Abstract

Objective.

To estimate the effect of filgrastim-sndz market entry on patient out-of-pocket costs and claim payments for filgrastim products.

Methods:

This study used a single interrupted time series design with longitudinal, nationally representative, individual-level claims data from IBM MarketScan®. Analyses included all outpatient and prescription claims for branded filgrastim (filgrastim and tbo-filgrastim) and biosimilar filgrastim (filgrastim-sndz) from January 1, 2014 to December 31, 2017. Outcomes of interest included changes in monthly claim payments and monthly patient out-of-pocket costs for filgrastim products.

Results.

In the baseline period (January 2014-February 2016) insurers paid an average of $ 472.21 (95% confidence interval [CI]: 465.38 to 479.03) for 480 mcg of branded filgrastim while patients paid an average of $ 49.26 (CI: 34.25 to 64.27). Filgrastim-sndz market entry was associated with a statistically significant and immediate one-month decrease in insurer payment of $30.77 (95% CI: −40.59 to −20.94) and a significant decrease in monthly insurer payment trend of $3.10 per month (95% CI: −3.90 to −2.31) relative to baseline. Long-term changes in patient out-of-pocket costs were modest and restricted to beneficiaries enrolled in high cost sharing plans.

Conclusions.

Biosimilar filgrastim availability led to significant immediate and long-term decreases in claims payments for filgrastim products, supporting efforts to facilitate biosimilar adoption in the United States. However, there were only slight changes in patient out-of-pocket costs, restricted to beneficiaries enrolled in high cost sharing plans suggesting the importance of further work assessing the relationship between biosimilars availability and patient out-of-pocket costs.

Keywords: biosimilars, patient out-of-pocket costs, insurer payments, filgrastim, commercial insurance

Précis:

The U.S. availability of a filgrastim biosimilar effectively reduced insurer costs for filgrastim products but did not significantly impact overall patient out-of-pocket costs.

Introduction

Biologics, large, complex molecular therapies made from living organisms, have transformed the pharmaceutical landscape by providing novel treatments for high burden diseases [1]. While biologics are not new drugs – Humulin®, although not officially recognized as a biologic by the Food and Drug Administration (FDA) until March 23, 2020, was the first DNA recombinant product in the US and launched in 1982 - recent biotechnological advances have allowed for an exponential growth of the biologic market [2]. Despite their promise, the high costs of biologics represent a growing challenge for patients, payers and health systems. Limited patient access to biologics due to insurer cost containment policies, such as prior authorization, or financially burdensome out-of-pocket costs have been well documented [3–6]. Biologics are a significant driver of drug spending growth. In 2015, they represented less than 2% of US drug prescriptions but made up approximately 38% of all US drug spending [7]; in the period between 2010 and 2015, biologics accounted for 70% of the US drug spending growth [8].

As the use of biologics has grown, so has the need for effective cost containment. One means to achieve such cost containment has been through the development and utilization of biosimilars which are cheaper, highly similar but inexact copies of the referent (or brand name) biologic. Health economic theory suggests that biosimilars should lower healthcare costs through two mechanisms [9,10]. The first is through uptake and utilization of a less expensive product (the biosimilar). The second is through manufacturers lowering the price of branded biologics in response to the increased price competition generated by market entry of the biosimilar [9]. Biosimilar availability should result in lower prices across an entire product class, lower patient costs for biologics, and increased patient access. One study estimated that biosimilar adoption in the United States could generate upwards of $44 billion in healthcare cost savings over a 10-year period (2014 to 2024) [11]. However, in Europe, where biosimilars first reached the market in 2006 [12], there has been variation between actual and predicted cost-savings to insurers and patients [13].

September 2015 brought the U.S. launch of filgrastim-sndz, a biosimilar of filgrastim, a drug primarily indicated for neutropenia prophylaxis in cancer patients undergoing treatment with myelosuppressive chemotherapy [14]. This was the first biosimilar to gain U.S. FDA approval and provides a natural experiment with which to empirically evaluate the theorized benefits of biosimilar market entry in the United States. While a few studies have described filgrastim-sndz uptake, these have been descriptive and largely focused on the Medicare population [15–17]. Whether filgrastim-sndz market entry was associated with significant changes in claims payments and patient out-of-pockets costs for branded filgrastim remains unknown.

We used individual-level pharmacy and outpatient claims [13] to estimate the association between filgrastim-sndz availability in the United States and claims payments and beneficiaries’ out-of-pocket costs for filgrastim. Considering the European experience, we hypothesized that there would be a significant lag between filgrastim-sndz launch and widespread utilization. We also hypothesized that, due to increased price competition associated with biosimilar filgrastim market entry, claims payments for branded filgrastims would decrease. Finally, because deductibles and coinsurances are calculated from drug list prices (unlike copayments which are fixed by the insurer), we further hypothesized that if there were reductions in charges, as known from the claims payments, these would lead to lower patient out-of-pocket costs [18].

Methods

Data

We used two data sources and focused on the period from January 1, 2014 to December 31, 2017. Drug, medical and spending information were derived from the IBM MarketScan® Commercial Claims and Encounters (CCAE) Database. The CCAE Database contains longitudinal, inpatient, outpatient, and prescription drug claims for over 47 million patients aged 0 to 64 years old with employer-based insurance. Data come mainly from large employers and captures patient demographics, spending, medical, drug, and enrollment information [19]. We also used data from the U.S. Bureau of Labor Statistics (BLS) on the Consumer Price Index (CPI) of medical care to adjust our cost estimates for inflation over time [20]. The CPI Medical Care index is one of the eight CPI indexes derived by the U.S. BLS and is specifically designed to measure inflation for medical care services and medical care commodities in the United States [21]. This index captures both prescription drug and health insurance related price changes. As all our data were deidentified, this study was exempt from review by the Johns Hopkins Bloomberg School of Public Health Institutional Review Board.

Analytical Sample

Filgrastim products are available for purchase in retail pharmacies but are most frequently administered by clinicians in the outpatient setting. Because of this, our analytical sample consisted of all prescription and outpatient claims for branded (filgrastim, and tbo-filgrastim) and biosimilar (filgrastim-sdnz) filgrastims from January 1, 2014 to December 31, 2017. These were identified in the prescription claims using National Drug Codes (NDC) and in the outpatient claims using Healthcare Common Procedure Coding System (HCPCS) procedure codes. We excluded claims missing quantity or unit measures or missing the enrollee’s identification numbers or health plan type information. Consistent with other studies and due to the payment structure of capitated health plans, we also excluded claims from patients belonging to partially or fully capitated health plan [22].

Outcomes of Interest

Our first outcome of interest was the monthly average claim payment for branded filgrastim. Claim payments are calculated as the amount eligible for payment by pharmacies or providers after applying respective pricing guidelines and before applying any patient cost-sharing. As such, claim payments amounts reflect that reimbursement guidelines differ between pharmacy-dispensed and clinic-administered drugs. While claim payments reflect insurers’ discounts, the manufacturers’ rebates, which are proprietary information, are not captured by our outcome. Our second outcome of interest was the monthly average patient out-of-pocket (OOP) cost for a branded filgrastim. Patient OOP costs are the sum of their deductible, coinsurance, copayment and dispensing fees, when applicable. These variables are provided by MarketScan® where for each claim, the deductible is defined as the amount of total payment applied towards the beneficiary’s deductible and coinsurance is defined as the amount of coinsurance applied towards a patient’s OOP maximum [19].

Outcomes were aggregated at the month level. For example, monthly claims payments for branded filgrastim were calculated by summing claims payments for branded filgrastim in a given month and dividing this amount by the number of branded filgrastim claims for that month.

Standardizing Claims Payments and Patient Costs

Filgrastim products are only available as either a 300 mcg or 480 mcg single dose prefilled syringe or single dose vial [14]. For ease of comparison across filgrastim products and because of its clinical practicality, we standardized all costs and payments to a 480-mcg formulation. First, we identified the amount (in micrograms) of filgrastim product billed in each prescription claim from the associated NDC codes, which indicated whether a patient received a 300 mcg or a 480 mcg formulation. In the outpatient clinic setting, filgrastim products, while still only available as a 300 or 480 mcg formulation, can be billed in units of 1, 5, 300, or 480 micrograms. We used information contained in the HCPCS code, and the number of units dispensed, to identify the number of micrograms of filgrastim product billed. Then, for each claim (either pharmacy or medical), we transformed our spending outcomes (claims payments and patient OOP costs) to spending per microgram of filgrastim by dividing spending amount by number micrograms of filgrastim billed. This was then multiplied by 480 in order to arrive at spending per 480 mcg. Additionally, to assure comparability of our monthly estimates across the study period, we adjusted for inflation using the Medical Care CPI [20] and present all our estimates in January 2014 U.S. dollars.

Potential Determinants of Utilization

We also assessed insurance characteristics that may be associated with differential filgrastim product utilization and biosimilar filgrastim uptake. These included patient health plan type, subclassified into Exclusive Provider Organization (EPO), Point of Service (POS), Preferred Provider Organization (PPO), Consumer Directed Health Plan (CDHP) and High Deductible Health Plan (HDHP) and an indicator for whether the claim was for an outpatient service or a prescription.

Statistical Analysis

We began with descriptive statistics to examine branded and biosimilar filgrastim utilization and spending trends over our study period. Given the expected lag between the launch of a new drug and its adoption [23], we empirically determined the lag time between biosimilar filgrastim market entry and its utilization. Because of its demonstrated utility in the econometrics and interrupted time series (ITS) literature [24, 25], we used a structural break test of unknown break point with a sup-Wald statistic, as described by Piehl et al, 2003 [24] and more recently in Baicker and Svoronos 2019 [25], to determine the change point in branded filgrastim utilization for use in our main ITS analysis. Then, we used an ITS design with ordinary least squares (OLS) regression to estimate the impact of biosimilar filgrastim market entry on the claims payments and patient OOP pocket costs for branded filgrastim. Each model allowed for testing for both immediate changes (level shift) and long-term changes in outcome trend (change in slope). We tested for autocorrelation using the Durbin-Watson statistic [26] and accounted for it using Newey-West standard errors [27] with a lag value as determined by the Cumby-Huizinga test for autocorrelation [28]. We assessed for nonstationarity using the augmented Dickey-Fuller test [29].

While we did not expect claims payments to display a seasonal pattern, patient OOP costs generally decrease throughout the calendar year as beneficiaries reach their maximum OOP and deductible amount. We visually inspected our outcomes for seasonality using run-sequence plots [30] and accounted for it using monthly dummy variables, which flexibly capture any seasonal effects such as changing patient OOP costs over time. All statistical analyses were conducted using SAS version 9.4 (SAS Institute Inc., Cary, NC, USA) and Stata/SE, version 15 (StataCorp, College Station, TX, USA).

Sensitivity Analyses

Biosimilar filgrastim launched in September 2015 but gained FDA approval in March 2015 leaving a period of time during which branded filgrastim manufacturers may have negotiated prices in response to the news of biosimilar filgrastim’s approval. To address these potential anticipatory effects, we ran a sensitivity analysis in which we calculated the pre-launch trend for our ITS analyses using only data from January 1, 2014 to February 28, 2015, just prior to filgrastim-sndz FDA approval, and reran the models.

While tbo-filgrastim is a branded biologic, it was introduced as a follow-on product to filgrastim [31]. To the extent that tbo-filgrastim may not be representative of a typical branded biologic, we ran a sensitivity analysis in which our analytical sample was restricted to filgrastim only. Finally, as all filgrastim products are packaged as either single-dose or single-vial, we would expect all claims in our analytical sample to be for either 300 mcg, 480 mcg or some combination of both. To the extent that claims for dosages that do not meet these guidelines are systematically different from the rest, we ran a sensitivity analysis in which our analytical sample was restricted to claims for 300 mcg, 480 mcg, or any combination of these two doses.

Results

Intervention Point Determination

The most statistically meaningful breakpoint in branded filgrastim utilization occurred in February 2016, four months after the September 2015 release of biosimilar filgrastim (sup-Wald = 204.40; p< 0.001). This supports the use of ITS in this setting [25]. Therefore, despite that biosimilar filgrastim was launched in September 2015, our “pre-intervention” period was from January 1, 2014 to February 29, 2016 and the “post-intervention” period was from March 1, 2016 to December 31, 2017.

Overall Branded and Biosimilar Filgrastim Utilization

We identified 72,948 filgrastim product claims filed between January 1st, 2014 and December 31, 2017. Of these, 5,838 (8.0%) were filed for beneficiaries in a capitated health plan and were not included in our analysis. We excluded 3,780 (5.6%) of the 67,110 remaining claims because they lacked quantity or unit measures (270), enrollee identification numbers (110) or health plan information which represents between 669-779 beneficiaries (mean age (SD) 52.3 (14.0) years; 62.3 % female). Our final analytical sample consisted of 63,330 filgrastim product claims: 39,360 claims in the pre-intervention period and 23,970 claims in the post-intervention period.

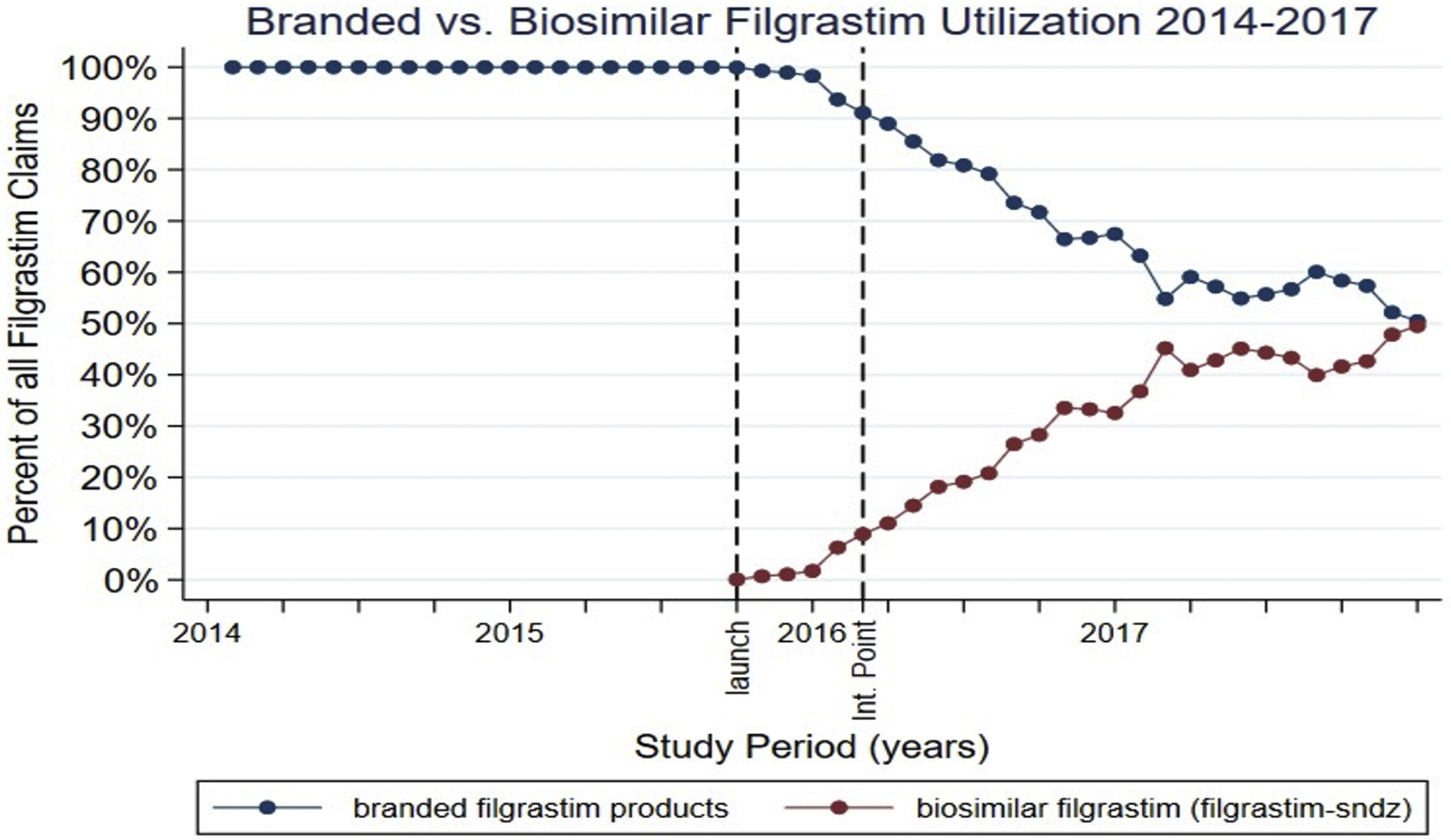

These claims represent 11,195 beneficiaries (mean age (SD): 49.0 (14.7) years, 63.2% female) who filed an average of 5.7 claims (SD: 9.3). The majority of claims (74.2%) were filed in the outpatient clinic setting. Beneficiaries enrolled in a PPO plan represented the majority of claims (70.2%), followed by those in a HDHP (21.4%), and in a CDHP (12.8%) plan with fewer beneficiaries filing as part of a POS (6.70%) or an EPO (1.74%) plan. In the months following the launch of filgrastim-sndz, branded filgrastim market share, as percent of total filgrastim product claims, decreased significantly (Figure 1). It reached its lowest point in December 2017, when branded filgrastim represented only 50.5% of all filgrastim product claims.

Fig 1.

Branded versus biosimilar filgrastim utilization (2014-2017). Launch corresponds to September 2015, the month biosimilar filgrastim (filgrastim-sndz) was launched in the United States. Int. point indicates intervention point (February 2016).

Overall, filgrastim utilization did not significantly change following biosimilar market entry. The level change in filgrastim product claims count was 200 fills/month (95% CI: −215 to 615) and the change in filgrastim product claims count trend relative to the pre-intervention trend was of 9 fills/month (95% CI: −17 to 35)

Baseline Characteristics and Trends in Filgrastim Claims Payments and Patient OOP Costs

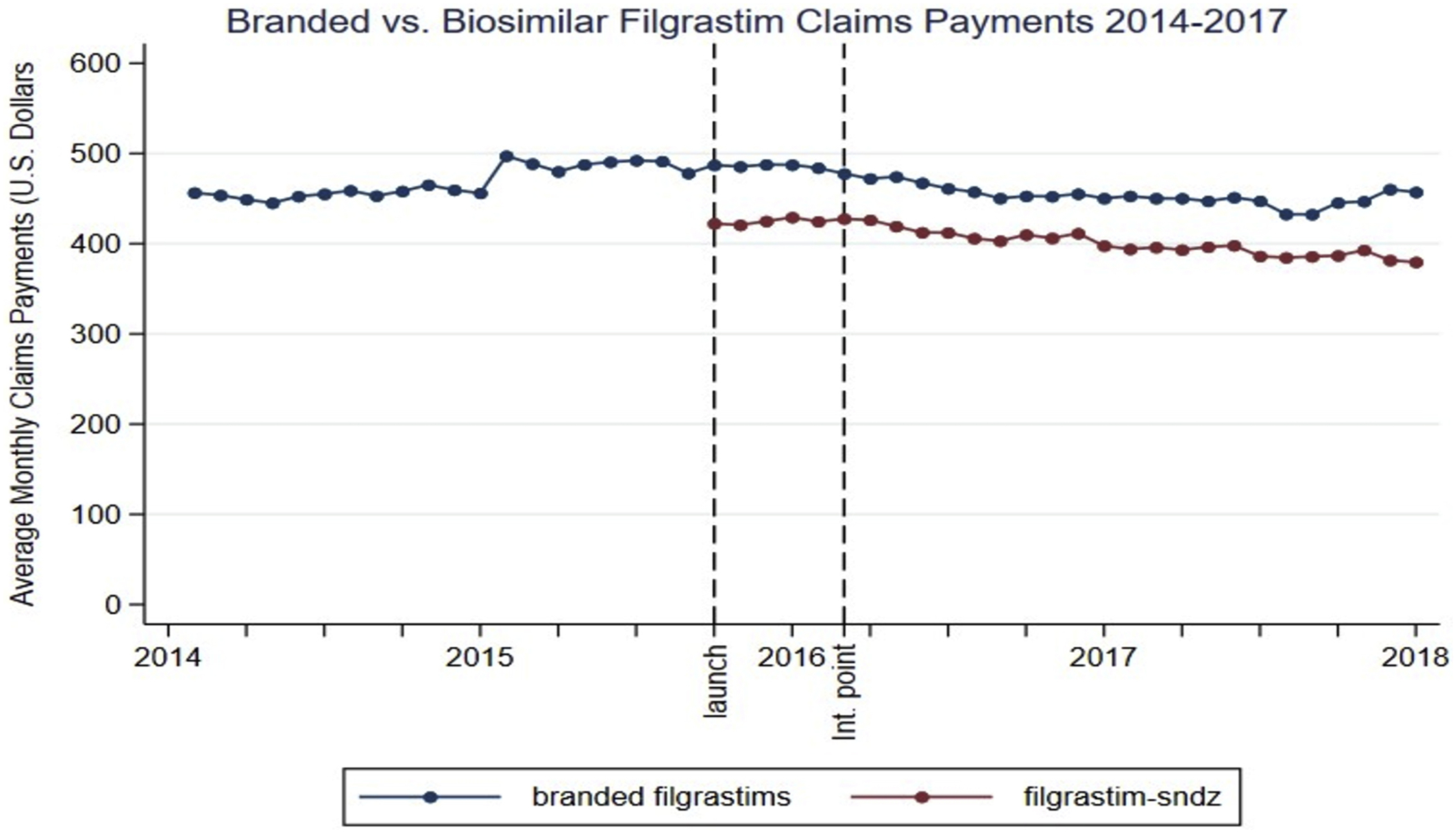

In the pre-intervention period, the average claims payment (Figure 2) and average patient OOP cost for 480 mcg of branded filgrastim was $472.21 (95% CI 465.38 to 479.03) and $49.26 (95% CI: 34.25 to 64.27), respectively. Inflation adjusted claims payments increased at an average rate of $1.79 per month (95% CI: 1.24 to 2.33) while patient OOP costs did not significantly change (average change: $0.19; 95% CI: −0.91 to 1.30).

Fig 2.

Average monthly claims payments for branded vs biosimilar filgrastim from January 2014 to December 2017. Launch corresponds to the launch month of biosimilar filgrastim (September 2015). Average monthly claims payments are adjusted for inflation using the Medical Care Consumer Price Index and all amounts are presented in January 2014 US dollars. Int. point indicates intervention point (February 2016).

Biosimilar Filgrastim Availability, Filgrastim Claims Payments and Patient Out-of-Pocket Costs

Biosimilar filgrastim market entry was associated with significant reductions in claims payments for branded filgrastim. (Table 1) There was an immediate (in first month) decrease in average claims payments/480 mcg of $30.77 (95% CI: −40.59 to −20.94) which represents a 6.52% reduction relative to February 2016. There was also an average reduction of approximately $3.10 a month (95% CI: 2.31 to 3.90) in the claims payments/480 mcg trend relative to the pre-intervention trend. At the end of our study period, the average claims payment for branded filgrastim was $441.47/480 mcg whereas our model estimated it would have been $538.58/480 mcg without the introduction of biosimilar filgrastim, which represents an18.0% relative reduction in average claims payment. A similar pattern was observed across all health plan types (Table 1).

Table 1.

Association between the market entry of biosimilar filgrastim and branded filgrastim products claims payments

| Change in Average Claims Payments for 480 mcg of Branded Filgrastim (in U.S. Dollars a) | ||

|---|---|---|

| Level Change b | Slope Change c | |

| All Branded Filgrastim products, Estimate, (95% CI) | − 30.77 (−40.59: −20.94) * | −3.10 (−3.90: −2.31) * |

| By Health Plan Type Estimate, (95% CI) | ||

| PPO | −32.66 (−41.31: −24.03) * | −2.85 (−3.60: −2.09) * |

| HDHP | −27.23 (−44.21: −10.26) * | −3.65 (−4.74: −2.55) * |

| CDHP | −36.22 (−58.47: −13.97) * | −3.43 (−5.05: −1.82) * |

Abbreviations: PPO: Preferred Provider Organization, HDHP: high deductible health plan, CDHP: consumer directed health plan

Payments adjusted for inflation using the Medical Care Consumer Price Index and all amounts are presented in January 2014 U.S. Dollars

Level change represents the average level change in claims payments amount following the intervention point (February 2016)

Slope change represents the average monthly change in claims payments trend over the post-intervention period relative to the baseline trend

p <0.001

Meanwhile, overall patient OOP costs and patient copayments, deductibles, and coinsurance amounts for branded filgrastim did not significantly change following biosimilar marker entry when looking at data pooled for all health plan types. (Table 2) However, among beneficiaries enrolled in plans with high levels of cost-sharing (HDHP and CDHP plans) we found a significant decrease in monthly trend of OOP costs relative to baseline. (Table 2) Relative to the pre-intervention trend, patients in HDHP and CDHP plans experienced an average reduction in their OOP costs/480 mcg of approximately $ 0.59 a month (95% CI: −1.03 to −0.14) and $ 0.79 a month (95% CI: −1.38 to −0.19) respectively. This represents a relative reduction in monthly average OOP cost/480 mcg of 1.20% for HDHP enrollees and 1.60 % for CDHP enrollees. On average, from March 1st, 2016 to December 31, 2017, patients paid $49.77/480 mcg (95% CI: 44.43 to 55.11) for branded filgrastim, and $23.53/480 mcg (95% CI: 20.59 to 26.46) for biosimilar filgrastim.

Table 2.

Association between the market entry of biosimilar filgrastim and patient out-of-pocket costs for branded filgrastim products

| Change in Average Patient Out-of-Pocket Cost for 480 mcg of Branded Filgrastim (in U.S. Dollars a) | ||

|---|---|---|

| Level Change b | Slope Change c | |

| All Branded Filgrastim products, Estimate, (95% CI) | −0.20 (−5.29: 4.90) | −0.08 (−0.41: 0.24) |

| By Health Plan Type Estimate, (95% CI) | ||

| PPO | −2.58 (−8.43: 3.27) | 0.02 (−0.36: 0.39) |

| HDHP | 0.81 (−6.94: 8.56) | −0.59 (−1.03: −0.14) * |

| CDHP | −3.81 (−13.93: 6.31) | −0.79 (−1.38: −0.19) * |

Abbreviations: PPO: Preferred Provider Organization, HDHP: high deductible health plan, CDHP: consumer directed health plan

Costs adjusted for inflation using the Medical Care Consumer Price Index and all amounts are presented in January 2014 U.S. Dollars

Level change represents the average level change in patient out-of-pocket costs following the intervention point (February 2016)

Slope change represents the average monthly change in cost trend over the post-intervention period relative to the baseline trend

p <0.05

Sensitivity Analyses

Our first sensitivity analyses, in which the pre-launch trend was calculated only with data from January 1, 2014 to February 28, 2015, supports the findings of our main analyses and results are presented in eTable2 of the online appendix. Our second sensitivity analysis, in which our analytical sample was restricted to referent filgrastim claims, also supports the findings of our main analysis are results are presented in eTable3 of the online appendix. In our final sensitivity analysis, we found that 82.9% of our analytical sample consisted of claims for 300 mcg, 480 mcg or a combination of these and restricted our analytical sample to these claims. Results again supported our main analysis and are presented in eTable4 of the online appendix.

Discussion

Following biosimilar filgrastim market entry, there was a rapid and significant decrease in branded filgrastim utilization which was due to a rapid and significant uptake of biosimilar filgrastim. Using an econometrics method [25] we quantified this break in utilization and found that significant uptake of biosimilar filgrastim began in February 2016. This corroborates previously published data on filgrastim-sndz uptake in Medicare [15,16] and Commercial [15] populations, as well as previous research on drug adoption which reported a typical delay of several months between the introduction of a new drug and its widespread adoption [23]. We also note that patient OOP costs were significantly lower for biosimilar than for branded filgrastim. To the extent that patients are (1) aware of their OOP costs, and (2) able to choose whether they receive a biosimilar version of a biological drug, biosimilar filgrastim’s lower OOP costs may have contributed to its rapid uptake.

We found that biosimilar filgrastim market entry was associated with significant immediate and long-term changes in branded filgrastim claims payments. These results did not vary by health plan type and were robust to sensitivity analyses. We can further characterize this reduction in claims payments by roughly approximating savings generated over the post-intervention period. Monthly savings due to reductions in branded filgrastim claims payments can be approximated by taking the average difference between the predicted claims payments trend had there been no biosimilar and the actual claims payments trend for a given month and multiplying it by the number of branded filgrastim claims for that month. Monthly savings in claims payments due to biosimilar uptake can be approximated by calculating the monthly average price difference between branded and biosimilar filgrastim and multiplying it by the number of biosimilar filgrastim claims for that month.

Summing these we find that filgrastim-sndz market entry was associated with approximately $3,663,741 in savings over the period from March 1, 2016 to December 31, 2017 with $3,302,408 coming from reductions in branded filgrastim claims payments and $361,333 coming from biosimilar filgrastim uptake. This represents savings of $152.85/480 mcg claim of which $137.78 comes from reduction in branded filgrastim insurer payments and $15.07 come from filgrastim-sndz uptake. This is a 33% reduction in the price/480 mcg of filgrastim product. These findings are similar to ones in Europe where one study of price evolution of filgrastim products across 23 European countries found an average reduction in price per dose before and after biosimilar market entry of approximately 37% [33]. This suggests that, in the case of filgrastim, market entry and availability of a biosimilar led to both immediate and long-lasting reductions in adjudicated biologic prices for insurers.

Assessing the relationship between biosimilar filgrastim market entry and patient OOP costs for branded filgrastim, we found that while overall patient OOP costs, including deductibles, copayments and coinsurance payments did not significantly change, beneficiaries enrolled in plans with high levels of cost sharing (HDHP and CDHP plans) experienced a small but statistically significant decrease in their OOP cost trend relative to the pre-intervention trend. This supports our hypothesis that biosimilar filgrastim market entry would decrease patient OOP costs through lower deductibles and coinsurances. However, since more than 70% of beneficiaries for filgrastim products were enrolled in a PPO plan, these cost decreases were not seen when we assessed patient out-of-pocket costs for all health plan types combined.

Despite significant reductions in branded filgrastim prices and low OOP costs for biosimilar filgrastim, we did not observe a significant increase in the volume of filgrastim product claims (branded and biologic) over our study period. This finding is supported by the health economics literature which has shown that prescription drugs, and more so essential drugs, have low price elasticity [34–36]. As filgrastim products are non-discretionary medicines used primarily in high-risk cancer patients and their use is encouraged by National Comprehensive Cancer Network (NCCN) guidelines [14, 37] we did not expect demand to be particularly elastic.

Limitations and Strengths

Our study has limitations. Claims data were limited to commercial claims; as payment structures and incentives vary significantly between commercial and public insurance, our findings may not be generalizable to public insurers and publicly-insured patients. However, as the majority of the U.S. population, 67.3% as of 2017 [38], is commercially insured, our study provides crucial information about an important portion of insurers and patients. Due to their payment structure and consistent with other studies, we excluded capitated health plans from our analyses [22]. Given this exclusion, our findings may not be generalizable to capitated health plans. However, capitated health plan claims represented only 8% of all filgrastim claims identified; while we encourage future research to investigate the effects of biosimilar market entry in capitated health plans, our study provides valuable information for the majority of filgrastim users. Another limitation of this study is that, due to the nature of claims, manufacturer rebates to insurers are not captured and we are not capturing net payments for filgrastim products. One recent study describing rebate trends for biologics in the Medicaid population found that manufacturers started offering substantial rebates following biosimilar market entry [39]. To the extent that these findings are generalizable to a commercially insured population our study likely underestimates the insurer savings associated with biosimilar filgrastim market entry. Another consideration is that this study characterizes the market entry of a single (and first) U.S. biosimilar. There may be some limitations as to the generalizability of our results to other biosimilars entering the U.S. market. Also, despite rigorous efforts to consider and adjust for confounding in our analysis, there may still be some other unobservable time variant factors we are not accounting for.

Yet this work has many strengths. First, instead of relying on a visual trend assessment to determine the lag in biosimilar filgrastim adoption, we used an econometrics method to empirically determine when branded filgrastim utilization started to significantly change. This allowed us to determine that ITS was a suitable estimation method for our question and maximized our signal-to-noise ratio by identifying the “best” intervention point for the purposes of ITS [25]. Second, this study is novel in that it is the first, we believe, to empirically estimate the effect of market entry of a new biosimilar on insurer payments and patient out-of-pocket costs in the United States. Third, this study assessed insurer payments and patient out-of-pocket costs by health plan type. This informed why certain costs were impacted while others were not. Finally, as our claims payments variable captured the different reimbursement structures used in the outpatient and the prescription setting, our study estimates reflect the variability in drug prices paid by insurers.

Implications and Future Research

Our results suggest that, in the case of filgrastim, market entry of a biosimilar led to significant savings in insurer payments for branded filgrastim as well as modest patient out-of-pocket cost reductions for beneficiaries enrolled in high cost sharing health plans. We have theorized that these savings are due to an increase in price competition due to the entry of a lower priced, highly similar product. As more biosimilars gain approval and are launched in the U.S. market, future research should examine (1) the impact of entry of a new biosimilar on cost and utilization in other, non-filgrastim drug classes and (2) the effect of additional biosimilar competition in drugs classes for which there are multiple competing biosimilar products.

Conclusions

In the case of filgrastim, we found that biosimilar availability led to significant immediate and long-term decreases in claims payments for filgrastim products as well as modest decreases in patient out-of-pocket costs restricted to patients in high cost sharing plans. These findings support health policy efforts to reduce roadblocks to widespread biosimilar approval and adoption in the United States.

Supplementary Material

Highlights.

Targeted policy efforts regarding biosimilars need to be informed by empirical evidence as to their cost containment potential. The 2015 launch of filgrastim-sndz, the first U.S. biosimilar, provides a natural experiment in which to evaluate the biosimilar experience in the United States.

This study is the first, we believe, to empirically estimate the effect of market entry of a new biosimilar on commercial insurer payments and patient out-of-pocket costs in the United States.

In the case of filgrastim, the availability of a biosimilar was effective in reducing claims payments for filgrastim products. Patient savings were restricted to beneficiaries enrolled in high cost sharing health plans.

Acknowledgments

Funding/Support: This work was supported by the pharmacoepidemiology training grant 1T32HL139426-1 from the National Heart, Lung and Blood Institute.

Role of the Funder/Sponsor: The funder had no role in the design and conduct of the study; collection, management, analysis, and interpretation of the data; preparation, review, or approval of the manuscript; and decision to submit the manuscript for publication.

Footnotes

Publisher's Disclaimer: This is a PDF file of an unedited manuscript that has been accepted for publication. As a service to our customers we are providing this early version of the manuscript. The manuscript will undergo copyediting, typesetting, and review of the resulting proof before it is published in its final form. Please note that during the production process errors may be discovered which could affect the content, and all legal disclaimers that apply to the journal pertain.

Conflicts of Interest: Dr. Alexander reports personal fees from IQVIA, personal fees from Monument Analytics, and personal fees from OptumRx, outside the submitted work; Dr. Trujillo, Dr. Segal and Dr. Mouslim report no conflicts of interest and have nothing to disclose.

Conflict of Interest Disclosures: Dr Alexander reported receiving personal fees from IQVIA Monument Analytics, and OptumRx outside the submitted work. Dr Alexander is the past Chair of FDA’s Peripheral and Central Nervous System Advisory Committee; has served as a paid advisor to IQVIA; is a co-founding Principal and equity holder in Monument Analytics, a healthcare consultancy whose clients include the life sciences industry as well as plaintiffs in opioid litigation; and is a member of OptumRx’s National P&T Committee. This arrangement has been reviewed and approved by Johns Hopkins University in accordance with its conflict of interest policies.

No other disclosures were reported.

References

- 1.Morrow T, Felcone LH. Defining the difference: What Makes Biologics Unique. Biotechnol Healthc. 2004;1(4):24–29. [PMC free article] [PubMed] [Google Scholar]

- 2.Kinch MS. An overview of FDA-approved biologics medicines. Drug Discov Today. 2015;20(4):393–398. doi: 10.1016/j.drudis.2014.09.003 [DOI] [PubMed] [Google Scholar]

- 3.Baum SJ, Toth PP, Underberg JA, Jellinger P, Ross J, Wilemon K. PCSK9 inhibitor access barriers—issues and recommendations: Improving the access process for patients, clinicians and payers. Clin Cardiol. 2017;40(4):243–254. doi: 10.1002/clc.22713 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Navar AM, Taylor B, Mulder H, et al. Association of Prior Authorization and Out-of-pocket Costs With Patient Access to PCSK9 Inhibitor Therapy. JAMA Cardiol. 2017;2(11):1217–1225. doi: 10.1001/jamacardio.2017.3451 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5.Heidari P, Cross W, Crawford K. Do out-of-pocket costs affect medication adherence in adults with rheumatoid arthritis? A systematic review. Semin Arthritis Rheum. 2018;48(1):12–21. doi: 10.1016/j.semarthrit.2017.12.010 [DOI] [PubMed] [Google Scholar]

- 6.Boytsov N, Zhang X, Evans KA, Johnson BH. Impact of Plan-Level Access Restrictions on Effectiveness of Biologics Among Patients with Rheumatoid or Psoriatic Arthritis. PharmacoEconomics - Open. 2020;4(1):105–117. doi: 10.1007/s41669-019-0152-1 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Miller S The $250 Billion Potential of Biosimilars. April 2013. http://lab.express-scripts.com/lab/insights/industry-updates/the-$250-billion-potential-of-biosimilars. Accessed November 1, 2019.

- 8.Coukell A Specialty Drugs and Health Care Costs Pew Charitable Trusts, Drug Spending Research Initiative. http://pew.org/1MRtwwM. Published 2015. Accessed October 31, 2019. [Google Scholar]

- 9.Blackstone EA, Joseph PF. The Economics of Biosimilars. Am Health Drug Benefits. 2013;6(8):469–478. [PMC free article] [PubMed] [Google Scholar]

- 10.McCamish M, Yoon W, McKay J. Biosimilars: biologics that meet patients’ needs and healthcare economics. Am J Manag Care. 2016;22(13 Suppl):S439–S442. [PubMed] [Google Scholar]

- 11.Mulcahy AW, Predmore Z, Mattke S. The Cost Savings Potential of Biosimilar Drugs in the United States: https://www.rand.org/pubs/perspectives/PE127.html. Published 2014. Accessed February 5, 2020.

- 12.Schiestl M, Zabransky M, Sörgel F. Ten years of biosimilars in Europe: development and evolution of the regulatory pathways. Drug Des Devel Ther. 2017;11:1509–1515. doi: 10.2147/DDDT.S130318 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Grabowski H, Guha R, Salgado M. Biosimilar competition: lessons from Europe. Nat Rev Drug Discov. 2014;13(2):99–100. doi: 10.1038/nrd4210 [DOI] [PubMed] [Google Scholar]

- 14.Awad M, Singh P, Hilas O. Zarxio (Filgrastim-sndz): The First Biosimilar Approved by the FDA. Pharm Ther. 2017;42(1):19–23. [PMC free article] [PubMed] [Google Scholar]

- 15.Karaca-Mandic P, Chang J, Go R, Schondelmeyer S, Weisdorf D, Jeffery MM. Biosimilar Filgrastim Uptake And Costs Among Commercially Insured, Medicare Advantage. Health Aff (Millwood). 2019;38(11):1887–1892. doi: 10.1377/hlthaff.2019.00253 [DOI] [PubMed] [Google Scholar]

- 16.Kozlowski S, Birger N, Brereton S, et al. Uptake of the Biologic Filgrastim and Its Biosimilar Product Among the Medicare Population. JAMA. 2018;320(9):929–931. doi: 10.1001/jama.2018.9014 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 17.Socal MP, Anderson KE, Sen A, Bai G, Anderson GF. Biosimilar Uptake in Medicare Part B Varied Across Hospital Outpatient Departments and Physician Practices: The Case of Filgrastim. Value Health. February 2020. doi: 10.1016/j.jval.2019.12.007 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 18.Smeeding J, Malone DC, Ramchandani M, Stolshek B, Green L, Schneider P. Biosimilars: Considerations for Payers. Pharm Ther. 2019;44(2):54–63. [PMC free article] [PubMed] [Google Scholar]

- 19.IBM MarketScan Research Databases for Health Services Researchers. April 2019. https://www.ibm.com/downloads/cas/6KNYVVQ2. Accessed February 1, 2020.

- 20.U.S. Bureau of Labor Statistics. Consumer Price Index for All Urban Consumers: Medical Care Commodities in U.S. City Average. FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/CUUS0000SAM1. Published January 1, 1984. Accessed March 10, 2020. [Google Scholar]

- 21.How BLS Measures Price Change for Medical Care Services in the Consumer Price Index : U.S. Bureau of Labor Statistics; https://www.bls.gov/cpi/factsheets/medical-care.htm. Accessed April 6, 2020. [Google Scholar]

- 22.Preussler JM, Mau L-W, Majhail NS, et al. Administrative Claims Data for Economic Analyses in Hematopoietic Cell Transplantation: Challenges and Opportunities. Biol Blood Marrow Transplant J Am Soc Blood Marrow Transplant. 2016;22(10):1738–1746. doi: 10.1016/j.bbmt.2016.05.005 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23.Lublóy Á Factors affecting the uptake of new medicines: a systematic literature review. BMC Health Serv Res. 2014;14. doi: 10.1186/1472-6963-14-469 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 24.Piehl AM, Cooper SJ, Braga AA, Kennedy DM. Testing for Structural Breaks in the Evaluation of Programs. Rev Econ Stat. 2003;85(3):550–558. doi: 10.1162/003465303322369713 [DOI] [Google Scholar]

- 25.Baicker K, Svoronos T. Testing the Validity of the Single Interrupted Time Series Design. National Bureau of Economic Research; 2019. doi: 10.3386/w26080 [DOI] [Google Scholar]

- 26.Durbin J, Watson GS. Testing for Serial Correlation in Least Squares Regression. Biometrika. 1950;37(3-4):409–428. doi: 10.1093/biomet/37.3-4.409 [DOI] [PubMed] [Google Scholar]

- 27.Newey WK, West KD. A Simple, Positive Semi-Definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix. Econometrica. 1987;55(3):703–708. doi: 10.2307/1913610 [DOI] [Google Scholar]

- 28.Cumby RE, Huizinga J. Testing the Autocorrelation Structure of Disturbances in Ordinary Least Squares and Instrumental Variables Regressions. Econometrica. 1992;60(1):185–195. doi: 10.2307/2951684 [DOI] [Google Scholar]

- 29.Dickey DA, Fuller WA. Distribution of the Estimators for Autoregressive Time Series With a Unit Root. J Am Stat Assoc. 1979;74(366):427–431. doi: 10.2307/2286348 [DOI] [Google Scholar]

- 30.Thompson JM. Visual Representation of Data Including Graphical Exploratory Data Analysis In: Hewitt CN, ed. Methods of Environmental Data Analysis. Environmental Management Series. Dordrecht: Springer Netherlands; 1992:213–258. doi: 10.1007/978-94-011-2920-6_6 [DOI] [Google Scholar]

- 31.Agboola F, Reddy P. Conversion from Filgrastim to Tbo-filgrastim: Experience of a Large Health Care System. J Manag Care Spec Pharm. 2017;23(12):1214–1218. doi: 10.18553/jmcp.2017.23.12.1214 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32.Questions about Single-dose/Single-use Vials | Injection Safety | CDC. Published June 20, 2019. Accessed June 9, 2020 https://www.cdc.gov/injectionsafety/providers/provider_faqs_singlevials.html

- 33.Quintile IMS. The Impact of Biosimilar Competition in Europe. Published online May 2017. [Google Scholar]

- 34.Lexchin J, Grootendorst P. Effects of prescription drug user fees on drug and health services use and on health status in vulnerable populations: a systematic review of the evidence. Int J Health Serv. 2004;34(1):101–122. doi: 10.2190/4M3E-L0YF-W1TD-EKG0 [DOI] [PubMed] [Google Scholar]

- 35.Skipper N On the Demand for Prescription Drugs: Heterogeneity in Price Responses. Health Economics. 2013;22(7):857–869. doi: 10.1002/hec.2864 [DOI] [PubMed] [Google Scholar]

- 36.Tamblyn R, Laprise R, Hanley JA, et al. Adverse events associated with prescription drug cost-sharing among poor and elderly persons. JAMA. 2001;285(4):421–429. doi: 10.1001/jama.285.4.421 [DOI] [PubMed] [Google Scholar]

- 37.Crawford J, Becker PS, Armitage JO, et al. Myeloid Growth Factors, Version 2.2017, NCCN Clinical Practice Guidelines in Oncology. J Natl Compr Canc Netw. 2017;15(12):1520–1541. doi: 10.6004/jnccn.2017.0175 [DOI] [PubMed] [Google Scholar]

- 38.Berchick ER, Hood E, Barnett JC. Health Insurance Coverage in the United States: 2017.; 2018. https://www.census.gov/content/dam/Census/library/publications/2018/demo/p60-264.pdf. Accessed April 4, 2020.

- 39.San-Juan-Rodriguez A, Gellad WF, Good CB, Hernandez I. Trends in List Prices, Net Prices, and Discounts for Originator Biologics Facing Biosimilar Competition. JAMA Netw Open. 2019;2(12):e1917379–e1917379. doi: 10.1001/jamanetworkopen.2019.17379 [DOI] [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.