Abstract

The coronavirus pandemic and the economic crisis in 2020 are accelerating digital transformation. During and after the crisis, there are opportunities and needs for remote work facilities, online services, delivery drones, etc. We discuss how unmanned technologies can cause a long‐term employment decrease, and why compensation mechanisms may not work.

Using the internationally comparable Frey–Osborne methodology, we estimated that less than a third of employees in Russia work in professions with a high automation probability. Some of these professions can suffer the most during quarantine measures; employment in traditional services can be significantly reduced. By 2030, about half of the jobs in the world and a little less in Russia will need to adapt during the fourth industrial revolution because they are engaged in routine, potentially automated activities. In the regions, specializing in manufacturing, this value is higher; the lowest risk is in the largest agglomerations with a high share of digital economy, greater and diverse labour markets. Accelerating technological change can lead to a long‐term mismatch between the exponential increase in automation rate and compensating effects of retraining, new jobs creation and other labour market adaptation mechanisms. Some people will not be ready for a life‐long learning and competition with robots, and accordingly there is a possibility of their technological exclusion. The term “nescience economy” and corresponding assessment method were proposed. Using an econometric model, we identified factors that reduce these risks: human capital concentration, favourable business climate, high quality of life and ICT development. Based on these factors, some recommendations for authorities were proposed in the conclusion.

Keywords: diffusion of innovations; 4th industrial revolution; automation; digital economy; economic crisis; ICT innovations; robots; Russian regions; technological change; technological exclusion, covid‐19

Resumen

La pandemia de coronavirus y la crisis económica de 2020 están acelerando la transformación digital. Durante y después de la crisis, hay oportunidades y necesidades de instalaciones de teletrabajo, servicios en línea, drones de entrega, etc. Se discute cómo las tecnologías no tripuladas pueden causar una disminución del empleo a largo plazo y por qué es posible que los mecanismos de compensación no funcionen.

Utilizando la metodología comparable internacionalmente de Frey‐Osborne, se estimó que menos de un tercio de los empleados en Rusia trabajan en profesiones con una alta probabilidad de automatización. Algunas de estas profesiones pueden ser las que más sufran durante las medidas de confinamiento y el empleo en los servicios tradicionales puede reducirse considerablemente. Para 2030, cerca de la mitad de los puestos de trabajo en el mundo y algo menos en Rusia tendrán que adaptarse durante la cuarta revolución industrial porque realizan actividades rutinarias y potencialmente automatizables. En las regiones especializadas en manufacturas, este valor es más alto; el riesgo más bajo se da en las mayores aglomeraciones con una alta participación en la economía digital, y mercados de trabajo mayores y más diversos. La aceleración del cambio tecnológico puede conducir a un desajuste a largo plazo entre el aumento exponencial de la tasa de automatización y los efectos compensatorios del reciclaje laboral, la creación de nuevos empleos y otros mecanismos de adaptación del mercado laboral. Algunas personas no estarán preparadas para un aprendizaje de por vida y a competir con robots, y por lo tanto existe la posibilidad de una exclusión tecnológica. Se propone el término “economía de la nesciencia” y el correspondiente método de evaluación. Mediante un modelo econométrico, se identificaron los factores que reducen esos riesgos: la concentración de capital humano, un clima empresarial favorable, una alta calidad de vida y el desarrollo de las TIC. Tomando como base estos factores, en las conclusiones se propusieron algunas recomendaciones para las autoridades.

1. INTRODUCTION

Several authors document the beginning of a new industrial revolution, or “industry 4.0” (Hawken, Lovins, & Lovins, 2013; Schwab, 2017) and new techno‐economic paradigm (Pérez, 2003), which features are universal digitalization, robotization (Ford, 2015) and the formation of smart networks. Many of the new technologies are disruptive, capable of completing the development of entire sub‐sectors, and therefore potentially leading to an increase in the level of structural (technological) unemployment. For example, in the USA in the last 10 years there has been an increasing gap between the positive dynamics of labour productivity and stagnant employment (Acemoglu & Restrepo, 2017; Brynjolfsson & McAfee, 2014). This may be partly because of robot development. They are automatic devices intended for carrying out production and other operations previously performed by humans (Rifkin, 1996): complex computer programs (bots), industrial robots, smart homes, smartphones, etc.

According to the previous estimates (Brynjolfsson & McAfee, 2014; Manyika et al., 2017), about half of the jobs in the world can be automated by 2030–2035. The disruption effects on employment predominantly play at the first stage of technological change (Pérez, 2003), then compensation mechanisms operate (Vivarelli, 2014) and capacity to use unskilled labour force grow; jobs will be created in new industries (Berger & Frey, 2015; World Bank, 2016). Therefore, it is important to understand how the threats of automation (The Future of Jobs, 2016) are related to the formation of long‐term technological unemployment and potential social exclusion. Among countries and regions, the automation potential and subsequent social consequences are different (Berger & Frey, 2016a; Manyika et al., 2017).

Previously, each wave of new technologies created more jobs than destroy (Gera & Singh, 2019 ; Kapeliushnikov, 2019; Pérez, 2003; Stewart, De, & Cole, 2015; Vivarelli, 2014). 1 But the speed of the processes did not exceed the life of one generation, therefore, adaptation occurred naturally as older and less adapted generations retired. Before 2020, the thesis of the human labour replacement was considered by some experts as an exaggeration (Gera & Singh, 2019; Kapeliushnikov, 2019). In Russia and most of the developing countries, where the density of industrial robots is several times lower than the world average (IFR, 2019), such discussions were even less supported (Kapeliushnikov, 2019). However, the situation changed dramatically at the beginning of 2020.

The coronavirus pandemic (covid‐19) and the subsequent economic crisis associated with the pandemic and falling oil prices, are accelerating long overdue digital transformation (Vedev, Drobyshevsky, Knobel, Sokolov, & Trunin, 2020). During and after the crises, there will be many opportunities and need for remote work facilities, online services, medical robots‐assistants, delivery drones, Internet of things, industrial robots, etc. As a result of quarantine measures, the demand for traditional personal services (hotels, restaurants, tourism, public entertainment, sport, etc.) (Leibovici, Santacreu, & Famiglietti, 2020) will be reduced several times; employees across the world were transferred to remote and precarious work. Small and medium‐sized businesses will suffer greatly, labour reductions and withdrawal into the informal sector can be significant; large companies and the budget sector may also decline because of the crisis. Moreover, there is little reason to believe that business and people will return to previous offline conditions: remote work gives more opportunities and freedom for creative professionals, and employers save on less demanded specialists. Certainly, employment in offline professions may shrink. Our paper attempts to identify these short‐ and long‐term risks.

The purpose of the work is to raise awareness and intensify scientific discussion about the possible social consequences of digitalization and automation in developing countries with the example of Russia. Our paper suggests methods and describes the results of preliminary assessments. The approach, used in this work, does not solve the problem of predicting these phenomena but may serve in determining the pessimistic scenario. In fact, we set up a thought experiment in our work: what will happen in the Russian regions if simultaneous automation happens, considering existing and emerging technologies? The short‐term effects of the coronavirus pandemic turned out to be quite similar, although so far there is no data to confirm this thesis. It is a natural experiment for testing technologies and the labour market of the future.

The following section describes a possible impact of new technologies on employment in Russia and abroad. Next, we introduced our research methodology. In the results, a preliminary assessment of automation risks in the Russian regions is given. Some recommendations for federal, regional authorities and individuals are proposed in the conclusion.

2. LITERATURE REVIEW

The effect of technological change on employment is devoted to the work of major scientists and thinkers (Pigou, 1933; Ricardo, 1951; Say, 1964 and others). Based on the previous review (Vivarelli, 2014), we can identify several main mechanisms that compensate a decline in employment as a result of new technology implementation. However, every mechanism has its own limitations in modern Russia and may have similar ones in many developing countries.

2.1. Reduced prices

New technologies contribute to lower prices for products, as they increase production efficiency (Pigou, 1933; Stoneman, 1995; Vivarelli, 1995). Lower prices stimulate demand, which leads to an increase in production and employment. An example is Uber and an increase in the number of registered taxi drivers. However, prices fall in perfect competition, which is not the case for most of the Russian markets. The public sector’s share in Russian GDP exceeds 43%, and many markets are monopolized, or their prices are regulated by the state (Abramov, Aksenov, Radygin, & Chernova, 2018).

2.2. Investments

The accumulation of investments in the period between the reduction of costs due to innovation and the subsequent decrease in prices; than it may increase capital investments in production and jobs (Marshall 1961; Ricardo, 1951; Stoneman, 1995). A classic example in Russia is industrialization in the early Soviet period due to enlargement, mechanization of agriculture and the extraction of natural rent. In conditions of high investment risks in modern Russia, investors prefer to withdraw capital abroad. Investments can also be directed to highly automated industries with low employment such as automated production, unmanned vehicles, etc. Almost any new enterprise requires a significantly smaller number of employees.

2.3. Reduction of wages

Reduction of costs by reducing wages, working hours lead to increase in capital investments and new jobs (Pigou, 1933; Venables, 1985). In Russia, there are administrative restrictions on staff cuts, especially during economic crises (Zubarevich, 2015). A similar situation is observed in 2020, when, despite the decline in turnover, enterprises were recommended not to reduce employment. Some of the workers are transferred to underemployment and to the informal sector of the economy (self‐employed), which can hide real problems and slow down the structural adaptation of the labor market.

2.4. Increased incomes

Increased incomes due to growing labour productivity should lead to increased demand and employment in other sectors (Vivarelli, 2014). However, additional incomes can be spent on acquiring foreign durable goods, as well as rise in real estate prices, especially in poor institutional environment. It may have limited impact, including due to possible inflation. Since 2014, an increase in the productivity in Russia was not accompanied by income growth (Barinova & Zemtsov, 2020). In the 2020 crisis, household income and global demand may decline significantly.

2.5. Creation of new products and services

The emergence of new industries, new products and services will lead to increased demand for labour (Aghion & Howitt, 1994; Nelson & Phelps, 1966). Low entrepreneurial and innovative activity in Russia limits the development opportunities for new industries and new products (Zemtsov, Barinova, & Semenova, 2019; Zemtsov & Kotsemir, 2019).

Vivarelli (2014), after conducting a detailed review of econometric studies, notes that process innovations, such as automation, predominantly reduce employment, however there are compensating mechanisms associated with new products, lower prices and higher incomes.

2.6. Automation risks

It is highly relevant to assess the possible risks of automation due to the mentioned above imperfections of the labour markets, especially in times of economic crisis. Previous technological changes have not led to a long‐term increase in unemployment (Kapeliushnikov, 2019; Perez, 2003). For example, the increase in agriculture labour productivity due to mechanization in the former USSR was accordingly compensated by the migration from rural settlements to cities and appearance of new industrial professions. However, as mentioned earlier, the digital transformation has accelerated significantly in the context of the 2020 crisis.

In recent years, dozens of studies have been published to assess the potential automation of workplaces. A start was made by the article (Frey & Osborne, 2017). The authors proposed a function of automation probability for each profession based on three criteria: perception and manipulation, creative (David, 2015) and social intelligence. Several professional groups have a low probability (less than 0.01): doctors, social workers, creative and STEM professions, scientists, mentors and top managers. Among the most vulnerable professions (above 0.99) are: seamstresses, technicians, insurance, tax and tourist agents, bank clerks, librarians, call centre staff, etc. In the US, about 47% of employees are vulnerable, that is, they have a probability higher than 0.7. Many of these professions involve personal contact with clients, while not requiring high social intelligence (Leibovici et al., 2020). Therefore, they may suffer during the crisis transformation in 2020. First, routine, but the most crucial areas, such as logistics and production, were highly automated, now is a time for an increasing number of services, sales, construction, and as a result of artificial intelligence development even science and engineering will be greatly transformed. People’s qualifications and competences are the main factors that may reduce the likelihood of automation. As a long result, personal offline services will be performed only by the best professionals, and only rich people can afford it; most of the services will be online and automated. Other offline businesses that do not succeed or fail to undergo a digital transformation (website, online orders and sales, Internet banking, etc.) are likely to be marginalized.

These processes will have high spatial differentiation. For example, in the USA, the greatest vulnerability is observed in the cities of Las Vegas, Los Angeles and Houston, where the entertainment sphere is developed. The hotel sector, restaurant business, tourism are the most susceptible according to (Frey & Osborne, 2017) and they are most affected during the 2020 crisis (Leibovici et al., 2020). The least vulnerable are Boston, Washington, DC, New York and San Francisco, where R&D, information and communication technologies (ICT), biotechnology and other creative industries are represented (Florida, 2002). In these sectors, the share of remote, non‐permanent employment and digitalization rates were already higher, therefore, the damage from the crisis should be lower, while the market demand for online services is maintained.

Using a similar technique, studies have been conducted in many countries (Table 1). The lower potential of automation in developed countries is associated with a higher digitalization rate (World Bank, 2016) and human capital concentration.

TABLE 1.

Estimates of the proportion of potentially automated workforce, %

The Frey–Osborne approach has been criticized many times, since professions cannot be completely automated. Over the past decades, only a few professions have disappeared from employment classifiers, for example, the profession of a stenographer was officially eliminated in Russia in 2018. Within professions and sectors, labour is redistributed between routine and creative activities. In general, the need for more educated and qualified specialists is growing in the world. Therefore, experts at the McKinsey Global Institute (Chui, Manyika, & Miremadi, 2015; Manyika et al., 2017) analysed 2000 production tasks in 800 US occupations and estimated the proportion of time workers spend on performing routine operations. About 49% of work time can be automated, but only 5% of professions can be fully automated.

According to surveys of top managers and expert polls (Cosbey et al., 2016; Le Clair et al., 2016; The Future of Jobs, 2016), employment in mining, manufacturing, banking services will decrease because of automation. In Russia, according to estimates of the SuperJob recruiting portal, by 2024 about 20% of those employed will lose their jobs, and the unemployment rate may increase to 20–25% by 2022.

In a paper by Acemoglu & Restrepo (2017), data on industrial robots implementations in the United States in 1990–2007 were used to show that increase in the number of robots (one per 1,000 employees) leads to a decrease in the share of employees (0.18–0.4 percentage points), and wages (0.25–0.5) in local labour markets, also considering the impact of imports from other countries, reducing routine work and ICT development. At the same time, estimates of unemployment in the USA do not include the ever‐increasing number of disabled, part‐time and forced retirees (Jordan, 2016).

The reduction and redistribution of employment may not lead to negative social consequences, since the labour market is gradually adapting, the share of non‐routine, creative activity, freelance is increasing, and the share of working time is decreasing (Kapeliushnikov, 2019; Morgan, 2019). The very concept of the natural unemployment rate may disappear. Already by 2016 in Russia, about 88.1% of workers were included in different forms of precarious employment, although significant regional differences persisted (Bobkov, Kvachev, & Novikova, 2018). But with the rapid crisis transformation, the risks of social exclusion increase significantly.

3. RESEARCH METHODS AND DATA

There are three main approaches to assess potential employment automation: analysis of professional groups, share of routine work tasks and expert surveys. The latter were not used for regional estimates because of their high cost and low verifiability. Other methods require strong assumptions about the compliance of routine tasks in the US and other countries’ professions and industries as the author is not aware of initial calculations for developing nations. For preliminary assessments, these methods are applicable, but they do not consider demographic, migration, social and other trends.

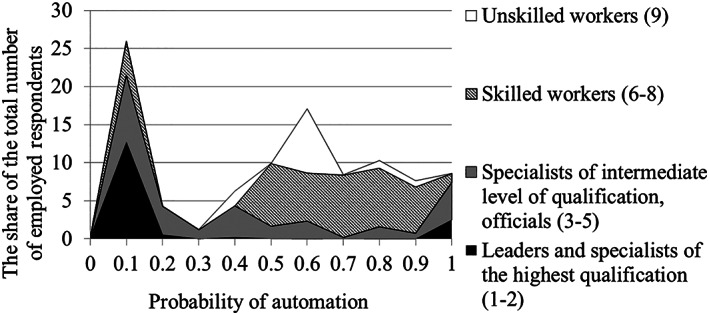

RLMS‐HSE data 2 can be used for Russian case estimates by the Frey–Osborne method (Frey & Osborne, 2017). After comparing classifications from original work (Frey & Osborne, 2017) and RLMS‐HSE data from 18,000 respondents (Zemtsov, 2017), the probability of automation was determined for only 3,325 respondents (Figure 1). As a result, 26.5% of the sampled work in professions that have a high, more than 70%, probability of automation (Table 1). Such professions are among the most‐common in Russia: drivers (7 million people; automation probability estimate ≈98%), sellers (6.8 million people; ≈98%), movers (2.3 million people; ≈72%), cleaners (2.1 million people; ≈83%). Some of these professions could suffer the most during the accelerated business digital transformation in early 2020 (Leibovici et al., 2020). Many businesses transferred their employees to remote work, but in the absence of customers due to quarantine measures, bankruptcy is highly likely. These offline professions will continue to exist, but their employment can be significantly reduced.

FIGURE 1.

Distribution of integrated professional groups (in parentheses are their numbers in the classification of RLMS‐HSE, that is, ISCO‐88) according to the probability of automation

However, there are some doubts about the representativeness of the RLMS‐HSE dataset in relation to the structure of professions in Russia and abroad since it is only 3,325 cases out of 18,000 respondents. Unfortunately, the sample is not representative for regions, and therefore the data is not applicable for the main task.

For regional estimations, the McKinsey Global Institute methodology (Manyika et al., 2017) was applied, which smoothed the shortcomings of the first approach. We used the official data of the Russian statistical service about permanent workers in the formal sector, broken down by regions and economic activities.

The estimates for both approaches (Table 1) show that the potential automation rate in Russia is lower than in most developed and developing countries, although a higher value could be expected due to the low economy complexity and low labour productivity. It can be easily explained since the estimates considered only formal and permanent employment. And it is highly concentrated in the public services sector, education and healthcare, where social and creative intelligence is actively used (Table 2).

TABLE 2.

Assessment of the automation potential for economic activities in Russia

| NACE Rew.2 | Share of potentially automated workforce in economic activity, % | Number of permanent formal employees in 2018, million people | Share of economic activity in formal permanent employment in Russia, % | Number of permanent formal employees by 2030, million people |

|---|---|---|---|---|

| Accommodation and food service activities | 73 | 0.83 | 1.9 | 0.22 |

| Manufacturing | 60 | 6.88 | 15.6 | 2.75 |

| Agriculture, forestry and fishing | 58 | 1.49 | 3.4 | 0.62 |

| Retail trade/wholesale and retail trade; repair of motor vehicles and motorcycles | 53/44 | 5.71 | 12.9 | 2.9 |

| Mining and quarrying | 51 | 0.99 | 2.2 | 0.49 |

| Construction | 47 | 2.41 | 5.5 | 1.28 |

| Transportation and storage | 45.8 | 3.24 | 7.3 | 1.39 |

| Electricity, gas, steam and air conditioning supply | 2.02 | 4.6 | 1.13 | |

| Other service activities | 44 | 0.32 | 0.7 | 0.16 |

| Financial and insurance activities | 43 | 1.03 | 2.3 | 0.59 |

| Arts, entertainment and recreation | 41 | 0.84 | 1.9 | 0.5 |

| Real estate | 40 | 1.41 | 3.2 | 0.85 |

| Public administration and defence; compulsory social security | 39 | 3.44 | 7.8 | 2.1 |

| Information and communication | 36 | 1.09 | 2.5 | 0.7 |

| human health and social work activities | 36 | 4.17 | 9.4 | 2.67 |

| Professional, scientific and technical activities | 35 | 2.11 | 4.8 | 1.37 |

| Administrative and support service activities | 35 | 1.25 | 2.8 | 0.76 |

| Education | 27 | 4.92 | 11.1 | 3.59 |

| All sectors | 44.78 | 44.15 | 100 | 24.08 |

Note: The dark background highlighted the industries, in which the automation potential is higher than the global average; least affected industries are highlighted in italics.

Automation itself does not lead to unemployment, but it increases the need to continuously update knowledge, skills, to be prepared for changes and to maintain creativity. About 80% of employees in Russia are not ready to work in highly competitive, technologically sophisticated markets (Butenko et al., 2017). It is similar in many developing countries as an average employee is engaged in low‐skilled work requiring routine actions and do not seek to improve their skills.

There is a risk that many people will not be able to adapt; therefore, they will be excluded from modern processes associated with the creation, development, and diffusion of new ideas, technologies and products. We proposed to call this new sector “nescience economy” (Zemtsov, 2017, 2018; Zemtsov et al., 2019) as opposed to the “knowledge economy” (Powell & Snellman, 2004). During the pandemic, accelerated digitalization and disappearance of offline businesses are leading to employment reduction and transfer of a substantial part of employees to informal sector in the least developed Russian regions. For example, temporary labor migrants (security guards, sellers, others) massively returned from the largest agglomerations to the rural areas. High digital inequality among the population leads to the exclusion of the least educated and aged residents from the use of many modern services. A low level of trust, especially among this group, reduces the possibility of using new technologies, such as Internet banking, online ordering of goods, electronic payment for housing and communal services, etc. To save employment, it will be necessary to introduce training programmes for computer and digital literacy, retraining programmes for new professions and encourage entrepreneurial initiatives. It is highly possible that governments and the labour market will respond to technological challenges during and after the economic crisis with a delay, since these actions take time and compensating mechanisms are limited in developing countries. That is, there will be a gap between an increasing number of unemployed people and new vacancies (Brynjolfsson & McAfee, 2014).

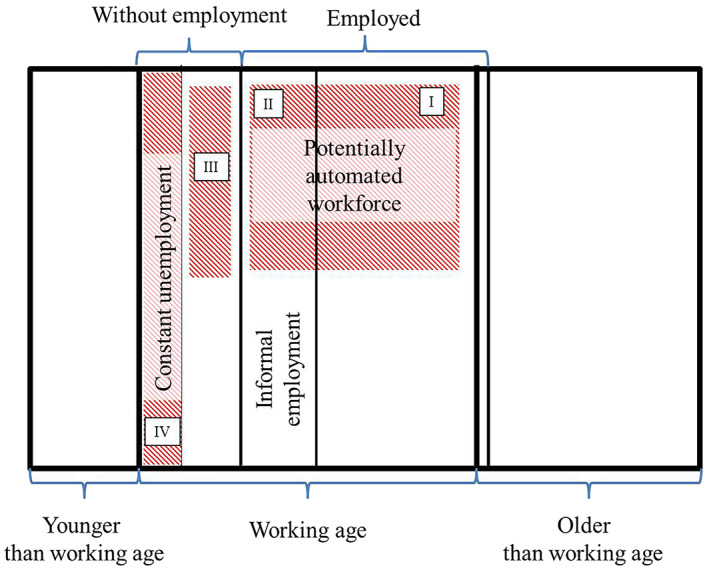

These changes may affect not only permanent workers, but also freelancers and those partially employed in the informal sector, which were not considered in previous calculations. Therefore, we tried to estimate the share of all working age population potentially exposed to and affected by total digitalization and automation (NSE). The high value of this indicator increases risks of social exclusion and the “nescience economy” formation. It was calculated using the following equations: where i is a region; t is the year; NSE is the number of working age people who are vulnerable to technological exclusion because of total digitalization and potential automation (40.8 million people in Russia in 2018); AE is the number of formally employed, subject to total digitalisation and potential automation, million people (I in the Figure 2; 26); AIE is the number of people employed in the informal sector, potentially exposed to total digitalization and affected by potential automation, million people (II; 7.69); ANE is the number of non‐working citizens, who do not consider themselves unemployed, potentially affected by total digitalization and automation, million people (III; 2.93); CUE is the number of permanent unemployed, million people (IV; 4.26).

FIGURE 2.

The structure of population in Russia with potential “nescience economy” (spheres shaded by the background)

At first, we used the share of formally employed (AUT) susceptible to potential total digitalization and automation according to the proposed technique in Table 1 (Manyika et al., 2017): where E is the number of employees, million people (68.39 mln persons); IE is the share of employed in the informal sector, %.

Second, based on the sectoral structure of informal employment, the coefficient of its potential automation (AUT *) was estimated. As expected, its value turned out to be higher than for the formal sector, since the share of trade and other offline services is higher. In the sector, routine labour, based on personal interactions, prevails. For comparison, the share of the informal sector potentially affected by automation is 53% (52.2% for men, 54% for women; 51.9% for citizens, 54.8% for the villagers):

| (3) |

where AIE is the number of people employed in the informal sector, potentially affected by automation, million people.

The number of non‐working citizens who do not consider themselves unemployed (ANE) is calculated by excluding from the working population (WAP), the employed and “permanent” unemployed (CUE) (see explanation below). This category of citizens is very heterogeneous, including students, renters, homemakers, those engaged in subsistence farming, etc., but estimates of possible technological exclusion cannot be lower than for informal workers (AUT*), since many of them do not participate in the creation and development of new technologies:

| (4) |

In our calculations, it is methodologically incorrect to use the current number of unemployed, as it is changing, and people may be in the process of retraining. Therefore, the number of “permanent” unemployed (CUE) was calculated based on the minimum unemployment rate for each region in 1995–2015 according to the International Labour Organization methodology (minUE). It is assumed that minUE will not fall lower during total digitalization and automation; it can be considered natural unemployment rate for the region:

| (5) |

where EAP is labour force (economically active population), mln people (76,588).

The described methodology does not consider demographic (decrease in the share of the working‐age population) and socio‐economic (dynamics of the cost of robots and labour) trends. For more accurate estimates and understanding exclusion factors is necessary conducting specialized sociological surveys.

To identify the factors that may reduce the described risks and to assess adapting strategies for different regions, we formulated several hypotheses based on the literature review.

The most adaptable richer and more educated citizens concentrated in the largest cities, where adaptation capacity is also higher due to a more diverse labour market (agglomeration effects) and greater opportunities for starting a business (McCann & Van Oort, 2019; Zemtsov et al., 2019; Zemtsov & Tsareva, 2018). 3

The higher is the average education level, and accordingly qualification, the faster communities can adapt and create new jobs (Arntz, Gregory, & Zierahn, 2016; Kuzminov, Sorokin, & Froumin, 2019; Zemtsov et al., 2019). Getting new knowledge and skills, including those related to digital technologies, is easier for people with higher education.

The richer regional community, the better its quality of living, the more adaptive it will be, because its residents have a reserve of funds for digital or other retraining, moving, starting a new business, etc. (Arntz et al., 2016; Chang & Huynh, 2016; Frey & Osborne, 2017). In addition, this is an indicator of the regional attractiveness for high‐skilled specialists who will determine regional development during and after the crisis.

Entrepreneurial activity and institutional conditions for the development of small business (Barinova, Zemtsov, & Tsareva, 2018; Bosma, Sanders, & Stam, 2018; Zemtsov et al., 2019) determine the possibilities for creating new areas of employment, realizing the creative potential of residents.

ICT development indicates digital divide rate. ICT contributes to the new markets and the new areas of employment (World Bank, 2016); the higher the digitalization rate in a region, the more adaptive it is. It may also indicate that a certain level of automation has already been achieved, and part of the population has adapted (Baburin & Zemtsov, 2017; Zemtsov et al., 2019).

According to the hypotheses, we proposed an empirical model:

| (8) |

where, dNSE – share of working age population potentially exposed to and affected by automation, which increases risks of social exclusion, %; const – constant; Agglom – urbanization, %; HumCap – human capital: share of urban employees with higher education, %; LifeQuality – income, rubles; EntrInstit – institutions for entrepreneurship: number of small firms per capita; ICT – ICT development: the share of households with internet access, %; Control – control variable: the share of potentially automated workforce (table 3), %.

TABLE 3.

Average values of regional characteristics for several groups

| Group of factors. Affecting automation | Main indicators \ Groups of regions by the share of potentially automated workforce, % | 1. > 46% | 2. 45–46% | 3. 44–45% | 4. 42–44% | 5. < 42% |

|---|---|---|---|---|---|---|

| Economic structure | The share of manufacturing in GRP. % | 27.5 | 19.8 | 17.5 | 9.4 | 5.4 |

| Agglomeration effects and human capital | The share of employed urban citizens with higher education, % (Zemtsov & Kotsemir, 2019) | 9.5 | 10.5 | 11.7 | 12.7 | 5.9 |

| Economic development and quality of life | GRP per capita in constants prices, thousand rubles | 281 | 348 | 628 | 556 | 205 |

| Unemployment rate on average per year. % | 5.08 | 5.13 | 6.19 | 6.34 | 13.1 | |

| Average monthly wage. Rubles | 25.7 | 27.5 | 33.5 | 44.4 | 26.1 | |

| Share of people employed in the informal sector. % | 21.7 | 21.5 | 20.4 | 19.2 | 38.4 | |

| Share of employed in state and municipal organizations, % | 37.7 | 40 | 43.3 | 50 | 69.9 | |

| Entrepreneurship and institutions | The number of small enterprises per capita | 25.5 | 25.1 | 29.5 | 24.5 | 14.5 |

| Investment Risk Index (RAEX) | 0.96 | 0.96 | 1.05 | 1.19 | 1.55 | |

| ICT and new technologies | Share of organizations having a website, % | 43.9 | 43 | 40.7 | 43.2 | 34.7 |

| The number of PCT patent applications for inventions per capita | 3.97 | 4.01 | 4.56 | 6.07 | 2.07 |

To assess agglomeration effects, we used the share of urban residents and the share of regional capital residents as the proper indicators of economic activity concentration and diversity in a region. There are many assessment approaches in the literature: market size, market access, diversification, etc. (De Groot, Poot, & Smit, 2009; Zemtsov & Tsareva, 2018), but it was important to understand how global urbanization trends can reduce social risks of automation as it was during industrialization in the twentieth century (Kapelyushnikov, 2019).

We consider the sum of knowledge, abilities and skills used by regional community in economic activity as its human capital (Becker, Murphy, & Tamura, 1990; Zemtsov et al., 2019; Zemtsov & Kotsemir, 2019). For the assessment, we used the share of employees with higher education, assuming that this is the most productive, skilled and adaptable part of regional communities. Although there are different approaches at the regional level (Faggian, Modrego, & McCann, 2019; Gennaioli, La Porta, Lopez‐de‐Silanes, & Shleifer, 2013), including literacy rates, average years of education, numbers of students, etc. We need to evaluate how the global process of tertiary education spread can reduce the social risks.

To assess wealth and quality of life in a region, we used an average income (Barinova & Zemtsov, 2020). Of course, this is a rather simplified indicator, since the concept of quality of life is more multifactorial, it includes living conditions, happiness, life expectancy, etc. Using the mean instead of the median does not consider inequalities within the region. However, this is enough for our task of rough assessing the impact of residents’ incomes, their accumulated capital, on the ability to adapt to technological changes. On average, the income level of residents in most countries grew after the 2008 crisis (Alvaredo, Chancel, Piketty, Saez, & Zucman, 2018), although the growth rate decreased significantly, and in many poorly developed regions it became negative. For example, in Russia average incomes have been declining since 2014 despite the slow GDP growth (Barinova & Zemtsov, 2020).

We examined the density of small business to assess business environment, regional attractiveness for investors, residents, and accordingly its adaptability (Barinova et al., 2018; Zemtsov et al., 2019; Zemtsov & Tsareva, 2018). It also measures involvement of the community in new products creation. Entrepreneurial activity was growing during the last years due to a sharp decrease in the cost of IT startups, creating Internet platform development such as Alibaba, AirBnB, Uber, etc. (Burtch , Carnahan, & Greenwood, 2018). In post‐soviet countries, the entrepreneurial activity rate is traditionally lower, and therefore opportunities for reducing social threats are not obvious (Barinova et al., 2018; Barinova, Zemtsov, & Tsareva, 2019; Dheer, 2017). In addition, during the current crisis, small and medium‐sized businesses will suffer significantly, as the restrictions imposed on citizens mobility have reduced demand by 60‐90% in tourism, catering, entertainment sector, trade, construction, etc.

Information technology usage has risen significantly over the past decade, but the rate of digital inequality is quite high in the world and especially in Russia (Baburin & Zemtsov, 2017). It drastically limits the adaptation opportunities for the least developed territories. The digital divide includes inequalities in Internet access, online skills and tangible outcomes of Internet use (Scheerder, van Deursen, & van Dijk, 2017). It not only simply extends traditional forms of inequality, but also may include new forms of social exclusion, especially during the crisis. We use the share households with internet access. To a certain extent, this is also an indicator of new technology implementation in a regional economy. Many other ICT development indicators, such the share of firms with websites, number of personal computers, mobile Internet usage, the share of online services, etc., are highly correlated with the selected one at the regional level. As an example, in Moscow, 87% of households have access to broadband Internet, and less than 68% in the least developed regions of the North Caucasus. But in Moscow, only 50% of respondents used the Internet to order goods and services, and less than 15% in Dagestan. Even in Moscow, almost 50% of firms did not place orders online, and for example, in Dagestan, more than 80%.

4. RESULTS

4.1. Potential employment automation

The most vulnerable to potential automation in Russia are hotel and restaurant industries (73% of permanent employees), manufacturing (60%), agriculture and forestry (58%), retail (53%), and the least potentially automated are education (27%), ICT, R&D (35%) and healthcare (36%) (Table 2). Until 2020, even in hotels and restaurants, the automation rate was low, since most of them were working for local markets and there are a lot of non‐routine actions, personal communication, especially in the most expensive establishments. But the pandemic and the economic crisis will lead to increased competition and need for further digital transformation for survival. Robotic hotels, automated cooking, and dron grocery delivery are among the most sought‐after technologies during the pandemic.

According to our estimations, around 44.8% (19.8 million) of permanent formal employment in Russia may suffer from potential digitalization and automation (Table 2), which is lower or comparable with most of developed countries (Table 1). In Russia 34% of employees work in industries that are potentially more than 50% susceptible to automation (Table 2). Accommodation and food services, some manufacturing (automotive and aviation industries) and offline retail trade may suffer greatly during the crisis. If the described trends are realized, then by 2030 in Russia there will be a different structure of the economy with a significantly smaller number of formal permanent employees, about 20 million people out of 75 million workforce, and a higher share of tertiary and quaternary sectors (last column in the Table 2). Fortunately, a significant part of the population is already engaged in more digitalized and less potentially automated sectors: ICT, education, online services, health care and public administration (Gimpelson & Kapeliushnikov, 2015). These knowledge‐intensive sectors can grow even during pandemic and crisis; digital, medical and online services, distance education, public services are still and even more required.

The differences between the regions is more than 10%: the maximum value is 47.6% in the industrial Leningrad Region, nearby St. Petersburg, with advanced automotive industries (“Toyota,” “General Motors,” “Nissan,” “Hyundai” and “Ford” factories); the minimum is 37.1% in the least developed Republic of Tyva, in the central part of Eurasia, with large public and informal sectors. As in the case with countries, it does not exceed the inter‐sectoral differences (Table 2).

About 30% of the total number of potential technological unemployed is concentrated in the largest regions (Zemtsov, 2017): Moscow (2 million people; 43.1%); St. Petersburg (0.9; 44.2); Moscow region (0.94; 45.5), Sverdlovsk (0.7; 46) region; Krasnodar Territory (0.64; 45.1) and Tatarstan (0.6; 45.9). An increase in their numbers in the previous decade was observed as a result of a growing retail and agriculture sector employment in the least developed regions (Ingushetia, Chechnya), growth of the manufacturing industry due to attraction of relevant foreign investors into proactive regions (St. Petersburg, Novosibirsk, Kaluga, Tyumen and Belgorod regions) and expansion of oil and gas industries in northern territories (Nenets and Yamalo‐Nenets autonomous districts). Table 3 presents average indicators characterizing several groups of regions, identified according to their automation risks 4.

The highest share of the manufacturing industry in the GRP is a factor of higher automation susceptibility (> 46%), since the use of industrial robots and unmanned technologies is most common in machine building. Regions with a high share of manufacturing (group 1: Lipetsk, Kaluga, Leningrad, Vladimir regions, etc. (Figure 4)), have lower wages and poorer education, which also increases their vulnerability. But the regions with low level of investment risks and medium entrepreneurial activity can smooth out the effects of robotization (group 2: Perm, Sverdlovsk Voronezh, Yaroslavl, Kaliningrad regions, Tatarstan, etc.). The real unemployment rate is inversely proportional to the level of potential automation, which can be explained by political measures to control unemployment (Zubarevich, 2010). In group 4 with low potential automation rates (42–44%), there are regions with a high levels of development, innovation potential, higher wages and average education level (Moscow, Tomsk region). The lowest indicators of potential automation (<42%) are observed in the least developed regions (group 5: Dagestan, Altai, Tyva, Ingushetia, Chechnya, etc.) with the highest share of the public sector, high unemployment and higher share of informal employment. These are the regions with the least ICT development and innovation potential, and with low human capital concentration. In these regions, the low potential of automation is associated with very backward technological and socio‐economic development.

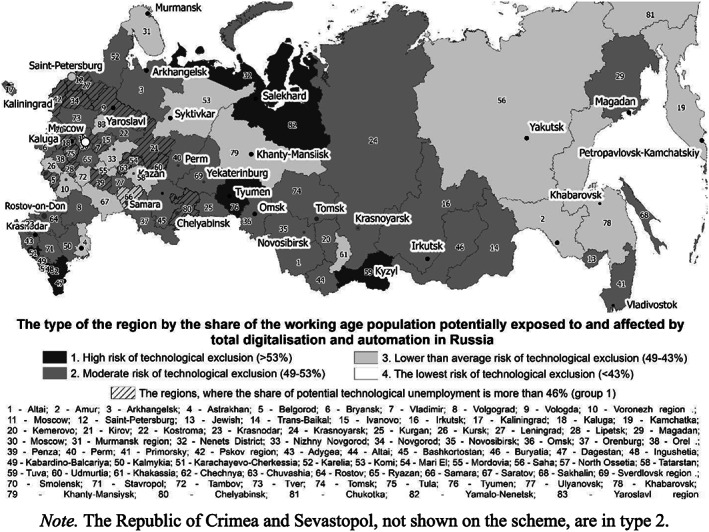

FIGURE 4.

The working age population potentially exposed to and affected by total digitalization and automation in the Russian regions in 2018. Note: The Republic of Crimea and Sevastopol, not shown on the scheme, are in group 2

4.2. Potential technological exclusion

The diffusion of new technologies in Russia may lag in time from developed countries (except global cities like Moscow and St. Petersburg), but then it spreads exponentially (Baburin & Zemtsov, 2017). This is due to low social, technological ties and geographical distances between leading enterprises, novators in the advances regions and lagging regional communities at the initial phase. A similar pattern can be found in other large developing countries such as China, India or Brazil (Comin, Hobijn, & Rovito, 2006). Most regions may not be ready for the increased burden on the social sphere if many working age people are rapidly excluded from economic activity.

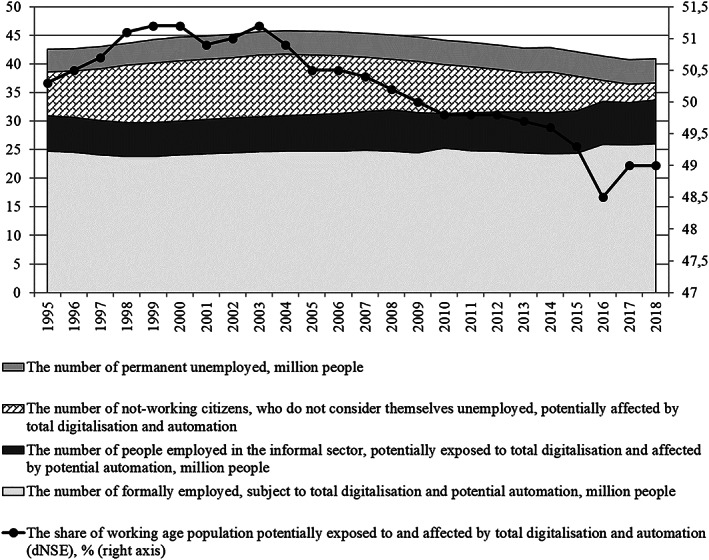

During the last decade, the number of working age population potentially exposed to and affected by future total digitalization and automation in Russia decreased from 45 to 40.8 million people (9.4%), but their share reduced not so significantly: from 50.2% to 49% (Figure 3). There was slow labour market adaptation: older and less prepared generations was leaving; employment in less susceptible to potential automation sectors grew faster: education, ICT, internet‐services, etc. It was a period of fast digitalization of many sectors. At the same time, involvement of the population in economic activity increased as the share of non‐working citizens reduced significantly. However, in the last years, the number of informal employees grew. In 2020, it is expected that their number will increase by several million, as it has already happened in previous crisis periods.

FIGURE 3.

Dynamics of working age population potentially exposed to and affected by total digitalization and automation

The maximum rate of working age population who are vulnerable to technological exclusion is in the least developed southern and mountain regions: Ingushetia (61%), Chechnya (57), Dagestan (54), Karachay‐Cherkessia (53), Tyva (53). These regions are characterized by a low level of general socio‐economic development, a high proportion of the informal sector and rural residents, lower concentration of human capital and the highest digital divide (Figure 4). Due to low formal and permanent employment, low labour costs and backward technological development these same regions have the modest potential for automation, and, accordingly, the lowest prospects for labour productivity growth (group 5 in Table 3). The combination of low opportunities for labor productivity increasing and high social risks can lead to the most dramatic social consequences and the imbalance of regional budgets, which are already largely dependent on federal support.

The highest and growing risks are identified in the northern oil and gas producing regions (Nenets and Yamalo‐Nenets autonomous districts), in which automation potential is high. Many northern settlements during the Soviet period were overpopulated because surcharges were allocated for living in the north. With the collapse of the USSR, these settlements found themselves in a grave social and economic crisis. Now, most of those employed in these regions are shift workers from other territories. The fall in oil prices and mining automation create conditions for the subsequent social exclusion of many permanent and temporary employees. Although automation trends were not so obvious in remote and sparsely populated areas, where oil and gas production require non‐routine actions; creative approach is essential in conditions of scarce, more expensive and inaccessible resources and machines. The risks of social exclusion mostly grew in regions, where the raw material sector was developing rapidly.

The lowest risks for social exclusion as well as potential automation are in the largest agglomeration, Moscow, with a high share of digital economy, greater and diverse labour markets.

We confirmed our hypotheses about several factors (Table 4), affecting “nescience economy” formation and additionally verified the results of the primary comparative analysis (Table 3). Accordingly, it helps to identify the mechanisms to adapt and reduce the possible negative impact of technological change (Zemtsov, 2017, 2018; Zemtsov et al., 2019).

TABLE 4.

Factors affecting the share of working age population who are vulnerable to technological exclusion

| Model | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Constant | 0.84* (0.44) | 0.6 (0.45) | 0.67 (0.44) | 0.59 (0.43) | 0.64 (0.44) |

| The share of regional capital residents, % | −0.06**(0.02) | ||||

| The share of employed urban citizens with higher education, % | −0.03*(0.014) | ||||

| The average incomes(considering cost of living), thousand rubles | −0.001**(0.004) | ||||

| The number of small firms per capita | −0.016*** (0.006) | ||||

| The share of households with internet access, % | −0.006*** (0.002) | ||||

| The share of potential technological unemployment, % | 0.83*** (0.12) | 0.89*** (0.12) | 0.87*** (0.11) | 0.88*** (0.11) | 0.86*** (0.11) |

| R2 | 0.75 | 0.75 | 0.75 | 0.75 | 0.75 |

| Within R2 | 0.13 | 0.14 | 0.14 | 0.16 | 0.13 |

| Schwartz criterion | −3724 | −3736 | −3730 | −3748 | −3727 |

Notes: Panel model with fixed effects. Dependent variable is the share of working age population potentially exposed to and affected by potential total digitalization and automation. 731 observations during 2009–2018. All variables are logarithmic. Robust standard errors are in brackets.

The most significant and the main factors, as expected, were the share of urban employees with higher education (human capital) and the share of regional capital residents: the higher these values, the lower are the risks of potential total digitalization and automation. If the share of capital citizens in a region is 1% higher than in others, then its risks are 0.06% lower. Richer communities are also less vulnerable: if in a region the income is higher by 1% than in others, then its social exclusion risks are lower by 0.001%. Favourable institutional conditions for entrepreneurial activity and a high level of digitalization (households with internet access) are also observed in regions with lower social exclusion risks. In regions with developed manufacturing industries and higher share of potential technological unemployment, the social exclusion risks are higher, as we established earlier (Table 3).

Hereby, the mentioned global trends (urbanization, increasing role of tertiary education, digitalization and entrepreneurial activity growth) helped to reduce the negative consequences of the technological revolution. But the 2020 economic crisis may dramatically cut small and medium‐sized businesses and negatively affect incomes in most of the countries and regions.

5. CONCLUSION AND RECOMMENDATIONS

Our estimations do not give a definite answer to the question of how many people will suffer from the technological changes (total digitalization, automation, etc.). Nevertheless, using our proposed methods helps to evaluate and compare these risks between countries and regions.

Previous technological changes, occurring throughout the life of affected generations, have not led to a long‐term increase in unemployment. Until 2020, the speed of digitalization and automation was slowed down due to economic (high cost of robots and its implementation in comparison with cheep labour), political (fear of social consequences), legal (ban on the introduction of some technologies) and other restrictions. However, the forced digital transformation has accelerated significantly during and after the 2020 crisis.

Competitive businesses around the world go online, transfer many employees to remote work, and introduce new technological solutions. But many small and medium‐sized businesses are threatened with bankruptcy, since demand for their services and goods have repeatedly fallen during quarantine measures. The risk of high unemployment is simultaneously associated with total digitalization and possible temporary extinction of offline personal services: restaurants, hotels, tourism, entertainment, etc. Most of the traditional professions will not disappear, but employment may significantly decrease. In the long term, most common professions are considered potentially highly automated: sellers, security guards, movers, drivers, etc.

According to our estimations, about 44% of permanent employees (≈20.2 million) in the formal sector in Russia need to adapt during total digitalization and the fourth industrial revolution because they are engaged in routine, potentially automated activities. However, this value is lower than the world average due to relatively high share of knowledge‐intensive industries (education, healthcare, finance, ICT), in which social and creative intelligence are important. Also, the share of electronics and mechanical engineering in Russia is generally low, and these industries are among the most susceptible to automation. Corresponding patterns can also be found at the regional level. In the Russian regions, specializing in manufacturing (Kaluga, Leningrad, Vladimir, Lipetsk, etc.), the risk of automation is higher; more than 46% of formal employment are potentially exposed to automation. The lowest risk (<42%) is in the largest agglomerations with a high achieved share of the digital economy: Moscow, St. Petersburg, Kazan, Novosibirsk, Yekaterinburg, etc. Ongoing processes may lead to old industrial and “old service” region formation with a long‐term low permanent employment rate.

The labour markets are gradually adapting (Smith & Anderson, 2014): new products and online‐services, new industries (distance education, telemedicine, biotechnologies, internet of things, etc.), transition from routine to more complex, responsible and creative tasks, precarious work. However, accelerating technological change can lead to a long‐term mismatch between the exponential increase in automation rate, the compensating effect of retraining and new jobs creation. Some people will not be ready for a life‐long learning, development of new ideas, technologies and products, competition with robots, migration, and accordingly there is a possibility of their technological or even social exclusion. The term “nescience economy” was proposed to describe these processes. Social risks do not come from digitalization and automation processes per se, but from the inability and impossibility to adapt. We are talking about the formation of a group of people, using pension and social benefits as a source of income, as well as leading a subsistence economy. This will be a sector of shadow employment, semi‐legal part‐time jobs with no use of modern technologies, low living standards, and high mortality rates.

To assess these risks, we considered total digitalization and automation processes in informal sector and permanent unemployment. The share of the working age population exposed to and affected by potential total digitalization and automation may vary greatly. The maximum rate is in the least developed Russian regions with a low level of technological development, a high proportion of the informal sector and the least adaptable rural residents. In similar countries and regions, there will be double pressure on the budget: there are no internal conditions for productivity growth through automation (low labour cost, no technology or human capital, inefficient institutions) and, consequently, decrease in revenues is possible, but at the same time social exclusion risks during total digitalization are potentially the highest, which greatly increases social expenditures in the future. Our econometric calculations show that the risks of potential technological and social exclusion are lower in highly urbanized Russian regions with a high concentration of human capital, higher incomes, favourable institutional conditions for business development, and developed ICT infrastructure.

Based on the determined factors, several recommendations can be formulated to minimize the described risks.

Crisis is a good time for learning and self‐education. For individuals, it is important to learn how to use digital technologies, to develop soft skills, to stimulate their own social and creative intelligence. In any profession, similar skills will be required, and in the future, say 10–15 years, any work will require interaction with a collaborative robot or digital bot. In general, it is important to be involved in one of areas that are less susceptible to automation: creative industries (research, art), entrepreneurship, STEM (science, technology, engineering and mathematics), social interaction (social workers, teachers, psychologists, etc.); changing conditions (emergency workers); management or mentoring (mentors, clergy, coaches, etc.) (Kuzminov et al., 2019; Zemtsov, 2017, 2018; Zemtsov et al., 2019).

The goals of the state government should include support for retraining and job creation programmes. The expansion of ICT infrastructure (including broadband internet, 5G) will create the conditions for the new industry formation: 3D printing, augmented and virtual reality technologies, telemedicine, internet of things, etc. It is essential to convert all public services into electronic form. During the crisis, it is necessary to support public and private demand for services and products of R&D, ICT, biotechnology and other creative industries, which will become the basis for the formation of a new techno‐economic paradigm (Perez, 2003). According to the national project “Digital economy” in Russia by 2024, it is planned to prepare and graduate more than 270,000 people with key digital competencies; about 10 million people will be trained in online digital literacy programmes. For these purposes, 50 centres for accelerated training will be introduced as a result of private‐public partnership. Nearly 1,500 of the best STEM educational organizations will receive grants for their experience distribution as well as 33,000 students. This is consistent with the new US science education strategy “Charting a course for success: America’s strategy for STEAM education” (Semenova, Zemtsov, & Polyakova, 2019). During the crisis and corresponding budget cuts, it is essential to maintain this program.

For regional and local authorities worldwide, it will be necessary to develop adaptation programmes for the digital economy, which can vary depending on the type of region within the framework of smart specialization and potential threats. In general, programmes may include measures to create continuous STEM and entrepreneurship training systems, including distance education. To create incentives for local authorities, it is necessary to transfer taxes from small and medium‐sized businesses to local budgets (Barinova et al., 2019).

Modern measures to support entrepreneurship can be divided into short‐term and long‐term (Barinova, Zemtsov, & Tsareva, 2020). The short‐term measures, introduced in many countries, are designed to mitigate the negative effects of the pandemic and the crisis: the deferment of payments on taxes, loans and rents, support for consumer demand by issuing subsidies to vulnerable groups of the population (Vedev et al., 2020). Long‐term measures should be focused on adapting to new techno‐economic paradigm. Reducing investment risks by lowering taxes, simplification of procedures (“regulatory guillotine”) (Barinova et al., 2019) will lead to greater opportunities for citizens to participate in entrepreneurial and creative activities. On the one hand, the crisis slowed down the implementation of state projects, on the other hand, the pandemic contribute to accelerated digital transformation of private businesses, therefore, the rapid digitalization of public services, business climate improvement may be more relevant than ever.

For the leading regions such as Moscow, St. Petersburg, Tatarstan, Samara and Novosibirsk, measures are needed to accelerate technology companies in industrial parks, stimulate venture capital concentration in public‐private partnership and increase funding for industry‐related grants for R&D in universities (Pierrakis & Saridakis, 2017; Zemtsov, Eremkin, & Barinova, 2015; Zemtsov & Kotsemir, 2019). It will be necessary to significantly increase funding for education and R&D, as well as to promote distance and dual (industry‐related) education and innovative vouchers to intensify the links between education, science and business (Zemtsov et al., 2015, 2019). For the regions with developed manufacturing, it is advisable to strengthen the interactions between companies and their suppliers, financial institutions, multinational corporations to create and develop local clusters. In the lagging regions, measures are required to train entrepreneurship, legalize informal employment, and consulting (Barinova et al., 2019).

It is likely that the 2020 crisis will be the end of the fifth Kondratieff cycle (Perez, 2003). And we will be facing a new economy during and after new industrial revolution (Industry 4.0). But such crises are usually longer and harder because it will take time to find new technological solutions to accelerate economic growth. A significant structural change towards the knowledge‐based industries may occur; countries and regions that have pursued a proactive innovation policy, formed a high‐tech sector, supported start‐ups, will be able to succeed.

ACKNOWLEDGEMENTS

Earlier versions of this paper were presented at the 59th congress of European Regional Science Association in Lyon, France in August 2019 and IGU Thematic Conference “Practical Geography and XXI Century Challenges” in June 2018 in Moscow, Russia. The author thanks Professors Vyacheslav Baburin and anonymous referees for their constructive comments.

Zemtsov S. New technologies, potential unemployment and ‘nescience economy’ during and after the 2020 economic crisis. Reg Sci Policy Pract. 2020; 12 723–743. 10.1111/rsp3.12286

Footnotes

However, there was a temporary surge in unemployment in certain industries and regions, and accordingly social protests. The most widespread event in history is the Luddite movement in England during the Industrial Revolution (Jones, 2006).

Many young rural residents in Russia have part‐time jobs in large cities in security, trade, construction and other potentially highly automated industries that do not require high qualifications. Recently, the risks of social exclusion for them have increased significantly.

REFERENCES

- Abramov, A. E. , Aksenov, I. , Radygin, A. , & Chernova, M. (2018). The public sector of the Russian economy: It's size and dynamics. Retrieved from https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3211986

- Acemoglu D., & Restrepo P. (2017). Robots and jobs: Evidence from US labor markets. NBER Working Paper 23285.

- Aghion, P. , & Howitt, P. (1994). Growth and Unemployment. The Review of Economic Studies, 61(3), 477–494. [Google Scholar]

- Alvaredo F., Chancel L., Piketty T., Saez E., Zucman G. (Eds.). (2018). World inequality report 2018. Cambridge, MA: Belknap Press.

- Arntz M., Gregory T., & Zierahn U. (2016). The risk of automation for jobs in OECD countries: A comparative analysis. OECD Social, Employment, and Migration Working Paper189.

- Baburin, V. L. , & Zemtsov, S. P. (2017). Modelling of diffusion of innovation and typology of Russian regions: A case study of cellular communication. Izvestiya Rossiiskaya Akademii Nauk, Seriya Geograficheskaya, (4), 17–30. (In Russian) [Google Scholar]

- Barinova, V. , & Zemtsov, S. (2020). Inclusive growth and regional sustainability of Russia. Regional Research of Russia, 10(1), 10–19. [Google Scholar]

- Barinova, V. A. , Zemtsov, S. P. , & Tsareva, Y. V. (2018). Entrepreneurship and institutions: Does the relationship exist at the regional level in Russia? Voprosy Ekonomiki, 6, 92–116 (In Russian). 10.32609/0042-8736-2018-6-92-116 [DOI] [Google Scholar]

- Barinova V. A., Zemtsov S. P., & Tsareva Y. V. (2019). Government support of small and medium sized entrepreneurship in Russia. Russian economy in 2018. Trends and Outlooks (Issue 40). Moscow. IEP. pp. 543–563.

- Barinova, V. A. , Zemtsov, S. P. , & Tsareva, Y. V. (2020). Small and medium enterprises in Russia and regions in 2019–2020. Russian Economy in 2019. Trends and Outlooks (Issue 41) (pp. 279–290). Moscow: IEP. [Google Scholar]

- Becker, G. S. , Murphy, K. M. , & Tamura, R. (1990). Human capital, fertility, and economic growth. Journal of political economy., 98(5), S12–S37. [Google Scholar]

- Berger, T. , & Frey, C. (2015). Industrial renewal in the 21st century: Evidence from US cities. Regional Studies, 51(3), 1–10. [Google Scholar]

- Berger, T. , & Frey, C. (2016a). Did the computer revolution shift the fortunes of US cities? Technology shocks and the geography of new jobs. Regional Science and Urban Economics, 57, 38–45. [Google Scholar]

- Bobkov, V. , Kvachev, V. , & Novikova, I. (2018). Precarious Employment in the Regions of Russian Federation: Sociological Survey Results. Economy of Region, 2(1), 366–379. [Google Scholar]

- Bonin, H. , Gregory, T. , & Zierahn, U. (2015). Übertragung der Studie von Frey/Osborne (2013) auf Deutschland. Kurzexpertise im Auftrag des Bundesministeriums für Arbeit und Soziales. (No. 57). ZEW Kurzexpertise. [Google Scholar]

- Bosma, N. , Sanders, M. , & Stam, E. (2018). Institutions, entrepreneurship, and economic growth in Europe. Small Business Economics, 51(2), 483–499. [Google Scholar]

- Brynjolfsson, E. , & McAfee, A. (2014). The second machine age: Work, progress, and prosperity in a time of brilliant technologies. New York City: WW Norton & Company. [Google Scholar]

- Burtch, G. , Carnahan, S. , & Greenwood, B. (2018). Can you gig it? An empirical examination of the gig economy and entrepreneurial activity. Management Science, 64(12), 5497–5520. [Google Scholar]

- Butenko, V. , Polunin, K. , Kotov, I. , Sycheva, E. , Stepanenko, A. , Zanina, E. , … Topolskaya, E. (2017). Russia 2025: From personnel to talents. The boston consulting group: Moscow. [Google Scholar]

- Chang, J. H. , & Huynh, P. (2016). ASEAN in transformation: The future of jobs at risk of automation. Geneva: ILO. [Google Scholar]

- Chui, M. , Manyika, J. , & Miremadi, M. (2015). Four fundamentals of workplace automation. McKinsey Quarterly, 29(3), 1–9. [Google Scholar]

- Comin D., Hobijn B., & Rovito E. (2006). Five facts you need to know about technology diffusion. National Bureau of Economic Research Working Paper 11928.

- Cosbey, A. , Mann, H. , Maennling, N. , Toledano, P. , Geipel, J. , & Brauch, M. (2016). Mining a mirage. Reassessing the shared‐value paradigm in light of the technological advances in the mining sector. Geneva: International Institute for Sustainable Development. [Google Scholar]

- David, H. (2015). Why are there still so many jobs? The history and future of workplace automation. The Journal of Economic Perspectives, 29(3), 3–30. [Google Scholar]

- De Groot, H. , Poot, J. , & Smit, M. (2009). Agglomeration externalities, innovation and regional growth: Theoretical perspectives and meta‐analysis. In Handbook of regional growth and development theories (pp. 256–282). Cheltenham: Edward Elgar Publishing. [Google Scholar]

- Dheer, R. (2017). Cross‐national differences in entrepreneurial activity: role of culture and institutional factors. Small Business Economics, 48(4), 813–842. [Google Scholar]

- Faggian, A. , Modrego, F. , & McCann, P. (2019). Human capital and regional development. In Handbook of regional growth and development theories (pp. 149–171). Cheltenham: Edward Elgar Publishing. [Google Scholar]

- Florida, R. (2002). The rise of the creative class. New York: Basic Books. [Google Scholar]

- Ford, M. (2015). Rise of the robots: Technology and the threat of a jobless future. New York: Basic Books. [Google Scholar]

- Frey, C. B. , & Osborne, M. A. (2017). The future of employment: how susceptible are jobs to computerisation? Technological Forecasting and Social Change, 114, 254–280. [Google Scholar]

- Gennaioli, N. , La Porta, R. , Lopez‐de‐Silanes, F. , & Shleifer, A. (2013). Human capital and regional development. The Quarterly Journal of Economics., 128(1), 105–164. [Google Scholar]

- Gera, I. , & Singh, S. (2019). Critique of Economic Literature on Technology and Fourth Industrial Revolution: Employment and the Nature of Jobs. The Indian Journal of Labour Economics., 62(4), 715–729. [Google Scholar]

- Gimpelson, V. , & Kapeliushnikov, R. (2015). Polarization or upgrading? Evolution of Employment in Transitional Russia. Voprosy economiki. No., 7, 87–119. (In Russian) [Google Scholar]

- Hawken, P. , Lovins, A. , & Lovins, L. (2013). Natural capitalism: The next industrial revolution. London: Routledge. [Google Scholar]

- IFR . (2019). World robotics. Retrieved from https://ifr.org [Google Scholar]

- Jones, S. (2006). Against technology: From Luddites to neo‐Luddism. London: Routledge. [Google Scholar]

- Jordan, J. (2016). Robots. Boston, MA: MIT Press. [Google Scholar]

- Kapeliushnikov, R. (2019). The phantom of technological unemployment. Russian Journal of Economics, (5), 88–116. [Google Scholar]

- Knowles‐Cutler, A. , Frey, C. , & Osborne, M. (2014). Agile town: The relentless march of technology and London’s response. London: Deloitte. [Google Scholar]

- Kuzminov, Y. A. , Sorokin, P. , & Froumin, I. (2019). Generic and specific skills as components of human capital: New challenges for education theory and practice. Foresight and STI Governance, 13(2), 19–41. 10.17323/2500-2597.2019.2.19.41 [DOI] [Google Scholar]

- Lamb, C. (2016). The talented Mr. Robot. The impact of automation on Canada’s workforce. Brookfield Institute for Innovation + entrepreneurship (BII+E). Toronto: Brookfield Institute for Innovation + entrepreneurship (BII+E). [Google Scholar]

- Le Clair, K. , Gownder, J. , Koetzle, L. , Goetz, M. , Lo Giudice, D. , McQuivey, J. , … Lynch, D. (2016). The future of white‐collar work: Sharing your cubicle with robots. Cambridge: Forrester. [Google Scholar]

- Leibovici, F. , Santacreu, A. , & Famiglietti, M. (2020). Social distancing and contact‐intensive occupations. Federal reserve bank of St. Louis. Retrieved from https://www.stlouisfed.org/on-the-economy/2020/march/social-distancing-contact-intensive-occupations [Google Scholar]

- Manyika, J. , Chui, M. , Miremadi, M. , Bughin, J. , George, K. , Willmott, P. , & Dewhurst, M. (2017). A future that works: Automation, employment, and productivity. New York: McKinsey Global Institute. [Google Scholar]

- McCann, P. , & Van Oort, F. (2019). Theories of agglomeration and regional economic growth: A historical review. In Handbook of regional growth and development theories (pp. 19–33). Cheltenham: Edward Elgar Publishing. [Google Scholar]

- Morgan, J. (2019). Will we work in twenty‐first century capitalism? A critique of the fourth industrial revolution literature. Economy and Society, 48(3), 371–398. [Google Scholar]

- Nelson, R. R. , & Phelps, E. S. (1966). Investment in humans, technological diffusion, and economic growth. The American Economic Review, 56(1/2), 69–75. [Google Scholar]

- Pajarinen, M. , & Rouvinen, P. (2014). Computerization threatens one third of Finnish employment. ETLA Brief, 22(13.1), 1–6. [Google Scholar]

- Pérez, C. (2003). Technological change and opportunities for development as a moving target. Trade and Development: Directions for the 21st Century, 100, 109–130. [Google Scholar]

- Pierrakis, Y. , & Saridakis, G. (2017). Do publicly backed venture capital investments promote innovation? Differences between privately and publicly backed funds in the UK venture capital market. Journal of Business Venturing Insights, 7, 55–64. [Google Scholar]

- Pigou, A. (1933). The theory of unemployment. London: Macmillan. [Google Scholar]

- Powell, W. , & Snellman, K. (2004). The knowledge economy. Annual Review of Sociology, 30, 199–220. [Google Scholar]

- Ricardo, D. (1951). In Sraffa P. (Ed.), The works and correspondence of David Ricardo: Principles of political economy and taxation, volume 1. Cambridge: Cambridge University Press. [Google Scholar]

- Rifkin, J. (1996). End of work. New York: G. P. Putnam's Sons. [Google Scholar]

- Say, J. (1964). A treatise on political economy or the production, distribution and consumption of wealth. New York: M. Kelley. [Google Scholar]

- Schattorie, J. , de Jong, A. , Fransen, M. , & Vennemann, B. (2014). De impact van automatisering op de Nederlandse Arbeidsmarkt. London: Deloitte. [Google Scholar]

- Scheerder, A. , van Deursen, A. , & van Dijk, J. (2017). Determinants of Internet skills, uses and outcomes. A systematic review of the second‐and third‐level digital divide. Telematics and Informatics., 34(8), 1607–1624. [Google Scholar]

- Schwab, K. (2017). The fourth industrial revolution. London: Penguin UK. [Google Scholar]

- Semenova, R. , Zemtsov, S. , & Polyakova, P. (2019). STEAM‐education and IT‐employment as factors of adaptation to the digital transformation of the economy in the regions of Russia. Innovations, 253(11), 2–14. (in Russian) [Google Scholar]

- Smith, A. , & Anderson, J. (2014). AI, robotics, and the future of jobs. Washington, D.C.: Pew Research Center. [Google Scholar]

- Stewart I., De D., & Cole A. (2015). Technology and People: The great job‐creating machine. London: Deloitte. [Google Scholar]

- Stoneman, P. (1995). Handbook of the economics of innovation and technological change. Oxford: Blackwell. [Google Scholar]

- The Future of Jobs . (2016). Employment. Skills and Workforce: Strategy for the Fourth Industrial Revolution. Geneva: World Economic Forum. [Google Scholar]

- Vedev A., Drobyshevsky S., Knobel A., Sokolov I., & Trunin P. (2020). Scenarios of development of economic situation in Russia in 2020 and offers on macroeconomic policy. Monitoring of Russia's economic outlook: Trends and challenges of socio‐economic development, 106, 3–9. [Google Scholar]

- Venables, A. (1985). The economic implications of a discrete technical change. Oxford Economic Papers, 37(2), 230–248. [Google Scholar]

- Vivarelli, M. (1995). The economics of technology and employment: Theory and empirical evidence. Aldershot: Edward Elgar. [Google Scholar]

- Vivarelli, M. (2014). Innovation, employment and skills in advanced and developing countries: A survey of economic literature. Journal of Economic Issues, 48(1), 123–154. [Google Scholar]

- Wakao Y. & Osborne M. (2015). Percent of jobs in Japan in the Next 20 years. Retrieved from https://www.nri.com/~/media/PDF/jp/news/2015/151202_1.pdf

- World Bank . (2016). World development report 2016: Digital dividends. Washington, DC: World Bank. doi:10.1596/978‐1‐4648‐0671‐1 [Google Scholar]

- Zemtsov, S. (2017). Robots and potential technological unemployment in the Russian regions: review and preliminary results. Voprosy Economiki, 7, 142–157. (In Russian) [Google Scholar]

- Zemtsov, S. (2018). Will robots be able to replace people? Assessment of automation risks in the Russian regions. Innovations, (4), 2–8. (In Russian) [Google Scholar]

- Zemtsov, S. , Barinova, V. , & Semenova, R. (2019). The risks of digitalization and the adaptation of Rregional labor markets in Russia. Foresight and STI Governance, 13(2), 84–96. 10.17323/2500-2597.2019.2.84.96 [DOI] [Google Scholar]

- Zemtsov, S. , & Kotsemir, M. (2019). An assessment of regional innovation system efficiency in Russia: The application of the DEA approach. Scientometrics, 120(2), 375–404. [Google Scholar]

- Zemtsov, S. , & Tsareva, Y. (2018). Entrepreneurial activity in the Russian regions: How spatial and temporal effects determine the development of small business. Journal of the New Economic Association, 37(1), 145–165. [Google Scholar]

- Zemtsov, S. P. , Eremkin, V. A. , & Barinova, V. A. (2015). Factors of attractiveness of the leading Russian universities. Overview of literature and econometric analysis. Educational Studies, 4, 201–233. (In Russian) [Google Scholar]

- Zubarevich, N. (2010). Russian regions: Inequality, crisis and modernization. Moscow: Independent Institute for Social Policy. (In Russian) [Google Scholar]

- Zubarevich, N. (2015). Regional projection of the new Russian crisis. Voprosy economiki. No., 4, 37–52. (In Russian) [Google Scholar]