“Would you tell me, please, which way I ought to go from here?” - Alice; “That depends a good deal on where you want to get to.” - The Cheshire Cat

-Lewis Carroll, Alice's Adventures in Wonderland and Through the Looking-Glass

Recent advances in medicine have centered around the development of biologic and targeted therapies. While these expensive biopharmaceuticals help optimize the outcome, there is resultant increased spending on healthcare and widening of health inequality. Can this chasm be bridged?

Biologics, Biosimilars, Biomimics, and Biobetters

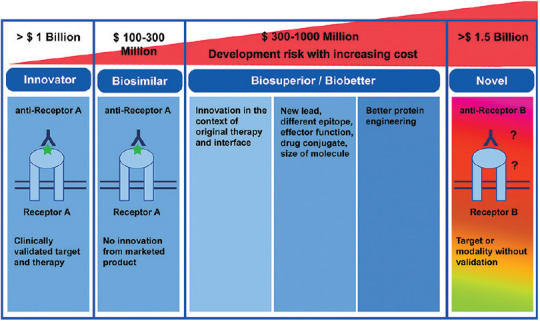

Biologics are medicines, active drug substance of which is made by or derived from a living organism, using processes such as recombinant DNA technology with controlled gene expression.[1,2,3] They have become part of the standard of care in several cancers, hematological, cardiovascular, autoimmune, retinal diseases, and specific rare genetic conditions.[1,4] Biologics are driven by years of dedicated research and innovation. They are relatively unstable large molecule proteins, involving complex manufacturing processes, with a specific and narrow spectrum of indications for use in relatively rare and often orphan diseases [Fig. 1]. Being invariably patented and expensive, these life-saving treatment modalities are often out of reach of patients in large parts of the developing world and add significantly to the cost of healthcare in developed countries that practice socialized medicine. In the United States (US), for example, 36% of overall drug expenditure is on biologics.[5]

Figure 1.

Innovator, biosimilar, biosuperior and novel medicine – the difference (adapted from https://www.drugdiscoverytrends.com/nextgeneration- of-biosimilars-and-biobetters-challenges-and-opportunities)

A biosimilar is a “biological product highly similar to the approved innovator product, with no clinically meaningful differences in safety, purity, and potency”.[1,2,3] Also known synonymously as follow-on biologics, biogenerics, similar biologics, similar biotherapeutic products, and generic biologics, biosimilars offer relatively less expensive, widely available, and affordable treatment options, and overall, improve access to care.[1,2,3] Biosimilars are made frugally in half the time and at about a tenth of the cost of the innovator biologic.[6] Approval is based on demonstration of analytical proof of biosimilarity, an animal study on toxicity, and a brief clinical study, and not on independently establishing the safety and efficacy of the proposed product [Fig. 1].[7,8] The process of development of a biosimilar essentially bypasses the discovery stage (as the therapeutic target is already known), phase II study (as the dosage, efficacy, and side effects are similar to the innovator product), and extensive clinical trials [Supplementary Fig 1 (219.9KB, tif) .].[1,2,3,7,8] Thus, the cost of the biosimilar can be driven down substantially in a market that is already well-primed to use the innovator product, with a good potential for a market share and profit. However, the pricing currently is only 20-40% lower than that of the innovator product.[9] There seems to be a scope to lower the price of biosimilars from the current level. Public policies should adequately address this aspect. Patient access to biologic treatments has grown as much as 100% following the availability of biosimilars.[10]

Biomimics are unregulated, non-comparable biologics, which, fortunately, have withered away. “Authorized” biologics/biosimilars are cheaper versions of innovator products produced by innovator companies themselves to increase patient access and compete with biosimilars by their competitors while continuing to manufacture and maintain the pricing on the approved innovator product in its niche.[11]

Biobetters or me-betters are new highly differentiated and potent biosuperiors based on an existing approved biologic, delivered out of better scientific research and antibody technologies to create an enhanced therapeutically beneficial mechanism of action, or potency improvement, increased bio-availability, longer half-life, better safety and immunogenicity, and better and broader efficacy.[12] The scope of biobetters is essentially to treat refractory or relapsed patients or those who have inconvenient dosing systems or safety concerns.[12]

The Emergence of Biosimilars

The European Union (EU) adapted a framework for biosimilars in 2004, which paved the way to the approval of the first biosimilar human recombinant growth hormone, Omnitrope (somatropin, Sandoz, Holzkirchen, Germany) by the European Medicines Agency (EMA) in 2006.[13] Biologics Price Competition and Innovation Act, part of the Affordable Care Act of 2010, created a US biosimilars pathway. The US Food and Drug Administration (FDA) approved Zarxio (filgrastim; Sandoz, Holzkirchen, Germany) in 2015.[14] The number of biosimilar approvals has touched 58 by EMA and 29 by FDA by January 2021, clearly showing a rising trend.[13,14] The World Health Organization has developed a general framework for the standardization and evaluation of “similar biotherapeutic products”.[1,2,3]

India – The Quiet Leader

Quietly and steadily, India has led the world in the approval and clinical use of “similar biologics”, the nomenclature that it uses for biosimilars. Beginning with the approval of the first known biosimilar - hepatitis-B vaccine in 2000, when no specific approval frameworks existed, India now has a clear policy, processes, and approval standards for biosimilars and has close to 100 approved products.[15,16] India has developed an active biosimilar development ecosystem with 201 products by 52 Indian manufacturers currently in the pipeline.[16] The Associated Chambers of Commerce of India has projected that the global market for biosimilars will have reached $240 billion by 2030, with the Indian market contributing to about $35 billion.[17]

Biosimilars in Ophthalmology

India was also the first-mover in biosimilars in ophthalmology, with the approval of Razumab (Intas Pharmaceuticals, Ahmedabad, India), the world's first biosimilar to ranibizumab (Genentech, San Francisco, CA, USA) in 2015, followed by several biosimilars to bevacizumab (F. Hoffmann La-Roche AG, Basel, Switzerland) [Table 1].[16,18] There are several other Indian biosimilars to ranibizumab in various phases of development.[16] With the patent cliff impending for the blockbuster innovator drug aflibercept (Regeneron, Tarrytown, NY, USA), its prospective biosimilars are in the pipeline. Other ophthalmologically relevant biosimilars are shown in Table 1.[13,14,18,19]

Table 1.

Biosimilars relevant to ophthalmology approved in India

| Innovator | Biosimilar (examples) | Indications |

|---|---|---|

| Bevacizumab | BevaciRel, Bevatas, Cizumab, Krabeva, Zybe | Anti-vascular endothelial growth factor |

| Ranibizumab | Rabumab | Anti-vascular endothelial growth factor |

| Adalimumab | Adfrar, Exemptia | Non-infectious uveitis |

| Infliximab | Infimab | Non-infectious uveitis |

| Tissue plasminogen activator | MiRel | Hyphema, vitreous hemorrhage, submacular hemorrhage, congenital cataract surgery etc |

| Rituximab | Acellbia, Maball, MabTas, Reditux, RituxiRel | Orbital inflammation, thyroid eye disease, lymphoma etc |

| Interferon alpha-2b | Intalfa, Reliferon, Shanferon, Zavinex | Ocular surface squamous neoplasia |

| Darbepoietin alpha, Epoietin alpha, Erythropoietin | Actorise, Cresp, Darbatitor, Ceriton, Epofer, Epofit, Erykine, Epotin, Erypro, Wepox, Relipoietin, Shanpoietin, Eporec, Repoitin, Zyrop | Neuroprotection |

| Streptokinase | Myokinase, Shankinase | Fibrin exudate, central retinal vein occlusion |

| Filgrastim, Peg-filgrastim | Emgrast, Fegrast, Grafeel, Neukine, Nufil, Religrast Neupeg, Pegex, Peg-grafeel | Chemotherapy-related neutropenia in ocular malignancies such as retinoblastoma |

Conclusion

Biosimilars in ophthalmology represent a unique and an earnest opportunity to democratize high-end medical care and ratchet up access to care to those who deserve, yet decrease the burden on healthcare systems. While the manufacturers should concentrate on optimizing the safety and pricing of these game-changers, a cultural and an informed cognitive transformation and trust are needed to change the mindset of the treating ophthalmologists and regulators to rapidly transition to biosimilars.

Stages in the process of drug development for biosimilar drugs as compared to innovator drugs (adapted from Agbogbo FK, Ecker DM, Farrand A, Han K, Khouri A, Martin A, et al. Current perspectives on biosimilars. J Ind Microbiol Biotechnol 2019; 46, 1297–13110

References

- 1.Farhat F, Torres A, Park W, de Lima Lopes G, Mudad R, Ikpeazu C, et al. The concept of biosimilars: From characterization to evolution-a narrative review. Oncologist. 2018;23:346–52. doi: 10.1634/theoncologist.2017-0126. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2.Declerck PJ. Biologicals and biosimilars: A review of the science and its implications. GaBI J. 2012;1:13–6. [Google Scholar]

- 3.FDA. Biologics Price Competition and Innovation Act of 2009. [[Last accessed on 2020 Oct 17]]. Available from: https://www.fda.gov/media/78946/download .

- 4.Sylvester K, Rocchio M, Beik N, Fanicos J. Biosimilars: An emerging category of biologic drugs for emergency medicine practitioners. Curr Emerg Hosp Med Rep. 2013;1:226–35. [Google Scholar]

- 5.Medicine Use and Spending in the U.S. A Review of 2018 and Outlook to 2023. May 2019, [[Last accessed on 2020 Oct 17]]. IQVIA Institute for Human Data Science. Available from: https://www.iqvia.com/-/media/iqvia/pdfs/institute-reports/medicine-use-andspending-in-the-us---a-review-of-2018-outlook-to-2023.pdf?_=1602972025818 .

- 6.Agbogbo FK, Ecker DM, Farrand A, Han K, Khouri A, Martin A, et al. Current perspectives on biosimilars. J Ind Microbiol Biotechnol. 2019;46:1297–311. doi: 10.1007/s10295-019-02216-z. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7. [[Last accessed on2021 Jan 17]]. Available from: http://www.fda.gov/drugs/biosimilars/biosimilar-development-review-and-approval .

- 8.Kirchhoff CF, Wang XM, Conlon HD, Anderson S, Ryan AM, Bose A. Biosimilars: Key regulatory considerations and similarity assessment tools. Biotechnol Bioeng. 2017;114:2696–705. doi: 10.1002/bit.26438. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9. [[Last accessed on 2021 Jan 17]]. Available from: https://www.pharmaceutical-technology.com/comment/commentwhat-are-the-incentives-and-challenges-to-biosimilar-development-5751024/the .

- 10.Danese S, Bonovas S, Peyrin-Biroulet L. Biosimilars in IBD: From theory to practice. Nat Rev Gastroenterol Hepatol. 2017;14:22–31. doi: 10.1038/nrgastro.2016.155. [DOI] [PubMed] [Google Scholar]

- 11. [[Last accessed 2021 Jan 17]]. Available from: https://www.centerforbiosimilars.com/view/opinion-the-year-ahead-in-biosimilar-developments .

- 12. [[Last accessed on 2021 Jan 17]]. Available from: https://www.drugdiscoverytrends.com/next-generation-of-biosimilars-and-biobetters-challenges-and-opportunities/

- 13. [[Last accessed on 2021 Jan 17]]. Available from: https://www.gabionline.net/Biosimilars/General/Biosimilars-approved-in-Europe .

- 14. [[Last accessed on 2021 Jan 17]]. Available from: https://www.fda.gov/drugs/biosimilars/biosimilar-product-information .

- 15.Guidelines on Similar Biologics; Regulatory Requirements for Marketing Authorization in India, 2012, revised 2016. [[Last accessed on 2021 Jan 17]]. Available from: https://nib.gov.in/NIB-DBT2016.pdf . [DOI] [PubMed]

- 16. [[Last accessed on 2021 Jan 17]]. Available from: https://birac.nic.in/webcontent/Knowledge_Paper_Clarivate_ABLE_BIO_2019.pdf .

- 17. [[Last accessed on 2021 Jan 17]]. Available from: https://www.sathguru.com/Publication/download/Biosimilars-WhitePaper-report.pdf .

- 18. [[Last accessed on 2021 Jan 17]]. Available from: https://www.gabionline.net/Biosimilars/General/Similar-biologics-approved-and-marketed-in-India .

- 19.Sharma A, Kumar N, Parachuri N, Bandello F, Kuppermann BD, Loewenstein A. Biosimilars for retinal diseases: An update. Am J Ophthalmol. 2020 doi: 10.1016/j.ajo.2020.11.017. doi: 10.1016/j.ajo.2020.11.017. [DOI] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Stages in the process of drug development for biosimilar drugs as compared to innovator drugs (adapted from Agbogbo FK, Ecker DM, Farrand A, Han K, Khouri A, Martin A, et al. Current perspectives on biosimilars. J Ind Microbiol Biotechnol 2019; 46, 1297–13110