ABSTRACT

Prescription drug spending in the USA has soared, fueled by rising drug prices. A critical mechanism for restraining drug prices is the formulary tiering system. Although tiering should reflect the cost of a drug—and reward patients who choose less-expensive drugs—something is seriously amiss. Using Medicare claims data from roughly one million patients between 2010 and 2017, this article finds troubling amounts of distorted tiering and wasted cost. Increasingly, generics are shifted to more expensive—and therefore less accessible—tiers. The percentage of generics on the least-expensive tier drops from 73% to 28%; the percentage of drugs on inappropriate tiers rises from 47% to 74%. Considering only costs paid by patients and the federal Low-Income Subsidy Program, tier misplacement cumulatively costs society $13.25 billion over the time period. An unruly problem demands a disruptive solution. This article advances the counterintuitive regulatory reform that tiering should be based on a drug’s list price. Yes, list price—that roundly dismissed figure—should become the touchstone. This would deter incentive-distorting rebate schemes while recognizing that many people already pay list price. It is a remarkably streamlined approach for cutting through a wide swath of perverse incentives and manipulations.

Keywords: drugs, formulary, pharmaceuticals, pricing, regulation, tier

I. INTRODUCTION: FORMULARY GAMES

Prescription drug spending in the USA has soared in the last decade, fueled by rising drug prices.2 Designer drugs, arriving with stunning price tags, are grabbing headlines,3 but day-to-day increases on ordinary medications are causing their fair share of pain. These included medicines for treating arthritis, diabetes, reflux, depression, high blood pressure, and high cholesterol.4

The pain of these rising prices reverberates through many levels of the system, including household consumer budgets. Nearly one in four Americans say that affording their prescription drugs is difficult, whereas three in 10 say they have not taken their medicines as prescribed due to costs.5 Government budgets are strained as well, as taxpayers support the increased costs of Medicare, Medicaid, and other government programs.6

With drug spending and other healthcare costs on the rise, healthcare has become a key focus across the nation. Eighty percent of polled voters consider healthcare an extremely or very important issue, more than any other topic.7 Moreover, the anxiety about healthcare costs cuts across party lines: 87% of Democrats and 72% of Republicans consider it a critical issue, making it the first and third most pressing concern for each voter bloc, respectively.8 In the first four debates of the 2020 election, Democratic presidential hopefuls spent more time discussing healthcare than any other topic—roughly twice as much as other frequently mentioned topics such as foreign policy and climate change.9 In the polarized political climate of this era, one would be hard pressed to think of another issue that so unifies the American public.

A critical mechanism for restraining drug spending is the formulary system, which dictates the drugs for which patients will receive reimbursement. The roots of the system can be traced back to the American Revolution—when the Continental army developed a list of reliable medicines—although modern formulary systems have gradually expanded far from their historic roots. Today’s formularies are divided into tiers that determine just how much a patient will pay. When drugs are on low tiers, such as Tiers 1 and 2, the patient pays less. When drugs are on high tiers, such as Tiers 4 and 5, the patient pays more.

In theory, tiering reflects the cost of a drug—and rewards patients who choose generics over brands.10 The patient’s copay is less, the cost to the healthcare system on the whole is less, and the market for cheaper drugs thrives. In other words, tiering should be part of a virtuous cycle creating the proper market and system incentives. That is the concept, in theory, but something is seriously amiss. In fact, the tiering system has gone off its rails.

Prior to this article, anecdotal evidence had suggested that something odd is happening in the tiering system. Press reports and scattered lawsuits have hinted that at least some health plans are punishing patients for purchasing generics, rather than brand-name drugs, or excluding generics from reimbursement.11 In light of these clues, this study set out to examine, on a systematic basis, whether tiers are doing their jobs. The study follows roughly one million Medicare patients from 2010 to 2017. In the process, the study finds clear evidence of widespread irrational tiering and wasted spending. By placing costly brand-name drugs on preferred tiers while placing cheaper generics on more-expensive tiers, the principal actors involved have cost patients and the government billions of dollars.

To understand how dollars are wasted within the formulary system, the study focuses on whether cheaper drugs are being placed on more-expensive tiers relative to more expensive competitors. In order to define competing drugs, the study applies the novel concept of ‘therapeutic competitors’, a term that has not been previously used in the literature.

An existing term of art, ‘therapeutic equivalent’ is too narrow to fully capture market dynamics. To be therapeutically equivalent under the Food and Drug Administration’s (FDA’s) definition, the main active ingredients must be the same, as well as the dosage form, route of administration, and strength.12 Drug companies compete with drugs far beyond drugs that mirror each of these parameters. Thus, equivalence provides only a limited view of market competition. Other drug classification systems fail to capture the full competitive picture, particularly with drugs that are marketed for off-label uses.13

Drug companies undoubtedly know which drugs compete with their own, even if those drugs only compete off-label or in certain subsections of the market. The concept of ‘therapeutic competitors’ encompasses this broader range of market dynamics. As described below,14 this study examines a subset of therapeutic competitors defined as drugs containing the same active ingredient. Within this framework, the study quantitatively examines certain instances of irrational tiering in the formulary system—specifically, instances in which two or more drugs with the same active ingredient (such as a brand and a generic) are improperly placed on the same tier or when the cheaper drug is placed on a more-expensive tier.

The results are striking, but empirical results are of little use to society if they simply set off rounds of finger-pointing—an activity that has been rampant in Washington DC since the nation has focused its attention on drug pricing. Drug companies blame both health insurers and middle players known as pharmacy benefit managers (PBMs); PBMs blame drug companies; and so on.15 Finger-pointing exercises, however, are rarely productive (except perhaps in piano practice). And as academic literature suggests, there is plenty of blame to go around.16 To varying degrees, many players are profiting on the backs of patients and the government. These players are, after all, profit-making entities, and they are likely to respond to the incentives created by the system. Thus, at the end of the day, finger-pointing merely distracts from the task at hand: creating a better legal framework that more successfully aligns public and private incentives. And in a free-market system, those incentives necessarily include encouraging the competitive forces that erode monopoly positions and bring prices to competitive levels.

Price, of course, is a murky term in the world of prescription drugs. Drug companies point out—and rightfully so—that headline-grabbing list prices do not necessarily reflect the price of an individual drug purchase.17 Rather, the actual price of an individual drug purchase can only be determined after subtracting rebate amounts, which themselves will be determined long after the patient has left the drug counter. Those rebates will be calculated based on complex formulas established in contracts between drug companies and middle players known as PBMs.18 Drug companies and PBMs assert that the pricing information is a trade secret, with the result that health plans, and even plan auditors, are not allowed to know the full terms of the contracts or the net price of drugs.19 In other words, true net price is a slippery term that is disassociated from key buying moments and decisions.20

An unruly problem demands a disruptive solution, and therein lies the startling recommendation that emerges from this work. ‘One actually need not know the true net price.’ Rather, one can restore sanity to drug pricing without the parties actually knowing the true price. To repeat for emphasis, one can fix price without knowing the price, at least in the context described in this article. To accomplish this feat of magic, tiering should be based on list price. Yes, list price—that badly maligned, roundly dismissed figure—should become the touchstone.

Focusing on list price eliminates the need to ferret out and decipher complex deals. It also avoids the practical problem of navigating around the parties’ claims that trade secret law protects net price information.21 Further, focusing on list price is grounded in the reality that many patients payment do reflect the list price, either because (i) they must pay the full list price before reaching a deductible, (ii) they lack complete drug coverage or any drug coverage at all, or 3) their co-sharing payment is determined as a percentage of the list price.22

Using list price also has the happy side effect of disincentivizing the rebate and quasi-kickback games that drug companies use and middle players demand. Those games are like raising the price of a jacket before a sale, so the sale price looks appealing.23 Unfortunately, many people end up paying the pre-sale price for the jacket—and, of course, many people pay the full price for drugs.24 Worse yet, as this study demonstrates, drug prices are rising at a faster pace than rebates, with the result that the rebates only begin to offset the substantial increases.25 Finally, rebate games create bloated spending (because middle players pocket the spread) and harm competition (because drug companies provide rebates so that cheaper competitors are disadvantaged).

Despite widespread recognition of the problem, complex legislative and regulatory attempts to reform this practice have failed.26 In contrast, a simple, Congressional or regulatory mandate that government programs use list prices for tiering would sweep aside the incentives for playing the rebate game. Back-room negotiations and tempting rebate payments would not matter. The price is the price.

Although there is no silver bullet, and all approaches have challenges, basing tiering on list price is a remarkably streamlined approach for cutting through a wide swath of perverse incentives and manipulations. After all, at the end of the day, it is the price that matters.

II. FORMULARIES, DRUGS, AND PRICES: AN OVERVIEW OF THE HEALTHCARE SYSTEM

II.A. A Brief History of Formularies

Formularies, at the most basic level, are a list of medicines. Formularies for hospitals have existed in the USA since the days of the American Revolution when the Lititz Pharmacopeia was published in 1778 for use by the Continental forces.27 It was not until 1816, however, that a formulary for a private civilian hospital was compiled, which was called the Pharmacopeia of the New York Hospital.28 Four years later, the first national pharmacopeia in the USA was published, with the objective of ‘select [ing] from among substances which possess medicinal power, those, the utility of which is most fully established and best understood’.29 It is unclear when the transition of terminology from ‘pharmacopeia’ to ‘formulary’ occurred in the USA.30 Historians document, however, that the idea of a formulary as a simple clinical management tool was established in the USA early on in its history.

Following World War II, formularies expanded beyond the role of merely identifying clinical sufficiency and entered the realm of supply and inventory management. The immense scale and sophistication of the penicillin development effort during the war marked a new era for the pharmaceutical industry’s approach to developing drugs, ushering in unprecedented levels of new development and mass production.31 As many more medications became available to treat a range of diseases, hospitals began to use formularies for managing and controlling their drug inventory and supply needs.32 Formularies edged closer to government regulation in 1965. In that year, the private, nonprofit organization for evaluating hospitals—now, known as The Joint Commission—began requiring that hospitals maintain an active Pharmacy and Therapeutics Committee that would communicate on drug-use issues.33 At this point, formularies were recognized as a useful tool for hospitals, rather than a broad tool for all health insurers, and governmental agencies had yet to apply formal, widespread regulation.

The first, widespread, formal government regulation of formularies—outside of episodes such as military use in the American Revolution—occurred with the passage of the Social Security Amendments of 1965. In addition to having an impact on drug development, the period following World War II saw changing attitudes about federal administration of the Social Security Program.34 Prior to that time, states were viewed as the preferred administrators of health insurance and other forms of social insurance. Following World War II, the view shifted entirely, and states were viewed as unreliable and inefficient administrators of social welfare programs, who, by handling the same social problems in highly disparate ways, created chaos rather than coherence.35

As a practical matter, states were already too embedded in the welfare system to be swept aside.36 Thus, when the Social Security Amendments of 1965 created the Medicare and Medicaid Programs, the Amendments established Medicaid as a joint effort between the federal and state governments to provide basic hospital insurance for the poor.37 The same legislation established Medicare, designed to provide basic hospital insurance for the elderly, as a program administered by the Federal Government.38 Thus, 1965 marked the beginning of formal, federal government regulation of formularies, but only in their capacity as a useful tool for hospitals.

In the 1970s, formularies evolved beyond hospital use to become an essential cost control tool for health insurers in the outpatient realm. Unexpectedly high Medicare expenditures, rapid inflation, expansion of hospital expenses and profits, and changes in medical care contributed to the escalating healthcare costs in the 1970s.39 The increasing healthcare costs drove a paradigm shift in health insurance, away from fee-for-service reimbursement and toward a managed care environment.40 Enrollment in managed care organizations surged, and insurers began to look for ways to control costs, including the prescription drug benefit.41 Most health plans already had experience with hospital formularies, and insurers initially considered using formularies that took a unified approach to medications for inpatient and outpatient care.42 The cost of medication varied tremendously, however, between hospital pharmacies and community pharmacies, even for the same drug.43 Insurers, therefore, needed a separate outpatient formulary.

As formularies entered into widespread use for cost control, however, they had yet to expand into the final, key role for today’s modern formulary: a tool for drug selection and rebate negotiations with drug manufacturers. This final step would fall into place through a combination of the 1980s Hatch–Waxman Act (for the rapid approval of generic drugs)44 and the Medicare Modernization Act of 2003 (offering prescription drug benefits to all Medicare beneficiaries).45 Hatch–Waxman created a wave of generics entering the market, including multiple generic versions of some medications.46 With the influx of competing drugs, brand companies began offering rebates to health insurers, in exchange for preferred placement on formularies.47

In the Medicare Modernization Act, Congress expanded Medicare to include widespread coverage of drugs that patients purchased at a retail pharmacy, as opposed to those related to hospital stays.48 Just as Hatch–Waxman brought a wave of additional competing drugs, the Medicare Modernization Act brought a wave of additional patients who had insurance coverage for day-to-day prescription medications. Thus, throughout the early 21st century, the modern formulary system evolved into a tool that health insurers used, not just for cost control but also for drug selection and as leverage with manufacturers to obtain rebates.

Implementation of the Medicare Modernization Act also transformed the rising PBM industry in healthcare. PBMs originated in the 1970s, emerging largely as claims processors.49 The industry changed in the 1990s, with the advent of electronic claims. That shift, however, was minor in comparison to the tectonic shift that occurred as the Medicare Modernization Act became fully implemented in 2006.50 With the influx of new patients having prescription drug coverage, PBMs took on a new responsibility for their clients, the insurers: negotiating rebates with drug manufacturers, as well as helping design and manage formularies. This final, historic shift led to the modern formulary as a drug choice tool for health insurance plans with the dual goals of clinical effectiveness and cost control. In the words of one PBM executive, tiering is designed to ‘encourage desirable outcomes while saving considerable costs….Treatment—not just prescribing—becomes better and more cost-effective. Ultimately, overall health care improves’.

II.B. The Modern Formulary

The majority of patients in the USA rely on a health insurance plan to cover at least part of their prescription drug cost. As described above, the core of this system is a plan’s drug formulary, which determines both which drugs will be covered by insurance and how much customers will pay through the plan.51 In the modern context, formularies also function as a way of translating complicated pricing information into relatively easily understood, out-of-pocket costs for individual insurance plan subscribers.

Insurance companies create formularies to differentiate preferred and nonpreferred drugs by using a multi-tier system. When a drug is on the lowest tier—tier one—patients who buy the drug have lower cost-sharing burdens; when drugs are on higher tiers, patients pay more. A patient’s payment can come in the form of a flat copay, a percentage of the cost of the drug (which is known as co-insurance), or a combination of both.52 Thus, when drugs are on the same tier, patients will have the same copay amount, regardless of the drug’s wholesale price. Any co-insurance amount, however, could vary.

The following is an example of a five-tier formulary, provided by a BlueShield health plan, which is typical of five-tier formularies:53

| Tier 1 | The prescription drug tier that consists of the lowest-cost tier of prescription drugs: most are generic. |

| Tier 2 | The prescription drug tier that consists of medium-cost prescription drugs: most are generic and some brand-name prescription drugs. |

| Tier 3 | The prescription drug tier that consists of high-cost prescription drugs: most are brand-name prescription drugs. |

| Tier 4 | The prescription drug tier that consists of the higher-cost prescription drugs: most are brand-name prescription drugs and some specialty drugs. |

| Tier 5 | The prescription drug tier that consists of the highest-cost prescription drugs: most are specialty drugs. |

Although specialty drugs are normally placed on nonpreferred tiers, the definition of a specialty drug can vary among plans and within literature. Medicare sets a floor (at least $670 per month in 2019) to define a drug as ‘specialty’.54 Beyond Medicare and in general, high list prices tend to distinguish specialty drugs from other drugs, along with four corollary features: treating rare conditions, requiring special handling, using a limited distribution network, or necessitating ongoing clinical assessment and monitoring.55

An insurance plan will normally cover only the drugs listed on its formulary tiers. For all other (nonlisted) drugs, patients will have to pay the full price out of their own pockets.56

One can think of tiering as loosely analogous to product placement in a grocery store. A company will sell more of its soda cans if the cans are placed on the end-cap display of a grocery aisle than on the top shelf of the drinks section. Thus, to the extent tier placement is intended to incentivize the purchase of drugs that the health plan prefers, the plan is placing the drugs certain drugs on the end cap. The term ‘loosely analogous’ is used because patients cannot decide what prescription medicine to purchase alone. The doctor’s prescription drives the purchase, and both patient and doctor may suffer from insufficient information to make pricing-based choices. Thus, being on the ‘end-cap’ of the prescription drug-pricing tier is not a perfect incentivizing mechanism. Nevertheless, the tiering system is designed to drive choices in the market, however imperfectly that market operates.

In modern formularies, one of the most important factors for tier placement involves deals between PBMs and drug manufacturers. As described above, PBMs are the middle players who negotiate with drug companies on behalf of health plans and help the plans create their formularies.57 PBMs that can promise drug companies a certain amount of revenue (ie sales volume) from a particular health plan can obtain sizable rebates off the list price for a particular drug. In theory, the PBM’s ability to negotiate with drug companies should lead to lower prices for prescription drugs, ultimately improving consumer welfare for individuals.58

In short, the modern formulary theoretically serves not only as a tool for ensuring that drugs are clinically effective, it also helps to control the cost of prescription medication, minimizing health plan spending and patient out-of-pocket costs. This is accomplished through a combination of prioritizing generics over brand drugs and preferred brands over nonpreferred brands. Price, however, is a slippery term in the modern world of pharmaceuticals.

II.C. The Price of a Drug

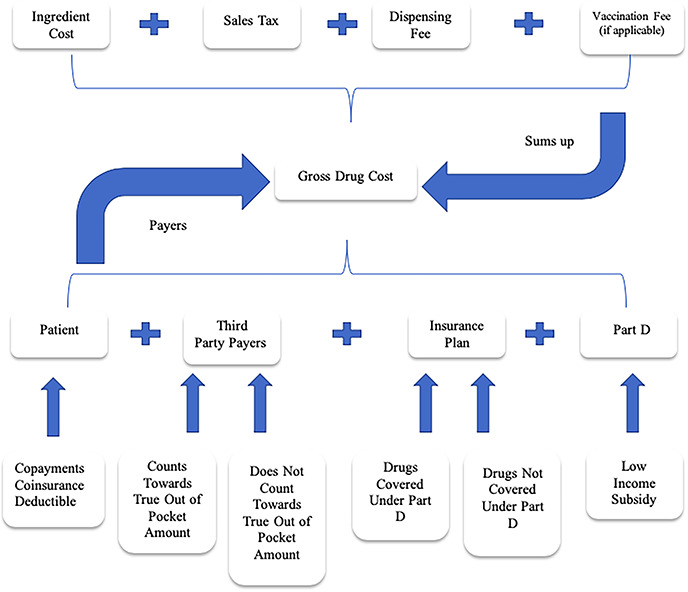

The strange and shrouded notion of price in the pharmaceutical industry begins in a perfectly ordinary fashion. Drug companies sell their product to wholesalers. The price of a drug, however, will quickly dissolve into a tangle of timing oddities, rebates, and an impressively obscure alphabet soup of terms used in the industry—wholesale acquisition cost (WAC),59 maximum allowable cost (MAC),60 average wholesale price (AWP),61 average sales price (ASP),62 estimated acquisition cost (EAC),63 and others—many of which lack a consistent definition, are unverified, or are not based on actual sales transactions. Despite all of this, drug price begins with drug companies selling their products to wholesalers; that basic price is already reported to the federal government. The figure, which must be based on actual sales, is statutorily defined and reported to the Centers for Medicare and Medicaid Services (CMS).64 For simplicity, this paper will refer to this critical figure as the wholesale price of the drug.

Various other indexes are available as a measure of wholesale price, although each one is flawed. For example, drug companies voluntarily supply reports to third-party commercial services that, in theory, report the price at which the companies sell to wholesalers.65 Drug-makers also voluntarily provide the average of that cost to the third-party commercial services.66 Both sets of figures are unverified, and the Health and Human Services (HHS) Office of Inspector General has reported that those numbers are not necessarily based on actual sales.67

In theory, the patient would pay the wholesale price with a small markup for the wholesaler’s profit—in other words, the ‘list price’. In many circumstances, however, the list price is only the beginning. Drug companies offer substantial rebates to health plans, generally in recognition of the volume of product that the health plan’s patients will purchase.

This critical juncture is where the system begins to go off the rails. As noted above, middle players, known as PBMs negotiate prices on behalf of their health plan clients. The health plans pay PBMs based on the size of the discount that the PBM can wrestle from the drug company, sometimes even allowing the PBMs to pocket part of the spread.68 This method—called spread pricing69— should lead PBMs to negotiate more substantial discounts, which would, in turn, lower net prices. After all, one would negotiate hard for discounts if one’s pay were determined by the size of that discount.

Perverse incentives and strategic behaviors, however, have derailed the process. To increase the spread and profitability for the PBMs, drug companies can raise the list prices of their drugs and then offer steeper rebates. As a result, PBMs can report a greater spread, thereby increasing their pay, even if net price remains the same or increases.70 This creates upward pressure on drug prices, as drug companies offer—and PBMs demand—greater and greater spreads.

The spread pricing and rebate system might be less of a problem if no one actually paid the higher price but many people do. Some health plans require that patients pay the full amount for a drug until reaching a deductible level.71 The full amount is the list price and ignores all rebates. Other plans require that patients pay a co-share amount based on a percentage of the full list price.72 Some patients lack health insurance or lack plans that cover medications.73 Even when full Medicare coverage is in place, gaps can occur that leave patients paying the full cost of the drug.74 Most importantly, prices are rising faster than rebates.75 Thus, for those who do not pay the full list price, the cost of drugs is increasing at an alarming rate, even with rebates.

The timing of rebates completely obscures the actual price of any individual drug transaction. When a patient goes to the pharmacy to purchase a prescription drug, the price includes the list price—that is, the wholesale price with markup for the wholesaler’s profit—plus a small markup for the pharmacists. To cover that cost, the pharmacist collects the patient’s copay or co-insurance amount, along with the insurance plan’s contribution (generally processed by the PBM).76 Rebates arrive long after the patient has left the pharmacy counter. A health plan’s PBM will provide rebates to the health plan that cover a large number of drug transactions and likely a large number of drugs. Thus, for example, a health plan knows what it paid for a particular patient’s heart medication at the point of the sale—and what it paid overall for all transactions. Nevertheless, the plan never knows the true net price, because the rebate on that purchase will be lumped with rebates for many other transactions and delivered long after the patient has left the pharmacy counter.

Timing and aggregation are not the only issues obscuring net prices. After all, a plan could simply disaggregate those prices to obtain net prices, at least some time down the road. The rebate amounts, however, normally flow from long and complex calculations that are set out in contracts between the PBM and the drug company. Drug companies and PBMs claim that net prices, and the calculations that produce those net prices, are trade secrets. Although courts have not squarely addressed whether that information constitutes a trade secret77 and academics have cast doubt on the claim,78 the information is fiercely guarded, even from the PBMs’ own client, the health plan. The health plan’s auditors are not even allowed full access to the terms.79 As a result, actual net prices are hidden—from the patient, from the health plan, from government regulators, and from pesky academics. Lack of information makes it difficult for government regulators to ferret out inappropriate behavior—or reform the process—and for patients to make fully informed decisions about drug purchases and health plan purchases.

Moreover, the PBM industry is highly concentrated, with three PBMs controlling 85% of the market.80 Given the market structure, PBMs reportedly engage in lockstep demands, making it difficult for health plans to bargain for different terms.81

The system benefits drug manufacturers as well. In exchange for the lucrative rebates that drive PBM profitability, drug manufacturers can demand that the PBM guarantee a certain volume flow from the health plan’s patients by giving their drugs exclusive or preferred formulary placement. These volume rebates allow drug companies that hold a substantial position in the market to prevent new competitors from gaining ground.

In competition terms, one can conceptualize this as a form of raising rivals’ costs, that is, engaging in a behavior that will impose costs on your competitor without imposing similar costs on you.82 Imagine if Budweiser approached bar owners in a state offering $1 off each bottle of Bud sold, if the owners agree not to put any craft beers on the menu.83 If the bar owners normally sell two million bottles of Bud in a year, that offer is worth $2 million. Now imagine a small craft beer company trying to break into the market—an entrant that might start off by selling 10,000 bottles at $3 each. Even if the new entrant discounted the price down to a single penny per bottle in comparison to the normal $3 price, the bar owners would save only about $30,000. The new entrant could never match Budweiser’s $2 million offer to the PBM. And remember, the PBM will be paid based on the amount of the discount spread, and it may even be able to pocket the spread.

The danger of volume rebates can be more pronounced in the context of large drug manufacturers offering a variety of drugs. A drug company offering multiple drugs can use its market dominance in one drug to protect its less competitive drug. And of course, brand drugs whose patents are expiring may hold monopoly positions that allow for this type of volume rebate behavior.84

Anecdotal evidence has hinted at abuses in the formulary system, driven by the incentive structure in place and the type of strategic behaviors described above. One lawsuit alleged that health insurance plans essentially excluded a lower-priced version of the arthritis drug Remicade, following bundled rebate deals from the brand.85 Another alleged that a vaccine company significantly raised its prices for any consumers that did not buy a certain number of its bundled drugs, in order to prevent customers from jumping ship to a recently introduced competitor.86 Another alleged that a company used bundled rebates and exclusive formulary contracts to disadvantage competitors of the blockbuster dry eye medication, Restasis.87

Outside the lawsuit setting, press and individual reports have described patients paradoxically paying a ‘higher’ co-share for filling their prescriptions with the generic and a lower co-share for buying the brand.88 The press piece reported of pharmacists being told in 2017 that some Medicare plans, with formularies designed by the same PBM, would cover only the brand version of 12 drugs, despite the fact that some of the drugs had generic competitors on the market.89 In the same vein, generics and consulting industry sources have asserted that patients are being overcharged for generics and that generics are being placed on irrational tiers, harming the generics industry and inflating patient costs.90 These sources provide few details on the assertions, however.

Although academic research on tier placement is sparse, the literature suggests that over the past decade, a number of players in the pharmaceutical industry have engaged in strategic behavior related to tiering. One paper, for instance, found that insurers used tiers as a way around the Affordable Care Act’s laws barring discrimination based upon preexisting conditions.91 Patients who are human immunodeficiency virus (HIV) positive may have greater medical needs and higher-cost medications. By placing all HIV drugs on the highest-cost tier, insurance companies discourage high-cost, HIV-positive patients from enrolling.92

Researchers also have identified tiering behaviors designed to evade other aspects of the Affordable Care Act, such as those related to the Essential Health Benefits Provision.93 This provision requires that health insurers must cover at least one drug in each class and that all drugs must be covered in six protected classes. The provision does not regulate related dimensions of formulary design, such as cost-sharing and tier placement.94 As a result, insurers may comply with the Affordable Care Act while also undermining the Act’s goals of expanding prescription drug access for patients by manipulating tier placement. One econometric study, for example, found that while insurers complied with the Affordable Care Act’s provisions to cover additional drugs, compliance increased the probability that a newly covered drug was assigned to a more-costly formulary tier.95

Along the same lines, protests alleging discrimination in tiering have been lodged with state and federal regulatory agencies. For example, two groups filed an administrative complaint with the federal Department of Health and Human Services’ Office for Civil Rights arguing that four insurers violated the Affordable Care Act’s nondiscrimination provisions through adverse tiering on their plans in the federal health exchange in Florida.96 The complaint settled, with the insurers agreeing to improve the tier placement of HIV medications, which would, in turn, make those medications more affordable.97 In Georgia, letters from a state senator and a coalition of groups successfully convinced the Georgia Department of Community Health to maintain certain HIV medications on the preferred tier of the state’s Medicaid formulary, rather than downgrading them.98

Studies outside the academic realm report other types of concerns with formularies and tiering. One investigative journalism piece, for example, found that when pharmaceutical companies gave perks to doctors voting on Medicaid systems, those doctors were more likely to recommend placement of the pharmaceuticals on state formularies.99

In light of the many allegations, the study sets out to examine empirically whether evidence exists of widespread irrational tiering—along with problems created by that irrationality—and if so, how to address the problems. To do so, the study follows roughly one million Medicare patients from 2006 to 2017, examining all of the cohort’s drug purchase claims filed during this period. These data are available for purchase from the federal government through the CMS.100

Medicare provides a particularly useful pool of information for studying health insurance tiering. The availability of detailed, government-verified claims data provides an excellent basis for empirical research, particularly given that similar information on private insurance plan patients is not available to researchers.101 Moreover, Medicare has significant market presence and purchasing muscle, accounting for 29% of the money spent on prescription drugs in the USA. Compared with an analysis of all insurance plans with prescription drug coverage, however, there is presumably less variation in a number of factors, including: the drugs the cohort buys, how the drugs are covered by their insurance, the prices that they pay, the kind of rebates one expects the plans to obtain, etc.102 Nevertheless, certain problems within the Medicare system are likely to apply to the US health insurance system as a whole, making Medicare a fertile research venue. Moreover, for reasons of political expediency discussed below, it may be easier to craft initial reforms within the Medicare system.103

Developing a methodology to test the hypothesis was no easy task, given that legislators, regulators, and researchers are caught in a bind. As noted above, drug companies assert that drug prices constitute trade secrets. Thus, true price is shielded even from health plans themselves—wrapped in layers of aggregated rebates, which are paid long after any individual drug purchase takes place.104 Worse yet, there is no consistent definition or list of brand versus generic drugs.105

The study’s analysis breaks through these barriers to reveal what is happening behind the tiering curtain. A detailed methodology, including statistical significance testing, will be made available to guide future researchers who wish to expand on or confirm the results.106

The results of the study confirm that the manner in which drugs are currently being placed on formulary tiers is adversely affecting patients and costing society. The sections below will describe the results and analyses in detail, but key conclusions include the following:

From 2010 to 2017, the percentage of generics on the least-expensive tier drops from 73% to 28%. The shift creates considerable burden for patients, given that the average copay triples when a drug moves from the first tier even up to just the second tier.

During the same period, the percentage of drugs placed on inappropriate tiers in relation to drugs with the same active ingredient increases from 47% to 74%.

Considering only patient out-of-pocket costs and payments from the federal Low-Income Subsidy program, abuses of the formulary system conservatively costs $13.25 billion over the eight-year period, with the costs rising significantly from the beginning to the end of the period.

After factoring in rebates, the average dosage-unit price for brand drugs increases by 313%, whereas the average dosage-unit price for generics remains stable.

III. STUDY DETAILS AND RESULTS

A few notes may be helpful at the outset. First, CMS began recording complete formulary data in 2010.107 Thus, certain analyses cover only the eight-year period from 2010 to 2017, rather than the entire 12-year study period. In addition, although the number of tiers in a health plan’s formulary can range from three to seven, the study finds that plans with five tiers were the most common configuration within the data. This finding is consistent with other reports.108 Thus, for the calculations related to tiering, the study focuses on five-tier plans. Finally, although data on the rebates for individual drug purchases are never available in any form, the Medicare Trustees Report provides average rebate data across all drugs for a particular year. That figure could be used to derive the average rebates for brand drug manufacturers, a calculation that is set out in Appendix A2.

Before delving into an analysis of formulary tiering, the study begins by examining the availability of drugs and the amounts that patients paid for their prescriptions, to verify the commonly held assumption that the rising availability of generic drugs leads to lower patient expenditures. This assumption lies behind modern initiatives to increase the number of available generics as an antidote to concerns about rising pharmaceutical prices and patient costs.109

An examination of the claims data finds that over the time period, an increasing percentage of the drugs on formularies were, indeed, generics rather than brands.110 If the formulary tier system works as hypothesized, patient expenditure should, therefore, decrease. However, the study shows an entirely different picture. Patients, on average, pay more for both brand and generic drugs between 2006 and 2017. In this 12-year period, the average amount patients pay for brand drugs increases drastically, rising from $18 to $47. Thus, a patient’s out-of-pocket payment for each brand drug more than doubles during the 12 years of the study—and this is only for prescriptions that were covered. Although the increase in average price paid is less stark, generic prices still rise 75%, from $4 to $7. Given these results, the study finds that the growing prevalence of generics has not prevented rising costs for consumers. In other words, from the perspective of what a patient specifically pays out-of-pocket, more generic drugs alone do not solve the problem of rapidly increasing drug prices.111

It is important to emphasize that these figures are for patient out-of-pocket costs. During the same period, the net price of generic drugs stays roughly stable.112 One would not expect the patient’s payment burden to rise 75% for generics when the insurance plan’s cost of acquiring those drugs remains the same.

III.A. Broadening the Lens: Dosage-Unit Prices for Brands and Generics

The analyses above examine average patient out-of-pocket costs for brand and generic drugs. To broaden the lens on drug prices, the study examines other aspects of drug prices—not just those paid by the patient. Drugs can be dispensed in different dosages, creating the need for a method of normalizing dosages and prices across different drugs. To solve this problem, the study uses a novel metric: the average dosage-unit price.

Consider an analogy from the beer industry. Imagine a 12-pack of Bud Light cans standing next to a single bottle of Heineken. To compare pricing between the two, one would need to consider the price of one ounce of Bud Light in comparison to one ounce of Heineken.

As described below, this novel metric also allows the study to examine the ever-elusive category of prices after rebates. Specifically, the study finds that rebates are not fully eliminating price increases. Rather, the price of brand drugs continues to rise at an astonishing pace, even after factoring in rebates. Moreover, the cost of a brand drug far exceeds the cost of a generic. After factoring in rebates,113 the average dosage-unit price of brand drugs overwhelmingly exceeds that of generic drugs. In the discussion below, the article uses the term, ‘net price’, to refer to the price after factoring in rebates.

As described above,114 net prices are important for understanding the true price trajectory of a drug. If the list price of a drug rises, but the drug company discounts the drug by the amount of the rise or more in the form of a rebate, it would be misleading to suggest that the price has risen at all. With drug companies asserting that net price information constitutes a trade secret—a secret so delicate that it cannot be revealed even to the health plan itself—one cannot fully analyze drug prices.

This conundrum has stymied researchers and policymakers for years. Drug companies can defend against criticisms of rising drug prices by noting that prices are lower than anyone realizes due to rebates—and then refuse to reveal any information about the rebates. Any discussion of drug prices becomes a game of shadow boxing.

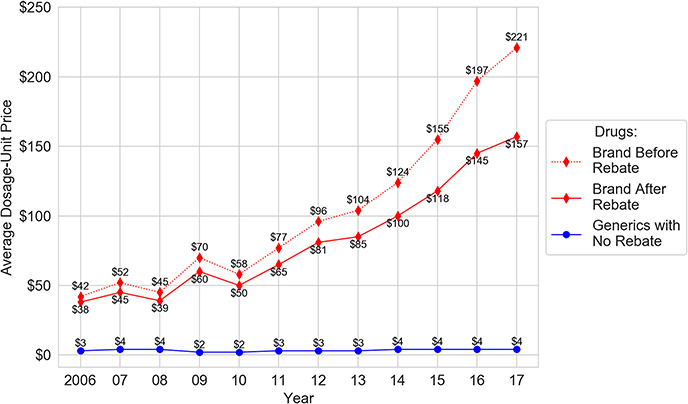

The study breaks this impasse. Using actual claims data and applying the methodology of dosage-unit price, the study shows that net prices climb dramatically between 2006 and 2017. As Figure 1 demonstrates, ‘after rebates’, the average dosage-unit prices for brand drugs experiences a shocking 313% increase across the decade. Specifically, the average dosage-unit price of brand drugs after rebate increases from $38 to $157, whereas generic drugs remain at a relatively stable $3–4.

Figure 1.

Average dosage-unit price.

One should note the following: The previous section found that the out-of-pocket costs patients pay for generics rises 75% to roughly $7 per prescription across the study period. This section finds that the average dosage-unit price ‘health insurers’ pay remains roughly stable. Thus, patient expenditures for generics are rising, whereas insurers pay roughly the same amount for generics over time.

In short, although rebates rise over the decade, prices rise faster, outstripping the effects of the rebates. Most important, the prices for brand drugs, both before and after rebates, soar far above the price of generic drugs.

The net price, however, is not the only relevant figure; understanding the list price is important for a different aspect of price trajectory. Quite simply, many people do pay the full list price—at least at certain times—and others have payments that are tied to the list price. Specifically, some patients pay full price until reaching a deductible; some pay co-insurance as a percentage of the list price, rather than a flat copay. Thus, the study also examines list price information.

Unsurprisingly, the trajectory for the list prices paid by health insurance plans is far worse than for net prices. Between 2006 and 2017, the average dosage-unit list price for brand drugs rises dramatically from $42 to $221, a 426% increase. In contrast, the average dosage-unit price that health plans pay for generics remains relatively stable at a low $3 to $4.115

III.B. The Shrinking Access to Generics

No matter how broad the lens, prices alone do not explain the full story of drug accessibility in the USA. As discussed in previous sections, insurers organize their drugs within tiered formularies. Tiering ought to reflect the cost of a drug, with cheaper generics placed on lower, less-expensive tiers and expensive brand drugs placed on higher, more-expensive tiers. Insurers reward patients who choose cheaper drugs by requiring smaller copays; more expensive drugs on higher tiers, in contrast, command progressively large copays.116 The formulary system, in theory, drives down patients’ copays, reduces overall healthcare costs, and promotes the market for cheaper drugs.

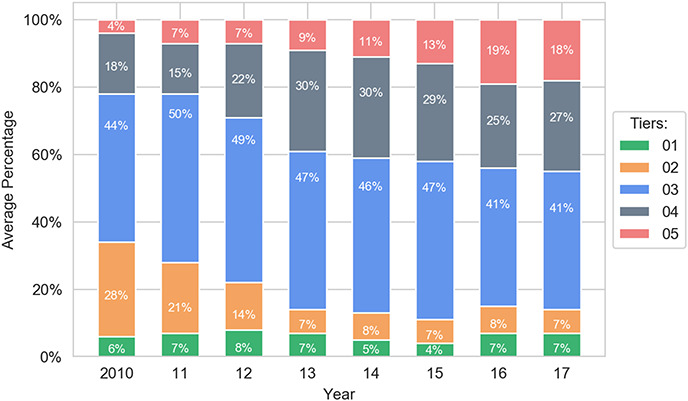

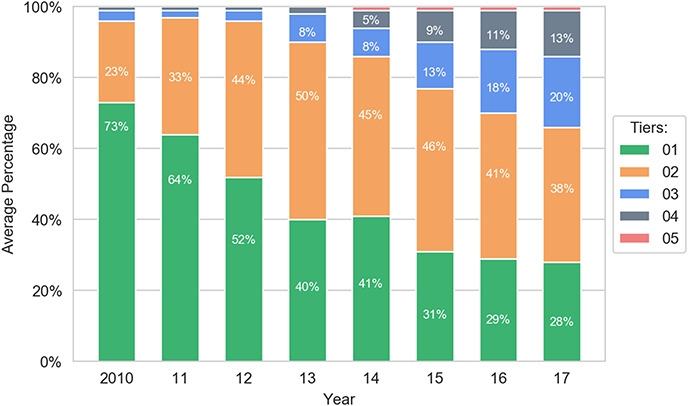

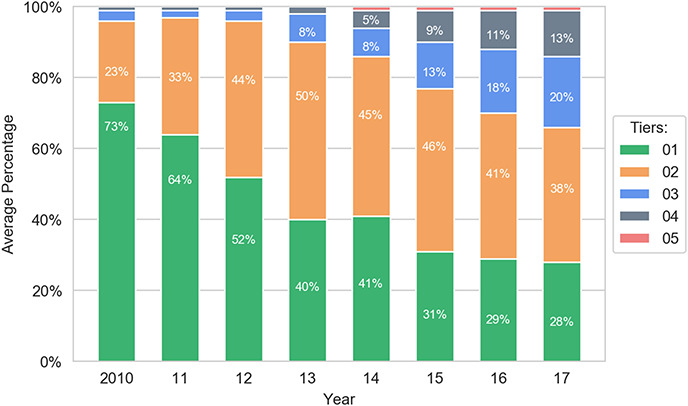

The primary goal of the study involved empirically assessing whether the formulary system is working as it should. Strikingly, the analysis reveals strong evidence of distorted tier placement for generic drugs. First, generics are increasingly placed on tiers that have higher costs for patients. For example, in 2010, 96% of generics are placed on the two least-expensive tiers combined, formulary Tiers 1 and 2; by 2017, this number shrinks to 66%. In particular, there is a serious decrease in the percentage share of generics on Tier 1—the tier with the lowest cost for consumers—compared with all other tiers. On that golden tier, the percentage of generics drops from 73% to 28% between 2010 and 2017.117 This occurs even though the cost that health plans pay for generics remains stable.118

One might speculate that the reduction of the percentage of generics on the first tier occurs because health plans are choosing one generic to favor over another generic. However, given that tiering should reflect price119 and generics do not compete on price,120 there should be no reason to preference certain generics over others in the widespread manner that the study reveals, absent other economic distortions. To the extent additional economic distortions are occurring, it may reflect other market dynamics that are beyond the scope of this paper.

The data also show an increase in the percentage of generics on Tier 2, rising from 23% to 38%. Similarly, the percentage of generic drugs on Tiers 3 and 4 grows from a negligible number to a combined 33% in 2017. Together, these represent a significant shift toward more-expensive tiers for generics. In general, generics are noticeably shifted from Tier 1 to higher tiers, with Tier 2 now containing a plurality of the generics. Nevertheless, although the percentage of generic drugs on Tiers 1 and 2 significantly decreases during 2010–2017, nearly three in five generic drugs are still assigned to the first two tiers. Thus, the major trend in generics is a shift from Tier 1 to Tier 2.

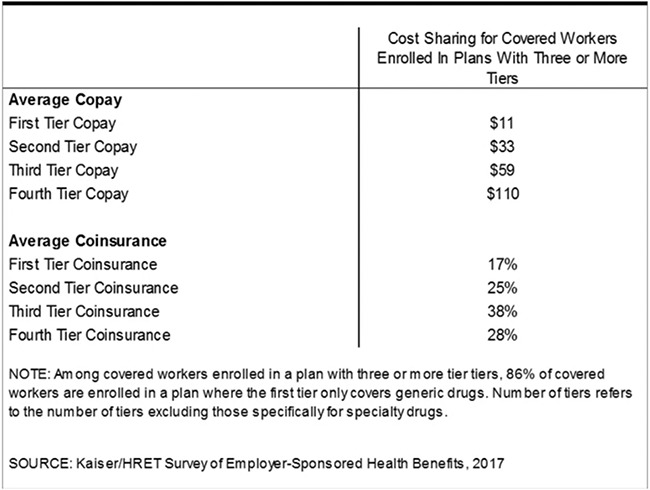

Pushing generics toward more-expensive tiers—even from Tier 1 to Tier 2—has significant cost implications for consumers. According to one study, the average copay increases three-fold when a drug moves from Tier 1 to Tier 2, increasing from $11 to $33 as shown in Figure 3.122 Such copay amounts can add up quickly for a patient using multiple medications across the entire year. Moreover, this increase in patient out-of-pocket payments occurs despite the fact that the price health plans pay for generics on Tier 2 is roughly the same as on Tier 1, as shown in the section below.123

Figure 3.

Average copayment and co-insurance for the different tiers among workers with insurance plans with three or more tiers.124

As a general matter, formularies are intended to be designed so that drugs are separated onto different tiers according to their price, with the exception of higher-priced specialty generics and specialty brands grouped together on Tier 5.125 Thus, an initial consideration concerns whether it makes sense from a price perspective to have brands and generics on the same tier—that is, to what extent are brands and generics priced similarly.

The study answers this question using rigorous and conservative statistical comparison testing of brands and generics placed on the same tier.126 Subsequent analysis confirms that in the case of all tiers except for Tier 1, brand and generic drugs should not be placed on the same tier: the dosage-unit price for brands is simply far greater than the dosage-unit price for generics. Only for Tier 1 do brands and generics sometimes belong together, given that some brand prices are as low as the price range for generics.

III.C. Irrational Tiering

Academic literature has explained that the prize of avoiding generic substitution drives many strategic games in modern pharmaceutical markets.127 For example, in what is euphemistically known as ‘life cycle management’, brand drug companies alter various aspects of a drug—such as a drug’s dosage, formulation, or delivery system—shifting the market away from the version of their drug that is facing generic competition.128 As a result, simply comparing drugs with their generic counterparts may not fully capture the competitive dynamics of the market. Thus, this section of the study looks beyond brand drugs and their direct generic substitutes, expanding the comparison to consider drugs with the same active ingredient. For example, a brand drug in tablet form may be compared to a generic with the same active ingredient in capsule form, with a different dosage, etc.

Of course, an approach that truly considers the entire competitive landscape would also encompass competitors that have drugs with different active ingredients. Drug companies undoubtedly know who their competitors are, even if those drugs only compete off-label or in certain subsections of the market. One could think of such as approach as comparing therapeutic competitors, a term that has not been used previously in the literature.129 Identifying all such therapeutic competitors in order to compare their formulary placement would be a truly daunting task. Nevertheless, the study successfully expands the comparison to a degree by examining a subset of therapeutic competitors—specifically, drugs containing the same active ingredient.130

Comparing active ingredients, of course, is not a perfect measurement of substitutability. Certain routes of administration, for example, may be particularly expensive, although they may be better suited for a patient’s condition. Nevertheless, the dosage-unit price calculations and the comparisons of brand costs with costs of generics demonstrate that brands and generics, on the whole, have vastly different prices.131 Thus, although there may be outlying examples, brands and generics, as a general matter, should not be on the same tier—which means that brands and generics of the same active ingredient certainly should not be on the same tier.

Thus, this section of the study undertakes an empirically original analysis of ‘irrational tiering’ in the formulary system—instances in which a brand and a generic with the same active ingredient are placed on the same tier or when the generic is placed on a more-expensive tier.132 Given that the CMS began recording complete formulary data in 2010, the analyses in this section focus only on claims from 2010 to 2017, rather than the 12-year study period for pricing data.133

To ensure a valid comparison among drugs that have the potential for direct competition with each other, the study examines only the subgroup of generics and brand drugs that have the same active ingredient within the same, single health plan formulary. Generics with such brand competitors represent a relatively small portion of the drugs on five-tier formularies, with the average percentage of these drugs dropping from 32% to 29% between 2010 and 2017. Thus, it is important to note that in the section below, the study demonstrates that a minor change to tier placement for a limited percentage of drugs could lead to massive cost savings for patients and the federal government.

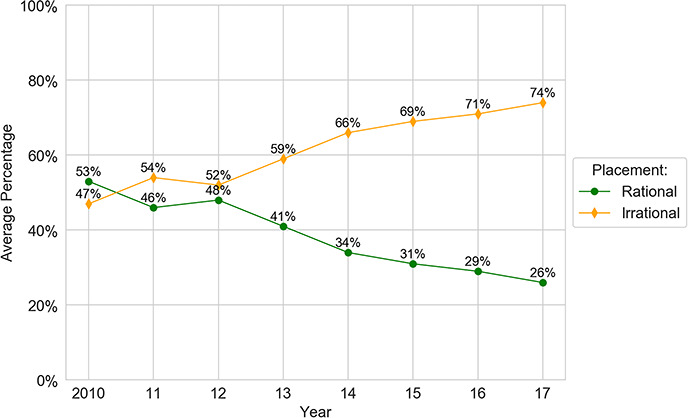

Even looking at this limited group, the study finds troubling evidence of irrational tiering. In 2015, for example, 69% of generics experience at least one abnormal placing relative to more expensive drugs with the same active ingredient. Moreover, the trend is worsening over time. Specifically, the study finds that the percentage of all generics that are irrationally tiered rises from 47% in 2010 to 74% in 2017.

The problem is not just that generics are being placed on the same tiers as brands with the same active ingredient; increasingly, the generic is being placed on a ‘worse’ tier. Within the cohort of irrational placements, the distortion of same-tier placement drops from 98% to 93%, whereas worse-tier placement more than triples from 2% to 7%. Thus, the combination of all results demonstrates that irrational tiering of generics is increasing, with an increasing share of misplacements shifting toward placing generics on a ‘more-expensive’ tier than a brand competitor with the same active ingredient. Both of these trends indicate increasing irrationality in the tier-placement system.

III.D. Wasted Spending Due to Irrational Tier Placement

Clearly, the formulary system is not working as intended. The question now is: how much does improper drug placement affect spending? Addressing the question requires a definition of spending.

III.D.i. Defining Spending

As described above, although average rebate information can be calculated for brand drugs, the rebate for any particular drug is not available. Thus, calculating true wasted costs when looking at a subset of drugs would be difficult to accomplish with precision. This particular challenge has confounded pharmaceutical researchers in other circumstances, leaving uncertainty in its wake.

The study, however, is able to overcome this perennial problem. Although net price remains out of reach, one can measure certain types of spending for which detailed data are available. Thus, the study examines spending by calculating what patients actually paid out of their own pockets for an individual drug purchase, combined with any amount that the federal government paid for that purchase in the form of its Low-Income Subsidy Program.134 These amounts provide a concrete and reliable method for measuring true dollars out the door.

Details on the calculation of the cost to patients and the federal government can be found at Appendix A3, but a few points are worth noting here. First, the calculation is based on the assumption that abnormally placed generics should have been placed a single tier below their actual tier placement. This is a highly conservative estimate; there are likely circumstances in which the difference in tier placement should be greater, based on the cost differential.

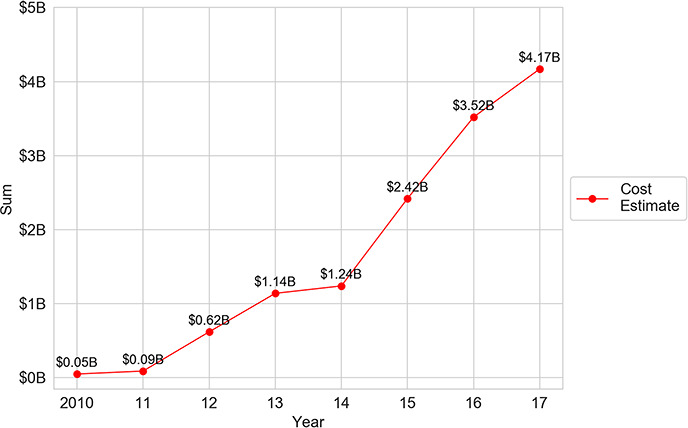

Second, Medicare enrollments135 play an important role in driving up wasted costs. In 2010, irrationally tiered generics leads to more than $50 million of wasted spending. By 2017, the amount of wasted spending increases by nearly a factor of 83, reaching $4.17 billion. This dramatic increase flows both from the continuous increase in Medicare drug prescription plan enrollees and the increase in the cost of irrationally tiered generics per beneficiary. In other words, when the number of plan enrollees increases, the amount of spending increases, as does the amount of waste from that spending.

Third, the results are likely to seriously understate the costs of irrational tiering from another perspective, as well. Specifically, the study examines only brand drugs with a generic competitor having the same active ingredient. A drug may have other types of therapeutic competitors, such as another drug with a different active ingredient that could treat the same disease state or a subsection of the population with the disease state, even if it might not treat all patients. To the extent that other forms of therapeutic competitors are cheaper and there is irrational tiering, those would be added costs to the patient and to the government. Even with these conservative approaches, the total wasted spending across the 2010–2017 study period amounts to $13.25 billion.

III.E. Implications and Limitations

As noted above,136 examining Medicare claims data provides a useful approach for understanding the inner workings of the health insurance system and the pharmaceutical industry. Four elements make the Medicare system a particularly attractive venue for researchers: (i) Medicare accounts for 29% of prescription drug spending in the USA; (ii) the detailed, government-verified claims data available from the CMS are unavailable from private insurers; (iii) certain problems in Medicare are likely to appear in the health insurance system in general; and (iv) reforms may be easier to craft for the Medicare system as an initial matter, before venturing into reforms of the private insurance market.

Nevertheless, there would be limitations in generalizing from the Medicare system to the whole. These may include less variation in the drugs the cohort buys, how the drugs are covered by their insurance, the prices that they pay, the kind of rebates one expects the plans to obtain, and so on. For example, an industry analyst report concludes that rebates amount to a far larger percentage of point-of-service spending for drug spending in Medicare Part D than in private health insurance planes.137 In Medicare, rebates amount to 22% of spending; in private plans, the percentage is 12%, almost half of that amount.138 The analyst report hypothesizes that patients may have different preferences in shopping for private plans than they do in shopping for Medicare plans. Prescription coverage is purchased separately with Medicare plans, in contrast to private plans, which may lead patients to evaluate the plans, and the interactions between elements of the plans, differently.

It is possible that given differences in the private insurance and Medicare markets, brand drug companies are relying less on rebates to drive consumers to their drugs and more on coupons. With coupons and similar systems, drug companies reimburse a patient for all or part of the patient’s copayment or co-insurance.139 Patients pay less at the pharmacy counter. They may pay more; however, given that the insurance plan’s cost for the higher-priced drug will filter through to higher premiums. For this reason, Medicare does not allow the use of coupons, and some private plans discourage coupons by refusing to count the amount covered by a coupon in a patient’s deductible.140 And in the long run, of course, patients may pay more as lower-priced substitutes are unable to gain much of a foothold in the market or are discouraged from entering the market at all.

The point is simply that differences between the private insurance market and Medicare insurance markets counsel caution in comparing the two. Comparisons between the two may be instructive but not necessarily conclusive.

One should also note that the study does not examine how rebate dollars that are returned to the health plan (as opposed to those retained by the PBMs) might flow back into overall costs in the system. There is some evidence that rebates help to defray ‘premium’ costs—that is, the cost paid to enroll in a health plan—to patients.141 One would have to determine how much flows back into premium reduction (as opposed to executive pay or other expenditures), how those flowbacks affect the payment allocations among different types of patients. For example, some have suggested that to the extent rebates reduce premiums, they have the effect of shifting burdens away from healthy patients and onto sick patients, the opposite of the manner in which an insurance system is supposed to operate. 142

One would also have to calculate how much of the premium reduction is inadvertently funded by increased government subsidies through the Low-Income Subsidy Program and potentially other increased reimbursements from Medicare. For example, the increased prices that fuel rebates also push patients more quickly into the portion of Medicare in which the government picks up 80% of a patient’s costs.143 Thus, rebates can have the effect of shifting expenditures from the health plan to the federal government.144 All of these variables transform any calculation of how rebate dollars flow into overall system expenditures into an exercise fraught with uncertainty and potential inaccuracies. And of course, much of the necessary information is claimed as a trade secret and deeply hidden.145 Thus, calculating the increased amounts patients must pay out of pocket, along with the portion of that payment subsidized by the government, provides a useful window into a tangible and immediate impact on those parties. Moreover, given the complexities and timing shifts of the healthcare reimbursement one would expect significant leakage to occur, even if every penny of the rebate dollars—both the dollars retained by the PBMs and the dollars returned to the health plans—were to flow back into premium reduction, which is an unlikely scenario itself.

Finally, interactions between drug costs and other elements of an insurance plan, both for the patient and for the plan, raise tantalizing questions for future research. Medication purchasing is only one element of the overall risk profile of a patient, and it creates a form of signaling effect for both the patient and the plan. In other words, plans want more people with a more profitable risk profile, and patients want plans that cover their needs. The issue is more complicated than simply trying to attract healthy patients and discourage those who are less healthy—something that could be accomplished by placing medications for HIV, for example, on a less-favored tier, thereby discouraging patients who might impose a range of nonmedication costs on a plan. On a more complex level, suppose that certain conditions are more profitable for a plan given reimbursement levels or other factors. In that case, if the plan believes that patients may prefer brand drugs for that disease state, the plan might choose to place both the brand and generic on a favorable tier to attract patients with that disease state—or do the reverse if it wished to discourage such patients. Comparisons between stand-alone Medicare Part D drug plans and certain types of Medicare plans that also offer Part D coverage146 could provide the opportunity to tease out some of these effects.

The results of the study, nevertheless, point to a clear, unmistakable conclusion: we do not nearly live in an ideal world. The current formulary tier system for drug coverage, which is intended to reduce both patient and government expenditures for prescription drugs, is being manipulated to the advantage of insurers, drug manufacturers, and PBMs seeking greater profits at the expense of patients. Based purely on cost, the standard for drug placement should be that cheaper generic alternatives are placed on lower, less-expensive tiers with lower copays, whereas more-expensive brand drugs should be placed on higher, more-expensive tiers requiring higher copays.147

Although insurers maintain that their formularies are structured according to this ideal,148 the study’s examination paints a different picture. Brand and generic drugs are increasingly placed together on the same tiers, despite significant cost differences between the two. Within the nebulous haze that is the formulary system, few things are clearer than the fact that the current system is being gamed and costing society dearly. Observations such as these are most useful, however, if they illuminate potential pathways for reform.

IV. THE PROBLEM AND ITS SOLUTIONS149

Only a few solutions have been proposed to correct abuses of the formulary system, in part, because formulary abuses seem to be a recently identified phenomenon.150 One Canadian academic suggested designing formularies based on evidence of head-to-head comparisons of drug efficacy and cost-effectiveness analyses with competing medications, including real-world, postmarketing evaluations of effectiveness. 151 The approach would establish a set of predetermined criteria in the formulary placement process, restricting how certain drugs could be added or removed from formularies. Such an approach, however, would be far easier to implement in a nation with a single-payor system, such as Canada, than in the USA.

Generics industry actors, naturally, wish to restrict the ability of insurance plans to place brand drugs on lower, less-expensive tiers.152 Similarly, the CMS proposed—and subsequently scrapped—a rule that the lower tiers should be exclusively reserved for generic drugs, with higher tiers reserved for brand drugs.153 Although these approaches would be an improvement over the current system, they leave much room for mischief. There is no single, accepted definition of what is a generic, and brand drug companies engaged in strategic behavior regarding the term. For example, anecdotal evidence has revealed brand companies withdrawing their product from the market so that the generic version, as the only one on the market, would be treated as a brand under reimbursement procedures.154 Moreover, the term ‘generic’ itself has become muddied by the entrance of so-called authorized generics. Authorized generics are versions made or licensed by the brand company using the generic name of the drug, normally at a lower price than the brand. Any system that relies on a name with no agreed definition of the naming convention is likely to encounter serious problems.155 At the end of the day, one can call something a brand, a generic, or an elephant. It is the price that matters.

IV.A. Focusing on List Price

To solve the game playing and waste, one must return to the core rationale of the tiering system. Specifically, what is the tiering system intended to accomplish, and how might society direct the system back to its goals, despite the complexities and competing incentives. As a touchstone for the inquiry, modern tiering systems are supposed to be based on the price of the drug, a rationale that is explicitly set out both in the academic literature and in insurance plan materials.156 But what price? As described above, price is a slippery and murky concept.157

One might argue that tiering should be based on the net price. After all, that is the bottom-line cost to the health insurer. Basing tiering on net price, however, presents a host of problems. The first is that true net price is hidden—from the health insurance plan, auditors, and regulators. This disappearing act makes it nearly impossible to track and monitor strategic or even downright illegal behavior. The convoluted nature of net price also blunts its ability to operate as a signaling mechanism—for patients or even for health plans.158

Most important, volume rebates allow companies with market power to provide deals that cheaper, new entrants cannot meet. This is particularly problematic in the context of new generic entering the market in the face of brand drugs coming off patent, when those patents may have created a monopoly position in the market. Thus, net price in the context of volume rebates may create insurmountable barriers to competition, undermining the goal of having generic drugs bring down the price of prescription medication. The long-term benefits of generic competition may be left in the dust. In short, net price as a solution to tiering leaves much to be desired.

A problem of this magnitude and degree of challenge requires an innovative solution. The sweeping solution that this paper offers is that tiering should be based on ‘list’ price. Yes, list price, a term that is roundly dismissed because it does not embody the hidden rebate deals. Nevertheless, list price should be the key component in determining the tier placement for all drugs. And as the discussion below will explain, list price is the perfect regulatory solution for bringing some measure of sanity to the tiering system.

First, basing tiering on list price brings an end to the rebate and quasi-kickback games that can harm competition and contribute to rising prices.159 One cannot overestimate how difficult the rebate problem has been to address. Despite widespread recognition of the problem involving rebates, regulatory attempts to reform this practice have failed. Most recently, in February 2019, the Trump administration proposed a rule to alter safe harbor protections under the federal Anti-Kickback statute so that drug companies would be prohibited in federal healthcare programs from paying rebates tied to a percentage of a drug’s list price to PBMs under federal health programs.160 The proposal was limited in some aspects, offering two new safe harbor provisions: one that would have allowed PBMs to negotiate rebates with drug manufacturers as long as those rebates were shared directly with patients at the point of sale and another that would have allowed PBMs to receive fixed fees for services provided on behalf of insurers.161 In a report released in May, however, the Congressional Budget Office (CBO) projected total prescription drug costs in the USA would not decrease if the proposed rule were finalized.162 The CBO predicted that under the rule, drugmakers would ‘offer the renegotiated discounts in the form of chargebacks’ instead of lowering drug list prices.163 As a result, the CBO estimated that the rule would have increased government spending by a total of $177 billion from 2020 to 2029.164 The administration eventually pulled the proposal to eliminate drug rebates in July.165

In addition to the risk of developing new games, efforts to reform rebates have been stymied by the concern that drug companies could simply pocket the amounts previously offered as rebates without lowering prices. In the CBO’s assessment of the Trump administration’s proposal to eliminate rebates, for example, the agency predicted that drug companies would ‘withhold about 15% of the amounts they currently rebate to PBMs in Part D and would negotiate discounts approximately equal to the remaining 85%’.166 Rather than lowering list prices, the agency expected that manufacturers would pocket most of the savings themselves rather than pass them on to consumers.167 Without the capacity to negotiate drug discounts, Medicare would have to bear the brunt of the costs, leading to increases in premiums and government spending.168

Focusing on list price, however, has the potential to directly address high pharmaceutical prices, while avoiding the unintended consequences of directly eliminating rebates. If tiers were based on list price, a drug company that raised its price to give space for rebates and other payments to PBMs would find that the strategy backfires. The high list price would drive the company’s product to a less-advantageous tier, in comparison to cheaper substitutes. This would flip the perverse incentives of the current system—in which ‘raising’ prices provides a competitive advantage—on its head.169 And as one would expect in a free-market system, lower price would make a company more competitive.170 Hidden negotiations and tempting rebate deals would not matter, regardless of whether payments were designed as rebates, chargebacks, or in some other manner; they simply would not factor into competitive placement.

Basing tiering on list prices provides additional advantages. The approach sidesteps the need for greater transparency regarding negotiations between PBMs and drugmakers by avoiding the practical problem of navigating around claims to trade secret protection.171 No one claims that ‘list’ price is a trade secret. Moreover, Medicare regulations already requires drug companies to report the list price, including providing penalties for failure to report.

Basing tiering on list price potentially could be accomplished with regulatory changes through the Department of Health and Human Services that could be mandated by Congress. The CMS, the part of HHS that oversees Medicare,172 already exercises authority over formularies and formulary design.173 Medicare’s Prescription Drug Manual, as updated in 2018, specifies that a plan must include ‘Provision of an Adequate Formulary’, and that the agency will ‘consider specific drugs, tiering and utilization management strategies employed in each formulary’.174 At present, the Manual suggests that CMS’ exercise of authority will revolve around ensuring that plans follow common practice in the industry. For example, the Manual notes that plans are encouraged to submit formularies similar to those in widespread use today, and that the Agency will identity outliers for further evaluation.175

As of 2018, CMS’ Manual identifies its authority to regulate formularies as flowing from the Medicare Modernization Act of 2003, with its requirement that a plan’s categorization system does not ‘substantially discourage enrollment by any group of beneficiaries’.176 Earlier CMS guidelines on formularies, however, describe the goal of the Medicare Modernization Act (and the Agency’s guidelines, themselves) in terms of cost, explaining that the CMS will review plans to ‘assure that beneficiaries receive clinically appropriate medications at the lowest possible costs’ and that ‘the goal is for plans to provide high-quality cost-effective drug benefits by negotiating the best possible prices and using effective drug utilization management techniques’.177

To the extent CMS’ earlier view of its authority is accurate, the Agency could reach beyond simply requiring that plans look like other plans on the market and specify tiering according to list prices, in the interests of providing high-quality cost-effective drug benefits. Even if courts were to conclude that CMS’ authority under the Medicare Modernization Act is narrower, the basic pathway exists. With CMS already reviewing and providing guidance on formularies, Congress could provide any additional authority necessary to further regulate formularies.

Given that CMS already requires that drug companies submit their list prices, 178 the Agency has the necessary information. Expansion of the regulations to provide for verification of the information, along with a willingness to enforce the regulation, would be important.179 Although companies that provide inaccurate reports can be subject to civil monetary penalties or terminated from the drug rebate program, compliance problems have existed in the past. For example, in 2008, over half of the manufacturers did not fully comply with the quarterly submission requirements and three-quarters did not fully comply with monthly requirements.180 Over time, the Office of Inspector General has indicated a willingness to step up enforcement efforts.181 The Inspector General’s Office even suggested that CMS use its authority to impose $10,000 per day fines for late reporting.182 Nevertheless, the existence of open list pricing creates an easy avenue for developing a modicum of accountability.

Ideally, tiering reforms would be applied to all insurance plans. The political difficulty of instituting such a broad change for the entire healthcare insurance industry, however, could be challenging, and the prospect of wading into the treacherous waters of the private healthcare market would be daunting. Instead, moving tiering to list prices would be more easily adopted through the Medicare system, which has the potential to create ripple effects in the private insurance market.

IV.B. Staying Ahead of the Game

Legislative and regulatory changes happen slowly and infrequently. In contrast, strategic behavior by the players in the system constantly shifts and evolves. As any chess player can attest, blocking the last move will never be enough to succeed. One has to play forward, anticipating reactions and setting pathways for managing likely responses. With this in mind, two additional sets of reforms would be important within the CMS regulatory approach: transparency and rational tiering rules.

IV.B.i. Transparency

Creating tiers based on list price is a sensible departure from the current system. Nevertheless, without transparency regulations and the capacity for enforcement, the formulary system remains ripe for abuse. Strategic behaviors can simply shift their forms—from gaming the tiering system, to gaming net prices, to gaming list prices, to new games.

Information symmetry is one of the prerequisites for functioning markets,183 and, as many scholars have observed,184 the healthcare and insurance markets are plagued by asymmetric information—with sophisticated institutions having vastly more knowledgeable than individual consumers. Although formulary tiers are supposed to serve as a way of partially addressing this information asymmetry, the murkiness permeating the formulary system can only enhance the likelihood that insurers construct irrational tiers. To ensure that the door guarding formulary tiers is closed to further abuse, as well as to prevent arbitrary construction of tiers, it is imperative to accompany tiering based on list price with regulations heightening transparency.185