Abstract

This paper examines heterogeneity in time discounting among a representative sample of elderly Americans, as well as its role in explaining key economic behaviors at older ages. We show how older Americans evaluate simple (hypothetical) inter-temporal choices in which payments today are compared with payments in the future. Using the indicators derived from this measure, we then demonstrate that differences in discounting patterns are associated with characteristics of particular importance in elderly populations. For example, cognitive deficits are associated with greater impatience, whereas bequest motives are associated with less impatience. We then relate our discounting measure to key economic outcomes and find that impatience is associated with lower wealth, fewer investments in health, and less planning for end of life care.

Keywords: impatience, time preference, self-control, retirement, health, insurance

JEL classifications: D01, D03, D12, D14, D90, E21, G11, I12, I13, J26

Many economic and psychological studies have sought to explore how people make inter-temporal decisions, but most previous research on impatience and its impact on economic and other outcomes has focused mainly on younger individuals (c.f., Burks et al. 2009; Chabris et al. 2008; Schreiber and Weber 2015; Sutter and Kocher 2013). Yet understanding how older individuals make decisions with inter-temporal dimensions is of importance, inasmuch as older people make critically consequential financial decisions that affect the remainder of their lives. Examples include how much to save and spend, when to work versus claim Social Security benefits, whether and how much to invest in health and health insurance, whether to sell one’s home and move, and many other factors central to retirement well-being.

There is also little known about the extent of heterogeneity with regard to time preferences among the elderly, and how such diversity might relate to personal characteristics. If time preference varies systematically with demographic or cultural characteristics, this could have important implications for how economic outcomes vary for the elderly within society. Moreover, time preference could potentially change in old age, something that can only be studied with data on elderly individuals. Aging involves reduced life expectancy, and lower probability of survival could potentially affect discounting of the future. Empirical evidence on whether and how life expectancy affects inter-temporal choice, however, is scarce.1 Some aspects of cognitive functioning also become increasingly difficult at older ages, but little is known about how this might affect intertemporal decision-making. For all of these reasons, it is of interest to delve into questions about inter-temporal choice among the elderly.

In this paper we present and analyze time discounting metrics in a representative sample of individuals age 70+. Specifically, we use a purpose-built survey module we devised for the 2014 Health and Retirement Study (HRS). The key survey items asked respondents to evaluate simple (hypothetical) intertemporal choices in which payments now are compared with payments one year in the future. Respondents’ choices reveal the interest rate that makes each individual indifferent between the smaller, sooner and larger, later payments, i.e., an annual Internal Rate of Return (IRR). Under a set of maintained assumptions on the choice environment and the functional form of utility, the IRR is informative about underlying time preference parameters. For example, under maintained assumptions and the additional assumption of exponential discounting, the IRR corresponds to the exponential discount rate. Under quasi-hyperbolic discounting, it is a function of both the short-term discount rate and the long-term exponential discount rate. Our measure is not designed to distinguish between these different forms of discounting; rather here our focus is on whether time discounting in general is heterogeneous among the elderly, and whether it is associated with important life decisions that the older population confronts.

Henceforth, we refer to an individual’s revealed annual IRR2 as the “annual time discount rate.” We use the measure to examine the levels of and heterogeneity in annual discount rates among the elderly, and we study how this heterogeneity varies with personal characteristics. Moreover, we leverage the rich information about retirement, wealth accumulation, and health behaviors reported in the HRS to evaluate how and whether such heterogeneity helps explain differences in important economic behaviors across older individuals.

To preview results on heterogeneity and determinants, we show that the mean (median) value of the implied discount rate used by our older population to discount future payments is 0.54 (0.58), with a standard deviation of 0.35. We discuss alternative interpretations of this seemingly extreme high degree of impatience, and compare to previous findings with younger populations. Our measure of time discount rates rises with age, whereas whites and the better-educated have lower discount rates, as do individuals with bequest motives. An indicator for mental shortfall is associated with significantly higher discount rates. An index of serious health conditions is associated with 11–30 percent lower discount rates.

When we relate our discounting measure to behaviors of interest using multiple regression models, several notable results emerge. Net wealth is significantly lower for the least patient. We also find that the impatient are less likely to engage in healthy behaviors and to have made provision for end of life challenges. And finally, our analysis shows that Social Security claiming ages are not significantly related to the discount rates.

The next section offers a brief literature review. Next we outline our methodology, and the subsequent section provides descriptive statistics regarding the distribution of discounting factors in the elderly population. Last, we analyze the relationships between our measured discount rates and several important economic and health outcomes. A final section concludes.

Background

Economic theory holds that time preference plays a crucial role in decision-making about inter-temporal tradeoffs. Nevertheless, people are heterogeneous, so those who discount the future more will place a higher value on current versus future consumption. This, in turn, will prompt them to save less and possibly run out of money in old age. Similarly, someone who discounts the future very heavily might claim Social Security benefits earlier, thus committing himself to lower old-age payments the rest of his life. And people who discount the future may make decisions about their own health that expose them to greater risks in old age.

Accordingly, we seek to determine the extent of time discounting in the older population. Moreover, we investigate whether such preferences can help explain heterogeneity in a wide range of decisions including how long to work, whether to invest in one’s own health, whether to purchase long-term care, and what provisions to make regarding the end of one’s life.3 Extreme levels of impatience may also be an indicator of present-biased preferences (Rabin, 2002), as captured by models like the quasi-hyperbolic discounting model (see Laibson, 1996). This type of time discounting implies dynamic inconsistency and can lead to preference reversals, for example individuals stopping work earlier than they had previously planned.

Methods

We designed and implemented a survey module in the 2014 HRS to elicit time discounting patterns among adults over the age of 70.4 We gave respondents who were randomly selected to respond to this module a list of money choices where they considered receiving different payments at different points in time. The decision in the inter-temporal choice exercise was between “$100 today” and some larger amount $Y that would be received 12 months in the future (see the Online Appendix for the wording of our module).

Everyone taking the survey module first received a choice between a hypothetical payment of $100 today versus a delayed payment of $154 twelve months from today. If the respondent indicated that he preferred the later payment, he was shown a smaller delayed amount. If, however, the respondent favored the early payment, he was shown a larger delayed amount. Several such choices were provided until each respondent had indicated the value of Y (or equivalently, the implied annual rate of return) to which he was indifferent, when comparing receiving $100 now versus waiting 12 months. In this way, we obtained an indicator of each respondent’s implied internal rate of return.5

A standard set of maintained assumptions about the choice environment used in the economics literature permits the researcher to infer individual rates of time preference from such a setup. Key assumptions include: linear utility over modest stakes; that respondents treat monetary rewards like consumption opportunities; no credit constraints over a year time horizon; credible payments; and time stationarity of utility. Assuming exponential discounting, the IRR then corresponds to the respondent’s annual exponential discount rate.6

The particular values in our choice exercise were chosen to match the magnitudes of real rewards used in typical incentivized intertemporal choice experiments, which are a standard approach for measuring time discounting.7 Falk et al. (2014) showed that the survey measure we use is a strong and significant predictor of time discounting in incentivized choice experiments.8 Furthermore, Falk et al. (2015) found that the survey discounting measure predicted important outcomes such as savings and human capital accumulation in younger population samples around the world. That evidence provides confidence that our survey measure does capture a trait that is related to behavior under real stakes, despite the hypothetical payments and particular parameter values.

The survey also included a question that could potentially be a proxy for present-bias, which asked about postponing. The latter measure provides a Procrastinator Score for each respondent.9

To the database of survey module responses, we appended information from the HRS Core dataset on several important socio-economic and demographic variables that might be correlated with time discounting.10 These included age, sex, race/ethnicity, education, religion, and an indicator for whether the individual was currently married. In case bequest motives are relevant for respondent’s perceived time horizons and discounting, we also include indicators for the individual’s number of living children and self-reported probability of leaving a bequest. Another potentially relevant control is a cognition score, following Dohmen et al. (2010, 2012) who found a positive correlation between impatience and cognition for a younger population. Since economic theory suggests that life expectancy might influence time discounting, we also consider an index of self-reported serious health conditions. The index is the sum of variables indicating whether the respondent had been told by a doctor that he had cancer, lung disease, a heart condition, or a stroke. A separate variable indicates whether an individual reported having been diagnosed with any kind of cognitive deficit (mental shortfall). The data also include an indicator of whether the respondent was relatively optimistic about his subjective life expectancy (compared to the relevant actuarial age/sex life table). In some models we also control for (ln) household income, as a proxy for access to credit.11

Time Discounting Among the Elderly: Results

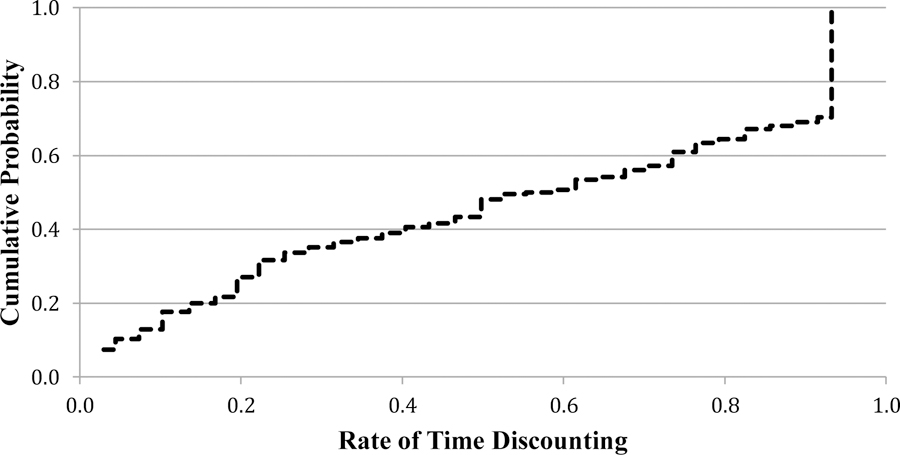

Figure 1 reports the distribution of measured discount rates derived from respondents’ answers to the questions described above. The mean (median) value of the discount rate for our older population is 0.54 (0.58), with a minimum of 0.03, a maximum of 0.93, and a standard deviation of 0.35.12 Note that the category of maximum discount rates is right-censored and thus 0.93 is a lower-bound for the discount rates of individuals in that category.

Figure 1. Cumulative Distribution of Measured Rates of Time Discounting for Older (70+) HRS Respondents.

Note: This figure reports the cumulative distribution function (cdf) of rates of time discounting for the N = 591 respondents of a survey module implemented in the 2014 HRS.

Previous studies have used samples that include younger individuals, and have often found average discount rates that are lower than those observed for the age 70+ population. For example, using a similar methodology to ours involving choices between early and delayed monetary payments, Goda et al. (2015) found an average discount rate of 0.29 for the Rand American Life Panel and the Understanding America Study, both datasets intended to be representative of US adults of all ages. Harrison et al. (2002) found an average discount rate of 0.28 in a representative sample of the Danish adult population, and Dohmen et al. (2012) reported an average discount rate in the range of 0.28 to 0.30 for a representative sample of German adults. Warner and Pleeter (2001) used a different methodology involving much larger financial stakes than the typical experimental study. They estimated discount rates from the choices made by members of the US military between alternative pension schemes. They reported a discount rate in the range of 0.10 to 0.19 for officers, and 0.33 to 0.50 for enlisted soldiers, more or less in line with the experimental studies.13

Although the majority of prior studies estimating individual discount rates using experiments or inter-temporal choices, and younger samples, have reported estimated discount rates lower than the ones we find for the elderly, previous estimates are still substantially above market interest rates (with the notable exception of Simon et al. (2015)). Such results contrast with the prediction of many economic models that people save only to earn interest, and market interest rates adjust towards rates of time preference.14 While the subject remains an area of debate, there are some reasonable explanations for the discrepancy. One could be a systematic tendency to overestimate time preference rates due to the relatively low stakes offered in many previous studies. Indeed, there is evidence from experiments and survey studies that discount rates tend to decrease as stakes increase.15 Another possibility is that the motives for purchases of financial assets and the mechanisms determining interest rates may be poorly understood, particularly when time preferences are heterogeneous and correlated with other preferences and characteristics. Regardless of the interpretation of the level of discounting measures, previous studies have found that the measures provide a useful index for explaining impatient life behaviors, as discussed above.

In Table 1 we report linear regressions of time discounting on personal characteristics. Our approach is to start with a sparse specification that uses explanatory variables that are most plausibly endogenous (column 1), and in subsequent columns, we add controls for variables that are also potentially important determinants of time discounting, but could be partly endogenous. To the extent that coefficients of interest are similar across specifications, this is reassuring about the robustness of the finding. In Column 1 we see a positive and statistically significant relationship with age, on the order of about 5 percentage points per ten years of age. Compared to the mean time discounting rate of 54 points, this is about a 9 percent change. While the effect is not enormous, it is economically meaningful and suggests that rates of impatience rise with age.16 This magnitude is quite robust across specifications that add more controls.

Table 1.

Correlates of the Time Discount Rate for Older HRS Respondents

| Time Discount Rate | ||||||

|---|---|---|---|---|---|---|

| Age | 0.005 | * | 0.006 | ** | 0.005 | * |

| (0.003) | (0.003) | (0.003) | ||||

| Male | 0.007 | 0.028 | 0.034 | |||

| (0.030) | (0.031) | (0.031) | ||||

| White | −0.080 | * | −0.074 | * | −0.069 | * |

| (0.042) | (0.042) | (0.042) | ||||

| Hispanic | 0.080 | * | 0.061 | 0.057 | ||

| (0.048) | (0.048) | (0.048) | ||||

| Education years | −0.008 | −0.007 | −0.006 | |||

| (0.006) | (0.006) | (0.006) | ||||

| Married | −0.006 | −0.012 | 0.001 | |||

| (0.030) | (0.030) | (0.032) | ||||

| Cognition score | −0.002 | −0.002 | −0.001 | |||

| (0.004) | (0.004) | (0.004) | ||||

| Christian | 0.069 | 0.075 | 0.073 | |||

| (0.063) | (0.061) | (0.061) | ||||

| Jewish | −0.017 | −0.025 | −0.019 | |||

| (0.110) | (0.106) | (0.107) | ||||

| Procrastinator score | −0.004 | −0.004 | −0.004 | |||

| (0.004) | (0.004) | (0.004) | ||||

| Optim.10+ years | −0.017 | −0.024 | −0.021 | |||

| (0.029) | (0.028) | (0.028) | ||||

| Have living children | 0.075 | 0.076 | 0.081 | |||

| (0.058) | (0.056) | (0.056) | ||||

| Leave any bequest | −0.117 | *** | −0.125 | *** | −0.115 | *** |

| (0.034) | (0.034) | (0.034) | ||||

| Poor health index | −0.046 | *** | −0.045 | *** | ||

| (0.017) | (0.017) | |||||

| Mental shortfall | 0.216 | *** | 0.210 | *** | ||

| (0.069) | (0.071) | |||||

| Ln(HH income) | −0.023 | ** | ||||

| (0.010) | ||||||

| Intercept | 0.302 | 0.271 | 0.498 | * | ||

| (0.243) | (0.244) | (0.270) | ||||

| N | 591 | 591 | 591 | |||

| R-squared | 0.111 | 0.129 | 0.133 | |||

| Mean of dep. Var. | 0.541 | |||||

| Std.dev. of dep. Var. | 0.345 | |||||

Note:

Significant at 0.10 level

Significant at 0.05 level

Significant at 0.01 level.

Tobit analysis; missing value dummies also included. See text and appendices A and B for variable definitions.

Age variation in discounting might reflect a cohort effect, or it could instead be associated with the aging process. There is limited previous evidence on how time preference changes over the life cycle. Falk et al. (2015) find some evidence that patience declines with age across a range of different countries. Since cohorts differ in historical and life experiences across countries, their findings might be more consistent with a relationship of time discounting and aging per se. Longitudinal data at the individual level are needed to provide more definitive evidence on cohort versus age effects.

Our results also show that Whites have systematically lower measured rates of time discounting than nonwhites, by about 7 percentage points (11 percent relative to the mean); there is no statistically significant differential effect for Hispanics, once controls for health and income are included.17 Interestingly, scoring higher on the cognitive ability18 measure is not significantly related to time discounting, controlling for education.19 Individuals with bequest motives are significantly less impatient, and the magnitude of the difference is large: approximately 11 percentage point lower time discount rate, across all specifications. This is consistent with Butler and Teppa (2007) who found that those without dependent children were more likely to take lump sum cashouts from their pensions, which they surmised might be due to having higher discount rates. The Procrastinator Score measure turns out to be largely unrelated to the discounting measure.

Self-reported health problems, some of them severe enough to imply reduced life expectancy, are significantly related to time discounting. The index is associated with lower discount rates, which could potentially reflect survivorship bias, such that more patient individuals are more likely to survive serious health conditions. Indeed, we show below that more patient individuals take greater precautions in the health domain. The indicator for optimism about life expectancy is not statistically significant.

Economic theory predicts that reduced life expectancy should increase discounting of the future, yet empirical evidence on this point has been scarce, to date.20 Some of our findings are consistent with this prediction including the increase in impatience with age, and the decrease in impatience for individuals with bequest motives and thus, effectively, a longer time horizon. Some of the other findings are less consistent, specifically the lack of a significant relationship between time discounting and the subjective measures of life expectancy.

We also find that discount rates are higher for individuals who report a mental shortfall: for them, discount rates are 21 percentage points (39 percent) higher than average.21 The mechanism could potentially be reduced life expectancy, or it could reflect a systematic impact of mental impairment on decision-making. If mental impairment and eventual dementia lead to more impatient choices, this has important implications for the outcomes of those so affected among the elderly.22

In the Online Appendix, we also check robustness by estimating Tobit models that account for the right-censoring of discount rates. Results are qualitatively similar and in terms of statistical significance, after accounting for censoring of the dependent variable.

Associations between Time Discounting and Key Economic Behaviors

Tables 2 through 5 show how key outcomes of interest are related to our discounting measure. These include respondents’ net wealth, a Healthy Behaviors Index,23 how well prepared people are for end of life contingencies, and retirement behaviors. For each outcome, we first regress it on the rate of time discounting alone. Because time discounting is correlated with other characteristics that might affect the economic outcome in question, we then add controls in subsequent columns, starting with a plausibly exogenous set, and then we add controls that might be more endogenous. Clearly exogenous controls include some of the socio-demographic controls and traits used in Column 1 of Table 1 (age, sex, race/ethnicity, years of education, marital status, cognition score, religion, and procrastinator score). Indicators for health conditions and optimism act as controls for life expectancy, but are more likely to be endogenous. A final model in each case also includes the log of household income as a proxy for credit constraints.24 In general, we find that the results for the observable variables of interest are robust to the inclusion of controls, though quantitative estimates should be treated with care if omitted variable bias remains.

Table 2.

Association of Net Wealth and the Time Discount Rate for Older HRS Respondents

| Net wealth ($1,000) | ||||||

|---|---|---|---|---|---|---|

| Discount rate | −356.323 | ** | −171.124 | −219.016 | ** | |

| (174.394) | (147.775) | (101.108) | ||||

| Age | −5.215 | −11.964 | ||||

| (5.211) | (12.067) | |||||

| Male | −9.123 | 54.449 | ||||

| (99.666) | (92.438) | |||||

| White | 221.080 | ** | 275.762 | |||

| (106.406) | (169.541) | |||||

| Hispanic | 570.630 | 535.272 | ||||

| (480.285) | (389.283) | |||||

| Education years | 68.110 | ** | 87.665 | * | ||

| (30.301) | (50.300) | |||||

| Married | 106.740 | 271.946 | ||||

| (92.718) | (188.044) | |||||

| Cognition score | 12.425 | 15.215 | ||||

| (14.009) | (16.830) | |||||

| Christian | −137.111 | −192.750 | ||||

| (233.034) | (256.023) | |||||

| Jewish | 481.348 | 537.810 | ||||

| (502.600) | (528.132) | |||||

| Procrastinator score | 8.606 | 11.026 | ||||

| (14.584) | (16.158) | |||||

| Optim. live 10+ years | −139.236 | −83.648 | ||||

| (130.349) | (105.088) | |||||

| Have living children | 150.455 | 229.131 | ||||

| (164.890) | (231.928) | |||||

| Leave any bequest | 154.167 | 268.252 | *** | |||

| (154.120) | (77.524) | |||||

| Poor health index | 38.968 | |||||

| (63.466) | ||||||

| Mental shortfall | −255.104 | |||||

| (211.226) | ||||||

| Ln(HH income) | −287.770 | |||||

| (390.445) | ||||||

| Intercept | 675.190 | *** | −495.734 | 2434.373 | ||

| (99.343) | (563.588) | (3628.132) | ||||

| N | 591 | 591 | 591 | |||

| R-squared | 0.007 | 0.056 | 0.093 | |||

| Mean of dep. vars | 482.537 | |||||

| Std.dev. of dep. vars | 1,447.398 | |||||

See notes to Table 1.

Table 5.

Association of Social Security Claiming Age, the Difference between Expected and Actual Social Security Claiming Age, and the Time Discount Rate for Older HRS Respondents

| A. Age received Social Security | B. Actual - Expected Soc Sec Claim Age | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Discount rate | −0.449 | −0.432 | −0.445 | −0.076 | −0.047 | −0.053 | ||||||

| (0.275) | (0.294) | (0.294) | (0.370) | (0.413) | (0.424) | |||||||

| Age | 0.089 | *** | 0.098 | *** | 0.089 | ** | 0.092 | ** | ||||

| (0.023) | (0.023) | (0.043) | (0.043) | |||||||||

| Male | 0.200 | 0.277 | −0.214 | −0.179 | ||||||||

| (0.202) | (0.204) | (0.297) | (0.305) | |||||||||

| White | −0.229 | −0.269 | −0.374 | −0.363 | ||||||||

| (0.314) | (0.313) | (0.426) | (0.431) | |||||||||

| Hispanic | 0.548 | 0.540 | 0.493 | 0.425 | ||||||||

| (0.339) | (0.354) | (0.547) | (0.560) | |||||||||

| Education years | 0.108 | *** | 0.104 | *** | 0.017 | 0.019 | ||||||

| (0.034) | (0.035) | (0.052) | (0.053) | |||||||||

| Married | −0.017 | −0.149 | 0.052 | −0.015 | ||||||||

| (0.194) | (0.208) | (0.290) | (0.311) | |||||||||

| Cognition score | −0.038 | −0.039 | 0.023 | 0.018 | ||||||||

| (0.026) | (0.025) | (0.042) | (0.043) | |||||||||

| Christian | −0.451 | −0.494 | −0.177 | −0.146 | ||||||||

| (0.445) | (0.460) | (0.545) | (0.554) | |||||||||

| Jewish | 1.137 | 1.030 | −2.726 | *** | −2.590 | ** | ||||||

| (0.935) | (0.917) | (1.000) | (1.010) | |||||||||

| Procrastinator score | 0.001 | 0.008 | 0.036 | 0.037 | ||||||||

| (0.029) | (0.029) | (0.046) | (0.046) | |||||||||

| Optim10+ | 0.185 | 0.142 | 0.320 | 0.279 | ||||||||

| (0.190) | (0.195) | (0.272) | (0.281) | |||||||||

| Have living children | −0.452 | −0.427 | −0.263 | −0.240 | ||||||||

| (0.594) | (0.601) | (0.941) | (0.943) | |||||||||

| Leave any bequest | 0.114 | −0.028 | 0.467 | 0.417 | ||||||||

| (0.256) | (0.277) | (0.441) | (0.468) | |||||||||

| Poor health index | −0.214 | * | −0.158 | |||||||||

| (0.111) | (0.163) | |||||||||||

| Mental shortfall | −0.668 | −1.875 | *** | |||||||||

| (0.748) | (0.465) | |||||||||||

| Ln(HH income) | 0.190 | 0.055 | ||||||||||

| (0.121) | (0.149) | |||||||||||

| Intercept | 63.653 | *** | 56.921 | *** | 54.662 | *** | −0.141 | −7.619 | ** | −8.199 | ** | |

| (0.174) | (1.974) | (2.367) | (0.248) | (3.555) | (4.007) | |||||||

| N | 465 | 465 | 465 | 350 | 350 | 350 | ||||||

| R-squared | 0.006 | 0.097 | 0.116 | 0.000 | 0.063 | 0.069 | ||||||

| Mean of dep. vars | 63.413 | −0.181 | ||||||||||

| Std.dev. of dep. vars | 2.041 | 2.466 | ||||||||||

See notes to Table 1.

Net Wealth.

The first four columns of Table 2 show that, regardless of whether we hold other factors constant, there is a strong and statistically significant relationship between respondents’ rate of time discounting and their net wealth (the latter is measured in thousands). Specifically, those with higher discount rates have lower wealth, and the coefficient magnitudes are large across all four columns. Focusing on the columns including controls, a discounting coefficient of around −219 suggests that someone with a discount rate one standard deviation above the mean would have 16 percent less wealth than his counterpart at the mean (=0.35*375/482). Goda et al. (2013) found a large and significant correlation between time discounting and retirement wealth, for younger age groups, and Hurd and Rohwedder (2013) reported lower wealth for those indicating they had a short planning horizon. Our results are also consistent with the idea that discount rates measured in old age are informative for understanding variation in retirement wealth. Interestingly, the relationship of wealth with education is positive and significant when household income is excluded. Overall, the models account for between 11–12 percent of variation in the wealth variable.

Health.

We next turn to an examination of how a Healthy Behaviors Index varies according to the discount rate and other factors. The index is the sum of indicators for had flu shot, and (as appropriate) got mammogram/Pap smear or prostate test; nonsmoker; healthy drinker (≤ 1 drink/day). Table 3 shows that people having higher discount rates are less likely to engage in these healthy behaviors, and the relationships are statistically significant. Quantitatively, they are on the small side: for instance, an individual with a standard deviation higher discount rate would have about 3 percent more healthy behaviors than average (=0.35*0.25/3.3).25 Chabris et al. (2008) documented a relationship between discount rates and health behaviors for several samples of individuals with different age ranges, all much younger than our sample, and Sutter and Kocher (2013) reported similar results for high school age students. Our results confirm that discount rates are also related to health behaviors towards the end of life. We find that age also has a positive and significant coefficient in the regression explaining health behaviors, though the magnitude is again small. Men have significantly fewer healthy behaviors, as measured by our Healthy Behaviors Index.

Table 3.

Association of Health Index with the Time Discount Rate for Older HRS Respondents

| Healthy Behaviors Index | ||||||

|---|---|---|---|---|---|---|

| Discount rate | −0.300 | ** | −0.269 | ** | −0.254 | * |

| (0.126) | (0.129) | (0.130) | ||||

| Age | 0.039 | *** | 0.040 | *** | ||

| (0.008) | (0.008) | |||||

| Male | −0.273 | *** | −0.311 | *** | ||

| (0.099) | (0.100) | |||||

| White | 0.083 | 0.071 | ||||

| (0.126) | (0.123) | |||||

| Hispanic | 0.058 | 0.106 | ||||

| (0.159) | (0.157) | |||||

| Education years | 0.018 | 0.014 | ||||

| (0.018) | (0.017) | |||||

| Married | 0.110 | 0.067 | ||||

| (0.093) | (0.098) | |||||

| Cognition score | 0.012 | 0.011 | ||||

| (0.011) | (0.011) | |||||

| Christian | 0.306 | 0.305 | ||||

| (0.223) | (0.233) | |||||

| Jewish | 0.148 | 0.097 | ||||

| (0.305) | (0.306) | |||||

| Procrastinator score | −0.011 | −0.012 | ||||

| (0.013) | (0.013) | |||||

| Optim. live 10+ years | −0.125 | −0.141 | ||||

| (0.087) | (0.088) | |||||

| Have living children | −0.298 | −0.320 | * | |||

| (0.188) | (0.184) | |||||

| Leave any bequest | 0.136 | 0.132 | ||||

| (0.108) | (0.109) | |||||

| Poor health index | 0.045 | |||||

| (0.050) | ||||||

| Mental shortfall | 0.262 | |||||

| (0.175) | ||||||

| Ln(HH income) | 0.070 | ** | ||||

| (0.033) | ||||||

| Intercept | 3.466 | *** | −0.148 | −0.912 | ||

| (0.079) | (0.772) | (0.833) | ||||

| N | 514 | 514 | 514 | |||

| R-squared | 0.011 | 0.111 | 0.123 | |||

| Mean of dep. vars | 3.305 | |||||

| Std.dev. of dep. vars | 0.970 | |||||

See notes to Table 1.

End of Life Provision.

We are also interested in whether impatient people are also less likely to put into place precautions around their end-of-life challenges. Understanding decisions about end of life care is important, given the large impact of end of life care on health care costs in the United States (De Nardi, French, and Jones 2010). We provide some first evidence on whether variation in time discounting is related to such decisions. Our End of Life Index is a count of the number of affirmative responses each respondent gave to questions about whether he had long-term care insurance, a power of attorney, a living will, and had discussed end of life medical care plans with others. The mean (median) value of this index is 1.7 (2), with a standard deviation of 1.3.

Table 4 shows the results from our descriptive regressions. Our sample size is somewhat attenuated since almost six percent of the sample did not respond to all the questions comprising the End of Life Index. The first column confirms a negative and statistically significant relationship of the discounting measure to the end of life index, so impatience is inversely related to taking health precautions around the end of life. Nevertheless the coefficient is attenuated and significance falls with the inclusion of other controls. Other significant relationships include the positive and significant effect of age, where 15 additional years of age would be associated with half a point increase in the End of Life score, or an improvement of 27% (from the mean of 1.7). Whites also score about 0.5 points higher than nonwhites (30 percent), while Hispanics score 0.7 points (41 percent) lower than non-Hispanics, and both effects are strongly significant. Years of education has a significant, positive relationship with the index, with 1 more year associated with 0.1 point increase (6 percent). The only other factor which is notably negatively associated with making End of Life provisions is being married, such that married individuals score 0.34 points (or 20 percent) below their single counterparts.

Table 4.

Association of the End of Life Index with the Time Discount Rate for Older HRS Respondents

| End of Life Index | ||||||

|---|---|---|---|---|---|---|

| Discount rate | −0.599 | *** | −0.202 | −0.190 | ||

| (0.164) | (0.159) | (0.162) | ||||

| Age | 0.030 | ** | 0.029 | ** | ||

| (0.012) | (0.012) | |||||

| Male | −0.140 | −0.177 | ||||

| (0.115) | (0.119) | |||||

| White | 0.544 | *** | 0.521 | *** | ||

| (0.149) | (0.149) | |||||

| Hispanic | −0.710 | *** | −0.661 | *** | ||

| (0.164) | (0.171) | |||||

| Education years | 0.106 | *** | 0.102 | *** | ||

| (0.020) | (0.020) | |||||

| Married | −0.313 | *** | −0.340 | *** | ||

| (0.111) | (0.115) | |||||

| Cognition score | 0.021 | 0.020 | ||||

| (0.014) | (0.014) | |||||

| Christian | 0.332 | 0.301 | ||||

| (0.259) | (0.255) | |||||

| Jewish | 0.627 | 0.576 | ||||

| (0.483) | (0.480) | |||||

| Procrastinator score | −0.008 | −0.008 | ||||

| (0.015) | (0.015) | |||||

| Optim10+ | −0.027 | −0.030 | ||||

| (0.106) | (0.108) | |||||

| Have living children | 0.283 | 0.261 | ||||

| (0.235) | (0.234) | |||||

| Leave any bequest | 0.081 | 0.056 | ||||

| (0.122) | (0.125) | |||||

| Poor health index | 0.059 | |||||

| (0.060) | ||||||

| Mental shortfall | 0.274 | |||||

| (0.234) | ||||||

| Ln(HH income) | 0.070 | |||||

| (0.054) | ||||||

| Intercept | 1.973 | *** | −3.126 | *** | −3.608 | *** |

| (0.105) | (1.064) | (1.182) | ||||

| N | 487 | 487 | 487 | |||

| R-squared | 0.026 | 0.256 | 0.261 | |||

| Mean of dep. var. | 1.655 | |||||

| Std.dev. of dep. var. | 1.264 | |||||

See notes to Table 1.

Retirement Behavior.

Next we turn to an examination of how retirement patterns vary across more, versus less, patient HRS respondents. Two outcomes are of interest in Table 5: Panel A investigates the age at which people initiated their Social Security benefits, or what is often termed the Social Security claiming age, while Panel B focuses on the difference between peoples’ actual Social Security claiming age and their expected claiming age.26

The analysis in Panel A suggests that only age and education are positively and significantly associated with respondents’ Social Security claiming ages. Poor health is also associated with a marginally significant reduction in claiming age. The point estimate for the discounting measure is substantial and negative, as would be expected if more impatient people placed less weight on earning money for future, post-retirement consumption. Nevertheless this relationship is not statistically significant.

Results in Panel B show that discount rates are negatively associated with the difference between actual and expected claiming ages, but the relationship is not statistically significant. That least patient people claimed earlier than expected is consistent with the preference reversal behavior of Rabin (2002) mentioned above. Beyond age, little else is associated with this difference other than being Jewish (negative and significant) and mental shortfall (also negative and significant).

Our findings regarding retirement outcomes contrast to some extent with evidence from Schreiber and Weber (2016). They conducted an online survey with roughly 3,000 German newspaper readers, and they reported that a measure of present bias was associated with earlier retirement and a greater discrepancy between planned and actual retirement ages, in the direction of retiring earlier than expected. One possible explanation for the difference in our results is that their measure of present bias was formatted differently from ours. Another possible explanation is that they used self-reported retirement age, such that respondents offered their own subjective definition of what it means to be retired. Our approach uses a more objective, although not necessarily better, approach to measuring retirement, namely the Social Security claiming age collected in real time in the HRS panel.

In the Online Appendix we check an alternative specification for the discounting variable accounting for censoring. Specifically, we include a dummy variable for right-censored discount rates, as well as a variable that measures uncensored discount rates. We find the same qualitative relationships of discounting to outcomes as shown in Tables 2 through 5; at the same time, the results are typically strongest and statistically significant for the censored category. The coefficient for uncensored discount rates is always the same sign but sometimes not statistically significant. These latter findings are not surprising given that the censored category captures individuals with the most extreme impatience. There are only two notable differences in the results based on this alternative specification: Discounting is no longer statistically significant for the Healthy Behaviors Index, in the specification with all controls; (censored) discount rates become statistically significant in the regressions for Social Security claiming ages, with the most impatient individuals claiming earlier.

Conclusions and Policy Implications

To date, the literature on impatience and discount rates has not focused on the elderly nor has much work been done on the role of time discounting regarding important decisions in retirement and near the end of life. Using a purpose-built module in the HRS, we have developed experimental elicitations of time discounting over money to show that the mean (median) value of the discount rate for our older population is 0.54 (0.58), with a standard deviation of 0.35. Our discounting measures rise with age. We also show that Whites and the better-educated have lower discount rates. Individuals with bequest motives choose more patiently in the discounting measure. Being diagnosed with a cognitive deficit is associated with higher discount rates.

When we relate our impatience measures to behaviors of interest using multiple regression models, several interesting results emerge. Net wealth is significantly lower for the least patient, probably indicating that the least patient save less and therefore arrive at old age with fewer assets. We also find that the impatient are much less likely to engage in healthy behaviors and to have made provision for end-of-life challenges. Finally, our analysis shows that Social Security claiming ages are not significantly related to the IRRs.

Our findings add to the literature on discounting behavior as well as to the understanding of decision processes in later life. For instance, the existence of widespread impatience among older Americans suggests that people might be willing to take less than actuarially fair incentives in exchange for working longer, particularly if they had access to lump sums.27 Increasing immediate rewards to other behaviors could also encourage choices such as investing in one’s health and making end of life decisions in advance of need.

Future work can pursue some intriguing questions raised by our findings on time discounting. One concerns the explanation for the relationship of age to time discounting. Since almost all data sets measuring discount rates are cross-sectional, it has not been possible to disentangle cohort effects from effects of the aging process. Finding that discount rates vary with age in the relatively narrow age band of our sample casts some doubt on the cohort explanation, although the evidence is clearly not definitive. If it is the process of aging that affects discount rates, what could be the mechanism? One might be reduced survival probability, in line with the finding that diagnosis of serious health conditions is also associated with higher discount rates. The relationship between mental shortfall and discount rates also hints at possible consequences of Alzheimer’s and related conditions having systematic impacts on decision-making, something that calls for further study.

Future work on the older population could also parse out the distinction between different forms of time discounting, such as exponential versus quasi-hyperbolic. In our telephone-based module in the HRS survey of the elderly, we could not implement the more complex and time-consuming measures that might be useful in drawing this distinction (see Frederick et al., 2002 and Augenblick et al., 2015). Disentangling exponential from other forms of discounting could be useful because of the differing welfare and policy implications. Specifically, the dynamic inconsistency that arises from non-exponential discounting raises concerns about self-control problems. The possibility of dynamically inconsistent time preferences has prompted policy discussions about interventions that could potentially correct sub-optimally low savings rates (Ashraf, Karlan, and Yin 2006), overconsumption of harmful goods such as smoking and drinking (Camerer et al. 2003), poverty (Carvalho, Meier, and Wang 2016), financial illiteracy (Lusardi and Mitchell 2007), and financial mistakes over the life cycle (Agarwal et al. 2009). Likewise there is substantial interest in finding ways to encourage people to delay retirement so they can enjoy greater Social Security benefits at older ages (Alleva 2016; Maurer et al. 2016; 2017).

Acknowledgments

The research reported herein was performed pursuant to a grant from the U.S. Social Security Administration (SSA) funded as part of the Michigan Retirement Research Center. The authors also acknowledge support from the Pension Research Council/Boettner Center at the Wharton School of the University of Pennsylvania. They have also benefited from expert programming assistance of Yong Yu. Mitchell is a Trustee of the Wells Fargo Advantage Funds and has received research support from TIAA. This is part of the NBER Program on the Economics of Aging. Opinions and conclusions expressed herein are solely those of the authors and do not represent the opinions or policy of the SSA, any other agency of the Federal Government, or any institution with which the authors are affiliated.

Appendix A. Variables Used in the Analysis

Economic and Health Outcomes

Net Wealth: All household assets minus debt, including home.

Healthy Behaviors Index: Sum of scores for had flu shot, and (as appropriate) got mammogram/Pap smear or prostate test; nonsmoker; healthy drinker (≤ 1 drink/day)

End of Life Index: sum of scores for had LTC, living will, disability care, power of attorney.

Age Received SocSec: Actual age claimed Social Security

Act-Expected SocSec Claim Age: Actual – Expected (at baseline) Social Security claim age

Preferences and Socio-Demographic Controls

Ln (HH income): Set to zero if income is zero.

Procrastinator Score: Self-reported response to question “How well does the following statement describe you as a person? I tend to postpone things even though it would be better to get them done right away. Use a scale from 0 to 10, where 0 means “does not describe me at all” and a 10 means “describes me perfectly”. Use the values in-between to indicate where you fall on the scale.”

Cognition Score: This is the sum of the Total Word Recall summary plus the Mental Status summary. The Total Word Recall summary is the sum of each respondent’s immediate and delayed word recall scores. The Mental Status summary adds the scores for the respondent’s Serial 7’s, Backwards counting from 20, and Object, Date, and President/Vice-President naming tasks. The total cognition score sums the total word recall and mental status summary scores, resulting in a range of 0–35.

Age: Self-reported

Male: Self-reported

Race/ethnicity: Self-reported

Education (years): Self-reported

Married: Self-reported

Christian/Jewish/other: Self-reported

Optimistic live 10+ years: Equal to 1 if the respondent’s self-reported probability of living 10 more years exceeded the age/sex specific value in a cohort life table, 0 else.

Living Children: Number of living children, self-reported.

Leave a bequest: Self-reported probability of leaving a bequest.

Poor Health Index: Count of diagnosed with cancer/lung disease/heart condition/stroke, self-reported.

Mental shortfall: Yes if: “self-reported doctor has ever told you that you have dementia, senility, or any other serious mental impairment or Alzheimer’s Disease?” If the respondent answered either question with a “yes” response, we coded him as reporting a mental shortfall.

Appendix B. Descriptive Statistics for Key Variables

| N | Mean | St.dev. | Min | Median | Max | |

|---|---|---|---|---|---|---|

| IRR | 591 | 0.54 | 0.35 | 0.03 | 0.58 | 0.93 |

| Net wealth ($1,000) | 591 | 483 | 1,447 | −196 | 175 | 25,000 |

| Healthy Behaviors Index | 514 | 3.31 | 0.97 | 1 | 3 | 5 |

| End of Life Index | 487 | 1.66 | 1.26 | 0 | 2 | 4 |

| Impatience index | 575 | −0.01 | 1.50 | −2.62 | −0.01 | 3.38 |

| Age Received SocSec | 465 | 63.41 | 2.04 | 60 | 62.8 | 73.1 |

| Act-Expected SocSec Claim Age | 350 | −0.18 | 2.47 | −14 | 0.1 | 9.1 |

| Age | 591 | 79.03 | 5.69 | 71 | 78 | 99 |

| Male | 591 | 0.38 | 0.49 | 0 | 0 | 1 |

| White | 591 | 0.85 | 0.36 | 0 | 1 | 1 |

| Hispanic | 591 | 0.10 | 0.30 | 0 | 0 | 1 |

| Education years | 591 | 12.38 | 3.24 | 0 | 12 | 17 |

| Married | 591 | 0.47 | 0.50 | 0 | 0 | 1 |

| Cognition score | 591 | 21.39 | 4.60 | 7 | 22 | 34 |

| Christian | 591 | 0.93 | 0.25 | 0 | 1 | 1 |

| Jewish | 591 | 0.02 | 0.13 | 0 | 0 | 1 |

| Procrastinator score | 591 | 4.75 | 3.44 | 0 | 5 | 10 |

| Optim. live10+years | 591 | 0.54 | 0.50 | 0 | 1 | 1 |

| Have living children | 591 | 0.92 | 0.28 | 0 | 1 | 1 |

| Leave any bequest | 591 | 0.69 | 0.46 | 0 | 1 | 1 |

| Poor health index | 591 | 0.85 | 0.86 | 0 | 1 | 4 |

| Mental shortfall | 591 | 0.02 | 0.12 | 0 | 0 | 1 |

| Ln(HH income) | 591 | 10.36 | 1.16 | 0.00 | 10.39 | 13.54 |

Footnotes

One exception is Oster, Shoulson, and Dorsey (2013), who show that individuals who are diagnosed with Huntington’s disease at an early age make decisions consistent with greater discounting of the future. Sunde and Dohmen (2016) have a nice recent review of preferences and aging, but they focus mainly on risk attitudes and not time preferences as we do here.

The IRR is the interest rate, which sets equal the net present value of the future money amount and the money amount offered today.

Meier and Sprenger (2015) report stability in peoples’ attitudes toward time discounting over a time span of two years, but Dohmen et al. (2010) report some fluidity over the life cycle.

For a description of the HRS data see http://www.rand.org/labor/aging/dataprod/hrs-data.html. Our survey module was fielded immediately after HRS respondents completed their regular bi-annual surveys. The research sample was limited to subjects age 70+, roughly the midpoint of the age range of HRS respondents.

See the Online Appendix for detail on the computation method and how we handled non-responses.

Under an alternative assumption about discounting such as quasi-hyperbolic, the IRR is a function of both the exponential discount rate, delta, and a short term discount rate, beta. Due to time constraints in the survey, we did not attempt to implement more complex measures designed to separately identify delta and beta for each individual.

The experiment-based approach is based on the idea using real incentives is better for accurately measuring time preference than using hypothetical incentives. Given experimenter budget constraints, the stakes used in experiments are necessarily modest. It is also typically too costly to conduct such experiments in larger, representative samples. See Harrison, Lau, and Williams (2002) for a seminal paper on using choice experiments to measure individual discount rates in a representative sample.

Falk et al. (2014) had subjects participate in incentivized intertemporal choice experiments and also answer a battery of different survey questions about time discounting. The survey measure we use is based on one of the best predictors of choices in those incentivized experiments (a measure that is part of the Falk et al. Preference Survey Module).

The Procrastinator Score is measured by the respondent’s answer to this question: How well does the following statement describe you as a person? I tend to postpone things even though it would be better to get them done right away. Use a scale from 0 to 10, where 0 means “does not describe me at all” and a 10 means “describes me perfectly”. Use the values in-between to indicate where you fall on the scale.

Most variables were taken from the RAND HRS datafile (see footnote 6) though in a few cases we used 2014 HRS wave variables which had not yet been integrated into the RAND file.

Appendix A lists all control variables with definitions, and means of all variables appear in Appendix B. More information on variable construction appears in the Online Appendix.

These are computed as described in the Online Appendix. In the paper we report all discount rate values compounded semi-annually, since results are not particularly sensitive to different compounding periodicities.

A caveat regarding the latter results concerns a potential confound due to credit constraints. In a follow-up paper, Simon et al. (2015), returned to the US military sample but used a pension choice setting that they argue avoids confounds due to credit constraints. They found much lower discount rates, on the order of 0.07 for enlisted and 0.02 – 0.04 for officers.

The levels of measured discount rates also imply extreme long-term impatience, in the context of the exponential discounting model. With alternative discounting assumptions, implications for long-term patience can be less extreme.

See Frederick et al. (2002) for a discussion of the so-called magnitude effect. Sensitivity of discounting to stake sizes is not consistent with typical discounting models, including exponential and quasi-hyperbolic.

The positive relationship between age and time discount rates may help account for the finding that older persons are more likely to cash out their pension balances around the time of retirement (c.f., Hurd and Panis, 2006).

Hurd and Panis (2006) report that Blacks are more likely to cash out their pension balances than Whites, which could be explained by the lower discount rates we measure for Whites in our analysis.

The measurement of cognition in the HRS is detailed in Fisher et al. (2015).

A number of other studies have studied how cognitive ability affects impatience including Benjamin et al., (2013) and Dohmen et al. (2010), though not for the older population as here.

One exception is Oster, Shoulson, and Dorsey (2013), who studied individuals diagnosed with Huntington’s disease at an early age; learning about the disease was associated with changes in behavior such as choosing to retire earlier, which could reflect greater discounting of the future. Our sample of the elderly provides another opportunity to shed light on this question, but with direct measures of time discounting, and provides converging evidence with Oster, Shoulson, and Dorsey (2013).

Individuals with severe dementia or Alzheimers had proxy interviews and were excluded from our module sample.

This is measured as the number of precautionary health practices undertaken by the respondent such as getting a flu shot, not smoking, not drinking to excess, and having the relevant gender-appropriate annual exams (e.g., prostate exams, Pap and mammograms).

If individuals expect expenses to come up within the next year, and are unable to borrow against future income, this could lead them to choose the early payments in the discounting measure, even if they have low discount rates. We use income as a proxy for access to credit, lacking a better proxy in the HRS.

Our findings suggest that, while impatience is relevant for explaining heterogeneity in health behaviors, the contribution is modest in size. This could explain why incentives for health behaviors designed to counteract impatience by making present benefits larger do not have particularly long-lasting effects; see McConnell (2016).

Our findings suggest that, while impatience is relevant for explaining heterogeneity in health behaviors, the contribution is modest in size. This could explain why incentives for health behaviors designed to counteract impatience by making present benefits larger do not have particularly long-lasting effects; see McConnell (2016).

The respondent’s expected claiming age is taken from the earliest reported HRS wave. Both analyses include only the subset of HRS respondents with nonmissing and nonzero actual and expected claiming ages.

See Maurer, Mitchell, Rogalla and Schimetschek (2017) for a theoretical analysis of this potential policy reform.

Contributor Information

David Huffman, Department of Economics, University of Pittsburgh, 4901 Wesley Posvar Hall, 230 South Bouquet Street, Pittsburgh PA 15260.

Raimond Maurer, Finance Department, Goethe University, Theodor-W.-Adorno Platz 3, 60323 Frankfurt am Main, Germany.

Olivia S. Mitchell, The Wharton School of the University of Pennsylvania, Dept of Business Economics & Policy, 3620 Locust Walk, St 3000 Steinberg Hall-Dietrich Hall, Philadelphia, PA 19104

References

- Agarwal S, Driscoll JC, Gabaix X, and Laibson D (2009). “The Age of Reason: Financial Decisions over the Life Cycle and Implications for Regulation.” Brookings Papers on Economic Activity. (2): 51–101. [Google Scholar]

- Alleva B (2016). “Discount Rate Specification and the Social Security Claiming Decision.” Social Security Bulletin. 76(2): 1–15. [Google Scholar]

- Ashraf N, Karlan D, and Yin W (2006). “Tying Odysseus to the Mast: Evidence from a Commitment Savings Product in the Philippines.” Quarterly Journal of Economics. 121(2): 635–672. [Google Scholar]

- Benjamin DJ, Brown SA, and Shapiro JM (2013). “Who is ‘Behavioral?’ Cognitive Ability and Anomalous Preferences.” Journal of the European Economic Association. 11 (6): 1231–55 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Burks SV, Carpenter JP, Goette L, and Rustichini A (2009). “Cognitive Skills Affect Economic Preferences, Strategic Behavior, and Job Attachment.” PNAS 106 (19): 7745–50. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Butler M, Teppa F (2007). “The Choice between an Annuity and a Lump Sum: Results from Swiss Pension Funds.” Journal of Public Economics. 91(10): 1944–1966 [Google Scholar]

- Camerer C, Issacharoff S, Loewenstein G, O’Donoghue T, and Rabin M (2003). “Regulation for Conservatives: Behavioural Economics and the Case for “Asymmetric Paternalism”. U Penn Law Review. 1151:1211–54. [Google Scholar]

- Carvalho LS, Meier S, and Wang SW (2016). “Poverty and Economic Decision-Making: Evidence from Changes in Financial Resources at Payday.” American Economic Review. 106(2): 260–294. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Chabris CF, Laibson D, Morris CL, Schuldt JP, and Taubinsky D (2008). “Individual Laboratory-measured Discount Rates Predict Field Behavior.” Journal of Risk and Uncertainty. 37(2–3): 237–269. [DOI] [PMC free article] [PubMed] [Google Scholar]

- De Nardi M, French E, and Jones JB (2010). “Why do the Elderly Save? The Role of Medical Expenses.” Journal of Political Economy. 118(1): 39–75. [Google Scholar]

- Dohmen T, Falk A, Golsteyn B, Huffman D, and Sunde U (Forthcoming). “Risk Attitudes across the Life Course.” Economic Journal. [Google Scholar]

- Dohmen T, Falk A, Huffman D, and Sunde U (2012). “Interpreting Time Horizon Effects in Inter-Temporal Choice.” IZA DP No. 6385.

- Dohmen T, Falk A, Huffman D, and Sunde U (2010). “Are Risk Aversion and Impatience Related to Cognitive Ability?” American Economic Review. 100(3): 1238–1260. [Google Scholar]

- Falk A, Becker A, Dohmen T, Huffman D and Sunde U (2014). “An Experimentally-Validated Survey Module of Economic Preferences.” University of Oxford Working Paper. [Google Scholar]

- Falk A, Becker A, Dohmen TJ, Enke B, Huffman D, and Sunde U (2015). “The Nature and Predictive Power of Preferences: Global Evidence.” (No. 11006). CEPR Discussion Paper. [Google Scholar]

- Fisher G, Hassan H, Faul JD, Rodgers WL, and Wei DR (2015). Health and Retirement Study Imputation of Cognitive Functioning Measures: 1992 – 2012. (Final Release Version). http://hrsonline.isr.umich.edu/modules/meta/xyear/cogimp/desc/COGIMPdd.pdf

- Frederick S, Loewenstein G, and O’donoghue T (2002). “Time Discounting and Time Preference: A Critical Review.” Journal of Economic Literature. 40(2), 351–401. [Google Scholar]

- Goda GS, Levy M, Manchester CF, Sojourner A, and Tasoff J (2015). “The Role of Time Preferences and Exponential-Growth Bias in Retirement Savings.” NBER WP 21482.

- Harrison GW, Lau MI, and Williams MB (2002). “Estimating Individual Discount Rates in Denmark: A Field Experiment.” American Economic Review. 92(5), 1606–1617. [Google Scholar]

- Hurd M and Panis S (2006). “An Analysis of the Choice to Cash Out, Maintain, or Annuitize Pension Rights upon Job Change or Retirement.” Journal of Public Economics. 90 (12): 2213–2217 [Google Scholar]

- Hurd M and Rohwedder S. (2013). “Heterogeneity in Spending Change at Retirement.” The Journal of the Economics of Ageing. 1–2: 60–71. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Lusardi A, Mitchell OS (2007). “Baby Boomer Retirement Security: The Roles of Planning, Financial Literacy, and Housing Wealth.” Journal of Monetary Economics. 54(1): 205–224. [Google Scholar]

- Maurer R, Mitchell OS, Schimetschek T, and Rogalla R (2017). “Will They Take the Money and Work? An Empirical Analysis of People’s Willingness to Delay Claiming Social Security Benefits for a Lump Sum.” Journal of Risk and Insurance. Available online November 2016. [Google Scholar]

- Maurer R, Mitchell OS, Rogalla R, and Schimetschek T (2017). “Optimal Social Security Claiming Behavior under Lump Sum Incentives: Theory and Evidence.” PRC Working Paper. [Google Scholar]

- McConnell M (2013). “Behavioral Economics and Aging.” The Journal of the Economics of Ageing. 1–2: 83–89. [Google Scholar]

- Meier Stephan and Sprenger Charles. 2015. “The Stability of Time Preferences.” Review of Economics and Statistics. 97(2): 273–286. [Google Scholar]

- Oster E, Shoulson I, and Dorsey ER (2013). “Optimal Expectations and Limited Medical Testing: Evidence from Huntington Disease.” American Economic Review. 103(2): 804–830. [DOI] [PubMed] [Google Scholar]

- Rabin M 2002. “A Perspective on Psychology and Economics.” European Economic Review. 46(4): 657–685. [Google Scholar]

- Schreiber P and Weber M (2016). “The Influence of Time Preferences on Retirement Timing.” University of Mannheim Discussion Paper. [Google Scholar]

- Schreiber P and Weber M (2015). “Time Inconsistent Preferences and the Annuitization Decision.” CEPR Discussion Paper No. DP10383. University of Mannheim. [Google Scholar]

- Simon CJ, Warner JT, & Pleeter S (2015). “Discounting, cognition, and financial awareness: New evidence from a change in the military retirement system.” Economic Inquiry. 53(1), 318–334. [Google Scholar]

- Sunde U and Dohmen T (2016). “Aging and Preferences.” The Journal of the Economics of Ageing. 7: 64–68. [Google Scholar]

- Sutter M and Kocher MG 2013. “Impatience and Uncertainty: Experimental Decisions Predict Adolescents’ Field Behavior.” American Economic Review. 103(1): 510–531. [Google Scholar]

- Warner JT, and Pleeter S (2001). “The Personal Discount Rate: Evidence from Military Downsizing Programs.” American Economic Review. 91(1): 33–53. [Google Scholar]