Abstract

Poverty has consistently been linked to poor mental health and risky health behaviors, yet few studies evaluate the effectiveness of programs and policies to address these outcomes by targeting poverty itself. We test the hypothesis that the earned income tax credit (EITC)—the largest U.S. poverty alleviation program—improves short-term mental health and health behaviors in the months immediately after income receipt. We conducted parallel analyses in two large longitudinal national data sets: the National Health Interview Survey (NHIS, 1997–2016, N=379,603) and the Panel Study of Income Dynamics (PSID, 1985–2015, N=29,808). Outcomes included self-rated health, psychological distress, tobacco use, and alcohol consumption. We employed difference-in-differences analysis, a quasi-experimental technique. We exploited seasonal variation in disbursement of the EITC, which is distributed as a tax refund every spring: we compared outcomes among EITC-eligible individuals interviewed immediately after refund receipt (Feb-Apr) with those interviewed in other months more distant from refund receipt (May-Jan), “differencing out” seasonal trends among non-eligible individuals. For most outcomes, we were unable to rule out the null hypothesis that there was no short-term effect of the EITC. Findings were cross-validated in both data sets. The exception was an increase in smoking in PSID, although this finding was not robust to sensitivity analyses. While we found no short-term “check effect” of the EITC on mental health and health behaviors, others have found long-term effects on these outcomes. This may be because recipients anticipate EITC receipt and smooth their income accordingly.

Keywords: difference-in-differences, earned income tax credit, poverty alleviation, mental health, health behaviors

INTRODUCTION

Poverty and low socioeconomic status have consistently been linked to poor physical and mental health.1–3 In particular, financial stress and lack of income have been shown to be strong predictors of psychological distress and poor mental health.4 This in turn is thought to increase risky health behaviors like smoking and alcohol consumption, which may represent coping mechanisms to deal with repeated psychosocial stressors, or consequences of the chronic stress of poverty that leads to poor decision-making and reduced cognitive “bandwidth” to resist temptation goods.5–8 Poverty may also reduce access to healthcare and the ability to afford mental health and substance use treatment.9 Alternately, low-income groups are often selectively targeted by tobacco and alcohol industry marketing strategies, which may explain this association.10–12

Despite extensive literature documenting the links between poverty, mental health, and health behaviors, there is limited work in high-income countries testing the effectiveness of programs and policies to address mental health and substance use by targeting poverty itself. Randomized controlled trials of cash transfers abroad have shown that income receipt improves mental health among recipients.13–19 In the U.S., a recent trial found that a conditional cash transfer program led to reductions in adolescent aggression and substance use, but no improvements in mental health.20 U.S. government transfer payments have been associated with higher rates of smoking, social drinking, mortality, and drug-related hospitalizations shortly after income receipt, a phenomenon known as the “check effect.”21–23 These mixed findings may be because individual psychological and behavioral responses to income receipt are complex and variable, e.g., depending on the frequency, size, and dependability of payments, and on characteristics of the recipient.24

The largest U.S. poverty alleviation program is the earned income tax credit (EITC). The EITC is distributed to low-income working families in the form of a lump-sum refund during tax season (typically February to April). In 2018, 25 million individuals and families received approximately $63 billion with an average refund of $2,488 per household.25 Most studies suggest that the EITC reduces poverty and increases employment, and that effects are stronger among single mothers,26,27 although the evidence is mixed for employment.28 Additionally, the EITC has been shown to reduce smoking, improve food security, and increase purchase of healthy foods,29–32 contributing to its potential cost effectiveness as a health policy investment.33 It also increases access to health insurance, which may improve access to healthcare, including mental health and substance use treatment.31,34–36 At the same time, studies have shown that it is associated with worsened metabolic markers in adults and increased obesity among adults and children.29,37 The negative impacts of the EITC on health behaviors may be because the added income is spent on unhealthy goods; in economic terms, unhealthy foods, tobacco, and alcohol may be “normal goods” that individuals purchase more when they have more available income, although recent evidence tends to refute this idea.38 Alternately, it may be because of the work requirement; EITC recipients often work in low-wage stressful jobs, and consumption of unhealthy food, tobacco, and alcohol may represent coping mechanisms to deal with the added stress.7

With regards to mental health, two studies found that EITC-eligible mothers showed improvements in depressive symptoms, happiness, and self-esteem, and fewer poor mental health days.39,40 While these studies relied on older data (prior to 2002), studies using more recent data found that the EITC is associated with a decrease in suicides.41,42 All of these studies relied on crude proxies for EITC eligibility (e.g., educational attainment or presence of a state EITC program); while these proxies are intended to reduce bias by addressing the confounding between earned income and health, they also result in misclassification that could introduce bias even if it is non-differential.43

In the present study, we examined the effect of the EITC on mental health and health behaviors. We take advantage of seasonal variation in EITC refund receipt to identify its short-term effects using quasi-experimental methods. Examining the effects of the EITC in the short term in particular has important public health implications. On the one hand, finding adverse outcomes on health behaviors akin to the “check effect” described above may imply the need for adjustments to the policy to minimize these impacts. Additionally, understanding how low-income individuals respond to poverty alleviation in the form of lump-sum disbursements (in contrast to more frequent disbursements such as increased minimum wage) may also inform the design of future income programs and policies and adds to our knowledge of consumption smoothing in this context. To fill this gap in the literature, we employ two large diverse national datasets with detailed sociodemographic information on participants to more accurately classify individuals’ EITC eligibility. This research comes at an important time when state and federal governments are actively discussing expansions to the EITC program.

METHODS

Sample

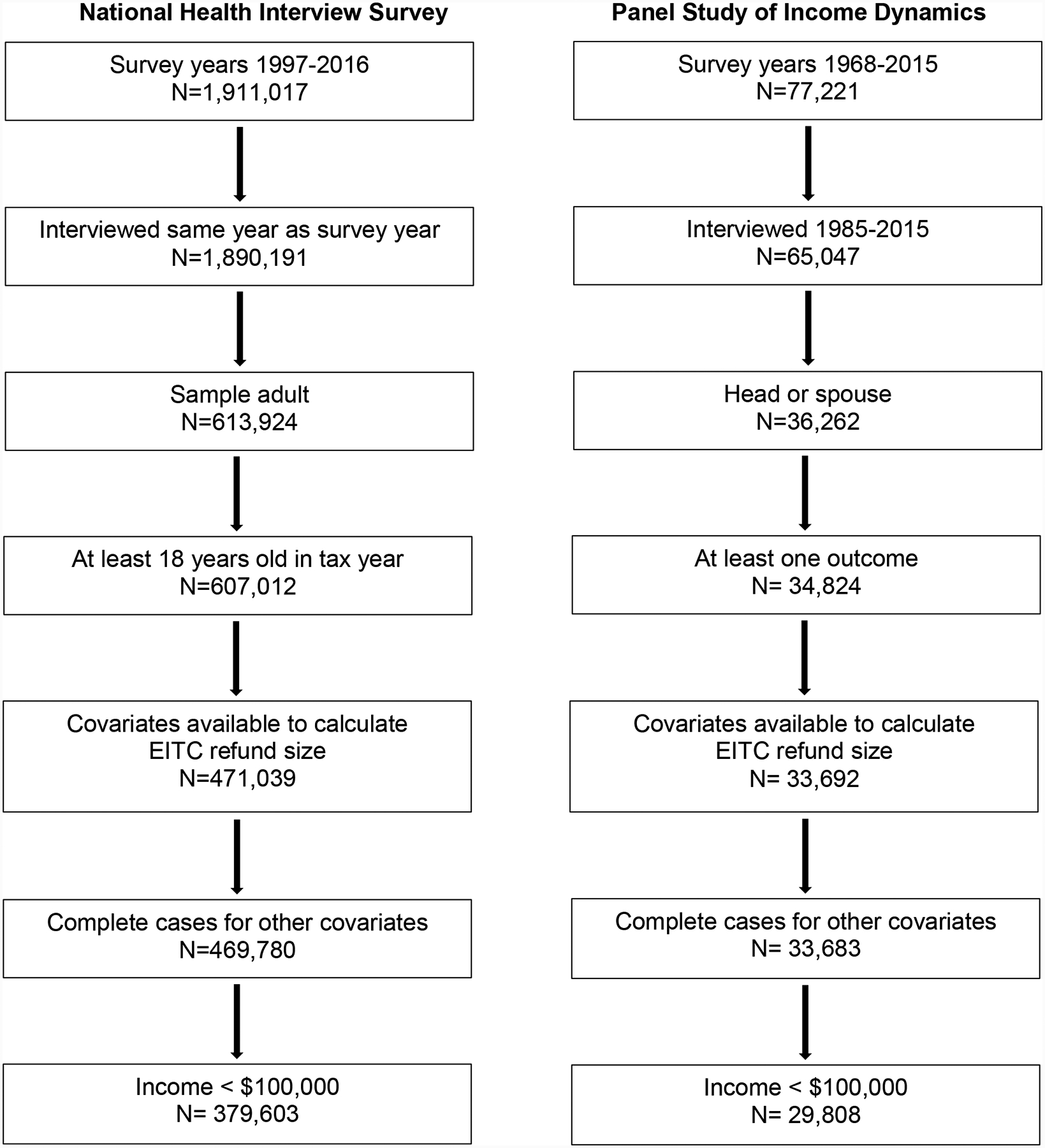

For this study, we conducted parallel analyses in two large longitudinal national datasets (Figure 1). The first was the National Health Interview Survey (NHIS), a serial cross-sectional household survey. We used the 1997–2016 survey waves, as prior waves differed in survey design and content. The second was the Panel Study of Income Dynamics (PSID), a longitudinal household survey interviewing the same families since 1968.44 We used the 1985–2015 survey waves, which included our outcomes of interest. We also restricted the sample to those with income greater than $0 and less than $100,000, to make the “control” group more comparable to EITC-eligible individuals. The sample included 379,603 persons in NHIS and 29,808 persons (181,784 person-years) in PSID.

Figure 1.

Sample Flowchart

Note: Due to the structure of each data set, exclusion criteria were tailored to be appropriate for each sample. In PSID, not all outcomes were asked in all survey years (Supplemental Table 1), resulting in differing numbers of observations (Table 1). EITC: earned income tax credit.

Exposure

The primary exposure was the amount of EITC for which individuals were eligible, rescaled to thousands of inflation-adjusted U.S. dollars for ease of interpretation. As in most national surveys, NHIS and PSID do not include questions about EITC receipt. Therefore, the EITC refund size for which an individual was eligible was calculated using the Taxsim27 package for Stata, which uses U.S. Internal Revenue Service (IRS) tax formulas that incorporate changes in federal and state legislation for every year.45 Taxsim inputs included age and marital status of the household head, pre-tax household income, number of children under 18 living in the home, state of residence, and tax year. Previous studies have shown that about 80% of households actually received the EITC refund for which they were eligible, so this approach results in some measurement error; however, it is analogous to an intent-to-treat approach and is likely to underestimate the EITC’s effects among those who actually received the refund. This strategy has been used in numerous prior studies of the EITC’s effects on economic and health outcomes.29,46–53 Variation in the EITC results from changes to the IRS formulas over time and implementation of state EITC programs that provide an additional supplement to the federal refund. Roughly half of states have implemented supplemental EITC programs over the past decades.54 Supplemental Figure 1 illustrates variation in mean EITC refund size in this sample, by year and number of children.

Outcomes

We examined several outcomes related to mental health and health behaviors that were similar in both NHIS and PSID and were likely to change in the short term, i.e., within 1–2 months of refund receipt. Most prior work has examined the effects of the EITC on year-to-year changes in outcomes, although a handful have examined short-term outcomes in the range that we evaluate here.29,46,55 We are unable to examine much shorter follow-up times, e.g., days to weeks, because we are not able to determine the exact date on which eligible individuals received their refunds using NHIS and PSID.

In NHIS, self-rated health was captured as a binary variable representing currently having better/same health (versus worse) compared to the prior year. In PSID, we constructed a binary variable representing whether the participant currently had excellent or very good health (versus good, fair, or poor). In both data sets, mental health was assessed via the Kessler-6 (K6) scale, a validated questionnaire that captures psychological distress and that was developed to screen for mental illness in the general population. Higher scores indicate greater psychological distress (range 0–24).56,57 In both data sets, smoking questions included a binary variable for current smoking status and a continuous variable for number of cigarettes smoked per day (zero for non-smokers). PSID included a binary variable for current alcohol consumption. While NHIS also included a variable for alcohol consumption, this question referred to consumption during the past year; because our identification strategy focuses on short-term variation in health outcomes, we did not include this outcome.

In NHIS, outcomes were asked for all adults in the sample, one per household. In PSID, the K6 was only asked for either the head of household or the spouse, while other outcomes were available for both the head and spouse. In PSID, not all outcomes were asked in all survey years (Table 1), resulting in differing numbers of observations for some outcomes (Supplemental Table 1). We did not impute missing outcome variables, as this is thought to add noise to resulting estimates.58

Table 1.

Sample Characteristics

| NHIS | PSID | |||

|---|---|---|---|---|

| No. Persons | 379,603 | 29,808 | ||

| No. Person-years | - | 181,784 | ||

| Panel A. Demographics | Mean (SD) or % | Mean (SD) or % | ||

| Female | 56.3 | 53.5 | ||

| Age (years) | 47.2 (18.2) | 39.58 (13.08) | ||

| Completed high school | 79.8 | 82.8 | ||

| Married | 56.2 | 52.3 | ||

| Race | ||||

| White | 60.1 | 53.1 | ||

| Black | 15.9 | 36.9 | ||

| Hispanic | 16.1 | 8.3 | ||

| Other | 7.9 | 1.7 | ||

| Number of children | 0.6 (1.1) | 1.0 (1.2) | ||

| Household pre-tax earned incomea | 41,558 (25,982) | 42,114 (26,628) | ||

| EITC eligible | 23.2 | 27.7 | ||

| Total EITC among those eligiblea | 2,188 (1,907) | 1,702 (1,578) | ||

| Panel B. Outcomes | Mean (SD) or % | No. persons | Mean (SD) or % | No. person-years |

| Self-rated healthb | 90.0 | 379,203 | 55.0 | 181,596 |

| Psychological distress | 2.8 (4.2) | 374,26 | 3.5 (3.9) | 39,118 |

| Currently smoke | 23.4 | 378,115 | 24.6 | 73,630 |

| No. cigarettes per day (overall) | 3.2 (7.7) | 377,017 | 3.4 (7.7) | 72,940 |

| No. cigarettes per day (smokers) | 13.9 (10.2) | 87,324 | 13.9 (9.9) | 19,841 |

| Currently drink alcohol | - | 59.8 | 81,458 |

Note: PSID sample drawn from survey years 1985–2015. NHIS sample drawn from survey years 1997–2016. Samples were restricted to households with income above $0 and below $100,000. EITC: earned income tax credit; NHIS: National Health Interview Survey; PSID: Panel Study of Income Dynamics; SD: standard deviation.

Inflation-adjusted U.S. dollars

Binary variable representing “better” or “same” compared with last year (versus “worse”) in NHIS, and “excellent” or “very good” (versus “good,” “fair,” or “poor”) in PSID.

Covariates

Covariates included race, gender, age, age-squared, education, marital status, number of children under 18 living in the home, pre-tax inflation-adjusted household income, income-squared, and year and state fixed effects (i.e., indicator variables).

Statistical Analysis

We first tabulated participant characteristics in each sample. We then estimated the short-term effect of the EITC using a difference-in-difference (DiD) approach for each sample. We took advantage of the fact that over 90% of EITC recipients received their refunds during the months of February, March, and April,59 while NHIS and PSID interviews take place throughout the year and their timing is unlikely to be confounded by individual characteristics. This seasonal variation creates a natural experiment in which EITC recipients interviewed in February-April are interviewed soon after they have received the refund, while those interviewed in May-January have more distant exposure to the refund. Therefore, in each data set, we compared EITC-eligible individuals interviewed in February-April to those interviewed in May-January. In order to factor out seasonal trends in these outcomes over the course of the year, we “differenced out” seasonal differences among non-eligible individuals (i.e., those who were calculated by Taxsim to have received zero EITC based on their demographic characteristics). This approach has been used in prior studies of the short-term effects of the EITC, and additional details are available in the Supplement.29,46,55

Secondary Analyses

To assess whether the effect of the EITC varies by marital status, we conducted a stratified analysis with separate models for unmarried and married individuals.

To examine the robustness of our results, we conducted the analysis using several alternative model specifications. First, to make the non-eligible group more comparable to those who were EITC-eligible, we restricted the sample to those with income >$0 and <$50,000. Second, we examined the effect of the federal EITC only (i.e., excluding state EITC refunds from the exposure). This removes any possible confounding by time-varying state characteristics that might be associated with state EITC program implementation and the health outcomes of interest; state fixed-effects were not included in these federal EITC models. Additional robustness checks are described in the Supplement.

Assumptions for DiD

DiD models assume that the trends in outcomes during the non-exposed months (i.e., May-January) are similar in the treatment and control groups. To assess this “parallel trends assumption,” we plotted trends in outcomes over the course of the year and visually examined whether trends were parallel between EITC-eligible and non-eligible individuals during May-January. We also conducted a “placebo test” by examining the effect of the EITC during different parts of the year in which participants were unlikely to receive the EITC refund. For this analysis, we used May-August as our treatment period and September-December as our control period, excluding participants interviewed in January-April altogether. We would expect to find no effect of the EITC using this model.

Another assumption of DiD is that seasonal trends in the outcomes would have been the same in the treatment and control groups in the absence of the intervention (i.e. the EITC refund). While this counterfactual assumption cannot be empirically tested, we assessed whether there were differential seasonal trends with respect to demographic characteristics between eligible and non-eligible individuals. To do this, we conducted a DiD analysis parallel to our primary analysis, in which we regressed each demographic characteristic (e.g., age, gender) on EITC eligibility, season of interview, and the interaction between these two variables.

Ethics Approval

Ethics approval was obtained from the Institutional Review Board of the senior author’s institution (protocol #17–23255).

RESULTS

Participant Characteristics

Demographic characteristics were similar across NHIS and PSID, with about 55% of participants being female, about 80% having completed high school, and about half being married (Table 1). NHIS had a higher percentage of white and Hispanic participants and a lower percentage of black participants compared with PSID. The mean pre-tax household income in NHIS ($41,558, standard deviation [SD] $25,982) was similar to that in PSID ($42,114, SD $26,628). Roughly a quarter of each sample was eligible for the EITC, and mean EITC refund size among EITC-eligible individuals was $2,188 (SD $1,907) for NHIS and $1,702 (SD $1,578) for PSID. In both data sets, EITC-eligible individuals were more likely to be female, younger, and black or Hispanic, with lower educational attainment and income compared with non-eligible individuals, although sample characteristics were similar for those interviewed in February-April compared with May-January (Supplemental Tables 2–3).

In NHIS, 90% of participants reported currently having the same or better self-rated health compared to the previous year, while in PSID 55% or participants reported currently having excellent or very good health (Table 1). Psychological distress scores were 2.8 (SD 4.2) in NHIS and 3.5 (SD 3.9) in PSID. In both samples, about 24% reported currently smoking, and participants smoked an average of about three cigarettes per day. In PSID, 59.8% of participants reported current alcohol consumption.

Short-term Effects of the EITC

In NHIS and PSID, we were unable to rule out the null hypothesis that there was no association between receipt of the EITC and short-term changes in any outcome in either the main sample or the further income-restricted sample (Table 2).

Table 2.

Short-term Effects of the Earned Income Tax Credit on Mental Health and Health Behaviors

| Effect per $1,000 of EITC refund: β(95% CI) | ||||

|---|---|---|---|---|

| National Health Interview Survey | Panel Study of Income Dynamics | |||

| Outcome | Model 1: Income < $100k | Model 2: Income < $50k | Model 1: Income < $100k | Model 2: Income < $50k |

| Self-rated health | −0.0016 (−0.0033, 0.00002) | −0.0017 (−0.0036, 0.0002) | −0.0019 (−0.0066, 0.0027) | −0.0025 (−0.0075, 0.0025) |

| Psychological distress | −0.0020 (−0.025, 0.021) | −0.0075 (−0.034, 0.019) | 0.024 (−0.041, 0.089) | 0.015 (−0.055, 0.085) |

| Currently smoke | −0.0002 (−0.0029, 0.0017) | −0.0009 (−0.0033, 0.0015) | 0.0030 (−0.0022, 0.0081) | 0.0042 (−0.0013, 0.0098) |

| Number cigarettes per day | 0.020 (−0.020, 0.061) | 0.072 (−0.032, 0.18) | 0.064 (−0.021, 0.15) | 0.041 (−0.054, 0.14) |

| Currently drink alcohol | 0.0024 (−0.0035, 0.0082) | 0.0030 (−0.0034, 0.0094) | ||

p < 0.05

Note: N = 379,603 in NHIS and 29,808 in PSID. Coefficients represent the interaction between a continuous variable for amount of EITC refund (in thousands of inflation-adjusted U.S. dollars) and a binary variable for being interviewed in February-April. Analysis is restricted to households with income above $0 and below $100,000. Model 2 further restricts to households with income below $50,000. All models adjust for gender, race, age, age-squared, education, marital status, number of children, inflation-adjusted pre-tax household income, income-squared, as well as fixed effects for state and year. PSID models include robust standard errors clustered at the individual level. EITC: earned income tax credit; NHIS: National Health Interview Survey; PSID: Panel Study of Income Dynamics.

Secondary Analyses

In both NHIS and PSID, there were no differences in effect estimates for the unmarried and married samples (Supplemental Table 4). When examining only the effect of the federal EITC, in NHIS and PSID there was no association between EITC receipt and short-term changes in any outcome (Supplemental Table 5). Results of additional secondary analyses are presented in the Supplement (Supplemental Tables 6–7).

DiD Assumptions

We evaluated the parallel trends assumption by graphically comparing the slopes of each outcome during May-January for both EITC-eligible and non-eligible individuals (Supplemental Figures 2–3). For both NHIS and PSID, the graphs demonstrated roughly parallel trends during these months for most outcomes. The only exception was alcohol use in PSID; regression results for this outcome should therefore be interpreted with caution.

In the placebo test in both NHIS and PSID, there was no association between EITC refund size and any outcome when setting May-August as the exposure period (Supplemental Table 8).

Seasonal trends in sample composition were similar when comparing EITC-eligible and non-eligible participants across many demographic characteristics (Supplemental Table 9). The exceptions were black race in NHIS, and age, number of children, and income in PSID. This indicates that NHIS and PSID unintentionally interviewed participants of different sociodemographic backgrounds at different times of the year. We controlled for each of these characteristics in our analyses, although we cannot rule out the possibility of differences in other unmeasured confounders, a limitation of any DiD analysis.

DISCUSSION

This study provides evidence on the short-term effects of the EITC on mental health and health behaviors using a quasi-experimental approach and cross-validating findings across two large national data sets. Almost without exception, coefficients were small and we were unable to rule out the null hypothesis that there was no short-term effect of the EITC in the months after refund receipt on any outcome.

Prior research on the short-term effects of the EITC and other income supplements on mental health and health behaviors is inconsistent. On the one hand, our findings contrast with studies finding a “check effect,” in which there is increased substance use after the receipt of government benefits.21–23 On the other hand, prior studies have found that the EITC is also associated with reductions in smoking (particularly among pregnant women), improvements in food security, and worsened metabolic markers in adults.29,60–62 Other work found that the EITC refund is often spent on paying down debt—which may support the hypothesis of consumption smoothing—and on big-ticket items (e.g., vehicles, large appliances) that may or may not affect mental health and health behaviors in the short term.52,63–65 How income is received may also be a factor; for instance, prior work have shown that infrequent cash disbursements increase expenditures on “temptation” goods such as alcohol relative to more frequent disbursements.66 Another recent study found no short-term effects of the EITC on healthcare expenditures among adults,55 which again may either suggest consumption smoothing or differences in how people spend lump-sum versus more frequent payments.

Our study contrasts with findings from other studies of the long-term effects of the EITC that have found beneficial effects on mental health outcomes like depressive symptoms and suicide, as well as other outcomes like child development and test scores.39,42,50,67 Practically speaking, this may reflect a difference in sample populations or study design between this study and prior analyses. It may also be that the EITC’s effects accumulate over time, e.g., through increased investment in household resources. Alternately, this inconsistency may be because these studies examined other aspects of EITC policy (i.e., the 1990s EITC expansion and state EITC programs), or because of differences in the outcomes examined. Future studies should attempt to examine the short-term effects of the EITC on a wider range of mental health outcomes; NHIS and PSID only include psychological distress as measured by the K6. Finally, it may be that any short-term mental health benefits are outweighed by the stress of actually completing tax paperwork and uncertainty in the timing of disbursement of the tax refund. Research has also shown that tax filers who receive the EITC are more likely to be audited than most other tax filers, although audit rates are still relatively low.68,69

Strengths of this study include testing the effects of the EITC on a range of outcomes in two large data sets using a quasi-experimental study design. There are also several limitations. First, there may be misclassification, i.e., in that we cannot determine the exact timing of EITC refund receipt and we impute EITC eligibility based on self-reported demographic characteristics and income. This may lead to measurement error that contributes to null findings, although prior work using coarser categories of income has demonstrated health effects of the EITC,29 and this strategy is an alternative to—and perhaps an improvement on—prior studies that use crude proxies for EITC eligibility (e.g., educational attainment or presence of a state EITC program). On the other hand, using self-reported income rather than educational attainment to impute EITC eligibility may introduce bias, in that possible unmeasured confounders like cognitive skills may lead more savvy individuals to respond to EITC policy by altering their employment to maximize their refund size, and these confounders may also be associated with later mental health. Second, the violations in the DiD parallel trends assumption for smoking and alcohol in some models suggest that there may be underlying seasonal trends in these outcomes that complicate the interpretation of the results. Third, DiD analyses assume that seasonal trends in the outcomes among the EITC-eligible and non-eligible would have been the same in the absence of the EITC, a counterfactual scenario that is fundamentally untestable. Nevertheless, we conduct several analyses that probe this assumption.

CONCLUSIONS

In summary, we find no short-term effects of the EITC on mental health and health behaviors, consistent with several recent studies showing limited effects of the EITC in the months after refund receipt. This suggests that consumption smoothing dampens any “check effect,” and that future work should focus on evaluating the medium-, long-term, and cumulative effects of this important poverty alleviation program. This work also highlights the importance of leveraging multiple sources of variation to examine social policies’ effects, in order to best understand mediating pathways and implications for population health and health disparities.

Supplementary Material

Highlights.

We examined the effect of the largest US poverty alleviation policy on health.

We found no short-term effects of the EITC on mental health and health behaviors.

Seasonal income smoothing may result in long-term rather than short-term effects.

ACKNOWLEDGEMENTS

This work was supported by grants from the Robert Wood Johnson Foundation, the National Institutes of Health (grant number K08 HL132106), the UCSF Hellman Fellows Fund, the UCSF Irene Perstein Award, and the UCSF National Center of Excellence in Women’s Health. The collection of Panel Study of Income Dynamics data used in this study was partly supported by the National Institutes of Health under grant number R01 HD069609 and R01 AG040213, and the National Science Foundation under award numbers SES 1157698 and 1623684. The views expressed here do not necessarily reflect the views of the funders. The study funders had no role in study design; collection, analysis, and interpretation of data; writing the report; and the decision to submit the report for publication.

Abbreviations:

- DiD

difference-in-differences

- EITC

earned income tax credit

- IRS

Internal Revenue Service

- NHIS

National Health Interview Survey

- PSID

Panel Study of Income Dynamics

- SD

standard deviation

Footnotes

Publisher's Disclaimer: This is a PDF file of an unedited manuscript that has been accepted for publication. As a service to our customers we are providing this early version of the manuscript. The manuscript will undergo copyediting, typesetting, and review of the resulting proof before it is published in its final form. Please note that during the production process errors may be discovered which could affect the content, and all legal disclaimers that apply to the journal pertain.

Financial disclosure: No financial disclosures were reported by the authors of this paper.

REFERENCES

- 1.Kawachi I, Adler NE, Dow WH. Money, schooling, and health: Mechanisms and causal evidence. Ann N Y Acad Sci. 2010;1186:56–68. Accessed Jun 19, 2019. doi: 10.1111/j.1749-6632.2009.05340.x. [DOI] [PubMed] [Google Scholar]

- 2.Muennig P Health selection vs. causation in the income gradient: What can we learn from graphical trends? J Health Care Poor Underserved. 2008;19(2):574–579. http://europepmc.org/abstract/med/18469427. Accessed Jun 19, 2019. doi: 10.1353/hpu.0.0018. [DOI] [PubMed] [Google Scholar]

- 3.Muennig P, Fiscella K, Tancredi D, Franks P. The relative health burden of selected social and behavioral risk factors in the united states: Implications for policy. Am J Public Health. 2010;100(9):1758–1764. Accessed Jun 19, 2019. doi: 10.2105/AJPH.2009.165019. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Burns JK. Poverty, inequality and a political economy of mental health. Epidemiology and Psychiatric Sciences. 2015;24(2):107–113. https://www.cambridge.org/core/journals/epidemiology-and-psychiatric-sciences/article/poverty-inequality-and-a-political-economy-of-mental-health/F00963B427E906505713B63317CBD6F8. Accessed Mar 19, 2020. doi: 10.1017/S2045796015000086. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5.Cerda M, Johnson-Lawrence V, Galea S. Lifetime income patterns and alcohol consumption: Investigating the association between long-and short-term income trajectories and drinking. Soc Sci Med. 2011;73(8):1178–1185. http://hdl.handle.net/2027.42/107392. Accessed Aug 23, 2019. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Jamal A, Phillips E, Gentzke AS, et al. Current cigarette smoking among adults — united states, 2016. MMWR. Morbidity and mortality weekly report 2018;67(2):53–59. https://www.ncbi.nlm.nih.gov/pubmed/29346338. doi: 10.15585/mmwr.mm6702a1. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Schneiderman N, Ironson G, Siegel SD. Stress and health: Psychological, behavioral, and biological determinants. Annual review of clinical psychology. 2005;1(1):607–628. https://www.ncbi.nlm.nih.gov/pubmed/17716101. doi: 10.1146/annurev.clinpsy.1.102803.144141. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.Epel ES, Lithgow GJ. Stress biology and aging mechanisms: Toward understanding the deep connection between adaptation to stress and longevity. J Gerontol A Biol Sci Med Sci. 2014;69 Suppl 1:10 Accessed Jun 19, 2019. doi: 10.1093/gerona/glu055. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9.Ahmed SM, Lemkau JP, Nealeigh N, Mann B. Barriers to healthcare access in a non-elderly urban poor american population. Health & Social Care in the Community. 2001;9(6):445–453. https://onlinelibrary.wiley.com/doi/abs/10.1046/j.1365-2524.2001.00318.x. Accessed Mar 19, 2020. doi: 10.1046/j.1365-2524.2001.00318.x. [DOI] [PubMed] [Google Scholar]

- 10.LaVeist TA, Wallace JM. Health risk and inequitable distribution of liquor stores in african american neighborhood. Social Science & Medicine. 2000;51(4):613–617. http://www.sciencedirect.com/science/article/pii/S0277953600000046. Accessed Mar 19, 2020. doi: 10.1016/S0277-9536(00)00004-6. [DOI] [PubMed] [Google Scholar]

- 11.Romley JA, Cohen D, Ringel J, Sturm R. Alcohol and environmental justice: The density of liquor stores and bars in urban neighborhoods in the united states. J Stud Alcohol Drugs. 2007;68(1):48–55. 10.15288/jsad.2007.68.48. doi: 10.15288/jsad.2007.68.48. [DOI] [PubMed] [Google Scholar]

- 12.Lee JG, Henriksen L, Rose SW, Moreland-Russell S, Ribisl KM. A systematic review of neighborhood disparities in point-of-sale tobacco marketing. Am J Public Health. 2015;105(9):e8–e18. 10.2105/AJPH.2015.302777. doi: 10.2105/AJPH.2015.302777. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Angeles G, de Hoop J, Handa S, Kilburn K, Milazzo A, Peterman A. Government of malawi’s unconditional cash transfer improves youth mental health. Soc Sci Med. 2019;225:108–119. Accessed Jun 19, 2019. doi: 10.1016/j.socscimed.2019.01.037. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 14.Baird S, Hoop Jd, Özler B. Income shocks and adolescent mental health. J Human Resources. 2013;48(2):370–403. http://jhr.uwpress.org/content/48/2/370. Accessed Aug 29, 2019. doi: 10.3368/jhr.48.2.370. [DOI] [Google Scholar]

- 15.Kilburn K, Hughes JP, MacPhail C, et al. Cash transfers, young women’s economic well-being, and HIV risk: Evidence from HPTN 068. AIDS and Behavior. 2019;23(5):1178–1194. 10.1007/s10461-018-2329-5. doi: 10.1007/s10461-018-2329-5. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 16.Fernald LCH, Hamad R, Karlan D, Ozer EJ, Zinman J. Small individual loans and mental health: A randomized controlled trial among south african adults. BMC Public Health. 2008;8(1):409 10.1186/1471-2458-8-409. doi: 10.1186/1471-2458-8-409. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 17.Pereira A Cash transfers improve the mental health and well-being of youth: Evidence from the kenyan cash transfer for orphans and vulnerable children. UNICEF-IRC. 2016. https://www.unicef-irc.org/publications/801-cash-transfers-improve-the-mental-health-and-well-being-of-youth-evidence-from-the.html. Accessed Oct 8, 2019. [Google Scholar]

- 18.Owusu-Addo E, Renzaho AMN, Smith BJ. The impact of cash transfers on social determinants of health and health inequalities in sub-saharan africa: A systematic review. Health Policy Plan. 2018;33(5):675–696. https://academic.oup.com/heapol/article/33/5/675/4947872. Accessed Oct 8, 2019. doi: 10.1093/heapol/czy020. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19.Kilburn K, Thirumurthy H, Halpern CT, Pettifor A, Handa S. Effects of a large-scale unconditional cash transfer program on mental health outcomes of young people in kenya. J Adolesc Health. 2016;58(2):223–229. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4724529/. Accessed Oct 8, 2019. doi: 10.1016/j.jadohealth.2015.09.023. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.Morris PA, Aber JL, Wolf S, Berg J. Impacts of family rewards on adolescents’ mental health and problem behavior: Understanding the full range of effects of a conditional cash transfer program. Prev Sci. 2017;18(3):326–336. Accessed Jun 19, 2019. doi: 10.1007/s11121-017-0748-6. [DOI] [PubMed] [Google Scholar]

- 21.Dobkin C, Puller S. The effects of government transfers on monthly cycles in drug abuse, hospitalization and mortality. Journal of Public Economics. 2007;91(11–12):2137–2157. https://econpapers.repec.org/article/eeepubeco/v_3a91_3ay_3a2007_3ai_3a11-12_3ap_3a2137-2157.htm. Accessed Apr 22, 2019. [Google Scholar]

- 22.Evans WN, Moore TJ. The short-term mortality consequences of income receipt. Journal of Public Economics. 2011;95(11):1410–1424. https://ideas.repec.org/a/eee/pubeco/v95y2011i11p1410-1424.html. Accessed Apr 22, 2019. [Google Scholar]

- 23.Catalano R, McConnell W, Forster P, McFarland B, Shumway M, Thornton D. Does the disbursement of income increase psychiatric emergencies involving drugs and alcohol? Health Services Research. 2000;35(4):813–813. https://link.galegroup.com/apps/doc/A66459856/AONE?sid=lms. Accessed Oct 8, 2019. [PMC free article] [PubMed] [Google Scholar]

- 24.Gennetian LA, Shafir E. The persistence of poverty in the context of financial instability: A behavioral perspective. Journal of Policy Analysis and Management. 2015;34(4):904–936. https://onlinelibrary.wiley.com/doi/abs/10.1002/pam.21854. Accessed Oct 8, 2019. doi: 10.1002/pam.21854. [DOI] [Google Scholar]

- 25.Statistics for tax returns with EITC | EITC & other refundable credits. https://www.eitc.irs.gov/eitc-central/statistics-for-tax-returns-with-eitc/statistics-for-tax-returns-with-eitc. Accessed Aug 26, 2019.

- 26.Dahl Molly, Thomas DeLeire Jonathan Schwabish. Stepping stone or dead end? the effect of the EITC on earnings growth. National Tax Journal. 2009;62(2):329–346. http://www.jstor.org/stable/41790507. [Google Scholar]

- 27.Chetty R, Friedman JN, Saez E. Using differences in knowledge across neighborhoods to uncover the impacts of the EITC on earnings. American Economic Review. 2013;103(7):2683–2721. https://www.aeaweb.org/articles?id=10.1257/aer.103.7.2683. Accessed Apr 22, 2019. doi: 10.1257/aer.103.7.2683. [DOI] [Google Scholar]

- 28.Kleven H The EITC and the extensive margin: A reappraisal. . 2019(26405). https://EconPapers.repec.org/RePEc:nbr:nberwo:26405. [Google Scholar]

- 29.Rehkopf DH, Strully KW, Dow WH. The short-term impacts of earned income tax credit disbursement on health. International journal of epidemiology. 2014;43(6):1884–1894. http://www.ncbi.nlm.nih.gov/pubmed/25172139. doi: 10.1093/ije/dyu172. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 30.Bitler M, Hoynes H, Kuka E. Do in-work tax credits serve as a safety net? J Human Resources. 2016;52(2):319–350. http://jhr.uwpress.org/content/early/2016/03/04/jhr.52.2.0614-6433R1. Accessed Mar 20, 2018. doi: 10.3368/jhr.52.2.0614-6433R1. [DOI] [Google Scholar]

- 31.Hoynes H, Miller D, Simon D. Income, the earned income tax credit, and infant health. American Economic Journal: Economic Policy. 2015;7(1):172–211. doi: 10.1257/pol.7.1.172. [DOI] [Google Scholar]

- 32.Averett S, Wang Y. The effects of EITC payment expansion on maternal smoking. Health Economics. 2013;22(11):1344–1359. doi: 10.1002/hec.2886. [DOI] [PubMed] [Google Scholar]

- 33.Muennig PA, Mohit B, Wu J, Jia H, Rosen Z. Cost effectiveness of the earned income tax credit as a health policy investment. American Journal of Preventive Medicine. 2016;51(6):874–881. http://www.sciencedirect.com/science/article/pii/S0749379716302495. Accessed Nov 20, 2019. doi: 10.1016/j.amepre.2016.07.001. [DOI] [PubMed] [Google Scholar]

- 34.Baughman RA. Evaluating the impact of the earned income tax credit on health insurance coverage. National Tax Journal. 2005;58(4):665–684. http://www.jstor.org/stable/41790297. [Google Scholar]

- 35.Baughman R, Duchovny N. State earned income tax credits and the production of child health: Insurance coverage, utilization, and health status. National tax journal. 2016;69:103–132. doi: 10.17310/ntj.2016.1.04. [DOI] [Google Scholar]

- 36.Lenhart O The effects of income on health: New evidence from the earned income tax credit. Review of Economics of the Household. 2019;17(2):377–410. https://ideas.repec.org/a/kap/reveho/v17y2019i2d10.1007_s11150-018-9429-x.html. Accessed Mar 19, 2020. [Google Scholar]

- 37.Schmeiser MD. Expanding wallets and waistlines: The impact of family income on the BMI of women and men eligible for the earned income tax credit. Health Econ. 2009;18(11):1277–1294. Accessed Dec 8, 2017. doi: 10.1002/hec.1430. [DOI] [PubMed] [Google Scholar]

- 38.Evans DK, Popova A. Cash transfers and temptation goods. Economic Development and Cultural Change. 2017;65(2):189–221. 10.1086/689575. doi: 10.1086/689575. [DOI] [Google Scholar]

- 39.Boyd-Swan C, Herbst CM, Ifcher J, Zarghamee H. The earned income tax credit, mental health, and happiness. Journal of Economic Behavior & Organization. 2016;126:18–38. http://www.sciencedirect.com/science/article/pii/S0167268115002942. Accessed Jun 20, 2019. doi: 10.1016/j.jebo.2015.11.004. [DOI] [Google Scholar]

- 40.Evans WN, Garthwaite CL. Giving mom a break: The impact of higher EITC payments on maternal health. American Economic Journal: Economic Policy. 2014;6(2):258–290. https://www.aeaweb.org/articles?id=10.1257/pol.6.2.258. Accessed Jun 20, 2019. doi: 10.1257/pol.6.2.258. [DOI] [Google Scholar]

- 41.Lenhart O The effects of state-level earned income tax credits on suicides. Health Economics. 2019. https://pureportal.strath.ac.uk/en/publications/the-effects-of-state-level-earned-income-tax-credits-on-suicides. Accessed Oct 8, 2019. doi: 10.1002/hec.3948. [DOI] [PubMed] [Google Scholar]

- 42.Dow WH, Godøy A, Lowenstein CA, Reich M. Can economic policies reduce deaths of despair? National Bureau of Economic Research Working Paper Series. 2019;No. 25787 http://www.nber.org/papers/w25787http://www.nber.org/papers/w25787.pdf. doi: 10.3386/w25787. [DOI] [Google Scholar]

- 43.Dosemeci M, Wacholder S, Lubin JH. Does nondifferential misclassification of exposure always bias a true effect toward the null value? Am J Epidemiol. 1990;132(4):746–748. https://academic.oup.com/aje/article/132/4/746/102304. Accessed Oct 8, 2019. doi: 10.1093/oxfordjournals.aje.a115716. [DOI] [PubMed] [Google Scholar]

- 44.Panel study of income dynamics, public use dataset. produced and distributed by the survey research center, institute for social research, university of michigan, ann arbor, MI 2017.

- 45.Feenberg D, Coutts E. An introduction to the TAXSIM model. Journal of Policy Analysis and Management. 1993;12(1):189–194. https://econpapers.repec.org/article/wlyjpamgt/v_3a12_3ay_3a1993_3ai_3a1_3ap_3a189-194.htm. Accessed Dec 8, 2017. [Google Scholar]

- 46.Hamad R, Collin DF, Rehkopf DH. Estimating the short-term effects of the earned income tax credit on child health. Am J Epidemiol. 2018;187(12):2633–2641. Accessed Apr 22, 2019. doi: 10.1093/aje/kwy179. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 47.Hamad R, Rehkopf DH. Poverty, pregnancy, and birth outcomes: A study of the earned income tax credit. Paediatric and Perinatal Epidemiology. 2015;29(5):444–452. http://onlinelibrary.wiley.com/doi/10.1111/ppe.12211/abstract. doi: 10.1111/ppe.12211. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 48.Hamad R, Rehkopf DH. Poverty and child development: A longitudinal study of the impact of the earned income tax credit. Am J Epidemiol. 2016;183(9):775–784. Accessed Dec 8, 2017. doi: 10.1093/aje/kwv317. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 49.Scholz JK. The earned income tax credit: Participation, compliance, and anti-poverty effectiveness. National Tax Journal. 1994;47 Accessed Jun 21, 2019. [Google Scholar]

- 50.Dahl GB, Lochner L. The impact of family income on child achievement: Evidence from the earned income tax credit. American Economic Review. 2012;102(5):1927–1956. https://www.aeaweb.org/articles?id=10.1257/aer.102.5.1927. Accessed Jun 21, 2019. doi: 10.1257/aer.102.5.1927. [DOI] [Google Scholar]

- 51.Barrow L, McGranahan L. The effects of the earned income credit on the seasonality of household expenditures. National Tax Journal. 2000;53(4):1211–1244. https://ideas.repec.org/a/ntj/journl/v53y2000i4p1211-44.html. Accessed Apr 2, 2020. [Google Scholar]

- 52.Goodman-Bacon A, McGranahan L. How do EITC recipients spend their refunds? Economic Perspectives. 2008(Q II):17–32. https://ideas.repec.org/a/fip/fedhep/y2008iqiip17-32nv.32no.2.html. Accessed Oct 8, 2019. [Google Scholar]

- 53.McGranahan L, Schanzenbach DW. The earned income tax credit and food consumption patterns. Federal Reserve Bank of Chicago; 2013. [Google Scholar]

- 54.Davison G, Roll S, Taylor S, Grinstein-Weiss M. The state of state EITCs: An overview and their implications for low- and moderate-income households. Center for Social Development Research. 2018. https://openscholarship.wustl.edu/csd_research/615. Accessed Oct 8, 2019. doi: 10.7936/K7WM1CZ0. [DOI] [Google Scholar]

- 55.Hamad R, Niedzwiecki MJ. The short-term effects of the earned income tax credit on health care expenditures among US adults. Health Serv Res. 2019. Accessed Oct 8, 2019. doi: 10.1111/1475-6773.13204. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 56.Kessler RC, Andrews G, Colpe LJ, et al. Short screening scales to monitor population prevalences and trends in non-specific psychological distress. Psychol Med. 2002;32(6):959–976. Accessed Oct 8, 2019. doi: 10.1017/s0033291702006074. [DOI] [PubMed] [Google Scholar]

- 57.Prochaska JJ, Sung H, Max W, Shi Y, Ong M. Validity study of the K6 scale as a measure of moderate mental distress based on mental health treatment need and utilization. Int J Methods Psychiatr Res. 2012;21(2):88–97. Accessed Oct 8, 2019. doi: 10.1002/mpr.1349. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 58.von Hippel PT. Regression with missing ys: An improved strategy for analyzing multiply imputed data. Sociological Methodology. 2007;37(1):83–117. https://journals.sagepub.com/doi/full/10.1111/j.1467-9531.2007.00180.x. doi: 10.1111/j.1467-9531.2007.00180.x. [DOI] [Google Scholar]

- 59.LaLumia S The EITC, tax refunds, and unemployment spells. American Economic Journal: Economic Policy. 2013;5(2):188–221. https://www.aeaweb.org/articles?id=10.1257/pol.5.2.188. Accessed Dec 8, 2017. doi: 10.1257/pol.5.2.188. [DOI] [Google Scholar]

- 60.Strully Kate W., Rehkopf David H., Xuan Ziming. Effects of prenatal poverty on infant health: State earned income tax credits and birth weight. American Sociological Review. 2010;75(4):534–562. https://www.jstor.org/stable/20799476. doi: 10.1177/0003122410374086. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 61.Bartfeld J, Men F. Food insecurity among households with children: The role of the state economic and policy context. Soc Serv Rev. 2017;91(4):691–732. 10.1086/695328. doi: 10.1086/695328. [DOI] [Google Scholar]

- 62.Andrade FCD, Kramer KZ, Greenlee A, Williams AN, Mendenhall R. Impact of the chicago earned income tax periodic payment intervention on food security. Preventive Medicine Reports. 2014;16 https://www.ncbi.nlm.nih.gov/pmc/articles/PMC6849410/. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 63.Mendenhall R, Edin K, Crowley S, et al. The role of earned income tax credit in the budgets of low-income households. Soc Serv Rev. 2012;86(3):367–400. 10.1086/667972. doi: 10.1086/667972. [DOI] [Google Scholar]

- 64.Romich Jennifer L., Weisner Thomas. How families view and use the EITC: Advance payment versus lump sum delivery. National Tax Journal. 2000;53(4):1245–1265. http://www.jstor.org/stable/41789516. [Google Scholar]

- 65.Morduch J Income smoothing and consumption smoothing. Journal of Economic Perspectives. 1995;9(3):103–114. https://www.aeaweb.org/articles?id=10.1257/jep.9.3.103. Accessed Oct 8, 2019. doi: 10.1257/jep.9.3.103. [DOI] [Google Scholar]

- 66.White JS, Basu S. Does the benefits schedule of cash assistance programs affect the purchase of temptation goods? evidence from peru. Journal of Health Economics. 2016;46:70–89. http://www.sciencedirect.com/science/article/pii/S0167629616000175. Accessed Jun 21, 2019. doi: 10.1016/j.jhealeco.2016.01.005. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 67.Hamad R, Rehkopf DH. Poverty and child development: A longitudinal study of the impact of the earned income tax credit. Am J Epidemiol. 2016;183(9):775–784. Accessed Mar 20, 2018. doi: 10.1093/aje/kwv317. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 68.Guyton J, Leibel K, Manoli DS, Patel A, Payne M, Schafer B. The effects of EITC correspondence audits on low-income earners. National Bureau of Economic Research Working Paper Series. 2018;No. 24465 http://www.nber.org/papers/w24465http://www.nber.org/papers/w24465.pdf. doi: 10.3386/w24465. [DOI] [Google Scholar]

- 69.Paul Kiel JE. Who’s more likely to be audited: A person making $20,000 — or $400,000? ProPublica. 2018-12-12T10:00:00+0000 2018-12-12T10:00:00+0000. Available from: https://www.propublica.org/article/earned-income-tax-credit-irs-audit-working-poor. Accessed Oct 8, 2019. [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.