Abstract

This article projects business risk through deferent industrial scenarios in concentrated solar investments in the United Arab Emirates (UAE). Nationwide, the government seeks a sustainable solution through energy policy development and engagement of the stakeholders for clean energy generation at wider level in the long run. Support has been extended through various support schemes. In the current study, Monte Carlo simulations and net present value (NPV) risk are used to analyse the return on investment. A 5 MW concave solar panel project is evaluated. We have assessed the impact of local factors on profits through NPV. The study proposes that a higher NPV is expected if the concave solar panel project is financed 50% by Khalifa funding. The study also proposes a robust policy and highlights the opportunity of business profitability if the government subsidises land leasing with respect to each scenario. Additionally, the study also proposes a policy to maintain the interests of investors in the UAE.

Keywords: business profitability, concentrated solar power, environmental policy, Khalifa funding, renewable energy, risk evaluation, stakeholder engagement, sustainable development

1. INTRODUCTION

Continuous increasing energy demand and environmental issues motivated policymakers and researchers to work in the improvement of non‐fossil fuel economies. A tremendous increase in research on the development of non‐renewable energy sources such as solar energy, wind energy, biomass and tidal energy has been witnessed in the past few decades. The high focus was on solar energy generation, and current interest lies in high‐efficiency technologies for generating cleaner energy (Wicki & Hansen, 2019). Concentrated solar energy (CSE) was also developed for harnessing solar power. This technology uses a technologically improved mirror to concentrate solar radiation and convert it into energy.

The energy generation through concentrated solar power (CSP) is adopted at the global level. The estimate of solar power accounts for 18,000 TWh/year around the world, in which CSP technology can generate energy equal to 8,000 h per year (Trieb, Schillings, O'sullivan, Pregger, & Hoyer‐Klick, 2009). It is measured with the expansion of desert areas around the world (this is applicable in the context of UAE as well). The energy import from such a project reduces the burden of coal and fuel imports and eventually reduces greenhouse emissions. Such potential can be mapped with high spatial resolution. CSP technology has high potential in Australia, Africa, Central Asia, Canada, China, Central South America, India, Japan, Middle East, Mexico, Russia, the United States, South Korea and the EU.

Although this study investigates the UAE, the paper's findings have broader context applicability. Given the UAE's geographical condition, the country receives sufficient solar radiation for the generation of electricity. The electricity can be consumed locally by the industries and the households. Additionally, UAE shares border with Oman and Saudi Arabia; the electricity generated in excess can also be supplied to these neighbouring countries. Thus, the geographical advantage of the country can significantly host the investors willing to invest in the energy business. The policy endeavour can reduce the carbon footprints of the country and contribute to the sustainable goals of the country.

This study evaluates the energy generation business of 5 MW under various scenarios through net present value (NPV) risk and Monte Carlo simulations. The study presents four major scenarios' evaluation to understand the return on investment: (1) business as usual, (2) business support through Khalifa funding, (3) Khalifa funding and interest payment and (4) combination of bank borrowing, Khalifa funding, interest payments and premiums on electricity sales. In addition, the effect of land subsidies on the abovementioned scenarios was evaluated.

The study contributes to the literature in the following ways. First, the Khalifa funding has supported the business over the years in UAE. There is no explicit evidence of this support to renewable energy project in the academic literature of energy and business. Therefore, the extensive‐scale application of such supportive funding policy that can create a higher economic impact is represented through the current study. Second, the utilization of desert land in the form of land subsidies for sustainable businesses improves the attractiveness in the UAE for the investor. This proposition has not been made before in the literature, thus contributes to the existing literature. Third, the land subsidies generate significantly higher revenues; thus, the investor can make significantly higher profits (compared with the scene where the land is not subsidized) and pay tax on the sale of electricity, thereby increasing the financial reserve for the government. This revenue through tax might be further utilized to offer subsidies to similar projects, leading to sustainability in the long run. As this thought has not been found in the existing studies, it significantly contributes to the existing knowledge in the economic policies related to the investment in clean energy.

The rest of the paper is organised as follows. Section 2 puts forth the literature in brief, Section 3 presents the data and methodology and Section 4 highlights results and discussions. Finally, Section 5 concludes the study with policy, limitations and future course of action.

2. LITERATURE REVIEW

2.1. CSP technology and business potential

The business potential can be realised on the ground with decisive support in the form of investment, funding and innovation due to excessive cost of instalments at the beginning (Held et al., 2019; Yang, He, Xia, & Chen, 2019). Government at this stage makes supportive policies and schemes to promote CSP development. One such funding and incentives help EU countries to deploy such projects. Overall, the cost of technology will be lesser, and incentive schemes such as feed‐in tariff and subsidy can provide further development of CSP technology.

To grab an opportunity to develop solar energy in the form of CSP deployment, the country needs to implement smart policies. These policies are related to technological development and innovation (Peters, Schmidt, Wiederkehr, & Schneider, 2011; Craig, Brent, & Dinter, 2017; Potts, 2019). The progressive steps include R&D and incentives to the innovators that increase the deployment of projects. Large‐scale deployment may be possible with the help of incentives/subsidy provisions by regulatory bodies offered to the investors.

CSE technology is maturing around the world. The United States uses this technology to a considerable extent in the production of electricity. The United States is the first country that has begun to work on CSE technology development due to a large amount of solar energy resource in southeast states. The first commercially CSE plant was built in California in 1980. Later, a plant was constructed domestically in Arizona. 1 To promote the expansion, the U.S. Government and Energy department took initiatives for the development of such technology. In 2014, the American solar energy industry focused on the long‐term investment in solar technology in terms of CSE installation. The U.S. Department of Energy and private partners took a solar power initiative to increase electricity grids in the United States. As a result, with the supportive work of authority, five plants were operationalised in the United States at the end of 2014. 2 With the successful implementation of CSE technology in the United States, countries in Europe, South Africa, Australia, China, the United Kingdom and so forth also followed the trend. The government and private players jointly aided in the implementation.

The year 2008 saw a boom for CSE technology construction around the world. 3 The United States, Spain, Australia, Portugal, Egypt, China, UAE, and a few other countries adopted this technology. Green‐space, European Solar Thermal Power Industry, and IEA's Solar Paces Programmed on the supply of solar energy resource did a joint initiative of projection work in 2040. The estimated result shows that the capacity for energy production through CSE technology is expected to be increased from 36,853 to 600,000 MW from 2025 to 2040. The share of the CSE project in total energy supply will be accounted for 6% till 2050. With the growing demand for energy around the world and increasing renewable energy share, especially solar energy, will expand the market share.

Globally, CSE technology is expected to increase energy generation close to 11% of total energy till 2050. 4 Table 1 shows the region and targeted year.

TABLE 1.

Expected regions and targeted years

| Group | Country/region | 2020 (%) | 2030 (%) | 2040 (%) | 2050 (%) |

|---|---|---|---|---|---|

| 1 | Australia, Central Asia, Chile, India (Gujarat, Rajasthan), Mexico, Middle East, North Africa, Peru, South Africa, United States (southwestern region) | 5 | 12 | 30 | 40 |

| 2 | United States (outside of the southwestern region) | 3 | 6 | 13 | 20 |

| 3 | Europe (the vast majority of which is imported), Turkey | 3 | 6 | 10 | 15 |

| 4 | Africa (outside of the northern region), Argentina, Brazil, India (outside of the two states listed above) | 1 | 5 | 8 | 15 |

| 5 | Worldwide | 11 |

Source: Asiabiomass.jp

An example of a few big companies 5 involved in the CSP development around the world are Bright Source Energy (USA), Abengea solar (Spain, South Africa, Chile, and UAE Some), Siemens, Acciona (Spain), Solar Reserve (Spain, Chile, and South Africa), Trivelli Energia (Italy and Europe), Abros Green (Germany), and Torresol Energy (Spain). More than 20 GW is under construction worldwide. The United States and Spain are two leading market in the world. This development resulted due to government's support schemes like tax incentives, feed‐in tariff, subsidies, and renewable portfolio standard. Algeria, Egypt, and Morocco are developing CSE technology to increase solar energy production. UAE has already started to build large CSE plants. Australia, India, Iran, China, Italy, Mexico, Jordan, and South Africa are also working on to develop large‐scale CSE projects. 6 Usually, a strong government support and intervention are required by the government to involve other stakeholders in industrial projects (Garrone, Grilli, & Mrkajic, 2018; Pan, Chen, Sinha, & Dong, 2020; Quan, Wu, Li, & Ying, 2018; Shao, 2019).

2.2. CSE policy and management around the world

The IEA Roadmap for CSE development shows positive influence in the world market. 7 The total power capacity of CSE plant reached at 1 GW in 2010. This target is set to increase at 148 GW until 2020. It shows an estimated share of 1.3% of global energy production through CES plant. This target is further enhanced at 337 GW with an increased share of 3.8% of total energy production around the world. By 2040, the share of CSE in total installed capacity will be double (715 GW) that will account for 8.3% of total production. The long‐term development plan is set to be achieved until 2050 with an estimated installed capacity of 1,089 GW. This represents 11.3% of total global electricity production. To achieve this target, countries have developed some support mechanism. This mechanism includes a favourable investment environment for private investors, government and state policy, tax incentives, premium, research and development, innovation in technology and so forth. One successful example of this is the U.S. Loan Guarantee and Renewable Energy Grant Program, which supplies incentives to private investors in innovation. Research and development effort has been started in Australia, Europe, Russia, the UAE, China, and South Korea. A few incentive policies, such as feed‐in tariff or premium is implemented by Spain, Algeria, Israel, South Africa, and Indian states.

The regulatory mechanism must stimulate CSP development. These mechanisms consist of a private entity, government sector and international bodies. Policy measures are usually enunciated by the government with a given period. This may be on the short‐term or long‐term basis. The policy includes deployment support, investment support for manufacturing plants and innovation supports in the form of research and development and industrial development assistance (Grau, Huo, & Neuhoff, 2012; Horbach & Rammer, 2018; Pham, 2019; Zafar, Shahbaz, Hou, & Sinha, 2019). Subsidies feed‐in tariff, tax relief and concessions, fixed premiums and so forth measure to increase the deployment of CSP projects. Cooperation support of banks, regional government and central government enhances the chances of installation.

2.3. CSP and UAE and MENA region

The development of solar energy technology in UAE shows a positive influence on CSE technology development; this is due to government support and strong domestic market. The first CSE plants in UAE were built in Abu Dhabi in the year of 2014. 8 The financing supports were provided with the help of international and domestic banks. ACWA and Shanghai Electric have signed a contract to build the largest CSE Park in Dubai in a phase. The possibility was due to high support mechanism of the UAE government. UAE government privatised its economy in 1986 for private investors. Private players are free to invest in the energy sector. The main supportive policy is public–private partnership agreement and government surety on electricity buying and selling. The state government has monopoly power in the distribution and transmission of electricity. As a result, a significant share (90%) of electricity supplier are private entities. A high credit rating supports the financing facility within the region. Low rate of interest and credit availability boost investment in energy projects. Japanese and European banks have helped to invest in the UAE. Such trust in investment and policy supply minimal risk and certainty for investors to invest in the CSE projects.

UAE has planned to build a CSP project with the application of ‘Independent Power Produce’ model with investment support of Dhs 14.2 billion to provide clean energy to its residents. 9 The target year is 2020 to 2030. The strategic supports provision is started with Saudi Arabia's ACWA Power and the Silk Road Fund with the collaboration of China's Shanghai Electric with contractual basis. The tariff rate is not subsidised and relatively lower, which accounts for 7.3$c/kWh. 10

Implementation of CSE technology in the MENA region began in 2009 with investment through support programme. 11 The Trust Fund Committee of the Clean Energy Fund has planned to support the development of 1 GW of CSE project capacity and related infrastructure development with the sanctions of U.S. $750 million in five MENA regions, namely, Algeria, Egypt, Tunisia, Jordan, and Morocco. The initiative of MENA CSP Investment plan focuses on the financing and grants need for the MENA region with the development of CSE technology. 12 The funding is majorly supported by two organisations: Clean Energy and the World Bank. The aim was to promote the installation of 1,000 MW energy from CSE project in the MENA region with 100 MW proposal to Abu Dhabi in the same year. To address the climate change and carbon emission issues, Morocco was the first to invest in CSE projects in 2010 with a target to generate 40% of its energy from solar. 13 The development of such plant was assisted through contracts and public/private finance.

The successful development of CSP technology in MENA regions is dictated by its regulatory policies, governmental willingness and institutional framework. 14 Thus, the proposal improved the industrial environment and manufacturing potential with higher investment shares in the economy. A 2011 survey revealed the international business community around the world that faced obstacles associated with CSP development. These challenges hampered the development of business. Therefore, to improve, policy measures initiated with the cooperation of banks and to reduce the financial problem, CSP investors were supported by the government. These grants supported licencing, standard quality certification, joint ventures, start‐up and research and development for small‐scale project. The power purchase agreement, bidding process, integrated action plan and business models were put in place to effectively incorporate the policy into the system. The technical assistance criteria set with the instalment of 950 MW CSP plant that is projected to develop by 2020. Such assistance applies for small, medium and large CSP plants.

Investment support for CSP project in MENA region is supported by joint initiative of World Bank and Asian Development Bank with the development of Clean Technology Fund in 2009. 15 This is an action plan for co‐financing of nine commercial‐scale power plant and two transmission plans in five MENA regions. These regions are known as MENA CTF, which includes Algeria, Egypt, Jordan, Morocco, and Tunisia. The objective was to become a supplier of CSP energy in the domestic market. This policy created an opportunity for a local manufacturer to involve in manufacturing of CSP equipment. Under the Green Climate Fund, selected MENA region is expected to receive U.S. $100 billion in a year from 2020 onwards for the development of clean energy sources. These funding facilities can be arranged from private and public sources as well as bilateral and multilateral sources. Mediterranean Solar Plan is another such policy to promote MENA CSP project development in the region. As expected, this initiative has the potential to generate economic benefit in the form of job creation and increase CSP market share.

Development of CSE technology has shown positive growth in the MENA region. The potential to grow this technology is the immediate requirement and low‐cost technology to shift from coal to green energy. The potential can be seen in the fact that initial years of CSE technology development take 10–20 years with incentive policy of EURO 10 billion initial investment and extended payback guarantee for further two decades (Pitz‐Paal et al., 2012). In the economic point of view, the cost structure is still a critical area for concern. The estimated cost reduction of 50% to 60% shows the technological innovation that results potential to project deployment. The growth rate of 15% to 30% indicates CSE installation of 500 GW per year that achieves a 50% cost reduction in the 10‐year time period that ranges from 2021 to 2031.

2.4. Revenue models and funding options through Khalifa project

The governments set the feed‐in pricing policies, like feed‐in tariffs (FITs) and feed‐in premiums (FIPs); those policies have been deemed to be very powerful (Alizamir, de Véricourt, & Sun, 2016; Marques, Fuinhas, & Macedo, 2019; Pablo‐Romero, Sánchez‐Braza, Salvador‐Ponce, & Sánchez‐Labrador, 2017; Pantaleo et al., 2017; Ye, Rodrigues, & Lin, 2017) and essential to provide steady and stable income to the projects' owners as well as increase flexibility of banks loans. All this contribute to encouraging renewable energy projects around the world (Tomar & Tiwari, 2017).

Although these policies are promising, the main challenge encompasses the tariff or the premium percentage to the optimal level. 16 Furthermore, tariff systems are a matter of the information associated with the power division. Regulators and policymakers might not have access to the business information they need to create informed decisions. 17

For the current study, feed‐in premiums (FIPs) have been gradually adopted in liberalised electricity markets (such as those were opened to private sector involvement). Premiums are usually of two types: a fixed premium set on top of the market price, generally combined with a floor and cap to decrease risks or a floating (sliding) premium where a reference value (‘strike price’) is set, and the premium is calculated as the difference between the reference value and the reference market price. Caps and floors can be introduced to limit extreme profits or limit risks for investors when the electricity market price rises too high or falls too low. A variation of the FIP is the contract for difference: if the wholesale market price exceeds the strike price, the investors return the difference. 18

Regulatory and pricing policies need to be classified to specific contexts, looking at the technology type, energy demand, system size, business model, energy needs, and other characteristics that frequently vary from project to another.

To achieve equality and fairness between rural and investors, a few countries enforce national uniform tariffs. Tariff caps and standardised tariff calculation policies are elements used to set tariffs. For tariff caps, operators are free to apply tariff up to the cap, which is set based on the local conditions (e.g., the technology used, area and capacity). Also, in a few cases, tariff caps are applied by financing institutions. Standardised tariff calculation procedures (e.g., a cost‐plus approach) allow regulators to analytically evaluate and approve tariffs, while furthermore providing the basis for brief negotiations (MRC Report, 2018) 19.

Tariff constructions should also be planned to allow for flexible financing or payment models, such as pay‐as‐you‐go, power purchase agreements, business‐to‐business partnerships, lease or fee for service and community partnerships (Walters et al., 2015).

Also, a significant amount of trust needs to be built by the government for the protection of investors rights. Additionally, well‐formed policy support helps accelerate investment. Considering this, UAE provides Khalifa funding as a support for new entrepreneurs. Khalifa funding is a non‐profit effort of the government in the UAE to improve enterprise development in the UAE. Since 2014, several firms have been successfully set up using Khalifa funding. Khalifa funding is one of the key pillars to develop the socio‐economic condition of a nation by creating more jobs, empower the youths and, thus, can help in the development of the economy. In the current study, it is expected that the Khalifa fund can help sustainable business in the country.

2.5. Project evaluation under uncertainty

The renewable energy generation is usually competitive (Furlan & Mortarino, 2018; Guidolin & Guseo, 2016; Pitelis, Vasilakos, & Chalvatzis, 2019; Wang, Yan, Zhuang, & Zhang, 2019) due to several factors, such as cost (Robert, Sisodia, & Gopalan, 2017; van der Ploeg & Rezai, 2020), logistic issues (Chen & Su, 2019; Malladi & Sowlati, 2018), transmission (Chen et al., 2020; Mokryani, Hu, Papadopoulos, Niknam, & Aghaei, 2017; Soroudi, Rabiee, & Keane, 2017), demand (Robert et al., 2017), regulations (Sisodia, Soares, & Ferreira, 2016a, 2016b), policy (Abrell & Rausch, 2016; Albrizio, Kozluk, & Zipperer, 2017; Sisodia & Soares, 2015), loss (Quansah & Adaramola, 2019; Rahmani‐Andebili, 2017), storage (Robert, Sisodia, & Gopalan, 2018), investor's interest (Crago & Chernyakhovskiy, 2017; Kaya, Klepacka, & Florkowski, 2019; Linn & Shih, 2019), and efficiency (Brent & Ward, 2018). Since the cost of investment is high and given that renewable energy projects are irreversible (Flatland, Hove, Lavrutich, & Nagy, 2019), a key criterion for the investors to invest in renewable projects is the governmental support through regulatory schemes (Gatto & Drago, 2020; Stephenson & Shabman, 2019; Xie, Yuan, & Huang, 2017). Therefore, a feasibility study can be conducted through scenarios under uncertainty to evaluate and understand the investor's risk (Salehin et al., 2016; Sisodia et al., 2016a; Rosenfeld, Böhm, Lindorfer, & Lehner, 2020).

Throughout the literature, several methods are found that have gained the attention of researchers in the business valuation and decision making. The most popular ones are (1) discounted cash flows (DCF) and NPV, (2) multicriteria analysis (MA), and (3) real options approach (ROA). DCF and NPV are methods to find the present value of future returns on investments. An abundance of literature can be found where people have evaluated energy projects through DCF and NPV (Aba, Ladeinde, & Afimia, 2019; Leicester, Goodier, & Rowley, 2016). MA analyse the several important criteria to decide on the establishment of energy projects. For instance, refer to Kumar et al. (2017), Naz et al. (2017), Campos‐Guzmán, García‐Cáscales, Espinosa and Urbina (2019), Haddad, Liazid and Ferreira (2017), Mahdy and Bahaj (2018) and so forth. However, NPV with risk provides the simulations with Monte Carlo, and ROA provides a higher degree of flexibility in terms of taking up the new project, abandonment and delay of the energy project (Sisodia et al., 2016). Real options with NPV is a widely used method for determining systematic risk under policy regime (Fan, Xu, Yang, & Zhang, 2019; Fleten, Linnerud, Molnár, & Nygaard, 2016; Kim, Park, & Kim, 2017; Loncar, Milovanovic, Rakic, & Radjenovic, 2017; Penizzotto, Pringles, & Olsina, 2019; Shimbar & Ebrahimi, 2020). For the current study, we used the NPV risk method to evaluate various scenarios.

3. DATA AND METHODOLOGY

3.1. Data assumption and method

To address the research question, we have used various assumption in the local context. We highlighted several scenarios of using concave solar panels to produce energy. IRENA Report 20 (2018) estimates that the cost of electricity generation through solar in 2017 is $0.08 to produce a 1 kWh. Therefore, the cost of producing from 5 MW per year would be $3,504,000 (5X365X24X1000X0.08). Nevertheless, the same IRENA Report and ABD Report (2020) 21 also confirms that the price continues to fall; Observing the general trend, we estimated that the rate falls by 12.5% in 2020, and therefore, the cost of $3,066,000 per year was assumed. A list of cost and revenue variables have been considered for each scenario such as installation cost, operation and maintenance, government formalities, labour, and technology import.

It was assumed that for all the scenarios, the total cost would be similar, except for the scenario where the financing needs to be paid back along with the interest rates. The installation cost is assumed to be same throughout all scenarios and will be paid in the year zero of the project, while labour cost is expected to vary by 10% increase every fifth year through the project's lifetime. Similarly, we assumed operation and maintenance cost would have an increase of 5% every fifth year, while government formalities cost will have an increase of 25% and its cost distributed on the 20 years of the project. Technology import cost is expected to be borne by an investor in the year zero.

All the above‐listed variables may vary throughout for market and economic reasons. Therefore, we assumed three market possibilities that can affect the estimated values. In the light of this, optimistic (20% higher than most likely values) and pessimistic (20% lesser than the most likely values) cases are assumed. 22

Table 2 shows the main values assigned to this project:

TABLE 2.

Values assigned for concave solar power project

| Variables | Values |

|---|---|

| Cost of producing 1 kWh | $0.08 |

| Cost of producing from 5 MWh per year | 3,066,000 |

| Installation cost | 766,500 |

| Operation and maintenance (5% increment after every 5 years) | 306,600 |

| Government formalities | 20,000 |

| Labour (10% increment after every 5 years) | 613,200 |

| Technology import | 613,200 |

| Renting land | 613,200 |

| Other cost | 153,300 |

| Interest rate (when applied) | 10% |

| Premium (when applied) | 5% |

Source: Estimated by authors.

For the representation of high costs, a sensitivity of ±20% risk is added to the possible values using a triangulation distribution (triangulation distribution is used by Sisodia et al. (2016) for wind project evaluation). The primary costs considered in sensitivity are sales, land leasing, labour, operation and maintenance, installation cost, technology import and so forth.

In this project, four different scenarios are analysed based on the financial assumptions of the project. The main purpose of this study is to present the scenarios that would attract investors in the renewable energy business. Risk method has been used to analyse the NPV possibilities through Monte Carlo simulation with 5,000 iterations. The literature found that the generation of results with higher iteration stabilizes data output and enhances the predictability. In the study like ours, Sisodia et al. (2016) also used the 5,000 iterations to simulate the NPV results. Also, please refer to Driels and Shin (2004).

The following model has been used in the study with extended financial risk factors

| (1) |

where I represents an initial investment and R1, R2, R3, … R20 represent cash flows for years 1 to 20, respectively, over the 20 years of project life, whereas i indicates discount rate.

Additionally, we have incorporated the ±20% risk associated with the essential variables (mentioned in scenarios and results) for the calculation of NPVs of the project.

Given that the NPV is a reliable tool presented in the literature for the valuation of projects, several energy projects, as mentioned in Section 2.5, have applied the NPV model to model the business risk. The following factors make the NPV tool attractive to be used in the current study: (1) The industrial projects, such as the implementation of an energy harvesting unit, require high cost, and these projects last for 20–25 years. Over the extended period, inflation and other economic factors may change the value of returns on investment after the completion of the project. The NPV tool considers the time value of money, thus making the tool useful. (2) NPV uses the cash outflows, inflows and the factors associated with the risk, which make it a more comprehensive tool. (3) The NPV method not only helps in the decision of taking up the project (for instance, if NPV is greater than zero, then decision rule suggests to go for the project) but also presents the magnitude of returns, which allows the incorporation of decision makers subjectivity too (refer to Castro & Chousa, 2006; Low & Ng, 2018).

3.2. Presentation of scenarios

Under the current UAE regulatory framework, the United Arab Emirates supports renewable energy generation. The project life is assumed to be 20 years for all the scenarios. In the first scenario, we assumed that the total required cost for the project is financed from the bank (100% bank loan) with an interest rate of 10%. Thus, we considered that the owner's equity is zero, and the sale of electricity is tax‐free.

Hypothesis 1

Under the business as a usual framework, the investors of CSP may generate a significant return on investments.

Any intermittent project related to energy generation that have environmental priorities comes with higher cost of installation. Along with the higher cost, most of such projects are irreversible and therefore need protection and generous support through the government. It is assumed that the support of local banks, along with other funding bodies, is critical for the establishment of such projects. Scenario 2 assumes that the project owner finances 50% of the project cost, and the other 50% is aided by Khalifa funding. In this scenario, we assumed a 0% interest and 0% tax rate. It is also expected that the profit will boost by the support of Khalifa funding.

Hypothesis 2

Fifty percent support in energy investment through Khalifa funding in UAE can lead to higher returns on investment as compared with the business as usual scenario.

Banks are believed to be the pillars of economic development. Therefore, in order to be profitable and sustainable in the long run, the bank charges the interest rates, which is seen as a cost to the business. Nevertheless, most of the big business still rely on banks for development and expansion. The policy development through bank support to such investor is likely to boost economic performance. Business can utilize the support of angel investors and venture capitalists too. For the study, we assumed banks as a choice of borrowing for business. In the third scenario, we assumed that the project is 50% financed by Khalifa funding, along with 50% Bank loans and a 10% interest rate. Once the market is mature, it is assumed that there is no reason for the government to charge less interest on bank loans. However, since the initial cost of investment is high, support from Khalifa fund may boost the initial investment. Therefore, 10% of the loan interest seems realistic to be assumed in Scenario 3.

Hypothesis 3

Under the assumption that the energy project is funded 50% by a bank (with 10% interest rate) and 50% through Khalifa fund, the return on investment is relatively higher than the business as usual scenario in UAE.

Another way by which hosting countries can attract foreign direct investment and boost local investment is through paying premiums on the sales of energy per unit. This policy not only encourages the energy generation through sources but also prioritize the clean energy supply to the grid, thereby offering investors an extra financial advantage. Scenario 4 considers that 50% of the required project cost is covered by Khalifa funding, while the other 50% is accounted for by the bank at 10% interest rate. Since the project is expected to be aligned with the government's sustainable goals, the proposal for higher expansion of such business is assisted. In the first phase, the European government focused on feed in tariffs to generate higher investments from the consumer side. Thus, consumers were able to generate energy and consume it at the same time, also referred to as prosumers. Prosumers were incentivised by premium rates to produce clean energy. In the context, we assumed that the European model could be successful in the initial phase. Thus, for generating the clean energy and selling it to the government directly, the scenario assumes the receipt of an additional 5% of sales value as a premium.

Hypothesis 4

Through 50% bank borrowing at the rate of 10% interest rate and 50% Khalifa funding support with 5% premium payment on electricity sales, investment in CSP project can guarantee a higher return in comparison with business as usual scenario in UAE.

Scenarios 5A to 5D represent the policy instrument that can have a higher economic impact. Most of the land in UAE and Gulf is not arable, thus, except for the major cities where infrastructure development is the critical agenda, the country side land cannot be significantly utilized and just stay unused for over the years. Given that the potential to harness the solar energy is higher in UAE and Gulf due to supportive geographical condition, a part of this land can be utilized by offering it to solar investors at highly subsidized rates. This policy instrument will also economically develop the area due to plant set‐up without financially burdening the government. In these scenarios, 5A–5D, it is assumed that the regulators offer 100% subsidized lands to the investors. This scenario not only adds the value to investment attractiveness in the country but also has global implications. If the policy leads to significant economic advantage, it can be followed by neighbouring countries.

Hypothesis 5

Under an assumption in the scenarios from 5A to 5D, the land leasing at higher subsidized rates in the UAE for energy investment project, Scenarios 1–4 generate additional higher profits when compared with the scenarios where the land is not subsidized.

4. RESULTS AND ANALYSIS

We proposed four scenarios using NPV risk method to analyse the project profit possibilities through Monte Carlo simulation with 5,000 iterations. The 5,000 iterations have been implemented previously by Sisodia and Soares (2016). The major variables we considered in the scenarios are sales, labour/staff expense, renting land, operation and maintenance, installation cost and technology import cost. However, a higher cost on additional variables that reflect throughout the life of the project is expected as well. Therefore, we have considered a miscellaneous cost of 20% to account for this uncertainty.

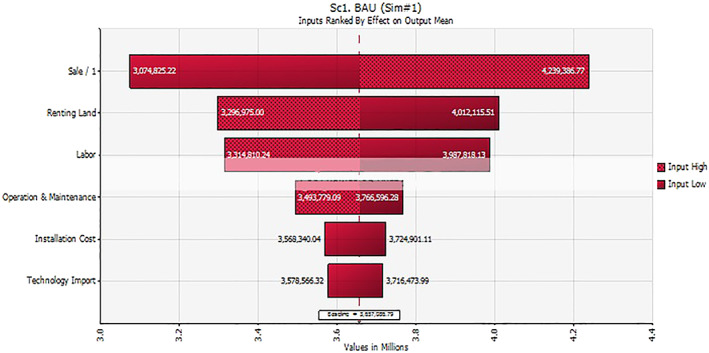

4.1. Scenario 1 (100% bank borrowing with 10% interest rate)

In this scenario, we assumed that the project would be 100% financed by the bank at 10% interest rate. The baseline NPV was 3.657 million dollars; the most significant variable in this scenario is sale. The maximum NPV through high sales can reach up to 4.239 million dollars. However, the worst case with 20% less of sale, the NPV can reduce to 3.074 million dollars.

Renting land and labour represents the second and third important variables, the higher values of renting land reduced the NPV by 3.296 million dollars, while at the lower end (−20%), renting land value improves the NPV by 4.012 million dollars. Similarly, labour cost with higher 20% reduced the NPV by 3.314 millions, and the lower range (−20%) improved the NPV by 3.987 million dollars.

Reduction in operation and maintenance, installation cost and technology import variables can also substantially improve the NPV risk by 3.766, 3.724, and 3.716, respectively.

Overall, the average NPV is positive; therefore, based on the NPV risk method, this scenario can be taken into consideration. Figure 1 represents Scenario 1.

FIGURE 1.

Tornado graph showing the NPV sensitivity in dollars in Scenario 1 [Colour figure can be viewed at wileyonlinelibrary.com]

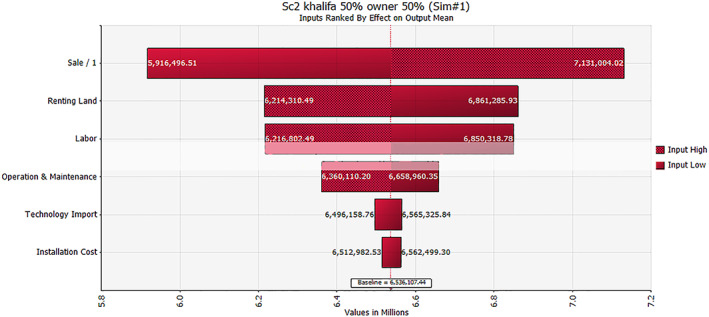

4.2. Scenario 2 (50% owner 50% Khalifa fund)

Scenario 2 assumed that the project would be 50% financed by the owner and 50% by Khalifa fund with no premiums. We predicted that the NPV would increase approximately by 50%.

After we computed the results with the Monte Carlo simulation with 5,000 iterations, we received 6.536 million dollars NPV as a baseline. Sales are computed as the most significant variable with higher and lower NPV ranging between 7.131 to 5.916 million dollars.

Renting land represents the second critical variables; the higher values of renting land is found to reduce the NPV by 6.214 million dollars, while lower values of renting land (by lesser 20%) enhance the NPV by 6.861 million dollars. The third significant observed variable was labour cost that reduced the NPV by 6.216 (at 20% higher cost) and shot up the NPV (at 20% lower cost) by 6.850 million dollars.

Reduction in operation and maintenance improves the NPV by 6.658 million dollars. Installation cost and technology import were seen to be insignificant in this scenario.

Overall, the average NPV is positive, and it showed better NPV than the first scenario. Therefore, this scenario can be taken up with the NPV rule. Figure 2 represents the results of Scenario 2.

FIGURE 2.

Tornado graph showing the NPV sensitivity in dollars in Scenario 2 [Colour figure can be viewed at wileyonlinelibrary.com]

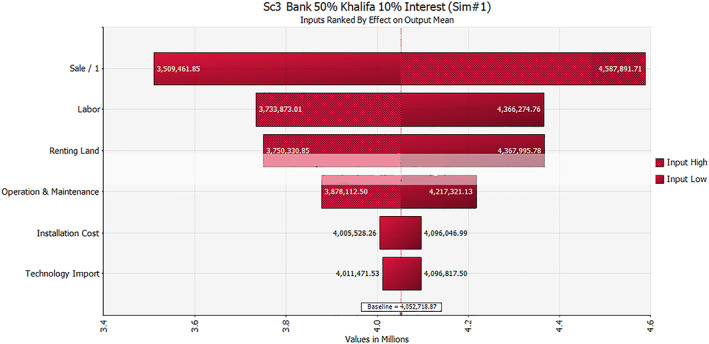

4.3. Scenario 3 (50% bank borrowing at 10% interest rate with 50% Khalifa fund)

This section shows the results of Scenario 3. We assumed that the project would be 50% financed by the bank at 10% interest rate and 50% by Khalifa. We hypothesised that the effect of Khalifa funding on the project with no premium could pose a higher profit through the NPV method.

With 5,000 iterations and with average simulated NPV of 4.052 million dollars, sales were the most significant variable leading to the fluctuation of NPV between 4.5 and 3.5 million dollars. Like the earlier scenario, renting land and labour represents the third important variables. Nonetheless, in this scenario, the higher values (+20%) of renting land reduced the NPV by 3.733 million dollars, while at the lower side (−20%), renting land improves the NPV risk by 4.366 million dollars. Additionally, with labour and staffing, the higher cost reduced the NPV by 3.750, and the lower values (−20%) improved the NPV by 4.367 million dollars.

Reduction in operation and maintenance improves the NPV by 4.217 million dollars, whereas installation cost and technology import are seen to be insignificant in Scenario 3.

It is noticed that the 10% interest rate further lowers the NPV, thus creating a new debt on the investor. Figure 3 represents the NPV variation in Scenario 3.

FIGURE 3.

Tornado graph showing the NPV sensitivity in dollars in Scenario 3 [Colour figure can be viewed at wileyonlinelibrary.com]

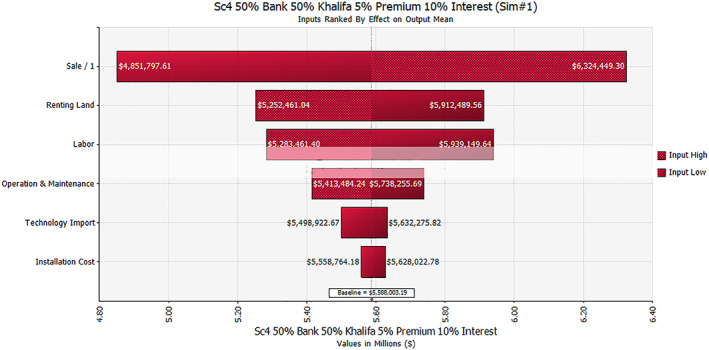

4.4. Scenario 4 (50% bank borrowing with 10% interest rate and 50% Khalifa fund with 5% premium support on sales)

In this scenario, we assumed that the project is 50% financed by the bank at 10% interest rate and 50% by Khalifa funding plus a 5% premium on electricity sales. We assumed that the effect of premium could balance the loss that the interest rate posed in Scenario 3.

With baseline NPV of 5.588 million dollars, sales were the most critical variable. The higher sales result in generating higher NPV by 6.324 million dollars, while in the worst situation, the lower sales generate NPV by 4.851 million dollars, leading to a broad risk margin. Renting of the land in this scenario with higher cost reduced the NPV by 5.252 million dollars, while lower renting land value improves the NPV by 5.912 million dollars. Similarly, labour and staffing cost ranged between 5.2 and 5.9 million dollars, with maximum and minimum costs.

On the one hand, reduction in operation and maintenance improves the NPV by 5.738 million dollars; on the other hand, installation cost and technology import are represented as less significant.

The higher observable positive effect of 5% premium rate on the NPV compared with the third scenario, indicates the higher profitability with NPV risk. Figure 4 represents the results of Scenario 4.

FIGURE 4.

Tornado graph showing the NPV sensitivity in dollars in Scenario 4 [Colour figure can be viewed at wileyonlinelibrary.com]

4.5. New proposal: land subsidised by the government

We assumed that the land would be subsidised for this project as it supports the sustainable goals of the UAE government to encourage and support investors. We assumed that the outcome would be more attractive for both investors and the UAE government. So, we used the NPV risk method on the same scenarios to show how it will affect the NPV. Therefore, the cost of renting land is eliminated in the current assumption.

Figure 5a–d shows the NPV sensitivity after eliminating the cost of renting land from the project in each scenario.

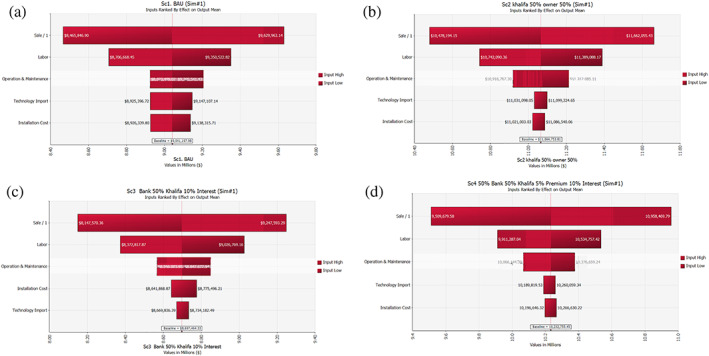

FIGURE 5.

(a) Tornado graph showing the NPV sensitivity in dollars after eliminating the cost of renting land in Scenario 1. (b) Tornado graph showing the NPV sensitivity in dollars after eliminating the cost of renting land in Scenario 2. (c) Tornado graph showing the NPV Sensitivity in dollars after eliminating the cost of renting land in Scenario 3. (d) Tornado graph showing the NPV Sensitivity in dollars after eliminating the cost of renting land in Scenario 4 [Colour figure can be viewed at wileyonlinelibrary.com]

Eliminating the cost of renting land has an enormous impact on the NPV of the project. All the four scenarios show a high positive impact on its NPV, which is more attractive to investors. Also, in the government's interest, it would boost the local economy while reaching the long‐run sustainability.

The results obtained out of four scenarios and related scenarios, 5A–5D, are summarised in Table 3.

TABLE 3.

Summary of NPVs from various scenarios

| Scenario no. | Description | Approx. NPV (in million USD) |

|---|---|---|

| 1 | Business as usual | 3.65 |

| 2 | Full support from Khalifa funding | 6.53 |

| 3 | 50% Khalifa funding + 10% interest rate | 4.05 |

| 4 | 50% bank borrowing at 10% interest rate + 50% Khalifa funding, and 5% premium | 5.58 |

| 5 A | Scenario 1 + free land | 9.04 |

| 5B | Scenario 2 + free land | 11.06 |

| 5C | Scenario 3 + free land | 8.69 |

| 5D | Scenario 4 + free land | 10.23 |

Through the presentation of the results of each scenario in Table 3, it was evident that land subsidisation is a robust policy tool. The NPV of the scenarios (5A–5D) varies from $8.69 million to $11.06 million, whereas in the scenarios (1–4), where land subsidies are not considered, the NPV varies from $3.65 to $6.53 million, which is significantly low compared with 5A–5D. Thus, it is indicated through results that land subsidies can play a critical role in attracting investors, and since the profits are significantly high, an ample of scope for the regulator to charge tax does exist, creating a win‐win situation for an investor in terms of higher returns, the government in the context of encouraging competition and collect higher revenue from taxes and the consumers as they can receive electricity at lower prices through increased suppliers in the market.

5. CONCLUSIONS

The study evaluated 5 MW of concentrated solar plants in the UAE. The results found by the NPV risk method proposed dissimilarities in the project performance (NPV) in each scenario. In general, a positive NPV is obtained from all scenarios. However, Scenarios 1 and 3 showed the least NPV, where the bank interest rate played a significant role in the reduction of the NPV comparing with the other scenarios. Through macroeconomics policies of marginal efficiencies of capital, it is evident that higher interest rates through bank borrowing reduce the willingness to borrow, thus affecting the businesses during the market expansion period. However, during a recession, when the government intervene in the economy by pumping money and reducing interest rates for enhancing market performance, this might be the ideal time for businesses to take loans. Alternatively, a policy in favour of energy project investment that discounts the interest rates for intermittent projects (also during economy expansion) can be an idea that can attract investors. Such consistent support will mean a great trust in the market and government, which can eventually attract the local and foreign investors in the short and long run. While, in Scenarios 2 and 4, the highest NPV where obtained, Khalifa fund and premium played the key role in these scenarios. Overall, the maximum NPV gained was from Scenario 2. Funding support through Khalifa funds has witnessed a few success stories in the UAE, where local investors were benefitted. For instance, a mention of various projects can be found in Malik and Abdallah (2019) and Minhas (2018). Since the cost of energy investment is high, government support in renewable business through funding has created a significant successful sustainable project (Carfora, Romano, Ronghi, & Scandurra, 2017; Saculsan & Mori, 2018; Schwerhoff & Sy, 2017). Thus, clear support is found in the literature that mentions a need for funding option available in the country's local context to support sustainable and clean energy. Although a Khalifa funding is specific to UAE, the concept can be generalised in the local business environment of various countries in the context of projects that require consistent government support and priority for accelerating energy businesses and generating cleaner energy. Taking into account the homogeneity in geography and culture, such policy can be generalised in neighbouring countries, such as Saudi Arabia, Oman, Kuwait and Bahrain, then compared with other far located countries, especially the one that may have geographical disadvantage in terms of reception of solar radiation annually. Additionally, with technological advancements, the production cost of concentrated solar panels has dropped significantly over a period of time, which has eventually reduced the levelized cost of electricity generation through the mentioned technology. Thus, globally, the importing of panels at cheaper rates can provide additional financial leverage to the companies to invest in their local countries, as long as their local government supports the clean energy business by not elevating the taxes on electricity generation and its sales.

A new proposal was identified during this study to understand the impact of eliminating the cost of renting land on the NPV of the project, assuming that the land will be offered on 100% subsidy by the country. It was estimated that 100% of land subsidy has a significant positive impact on the NPV of the project in all scenarios. Thus, the provision of subsidised land has a more significant economic impact, as shown in Table 3. This policy provision also indicates an opportunity for the government to tax the investor at a higher rate; thus, the economic benefit increases not only leaving the scope for investors to make significantly high profits but also have higher financial reserve through reasonable taxation.

Through the simulations, it is found that government support is critical in harnessing renewable energy projects. Despite the tremendous geographical potential to generate clean energy, clean energy is not significantly produced to be consumed locally at the domestic and industrial levels. Thus, it will not only encourage the utilisation of available land with high potential of clean energy generation but in turn also enhance the level of employability and economic development. Significant utilisation of land not only increases the chance of higher production of energy for local consumption but the extra generated energy can be transmitted to neighbouring countries as well, which can be a source of earning as well for the nation. The higher energy generation may also lead to lower electricity prices, and thus, it can boost the investors' interest in other industrial sectors too. Overall, the policies can be framed in the local context; however, it can also be primarily generalised to the global context depending on the availability of resources, government willingness to harness the potential and the participation by the stakeholders/investors.

The study also incorporates several limitations. (1) Given the nature of the study, a set of variables have been used, and their values, based on the logical framework and underlying literature, were assumed to represent the realistic situation in future. Nevertheless, in practice, when the project is implemented, the values may significantly affect due to factors such as regulators import policies affecting the total shipping cost, technology supply, labour policies, other operational costs and so forth. (2) The methodology that we used has a limitation as well. First, unlike the real options approach, the NPV method does not provide the flexibility in decision making for projects that need an expansion or needs to be delayed. Nevertheless, the objective of the study is to evaluate new project, so NPV method is robust as well in the current context. Second, in calculations, we used linear assumptions over different periods at several stages, which may vary in a realistic situation. Third, the study was conducted in 2019, and the current change in the business scenario due to Covid‐19 pandemic is not accounted for in the project, whereas, in the real situation, the project may have significantly less chance to be implemented in 2020. Fourth, the decision parameter of NPV is that if the value is higher than zero, the investor must accept the project. However, all the assumed scenarios in the study have values higher than zero; therefore, the subjectivity of the authors engaged in presenting the results of the study. (3) Fines and penalties associated with the mishandling of the operational and labour process are not incorporated in the project, which is another limitation.

In future studies, we propose more investigation concerning different stakeholders involved in the generation and consumption of clean energy. Additionally, since the availability of land is not a limitation, we recommend the government to frame a policy to offer highly subsidised land for such businesses that might encourage the local and foreign investors to invest in hefty projects within the country.

ACKNOWLEDGEMENTS

We are thankful and fortunate enough to get constant encouragement, support and guidance from all the teaching staff of the College of Business Administration, which helped us in completing our project work. No funding is received to execute this study. Although a due care is taken while writing a paper, methodology, and cost estimation, it is possible to have errors in the paper that can be revised during future projects.

Sisodia GS, Awad E, Alkhoja H, Sergi BS. Strategic business risk evaluation for sustainable energy investment and stakeholder engagement: A proposal for energy policy development in the Middle East through Khalifa funding and land subsidies. Bus Strat Env. 2020;29:2789–2802. 10.1002/bse.2543

Footnotes

Fulfilling the Promise of Concentrating Solar Power. Accessed on 18 February 2019.http://large.stanford.edu/courses/2013/ph240/rajavi1/docs/PoolSolarPower‐report‐3.pdf

2014: The year of concentrating solar power. Accessed on 18 February 2019. https://www.energy.gov/sites/prod/files/2014/10/f18/CSP‐report‐final‐web.pdf

Solar energy review: Technology, markets and policies. The World Bank Group. Accessed on 19 February 2019. http://freefutures.org/wpcontent/uploads/2014/02/2010_World_Solar_Energy_Review_Technology_Markets_and_Policies.pdf

Progress Seen in the Development of Concentrating Solar Power in India Accessed on 23 February 2019. https://www.asiabiomass.jp/english/topics/1210_04.html

CSP companies to look out for in 2018. Accessed on 19 February 2019. https://www.disruptordaily.com/8-csp-companies-look-2018/

Renewable Energy Technologies: cost analysis series. Concentrating Solar Power. IRENA Working Paper. Accessed on 19 February 2019.https://www.irena.org/documentdownloads/publications/re_technologies_cost_analysis-csp.pdf

Technology Roadmap‐Concentrating solar power, IEA. Accessed on 20 February 2019. https://www.iea.org/publications/freepublications/publication/csp_roadmap.pdf

APICORP Energy Research, 2017. Accessed on 20 February 2019.http://www.apicorparabia.com/Research/EnergyReseach/2017/APICORP_Energy_Research_V03_N02_2017.pdf

Dubai's ruler breaks ground world's biggest concentrated solar power projects. Accessed on 27 February 2019.https://gulfbusiness.com/dubais-ruler-breaks-ground-worlds-biggest-concentrated-solar-power-project/

Dubai increases capacity 4.4b CSP solar project. Accessed on 27 February 2019https://www.meed.com/dubai-increases-capacity-4-4bn-csp-solar-project/.

Middle East and North Africa Concentrating Solar Power Knowledge and Innovation Program. Accessed on 22 February 2019. https://www.cmimarseille.org/fr/node/3675

The Middle East and North Africa Concentrated Solar Power Knowledge and Innovation Program. Accessed on 22 February 2019. http://pubdocs.worldbank.org/en/608591486394607927/MENA-CSP-Knowledge-and-Innovation-Program-EN.pdf

Concentrated Solar Power projects in the Middle East and North Africa (MENA. Accessed on 22 February 2019. http://helioscsp.com/concentrated-solar-power-projects-in-the-middle-east-and-north-africa-mena/

MENA CSP Technical Assistance Program Project Approval Request Public Document. Accessed on 27 February 2019. http://pubdocs.worldbank.org/en/684591531831054791/4146-XCTFMB032A-Middle-East-and-North-Africa-region-Cover-Page-and-Project-Document-Revised.pdf

The Middle East and North Africa (MENA) Region Assessment of the Local Manufacturing Potential for Concentrated Solar Power (CSP) Projects. Accessed on 26 February 2019. http://siteresources.worldbank.org/INTMENA/Resources/CSP‐Job‐Study‐Eng‐Sum.pdf

IRENA (2016), Renewable Energy Policies in a Time of Transition, IRENA, Abu Dhabi

NREL (2016b), Financial incentives to enable clean energy Deployment, NREL, Golden, CO, www.nrel.gov/docs/fy16osti/65541.pdf.

CEER (Council of European Energy Regulators) (2016), Key Support Elements of RES in Europe: Moving Towards Market Integration, CEER

MRC Report, (2018). Electricity Supply Cost of Service Study – LEWA Lesotho. Accessed on 15 Januray 2020. https://nul-erc.s3.amazonaws.com/public/documents/reports/cost-of-service-study-1543817960.pdf

https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2018/Jan/IRENA_2017_Power_Costs_2018.pdf Downloaded 28 Apr 2020

https://www.adb.org/sites/default/files/publication/566266/adbi-wp1078.pdf Downloaded 28 Apr 2020

The 20% higher sales represent better NPV. Whereas 20% higher cost results in lower NPV. Therefore, the case is reciprocal in the context of costs.

REFERENCES

- Aba, M. , Ladeinde, A. , & Afimia, E. (2019). Economic evaluation of hybrid renewable energy systems for electricity generation in Nigeria: A discounted cash flow analysis. Journal of Energy Research and Reviews, 1–10. [Google Scholar]

- Abrell, J. , & Rausch, S. (2016). Cross‐country electricity trade, renewable energy and European transmission infrastructure policy. Journal of Environmental Economics and Management, 79, 87–113. 10.1016/j.jeem.2016.04.001 [DOI] [Google Scholar]

- Albrizio, S. , Kozluk, T. , & Zipperer, V. (2017). Environmental policies and productivity growth: Evidence across industries and firms. Journal of Environmental Economics and Management, 81, 209–226. 10.1016/j.jeem.2016.06.002 [DOI] [Google Scholar]

- Alizamir, S. , de Véricourt, F. , & Sun, P. (2016). Efficient feed‐in‐tariff policies for renewable energy technologies. Operations Research, 64(1), 52–66. 10.1287/opre.2015.1460 [DOI] [Google Scholar]

- Brent, D. A. , & Ward, M. B. (2018). Energy efficiency and financial literacy. Journal of Environmental Economics and Management, 90, 181–216. 10.1016/j.jeem.2018.05.004 [DOI] [Google Scholar]

- Campos‐Guzmán, V. , García‐Cáscales, M. S. , Espinosa, N. , & Urbina, A. (2019). Life cycle analysis with multi‐criteria decision making: A review of approaches for the sustainability evaluation of renewable energy technologies. Renewable and Sustainable Energy Reviews, 104, 343–366. 10.1016/j.rser.2019.01.031 [DOI] [Google Scholar]

- Carfora, A. , Romano, A. A. , Ronghi, M. , & Scandurra, G. (2017). Renewable generation across Italian regions: Spillover effects and effectiveness of European regional fund. Energy Policy, 102, 132–141. 10.1016/j.enpol.2016.12.027 [DOI] [Google Scholar]

- Castro, N. R. , & Chousa, J. P. (2006). An integrated framework for the financial analysis of sustainability. Business Strategy and the Environment, 15(5), 322–333. 10.1002/bse.539 [DOI] [Google Scholar]

- Chen, Y. K. , Koduvere, H. , Gunkel, P. A. , Kirkerud, J. G. , Skytte, K. , Ravn, H. , & Bolkesjø, T. F. (2020). The role of cross‐border power transmission in a renewable‐rich power system—A model analysis for northwestern Europe. Journal of Environmental Management, 261, 110194. 10.1016/j.jenvman.2020.110194 [DOI] [PubMed] [Google Scholar]

- Chen, Z. , & Su, S. I. I. (2019). International competition and trade conflict in a dual photovoltaic supply chain system. Renewable Energy, 151, 816–828. [Google Scholar]

- Crago, C. L. , & Chernyakhovskiy, I. (2017). Are policy incentives for solar power effective? Evidence from residential installations in the Northeast. Journal of Environmental Economics and Management, 81, 132–151. 10.1016/j.jeem.2016.09.008 [DOI] [Google Scholar]

- Craig, O. O. , Brent, A. C. , & Dinter, F. (2017). Concentrated solar power (CSP) innovation analysis in South Africa. South African Journal of Industrial Engineering, 28(2), 14–27. [Google Scholar]

- Driels, M. R. , & Shin, Y. S. (2004). Determining the number of iterations for Monte Carlo simulations of weapon effectiveness (No. NPS‐MAE‐04‐005). NAVAL POSTGRADUATE SCHOOL MONTEREY CA DEPT OF MECHANICAL AND ASTRONAUTICAL ENGINEERING. [Google Scholar]

- Fan, J. L. , Xu, M. , Yang, L. , & Zhang, X. (2019). Benefit evaluation of investment in CCS retrofitting of coal‐fired power plants and PV power plants in China based on real options. Renewable and Sustainable Energy Reviews, 115, 109350. 10.1016/j.rser.2019.109350 [DOI] [Google Scholar]

- Flatland, K. , Hove, M. T. , Lavrutich, M. , & Nagy, R. L. G. (2019). Irreversible investment in wind turbines: Life‐extension versus repowering.

- Fleten, S. E. , Linnerud, K. , Molnár, P. , & Nygaard, M. T. (2016). Green electricity investment timing in practice: Real options or net present value? Energy, 116, 498–506. 10.1016/j.energy.2016.09.114 [DOI] [Google Scholar]

- Furlan, C. , & Mortarino, C. (2018). Forecasting the impact of renewable energies in competition with non‐renewable sources. Renewable and Sustainable Energy Reviews, 81, 1879–1886. 10.1016/j.rser.2017.05.284 [DOI] [Google Scholar]

- Garrone, P. , Grilli, L. , & Mrkajic, B. (2018). The role of institutional pressures in the introduction of energy‐efficiency innovations. Business Strategy and the Environment, 27(8), 1245–1257. 10.1002/bse.2072 [DOI] [Google Scholar]

- Gatto, A. , & Drago, C. (2020). Measuring and modeling energy resilience. Ecological Economics, 172, 106527. 10.1016/j.ecolecon.2019.106527 [DOI] [Google Scholar]

- Grau, T. , Huo, M. , & Neuhoff, K. (2012). Survey of photovoltaic industry and policy in Germany and China. Energy Policy, 51, 20–37. 10.1016/j.enpol.2012.03.082 [DOI] [Google Scholar]

- Guidolin, M. , & Guseo, R. (2016). The German energy transition: Modeling competition and substitution between nuclear power and renewable energy technologies. Renewable and Sustainable Energy Reviews, 60, 1498–1504. 10.1016/j.rser.2016.03.022 [DOI] [Google Scholar]

- Haddad, B. , Liazid, A. , & Ferreira, P. (2017). A multi‐criteria approach to rank renewables for the Algerian electricity system. Renewable Energy, 107, 462–472. 10.1016/j.renene.2017.01.035 [DOI] [Google Scholar]

- Held, A. , Ragwitz, M. , Del Rio, P. , Resch, G. , Klessmann, C. , Hassel, A. , … Rawlins, J. (2019). Do almost mature renewable energy technologies still need dedicated support towards 2030? Economics of Energy & Environmental Policy, 8(2). 10.5547/2160-5890.8.2.ahel [DOI] [Google Scholar]

- Horbach, J. , & Rammer, C. (2018). Energy transition in Germany and regional spill‐overs: The diffusion of renewable energy in firms. Energy Policy, 121, 404–414. 10.1016/j.enpol.2018.06.042 [DOI] [Google Scholar]

- Kaya, O. , Klepacka, A. M. , & Florkowski, W. J. (2019). Achieving renewable energy, climate, and air quality policy goals: Rural residential investment in solar panel. Journal of Environmental Management, 248, 109309. 10.1016/j.jenvman.2019.109309 [DOI] [PubMed] [Google Scholar]

- Kim, K. , Park, H. , & Kim, H. (2017). Real options analysis for renewable energy investment decisions in developing countries. Renewable and Sustainable Energy Reviews, 75, 918–926. 10.1016/j.rser.2016.11.073 [DOI] [Google Scholar]

- Kumar, A. , Sah, B. , Singh, A. R. , Deng, Y. , He, X. , Kumar, P. , & Bansal, R. C. (2017). A review of multi criteria decision making (MCDM) towards sustainable renewable energy development. Renewable and Sustainable Energy Reviews, 69, 596–609. 10.1016/j.rser.2016.11.191 [DOI] [Google Scholar]

- Leicester, P. A. , Goodier, C. I. , & Rowley, P. (2016). Probabilistic evaluation of solar photovoltaic systems using Bayesian networks: A discounted cash flow assessment. Progress in Photovoltaics: Research and Applications, 24(12), 1592–1605. 10.1002/pip.2754 [DOI] [Google Scholar]

- Linn, J. , & Shih, J. S. (2019). Do lower electricity storage costs reduce greenhouse gas emissions? Journal of Environmental Economics and Management, 96, 130–158. 10.1016/j.jeem.2019.05.003 [DOI] [Google Scholar]

- Loncar, D. , Milovanovic, I. , Rakic, B. , & Radjenovic, T. (2017). Compound real options valuation of renewable energy projects: The case of a wind farm in Serbia. Renewable and Sustainable Energy Reviews, 75, 354–367. 10.1016/j.rser.2016.11.001 [DOI] [Google Scholar]

- Low, J. S. C. , & Ng, Y. T. (2018). Improving the economic performance of remanufacturing systems through flexible design strategies: A case study based on remanufacturing laptop computers for the Cambodian market. Business Strategy and the Environment, 27(4), 503–527. 10.1002/bse.2017 [DOI] [Google Scholar]

- Mahdy, M. , & Bahaj, A. S. (2018). Multi criteria decision analysis for offshore wind energy potential in Egypt. Renewable Energy, 118, 278–289. 10.1016/j.renene.2017.11.021 [DOI] [Google Scholar]

- Malik, M. , & Abdallah, S. (2019). Sustainability initiatives in emerging economies: A socio‐cultural perspective. Sustainability, 11(18), 4893. 10.3390/su11184893 [DOI] [Google Scholar]

- Malladi, K. T. , & Sowlati, T. (2018). Biomass logistics: A review of important features, optimization modeling and the new trends. Renewable and Sustainable Energy Reviews, 94, 587–599. 10.1016/j.rser.2018.06.052 [DOI] [Google Scholar]

- Marques, A. C. , Fuinhas, J. A. , & Macedo, D. P. (2019). The impact of feed‐in and capacity policies on electricity generation from renewable energy sources in Spain. Utilities Policy, 56, 159–168. 10.1016/j.jup.2019.01.001 [DOI] [Google Scholar]

- Minhas, W. A. (2018). Role of government. In Advancing entrepreneurship in the United Arab Emirates (pp. 173–189). Palgrave Macmillan, Cham, DOI: 10.1007/978-3-319-76436-8_7 [DOI] [Google Scholar]

- Mokryani, G. , Hu, Y. F. , Papadopoulos, P. , Niknam, T. , & Aghaei, J. (2017). Deterministic approach for active distribution networks planning with high penetration of wind and solar power. Renewable Energy, 113, 942–951. 10.1016/j.renene.2017.06.074 [DOI] [Google Scholar]

- Naz, M. N. , Mushtaq, M. I. , Naeem, M. , Iqbal, M. , Altaf, M. W. , & Haneef, M. (2017). Multicriteria decision making for resource management in renewable energy assisted microgrids. Renewable and Sustainable Energy Reviews, 71, 323–341. 10.1016/j.rser.2016.12.059 [DOI] [Google Scholar]

- Pablo‐Romero, M. D. P. , Sánchez‐Braza, A. , Salvador‐Ponce, J. , & Sánchez‐Labrador, N. (2017). An overview of feed‐in tariffs, premiums and tenders to promote electricity from biogas in the EU‐28. Renewable and Sustainable Energy Reviews, 73, 1366–1379. 10.1016/j.rser.2017.01.132 [DOI] [Google Scholar]

- Pan, X. , Chen, X. , Sinha, P. , & Dong, N. (2020). Are firms with state ownership greener? An institutional complexity view. Business Strategy and the Environment, 29(1), 197–211. 10.1002/bse.2358 [DOI] [Google Scholar]

- Pantaleo, A. M. , Camporeale, S. M. , Miliozzi, A. , Russo, V. , Shah, N. , & Markides, C. N. (2017). Novel hybrid CSP‐biomass CHP for flexible generation: Thermo‐economic analysis and profitability assessment. Applied Energy, 204, 994–1006. 10.1016/j.apenergy.2017.05.019 [DOI] [Google Scholar]

- Penizzotto, F. , Pringles, R. , & Olsina, F. (2019). Real options valuation of photovoltaic power investments in existing buildings. Renewable and Sustainable Energy Reviews, 114, 109308. 10.1016/j.rser.2019.109308 [DOI] [Google Scholar]

- Peters, M. , Schmidt, T. S. , Wiederkehr, D. , & Schneider, M. (2011). Shedding light on solar technologies—A techno‐economic assessment and its policy implications. Energy Policy, 39(10), 6422–6439. 10.1016/j.enpol.2011.07.045 [DOI] [Google Scholar]

- Pham, L. (2019). Does financial development matter for innovation in renewable energy? Applied Economics Letters, 26(21), 1756–1761. 10.1080/13504851.2019.1593934 [DOI] [Google Scholar]

- Pitelis, A. , Vasilakos, N. , & Chalvatzis, K. (2019). Fostering innovation in renewable energy technologies: Choice of policy instruments and effectiveness. Renewable Energy, 151, 1163–1172. [Google Scholar]

- Pitz‐Paal, R. , Amin, A. , Oliver Bettzuge, M. , Eames, P. , Flamant, G. , Fabrizi, F. , Holmes, J. , Kribus, A. , Van Der Laan, H. , Lopez, C. and Garcia Novo, F. (2012). Concentrating solar power in Europe, the Middle East and North Africa: Achieving its potential. In EPJ Web of Conferences (Vol. 33, p. 03004). EDP Sciences. [Google Scholar]

- Potts, S. (2019). An exploratory study of the South African concentrated solar power sector using the technological innovation systems framework (Doctoral dissertation, University of Pretoria).

- Quan, Y. , Wu, H. , Li, S. , & Ying, S. X. (2018). Firm sustainable development and stakeholder engagement: The role of government support. Business Strategy and the Environment, 27(8), 1145–1158. 10.1002/bse.2057 [DOI] [Google Scholar]

- Quansah, D. A. , & Adaramola, M. S. (2019). Assessment of early degradation and performance loss in five co‐located solar photovoltaic module technologies installed in Ghana using performance ratio time‐series regression. Renewable Energy, 131, 900–910. 10.1016/j.renene.2018.07.117 [DOI] [Google Scholar]

- Rahmani‐Andebili, M. (2017). Stochastic, adaptive, and dynamic control of energy storage systems integrated with renewable energy sources for power loss minimization. Renewable Energy, 113, 1462–1471. 10.1016/j.renene.2017.07.005 [DOI] [Google Scholar]

- Robert, F. C. , Sisodia, G. S. , & Gopalan, S. (2017, March). The critical role of anchor customers in rural microgrids: Impact of load factor on energy cost. In 2017 International Conference on Computation of Power, Energy Information and Commuincation (ICCPEIC) (pp. 398‐403). IEEE.

- Robert, F. C. , Sisodia, G. S. , & Gopalan, S. (2018). A critical review on the utilization of storage and demand response for the implementation of renewable energy microgrids. Sustainable Cities and Society, 40, 735–745. 10.1016/j.scs.2018.04.008 [DOI] [Google Scholar]

- Rosenfeld, D. C. , Böhm, H. , Lindorfer, J. , & Lehner, M. (2020). Scenario analysis of implementing a power‐to‐gas and biomass gasification system in an integrated steel plant: A techno‐economic and environmental study. Renewable Energy, 147, 1511–1524. 10.1016/j.renene.2019.09.053 [DOI] [Google Scholar]

- Saculsan, P. G. J. , & Mori, A. (2018). What can the Philippines learn from Thailands ENCON fund in overcoming the barriers to developing renewable energy resources. 6, 278–283. 10.18178/JOCET.2018.6.4.474 [DOI] [Google Scholar]

- Salehin, S. , Ferdaous, M. T. , Chowdhury, R. M. , Shithi, S. S. , Rofi, M. B. , & Mohammed, M. A. (2016). Assessment of renewable energy systems combining techno‐economic optimization with energy scenario analysis. Energy, 112, 729–741. 10.1016/j.energy.2016.06.110 [DOI] [Google Scholar]

- Schwerhoff, G. , & Sy, M. (2017). Financing renewable energy in Africa—Key challenge of the sustainable development goals. Renewable and Sustainable Energy Reviews, 75, 393–401. 10.1016/j.rser.2016.11.004 [DOI] [Google Scholar]

- Shao, J. (2019). Sustainable consumption in China: New trends and research interests. Business Strategy and the Environment, 28(8), 1507–1517. 10.1002/bse.2327 [DOI] [Google Scholar]

- Shimbar, A. , & Ebrahimi, S. B. (2020). Political risk and valuation of renewable energy investments in developing countries. Renewable Energy, 145, 1325–1333. 10.1016/j.renene.2019.06.055 [DOI] [Google Scholar]

- Sisodia, G. S. , & Soares, I. (2015). Panel data analysis for renewable energy investment determinants in Europe. Applied Economics Letters, 22(5), 397–401. 10.1080/13504851.2014.946176 [DOI] [Google Scholar]

- Sisodia, G. S. , Soares, I. , & Ferreira, P. (2016a). Modeling business risk: The effect of regulatory revision on renewable energy investment‐The Iberian case. Renewable Energy, 95, 303–313. 10.1016/j.renene.2016.03.076 [DOI] [Google Scholar]

- Sisodia, G. S. , Soares, I. , & Ferreira, P. (2016b). The effect of sample size on European Union's renewable energy investment drivers. Applied Economics, 48(53), 5129–5137. 10.1080/00036846.2016.1173176 [DOI] [Google Scholar]

- Soroudi, A. , Rabiee, A. , & Keane, A. (2017). Distribution networks' energy losses versus hosting capacity of wind power in the presence of demand flexibility. Renewable Energy, 102, 316–325. 10.1016/j.renene.2016.10.051 [DOI] [Google Scholar]

- Stephenson, K. , & Shabman, L. (2019). Does ecosystem valuation contribute to ecosystem decision making? Evidence from hydropower licensing. Ecological Economics, 163, 1–8. 10.1016/j.ecolecon.2019.05.003 [DOI] [Google Scholar]

- Tomar, V. , & Tiwari, G. N. (2017). Techno‐economic evaluation of grid connected PV system for households with feed in tariff and time of day tariff regulation in New Delhi—A sustainable approach. Renewable and Sustainable Energy Reviews, 70, 822–835. 10.1016/j.rser.2016.11.263 [DOI] [Google Scholar]

- Trieb, F. , Schillings, C. , O'sullivan, M. , Pregger, T. , & Hoyer‐Klick, C. (2009, September). Global potential of concentrating solar power. In SolarPACES Conference (pp. 15‐18).

- van der Ploeg, F. , & Rezai, A. (2020). The risk of policy tipping and stranded carbon assets. Journal of Environmental Economics and Management, 100, 102258. 10.1016/j.jeem.2019.102258 [DOI] [Google Scholar]

- Walters, T. , Esterly, S. , Cox, S. , Reber, T. , & Rai, N. (2015). Policies to spur energy access: Volume 1. Engaging the private sector in expanding access to electricity. Golden, CO: NREL. www.nrel.gov/docs/fy15osti/64460-1.pdf [Google Scholar]

- Wang, Y. , Yan, W. , Zhuang, S. , & Zhang, Q. (2019). Competition or complementarity? The hydropower and thermal power nexus in China. Renewable Energy, 138, 531–541. 10.1016/j.renene.2019.01.130 [DOI] [Google Scholar]

- Wicki, S. , & Hansen, E. G. (2019). Green technology innovation: Anatomy of exploration processes from a learning perspective. Business Strategy and the Environment, 28(6), 970–988. 10.1002/bse.2295 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Xie, R. H. , Yuan, Y. J. , & Huang, J. J. (2017). Different types of environmental regulations and heterogeneous influence on “green” productivity: Evidence from China. Ecological Economics, 132, 104–112. 10.1016/j.ecolecon.2016.10.019 [DOI] [Google Scholar]

- Yang, X. , He, L. , Xia, Y. , & Chen, Y. (2019). Effect of government subsidies on renewable energy investments: The threshold effect. Energy Policy, 132, 156–166. 10.1016/j.enpol.2019.05.039 [DOI] [Google Scholar]

- Ye, L. C. , Rodrigues, J. F. , & Lin, H. X. (2017). Analysis of feed‐in tariff policies for solar photovoltaic in China 2011–2016. Applied Energy, 203, 496–505. 10.1016/j.apenergy.2017.06.037 [DOI] [Google Scholar]

- Zafar, M. W. , Shahbaz, M. , Hou, F. , & Sinha, A. (2019). From nonrenewable to renewable energy and its impact on economic growth: The role of research & development expenditures in Asia‐Pacific Economic Cooperation countries. Journal of Cleaner Production, 212, 1166–1178. 10.1016/j.jclepro.2018.12.081 [DOI] [Google Scholar]