High default rates, poor credit, and increasing financial distress are associated with higher suicide rates in adults with ADHD.

Abstract

Attention-deficit/hyperactivity disorder (ADHD) exerts lifelong impairment, including difficulty sustaining employment, poor credit, and suicide risk. To date, however, studies have assessed selected samples, often via self-report. Using mental health data from the entire Swedish population (N = 11.55 million) and a random sample of credit data (N = 189,267), we provide the first study of objective financial outcomes among adults with ADHD, including associations with suicide. Controlling for psychiatric comorbidities, substance use, education, and income, those with ADHD start adulthood with normal credit demand and default rates. However, in middle age, their default rates grow exponentially, yielding poor credit scores and diminished credit access despite high demand. Sympathomimetic prescriptions are unassociated with improved financial behaviors. Last, financial distress is associated with fourfold higher risk of suicide among those with ADHD. For men but not women with ADHD who suicide, outstanding debt increases in the 3 years prior. No such pattern exists for others who suicide.

INTRODUCTION

Those who are diagnosed with attention-deficit/hyperactivity disorder (ADHD) (1) show strong biases toward immediate rewards over larger, delayed rewards (2) and are prospectively vulnerable to a variety of adverse behavioral and mental health outcomes across their life spans (3). In childhood, these outcomes include academic underachievement, grade retention, and social rejection (4). In adulthood, they include higher college dropout rates, poorer job performance, difficulty sustaining employment, and lower wages than peers of similar intelligence (5, 6). Children, adolescents, and adults who are diagnosed with ADHD also engage in more high-risk, impulsive behaviors, including substance abuse, self-injury, and suicide attempts (7, 8). These outcomes are often observed even among those who received evidence-based treatment for ADHD in childhood (9, 10).

Daily routines in Western societies require people to pay bills on time, make rent and mortgage payments, and keep track of investments and savings. Yet, despite awareness that adults with ADHD face difficulties managing these and other financials, the extent of such difficulties and their associations with individual well-being have not been evaluated with objective data. According to self-reports, adults with ADHD are more financially dependent on family members, face more difficulties paying bills, open fewer savings accounts, use credit cards more compulsively, and are more likely to use very high interest rate borrowing, such as pawnshops and payday loans, than others in the population (5, 8, 11, 12). To date, however, most data derive from adults who were followed up after being treated for ADHD in childhood or recruited via self-selected convenience sampling (e.g., Amazon Mechanical Turk). These recruitment strategies suffer from inherent limitations, including greater severity of ADHD for those enrolled in child treatment studies, systematic biases in self-reported credit and other financial outcomes, and small to modest sample sizes. Thus, the economic magnitude of population-wide effects of ADHD on objective financial outcomes is unknown. Improved understanding of relations among ADHD, financial behaviors, and suicide may have important implications for prevention and intervention.

Here, we provide previously unidentified findings regarding financial behaviors and suicide among adults with ADHD at the population level. We include analyses of changes in financial behaviors in the months and years preceding suicide. These analyses follow from “ideation-to-action” accounts of suicide, such as three-step theory (13). According to these models, many more people are capable of engaging in suicidal behaviors than attempt or die by suicide. Those who are capable and attempt are often motivated by psychological pain and hopelessness (14). Thus, three-step theory predicts a reduced sense of purpose and increased psychological distress before suicide. For some, worsening financials may contribute to psychological distress, whereas for others, psychological distress may contribute to worsening financials. Either way, any prospective association between worsening financials and later suicide among adults with ADHD could aid in identifying those at highest risk and serve as a springboard for additional research.

Using mental health data collected from the full Swedish population (N = 11.55 million) (15, 16) and a random sample of data on credit and defaults (N = 189,267) (17) for the period spanning 2002–2015, we evaluate financial outcomes across adulthood—including associations with suicide—among those 18 years and older with and without diagnoses of ADHD. These data yield the largest such sample reported to date. Given the very large sample and associated likelihood of identifying trivial effects as significant at any given time, we focus readers’ attention on 95% confidence intervals (CIs) across time, which are presented in graphs to follow. These 95% CIs include statistical adjustments for physical and mental health covariates. Details regarding regression equations and statistical controls including propensity score matching appear in Materials and Methods and in the Supplementary Materials, Sections A to C.

RESULTS

Lifetime prevalence of ADHD

In Sweden, all community care providers report International Classification of Diseases (ICD) (1) diagnostic codes for all physical and mental health conditions to the National Board of Health and Welfare (Socialstyrelsen; www.socialstyrelsen.se/english) (15). Between 2002 and 2015, full population registry data obtained from Statistics Sweden (16) revealed an ADHD lifetime prevalence of 0.015 based on ICD codes reported by physicians. This figure, which includes all individuals ever diagnosed with ADHD (61.3% male and 38.7% female), is well below the estimated lifetime prevalence of ADHD in the United States (18), consistent with lower rates of diagnosis in Europe than in North America (19). More conservative diagnostic practices in Sweden than in the United States make overdiagnosis in community settings an unlikely confounding explanation for any effects (20) and should be considered before generalizing to U.S. samples. Note that precise control over diagnostic practices is not possible in a population-based study.

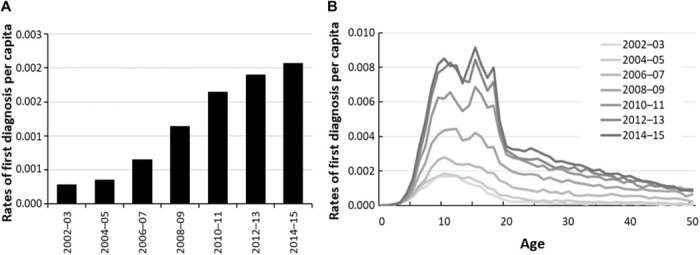

Our analyses reveal that rates of new diagnoses rose considerably from 2002 to 2015, with increases observed at all ages (Fig. 1A and the Supplementary Materials, Section C) (15). As a result, first-time diagnoses among 20- to 30-year-olds between 2010 and 2015 were higher than first-time diagnoses among 10- to 20-year-olds before 2006 (Fig. 1B and the Supplementary Materials, Section C). Nevertheless, within each biennium, most new cases of ADHD were diagnosed before age 20.

Fig. 1. Rates of ADHD diagnoses in the Swedish population (N = 11,549,190), including n = 177,336 ever diagnosed with ADHD and n = 11,371,854 never diagnosed with ADHD (15).

(A) Rates of new diagnoses per capita for biennia spanning 2002–2015. (B) Rates of new diagnoses per capita by age (years) across biennia spanning 2002–2015.

ADHD, credit, and financial behaviors

Associations between ADHD and various financial metrics and behaviors appear in Fig. 2. All graphs depict data on credit and defaults for a random sample of Swedes (17) (N = 189,267) for adults diagnosed with ADHD (n = 1,970) and those without ADHD (n = 187,297) across 4 years spanning 2010–2013. Analyses control for education, income, sex, psychiatric comorbidities (anxiety disorders, depression, substance use disorders, and autism spectrum disorder), and available physical health indicators (asthma and respiratory infections). We also ran analyses using propensity score matching on age, income, and education and found no significant changes in our findings.

Fig. 2. Associations between ADHD and finances.

Credit and defaults for a random sample of Swedes (17) (n = 1970 ever diagnosed with ADHD; n = 187,297 never diagnosed from 2010 to 2013). (A) Credit requests per month by age. Widening 95% CIs at older ages indicate fewer ADHD cases. (B) New consumer credits per month. (C) New arrears per month. For (A) to (C), y axis values are estimated, adjusting for education, income, sex, psychiatric comorbidities, and physical health. (D) Elevation in arrears for those with ADHD versus the population for everyone registered at the Enforcement Agency in January 2018 (21) (n = 5736 ever diagnosed with ADHD; n = 63,216 never diagnosed). (E) Percentage of people with unpaid claims diagnosed with ADHD by years delinquent. (F) Percentage of people in successive default risk bins diagnosed with ADHD. Increasing x axis scores indicate higher default risk. Proportions of the population and percentage default risk are as follows: bin 1 (0.47; 0 to 0.1%), bin 2 (0.11; 0.1 to 0.2%), bin 3 (0.07; 0.2 to 0.3%), bin 4 (0.05; 0.3 to 0.4%), bin 5 (0.03; 0.4 to 0.5%), bin 6 (0.02; 0.5 to 0.6%), bin 7 (0.05; 0.6 to 0.9%), bin 8 (0.05; 0.9 to 1.4%), bin 9 (0.05; 1.4 to 2.7%), bin 10 (0.05; 2.7 to 30.9%), and bin 11 (0.05; 30.9 to 97.7%). Hatched horizontal lines (E and F) show the population base rate of ADHD.

Credit and default data reveal that those diagnosed with ADHD show only a slightly elevated demand for credit compared with the general population before age 30. At later ages, however, their demand for credit continues to grow at a time when the rest of the population lowers its demand (Fig. 2A and the Supplementary Materials, Section C). This gap in demand stems from credit requests by individuals with ADHD being rejected. Hence, their high credit demand does not translate into greater credit access (Fig. 2B and the Supplementary Materials, Section C). Despite requesting more credit, those diagnosed with ADHD are granted less new consumer credit than the general population until about age 50.

Limited credit access for individuals with ADHD can be explained by poor debt repayment behavior. The Swedish National Enforcement Agency (Kronofogden) (21) enforces both public unpaid claims and claims by private collection agencies that are unsuccessfully collected. Kronofogden records show that adults with ADHD are more likely to incur new arrears than those without ADHD (Fig. 2C and the Supplementary Materials, Section C). By age 40, their default risk peaks at over six times that of the general population.

Examining arrears records reveals that adults with ADHD have higher rates of missed payments than others in every category of unpaid claims (Fig. 2D and the Supplementary Materials, Section C). The largest differences are observed for misuse of bank accounts (e.g., overdrafts), unpaid alimony, unpaid educational support, impounded property, and unpaid road taxes. In each of these categories, adults with ADHD are over four times more likely to incur arrears. However, many unpaid claims involve relatively small items (e.g., unpaid parking tickets).

Collectively, arrears have serious effects on individuals’ credit reports, as increasingly more entities check credit records. Each additional year with an arrear on one’s credit record causally reduces employment by 3 percentage points and wage earnings by $1000 for the most vulnerable members of the Swedish society (22). Default risk among those diagnosed with ADHD is a long-term problem, as indicated by their overrepresentation among those more than a decade in continuous default (Fig. 2E and the Supplementary Materials, Section C).

Given their poor credit history, adults with ADHD are overrepresented in higher default risk bins, which reflect poorer credit quality (Fig. 2F and the Supplementary Materials, Section C). The percentage of individuals diagnosed with ADHD increases exponentially with default risk. Compared with the general population, ADHD diagnoses are associated with a much lower likelihood of populating the lowest default risk bin (odds ratio, 0.14) and a much higher likelihood of populating the highest default risk bin (odds ratio, 3.49).

Associations between medication and arrears

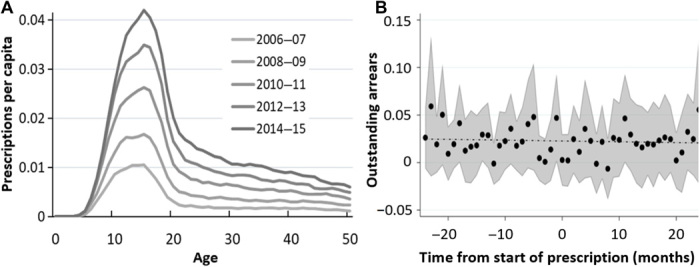

Socialstyrelsen data also allowed us to explore associations between sympathomimetic prescriptions for ADHD (e.g., methylphenidate, atomoxetine, amphetamine, and dextroamphetamine) (23) and financial outcomes. Figure 3 (and the Supplementary Materials, Section C) summarizes these prescription data across the population (15) and presents associations between prescriptions and financial behaviors for the random sample of Swedes for whom we observe credit and default data (17). Across all biennia, prescriptions were most common for those between ages 10 and 20 years (Fig. 3A and the Supplementary Materials, Section C). Nevertheless, rates of prescriptions rose roughly fourfold between 2006 and 2015 for all age groups. Yet, despite increased access to medication, there is no association between prescriptions and new arrears (Fig. 3B and the Supplementary Materials, Section C). Rather, similar rates of new arrears are observed in the 2 years before and after prescription. These data raise obvious questions about relations between medication adherence and financial outcomes given that almost half of adults with ADHD report less than full medication adherence, and given that nonadherence correlates with ADHD severity (24). Thus, it is possible that prescription medications were helpful for those who were fully medication compliant. Unfortunately, we do not have adherence data to analyze, so causal conclusions should not be inferred.

Fig. 3. Prescriptions for ADHD and associations between new prescriptions and arrears.

(A) Prescriptions per capita for the entire population, by age (years), across biennia spanning 2006–2015. Data are from the full Swedish population, including n = 177,336 individuals ever diagnosed with ADHD and n = 11,371,854 never diagnosed with ADHD (15). (B) Average number of new arrears in the 2 years preceding and following prescriptions for ADHD. No differences were found when data were analyzed separately for men versus women. Data are from the random sample on credit and defaults (17), including n = 1970 individuals ever diagnosed with ADHD and n = 187,297 never diagnosed with ADHD. Arrears are residualized, adjusting for education, income, sex, age, psychiatric comorbidities, and physical health, and can extend below zero.

Associations between finances and suicide

Last, we explore associations between financial outcomes and suicide. Our interest was to understand whether there is an interaction between financial condition and likelihood of suicide. To address this question, we obtained population statistics on suicide as a cause of death from the National Board of Health and Welfare (Socialstyrelsen) (15). The sample period is 2002–2015 (Supplementary Materials, Section C). For analyses using suicide as outcome, we controlled for education, income, sex, age, physical health, anxiety disorders, substance use disorders, and autism spectrum disorder. We conducted two sets of analyses. In the first analysis, we did not control for depression given (i) expected increases in depression before suicide (25), (ii) common neural vulnerability to unipolar depression and ADHD in brain regions implicated in anhedonia and reward processing (26, 27), and (iii) similar deficits in performance on delay discounting tasks among those with ADHD and those with depression (28). Collectively, these findings suggest common (transdiagnostic) etiological mechanisms across disorders (26). Under such circumstances, covarying depression removes variance attributable to shared vulnerability, a practice that has been criticized in the psychopathology literature because it creates statistical entities that distort etiology (29, 30). Nevertheless, we conducted a second set of analyses including depression as a covariate given likely interest among readers. Of note, propensity score matching did not change results for either set of analyses.

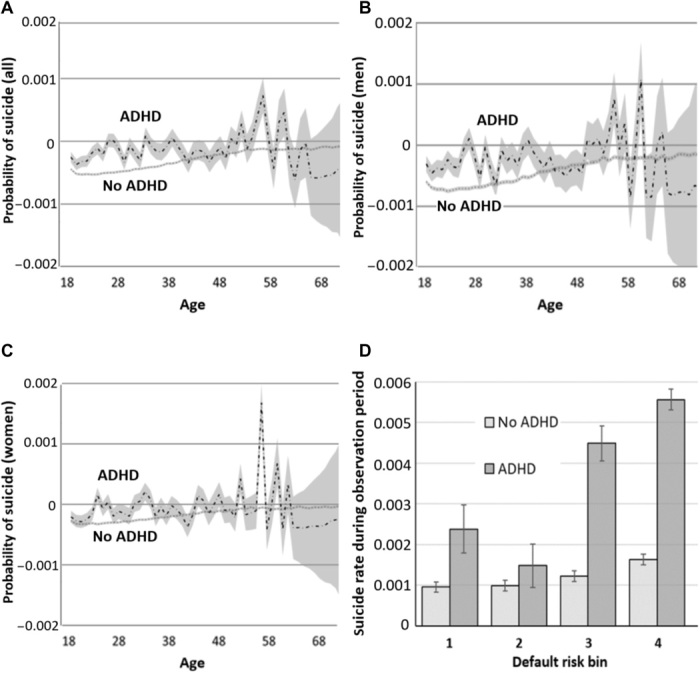

Results are reported in Fig. 4 (A to C). For the sample as a whole (Fig. 4A), those diagnosed with ADHD are more likely to die by suicide than those without ADHD at almost all ages below 60 years, consistent with previous research (31, 32). As shown in Fig. 4 (B and C), nearly identical results were obtained for men and women. We also document an interaction effect between ADHD and financial distress on suicide. On the basis of credit and default data covering 2010 to 2013 (17), disparities in death by suicide are much larger for those diagnosed with ADHD who are at high default risk (Fig. 4D and the Supplementary Materials, Section C). Those with ADHD who fall in the highest default risk bins (bins 3 to 4) suicide at three times the rate of those with ADHD in lower default risk bins (bins 1 to 2). Although effect sizes were reduced when depression was entered in the regression equations (Supplementary Materials, Section C), both men and women diagnosed with ADHD were still more likely to die by suicide at almost all ages less than 60 years. Furthermore, high rates of suicide among those with ADHD and especially poor credit (bins 3 to 4) were unchanged.

Fig. 4. Suicide outcomes by ADHD status.

(A) Probability of suicide during the observation period for all people with ADHD and without ADHD. (B) Probability of suicide for men diagnosed with ADHD versus without ADHD. (C) Probability of suicide for women with ADHD versus without ADHD. For (A) to (C), y axis values are estimated, adjusting for education, income, sex, psychiatric comorbidities, and physical health. No differences were found between men and women. Data are from the full Swedish population from 2002 to 2015 (n = 177,336 ever diagnosed with ADHD; n = 11,371,854 never diagnosed with ADHD) (15). Widening CIs above age 60 result from fewer ADHD cases. (D) Disparities in suicide rates for those with and without ADHD by default risk. Data are from a random sample of Swedes (17), collected between 2010 and 2013 (n = 1970 ever diagnosed with ADHD; n = 187,297 never diagnosed with ADHD). Increasing scores along the x axis indicate higher likelihood of default. We collapsed into four default risk bins to obtain stable estimates of suicide, given comparatively low base rates. Proportions of the population and percentage default risk are as follows: bin 1 (0.47; 0 to 0.1%), bin 2 (0.18; 0.1 to 0.3%), bin 3 (0.15; 0.3 to 0.9%), and bin 4 (0.20; 0.9 to 97.7%).

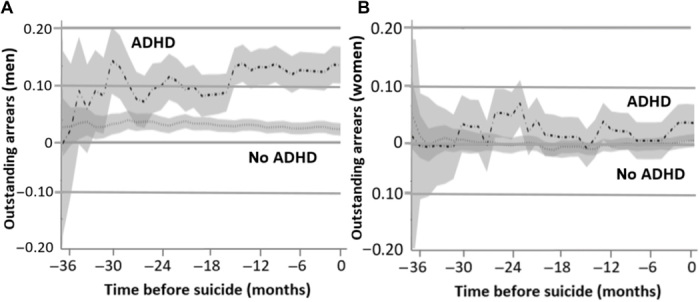

Next, we explore potential changes in financial pressure before suicide for those ever diagnosed with ADHD (n = 190) versus those never diagnosed with ADHD (n = 2120) using a January 2018 snapshot of everyone registered at the Enforcement Agency (Kronofogden) (21). Figure 5 (A and B) (and the Supplementary Materials, Section C) depicts outstanding debt in the 36 months leading up to suicide for men versus women, respectively, in this group, controlling for education, income, physical health, anxiety disorders, substance use disorders, and autism spectrum disorder. Arrear frequency increases significantly in the 3 years before suicide for men diagnosed with ADHD, but not for men without ADHD (Fig. 5A). In contrast, neither women diagnosed with ADHD nor women without ADHD show growth in arrears in the 3 years before suicide (Fig. 5B). Adding depression into the regression equation had no effect on growth in arrears in the 3 years before suicide for men or women diagnosed with ADHD. Although we do not infer a causal relation between financial distress and suicide for men from these data, findings underscore extreme impairment associated with ADHD across the life span, increased chaos in the years immediately preceding suicide, and, likely, need for targeted intervention.

Fig. 5. Growth in debt in the 36 months preceding suicide for those diagnosed with ADHD and those without ADHD.

Suicide data for the full Swedish population are merged with credit data obtained from the Swedish National Enforcement Agency (Kronofogden) mål database (41). Time to event (suicide) is indicated in months. (A) Estimated growth in debt (with 95% CIs) for men diagnosed with ADHD who suicided (n = 131) versus men diagnosed with ADHD who did not suicide (n = 1496). (B) Estimated growth in debt (with 95% CIs) for women diagnosed with ADHD who suicided (n = 59) versus women diagnosed with ADHD who did not suicide (n = 620). Regressions use data from a January 2018 snapshot of everyone registered at the Enforcement Agency who died by suicide, including n = 190 ever diagnosed with ADHD and n = 2120 never diagnosed with ADHD (21).

DISCUSSION

These results provide the first population-based, objective assessment of financial disadvantage faced by individuals diagnosed with ADHD, including associations with suicide. Previous studies documenting financial difficulties of people diagnosed with ADHD derive almost exclusively from self-reports collected from small- to modest-sized treatment-seeking or convenience samples. Such studies indicate overuse and misuse of credit cards, excessive and very high interest rate borrowing, and financial dependence on family members and welfare among adults diagnosed with ADHD (11, 12).

In a very large population sample, we measure the extent of financial distress and hardship among adults diagnosed with ADHD. Adjusting for income, education, psychiatric and health comorbidities, and substance use, problems with debt repayment and continuous default penetrate well into midlife, effects that are likely to become magnified as currently diagnosed young adults age. Because few adults were diagnosed in previous generations (Fig. 1B), assessing effects of persistent ADHD into late life is not yet possible in the Swedish population.

New sympathomimetic prescriptions for ADHD were unassociated with financial outcomes. Arrears per month remained constant in the 2 years preceding and following new prescriptions. These findings are consistent with recent longitudinal studies indicating modest effects of medication on functional outcomes among those with ADHD (9, 33), despite significant concurrent and long-term reductions in core ADHD symptoms such as hyperactivity and inattention (34, 35). Of note, although reduced criminal behavior has been reported among adults diagnosed with ADHD who receive pharmacological treatment (36), other studies find limited effectiveness of stimulants on work productivity and other functional and occupational outcomes (9, 37, 38). As we note above, however, many adults who receive prescriptions for ADHD do not refill them, and proper dosing is important to achieve clinical benefit (39). It is, therefore, possible that medications are more helpful for those who comply with treatment. Unfortunately, we do not have data on adherence, exposure periods, medication possession ratios, or doses.

Although direct causes of financial distress among adults with ADHD remain to be elucidated, a number of plausible mechanisms are suggested by the literature. As reviewed in our introductory paragraphs, adolescents and adults with ADHD suffer from persistent, pervasive functional impairment, as indexed by academic and vocational underachievement, high college dropout rates, poor job performance, difficulty sustaining employment, and lower wages than their peers (4–6). Young adults with ADHD are also more reliant financially on both their parents and social services and earn almost $600,000 less (United States) across their lifetimes than those without ADHD (11). Moreover, self-reported hyperactive and impulsive (but not inattentive) symptoms of ADHD in adulthood are associated with debt burden, high interest rate borrowing, late payments, and present bias in monetary delay discounting tasks, as expressed by preference for smaller, immediate rewards over larger, delayed rewards (12). Together, these findings indicate that compared with others in the population, adults with ADHD (i) have fewer resources at their disposal, which likely contributes to demand for credit, and (ii) are less able to make short-term decisions that translate into long-term financial benefits.

Regardless of mechanisms, our findings indicate that financial distress is associated with suicide among adults with ADHD. Previous reports reveal higher-than-normal rates of suicide among adolescents and adults diagnosed with ADHD in both treatment-seeking and population-based studies (31, 32, 40). However, findings of prospective associations between financial distress and suicide risk have not been reported previously. Participants diagnosed with ADHD whose credit fell in the highest default risk bins were three to four times more likely to die by suicide than both (i) those with ADHD who were at low risk of default and (ii) those without ADHD who had poor credit.

For those diagnosed with ADHD who suicided, men but not women experienced increasing financial distress in the 3 years beforehand. This finding will require future research to explain. For men, the finding is consistent with interpersonal and ideation-to-action frameworks whereby those who are capable to suicide are more likely to attempt when confronted with psychological pain and hopelessness (13, 14), both of which are associated with financial distress (see immediately below). We wish to emphasize, however, that given the descriptive nature of our study, we are unable to identify specific mechanisms or disentangle directions of causality. Thus, we do not know whether financial distress contributes directly to suicidal ideation and suicide for men, and whether both are influenced by unmeasured third variables or, more likely, some combination of factors. Future work should address these important questions. Nevertheless, our findings indicate objective associations between ADHD and a wide range of financial outcomes, with implications for the well-being of affected individuals as they move into middle and old age. On the basis of the data we present, many who are diagnosed with ADHD suffer from significant financial distress throughout adulthood, with likely implications for physical and psychological well-being.

Speculating about specific psychological mechanisms of suicide among those with ADHD and poor financials is even more difficult given that there is no literature base to draw from. One possibility is that poor financials mark more general distress brought about by functional impairment and poor social adjustment, both of which are well documented among adults with ADHD. Relatedly, unemployment, underemployment, and low wages could compromise a sense of purpose among those with ADHD. For men, such feelings may be more acute and difficult to deal with given traditional gender roles; increasingly poor financials may eventually induce a sense of hopelessness that worsens over time as debt accrues and dependence on others becomes entrenched. In turn, low self-worth and feelings of failure may eventually contribute to suicidal behaviors. Testing such notions and devising targeted interventions are potentially important avenues for future research. Such research will require careful planning to evaluate psychological outcomes, including those that may differ for men versus women. Such studies will be challenging given how difficult precise measurement of psychological outcomes is with large, longitudinal samples. Future research might also include financial data in attempts to predict suicide with machine learning algorithms. If successful, then such work could identify prospective vulnerability/risk, an important forerunner in developing effective prevention programs.

Overall, our findings add to a growing literature indicating widespread and persistent functional impairment among adults diagnosed with ADHD and highlight the need for more effective treatments across the life span. As noted above, previous research suggests benefits of pharmacologic treatment on quality of life and other outcomes (36, 38). However, many such studies focus on tests of statistical significance and do not consider clinical or economic significance. Effect sizes on functional outcomes are often modest and smaller than effect sizes for core symptoms (see above) (34). Furthermore, medications rarely remediate symptoms fully (36, 38). Our findings show that new prescriptions are unassociated with changes in a first-order financial behavior—debt repayment. Thus, simply obtaining a prescription is unlikely to address the severe financial distress associated with ADHD in adulthood. Future studies should address important questions regarding medication adherence, financial behaviors, and their associations with suicide to determine (i) whether sympathomimetic prescriptions are helpful for those who take them as prescribed and (ii) whether such medications are more versus less helpful for some individuals with ADHD than others.

MATERIALS AND METHODS

Data on ADHD and suicide for the period 2002–2015 were available for all adults in Sweden who were older than 18 years (N = 11,549,190). Registry data from the entire population were provided by Statistics Sweden (www.scb.se/en/) (16). These data include all individuals ever diagnosed with ADHD (n = 177,336) and never diagnosed with ADHD (n = 11,371,854). No exclusion criteria were used. In Sweden, physicians are required to report ICD (1) diagnostic codes for all physical and mental health conditions, World Health Organization (WHO) Anatomical Therapeutic Chemical codes (1) for all prescription medications, and ICD codes for cause of death to the Swedish National Board of Health and Welfare (Socialstyrelsen; www.socialstyrelsen.se/english) (15). We obtained ICD codes for ADHD, WHO codes for centrally acting sympathomimetics (including dose, purchase date, and prescription date), and ICD codes for suicide as a cause of death. In addition, we obtained credit and default data for a random sample (17) of N = 189,267 participants, including n = 1970 ever diagnosed with ADHD and n = 187,297 never diagnosed with ADHD. These data include consumer credit from 2010 to 2013 and credit inquiries and arrears from 2007 to 2013 from the Swedish National Enforcement Agency (Kronofogden; www.kronofogden.se/InEnglish.html) (21). Descriptive statistics for all variables, including statistical control variables (education, income, sex, psychiatric comorbidities, and physical health), appear in the Supplementary Materials, Section B, table S1 for the full sample, and the Supplementary Materials, Section B, table S2 for the credit and default sample. Technical details for Figs. 1 to 5, including regression equations, control variables, and propensity score analyses, are presented in the Supplementary Materials, Section C.

Supplementary Material

Acknowledgments

We thank T. Hirvikoski for sharing knowledge of ADHD in Sweden, J. Böjeryd and J. Orrenius for excellent research assistance, and both S. P. Hinshaw and A. Vander Stoep for helpful comments. Funding: We thank VINNOVA and the NIH (grant UL1TR002733) for the generous support. Author contributions: I.B.-D. and M.B. designed and directed the research, with T.P.B. assisting. M.B. analyzed the data, with assistance from J. Böjeryd and J. Orrenius. T.P.B. wrote the manuscript, with input from M.B. and I.B.-D. Competing interests: The authors declare that they have no competing interests. Data and materials availability: Complete registry data from the entire Swedish population provided by Statistics Sweden. Diagnostic data (2002–2016 International Classification of Diseases codes for ADHD), prescriptions per patient and month (2005–2016 World Health Organization Anatomical Therapeutic Chemical code N06Ba for centrally acting sympathomimetics including dose, purchase date, and prescription date), and cause of death [registry on cause of death (Dödsorsaksregistret, Socialstyrelsen) including date and ICD categories of X64–X84 for self-intentional] were obtained from Socialstyrelsen. Credit and default data were provided by the Swedish Enforcement Authority (Kronofogden) and a credit registry. External databases are available through an application procedure including a review by the Swedish Ethical Review Board for researchers in Sweden at Socialstyrelsen (www.socialstyrelsen.se/english), Statistics Sweden [www.scb.se/en/ (2018)], and Kronofogden Swedish Enforcement Authority [www.kronofogden.se/InEnglish.html (2018)]. All data needed to evaluate the conclusions in the paper are present in the paper and/or the Supplementary Materials. Additional data related to this paper are available on www.socialstyrelsen.se/english, www.scb.se/en/, and www.kronofogden.se/InEnglish.html.

SUPPLEMENTARY MATERIALS

Supplementary material for this article is available at http://advances.sciencemag.org/cgi/content/full/6/40/eaba1551/DC1

REFERENCES AND NOTES

- 1.World Health Organization, ICD-10 Classification of Mental and Behavioural Disorders (Author, Geneva, Switzerland, 1992).

- 2.Patros C. H. G., Alderson M., Kasper L. J., Tarle S. J., Lea S. E., Hudec K. L., Choice-impulsivity in children and adolescents with attention-deficit/hyperactivity disorder (ADHD): A meta-analytic review. Clin. Psychol. Rev. 43, 162–174 (2016). [DOI] [PubMed] [Google Scholar]

- 3.Beauchaine T. P., Zisner A., Sauder C. L., Trait impulsivity and the externalizing spectrum. Annu. Rev. Clin. Psychol. 13, 343–368 (2017). [DOI] [PubMed] [Google Scholar]

- 4.Loe I. M., Feldman H. M., Academic and educational outcomes of children with ADHD. J. Pediatr. Psychol. 32, 643–654 (2007). [DOI] [PubMed] [Google Scholar]

- 5.Barkley R. A., Fischer M., Smallish L., Fletcher K., Young adult outcome of hyperactive children: Adaptive functioning in major life activities. J. Am. Acad. Child Adolesc. Psychiatry 45, 192–202 (2006). [DOI] [PubMed] [Google Scholar]

- 6.Fletcher J. M., The effects of childhood ADHD on adult labor market outcomes. Health Econ. 23, 159–181 (2014). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Hinshaw S. P., Owens E. B., Zalecki C., Huggins S. P., Montenegro-Nevado A. J., Schrodek E., Swanson E. N., Prospective follow-up of girls with ADHD into early adulthood: Continuing impairment includes elevated risk for suicide attempts and self-injury. J. Consult. Clin. Psychol. 80, 1041–1051 (2012). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.Graziano P. A., Reid A., Slavec J., Paneto A., McNamara J. P., Geffken G. R., ADHD symptomatology and risky health, driving, and financial behaviors in college: The mediating role of sensation seeking and effortful control. J. Atten. Disord. 19, 179–190 (2015). [DOI] [PubMed] [Google Scholar]

- 9.Hinshaw S. P., Arnold L. E.; MTA Cooperative Group , ADHD, multimodal treatment, and longitudinal outcome: Evidence, paradox, and challenge. WIRES Cogn. Sci. 6, 39–52 (2015). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10.Hechtman L., Swanson J. M., Sibley M. H., Stehli A., Owens E. B., Mitchell J. T., Arnold L. E., Molina B. S. G., Hinshaw S. P., Jensen P. S., Abikoff H. B., Algorta G. P., Howard A. L., Hoza B., Etcovitch J., Houssais S., Lakes K. D., Nichols J. Q.; MTA Cooperative Group , Functional adult outcomes 16 years after childhood diagnosis of attention-deficit/hyperactivity disorder: MTA results. J. Am. Acad. Child Adolesc. Psychiatry 55, 945–952.e2 (2016). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11.Altszuler A. R., Page T. F., Gnagy E. M., Coxe S., Arrieta A., Molina B. S. G., Pelham W. E. Jr., Financial dependence of young adults with childhood ADHD. J. Abnorm. Child Psychol. 44, 1217–1229 (2016). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12.Beauchaine T. P., Ben-David I., Sela A., ADHD, delay discounting, and risky financial behaviors: A preliminary analysis of self-report data. PLOS ONE 12, e0176933 (2017). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Klonsky E. D., May A. M., The three-step theory (3ST): A new theory of suicide rooted in the “ideation-to-action” framework. Int. J. Cogn. Ther. 8, 114–129 (2015). [Google Scholar]

- 14.Van Orden K. A., Witte T. K., Cukrowicz K. C., Braithwaite S. R., Selby E. A., Joiner T. E. Jr., The interpersonal theory of suicide. Psychol. Rev. 117, 575–600 (2010). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15.Socialstyrelsen (Swedish National Board of Health and Welfare) (2018); www.socialstyrelsen.se/english.

- 16.Statistics Sweden (2018); www.scb.se/en/.

- 17.Credit and default data for a random sample of Swedes (2018). (20, July, 2018).

- 18.Merikangas K. R., He J.-P., Burstein M., Swanson S. A., Avenevoli S., Cui L., Benjet C., Georgiades K., Swendsen J., Lifetime prevalence of mental disorders in US adolescents: Results from the National Comorbidity Study-Adolescent Supplement (NCS-A). J. Am. Acad. Child Adolesc. Psychiatry 49, 980–989 (2011). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19.Kooij S. J. J., Bejerot S., Blackwell A., Caci H., Casas-Brugué M., Carpentier P. J., Edvinsson D., Fayyad J., Foeken K., Fitzgerald M., Gaillac V., Ginsberg Y., Henry C., Krause J., Lensing M. B., Manor I., Niederhofer H., Nunes-Filipe C., Ohlmeier M. D., Oswald P., Pallanti S., Pehlivanidis A., Ramos-Quiroga J. A., Rastam M., Ryffel-Rawak D., Stes S., Asherson P., European consensus statement on diagnosis and treatment of adult ADHD: The European Network Adult ADHD. BMC Psychiatry 10, 67 (2010). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.Paris J., Bhat V., Thombs B., Is adult ADHD being overdiagnosed? Can. J. Psychiatr. 60, 324–328 (2015). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21.Kronofogden Swedish Enforcement Authority (2018); www.kronofogden.se/InEnglish.html.

- 22.Bos M., Breza E., Liberman A., The labor market effects of credit market information. Rev. Financ. Stud. 31, 2005–2037 (2018). [Google Scholar]

- 23.World Health Organization (2018) Anatomical Therapeutic Chemical/Defined Daily Dose (WHO ATC/DDD); www.whocc.no/atc_ddd_index/.

- 24.Safren S. A., Duran P., Yovel I., Perlman C. A., Sprich S., Medication adherence in psychopharmacologically treated adults with ADHD. J. Atten. Disord. 10, 257–260 (2007). [DOI] [PubMed] [Google Scholar]

- 25.Hawton K., Casañas i Comabella C., Haw C., Saunders K., Risk factors for suicide in individuals with depression: A systematic review. J. Affect. Disord. 147, 17–28 (2013). [DOI] [PubMed] [Google Scholar]

- 26.Beauchaine T. P., Constantino J. N., Redefining the endophenotype concept to accommodate transdiagnostic vulnerabilities and etiological complexity. Biomark. Med 11, 769–780 (2017). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 27.Zisner A., Beauchaine T. P., Neural substrates of trait impulsivity, anhedonia, and irritability: Mechanisms of heterotypic comorbidity between externalizing disorders and unipolar depression. Dev. Psychopathol. 28, 1179–1210 (2016). [DOI] [PubMed] [Google Scholar]

- 28.Pulcu E., Trotter P. D., Thomas E. J., McFarquhar M., Juhasz G., Sahakian B. J., Deakin J. F. W., Zahn R., Anderson I. M., Elliott R., Temporal discounting in major depressive disorder. Psychol. Med. 44, 1825–1834 (2014). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 29.Lynam D. R., Hoyle R. H., Newman J. P., The perils of partialling. Assessment 13, 328–341 (2006). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 30.McDonough-Caplan H. M., Klein D. N., Beauchaine T. P., Comorbidity and continuity of depression and conduct problems from elementary school to adolescence. J. Abnorm. Psychol. 127, 326–337 (2018). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31.Ljung T., Chen Q., Lichtenstein P., Larsson H., Common etiological factors of ADHD and suicidal behavior: A population-based study in Sweden. JAMA Psychiat. 71, 958–964 (2014). [DOI] [PubMed] [Google Scholar]

- 32.Furczyk K., Thome J., Adult ADHD and suicide. Atten. Defic. Hyperact. Disord. 6, 153–158 (2014). [DOI] [PubMed] [Google Scholar]

- 33.Shaw M., Hodgkins P., Caci H., Young S., Kahle J., Woods A. G., Arnold L. E., A systematic review and analysis of long-term outcomes in attention deficit hyperactivity disorder: Effects of treatment and non-treatment. BMC Med. 10, 99 (2012). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 34.Faraone S. V., Glatt S. J., A comparison of the efficacy of medications for adult ADHD using meta-analysis of effect sizes. J. Clin. Psychiatry 71, 754–763 (2010). [DOI] [PubMed] [Google Scholar]

- 35.Fredriksen M., Halmøy A., Faraone S. V., Haavik J., Long-term efficacy and safety of treatment with stimulants and atomoxetine in adult ADHD: A review of controlled and naturalistic studies. Eur. Neuropsychopharmacol. 23, 508–527 (2013). [DOI] [PubMed] [Google Scholar]

- 36.Lichtenstein P., Halldner L., Zetterqvist J., Sjölander A., Serlachius E., Fazel S., Långström N., Larsson H., Medication for ADHD and criminality. N. Engl. J. Med. 367, 2006–2014 (2012). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 37.Gjervan B., Torgersen T., Nordahl H. M., Rasmussen K., Functional impairment and occupational outcome in adults with ADHD. J. Atten. Disord. 16, 544–552 (2012). [DOI] [PubMed] [Google Scholar]

- 38.Adler L. A., Spencer T. J., Levine L. R., Ramsey J. L., Tamura R., Kelsey D., Ball S. G., Allen A. J., Biederman J., Functional outcomes in the treatment of adults with ADHD. J. Atten. Disord. 11, 720–727 (2008). [DOI] [PubMed] [Google Scholar]

- 39.MTA Cooperatieve Group , A 14-month randomized clinical trial of treatment strategies for attention-deficit/hyperactivity disorder. Arch. Gen. Psychiatry 56, 1073–1086 (1999). [DOI] [PubMed] [Google Scholar]

- 40.Chronis-Tuscano A., Molina B. S. G., Pelham W. E., Applegate B., Dahlke A., Overmyer M., Lahey B. B., Very early predictors of adolescent depression and suicide attempts in children with attention-deficit/hyperactivity disorder. Arch. Gen. Psychiatry 67, 1044–1051 (2010). [DOI] [PMC free article] [PubMed] [Google Scholar]

- 41.Kronofogden Swedish Enforcement Authority mål database (2018); www.kronofogden.se/Allmannamal2.html.

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Supplementary material for this article is available at http://advances.sciencemag.org/cgi/content/full/6/40/eaba1551/DC1