ABSTRACT

Objective: The objective of this paper is to determine an upper price limit for an orphan drug by taken a broader perspective and, including also other monetary and non-monetary values for the society.

Methods: This model is based on the expected free cash flows and the required minimum rate of return for the investor. In addition we calculated an innovation premium resulting from cost savings due to the substitution effect and the monetary gain in QALYs of a new medicine. We selected Spinraza®, a first in class drug with only best supportive care as comparator, and Perjeta®, a first in class drug with already an actual treatment as comparator.

Results: The results show that Spinraza® leads to an innovation premium of € 78,966 and Perjeta® shows an innovation premium of € 4,388, because there were no cost savings. The analyses show the outcomes are sensitive to discount rate for QALYs.

Conclusion: The break-even price from only an investor perspective may not reflect the value of drug from a broader perspective. This study shows drug prices based on an innovation premium may be more representative of the actual value of innovation for the society.

KEYWORDS: Price, valuation, orphan, oncology, cost-effectiveness, reimbursement

Introduction

Pharmaceutical and biotechnology companies are increasingly launching innovative medicinal products with incremental cost-effectiveness ratios (ICERs), which often exceed the threshold considered as acceptable for reimbursement[1]. Once the drug price exceeds the threshold, authorities in many EU markets increasingly initiate price negotiations before a final reimbursement decision. [2] Similar price negotiations take place in Germany, France and The Netherlands. Although in other European countries, such as Italy, ICER is not yet an established criterion for decision making, presenting a study with an ICER exceeding € 30,000 may make negotiations more difficult.

For example, the Dutch Ministry of Health requested a discount of 80% from € 170,000 to € 34,000 for Orkambi (lumacaftor/ivacaftor combination therapy), a new drug for the treatment of cystic fibrosis, in October 2017. This € 34,000 is the break-even price, where the ICER for Orkambi becomes € 80,000 per QALY, which is the upper cost-effectiveness threshold in The Netherlands. However at such low prices, investors in healthcare will drop out and search for other sectors with higher returns. Nevertheless, there are cases where large discounts applied to contain excessive spending have kept the investment still profitable. The paradigmatic case is Sovaldi, the first highly effective hepatitis C drug. At an initial price per treatment cycle of US$ 84,000, the price was reduced on average to US$ 64,000 after less than one year in the US. In Europe, which arrived with a price per treatment of € 45,000, the price was reduced in every country, until less than € 10,000 in Italy. The price was therefore considered so excessive that the USA Senate intervened and opened a dispute with the producer [3], but the large number of treated patients meant that a large discount kept the investment profitable. In addition non-innovative drugs with little benefit have been approved with very high prices [4–7], as discussed in a review by Capri [8].

The current debate on high prices for drugs suffers from a number of methodological flaws. The use of upper acceptable thresholds for measures like ‘fair profit and marketing margin’ are based on accounting measures and can be questioned. [9] In addition thresholds for profit and marketing margins are subjective without any scientific justification in economic theory. In any case, the prices for orphan drugs could be much higher than for other drugs, because the costs for development can only be recouped on fewer patients. [10] A general assumption is that free market economics do not work for innovative drugs owing to information imbalance between the suppliers (drug companies), the prescribers (doctors) and the consumers (patients) and the failure of competition created by approval systems that create a temporary monopoly. This is a partial analysis, considering only national healthcare markets, but there is also an international financial market in biotechnology, where investors require a return of investment on their capital invested in company.

In a recent paper, we proposed a Pricing Model to assess the price of first in class innovative drugs from an investor’s perspective[10].This model applies concepts from economic valuation theory, which is based on the expected free cash flows and the required cost of capital. In a subsequent paper, we applied this concept in The Netherlands to orphan drugs with a positive clinical assessment and an incremental cost-effectiveness ratio exceeding € 80,000 per QALY. [11] The actual prices of the drugs in this analysis are in 50% lower than the minimum price based on the Discounted Cash Flow Model.

The objectives of this paper are to include additional scenarios in the Pricing Model (see Nuijten 2016) [10]in order to determine an upper price limit for a first in class orphan drug by taken a broader perspective, and to assess the impact of fine-tuning R&D costs and probabilities of failure for first in class drugs.

Methods

Concept

The concept of the new Pricing Model is briefly described, but details are provided in a previous publication. [12] The discounted cash flow is derived from the present value equation to calculate the time value of money and compounding returns.

NPV = CF1/((1 + r)1+ CF2/((1 + r)2+ – +CFn/ ((1 + r)n (Eq 1.)

Where

NPV = net present value

CF = (free) cash flow

n = the time in years before the future cash flow occurs

r = cost of capital

Cash flows from operations reflect the sales from the drugs, and the costs for R&D, production costs and marketing. The cost of capital or hurdle rate is the minimum rate that a company expects to earn when investing in a project, that is based on the average cost of capital in the pharmaceutical market for pharmaceutical (9%) and biotechnology companies (12%). [13] The cost of capital should not be based on the expectations at the time of the reimbursement application, but rather on the expectations at the time of investment. The discounted cash flow method is used to calculate the minimum of break-even (BE) price for the innovative drug, where the net present value is zero. When the BE price is higher than the actual drug price, the actual price may not attract investors, because the net present value becomes negative. For example, the required price of € 34,000 for Orkambi would lead to a negative net present value and consequently would not be sufficient for investors. However, if the BE price is substantially lower, the actual drug price may not be justified and more information is needed to determine if the price is reasonable. The input parameters are listed in Table 1. The time horizon for the cash flows is from year 1, following patent registration until the end of the patent period, which is 20 years. We assume that the product is registered at year 8 and obtains reimbursement within one year leaving 11 years for actual sales before the patent expires. The allocation of R&D failures to successful drugs obtaining EMEA or FDA approval is an important element in the valuation. The health authorities may only consider R&D costs, which are directly related to the new drug, whereas the R&D costs of the unsuccessful programs should be taken into account according to the principles of economic valuation. The probabilities of failure during the development (phase I, II and III) phases are derived from published literature. [10]

Table 1.

The input parameters for the discounted cash flow model

| Model parameter | Base case | Remarks |

|---|---|---|

| Cost of development (US$ million) |

US$ 701 million | Not specific for orphan disease or orphan drugs in oncology |

| Cost pre-clinical | US$ 217 million | |

| Phase I | € US$ 84 million | |

| Phase II | US$ 142 million | |

| Phase III | US$ 190 million | |

| Phase IV | US$ 68 million | |

| Years of development & approval | 8 years | |

| Population | Western markets: 947.1 million |

|

| Period between registration and reimbursement | 1 year | 1.5 year: risk of reimbursement failure based on increasing hurdles, especially for high priced orphan disease or orphan drugs in oncology+pricing negotiations |

| Net patent life | 12 years | |

| Cost of revenue | 40% | Not specific for orphan disease or oncology |

| Hurdle rate | 12% | 9%: pharmaceutical companies 18%: a higher risk for biotechnology companies in orphan drugs. 25%: premium for small firm risk and a higher risk for drugs in orphan disease area |

| Probability | Not specific for orphan disease or oncology | |

| - Phase I to II | 70% (failure – 30%) | |

| - Phase II to III | 39% (failure – 61%) | |

| - Phase III to FDA approval* | 69% (failure – 31%) | Assumption: same probability for EMA |

| - Eligibility | 90% | |

| - Probability of reimbursement | 90% | 80%: risk of reimbursement failure based on increasing hurdles, especially for high priced orphan drugs |

Application

Previously we applied the Discounted Cash Flow method to the projections of expensive drugs in The Netherlands, based on information from Dutch National Health Care Institute (‘Zorginstituut Nederland’ – Zin). [11,14] We selected in this previous orphan drugs with a positive clinical assessment and an ICER exceeding € 80,000 per QALY gained. We selected for this current research an orphan drug from our previous publication: Spinraza® (nusinersen) with an actual annual price of € 240,000 and a lower break-even price of € 95,860, which becomes € 114,837 in this new model because of minor different assumptions. In addition we include an orphan drug in oncology, Perjeta® (pertuzumab) with actual price of € 78,510 and a lower break-even price of € 63,082 for average treatment of 75,5 weeks. The Dutch health technology assessment reports are based on society perspective and therefore provide all relevant costs, which are required for the application of our concept. Therefore we applied our concept to Dutch healthcare setting instead of more well-known setting of England, where NICE only takes a payer perspective.

Price premium innovation

If policy makers are convinced of the value of innovative drugs based on concept of economic valuation, they may change the financial reimbursement rules for drugs with an ICER exceeding the threshold. Therefore we may consider an innovation premium for a first in class drug, if the clinical benefit exceeds the minimum required threshold to be considered superior to existing standard of care. For example in oncology, this threshold is three months overall survival (OS). [9] For orphan diseases, there may be accepted disease-specific thresholds, or these thresholds may be derived from clinical assessments by health authorities like NICE and AMNOG in respectively UK and Germany. The new innovative drug implicitly has a higher clinical benefit than standard treatment, because a similar clinical benefit would never justify a higher price and would lead to rejection for reimbursement with no need for price negotiations. The innovation premium is based on monetary and non-monetary values for society (patients, physicians, payers, providers and employers).

Monetary values – cost savings

The substitution effect of a new medicine may lead to substantial cost savings in other budgets, e.g., reduction of hospitalisation costs due to higher efficacy or reduction of treatment costs for adverse events resulting from a better safety profile. If we accept a societal perspective exceeding the silo’s in the budgeting systems in the health care system and other budgets (e.g. lost productivity), we can calculate the total cost savings from this broad perspective, which includes direct medical costs, direct non-medical costs, and indirect costs. [15]

Non-monetary values – QALYs

The clinical benefit will translate in a gain in QALYs by reduction of morbidity and/or an increase in survival, which are transferred into monetary values. This gain in QALYs can be transferred into a monetary value by applying the threshold for the incremental cost-effectiveness ratio. For example, if the threshold is € 40,000 per QALY, a gain in two QALYs corresponds with monetary gain of € 80,000. The threshold may be based on disease-specific thresholds depending on the severity of disease. For example, in oncology the threshold is € 80,000 per QALY in The Netherlands, which may also be applied for many orphan diseases. Consequently, the innovation premium reflects also the burden of disease, as a lower threshold for milder disease would translate into lower monetary gain and a lower innovation premium. The higher the QALY gain, the higher the uptake of the new drug, so the improvements in outcomes are also reflected in the cash flows. Hence the QALY gain has an effect on the economic value for investor (uptake) and society (monetary value of QALY).

Contrary to actual cost savings in euro from the substitution effect, this monetary gain from QALYs may be considered an intangible asset of innovation transferring Quality of Life into cost savings from a broader society perspective. The cost savings due to the substitution effect and the monetary gain in QALYs of a new medicine are additional gains for society, but were not yet included in our previous published Pricing Model [10], which is performed only from the investor’s perspective. Therefore the new upper price limit of the drug after inclusion of the innovation premium becomes:

P_up = P_break-even+I_premium (Eq. 2)

Where P_up = upper price limit

P_break-even is break-even price

I_premium is innovation premium

In fact, the society is still paying the break-even price: they pay the maximum price, but because of monetary savings, they actually pay the break-even price. Therefore the innovation premium is not an additional cost for society and but is transferred to the company in order to facilitate future clinical research for innovation.

For example, for Product X, the actual price is € 200,000 and the break-even price is € 120,000 based on the Pricing Model. The cost savings in the cost-effectiveness analysis from substitution effects are € 20,000. The gain in OS was 5 months and gain in QALYs was 0.5. When we apply upper threshold of € 80,000 this leads to € 40,000. The innovation premium is costs savings (€ 20,000) + monetary value of QALY gains (€ 40,000) is € 60,000. Hence the upper limit price is break-even price (€ 120,000)+innovation premium (€ 60,000) is € 180,000.

Fine-tuning parameters in the pricing model to orphan drugs

The previously published model is based on average R&D costs and average probabilities of failure during the development (phase I, II and III) phases from the published literature[10].However R&D costs may vary for low prevalence orphan drugs, as recruitment of sufficient patients may require more effort and time, which leads to higher costs [16]. In addition, the costs and probabilities of failure may be higher for the first on class new innovative drug for a disease, for which where there has only been best supportive care to treat the symptoms and complications of a disease. This especially is applicable for most recent new innovative orphan drugs, like for Spinraza® for spinal muscular atrophy. There is for these first in class drugs no existing infrastructure for setting up and running clinical trials based on previous clinical trial programs. For example there not yet project teams with clinical investigators, hospitals, universities and medical associations, based on previous clinical trial programs. The set-up of this initial R&D infrastructure requires an additional cost and the actual running of the clinical trials may suffer from lack of efficiency, because lack of any previous learning-curve effect in either the logistics (e.g. recruitment) and optimal trial design (e.g. inclusion criteria). Therefore the R&D costs as well as probabilities of failure may be higher for this type of first in class innovative drugs.

The type of innovation itself, for example a break-through innovation based on a completely different mechanism of action and substantial incremental benefits also may contribute to a higher BE price for a first in class drug. The investor may have included an additional risk due to the different mechanisms of action in the Discounted Cash Flow by higher failure probabilities in the cash flows and adding a risk premium to the hurdle rate. In addition the development and manufacturing process for break-through drugs may be substantially higher than for new generation drugs. Another type of first in class drugs is innovative drug for an indication, where there exist already medicinal treatments, for example, a new innovative drug for metastatic HER-positive breast cancer. R&D infrastructures exist already from the existing drugs, if we assume there is not a long-term gap between the clinical research of these drugs and the new drug. However, for a new biotech company with a first drug in this disease area, there are still additional costs for building up the relationships with the clinical investigators and other stakeholders. Their relationships with other companies from previous trial programs may create an entry barrier for the biotech company. In addition, the lack of experience from the side of the biotech company may still lead to inefficiencies in running the clinical trials. Hence the R&D costs and probabilities of failure are lower than for the first type of first in class drug, but they may still be higher than for other drugs. These ‘no first in class’ drugs are often ‘second or third in class’ drugs with similar mechanism of action than the initial drug, which created this new class.

Data for the model

Tables 2 and 3 show the input parameters for the assessment of the innovation premium for respectively Spinraza® and Perjeta®, which are derived from the health technology assessment (HTA) reports by the Dutch National Health Care Institute [17,18]. The budget impact sections of the HTA reports provide information on potential numbers of patients for The Netherlands (17.1 million), which were extrapolated to Western markets (947.1 million). These data were used in the Pricing Model to assess the BE prices for Spinraza® and Perjeta®. The calculation of the innovation premium was based on the costs, QALYs and life years gained in the cost-effectiveness (CE) sections of the HTA reports for Spinraza® and Perjeta®.

Table 2.

The input parameters for innovation premium of Spinraza®.

|

Total costs – lifetime |

||||

|---|---|---|---|---|

| Spinraza® | BSC | savings | ||

| Annual costs | Spinraza® | € 240,000 | € 0 | |

| - Medical costs | type 1 (43.2%) | € 47,700 | € 61,203 | € 13,503 |

| type 2 (54.1%) | € 14,265 | € 17,381 | € 3,116 | |

| type 3 (2.7%) | € 8,784 | € 10,316 | € 1,532 | |

| - Non-medical costs | type 1 (43.2%) | € 67,805 | € 67,805 | € 0 |

| type 2 (54.1%) | € 108,101 | € 108,101 | € 0 | |

| type 3 (2.7%) | € 59,378 | € 59,378 | € 0 | |

| - Total costs | type 1 (43.2%) | € 115,505 | € 129,008 | € 13,503 |

| type 2 (54.1%) | € 122,366 | € 125,482 | € 3,116 | |

| type 3 (2.7%) | € 68,162 | € 69,694 | € 1,532 | |

| QALYs | Discount 1.5% | Type 1 | Type 2, 3 | Gain |

| type 1 (43.2%) | 8.49 | 2.56 | 5.93 | |

| type 2 (54.1%) | 22.99 | 19.46 | 3.53 | |

| type 3 (2.7%) | 22.99 | 19.46 | 3.53 | |

| Life years | Discount 1.5% | Type 1 | Type 2, 3 | Gain |

| type 1 (43.2%) | 10.78 | 3.50 | 7.28 | |

| type 2 (54.1%) | 29.23 | 27.12 | 2.10 | |

| type 3 (2.7%) | 29.23 | 27.12 | 2.10 | |

| Incidence | 20 | |||

| Prevalence | 441 | |||

| Uptake | annual | 95%a |

aNot reported: assumption.

Table 3.

The input parameters for innovation premium of Perjeta®.

| |

|

Medical costs – lifetime |

|

|

| Discount 4% | PTD | TD | Savings | |

| Perjeta® | trastuzumab | |||

| trastuzumab | docetaxel | |||

| docetaxel | ||||

| Drug | total | € 205,136 | € 54,849 | |

| Perjeta® | € 77,570 | € 0 | ||

| other drugs | € 127,566 | € 54,849 | -€ 72,717 | |

| Administration | € 9,112 | € 6,631 | -€ 2,481 | |

| Adverse events | € 3,875 | € 3,718 | -€ 157 | |

| Other costs – no progression | € 8,814 | € 5,840 | -€ 2,974 | |

| Other costs – progression | € 27,442 | € 24,780 | -€ 2,662 | |

| Total |

|

€ 176,809 |

€ 95,818 |

-€ 80,991 |

| |

|

Non medical costs – lifetime |

|

|

| Discount 4% | PTD | TD | Savings | |

| Indirect costs | € 11,266 | € 11,972 | € 706 | |

| Transport | € 545 | € 418 | -€ 127 | |

| Total | € 11,811 | € 12,390 | € 579 | |

| |

|

Total costs |

|

|

| Discount 4% | PTD | TD | Savings | |

| € 188,620 | € 108,208 | -€81,570 | ||

| |

|

QALYs |

|

|

| Discount 1.5% | PTD | TD | Gain | |

| QALYs | 3.76 | 2.70 | 1.06 | |

| Life years | 5.51 | 4.11 | 1.40 | |

| Incidence | 520 | |||

| Uptake | year 1 | 60% | ||

| year 2 | 80% | |||

| year 3 | 90% | |||

We incorporated a scenario for Spinraza®, a first in class drug in a disease with only best supportive care, based on following assumptions: increase of hurdle rate from 12% to 18%, 10% increase of R&D and marketing costs, and 10% increase of failure of clinical trials.

For Perjeta®, a first in class drug, where there exist already medicinal treatments, we included the following more conservative scenario: increase of hurdle rate from 12% to 16%, 5% increase of R&D and marketing costs, and 5% increase of failure of clinical trials.

Results

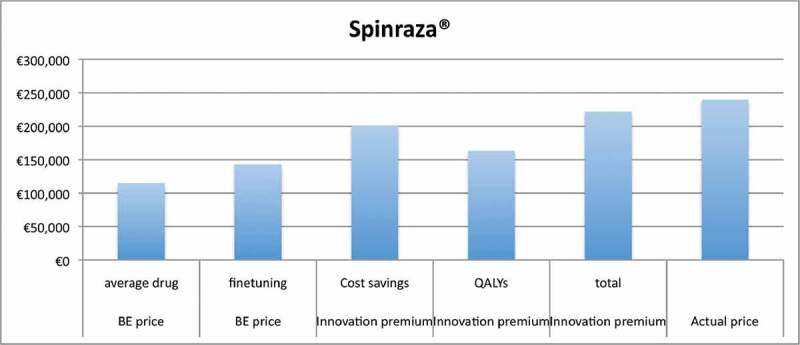

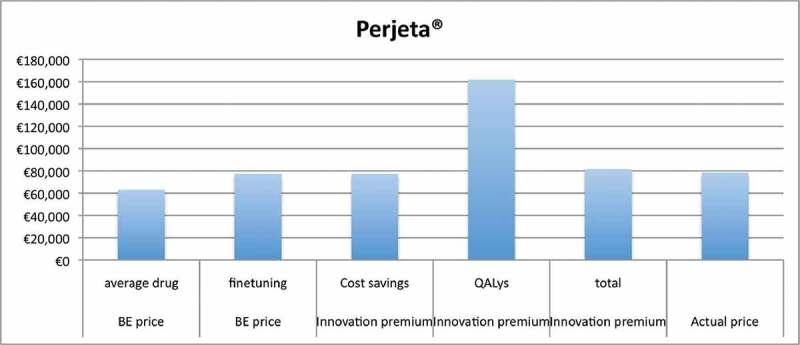

Table 4 shows the innovation premium for Spinraza® (Figure 1) and Perjeta® (Figure 2). The fine-tuning of parameters in the Pricing Model for Spinraza® increases the BE price from € 114,837 to € 143,052. The substitution effect of Spinraza® leads to an innovation premium of € 58,402, which increases the BE price from € 143,052 to € 201,454. The gain in QALYs leads to an innovation premium of € 20,554 and new drug price of €163,606, when the discount rate for QALYs is 1.5%. The combined innovation premium resulting from cost savings and QALY gain is € 78,966 and the corresponding new drug price is € 222,018. Discounting of QALYs at similar rate as costs (4%) reduces the innovation premium for QALYs gain from € 20,554 to € 14,494. This approach results in a new overall drug price of € 215,948 instead of € 222,018 with 1.5% discounting.

Table 4.

Results for Spinraza® and Perjeta®

| Drug price | Spinraza® | |||||

| Discounting | costs | 4.0% | 4.0% | |||

| QALYs | 1.5% | 4.0% | ||||

| savings | price | savings | price | |||

| Actual price | € 240,000 | € 240,000 | ||||

| BE price | average drug | € 114,837 | € 114,837 | |||

| fine-tuning | € 143,052 | € 143,052 | ||||

| Innovation premium | cost savings | total costs | € 58,402 | € 201,454 | € 58,402 | € 201,454 |

| gain QALYs | € 20,554 | € 163,606 | € 14,494 | € 157,546 | ||

| total | € 78,966 | € 222,018 | € 72,896 | € 215,948 | ||

| Drug price | Perjeta® | |||||

| Discounting | costs | 4.0% | 4.0% | |||

| QALYs | 1.5% | 4.0% | ||||

| savings | price | savings | price | |||

| Actual price | € 78,510 | € 78,510 | ||||

| BE price | average drug | € 63,082 | € 63,082 | |||

| fine-tuning | € 77,207 | € 77,207 | ||||

| Innovation premium | cost savings | medical costs | -€ 80,991 | € 63,082 | -€ 80,991 | € 63,082 |

| non-medical costs | € 579 | € 77,786 | € 579 | € 77,786 | ||

| total costs | - € 80,412 | € 77,207 | - € 80,412 | € 77,207 | ||

| gain QALYs | € 84,800 | € 162,007 | € 78,831 | € 156,038 | ||

| total | € 4,388 | € 81,595 | - € 1,581 | € 77,207 |

Figure 1.

Results for Spinraza®.

Figure 2.

Results for Perjeta®.

Table 4 shows similar analyses for Perjeta®. The fine-tuning of parameters in the Pricing Model for Perjeta® increases the BE price from € 63,082 to € 77,207. These results show that there is no innovation premium for substitution effects, as there are no cost savings for total costs (even extra costs of € 80,412). There are small cost savings for non-medical costs (€ 579), but increase of medical costs (€ 80,991) is much higher. The BE price remains € 77,207, as there is no innovation penalty in our concept. The gain in QALYs leads to an innovation premium of € 84,800 and € 78,831 at respectively 1.5% and 4% discount rate for QALYs. The combined innovation premium is € 4,388, when the discount rate for QALYs is 1.5%. This analysis results in an increase from € 77,207 (BE price) to € 81,595. There is no combined innovation premium for discount rate of 4% for QALYs, because the premium resulting from QALYs gain (€ 78,831) is more than off-set by additional total costs (€ 80,412).

Discussion

The current pricing negotiations by health authorities with pharma and biotech companies are often based on upper acceptable thresholds for measures like ‘fair profit and marketing margin’, and therefore the requested discounts are not justified by any economic theory. It should be remembered, however, that fair profit is one of the central elements in the debate on just price, a debate that has not yet produced solutions applicable to the definition of drug prices [19–21]. This is precisely why this model focuses on average R&D costs and average probabilities of failure during the development and on return on investment, followed by the premium innovation. In this way the model does not include any efficiency left to the company.

In this paper we explored scenarios in order to determine an upper price limit for first in class orphan drugs by taken a broad perspective and including substitution effects for medical and non-medical costs and monetary values of QALY gains. In addition we assessed the impact of fine-tuning R&D costs and probabilities of failure for first in class drugs. The analyses show different results for Spinraza® and Perjeta®, which may be explained by different indication: orphan disease versus orphan indication in oncology.

The analyses show also different impacts of similar impact of the innovation premium resulting from a gain in QALYs. This innovation premium is € 20,554 for Spinraza® and € 84,800 for Perjeta®, when discounted at 1.5%. The innovation premium is respectively € 14,494 and € 78,831 at 4% discounting. The higher impact of mortality in oncology than in chronic disease explains the high innovation premium for Perjeta®.

The results show that the impact of choice of discount rate for QALYs gained on the innovation premium is substantial, especially for Perjeta®, where the overall combined innovation premium is only based on the gain in QALYs because of a negative substitution effect for costs. At 1.5% discounting of QALYs there is an innovation premium of € 4,388, but at 4% discounting there is no innovation premium left. Because we consider QALYs as a monetary value, we may use the same discount rate of costs. On the other hand, we may argue that we accept the assumption that ‘value of health grows over time’ and this higher value is transformed into the corresponding monetary values by applying the threshold for the incremental cost-effectiveness ratio (e.g. € 80,000 per QALY in The Netherlands). We reported the results in two scenarios in order to show the implications of this methodological choice. Regardless of this issue, we may conclude that innovation premium is country-specific because of different discount rates and may vary between countries, reflecting the actual value of innovation for each country and the fact that price negotiations are country-specific.

The results for Perjeta® show that there is not an innovation premium for substitution effects, as there are no cost savings for total costs. There is no innovation penalty in our concept, because we selected drugs with a positive clinical assessment. Secondly, the BE price is the minimum price for the investor and therefore any lower drug price is not possible based on economic valuation theory.

The calculation of the cost savings from the substitution effect may not reflect the actual opportunity costs for the society. The unit costs (e.g. consultations and procedures) are not determined by demand and supply mechanisms in the healthcare market and therefore may not reflect the actual opportunity cost. The resource utilisation is also derived from an imperfect market. Market mechanisms usually increase the efficiency of the healthcare process and consequently optimise the resource utilisation. Therefore unit costs and units of resource utilisation may not reflect actual value in a free market.

We assessed the impact of fine-tuning R&D costs and probabilities of failure for first in class drugs, which increases the BE price for Spinraza® from € 114,837 to € 143,052. After inclusion of innovation premium, the new upper price becomes € 222,018 with 1.5% discounting of QALYs and € 215,948 with 4% discounting. Both upper prices (€ 222,018 and € 215,948) remain respectively 7.5% and 10% below the actual price of Spinraza® (€ 240,000). The BE price for Perjeta® increases from € 63,082 to € 77,207 and after inclusion innovation premium becomes € 81,595 which is 4% higher than the actual price of € 78,510. There is no combined innovation premium for discount rate of 4% for QALYs, because the premium resulting from QALYs gain (€ 78,831) is more than off-set by additional total costs (€ 80,412).

We propose an assessment of the innovation premium based on the quantification of the clinical benefit in monetary gains for the society. Uijl and Lowenberg already proposed this innovation premium, but they link the profit margin to the level of clinical benefit provided by the new drug: drugs that provide a higher level of clinical benefit, in their model, receive a higher profit percentage based on the ASCO Value in Cancer Care Framework or the ESMO Magnitude of Clinical Benefit Scale (ESMO-MCBS). They distinguish marginal, moderate and high clinical benefit and use assumed profit margins of 20%, 30% and 40%, respectively. This ASCO Value may be alternative threshold, but we do not recommend the use of profit margins because of its methodological constraints of these subjective measures, as we described previously.

Perhaps the most important limitation of this study is implicit the lack of information that is present in the real world. As in other areas, the solutions are influenced by the economics of information [22], and in our case the deficient data is represented by the investment costs, that is the real costs of R&D. As we have already mentioned, this also greatly limits the economic evaluations by payers when they are faced with the decision to compare an ICER with a budget impact. In fact a budget impact model should also be contained based on the excess profit that it could generate, but once again to estimate the profits it is essential to know the fixed costs, i.e. the R&D cost, but for the investor this information is less necessary.

It will be interesting to investigate in future work how to make investors’ interest compatible with that of the public payer in order to be able to calculate prices in a more balanced way.

Conclusion

This study shows that inclusion of an innovation premium provides a more balanced assessment of the high prices of orphan drugs. The analysis shows that the fine-tuning of the parameters to type of ‘first in class drug’ is appropriate. The break-even price from only an investor perspective may not reflect the value of drug from a broader perspective. Therefore the drug prices based on an innovation premium may be more representative of the actual value of innovation for the society.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- [1].Nuijten MJ, Dubois DJ.. Cost-utility analysis: current methodological issues and future perspectives. Front Pharmacol. 2011. June 8;2:29. [DOI] [PMC free article] [PubMed] [Google Scholar]

- [2].Available from: https://www.nice.org.uk/news/feature/changes-to-nice-drug-appraisals-what-you-need-to-know

- [3].USA Senate, Committee on Finance, Committee on finance USS . The price of Sovaldi and its impact on the U.S. health care system. Washington: U.S.: Government Publishing Office; 2014. July 11. 2015 December. [Google Scholar]

- [4].Morgan S, Bathula HS, Moon S, et al. Pricing of pharmaceuticals is becoming a major challenge for health systems. BMJ. 2020;368:l4627. [DOI] [PubMed] [Google Scholar]

- [5].Vivot A, Jacot J, Zeitoun JD, et al. Clinical benefit, price and approval characteristics of FDA-approved new drugs for treating advanced solid cancer, 2000–2015. Ann Oncol. 2017;28:1111–9. [DOI] [PubMed] [Google Scholar]

- [6].Salas-Vega S, Iliopoulos O, Mossialos E. Assessment of overall survival, quality of life, and safety benefits associated with new cancer medicines. JAMA Oncol. 2017;3(3):382–390. [DOI] [PubMed] [Google Scholar]

- [7].Davis C, Naci H, Gurpinar E, et al. Availability of evidence of benefits on overall survival and quality of life of cancer drugs approved by European medicines agency: retrospective cohort study of drug approvals 2009–13. BMJ. 2017;359:j4530. [DOI] [PMC free article] [PubMed] [Google Scholar]

- [8].Capri S. High prices of new drugs: we are ready to do whatever it takes. Università Cattaneo Working Papers, N. 8; 2020

- [9].Uyl-de Groot CA, Löwenberg B. Sustainability and affordability of cancer drugs: a novel pricing model. Nat Rev Clin Oncol. 2018;15:405–406. [DOI] [PubMed] [Google Scholar]

- [10].Nuijten MJC, Vis J. Evaluation and valuation of innovative medicinal products. J Rare Dis Res Treat. 2016;2(1):1–11. [Google Scholar]

- [11].Nuijten M, Fugel HJ, Vis J. Evaluation and valuation of the price of expensive medicinal products: application of the discounted cash flow to orphan drugs. Int J Rare Dis Disord. 2018. DOI: 10.23937/ijrdd-2017/1710005 [DOI] [Google Scholar]

- [12].Nuijten MJC, Vis J. Economic comments on proposal for a novel cancer drug pricing model. Nat Rev Clin Oncol. 2018. September;15(9):587. [DOI] [PubMed] [Google Scholar]

- [13].Harrington S. Cost of capital for pharmaceutical, biotechnology, and medical device firms; 2009. November 13. Prepared for The Handbook of the Economics of the Biopharmaceutical Industry.

- [14].Available from: https://www.horizonscangeneesmiddelen.nl

- [15].Guideline for economic evaluations in healthcare; 2016. June 16.

- [16].Berdud M, Drummond M, Towse A. Establishing a reasonable price for an orphan drug. OHE Research Paper 18/05; 2018, London: Office of Health Economics.Ref Hay. 2014. [DOI] [PMC free article] [PubMed] [Google Scholar]

- [17].Pakketadvies nusinersen (Spinraza®) . Zorginstituut Nederland Pakket; 2018. February 5. Referentie: 2018003862.

- [18].Pakketadvies pertuzumab (Perjeta®) . Zorginstituut Nederland Pakket; 2016. January 20. Referentie: 2015071828.

- [19].Abbott FM. Excessive pharmaceutical prices and competition law: doctrinal development to protect public health. UC Irvine Law Rev. 2016. December;6(3):281–320. [Google Scholar]

- [20].Council of Europe Resolution . Council conclusions on strengthening the balance in the pharmaceutical systems in the European Union and its member states; 2016. p. 269. Available from: https://www.consilium.europa.eu/en/press/press-releases/2016/06/17/epsco-conclusions-balance-pharmaceutical-system

- [21].OECD . Pharmaceuticals issues 2018. Available from: http://www.oecd.org/els/health-systems/pharmaceuticals.htm

- [22].Stiglitz JE. The revolution of information economics: the past and the future. NBER Working Paper No. 23780; 2017. September.