type in the Outer Coastal Plain Mixed Forest Ecoprovince. Fig. 2 also demonstrates an example of the treatment of thinning of site class IV for the planted pine forest type in the Outer Coastal Plain Mixed Forest Ecoprovince as well. Thinning is simulated as a removal of 35% of standing volume, recalculation of age based on the growth equation at the reduced density, and then continuation of growth from that recalculated age.

Fig. 2.

Example yield curve with and without thinning for the planted pine forest type across a range of site classes in the Outer Coastal Plain Mixed Forest Ecoprovince.

3.1.2. Demand side data components

When used to meet an exogenous forest products demand level (domestic consumption, imports, and exports), LURA determines the optimal combination and allocation of harvested logs and manufacturing byproducts. Table 2 provides a basic listing of LURA commodities, units of measure, mills, initial demand value, and initial trade values. Initial demand is based on apparent consumption (production plus exports less imports) as reported by FAO (2014). For each mill, LURA input data indicates what products are produced, total capacity by product, and biomass input per unit of output. Other technical processing inputs include energy requirements and associated costs. LURA accounts for the location of each mill (Fig. 1), and calculates the distance from each individual plot to the mill as a proxy for total hauling distance. In total, LURA represents 2365 forest product mills and Electricity Generating Units (EGU). Softwood lumber comprises the largest number of mills with 561. Data for these mills were derived from an updated version of Spelter et al. (2009) with locations placed in the city of reference. The second largest grouping of mills is pulp and paper whose 418 location and capacities are based on a combination of the Lockwood Post (RISI 2012) and Smith et al. (2003). The remaining data is sourced from references from a variety of sources (Biomass Magazine 2015; Spelter 1996; Spelter and Toth 2009). Non-traditional forest products such as electricity generation are also included based on information from the U.S. Energy Information Agency (EIA). In order to determine the amount of biomass fuel currently consumed for electricity generation, 2012 EIA-923 data for electric generation units were matched to 2012 EIA 860 data to obtain the fuel consumption and geographic coordinates of each plant. Generator fuel type was filtered to include only biomass feedstocks (agricultural crop byproducts, wood and wood waste solids, other biomass solids) for the 152 direct-fired boilers. Facility type includes traditional electric utilities, independent power producers, and industrial cogeneration and noncogeneration facilities (EIA sector number 1,2,3,6,7), but not commercial facilities. The 530 Co-firing boilers are coal fired with the potential co-firing rate based on Abt et al. (2010).4 We make the assumption that these boilers utilize wood pellets as the heat source.

Table 2.

LURA forest product classification and initial 2014 values.

| Forest Product | Facilities | Capacity | Domestic Demand | Exports | Imports |

|---|---|---|---|---|---|

| 1000 cubic meters | |||||

| Softwood roundwood | 14,646 | 650 | |||

| Hardwood roundwood | 1830 | 371 | |||

| Softwood lumber | 561 | 64,778 | 68,881 | 4313 | 19,212 |

| Hardwood lumber | 290 | 21,895 | 15,632 | 3451 | 837 |

| Softwood plywood | 57 | 9005 | 9269 | 655 | 2420 |

| Hardwood plywood | 29 | 3634 | 3028 | ||

| Oriented strandboard | 39 | 20,017 | 20,563 | 564 | 4446 |

| Hardboard | 19 | 709 | 373 | 218 | |

| Insul_board | 49 | 6188 | 4873 | 284 | |

| MDF | 15 | 3596 | 4303 | 535 | 1841 |

| 1000 metric tonnes | |||||

| Chemical pulp | 116 | 56,357 | 6758 | 5064 | |

| Mechanical pulp | 20 | 1912 | 29 | 39 | |

| Newsprint | 11 | 2730 | 3591 | 800 | 2116 |

| Printing & writing_paper | 82 | 17,861 | 17,484 | 2322 | 4922 |

| Paperboard | 189 | 59,197 | 43,238 | 8414 | 2321 |

| Tissue | 67 | 8260 | 7029 | 152 | 298 |

| Wood pellets | 139 | 6124 | 2243 | 2909 | 152 |

| BioPower | 152 | 1235 | 1029 | ||

| Pellets for coal cofire | 530 | 124 | 103 | ||

| Softwood mill chips | 4780 | 60 | |||

| Hardwood mill chips | 843 | 26 | |||

| Recycled paper | 18,883 | 811 | |||

Domestic demand is shifted over time based on elasticities for key macroeconomic drivers from Ince et al. (2011) for solid wood products and Latta et al. (2016) for paper products. These elasticities allow us to develop projections of exogenous forest product demand that calibrate directly to AEO scenarios (or any modeled projection that includes estimates of GDP and housing starts). For example, LURA assumes income elasticities of 0.39 and 0.22 for softwood and hardwood lumber, respectively, and a housing elasticity of 0.49 for softwood lumber (hardwood lumber is assumed to be perfectly inelastic). Changes in paper demand take into account the increasing role of online media in future demand for newsprint and printing and writing paper. One advantage of this approach is that it is easily updated and replicable across other models (meaning LURA can be calibrated to any set of macroeconomic projections). Since AEO projections are updated annually, the model can be calibrated to new forest product demand projections, resulting in updated LULUCF projections annually.

For each mill, the model assumes a product-specific capacity and input-output processing coefficients that correspond to the raw biomass or intermediate product requirement per unit of processed product output. The sources of this data are as varied as the location and capacity data described above. The largest contributors to the data were reports by the Consortium for Research on Renewable Industrial Materials (CORRIM). CORRIM data for regional softwood lumber, hardwood lumber, plywood, oriented strandboard, particleboard, and medium density fiberboard are available from the U.S. Life Cycle Inventory Database (NREL 2012). Other products data were assembled from either the U.S. Forest Products Module (USFPM) (Ince et al. 2011) or the Forest and Agriculture Sector Optimization Model (FASOM) (Beach et al. 2010). LURA allocates raw and processed materials between plots, mills and ports to meet exogenous domestic and export demand targets.

3.1.3. Foreign trade data components

Trade limits are calibrated to FAO statistics on U.S. trade in wood products. Individual trading partners are not considered in the model currently. Instead, the model assumes one “rest of world” trading partner and aggregates FAO import and export statistics for each forest product (FAO 2014). The total exogenous import/export levels are then apportioned to the individual ports shown in Fig. 1 based on the U.S. International Trade Commission5 port specific trade data. The proportions of forest product imports/exports for each port are based on the 2009–2013 time period average values and represent 98% of the total value of forest products trade over that period. The resulting proportions for 126 export and 120 import sites are represented explicitly in the model as a capacity kpc for each port p and commodity c. All imports originating at those sites and paying transport to U.S. forest products facilities and vice versa for exports. An exception is final forest products for direct consumption for which here is no demand location. This is also true for transport of domestic final products to demand.

3.2. Methods

This analysis utilizes the LURA modeling system to meet an exogenous forest products demand level through optimal allocation sequentially over time of primary and secondary forest derived commodities. Within a single time period, n, the static phase determination of the optimal resource allocation is accomplished through minimization of the total cost variable C (defined in Eq. 12) while meeting a variety of constraints within a linear programming formulation. Between time periods, the dynamic phase, forest inventories are updating to account for static phase harvest levels and inter-period growth, demand and trade levels are updated accounting for changes in macroeconomic parameters, and forest products processing and port capacities are adjusted to account for depreciation and changes in demand.

3.2.1. Static phase model solution

The static phase LURA solution minimizes the cost, C, of supplying forest products to meet an exogenous level of demand subject to a series of constraints.

3.2.1.1. Commodity balance constraints.

Eq. 1 represents the balance of log products harvested by clearfelling H and partial harvest P delivered T to mills or export. The parameter yfc denotes the proportion of total harvests from condition class f used to produce commodity c and a partial harvest removal of 35% is assumed. The total allocation of harvested logs from condition class f (Hf * yfc for clearcuts and Pf * 0.35 * yfc for thinnings) for the production of commodity c is equal to the amount transported to all mills (∑m (Tfcm), where m is the set of all mills), ports (∑p(Tfcp)) where p is the set of all ports), and wasted wood product (Wfc).6 This condition holds for all condition classes and commodities.

| (1) |

Eqs. 2 and 3 represent the mill-level manufacturing M balance for all primary and secondary commodities supplied as inputs and produced as outputs respectively. In this formulation, x represents the set of possible manufacturing production processes including input mixes for mill m, and c′ represents the commodity c that is used as an intermediate input in production process x. The manufacturing consumption balance ensures that total use of inputs to produce final commodity c at mill m is equal to all incoming material from forest plots (∑f Tfcm), other mills (∑m′ Tm′cm), ports (∑p Tpcm) and recycled material (Rm).

| (2) |

Likewise, the manufacturing production balance ensures that total supply of outputs of primary and secondary commodity c at mill m is equal to all outgoing material to other mills (∑m′ Tmcm′), ports (∑p Tmcp), final demand (Tmcd) and unused material (Wmc).

| (3) |

Finally, in static mode, LURA includes a constraint forcing the transportation T of each commodity c across all supplying locations l, including FIA plots, mills, and ports, to final demand to balance with aggregate U.S. consumption qc.

| (4) |

3.2.1.2. Other constraints.

In addition to balancing commodity flows there are a set of constraints to control how forest commodities enter the market including domestic harvest and recycled paper. We begin with the harvest variable Hf representing total area harvested by FIA forest condition class f, total area harvested is restricted to be less than the land endowment in the forestry system. Land endowments for each condition class (af) are determined initially by the intensity of the FIA forest inventory sample with each county of the conterminous United States and then adjusted to reflect prior time periods harvest decisions:

| (5) |

Harvest of publicly owned forest condition classes Hf′ and Pf′ are constrained by Eqs. 6 and 7 which limit harvest levels from clearcut (Hf′ * yf′c) and thinnings of 35% of the standing volume (Pf′ * 0.35 * yf′c) at the county and state levels to fall within reported levels from the last 20 years. In Eq. 6, f′ represents the public forest condition classes within county b which must be less than or equal to the highest reported county-level harvest over the last four national Resource Planning Assessment (RPA) Timber Products Output (TPO) reporting periods given as gbu.

| (6) |

While public harvests are allowed to fluctuate at the county level, they are constrained for publicly owned forest condition classes f*within each state j to equal the average TPO state-level reported harvests gsavgover that same time period.

| (7) |

The sum of the variable representing mill-level recycled paper Rm consumed across all mills (∑m Rm) must be less than or equal to the supply of recycled paper r which is determined initially from historic consumption then updated from the prior time periods solution.

| (8) |

For each mill m and commodity c combination, the sum over the available production processes x of the mill production variable Mmx is constrained by the existing capacity level km. Initial capacity limits kmc are based on a variety of federal, state, and industrial trade group reports. In subsequent time periods that capacity is adjusted by prior period profitability and changes in macroeconomic variables as described in the dynamic phase section.

| (9) |

We also assume limits on trade for exports and imports of forest products (Eqs. 10 and 11, respectively). Exported forest products c are greater than or equal to the amount of each forest product delivered directly from plot to export port , and from mill to export port . Total imports at each import port are greater than or equal to the sum of all products delivered from import port pi to mill m for secondary processing, plus recycled forest product remaining from previous periods. Similar to mill capacity, individual port capacity kpc is allowed to grow over time and is based on the relative transportation cost efficiency of the specific port.

| (10) |

| (11) |

3.2.1.3. Total costs.

The total cost variable C include harvest costs h, transportation costs tlcl′ of hauling forest products between forest plot, mill and port locations l and l′ for additional processing, consumption, and exporting, and a waste cost w, for unused commodity disposal. The primary cost component included in the objective function is the costs of transporting raw biomass and processed forest products between plots, mills, and ports. Transportation costs tlcl′ for commodity c are based on the Euclidian distance between source location l and destination location l′ with diesel fuel costs determined using a fuel efficiency of 5.5 miles per gallon and prices from AEO. Time variable costs include a 15 min load time and are based on a speed of 15 mph for the first 5 miles, 45 mph for the next 10 miles and 55 mph for the remaining distance and are assessed at a $50/h labor rate. These one-way costs are then doubled to account for round trip hauling. Hauling capacities are 38 m3 for solid wood products such as logs and lumber and 12.5 bone dry tons per load for wood chips and pulp products. Total costs are depicted by Eq. 12.

| (12) |

3.2.2. Dynamic phase model solution

3.2.2.1. Forest inventory updates.

The forest dynamic phase involves first updating the acreage to reflect harvesting and fire disturbance in Eqs. 13–15 and then the inventory to reflect forest growth in Eq. 16. The fire disturbance is based in two primary assumptions. The fire interval assumption is that the acreage burned in each county ϕf will be the same as the 2004–2014 annual average reported by the National Interagency Coordination Center. The burn intensity assumption is that 50% of the burned acreage results in the loss of all live trees and the fire damage on the remaining acreage is reflected in the yield tables through lower live tree stocks in older age classes. For all FIA condition classes f, the next period’s acreage is determined by adjusting the area to reflect regeneration Hf and partial harvesting Pf and then accounting for the 50% of remaining area that would be burned and entirely combusted.

| (13) |

| (14) |

| (15) |

Next the plot inventory needs to be updated to reflect its annual growth rate. Yields are generated for both the unharvested (Eq. 13), harvested (Eq. 14) and thinned (Eq. 15) components of the plot (see Fig. 2 for example). Eq. 16 thus uses the von Bertalanffy slope βeus and asymptope αeus ecosystem, forest type, and site class specific growth parameters to increase the FIA plot f stocking level yfc using from ages n to n + 1.

| (16) |

3.2.2.2. Forest products demand update.

For each commodity c, aggregate U.S. consumption in time period n is updated to period n + 1 by multiplying the current consumption level qcn by one plus the product of the elasticity of demand σ for commodity c with respect to macroeconomic indicator θ, σcθ, by the change in that indicator for all indicators relevant to the commodity demand as given by Eq. 17.

| (17) |

3.2.2.3. Forest bioenergy demand update.

For EGUs that fire coal and syncoal fuel types, the boiler heat input (in MMBTu) of each boiler at a facility was multiplied by efficiency coefficients following Abt et al. (2010) in Table 1. Boiler capacity was transformed to tons of biomass, and summed over all boilers at a facility for total capacity of biomass input. Then, we use national projections of biopower demand (in Mwh) to be consistent with the AEO scenarios. AEO projections of biomass electricity were introduced for each of the representative scenarios to account for projected forest bioenergy demand. There are no regional restrictions governing biomass utilization for electricity generation. Instead, the model determines the amount of biomass consumption for each electricity generation facility (and the feedstock mix) to minimize the costs of meeting national energy targets. Biomass consumption cannot surpass total co-firing capacity for any given facility.

3.2.2.4. Capacity update.

The capacity adjustment for both mills and ports is based on a two-step adjustment process in which both forest product demand growth and the relative competitiveness of a specific mill in terms of supply costs will drive the extent to which capacity grows. That is, capacity growth at any given mill will be a function of capital depreciation, aggregate demand growth, forest inventories in proximity to the mill, and marginal supply costs.

In the first step the weighted average delivered input supply costs zl are calculated at each location l (mill m or port p) as given by Eq. 18, and the weighted average delivered input supply costs νc are calculated at for each commodity c as given by Eq. 19 based on the locations transportation cost tl′cl weighted by the amount of commodity c transported to location l, Tl′cl.

| (18) |

| (19) |

In the second step (Eqs. 20 and 21) all mill or port locations l capacity kl.c to produce commodity c is depreciated based on a common rate δ of 5% and then expanded to accommodate any demand change (positive or negative), represented by a percentage change in qcn. Capacity expansion is only allowed for mills or port that are cost competitive. That is average supply costs, zl, must be lower than the average input supply costs, νc, for the commodity c produced at the location l for location l to see expansion in capacity commensurate with demand growth for commodity c between periods n and n + 1.

| (20) |

| (21) |

Thus, the conditionals zl ≤ Vc and zl > Vc will determine whether a mill will see net growth or depreciation in capacity over time. Mills that are surrounded by growing or densely populated forest resources and are located relatively close to other mills, EGUs, and ports will experience lower marginal supply costs than mills that are relatively isolated and require longer hauling distances will face steeper marginal supply costs. The approach outlined in Eqs. 18–21 recognizes the relative cost efficiency of certain mills and thus capital expansion is indirectly driven by demand growth and input supply costs.

3.2.2.5. Recycled paper supply update.

The next period’s available recycled paper rn + 1 is a function of the sum of the prior periods total paper consumption πcn multiplied by a recovery rate μc for commodity c. Currently recycling opportunities exist only for paper commodities.

| (22) |

4. Scenario design

We develop three scenarios reflecting differences in macroeconomic conditions projected under the AEO 2015. Each AEO scenario includes a number of assumptions regarding growth rates in key macroeconomic variables that influence projected energy and industrial sector activity in the National Energy Modeling System (NEMS) used to produce the AEO. The set of scenarios here represents a small subset of the full set of alternative scenarios developed for the AEO (which typically provides results from up to 30 alternative future cases). The three scenarios: AEO Reference Case, AEO Low Economic Growth, and AEO High Economic Growth were chosen specifically to evaluate the impact of alternative economic and bioenergy demand growth assumptions on LULUCF emissions.

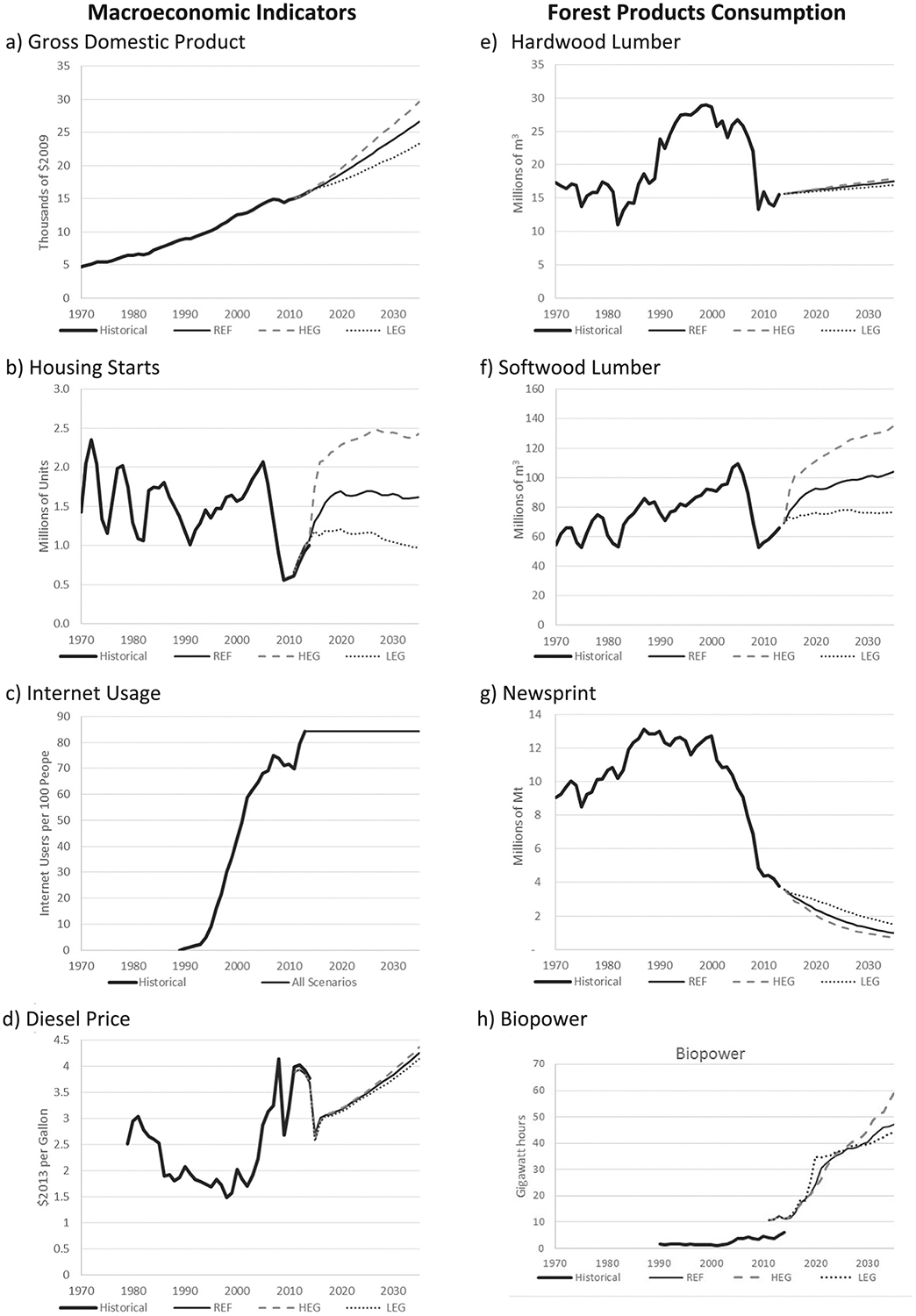

A number of simulation parameters and results published under the AEO are used to drive future LURA forest products demand conditions. Fig. 3 panels a-d present historical and projected levels for a subset of these macroeconomic drivers. This includes GDP growth, population growth, housing starts, demand for forest bioenergy, and various fossil fuel prices (particularly diesel, which is the primary energy cost for transporting biomass between plots and demand points). We use income and housing start elasticities to calibrate demand growth over time to AEO scenario assumptions. GDP growth (Fig. 3a) ranges1.3%–4.1% annually from the Low to High economic growth scenarios. Housing starts (Fig. 3b) vary greatly across the AEO scenarios. In the AEO Reference Case and Low Economic Growth scenarios, housing starts decline by 2040, but increase for the High Economic Growth case. In 2040, housing starts are approximately 56% higher with high economic growth than under the AEO Reference Case. Internet usage (Fig. 3c) as measured by internet users7 per 100 persons from the World Bank and the International Telecommunication Union (World Bank 2014) is not part of the AEO and therefore we hold it constant at recent levels for all scenarios. Finally, diesel prices (Fig. 3d) in all three scenarios show a strong rising trend with little variation between them.

Fig. 3.

Macroeconomic indicators.

Fig. 3 panels e-h provide a few examples of projected forest product demand levels associated with the scenario-specific macroeconomic drivers. Hardwood lumber (Fig. 3e) is assumed to be less income inelastic and does not respond to housing starts in our model, thus projected demand does not vary much between scenarios. While Softwood lumber demand (Fig. 3f) is extremely sensitive to economic projections and housing starts, deviating approximately 30% from the Reference Case scenario in the low and high economic growth scenarios by 2035. Newsprint (Fig. 3g) and printing and writing papers are different in that they include an internet usage elasticity in addition to GDP which help explain the structural shift in consumption beginning in the 1990’s. The effect of this shift is so strong that consumption in the High Economic Growth Case is actually below the Reference Case as higher income leads people to shift away from printed media at a faster rate reducing demand. Additionally, some key forest products do not vary at all with income and are calibrated either directly to the AEO projections (such as biopower (Fig. 3h), or do not vary across AEO scenarios, such as wood pellets. The nascent pellet market has insufficient data to allow income elasticity estimation and thus pellet demand is based on a static domestic demand level and an additional 5 billion tonnes of new Southeastern U.S. capacity coming online by 2017 with all additional production absorbed by an expansion in exports.

5. Results

The model was solved for 21 years on annual time steps covering the 2014–2035 time period. Annual model results are saved for both individual FIA plots representing forest supply and sequestration as well as individual forest products manufacturing facilities along with the ports covering intermediate and final forest product production consumption and trade. This results section focuses on the AEO reference scenario. The focus will first be on types of aggregate CO2 emissions and sequestration, and then on mapping the average CO2 accounts for the FIA plot grid over the time period highlighting regional differences. Next we investigate net emissions by ownership. Finally, we bring in results from the other AEO scenarios illustrating how differences in macroeconomic parameters can change potential future net sectoral emissions. All results presented here take an atmospheric approach to GHG accounting with additions to atmospheric carbon, or terrestrial pool emissions, shown as positive values and reductions in atmospheric GHG pools as they are sequestered in terrestrial accounts such as trees shown as negative values.

5.1. AEO reference case projections by emissions type

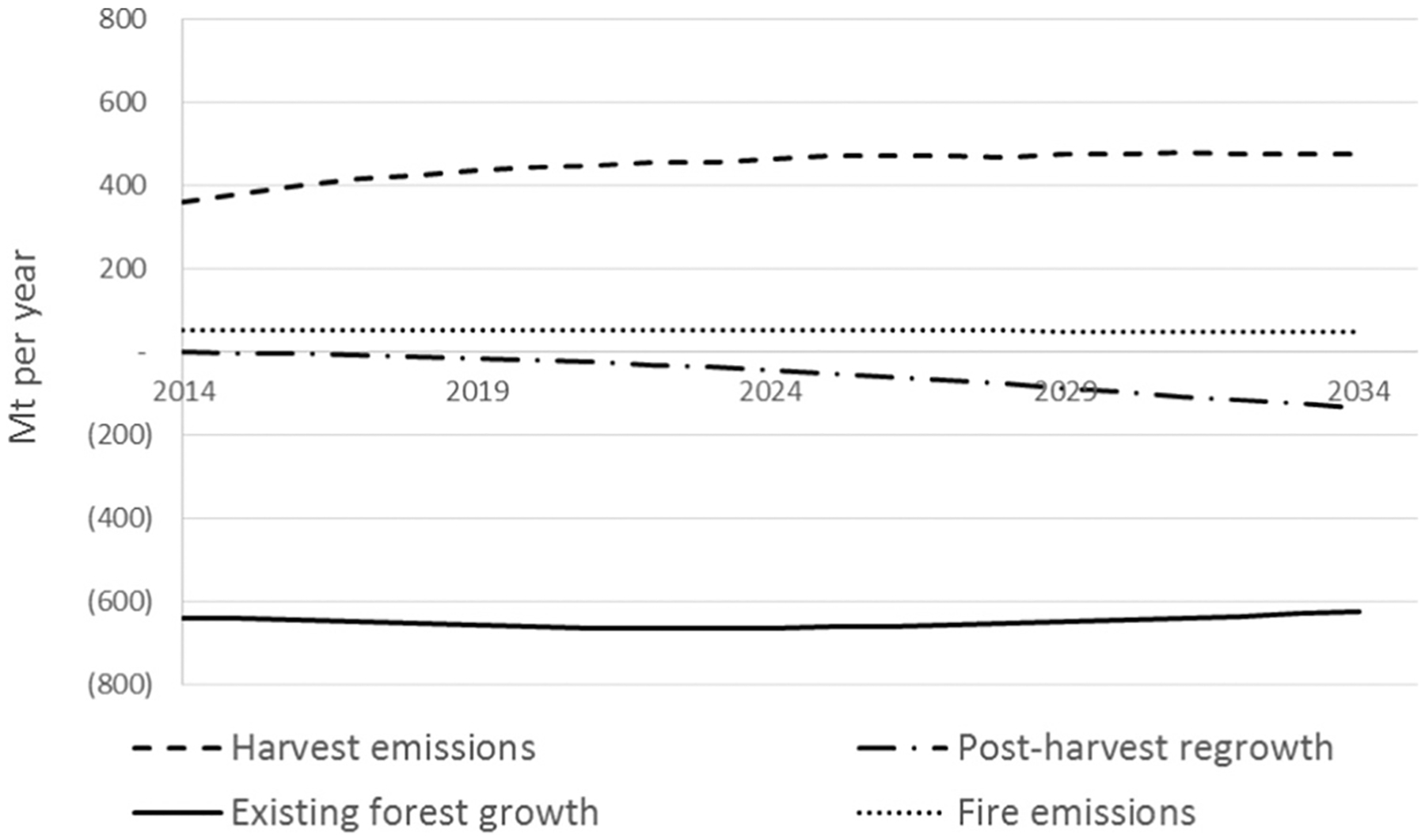

The projections for net annual CO2 emissions by emissions source are presented in Fig. 4. Evaluation of Fig. 4 highlights basic trends in future changes in above ground live tree carbon. The largest component of net CO2 emissions is the sequestration associated with growth of the existing trees (shown as negative values). This sequestration value begins at 640 Mt CO2 per year in 2014 and slowly declines to 624 Mt CO2 per year by 2035. This slow decline in growth of existing forest is attributable largely to harvesting of trees for use in forest products and to a lesser extent loss of forest area to fire. The largest emission (positive value) shown in Fig. 4 is the immediate emissions associated with the harvesting of trees as they leave the forest GHG pool, which begins in 2014 at 361 Mt CO2 per year and increases to 476 Mt CO2 per year by 2035. The emissions associated with fire are much lower, decreasing slightly from 50 to 48 Mt CO2 per year over the 21-year time horizon. Forest management in LURA is either accomplished through a partial harvest releasing growing space to remaining trees or a total harvest. As forest area is harvested or burned it is regenerated either by planting or natural regeneration and the growth of that regenerated forest has an increasing role in the aggregate accounting of aboveground live tree carbon. Regenerated forest tree carbon values begins at 2 Mt CO2 per year in 2014 and becomes an increasing larger component of overall forest GHG sequestration as new acres are planted each year and recent plantations become fully established ending at 135 Mt CO2 per year, or 18% of the total forest aboveground live tree carbon growth.

Fig. 4.

Projected U.S. above ground CO2 changes by emissions source.

5.2. AEO reference case projections by region

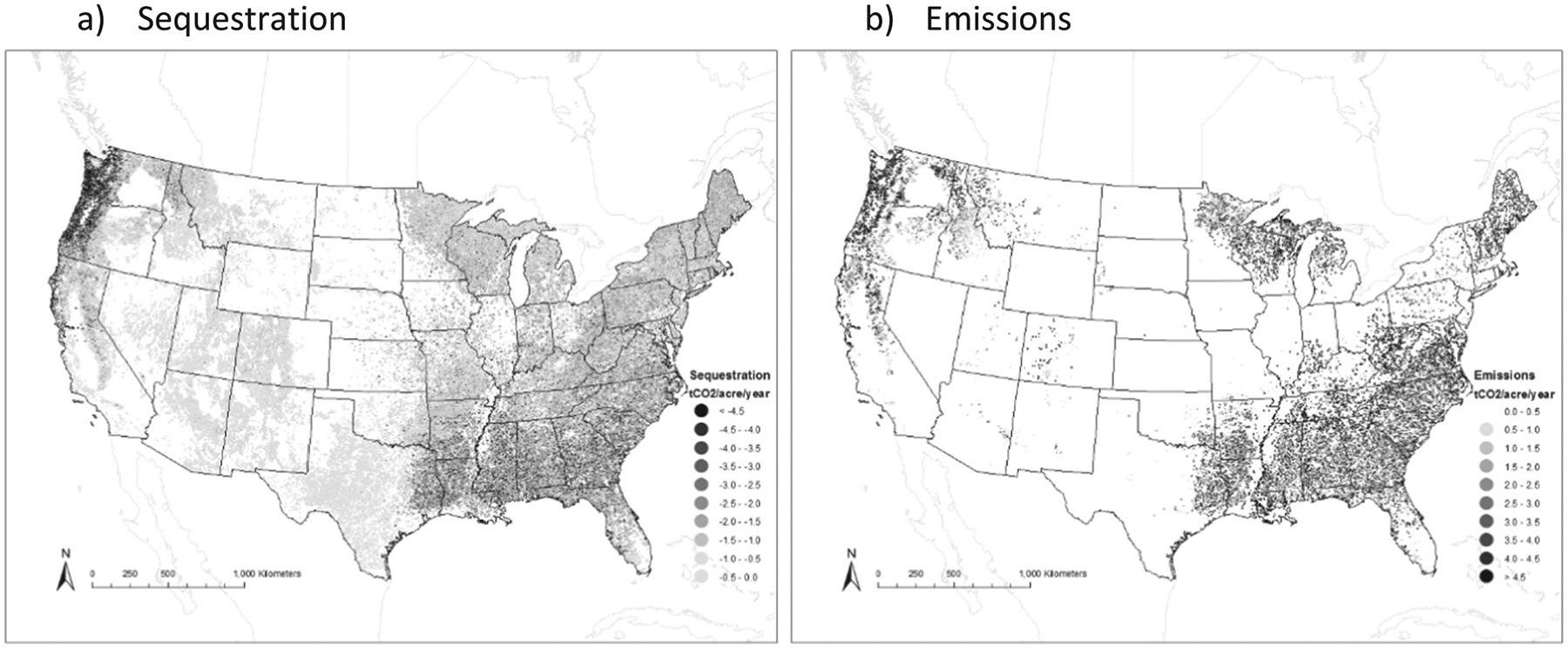

Because LURA maintains the supply representation at the individual FIA plot level without aggregating to regions or other strata it is possible to display the changes in aboveground live tree CO2 at the same scale at with the original FIA data is collected. While carrying this level of disaggregation throughout the modeling time horizon provides a wealth of potential avenues to display CO2 fluxes, it does present problems in being able to convey such changes in a single figure. One such way to consolidate results and still convey the regional differences is to map the average annual changes to aboveground live tree CO2 over a 20-year modeling time period from 2015 to 2035. Fig. 5(a) shows that 20-year average annual carbon sequestration for the conterminous United States. Darker shading represents higher levels of sequestration found mostly in the U.S. Pacific Northwest forests west of the Cascade Mountains as well as the productive private forests of the U.S. Southeast and Southcentral states. The lighter shades indicates lower rates of sequestration are found in the lower productivity forests of the Rocky Mountains and hardwood dominated forests of the Northern states. Fig. 5(b) shows net emissions over the 20-year time period from forest harvesting and fire, and are centered around the burgeoning forest industry of the U.S. South as well as the lumber-dominated industry of the Pacific Northwest Coast and pulp-dominated industry of the North. Just as the darker sequestration values of Fig. 5(a) bear a close resemblance to the forest productivity map shown in Fig. 1, the darker emission values of Fig. 5(b) closely follow the mill map found in that same figure.

Fig. 5.

Spatial representation of average annual projected sequestration and emissions from net growth and forest harvests on the landscape over the 2015–2035 time period.

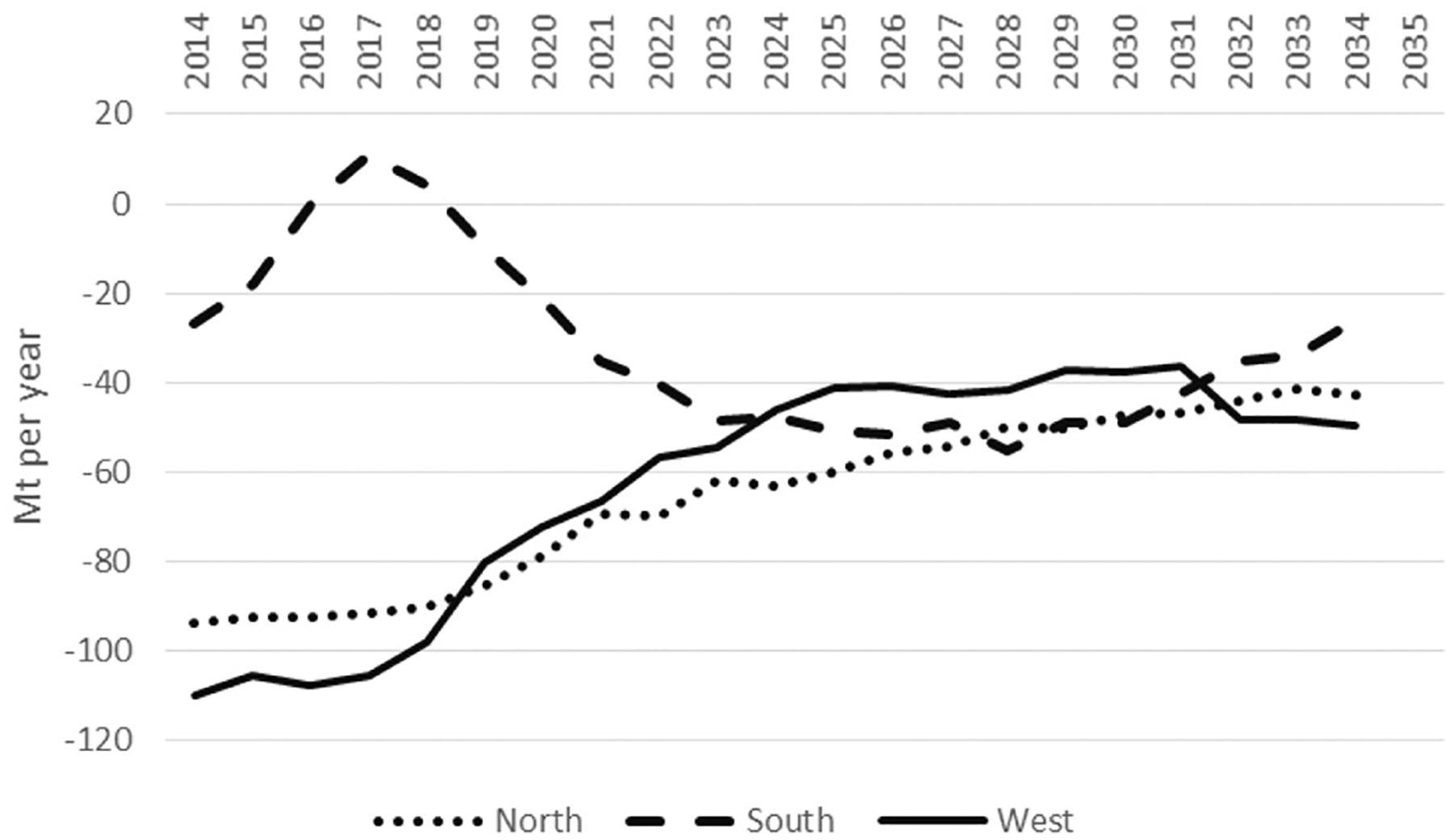

While Fig. 5 reinforces our intuitive expectations that sequestration should be highly correlated with both forest productivity and emissions with the locations of forest product manufacturing facilities, it does little to help us evaluate the aggregate contribution of those accounts across the U.S. Fig. 6 presents the aggregated tree carbon fluxes by major U.S. regions, highlighting not only the differences between those regions but also the different ways those regional fluxes are changing over time. The North and West regions both show a consistent decline, or slowing in gross tree carbon sequestration rates over the modeling time horizon. Base period (2014) tree carbon sequestration rates in the West begin at −164 Mt CO2 per year with a net sequestration rate of −110 Mt CO2 per year when harvest emissions are included. Tree carbon sequestration rates decline by an average of 4.5 Mt CO2 per year each year through 2030. This rate of change switches to an increase in net sequestration of 2.5 Mt CO2 per year for the final five years of the projection horizon. The North region has an initial tree carbon sequestration rate of −153 Mt CO2 per year in 2014 and net sequestration of −93 MtCO2. This net sink decreases by approximately 2.5 MtCO2 per year through 2035, with a more consistent rate of change than the West.

Fig. 6.

Regional net sequestration CO2 flux projections (2014–2034).

The South has a higher initial annual sequestration rate than the West or North regions, with tree carbon sequestration totaling −273 MT CO2 per year, but a smaller initial net flux of −27 MtCO2. Similar to other regions, this flux declines initially (2015–2017) and the net regional sequestration flux converts from emissions sink to source by 2017. This large initial flux change is driven by several factors. First, demand grows rapidly for rapidly certain product categories such as softwood lumber (driven by housing starts) and biopower feedstock in the first few years of the simulation horizon, even in the Reference case scenario. To meet this demand surge, clear cut harvests, thinnings, and residual biomass utilization increase in the U.S. South in the beginning of the simulation horizon relative to the initial period. This increases the net emissions flux for the next three periods (2015–2017), causing the U.S. South to shift from annual emissions sink to source. The primary supply-side factor causing the shift to lower sequestration initially is that underperforming plots (e.g, older stands) are being harvested to meet demand growth and then regenerated, which leads to this initial drawdown in stocks as underperforming plots tend to hold more carbon and release more emissions per-unit area when they are harvested.

Following this rapid initial demand surge, demand growth tapers off for the remainder of the simulation horizon. However, beginning in 2018 the regrowth of regenerated forests following harvests slows the increases in emissions. By 2019, the region shifts back to an emissions sink, and net sequestration increases consistently for the next nine simulation years as regenerated plots rapidly accumulate additional carbon. The second phase of rising sequestration despite increasing demand for wood products is driven by higher growth rates associated with these regenerated plots/stands. The final phase in which sequestration rates begin to decline in the U.S. South once again (from 2028 on) is driven by forest extent and favorable processing capacity distribution (both over space and products). The South region absorbs most of the increased in future demand and hence capacity and biomass removals expand long term, which begins to decrease sequestration levels. By the end of the simulation horizon, the net regional sequestration level ends up close to the initial net flux of −27 MtCO2 per year.

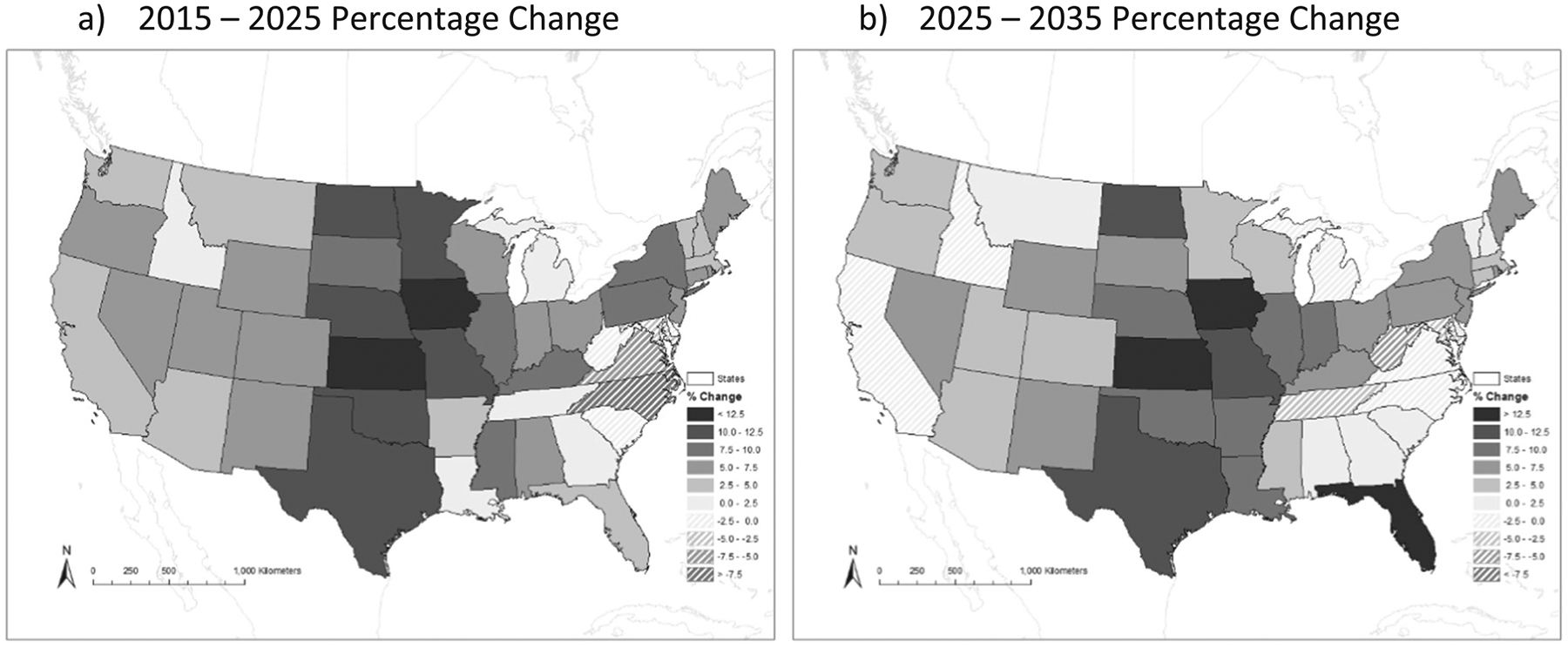

5.3. AEO reference case state-level above ground carbon stock change projections

Fig. 7(a) and (b) are maps that present the percent change in above ground live tree carbon stocks by state for the AEO Reference Case Scenario. These changes align fairly well with the aggregated regional flux projections discussed above, but also illustrate the intra-region heterogeneity in projected changes, both over space (by state) and over time (2015–2025 and 2025–2035 periods, respectively). Spatial heterogeneity in forest carbon flux impacts is driven by locations of the primary resource base, productivity, and locations of current forest product processing mills. North Carolina, Virginia, South Carolina, and Tennessee all see significant reductions in live-tree carbon by the end of the simulation horizon due to a high concentration of forest product mills and bioenergy demand points. Relatively high levels of removals throughout the horizon lead to a reduction in standing carbon. This regional decrease differs from the continued net sequestration in other parts of the U.S. that see increased live tree carbon over time (in particular out west and for most of the Midwest).

Fig. 7.

Spatial representation of projected sequestration and emissions from net growth and forest harvests on the landscape.

Temporal differences in projected stock changes are also important to note. For some Southern states (including NC and VA), the net stock change impact is larger for the first 10 years of the projections horizon than for the last 10 years. For example, the NC live tree CO2 stock declines by more than 8% by 2025, but stocks recover as stands regenerate and the projected net change is less than 2% by 2035. This information indicates that early mitigation action in states with significant stock impacts by 2025 would greatly benefit from forest mitigation policy action (e.g., prices incentives to promote afforestation or improved forest management).

5.4. AEO reference case projections by Forest owner

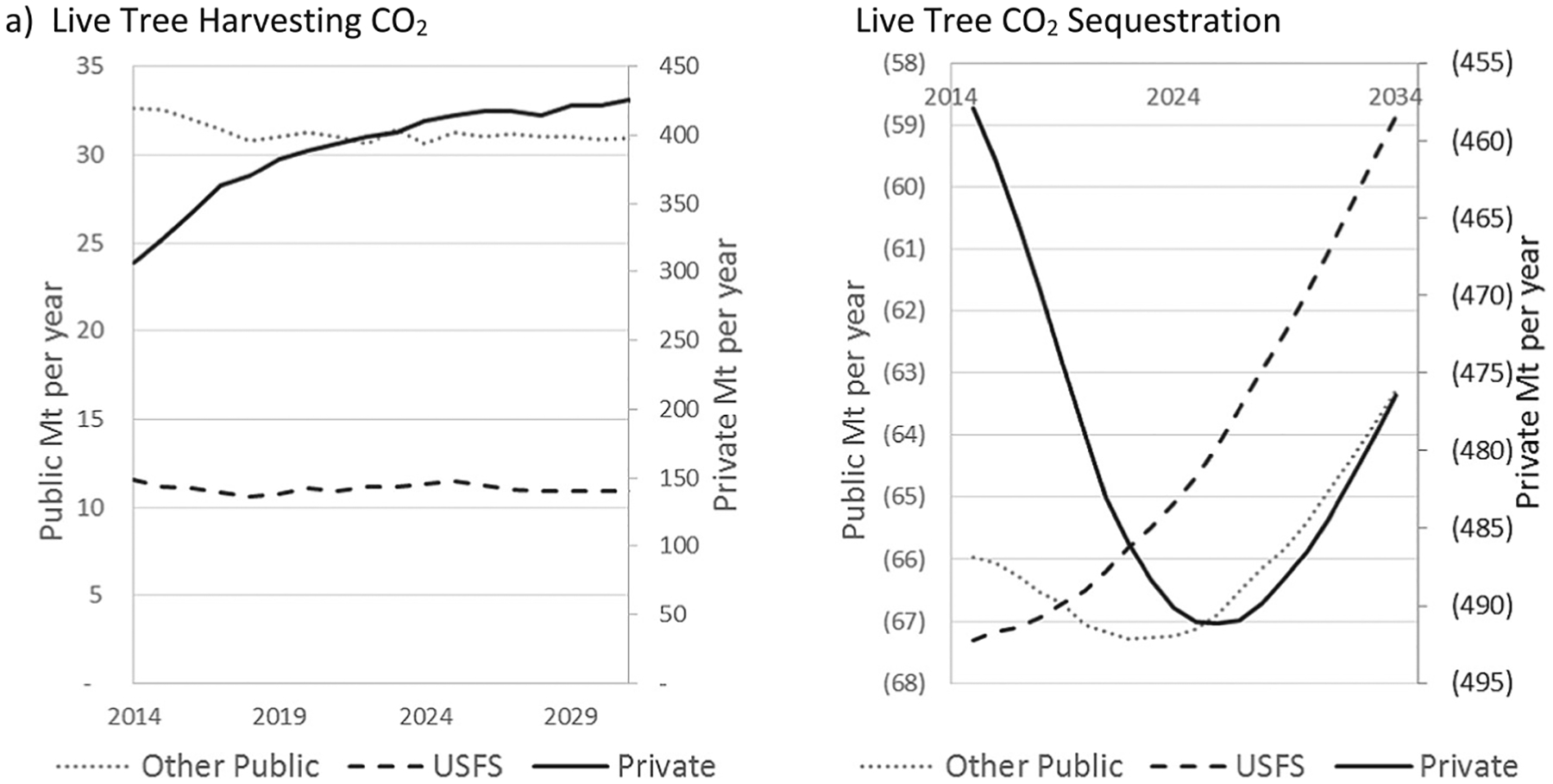

Influences from the regional differences and emissions sources highlighted in the sections above can be seen in the results disaggregated by forest owner group. Fig. 8 shows the harvest-related emissions and sequestration for three major forest owner groups; Private, National Forests (USFS), and Other public owners including federal, state, and local publically owned forests. Harvesting emissions are largely concentrated on private lands where the values begin at 400 Mt CO2 per year, which is over 10 times the 39 Mt CO2 emitted from USFS lands and 33 times the other public emissions of 12 MT CO2 per year. Assumptions regarding the non-price responsiveness of public timber harvesting lead to the increases in future harvest levels being borne almost exclusively from private land. This leads to an increases in private harvesting emissions ending at 734 Mt CO2 per year while only 41 Mt CO2 is emitted from USFS lands and 15 MT CO2 per year from other public lands.

Fig. 8.

National net sequestration CO2 flux projections by ownership class (2014–2034).

Live tree CO2 sequestration over the 21-year projection period also shows fundamental differences between public and private ownership groups. Despite low harvest emissions on public lands each group experiences slow declines in the rate of live tree carbon uptake with USFS forests falling from −147 to −101 Mt CO2 per year between 2014 and 2035 and Other Public falling from −99 to −70 Mt CO2 per year over the same period. As a result of the increase in harvesting emissions associated with meeting higher level of future forest products demand from private forests, net emissions fall from −297 to 58 Mt CO2 per year.

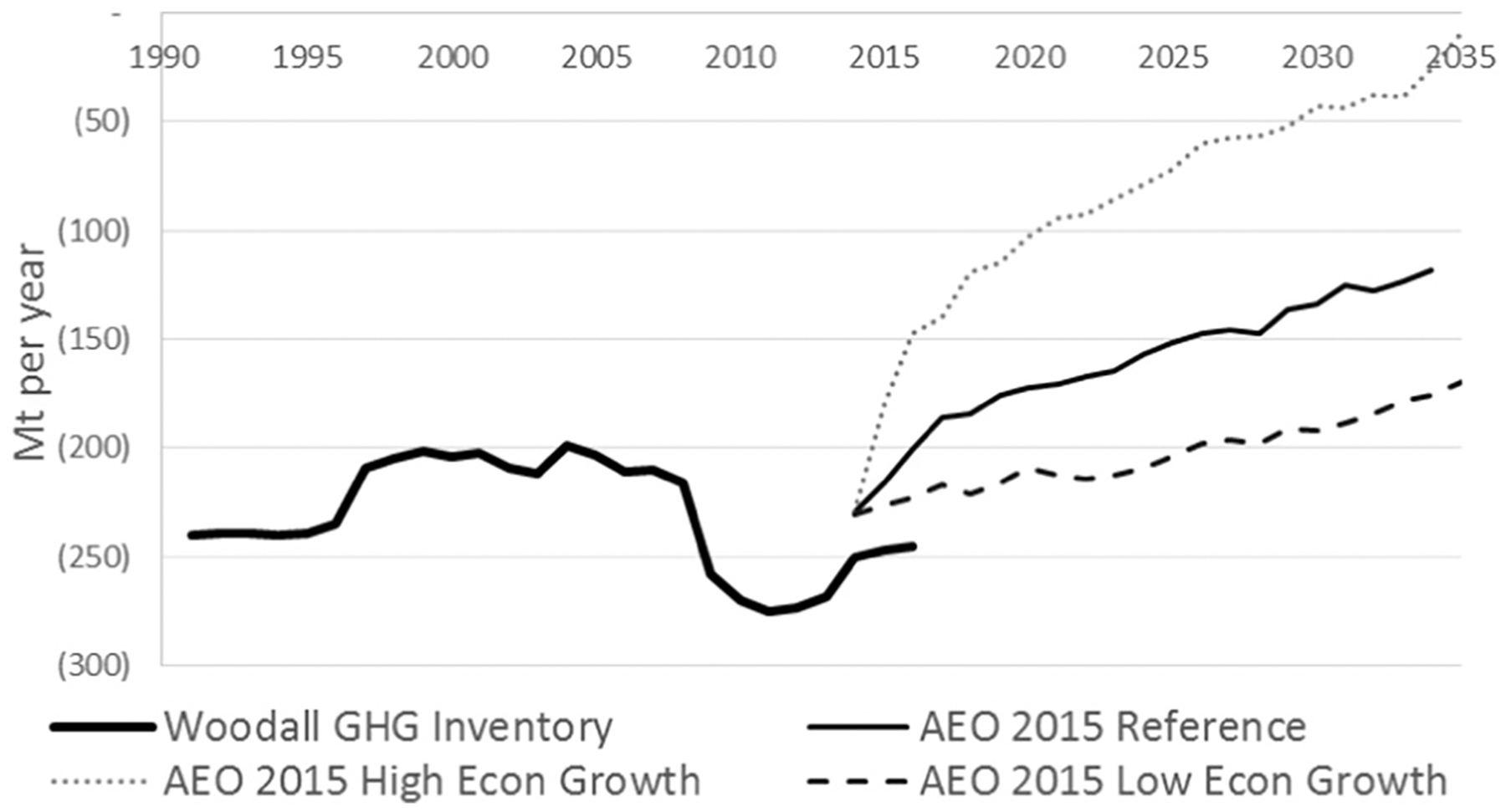

5.5. Alternate AEO scenario projections

Thus far we have focused on the basic trends in aboveground live tree carbon based on the 2015 AEO Reference Case macroeconomic outlook. These basic trends are important to consider and warrant investigation, but it is also important to demonstrate the importance and impact of varying macroeconomic indicators on expected or projected potential future tree carbon/CO2 emissions. Hence from this point on we rely on those trends as a backdrop on which to evaluate changes in only the aggregate GHG emissions while understanding that there will be important differences across GHG account types, owners, and regions. Fig. 9 presents the net aboveground live tree carbon GHG accounts for the 2015 AEO Reference, High Economic Growth, and Low Economic Growth cases. We also include 1990–2015 historical estimated net annual changes in carbon stocks of aboveground forest biomass (Woodall et al. 2015). These estimates of projected flux over these macroeconomic scenarios range from 84 Mt CO2 per year in the near term (2015–2020) and is higher still at 174 Mt CO2 per year over the longer-term (2030–2035).

Fig. 9.

Projected above ground live tree CO2 sequestration across the AEO macroeconomic scenarios.

In all three cases (AEO Reference and the high and low economic scenarios), the underlying trend is one of a forest that is increasing in carbon, but at a decreasing rate. In the AEO Reference Case, the 2014 changes in the aboveground live tree carbon pool result in net emissions level of −230 Mt CO2 per year while that reduction of atmospheric carbon slows over time to −118 Mt CO2 per year by 2035, a reduction of 49%. These results are consistent with the sink decline projected by Wear and Coulston (2015). In the 2014 AEO Low Economic Growth case, the lower rate of GDP growth and its associated demand as well as lower housing starts ease but does not reverse that decline in sequestration, resulting in only 29% reduction as (−230 to −8 Mt CO2 per year from 2014 to 2035). The 2015 High Economic Growth case reflects high GDP growth and housing starts that return to the pre-housing market collapse of 2007 by 2016. This outlook leads to a rapid decline in the annual sink, which is reduced from −230 to −10 Mt CO2 per year from 2014 to 2035 (a decline of more than 96%) in this scenario. This difference is driven by a substantial increase in harvest emissions under this High Economic Growth case, which are approximately 10% higher in 2015 than under the Reference Case, and grow to a difference of more than 18% by the end of the projection horizon.

6. Discussion

This study and the underlying LURA model represent an important improvement in our ability to generate spatially explicit projections of future GHG emissions. This modeling framework maintains the forest inventory data that forms the basis of U.S. forest emissions inventory, represents emissions from harvesting or fire releases of tree carbon, and gross sequestration in the form growth on existing or regenerated forests. We maintain the spatial detail on the demand side as the location of manufacturing facilities and distances logs and mill byproducts must travel drive those harvesting decisions. The resulting solution, or set of solutions, provide not a forecast of future occurrences but rather a range of possible outcomes and related metrics that can provide insight for forest-related climate policy or management decisions.

Our projections illustrate the importance of including and evaluating underlying economic conditions in addition to biophysical conditions on modeled forest sector outcomes. As individual forest product markets are more or less sensitive to projected economic conditions (namely, housing starts), changing economic outlooks can lead significant differences in projected emissions. For instance, greater anticipated economic growth that stimulates housing starts (AEO High Economic Growth) drives softwood and hardwood lumber harvests and reduces annual sequestration rates. The difference between CO2 outcomes in the AEO Reference and High Economic Growth scenarios in 2030 amounts to approximately 91 TgCO2 per year, or a 12% change relative to the baseline (approximately 1% of total U.S. projected emissions). While seemingly insignificant relative to total emissions, this 91 TgCO2 is meaningful as it represents approximately 5.2% of the total 26%–28% emissions reduction obligation that the U.S. has laid out in its NDC (relative to 2005). Thus, if LULUCF emissions deviate from one expected set of conditions (e.g., anticipated baseline) to another (improved economic outlook), this could make achieving NDC emissions reductions commitments difficult without additional policy interventions.

Scenario analyses can prove helpful for defining a range of potential outcomes as influenced by broader macroeconomic outlooks, such as those provided by AEO scenarios. The LURA projections presented here lie within the range of the high and low sequestration scenarios from the 2016 BR report. While this serves as a meaningful validation of the projection totals, there are several key results we can draw from the LURA projections. First, consistent with other recent studies (Wear and Coulston 2015; Tian et al. In Press), the U.S. forest sector is projected to be a sink in the future, but the size of this sink could diminish without strategic investments in improved forest management or new planting to stimulate the forest carbon stock.

However, unlike other recent studies (Wear and Coulston 2015), our regional results show that the South region could continue to be a strong carbon sink over the longer term once carbon stocks on previously harvested stands recover. While near term harvests increase in the face of bioenergy and wood pellet demand (which reduces sequestration early in the simulation horizon), forest regeneration and declining pulp demand lead to a decrease in emissions over time. The North and West regions are the primary drivers of the declining flux, primarily due to aging stands and continued high levels of fire disturbance in the future. This key result could be used to help prioritize resources or policy interventions to increase carbon sequestration, especially in those regions. Given the productivity of southern forests, emphasis on improved forest management, replanting, or afforesting in the South could result in significant carbon benefits within 10–15 years, which is a meaningful policy time frame for post-2020 climate agreements. Furthermore, our results highlight states or regions in which early mitigation action can potentially abate near and long term losses in forest carbon stocks in states that show a strong decline in near-term carbon accumulation (such as the Virginias and Carolinas). Simultaneously, fire suppression efforts in the West (like fuel treatments) could temporarily reduce fire disturbance risk, though it is debatable whether fuel treatments result in long term carbon benefits. Future analyses using the LURA model will attempt to evaluate the economic costs of targeted mitigation action in high risk areas.

6.1. Caveats and limitations

US LULUCF changes are influenced part by a number of drivers. While this study focuses on the general economy (macroeconomic indicators), future LULUCF changes are also driven by levels of fire and forest disturbance, policy decisions, and land use change. Potential changes in foreign trade with varying macroeconomic conditions can also influence results. Also, the model currently does not capture projected conversion of managed forests for urban and residential development as previous studies have (e.g., Wear and Coulston 2015), though this is a natural extension of the current modeling framework.

Perhaps the most important limitation, the recursive dynamic structure of LURA does not allow for endogenous forest management changes or land use change (afforestation) in anticipation of future demand. Previous studies have demonstrated the importance of intertemporal dynamics on trajectories of forest land use and management (Sohngen and Sedjo 2000; Alig et al. 2010; Latta et al. 2013; Tian et al. In Press). Optimal control models with perfect foresight of future economic conditions manage the forest system while accounting for the scarcity value of the resource over long time horizons. Endogenous management changes in anticipation of future demand or market/policy stimuli can lead to improved near-term carbon outcomes. Inclusion of intertemporal management and exogenous land use change projections are not captured in this application of the LURA framework, and inclusion of each would clearly change the LULUCF emissions projected by the model. Future work will attempt to address this limitation through iterative modeling, allowing intertemporal forest sector or CGE models to project aggregate land use changes, and then downscaling land use change and calibrating total harvest levels in LURA for scenario analysis.

Despite these limitations, the results of this analysis are nonetheless meaningful in that we illustrate the sensitivity of baseline LULUCF projections to economic conditions using a detailed spatial allocation model with explicit connections between the forest resource base (plots) and demand points (mills/ports). Our projections capture changes in the resource base over time, which influence economic outcomes and the extent and spatial distribution of harvest decisions, leading to more spatially refined estimates of where and when emissions are likely to occur, and how the resulting harvest is allocated. This information could be used to propose multiple or “adaptive” LULUCF projections in which obligations could be tied to realize economic conditions. Furthermore, spatially explicit projections information can be used to inform targeted policy interventions that incentivize additional management, land use change, or wood product use to decrease net LULUCF emissions and increase net sequestration.

Appendix A. List of symbols

This appendix listing symbols used in the paper has been organized into three groupings; sets, parameters, and variables. Sets, for which we have used lower case letters, are collections of things overs which the model is defined. Parameters, again designated by lower case letters, represent exogenous data which may or may not be defined over a group of sets. Finally, upper case letters indicate endogenous variables determined by the model which may or may not be defined over a group of sets.

Sets

b is the set of counties

c is the set of forest products commodities

d is the subset of locations represented by final forest commodity demand

e is the set of forested ecoprovinces

f is the subset of locations represented by 350,000 forested FIA condition classes

j is the set of states

l is the set of all sectoral locations including FIA condition classes, mills, ports, and demand

m is the subset of locations represented by forest product manufacturing mills

n is the subset of time steps (which can be either years for demand or ages for condition classes)

p is the subset of locations represented by forest product foreign trade ports where the subset of export port locations px are treated as a different set of locations from the subset of import ports pi even when at the same physical address

s is the set of forest site productivity classes

u is the set of forest types

x is the set of forest product manufacturing processes

θ is the set of macroeconomic demand shifters

Parameters

af forest area parameter for FIA condition class f available for harvest

gj parameter indicating annual public owner x in state j over the last twenty years with the superscript indicating either u for an upper level or avg. for an average level

h parameter indicating log harvest cost

ic′xc parameter indicating input of commodity c′ used to produce commodity c using production process x

klx parameter indicating capacity at location l (could be a mill, m or a port, p) using production process x

oc′xc parameter indicating output of commodity c produced when commodity c′ is consumed as an input using production process x

qc parameter indicating aggregate U.S. consumption quantity of commodity c

r parameter indicating total recycled paper availability

tl′cl parameter indicating transported cost of moving commodity c from location l′ to location l

w parameter indicating a harvest cost applied to wasted (or unused) forest material

yfc yield parameter for commodity c on FIA condition class f

αeus yield equation asymptote parameter for ecoprovince e, forest type u, and site class s

βeus yield equation slope parameter for ecoprovince e, forest type u, and site class s

ϕf parameter indicating proportion of the FIA condition class to be burned each year (based off 10-year county-level average)

λeu parameter indicating proportion of the forest area by ecoprovince e and forest type u that FIA condition class data indicates has seen some sort of partial harvesting

μc parameter indicating recycled commodity recovery rate (currently non-zero for paper commodities only)

δ parameter indicating annual capacity depreciation rate (assumed to be 5%)

Variables

C variable indicating a total cost

Hf variable indicating a regeneration harvest scheduled for FIA condition class f

Mmx variable indicating manufacturing at mill m using production process x

Pf variable indicating a partial harvest scheduled for FIA condition class f

Rm variable indicating recycled paper used at mill m

Tl′cl variable indicating transported amount of commodity c from location l′ to location l

Wlc variable indicating unused harvested commodity c at location l

Footnotes

Many parties also pledge climate change adaptation goals through these INDCs, but the focus of this manuscript is on GHG emissions reductions goals and the role of the forest sector.

In June 2017, the U.S. announced its intention to withdraw from the Paris Agreement and to renegotiate its contributions to the Paris Agreement or for an entirely new agreement. It is possible the U.S. forest sector could play a meaningful role in future U.S. commitments, both in terms of how projected U.S. forest emissions relate to total projected anthropogenic emissions under a new future baseline, and in terms of net mitigation potential that forest-related activities could provide.

For example, consider an FIA plot with four subplots—two that are younger stands, and two that older. The subplots are allocated to common condition classes with similar composition and age-class structure.

See Table 4 (http://nicholasinstitute.duke.edu/sites/default/files/publications/near-term-market-and-ghg-implications-of-forest-biomass-in-southeast-paper.pdf) for maximum cofiring specification for 14 coal boiler types.

U.S. International Trade Commission (USITC) Interactive Tariff and Trade Database (DataWeb) http://DataWeb.usitc.gov

Wasted wood product includes roundwood left unused at the harvest site.

An internet user is defined as anyone who has accessed the internet in the past 12 months through any type of device (e.g. computer, phone) from any location.

References

- Abt RC, Galik CS, Henderson JD, 2010. The Near-Term Market and Greenhouse Gas Implications of Forest Biomass Utilization in the Southeastern United States Working Paper. CCPP 10–01. Climate Change Policy Partnership, Duke University, Durham, NC. [Google Scholar]

- Alig R, Latta G, Adams D, McCarl B, 2010. Mitigating greenhouse gases: the importance of land base interactions betweenforests, agriculture, and residential development in the face of changes in bioenergy and carbon prices. For. Policy Econ 12, 67–75. [Google Scholar]

- Beach RH, Adams D, Alig R, Baker J, Latta GS, McCarl BA, Murray BC, Rose SK, White E, 2010. Model Documentation for the Forest and Agriculture Sector Optimization Model with Greenhouse Gases (FASOMGHG). RTI International Available online at. http://www.cof.orst.edu/cof/fr/research/tamm/FASOMGHG_Model_Documentation_Aug2010.pdf (last accessed October 1, 2010).

- Biomass Magazine, 2015. Biomass Magazine’s Pellet Producer List. http://biomassmagazine.com/plants/listplants/pellet/US/ (last accessed August 31, 2015).

- Cleland DT, Freeouf JA, Keys JE, Nowacki GJ, Carpenter CA, and McNab WH 2007. Ecological Subregions: Sections and Subsections for the conterminous United States. Gen. Tech. Report WO-76D [Map on CD-ROM] (A.M. Sloan, cartographer) Washington, DC: U.S. Department of Agriculture, Forest Service, presentation scale 1:3,500,000; colored. [Google Scholar]

- FAO, 2014. FAO online forestry statistics. http://www.fao.org.

- FAO, 2015. Global Forest Resources Assessment 2015 FAO Forestry Paper No. 1 The Food and Agricultural Organization of the United Nations (FAO), Rome. [Google Scholar]

- Galik CS, Abt RC, 2016. Sustainability guidelines and forest market response: an assessment of EU pellet demand in the southeastern U.S. GCB Bioenergy 8, 658–669. [Google Scholar]

- Galik CS, Abt RC, Latta G, Vegh T, 2015. The environmental and economic effects of regional bioenergy policy in the southeastern US. Energy Policy 85 (2015), 335–346. [Google Scholar]

- Galik CS, Abt RC, Latta G, Méley A, Henderson JD, 2016. Meeting renewable energy and land use objectives through public-private biomass supply partnerships. Appl. Energy 172, 264–274 15 June 2016. [Google Scholar]

- Ince PJ, Kramp AD, Skog KE, Spelter HN, Wear DN, 2011. U.S. forest products module: a technical document supporting the Forest Service 2010 RPA assessment In: Research Paper FPL-RP-662. U.S. Department of Agriculture, Forest Service, Forest Products Laboratory, Madison, WI: (61 pp.). [Google Scholar]

- IPCC, 2014. In: Edenhofer O, Pichs-Madruga R, Sokona Y, Farahani E, Kadner S, Seyboth K, Adler A, Baum I, Brunner S, Eickemeier P, Kriemann B, Savolainen J, Schlömer S, von Stechow C, Zwickel T, Minx JC (Eds.), Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA. [Google Scholar]

- Latta GS, Baker JS, Beach RH, Rose SK, McCarl BA, 2013. A multi-sector intertemporal optimization approach to assess the GHG implications of U.S. forest and agricultural biomass electricity expansion. J. For. Econ 19 (4), 361–383. [Google Scholar]

- Latta G, Plantinga A, Sloggy M, 2016. The effects of Internet use on global demand for paper products. J. For 114 (4), 433–440. [Google Scholar]

- Nepal P, Ince PJ, Skog KE, Chang SJ, 2012. Projection of U.S. forest sector carbon sequestration under U.S. and global timber market and wood energy consumption scenarios, 2010–2060. Biomass Bioenergy 45 (10), 251–264. [Google Scholar]

- NREL, 2012. U.S. Life Cycle Inventory Database National Renewable Energy Laboratory Accessed August 31, 2015 http://www.nrel.gov/lci/.

- Pan Y, Birdsey RA, Fang J, Houghton R, Kauppi PE, Kurz WA, Phillips OL, Shvidenko A, Lewis SL, Canadell JG, Ciais P, Jackson RB, Pacala SW, McGuire AD, Piao S, Rautiainen A, Sitch S, Hayes D, 2011. A large and persistent carbon sink in the world’s forests. Science 333, 988–993. [DOI] [PubMed] [Google Scholar]

- RISI Inc, 2012. Lockwood-Post Directory of Pulp & Paper Mills, The Americas 2011 Traveler’s Edition. Resource Information Systems, Inc. [Google Scholar]

- Roesch FA, Reams GA, 1999. Analytical alternatives for an annual inventory system. J. For 97 (12), 33–37. [Google Scholar]

- Smith BR, Rice RW, Ince PJ, 2003. Pulp capacity in the United States, 2000 In: Gen.Tech. Rep. FPL-139 U.S. Dept. of Agriculture, Forest Service, Forest Products Laboratory, Madison, WI: (23 pages). [Google Scholar]

- Sohngen B, Sedjo R, 2000. Potential carbon flux from timber harvests and management in the context of a global timbermarket. Clim. Chang 44, 151–172. [Google Scholar]

- Spelter H, 1996. Capacity, production, and manufacture of woodbased panels in the United States and Canada In: Gen. Tech. Rep. FPL–GTR–90 U.S. Department of Agriculture, Forest Service, Forest Products Laboratory, Madison, WI: (17 pp.). [Google Scholar]

- Spelter H, Toth D, 2009. North America’s wood pellet sector In: Research Paper FPL-RP-656. U.S. Department of Agriculture, Forest Service, Forest Products Laboratory, Madison, WI: (21 pp.). [Google Scholar]

- Spelter H, McKeever D, Toth D, 2009. Profile 2009: softwood sawmills in the United States and Canada In: Res. Pap. FPL-RP-659 U.S. Department of Agriculture, Forest Service, Forest Products Laboratory, Madison, WI: (55 pp.). [Google Scholar]

- Tian X, Sohngen B, Baker JS, Ohrel S, 2017. Will the U.S. forest sector continue to be a carbon sink? Land Econ (In Press). [DOI] [PMC free article] [PubMed] [Google Scholar]