Abstract

Becker’s theory of home production suggests substitutability between consumption spending and home production. Using panel data with detailed information on spending and time use, we analyze house-holds’ ability to replace consumption spending by home produced counterparts. Keeping wages fixed and changing lifetime resources by the shock to housing wealth during the Great Recession we estimate an elasticity of substitution that is consistent with a Life-Cycle Becker model. However, we estimate that only about 11% of total spending is replaceable by home production, which, in contrast to prior literature, makes it unlikely that home production fully mitigates the consequences of wealth shocks to well-being.

Keywords: Home production, Consumption, Wealth shocks, Great Recession, D12, D13, J22, J26

1. Introduction

In his seminal work, Becker (1965) argues that consumption is ‘produced’ by two inputs: market expenditures (e.g. consumption spending) and time (e.g. home production). The relative price of time determines the share of consumption spending and home production in the chosen consumption bundle. Hence, consumption expenditures are only a proxy for actual consumption as ‘time’ can be used to increase consumption, and therefore well-being, beyond spending (Aguiar and Hurst, 2005). Theoretically, consumption spending can be substituted by time without changing well-being. Moreover, the theory of home production suggests that people will substitute away from consumption spending as the opportunity cost of time drops, both intertemporarily and intratemporarily (Aguiar et al., 2012). Shifting away from consumption spending to home production allows people to smooth consumption in response to shocks in income (Hicks, 2015), and by extension, in response to shocks to economic resources more generally, including wealth shocks.

Empirical evidence largely corroborates the smoothing function of home production to different transitory income shocks. Firstly, the drop in consumption spending at retirement that was long considered to be inconsistent with the predictions of the Life-Cycle Hypothesis, known as the Retirement- Consumption Puzzle1 may partially be explained by the increases in time spent in home production at retirement.2 Secondly, it is found that home production fluctuates over the business cycle3 as people spend more time in home production when unemployed.4 Home production mitigates the consequences to well-being of income losses due to unemployment in a manner similar to a formal unemployment insurance mechanism (Guler and Taskin, 2013). Thirdly, but less clear, is the effect of health shocks on home production decisions.5

These three shocks decrease available income and the relative price of time simultaneously. Hence, it remains unclear to what extent increases in home production are due to replacing consumption spending by home production or because of substitution between consumption and non-work time. In this paper, we directly examine the extent to which consumption spending is replaced by home production. The ability of households to replace consumption spending by home production is important as it indicates the extent to which households can keep their consumption bundle constant by adjusting the factors of consumption expenditures and time when facing a shock to economic resources. Following previous literature we focus on the elasticity of substitution, but, in addition, we point out that the share of spending that can be replaced by home production is an important determinant of the ability to smooth consumption: if a household spends little on goods that could be home produced, its main response to an income loss will be to reduce consumption spending. In this paper we pay attention to both the elasticity of substitution and to budget shares that are substitutable.

Aguiar and Hurst (2005) have estimated the extent to which retirees can replace food outside of the home by preparing meals at home. They conclude that retirees are able to smooth consumption by substituting expenditures and time. Compared to Aguiar and Hurst (2005), we make three contributions. Firstly, we take a broader definition of replaceable consumption spending by adding housekeeping, gardening, home repair, and vehicle maintenance services to dining out and relate these consumption components to home produced counterparts in order to estimate an elasticity of substitution. We show that taking a definition beyond food consumption and production is important for the estimated elasticity of substitution. Secondly, we use panel data to estimate the extent of smoothing from within-person variation over time which is more consistent with the life-cycle framework. Thirdly, we estimate the substitutability between spending and home production by keeping the opportunity cost of time (e.g. wages) fixed while changing lifetime resources (e.g. wealth).6 Aguiar and Hurst (2005) identify the substitution between spending and home production from an anticipated fluctuation in income (e.g. retirement). However, the opportunity cost of time is likely to change with the change in employment possibilities at retirement (Ghez and Becker, 1975).

Keeping the opportunity cost of time fixed (e.g. retirees) and using a negative shock to lifetime resources from housing wealth drops in the Great Recession (Christelis et al., 2015; Angrisani et al., 2015), we estimate an elasticity of substitution between home production and substitutable consumption. With this elasticity, it is possible to infer retirees’ ability to replace consumption spending by home production when facing a shock to economic resources. Using a unique panel data set with detailed information on both consumption spending and time use from the Health and Retirement Study (HRS) and the Consumption and Activities Mails Survey (CAMS), we estimate an elasticity of −0.65. The estimated elasticity is statistically not different from an elasticity of −1.0, which is consistent with the theoretical Becker model in a life-cycle framework. This result is robust to different specifications. We provide some evidence that households that are credit constrained reduce consumption more in response to a wealth shock than unconstrained households, consistent with Mian and Sufi (2011), but their elasticity of substitution is not disproportionally larger. At the mean, our elasticity implies an opportunity cost of time of $5.20.

Although the estimated elasticity of substitution suggests that well-being can be smoothed by substituting home production for consumption spending, as suggested by Becker, we find limited scope for substitution. According to our classification scheme, only about 11% of total consumption spending is spent on goods and services that are potentially substitutable by home production. Therefore, it is unlikely that households can consume the same consumption bundle by reallocating time to home production when facing an income shock of substantial magnitude. This limited ability has important implications for the role of home production in welfare analyses. If just 11% of total consumption spending can potentially be replaced, the importance of home production in smoothing well-being is likely to be overstated in analyses that focus on the elasticity of substitution only.

The remainder of the paper is organized as follows. Section 2 describes the HRS/CAMS data. Descriptive statistics of time use and consumption spending are presented in Section 3. To analyze home production formally, Section 4 presents the theoretical framework and the empirical model that is rooted in the theoretical framework. Estimation results are shown in Section 5. Conclusions regarding the substitutability of home production and market consumption can be found in Section 6.

2. Data

The data for our empirical analyses come from the Health and Retirement Study (HRS), a longitudinal survey that is representative of the U.S. population over the age of 50 and their spouses. The HRS conducts core interviews of about 20,000 persons every two years. In addition the HRS conducts supplementary studies to cover specific topics beyond those covered in the core surveys. The time-use and spending data we use in this paper were collected as part of such a supplementary study, the Consumption and Activities Mail Survey (CAMS).

Health and Retirement Study Core interviews

The first wave of the HRS was fielded in 1992. It interviewed people born between 1931 and 1941 and their spouses, irrespective of age. The HRS re-interviews respondents every other year. Additional cohorts have been added so that beginning with the 1998-wave the HRS is representative of the entire population over the age of 50. The HRS collects detailed information on the health, labor force participation, economic circumstances, and social well-being of respondents. The survey dedicates considerable time to elicit income and wealth information, providing a complete inventory of the financial situation of households. In this study we use demographic and asset and income data from the HRS core waves spanning the years 2002 through 2010.

Consumption and Activities Mail Survey

The CAMS survey aims to obtain detailed measures of time use and total annual household spending on a subset of HRS respondents. These measures are merged to the data collected on the same households in the HRS core interviews. The CAMS surveys are conducted in the HRS off-years, that is, in odd- numbered years. Questionnaires are sent out in late September or early October. Most questionnaires are returned in October and November. CAMS thus obtains a snap-shot of time use observed in the fall of the CAMS survey year.

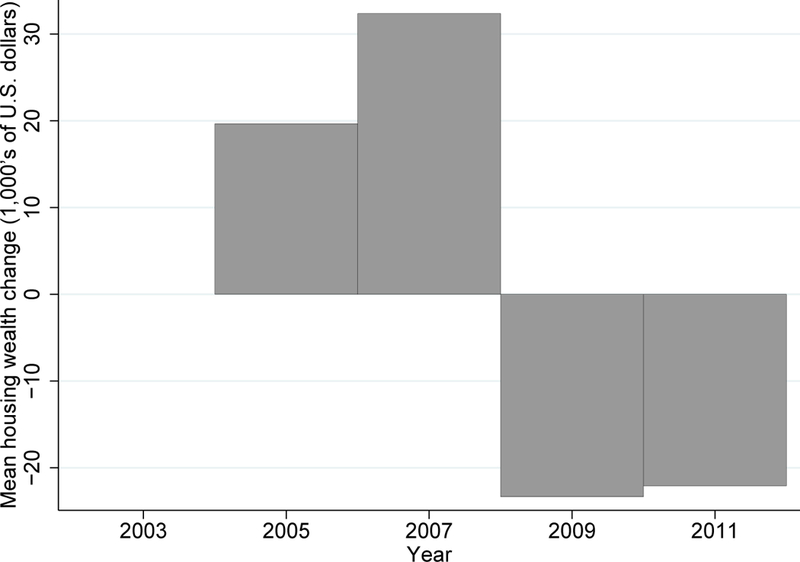

Since the timing of the fielding of the HRS (even years) and CAMS (odd years) surveys are different, the variables in CAMS are merged to the preceding HRS wave, e.g. CAMS 2005 to HRS 2004, etc. As a consequence, there is a temporal misalignment between measured wealth in HRS and actual wealth at the time spending was undertaken and measured in CAMS. However, this temporal misalignment is likely to have minor consequences for our analysis as house prices were near their peak during both HRS 2006 and CAMS 2007 (Figure 1 in Angrisani et al. (2015)) and fell substantially in HRS 2008 and CAMS 2009. We define the recessionary period as the period from CAMS 2007 to CAMS 2009 which assigns the recessionary interval to the demographic and wealth changes observed between HRS 2006 and HRS 2008.

Figure 1:

Wave-to-wave changes in housing wealth

Source: RAND HRS. Based on the variable HwAHOUS (the value of primary residence). Shown differences are computed by taking the average of individual-level differences in HwAHOUS in consecutive waves. Housing wealth is deflated using the Consumer Price Index of the Bureau of Labor Statistics. Due to the temporal misalignment between HRS and CAMS surveys, housing wealth corresponds to the (even) year preceding the odd-numbered year in CAMS.

Starting in the third (2005) wave of CAMS, both respondents in a couple household were asked to complete the time use section, so that the number of respondent-level observations on time use in each wave was larger for the waves from 2005 and onwards compared to the first two 2001 and 2003 waves. We use the time use and spending reported by the main respondent which leaves us with one observation per household per wave. Households were chosen at random from the entire pool of households who participated in the prior HRS core interview.

In this study we use CAMS data from 2005, 2007, 2009 and 2011. The CAMS data can be linked to the rich background information that respondents provide in the HRS core interviews. Rates of item nonresponse are very low (mostly single-digit), and CAMS spending totals aggregate closely to those in the CEX (Hurd and Rohwedder, 2009). The time use data aggregate closely to categories of time use in the American Time Use Study (Hurd and Rohwedder, 2007).

Respondents were asked about a total of 31 time use categories in wave 1; wave 2 added two more categories; wave 4 added 4 additional categories. Thus, since CAMS 2007 the questionnaire elicits 37 time use categories. Using wave 3 to 6 in this paper, we have 33 time use categories available longitudinally. For most activities respondents are asked how many hours they spent on this activity ”last week.” For less frequent categories they were asked how many hours they spent on these activities ”last month.” Hurd and Rohwedder (2008) provide a detailed overview of the time use section of CAMS, its design features and structure, and descriptive statistics. A detailed comparison of time use as recorded in CAMS with that recorded in the American Time Use Survey (ATUS) shows summary statistics that are fairly close across the two surveys, despite a number of differences in design and methodology (Hurd and Rohwedder, 2007).

Only some of the time use categories can be used in home production as a substitute for market purchased goods. For example, time spent cooking can substitute for spending on dining out whereas time spent taking a nap has no substitution possibilities. From 2005 the CAMS data is designed to facilitate studies of home production and possible substitution with market purchased goods. The time use section asks about time spent on various home production activities and there is a direct mapping of these to elicited categories of spending that potentially lend themselves to substitution with home production. We follow this design in the categorization of home production activities and substitutable spending. For details, see Table A.10 in the Online Appendix. Time in home production is the sum of the following time use categories:

House cleaning

Washing, ironing or mending clothes

Yard work or gardening

Shopping or running errands

Preparing meals and cleaning up afterwards

Taking care of finances or investments, such as banking, paying bills, balancing the checkbook, doing taxes, etc.

Doing home improvements, including painting, redecorating, or making home repairs

Working on, maintaining, or cleaning car(s) and vehicle(s)

Respondents were asked about a total of 39 spending categories in the CAMS waves. For nondurable goods and services, the respondent is asked how much was spent in each category and is sometimes given the option, depending on the survey wave and category, of reporting the amount spent weekly, monthly, or yearly. For frequent spending categories, such as gasoline and food, respondents are given the option of reporting all three periodicities, while less frequent spending categories such as mortgage and utilities are only given monthly or yearly options. For durable goods, the respondent is asked to indicate whether the household purchased the item in the ”past 12 months,” and, to the best of their ability, provide the purchase price.

Whereas prior research has focused on total (non-durable) consumption or very particular spending components such as dining out, we are interested in all spending categories that can potentially be replaced by spending time in home production and the CAMS data allow mapping the aforementioned time use categories to spending categories. By the same token we can quantify the fraction out of total spending that is substitutable, and note that in an industrialized setting like the U.S., many spending categories cannot be home produced, such as utilities, mortgage/rent, insurances, subscriptions, trips/vacation/hobbies, etc. Table A.11 in the Online Appendix gives an overview of the consumption spending definitions in CAMS and the classification into substitutable consumption. We define the sum of these spending categories as “substitutable consumption” since the good or service has both market and home versions. The redesign of the time use categories elicited in CAMS between 2003 and 2005, implemented by Hurd and Rohwedder, facilitates the direct mapping between time use and spending categories.7 The following shows the mapping between the market purchases on the left and time used in home production on the right.

Housekeeping services ⇔ House cleaning, washing, ironing or mending clothes

Washing/drying machine (durable) ⇔ Washing, ironing or mending clothes

Gardening services ⇔ Yard work or gardening

Dining out ⇔ Preparing meals and cleaning up afterwards

Dishwasher (durable) ⇔ Preparing meals and cleaning up afterwards

Homerepair services ⇔ Doing home improvements, including painting, redecorating, or making home repairs

Vehicle maintenance services ⇔ Working on, maintaining, or cleaning car(s) and vehicle(s)

Thanks to the richness of the CAMS data we can take a broader view on substitutable consumption spending than one that focuses only on a single market good such as dining out, yet we do not assume that all (non-durable) consumption can be replaced which would be inappropriate in an economy that has moved far beyond subsistence.

The mapping between aforementioned categories may mean that we miss some relevant categories of home production or of substitutable spending despite having a data set particularly designed for such mapping. Given the HRS is a general-purpose survey, there were limits on the level of detail and hence survey time that could be spent on eliciting time use and spending. Therefore, it is likely that our estimated share of substitutable consumption spending is a lower bound because not all substitutable consumption fits in the 39 spending categories. For example, financial management is a category of time use recorded in CAMS but the hiring of a financial advisor is not explicitly a category of consumption spending. However, according to the categorization of consumption spending in Table A.11 in the Online Appendix a great deal of spending cannot be substituted by time use, so the actual share is probably not much greater than our estimate.

To the best of our knowledge there is only a handful of papers that uses panel data with detailed information on both consumption spending and time use. The data in Colella and Van Soest (2013) is such an example but is restricted to the Netherlands for the period 2009–2012. Some home production papers only have information regarding time use (Burda and Hamermesh, 2010; Aguiar et al., 2013). Data with information on both consumption and time use are often imperfect because of a cross-sectional setting (Aguiar and Hurst, 2005; Ahn et al., 2004) or because of a focus on a very specific expenditure such as food (Aguiar and Hurst, 2005; Velarde and Herrmann, 2014; Griffith et al., 2016; Hicks, 2015).

3. Descriptive statistics

3.1. . Summary statistics

In Table 1 we present summary statistics for our sample of persons aged 51–80, who own a house, who have not moved since the previous period, and who have been retired since the previous period. For details on the selection of the sample we refer to Table A.9 in the Online Appendix. Section 4 discusses the importance of these restrictions to our sample. In the sample of retirees aged 51–80, 79.8% own a house. Gross housing wealth, defined as self-reported house value, makes up 64.3% of gross total wealth (including IRA’s and Keoghs) on average. Hence, analyzing retired homeowners and their housing wealth is important both in terms of the number of individuals and in terms of their most important asset.

Table 1:

Summary statisticsa

| Mean | SD | Min. | Max. | P50 | |

|---|---|---|---|---|---|

| Consumption spending (USD/y) | |||||

| Dining out | 1,566 | 2,141 | 0 | 32,546 | 908 |

| Housekeeping services | 314 | 930 | 0 | 18,873 | 0 |

| Gardening services | 373 | 960 | 0 | 16,273 | 0 |

| Home repair services | 1,085 | 2,557 | 0 | 40,000 | 160 |

| Vehicle maintenance | 546 | 715 | 0 | 8,298 | 325 |

| Dishwasher | 20 | 105 | 0 | 1,048 | 0 |

| Washing machine/Dryer | 67 | 266 | 0 | 2,831 | 0 |

| Substitutable | 3,970 | 4,357 | 0 | 50,105 | 2,674 |

| Total | 36,287 | 22,884 | 2,090 | 251,884 | 31,112 |

| Time use (h/w) | |||||

| House cleaning | 4.7 | 5.6 | 0.0 | 56.0 | 3.0 |

| Laundry | 2.5 | 3.0 | 0.0 | 40.0 | 2.0 |

| Gardening | 2.8 | 5.2 | 0.0 | 70.0 | 1.0 |

| Shopping | 3.8 | 3.7 | 0.0 | 45.0 | 3.0 |

| Cooking | 6.8 | 6.3 | 0.0 | 45.0 | 5.0 |

| Financial management | 0.9 | 1.3 | 0.0 | 20.9 | 0.5 |

| Home maintenance | 0.7 | 1.8 | 0.0 | 27.9 | 0.0 |

| Vehicle maintenance | 0.4 | 1.1 | 0.0 | 27.9 | 0.0 |

| Home production | 22.6 | 16.2 | 0.0 | 171.6 | 19.2 |

| Financial characteristics (USD) | |||||

| Housing wealth (/1000) | 211 | 209 | 0 | 3,134 | 156 |

| Mortgage (/1000) | 22 | 60 | 0 | 1,149 | 0 |

| Financial wealthb/1000) | 246 | 616 | 0 | 16,027 | 68 |

| Debtc | 2,540 | 11,294 | 0 | 261,189 | 0 |

| Stock wealth (/1000) | 86 | 438 | 0 | 13,389 | 0 |

| P(Bequest > 10k) | 75.4 | 34.5 | 0.0 | 100.0 | 95.0 |

| Demographic characteristicsd | |||||

| Age | 70.9 | 5.8 | 53.0 | 80.0 | 71.0 |

| Poor healthe | 0.08 | 0.26 | 0.00 | 1.00 | 0.00 |

| Partner retired | 0.37 | 0.48 | 0.00 | 1.00 | 0.00 |

| Partner poor health | 0.04 | 0.18 | 0.00 | 1.00 | 0.00 |

| Couple | 0.60 | 0.49 | 0.00 | 1.00 | 1.00 |

| Wave 2007 | 0.34 | 0.47 | 0.00 | 1.00 | 0.00 |

| Wave 2009 | 0.33 | 0.47 | 0.00 | 1.00 | 0.00 |

| Wave 2011 | 0.33 | 0.47 | 0.00 | 1.00 | 0.00 |

Summary statistics are presented for our sample of 2,500 observations. Monetary measures are expressed in 2011 US dollars using the Consumer Price Index of the Bureau of Labor Statistics.

Defined by the sum of checking accounts, stocks, bonds, IRA’s and Keoghs, and CD’s; excludes pension wealth.

Other than mortgage.

Demographic characteristics are presented in levels here. The changes in health and household situation, as used in the regression analysis, are presented in Table A.12.

The dummy of poor health is constructed by using the response ‘poor’ to the self-reported health question in HRS (RwSHLT).

According to our classification (in dollars per year), only about 11% of total consumption spending can potentially replaced by home production. This makes the substitutable consumption spending a small but non-negligible part of total consumption spending. This share of total spending that is potentially replaceable has important consequences for the importance of home production in smoothing well-being. Even if the elasticity for the replaceable categories is −1.0 it is unlikely that households fully smooth well-being by replacing spending by home production if most of the spending components cannot be replaced. Therefore, this simple descriptive statistic is essential in understanding the importance of home production in welfare analyses.

Regarding people’s time use (in hours per week),8 we observe that people engage in home production for about 23 hours per week on average (Table A.10). About 30% of home production is devoted to preparing meals and about 21% to cleaning the house on average. However, there is substantial variation around the means of time use categories suggesting that many people either spend a lot more or a lot less time on home production activities than the average.

Table 1 shows summary statistics of our analytic sample. In line with earlier literature, we note a high skewness in wealth. For the households observed in our sample, housing wealth is more evenly distributed than financial wealth (defined by the sum of checking accounts, stocks, bonds, IRA’s and Keoghs, and CD’s; excludes pension wealth). Because our sample consists of retirees, most people have already repaid their mortgage. Therefore, gross housing wealth equals net housing wealth for most persons. To see the changes in housing wealth across the waves we refer to Figure 1 in Section 4.2. Figure A.2 in the Online Appendix shows that the evolution of house prices as measured in the HRS closely follows that of the House Price Index.

We use responses to the question about the subjective probability of leaving a bequest greater than 10,000 dollars (P(Bequest > 10k)) as a measure of bequest intentions.9

3.2. Consumption spending over time

Table 2 shows household spending over different waves. Spending declined over time at about three, seven, and two percent per wave respectively, reflecting the aging of the sample in panel and a corresponding small reduction in average household size, but it dropped more during the Great Recession by about seven percent from 2007 to 2009. However, comparing wave 2007 to wave 2009 shows that total substitutable consumption decreased by about 16%. This larger drop in substitutable consumption implies that households’ spending on substitutable consumption has a stronger cyclical reaction than total spending. Apparently households found it easier to shift away from consumption spending that is well substitutable by home production. We continue to find this heightened response in substitutable consumption when we alter the definition of substitutable consumption to exclude durables (e.g. dishwasher) or include supplies/materials (e.g. materials used by service-providers) as shown in the budget shares.

Table 2:

Household level consumption spending (US dollars per year)a

| Wave 2005 (N=742) | Wave 2007 (N=838) | |||||||

|---|---|---|---|---|---|---|---|---|

| Mean | S.D. | % Total | % Resp. | Mean | S.D. | % Total | % Resp. | |

| Dining out | 1,795 | 2,996 | 4.5 | 89.2 | 1,761 | 2,932 | 4.5 | 86.8 |

| Housekeeping services | 432 | 1,407 | 1.1 | 49.9 | 390 | 1,230 | 1.0 | 47.5 |

| Gardening services | 486 | 1,621 | 1.2 | 41.9 | 429 | 1,235 | 1.1 | 40.2 |

| Home repair services | 1,403 | 3,587 | 3.5 | 59.5 | 1,412 | 3,780 | 3.6 | 58.4 |

| Vehicle maintenance | 632 | 803 | 1.6 | 88.3 | 558 | 736 | 1.4 | 84.5 |

| Dishwasher | 21 | 107 | 0.0 | 4.5 | 24 | 113 | 0.0 | 4.8 |

| Washing machine/Dryer | 71 | 267 | 0.0 | 9.5 | 82 | 294 | 0.0 | 10.3 |

| Substitutable consumption | 4,841 | 5,784 | 12.1 | 98.4 | 4,656 | 6,097 | 12.0 | 97.1 |

| Substitutable consumption (excl. durables) | 4,749 | 5,758 | 11.8 | 98.3 | 4,549 | 6,069 | 11.7 | 96.8 |

| Substitutable consumption (incl. mat.) | 6,540 | 7,162 | 16.3 | 99.9 | 6,266 | 7,436 | 16.1 | 99.4 |

| Total consumption | 40,120 | 28,141 | 100.0 | 100.0 | 38,856 | 26,459 | 100.0 | 100.0 |

| Wave 2009 (N=825) | Wave 2011 (N=837) | |||||||

| Mean | S.D. | % Total | % Resp. | Mean | S.D. | % Total | % Resp. | |

| Dining out | 1,472 | 1,959 | 4.1 | 86.8 | 1,683 | 2,349 | 4.8 | 84.7 |

| Housekeeping services | 291 | 927 | 0.8 | 43.6 | 296 | 857 | 0.8 | 41.6 |

| Gardening services | 348 | 803 | 1.0 | 42.7 | 363 | 830 | 1.0 | 43.2 |

| Home repair services | 1,176 | 2,720 | 3.3 | 54.5 | 1,059 | 3,083 | 3.0 | 53.6 |

| Vehicle maintenance | 556 | 724 | 1.5 | 82.9 | 545 | 726 | 1.5 | 83.3 |

| Dishwasher | 18 | 103 | 0.0 | 3.5 | 18 | 99 | 0.0 | 3.8 |

| Washing machine/Dryer | 69 | 278 | 0.0 | 9.1 | 45 | 204 | 0.0 | 8.0 |

| Substitutable consumption | 3,930 | 4,402 | 10.9 | 97.4 | 4,009 | 4,768 | 11.3 | 97.2 |

| Substitutable consumption (excl. durables) | 3,843 | 4,350 | 10.6 | 97.2 | 3,946 | 4,750 | 11.2 | 97.1 |

| Substitutable consumption (incl. mat.) | 5,320 | 5,274 | 14.7 | 99.2 | 5,402 | 5,940 | 15.3 | 99.5 |

| Total consumption | 36,122 | 23,155 | 100.0 | 100.0 | 35,348 | 21,247 | 100.0 | 100.0 |

Monetary measures are expressed in 2011 US dollars using the Consumer Price Index of the Bureau of Labor Statistics. ”% Total” is the percentage of total spending. ”% Resp.” is the percentage of respondents reporting any spending on [x].

Similar to the average presented in Table 1, substitutable consumption is about 11% of total consumption spending across the waves. Dining out constitutes the biggest component of substitutable consumption spending. This expenditure could be well substituted for by home production in the form of home cooking.10 Standard deviations of the spending categories are relatively large compared to the mean. The relative size of the standard deviation compared to the mean is much smaller for the total of consumption spending. This suggests that there is especially large (cross-sectional) heterogeneity in consumption spending that could be substituted for by home production activities. We observe that virtually all households have expenditures that could be replaced by home production.

3.3. Time use over time

Table 3 shows the time spent in home production activities by wave. These activities can be used as a substitute for the market bought goods and services shown in Table 2. The aggregate of home production activities shows that a non-negligible part of the weekly available time is spent on home production (almost 24 hours per week) and that virtually all persons engage in some form of home production (about 99% of respondents).11

Table 3:

Time use in home production activities (hours per week)a

| Wave 2005 (N=742) | Wave 2007 (N=838) | |||||||

|---|---|---|---|---|---|---|---|---|

| Mean | S.D. | % Total | % Resp. | Mean | S.D. | % Total | % Resp. | |

| House cleaning | 4.5 | 5.5 | 19.5 | 82.1 | 5.2 | 6.8 | 21.8 | 83.6 |

| Laundry | 2.7 | 3.3 | 11.7 | 75.0 | 2.6 | 3.3 | 10.9 | 72.2 |

| Gardening | 2.7 | 4.6 | 11.7 | 56.0 | 3.0 | 5.3 | 12.6 | 58.4 |

| Shopping | 4.1 | 4.3 | 19.0 | 90.5 | 3.9 | 4.0 | 16.3 | 87.8 |

| Cooking | 7.0 | 6.3 | 30.3 | 86.6 | 7.0 | 7.0 | 29.3 | 87.0 |

| Financial management | 0.9 | 1.3 | 3.9 | 85.4 | 1.0 | 1.7 | 4.2 | 83.2 |

| Home maintenance | 1.0 | 3.0 | 4.3 | 47.2 | 0.9 | 2.3 | 3.8 | 45.2 |

| Vehicle maintenance | 0.3 | 0.6 | 1.3 | 50.0 | 0.4 | 0.9 | 1.7 | 49.5 |

| Home production | 23.1 | 16.5 | 100.0 | 99.0 | 23.9 | 19.0 | 100.0 | 98.6 |

| Wave 2009 (N=825) | Wave 2011 (N=837) | |||||||

| Mean | S.D. | % Total | % Resp. | Mean | S.D. | % Total | % Resp. | |

| House cleaning | 5.0 | 6.0 | 21.4 | 83.2 | 4.8 | 5.9 | 20.6 | 81.4 |

| Laundry | 2.8 | 4.1 | 12.0 | 74.9 | 2.6 | 3.4 | 11.2 | 72.0 |

| Gardening | 2.9 | 5.8 | 12.4 | 56.6 | 3.0 | 6.3 | 12.9 | 55.7 |

| Shopping | 4.0 | 4.0 | 17.1 | 89.4 | 4.0 | 3.9 | 17.2 | 88.7 |

| Cooking | 6.8 | 6.0 | 29.1 | 88.2 | 7.1 | 6.8 | 30.5 | 87.5 |

| Financial management | 0.8 | 1.2 | 3.4 | 83.2 | 0.9 | 1.4 | 3.9 | 83.5 |

| Home maintenance | 0.7 | 2.3 | 3.0 | 42.3 | 0.7 | 1.8 | 3.0 | 39.7 |

| Vehicle maintenance | 0.4 | 1.1 | 1.7 | 47.3 | 0.4 | 1.2 | 1.7 | 46.6 |

| Home production | 23.4 | 17.2 | 100.0 | 98.4 | 23.3 | 18.7 | 100.0 | 98.5 |

”% Total” is the percentage of total spending. ”% Resp.” is the percentage of respondents reporting any spending on [x].

Most of the home production is devoted to meal preparation. Together with house cleaning, this accounts for about half of total time spent in home production. More than 80% of the sample spends some time on these two home production activities. About 90% of the people engage in shopping activities although the average time spent in this activity is somewhat smaller than the time spent in house cleaning and cooking. Unlike activities such as house cleaning, cooking and doing the laundry, it is harder to buy the service of shopping on the market which may explain the relatively high percentage of persons engaging in this activity. Approximately half of the people engage in gardening and maintenance of the home and vehicles but the amount of time spent in these activities is fairly small. More than 80% of the sample spend time on managing their finances, but the amount of time spent in this activity is only about an hour per week.

While a non-negligible part of the weekly available time is devoted to home production activities on average, there is a lot of (cross-sectional) variation around this average as the standard deviations of most activities are about the same size as the averages (or larger). However, the variation across waves is small despite the observed drop in substitutable consumption spending in Table 2.

Together, Table 3 and Table 2 give some cross-sectional evidence on the substitution between consumption spending and home production activities. To capture the possible substitution effects more formally, we present a theoretical framework including a simple life-cycle model augmented with home production and wealth shocks in the next section. The purpose of this theoretical framework is not to estimate a structural model, but to justify our empirical identification method presented in Section 4.2.

4. Model

4.1. Theoretical predictions

We embed our empirical model in a theoretical framework that builds on Becker (1965). We extend the seminal work of Becker in two simple ways. First, by augmenting the original Becker model with additional information on substitutable and non-substitutable consumption spending categories we identify an important measure of interest in addition to the elasticity of substitution to empirically test the full smoothing of home production. For details of the model we refer to Appendix A. The original Becker model assumes that all spending can be replaced by home production. Conditional on the assumption of constant returns to scale in the home production function, Becker predicts an elasticity of substitution of −1. Hence, there is full substitution between spending and home production such that households can smooth an income shock to well-being by replacing spending by home production. But if only a share of total consumption is substitutable, we should examine the elasticity of substitution between home production and substitutable consumption spending

| (1) |

with hnt home production, substitutable consumption spending, and w the shadow price of time. We identify the elasticity of substitution by our empirical model. The average share of substitutable consumption, p, can be measured from simple descriptive statistics.

Second, by introducing Becker’s framework in a simple life-cycle model with non-deterministic wealth (e.g. introducing wealth shocks) we can identify a valid and relevant instrumental variable to estimate the elasticity of substitution. For details of the model we refer to Appendix A. Since a wealth shock only affects the hours choice in home production through its effect on the monetary budget constraint (Equation 12), and thus through spending possibilities, it is a valid instrument to estimate the effect of spending on home production. Prior research has shown that consumption spending is responsive to changes in wealth.12 This marginal propensity to consume out of wealth (MPC) is particularly large with shocks in housing wealth (Case et al., 2005,0; Paiella and Pistaferri, 2016). Hence, wealth shocks are likely to be a relevant instrument.

4.2. Empirical model

To estimate the elasticity of substitution between home production and substitutable consumption spending we specify the following econometric model in first-differences:

| (2) |

where X is a vector of control variables including individual- and household characteristics, ε is the error term, and

| (3) |

Since might be endogenous to hint, we estimate an IV-GMM model that exploits the shock in housing wealth during the Great Recession as an instrumental variable. We use the change in the (log of the) value of the primary residence13 during the Great Recession (DGRΔln(Wit)), which following the literature, we assume to be unexpected, as an instrumental variable. We exclude from our sample persons who change houses, so that we measure price movements and not movements to bigger or smaller homes. See Figure 1 for the average change in housing wealth over the waves. According to the theoretical framework, the validity of the instrument comes from the fact that wealth shocks only enter the budget for consumption spending and do not affect the time budget of retirees. The first-stage therefore estimates the effect of the wealth shock on consumption possibilities

| (4) |

where βc2 measures the marginal propensity to consume (MPC) out of the wealth shock. Angrisani et al. (2015) and Christelis et al. (2015) show that this unexpected and sufficiently large and persistent shock decreased consumption spending. The average wave-to-wave change in reported housing wealth that is used in the first-stage is presented in Figure 1.

We condition the elasticity on a set of observable personal and household characteristics Xit. This vector includes age, health, period, marital status as well as information regarding the health and retirement statuses of a spouse if any.14 Due to our first-difference specification we condition on shocks in health15 and changes in marital status.16 We combine quadratic age-effects with semi-parametric age effects in the age of 62, 65 and 70.17 These ages correspond to the Social Security earliest claiming age, the full- benefit claiming age,18 and the latest benefit claiming age.

5. Estimation results

5.1. Baseline estimates

5.1.1. Second stage results

Estimation results are presented in Table 4. Our preferred specification (column 3) indicates that the elasticity of substitution between home production and substitutable consumption spending is −0.65 and significant at the 10% level.19 An elasticity of −0.65 means that a 10% decrease in consumption spending that is replaceable by home production increases home production by 6.5%. Becker’s theoretical model in a life-cycle context suggests an elasticity of βn2 = −1 for full substitution between consumption spending and home production (Equation 12). A t-test indicates that we cannot reject an elasticity of substitution of −1. Under this elasticity, home production fully substitutes replaceable consumption spending.

Table 4:

Estimation resultsa

| (1) Full sample |

(2) Full sample |

(3) Full sample |

(4) Fuller-k |

(5) Age 65–81 |

(6) Non-poorb health |

(7) Couples |

(8) Women |

|

|---|---|---|---|---|---|---|---|---|

| Second-stage: Δln(hint) | ||||||||

| −0.50* | −0.62* | −0.65 * | −0.56 * | −0.57* | −0.60* | −0.76 | −0.43 | |

| (0.29) | (0.36) | (0.37) | (0.30) | (0.31) | (0.34) | (0.49) | (0.31) | |

| First-stage: | ||||||||

| 0.15*** | 0.14** | 0.14** | 0.14** | 0 17*** | 0 17*** | 0.15** | 0.16** | |

| (0.05) | (0.06) | (0.06) | (0.06) | (0.06) | (0.06) | (0.06) | (0.07) | |

| H0: βn2 = −1 | [0.09] | [0.29] | [0.35] | [0.13] | [0.16] | [0.24] | [0.62] | [0.06] |

| Observations (N × T) | 2,500 | 2,500 | 2,500 | 2,500 | 2,152 | 2,309 | 1,511 | 1,583 |

| F-statistic | 7.88 | 6.28 | 5.90 | 5.90 | 8.91 | 6.55 | 7.22 | 5.75 |

| Demographic controls | No | No | Yes | Yes | Yes | Yes | Yes | Yes |

| Period dummies | No | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Notes: Heteroskedasticity and autocorrelation robust SE’s in parentheses,

denotes significant at the 10% level,

5%,

1%.

βn2 = −1 tests whether the elasticity is significantly different from minus one. P-values in square brackets. 2011 US dollars. See the Online Appendix for full regression results.

Time use and spending are inverse hyperbolic sine transformed. Top and bottom 1% of the sample in each survey wave are trimmed.

People in non-poor health is based on the self-reported health question in HRS (RwSHLT).

Although prior literature on the MPC out of wealth (particularly (Christelis et al., 2015) and (An-grisani et al., 2015)) supports the relevance of our instrumental variable, the F-statistic’s rule-of-thumb suggests that the instrument might not be strong. Therefore, we test our estimation results with a Fuller-k estimator which is more robust to possibly weak instruments (Yogo, 2004). Estimation results of the elasticity are robust to using the Fuller-k estimator as the results indicate an elasticity of −0.56 that is statistically not different from −1.

Table 4 (columns 5 through 8) compares the estimated elasticity for different demographic groups based on respondents’ gender, marital status, health, education, and age. Hurd and Rohwedder (2013) find that spending changes at retirement differ depending on demographic characteristics. In part this heterogeneity may be explained by the willingness to increase home production, but also by the ability or necessity to respond to spending changes by home production (Hurd and Rohwedder, 2006). For example, healthy individuals are likely to have relatively more healthy non-work time available which makes it easier to increase home production; couples have more possibilities to coordinate time use decisions within the household (Hayashi et al., 1996). Therefore, a priori we expect that the findings of Hurd and Rohwedder (2013) translate into heterogeneity in the elasticity of substitution.

We estimated variations of our preferred specification in Table 4, column (3), adding an interaction of the coefficient on the change in consumption spending with a demographic of interest, such as health (good vs. bad health, results not shown). In none of those estimations was there a statistically significant difference between the subgroups. The same conclusion holds when estimating separate regressions for each subgroup. However, it should be noted that the point estimates of the elasticity of substitution for the respective smaller subgroup (poor health, singles, males) are relatively imprecise due to large standard errors. The estimates for the larger demographic subgroups are somewhat more precisely estimated and show plausible patterns (Table 4, columns 5 8), even though no firm conclusions can be drawn from these due to lack of statistical significance. With that in mind we note that, according to the point estimates for the larger subgroups, the elasticity appears to be slightly larger for those whose health is at least good or better, and larger yet for couples, maybe because they have the opportunity to coordinate and share their home production activities with their spouse. The point estimate of the elasticity for women is smaller than that for the entire population, possibly due to them already engaging in more home production in the absence of any shock so that the scope for further increases in home production is somewhat more limited for them.

The second determinant of substitution is the share of potentially replaceable consumption spending, but we find little variation in the share across identifiable groups. A simple OLS regression of the share of substitutable consumption spending (pit) on characteristics shows that only women have a statistically significant 1%-point smaller share of total consumption that is spent on substitutable spending than men (Table A.3). However, this effect is small in absolute terms, e.g. 11% versus 12%. We find no such statistically significant differences between age groups, couples/singles, and poor/non-poor health. Therefore, we conclude that p is non-negligible but small for much of the population, so that even with a large elasticity of substitution it is unlikely that home production could fully replace consumption spending drops to maintain well-being.20

5.1.2. First stage results

Turning to the first stage estimates, we find that the estimated coefficient of the instrument implies that a 10% decrease in housing wealth during the Great Recession decreased home production substitutable consumption spending by 1.4%.21 To test for non-linear effects of the wealth drop in the MPC, we present consumption spending responses to housing wealth for different quartiles of changes in housing wealth during the Great Recession in Table A.8. The estimation results suggest that the MPC of homeowners with more substantial drops in housing wealth is about the same as the average MPC; the interaction effects are not statistically significant. Moreover, allowing for non-linear responses in the MPC does not alter the main conclusions regarding the elasticity of substitution.

The MPC out of wealth we find is somewhat larger than reported by Christelis et al. (2015) (0.56%). However, their elasticity is based on cross-sectional recall data since the peak of the market using the 2009 Internet Survey of the HRS. Angrisani et al. (2015) estimate a non-recession and recession-specific elasticity. The non-recession elasticity is not significant, the recession-specific elasticity is larger than our elasticity (about 4%). By replicating their approach in which we allow for a non-recession (2005–2007) and recession (2007–2009) MPC we come to similar conclusions. We do not find a significant effect of the non-recession period while the MPC in the recession period is 1.4% (not reported here).22 The elasticity found by Campbell and Cocco (2007) is most in line with our estimated elasticity between consumption spending and housing wealth (1.2%).

The estimated elasticity is identified by the significant effect of the instrument DGRΔln(Wit) on consumption spending. We performed several robustness checks. To verify that a housing wealth shock led to the decline in consumption spending, we added to our basic specification financial wealth or stock wealth among homeowners. To guard against other determinants of spending change that might be correlated with house price change we estimated the effect of shocks to financial wealth among renters. As detailed in Table A.4, we found no significant effects on consumption spending in these specifications, supporting the view that much of the responses in consumption can be explained by housing wealth shocks as suggested by prior literature (Case et al., 2005,0; Paiella and Pistaferri, 2016).23

5.1.3. Shadow price of time

We can use our estimates to find the average shadow price of time among the sample of persons used in the regression analysis. Average consumption spending on home production substitutable goods and services is 3,970 dollars per year. The average number of hours spent in home production is 22.6 hours per week. The elasticity implies that, on average, a drop in consumption spending of 40 dollars (per year) on home production substitutable market goods and services increases home production activities by about 9 minutes per week or about 7.6 hours per year. The combination of these facts imply a shadow price of about $5.20 per hour.

For comparison, this shadow price is somewhat smaller than minimum wages in the US, but a shadow price below the minimum wage is plausible for the sample of retirees as the reservation wage drops in retirement (Ghez and Becker, 1975). The estimated shadow price is somewhat higher than the replacement cost approach (about 4 dollars) that is generally used to express home production in monetary terms (Frick et al., 2012). An estimated shadow wage that is much higher than these assumed monetary values of home production would suggest that the assumed monetary value of an hour of home production is smaller than the drop in consumption spending and, hence, it is unlikely that households can replace the monetary value of consumption spending by home production. Our estimate of 5.20 dollars implies that increasing home production by one hour allows households to replace consumption spending worth 5.20 dollars. Since 5.20 dollars is in the range of the replacement cost (about 4 dollars) and minimum wage approaches (about 7.25 dollars) it is likely that households are able to replace substitutable consumption spending by home produced counterparts in monetary terms on average.

The variation in consumption spending and in time use by education levels leads to variation in the shadow price of human capital. As shown in Table A.7 in the Online Appendix, the average varies from 2.9 dollars among those lacking a high school degree to 9.4 dollars among those with a college degree.

5.1.4. Alternative measures of substitutable consumption

In Table 5 we take our preferred specification (3) and re-estimate but using varying definitions of substitutable consumption spending. The results indicate that the main conclusions do not change whether durables and supplies/materials are included or excluded (see lines (2), (3), and (4)). Nor do they change when services regarding the home and garden are excluded (see (5), (6)). This is important because causal identification is based on house price drops that may especially drive housing-related spending. Excluding housekeeping services (see (7)) results in little variation in the estimates.

Table 5:

Elasticities with different definitions of consumption spending

| Definition | First-stage | Second-stage | |||||

|---|---|---|---|---|---|---|---|

| Coeff. | S.E. | Coeff. | S.E. | βn2 = −1 | Obs. | ||

| Dependent variable: Home production (h/w) | |||||||

| (1) | 0.14** | (0.06) | −0.65* | (0.37) | [0.35] | 2,500 | |

| (2) | (1) − durables | 0.12** | (0.06) | −0.71* | (0.44) | [0.51] | 2,500 |

| (3) | (1) + suppl./material | 0.14** | (0.06) | −0.61** | (0.31) | [0.21] | 2,504 |

| (4) | (1) + suppl./material, clothing | 0.13** | (0.06) | −0.67** | (0.35) | [0.35] | 2,507 |

| (5) | (1) − home repair services | 0.12** | (0.06) | −0.74* | (0.45) | [0.56] | 2,491 |

| (6) | (1) − home repair/gardening services | 0.12** | (0.06) | −0.74* | (0.45) | [0.56] | 2,490 |

| (7) | (1) − housekeeping services | 0.14** | (0.06) | −0.62* | (0.38) | [0.31] | 2,501 |

| (8) | (1) − dining out | 0.09 | (0.07) | −0.98 | (0.83) | [0.98] | 2,493 |

| (9) | dining out only | 0.30*** | (0.11) | −0.29* | (0.17) | [0.00] | 2,489 |

| Dependent variable: Cooking (h/w) | |||||||

| (10) | dining out only | 0.30*** | (0.11) | −0.06 | (0.12) | [0.00] | 2,495 |

Notes: Heteroskedasticity and autocorrelation robust SE’s in parentheses,

denotes significant at the 10% level,

5%,

1%. βn2 = ‒1 tests whether the elasticity is significantly different from minus one. P-values in square brackets. 2011 US dollars.

Rows (8) and (9) show the importance of dining out in driving the results. Excluding dining out from substitutable consumption (row (8)) shows a large elasticity but with a large standard error because of a reduced reaction in spending to housing wealth in the first stage. Row (9) uses the disaggregated spending category of dining out and shows a small elasticity of substitution despite a substantial reaction in spending to housing wealth.

Following Aguiar and Hurst (2005) we present the substitutability between cooking and dining out in row (10). Although dining out expenses are relatively responsive to the wealth shock, the results indicate that retirees do not substitute cooking and dining out when facing a wealth shock. Rather they are likely to increase home production activities other than cooking as a response to decreased dining out expenses. This implies that households choose a different consumption bundle given the reoptimization of their utility function. Therefore, we conclude that households primarily respond to a decrease in housing wealth through dining out expenditures and increasing home production in non-food categories.24 This result indicates the importance of expanding consumption definitions beyond food production and spending, like Aguiar and Hurst (2005). The elasticity of substitution based on food consumption and production is much smaller (−0.06) than the elasticity based on broader definitions of consumption spending and home production (−0.65), despite the fact that households primarily respond to a housing wealth shock by cutting dining out expenditures.

5.2. Robustness to local labor market effects

Our identification from the Great Recession depends on unexpected (large) changes in house value, but it raises two concerns. Firstly, the drop in house prices might change the propensity to repair the house as this spending category is found to be positively related to transitory shocks (Gyourko and Tracy, 2006). We verify a large drop in spending on home repair services in Table 2. However, columns (5) and (6) in Table 5 show that excluding such services from our analysis does not alter the main conclusions.

Secondly, there might be an effect of the Great Recession on local market prices through local labor markets. Using scanner data, Kaplan et al. (2016) and Stroebel and Vavra (forthcoming) suggest that prices of goods and services dropped substantially in regions that experienced large house price drops during the Great Recession. First, it should be noted that those conclusions are based on retail prices of tradable goods in grocery and drugs stores and does not include prices of potentially replaceable spending categories analyzed in our paper. Second, such price changes do not change the estimated elasticity of substitution if the relative price change of market consumption goods and home production is constant which is in line with the replacement-cost approach of valuing home production (Frazis and Stewart, 2011).25 Unfortunately, our expenditure data do not differentiate between quantity and prices much like the analysis of Mian et al. (2013). Therefore, we might overestimate the actual consumption responses to the shock in housing wealth.

To illustrate: if we assume that the relative prices of market goods decreased by 15–20% on average, as suggested by Stroebel and Vavra (forthcoming), the actual elasticity would be −0.76 rather than our estimate of −0.65 (calculated as −0.65*(1/0.85)), leaving our main conclusions on the substitutability of spending and home production intact.

To address the issue of the relationship between local labor markets and price changes, in additional analyses, we control for local labor market effects (see Table 6), such as the regional unemployment rate and regional House Price Index of nine census divisions (URd and HPId respectively).26 To examine whether our results depend on regions most severely affected we excluded the top 25% changes in regional unemployment rates and and the regional House Price Index (column (3) and (6) in Table 6 respectively). We find an elasticity of substitution of similar magnitude to our main estimates.

Table 6:

Estimation results correcting for local labor market effects

| (1) Full sample |

(2) Full sample |

(3) No largea changes UR |

(4) Full sample |

(5) Full sample |

(6) No largeb changes HPI |

(7) Full sample |

|

|---|---|---|---|---|---|---|---|

| Second-stage: Δln(hint) | |||||||

| −0.68 * | −0.68* | −0.72* | −0.67 * | −0.68* | −0.75* | −0.68* | |

| (0.39) | (0.39) | (0.43) | (0.38) | (0.39) | (0.46) | (0.39) | |

| ΔURdc | 0.02 (0.04) |

−0.04 (0.05) |

|||||

| Δ(URd − UR) | 0.05 (0.05) |

||||||

| ΔHPId(/100)d | −0.33** (0.16) |

−0.41** (0.21) |

|||||

| Δ(HPId − HPI)(/100) | −0.32* (0.17) |

||||||

| First-stage: | |||||||

| DGRΔln(Wit) | 0.13** | 0.13** | 0.13** | 0.14** | 0.13** | 0.13** | 0.13** |

| (0.06) | (0.06) | (0.06) | (0.06) | (0.06) | (0.06) | (0.06) | |

| H0: βn2 = −1 | [0.41] | [0.42] | [0.52] | [0.39] | [0.40] | [0.59] | [0.40] |

| Observations (N × T) | 2,491 | 2,491 | 1,832 | 2,491 | 2,491 | 1,890 | 2,491 |

| F-statistic | 5.32 | 5.33 | 4.76 | 5.39 | 5.36 | 4.41 | 5.36 |

Notes: Heteroskedasticity and autocorrelation robust SE’s in parentheses,

10% level,

5%,

1%. βn2 = − 1 tests perfect elasticity. P-values in square brackets. 2011 US dollars.

Deleting the top 25% observations with respect to division-specific changes in unemployment rates and HPI respectively.

URd and HPId are the regional unemployment rate and House Price Index in census division d respectively.

5.3. Heterogeneous elasticities

We first examine heterogeneity in the response of spending to the housing wealth shock. Prior analyses have primarily explained the mechanism for consumption out of housing wealth by credit-constraints and bequest motives.27 In particular, credit-constrained households and households with a high bequest motive are more responsive to changes in wealth. This leads to heterogeneity in the MPC (Jappelli and Pistaferri, 2014). We include in the first stage interactions between shocks to housing wealth and (1) housing wealth itself; (2) mortgage amount; (3) net housing wealth; (4) financial wealth; (5) debt; and (6) the subjective probability of a bequest of more than 10,000 (Table 7). The results suggest households responded more strongly to the shock in housing wealth when housing net worth was higher prior to the shock.28 In line with Mian et al. (2013), these are most likely the households that faced a larger reduction in credit limits during the Great Recession.29 We find no significantly different MPC’s for households with high or low financial wealth and debt, although it should be noted that the inclusion of information regarding bequests makes estimates more imprecise. These results are robust to the inclusion of the subjective probability of leaving a bequest of at least 100,000 dollars instead of 10,000 (not reported here).

Table 7:

Heterogeneity in the elasticity of substitution

| Interactions with | Interactions with | Interactions with | ||||

|---|---|---|---|---|---|---|

| Housing wealth | Financial wealth | Bequest probability | ||||

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Second-stage: Δln(hint) | ||||||

| −0.67 * | −0.92 | −0.58 * | −0.24 | −0.80 | −0.58 | |

| (0.40) | (0.60) | (0.34) | (0.26) | (0.66) | (0.44) | |

| 0.11 (0.19) |

0.20 (0.25) |

|||||

| 0.00 (0.00) |

0.00 (0.00) |

|||||

| −0.10 (0.92) |

0.43 (0.56) |

|||||

| First-stage: | ||||||

| DGRΔln(Wit ) | 0.12** | 0.10 | 0.10 * | 0.10 | 0.12 | 0.10 |

| (0.06) | (0.09) | (0.05) | (0.09) | (0.09) | (0.09) | |

| DGRΔln(Wit) · (W − Mort)it−1(/1000) | 0.07 * | 0.09** | 0.09** | 0.09** | ||

| (0.04) | (0.04) | (0.04) | (0.04) | |||

| DGRΔln(Wit) · Finit−1(/1000) | 0.01 | 0.22 | 0.01 | 0.01 | ||

| (0.17) | (0.20) | (0.17) | (0.17) | |||

| DGRΔln(Wit) · Debtit−1(/1000) | 0.00 | 0.00 | 0.00 | 0.00 | ||

| (0.00) | (0.00) | (0.00) | (0.00) | |||

| DGRΔln(Wit) · P(Beq > 10k)it−1(/100) | −0.05 | −0.05 | −0.05 | −0.05 | ||

| (0.12) | (0.12) | (0.11) | (0.12) | |||

| H0: βn2 = − 1 | [0.41] | [0.89] | [0.21] | [0.00] | [0.76] | [0.34] |

| Observations (N × T) | 2,500 | 2,414 | 2,500 | 2,414 | 2,414 | 2,414 |

| F-statistic | 4.35 | 1.88 | 5.79 | 1.88 | 5.79 | 1.88 |

Notes: Standard errors reported in parentheses are robust to heteroskedasticity and autocorrelation,

denotes significant at the 10% level,

at the 5% level and

at the 1% level. P-values reported in square brackets. 2011 US dollars. All regressions include demographic controls and period dummies

Using these interaction terms as additional instruments for identification of the IV-GMM model, we estimate the extent to which MPC heterogeneity leads to heterogeneity in the elasticity of substitution between consumption and home production. Estimation results can be observed in Table 7. Estimated coefficients for the heterogeneity in the elasticity are not significantly different from zero. Hence, we conclude that housing equity, financial equity, and the bequest motive are not important for the elasticity of substitution between consumption spending and home production. Since more leveraged households respond more strongly in consumption spending, they also substitute more consumption and home production but not disproportionally more than less leveraged households.

6. Conclusion

The theory of home production suggests that people substitute away from consumption spending to home production when facing a negative economic shock (Becker, 1965). Shifting away from consumption spending to home production allows people to smooth consumption in response to decreases in economics resources. This is relevant as home production might be used to mitigate the consequences of shocks to well-being. Prior empirical studies confirm increases in home production when facing retirement, unemployment, and disability. However, in these studies it remains unclear to what extent increases in home production are due to replacing consumption spending because of an increase in non-work time, or due to substitution between consumption and non-work time. This paper sheds new light on the importance of home production in welfare analyses by focusing on the elasticity of substitution estimated over the retired population, thus holding constant non-work time, but also on the share of spending that is potentially substitutable.

Aguiar and Hurst (2005) have estimated the extent to which food-outside-of-the-home is replaced by preparing meals at home at retirement. They conclude that retirees are able to smooth consumption by substituting time for expenditures. In the current paper we make three contributions compared to Aguiar and Hurst (2005). Firstly, we take a broader definition of replaceable consumption spending by adding housekeeping, gardening, home repair, and vehicle maintenance services to dining out and relate these spending components to home produced counterparts in order to estimate an elasticity of substitution. We show that taking broader definitions of consumption spending and home production is important for the conclusions regarding the elasticity of substitution. Secondly, we use panel data to estimate the extent of smoothing from within-person variation over time which is more consistent with a life-cycle framework. Thirdly, we estimate the substitutability between spending and home production by keeping the opportunity cost of time (e.g. wages) fixed and changing lifetime resources (e.g. wealth).

A negative shock to lifetime resources from the house price declines during the Great Recession is used to estimate the elasticity of substitution between home production and consumption spending of retirees. Using a life-cycle framework augmented with home production and wealth shocks, we assert that the unexpected and substantial drop in house prices is a valid and relevant instrumental variable to estimate the effects of consumption spending on home production, that is, the drop in house prices does not affect the time use decisions of retirees, and the shock to housing wealth decreases consumption spending possibilities in a sizeable way. Exploiting the unique panel data set from combining HRS and CAMS, with detailed information on both consumption spending and time use, we estimate an elasticity of substitution between home production and consumption spending of −0.65. This elasticity is consistent with predictions from the theoretical Becker model in a life-cycle framework. This result is robust to different specifications. We provide some evidence that the substitutability is induced by households with borrowing possibilities through home equity, although the elasticity is not disproportionally larger for these households. At the mean, our elasticity implies an opportunity cost of time of $5.20. For our sample of retirees, it is likely that this implies households are able to replace substitutable consumption spending by home produced counterparts.

Although our overall results are consistent with Becker, according to our classification only about 11% of total consumption spending is spent on goods and services that are potentially substitutable by home production. The other 89% of consumption spending does not have home produced counterparts (e.g. utilities). Here, it should be noted that the budget share of substitutable consumption depends on the time use and spending categories elicited in CAMS. Despite having a data set particularly designed for the mapping between time use and spending we may miss some relevant categories of home production or of substitutable spending. However, our categorization of consumption spending and alternative scenarios thereof support the fact that the majority of spending cannot be substituted by time use.

The small fraction of total spending that is potentially replaceable suggests that it is unlikely that home production can fully mitigate the effects of decreased consumption spending possibilities for well-being despite the rather large elasticity of substitution. It is likely that economic shocks force people to choose a different consumption bundle. Hence, given our results, the smoothing function of home production for well-being is likely to be overstated in analyses that focus on the elasticity of substitution only, or that infer the total elasticity from a sub-category of spending, like dining-out.

Supplementary Material

Acknowledgments

The work was supported by grants from the Social Security Administration through the Michigan Retirement Research Center (Grant #RRC08098401 – 06), the National Institute on Aging (R01AG035010, PI: Rohwedder), and the Leiden University Fund/ van Walsem (Grant #4414=3 – 9 – 13nV;vW). We have benefited from discussions with Rob Alessie, Adam Blandin, David Boisclair, Jochem de Bresser, Joseph Briggs, Agar Brugiavini, Monika Bütler, Christopher Carroll, Maria Casanova, Yoosoon Chang, Zsombor Cseres-Gergely, Ben Etheridge, Roozbeh Hosseini, Erik Hurst, Arie Kapteyn, Dirk Krueger, Italo Lopez-Garcia, Hamish Low, Melanie Lürhmann, Raffaele Miniaci, Raun van Ooijen, Kim Peijnenburg, Luigi Pistaferri, Thomas Post, Mariacristina Rossi, Gianluca Violante, Eliana Viviano, Tammy Schirle, Arthur van Soest, Pascal St-Amour, Anthony Webb, Guglielmo Weber, Jocelyn Wikle, Robert Willis, and Joachim Winter. Furthermore, we would like to thank colleagues and participants at the 21st IPDC, Budapest, the Department of Economics Research Seminar Series, Leiden, the 4th ECB Conference on Household Finance and Consumption, Frankfurt, the Netspar IPW, Leiden, the QSPS Workshop, Logan UT, the IAEE, Milan, Future Well-Being of the Elderly, Montréal, and the Venice Summer Institute 2017, Venice. Finally, we would like to thank the editor, Brigitte Madrian, and two anonymous referees for helpful suggestions that improved the paper. The findings and conclusions expressed are solely those of the authors and do not represent the opinions or policy of the Social Security Administration, any agency of the Federal government, or the Michigan Retirement Research Center.

A Theoretical framework

Here we present the more extensive theoretical framework in which we introduce home production and wealth shocks in a simple life-cycle model building on Becker (1965).30 Formally, we allow for a single-person household and introduce hours spent in home production hnt next to the classical market consumption spending cmt. Since we focus on retirees, we assume a corner solution in which labor supply is absent and where retirement is an absorbing state. Hence, individuals maximize the following utility function with respect to home production (hnt) and consumption spending (cmt):

| (5) |

with

| (6) |

where t is the time period, δ is the discount factor, T the time horizon of the person, and lt leisure time. vt are the personal- and household characteristics that influence utility directly known as taste-shifters (e.g. age, household size, number of children). In Equation 6 we assume that ct is a vector of different consumption goods and services such that ct represents a consumption bundle. Individuals maximize Equation 5 under the time budget (Equation 7) and monetary budget constraint (Equation 8)

| (7) |

| (8) |

| (9) |

where At is the amount of assets at time t, r is a constant real interest rate, H the total time-endowment (e.g. 24 hours per day) and bt non-labor income (e.g. retirement income).

Solving the maximization problem subject to the constraints gives the following first-order conditions for consumption spending and home production:

| (10) |

| (11) |

where , is the marginal utility of wealth, and wt the shadow price of time.31 Earlier analysis of the substitution between home production and spending by Rupert et al. (1995,2000); Gelber and Mitchell (2012); Aguiar and Hurst (2007); Aguiar et al. (2013) assume λt fixed and change the opportunity cost of time. In the current analysis, we change λt by stochastic changes in wealth (ξt) and fix the opportunity cost of time by focussing on the corner solution of retirees only (hmt = 0). This changes the monetary budget constraint to:

| (12) |

where ξt yields a shock32 in the value of wealth available at time t that is unexpected and therefore affects the marginal utility of wealth (λt increases).

Full smoothing of consumption in response to shocks to the marginal utility of wealth implies

| (13) |

which, given constant returns to scale in ct = f(cmt, hnt), would imply

| (14) |

However, the share (1 − p) of consumption categories depends only on market expenditures and is not substitutable by home production whereas a share of p categories is substitutable

| (15) |

Together Equation 14 and 15 suggest that full smoothing, under constant returns to scale of f, would imply

| (16) |

Since depends on p, to analyze the extent to which households are able to smooth consumption when experiencing a shock to the marginal utility of wealth it is important to identify both p and the elasticity of substitution between home production and substitutable consumption spending .

Footnotes

Found by, among others, Mariger (1987); Robb and Burbidge (1989); Banks et al. (1998); Bernheim et al. (2001); Miniaci et al. (2010); Hurst (2003); Ameriks et al. (2007); Haider and Stephens (2007); Battistin et al. (2009); Aguila et al. (2011); Hurd and Rohwedder (2013).

Schwerdt (2005); Aguiar and Hurst (2005); Hurst (2008); Stancanelli and Van Soest (2012); Velarde and Herrmann (2014).

Benhabib et al. (1991); Greenwood and Hercowitz (1991); Rupert et al. (2000); Hall (2009); Karabarbounis (2014).

Ahn et al. (2004); Burda and Hamermesh (2010); Krueger and Mueller (2012); Colella and Van Soest (2013); Aguiar et al. (2013).

For comparison, Rupert et al. (1995, 2000); Gelber and Mitchell (2012); Aguiar and Hurst (2007); Aguiar et al. (2013) fix lifetime resources and identify elasticities between spending and home production by changes in the opportunity cost of time.

An important improvement for the mapping between time use and spending is the splitting of relevant spending categories into supplies/materials and services.

Reporting more than 168 hours per week implies multitasking in the data.

In the HRS, respondents are asked about their expected bequests. More specifically, respondents are asked about the likelihood (0–100%) to leave a bequest. Building on McGarry (1999) we use this information to infer the strength of the bequest motive and its effect on wealth holdings. This is important since the bequest motive is a source of heterogeneity in the marginal propensity to consume out of wealth, as suggested by Jappelli and Pistaferri (2014).

One might argue that home cooking is not a perfect substitute to dining out as dining out might be viewed as a luxury good. Nonetheless, Table 2 shows that about 85% of the sample has dining out expenditures. This 85% is fairly constant across the business cycle, but spending is decreased in the downturn. This suggests that the frequency of dining out has decreased or people have shifted towards cheaper alternatives which supports the idea that home cooking is a substitute for dining out.

Hence, issues regarding left-censoring of the home production variable in regression models are negligible.

See for example Case et al. 2005,0; Carroll et al. 2011; Campbell and Cocco 2007; Angrisani et al. 2015; Christelis et al. 2015; Mian et al. 2013; Kaplan et al. 2016; Paiella and Pistaferri 2016.

Based on the HwAHOUS variable in the RAND HRS files. To see that this variable resembles other indices of house price movements we refer to Figure A.1 and A.2 in the Online Appendix.

Estimation results are highly robust to excluding information regarding the spouse (not reported here).

Estimation results are highly robust to excluding changes in health (not reported here).

Estimation results are highly robust to excluding changes in marital status (not reported here).

Estimation results are highly robust to excluding such semi-parametric age effects (not reported here).

The Full Retirement Age is 65 for all persons born before 1938.

We assume full sharing of the household in consumption spending. Nonetheless, the estimated elasticity is highly robust to a variety of equivalence scales (not reported here) to correct market consumption spending such as the Oxford equivalence scale, OECD equivalence scale, and the Square root scale. All estimates show an elasticity of substitution of about −0.65.

Table A.3 also shows estimation results of the simple OLS for the (unrestricted) sample including non-retirees and renters. These results suggest that p. the share of substitutable spending, is not different for non-retirees, but about 3%-points lower for renters. However, in absolute term differences are small which suggests that our conclusions regarding the smoothing function of home production are likely to hold for the whole population, even if heterogeneity in the elasticity of substitution is large.

We find that households only responded to the drop in housing wealth by adjusting consumption spending that are replaceable by home production (see Table A.6). We find an MPC of zero for total consumption spending and non-substitutable consumption spending. The MPC for substitutable consumption is largely driven by the MPC of dining out.

Differences between estimates from Angrisani et al. (2015) and ours are likely to come from different samples taken as our sample consists of persons aged 51–80, who own a house, who have not moved since the previous period, and who have been retired since the previous period. Our more restricted sample is necessary for the identification of our empirical model.

Table A.5 shows that conclusions do not change when we condition our excluded instrument on a first lag in the absolute value of the house (ln(Wit‒1)), a second-order difference in housing wealth (Δ2ln(Wit)), and different indicators of financial trends such as the U.S. House Price Index (HPIt ), the national unemployment rate (URt ), and the S&P500 index (S&P500t ). This also holds for conditioning on the housing wealth changes right after the Great Recession (D2011Δln(Wit)).

More particularly, by looking at the time spent in dining out we can conclude that this decrease in dining out expenditures is largely due to the downsizing of the quality of dining out and not because of a decrease in time spent dining out.

In the case of retirees this approach might be more consistent with actual behavior than the opportunity-cost approach that assumes that an hour of home production is valued at the individual’s market wage.

With d differentiating between New England (NE), Middle Atlantic (MA), East North Central (ENC), West North Central (WNC), South Atlantic (SA), East South Atlantic (ESA), West South Atlantic (WSA), Mountain (Mount), and Pacific (Pacif). Although the development of the house price index differs substantially between regions (Figure A.3), this is less so for the unemployment rate (Figure A.4).

Campbell and Cocco (2007); Kopczuk and Lupton (2007); Cooper (2013); Mian et al. (2013); Kaplan et al. (2016); Paiella and Pistaferri (2016); Agarwal and Qian (2017).

Table 7 shows different specification indicating that the consumption response to the shock in housing wealth is stronger for a higher net value of the house (W ‒ Mortg). Differences in (net) financial wealth (Fin, Debt) does not induce heterogeneity in responses. A higher probability to leave a bequest of at least 10,000 dollars (P(Beq > 10k)) does not induce heterogeneity either.

In the opposite direction Mian and Sufi (2011) find increases in borrowing in response to increases in home equity.

And extensions by, among others, Gronau (1977,9); Apps and Rees (1997); Rupert et al. (1995, 2000); Apps and Rees (2005).

In the case of retirees this does not represent the wage.

This shock can consist of both permanent (ξt) and transitory (ωt) shocks: ξt = ζt + ωt. We assume that consists of both financial and housing wealth and that housing is a pure investment good and that there is no consumption component to owning a house. Although financial wealth is more liquid, we assume that both are equally important in consumption decisions. For empirical evidence on the importance of housing wealth for consumption decisions, see for example Case et al. 2005,0; Carroll et al. 2011; Campbell and Cocco 2007; Angrisani et al. 2015; Christelis et al. 2015; Mian et al. 2013; Kaplan et al. 2016; Paiella and Pistaferri 2016. Case et al. (2005), Case et al. (2013), and Paiella and Pistaferri (2016) even argue that the sensitivity of consumption to unexpected changes in housing wealth is greater than the sensitivity to unexpected changes in financial wealth. Campbell and Cocco (2007) argue that housing wealth is important for consumption decisions primarily through perceived wealth and borrowing constraints, although bequest motives may also play an important role for older households (Bernheim, 1991; Alessie et al., 1997,9; Skinner and Zeldes, 2002; Kopczuk and Lupton, 2007). There is empirical evidence that both permanent and transitory shocks in housing wealth affect consumption spending (Contreras and Nichols, 2010) as well as anticipated and unanticipated shocks in housing wealth (Paiella and Pistaferri, 2016).

References

- Agarwal Sumit and Qian Wenlan. Access to home equity and consumption: Evidence from a policy experiment. The Review of Economics and Statistics, 99(1):40–52, 2017. [Google Scholar]

- Aguiar Mark and Hurst Erik. Consumption versus expenditure. Journal of Political Economy, 113(5): 919–948,2005. [Google Scholar]

- Aguiar Mark and Hurst Erik. Life-cycle prices and production. American Economic Review, 97(5): 1533–1559, 2007. [Google Scholar]

- Aguiar Mark, Hurst Erik, and Karabarbounis Loukas. Recent developments in the economics of time use. Annual Review of Economics, 4:373–397, 2012. [Google Scholar]

- Aguiar Mark, Hurst Erik, and Karabarbounis Loukas. Time use during the Great Recession. American Economic Review, 103(5):1664–1696, 2013. [Google Scholar]