Abstract

The COVID‐19 pandemic has altered life in innumerable ways in many countries across the globe. In this article I review what the virus did to patterns of US and Brazilian exports of major commodities during the first surge of the virus during April and May 2020, and also speculate on what may happen during the beginning of North American winter in late 2020. The analysis highlights how grains versus meats have been vulnerable to trade disruptions due to the coronavirus pandemic. US exports of beef and pork were particularly impacted by a wave of processing facility shutdowns in the wake of COVID‐19 outbreaks among workers. Poultry exports saw declines from their highs but remain strong, even though poultry‐processing facilities have also faced issues with outbreaks and shutdowns. Trends in 2020 grain and oilseed exports have not been affected by the pandemic.

Keywords: Beef, commodity, corn, COVID‐19, exports, pork, poultry, soybeans, trade

JEL Codes: Q17, Q18

Introduction

The COVID‐19 pandemic has altered life in innumerable ways in many countries across the globe. We are still in the early days of understanding the virus: both what it does to the human body and what it does to economies. It is clear, though, that the virus will continue to have profound impacts on most sectors of our economy, and commodity agriculture is no exception.

The purpose of this article is to review what the virus did to patterns of exports of major US commodities during the first surge of the virus in spring 2020, and also to speculate on what may happen during North American winter in late 2020 and 2021.

As COVID‐19 began to spread outside of China, consumer reactions to lockdowns around the world were to hoard staple foods like pasta and flour. Bare shelves led some to worry about food security and several countries considered, and some implemented, export bans on staple food commodities (Espitia, Rocha, and Ruta 2020 and Glauber et al. 2020). Lockdowns greatly reduce economic activity in general, and global GDP is forecasted to drop by as much as 4% in 2020, with more hopeful estimates in the range of a 1.5%–2% drop in GDP (Haugh, Pain, and Salins 2020; McKibbin and Roshen 2020). How this translates to agricultural commodity trade flows is hard to predict, but early forecasts from Barichello (2020) suggest real trade value of Canadian agricultural products could drop by 12%–20%.

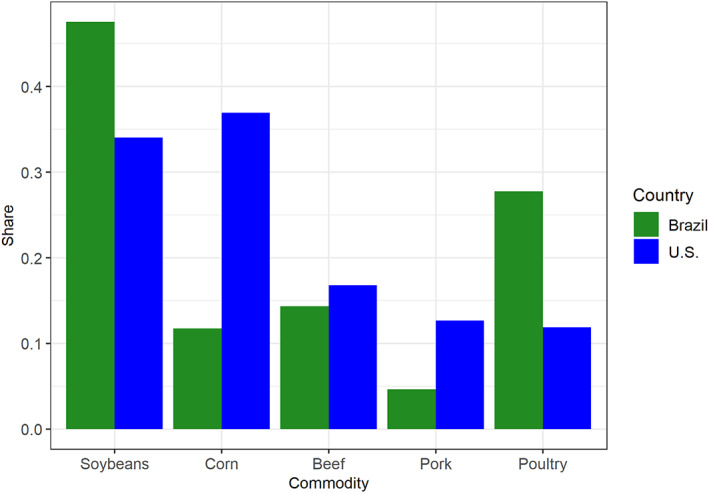

At the time of writing, we are three quarters of the way through 2020 and have learned a lot about the virus's effects on the global economy in the first several months of the pandemic. In this article I provide a detailed comparison of how US exports of soybeans, corn, beef, pork, and poultry in the first eight months of 2020 compared to the previous seven years. Additionally, I do the same for the 2020 Brazilian exports of the same commodities. I chose the US and Brazil as companions to study because both countries are major exporters of the commodities of interest, and the US and Brazil are generally the biggest competitors in the effort to supply China's strong demand for raw agricultural commodities (Gale, Valdes, and Ash 2019; Haley, 2020). Figure 1 shows the US and Brazilian share of the world's exports by 2019 US dollar value. Brazil has nearly 50% of the share of soybean exports and nearly 30% of the world's poultry exports, while the U.S. has nearly 40% of the world's share of corn exports. Both countries have about 15% share of the worlds beef exports, but the US has stronger pork exports with about 13% compared to Brazil's roughly 5%.

Figure 1.

U.S. and Brazil Share of Export Value, 2019 USD. Note: Data from worldstopexports.com. Bars show the US and Brazilian shares of the value of exports of each commodity in 2019 [Color figure can be viewed at wileyonlinelibrary.com]

This analysis highlights how grains versus meats have been vulnerable to trade disruptions due to the coronavirus pandemic. US exports of beef and pork were particularly impacted by a wave of processing facility shutdowns in the wake of COVID‐19 outbreaks among workers. Poultry exports saw declines from their highs but remain strong, even though poultry processing‐facilities have also faced issues with outbreaks and shutdowns (Hart et al. 2020). For pork this is likely due to record demand for exports to China, following a devastating bout with African swine fever that reduced their herd by nearly half (Haley and Gale 2020).

At the same time, 2020 trends in grain and oilseed exports seemingly have not been affected by the pandemic. For now, shutdowns in meat‐processing capacity seem to be driving the differences between the impacts and not concerns about the virus being transmitted through contaminated meat or other issues. Recently, however, Brazilian meatpackers signed declarations, at China's request, that their exports do not contain the novel coronavirus. This hints that contaminated meat, whether real or perceived, could have an impact on meat exports into China in the future (Mano and Figueiredo 2020).

Commodity Exports in the First COVID‐19 Wave

Both the United States and Brazil have endured rapid spread of the virus and are number one and three in terms of total cases in the world at the time of writing. In this section, we will compare how US and Brazil's exports of soybeans, corn, beef, pork, and poultry have fared against this backdrop.

Soybean and Corn Exports

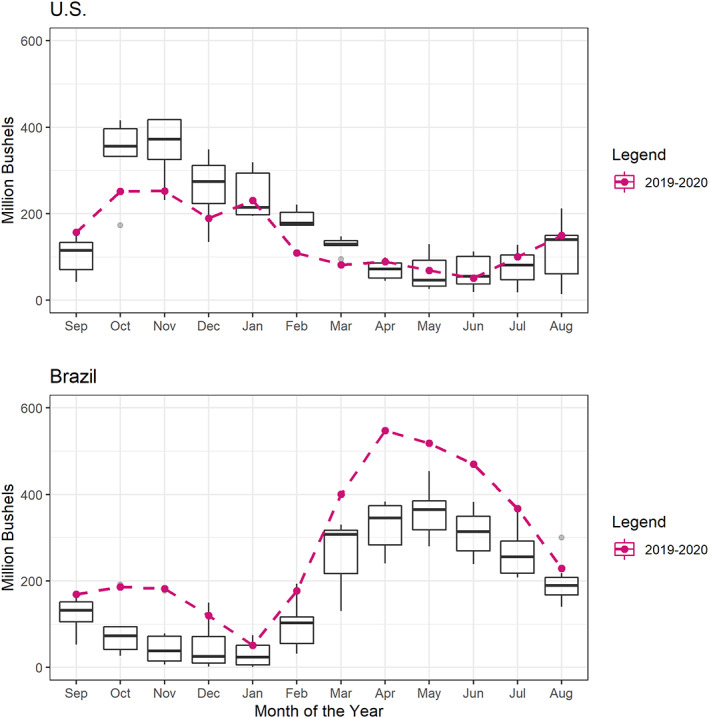

Since soybeans and corn are harvested once per year, and both US soybeans and corn and Brazilian soybeans for the 2019–2020 crop year were harvested before the pandemic hit the two countries, there were no pandemic related disruptions to production. There potentially could have been disruptions to distribution, so we examine exports of soybeans and corn from the US and Brazil in this section. Figures 2 and 3 show the US and Brazil's current marketing year exports of soybeans and corn compared to exports since 2012 (2013–2018 data are used to make the boxplots shown, while exports from September 2019–August 2020 are highlighted in pink). I use data from 2013–2020 because global trade, especially with the rise of Brazil has changed rapidly in the last 10 years. Earlier data would not be relevant for comparison. Also, given the small sample size, I did not want the impacts of the 2012 drought in the US to dominate the picture since it impacted corn, soybeans, and cattle markets significantly.

Figure 2.

US and Brazil Monthly Exports of Soybeans, 2013–2020. Note: Boxplots are drawn illustrating the distribution of exports in a given month across the years 2013–2020. Exports for 2020 to date are highlighted in pink. US export data from USDA AMS Federal Grain Inspection Service, accessed at https://fgisonline.ams.usda.gov/ExportGrainReport/ on 2020‐09‐29. Brazil export data from Comex Stat, http://comexstat.mdic.gov.br/en/home. Data was accessed on 2020‐09‐29 [Color figure can be viewed at wileyonlinelibrary.com]

Figure 3.

US and Brazil Monthly Exports of Corn, 2013–2020. Note: Boxplots are drawn illustrating the distribution of exports in a given month across the years 2013–2020. Exports for 2020 to date are highlighted in pink. US export data from USDA AMS Federal Grain Inspection Service, accessed at https://fgisonline.ams.usda.gov/ExportGrainReport/ on 2020‐09‐29. Brazil export data from Comex Stat, http://comexstat.mdic.gov.br/en/home. Data was accessed on 2020‐09‐29 [Color figure can be viewed at wileyonlinelibrary.com]

Looking at figure 2, it is notable that US soybean exports in February and March 2020 were at the lowest levels of the period considered, despite the Phase One trade agreement signed on January 15, 2020 that included China's promise to increase purchases of US soybeans (prior to the trade war over half of all US soybean exports went to China). At the same time Brazil had a record soybean harvest in 2020 and their exports have been at record levels from February to June 2020 (BBC, 2020; Lawder et al. 2020).

Looking at exports of soybeans in March, April, and May, there is no evident effect of the virus or lockdowns in the US. These are typically months when exports experience seasonal lows in the US anyway. Figure 3 similarly shows no obvious effects on corn exports. In fact, corn exports during April 2020 were near the top of the seasonal range over the period considered.

Beef, Pork, and Poultry Exports

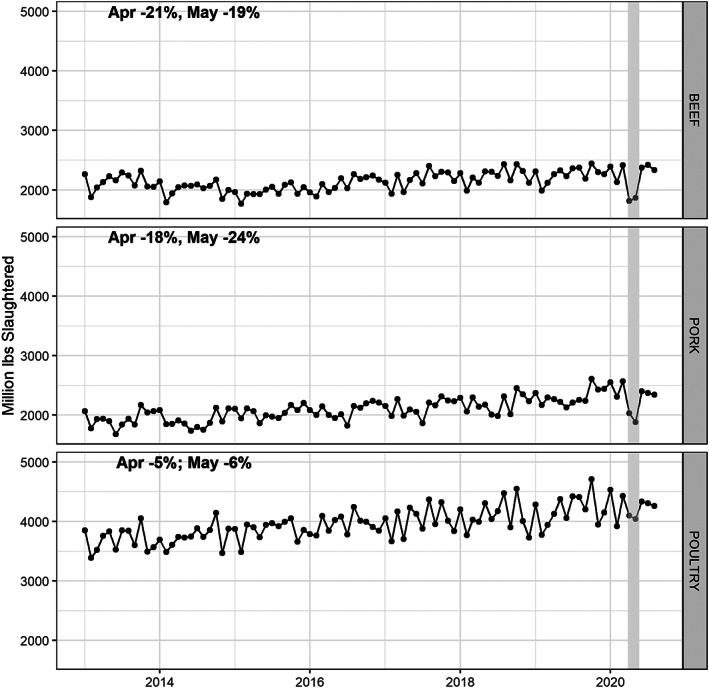

The months of April and May were particularly disruptive to meat production in the US as outbreaks of the virus at meat‐processing facilities idled a significant portion of slaughter capacity, which caused an unprecedented rise in the spread between wholesale meat and livestock prices (Lusk, Tonsor, and Schulz 2020). Figure 4 shows monthly commercial slaughter of beef, pork, and poultry from 2013–August 2020 in the United States. The vertical gray bars highlight April and May 2020, which was the height of the disruption to meat‐processing capacity. Beef processing was most impacted in April, with production declining 21% from the average of January, February, and March 2020 production levels. In May, beef production was still off by 19%. June, July, and August 2020 production levels were near the highs experienced prior to the pandemic shutdowns.

Figure 4.

Monthly Commercial Slaughter of Commercial Beef, Pork, and Poultry, 2013‐Aug 2020. Note: Data from NASS QuickStats https://quickstats.nass.usda.gov/. Highlighted portion is April and May 2020. Annotation shows the percent change in April and May 2020 from the average of January, February, and March 2020 production levels

Pork processing in the US experienced a similar magnitude of reduction in production, but the lows were experienced in May rather than April 2020. Pork production was down 18% in April and 19% in May 2020 compared with the average of January, February, and March 2020 production levels.

Poultry production in the US experienced a more moderate disruption, with April production down 5% and May production down 6% from the average of January, February, and March 2020 production levels. While down modestly from the three‐month prior average, both April and May production were still within the typical range, and actually higher than production in February 2020.

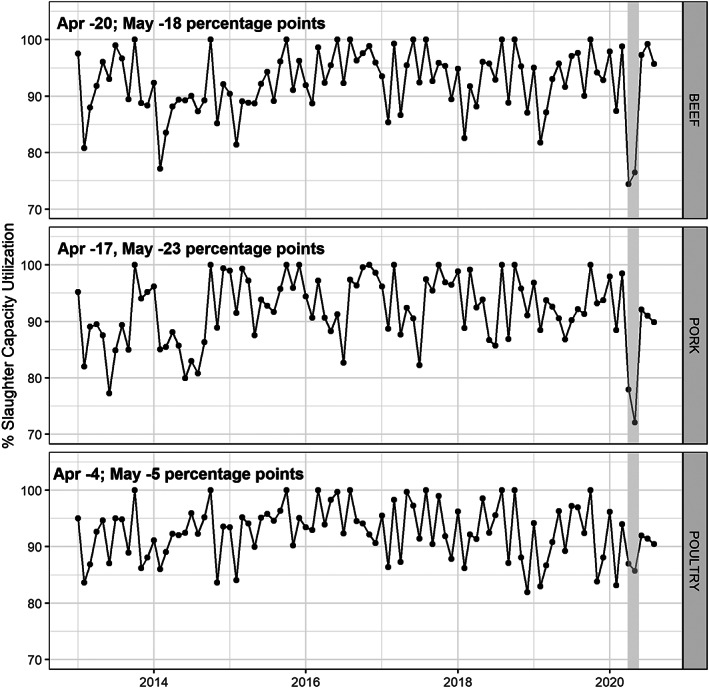

This reduction in production represented significant portions of slaughter capacity for beef and pork in the US (Hahn et al. 2020). This is shown in Figure 5. I estimate slaughter capacity as the maximum value of the monthly production number over the previous 12 months (Tonsor and Schulz 2020). Beef slaughter capacity was down 20% and 18% in April and May 2020, respectively, compared to the average of the first three months of 2020. Pork was down 17% and 23%, and poultry was down only 4% and 5% over the same time period. Figures 4 and 5 show that there was significant disruption to both the production level and capacity utilization of beef and pork in the U.S. during the months of April and May 2020.

Figure 5.

Monthly Commercial Slaughter Capacity Utilization Beef, Pork, and Poultry, 2013‐Aug 2020. Note: Data from NASS QuickStats https://quickstats.nass.usda.gov/. Highlighted portion is April and May 2020. Annotation shows the percentage points change in April and May 2020 capacity utilization from the average of January, February, and March 2020 levels. Maximum capacity is estimated to be the maximum monthly production level over the previous 12 months. Capacity utilization is defined as current month production divided by maximum capacity times one hundred

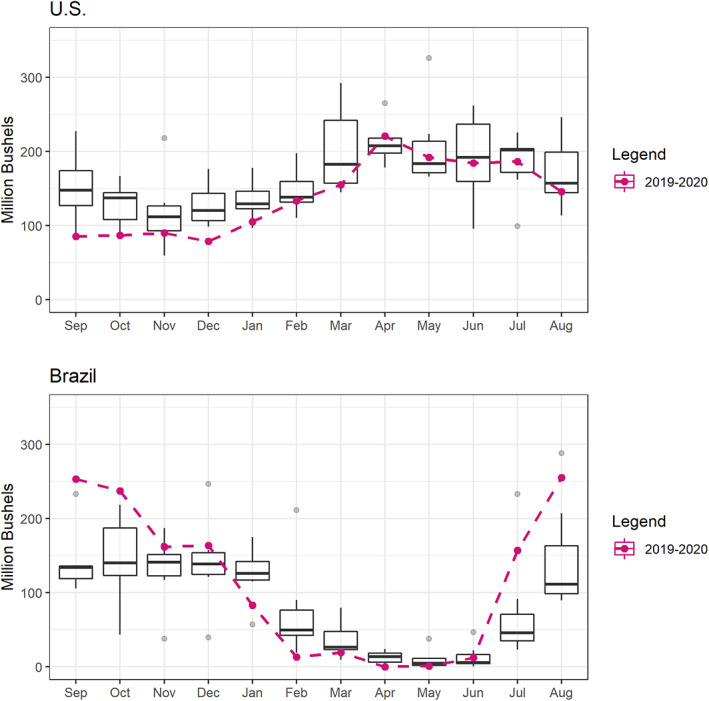

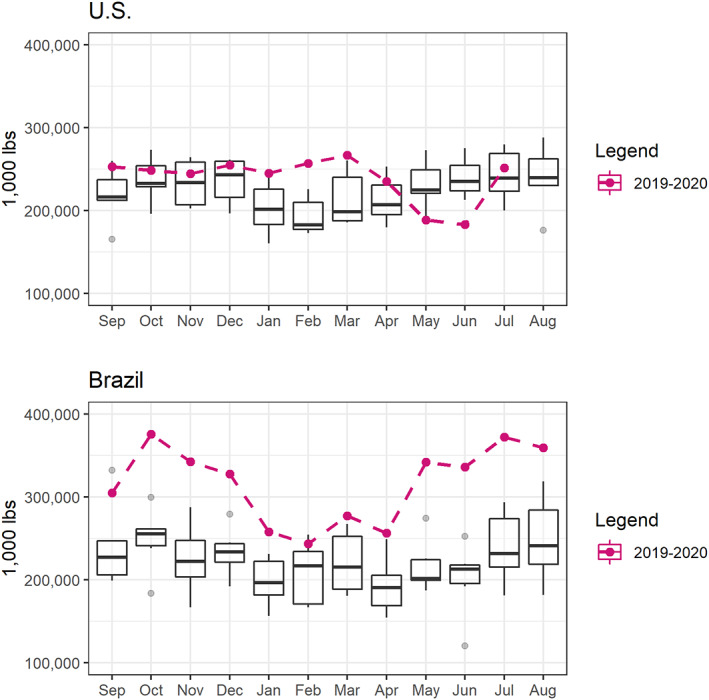

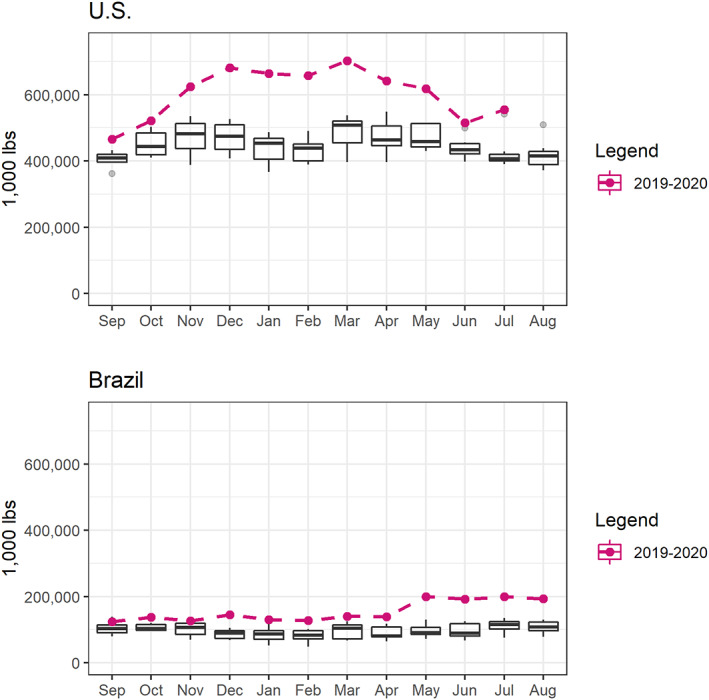

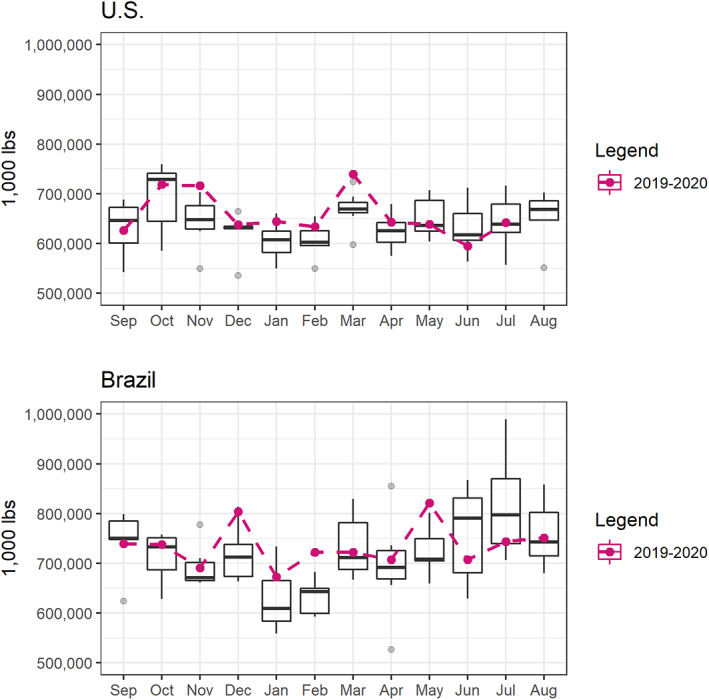

Brazil also struggled with COVID‐19 outbreaks in meat‐processing facilities, but to my knowledge there are no monthly production statistics available, so there is no way to know if the outbreaks were significant enough to idle an important proportion of processing capacity (Mano 2020). We can, however, compare monthly meat exports from the US and Brazil. Figures 6, 7, 8 show exports of beef, pork, and poultry from the US and Brazil. Boxplots summarize the exports for each month over the 2013–2019 period, while exports for September 2019 through August 2020 are shown in pink. In the case of beef and pork (and to a lesser extent also in poultry) the effect of temporary shortages caused by meat‐processing facility shutdowns seems to be evident. January through March saw both the US and Brazil exporting beef at the top of the range for the time period considered. As outbreaks in the US shut down processing facilities in March, April, and May, beef exports plummeted nearly 30%, from 267.1 million lbs. in March to 188.5 million lbs. in May. That is a reduction of about 79 million lbs. of beef from the US During the same time period, Brazil's exports of beef grew by about 65 million lbs. between March and May, a 19% increase. While this analysis cannot deduce causality, the inverse correlation suggests that Brazilian beef was a popular substitute for reduced US beef on the world market.

Figure 6.

US and Brazil Monthly Exports of Beef, 2013–2020. Note: Boxplots are drawn illustrating the distribution of exports in a given month across the years 2013–2020. Exports for 2020 to date are highlighted in pink. US export data from USDA ERS Livestock and Meat Trade Data, accessed at https://www.ers.usda.gov/data‐products/livestock‐and‐meat‐international‐trade‐data/ on 2020‐09‐29.. Brazil export data from Comex Stat, http://comexstat.mdic.gov.br/en/home. Data was accessed on 2020‐09‐29 [Color figure can be viewed at wileyonlinelibrary.com]

Figure 7.

US and Brazil Monthly Exports of Pork, 2013–2020. Note: Boxplots are drawn illustrating the distribution of exports in a given month across the years 2013–2020. Exports for 2020 to date are highlighted in pink. US export data from USDA‐ERS Livestock and Meat Trade Data, accessed at https://www.ers.usda.gov/data‐products/livestock‐and‐meat‐international‐trade‐data/ on 2020‐09‐29. Brazil export data from Comex Stat, http://comexstat.mdic.gov.br/en/home. Data was accessed on 2020‐09‐29 [Color figure can be viewed at wileyonlinelibrary.com]

Figure 8.

US and Brazil Monthly Exports of Poultry, 2013–2020. Note: Boxplots are drawn illustrating the distribution of exports in a given month across the years 2013–2020. Exports for 2020 to date are highlighted in pink. US export data from USDA‐ERS Livestock and Meat Trade Data, accessed at https://www.ers.usda.gov/data‐products/livestock‐and‐meat‐international‐trade‐data/ on 2020‐09‐29. Brazil export data from Comex Stat, http://comexstat.mdic.gov.br/en/home. Data was accessed on 2020‐09‐29 [Color figure can be viewed at wileyonlinelibrary.com]

Pork exports tell a very similar tale, but we can see that exports from both the US and Brazil had been running at record levels. In the case of the US the reduction of pork exports between March and May was 84 million lbs. or about a 14% reduction. Note that even with this March to May reduction, the May 2020 pork export number was the highest in our sample. Brazil increased pork exports between March and May by 60.5 million lbs. or 30%.

Poultry exports from the US between March and May fell by 100 million lbs., or about 16%. US exports of poultry had also been trending near the top of the range January through March, before experiencing a significant drop in April and May. Yet the April and May 2020 export numbers were still well within the typical range for this sample. It is not as compelling to assert that the March to May declines were caused by the COVID‐19 shutdowns as in the case of beef and pork: the percentage changes from March to May are not as large as in beef and pork, May exports did not drop from April levels, and the response in Brazilian exports was not as pronounced (12% increase). Notably, Brazil's May increase in poultry exports was given back as June levels are in line with the historical range.

This analysis does not prove that reduced production during April and May 2020 was the cause of reduced US exports and increased Brazilian exports for beef and pork in April, May, and June 2020, but it suggests that production disruptions played a substantial part. In the next section, we try to extrapolate what might play out for meat exports especially during the upcoming winter in North America various scenarios of COVID‐19 spread.

Medium Term Export Prospects

It seems export prospects for grains and oilseeds have largely been unaffected, but that the effects of beef‐ and pork‐processing facility shutdowns were significant. As viral spread continues, keeping outbreaks out of meat‐processing facilities will be key to minimizing production disruptions and export shipments flowing for both the US and Brazil.

Both the US and Brazil have continued to see large numbers of new COVID‐19 cases throughout the summer and fall of 2020, yet there have not been meat‐processing facility outbreaks on the scale of what happened in April and May of 2020. For the US this is shown in figure 4 by the fact that June, July, and August meat production rebounded to near pre‐April 2020 levels. Hopefully this means that the facilities in both countries have learned how to make the environment safer for workers to protect themselves from exposure, which would insulate the industry and protect workers if the virus continues to spread in the broader population for some time.

The length and duration of the COVID‐19‐induced recession is another medium term risk factor for commodity exports, especially meats. The IMF projects −4.9% in global gross domestic product (GDP) for 2020 (IMF 2020). Global demand for meats would be particularly harmed by extended recessionary pressures, compared to corn and soybeans. Prior experience from the Great Recession showed that quantities of meats consumed during the Great Recession generally held steady compared to prerecession levels, but likely because of low prices (Darko and Eales 2013).

Are Grains and Oilseed Exports Immune to the Dangers of COVID‐19?

The biggest wildcard is the possibility for grain and oilseed exports to see disruptions. To date, grain and oilseed markets have not been impacted by the virus since no elements of the supply chain are labor intensive or require many workers in close quarters. Therefore, we have not seen any major disruptions to exports on grains or oilseeds due to COVID‐19.

There is potential for policy instability caused by COVID‐19 to impact grain and oilseed exports, however. Countries implemented or threatened to implement export bans on staple crops like wheat and soybeans in the early days of the pandemic.

Also, if outbreaks of the virus are unchecked, it would be possible to imagine some countries implementing import bans on commodities from countries where the virus is surging. Even if it is not possible for the virus to be transmitted from the actual physical commodity, the crew of the cargo ships could be perceived as threat. Given China's recent request that Brazilian meatpackers sign a declaration that their shipments are virus‐free, this type of import ban seems to be on the table. This type of ban could affect all commodities, not just meat products.

Conclusions

In this article I have given an overview of what happened with exports of soybeans, corn, beef, pork, and poultry in the US and Brazil in the early months of the COVID‐19 pandemic outside of China. Grain, oilseed, and poultry export shipments have been relatively unaffected, but beef and pork export shipments experienced significant reductions with Brazil filling the shortfall in both cases. Then, I shared some thoughts on COVID‐19 containment scenarios and what they could mean for export prospects of these commodities in the next year to year‐and‐a‐half. The best case scenario for all aspects of the economy, including commodity exports, is the swift and lasting containment of COVID‐19.

This analysis comes with plenty of limitations. COVID‐19 is a disruption to daily life not seen in the US since the influenza pandemic of 1918/1919. Nuanced predictions of what will happen to specific markets is not practical, sample sizes being too small and a lack of previous cases to inform forecasts and confidence intervals limit our ability to analyze the situation with typical statistical tools.

However, we have been in the midst of this pandemic long enough to learn some things. We are far enough into the pandemic to know that it and its necessary remedies do tremendous harm to the economy. Meat supply chains are especially vulnerable, and disruptions to processing capacity harms farmers, processors, consumers, and our trading partners. Robust free trade will help countries all over the world deal with temporary shortages caused by flareups of the virus wherever they occur in their food systems.

As time goes on we will learn a lot from our experience fighting this virus. Future work should explore how to make meat processing more resilient; specifically, work on what precautions are effective to protect workers' health and keep the system up and running will help the industry face future challenges.

Mindy L. Mallory is an associate professor and Clearing Corporation Chair of Food and Agricultural Marketing at the Department of Agricultural Economics at Purdue University.

Editor in charge: Craig Gundersen

References

- Barichello, Richard . 2020. The COVID‐19 Pandemic: Anticipating its Effects on Canada's Agricultural Trade. Canadian Journal of Agricultural Economics 68(2): 219–224. 10.1111/CJAG.12244. [DOI] [Google Scholar]

- BBC . 2020. A Quick Guide to the U.S.‐China Trade War. BBC News, January 16, 2020 https://www.bbc.com/news/business-45899310 (accessed October 14, 2020).

- Darko, Francis , and James S. Eales. 2013. Meat Demand in the US during and after the Great Recession. Paper presented at the Annual Meeting of the Agricultural and Applied Economics Association, Washington, D.C.

- Hahn, William , Knight Russell, Davis Christopher G., Cessna Jerry, Haley Mildred, Ha Kim, and Grossen Grace. 2020. Livestock, Dairy, and Poultry Outlook: June 2020. Washington DC: U.S. Department of Agriculture, LDP‐M‐312.

- Gale, Fred , Constanza, Valdes , and Ash Mark. 2019. Interdependence of China, United States, and Brazil in Soybean Trade. Washington DC: U.S. Department of Agriculture, ERS Oil Crops Outlook Report No. OCS‐19F‐01.

- Glauber, Joseph , Laborde David, Martin Will, and Vos Rob. 2020. COVID‐19: Trade Restrictions Are Worst Possible Response to Safeguard Food Security. International Food Policy Research Institute, March 27, 2020, https://www.ifpri.org/blog/covid-19-trade-restrictions-are-worst-possible-response-safeguard-food-security (accessed October 14, 2020).

- Haley, Mildred . 2019. Pork/Hogs: Fourth‐Quarter Pork Production Revised Upward to Reflect Faster‐Paced Slaughter Rate. Livestock, Dairy, and Poultry Outlook. Washington DC: U.S. Department of Agriculture, ERS Situation and Outlook Report No. LDP‐M‐305.

- Haley, Mildred, Gale, Fred, 2020. African Swine Fever Shrinks Pork Production in China, Swells Demand for Imported Pork. Amber Waves: The Economics of Food, Farming, Natural Resources, and Rural America, United States Department of Agriculture, Economic Research Service, vol. 0(01), February.

- Hart, Chad E. , Hayes Dermont J., Jacobs Keri L., Schulz Lee L., and Crespi John M.. 2020. The Impact of COVID‐19 on Iowa's Corn, Soybeans, Ethanol, Pork, and Beef Sectors. CARD Policy Brief, Iowa State University.

- International Monetary Fund . 2020. A Crisis Like No Other, An Uncertain Recovery. World Economic Outlook Update June 2020, https://www.imf.org/en/Publications/WEO/Issues/2020/06/24/WEOUpdateJune2020 (accessed October 14, 2020).

- Espitia, Alvaro , Rocha Nadia, and Ruta Michele. 2020. Covid‐19 and Food Protectionism: The Impact of the Pandemic and Export Restrictions on World Food Markets. Working Paper No. 9253, World Bank Policy Research.

- Lawder, David , Shalal Andrea, and Mason Jeff 2020. What's in the U.S.‐China Phase 1 Trade Deal. Reuters, January 15, 2020, https://www.reuters.com/article/us-usa-trade-china-details-factbox/whats-in-the-u-s-china-phase-1-trade-deal-idUSKBN1ZE2IF (accessed October 14, 2020).

- Lusk, Jayson L. , Tonsor Glynn, and Schulz Lee L.. 2020. Beef and Pork Markeing Margins and Price Spreads during COVID‐19. Applied Economics Perspectives and Policy. . 10.1002/aepp.13101. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Mano, Ana 2020. Nine Meat Plants in Southern Brazil Face COVID‐19 Outbreaks. Reuters, April 30, 2020, https://fr.reuters.com/article/us-health-coronavirus-brazil-meatpackers-idUSKBN22C2J8 (accessed October 14, 2020).

- Mano, Ana , and Figueiredo Nayara. 2020. Brazil Meatpackers Declare Exports Free from Coronavirus at China's Request. Reuters, June 23, 2020, https://www.reuters.com/article/us-brazil-meatpackers/brazil-meatpackers-declare-exports-free-from-coronavirus-at-chinas-request-idUSKBN23U38E (accessed October 14, 2020).

- McKibbin, Warwick , and Roshen Fernando. 2020. The Global Macroeconomic Impacts of COVID‐19: Seven Scenarios. CAMA Working Paper No. 19/2020.

- Tonsor, Glynn , and Schulz Lee. 2020. Assessing Impact of Packing Plant Utilization on Livestock Prices. Kansas State University Department of Agricultural Economics Extension Publication KSU‐AgEcon‐GTT‐2020.2.