Abstract

In sub-Saharan Africa, accessibility to affordable quality care is often poor and health expenditures are mostly paid out of pocket. Health insurance, protecting individuals from out-of-pocket health expenses, has been put forward as a means of enhancing universal health coverage. We explored the utilization of different types of healthcare providers and the factors associated with provider choice by insurance status in rural Nigeria. We analysed year-long weekly health diaries on illnesses and injuries (health episodes) for a sample of 920 individuals with access to a private subsidized health insurance programme. The weekly diaries capture not only catastrophic events but also less severe events that are likely underreported in surveys with longer recall periods. Individuals had insurance coverage during 34% of the 1761 reported health episodes, and they consulted a healthcare provider in 90% of the episodes. Multivariable multinomial logistic regression analyses showed that insurance coverage was associated with significantly higher utilization of formal health care: individuals consulted upgraded insurance programme facilities in 20% of insured episodes compared with 3% of uninsured episodes. Nonetheless, regardless of insurance status, most consultations involved an informal provider visit, with informal providers encompassing 73 and 78% of all consultations among insured and uninsured episodes, respectively, and individuals spending 54% of total annual out-of-pocket health expenditures at such providers. Given the high frequency at which individuals consult informal providers, their position within both the primary healthcare system and health insurance schemes should be reconsidered to reach universal health coverage.

Keywords: diaries, healthcare utilization, provider choice, health insurance, Nigeria

Introduction

In sub-Saharan Africa, access to good quality health care is often limited and financial constraints are a major barrier to seeking health care (World Health Organization and World Bank, 2017). More than one-third of total healthcare expenditures are financed out of pocket by patients (World Bank, 2019), pushing many individuals below the poverty line (Wagstaff et al., 2018). Consequently, individuals regularly seek care at informal providers who often provide low-cost but also low-quality health care (Sudhinaraset et al., 2013). To decrease morbidity and mortality, health system improvements are needed that focus on improving the quality and accessibility of care (Kruk et al., 2018). This includes access to health insurance programmes, which can contribute to universal health coverage (UHC) by providing financial protection (World Health Organization, 2012), access to improved quality health care (Gustafsson-Wright and Schellekens, 2013) or both.

Nigeria, the most populous country in sub-Saharan Africa (World Bank, 2019), has among the highest out-of-pocket health expenditures and the poorest health indicators in the world (World Health Organization, 2018). The Nigerian government has shown commitment to achieve UHC (World Health Organization, 2014), which means that the population should have access to good quality health services and protection from financial hardship, mainly through avoiding high out-of-pocket payments (World Health Organization, 2012). Nevertheless, in 2016, 75% of health expenditures were paid out-of-pocket (World Health Organization, 2019) and <5% of the population was enroled in the National Health Insurance Scheme (Odeyemi, 2014; Uzochukwu et al., 2015). Large disparities in health status and access to affordable and quality health care exist across the country, particularly in rural areas (Chankova et al., 2006; Onwujekwe et al., 2011; Okpani and Abimbola, 2015). In addition, as in other sub-Saharan African countries, informal medicine vendors are the important provider of health services for rural and low-income populations (Beyeler et al., 2015; Prach et al., 2015; Liu et al., 2016; Durowade et al., 2018), but they are rarely covered through insurance schemes.

To enhance UHC in Kwara state, its government introduced the Kwara State Health Insurance (KSHI) programme, a private subsidized health insurance scheme. The KSHI aims to strengthen both healthcare demand, by providing access to subsidized health insurance, and supply, by upgrading and monitoring the quality of health care at the facilities linked to the KSHI. The objective of this article is to obtain a better understanding of healthcare-seeking behaviour and provider choice among individuals with access to the KSHI programme, including the choice to seek health care from informal providers, to gain insights in the question how the expansion of health insurance among vulnerable groups and low-income populations can affect UHC.

To that end, we use ‘health diaries’ data that capture an individual’s illnesses, injuries, healthcare utilization and health expenditures on a weekly basis (Collins et al., 2010; Janssens et al., 2018). Healthcare utilization is often studied based on household surveys that collect data with relatively long recall periods. Such surveys are especially likely to capture catastrophic health episodes, which are more easily recalled after several months. Less severe health episodes, for which care is not sought, or sought at informal providers, are more likely forgotten and underreported. Weekly surveys instead can provide granular insights into the full extent of healthcare utilization (Geng et al., 2018), and we therefore expect to capture a larger number of health episodes compared with household surveys with longer recall periods (Bhandari and Wagner, 2006; Das et al., 2012). The diaries can thereby provide a more detailed picture of an individual’s healthcare utilization and particularly insights in the role of informal medicine vendors in the primary health system, without a recall bias confounding our findings. As such, the results of this study are relevant for health policymakers and health insurance programmes aiming to expand UHC and accessibility to healthcare services in resource-limited settings.

Key Messages

This article analyses healthcare-seeking behaviour and provider choice using year-long weekly health diaries data for a sample of insured and uninsured individuals in rural Nigeria.

Insurance coverage was associated with significantly higher utilization of formal and better-quality health care.

Visits to informal providers, mainly patent and proprietary medicine vendors, represented a large share of total health visits and out-of-pocket health spending even among the insured.

To reach universal health coverage, the prominent role of informal providers within primary healthcare systems and their position in health insurance schemes should be reconsidered.

Materials and methods

Study population

Since 2007, the Kwara State Government gradually rolled out the KSHI together with health maintenance organization Hygeia Ltd, the Health Insurance Fund and the PharmAccess Foundation. Kwara state hosts mostly rural communities and is the fourth poorest state in Nigeria (Gustafsson-Wright and Schellekens, 2013). Healthcare facilities linked to the KSHI were upgraded and subjected to quality monitoring by SafeCare, a quality improvement programme developed by the PharmAccess Foundation (Johnson et al., 2016; Safe Care, 2019). At the time of this study, enrolment in the KSHI was voluntary and on an individual basis. The insurance premium was subsidized at 97%, and the annual co-premium that individuals paid themselves to enrol in the scheme was 300 Nigerian Naira (NGN; 1 USD ≈ 157 NGN, exchange rate 1 April 2012; OANDA, 2019). The benefit package consisted mainly of primary and secondary health care (including human immunodeficiency virus/acquired immune deficiency syndrome treatment and hypertension and diabetes care). In April 2012, approximately 60 900 individuals were actively enroled in the KSHI, which was 47% of the target population. Individual insurance status could change over time since enrolment was on an annual basis and individuals had to actively renew their policy. The annual renewal rate was 58%. The KSHI is described in more detail elsewhere (Hendriks et al., 2014; Gustafsson-Wright et al., 2018).

Study design and sampling

We use data from a Financial and Health Diaries study (Janssens et al., 2018) that was conducted among households who had access to the KSHI programme. The overall aim of the study was to enhance understanding of the healthcare-seeking behaviour and financial lives of households targeted by the programme. The study was conducted in the surroundings of three towns in Edu Local Government Area, Kwara North: Shonga, Bacita and Lafiagi. At the time of the study, the KSHI was linked to one health facility in each of these towns. A total of 16 sampling clusters or areas were selected: one area per town and four to five randomly selected rural areas within a 15-km radius of the town. Within each of these 16 areas, households were randomly sampled and stratified by insurance status prior to data collection. The target sample size was 60 insured households and 60 uninsured households. Within an area, insured and uninsured households were sampled proportional to the size of the insured and uninsured population in the area, respectively. The study protocol was approved by the Ethical Review Committee of the University of Ilorin Teaching Hospital in Nigeria (4 August 2008, UITH/CAT/189/11/782).

Data collection

Prior to data collection, study information was provided in English, Yoruba or Nupe to the sampled households and informed consent was obtained from the household head or most informed household member by written signature or fingerprint. An exploratory qualitative study based on in-depth interviews was conducted in November and December 2011 to gain a detailed understanding of financial and health behaviours in the study area to inform the design of the quantitative research instruments. Data were collected from March 2012 to June 2013 through weekly structured interviews. The total sample of 120 households first completed a baseline survey that included the following themes: household composition, demographics, socio-economic situation, employment and income, health and health insurance, financial assistance and household assets. After this baseline survey, weekly financial and health diaries data were collected for 52 weeks among all financially active adults in the households, both male and female, through private interviews. The financial diaries included themes to gain detailed insights into the financial cash flows within households. This article focuses on the health diaries component, which covered for all household members (both adults and children) every single health episode (any illness or injury) that had occurred in the 7 days prior to each weekly interview. For every health episode, the diaries recorded the start day of the episode, self-reported symptoms, how many days the individual was not able to perform his or her daily activities, whether or not a healthcare provider was consulted, who in the household decided on the consultation, and for each consultation, data were recorded on the day of the consultation, the type of healthcare provider that was consulted, the name of the provider if this was a health facility and how much was spent out-of-pocket on the consultation.

A total of six interviewers received an extensive training followed by a 3-week ‘warm-up’ period for both interviewers and households to get familiar with the study and data collection tool. Because of the low literacy levels in the area, respondents were not asked to keep actual written diaries themselves, but they were personally interviewed on a weekly basis. Households were visited by the same interviewer over the course of the full study period to facilitate rapport building and enhance trust. Data were collected on paper-based questionnaires and entered into a computer-based database by qualified data entrants for the first 3 months. Thereafter, data were collected using laptops. The study team implementing the diaries data collection monitored the data on a regular basis for inconsistencies and outlier values, which was provided as feedback to the interviewers throughout the year. In May–June 2013, an endline survey, comparable to baseline, was conducted. More detailed information on the study can be found elsewhere (Janssens et al., 2015).

Analysis

The analyses focus on healthcare provider choices for unexpected health episodes and unplanned consultations. Consultations for preventive services (antenatal care, health check-up, circumcision, immunization) were excluded from the diaries database. Health episodes with missing data on key variables (individual’s gender and age, health episode type, insurance status and consulted healthcare provider) were excluded from the analyses. Definitions of key variables and concepts are shown in Box 1. We described the household and individual characteristics by using data from the baseline and endline surveys.

Box 1.

Definitions of key concepts and variables

| Health episode | Defined as an illness or injury reported during the weekly interview, which may last, and be reported, for several consecutive weeks. Health episodes are symptoms as described by respondents, without verification of medical records |

| Provider type | Provider choice was classified in four categories:

|

| Insurance status | Insurance status (insured/uninsured) at the time of a health episode was based on weekly administrative data available through the KSHI and Hygeia Ltd |

| Health episode category | We categorized the symptoms using the Global Burden of Disease classification to:

|

| Health episode severity |

|

| Seasonality |

|

| Household location |

|

| Household wealth | Categorized as ‘low’, ‘medium’ and ‘high’, corresponding to the first, second and third terciles of the wealth index generated using principle component analysis on household size, type of housing, and household assets recorded at baseline |

| Out-of-pocket health expenditure | Continuous variables including payments made by the individual per consultation and excluding health insurance premium, transportation costs and medical expenses reimbursed by the insurance |

To evaluate factors associated with individuals’ healthcare provider choice, we constructed a multivariable multinomial logistic regression model adjusted for clustering at the level of a sampling area. Provider choice was classified into the following four categories of increasing quality: no provider (0), informal provider (1), non-upgraded facility (2) and upgraded facility (3), without assuming a linear increase in quality between provider types. The upgraded facilities are the facilities covered by the insurance scheme for individuals enroled in the scheme. In case an individual visited multiple providers for one health episode, we used the healthcare provider with the highest level of quality to define our dependent variable. Thus, we assume that a formal provider was consulted when both formal and informal providers were visited and, in case both upgraded and non-upgraded formal providers were consulted, we categorized this as a visit to an upgraded facility. Variables with missing data, other than the key variables mentioned above, were multiply imputed (N = 10).

The primary exposure variable was insurance status at the time of the health episode. We stepwise (backward and forward) tested health episode variables (type of illness or injury, ability to perform daily activities, season), individual level variables (gender, age, presence of a chronic disease, health-related decision-maker) and household level variables (gender and education of the household head, rural/urban location, household size, household wealth) and included them in the model in case they were significant at the 0.1 significance level. In additional analyses, we explored interactions with insurance status. Data were analysed using STATA version 12.0 (StataCorp LP, College Station, TX, USA).

Results

Study population

Of the 120 sampled households, one household split up during the study, resulting in 121 households included in the analyses. Of the 920 individuals residing in these households, 331 individuals (36%) did not experience a health episode during the study period and were excluded. The remaining 589 individuals reported 1825 episodes, of which 64 episodes (3.5%) and 17 individuals (2.9%) were excluded because of missing data on key variables. As a result, we included in the analyses 572 individuals, residing in 116 households, who reported 1761 episodes (Figure 1).

Figure 1.

Flowchart of the study population included in the analysis

Table 1 shows that 89% of household heads were male and 39% of household heads did not receive any education. Seventy-five percent of households were stratified in rural areas, and the mean household size was 7.2. Of the individuals included in the analyses, slightly more females (55%) participated, 54% of individuals were below 15 years of age, 10% self-reported a chronic disease and 30% self-decided whether to seek health care or not (Table 1). More than one-third (34%) of individuals were insured for at least some time during the 52-week study period. Among the insured, the median duration of insurance coverage during the study period was 41 weeks [interquartile range (IQR): 31–47]. A median of two health episodes (IQR: 1–4) was reported per individual.

Table 1.

Household and individual characteristics

| n (%)/mean (SD)/ median (IQR) | |

|---|---|

| Household level (N = 116) | |

| Gender household head, n (%) | |

| Male | 103 (88.8) |

| Female | 13 (11.2) |

| Education household head, n (%) | |

| No school at all | 45 (39.1) |

| Pre-primary/primary | 22 (19.1) |

| Secondary | 24 (20.9) |

| Tertiary | 24 (20.9) |

| Missing | 1 |

| Household wealth, n (%) | |

| Low | 39 (33.6) |

| Medium | 38 (32.8) |

| High | 39 (33.6) |

| Location, n (%) | |

| Rural | 87 (75) |

| Urban | 29 (25) |

| Household size, mean (SD) | 7.2 (3.6) |

| Individual level (N = 572) | |

| Gender, n (%) | |

| Male | 255 (44.6) |

| Female | 317 (55.4) |

| Age (years), median (IQR) | 11 (4–35) |

| Age group (years), n (%) | |

| <5 | 152 (26.6) |

| 5–14 | 157 (27.4) |

| 15–49 | 211 (36.9) |

| ≥50 | 52 (9.1) |

| Insurance status during diaries, n (%) | |

| Never insured | 377 (65.9) |

| Ever insured | 195 (34.1) |

| Ever insured: duration insured (weeks), median (IQR) | 41 (31–47) |

| Presence of chronic diseasea, n (%) | |

| No | 477 (90.3) |

| Yes | 51 (9.7) |

| Missing | 44 |

| Healthcare-seeking decision-making, n (%) | |

| Someone else decides | 352 (70) |

| Decides self | 151 (30) |

| Missing | 69 |

| Number of health episodes, median (IQR) | 2 (1–4) |

SD, standard deviation; IQR, interquartile range

Self-reported at the endline survey.

Reported health episodes

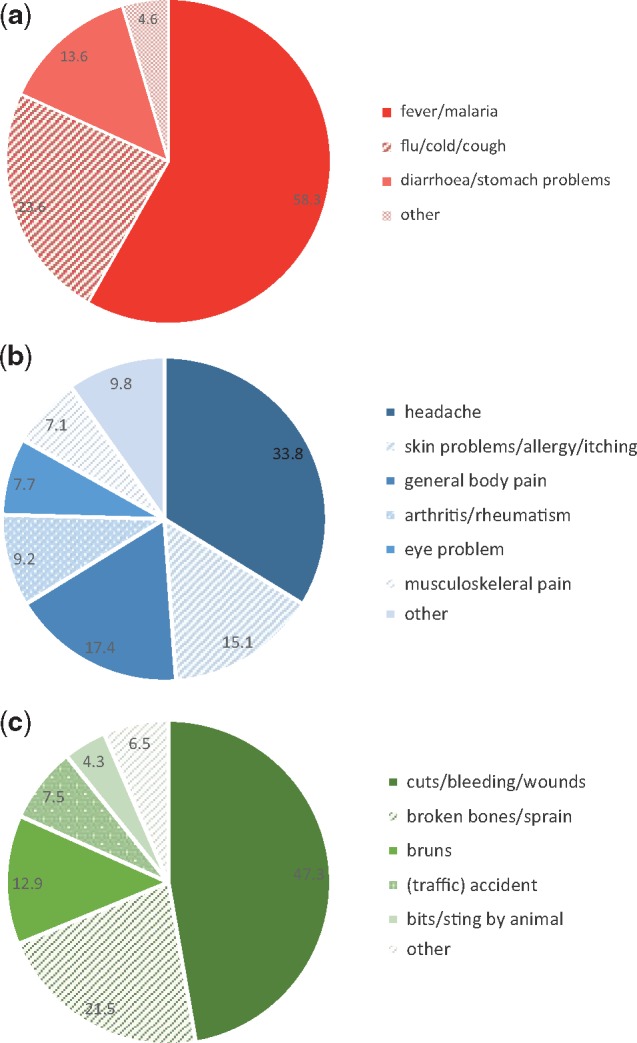

Of the 1761 reported episodes included in the analyses, 1277 (73%) were related to communicable diseases, 391 (22%) were related to non-communicable diseases and 93 (5%) were related to injuries (Table 2). Fever/malaria, headache and cuts/bleeding/wounds were the most frequently reported symptoms in communicable diseases, non-communicable diseases and injury categories, respectively (Figure 2a–c). The types of symptoms were not significantly different between insured and uninsured periods. In 598 of the 1761 (34%) episodes, the individual was insured at the time of the episode (hereafter ‘insured episodes’, Table 2). In 42% of the episodes, individuals were unable to perform daily activities for one or more days, which we use as a proxy for episode severity. Of all episodes, 62% occurred in the wet season, and significantly more often among the uninsured than the insured (64 vs 58%, P = 0.034).

Table 2.

Characteristics of reported health episodes stratified by insurance status at the time of the health episode

| All health episodes (N = 1761) |

Insurance status at time of health episode |

P-value | |||||

|---|---|---|---|---|---|---|---|

| Uninsured |

Insured |

||||||

| N | n (%) | N | n (%) | N | n (%) | ||

| Panel A: health episodes | |||||||

| Type of health episode | 1761 | 1163 | 598 | 0.475 | |||

| Communicable diseases | 1277 (72.5) | 848 (72.9) | 429 (71.7) | ||||

| Non-communicable diseases | 391 (22.2) | 259 (22.3) | 132 (22.1) | ||||

| Injuries | 93 (5.3) | 56 (4.8) | 37 (6.2) | ||||

| Health episode severity | 1761 | 1163 | 598 | 0.904* | |||

| Less severe: able to perform daily activities | 1002 (58.4) | 668 (58.5) | 334 (58.2) | ||||

| More severe: unable to perform activities for ≥1 day | 714 (41.6) | 474 (41.5) | 240 (41.8) | ||||

| Missing | 45 | 21 | 24 | ||||

| Time of health episode | 1761 | 1163 | 598 | 0.034 | |||

| During the dry season | 673 (38.2) | 424 (36.5) | 249 (41.6) | ||||

| During the wet season | 1088 (61.8) | 739 (63.5) | 349 (58.4) | ||||

| Panel B: consultations | |||||||

| Healthcare provider consulted | 1761 | 1163 | 598 | 0.107 | |||

| Yes | 1576 (89.5) | 1031 (88.7) | 545 (91.1) | ||||

| No | 185 (10.5) | 132 (11.3) | 53 (8.9) | ||||

| Number of consultations per episode | 1576 | 1031 | 545 | 0.072 | |||

| 1 | 1456 (92.4) | 959 (93.0) | 497 (91.2) | ||||

| 2 | 101 (6.4) | 57 (5.5) | 44 (8.1) | ||||

| ≥3 | 19 (1.2) | 15 (1.5) | 4 (0.7) | ||||

| Time between reported health episode and first consultation | 1576 | 1031 | 545 | <0.001* | |||

| Same day | 738 (52.5) | 444 (43.1) | 294 (61.9) | ||||

| Next day | 416 (29.6) | 289 (28) | 127 (26.7) | ||||

| Two or more days | 251 (17.9) | 197 (19.1) | 54 (11.4) | ||||

| Missing | 171 | 101 | 70 | ||||

| Number of different provider types consulted | 1576 | 1031 | 545 | 0.392 | |||

| One provider type | 1529 (97) | 1003 (97.3) | 526 (96.5) | ||||

| Two provider types | 47 (3) | 28 (2.7) | 19 (3.5) | ||||

| Type of provider consulted | |||||||

| Informal provider | 1576 | 1203 (76.3) | 1031 | 804 (78.0) | 545 | 399 (73.2) | 0.034 |

| Non-upgraded facility | 1576 | 279 (17.7) | 1031 | 224 (21.7) | 545 | 55 (10.1) | <0.001 |

| Upgraded facility | 1576 | 141 (8.9) | 1031 | 31 (3.0) | 545 | 110 (20.2) | <0.001 |

For categorical variables, P-values were calculated using the chi-square test, and for continuous variables, P-values were calculated using the Wilcoxon–Mann–Whitney test. SD, standard deviation.

P-value was calculated excluding the category ‘Missing’.

Figure 2.

(a) Reported symptoms for health episodes classified as communicable diseases (N = 1277) (b) Reported symptoms for health episodes classified as non-communicable diseases (N = 391) (c) Reported symptoms for health episodes classified as injuries (N = 93)

Healthcare provider consultations

Table 2 (panel B) provides more information on the consultations related to the episodes. In 1576 out of all episodes (90%), a healthcare provider was consulted and, in most of these episodes (92%), providers were consulted once (Table 2). In 1529 episodes (97% of 1576 episodes with a consultation), the individual consulted one type of provider. For 47 episodes (3%), two provider types during the same episode were consulted, 45 of these episodes (96%) involved a combination of a formal and informal provider. For 62% of insured episodes, a provider was consulted on the same day as the reported onset of the episodes, whereas this was 43% among uninsured episodes (P < 0.001). Individuals consulted upgraded facilities in 20% of insured episodes, compared with 3% of uninsured episodes (P < 0.001). Non-upgraded facilities were more often consulted for uninsured episodes than for insured episodes (22 vs 10%, P < 0.001). The same holds for informal providers, which individuals visited for 78% of uninsured episodes and for 73% of insured episodes (P = 0.034). Informal provider visits constituted of patent and proprietary medicine vendors (PPMVs), chemists and drug peddlers (96%) and traditional healers (4%).

Out-of-pocket expenditures

Uninsured episodes were associated with higher mean out-of-pocket health expenditures (717 NGN) compared with insured episodes (576 NGN, Table 3). Mean out-of-pocket health expenditures per episode were the highest at non-upgraded facilities (1593 NGN), followed by informal providers (488 NGN) and upgraded facilities (376 NGN). Mean out-of-pocket health expenditures were significantly different for insured vs uninsured episodes only at upgraded facilities where the insurance scheme provided financial coverage for enrolees (144 NGN vs 1199 NGN, P < 0.001, respectively). Annual individual out-of-pocket health expenditures were the highest at informal providers (1026 NGN) and constitute 54% of total health expenditures. Although the average out-of-pocket healthcare expenditure at informal providers was lower for uninsured episodes, the high frequency of informal provider visits contributed to the large share of annual health expenditures. At non-upgraded and upgraded facilities, yearly individual health expenditures were 777 NGN (41%) and 93 NGN (5%), respectively. Total yearly healthcare expenditures at upgraded facilities were low due to low utilization for uninsured episodes and low out-of-pocket expenditures for insured episodes.

Table 3.

Out-of-pocket health expenditure in the study population (N = 572)

| Total number of health episodesa | Mean expenditure per health episode (NGN) | Mean expenditure per uninsured health episode (NGN) | Mean expenditure per insured health episode (NGN) | P-value (uninsured vs insured)b | Mean expenditure per individual per year (in NGN)c | Proportion of expenditure by provider type over total expenditure (%) | |

|---|---|---|---|---|---|---|---|

| Informal provider | 1203 | 488 | 473 | 518 | 0.217 | 1026 | 54.1 |

| Non-upgraded facility | 279 | 1593 | 1525 | 1872 | 0.282 | 777 | 41.0 |

| Upgraded facility | 141 | 376 | 1199 | 144 | <0.001 | 93 | 4.9 |

| Total | 1623 | 668 | 717 | 576 | <0.001 | 1896 | 100.0 |

Note: medical expenses paid for by the insurance are excluded.

The total number of health episodes excludes 185 health episodes for which no provider was consulted and includes 47 health episodes for which two provider types were consulted. This results in a total of 1623 health episodes.

Calculated using the Wilcoxon–Mann–Whitney test.

We did not calculate the yearly costs for insured and uninsured individuals since insurance status can change over time.

Factors associated with healthcare provider choices

Table 4 presents estimates of a multivariable multinomial logistic regression that models the type of healthcare provider consulted as a function of health episode attributes, individual demographics and household characteristics. Individuals were 10 times more likely to seek care at upgraded facilities compared with not seeking care when experiencing an insured instead of uninsured episode [relative risk ratio (RRR): 10.49], whereas insurance status was not associated with consulting non-upgraded facilities or informal providers. In other words, the demand for informal care was equally high irrespective of insurance status. Wealthier households were more likely to seek care at non-upgraded facilities (RRR: 2.89). The likelihood to visit upgraded facilities was smaller for injuries and non-communicable diseases than for communicable disease episodes (RRR: 0.19 and 0.51, respectively). Episode type was not associated with healthcare utilization at non-upgraded facilities and informal providers. The likelihood to visit upgraded facilities was larger for episodes that occurred in the wet season (RRR: 2.69).

Table 4.

Results of the multinomial logistic regression analysis on factors associated with healthcare provider choices with no provider consulted as reference (N = 1761)

| Informal provider |

Non-upgraded facility |

Upgraded facility |

||||

|---|---|---|---|---|---|---|

| Relative risk ratio | 95% CI | Relative risk ratio | 95% CI | Relative risk ratio | 95% CI | |

| Health episode level | ||||||

| Insurance status | ||||||

| Uninsured | 1.00 | – | 1.00 | – | 1.00 | – |

| Insured | 1.33 | 0.83–2.14 | 0.78 | 0.41–1.46 | 10.49*** | 5.88–18.72 |

| Type of health episode | ||||||

| Communicable | 1.00 | – | 1.00 | – | 1.00 | – |

| Non-communicable | 1.08 | 0.71–1.64 | 0.68 | 0.45–1.03 | 0.51* | 0.3–0.87 |

| Injury | 0.82 | 0.45–1.49 | 0.95 | 0.37–2.41 | 0.19* | 0.05–0.68 |

| Health episode severity | ||||||

| Less severe: able to perform daily activities | 1.00 | – | 1.00 | – | 1.00 | – |

| More severe: unable to perform activities for ≥1 day | 2.19*** | 1.56–3.08 | 8.63*** | 5.57–13.35 | 4.31*** | 2.08–8.94 |

| Season | ||||||

| Dry season | 1.00 | – | 1.00 | – | 1.00 | – |

| Wet season | 1.36 | 0.78–2.39 | 1.13 | 0.57–2.23 | 2.69* | 1.24–5.8 |

| Individual level | ||||||

| Age group | ||||||

| <5 | 1.00 | – | 1.00 | – | 1.00 | – |

| 5–14 | 0.82 | 0.52–1.31 | 0.78 | 0.42–1.47 | 1.83 | 0.8–4.17 |

| 15–49 | 1.15 | 0.7–1.87 | 1.47 | 0.94–2.31 | 1.20 | 0.56–2.6 |

| 50+ | 0.84 | 0.53–1.32 | 0.46 | 0.16–1.3 | 0.63 | 0.23–1.73 |

| Household level | ||||||

| Education household head | ||||||

| No school at all | 1.00 | – | 1.00 | – | 1.00 | – |

| Pre-primary/primary | 0.58 | 0.31–1.05 | 0.25* | 0.08–0.79 | 0.74 | 0.35–1.56 |

| Secondary | 0.69 | 0.41–1.14 | 0.88 | 0.37–2.09 | 0.49 | 0.19–1.24 |

| Tertiary | 0.92 | 0.58–1.46 | 1.21 | 0.55–2.65 | 0.84 | 0.48–1.46 |

| Wealth | ||||||

| Low | 1.00 | – | 1.00 | – | 1.00 | – |

| Middle | 0.83 | 0.52–1.33 | 1.12 | 0.52–2.42 | 1.40 | 0.8–2.46 |

| High | 1.47 | 0.87–2.49 | 2.89* | 1.16–7.22 | 1.02 | 0.52–2.02 |

| Location | ||||||

| Rural | 1.00 | – | 1.00 | – | 1.00 | – |

| Urban | 0.87 | 0.66–1.14 | 0.66 | 0.15–2.9 | 2.04** | 1.36–3.04 |

CI, confidence interval.

P < 0.05,

P < 0.01,

P < 0.001.

Individuals with more severe episodes were more likely to seek care at any provider type compared with individuals with less severe episodes (Table 4). Table 5 shows that the association between episode severity and healthcare provider choice was modified by insurance status. The results show that, for less severe episodes, insured individuals were more likely to seek care at upgraded facilities compared with uninsured individuals (RRR: 23.40). This pattern was not observed for individuals with less severe episodes at non-upgraded facilities and informal providers. For more severe episodes, both insured and uninsured individuals patronize upgraded facilities, but the likelihood was substantially higher among the insured. Healthcare provider choice was not associated with other individual characteristics (gender, age, presence of a chronic disease, and healthcare-seeking decision-maker).

Table 5.

Interaction between insurance status and health episode severity in the multinomial logistic regression analysis with no provider consulted as reference (N = 1761)

| Informal provider |

Non-upgraded facility |

Upgraded facility |

||||

|---|---|---|---|---|---|---|

| Relative risk ratio | 95% CI | Relative risk ratio | 95% CI | Relative risk ratio | 95% CI | |

| Uninsured | ||||||

| Less severe: able to perform daily activities | 1.00 | – | 1.00 | – | 1.00 | – |

| More severe: unable to perform activities for ≥1 day | 2.72*** | 1.76–4.21 | 10.58*** | 6.08–18.41 | 11.87*** | 5.22–26.99 |

| Insured | ||||||

| Less severe: able to perform daily activities | 1.57 | 0.9–2.76 | 0.88 | 0.4–1.95 | 23.4*** | 7.79–70.34 |

| More severe: unable to perform activities for ≥1 day | 2.21* | 1.2–4.06 | 5.1*** | 2.25–11.59 | 51.38*** | 19.12–138.11 |

Covariates included in the multinomial logistic regression model are type of health episode, season, individual’s age group, education of the household head, wealth and location. CI, confidence interval.

P < 0.05,

P < 0.01,

P < 0.001.

Discussion

We used health diaries data, collected for a full year on a weekly basis, to provide a detailed understanding of healthcare utilization among a rural low-income population in the context of a subsidized private health insurance programme aiming to expand UHC. The study targeted a representative sample of households in northern Kwara state, Nigeria. In approximately one-third of observed health episodes, individuals had insurance coverage and could access free health care at three facilities that were upgraded through the KSHI programme. Also, uninsured individuals could access care at these facilities to benefit from the improved quality of care, albeit at a fee.

Our results are partially consistent with previous survey-based studies on the KSHI programme, which show a significant increase in the utilization of formal care among insured individuals in a different region in Kwara state (Bonfrer et al., 2018; Gustafsson-Wright et al., 2018). In our study, higher utilization of formal health care for insured compared to uninsured health episodes was driven by higher utilization of upgraded facilities. Upgraded facilities in the KSHI programme were visited during 20% of insured episodes compared with only 3% of uninsured episodes. Contrary to programme implementers’ expectations, individuals with an uninsured episode did not access the upgraded facilities to benefit from the improved quality care. Since the KSHI is a voluntary insurance with individual enrolment, this could be a selection effect: insured and uninsured individuals may have differed in their propensity to use health care from these upgraded facilities even before the programme, for instance due to differences in access or distance to the facilities, or differences in health status and the type of health care needed (Kramer, 2017; Okunogbe et al., 2018). Alternatively, for the insured, financial coverage through insurance may have been a decisive determinant of provider choice, whereas for the uninsured, the upgrading of facilities and improved quality of care alone did not sufficiently increase the attractiveness of these facilities. Overcrowding of these facilities by the insured, resulting in an associated increase in waiting times and shortage of staff, may have offset any attractive impacts of the improved medical and technical quality at the upgraded facilities (Bonfrer et al., 2018).

Importantly, the design of the diaries study allowed us to generate substantially more granular insights into healthcare utilization for the full set of minor and major health events. We found that even insured individuals mostly accessed care at informal providers. Although average expenditures at informal providers are lower than at formal providers, the higher frequency of informal provider visits drives up the share of total out-of-pocket expenditures spent at such providers. Overall, the study population spent more than half of their total annual out-of-pocket healthcare expenditures at informal providers, which is more than three times the KSHI premium. Utilization of informal providers was only five percentage points lower for insured than for uninsured episodes (73 vs 78%). This is consistent with previous survey-based studies on the KSHI programme, with Bonfrer et al., (2018) and Gustafsson-Wright et al. (2018) finding a reduction of 7.6 and 8.3 percentage points in the utilization of informal care after introducing insurance, respectively. The weekly diaries however estimated that an individual consulted an informal provider 2–3.5 times more often per year than what was reported in the household surveys (Gustafsson-Wright et al., 2018) or other surveys conducted in Nigeria using a 1-month recall period (Onwujekwe et al., 2011; Sudhinaraset et al., 2013; Latunji and Akinyemi, 2018). These findings suggest that surveys, with longer recall periods, underestimate the utilization of informal providers and thus may overstate the impacts of health insurance. In addition, although health expenditures at informal providers are generally not covered by most insurance schemes, the current study shows that annual out-of-pocket expenditures at informal providers represent a major share of total expenditures.

In our study, informal providers were almost exclusively PPMVs, which are widespread in Kwara state (Liu et al., 2016). Individuals often seek primary care at PPMVs for common illnesses and to buy drugs for which formal care may not be necessary (Brieger et al., 2004; Prach et al., 2015). However, more severe conditions, such as fever and malaria, warrant a formal diagnosis and examination by a clinician. Although our study was not designed to assess if provider choice affects patient health outcomes, we found that episode severity was positively associated with healthcare utilization, including an increase in visits to informal providers. This study not only highlights the central role that PPMVs play but also raises concerns regarding the quality of health care that individuals with severe health symptoms receive.

To expand UHC in Nigeria, it seems imperative to rethink the position of PPMVs and strengthen the quality of their services, which are generally not covered by health insurance. Private drug vendors also play an important role in primary health systems of many other sub-Saharan African countries because of convenience, affordability and social and cultural effects (Sudhinaraset et al., 2013). Indeed, a study in rural Kenya showed that individuals consulted private drug vendors despite free access to facility-based health care (Bigogo et al., 2010). On the other hand, out-of-pocket health expenditures are relatively high in Nigeria (World Bank, 2019). Health system analyses may therefore be needed before extrapolating our findings on the utilization of informal drug vendors to other resource-limited settings.

Conditional on basic quality standards, informal providers or PPMVs may be included in health insurance programmes, for instance for the treatment of well-specified less severe illnesses or injuries (Beyeler et al., 2015; Liu et al., 2016; Durowade et al., 2018). Training of PPMVs to perform simple diagnostic tests and procedures could reduce the high burden on health facilities and reduce patients’ travel and waiting time. Coverage of more expensive medication and procedures obtained from PPMVs could increase the attractiveness of health insurance.

At the same time, a challenge for health insurance providers may be the quality of care provided by PPMVs. Although previous studies have successfully engaged drug vendors for the delivery of primary care, interventions are needed to improve their knowledge and practices (Beyeler et al., 2015; Liu et al., 2016). Within the KSHI programme, the quality of care provided within the upgraded healthcare facilities was evaluated and monitored using SafeCare standards. SafeCare developed standards and an assessment methodology to support the improvement of the quality of healthcare facilities in low- and middle-income countries (Johnson et al., 2016; Safe Care, 2019). A similar type of accreditation system could be developed for PPMVs in conjunction with professional boards and organizations, not only in Nigeria (Liu et al., 2016) but also in other settings in sub-Saharan Africa. A first step could be a PPMV self-monitoring tool, which subsequently generates advice for quality improvements.

Another challenge for health insurance providers may be the increase in insurance premiums. Inclusion of non-catastrophic expenditures at PPMVs in health insurance schemes increases expected costs for the insurance provider and thus insurance premiums. Because insurance premiums are typically a multiple of the average or expected insurance payouts, the increase in premiums would be a multiple of the increase in estimated costs. In addition, the information asymmetries that give rise to adverse selection and overutilization of health care are expected to be more pronounced in the case of non-catastrophic illnesses and injuries (Zhang and Wang, 2008; De Allegri et al., 2009; Kramer, 2017), which could potentially increase health insurance premiums even further.

Using weekly diaries data offers advantages compared with standard household surveys that collect data infrequently (Collins et al., 2010; Geng et al., 2018). The granular data allowed us to present a comprehensive overview of healthcare utilization of different provider types, including delays in seeking health care and seasonality of health episodes. Furthermore, the detailed data on out-of-pocket health expenditures per health episode helped demonstrate high annual out-of-pocket health expenditures at informal providers. A Hawthorne effect could be a potential limitation of a diaries approach, in the sense that the weekly interviews may have increased health awareness and changed health behaviour. However, a previous study found no effect of these diaries on financial behaviour (Janssens et al., 2017). A financial diaries study from Uganda also did not observe a change in financial behaviour during the study (Smits and Günther, 2018). Another potential drawback of diaries vs less frequent survey-based data is related to their labour intensity, time intensity and resource intensity. Because of their high frequency, sample sizes in diaries studies are often smaller than in large-scale household surveys, limiting the number of infrequent but catastrophic health events that one can expect to record through diaries data.

To conclude, our study shows that insured individuals with better access to improved quality care and protection against healthcare expenses utilized these benefits only to a limited extent. Utilization of informal providers was high for both insured and uninsured health episodes. In this resource-limited rural setting, informal providers such as PPMVs remain an important source of care even when health insurance is introduced and health facilities are upgraded. The quality improvements of facilities linked to the insurance scheme did not seem to attract uninsured individuals, as their utilization of formal curative care was low. To reach UHC, the position of PPMVs within the primary healthcare system and within health insurance schemes needs to be reconsidered and quality management systems require further development.

Acknowledgements

We gratefully acknowledge the PharmAccess Foundation and the Health Insurance Fund for funding and facilitating our research, as well as the Netherlands Organization for Scientific Research (NWO Veni Grant no. 451-10-002) and the CGIAR research programmes for Agriculture, Nutrition and Health (A4NH) and Policies, Institutions and Markets. We thank Gordon K Osagbemi for excellent coordination of the field team, David Pap and Mike Murphy for outstanding programme and data management, Annegien Wilms and Sicco van Gelder for continuous collaboration and Peju Adenusi from Hygiea Ltd. Most of all, we are grateful for our respondents’ time, patience and dedication to the study.

Conflict of interest statement. None declared.

Ethical approval. The study protocol was approved by the Ethical Review Committee of the University of Ilorin Teaching Hospital in Nigeria (4 August 2008, UITH/CAT/189/11/782).

References

- Beyeler N, Liu J, Sieverding M.. 2015. A systematic review of the role of proprietary and patent medicine vendors in healthcare provision in Nigeria. PLoS One 10: e0117165. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Bhandari A, Wagner T.. 2006. Self-reported utilization of health care services: improving measurement and accuracy. Medical Care Research and Review 63: 217–35. [DOI] [PubMed] [Google Scholar]

- Bigogo G, Audi A, Aura B. et al. 2010. Health-seeking patterns among participants of population-based morbidity surveillance in rural western Kenya: implications for calculating disease rates. International Journal of Infectious Diseases 14: e967–973. [DOI] [PubMed] [Google Scholar]

- Bonfrer I, Van de Poel E, Gustafsson-Wright E, van Doorslaer E.. 2018. Voluntary health insurance in Nigeria: effects on takers and non-takers. Social Science & Medicine 205: 55–63. [DOI] [PubMed] [Google Scholar]

- Brieger WR, Osamor PE, Salami KK, Oladepo O, Otusanya SA.. 2004. Interactions between patent medicine vendors and customers in urban and rural Nigeria. Health Policy and Planning 19: 177–82. [DOI] [PubMed] [Google Scholar]

- Chankova S, Nguyen H, Chipanta D. et al. 2006. A Situation Assessment of Human Resources in the Public Health Sector in Nigeria. Bethesda, MD: Abt Associates Inc. [Google Scholar]

- Collins D, Morduch J, Rutherford S, Ruthven O.. 2010. Portfolios of the Poor: How the World’s Poor Live on $2 a Day. New Jersey: Princeton University Press. [Google Scholar]

- Das J, Hammer J, Sánchez-Paramo C.. 2012. The impact of recall periods on reported morbidity and health seeking behavior. Journal of Development Economics 98: 76–88. [Google Scholar]

- De Allegri M, Sauerborn R, Kouyaté B, Flessa S.. 2009. Community health insurance in sub-Saharan Africa: what operational difficulties hamper its successful development? Tropical Medicine & International Health 14: 586–96. [DOI] [PubMed] [Google Scholar]

- Durowade KA, Bolarinwa OA, Fenenga CJ, Akande TM.. 2018. Operations and roles of patent and proprietary medicine vendors in selected rural communities in Edu Local Government Area, Kwara State, north-central Nigeria. Journal of Community Medicine and Primary Health Care 30: 75–89. 89. [Google Scholar]

- Geng X, Janssens W, Kramer B, van der List M.. 2018. Health insurance, a friend in need? Impacts of formal insurance and crowding out of informal insurance. World Development 111: 196–210. [Google Scholar]

- Gustafsson-Wright E, Popławska G, Tanović Z, van der Gaag J.. 2018. The impact of subsidized private health insurance and health facility upgrades on healthcare utilization and spending in rural Nigeria. International Journal of Health Economics and Management 18: 221–76. [DOI] [PubMed] [Google Scholar]

- Gustafsson-Wright E, Schellekens O.. 2013. Achieving Universal Health Coverage in Nigeria One State at a Time: A Public-Private Partnership Community-Based Health Insurance Model. Washington, DC: Brookings Institution. [Google Scholar]

- Hendriks ME, Wit F, Akande TM. et al. 2014. Effect of health insurance and facility quality improvement on blood pressure in adults with hypertension in Nigeria: a population-based study. JAMA Internal Medicine 174: 555. [DOI] [PubMed] [Google Scholar]

- Janssens W, Kramer B, Swart L.. 2017. Be patient when measuring hyperbolic discounting: stationarity, time consistency and time invariance in a field experiment. Journal of Development Economics 126: 77–90. [Google Scholar]

- Janssens W, Kramer B, van der List M, Lohr C, Langedijk-Wilms A.. 2015. An Overview of the Financial and Health Diaries Study in Nigeria and Kenya. Amsterdam: PharmAccess Foundation.

- Janssens W, Kramer B, van der List M, Pap D.. 2018. Financial and Health Diaries 2012–2013: A year-long weekly panel of farming households in Nigeria and Kenya. Amsterdam: Amsterdam Institute for Global Health and Development; IFPRI.

- Johnson MC, Schellekens O, Stewart J. et al. 2016. SafeCare: an innovative approach for improving quality through standards, benchmarking, and improvement in low- and middle- income countries. Joint Commission Journal on Quality and Patient Safety 42: 350–71. [DOI] [PubMed] [Google Scholar]

- Kramer B. 2017. From awareness to adverse selection: cardiovascular disease risk and health insurance decisions. SSRN Scholarly Paper No ID 2636210. Social Science Research Network, Rochester, NY.

- Kruk ME, Gage AD, Joseph NT. et al. 2018. Mortality due to low-quality health systems in the universal health coverage era: a systematic analysis of amenable deaths in 137 countries. The Lancet 392: 2203–12. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Latunji OO, Akinyemi OO.. 2018. Factors influencing health-seeking behaviour among civil servants in Ibadan, Nigeria. Annals of Ibadan Postgraduate Medicine 16: 52–60. [PMC free article] [PubMed] [Google Scholar]

- Liu J, Prach LM, Treleaven E. et al. 2016. The role of drug vendors in improving basic health-care services in Nigeria. Bulletin of the World Health Organization 94: 267–75. [DOI] [PMC free article] [PubMed] [Google Scholar]

- OANDA. 2019. Currency Converter.

- Odeyemi I. 2014. Community-based health insurance programmes and the National Health Insurance Scheme of Nigeria: challenges to uptake and integration. International Journal for Equity in Health 13: 20. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Okpani AI, Abimbola S.. 2015. Operationalizing universal health coverage in Nigeria through social health insurance. Nigerian Medical Journal 56: 305–10. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Okunogbe A, Kramer B, Pradhan M, de Jager A, Janssens W.. 2018. Health Shocks, Health Insurance, Household Welfare & Informal Coping Mechanisms: Evidence from Nigeria https://yemiokunogbe.com/wp-content/uploads/2018/11/Dissertation_Adeyemi-Okunogbe_Health-Shocks_website.pdf, accessed 23 April 2019.

- Onwujekwe O, Onoka C, Uzochukwu B, Hanson K.. 2011. Constraints to universal coverage: inequities in health service use and expenditures for different health conditions and providers. International Journal for Equity in Health 10: 50. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Prach LM, Treleaven E, Isiguzo C, Liu J.. 2015. Care-seeking at patent and proprietary medicine vendors in Nigeria. BMC Health Services Research 15: 231. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Safe Care. 2019. SafeCare—Basic Healthcare Standards.

- Smits J, Günther I.. 2018. Do financial diaries affect financial outcomes? Evidence from a randomized experiment in Uganda. Development Engineering 3: 72–82. [Google Scholar]

- Sudhinaraset M, Ingram M, Lofthouse HK, Montagu D.. 2013. What is the role of informal healthcare providers in developing countries? A systematic review. PLoS One 8: e54978. [DOI] [PMC free article] [PubMed] [Google Scholar]

- University of Washington. 2019. Global Burden of Disease (GBD). Institute for Health Metrics and Evaluation http://www.healthdata.org/gbd, accessed June 12, 2019. [Google Scholar]

- Uzochukwu BSC, Ughasoro MD, Etiaba E. et al. 2015. Health care financing in Nigeria: implications for achieving universal health coverage. Nigerian Journal of Clinical Practice 18: 437–44. 444. [DOI] [PubMed] [Google Scholar]

- Wagstaff A, Flores G, Smitz M-F. et al. 2018. Progress on impoverishing health spending in 122 countries: a retrospective observational study. The Lancet Global Health 6: e180–92. [DOI] [PubMed] [Google Scholar]

- World Bank. 2019. World Development Indicators https://data.worldbank.org/indicator/, accessed 25 January 2019.

- World Health Organization. 2012. What Is Universal Health Coverage? http://http:/www.who.int/features/qa/universal_health_coverage/en/index.html, accessed 8 April 2019.

- World Health Organization. 2014. Presidential Summit on Universal Health coverage Ends in Nigeria https://www.afro.who.int/news/presidential-summit-universal-health-coverage-ends-nigeria, accessed 12 May 2019.

- World Health Organization. 2018. Key Country Indicators—Data from 2004 to 2017 http://apps.who.int/gho/data/node.cco.latest?lang=en, accessed 30 January 2019.

- World Health Organization. 2019. Global Health Expenditure Database http://apps.who.int/nha/database/ViewData/Indicators/en, accessed 7 April 2019.

- World Health Organization, World Bank. 2017. Tracking Universal Health Coverage: 2017 Global Monitoring Report. Geneva, Switzerland: World Health Organization. [Google Scholar]

- Zhang L, Wang H.. 2008. Dynamic process of adverse selection: evidence from a subsidized community-based health insurance in rural China. Social Science & Medicine 67: 1173–82. [DOI] [PubMed] [Google Scholar]