Abstract

The spillover effect of cigarette taxes on youth marijuana use has been the subject of intense public debate. Opponents of cigarette taxes warn that tax hikes will cause youths to substitute toward marijuana. On the other hand, public health experts often claim that because tobacco is a “gateway” drug, higher cigarette taxes will deter youth marijuana use. Using data from the National and State Youth Risk Behavior Surveys (YRBS) for the period 1991–2017, we explore the relationship between state excise taxes on cigarettes and teen marijuana use. In general, our results fail to support either of the above hypotheses. Rather, we find little evidence to suggest that teen marijuana use is sensitive to changes in the state cigarette tax. This null result holds for the sample period where cigarette taxes are observed to have the largest effect on teen cigarette use and across a number of demographic groups in the data. Finally, we find preliminary evidence that the recent adoption of state e-cigarette taxes is associated with a reduction in youth marijuana use.

Keywords: cigarette taxes, teen marijuana use, e-cigarette taxes, youth risky behavior

JEL Codes: H71, H75, I12, I18, K42

I. INTRODUCTION

Cigarette taxes have long been lauded by anti-smoking advocates and policymakers as an effective tool to curb youth cigarette use (Chaloupka, Straif, and Leon, 2011; Marr and Huang, 2014; U.S. Department of Health and Human Services, 2014; Truth Initiative, 2019). Indeed, the American Academy of Pediatrics strongly recommends tax increases on all tobacco products to discourage youth tobacco use initiation (American Academy of Pediatrics, 2015). Beyond reducing negative consumption externalities, deterring youth smoking may also have an efficiency rationale if teens are more likely than adults to have time-inconsistent preferences and hyperbolically discount the future (Underwood, 2013; Huang, Hu, and Li, 2017), thereby imposing “internality” costs on their future selves (Gruber and Köszegi, 2001).

In recent years, support for cigarette taxes has been strong and bipartisan. Voters generally prefer cigarette tax increases to budget cuts and favor earmarking a portion of the tax revenue for tobacco prevention efforts (Boonn, 2019a). Even smokers often support cigarette tax increases when the revenues are targeted at youth smoking prevention (Chaloupka, Powell, and Warner, 2019) or if they believe the tax hikes will serve as a self-control device (Gruber and Mullainathan, 2005).

Opponents of higher cigarette taxes have claimed that many smokers are rationally addicted to tobacco (Becker and Murphy, 1988) and warn that higher prices will have unintended consequences such as encouraging youths to substitute toward marijuana and other harder drugs (Chaloupka et al., 1999). According to recent data from Monitoring the Future, the rate of daily marijuana use has actually surpassed the rate of daily cigarette use among high school seniors, which some have attributed, in part, to anti-tobacco efforts (Khazan, 2015).

On the other hand, a large literature in medicine and public health suggests that tobacco is a “gateway drug” and that use during adolescence will encourage subsequent consumption of harder drugs (Kandel, 1975; Ellickson, Hays, and Bell, 1992; Lai et al., 2000; American Academy of Pediatrics, 2013; Suerken et al., 2014), which could include the combined consumption of marijuana and tobacco in the form of a “spliff” (Hammersley and Leon, 2006). However, outside of research performed on mice in the lab,1 none of these studies take into account the potentially endogenous relationship between tobacco use and the use of other substances. For instance, the National Center on Addiction and Substance Abuse (2003) concludes that “reducing teen smoking can be a singularly effective way to reduce teen marijuana use” simply because survey evidence indicates that teens who smoke cigarettes are also more likely to try marijuana.

This study breaks the simultaneity in youth cigarette and marijuana consumption by exploring the relationship between state cigarette excise taxes and teen marijuana use. While a handful of studies have used cross-state variation in cigarette taxes to identify effects on youth marijuana use, estimates from this type of research design could be biased due to unobservables at the state level, including anti-tobacco sentiment (DeCicca, Kenkel, and Mathios, 2002, 2008). To our knowledge, only one previous study uses within-state variation to identify the relationship between cigarette taxes and youth marijuana use. Using data for the period 1990–1996, Farrelly et al. (2001) find that higher cigarette taxes are associated with decreases in the intensity of marijuana use among 12- to 20-year-olds. Since 1996, 48 states and the District of Columbia raised their per-pack excise tax on cigarettes, nearly half of all states increased their tax on three or more occasions, and 17 states passed tax increases exceeding one dollar per pack.

Using data from the National and State Youth Risk Behavior Surveys (YRBS) for the period 1991–2017, we first confirm the negative relationship between state excise taxes on cigarettes and teen cigarette use that has been documented in prior research (Carpenter and Cook, 2008). We also confirm that this relationship grows substantially weaker over time (Hansen, Sabia, and Rees, 2017). Next, we explore the relationship between cigarette taxes and teen marijuana use. Because the YRBS data cover such a long period of time, and the frequency and magnitude of state cigarette tax hikes increased markedly following the 1998 Master Settlement Agreement (MSA), we are able to exploit significantly more policy variation than Farrelly et al. (2001). In general, we find little evidence to suggest that teen marijuana use is sensitive to state-level changes in the per-pack cigarette tax. Specifically, our estimates on the relationship between cigarette taxes and teen marijuana use are generally small in magnitude and statistically indistinguishable from zero, and these null results hold across various model specifications and when we split the sample by gender, race, or age. Only for respondents ages 14 and younger do we uncover some evidence of a negative relationship between cigarette taxes and frequent marijuana use.

In addition to exploring the effects of state cigarette taxes, we also examine how medical and recreational marijuana legalization affects youth cigarette and marijuana use. We find that medical marijuana laws (MMLs) are associated with decreases in both teen cigarette and marijuana consumption, suggesting these goods may be complements among youths. Similarly, recreational marijuana laws (RMLs) are negatively associated with teen cigarette and marijuana use, but the relationship between RMLs and cigarette use is estimated with imprecision.

Finally, we provide the first evidence on the relationship between state electronic cigarette taxes and youth marijuana use. Here, we find that the enactment of an e-cigarette tax is associated with a 7 percent reduction in youth marijuana use, consistent with the hypothesis that e-cigarettes and marijuana are complements. However, given that this estimate is based on limited policy variation, we view this evidence as preliminary and worthy of future investigation.

The remainder of the paper is organized as follows. We begin with a history of cigarette taxes in the United States and review the relevant literature. In Section III, we describe our data and empirical strategy; in Section IV, we report our principal estimates; in Section V, we briefly discuss coefficient estimates on indicators for medical and recreational marijuana legalization; and in Section VI, we include a preliminary analysis of e-cigarette taxes. Section VII concludes.

II. BACKGROUND

A. Cigarette Taxes in the United States

The first federal cigarette tax in the United States was levied in 1864 as a revenue measure for the Civil War (Tax Foundation, 2019). Over the course of the next century, the tax fluctuated in response to government revenue requirements, which generally corresponded to oscillating periods of war and peace. For instance, in 1951, the federal cigarette excise tax increased from 7 to 8 cents per pack to help fund the Korean War (Committee on Preventing Nicotine Addiction in Children and Youths, 1994). Federal cigarette taxes were last increased in 2009, with the tax going up from $0.39 to $1.01 per pack (American Lung Association, 2019).

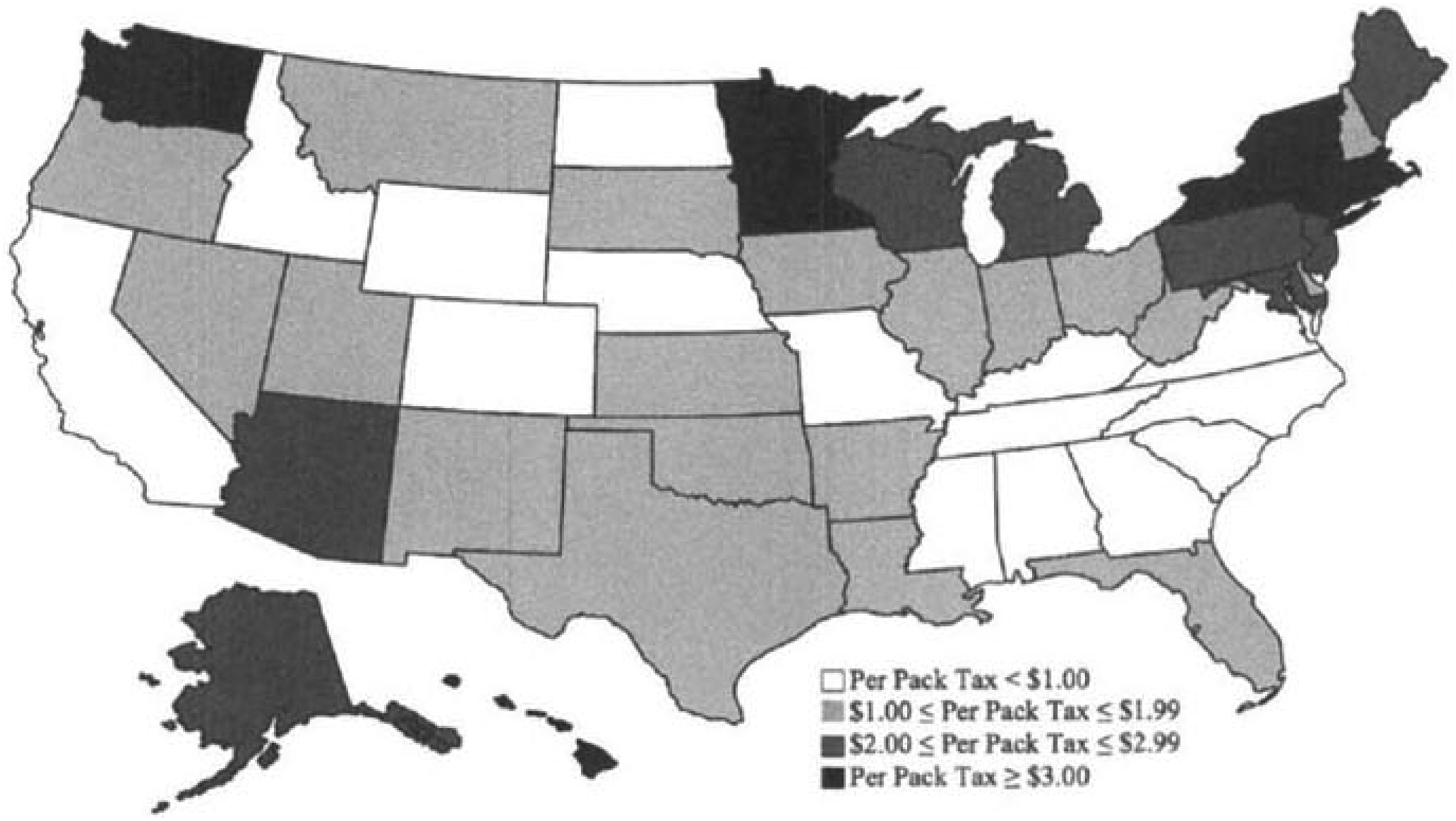

In 1921, Iowa became the first state to implement a cigarette tax and other states were soon to follow. By 1969, all 50 states and the District of Columbia imposed taxes on cigarettes.2 Likely due to large gaps between state cigarette tax rates, organized smuggling and illegal diversion of cigarettes increased during the 1960s and 1970s. In response, the government enacted the Federal Cigarette Contraband Act, which prohibits the transportation, distribution, receipt, or purchase of more than 10,000 “unstamped” cigarettes (Committee on Preventing Nicotine Addiction in Children and Youths, 1994; Bureau of Alcohol, Tobacco, Firearms and Explosives, 2018).3 Currently, New York and the District of Columbia tax cigarettes at the highest rates, imposing per-pack taxes of $4.35 and $4.94, respectively. Missouri levies the lowest cigarette tax at $0.17 per pack (Centers for Disease Control and Prevention, 2019). Figure 1 shows state per-pack cigarette tax rates as of 2017, the last year of our sample period.

Figure 1.

State Cigarette Taxes in 2017

B. Cigarette Taxes and Youth Cigarette Use

A number of studies have estimated the relationship between state cigarette taxes and youth cigarette use.4 While much of this literature relies on tax variation across states,5 making it difficult to control for unobserved factors at the state level, more recent papers exploit within-state tax variation (DeCicca, Kenkel, and Mathios, 2002, 2008; Carpenter and Cook, 2008; Hansen, Sabia, and Rees, 2017).

Using data from the National Educational Longitudinal Study, DeCicca, Kenkel, and Mathios (2002) find that state cigarette taxes passed between 1988 and 1992 have no observable effect on youth smoking participation. A follow-up study by DeCicca, Kenkel, and Mathios (2008) explores heterogeneity in cigarette tax effects at the smoking initiation and cessation margins. They find that tax hikes are ineffective at deterring smoking at the initiation margin, which largely affects teens.

In contrast to DeCicca, Kenkel, and Mathios (2002, 2008), Carpenter and Cook (2008) rely on a substantially longer panel of data with larger and more frequent changes in the state cigarette tax. Using data from the National, State, and Local YRBS for the period 1991–2005, Carpenter and Cook (2008) estimate the effect of state cigarette taxes on smoking participation and frequent smoking among youths.6 Their results indicate that a one-dollar increase in the per-pack tax (in 2005 dollars) reduces smoking participation by 10–20 percent. Similarly, they find that a one-dollar tax increase reduces the incidence of frequent smoking by 18–30 percent.7

Hansen, Sabia, and Rees (2017) revisit the work of Carpenter and Cook (2008) and draw upon four additional waves of YRBS data (2007, 2009, 2011, and 2013). Their results suggest that the relationship between cigarette taxes and youth smoking has weakened over time. While they confirm Carpenter and Cook’s (2008) results for the period 1991–2005, they find little evidence to suggest that cigarette taxes reduced youth smoking for the years 2007–2013.8 Hansen, Sabia, and Rees (2017) hypothesize that recent state cigarette taxes may be less effective at deterring teen smoking because the marginal youth smoker is now more price inelastic. This could be due to effective anti-smoking campaigns in the 1990s and 2000s, such that price-sensitive youths reduced their smoking participation, leaving only youths in the market whose marginal utility from smoking is very high.

C. Youth Marijuana Use

There is a substantial literature on the determinants of youth marijuana use. Previous studies have estimated the effects of MMLs and RMLs (Anderson, Hansen, and Rees, 2015; Pacula et al., 2015; Dilley et al., 2019; Anderson et al., 2019), marijuana decriminalization (Dills, Goffard, and Miron, 2017), the minimum legal drinking age (Crost and Rees, 2013), youth cohort size (Jacobson, 2004), high school graduation requirements (Hao and Cowan, 2019), and state education requirements for substance use prevention (Carpenter et al., 2019).

To our knowledge, only a handful of papers have estimated the relationship between cigarette taxes and youth marijuana use. However, with one exception, these papers do not exploit within-state changes in the cigarette tax, leaving their estimates potentially biased due to unobserved factors at the state level, such as preferences and attitudes (Pacula, 1998a, 1998b; Chaloupka et al., 1999).9 The exception is Farrelly et al. (2001), who use data from the National Household Survey on Drug Abuse (NHSDA) for the period 1990–1996. These authors find that higher cigarette taxes are associated with decreases in the intensity of marijuana use among individuals 12–20 years of age and may also lead to modest reductions in the probability of use among similarly aged males.

D. Contributions

Our research makes a number of important contributions. First, the estimated cigarette tax effects we present below are based on more policy variation than was used by any previous study on youth cigarette or marijuana use. We extend the panel observed in Hansen, Sabia, and Rees (2017) by adding the two most recent waves of YRBS data (i.e., 2015 and 2017). Between 2013 and 2017, 17 states and the District of Columbia increased their per-pack tax on cigarettes10 and many of these increases were substantial. For instance, California increased its cigarette tax in 2017 by over 200 percent from $0.87 to $2.87. To take another example, Nevada increased its cigarette tax in 2016 from $0.80 to $1.80. Even some historically low-tax states have passed large tax increases in recent years. In 2016, Louisiana increased its tax from $0.36 to $1.08. Moreover, during the period 2013–2017, the first federally funded anti-smoking campaign was implemented and the use of e-cigarettes among teens surged (Centers for Disease Control and Prevention, 2016; Surgeon General, 2019).

Second, given the years we observe, we can compare estimated effects for the pre- and post-2005 periods, when cigarette taxes have been shown to have more and less bite, respectively (Hansen, Sabia, and Rees, 2017). Third, because Farrelly et al. (2001) use data from over two decades ago, we believe a fresh investigation of the relationship between state cigarette taxes and youth marijuana use is needed. Finally, between 2010 and 2017, 7 states (CA, KS, LA, MN, NC, PA, and WV) and the District of Columbia passed e-cigarette taxes. To our knowledge, this paper is the first to estimate the relationship between e-cigarette taxes and youth marijuana use.

III. DATA AND EMPIRICAL STRATEGY

A. YRBS Data

Our data come from the National and State YRBS for the period 1991–2017 and are repeated cross-sectional in nature.11 These data are used by government agencies to follow trends in the behaviors of high school students, including physical activity, unhealthy eating, suicidality, violence, sexual activity, and the use of tobacco, alcohol, and illicit substances. The National YRBS are carried out biennially by the Centers for Disease Control and Prevention (CDC), while the State YRBS are coordinated by the CDC and administered by state education and health agencies.12 The National and State YRBS generally mirror each other in terms of content, and it has become commonplace for researchers to pool these two data sources.13 Pooling the National and State YRBS ensures that identification is based off of as many state-level changes in the cigarette tax as possible (Appendix Tables 1 and 2). In odd years from 1991 to 2017, we observe 9 states increasing their cigarette tax once, 13 states increasing their tax twice, 5 states increasing their tax three times, and 23 states and the District of Columbia increasing their tax four or more times.14

Our initial analysis focuses on the same outcomes explored by Carpenter and Cook (2008) and Hansen, Sabia, and Rees (2017). Specifically, YRBS respondents were asked:

“During the past 30 days, on how many days did you smoke cigarettes?”

Current Cigarette User is set equal to 1 if a student reported smoking cigarettes at least once during the past 30 days, and set equal to 0 otherwise. We set the variable Frequent Cigarette User as equal to 1 if a student reported smoking cigarettes during at least 20 of the past 30 days, and set equal to 0 otherwise.15

Regarding marijuana use, YRBS respondents were asked:

“During the past 30 days, how many times did you use marijuana?”

Current Marijuana User is set equal to 1 if a student reported smoking marijuana at least once during the past 30 days, and set equal to 0 otherwise. We set the variable Frequent Marijuana User as equal to 1 if a student reported smoking marijuana at least 20 times during the past 30 days, and set equal to 0 otherwise.16

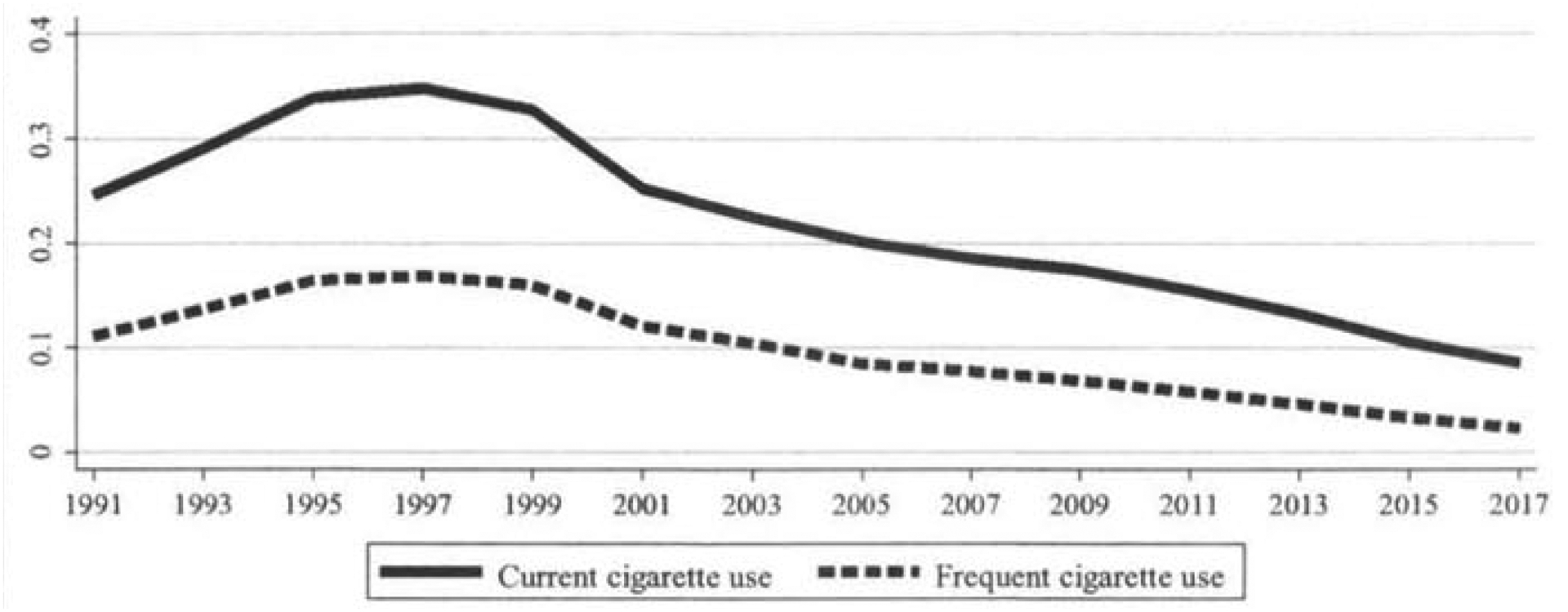

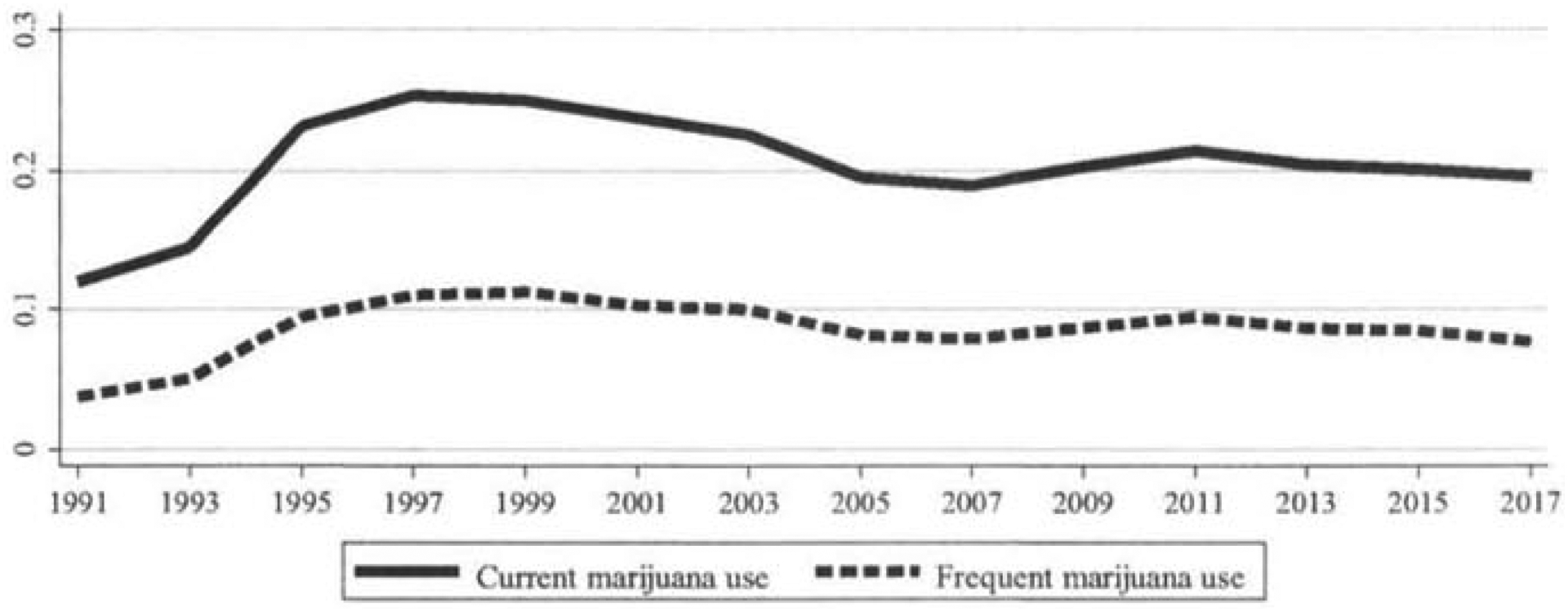

On average, we find that 17.9 percent and 7.5 percent of high school students reported current and frequent cigarette use, respectively (Table 1). Teen cigarette use increased from 1991 to 1997 but has been steadily declining since (Figure 2). YRBS respondents reported current and frequent marijuana use rates of 19.8 percent and 8.3 percent, respectively. While teen marijuana use also increased at the beginning of our sample period, it has stayed relatively constant since 1997 (Figure 3).17

Table 1.

Descriptive Statistics

| Mean | Description | |

|---|---|---|

| Dependent variables | ||

| Current Cigarette User | 0.179 | = 1 if respondent reported smoking cigarettes during at least one of the past 30 days, = 0 otherwise |

| Frequent Cigarette User | 0.075 | = 1 if respondent reported smoking cigarettes during at least 20 of the past 30 days, = 0 otherwise |

| Current Marijuana User | 0.198 | = 1 if respondent reported smoking marijuana at least once in the past 30 days, = 0 otherwise |

| Frequent Marijuana User | 0.083 | = 1 if respondent reported smoking marijuana at least 20 times during the past 30 days, = 0 otherwise |

| Independent variables | ||

| Cigarette Tax | 2.27 | State per-pack cigarette tax (2017 dollars) |

| Any E-Cigarette Tax | 0.008 | = 1 if state has an e-cigarette tax, = 0 otherwise |

| Clean Indoor Air Law | 0.379 | = 1 if state has banned smoking in workplaces/restaurants/bars, = 0 otherwise |

| MML | 0.344 | = 1 if state has a legalized medical marijuana, = 0 otherwise |

| RML | 0.013 | = 1 if state has a legalized recreational marijuana, = 0 otherwise |

| Decriminalization | 0.331 | = 1 if state has decriminalized marijuana, = 0 otherwise |

| Beer Tax | 0.322 | State beer tax per gallon (2017 dollars) |

| BAC 0.08 Law | 0.829 | = 1 if state has a 0.08 BAC law, = 0 otherwise |

| Income | 10.7 | Natural log of state per capita income (2017 dollars) |

| Unemployment | 5.66 | State unemployment rate |

| Male | 0.482 | = 1 if respondent is male, = 0 otherwise |

| Gender Missing | 0.005 | = 1 if information on gender is missing, = 0 otherwise |

| Age 14 or Younger | 0.136 | = 1 if respondent is 14 years of age or younger, = 0 otherwise |

| Age 15 | 0.255 | = 1 if respondent is 15 years of age, = 0 otherwise |

| Age 16 | 0.260 | = 1 if respondent is 16 years of age, = 0 otherwise |

| Age 17 | 0.226 | = 1 if respondent is 17 years of age, = 0 otherwise |

| Age 18 or Older | 0.114 | = 1 if respondent is 18 years of age or older, = 0 otherwise |

| Age Missing | 0.009 | = 1 if information on age is missing, = 0 otherwise |

| 9th Grade | 0.274 | = 1 if respondent is in 9th grade, = 0 otherwise |

| 10th Grade | 0.262 | = 1 if respondent is in 10th grade, = 0 otherwise |

| 11th Grade | 0.240 | = 1 if respondent is in 11th grade, = 0 otherwise |

| 12th Grade | 0.202 | = 1 if respondent is in 12th grade, = 0 otherwise |

| Grade Missing | 0.022 | = 1 if information on grade is missing, = 0 otherwise |

| Non-Hispanic White | 0.573 | = 1 if respondent is non-Hispanic white, = 0 otherwise |

| Black | 0.133 | = 1 if respondent is black, = 0 otherwise |

| Hispanic | 0.150 | = 1 if respondent is Hispanic, = 0 otherwise |

| Other Race/Ethnicity | 0.109 | = 1 if respondent is an “other” race/ethnicity, = 0 otherwise |

| Race/Ethnicity Missing | 0.034 | = 1 if information on race/ethnicity is missing, = 0 otherwise |

| N = 1,463,998 |

Note: Means are based on unweighted data from the National and State YRBS for the period 1991–2017.

Figure 2.

Teen Cigarette Use, 1991–2017

Note: Based on unweighted data from the National and State YRBS for the period 1991–2017.

Figure 3.

Teen Marijuana Use, 1991–2017

Note: Based on unweighted data from the National and State YRBS for the period 1991–2017.

B. Empirical Strategy

To estimate the relationship between cigarette taxes and youth smoking behaviors, and to control for economic conditions and other policies (as well as any changes in the composition of YRBS respondents), we call upon a difference-in-differences framework. Specifically, our estimating equation is

| (1) |

where i indexes individuals, s indexes states, and t indexes years. The dependent variable, Yist, represents one of the four possible outcomes listed in Table 1 (Current Cigarette User, Frequent Cigarette User, Current Marijuana User, and Frequent Marijuana User). Following Carpenter and Cook (2008) and Hansen, Sabia, and Rees (2017), we estimate Equation (1) as a logit model. The variable of interest, Cigarette Tax, is equal to the per-pack excise tax on cigarettes (in 2017 dollars) in state s during year t.18 The vectors vs and wt represent state and year fixed effects, respectively. One advantage of using the combined National and State YRBS data set is that it often contains thousands of individuals per state-year. If we observed small state-year cell sizes, a concern would be our ability to generate consistent parameter estimates from a logit model that includes state and year fixed effects. In all regressions, we correct our standard errors for clustering at the state level (Bertrand, Duflo, and Mullainathan, 2004).

The vector X1ist includes individual-level controls for gender, age, grade, and race/ethnicity,19 while X2st includes state-level controls for whether the state taxes e-cigarettes (Any E-Cigarette Tax),20 the presence of a clean indoor air law (Clean Indoor Air Law),21 marijuana policies (MML, RML, and Decriminalization),22 alcohol policies (Beer Tax and BAC 0.08 Law),23 and economic conditions (Income and Unemployment). Table 1 provides means and definitions for the variables included in X1ist and X2st. Appendix Table 3 lists the data sources for the state-level covariates.

IV. RESULTS

A. Cigarette Taxes and Youth Cigarette Use

We begin by documenting the relationship between state excise taxes on cigarettes and youth cigarette consumption. Table 2 presents estimates of the relationship between cigarette taxes and youth cigarette use for the period 1991–2017. Without controlling for the individual- or state-level covariates listed in Table 1, the estimated coefficient on Cigarette Tax implies that a one-dollar tax increase (in 2017 dollars) is associated with a 1-percentage-point decrease in the likelihood a YRBS respondent reported smoking cigarettes at least once during the past 30 days (i.e., our definition of “current” cigarette use), and this estimate is statistically significant at the 1 percent level. In Column (2), the estimated effect falls slightly when we add the individual-level controls for gender, age, grade, and race/ethnicity. When adding the state-level controls for other policies and economic conditions (Column (3)), our estimate of β1 falls further to −0.006 but remains statistically significant at the 5 percent level.

Table 2.

Cigarette Taxes and Youth Cigarette Use, 1991–2017

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Current Cigarette User | Current Cigarette User | Current Cigarette User | Frequent Cigarette User | Frequent Cigarette User | Frequent Cigarette User | |

| Cigarette Tax | −0.010*** (0.002) | −0.008*** (0.003) | −0.006** (0.002) | −0.007*** (0.002) | −0.006*** (0.002) | −0.005*** (0.001) |

| Mean | 0.179 | 0.179 | 0.179 | 0.075 | 0.075 | 0.075 |

| Individual-level covariates | No | Yes | Yes | No | Yes | Yes |

| State-level covariates | No | No | Yes | No | No | Yes |

Notes: Each column represents an average marginal effect from a logit regression based on data from the YRBS for the period 1991–2017. The individual- and state-level covariates are listed in Table 1. All models control for state fixed effects and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. N = 1,463,998. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

In Columns (4)–(6), we replace Current Cigarette User with Frequent Cigarette User and re-estimate Equation (1). When controlling for individual- and state-level covariates, the estimated coefficient on Cigarette Tax suggests that a one-dollar increase in the tax is associated with a 0.5-percentage-point decrease in the likelihood a high school student reported smoking cigarettes during at least 20 of the past 30 days.

The estimates in Columns (3) and (6) of Table 2 imply semi-elasticities of −3.4 and −6.7, respectively. That is, a one-dollar increase in the cigarette tax is associated with a 3.4 percent reduction in the likelihood of current cigarette use and a 6.7 percent reduction in the likelihood of frequent cigarette use.

In Appendix Table 4, we present estimates for the years 1991–2005 and 2007–2017, separately. Consistent with Hansen, Sabia, and Rees (2017), we find that our estimates for the full sample period are driven by the earlier cigarette tax hikes and that tax increases for more recent years have no observable bite.24 Estimated cigarette tax effects by gender, race, and age tell a similar story (Appendix Tables 5 and 6). Across all subgroups, there is evidence that tax increases were only effective at reducing teen cigarette use during the earlier years of our sample period. These results are consistent with the notion that continually rising tax rates have prompted price-sensitive youths to quit smoking, leaving only price-insensitive youths in the market (Courtemanche and Feng, 2019). Hansen, Sabia, and Rees (2017, p. 73) conclude that the post-2005 cohorts include more “hardcore” teens whose “smoking decisions are insensitive to cost.”

B. Cigarette Taxes and Youth Marijuana Use

Table 3 presents estimates on the relationship between state cigarette taxes and teen marijuana use. In general, we find little evidence to support the notion that teen marijuana use is sensitive to changes in the cigarette tax. The estimated coefficient on Cigarette Tax is uniformly positive in sign but small in magnitude and, with one exception, statistically indistinguishable from zero. Ninety-five percent confidence intervals around the estimates of β1 suggest that the effect of a one-dollar cigarette tax increase on current marijuana use is no larger than 1.1 percentage points and the effect of a one-dollar tax increase on frequent marijuana use is no larger than 0.5 percentage points.25

Table 3.

Cigarette Taxes and Youth Marijuana Use, 1991–2017

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Current Marijuana User | Current Marijuana User | Current Marijuana User | Frequent Marijuana User | Frequent Marijuana User | Frequent Marijuana User | |

| Cigarette Tax | 0.004* (0.002) | 0.003 (0.004) | 0.005 (0.003) | 0.002 (0.001) | 0.001 (0.002) | 0.002 (0.001) |

| Mean | 0.198 | 0.198 | 0.198 | 0.083 | 0.083 | 0.083 |

| Individual-level covariates | No | Yes | Yes | No | Yes | Yes |

| State-level covariates | No | No | Yes | No | No | Yes |

Notes: Each column represents an average marginal effect from a logit regression based on data from the YRBS for the period 1991–2017. The individual- and state-level covariates are listed in Table 1. All models control for state fixed effects and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. N = 1,463,998. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

In Table 4, we present estimates separately for the years 1991–2005 and 2007–2017. While the sign on the estimated relationship between cigarette taxes and teen marijuana use becomes negative when we restrict our focus to the years 1991–2005, it remains small in magnitude and statistically insignificant. Furthermore, our estimates for frequent marijuana use stand in contrast to those presented in Farrelly et al. (2001), who find that higher cigarette taxes are associated with decreases in the intensity of marijuana use among 12- to 20-year-old NHSDA respondents for the period 1990–1996.26 Not surprisingly, we find no evidence of a relationship between cigarette taxes and marijuana use during the later years of our sample.27

Table 4.

Cigarette Taxes and Youth Marijuana Use, 1991–2005 versus 2007–2017

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| 1991–2005 | 2007–2017 | 1991–2005 | 2007–2017 | |

| Current Marijuana User | Current Marijuana User | Frequent Marijuana User | Frequent Marijuana User | |

| Cigarette Tax | −0.008 (0.008) | 0.005 (0.003) | −0.003 (0.004) | 0.002 (0.002) |

| Mean | 0.205 | 0.194 | 0.080 | 0.085 |

| N | 528,417 | 935,581 | 528,417 | 935,581 |

Notes: Each column represents an average marginal effect from a logit regression based on data from the YRBS for the indicated period. All models control for the covariates listed in Table 1, state fixed effects, and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

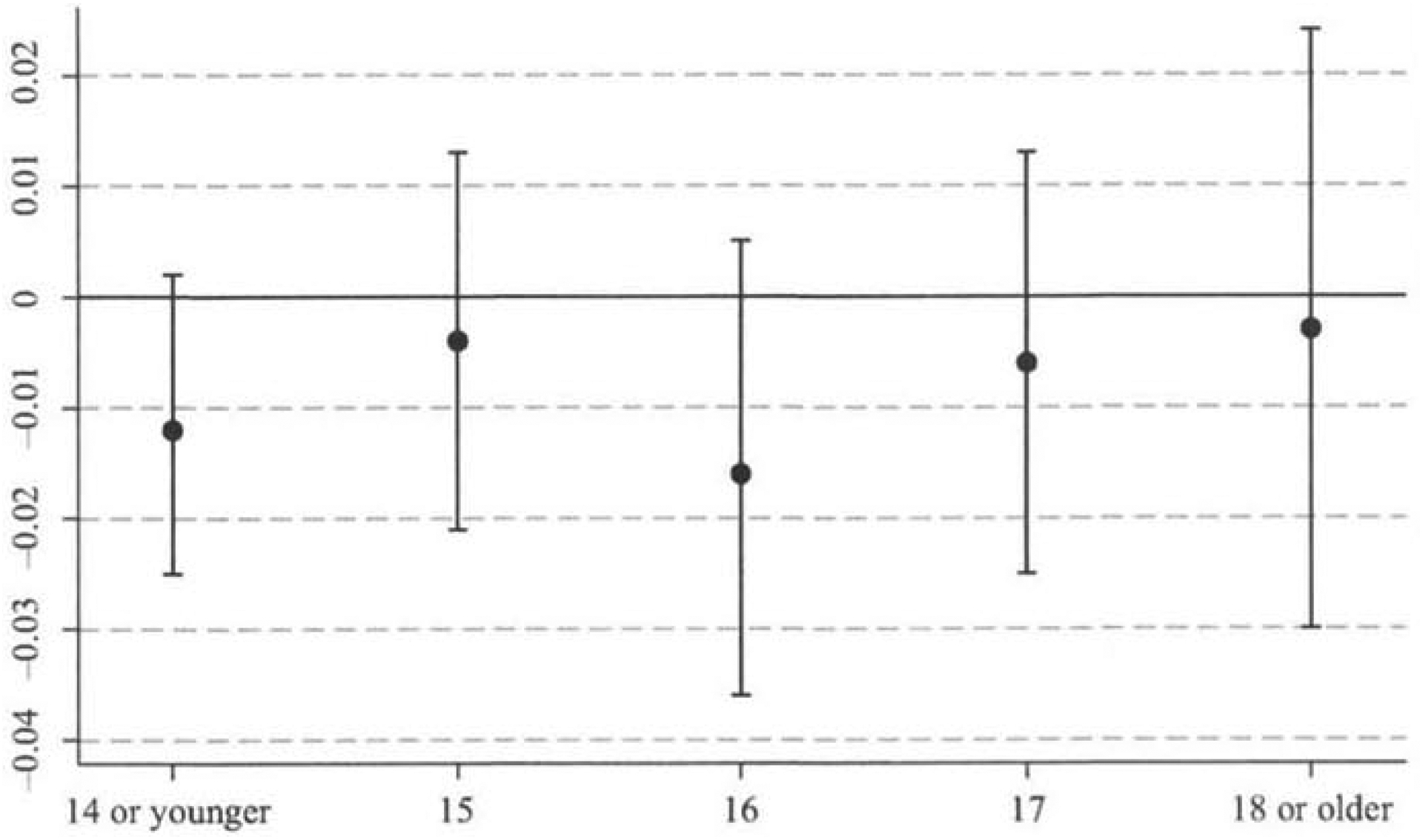

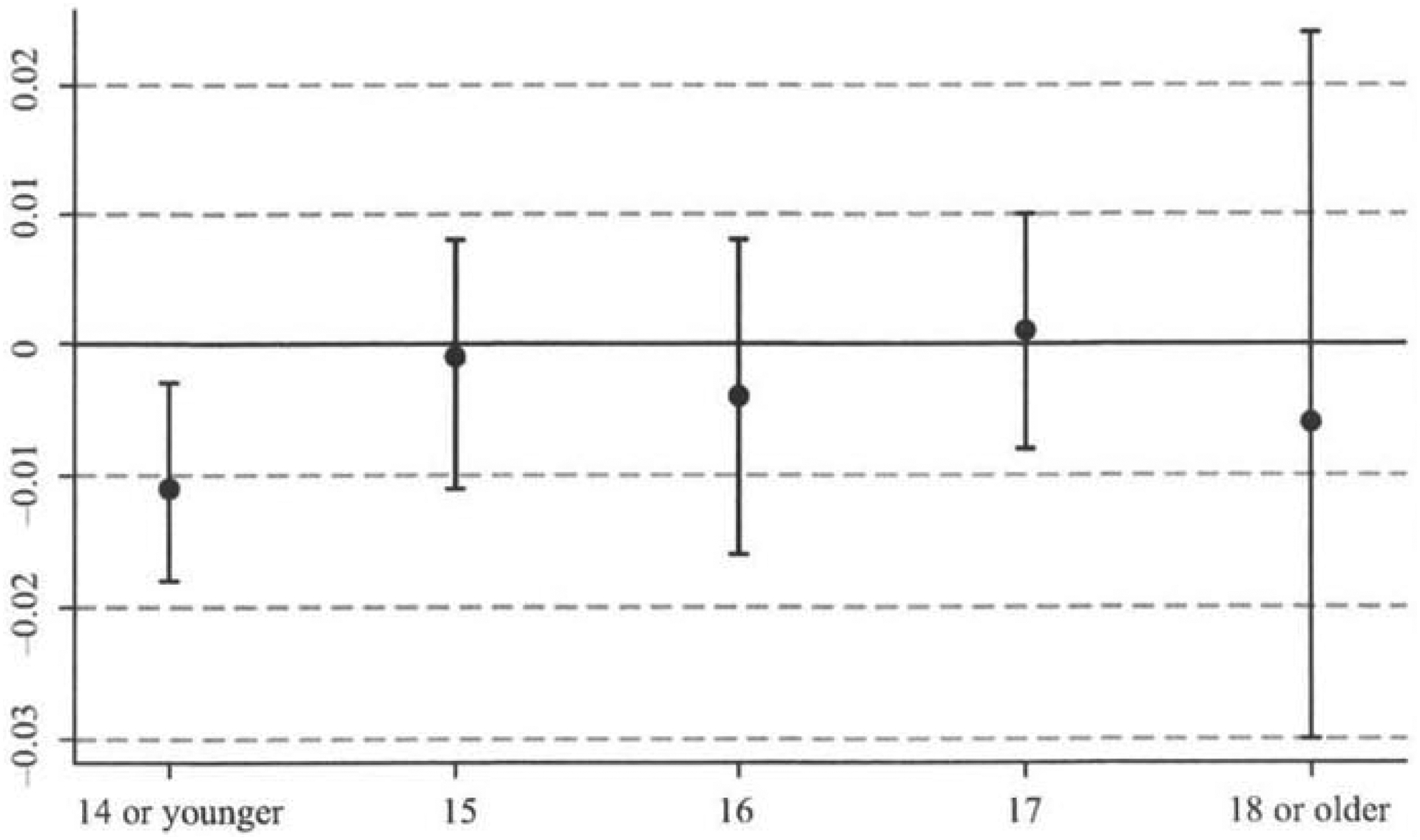

Table 5 shows estimates on the relationship between cigarette taxes and marijuana use by gender and race for the period 1991–2005. While it is worth noting that all estimates are negative in sign, which is consistent with a story of complementarity, none are statistically significant at conventional levels. Figures 4 and 5 show coefficient estimates on Current Marijuana User and Frequent Marijuana User, respectively, by age for the period 1991–2005. With one exception, these estimates are also statistically indistinguishable from zero. The lone statistically significant estimate provides some evidence that cigarette taxes are negatively associated with frequent marijuana use among respondents 14 years of age or younger. Taken together, the results in Tables 3–5 and Figures 4 and 5 suggest that teen marijuana use is generally insensitive to changes in the state cigarette tax.28

Table 5.

Cigarette Taxes and Youth Marijuana Use by Gender and Race, 1991–2005

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Males | Females | White | Non-White | |||||

| Current Marijuana User | Frequent Marijuana User | Current Marijuana User | Frequent Marijuana User | Current Marijuana User | Frequent Marijuana User | Current Marijuana User | Frequent Marijuana User | |

| Cigarette Tax | −0.010 (0.009) | −0.004 (0.005) | −0.006 (0.008) | −0.001 (0.003) | −0.004 (0.006) | −0.002 (0.004) | −0.011 (0.012) | −0.001 (0.007) |

| Mean | 0.233 | 0.113 | 0.178 | 0.06 | 0.199 | 0.082 | 0.209 | 0.089 |

| N | 255,392 | 255,392 | 271,302 | 271,302 | 329,627 | 329,627 | 171,924 | 171,924 |

Notes: Each column represents an average marginal effect from a logit regression based on data from the YRBS for the period 1991–2005. All models control for the covariates listed in Table 1, state fixed effects, and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

Figure 4.

Cigarette Taxes and Current Marijuana Use by Age, 1991–2005

Notes: Average marginal effects (and their 95 percent confidence intervals) come from logit regressions based on data from the YRBS for the period 1991–2005. All models control for the covariates listed in Table 1, state fixed effect and year fixed effects. Standard errors are corrected for clustering at the state level.

Figure 5.

Cigarette Taxes and Frequent Marijuana Use by Age, 1991–2005

Notes: Average marginal effects (and their 95 percent confidence intervals) come from logit regressions based on data from the YRBS for the period 1991–2005. All models control for the covariates listed in Table 1, state fixed effect and year fixed effects. Standard errors are corrected for clustering at the state level.

V. MEDICAL AND RECREATIONAL MARIJUANA LEGALIZATION

In the first two columns of Table 6, we show the estimated coefficients on the variables MML and RML that correspond to the regressions from Columns (3) and (6) of Table 2. The presence of an MML, which Anderson, Hansen, and Rees (2015) find to be consistently negatively associated with marijuana use among YRBS respondents, is associated with reductions in both current and frequent teen cigarette use. Within the context of the findings in Anderson, Hansen, and Rees (2015), our estimates suggest that youths may consume cigarettes and marijuana as complementary goods.29

Table 6.

Marijuana Policies and Youth Cigarette and Marijuana Use, 1991–2017

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Current Cigarette User | Frequent Cigarette User | Current Marijuana User | Frequent Marijuana User | |

| Cigarette Tax | −0.006** (0.002) | −0.005*** (0.001) | 0.005 (0.003) | 0.002 (0.001) |

| MML | −0.011** (0.005) | −0.009*** (0.003) | −0.010** (0.005) | −0.006* (0.003) |

| RML | −0.006 (0.008) | −0.001 (0.010) | −0.009** (0.004) | −0.004 (0.004) |

| Mean | 0.179 | 0.075 | 0.198 | 0.083 |

Notes: Each column represents average marginal effects from a logit regression based on data from the YRBS for the period 1991–2017. All models control for the covariates listed in Table 1, state fixed effects, and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. N = 1,463,998. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

In the last two columns of Table 6, we show the estimated coefficients on the variables MML and RML that correspond to the regressions from Columns (3) and (6) of Table 3. The legalization of marijuana, whether for medical or recreational purposes, is negatively associated with teen marijuana use. These results are consistent with the findings in Anderson, Hansen, and Rees (2015) and Anderson et al. (2019) and the argument that it is more difficult for teenagers to obtain marijuana as drug dealers are replaced by licensed dispensaries that require customers to be 21 years of age.

VI. PRELIMINARY ANALYSIS OF E-CIGARETTE TAXES

An emerging literature has examined the determinants of teen e-cigarette use and whether policies that raise the costs of accessing e-cigarettes have unintended spillover effects on youth tobacco consumption. Using data from Monitoring the Future and exploiting within-market variation in e-cigarette prices, Pesko et al. (2018) find that a 10 percent increase in the price of e-cigarette disposables is associated with an 18 percent decrease in the average number of vaping days reported by students.30 To our knowledge, no prior study has estimated the effect of e-cigarette taxes on teen e-cigarette or traditional cigarette use.

The literature on the relationship between state-level e-cigarette laws and traditional cigarette use among teens has produced mixed findings. For instance, using data from the National Survey of Drug Use and Health, Friedman (2015) finds that state bans on e-cigarette sales to minors are associated with an increase in recent cigarette smoking among 12- to 17-year-olds, consistent with the hypothesis that e-cigarettes and traditional cigarettes are substitutes. On the other hand, using Monitoring the Future data, Abouk and Adams (2017) find that e-cigarette sales bans are associated with reductions in cigarette smoking among U.S. high school seniors.

Only one study of which we are aware has estimated the relationship between e-cigarette policies and marijuana use. Using data from the National YRBS for the period 2007–2013, Pesko, Hughes, and Faisal (2016) find that minimum legal purchase age requirements for electronic nicotine delivery systems are negatively related to teen e-cigarette use, positively related to teen cigarette use, and have no observable effect on teen marijuana use.

In Table 7, we provide exploratory estimates of the effect of state e-cigarette taxes on teen e-cigarette,31 traditional cigarette, and marijuana use. Following Abouk et al. (2019) and Pesko, Courtemanche, and Maclean (2019), we consider a binary indicator for whether state s during year t was enforcing an e-cigarette tax. The choice to use a simple dichotomous variable is due, in large part, to the difficulty in harmonizing magnitudes of excise and ad valorem taxes.32

Table 7.

E-Cigarette Taxes and Youth E-Cigarette, Cigarette, and Marijuana Use

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| 2015–2017 | 1991–2017 | 1991–2017 | ||||

| Current E-Cigarette User | Frequent E-Cigarette User | Current Cigarette User | Frequent Cigarette User | Current Marijuana User | Frequent Marijuana User | |

| Any E-Cigarette | −0.034* (0.019) | −0.008** (0.003) | −0.013 (0.012) | −0.016 (0.011) | −0.013** (0.005) | −0.005 (0.004) |

| Tax | ||||||

| Mean | 0.182 | 0.027 | 0.179 | 0.075 | 0.198 | 0.083 |

| N | 355,677 | 355,677 | 1,463,998 | 1,463,998 | 1,463,998 | 1,463,998 |

Notes: Each column represents an average marginal effect from a logit regression based on data from the YRBS for the indicated period. All models control for the covariates listed in Table 1, state fixed effects, and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

Before reporting our findings, it is important to note limitations. The YRBS only began asking consistent questions about e-cigarette use in 2015, severely limiting the amount of policy variation available to identify e-cigarette consumption effects. While our traditional cigarette and marijuana use effects are identified off of the 7 states (CA, KS, LA, MN, NC, PA, and WV) that enacted e-cigarette taxes between 2010 and 2017, our e-cigarette consumption effects are identified off of only 3 states (CA, PA, and WV).

In the first two columns of Table 7, our results show that the enactment of an e-cigarette tax is associated with a 3.4-percentage-point reduction in current e-cigarette use and a 0.8-percentage-point reduction in frequent e-cigarette use. This result is consistent with the hypothesis that youths are sensitive to changes in the cost of obtaining e-cigarettes.33 We also find some evidence that e-cigarette taxes are negatively related to youth cigarette use, although these estimated effects are not statistically significant. Finally, it appears that e-cigarettes and marijuana may be complements for youths. The enactment of an e-cigarette tax is associated with a 1.3-percentage-point decline in current marijuana use and a (statistically insignificant) 0.5-percentage-point decline in frequent use.34 However, these estimates should be interpreted with caution as they are based on limited post-treatment data and relatively few policy changes.

VII. CONCLUSION

As the legalization of marijuana proliferates throughout the United States, there is a growing concern among policymakers that an increase in adolescent marijuana use will follow.35 In turn, a number of strategies have been proposed to reduce marijuana use among youths. Among these strategies has been a call to reduce youth cigarette consumption, despite the fact that there is scant empirical evidence to suggest that cigarettes and marijuana are complementary (or substitute) goods. State excise taxes on cigarettes are a commonly proposed policy lever to deter youth cigarette use (Chaloupka, Straif, and Leon, 2011; Marr and Huang, 2014; U.S. Department of Health and Human Services, 2014; Truth Initiative, 2019).

Using data from the National and State YRBS for the period 1991–2017, we explore the relationship between state excise taxes on cigarettes and teen marijuana use. In general, we find little evidence to suggest that teen marijuana use is responsive to changes in the state cigarette tax, and this null finding holds when we focus on the period where taxes are observed to have the greatest effect on teen cigarette consumption (i.e., the years 1991–2005). We also find limited evidence of a relationship between state cigarette taxes and marijuana use when we split the sample by gender, race, or age.

In addition to examining state cigarette taxes, we estimate the effect of medical and recreational marijuana legalization on youth cigarette and marijuana use. We find that both state MMLs and RMLs are associated with decreases in teen marijuana consumption, consistent with the hypothesis that selling to minors becomes a relatively risky proposition for licensed marijuana dispensaries. In addition, we find that MMLs are associated with decreases in teen cigarette use.

Finally, we provide the first set of estimates on the relationship between state e-cigarette taxes and teen marijuana use. Specifically, the implementation of an e-cigarette tax is associated with a 7 percent reduction in current marijuana use, which is consistent with the hypothesis that e-cigarettes and marijuana are complementary goods among youths.

Understanding the general equilibrium effects of substance use policies is critical for optimal tax design (Pacula, 1997). Our study contributes along this dimension by showing that cigarette tax hikes in the United States have generally not led to spillover effects on youth marijuana use. Based on our preliminary analysis of state e-cigarette taxes, we believe future research should explore whether longer-run youth marijuana use is sensitive to raising the costs of accessing e-cigarettes.

ACKNOWLEDGMENTS

We thank Thanh Tam Nguyen for useful data assistance and Isaac Baumann for helpful editorial assistance. All errors are our own.

DISCLOSURES

Dr. Anderson has no financial arrangement that might give rise to conflicts of interest with respect to the research reported in this paper. Mr. Matsuzawa acknowledges support received from the Center for Health Economics & Policy Studies (CHEPS) at San Diego State University. Dr. Sabia acknowledges support from the CHEPS at San Diego State University, including grant support received from the Charles Koch Foundation and Troesh Family Foundation.

Appendix Table 1.

Number of YRBS Observations by State-Year, 1991–2017

| 1991 | 1993 | 1995 | 1997 | 1999 | 2001 | 2003 | 2005 | 2007 | 2009 | 2011 | 2013 | 2015 | 2017 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Alabama | 2,304 | 758 | 3,692 | 4,218 | 1,979 | 1,728 | 1,591 | 1,009 | 463 | 2,354 | 1,603 | 1,741 | 1,690 | 0 |

| Alaska | 0 | 0 | 1,578 | 0 | 0 | 0 | 1,380 | 0 | 1,218 | 1,264 | 1,216 | 1,133 | 1,329 | 1,270 |

| Arizona | 0 | 423 | 0 | 1,020 | 0 | 393 | 3,510 | 3,262 | 3,231 | 2,685 | 3,685 | 1,645 | 2,596 | 2,005 |

| Arkansas | 0 | 373 | 2,434 | 2,217 | 1,387 | 1,621 | 270 | 1,414 | 1,863 | 1,796 | 1,257 | 1,659 | 2,491 | 1,453 |

| California | 0 | 1,901 | 626 | 1,853 | 0 | 2,158 | 1,622 | 1,499 | 2,017 | 2,713 | 1,809 | 2,428 | 5,713 | 1,690 |

| Colorado | 0 | 256 | 102 | 258 | 0 | 622 | 0 | 1,422 | 0 | 1,590 | 1,668 | 274 | 263 | 1,365 |

| Connecticut | 0 | 0 | 226 | 1,833 | 0 | 0 | 0 | 2,274 | 1,995 | 2,327 | 1,978 | 2,410 | 2,441 | 2,346 |

| Delaware | 0 | 0 | 209 | 0 | 2,100 | 2,772 | 3,200 | 2,535 | 2,486 | 2,243 | 2,391 | 2,524 | 2,562 | 2,775 |

| District of Columbia | 0 | 0 | 483 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 300 | 0 | 0 | 0 |

| Florida | 0 | 0 | 512 | 650 | 0 | 5,000 | 5,212 | 4,800 | 5,015 | 5,572 | 7,329 | 6,734 | 6,948 | 5,819 |

| Georgia | 2,128 | 2,405 | 414 | 319 | 0 | 466 | 2,287 | 3,316 | 2,566 | 2,981 | 1,849 | 2,120 | 331 | 0 |

| Hawaii | 0 | 1,486 | 1,181 | 1,339 | 1,190 | 0 | 0 | 1,601 | 1,138 | 1,640 | 3,972 | 4,536 | 5,763 | 5,686 |

| Idaho | 4,009 | 3,862 | 0 | 0 | 0 | 1,756 | 1,645 | 1,595 | 1,337 | 2,058 | 1,893 | 2,077 | 2,025 | 1,765 |

| Illinois | 0 | 4,054 | 3,089 | 0 | 0 | 411 | 297 | 458 | 2,794 | 4,158 | 4,141 | 3,576 | 3,818 | 4,495 |

| Indiana | 0 | 0 | 0 | 0 | 0 | 171 | 1,949 | 1,620 | 2,586 | 1,440 | 2,940 | 815 | 2,005 | 0 |

| Iowa | 0 | 0 | 241 | 2,206 | 0 | 0 | 0 | 1,551 | 1,645 | 0 | 1,495 | 0 | 0 | 1,590 |

| Kansas | 0 | 167 | 0 | 200 | 0 | 0 | 290 | 1,850 | 1,629 | 2,131 | 2,057 | 2,023 | 0 | 2,305 |

| Kentucky | 0 | 0 | 333 | 1,393 | 0 | 0 | 1,482 | 3,575 | 3,569 | 1,619 | 1,785 | 2,164 | 2,380 | 1,870 |

| Louisiana | 0 | 0 | 719 | 543 | 0 | 0 | 641 | 143 | 1,203 | 1,326 | 1,014 | 950 | 0 | 1,029 |

| Maine | 0 | 239 | 1,499 | 1,978 | 0 | 1,462 | 1,754 | 1,281 | 1,251 | 8,272 | 8,926 | 8,083 | 8,717 | 8,776 |

| Maryland | 0 | 140 | 0 | 752 | 0 | 0 | 250 | 1,335 | 1,390 | 1,493 | 2,398 | 48,628 | 52,183 | 47,723 |

| Massachusetts | 0 | 3,460 | 4,235 | 5,300 | 4,186 | 252 | 209 | 251 | 3,617 | 2,540 | 2,864 | 2,648 | 3,300 | 3,156 |

| Michigan | 0 | 137 | 1,050 | 4,096 | 2,538 | 3,611 | 3,551 | 3,330 | 3,548 | 3,429 | 4,531 | 4,465 | 4,722 | 1,551 |

| Minnesota | 0 | 315 | 0 | 0 | 0 | 0 | 0 | 93 | 0 | 185 | 0 | 297 | 739 | 0 |

| Mississippi | 0 | 1,682 | 1,674 | 1,706 | 1,461 | 2,010 | 1,417 | 0 | 1,811 | 1,694 | 1,807 | 2,017 | 1,841 | 0 |

| Missouri | 0 | 178 | 5,200 | 1,405 | 1,588 | 2,047 | 1,754 | 1,912 | 1,821 | 1,634 | 339 | 1,802 | 1,577 | 1,757 |

| Montana | 0 | 2,406 | 2,422 | 2,348 | 2,782 | 2,669 | 2,533 | 2,856 | 3,774 | 1,721 | 3,902 | 4,632 | 4,286 | 4,581 |

| Nebraska | 2,295 | 3,503 | 0 | 0 | 0 | 0 | 2,607 | 3,490 | 0 | 0 | 2,583 | 1,677 | 1,564 | 1,341 |

| Nevada | 0 | 1,954 | 1,484 | 1,407 | 1,633 | 1,602 | 1,885 | 1,460 | 1,713 | 2,346 | 190 | 1,961 | 1,768 | 1,582 |

| New Hampshire | 0 | 2,590 | 2,043 | 0 | 0 | 0 | 1,281 | 1,246 | 1,610 | 1,472 | 1,395 | 1,597 | 14,466 | 11,792 |

| New Jersey | 0 | 0 | 0 | 678 | 0 | 2,119 | 284 | 1,747 | 666 | 2,171 | 1,709 | 1,996 | 206 | 0 |

| New Mexico | 2,770 | 640 | 0 | 260 | 0 | 143 | 95 | 5,064 | 2,604 | 5,175 | 5,351 | 5,027 | 8,131 | 5,436 |

| New York | 0 | 478 | 270 | 3,920 | 3,217 | 302 | 9,600 | 9,328 | 13,304 | 14,535 | 12,899 | 10,193 | 9,897 | 10,367 |

| North Carolina | 0 | 2,633 | 1,801 | 310 | 0 | 3,039 | 2,412 | 4,356 | 3,878 | 5,436 | 3,228 | 2,144 | 5,787 | 3,035 |

| North Dakota | 0 | 0 | 1,462 | 0 | 1,753 | 1,496 | 1,562 | 1,629 | 1,654 | 1,763 | 1,832 | 1,888 | 2,061 | 2,099 |

| Ohio | 0 | 2,894 | 538 | 2,608 | 1,997 | 220 | 1,402 | 267 | 2,396 | 0 | 1,310 | 1,585 | 226 | 0 |

| Oklahoma | 0 | 0 | 0 | 213 | 0 | 387 | 1,313 | 1,872 | 2,790 | 1,356 | 1,112 | 1,428 | 1,923 | 1,552 |

| Oregon | 0 | 185 | 0 | 0 | 0 | 181 | 0 | 269 | 0 | 243 | 0 | 0 | 0 | 0 |

| Pennsylvania | 0 | 346 | 635 | 258 | 0 | 0 | 314 | 393 | 209 | 3,041 | 419 | 259 | 3,193 | 3,518 |

| Rhode Island | 0 | 0 | 0 | 1,440 | 0 | 1,307 | 1,715 | 2,226 | 2,025 | 2,980 | 3,649 | 2,284 | 3,848 | 2,039 |

| South Carolina | 5,284 | 4,394 | 5,135 | 5,585 | 4,227 | 0 | 837 | 1,459 | 1,133 | 1,009 | 1,301 | 1,487 | 1,250 | 1,234 |

| South Dakota | 1,289 | 1,303 | 1,137 | 1,517 | 1,608 | 1,441 | 1,961 | 1,480 | 1,478 | 2,031 | 1,453 | 1,231 | 1,211 | 0 |

| Tennessee | 0 | 3,603 | 0 | 543 | 0 | 575 | 1,843 | 1,863 | 2,133 | 2,146 | 2,794 | 1,713 | 378 | 1,889 |

| Texas | 0 | 1,285 | 1,171 | 892 | 0 | 8,481 | 2,446 | 5,535 | 4,394 | 4,662 | 5,482 | 3,287 | 1,183 | 1,980 |

| Utah | 4,381 | 4,233 | 3,165 | 1,346 | 1,445 | 1,021 | 1,558 | 1,720 | 2,050 | 1,516 | 1,629 | 2,111 | 0 | 1,755 |

| Vermont | 0 | 8,319 | 6,817 | 8,134 | 8,713 | 9,019 | 8,147 | 9,115 | 8,232 | 11,183 | 8,356 | 0 | 20,162 | 20,015 |

| Virginia | 0 | 0 | 62 | 0 | 0 | 0 | 232 | 340 | 422 | 97 | 1,529 | 7,449 | 4,872 | 3,554 |

| Washington | 0 | 375 | 83 | 102 | 0 | 47 | 0 | 106 | 0 | 246 | 164 | 196 | 100 | 0 |

| West Virginia | 0 | 3,000 | 1,988 | 1,747 | 1,278 | 258 | 1,645 | 1,517 | 1,555 | 1,967 | 2,307 | 1,720 | 1,743 | 1,460 |

| Wisconsin | 0 | 3,143 | 0 | 1,533 | 1,287 | 2,224 | 2,164 | 2,431 | 2,166 | 3,024 | 3,513 | 2,715 | 0 | 1,966 |

| Wyoming | 0 | 0 | 1,626 | 1,931 | 1,569 | 2,669 | 1,500 | 2,283 | 1,988 | 2,639 | 2,277 | 2,796 | 2,245 | 0 |

Appendix Table 2.

State Nominal Per-Pack Cigarette Tax Rate, 1991–2017

| 1991 | 1993 | 1995 | 1997 | 1999 | 2001 | 2003 | 2005 | 2007 | 2009 | 2011 | 2013 | 2015 | 2017 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Alabama | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.43 | 0.43 | 0.43 | 0.43 | 0.43 | 0.43 | 0.68 |

| Alaska | 0.29 | 0.29 | 0.29 | 0.29 | 1.00 | 1.00 | 1.00 | 1.60 | 1.80 | 2.00 | 2.00 | 2.00 | 2.00 | 2.00 |

| Arizona | 0.15 | 0.18 | 0.18 | 0.58 | 0.58 | 0.58 | 1.18 | 1.18 | 2.00 | 2.00 | 2.00 | 2.00 | 2.00 | 2.00 |

| Arkansas | 0.21 | 0.22 | 0.32 | 0.32 | 0.32 | 0.32 | 0.59 | 0.59 | 0.59 | 1.15 | 1.15 | 1.15 | 1.15 | 1.15 |

| California | 0.35 | 0.35 | 0.37 | 0.37 | 0.87 | 0.87 | 0.87 | 0.87 | 0.87 | 0.87 | 0.87 | 0.87 | 0.87 | 2.87 |

| Colorado | 0.20 | 0.20 | 0.20 | 0.20 | 0.20 | 0.20 | 0.20 | 0.84 | 0.84 | 0.84 | 0.84 | 0.84 | 0.84 | 0.84 |

| Connecticut | 0.40 | 0.45 | 0.47 | 0.50 | 0.50 | 0.50 | 1.51 | 1.51 | 1.51 | 2.00 | 3.00 | 3.40 | 3.40 | 3.90 |

| Delaware | 0.14 | 0.24 | 0.24 | 0.24 | 0.24 | 0.24 | 0.24 | 0.55 | 0.55 | 1.15 | 1.60 | 1.60 | 1.60 | 1.60 |

| District of Columbia | 0.17 | 0.50 | 0.65 | 0.65 | 0.65 | 0.65 | 1.00 | 1.00 | 1.00 | 2.00 | 2.50 | 2.86 | 2.90 | 2.92 |

| Florida | 0.24 | 0.34 | 0.34 | 0.34 | 0.34 | 0.34 | 0.34 | 0.34 | 0.34 | 0.34 | 1.34 | 1.34 | 1.34 | 1.34 |

| Georgia | 0.12 | 0.12 | 0.12 | 0.12 | 0.12 | 0.12 | 0.12 | 0.37 | 0.37 | 0.37 | 0.37 | 0.37 | 0.37 | 0.37 |

| Hawaii | 0.38 | 0.48 | 0.60 | 0.60 | 1.00 | 1.00 | 1.30 | 1.40 | 1.60 | 2.00 | 3.00 | 3.20 | 3.20 | 3.20 |

| Idaho | 0.18 | 0.18 | 0.18 | 0.28 | 0.28 | 0.28 | 0.57 | 0.57 | 0.57 | 0.57 | 0.57 | 0.57 | 0.57 | 0.57 |

| Illinois | 0.30 | 0.30 | 0.44 | 0.44 | 0.58 | 0.58 | 0.98 | 0.98 | 0.98 | 0.98 | 0.98 | 1.98 | 1.98 | 1.98 |

| Indiana | 0.16 | 0.16 | 0.16 | 0.16 | 0.16 | 0.16 | 0.56 | 0.56 | 0.56 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Iowa | 0.31 | 0.36 | 0.36 | 0.36 | 0.36 | 0.36 | 0.36 | 0.36 | 1.36 | 1.36 | 1.36 | 1.36 | 1.36 | 1.36 |

| Kansas | 0.24 | 0.24 | 0.24 | 0.24 | 0.24 | 0.24 | 0.79 | 0.79 | 0.79 | 0.79 | 0.79 | 0.79 | 0.79 | 1.29 |

| Kentucky | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 | 0.30 | 0.30 | 0.60 | 0.60 | 0.60 | 0.60 | 0.60 |

| Louisiana | 0.16 | 0.20 | 0.20 | 0.20 | 0.20 | 0.24 | 0.36 | 0.36 | 0.36 | 0.36 | 0.36 | 0.36 | 0.36 | 1.08 |

| Maine | 0.31 | 0.37 | 0.37 | 0.37 | 0.74 | 0.74 | 1.00 | 1.00 | 2.00 | 2.00 | 2.00 | 2.00 | 2.00 | 2.00 |

| Maryland | 0.13 | 0.36 | 0.36 | 0.36 | 0.36 | 0.66 | 1.00 | 1.00 | 1.00 | 2.00 | 2.00 | 2.00 | 2.00 | 2.00 |

| Massachusetts | 0.26 | 0.26 | 0.51 | 0.51 | 0.76 | 0.76 | 1.51 | 1.51 | 1.51 | 2.51 | 2.51 | 2.51 | 3.51 | 3.51 |

| Michigan | 0.25 | 0.25 | 0.75 | 0.75 | 0.75 | 0.75 | 1.25 | 2.00 | 2.00 | 2.00 | 2.00 | 2.00 | 2.00 | 2.00 |

| Minnesota | 0.38 | 0.43 | 0.48 | 0.48 | 0.48 | 0.48 | 0.48 | 0.48 | 1.49 | 1.56 | 1.58 | 1.60 | 3.43 | 3.59 |

| Mississippi | 0.18 | 0.18 | 0.18 | 0.18 | 0.18 | 0.18 | 0.18 | 0.18 | 0.18 | 0.68 | 0.68 | 0.68 | 0.68 | 0.68 |

| Missouri | 0.13 | 0.13 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 |

| Montana | 0.18 | 0.18 | 0.18 | 0.18 | 0.18 | 0.18 | 0.70 | 1.70 | 1.70 | 1.70 | 1.70 | 1.70 | 1.70 | 1.70 |

| Nebraska | 0.27 | 0.27 | 0.34 | 0.34 | 0.34 | 0.34 | 0.64 | 0.64 | 0.64 | 0.64 | 0.64 | 0.64 | 0.64 | 0.64 |

| Nevada | 0.35 | 0.35 | 0.35 | 0.35 | 0.35 | 0.35 | 0.35 | 0.80 | 0.80 | 0.80 | 0.80 | 0.80 | 0.80 | 1.80 |

| New Hampshire | 0.21 | 0.25 | 0.25 | 0.25 | 0.37 | 0.52 | 0.52 | 0.52 | 0.80 | 1.33 | 1.78 | 1.68 | 1.78 | 1.78 |

| New Jersey | 0.27 | 0.40 | 0.40 | 0.40 | 0.80 | 0.80 | 1.50 | 2.40 | 2.58 | 2.58 | 2.70 | 2.70 | 2.70 | 2.70 |

| New Mexico | 0.15 | 0.15 | 0.21 | 0.21 | 0.21 | 0.21 | 0.21 | 0.91 | 0.91 | 0.91 | 1.66 | 1.66 | 1.66 | 1.66 |

| New York | 0.39 | 0.39 | 0.56 | 0.56 | 0.56 | 1.11 | 1.50 | 1.50 | 1.50 | 2.75 | 4.35 | 4.35 | 4.35 | 4.35 |

| North Carolina | 0.02 | 0.05 | 0.05 | 0.05 | 0.05 | 0.05 | 0.05 | 0.05 | 0.35 | 0.35 | 0.45 | 0.45 | 0.45 | 0.45 |

| North Dakota | 0.30 | 0.29 | 0.44 | 0.44 | 0.44 | 0.44 | 0.44 | 0.44 | 0.44 | 0.44 | 0.44 | 0.44 | 0.44 | 0.44 |

| Ohio | 0.18 | 0.18 | 0.24 | 0.24 | 0.24 | 0.24 | 0.55 | 0.55 | 1.25 | 1.25 | 1.25 | 1.25 | 1.25 | 1.60 |

| Oklahoma | 0.23 | 0.23 | 0.23 | 0.23 | 0.23 | 0.23 | 0.23 | 1.03 | 1.03 | 1.03 | 1.03 | 1.03 | 1.03 | 1.03 |

| Oregon | 0.28 | 0.28 | 0.38 | 0.38 | 0.68 | 0.68 | 1.28 | 1.18 | 1.18 | 1.18 | 1.18 | 1.18 | 1.31 | 1.32 |

| Pennsylvania | 0.18 | 0.31 | 0.31 | 0.31 | 0.31 | 0.31 | 1.00 | 1.35 | 1.35 | 1.35 | 1.60 | 1.60 | 1.60 | 2.60 |

| Rhode Island | 0.37 | 0.37 | 0.56 | 0.61 | 0.71 | 0.71 | 1.32 | 2.46 | 2.46 | 3.46 | 3.46 | 3.50 | 3.50 | 3.75 |

| South Carolina | 0.07 | 0.07 | 0.07 | 0.07 | 0.07 | 0.07 | 0.07 | 0.07 | 0.07 | 0.07 | 0.57 | 0.57 | 0.57 | 0.57 |

| South Dakota | 0.23 | 0.23 | 0.23 | 0.33 | 0.33 | 0.33 | 0.53 | 0.53 | 1.53 | 1.53 | 1.53 | 1.53 | 1.53 | 1.53 |

| Tennessee | 0.13 | 0.13 | 0.13 | 0.13 | 0.13 | 0.13 | 0.20 | 0.20 | 0.20 | 0.62 | 0.62 | 0.62 | 0.62 | 0.62 |

| Texas | 0.26 | 0.41 | 0.41 | 0.41 | 0.41 | 0.41 | 0.41 | 0.41 | 1.41 | 1.41 | 1.41 | 1.41 | 1.41 | 1.41 |

| Utah | 0.23 | 0.27 | 0.27 | 0.27 | 0.52 | 0.52 | 0.70 | 0.70 | 0.70 | 0.70 | 1.70 | 1.70 | 1.70 | 1.70 |

| Vermont | 0.17 | 0.19 | 0.20 | 0.44 | 0.44 | 0.44 | 0.93 | 1.19 | 1.79 | 1.99 | 2.24 | 2.62 | 2.75 | 3.08 |

| Virginia | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 | 0.30 | 0.30 | 0.30 | 0.30 | 0.30 | 0.30 | 0.30 |

| Washington | 0.34 | 0.34 | 0.57 | 0.82 | 0.83 | 0.83 | 1.43 | 1.43 | 2.03 | 2.03 | 3.03 | 3.03 | 3.03 | 3.03 |

| West Virginia | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.55 | 0.55 | 0.55 | 0.55 | 0.55 | 0.55 | 0.55 | 1.20 |

| Wisconsin | 0.30 | 0.38 | 0.38 | 0.44 | 0.59 | 0.59 | 0.77 | 0.77 | 0.77 | 1.77 | 2.52 | 2.52 | 2.52 | 2.52 |

| Wyoming | 0.12 | 0.12 | 0.12 | 0.12 | 0.12 | 0.12 | 0.12 | 0.60 | 0.60 | 0.60 | 0.60 | 0.60 | 0.60 | 0.60 |

Appendix Table 3.

Sources for State-Level Covariates

| Sources | |

|---|---|

| Cigarette Tax | Orzechowski and Walker (2019) |

| E-Cig Tax | Tax Foundation (https://vaporproductstax.com/taxation-database/) |

| Clean Indoor Air Law | CDC STATE System (https://www.cdc.gov/statesystem/index.html) |

| MML | National Conference of State Legislatures (http://www.ncsl.org/research/health/state-medical-marijuana-laws.aspx) |

| RML | National Conference of State Legislatures (http://www.ncsl.org/research/health/state-medical-marijuana-laws.aspx) |

| Decriminalization | Marijuana Policy Project (https://www.mpp.org/issues/decriminalization/state-laws-with-alternatives-to-incarceration-for-marijuana-possession/) |

| Beer Tax | Tax Policy Center (https://www.taxpolicycenter.org/statistics/state-alcohol-excise-taxes) |

| BAC 0.08 Law | Freeman (2007) and Alcohol Policy Information System (https://alcoholpolicy.niaaa.nih.gov/apis-policy-topics/adult-operators-of-noncommercial-motor-vehicles/12) |

| Income | Bureau of Economic Analysis |

| Unemployment | Bureau of Labor Statistics |

Appendix Table 4.

Cigarette Taxes and Youth Cigarette Use, 1991–2005 versus 2007–2017

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| 1991–2005 | 2007–2017 | 1991–2005 | 2007–2017 | |

| Current Cigarette User | Current Cigarette User | Frequent Cigarette User | Frequent Cigarette User | |

| Cigarette Tax | −0.017** (0.007) | 0.003 (0.004) | −0.013*** (0.004) | 0.001 (0.002) |

| Mean | 0.270 | 0.128 | 0.127 | 0.045 |

| N | 528,417 | 935,581 | 528,417 | 935,581 |

Notes: Each column represents an average marginal effect from a logit regression based on data from the YRBS for the indicated period. All models control for the covariates listed in Table 1, state fixed effects, and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

Appendix Table 5.

Cigarette Taxes and Youth Cigarette Use by Gender and Race

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| 1991–2017 | 1991–2005 | 2007–2017 | 1991–2017 | 1991–2005 | 2007–2017 | |

| Current Cigarette User | Current Cigarette User | Current Cigarette User | Frequent Cigarette User | Frequent Cigarette User | Frequent Cigarette User | |

| Panel I: Males | ||||||

| Cigarette Tax | −0.002 (0.003) | −0.017** (0.007) | 0.005 (0.005) | −0.002 (0.002) | −0.011** (0.005) | 0.002 (0.003) |

| Mean | 0.188 | 0.275 | 0.139 | 0.081 | 0.133 | 0.052 |

| N | 706,028 | 255,392 | 450,636 | 706,028 | 255,392 | 450,636 |

| Panel II: Females | ||||||

| Cigarette Tax | −0.010*** (0.002) | −0.017* (0.009) | −0.000 (0.004) | −0.006*** (0.002) | −0.016*** (0.005) | −0.001 (0.001) |

| Mean | 0.170 | 0.265 | 0.117 | 0.068 | 0.121 | 0.038 |

| N | 750,952 | 271,302 | 479,650 | 750,952 | 271,302 | 479,650 |

| Panel III: White | ||||||

| Cigarette Tax | −0.009*** (0.003) | −0.012 (0.008) | −0.003 (0.005) | −0.005*** (0.002) | −0.011** (0.005) | −0.001 (0.003) |

| Mean | 0.201 | 0.292 | 0.142 | 0.091 | 0.148 | 0.054 |

| N | 838,895 | 329,627 | 509,266 | 838,895 | 329,627 | 509,219 |

| Panel IV: Non-White | ||||||

| Cigarette Tax | 0.001 (0.004) | −0.017** (0.008) | 0.007** (0.003) | −0.002 (0.002) | −0.013*** (0.005) | 0.003* (0.001) |

| Mean | 0.141 | 0.217 | 0.109 | 0.048 | 0.081 | 0.034 |

| N | 574,687 | 171,924 | 402,763 | 574,687 | 171,924 | 402,763 |

Notes: Each cell within each column represents an average marginal effect from a logit regression based on data from the YRBS for the indicated period. All models control for the covariates listed in Table 1, state fixed effects, and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

Appendix Table 6.

Cigarette Taxes and Youth Cigarette Use by Age

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| 1991–2017 | 1991–2005 | 2007–2017 | 1991–2017 | 1991–2005 | 2007–2017 | |

| Current Cigarette User | Current Cigarette User | Current Cigarette User | Frequent Cigarette User | Frequent Cigarette User | Frequent Cigarette User | |

| Panel I: Age <17 | ||||||

| Cigarette Tax | −0.007*** (0.002) | −0.019*** (0.007) | 0.002 (0.003) | −0.004*** (0.001) | −0.014*** (0.004) | 0.000 (0.001) |

| Mean | 0.153 | 0.243 | 0.105 | 0.057 | 0.104 | 0.033 |

| N | 952,887 | 331,513 | 621,374 | 952,887 | 331,513 | 621,374 |

| Panel II: Age ≥17 | ||||||

| Cigarette Tax | −0.005 (0.004) | −0.013 (0.010) | 0.003 (0.007) | −0.006** (0.003) | −0.013* (0.007) | 0.000 (0.004) |

| Mean | 0.228 | 0.316 | 0.175 | 0.107 | 0.167 | 0.07 |

| N | 498,366 | 187,682 | 310,684 | 498,366 | 187,682 | 310,684 |

Notes: Each cell within each column represents an average marginal effect from a logit regression based on data from the YRBS for the indicated period. All models control for the covariates listed in Table 1, state fixed effects, and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

Appendix Table 7.

Alternative Definitions of “Frequent” Marijuana Use

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Used Marijuana at Least 3 Times during Past 30 Days | Used Marijuana at Least 10 Times during Past 30 Days | Used Marijuana at Least 40 Times during Past 30 Days | OLS: Treating Marijuana Use as Continuous | |

| Cigarette Tax | 0.003 (0.002) | 0.002 (0.001) | 0.001 (0.001) | 0.072 (0.049) |

| Mean | 0.130 | 0.082 | 0.036 | 2.78 |

Notes: Columns (1)–(3) represent average marginal effects from logit regressions based on data from the YRBS for the period 1991–2017. Column (4) represents results from an ordinary least squares (OLS) regression, where respondents were assigned the midpoint of their chosen binned response. Respondents could choose among the following responses when asked how frequently they used marijuana in the past 30 days: 0 times, 1 or 2 times, 3–9 times, 10–19 times, 20–39 times, or 40 or more times. All models control for the covariates listed in Table 1, state fixed effects, and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. N = 1,463,998. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

Appendix Table 8.

OLS Estimates for Current Marijuana User

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| 1991–2017 | 1991–2017 | 1991–2017 | 1991–2005 | 2007–2017 | |

| Current Marijuana User | Current Marijuana User | Current Marijuana User | Current Marijuana User | Current Marijuana User | |

| Cigarette Tax | 0.003 (0.002) | 0.002 (0.004) | 0.004 (0.003) | −0.009 (0.008) | 0.005* (0.002) |

| Mean | 0.198 | 0.198 | 0.198 | 0.205 | 0.194 |

| N | 1,463,998 | 1,463,998 | 1,463,998 | 528,417 | 935,581 |

| Individual-level covariates | No | Yes | Yes | Yes | Yes |

| State-level covariates | No | No | Yes | Yes | Yes |

Notes: Each column represents results from an OLS regression based on data from the YRBS for the indicated period. The individual- and state-level covariates are listed in Table 1. All models control for state fixed effects and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

Appendix Table 9.

Cigarette Taxes and Youth Marijuana Use at School

| (1) | (2) | (3) | |

|---|---|---|---|

| 1991–2011 | 1991–2005 | 2007–2011 | |

| Marijuana Use at School1 | Marijuana Use at School | Marijuana Use at School | |

| Cigarette Tax | 0.001 (0.002) | −0.002 (0.003) | 0.003 (0.003) |

| Mean | 836,231 | 487,363 | 348,868 |

| N | 0.052 | 0.056 | 0.046 |

Notes: Each column represents an average marginal effect from a logit regression based on data from the YRBS for the indicated period. All models control for the covariates listed in Table 1, state fixed effects, and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

Marijuana Use at School is equal to 1 if the respondent reported smoking marijuana on school property at least once in the past 30 days, and equal to 0 otherwise.

Appendix Table 10.

Sensitivity of Cigarette Tax and Any E-Cigarette Tax Estimates to Controlling for Cigarette Minimum Legal Purchase Age Laws and E-Cigarette Sales Bans to Minors

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| 1991–2017 | 1991–2017 | 2015–2017 | ||||

| Current Cigarette User | Frequent Cigarette User | Current Marijuana User | Frequent Marijuana User | Current E-Cigarette User | Frequent E-Cigarette User | |

| Cigarette Tax | −0.007*** (0.003) | −0.005*** (0.002) | 0.005 (0.003) | 0.002 (0.001) | −0.045 (0.058) | 0.008 (0.014) |

| Any E-Cigarette Tax | −0.011 (0.012) | −0.015 (0.012) | −0.013** (0.005) | −0.005 (0.004) | −0.029* (0.017) | −0.007* (0.004) |

| Cigarette MLPA1 | 0.020 (0.012) | 0.009 (0.008) | 0.012 (0.008) | 0.007 (0.006) | 0.018 (0.029) | 0.007 (0.005) |

| E-Cigarette Sales Ban to Minors2 | 0.006 (0.005) | 0.002 (0.003) | −0.005 (0.004) | −0.004** (0.002) | 0.025 (0.017) | −0.0005 (0.004) |

| Mean | 0.179 | 0.075 | 0.198 | 0.083 | 0.182 | 0.027 |

| N | 1,463,998 | 1,463,998 | 1,463,998 | 1,463,998 | 355,677 | 355,677 |

Notes: Each column represents average marginal effects from a logit regression based on data from the YRBS for the indicated period. All models control for the covariates listed in Table 1, state fixed effects, and year fixed effects. Dependent variable means are reported. Standard errors, corrected for clustering at the state level, are in parentheses. Asterisks denote significance at the 1% (***), 5% (**), and 10% (*) levels.

Cigarette MLPA is equal to 1 if state s was enforcing a minimum legal purchase age for cigarettes of greater than 18 years of age during year t, and equal to 0 otherwise.

E-Cigarette Sales Ban to Minors is equal to 1 if state s was enforcing an e-cigarette sales ban to individuals under 18 years of age during year t, and equal to 0 otherwise.

Footnotes

Levine et al. (2011) find that dosing mice with nicotine increased their responsiveness to cocaine.

In addition to state excise taxes, hundreds of local jurisdictions levy taxes on cigarettes (Committee on Preventing Nicotine Addiction in Children and Youths, 1994).

Unstamped cigarettes are those not bearing the indicia of the state in which they originated. Initially, the Federal Cigarette Contraband Act set the limit at 60,000 unstamped cigarettes (Committee on Preventing Nicotine Addiction in Children and Youths, 1994). It has been estimated that “casual” cross-border cigarette smuggling still exists today (Lovenheim, 2008; Davis et al., 2014).

There is a large economic literature on the determinants of youth cigarette use in general. For instance, previous studies have estimated the effects of anti-smoking sentiment (DeCicca et al., 2008), peer smoking interactions (Krauth, 2007; Nakajima, 2007), parental influence (Powell and Chaloupka, 2005), compliance inspections of tobacco retailers (Abouk and Adams, 2017), youth access laws (Ross and Chaloupka, 2004), tobacco advertising (Beltramini and Bridge, 2001), and clean indoor air laws (McMullen et al., 2005).

Important exceptions include Dee (1999), Gruber (2000), Gruber and Zinman (2001), and Ringel and Evans (2001). These studies, however, come with notable limitations. All of them are restricted to tax variation prior to the 1998 MSA. As noted above, many of the tax hikes in the post-MSA era have been substantial. Gruber (2000) and Gruber and Zinman (2001) use information from the YRBS but observe only four waves of data. Because they use smoking information from birth certificate records, Ringel and Evans (2001) are only able to estimate tax effects on teen mothers.

Bader, Boisclair, and Ferrence (2011) and Guindon (2013) review much of the literature published prior to Carpenter and Cook (2008). Interestingly, despite the fact that they reviewed similar studies, Bader, Boisclair, and Ferrence (2011) and Guindon (2013) come to different conclusions. Bader, Boisclair, and Ferrence (2011) conclude that cigarette taxes reduce teen smoking, while Guindon (2013) concludes that there is not strong evidence that taxes affect teen smoking initiation.

Carpenter and Cook (2008) define “frequent smoking” as having smoked during at least 20 of the past 30 days.

In a recent working paper, Courtemanche and Feng (2019) corroborate Hansen et al.’s (2017) finding that the cigarette tax effect wanes over time and eventually disappears. However, they do find some evidence that tax increases may still reduce youth smoking in states where the baseline tax rate is low.

Using data from the 1984 National Longitudinal Survey of Youth (NLSY), Pacula (1998a) finds a negative, but statistically insignificant, relationship between cigarette taxes and the probability of marijuana use in the cross section. Pooling data from the 1983 and 1984 NLSY, Pacula (1998b) finds a negative relationship between cigarette prices (inclusive of taxes) and the probability of marijuana use. Using data from Monitoring the Future for the period 1992–1994, Chaloupka et al. (1999) find that higher cigarette prices (inclusive of taxes) reduce the level of marijuana consumption among current users but have no statistically significant effect on the probability of marijuana use.

We observe YRBS data before and after a cigarette tax change for 14 of these states. Appendix Table 1 shows the state-by-year number of observations in our sample, while Appendix Table 2 shows the nominal cigarette tax over time for all 50 states and the District of Columbia.

Previous researchers have used these data to study the effects of a wide range of public health policies, including anti-methamphetamine advertising (Anderson, 2010; Anderson and Elsea, 2015), state physical education requirements (Cawley, Meyerhoefer, and Newhouse, 2007), mandatory seatbelt laws (Carpenter and Stehr, 2008), and anti-bullying laws (Sabia and Bass, 2017).

For the national survey and a majority of state surveys, data collectors visit each participating school to administer the questionnaires. Data collection is handled in a manner to protect respondent privacy, preserve anonymity, and allow voluntary participation. The surveys are completed during one class period and students record their answers in computer-scannable booklets. When possible, desks are spread throughout the classroom and students are asked to cover their answers with an extra sheet of paper that is provided by the survey administrator. When finished, they seal their booklet in an envelope and place it in a box. For further details on the YRBS data-collection protocols, see Centers for Disease Control and Prevention (2013).

For examples, see Anderson, Hansen, and Rees (2015), Hansen et al. (2017), Anderson and Sabia (2018), and Courtemanche and Feng (2019).

In total, 49 states and the District of Columbia contributed data to the YRBS before and after a tax change. North Dakota is the only state for which we cannot exploit tax variation. We observe pre- and post-policy data for tax decreases in only two states (New Hampshire in 2013 and Oregon in 2005).

Respondents could choose among the following answers: 0 days, 1 or 2 days, 3–5 days, 6–9 days, 10–19 days, 20–29 days, or all 30 days.

Respondents could choose among the following answers: 0 times, 1 or 2 times, 3–9 times, 10–19 times, 20–39 times, or 40 or more times.

Because the cigarette and marijuana questions are worded differently in the YRBS, we cannot directly compare cigarette use with marijuana use over time. If we weight our YRBS estimates using sample weights generated from the Surveillance, Epidemiology, and End Results population data, the trends we observe are qualitatively similar to those shown in Figures 2 and 3.

Because states often implement cigarette tax increases on July 1st or later within a given year (Boonn, 2019b), we code Cigarette Tax as equal to the tax on July 1st in state s during year t. Our results change little if we instead use the cigarette tax during year t − 1 or during year t − 2 as our regressor of interest.

To retain sample size, we also control for a set of dummies that indicate whether information on gender, age, grade, or race/ethnicity is missing. Results are similar if we simply drop the observations that are missing information on any of these characteristics.

Despite the fact that state e-cigarette taxes are a relatively new phenomenon, there is some research to suggest that e-cigarettes serve as substitutes for traditional cigarettes among adults (Pesko, Courtemanche, and Maclean, 2019) and pregnant women (Abouk et al., 2019). Following Abouk et al. (2019) and Pesko, Courtemanche, and Maclean (2019), we code the variable Any E-Cigarette Tax as equal to 1 if state s was enforcing an e-cigarette tax during year t, and equal to 0 otherwise. In Section VI, we discuss estimated coefficients on Any E-Cigarette Tax.

There is some evidence that relatively strong clean indoor air laws may reduce the probability of smoking among youths (Ross and Chaloupka, 2004).

See Sarvet et al. (2018) for a review of the literature on medical marijuana laws and adolescent marijuana use.

Researchers have relied on beer taxes to proxy variations in alcohol price (Ruhm, 1996; Markowitz, Kaestner, and Grossman, 2005).

We should note that the negative and statistically significant estimates presented in Table 2 and Appendix Table 4 become statistically indistinguishable from zero when we include state-specific linear time trends as controls. However, there is a discussion as to whether controlling for state-specific linear trends in cigarette tax models is actually appropriate (Hansen et al., 2017; Courtemanche and Feng, 2019). On the one hand, state trends are designed to capture potentially important unobserved factors such as attitudes and preferences. On the other hand, controlling for them comes with the risk of using up potentially exogenous variation in state cigarette taxes. Furthermore, if the state-specific trends are correlated with taxes even after important unobservables have been “partialled out,” their inclusion could lead to “unreliable or even wrong-signed estimates” (Sheehan-Connor, 2010; Hansen et al. 2017, p. 72). If we regress Cigarette Tax on the state-level controls listed in Table 1, state fixed effects, and year fixed effects, we obtain an R2 of 0.897. If we include state-specific linear trends on the right-hand side of this regression, the R2 increases to 0.959. This implies that the trends are soaking up approximately 0.062 of the available variation in cigarette taxes.

In Columns (1)–(3) of Appendix Table 7, we consider alternative definitions of frequent marijuana use. Regardless of whether we define frequent use as having smoked marijuana at least 3, 10, or 40 times during the past 30 days, we find no evidence of a relationship between state cigarette taxes and frequent marijuana use. Similarly, we find no evidence of a relationship between taxes and teen marijuana use when we treat marijuana use as continuous variable (Column (4)).

When comparing our estimates to those of Farrelly et al. (2001), it is important to note that they define their measure of intensity as “the frequency of marijuana use in the past 30 days (1–30 days) conditional on use” (Farrelly et al., 2001, p. 56). In results not reported for the sake of brevity, we estimated the relationship between cigarette taxes and the frequency of marijuana use, conditioning on having smoked marijuana at least once in the past 30 days. Based on this alternative specification, we found little evidence that marijuana use on the intensive margin responds to changes in the cigarette tax.

The estimates presented in Table 4 are qualitatively similar if we control for state-specific linear time trends. Our results are also similar if we estimate the relationship between Cigarette Tax and Current Marijuana User via a linear probability model, rather than a logit specification (Appendix Table 8).

In Appendix Table 9, we consider an alternative marijuana-related outcome that was available in the YRBS through 2011. Specifically, we find no evidence of a relationship between state cigarette taxes and past-month marijuana use on school property.

Using data from the National Survey of Drug Use and Health, Behavioral Risk Factor Surveillance System (BRFSS), and Current Population Survey Tobacco Use Supplements, Choi, Dave, and Sabia (2019) find that the legalization of medical marijuana is associated with increases in marijuana consumption and decreases in cigarette smoking among adult populations.

Using data from the BRFSS, Pesko, Courtemanche, and Maclean (2019) find that e-cigarette taxes are negatively related to adult e-cigarette use and positively related to adult traditional cigarette use. Using data from the Current Population Survey Tobacco Use Supplements, Saffer et al. (2019) find evidence that the implementation of Minnesota’s e-cigarette tax led to increases in traditional cigarette use and reductions in smoking cessation among adult populations.

Respondents to the YRBS are asked, “During the past 30 days, on how many days did you use an electronic vapor product?” Measures of Current E-Cigarette User and Frequent E-Cigarette User are coded analogously to Current Cigarette User and Frequent Cigarette User, respectively.

As noted above, seven states (CA, KS, LA, MN, NC, PA, and WV) and the District of Columbia passed e-cigarette taxes between 2010 and 2017. Four of these tax changes are ad valorem taxes and four are excise taxes.