Abstract

Behavioral finance studies reveal that investor sentiment affects investment decisions and may therefore affect stock pricing. This paper examines whether the geographic proximity of information disseminated by the 2014–2016 Ebola outbreak events combined with intense media coverage affected stock prices in the U.S. We find that the Ebola outbreak event effect is the strongest for the stocks of companies with exposure of their operations to the West African countries (WAC) and the U.S. and for the events located in the WAC and the U.S. This result suggests that the information about Ebola outbreak events is more relevant for companies that are geographically closer to both the birthplace of the Ebola outbreak events and the financial markets. The results also show that the effect is more pronounced for small and more volatile stocks, stocks of specific industry, and for the stocks exposed to the intense media coverage. The event effect is also followed by the elevated perceived risk; that is, the implied volatility increases after the Ebola outbreak events.

Keywords: Ebola outbreak, Information dissemination, Geographic proximity, Media coverage; Investor sentiment

1. Introduction

One of the central issues in the behavioral finance literature is to explain why some market participants make seemingly irrational decisions. A relatively large number of studies show that “bad mood” and anxiety may affect investor sentiment. Anxiety drives investor sentiment against taking risks, contributes to pessimism regarding future returns and thus dictates asset price movements (see for e.g. Baker and Wurgler, 2007, Cen and Liyan, 2013, Lucey and Dowling, 2005).

Early studies observe, for instance, that the weather, which is a well-known driver of peoples’ mood, tends to positively commove with daily stock returns (Hirshleifer and Shumway, 2003). In more recent studies, Kaplanski and Levy, 2010a, Kaplanski and Levy, 2010b study the impact of sporting games and aviation disasters on investor sentiment. They find that aviation disasters negatively affect investor sentiment and temporarily increase the fear for trading. Donadelli et al. (2016) analyze whether investor sentiment, measured by results of the FIFA World Cup, is related to the U.S. sectoral stock returns. They find some support that sport sentiment is priced in the financial sector but not in other sectors. Yuen and Lee (2003) study risk-taking tendencies in various mood states. They show that people in a depressed mood have lower willingness to engage themselves in risky situations than people in positive or neutral mood states.

We focus on the 2014–2016 Ebola pandemic outbreak and we analyze its outbreak events based on World Health Organization (WHO)’s alerts and mass-media news on pandemic diseases to examine the effect on companies’ stock returns.

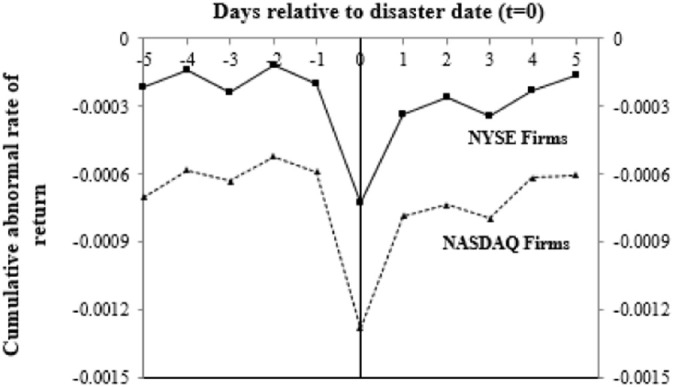

As a preliminary exploration, we plot cumulative abnormal returns surrounding the Ebola outbreak event days in Fig. 1 . We find negative cumulative abnormal returns on the event day and a reversal effect one day after the event. Possible reason for this effect may be that investors act irrationally to the news on the Ebola outbreak and after one day they stabilize their behavior.

Table 1.

Geographic proximity effect on financial markets.

The table reports the results of the following regression:

ri, t = γo + ∑j = 15γ1, jri, t − j + ∑k = 14γ2, kWDk, t + γ3Taxt + ∑l = 13γ4, lELl, t + εt,

where ri, t is the rate of return of stock i on day t with exposure of its operations towards the U.S., the WAC region, Europe, or All regions, γ0 is the regression intercept, ri, t − j is the lagged dependent variable—the jth previous day rate of return, WDk, t with k = 1, …, 4 are dummy variables for the day of the week (Monday, Tuesday, Wednesday, and Thursday), Taxt is a dummy variable for the first five days of the taxation year, and ELl, t with l = 1, 2, and 3, are dummy variables that denote the location where the event happened and equal 1 on the event day if the event happened in a specific region (either in the U.S., the WAC region, and Europe), and zero otherwise. The events occurred during the 2014–2016 Ebola outbreak period (3-year period) and include a total number of 103 event days of the disease outbreak. From the total number of events, 52 took place in the WAC region, 31 in the U.S., and 20 in Europe. Panel A depicts the regression results including the control variables whereas Panel B depicts the regression results without the control variables. The first line reports the regression coefficients, while the second line reports the corresponding t-values (in brackets). One, two, and three asterisks indicate a significance level of 10%, 5%, and 1%, respectively.

| Panel A: regression results including the control variables | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Exposure of the company to | γ0 | Rt − 5 | Rt − 4 | Rt − 3 | Rt − 2 | Rt − 1 | Mon. | Tue. | Wed. | Thu. | Tax | U.S. | WAC | Europe | R2 |

| U.S. only | − 0.0143 (− 3.002⁎⁎⁎) |

0.0129 (1.611) |

− 0.0132 (− 0.923) |

0.0283 (1.386) |

− 0.0111 (− 1.783⁎) |

0.0103 (3.448⁎⁎⁎) |

− 0.0231 (− 1.976⁎⁎) |

− 0.0133 (− 1.252) |

− 0.0160 (− 0.019) |

− 0.0211 (− 1.213) |

0.0285 (1.989⁎⁎) |

− 0.0259 (− 2.126⁎⁎) |

− 0.0163 (− 1.645⁎) |

− 0.0155 (− 1.591) |

0.4253 |

| WAC region | − 0.0522 (− 2.752⁎⁎⁎) |

0.0134 (1.604) |

− 0.0148 (− 1.110) |

0.0264 (1.113) |

− 0.0127 (− 1.887⁎) |

0.0118 (3.293⁎⁎⁎) |

− 0.0382 (− 1.691⁎) |

− 0.0223 (− 0.767) |

− 0.0122 (− 0.238) |

− 0.0103 (− 1.327) |

0.0226 (1.663⁎) |

− 0.0257 (− 2.108⁎⁎) |

− 0.0261 (− 1.970⁎⁎) |

− 0.0204 (− 1.690⁎) |

0.5811 |

| Europe | − 0.0251 (− 1.969⁎⁎) |

0.0153 (0.441) |

− 0.0128 (− 1.019) |

0.0245 (1.250) |

− 0.0102 (− 1.665⁎) |

0.0101 (1.959⁎⁎) |

− 0.0201 (− 1.675⁎) |

− 0.0115 (− 1.116) |

0.0150 (0.988) |

− 0.0118 (− 1.235) |

0.0150 (1.717⁎) |

− 0.0183 (− 1.987⁎⁎) |

− 0.0121 (− 1.687⁎) |

− 0.0188 (− 1.966⁎⁎) |

0.3736 |

| All | − 0.0308 (− 1.977⁎⁎) |

0.0172 (0.071) |

− 0.0138 (− 0.420) |

0.0251 (0.532) |

− 0.0114 (− 1.816⁎) |

0.0099 (3.688⁎⁎⁎) |

− 0.0212 (− 2.001⁎⁎) |

− 0.0254 (− 1.221) |

0.0154 (0.350) |

− 0.0170 (− 1.166) |

0.0288 (1.842⁎) |

− 0.0232 (− 2.020⁎⁎) |

− 0.0229 (− 1.965⁎⁎) |

− 0.0157 (− 1.780⁎) |

0.2332 |

| Panel B: regression results without the control variables | |||||||||||||||

| U.S. only | − 0.0125 (− 3.339⁎⁎⁎) |

− 0.0255 (− 3.317⁎⁎⁎) |

− 0.0151 (− 1.662⁎) |

− 0.0148 (− 1.550) |

0.4436 | ||||||||||

| WAC region | − 0.0413 (− 2.321⁎⁎) |

− 0.0245 (− 2.121⁎⁎) |

− 0.0248 (− 1.982⁎⁎) |

− 0.0192 (− 1.689⁎) |

0.5921 | ||||||||||

| Europe | − 0.0210 (− 1.995⁎⁎) |

− 0.0161 (− 1.992⁎⁎) |

− 0.0119 (− 1.682⁎) |

− 0.0176 (− 1.964⁎⁎) |

0.3524 | ||||||||||

| All | − 0.0289 (− 1.982⁎⁎) |

− 0.0229 (− 2.103⁎⁎) |

− 0.0224 (− 1.970⁎⁎) |

− 0.0153 (− 1.772⁎) |

0.2531 | ||||||||||

Fig. 1.

Cumulative abnormal rate of return (CAR). The figure depicts the Ebola outbreak effect surrounding the event day (t = 0) proxied by the CARs calculated using the market model for our sample of companies listed on the NYSE Composite and NASDAQ Composite. The events occurred during the 2014–2016 Ebola outbreak period (3-year period) and include a total number of 103 event days of the disease outbreak. The effect presented in the figure is based on a preliminary evaluation and it does not account for overlapping among the events' windows.

We begin our analysis by examining whether the geographic proximity of the information (disseminated by the Ebola outbreak events) to the financial markets has statistically significant impact on the U.S. stock prices. Motivated by Francis et al. (2007) and Engelberg and Parsons (2011), we anticipate that the Ebola outbreak events unequally affect investors’ mood—their sentiment about stock returns—depending on investors’ distance to the Ebola events from the markets. We classify the U.S. publicly listed companies into three groups depending on whether their operations have exposure to the U.S. only, the West African countries (WAC)1 , and Europe. We also distinguish among the Ebola outbreak events depending on where they occur (i.e., in the U.S., the WAC or Europe). We find that the Ebola outbreak event effect is the strongest for the stocks of companies with exposure of their operations to the WAC and the U.S. for the events located in the WAC and the U.S. This result suggests that the information about Ebola outbreak events is more relevant for companies that are geographically closer to both the birthplace of the Ebola outbreak events and the financial markets.

Second, we investigate whether there is a difference in the magnitude of the effect in portfolios classified by capitalization size. We find that the negative effect of the Ebola outbreak events is more pronounced for small companies relative to large companies. A potential explanation for this effect is that information dissemination is less effective for small cap stocks compared to large cap stocks.

Next, we examine whether the Ebola outbreak events affect investor sentiment proxied by the implied volatility. The results show that implied volatility increases following the Ebola outbreak event days but then subsides—indicating a mood-driven effect. In addition, we also build portfolios of securities sorted by volatility. The impact of the Ebola outbreak events on abnormal stock returns is negative and the most pronounced for small, illiquid, and more volatile stocks. For large, liquid, and less volatile stocks, the effect is also negative but of smaller magnitude.

Lastly, we evaluate the magnitude of the effect from the Ebola outbreak events for securities highly exposed in the media and securities belonging to a specific industry. We find evidence that the event effect is stronger for the securities exposed to the intense media coverage than for the securities receiving less media exposure. The event effect is also strong for securities belonging to the Healthcare equipment, Pharmaceutical, and Aviation industry.

Our paper makes the following contributions. With an important exception of Donadelli et al. (2017) who analyze various globally dangerous diseases and examine their impact upon pharmaceutical companies’ stock returns, our paper is fully focused on the impact of the Ebola outbreak events on the financial markets with the intent to analyze information dissemination and the importance of proximity of the event. Relating to the strand of literature that examines the effect of investor sentiment on the financial markets, our paper is closely related to Yuen and Lee (2003), Kaplanski and Levy, 2010a, Kaplanski and Levy, 2010b, Cen and Liyan (2013), and Donadelli et al. (2016) and shed new light on the role of geographic proximity of information to the financial markets and its psychological effects on investors’ decision making process. Our results show evidence that there is a clear relation between the relevancy of the Ebola outbreak events to investors’ actions and the magnitude of the event effect.

We contribute to the literature observing the effects of media coverage on investor sentiment, by considering the geographic proximity of the information to the financial markets. Our findings relate to Klibanoff et al. (1998), Fang and Peress (2009), Engelberg and Parsons (2011), Peress (2014), and Donadelli (2015) who find that investors react more to media covered events and pay more attention to stocks and news/events that are closer in distance to them.

The remainder of the paper goes as follows. Section 2 provides a theoretical background. Section 3 describes the data. Section 4 reveals the methodology and delineates the hypotheses tested in this study. Section 5 presents the results. Section 6 concludes the paper.

2. Theoretical background

The main hypothesis of this study asserts that the geographic proximity increases the impact of the information related to the 2014–2016 Ebola outbreak on the financial markets. This hypothesis relies on the observed relations between: companies' exposure to different geographic regions of operation, companies' size and type of industry in which they operate, the media coverage of disease outbreak, the fear, and anxiety that Ebola outbreak provokes, and investors' risk aversion to invest when fear and anxiety increase.

Several studies observe the relationship between investors' mood, anxiety, and asset pricing (Cen and Liyan, 2013, De Long et al., 1990). Our study is related to Kaplanski and Haim (2012) who observe the impact of negative events on holidays’ sentiment effect in the financial markets. They find positive and significant holiday sentiment effect and significant and negative war sentiment effect, which overtakes the positive holiday sentiment effect. Kamstra et al. (2003) study the impact of sunshine on asset prices. They find that due to seasonal characteristics, the return on the assets is lower when the daylight period is shorter.

Our study is also related to Kaplanski and Levy, 2010a, Kaplanski and Levy, 2010b, who study the impact of sporting games and aviation disasters on investor sentiment. They show that aviation disasters negatively affect investor sentiment and increase the fear for trading few days after the event. Alongside, several studies that analyze investors’ trading behavior and attitude towards risk taking confirm the fact that fear, anxiety, and depression are positively related to investors’ risk aversion (see, Hanock, 2002, Mehra and Sah, 2002).

Moreover, Yuen and Lee (2003) study risk-taking tendencies in various mood states. Their results show that people in a depressed mood have lower willingness to engage in risky situations than people in positive or neutral mood states. Donadelli et al. (2017) examine whether investor mood driven by various dangerous diseases is priced in pharmaceutical companies' stocks. They argue that global diseases should not trigger rational trading and they find positive effect upon pharmaceutical companies' stocks.

We focus on the 2014–2016 Ebola outbreak—a major disease outbreak, which was regarded as a public health emergency of international concern (PHEIC) by the WHO—to examine its impact on companies' stock returns. Our study contributes to this strand of literature by joining investor sentiment and the information flow from the geographically dispersed Ebola disease events. It adds up to the literature by examining investors' willingness to invest under the Ebola saturated state of mood. Finally, it observes investors' preference for investing in stocks of certain capitalization size and industry of operation.

Another set of studies identifies a relationship between the media as an information disseminator and investor sentiment. Blendon et al. (2004) study the intensity of media coverage of the Severe Acute Respiratory Syndrome (SARS) disease outbreak. They find that the media tends to disproportionately cover rare events, new events, and dramatic events—the ones that kill many people at once. Hence, as shown by Kepplinger and Hans Mathias (2008), when an unusual event occurs, the media starts hunting “newer” news on the same specific topic.

Klibanoff et al. (1998) show that investors assign more importance to news to which more attention has been given by the media than to news to which less importance has been assigned even if the news items have the same fundamental value. More specifically, Klibanoff et al. (1998) collect country-specific news reported on the New York Times front page and test investors' misperceptions, where investors incorrectly perceive the signals while predicting future fundamental security price behavior. The study finds that some investors react more to the fundamentals after well announced/publicized news thus affecting prices directly (see also Mairal, 2011, Peress, 2008).

Fang and Peress (2009) conduct research on media coverage and a cross-section of stock returns. They highlight the impact of the media on financial markets by studying return premiums on stocks for stocks with a media coverage versus stocks without a media coverage. Fang and Peress (2009) find that, on average, stocks not featured in the media gain 0.20% more per month than stocks that are covered more often.

Peress (2014) investigates the causal impact of the media on trading and price formation by observing newspaper strikes in several countries. He finds that, on strike days, trading volume falls by 12%, the dispersion of the stock returns and returns' intraday volatility is reduced by 7% whereas the aggregate returns show no signals. Donadelli (2015) measures policy-related uncertainty based on the volume of Google searches. He finds that a Google-searched-based uncertainty shock has sizable adverse effects on the U.S. macroeconomic conditions and it negatively affects the industrial production, equity prices, consumer sentiment, and consumer credit.

Several other studies observe the impact of a media coverage on specific industries. Huberman and Regev (2001) perform a case study to observe the financial market effects of a media coverage of a major breakthrough in cancer research. Interestingly, the bio-pharmaceutical companies in their sample responded significantly stronger to the breakthrough after enthusiastic public attention triggered by a Sunday New York Times article even though the main findings have already been reported five months earlier.

Our study is related to Francis et al. (2007) and Engelberg and Parsons (2011) who examine the role of a geographic location on an investor behavior and a firm decision-making process. Francis et al. (2007) find that a geographic proximity affects the dissemination of information. Geographically remote firms (usually rural firms) exhibit higher costs of debt than the firms located in the urban areas. To identify the role of a geographic proximity, Engelberg and Parsons (2011) measure media effects on stock returns at a local level. Their study finds that a local press coverage increases the trading volume of local investors up to 50%. Their results show that the media stimulates a local trading activity and that a geographic proximity matters. Differently than Engelberg and Parsons (2011), we examine the media coverage of global events having impact on companies exposed to different continental (geographic) locations of operations. In addition to the media coverage, we emphasize the role of trading intensity, stock variability, and liquidity, contributing to the literature on financial markets integration (Lucey et al., 2018).

3. Data

3.1. Ebola outbreak official announcements

The data examined cover the entire history of mass-media circulated Ebola outbreak events considered as public health emergency of international concern (PHEIC) by the WHO, in the period from January 2014 to June 2016. The entire period incorporates 103 events taking place on the U.S. territory (31 events), in Europe (20 events), and on the WAC territory (52 events). We divide the events in two categories: WHO reports and U.S. Newspapers Ebola Outbreak News. Events considered to be WHO reports are obtained from the official WHO website.2 The events considered as U.S. Newspapers Ebola Outbreak News are obtained from the LexisNexis article search engine. To retrieve the Ebola outbreak news from the LexisNexis, the search term “2014 Ebola outbreak” has been used. In addition, we set the engine to browse the three largest U.S. newspapers by circulation reporting on the events and companies of interest.3 About 51% of the news-events are published in The New York Times and the rest in The Washington Post and The Wall Street Journal.

The WHO reports that we encounter are official statements communicated to the public with regard to any new information related to the 2014–2016 Ebola outbreak. For example, on October 8, 2014, the first death case on the U.S. soil was publicly reported by the WHO.4 In addition, the WHO emergency committee stated the conditions and security guidelines for disease prevention. Usually, the mass media uses such WHO reports releases to communicate the information to the broader public.

The U.S. Newspapers Ebola Outbreak News are to some extent daily or weekly updates on the current situation and include, for example, news about the number of infected or dead people per day or cross-border transmissions of the disease. We consider the fact that regularly spaced updates may be anticipated by the financial investors and thus priced preceding the actual update. For this reason, the sample of announcements considers only those updates documenting a news-event for the first time (e.g., the first-time cross-border transmission, the first-time announcement of a death case in the U.S.). Such a strategy helps ensure the independence of subsequent as well as sequential announcements.

Under the U.S. Newspapers Ebola Outbreak News, we also include release dates of official statements provided by the government institutions of publicly traded companies to avoid a missing event-information bias. For instance, information disseminated in the media about a particular company's actions against the Ebola outbreak (e.g., a vaccine development approval by the government institutions) may positively affect that company as well as its competitors' stock prices. All announcements are categorized and summarized in Table A.2.

3.2. Stock market data

To test whether the geographic proximity of information to the financial markets has an impact on companies' stock returns, we employ the value-weighted5 total rates of return (see Table A.1 for definition) from the Center for Research in Security Prices (CRSP) of the New York Stock Exchange (NYSE) and NASDAQ Composite listed companies. In addition, we use the S&P500 index as a market performance benchmark. The NYSE Composite primarily contains large stocks generally characterized by good information dissemination whereas the NASDAQ Composite primarily includes some of the major tech stocks. Both markets were chosen for two reasons. First, they are the most closely followed in the world, thus very efficient with respect to dissemination of new information (Kaplanski and Levy, 2010a, Kaplanski and Levy, 2010b). Second, the U.S. stock markets are among the leading stock markets in the world and account for almost 50% of the global market (Hou et al., 2011).

To fully capture the impact of geographic proximity, we further use Bloomberg's and Bureau Van Dijk's “Orbis” databases to build the portfolios of companies which are listed on the U.S. stock markets (NYSE and NASDAQ) and have exposure towards the regions of interest that correspond to the Ebola outbreak events’ locations. We distinguish between exposures towards three different geographic regions: the U.S. only, the West African countries (WAC) region, and Europe. To ensure unbiased selection and categorization of the companies for each portfolio, we use the following four-step procedure.6 First, we select the companies by status: we are interested in active and publicly listed companies. Second, we further select the companies that have a domicile in the U.S. Third, we match each company according to its operation ownership 7 with the specific country or region of operation (i.e., towards its exposure to the U.S., the WAC, and Europe8 ). Fourth, we set up the period of operation of the companies from January 2014 to June 2016. At the end, the sample consists of all companies listed on the NYSE and NASDAQ Composite, from which 1040 are classified as having exposure towards the U.S. only, 89 are classified as also having exposure towards the WAC region, and 309 towards Europe. Table A.3 and Table A.4 summarize the companies filtered by this procedure.

To further analyze a potential differential effect regarding the company industry, company size, and stock volatility, we employ Fama and French's (1993) 10 value-weighted portfolios constructed by size and volatility, obtained from the CRSP. The industry based portfolio is created by selecting the 12 largest industries by contribution to the U.S. GDP in the period from January 2014 to June 2016. Industry data is acquired from the S&P Dow Jones Industry Index.

To measure investor sentiment, we employ the Chicago Board of Options Exchange's VIX and VXO9 indices which serve as proxies for investor sentiment (see Whaley, 2000).

To observe whether the intensity of a media coverage has a significant impact on specific companies, from the event category U.S. Newspapers Ebola Outbreak News, we build a subsample of events (or in this case, newspaper articles) which we consider as heavily covered in the media. To do this as well as to match each event with the corresponding stock or company, we refer to the LexisNexis's database for global news and business information. We use the number as well as the frequency of newspaper articles published about that stock in the media. We employ the LexisNexis “relevance score” to measure the quality of matching of an article to a specific company or stock. We use LexisNexis frequency of publishing score of 70% or above as a threshold to distinguish between the stocks with the intensive media coverage from the stocks without the intense media coverage. Lastly, the trading volume data (i.e., the proxy for trading intensity) and the price range and bid-ask spread (i.e., the proxies for stock market variability and liquidity) during the intense media coverage is obtained from the CRSP.

4. Methodology and hypotheses

We employ an event-study and regression based methodology to evaluate the impact of the 2014–2016 Ebola outbreak events on stock returns and to test the role of the geographic proximity of information.

The traditional event-study methodology is exercised to evaluate the general impact of the Ebola outbreak events upon companies’ stock returns through the one-factor and two-factor market models, as inspired by prior research (e.g., Donadelli et al., 2016, Fang and Peress, 2009, Peress, 2014). The one-factor model is estimated as:

| (1) |

where r i, t is the rate of return on stock i in period t and r m, t is the S&P500 rate of return, which serves as proxy for the market portfolio. The two-factor market model is estimated as:

| (2) |

where r i, t is the rate return on stock i in period t, r m, t is the S&P500 rate of return and r ind, t is the industry specific rate of return.

We begin our analysis by computing the cumulative abnormal returns (CARs) around the events considered. The abnormal returns (ARs) are defined as the difference between the actual rate of return of the stock considered and its ex-post expected rate of return over the whole length of the event window. We position 100 days in the estimation window and 11 days in the event window—5 days prior and 5 days after the event day noted as day 0 (for more on event study designs, see MacKinlay, 1997).

The sample of events that we observe is temporally clustered. Hence, the event study would suffer from overlapping windows if all events were considered. For this reason, we use only events with non-overlapping event windows (there is 40 such events). We use one of the two selection criteria to select events.

The first selection criterion is labelled as the last occurrence and chooses an event only if it is not followed by another event within 10 days after its occurrence. The second selection criterion is labelled as the first occurrence and selects events in chronological order (sequence). It starts with the first event in the sample, ignores all events showing up in the following 10 days, takes the next event in succession, ignores the following 10 days, and so on until the whole sample is exhausted. In a more illustrative way, assume there are five events taking place on dates ɗ0, ɗ1, ɗ2, ɗ3, and ɗ4 where ɗ1, ɗ2, and ɗ3 are temporally clustered. The last occurrence uses events for CAR calculation taking place on days ɗ0, ɗ3, and ɗ4 and the first occurrence chooses ɗ0, ɗ1, and ɗ4. With this strategy, we avoid unintentional bunching of events with overlapping windows in the same basket.

To observe whether the geographic proximity of information to the financial markets significantly affects stock returns, we run the following regression model (see, e.g., Kaplanski and Levy, 2010a, Kaplanski and Levy, 2010b, Kamstra et al., 2003, Brown and Warner, 1985):

| (3) |

where r i, t is the rate of return of stock i on day t, γ 0 is the regression intercept, r i, t − j is the lagged dependent variable—the jth previous day rate of return, WD k, t with k = 1, …, 4 are dummy variables for the day of the week (Monday, Tuesday, Wednesday, and Thursday), Tax t is a dummy variable for the first five days of the taxation year, and finally, EL l, t with l = 1, 2, and 3, are dummy variables that denote the location where the event happened and equal 1 on the event day if the event happened in a specific region (either in the U.S., the WAC region, or Europe), and zero otherwise.

The reason for including rates of return in previous days, r i, t − j in the regression in Eq. (3) is a potential presence of a serial correlation. A serial correlation is one of the known anomalies that may contaminate the results and may occur as a result of time-varying expected returns, non-synchronous trading, or transaction costs (see, e.g., Schwert, 1990a, Schwert, 1990b, Schwert, 2003, Campbell et al., 1993). We look at as many previous days' returns as is necessary to ensure that all significant correlations have been accounted for. In our case, it is the rates of return of the first five previous days. Following French (1980), Schwert (1990a), and Cho et al. (2007), we also acknowledge that the Ebola outbreak events may not be evenly distributed over the week either by the coincidence or by the nature of the events. We use dummies for each day of the week, WD it, to capture the so-called “Monday effects” or “weekend effect.”10 Lastly, we add a dummy for the first five days of the taxation year, Tax t, starting at January 1, to account for the so-called “turn-of-the-year effect” (see, e.g., Chien and Chen, 2008)11

To account for a potential reversal effect (driven by positive/negative sentiments), we also run the following regression:

| (4) |

where we look at the rate of return on the event day, E 0, t, and the first five subsequent trading days, E l, t (l = 1…5)12 (MacKinlay, 1997).

The following five hypotheses are tested in this study. First, we test whether the geographic proximity of information (disseminated by the Ebola outbreak events) has a statistically significant impact on the financial markets (more specifically, on companies' stock returns). We observe the U.S. publicly listed companies having exposure to events of three different geographic locations: the U.S. only, the WAC region, and Europe. We predict that the event effect (on the event day, i.e., day 0) will be strongest for the companies having exposure to the U.S. only and the WAC region since these companies are geographically closer to both the birthplace of the disease and to the financial markets (Engelberg and Parsons, 2011).

Second, we hypothesize that the event effect is stronger for the stock returns of small companies relative to large companies. This hypothesis is supported by the past research suggesting that local investors are usually the ones investing in small firms, thus their sentiment is affected by event information that is specific to the place and firm that they invest into (see, Brown and Cliff, 2005, Edmans et al., 2007).

Third, the Ebola outbreak as a type of event is perceived to increase bad mood as well as anxiety among investors, negatively affecting company returns. We proxy investor sentiment through stock price volatility. We hypothesize that the effect on the event day (i.e., day 0) is larger for more volatile stocks than for less volatile stocks (see, Kaplanski and Levy, 2010a).

Fourth, investors often hold very polarized stock portfolios. In our case, this means that some investors bet on a positive impact of the Ebola outbreak on certain stocks while others hold the opposite view. Having this in mind, we select the 12 largest industries, by contribution to the U.S. GDP, and test how (positively or negatively) the Ebola outbreak events affect each industry. We anticipate companies from the pharmaceutical and biotechnological industry to be positively affected whereas the companies from aviation and tourism sectors to experience a negative impact.

Fifth, previous studies confirm that the intense media coverage significantly affects stock returns, trading volume, stock liquidity, and stock variability (see, Fang and Peress, 2009). We hypothesize that the companies exposed to the intense media coverage are more affected by the Ebola outbreak events than the companies that receive less media exposure.

5. Results

5.1. Event study methodology

We now present the results of the event-study methodology. Fig. 2a–f depict the CARs around the event date whereas Table A.5–A.9 in the Appendix reveal the event study results in greater details.

Fig. 2.

Cumulative abnormal returns

Notes:Fig. 2a–e depict the cumulative abnormal returns (CARs) around the event day (t = 0) for portfolios of companies categorized by exposure towards different geographic locations, by their size, level of stock's volatility, industry of operation, and intensity of events' media coverage. Fig. 2f depicts companies trading volume, price range, and bid-ask spreads under high intensity of media coverage. The abnormal return on day t is calculated as the difference between the observed rate of return and the ex-post expected rate of return on day t. The one-factor market model rit = α0 + β1rm,t + εt, where rit is the return on stock i in period t and rm,t is the S&P 500 return, is estimated using a 100-day estimation window. The event selection procedure follows the last/first occurrence criteria which yields to a total number of 40 event days with non-overlapping event windows during the 2014–2016 Ebola outbreak period.

Fig. 2a shows that the one-factor market model CARs on the event day are statistically significant and negative for all three groups of the companies categorized by the exposure of their operations towards the regions of interest. Negative CARs are followed by a reversal effect on the first trading day following the event day. The CARs are the most negative for the companies having exposure to the WAC region (− 0.0198 and t-value of − 2.108), followed by the companies with the exposure to the U.S. only (− 0.0140 and t-value of − 6.114), and, followed by the companies with the exposure of their operations to Europe (− 0.0101 with t-value of − 6.887).

We use the two-factor model to match each company's CARs to the corresponding industry of operation and analyze whether the CARs are driven by the noise in the market (French and Roll, 1986). Similarly to the single factor model, the CARs for the companies with exposure of their operations to the U.S. only and to the WAC region are negative (− 0.0145 with t-value of − 6.163 for the U.S. and − 0.0192 with t-value of − 2.162 for the WAC region) and larger compared to the CARs for the companies with exposure of their operations to Europe (− 0.0135 with t-value of − 6.825). More evidence on these effects can be found in Table A.5.

In Fig. 2b and c, the portfolios of stocks are categorized by size and stock return volatility. Decile 10 (smallest firms) and decile 1 (highest volatility) show stronger negative CARs compared to the large and least volatile stocks (see also Tables A.6 and A.7). Furthermore, we find that aviation companies are the most negatively affected by the Ebola outbreak events whereas the companies producing healthcare equipment are on the other extreme and benefited the most (see Fig. 2d and Table A.8 for more details). Lastly, the companies under the intense media coverage exhibit stronger negative and statistically significant CARs compared to the companies that are not exposed to the intense media coverage (see, Fig. 2e). Under the intense media coverage, the trading volume, price range, and bid-ask spreads of the companies significantly increase around the event day (see Fig. 2f and Table A.9).

Overall, our event study analysis points to a negative impact of the Ebola outbreak events towards the U.S. companies' stock returns. We stress that the event study results are weaker than the regression results reported in the next section due to the fact that only 40 out of 103 events were employed in the CAR analysis—as a result of the event non-overlapping selection criteria.

5.2. Geographic proximity of information and financial markets

Panel A of Table 1 summarizes the results of the regression analysis in Eq. (3). Panel B of Table 1 presents the results of the regression without control variables. Panel A of Table 1 reveals that daily-rate-of-return coefficients of the companies with exposure of their operations to all regions are negative and significant to all event locations at the day of the event (i.e., to the events located in the U.S., the WAC, and Europe). As expected, the regression coefficient is the largest and statistically significant at 5% level for the companies with exposure of their operations to the WAC region and for the events located in the WAC region and in the U.S. (− 0.0261 and − 0.0257 for the WAC and the U.S. based events, respectively). Interestingly, the companies with exposure of their operations to the U.S. only region strongly react to the events located on the U.S. soil but less strongly to the other event locations. The regression coefficients for the companies with the exposure of their operations to Europe and event location in Europe are negative and significant, but of smaller magnitude.

The results regarding the control variables serial correlation , “Monday effects” (∑k = 1 4 WD k, t), and “turn-of-the-year effect” (Tax t) are similar to previous studies. The coefficients from lag 1 to lag 5, attributed to infrequent trading, happen to be both positive and negative and smaller compared to the coefficient on the event day. Similarly, the Monday coefficient is negative and the “turn-of-the-year effect” coefficient is positive and significant at least at 10% level. Coefficients for the other days of the week are mostly negative but insignificant (see Kaplanski and Levy, 2010b, Schwert, 1990a, Schwert, 1990b for similar results).

Lastly, to control for possible reversal effects we run the regression analysis in Eq. (4) for the securities with exposure to different regions of interest but for all event locations at ones. From Panel A of Table A.10 we can observe that the rate of returns from the first three days following the main event day are still negative, weaker, and significant (with significance varying from 10% level to 1% level) indicating a reversal behavior (see, Panel A of Table A.10, coefficients of E t, 1, E t, 2, and E t, 3 for all regions of exposure). We record no statistically significant coefficients on the fourth and fifth day following the main event day. Our results do not rule out the existence of an effect for the fourth and fifth day after the main event day but rather suggest that we could not observe it. This may be due to a small-time elapse between the events, greater variation in the period, and proliferation within the media.

To sum up, Table 1 accompanied by Table A.10 in the Appendix reveals that the event effect is present in all regions of interest and event locations. The stocks of the companies with exposure of their operations to the U.S. only and the WAC region exhibit a pronounced negative behavior, potentially as a result of the geographic proximity of the information to the financial markets. Furthermore, the tables show a reversal effect on the first day after the event day, persistent for three days and accompanied by negative/positive and statistically significant “Monday effects,” “turn-of-the-year effect,” and two-day significant serial correlation.

This provides support for our first hypothesis that the geographic proximity matters for the companies that are geographically closer to both the birthplace of the disease as well as to the financial market. There are two potential reasons for this. First, the investors feel that the U.S. only and the WAC region related companies are closer to the birthplace of the Ebola outbreak events, and thus, assume more relevance for (not) investing in them. Second, the media coverage affects investor sentiment especially for the companies with exposure of their operations to the U.S. and the WAC region than for the companies with exposure of their operations to Europe.

5.3. Event effect and firm size

Following Brown and Cliff (2005) and Edmans et al. (2007), we test whether the event effect is stronger for the stocks of small companies relative to the stocks of large companies. Table 2 reveals the regression results, where each dependent variable is the daily rate of return on a portfolio comprised of stocks belonging to a firm-size decile. Deciles rank from 1 to 10, where decile 1 is composed of the largest firms by size and decile 10 is composed of the smallest firms by size. Similarly to previous studies (e.g., Schwert, 1990b), on the day of the event, the event effect coefficients (corresponding to event locations: the U.S., the WAC, and Europe) tend to increase as size decreases. The regression coefficients for firms in decile 1 are − 0.0146, − 0.0142, and − 0.0132 for the events taking place in the U.S., the WAC, and Europe, respectively. The regression coefficients for firms in decile 10 are − 0.0519, − 0.0482, and − 0.0328 for the events taking place in the U.S., the WAC, and Europe, respectively.

Table 2.

Stocks classified by size.

The table reports the results of the following regression:

ri, t = γo + ∑j = 15ri, t − j + ∑k = 14γ2, kWDk, t + γ3Taxt + ∑l = 13γ4, lELl, t + εt,

where ri, t is the rate of return of stock i on day t classified by size, γ0 is the regression intercept, ri, t − j is the lagged dependent variable—the jth previous day rate of return, WDk, t with k = 1, …, 4 are dummy variables for the day of the week (Monday, Tuesday, Wednesday, and Thursday), Taxt is a dummy variable for the first five days of the taxation year, and ELl, t with l = 1, 2, and 3, are dummy variables that denote the location where the event happened and equal 1 on the event day if the event happened in a specific region (either in the U.S., the WAC region, and Europe), and zero otherwise. The events occurred during the 2014–2016 Ebola outbreak period (3-year period) and include a total number of 103 event days of the disease outbreak. From the total number of events, 52 took place in the WAC region, 31 in the U.S., and 20 in Europe. The first line reports the regression coefficients, while the second line reports the corresponding t-values (in brackets). One, two, and three asterisks indicate a significance level of 10%, 5%, and 1%, respectively.

| Size decile | γ0 | Rt − 5 | Rt − 4 | Rt − 3 | Rt − 2 | Rt − 1 | Mon. | Tue. | Wed. | Thu. | Tax | U.S. | WAC | Europe | R2 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Decile 1(largest firms) | − 0.0233 (− 1.672⁎) |

0.0651 (0.824) |

0.0731 (0.243) |

0.0541 (1.456) |

0.0639 (1.667⁎) |

0.0133 (1.644⁎) |

− 0.0167 (− 1.962⁎⁎) |

0.0052 (1.012) |

− 0.0033 (− 1.246) |

− 0.0032 (− 0.502) |

0.0234 (1.998⁎⁎) |

− 0.0146 (− 2.264⁎⁎) |

− 0.0142 (− 2.223⁎⁎) |

− 0.0132 (− 1.210) |

0.2769 |

| Decile 2 | − 0.0432 (− 1.831⁎) |

0.0932 (0.467) |

− 0.0083 (− 1.448) |

0.0073 (1.484) |

− 0.0137 (− 1.103) |

0.0148 (1.044) |

− 0.0235 (− 2.651⁎⁎⁎) |

0.0101 (1.314) |

− 0.0023 (− 1.223) |

− 0.0081 (− 0.107) |

0.0563 (1.657⁎) |

− 0.0255 (− 3.030⁎⁎⁎) |

− 0.0245 (− 2.191⁎⁎) |

− 0.0182 (− 1.932⁎) |

0.4053 |

| Decile 3 | − 0.0631 (− 1.615) |

0.0464 (0.902) |

− 0.0045 (− 1.522) |

0.0562 (1.100) |

− 0.0015 (− 1.895⁎) |

0.0342 (1.683⁎) |

− 0.0257 (− 2.138⁎⁎) |

0.0749 (0.033) |

0.0145 (0.214) |

− 0.0091 (− 1.134) |

0.0203 (1.774⁎) |

− 0.0243 (− 2.247⁎⁎) |

− 0.0235 (− 1.645⁎) |

− 0.0141 (− 1.767⁎) |

0.3143 |

| Decile 4 | − 0.0320 (− 1.854⁎) |

0.0235 (0.440) |

0.0142 (1.639) |

− 0.0235 (− 1.566) |

− 0.0266 (− 1.535) |

0.0255 (1.214) |

− 0.0160 (− 1.767⁎) |

0.0219 (0.036) |

0.0056 (1.261) |

− 0.0057 (− 0.145) |

0.0256 (1.872⁎) |

− 0.0209 (− 1.975⁎⁎) |

− 0.0113 (− 2.321⁎⁎) |

− 0.0092 (− 1.651⁎) |

0.2869 |

| Decile 5 | − 0.0241 (− 2.146⁎⁎) |

0.0334 (1.462) |

0.0407 (0.375) |

0.0448 (1.244) |

− 0.0197 (− 1.683⁎) |

0.0134 (2.213⁎⁎) |

0.0282 (− 1.755⁎) |

0.0535 (0.122) |

0.0035 (1.425) |

− 0.0065 (− 1.534) |

0.0251 (1.893⁎) |

− 0.0284 (− 2.128⁎⁎) |

− 0.0274 (− 1.696⁎) |

− 0.0155 (− 1.207) |

0.1398 |

| Decile 6 | − 0.0657 (− 1.953⁎) |

0.0376 (1.574) |

0.0775 (1.342) |

0.0185 (1.183) |

0.0494 (1.356) |

0.0135 (2.532⁎⁎) |

− 0.0321 (− 1.655⁎) |

− 0.0425 (− 0.134) |

0.0045 (1.124) |

− 0.0126 (− 0.153) |

0.0221 (1.854⁎) |

− 0.0333 (− 2.351⁎⁎) |

− 0.0312 (− 2.253⁎⁎) |

− 0.0161 (− 1.659⁎) |

0.4624 |

| Decile 7 | − 0.0442 (− 1.880⁎) |

0.0445 (0.102) |

0.0182 (0.944) |

0.0164 (1.171) |

− 0.0243 (− 1.567) |

0.0113 (1.979⁎⁎) |

− 0.0344 (− 2.201⁎⁎) |

0.0545 (0.423) |

0.0147 (0.050) |

− 0.0013 (− 0.352) |

0.0159 (1.968⁎⁎) |

− 0.0353 (− 2.121⁎⁎) |

− 0.0313 (− 1.961⁎) |

− 0.0113 (− 1.221) |

0.4840 |

| Decile 8 | − 0.0366 (− 1.975⁎⁎) |

0.0514 (0.037) |

− 0.0463 (− 1.284) |

0.0132 (0.219) |

− 0.0268 (− 1.872⁎) |

0.0126 (1.867⁎) |

− 0.0332 (− 1.742⁎) |

− 0.0236 (− 0.371) |

− 0.0061 (− 0.236) |

− 0.0062 (− 0.454) |

0.0174 (1.662⁎) |

− 0.0384 (− 4.124⁎⁎⁎) |

− 0.0337 (− 1.876⁎) |

− 0.0312 (− 1.910⁎) |

0.3343 |

| Decile 9 | − 0.0312 (1.673⁎) |

0.0258 (1.123) |

− 0.0233 (− 1.361) |

− 0.0287 (− 1.340) |

0.0139 (1.681⁎) |

0.0246 (1.976⁎⁎) |

− 0.0412 (− 1.659⁎) |

− 0.0121 (− 0.130) |

− 0.0081 (− 0.107) |

− 0.0044 (− 1.571) |

0.0123 (1.871⁎) |

− 0.0459 (− 4.053⁎⁎⁎) |

− 0.0410 (− 2.519⁎⁎) |

− 0.0324 (− 1.695⁎) |

0.1214 |

| Decile 10(smallest firms) | − 0.0421 (− 1.741⁎) |

0.0271 (0.490) |

0.0558 (0.467) |

0.0284 (1.026) |

− 0.0239 (− 1.852⁎) |

0.0323 (2.421⁎⁎) |

− 0.0487 (− 2.252⁎⁎) |

− 0.0462 (− 1.428) |

− 0.0091 (− 1.134) |

− 0.0035 (− 0.038) |

0.0132 (1.851⁎) |

− 0.0519 (− 2.916⁎⁎⁎) |

− 0.0482 (− 2.238⁎⁎) |

− 0.0328 (− 1.966⁎⁎) |

0.2502 |

Regarding the control variables, the serial correlation coefficients for 1 and 2 lags corresponding to the largest stocks are positive and significant. These results correspond to those of Schwert (1990b), who finds significant serial correlations for these variables when analyzing the S&P's Composite Index. Furthermore, large (in absolute terms) and significant “Monday effect” as well as “turn-of-the-year effect” are recorded throughout all size deciles.

Lastly, to control for possible reversal effects we return to the regression analysis in Eq. (4). On the day following the event day, the gap between the most extreme portfolios widens even more, potentially as a result of an investor reaction to the previous day event (from − 0.0140 for decile 1 to − 0.0524 for decile 10). We observe statistically significant reversal effects up to the third trading day after the event day (see Table A.11 in the Appendix).

To sum up, Table 2 and Table A.11 in the Appendix report that the event effect is more pronounced for small stocks rather than for large stocks from the event day to three days later. A potential explanation could posit that the information dissemination of small stocks is poorer than the information dissemination of large stocks. Due to the disparity between the small and large stocks, media can especially influence small stocks, for which the information dissemination is limited. For large stocks, information dissemination channels are already well-established and the role of media is more restrained (Fang & Peress 2009).

5.4. Event effect on implied volatility (VIX and VXO)

Following Baker and Wurgler (2007) who use implied volatility as a proxy for investor sentiment, we next test whether Ebola outbreak events affect the implied volatility. We employ two measures of the fear index,13 the VIX and VXO (see Whaley, 2000).

Fig. 3 shows the aggregated volatility pattern around the event days. It reveals a strong effect on the day of the event (at t = 0) and a mild persistence of the effect on the first day following the event day. In addition, we do not observe a return to the prevailing average value before the event. This result complies with previous findings showing that the market volatility is persistent (e.g., Baker and Wurgler, 2007). To test the significance of the volatility represented by VIX and VXO, we employ a matched-pair t-test. We observe statistically significant increase in volatility on the event day with t-values of t = 4.579 (P < 0.001) and t = 4.013 (P < 0.028) for VIX and VXO respectively.

Fig. 3.

Fear Index around the event days. The figure depicts the average value of VIX and VXO indices around the event day (t = 0). The 2014–2016 Ebola outbreak period is covered. It includes 40 non-overlapping events of the total 103 events.

Our results might indicate that the rapid increase in the implied volatility on the event day is due to a mood effect induced by the Ebola outbreak events. However, the increase in the volatility may also be due to an increase in the actual market volatility, which may coincidentally occur at the same time as the Ebola outbreak. For example, Schwert (2003) analyzes a long-time period of market volatility and finds that the monthly stock volatility was higher during banking crises and economic recessions. In our case, there may be other reasons for increased market volatility around the event day if an Ebola outbreak effect is related to some confounding variables (e.g., stock market crashes or economic crises).

5.5. Event effect and company risk

Baker and Wurgler (2007) study the impact of investor sentiment on a cross-section of stock returns. They find that investor sentiment has a stronger effect upon the securities with valuations that are difficult to arbitrage and subjective to evaluate. Inspired by their study, we examine the Ebola outbreak event effect on various groups of stocks (volatile vs. non-volatile). Table 3 reports the results, where each dependent variable is the daily rate of return on a portfolio composed of stocks that are divided into 10 deciles with respect to stock volatility. Decile 1 includes the most volatile and decile 10 includes the least volatile stocks.

Table 3.

Stocks classified by volatility.

The table reports the results of the following regression:

ri, t = γo + ∑j = 15γ1, jri, t − j + ∑k = 14γ2, kWDk, t + γ3Taxt + ∑l = 13γ4, lELl, t + εt,

where ri, t is the rate of return of stock i on day t classified by volatility, γ0 is the regression intercept, ri, t − j is the lagged dependent variable—the jth previous day rate of return, WDk, t with k = 1, …, 4 are dummy variables for the day of the week (Monday, Tuesday, Wednesday, and Thursday), Taxt is a dummy variable for the first five days of the taxation year, and ELl, t with l = 1, 2, and 3, are dummy variables that denote the location where the event happened and equal 1 on the event day if the event happened in a specific region (either in the U.S., the WAC region, and Europe), and zero otherwise. The events occurred during the 2014–2016 Ebola outbreak period (3-year period) and include a total number of 103 event days of the disease outbreak. From the total number of events, 52 took place in the WAC region, 31 in the U.S., and 20 in Europe. The first line reports the regression coefficients whereas the second line reports the corresponding t-values (in brackets). One, two, and three asterisks indicate a significance level of 10%, 5%, and 1%, respectively.

| Volatility decile | γ0 | Rt − 5 | Rt − 4 | Rt − 3 | Rt − 2 | Rt − 1 | Mon. | Tue. | Wed. | Thu. | Tax | U.S. | WAC | Europe | R2 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Decile 1 (highest volatility) | − 0.0831 (− 2.212⁎⁎) |

0.0240 (1.647⁎) |

0.0232 (1.532) |

0.0136 (1.653⁎) |

− 0.0131 (− 2.321⁎⁎) |

0.0018 (1.962⁎⁎) |

− 0.0133 (− 1.652⁎) |

− 0.0132 (− 1.732⁎) |

− 0.0124 (− 0.501) |

− 0.0131 (− 1.231) |

0.0136 (1.972⁎⁎) |

− 0.0492 (− 2.135⁎⁎) |

− 0.0463 (− 2.341⁎⁎) |

− 0.0401 (− 1.742⁎) |

0.3232 |

| Decile 2 | − 0.0821 (− 2.335⁎⁎) |

0.0147 (1.998⁎⁎) |

0.0244 (1.064) |

0.0124 (1.647⁎) |

− 0.0126 (− 2.025⁎⁎) |

0.0013 (1.714⁎) |

− 0.0128 (− 2.230⁎⁎) |

− 0.0127 (− 1.754⁎) |

− 0.0122 (− 0.627) |

− 0.0119 (− 1.024) |

0.0135 (1.863⁎) |

− 0.0483 (− 1.971⁎⁎) |

− 0.0415 (− 1.652⁎) |

− 0.0385 (− 2.074⁎⁎) |

0.5124 |

| Decile 3 | − 0.0366 (− 1.975⁎⁎) |

0.0213 (0.049) |

− 0.0463 (− 1.284) |

0.0139 (1.229) |

− 0.0268 (− 1.872⁎) |

0.0116 (1.864⁎) |

− 0.0132 (− 1.642⁎) |

− 0.0236 (− 0.371) |

− 0.0061 (− 0.236) |

− 0.0062 (− 0.454) |

0.0183 (1.645⁎) |

− 0.0462 (− 2.123⁎⁎) |

− 0.0367 (− 1.865⁎) |

− 0.0217 (− 1.934⁎) |

0.3021 |

| Decile 4 | − 0.0442 (− 1.880⁎) |

0.0445 (1.235) |

0.0482 (0.944) |

0.0123 (1.142) |

− 0.0243 (− 1.567) |

0.0125 (1.968⁎⁎) |

− 0.0130 (− 2.109⁎⁎) |

0.0545 (0.423) |

0.0147 (0.050) |

− 0.0013 (− 0.352) |

0.0161 (1.974⁎⁎) |

− 0.0414 (− 2.092⁎⁎) |

− 0.0333 (− 1.960⁎) |

− 0.0223 (− 0.323) |

0.4840 |

| Decile 5 | − 0.0342 (− 2.351⁎⁎) |

0.0135 (1.646⁎) |

0.0239 (1.437) |

0.0122 (0.365) |

− 0.0112 (− 1.932⁎) |

0.0022 (1.520) |

− 0.0116 (− 1.851⁎) |

− 0.0111 (− 1.238) |

− 0.0115 (− 0.231) |

− 0.0065 (− 1.534) |

0.0124 (1.725⁎) |

− 0.0369 (− 2.303⁎⁎) |

− 0.0292 (− 3.352⁎⁎⁎) |

− 0.0266 (− 1.651⁎) |

0.4157 |

| Decile 6 | − 0.0133 (− 1.966⁎⁎) |

0.0144 (1.667⁎) |

0.0231 (0.234) |

0.0127 (0.325) |

− 0.0114 (− 2.643⁎⁎) |

0.0023 (0.127) |

− 0.0108 (− 1.644⁎) |

− 0.0107 (− 0.025) |

− 0.0110 (− 0.019) |

− 0.0126 (− 0.153) |

0.0122 (1.643⁎) |

− 0.0271 (− 2.152⁎⁎) |

− 0.0235 (− 4.230⁎⁎⁎) |

− 0.0261 (− 1.845⁎) |

0.1208 |

| Decile 7 | 0.0128 (1.646⁎) |

0.0132 (1.714⁎) |

0.0117 (1.872⁎) |

0.0110 (1.262) |

− 0.0113 (− 4.119⁎⁎⁎) |

0.0009 (1.649⁎) |

− 0.0113 (− 1.742⁎) |

− 0.0105 (− 1.051) |

− 0.0108 (− 0.864) |

− 0.0013 (− 0.352) |

0.0103 (1.965⁎⁎) |

− 0.0247 (− 1.563) |

− 0.0219 (− 1.421) |

0.0249 (1.138) |

0.6121 |

| Decile 8 | 0.0131 (2.524⁎⁎) |

0.0123 (1.842⁎) |

0.0106 (1.971⁎⁎) |

0.0104 (0.103) |

− 0.0111 (− 1.742⁎) |

0.0012 (1.861⁎) |

− 0.0121 (− 1.821⁎) |

− 0.0105 (− 1.203) |

− 0.0103 (− 1.243) |

− 0.0105 (− 0.028) |

0.0095 (1.742⁎) |

− 0.0236 (− 1.976⁎⁎) |

− 0.0216 (− 3.915⁎⁎⁎) |

− 0.0227 (− 1.163⁎) |

0.3343 |

| Decile 9 | 0.0125 (3.348⁎⁎⁎) |

0.0103 (1.994⁎⁎) |

0.0112 (2.643⁎⁎⁎) |

0.0119 (1.977⁎⁎) |

− 0.0114 (− 1.205) |

0.0014 (1.763⁎) |

− 0.0110 (− 1.974⁎⁎) |

− 0.0104 (− 1.735⁎) |

− 0.0107 (− 1.023) |

− 0.0085 (− 1.162) |

0.0089 (1.667⁎) |

− 0.0177 (− 1.983⁎⁎) |

− 0.0108 (− 2.202⁎⁎) |

− 0.0118 (− 1.677⁎) |

0.2915 |

| Decile 10 (lowest volatility) | 0.0123 (3.224⁎⁎⁎) |

0.0132 (1.653⁎) |

0.0110 (2.284⁎⁎) |

0.0112 (3.095⁎⁎⁎) |

− 0.0110 (− 2.128⁎⁎) |

0.0016 (1.981⁎⁎) |

− 0.0102 (− 1.750⁎) |

− 0.0105 (− 1.767⁎) |

− 0.0106 (− 1.362) |

− 0.0100 (− 1.046) |

0.0033 (1.560) |

− 0.0149 (− 2.214⁎⁎) |

− 0.0109 (− 1.750⁎) |

− 0.0103 (− 1.652⁎) |

0.4512 |

Our results show that the event effect is intact for all deciles, except for decile 7. The regression coefficient on the day of the event is larger, negative, and highly significant for the most volatile stocks compared to the regression coefficient for the less volatile stocks, which is consistent with our third hypothesis in Section 4.

Regarding the control variables, “Monday effect” as well as “turn-of-the-year effect” variables show negative and statistically significant presence in stocks’ volatility for each portfolio employed.

The results of the regression in Eq. (4) are presented in Table A.12 in the Appendix. The coefficients for the days following the event day follow similar pattern. That is, the event effect magnitude is larger, negative, and significant for the stocks belonging to the highest volatility decile than for the stocks belonging to the least volatile decile.

5.6. Event effect on the U.S. industries

Table 4 reveals the regression results where stocks are classified by different industries. On the day of the event (for the events taking place in the U.S., the WAC, and Europe), all coefficients are large, negative, and significant, except for Healthcare equipment, Pharmaceutical, Biotechnology, and Food & Beverage industry. The stock returns of these four industries are positively affected by the Ebola outbreak. The results from Table 4 confirm our expectations, revealing evidence for the industry effect.

Table 4.

Event effect on U.S. Industries.

The table reports the results of the following regression:

ri, t = γo + ∑j = 15γ1, jri, t − j + ∑k = 14γ2, kWDk, t + γ3Taxt + ∑l = 13γ4, lELl, t + εt,

where ri, t is the rate of return of stock i on day t classified by industry of operation, γ0 is the regression intercept, ri, t − j is the lagged dependent variable—the jth previous day rate of return, WDk, t with k = 1, …, 4 are dummy variables for the day of the week (Monday, Tuesday, Wednesday, and Thursday), Taxt is a dummy variable for the first five days of the taxation year, and ELl, t with l = 1, 2, and 3, are dummy variables that denote the location where the event happened and equal 1 on the event day if the event happened in a specific region (either in the U.S., the WAC region, and Europe), and zero otherwise. The events occurred during the 2014–2016 Ebola outbreak period (3-year period) and include a total number of 103 event days of the disease outbreak. From the total number of events, 52 took place in the WAC region, 31 in the U.S., and 20 in Europe. The first line reports the regression coefficients, while the second line reports the corresponding t-values (in brackets). One, two, and three asterisks indicate a significance level of 10%, 5%, and 1%, respectively. The industries have been selected by their contribution to the U.S. GDP. Below presented, are the 12 largest by contribution industries according to S&P Dow Jones Industry Indexes.

| Industry name | γ0 | Rt − 5 | Rt − 4 | Rt − 3 | Rt − 2 | Rt − 1 | Mon. | Tue. | Wed. | Thu. | Tax | U.S. | WAC | Europe | R2 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Capital markets | − 0.0321 (− 2.225⁎⁎) |

0.0136 (0.221) |

0.0126 (1.076) |

0.0153 (0.442) |

0.0145 (1.044) |

0.0124 (2.132⁎⁎) |

− 0.0153 (− 1.752⁎) |

− 0.0113 (− 1.322) |

− 0.0134 (− 1.231) |

− 0.0163 (− 1.467) |

0.0135 (1.243) |

− 0.0121 (− 2.143⁎⁎) |

− 0.0131 (− 1.662⁎) |

− 0.0122 (− 1.915⁎) |

0.3509 |

| Healthcare equipment | 0.0448 (1.854⁎) |

0.0163 (1.647⁎) |

0.0165 (1.057) |

0.0164 (1.657⁎) |

0.0127 (1.794⁎) |

0.0145 (2.116⁎⁎) |

0.0123 (1.982⁎⁎) |

0.0142 (1.544) |

0.0216 (0.224) |

− 0.0134 (− 0.304) |

0.0131 (1.310) |

0.0249 (1.971⁎⁎) |

0.0251 (2.320⁎⁎) |

0.0224(1.757⁎) | 0.4291 |

| Crude oil | − 0.0563 (− 1.542) |

− 0.0147 (− 2.202⁎⁎) |

− 0.0167 (− 2.356⁎⁎) |

− 0.0145 (− 1.845⁎) |

− 0.0134 (− 1.656⁎) |

0.0019 (1.673⁎) |

− 0.0126 (− 1.929⁎) |

− 0.0156 (− 1.230) |

− 0.0145 (− 1.021) |

0.0147 (1.367) |

0.0038 (1.674⁎) |

− 0.0125 (− 1.962⁎⁎) |

− 0.0164 (− 1.646⁎) |

− 0.0112 (− 1.722⁎) |

0.2376 |

| Industrials | − 0.0474 (− 2.639⁎⁎) |

− 0.0192 (− 1.687⁎) |

− 0.0154 (− 0.341) |

− 0.0173 (− 1.532) |

− 0.0143 (− 0.013) |

0.0121 (1.676⁎) |

− 0.0138 (− 1.785⁎) |

− 0.0134 (− 0.174) |

− 0.0132 (− 1.447) |

0.0264 (1.456) |

0.0236 (0.085) |

− 0.0159 (− 1.983⁎⁎) |

− 0.0163 (− 1.965⁎⁎) |

− 0.0134 (− 1.826⁎) |

0.2049 |

| Materials | − 0.0121 (− 1.843⁎) |

− 0.0125 (− 1.941⁎) |

− 0.0147 (− 1.667⁎) |

− 0.0162 (− 2.162⁎⁎) |

− 0.0145 (− 1.992⁎⁎) |

− 0.0119 (− 2.223⁎⁎) |

− 0.0108 (− 1.662⁎) |

− 0.0113 (− 1.025) |

− 0.0122 (− 1.152) |

0.0155 (1.357) |

0.0134 (1.279) |

− 0.0147 (− 1.960⁎⁎) |

− 0.0151 (− 1.742⁎) |

− 0.0128 (− 1.646⁎) |

0.3516 |

| Information technology | 0.0437 (2.220⁎⁎) |

− 0.0131 (− 1.422) |

0.0143 (1.342) |

− 0.0157 (− 0.235) |

− 0.0122 (− 1.962⁎⁎) |

− 0.0115 (1.654⁎) |

− 0.0143 (− 1.685⁎) |

− 0.0164 (− 0.432) |

− 0.0126 (− 1.227) |

0.0143 (1.574) |

0.0205 (1.621) |

− 0.0156 (− 2.311⁎⁎) |

− 0.0138 (− 1.321) |

− 0.0122 (− 1.752⁎) |

0.2941 |

| Utilities | − 0.0215 (− 1.556) |

0.0119 (1.508) |

0.0146 (1.842⁎) |

− 0.0177 (− 1.662⁎) |

− 0.0175 (− 1.114) |

0.0114 (1.961⁎⁎) |

− 0.0152 (− 1.651⁎) |

− 0.0145 (− 1.475) |

− 0.0132 (− 1.121) |

− 0.0124 (− 1.042) |

− 0.0192 (− 1.325) |

− 0.0138 (− 1.970⁎⁎) |

− 0.0137 (− 1.651⁎) |

− 0.0118 (− 1.885⁎) |

0.1308 |

| Energy | − 0.0594 (− 1.967⁎⁎) |

− 0.0124 (− 1.654⁎) |

− 0.0138 (− 1.412) |

− 0.0153 (− 1.748⁎) |

− 0.0139 (− 1.894⁎) |

− 0.0110 (− 1.702⁎) |

− 0.0149 (− 1.822⁎) |

− 0.0156 (− 1.657) |

− 0.0132 (− 1.421) |

− 0.0158 (− 1.441) |

− 0.0102 (− 1.474) |

− 0.0162 (− 1.667⁎) |

− 0.0142 (1.644⁎) |

− 0.0127 (1.667⁎) |

0.3257 |

| Food & beverage | 0.0233 (2.274⁎⁎) |

− 0.0112 (− 1.338) |

− 0.0124 (− 1.255) |

− 0.0242 (− 0.497) |

− 0.0135 (− 1.733⁎) |

0.0124 (1.948⁎) |

0.0132 (1.758⁎) |

0.0142 (1.436) |

0.0136 (1.705) |

0.0114 (1.156) |

0.0207 (1.648⁎) |

0.0172 (1.972⁎⁎) |

0.0167 (1.981⁎⁎) |

0.0144 (1.740⁎) |

0.4452 |

| Aviation | − 0.0652 (− 1.995⁎⁎) |

− 0.0123 (− 1.445) |

0.0130 (1.501) |

0.0157 (1.358) |

0.0134 (1.345) |

0.0163 (1.927⁎) |

− 0.0121 (− 1.672⁎) |

− 0.0129 (− 1.525) |

0.0157 (1.116) |

0.0133 (0.248) |

− 0.0252 (− 1.963⁎⁎) |

− 0.0329 (− 1.965⁎⁎) |

− 0.0332 (− 2.104⁎⁎) |

− 0.0243 (− 1.655⁎) |

0.3640 |

| Pharma. | 0.0420 (1.861⁎) |

0.0132 (1.734⁎) |

0.0134 (1.656⁎) |

0.0124 (1.666⁎) |

0.0213 (1.232) |

0.0150 (1.911⁎) |

0.0155 (2.014⁎⁎) |

0.0126 (1.505) |

0.0138 (1.543) |

0.0148 (1.233) |

0.0151 (1.712⁎) |

0.0186 (1.841⁎) |

0.0192 (2.664⁎⁎⁎) |

0.0188 (2.229⁎⁎) |

0.3321 |

| Biotech. | 0.0461 (1.772⁎) |

0.0133 (1.854⁎) |

0.0244 (1.716⁎) |

0.0144 (1.649⁎) |

0.0216 (1.101) |

0.0211 (2.218⁎⁎) |

0.0208 (1.954⁎) |

0.0214 (1.056) |

0.0072 (1.127) |

0.0132 (1.521) |

0.0188 (1.991⁎⁎) |

0.0147 (2.112⁎⁎) |

0.0149 (1.987⁎⁎) |

0.0136 (2.662⁎⁎⁎) |

0.2825 |

A potential explanation is that investors anticipate an increase in cash flows for the industries due to, for example, investing in R&D or selling new medicines aimed at fighting the new pandemic disease. The results are related to Hirshleifer and Shumway (2003) who find that innovative efficiency and citations scaled by R&D expenditures positively determine future stock returns. A conclusion would be that the investor sentiment about the performance of certain industries may be an important element that drives investment decisions.

5.7. Event effect and media coverage

Following Kaplanski and Levy (2010b), we search the media for articles related to the Ebola outbreak disease to understand the scale and timing of the information salience and to evaluate the media coverage as a potential source of investor sentiment. Fig. 4a and b illustrate the number and frequency of media published articles about the Ebola outbreak.

Fig. 4.

Fig. 4a represents the number of articles published on the “Ebola outbreak” in the New York Times, Wall Street Journal, and Washington Post newspapers during the years 2014–2016. Fig. 4b depicts the normalized number of distinct, Ebola outbreak related newspaper articles published in the above-mentioned newspapers. The event dates (denoted as t = 0) are considered to be the official PHEIC statements. The number of articles is normalized relative to its peak value over the 11-day period. The black horizontal line represents the threshold level of 70% LexisNexis frequency of publishing score. Data is obtained using the LexisNexis database for global news and business information.

The number of articles published by the three most circulated U.S. newspapers increases rapidly in the year of 2014 (see Fig. 4a). In addition, the frequency of relevant news articles increases notably on the event day (see Fig. 4b). The news coverage intensifies in the next three days, having its maximum on the first day after the event day. The purpose of this observation is twofold. First, it supports the events’ intense media coverage presence. Second, it indicates the presence of sentiment effects.

We test whether the companies exposed to the intense media coverage are more affected by the Ebola outbreak events than the ones receiving less media exposure. The stock price reactions to the events are stronger for securities that are exposed to intense media coverage (see Panel A and Panel B of Table 5 ). In particular, the regression coefficients for the dummy variable EL l, t indicating the day of the event in different regions are higher for the securities exposed to the intense media coverage than for securities without the intense media coverage.

Table 5.

Intense media coverage effects on company securities.

The table reports the results of the following regression:

ri, t = γo + ∑j = 15γ1, jri, t − j + ∑k = 14γ2, kWDk, t + γ3Taxt + ∑l = 13γ4, lELl, t + εt,

where ri, t is the rate of return of stock i on day t with exposure of its operations towards the U.S., the WAC region, Europe, or All regions, γ0 is the regression intercept, ri, t − j is the lagged dependent variable—the jth previous day rate of return, WDk, t with k = 1, …, 4 are dummy variables for the day of the week (Monday, Tuesday, Wednesday, and Thursday), Taxt is a dummy variable for the first five days of the taxation year, and ELl, t with l = 1, 2, and 3, are dummy variables that denote the location where the event happened and equal 1 on the event day if the event happened in a specific region (either in the U.S., the WAC region, and Europe), and zero otherwise. The events occurred during the 2014–2016 Ebola outbreak period (3-year period) and include a total number of 103 event days of the disease outbreak. From the total number of events, 52 took place in the WAC region, 31 in the U.S., and 20 in Europe. Panel A depicts the regression results from the events and stocks without the intense media coverage (as in Panel A of Table 1) whereas Panel B depicts the regression results of the stocks with intense media coverage. The first line reports the regression coefficients whereas the second line reports the corresponding t-values (in brackets). One, two, and three asterisks indicate a significance level of 10%, 5%, and 1%, respectively.

| Panel A: regression results from events without intense media coverage | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Exposure of the company to | γ0 | Rt − 5 | Rt − 4 | Rt − 3 | Rt − 2 | Rt − 1 | Mon. | Tue. | Wed. | Thu. | Tax | U.S. | WAC | Europe | R2 |

| U.S. only | − 0.0143 (− 3.002⁎⁎⁎) |

0.0129 (1.611) |

− 0.0132 (− 0.923) |

0.0283 (1.386) |

− 0.0111 (− 1.783⁎) |

0.0103 (3.448⁎⁎⁎) |

− 0.0231 (− 1.976⁎⁎) |

− 0.0133 (− 1.252) |

− 0.0160 (− 0.019) |

− 0.0211 (− 1.213) |

0.0285 (1.989⁎⁎) |

− 0.0259 (− 3.126⁎⁎⁎) |

− 0.0163 (− 1.645⁎) |

− 0.0155 (− 1.591) |

0.4253 |

| WAC region | − 0.0522 (− 2.752⁎⁎⁎) |

0.0134 (1.604) |

− 0.0148 (− 1.110) |

0.0264 (1.113) |

− 0.0127 (− 1.887⁎) |

0.0118 (3.293⁎⁎⁎) |

− 0.0382 (− 1.691⁎) |

− 0.0223 (− 0.767) |

− 0.0122 (− 0.238) |

− 0.0103 (− 1.327) |

0.0226 (1.663⁎) |

− 0.0257 (− 2.108⁎⁎) |

− 0.0261 (− 1.970⁎⁎) |

− 0.0204 (− 1.690⁎) |

0.5811 |

| Europe | − 0.0251 (− 1.969⁎⁎) |

0.0153 (0.441) |

− 0.0125 (− 1.019) |

0.0245 (1.250) |

− 0.0102 (− 1.665⁎) |

0.0101 (1.959⁎⁎) |

− 0.0201 (− 1.675⁎) |

− 0.0115 (− 1.116) |

0.0150 (0.988) |

− 0.0118 (− 1.235) |

0.0150 (1.717⁎) |

− 0.0183 (− 1.987⁎⁎) |

− 0.0121 (− 1.687⁎) |

− 0.0188 (− 1.966⁎⁎) |

0.3736 |

| All | − 0.0308 (− 1.977⁎⁎) |

0.0172 (0.071) |

− 0.0136 (− 0.420) |

0.0251 (0.532) |

− 0.0114 (− 1.816⁎) |

0.0099 (3.688⁎⁎⁎) |

− 0.0212 (− 2.001⁎⁎) |

− 0.0254 (− 1.221) |

0.0154 (0.350) |

− 0.0170 (− 1.166) |

0.0288 (1.842⁎) |

− 0.0232 (− 2.020⁎⁎) |

− 0.0229 (− 1.965⁎⁎) |

− 0.0157 (− 1.780⁎) |

0.2332 |

| Panel B: regression results from events with intense media coverage | |||||||||||||||

| U.S. only | − 0.0283 (− 3.132⁎⁎⁎) |

0.0236 (1.429) |

− 0.0217 (− 0.910) |

0.0238 (1.268) |

− 0.0213 (− 1.736⁎) |

0.0210 (3.136⁎⁎⁎) |

− 0.0263 (− 1.988⁎⁎) |

− 0.0126 (− 1.200) |

− 0.0282 (− 1.019) |

− 0.0341 (− 1.234) |

0.0332 (1.974⁎⁎) |

− 0.0302 (− 3.122⁎⁎⁎) |

− 0.0291 (− 1.992⁎⁎) |

− 0.0258 (− 1.647⁎) |

0.4146 |

| WAC region | − 0.0538 (− 2.334⁎⁎) |

0.0375 (1.436) |

− 0.0249 (− 1.519) |

0.0346 (1.131) |

− 0.0319 (− 1.935⁎) |

0.0315 (1.958⁎) |

− 0.0390 (− 1.661⁎) |

− 0.0205 (− 1.272) |

− 0.0211 (− 0.105) |

− 0.0321 (− 1.207) |

0.0271 (1.675⁎) |

− 0.0349 (− 3.011⁎⁎⁎) |

− 0.0352 (− 1.971⁎⁎) |

− 0.0216 (− 1.652⁎) |

0.3395 |

| Europe | − 0.0327 (− 1.962⁎⁎) |

0.0254 (0.430) |

− 0.0221 (− 0.013) |

0.0354 (1.223) |

− 0.0207 (− 1.726⁎) |

0.0202 (1.923⁎) |

− 0.0227 (− 1.773⁎) |

− 0.0121 (− 1.156) |

0.0217 (1.018) |

− 0.0436 (− 1.255) |

0.0235 (1.717⁎) |

− 0.0215 (− 2.738⁎⁎⁎) |

− 0.0223 (− 2.104⁎⁎) |

− 0.0239 (− 1.668⁎) |

0.3217 |

| All | − 0.0320 (− 1.976⁎⁎) |

0.0291 (1.301) |

− 0.0218 (− 1.146) |

0.0315 (1.138) |

− 0.0245 (− 3.128⁎⁎⁎) |

0.0105 (3.207⁎⁎⁎) |

− 0.0231 (− 2.120⁎⁎) |

− 0.0265 (− 0.134) |

0.0252 (1.058) |

− 0.0431 (− 1.186) |

0.0260 (1.826⁎) |

− 0.0341 (− 1.962⁎⁎) |

− 0.0337 (− 1.985⁎⁎) |

− 0.0264 (− 1.802⁎) |

0.2931 |

To check for the persistency of the media effect, we employ the regression analysis in Eq. (4). The results are presented in Table A.14 in the Appendix. We find that the regression coefficients are higher for the events with the intense media coverage than for the events without intense media coverage, but the persistency of the effect is the same. These results support the role of the intense media coverage but also highlight possible sentiment effects.

On the one side, the Ebola outbreak events were publicly available on the day of the event and were absorbed in the market. On the other side, there is a persistence of the effect on the days following the event day. On these days, when the media is usually flooded with information on possibly disastrous causalities accompanied with live streaming and pictures, we detect a negative effect but of a smaller magnitude.

Table A.9 in the Appendix presents the results of the event study methodology that observe the impact of the intense media coverage on securities' performance around the event dates. Trading volume as a proxy for trading intensity shows an erratic behavior one day before the event day and up until three days after the event. Past research documents that unexpected and high-consequence events contribute to the trade turbulence in the markets increasing the volume of trades exponentially (Peress, 2014). The coefficients of the proxies for stock variability and liquidity—the price range and the bid-ask spread—increase only on the day of the event and they trend downward subsequently. This is consistent with our hypothesis that intense media coverage significantly affects stock returns, trading volume, stock liquidity, and stock variability and corroborates the results by Fang and Peress (2009).

To sum up, our results support the view that not only the event but also the intensity of the media coverage induces the effect in the stock market. The collective fear and shock of the disastrous event amplify the consequences of the event itself.

6. Concluding remarks

In this research, we find that the 2014–2016 Ebola outbreak events are followed by negative returns in the financial markets. Motivated by the studies showing that extreme events (e.g., aviation disasters, international sporting games, newspapers strikes; see Kaplanski and Levy, 2010a, Kaplanski and Levy, 2010b, Edmans et al., 2007, and Kaplanski and Levy, 2010a, Kaplanski and Levy, 2010b; Edmans et al. 2007, and Peress, 2014) may impose a strong transitory decline in the financial markets which is very different from the direct economic loss, we look for an explanation in the realm of behavioral finance. Indeed, behavioral finance studies show that the media coverage of drastic events such as Ebola outbreak events can enhance anxiety, bad mood, and fear which may induce risk aversion and pessimism among the investors.

We confirm that the geographic proximity of the information to the financial markets increases the importance of the event (related to the 2014–2016 Ebola outbreak) and its impact on companies' stock returns. We find that the event effect is present in all regions of interest. It is larger and statistically significant for the companies with exposure of their operations to the U.S. only and the WAC region as well as for the events located in these two regions, than for the events located in Europe and for the companies with exposure of their operations to Europe. Additional tests on the event effects reveal that the market sentiment has a larger effect on more volatile stocks, stocks with highly subjective valuations, stocks of small firms, and stocks of firms belonging to specific industries.

It is possible that the bad mood and anxiety induce an increase in the degree of risk aversion. We find that the implied volatility, as reflected through VIX and VXO, significantly increases on the day of the event, which may imply that the Ebola outbreak events also affect investors’ perceived risk. In addition, we observe persistence of the effect on the first day following the event day whereas we observe no return to the prevailing average value before the event. This result provides evidence that fear and anxiety, rather than rational behavior, affect investor decisions in the context of the Ebola outbreak.

Furthermore, we observe the relationship between the mass media and communication of risks. Our research confirms findings from the past research that high-consequence and low-probability events, such as the Ebola outbreak events, are overemphasized in the media and create sentiment effects. We find that the event effect is stronger for securities that are exposed to the intense media coverage compared to securities less covered in the media.

We can conclude that the media-driven pessimism and optimism—induced by the Ebola outbreak events—can significantly influence investors' decision-making process when investing in companies of different capitalization size and industry of operation.

The authors would like to thank Nuria Alemany, Igor Lončarski, Vasja Rant, Aleksandar Šević, Aljoša Valentinčič, and the participants at the 15th INFINITI Conference on International Finance in Valencia, Spain for their valuable comments and suggestions. Riste Ichev acknowledges co-financing by the University of Ljubljana, nr. 704-8/2016-110. All errors remain our own.

Supplementary data to this article can be found online at https://doi.org/10.1016/j.irfa.2017.12.004.

WAC region: Liberia, Guinea, Sierra Leone, Nigeria, Mali, and Senegal.

Printed and online subscription coverage on a national level is considered. http://www.cision.com/us/2014/06/top-10-us-daily-newspapers/.

WHO: Ebola response Roadmap Situation Report. http://apps.who.int/

Calculated from the stock market index whose elements are weighted in reference to the market value of companies’ outstanding shares.