Abstract

Background

Many cancer survivors struggle to choose a health insurance plan that meets their needs because of high costs, limited health insurance literacy, and lack of decision support. We developed a web‐based decision aid, Improving Cancer Patients’ Insurance Choices (I Can PIC), and evaluated it in a randomized trial.

Materials and Methods

Eligible individuals (18–64 years, diagnosed with cancer for ≤5 years, English‐speaking, not Medicaid or Medicare eligible) were randomized to I Can PIC or an attention control health insurance worksheet. Primary outcomes included health insurance knowledge, decisional conflict, and decision self‐efficacy after completing I Can PIC or the control. Secondary outcomes included knowledge, decisional conflict, decision self‐efficacy, health insurance literacy, financial toxicity, and delayed care at a 3–6‐month follow‐up.

Results

A total of 263 of 335 eligible participants (79%) consented and were randomized; 206 (73%) completed the initial survey (106 in I Can PIC; 100 in the control), and 180 (87%) completed a 3–6 month follow‐up. After viewing I Can PIC or the control, health insurance knowledge and a health insurance literacy item assessing confidence understanding health insurance were higher in the I Can PIC group. At follow‐up, the I Can PIC group retained higher knowledge than the control; confidence understanding health insurance was not reassessed. There were no significant differences between groups in other outcomes. Results did not change when controlling for health literacy and employment. Both groups reported having limited health insurance options.

Conclusion

I Can PIC can improve cancer survivors’ health insurance knowledge and confidence using health insurance. System‐level interventions are needed to lower financial toxicity and help patients manage care costs.

Implications for Practice

Inadequate health insurance compromises cancer treatment and impacts overall and cancer‐specific mortality. Uninsured or underinsured survivors report fewer recommended cancer screenings and may delay or avoid needed follow‐up cancer care because of costs. Even those with adequate insurance report difficulty managing care costs. Health insurance decision support and resources to help manage care costs are thus paramount to cancer survivors’ health and care management. We developed a web‐based decision aid, Improving Cancer Patients’ Insurance Choices (I Can PIC), and evaluated it in a randomized trial. I Can PIC provides health insurance information, supports patients through managing care costs, offers a list of financial and emotional support resources, and provides a personalized cost estimate of annual health care expenses across plan types.

Keywords: Health literacy, Cancer survivors, Self‐efficacy, Insurance, Health, Decision support techniques

Short abstract

Health insurance decision support and resources are needed to help manage care costs. This article describes a web‐based decision aid (I Can PIC), which was developed and evaluated in a randomized trial.

Introduction

Despite increasing access to health insurance after passage of the Affordable Care Act (ACA), patients with cancer and survivors often report inadequate insurance coverage and confusion when using insurance to offset health care expenses. Survivors cite high insurance costs 1, 2, confusing plan details 3, and lack of available decision support 4 as barriers to finding, maintaining, and using adequate coverage. Inadequate health insurance compromises cancer treatment and impacts overall and cancer‐specific mortality 5, 6, 7, 8. Uninsured and underinsured survivors report receiving fewer recommended cancer screenings 9, 10 and may delay or avoid needed follow‐up cancer care because of costs 11, 12, 13.

In addition to the substantial expense associated with health insurance, many individuals struggle to select and use insurance because of limited health insurance literacy 14, 15. Only 10% of individuals eligible for insurance feel they have adequate knowledge about plan differences and details 16, 17. Patients with cancer and survivors often want to maintain continuity of care by selecting a plan that includes their current providers or preferred hospitals in‐network 5, 6, 10. However, insurance plans can limit access to National Cancer Institute‐designated cancer centers 18, and plan networks can change annually. Health insurance decision support is thus paramount to delivering quality cancer care.

To better support health insurance decisions of patients with cancer and survivors, our team developed a health insurance decision tool, Improving Cancer Patients’ Insurance Choices (I Can PIC). I Can PIC (a) provides health insurance information using plain language, graphics, and examples from survivors of how they think about health insurance decisions; (b) tailors relevant information based upon individuals’ health conditions and cancer type(s); (c) provides personalized cost estimates of annual health care expenses across plan types; (d) offers support in discussing cost with clinicians; and (e) provides a list of financial and emotional support resources for those affected by cancer. This manuscript reports on a randomized trial comparing the I Can PIC decision tool to an attention control condition, a health insurance worksheet developed by the American Cancer Society's Cancer Action Network (ACS CAN) 19.

Materials and Methods

The I Can PIC decision aid was developed using a mixed methods approach. The content was based on qualitative interviews with cancer survivors that explored the challenges they faced selecting and using health insurance 3. It also included information that our study team reviewed and found important to plan selection. The study team included experts in health insurance decision support (M.C.P., A.R.B., T.D.M.), health economics (A.R.B., T.D.M.), cancer care delivery (L.M.K.), and financial toxicity of cancer care (M.C.P., A.J., L.M.K.). The content was written at a 6th grade reading level and was reviewed and edited by Health Literacy Media, a health communication company that uses evidence‐based best practices to address health literacy across a range of complex health topics. First, the tool includes plain language information about choosing health insurance during or after cancer treatment, tips for using health insurance during or after cancer treatment, and guidance on discussing costs of care with providers. The information is supplemented by engaging graphics.

Next, I Can PIC provides a personalized estimate of annual health care expenses based on the Medical Expenditure Panel Survey (MEPS). MEPS asks patients, as well as their medical providers and employers, about the specific types and costs of health services accessed by individuals in the U.S. These data include drugs commonly prescribed for specific type of cancers and their associated costs. It also collects data on health insurance coverage available to employed individuals, including associated costs, scope of benefits, and formularies. Using an algorithm to incorporate health status (including cancer type) and demographic information collected by the I Can PIC tool and MEPS data, personalized annual health care expenses were estimated for each user across plan types (high deductible health plans, preferred provider plans, and plans entered manually by users, if details were entered about premium, deductible, and cost‐sharing features). Details on the tool algorithm can be found here 20. We compared our results using our updated calculator to those used by other calculators (e.g., Clear Health Analytics 21), and results were consistent and similar. Annual total costs rather than only monthly costs were displayed based on research suggesting that total cost information presented in a simplified way can support consumer choice about health insurance 22, 23. See example display in supplemental online Appendix A. Because MEPS data are available for those in the private insurance market, and insurance plan selection differs for those seeking coverage through Medicare and Medicaid, this tool was developed and tested for those seeking insurance through their employer or the ACA Marketplace in two states (MO and IL).

After the personalized estimate of care costs across insurance plan types, I Can PIC displays a list of financial and emotional support resources for patients with cancer (see icanpic.org for more information).

Procedure

The randomized controlled trial was registered in clinicaltrials.gov (NCT12345678) and was approved by the Human Research Protection Office at Washington University in St. Louis (protocol number 20170405). The study was conducted between June 2018 and June 2019. Eligible individuals were English speaking, aged 18–64 years, residents of MO or IL, and not eligible for Medicare or Medicaid. Participants were recruited through online advertisements, community health centers, health and social service events, a cancer center, and a university research participant registry. In addition, physicians at a local cancer center gave the study team permission to review medical records and provide potentially eligible patients with information about study participation.

Participants could complete the study in person on a computer or tablet provided by us or at home depending on their preference. After completing consent, participants were randomized via computer random assignment, block size of 4, to either the I Can PIC decision tool or an attention control condition, the ACS CAN health plan worksheet 19. They were sent the assigned tool electronically, and we tracked the time spent on each section of I Can PIC (we could not track time spent on the control worksheet because it was hosted on the developer's Web site). Participants completed the intervention or control tool electronically on their own but could call the research staff with questions or could ask questions during a follow‐up reminder phone call. After viewing I Can PIC or attention control, participants responded to a survey. Participants in both groups were offered a plain‐language glossary of health insurance terms upon completion of the study. They were compensated with a $30 gift card for their time.

A follow‐up survey was administered by e‐mail or by phone based on participants’ preferences 3–6 months after initial participation to assess impact of the I Can PIC tool on health insurance decisions, financial toxicity, and whether participants delayed or avoided care because of cost. Participants received a $10 gift card for completing the follow‐up survey.

Measures

Participant Characteristics

Demographic data collected included age, gender, race, ethnicity, education, employment status, state of residence, and federal poverty level (FPL). The last variable was based on household size and income, grouped by <100% FPL, 100–250% FPL, 250–400% FPL, and >400% FPL because of insurance subsidy and cost‐sharing qualifications. Participants were also asked if they had employer‐based insurance, marketplace insurance, or no insurance at the time of participation in the study; the intervention group received tailored cost calculations based on their insurance market. Potential covariates included numeracy, health literacy, cancer type, time since cancer diagnosis, and the presence and number of other health conditions besides cancer. Participant numeracy was assessed using items from a validated objective numeracy scale 24 and the ability subscale of the Subjective Numeracy Scale 25, 26. The validated Single Item Literacy Screener was used to measure health literacy 27.

Primary Outcomes

Primary outcomes included health insurance knowledge, decision self‐efficacy, and decisional conflict. All three measures were assessed immediately after completing the I Can PIC or attention control and again at a 3–6 month follow‐up.

Health insurance knowledge was assessed with eight items based on our previous health insurance study 23 and the Henry J. Kaiser Foundation's health insurance quiz 28. Participants could answer true, false, or unsure, with incorrect or unsure responses coded as incorrect (see Table 3 for full measure). Higher scores indicate higher knowledge of health insurance.

Table 3.

Number of participants who answered knowledge questions correct by study conditions, n (%)

| Health insurance knowledge questions | I Can PIC (n = 98), n (%) | Attention control (n = 100), n (%) | p valuea |

|---|---|---|---|

| Your premium is the monthly bill you pay to have health insurance. T | 94 (95.92) | 93 (93.00) | .370 |

| A deductible is the amount of money you have to pay out of your own pocket for medical care each year before your insurance plan will start sharing the cost. T | 95 (96.94) | 92 (92.00) | .129 |

| Your monthly premium counts toward your deductible. F | 94 (95.92) | 86 (86.00) | .015 |

| Health insurance formulary is the list of prescription drugs your health plan will cover. T | 81 (82.65) | 42 (42.00) | <.0001 |

| In‐network doctors and hospitals are those that are closest to your home. F | 87 (88.78) | 91 (91.00) | .604 |

| There is no copayment for preventive care if you see a doctor who is part of your plans network. T | 71 (72.45) | 51 (51.00) | .002 |

| If a plan covers a percent of the bill and you pay the rest that is called coinsurance. T | 82 (83.67) | 49 (49.00) | <.0001 |

| You can stop paying your premium each month if you reach your out‐of‐pocket maximum. F | 96 (97.96) | 91 (91.00) | .033 |

T indicates the correct answer is true. F indicates the answer is false. Participants completed knowledge questions after viewing I Can PIC or attention control.

Pearson chi‐square for categorical variables.

Decision self‐efficacy was measured using six questions adapted from the validated low‐literacy version of the Decision Self‐Efficacy Scale (Cronbach's α 0.86–0.92) 29, in which higher scores indicate higher confidence making health insurance choices. Participants rated their confidence in their ability to effectively engage in the process of making an informed health insurance choice, including gathering health insurance information and identifying the plan that best suits their needs. A sample item from this measure is, “I feel confident that I can figure out the insurance choice that best suits me.” Response options include not confident (0), a little confident (2), or very confident (4).

The validated SURE version of the 4‐item Decisional Conflict Scale (Cronbach's α 0.54–0.65) 30, 31 was used to assess participants’ certainty in their ability to weigh the risks and benefits of each plan, access decision support, and choose the plan that is best for them. Higher values indicate more certainty about their health insurance choice. A cutoff value of 4 has been shown to be clinically significant. A sample item from the SURE measure is, “Do you feel sure about the best choice for you?” Response options include yes (1) or no (0).

Secondary Outcomes

Health insurance literacy was assessed immediately after completing I Can PIC or attention control, and at the 3‐6 month follow‐up time point. Financial toxicity and delay or avoidance of care due to costs was assessed at the 3‐6 month follow‐up time point.

Health insurance literacy was measured using two items from the validated Health Insurance Literacy Measure (HILM; Cronbach's α 0.93) 32. These items ask participants about their confidence understanding health insurance terms and estimating annual health care costs. Higher scores indicate higher health insurance literacy. A sample item we used from the HILM is, “Please state how confident would you feel that you… know how to estimate what you would have to pay for your health care needs in the next year, not including emergencies.” Response options include not confident (0), a little confident (2), or very confident (4). We used this measure in addition to the health insurance knowledge items because they examine distinct aspects of health insurance literacy 32, 33. The knowledge measure objectively assessed participants understanding of health insurance terms, whereas the HILM items assessed their self‐reported ability to understand and use health insurance.

Financial toxicity was assessed in the 3–6 month follow‐up survey using seven items from the Comprehensive Score for Financial Toxicity (Cronbach's α 0.92) 34. This validated measure assesses participants’ financial burden and emotional distress associated with the current and potential costs of their cancer treatment. It is scored so that higher scores indicate higher financial toxicity. A sample item we included is, “I worry about the financial problems I will have in the future as a result of my illness or treatment.” Response options include not at all (0), a little bit (1), somewhat (2), quite a bit (3), or very much (4).

Delay or avoidance of care because of cost was assessed via eight questions adapted from a previous study 35. Each question asked if participants had delayed or avoided a specific health care service because of cost in the previous 3–6 months, such as a follow‐up visit with their oncologist or prescription drugs for themselves or their family. They could answer yes (indicating they did delay), no (they did not delay), or not applicable (indicating they have not yet needed that type of service in 2019). During data collection, participants expressed confusion about the distinction between not delaying care and not needing care. “Not applicable” responses were thus recoded as not delaying care. First, the measure was scored by how many participants delayed any type of care. Second, we examined two items to assess whether there was a difference in delay of cancer care specifically.

Because we planned to recruit the majority of participants before or during open enrollment season, we explored I Can PIC's impact on plan choice. A total of 169 (82.0%) participants completed the first part of the study (I Can PIC or attention control and survey) between June 2018 and December 2019. We examined plan type choice intentions at the first time point (including keeping one's current plan) and asked the plan type individuals actually selected by the follow‐up time point. At follow‐up, participants were also asked if their plan was the same as their previous year plan. We examined the match between intended plan choice and actual plan choice; responses were considered a match if plan type chosen at follow‐up matched the intended plan type at the first study time point.

Statistical Analysis Plan

Descriptive statistics were calculated for all variables and were compared between groups using the chi‐square statistic or Fisher's exact test for categorical variables and the Kruskal‐Wallis test for continuous variables. Data on tool usage in the I Can PIC group were calculated by examining time spent overall and by section of the tool. The control condition link was hosted on a Web site managed by the developers of that tool, and thus time spent on that Web site could not be tracked.

Data were then examined for between‐group differences in primary outcomes (knowledge, decision self‐efficacy, and decisional conflict) after completing the first survey and at the 3–6 month follow‐up through the Kruskal‐Wallis test, chi‐square statistic, or Fisher's exact test as appropriate. Multivariable linear regression models examined the relation between group and continuous outcomes (knowledge and decision self‐efficacy), and multivariable logistic regression models examined the relation between group and categorical outcomes (decisional conflict, health insurance literacy, and whether or not patients intended to keep their health insurance plan), controlling for employment status because it differed between randomized groups and health literacy because of a priori planned analyses, given its relationship to numerous decision variables 36. To explore the difference in outcomes between two groups between two time points (upon completing the first survey and at follow‐up), mixed models included group, the time points (upon completing the first survey vs. follow‐up), and the interaction between group and time points. Missing data were excluded from analyses. All statistical tests were two‐sided with α set at a 0.05 level of significance. SAS version 9.4 (SAS Institute, Cary, NC) was used to perform all statistical analyses.

Results

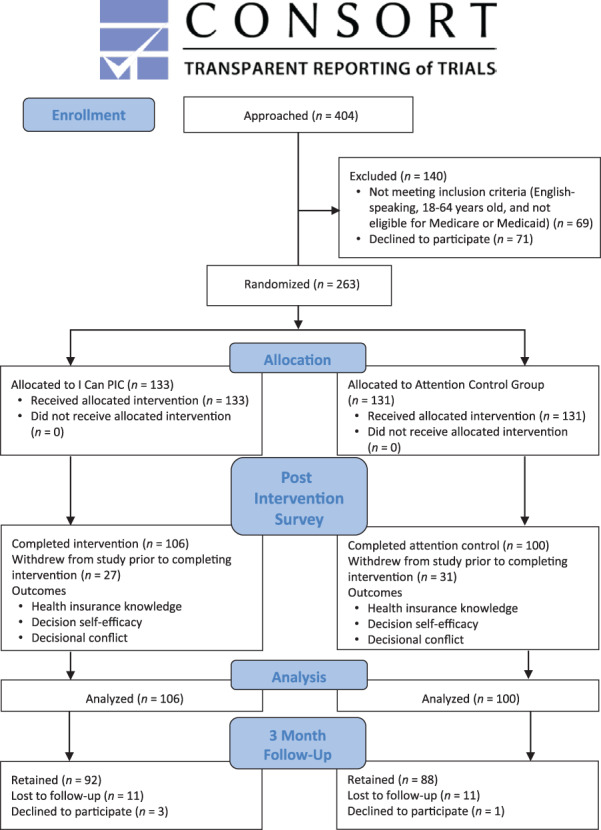

Figure 1 displays a CONSORT diagram of participants screened, enrolled, and participating in the study. Overall, 404 individuals were approached, and 335 were eligible. Of those, 263 (78.5%) enrolled and were randomized, and 206 (61.5%) completed the study. A total of 180 participants (87.4%) completed the 3–6 month follow‐up survey (92 in the I Can PIC group and 88 in the attention control group).

Figure 1.

Consort diagram. The consort diagram shows the flow of the randomized trial including subject enrollment, allocation, and data analysis.

Table 1 displays participant characteristics. There were no differences between the intervention and attention control groups across demographic or clinical characteristics, except that those in the intervention group were more likely to be employed than those in the control group. Employment status was included in all multivariable analyses as a result. Most study participants (87.9%) had employer‐based health insurance coverage prior to the study, although participants in the control group were more likely to have marketplace coverage than participants in the I Can PIC group (7.6% vs. 14.0%). A total of 93 of 106 (87.7%) I Can PIC users spent some time on every section of the tool. In total, I Can PIC users spent a median of 17.6 (range, 4.3–76.9) minutes using the tool. Most of that time was spent learning about health insurance terms and details (median, 4.9 minutes), followed by reviewing a personalized cost estimate (2.6 minutes) and considering their unique health needs (2.5 minutes).

Table 1.

Participant characteristics

| Characteristics | I Can PIC (n = 106) | Attention control (n = 100) | p valuea | Standardized difference |

|---|---|---|---|---|

| Age, mean (SD), yr | 52.41 (9.99) | 52.94 (9.35) | .703 | 0.055 |

| Gender, n (%) | .254 | 0.159 | ||

| Male | 42 (39.62) | 32 (32.00) | ||

| Female | 64 (60.38) | 68 (68.00) | ||

| Race, n (%) | 105 | 98 | .901 | 0.017 |

| White only | 85 (80.95) | 80 (81.63) | ||

| Other (including multiple) | 20 (19.05) | 18 (18.37) | ||

| Hispanic ethnicity, n (%) | 104 | 99 | <.999 | 0.056 |

| No | 101 (97.12) | 97 (97.98) | ||

| Education, n (%) | .488 | 0.172 | ||

| ≤High school or GED | 10 (9.43) | 9 (9.00) | ||

| Some college or technical training | 34 (32.08) | 40 (40.00) | ||

| College degree and higher | 62 (58.49) | 51 (51.00) | ||

| Percentage of federal poverty level, n (%) | 95 | 93 | .698 | 0.174 |

| <100 | 3 (3.16) | 6 (6.45) | ||

| 100–249 | 14 (14.74) | 14 (15.05) | ||

| 250–399 | 21 (22.11) | 23 (24.73) | ||

| 400+ | 57 (60.00) | 50 (53.76) | ||

| Employment status, n (%) | .001 | 0.461 | ||

| Employed | 92 (86.79) | 68 (68.00) | ||

| Unemployed | 14 (13.21) | 32 (32.00) | ||

| State of residence, n (%) | .369 | 0.125 | ||

| Illinois | 20 (18.87) | 24 (24.00) | ||

| Missouri | 86 (81.13) | 76 (76.00) | ||

| Insurance type at enrollment, n (%) | .355 | |||

| Employer‐based insurance | 96 (90.57) | 85 (85.00) | ||

| Marketplace insurance | 8 (7.55) | 14 (14.00) | ||

| No insurance | 2 (1.89) | 1 (1.00) | ||

| Numeracy | ||||

| Objective mean (SD), range | 3.35 (1.00), 0–4 | 3.38 (0.86), 0–4 | .789 | 0.033 |

| Subjective mean (SD), range | 4.11 (0.99), 1–5 | 4.20 (0.83), 1–5 | .946 | 0.097 |

| Health literacy (SILS), n (%) | .709 | 0.052 | ||

| Adequate | 90 (84.91) | 83 (83.00) | ||

| Limited | 16 (15.09) | 17 (17.00) | ||

| Time since diagnosis, n (%) | .670 | 0.120 | ||

| <1 yr | 30 (28.30) | 28 (28.00) | ||

| 1 yr to 2 yr 11 mo | 42 (39.62) | 45 (45.00) | ||

| 3–5 yr | 34 (32.08) | 27 (27.00) | ||

| Other health condition(s), n (%) | 97 | .337 | 0.209 | |

| None | 27 (27.84) | 21 (21.00) | ||

| One | 23 (23.71) | 32 (32.00) | ||

| Two or more | 47 (48.45) | 47 (47.00) | ||

| Type of cancer, n (%) | .849 | 0.328 | ||

| Breast | 33 (31.13) | 31 (31.00) | ||

| Gynecological | 10 (9.43) | 12 (12.00) | ||

| Genitourinary | 15 (14.15) | 13 (13.00) | ||

| Head and neck | 7 (6.60) | 3 (3.00) | ||

| Gastrointestinal | 11 (10.38) | 12 (12.00) | ||

| Lung | 5 (4.72) | 3 (3.00) | ||

| Skin | 5 (4.72) | 9 (9.00) | ||

| Hematologic | 3 (2.83) | 5 (5.00) | ||

| More than one | 13 (12.26) | 10 (10.00) | ||

| Other | 4 (3.77) | 2 (2.00) | ||

| Recruitment method, n (%) | .405 | 0.193 | ||

| Chart review | 63 | 57 | ||

| Research participant registry | 17 | 23 | ||

| Other (e.g., social media, flyer, in‐person at an event or clinic) | 26 | 20 |

Percentages might not total 100% because of rounding. The denominator for the percentages is the sum of patients across all categories, excluding missing values.

Chi‐square or Fisher's exact test for categorical variable; Kruskal‐Wallis test for continuous variable.

Abbreviations: GED, General Educational Development; SILS, Single Item Literacy Screener.

Table 2 displays bivariate analyses comparing measures assessed immediately after completing the I Can PIC or attention control. The I Can PIC group had significantly higher health insurance knowledge (mean correct, 89.3% vs. 74.4%; p < .0001) and confidence understanding health insurance terms as assessed by the HILM (53.8% vs. 32.3% very confident; p = .002). The attention control group had significant knowledge gaps, including whether one's premium counts toward a deductible (percentage who answered correctly, 95.9% vs. 86.0%; p = .015), whether there is a copay for preventive care (72.5% vs. 51.0%; p = .002), what a health insurance formulary means (82.7% vs. 42.0%; p = .0001), what coinsurance means (83.7% vs. 49.0%; p = .0001), and whether one has to keep paying a premium after reaching an out‐of‐pocket maximum for the calendar year (98.0% vs. 91.0%; p = .033; Table 3). Decisional conflict (certainty of choice mean, 3.06 and 2.70, respectively, p = .094; clinically significant conflict, 40.6% and 50.0%, p = .174) and decision self‐efficacy (mean, 75.4 and 73.6; p = .522) were not statistically significantly different between groups. Participants in the attention control group were more likely to report that they intended to keep their current plan (50.0% of I Can PIC group vs. 61.1% of attention control, p = .132), but this difference was also not statistically significant. Results did not change in multivariable analyses after controlling for health literacy and employment status (Table 4).

Table 2.

Bivariate outcomes after completion of I Can PIC or attention control by study conditions

| Measures | I Can PIC (n = 106) | Attention control (n = 100) | p valuea |

|---|---|---|---|

| Health insurance knowledge score | 98 | <.0001 | |

| Mean (SD) | 89.29 (12.31) | 74.38 (17.98) | |

| Range (possible 0–100) | 50–100 | 25–100 | |

| Certainty of choice (SURE) | .094 | ||

| Mean (SD), possible range 0–4 | 3.06 (1.34) | 2.70 (1.50) | .174 |

| No conflict, n (%) | 63 (59.43) | 50 (50.00) | |

| Significant conflict, n (%) | 43 (40.57) | 50 (50.00) | |

| Decision self‐efficacy | .522 | ||

| Mean (SD) | 75.39 (28.09) | 73.58 (26.41) | |

| Median | 87.50 | 79.17 | |

| Range (possible 0–100) | 0–100 | 8.33–100 | |

| HILM, n (%) | |||

| HILM 1–Confidence estimating cost of care | 43 (40.57) | 36 (36.00) | .501 |

| Very confident | 63 (59.43) | 64 (64.00) | |

| Not confident or a little confident | n = 99 | ||

| HILM 2–Confidence understanding health insurance terms | .002 | ||

| Very confident | 57 (53.77) | 32 (32.32) | |

| Not at all or a little confident | 32 (32.32) | 57 (53.77) | |

| Plan choice intentions | .132 | ||

| Keeping current plan | 92 | 90 | |

| Yes | 46 (50.00) | 55 (61.11) | |

| No | 46 (50.00) | 35 (38.89) |

The denominator for the percentages is the sum of patients across all categories, excluding missing values.

Chi‐square or Fisher's exact test for categorical variable; Kruskal‐Wallis test for continuous variable.

Abbreviation: HILM, Health Insurance Literacy Measure.

Table 4.

Multivariable analyses examining study condition on primary outcomes, controlling for employment status and health literacy (n = 206)

| Variables | Knowledgea (n = 198) | Decision self‐efficacya | Certainty of choice (SURE)b | Health insurance literacyb | |

|---|---|---|---|---|---|

| Confidence estimating cost of care | Confidence understanding terms (n = 204) | ||||

| Study group | |||||

| I Can PIC | 88.82% (85.74–91.91) | 70.04% (63.04–77.04) | REF | REF | REF |

| Attention control | 74.83% (71.77–77.88) | 69.31% (62.86–75.76) | OR 0.70 (0.40–1.24) | OR 1.50 (0.58–1.90) | OR 2.19 (1.21–3.94) |

| p value | <.0001 | .851 | .222 | .864 | .010 |

| Employment status | |||||

| Employed | 80.77% (77.47–84.07) | 72.03% (66.44–77.62) | REF | REF | REF |

| Unemployed | 76.98% (72.09–81.88) | 67.32% (58.81–75.83) | OR 0.91 (0.46–1.80) | OR 2.22 (1.02–4.79) | OR (2.14 1.00–4.56) |

| p value | .158 | .313 | .780 | .043 | .050 |

| Health literacy | |||||

| Adequate | 81.62% (78.84–84.41) | 74.86% (70.02–79.71) | REF | REF | REF |

| Limited | 76.14% (70.54–81.73) | 64.49% (55.02–73.95) | OR 0.41 (0.19–0.90) | OR 3.14 (1.22–8.06) | OR 2.73 (1.14–6.56) |

| p value | .073 | .046 | .026 | .017 | .025 |

Results are presented as least squares mean (95% confidence interval [CI]). Percent correct on the knowledge measure and mean decision self‐efficacy score could range from 0–100.

Results are presented as odds ratio (95% CI).

Abbreviation: REF, reference group.

At the 3–6‐month follow‐up time point, health insurance knowledge remained significantly higher among those in the I Can PIC versus attention control group (mean correct, 82.1 % vs. 74.96%; p = .002; Table 5). Those in the I Can PIC group reported lower financial toxicity than those in the attention control group (mean, 9.83 and 11.09; p = .345), but this difference was not statistically significant (see Table 5). Those in the I Can PIC group were also no more or less likely to delay or avoid care (23.9% vs. 27.3%; p = .605) or cancer‐specific care (12.0% vs. 13.6%; p = .736). There was no statistically significant difference between groups when assessing if reported intention to switch or not switch plans immediately after I Can PIC or attention control matched reported health insurance choice at follow‐up. Those in the intervention group were still more likely to be employed than those in the control group, and no other demographic factors were significantly different.

Table 5.

Study condition and primary outcomes at 3–6 month follow‐up

| Measures | I Can PIC (n = 92) | Attention control (n = 88) | p valuea |

|---|---|---|---|

| Age, mean (SD), yr | 52.36 (9.89) | 52.92 (9.62) | .699 |

| Race | .791 | ||

| White only | 76 (83.5) | 73 (82.0) | |

| Other (including multiple) | 15 (16.5) | 16 (18.0) | |

| Education, n (%) | .230 | ||

| <High school or GED | 7 (7.7) | 6 (6.7) | |

| Some college or technical training | 37 (40.7) | 26 (29.2) | |

| College degree and higher | 47 (51.6) | 57 (64.0) | |

| Health literacy (SILS), n (%) | .573 | ||

| Adequate | 76 (83.5) | 77 (86.5) | |

| Limited | 15 (16.5) | 12 (13.5) | |

| Employment status, n (%) | |||

| Employed | 62 (68.1) | 75 (84.3) | .011 |

| Unemployed | 29 (31.9) | 14 (15.7) | |

| Health insurance knowledge score, % | |||

| Mean (SD) | 82.07 (18.00) | 74.86 (17.32) | .002 |

| Range (possible 0–100) | 25–100 | 25–100 | |

| Certainty of Choice (SURE), n | 90 | ||

| Mean (SD), range 0–4 | 3.42 (1.09) | 3.38 (1.11) | .766 |

| No conflict, n (%) | 63 (70.00) | 60 (68.18) | .793 |

| Conflict, n (%) | 27 (30.00) | 28 (31.82) | |

| Decision self‐efficacy, n | 90 | ||

| Mean (SD) | 84.17 (24.00) | 79.26 (24.34) | .103 |

| Median | 100.00 | 91.67 | |

| Range (possible 0–100) | 0–100 | 8.33–100 | |

| Financial toxicity | 87 | ||

| Mean (SD) | 9.83 (6.52) | 11.09 (7.42) | .345 |

| Range (possible 0–28) | 0–27 | 0–27 | |

| Delay or avoidance of care due to cost, n (%) | |||

| Any care | .605 | ||

| No | 70 (76.09) | 64 (72.73) | |

| Yes | 22 (23.91) | 24 (27.27) | |

| Cancer care | .736 | ||

| No | 81 (88.04) | 76 (86.36) | |

| Yes | 11 (11.96) | 12 (13.64) |

The denominator for the percentages is the sum of patients across all categories, excluding missing values.

Chi‐square or Fisher's exact test for categorical variable; Kruskal‐Wallis test for continuous variable.

Abbreviations: GED, General Educational Development; SILS, Single Item Literacy Screener.

Discussion

Patients with cancer and survivors make up a high‐need population that has often been overlooked in past research on health insurance decision making 37. To our knowledge, I Can PIC is the first health insurance decision aid designed specifically for this population. I Can PIC is designed to facilitate purchasing adequate coverage whether the consumer is shopping for an employer‐sponsored or an ACA Marketplace plan. It can also be used in conjunction with a certified application counselor or navigator. Results suggest that individuals who used the I Can PIC tool knew more about health insurance and felt more confident understanding health insurance information; these benefits persisted over time. However, there were no statistically significant differences between groups in their decisional conflict, decision self‐efficacy, plan choice, self‐reported financial toxicity, or whether or not they delayed or avoided care because of costs.

There are several reasons why I Can PIC might not have impacted decisional conflict, decision self‐efficacy, or some secondary outcomes despite its substantial impact on knowledge about how to use health insurance. Some participants had already enrolled in their health insurance plan before participating in the study because of different open enrollment periods offered by various employers. It is possible that I Can PIC could better support choices of those who had options when administered immediately prior to or during open enrollment. Future studies could examine the timing of completing a health insurance decision support tool relative to open enrollment. Alternatively, studies could work to redesign I Can PIC to focus first on helping patients to (a) understand health insurance and how to use it to manage care, (b) talk to providers about care costs, (c) identify resources to help offset care costs, and then (d) choose a health insurance plan, if they are in open enrollment and able to change plans. We plan to test this redesign in a newly funded project within a center aimed at reducing cancer disparities 38.

In the follow‐up survey about delay or avoidance of care because of costs, participants often mentioned that they were not due for any needed health care or cancer care in the short 3–6‐month follow‐up time period. Of those who did delay or avoid care because of costs, they often had household incomes less than 250% of the federal poverty level. Future studies should consider following patients for a full year to ensure adequate time to examine health care use and consider addressing the needs of the most vulnerable patients who might be likely to delay or avoid care.

In addition, when asked about their main reasons for choosing a plan, the majority (68.2%) of participants mentioned that they had limited health insurance options available and could not switch plans even if they wanted to do so. Thus, our findings might have been impacted by individuals’ limited plan choices, regardless of how much the intervention might have improved health insurance knowledge and confidence selecting a plan. Alternatively, some individuals might have opted to pay higher costs for their plan to preserve their provider network 39 or might have experienced inertia about changing plans without a prompt to do so 40.

I Can PIC provided resources that patients could use to help offset the costs of care, including questions to ask their clinicians about care costs. However, the study did not engage clinicians through this process. There are numerous ways clinicians can help lower patients’ out‐of‐pocket costs, but many do not address these cost‐saving strategies during clinical encounters 41. Future studies might pair I Can PIC with a clinician‐ or system‐level intervention to reduce the burden of care costs on patients; we are piloting this approach in a subsequent project within a center aimed at reducing cancer disparities 38.

Strengths of the study include the use of stakeholder input to develop the tool, the use of health insurance literacy best practices developed by the team and reviewed by Health Literacy Media, the established health insurance decision support developed and tested in our past work 20, 23, 42 (adapted for those affected by cancer), the inclusion of patients with cancer across cancer types within 5 years of diagnosis when they often have increased treatment or surveillance needs, the use of both education and personalized cost estimates, and the addition of resources to support cost of care discussions and financial assistance. Limitations include the small sample size from a limited number of recruitment sites, the inability to pair study enrollment with variable open enrollment periods, the short follow‐up before which participants might not have needed to seek care, the relatively educated sample, and the focus on patients without engaging clinicians or the health care system about care costs. These limitations will be addressed in future studies building on this foundational work.

Conclusion

Our study suggests that I Can PIC might be a first step to improving health insurance plan decisions and supporting appropriate health care use by significantly improving health insurance knowledge. Future studies should continue to examine ways to reduce financial toxicity and improve the likelihood that patients can pay for needed care.

Author Contributions

Conception/design: Mary C. Politi, Abigail R. Barker, Aimee S. James, Timothy D. McBride

Provision of study material or patients: Rachel Grant, Nerissa George, Courtney Goodwin

Collection and/or assembly of data: Rachel L. Grant, Nerissa P. George, Jingxia Liu, Courtney M. Goodwin

Data analysis and interpretation: Mary C. Politi, Rachel L. Grant, Nerissa P. George, Abigail R. Barker, Aimee S. James, Lindsay M. Kuroki, Timothy D. McBride, Jingxia Liu, Courtney M. Goodwin

Manuscript writing: Mary C. Politi, Rachel L. Grant, Nerissa P. George, Abigail R. Barker, Aimee S. James, Lindsay M. Kuroki, Timothy D. McBride, Jingxia Liu, Courtney M. Goodwin

Final approval of manuscript: Mary C. Politi, Rachel L. Grant, Nerissa P. George, Abigail R. Barker, Aimee S. James, Lindsay M. Kuroki, Timothy D. McBride, Jingxia Liu, Courtney M. Goodwin

Disclosures

Mary C. Politi: Merck (RF); Timothy D. McBride Centene Corp (other–health policy committee). The other authors indicated no financial relationships.

(C/A) Consulting/advisory relationship; (RF) Research funding; (E) Employment; (ET) Expert testimony; (H) Honoraria received; (OI) Ownership interests; (IP) Intellectual property rights/inventor/patent holder; (SAB) Scientific advisory board

Supporting information

See http://www.TheOncologist.com for supplemental material available online.

Supplemental Appendices

Acknowledgments

Financial support for this study was provided by a grant from the American Cancer Society (#130798‐RSGI‐17‐018‐01‐CPHPS, Politi: PI). The funding agreement ensured the authors’ independence in designing the study, interpreting the data, writing, and publishing the report. Lindsay M. Kuroki, M.D., is a KL2 scholar of the Washington University Institute of Clinical and Translational Sciences. Her research is supported by the National Center for Advancing Translational Sciences of the National Institute of Health under Award Number KL2TR002346. The content is solely the responsibility of the authors and does not necessarily represent the official views of the National Institutes of Health.

Disclosures of potential conflicts of interest may be found at the end of this article.

No part of this article may be reproduced, stored, or transmitted in any form or for any means without the prior permission in writing from the copyright holder. For information on purchasing reprints contact Commercialreprints@wiley.com. For permission information contact permissions@wiley.com.

References

- 1. Warner EL, Park ER, Stroup A et al. Childhood cancer survivors’ familiarity with and opinions of the Patient Protection and Affordable Care Act. J Oncol Pract 2013;9:246–250. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2. Chino F, Peppercorn JM, Rushing C et al. Out‐of‐pocket costs, financial distress, and underinsurance in cancer care. JAMA Oncol 2017;3:1582–1584. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 3. George N, Grant R, James A et al. Burden associated with selecting and using health insurance to manage care costs: Results of a qualitative study of nonelderly cancer survivors. Med Care Res Rev 2018. [Epub ahead of print]. [DOI] [PubMed] [Google Scholar]

- 4. Dean LT, Moss SL, Rollinson SI et al. Patient recommendations for reducing long‐lasting economic burden after breast cancer. Cancer 2019;125:1929–1940. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5. Institute of Medicine (US) Committee on Health Insurance Status and Its Consequences . America's Uninsured Crisis: Consequences for health and health care. Washington, DC: National Academies Press, 2009. [PubMed] [Google Scholar]

- 6. Wilper AP, Woolhandler S, Lasser KE et al. Health insurance and mortality in US adults. Am J Public Health 2009;99:2289–2295. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7. Sommers BD. State Medicaid expansions and mortality, revisited: A cost‐benefit analysis. Am J Health Econ 2017;3:392–421. [Google Scholar]

- 8. Woolhandler S, Himmelstein DU. The relationship of health insurance and mortality: Is lack of insurance deadly? Ann Intern Med 2017;167:424–431. [DOI] [PubMed] [Google Scholar]

- 9. Amini A, Jones BL, Yeh N et al. Disparities in disease presentation in the four screenable cancers according to health insurance status. Public Health 2016;138:50–56. [DOI] [PubMed] [Google Scholar]

- 10. Garfield R, Licata R, Young K. The uninsured at the starting line: Findings from the 2013 Kaiser Survey of Low‐Income Americans and the ACA. Henry J Kaiser Family Foundation. 2014. [Google Scholar]

- 11. Parsons HM, Schmidt S, Harlan LC et al. Young and uninsured: Insurance patterns of recently diagnosed adolescent and young adult cancer survivors in the AYA HOPE study. Cancer 2014;120:2352–2360. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12. Kirchhoff AC, Lyles CR, Fluchel M et al. Limitations in health care access and utilization among long‐term survivors of adolescent and young adult cancer. Cancer 2012;118:5964–5972. [DOI] [PubMed] [Google Scholar]

- 13. Zheng Z, Jemal A, Banegas MP et al. High‐deductible health plans and cancer survivorship: What is the association with access to care and hospital emergency department use? J Oncol Pract 2019;15:e957–e968. [DOI] [PubMed] [Google Scholar]

- 14. Hoerl M, Wuppermann A, Barcellos SH et al. Knowledge as a predictor of insurance coverage under the affordable care act. Med Care 2017;55:428–435. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15. Zhao J, Han X, Zheng Z et al. Health insurance literacy, financial hardship and financial sacrifices among cancer survivors in the United States. J Clin Oncol 2019;37(suppl):1560a. [Google Scholar]

- 16. Hibbard JH, Jewett JJ, Engelmann S et al. Can Medicare beneficiaries make informed choices? Health Aff (Millwood) 1998;17:181–193. [DOI] [PubMed] [Google Scholar]

- 17. McCormack LA, Uhrig JD. How does beneficiary knowledge of the Medicare program vary by type of insurance? Med Care 2003;41:972–978. [DOI] [PubMed] [Google Scholar]

- 18. Kehl KL, Liao KP, Krause TM et al. Access to accredited cancer hospitals within federal exchange plans under the affordable care act. J Clin Oncol 2017;35:645–651. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19. American Cancer Society Cancer Action Network . Health plan worksheet: Know your coverage and costs. Available from https://www.fightcancer.org/sites/default/files/Health‐Plan‐Worksheet‐Know‐Your‐Coverage‐and‐Costs.pdf. 2015. Accessed May 16, 2018.

- 20. Politi MC, Barker AR, Kaphingst KA et al. Show Me My Health Plans: A study protocol of a randomized trial testing a decision support tool for the federal health insurance marketplace in Missouri. BMC Health Serv Res 2016;16:55. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21.How it works. Clear Health Analytics. Available from https://clearhealthanalytics.com/how-it-works/. 2018. Accessed December 2, 2019.

- 22. McGarry BE, Maestas N, Grabowski DC. Simplifying the Medicare Plan Finder tool could help older adults choose lower‐cost Part D plans. Health Aff (Millwood) 2018;37:1290–1297. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23. Politi MC, Kuzemchak MD, Liu J et al. Show Me My Health Plans: Using a decision aid to improve decisions in the federal health insurance marketplace. MDM Policy Pract 2016;1. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 24. Lipkus IM, Samsa G, Rimer BK. General performance on a numeracy scale among highly educated samples. Med Decis Making 2001;21:37–44. [DOI] [PubMed] [Google Scholar]

- 25. Fagerlin A, Zikmund‐Fisher BJ, Ubel PA et al. Measuring numeracy without a math test: Development of the subjective numeracy scale. Med Decis Making 2007;27:672–680. [DOI] [PubMed] [Google Scholar]

- 26. Zikmund‐Fisher BJ, Smith DM, Ubel PA et al. Validation of the subjective numeracy scale: Effects of low numeracy on comprehension of risk communications and utility elicitations. Med Decis Making 2007;27:663–671. [DOI] [PubMed] [Google Scholar]

- 27. Morris NS, MacLean CD, Chew LD et al. The Single Item Literacy Screener: Evaluation of a brief instrument to identify limited reading ability. BMC Fam Pract 2006;7:21. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 28. Health insurance quiz . Henry J Kaiser Family Foundation website. Available from https://www.kff.org/quiz/health-insurance-quiz/. 2019. Accessed May 16, 2018.

- 29. O'Connor AM. User manual‐decision self‐efficacy scale. Patient Decision Aids. Ottawa Hospital Research Institute website. Available from https://decisionaid.ohri.ca/docs/develop/Tools/Decision_SelfEfficacy.pdf. 1995. Accessed May 16, 2018.

- 30. Légaré F, Kearing S, Clay K et al. Are you SURE?: Assessing patient decisional conflict with a 4‐item screening test. Can Fam Physician 2010;56:e308–e314. [PMC free article] [PubMed] [Google Scholar]

- 31. Ferron Parayre A, Labrecque M, Rousseau M et al. Validation of SURE, a four‐item clinical checklist for detecting decisional conflict in patients. Med Decis Making 2014;34:54–62. [DOI] [PubMed] [Google Scholar]

- 32. Paez KA, Mallery CJ, Noel H et al. Development of the Health Insurance Literacy Measure (HILM): Conceptualizing and measuring consumer ability to choose and use private health insurance. J Health Commun 2014;19(suppl 2):225–239. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 33. Paez KA, Mallery CJ. A little knowledge is a risky thing: Wide gap in what people think they know about health insurance and what they actually know. Available from http://www.air.org/resource/little-knowledge-risky-thing-wide-gap-what-people-think-they-know-about-health-insurance. 2014. Accessed December 12, 2019.

- 34. de Souza JA, Yap BJ, Hlubocky FJ et al. The development of a financial toxicity patient‐reported outcome in cancer: The COST measure. Cancer 2014;120:3245–3253. [DOI] [PubMed] [Google Scholar]

- 35. Smith KT, Monti D, Mir N et al. Access is necessary but not sufficient: Factors influencing delay and avoidance of health care services. MDM Policy Pract 2018;3:2381468318760298. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 36. Amalraj S, Starkweather C, Naeim A. Health literacy, communication, and treatment decision‐making in older cancer patients. Ethics 2009;23. [PubMed] [Google Scholar]

- 37. Furtado KS, Kaphingst KA, Perkins H et al. Health insurance information‐seeking behaviors among the uninsured. J Health Commun 2016;21:148–158. [DOI] [PubMed] [Google Scholar]

- 38.$7.6 million funds center to fight cancer disparities in Missouri, Illinois [press release]. The Source. 2019.

- 39. Hibbard JH, Greene J, Sofaer S et al. An experiment shows that a well‐designed report on costs and quality can help consumers choose high‐value health care. Health Aff (Millwood) 2012;31:560–568. [DOI] [PubMed] [Google Scholar]

- 40. Kling JR, Mullainathan S, Shafir E et al. Comparison friction: Experimental evidence from Medicare drug plans. Q J Econ 2012;127:199–235. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 41. Kelly RJ, Forde PM, Elnahal SM et al. Patients and physicians can discuss costs of cancer treatment in the clinic. J Oncol Pract 2015;11:308–312. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 42. Zhao J, Mir N, Ackermann N et al. Show Me Health Plans: Dissemination of a web‐based decision aid for health insurance plan decisions. J Med Internet Res 2018;20:e209. [DOI] [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

See http://www.TheOncologist.com for supplemental material available online.

Supplemental Appendices