Abstract

Purpose

To provide an overview of important factors to consider when purchasing radiology artificial intelligence (AI) software and current software offerings by type, subspecialty, and modality.

Materials and Methods

Important factors for consideration when purchasing AI software, including key decision makers, data ownership and privacy, cost structures, performance indicators, and potential return on investment are described. For the market overview, a list of radiology AI companies was aggregated from the Radiological Society of North America and the Society for Imaging Informatics in Medicine conferences (November 2016–June 2019), then narrowed to companies using deep learning for imaging analysis and diagnosis. Software created for image enhancement, reporting, or workflow management was excluded. Software was categorized by task (repetitive, quantitative, explorative, and diagnostic), modality, and subspecialty.

Results

A total of 119 software offerings from 55 companies were identified. There were 46 algorithms that currently have Food and Drug Administration and/or Conformité Européenne approval (as of November 2019). Of the 119 offerings, distribution of software targets was 34 of 70 (49%), 21 of 70 (30%), 14 of 70 (20%), and one of 70 (1%) for diagnostic, quantitative, repetitive, and explorative tasks, respectively. A plurality of companies are focused on nodule detection at chest CT and two-dimensional mammography. There is very little activity in certain subspecialties, including pediatrics and nuclear medicine. A comprehensive table is available on the website hitilab.org/pages/ai-companies.

Conclusion

The radiology AI marketplace is rapidly maturing, with an increase in product offerings. Radiologists and practice administrators should educate themselves on current product offerings and important factors to consider before purchase and implementation.

© RSNA, 2020

See also the invited commentary by Sala and Ursprung in this issue.

Summary

The radiology artificial intelligence marketplace is rapidly maturing, with an increase in product offerings, and radiologists and practice administrators would likely benefit from education on current product offerings and important factors to consider before purchase.

Key Points

■ There are an increasing number of radiology artificial intelligence software offerings covering multiple clinical targets. Image interpretation can be subdivided into repetitive, quantitative, explorative, and diagnostic tasks.

■ Important factors to consider when purchasing include input from key decision makers, data ownership and privacy, cost structures, performance indicators, and potential return on investment.

Introduction

Artificial intelligence (AI) has demonstrated tremendous advancements in recent years for learning patterns from large-scale data, tackling problems like facial recognition and self-driving vehicles. In health care, AI has been used for a variety of tasks, including predicting hospital readmission rates (1–3), intensive care unit mortality (4), and identifying patients in intensive care units at risk for sepsis (5). AI has also been leveraged extensively for imaging tasks such as identification of intracranial hemorrhage at head CT (6) and identifying diabetic retinopathy at fundoscopic examinations (7,8).

With this progress in technology, there has been a concurrent explosion of medical AI companies aiming to solve problems in radiology. The 2019 Radiological Society of North America (RSNA) Annual Meeting had 173 self-identified radiology AI companies. Radiology is an appealing area of focus for AI because radiology images consist of a specified set of standard examination types and views, as well as some degree of structured reporting, depending on the institution’s guidelines. In contrast, the majority of the health care record is unstructured, and key information and diagnoses may exist in different areas.

The goal of this report is to briefly define the fundamental concepts and terminology in AI, highlight key stakeholders and important considerations in purchasing or adopting radiology AI software, and outline some of the current software offerings by AI companies. By the end of this report, we hope the reader will gain a deeper understanding of radiology AI technology, its potential value-adds to their practice, and identify key points and pitfalls that should be considered before purchasing. Although there are many companies that focus on nonimaging-related tasks such as automatic structured reporting or billing, in this report we will concentrate on tasks that are primarily focused on image interpretation. The authors do not name or endorse any specific companies, and therefore we do not report on any specific performance claims by vendors.

Fundamental Concepts and Terminology

The term AI has been used extensively, and occasionally loosely, in the past several years as a method to drive marketing and sales of medical software. AI encompasses a group of techniques that simulate human intelligence in machines (9). Deep learning is the most common type of AI adopted for image interpretation tasks, including those in radiology (9). The key difference between deep learning and other programming techniques is that in deep learning, an algorithm can automatically extract features and learn patterns in datasets without being given an explicit set of rules or list of features (10). To put it more concretely, rather than instructing software to identify hemorrhage by looking for increased attenuation on head CT images, deep learning allows us to provide the algorithm with examples of head CT scans with and without hemorrhage and allows the algorithm to learn the relevant imaging features to identify the differences. Whereas rules-based software applications are rigid, deep learning can achieve higher prediction and classification accuracy with increasing amounts of data (11). Last, and perhaps most exciting, because deep learning models are not given explicit instructions on features of interest in an image, well-trained models may be able to extract patterns that are beyond human perception (12). To maintain consistency, we will hereafter refer to companies using these techniques as “Radiology AI” companies.

Considerations for Purchasing Decisions

In this section we will review key factors that should be considered when purchasing AI tools or products. The Table provides an overview covering many of these topics that can be referenced during visits to exhibitor booths or when evaluating software for purchase.

Guidelines for Evaluating Radiology AI Companies

Motivations for AI Purchasing

Adoption of AI into radiology practices is in nascent stages, so to the reader we ask, What is your motivation for being an early adopter of AI technology in your practice? There are multiple potential benefits that may include quality, efficiency, or even marketability; however, downsides such as cost, usability, and changes to workflow must also be considered.

When considering quality improvement metrics like diagnostic accuracy, it is possible that AI may have a direct and substantial impact on patient care and safety. While quality improvement is always a high priority in radiology practices, quality improvement alone may not be sufficient to drive software adoption in mature health care economies unless direct cost or time savings can also be attributed to the software (13–15). For this reason, many AI companies focus primarily on improving practice efficiency, for example, increasing acquisition or interpretation speed (14,15). Saving the practice and radiologist valuable time each day can be translated directly into cost savings. Last, a more tangential appeal of AI implementation may be the ability to enhance marketing and brand management for a hospital system or practice (14). AI may serve as a means of differentiation for a practice, for both patients and physicians, which may bring its own economic benefits.

While AI software may be desirable for any of the above reasons, AI implementation has its own pitfalls, including image processing costs that may not be recoverable, overhead (time and cost) of implementation, and resistance to change and/or use from radiologists. In a fee-for-service model, improved diagnostic accuracy without associated cost savings or increased revenue may impede implementation, particularly in departments with tight operational budgets (14,15). There are also hidden costs of implementation that may not be readily apparent during initial evaluation or a “free demo.” Last, and perhaps most important, performance claims should be scrutinized, as metrics like sensitivity, specificity, positive predictive value, and negative predictive value can vary depending on a company’s testing methods or a hospital’s patient population.

Data Ownership and Privacy

Data ownership and patient privacy should be considered before software implementation (16). In regard to patient privacy, all medical software marketed for sale in the United States must be compliant with the Health Insurance Portability and Accountability Act guidelines for protection of health information. However, stricter regulations have recently been announced in Europe through the General Data Protection Regulation (17). The details are beyond the scope of this report; however, it is possible that some of these regulatory decisions will be adopted in the United States in coming years and affect the development of radiology AI software.

Risks to patient privacy can vary depending on the type of software implementation and data storage. Typically, AI algorithms can run in one of two ways, either locally on servers installed at the hospital and/or clinic or by data uploaded to a cloud infrastructure. Cloud infrastructure is more common as it decreases implementation costs, allows for easier software updates, and allows companies to scale more easily. The caveat to using a cloud-based infrastructure is that it requires data to leave the institution and therefore may carry a higher risk of data breach if on-site anonymization is not performed correctly. Conversely, algorithms that run locally at an institution may provide more real or perceived security; however, these local implementations also require more expensive on-site hardware such as servers, cooling systems, and secure storage and may not be easily scalable across multiple hospitals and scanners. It is important when reviewing options to include compliance and legal personnel earlier in the process rather than after the fact.

Regardless of implementation method, there should be clear guidelines on ownership and rights associated with the use of images processed by the algorithm and whether these images can be used by the company for further algorithm development. The authors’ recommendation is that any data processed by a company’s algorithm belongs exclusively to the institution and that any use of that data for further algorithm development such as training or testing must be approved explicitly. If an AI company would like to use patient data for product improvement, the agreement should be structured in such a way that the institution also receives some benefit for use of their data or the de-identified data are shared as a public good. Of note, ongoing algorithm improvement in a deployed environment is not yet allowable by the Food and Drug Administration (FDA), and all algorithms must be “frozen” in their current state upon deployment. Any algorithm update or improvement requires reapproval by the FDA (18).

Cost Structures

Cost structures for AI software vary, and most companies offer a subscription model as opposed to a capital purchase. Licensing options include per entire site, per workstation, per user, or per study licenses. Per study licenses can be beneficial for low-volume examinations, for example, an institution that is starting a cardiac MRI program but is still building a referral base. However, in most cases a sitewide or per workstation license that allows processing of an unlimited number of studies is the simplest option because it enables testing on a wider range of examination types. For example, a nodule detection algorithm developed for low-dose lung cancer screening CT studies may perform differently on full-dose CT angiograms. Or, how well will it work evaluating the lung bases in an abdominal CT study, and is the processing expense justified? In this setting, a broader license would be more valuable and eliminates the added burden of deciding prospectively which studies to process. As most companies are still in the process of acquiring users, they may be willing to tailor their payment structure based on the institution’s needs.

Reported Model Performance

Patient populations vary geographically with differing disease prevalence, demographic factors, and comorbidities. Furthermore, institutions may have different equipment manufacturers and imaging techniques such as varying CT reconstruction algorithms, unique MRI sequences, or customized mammography postprocessing curves. In advance of purchasing AI software, it is of paramount importance to determine whether or not the algorithm will perform well at your institution. Algorithms trained on patient populations with a certain disease prevalence may be unintentionally biased (16) and may not perform well at another site with a different distribution of disease. This variability is particularly evident if an algorithm was trained with limited data (19,20). For this reason, it may be worth inquiring if the company is able to report the algorithm’s performance using a retrospective dataset from your own institution, calibrate the algorithm on your institutional data, or modify operating points to adjust false-positive and false-negative rates. It is also useful to request a customer list from them and reach out to others who have purchased and are using their product to get real-world user feedback. Following implementation, ongoing quality control is necessary to detect any potential drift or bias in algorithm performance. Currently, algorithms cannot be retrained during live implementation, and minor changes in scanner parameters or acquisition protocols could have unforeseen effects on algorithm performance.

Academic and Industry Collaborations

In many cases, AI radiology software represents uncharted territory. The vast majority of AI radiology companies are nascent and working on their initial clinical offerings. Because of this, many companies seek partnerships with institutions for clinical feedback or even codevelopment. Questions about ownership of data and intellectual property often arise during codevelopment, which can be difficult to address. An institution commonly provides data and medical expertise, whereas the industry partner provides technical expertise, engineering support, and productization strategies that may incorporate several years of prior effort and investment. Clear delineation of ownership of any resultant algorithm, software, or datasets is important to address in advance and, if applicable, the route for approval through the institution’s technology transfer or licensing office. In the case that sharing of intellectual property is not possible, a common paradigm is to offer discounts on the product for a fixed period of time. It is the institution’s responsibility to evaluate the time and overhead of codevelopment against the downstream benefits. These cautions are important to keep in mind even when working with other academic institutions, health care enterprises, and even other departments within your own institution.

Key Decision Makers in AI Software Purchasing

Radiology practices consist of several key stakeholders who may be involved in purchasing decisions for AI software. Each stakeholder considers a different aspect of the purchasing decision, and all stakeholders must be in agreement before a purchasing decision can be made.

Hospital and Practice Administration

The primary goal for the hospital or practice administrator is to evaluate the medicolegal, compliance, and financial viability of any purchase. Medicolegal viability hinges greatly on patient privacy and security as discussed above. Financial viability depends largely upon on the return on investment (ROI) for implementation, whether real or perceived. Because there are currently no insurance reimbursements for use of radiology AI software, ROI must be evaluated in one of two ways: quality improvement or efficiency improvement.

Quality improvement includes tasks such as increasing diagnostic accuracy or reducing errors, theoretically reducing downstream costs and/or decreasing liability. However, this value proposition can be a difficult sell as the financial ROI is difficult to calculate and requires several assumptions. For example, a decrease in liability would be difficult to prove unless there was a recent case at the institution that could have been avoided by a specific algorithm on the market. In theory, quality improvement could also generate ROI through marketability and increasing imaging volume; however, quantification of this improvement similarly requires many assumptions and is difficult to calculate prospectively.

Unlike quality improvements, efficiency improvement is easier to demonstrate as an ROI. For example, practices can measure the difference in study read times with and without the AI software. Time savings can be directly translated into person-hours and subsequent cost savings. In the nascent stages of radiology AI software, saved person-hours may be the quickest and most efficacious method to demonstrate value. As an added benefit, AI software geared toward increasing efficiency for repetitive or mundane tasks could be used to attract radiologists to join the practice in a competitive market.

Information Technology Office

Information technology staff are responsible for determining technical feasibility for implementation, safety, and security issues of any new software, as well as addressing patient privacy issues in conjunction with hospital administration. They must also understand infrastructure requirements of the new software and any potential bottlenecks or incompatibilities new software would cause to existing infrastructure.

Once preliminary feasibility is addressed, the software’s output must be incorporated into the workflow. For example, a simple implementation may send a new series to the picture archiving and communication system (PACS) to display the output directly to the radiologist. Alternatively, the results could be pushed directly into the dictation platform. However, the most robust implementations of AI software, such as the ability to edit or remove detected findings, require installation of vendor-specific software on individual workstations. These implementations require consideration of hardware requirements and compatibility at each workstation and can add complexity to implementation.

Last, management of ongoing support should be addressed, including responsible parties for maintaining uptime, assignment of dedicated company staff to each site, and how software updates will be handled. The latter is of increased importance in AI software as it is expected to be updated with new algorithms or features much more rapidly than other clinical software.

Clinicians

The last important decision makers are the end users, which in most cases are radiologists, but other clinicians, including cardiologists and neurologists, can also drive adoption. To many radiologists, nonimage interpretive workflow disruptors have shown to decrease radiologist satisfaction, adversely affect radiologist workload, and decrease self-perceived quality of image interpretation (21–23). In the current landscape of high volumes and monitored turnaround times, any decrease in efficiency will be detrimental to the practice. Serving the needs of radiologists requires maintaining a balance between providing additional useful information while minimizing false-positive findings, unnecessary clicks, and mouse mileage. Length of time required for educating users on using new software must also be considered, as many radiology AI software packages may function differently than what the clinician is accustomed to. Launching a separate application window, which is a frequently used implementation for many breast and prostate MRI workflows, is generally viewed as inconvenient. Intrinsic limitations in this method include limited workstations with the installed secondary software, lag time between pushing studies from PACS to the secondary software package, and populating results from the secondary software back into PACS and dictation software. The most successful AI companies will minimize these barriers by direct and seamless integration with PACS; however, this integration can increase software complexity, development time, and cost of distribution.

Beyond workflow, radiologists may also want to know if false-positive or false-negative findings can be investigated to understand the underlying cause. While in the past AI algorithms were considered “black boxes” that could not be interrogated, modern architectures allow highlighting the areas or features of interest on an image, even if the underlying rationale cannot be determined. AI software that includes this capability will increase the likelihood of radiologist adoption.

State of the Market

In this section, we provide an overview of the state of the radiology AI market as of November 2019.

Methods

A preliminary list of radiology AI companies was identified by aggregating all vendors listed in the machine learning or artificial intelligence categories from the RSNA and Society of Imaging Informatics in Medicine (SIIM) conferences from 2016 to 2019. RSNA was chosen as it is the largest radiology-centric conference and SIIM due to its focus on informatics and large vendor presence. Before 2016, AI software vendors were not listed as a separate category at either conference, making identification difficult. We also did not review current offerings by large original equipment manufacturers that may be integrated directly into imaging equipment or PACS software.

The preliminary list was combined with information gathered directly from each company’s website, marketing brochures, and online blogs such as Imaging Technology News Online (www.itnonline.com) and AuntMinnie.com. Inclusion criteria for algorithms included those using deep learning for image analysis tasks such as detection, classification, or measurement of findings. Exclusion criteria included those algorithms tailored toward image enhancement, natural language processing in reporting, or workflow management. FDA and/or Conformité Européenne (CE) approval status for each algorithm was determined from official public press releases in most cases. Company net worth was determined by publicly available numbers on repositories from Crunchbase.com and CBInsights.com.

Overview

In comparison to other medical software, the radiology AI software market is in its infancy. The year 2016 was the first year radiology AI companies had a significant presence at major conferences such as SIIM and RSNA. Since then, the list of radiology AI vendors has increased exponentially, although software adoption is still in relatively early stages and varies with the aspect of radiology workflow being targeted. Software for image interpretation has been adopted more slowly, mostly due to longer development times, stricter requirements for FDA approval, and nuances of integration into workflow (24). As such, fewer image interpretation algorithms have been cleared through the FDA for clinical use, and many are still marketed as research tools only. Conversely, software that targets image reconstruction, clinical decision support, workflow management, and automated structured reporting may be FDA approved more rapidly and used in clinical practice.

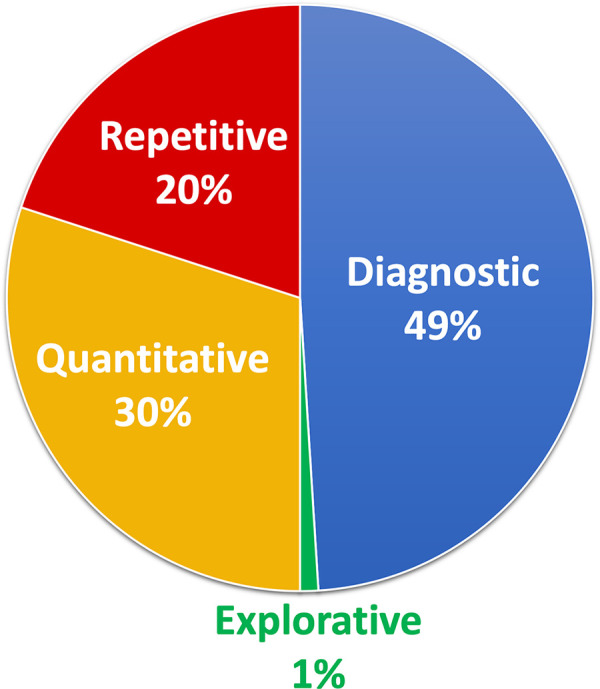

Companies focusing on image interpretation can be divided into four major areas of tasks: repetitive, quantitative, explorative, and diagnostic (Fig 1). Repetitive tasks mainly target high-volume, low-complexity tasks such as lung nodule detection or tracking of multiple sclerosis lesions. Quantitative tasks include measuring volume of emphysema at chest CT or measuring bone density. Explorative algorithms are designed to allow a radiologist to select an area of interest with a pathology they may not be familiar with (for example, fibrotic lung disease), and return similar-appearing regions from other scans in a database with associated diagnoses. Last, diagnostic tasks include things like detection of pneumonia on chest radiographs, classification of breast lesions, and scoring of liver tumors.

Figure 1:

Artificial intelligence companies by type of task (repetitive, quantitative, diagnostic, or explorative) of 119 software offerings. Repetitive tasks mainly target high-volume, low-complexity tasks such as lung nodule detection or tracking of multiple sclerosis lesions. Quantitative tasks include measuring volume of emphysema on chest CT images or measuring bone density. Explorative algorithms are designed to allow a radiologist to select an area of interest on an image and return similar-appearing regions from other scans with associated diagnoses. Last, diagnostic tasks cover the majority of remaining algorithms and include functions such as detection of pneumonia on chest radiographs, classification of breast lesions, and grading of liver tumors.

The level of venture capital funding has increased in tandem with the increase of companies competing in this space and as radiologists, researchers, and investors alike have begun to appreciate the potential size of the market. Radiologists have largely shifted from fearing AI to embracing it, and early successes and increasing numbers of FDA approvals have mitigated risks for investors. Based on publicly available records, the world market cap specifically for image analysis in 2019 across 119 software products was $1.2 billion dollars and is projected to hit $2.0 billion by 2022 based on linear regression (Fig 2).

Figure 2:

Total market capitalization for radiology artificial intelligence (AI) companies by year (dark blue) demonstrating continued growth in market size. Linear regression (dashed line) projects a market size of $2.0 billion by 2022.

A comprehensive overview of companies is available on the website hitilab.org/pages/ai-companies.

Current Offerings by Anatomic Location

At the time of writing, we identified 119 image analysis software product offerings from 55 companies. Of these, 46 algorithms currently have FDA and/or CE approval. FDA and CE approval are grouped together for the purposes of this article as we noted in most cases that CE approval predicts FDA approval within the next 2 years, whether it is full FDA clearance or traditional premarket pathway for medical devices (510[k], de novo, or premarket approval). The 510(k) approval is a fast-track FDA clearance that is based on similar devices that have received approval in the past. However, the regulation surrounding these algorithms is actively changing as the FDA recognizes that the product that originally meets FDA standards may frequently change as updates are released by the developers. The FDA is now evaluating these companies through the Software Precertification (Pre-Cert) Pilot Program as part of the Digital Health Innovation Action Plan to adjust for the requirements posed by these new medical “device” companies (25). Approvals by regulatory bodies in Asia are not included in Figure 2 as the progression to FDA approval was less certain throughout the course of our research.

In this section, algorithms are divided by subspecialty as follows: head and neck, breast, chest, cardiac, body, musculoskeletal and spine, nuclear medicine, and pediatrics. Each subspecialty has further been divided into four imaging modalities: radiography, CT, MRI, and US (Fig 3). For streamlining in the breast imaging section, the radiography category represents two-dimensional mammography and the CT category represents three-dimensional tomosynthesis. Similarly, for nuclear medicine, the CT column represents PET/CT and the MRI column represents PET/MRI. There are currently no companies focusing on planar nuclear medicine studies.

Figure 3:

Distribution of current radiology artificial intelligence (AI) software offerings. The left panel represents the frequency of all radiology AI software offerings by subspecialty and modality, whereas the right panel demonstrates only those with Food and Drug Administration (FDA) and/or Conformité Européenne (CE) mark of approval at the time of writing (November 2019). Nucs = nuclear medicine, Peds = pediatric, XR = radiography.

Currently, a plurality of companies focus on lung CT and two-dimensional mammography (Fig 3). Nodule detection on chest CT scans has been a major focus for multiple reasons, including the binary classification task (present vs absent), the availability of large public datasets for training such as from the Lung Image Database Consortium (26), and easily quantifiable metrics to drive adoption, such as improved detection rates or decreased read times. Similarly, mammography has been targeted due to the sheer volume of studies (about 40 million screening mammography studies are performed annually in the United States [27]) and the high resultant associated time and cost of breast cancer screening (approximately $7.8 billion in 2010 [28]), which can be substantially reduced with even modest improvement in recall or biopsy rates.

It is also worth noting that several modalities and organ systems currently have little or no activity, including US, pediatrics, and nuclear medicine. These areas are ripe for innovation: Some potential high-volume targets include pediatric head US for neonatal hemorrhage, extremity US for deep vein thrombosis, or renal US for quantified grading of hydronephrosis.

Head and Neck

Most software focuses on head CT scans for detection and volume quantification of hemorrhagic and ischemic stroke. Some companies use the results to triage cases (ie, moving most concerning cases to the top of the worklist), which could be helpful to identify truly emergent studies in the emergency department, where all cases may be labeled as “STAT.” There is also one current offering that analyzes for ischemic stroke and pushes a mobile notification to the provider’s cell phone if there are suspicious findings. Other offerings on head CT include quantifying traumatic brain injuries by measuring midline shifts and measuring ventricular size.

Most brain MRI analysis is focused on multiple sclerosis lesion detection and volumetric measurement. Other offerings include volumetry for anatomic regions (eg, hippocampal volume), classification and progression of dementia, and whole brain volumetry for chronic traumatic brain injury.

Breast

As previously discussed, breast imaging has been a major area of interest and accounts for approximately 14% of the market. Current offerings include a range from triaging solutions that prioritize concerning studies to full lesion detection and classification. Lesion detection and classification software typically provides a lesion score based on suspicious characteristics, and some allow customization of the sensitivity and specificity of detection. One algorithm claims to increase sensitivity and specificity of mass and calcification detection when compared with standard breast computer-aided detection software in dense breasts and touts false-positive rates that are similar to those of a trained radiologist.

Software for other breast imaging modalities, including tomosynthesis, MRI, and US, are currently in their early stages. Currently, only one tomosynthesis analysis product is FDA approved, and this approved product has claims to improve cancer detection, reduce unnecessary recalls, and decrease radiologist reading time by a large margin.

MR image interpretation includes characterizing user-selected regions of interest and providing a malignancy risk score. It is important to note that in these applications, the detection of breast MR lesions is not automatic and requires the radiologist to select an area of interest before classification. This requirement may be due to differences in FDA approval requirements for detection versus classification software.

US applications are similar and include assignment of Breast Imaging Reporting and Data System score based on a user-selected region of interest. One application claims increased sensitivity and specificity with a concurrent reduction in benign biopsy rates.

Chest

Chest imaging is the most frequently targeted area for AI software, currently accounting for approximately 35% of offerings. The scope of chest CT analysis is broad due to a larger number of potential diagnoses. Of these, lung nodule detection is the most common use case and could have a major impact on lung cancer screening. Nodule classification, tracking, and clinical decision support are also offered but are less common due to difficulty in obtaining ground truth data for model development. Other applications include worklist triaging for pneumothorax and pulmonary embolism, quantification and characterization of chronic lung disease, and detection of rib and spine fractures. At the time of writing there are 25 total offerings, of which 11 are FDA approved.

Chest radiography is also an active area of development, including detection of consolidation and/or pneumonia, cardiomegaly, pneumothorax, rib fractures, and lung nodules. Less popular algorithms include localizing central line and endotracheal tube positions. Last, tuberculosis screening applications are available but mostly deployed internationally in countries such as India where the disease prevalence and radiology shortage is more severe (29).

Cardiac

There is a relative paucity of companies working in the cardiac space, which is somewhat surprising given the high prevalence of cardiovascular disease in the United States. This scarcity may be in part due to the relative lower volume of coronary CT, CT angiography, and cardiac MRI when compared with chest CT. Current applications include coronary CT for quantification of arterial calcification, vessel stenosis, and measurement of valvular stenosis. In echocardiography, applications include automated measurement of ejection fraction and ventricular volume. In cardiac MRI, there is one company that performs quantitative analysis of hemodynamics, ventricular function, and severity of valvular disease.

Body

There are relatively few applications of AI in the abdomen and pelvis. Detection of free air, hemorrhage, and aortic dissection and/or aneurysm are among the few in CT analysis. Other applications include detection and characterization of hepatic tumors at MRI and automated processing and detection of lesions at CT colonography. Currently, none are FDA or CE approved.

Musculoskeletal and Spine

Offerings in this space are diverse and most focus on radiographs rather than CT or MRI. CT and MRI applications include spine fractures on CT scans and evaluation of osteoarthritis or ligamentous injury on knee MR images. Radiograph analysis again includes grading osteoarthritis in the knee, hip angle measurement, and fracture detection in the extremities and spine. Currently, the only FDA-approved algorithm is for detection of spine fractures on CT scans, and CE-approved algorithms include osteoarthritis classification based on Osteoarthritis Research Society International criteria.

Nuclear Medicine

Nuclear medicine applications in AI are rare, possibly due to the relatively low prevalence of these studies, coupled with the large variety of study types. Of nuclear medicine studies, PET/CT is the most common application. Current offerings include lung cancer staging in PET/CT, PET tracer binding quantification for dementia characterization on brain PET images, and quantification of the heterogeneity of tumor uptake to evaluate malignancy risk of the tumor. No nuclear medicine applications are currently FDA or CE approved.

Pediatrics

All current pediatric radiology applications focus on bone age classification. There are currently three companies in this space and although some are used clinically in Asia, none are FDA or CE approved.

Nonimage Interpretation

In this section, we will touch briefly on companies that focus on tasks other than direct image interpretation. These companies are not included in the previous figures.

Image Reconstruction

Several companies aim to improve the image quality of two- and three-dimensional modalities. In radiography, solutions include automatically correcting overexposure. In US, applications include real-time adjustment of gain to optimize image quality. In CT, several companies aim to improve image reconstruction techniques using AI to allow dose reductions without compromising image quality. Last, in nuclear medicine, applications include generating a virtual “full-dose” PET image using low-dose or shortened acquisition time images, thereby reducing radiotracer dose or imaging time. These are all currently FDA approved.

Exchange Platforms

Last, there are several companies that focus on building a radiology AI marketplace. Rather than develop AI algorithms, these companies aggregate multiple third-party algorithms into a single platform and allow a practice to select the algorithms of interest. There are pros and cons to this approach; pros include a larger selection of algorithms and an easy “one-stop shop” to see a large number of applications. The cons are that increased choice for a single clinical problem, such as lung nodule detection, can add confusion to purchasing decisions and does not directly address the need to pilot algorithms in-house to evaluate their efficacy. Furthermore, in order for multiple algorithms to exist in a single platform, many native software features, such as the ability to edit or remove detected lung nodules, may be disabled, as the algorithm integration is not as deep.

Conclusion

The promise and potential benefits of radiology AI software continue to grow, and radiologists, practice administrators, and IT staff must continue to educate themselves on the potential benefits, drawbacks, and costs of implementation. We encourage the reader to consider using the guidelines in the Table when evaluating companies to ensure all aspects of a purchasing decision are considered. Deployed correctly, these software can be a boon to both patients and providers in an ever-evolving health care setting with increasing imaging volumes and complexity.

Disclosures of Conflicts of Interest: Y.T. disclosed no relevant relationships. B.V. disclosed no relevant relationships. E.K. disclosed no relevant relationships. A.P. Activities related to the present article: disclosed no relevant relationships. Activities not related to the present article: disclosed ACR Innovation grant to author’s institution for project using AI to establish benchmark for radiology report complexity. Other relationships: disclosed no relevant relationships. J.G. disclosed no relevant relationships. N.S. disclosed no relevant relationships. H.T. Activities related to the present article: disclosed no relevant relationships. Activities not related to the present article: disclosed consultancy fees paid to author from Arterys and Verily. Other relationships: disclosed no relevant relationships.

Abbreviations:

- AI

- artificial intelligence

- CE

- Conformité Européenne

- FDA

- Food and Drug Administration

- PACS

- picture archiving and communication system

- ROI

- return on investment

- RSNA

- Radiological Society of North America

- SIIM

- Society of Imaging Informatics in Medicine

References

- 1.Morgan DJ, Bame B, Zimand P, et al. Assessment of Machine Learning vs Standard Prediction Rules for Predicting Hospital Readmissions. JAMA Netw Open 2019;2(3):e190348. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2.Huang K, Altosaar J, Ranganath R. ClinicalBERT: Modeling Clinical Notes and Predicting Hospital Readmission. arXiv: 1904.05342 [cs.CL] [preprint]. https://arxiv.org/abs/1904.05342. Posted April 11, 2019. Accessed December 10, 2019.

- 3.Hopkins BS, Yamaguchi JT, Garcia R, et al. Using machine learning to predict 30-day readmissions after posterior lumbar fusion: an NSQIP study involving 23,264 patients. J Neurosurg Spine 2019;32(3):1–8. [DOI] [PubMed] [Google Scholar]

- 4.Norrie J. Mortality prediction in ICU: a methodological advance. Lancet Respir Med 2015;3(1):5–6. [DOI] [PubMed] [Google Scholar]

- 5.Shimabukuro DW, Barton CW, Feldman MD, Mataraso SJ, Das R. Effect of a machine learning-based severe sepsis prediction algorithm on patient survival and hospital length of stay: a randomised clinical trial. BMJ Open Respir Res 2017;4(1):e000234. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Kuo W, Hӓne C, Mukherjee P, Malik J, Yuh EL. Expert-level detection of acute intracranial hemorrhage on head computed tomography using deep learning. Proc Natl Acad Sci U S A 2019;116(45):22737–22745. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Grzybowski A, Brona P, Lim G, et al. Artificial intelligence for diabetic retinopathy screening: a review. Eye (Lond) 2020;34(3):451–460 [Published correction appears in Eye (Lond) 2020;34(3):604.]. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.Raman R, Srinivasan S, Virmani S, Sivaprasad S, Rao C, Rajalakshmi R. Fundus photograph-based deep learning algorithms in detecting diabetic retinopathy. Eye (Lond) 2019;33(1):97–109. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9.Hosny A, Parmar C, Quackenbush J, Schwartz LH, Aerts HJWL. Artificial intelligence in radiology. Nat Rev Cancer 2018;18(8):500–510. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10.Bell J. What is machine learning. In: Machine Learning. Indianapolis, Ind: Wiley, 2015; 1–16. [Google Scholar]

- 11.Figueroa RL, Zeng-Treitler Q, Kandula S, Ngo LH. Predicting sample size required for classification performance. BMC Med Inform Decis Mak 2012;12(1):8. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12.Russakovsky O, Deng J, Su H, et al. ImageNet Large Scale Visual Recognition Challenge. arXiv: 1409.0575 [cs.CV] [preprint]. https://arxiv.org/abs/1409.0575. Posted September 1, 2014. Accessed December 15, 2019.

- 13.Fryback DG, Thornbury JR. The efficacy of diagnostic imaging. Med Decis Making 1991;11(2):88–94. [DOI] [PubMed] [Google Scholar]

- 14.Liew C. The future of radiology augmented with Artificial Intelligence: A strategy for success. Eur J Radiol 2018;102:152–156. [DOI] [PubMed] [Google Scholar]

- 15.Rodríguez-Ruiz A, Krupinski E, Mordang JJ, et al. Detection of Breast Cancer with Mammography: Effect of an Artificial Intelligence Support System. Radiology 2019;290(2):305–314. [DOI] [PubMed] [Google Scholar]

- 16.Geis JR, Brady AP, Wu CC, et al. Ethics of Artificial Intelligence in Radiology: Summary of the Joint European and North American Multisociety Statement. Radiology 2019;293(2):436–440. [DOI] [PubMed] [Google Scholar]

- 17.Yuan B, Li J. The Policy Effect of the General Data Protection Regulation (GDPR) on the Digital Public Health Sector in the European Union: An Empirical Investigation. Int J Environ Res Public Health 2019;16(6):1070. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 18.U.S. Food and Drug Administration . Artificial Intelligence and Machine Learning in Software as a Medical Device. https://www.fda.gov/medical-devices/software-medical-device-samd/artificial-intelligence-and-machine-learning-software-medical-device. Published 2019. Accessed April 30, 2020.

- 19.Yamashita R, Nishio M, Do RKG, Togashi K. Convolutional neural networks: an overview and application in radiology. Insights Imaging 2018;9(4):611–629. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.European Society of Radiology (ESR). What the radiologist should know about artificial intelligence - an ESR white paper. Insights Imaging 2019;10(1):44. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21.Lee MH, Schemmel AJ, Pooler BD, et al. Radiology Workflow Dynamics: How Workflow Patterns Impact Radiologist Perceptions of Workplace Satisfaction. Acad Radiol 2017;24(4):483–487. [DOI] [PubMed] [Google Scholar]

- 22.Dikici E, Bigelow M, Prevedello LM, White RD, Erdal BS. Integrating AI into radiology workflow: levels of research, production, and feedback maturity. J Med Imaging (Bellingham) 2020;7(1):016502. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23.Schemmel A, Lee M, Hanley T, et al. Radiology Workflow Disruptors: A Detailed Analysis. J Am Coll Radiol 2016;13(10):1210–1214. [DOI] [PubMed] [Google Scholar]

- 24.Choy G, Khalilzadeh O, Michalski M, et al. Current Applications and Future Impact of Machine Learning in Radiology. Radiology 2018;288(2):318–328. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 25.Gottlieb S. FDA Announces New Steps to Empower Consumers and Advance Digital Healthcare. https://www.fda.gov/news-events/fda-voices/fda-announces-new-steps-empower-consumers-and-advance-digital-healthcare. Published 2017. Accessed December 25, 2019.

- 26.Armato SG 3rd, McLennan G, McNitt-Gray MF, et al. Lung image database consortium: developing a resource for the medical imaging research community. Radiology 2004;232(3):739–748. [DOI] [PubMed] [Google Scholar]

- 27.MQSA Insights. https://www.fda.gov/radiation-emitting-products/mqsa-insights/2019-scorecard-statistics. Accessed April 30, 2020.

- 28.O’Donoghue C, Eklund M, Ozanne EM, Esserman LJ. Aggregate cost of mammography screening in the United States: comparison of current practice and advocated guidelines. Ann Intern Med 2014;160(3):145. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 29.Kumar R, Pal R. India achieves WHO recommended doctor population ratio: A call for paradigm shift in public health discourse! J Family Med Prim Care 2018;7(5):841–844. [DOI] [PMC free article] [PubMed] [Google Scholar]