Abstract

In this paper we will briefly review how changes in brain and in cognitive and social functioning, across the spectrum from normal to pathological aging, can lead to decision-making impairments which increase abuse-risk in many life domains (e.g. health-care, social-engagement, financial management). The review will specifically focus on emerging research identifying neural, cognitive and social markers of declining financial decision-making capacity in older adults. We will highlight how these findings are opening avenues for early detection and new interventions to reduce exploitation risk.

Keywords: Capacity assessment, decision-making, elder abuse, financial capacity, financial exploitation

I. Prevalence and determinants of financial exploitation risk

Scope of the problem.

Among older adults, sudden and unexpected financial losses due to exploitation can have devastating consequences. Relatives may be forced to take on unexpected financial burdens or exploited older adults may be forced onto public entitlement systems. A rapidly aging population means that the size and scope of this problem will continue to grow. Financial exploitation in older adulthood has become a significant public health problem that requires surveillance, education and intervention.

Financial exploitation is a common form of elder mistreatment (Acierno et al., 2010; Jackson and Hafmeister, 2011). In a recent survey of financial exploitation in New York State, more than 4000 community-dwelling older adults were surveyed for experiences with a range of exploitation scenarios; including, theft, misappropriation or coercion resulting in financial loss, impersonation to obtain property or services, or hardship experienced due to loss of agreed upon financial contributions (Peterson, Burnes, Caccamise, Mason, Henderson and Wells, 2014). The estimated prevalence of financial exploitation was 4.7% with an annual incidence of 2.7%, providing sobering evidence of the potential scope of the problem. These results were consistent with previous prevalence studies (e.g. Lichtenberg, Stickney and Paulson, 2013 and see Lichtenberg, 2016 for a review) and suggest approximately 1 in 20 adults can be expected to experience some form of financial exploitation past the age of 60, an incidence rate eclipsing many age-related diseases. These are almost certainly underestimates of the true prevalence, as many older adults are unaware of or unwilling to report exploitation (Pak and Shadel, 2011).

Losses by older adult victims of financial exploitation are estimated at more than $3 billion annually (National Committee for the Prevention of Elder Abuse, 2011). This will accelerate in the coming decades as the baby boomer generation continues its march into older adulthood, taking its place as the wealthiest generation in American history, and providing an increasingly lucrative target population for exploitation. Even if exploitation rates stay at current levels, the enormous growth in the older population will lead to dramatic increases in the number of potential victims. Further, these demographic shifts are occurring at the same time as technological advances are opening up new and potent opportunities for exploitation through password theft, computer malware, or misleading advertisements specifically targeting older adults. Economic losses due to exploitation may reflect only a small fraction of the true cost of this growing public health problem. Financial exploitation is associated with greater rates of hospitalization and long term care admissions as well as poor physical and mental health and higher mortality (Deem, 2000, Dong & Simon, 2013a, 2013b; Lantz, House, Mero, & Williams, 2005). Further, the vast majority of exploitation cases involve family members or close acquaintances and likely go unreported or ignored (Acierno et al., 2010; Peterson et al., 2014). Given the potential scope of the problem, identifying the determinants of financial exploitation risk is necessary (Pillemer, Connolly, Breckman, Spreng, & Lachs, 2015).

Determinants of financial exploitation.

Demographic risk factors for financial exploitation include age, lower education and income levels (James, Boyle and Bennett, 2014; Laumann, Leitsch and Waite, 2008) as well as household size and race (Beach, Schulz, Castle and Rosen, 2010; Laumann et al., 2008; Peterson et al., 2014). While these socio-demographic factors are critical for informing broader policy and public health initiatives, they provide only marginal benefit for identifying at-risk individuals. Recent studies have identified individual, or person-centered, risk factors for financial exploitation. Foremost among these is reduced cognitive functioning in older adulthood (e.g. James et al., 2014) and Mild Cognitive Impairment (MCI, Han, Boyle, James, Yu and Bennett, 2015). Slowed processing speed was specifically identified as a robust predictor of exploitation risk in both normal aging and MCI cohorts. However lower performance on other cognitive factors, including episodic, semantic and working memory, as well as a global index of cognitive function, was also associated with increased susceptibility to scams in older adults (James et al., 2014). These findings, as well as investigations of ‘financial capacity’ in aging and brain disease (e.g. Marson, Sawrie, Snyder, McInturff, Stalvey, Boothe, et al., 2000; Marson, Martin, Wadley, Griffith, Snyder, Goode, et al., 2009), suggest that cognitive changes associated with aging and brain disease may impair decision-making abilities, leading to heightened financial vulnerability in these populations (e.g. Boyle et al., 2012).

In addition to cognitive predictors, several studies have also identified psychosocial factors associated with financial vulnerability. These include depression (Beach et al., 2010), reduced feelings of well-being (James et al., 2014), lower levels of social support and loneliness (James et al., 2014), and a need for sociability (Lichtenberg et al., 2013). In a recent study of aging and social networks (the relational environment in which older adults are embedded, Schafer and Koltai, 2015), older adults with denser social networks, i.e. those whose friends are also friends, are less likely to be victims of abuse. Interestingly however, risks also accrue with deeper social embeddedness, as perpetrators of abuse are often found within an older adult’s social network. Consistent with this latter idea, social changes in aging may be a particularly important determinant of exploitation risk as exploitation, by definition, is a social transaction. Further, as observed by Schafer and Koltai (2015), the vast majority of financial loss occurs at the hands of a known other, with many incidents involving close family members (Acierno et al., 2010). Taken together these findings highlight the importance of considering both cognitive and social aspects of decision-making capacity when assessing exploitation risk.

Increasingly, decision-making capacity in older adulthood has been investigated by studying brain changes and their behavioral correlates in older adulthood (see Samanez-Larkin and Knutsen, 2015 for a review). These studies in turn are opening the door for the identification of neural markers of financial capacity, decision-making, and exploitation risk (e.g. Griffith et al., 2010; Stoeckel, 2013; and see Samanez-Larkin, 2013 for a discussion).

The determinants of financial decision-making and exploitation risk in older adulthood have become increasingly well-defined, from cognitive decline, to changes in socio-emotional functioning, to alterations in brain structure and function. These factors have yet to be integrated into a comprehensive framework that can help guide the development of clinically-relevant, person-specific markers of exploitation risk. The present paper is intended to help address this gap. We first review how age-associated changes in neural, cognitive and socio-emotional functioning influence decision-making in older adulthood. We then examine how changes in decision-making ability may increase abuse risk, with a specific focus on financial vulnerability and exploitation. From this brief review, we propose an integrated neurobehavioral framework for investigating financial exploitation risk, and review several assessment tools, developed in our laboratories, to measure financial competence and decision-capacity. Finally, we propose a neuroscience-based research agenda to improve early detection of financial exploitation risk in aging and brain disease.

II. Decision-making and financial exploitation risk in older adulthood

The portrayal of older adults as poor decision-makers, vulnerable to exploitation and abuse, continues to propagate through the popular media and in the scientific literature. However, this stereotype has surprisingly mixed empirical support, as older adults often show better or more adaptive decision-making abilities relative to their younger counterparts in many contexts (Ross, Grossman and Schryer, 2014). Over the past decade the field of decision-science and, more recently, decision-neuroscience (Samanez-Larkin, 2015), has begun to provide a more nuanced picture of the cognitive, affective, social and neural determinants of decision-making capacity in older adults.

Adaptive decision-making is an emergent property of interacting cognitive, affective and social processes. Age-related changes to brain structures and functions associated with these component processes, or their interactions, alter decision-making ability, potentially leading to increased exploitation risk (Samanez-Larkin, 2013). In this section, we briefly review recent scientific advances in mapping the behavioral (i.e. cognitive, emotional, social) and neural determinants of altered decision-making in older adults and suggest how these changes may relate to increased vulnerability to exploitation and abuse.

(i). Cognitive changes.

Normal aging is associated with specific reductions in cognitive control processes necessary to flexibly adapt to novel or shifting environmental contingencies. These capacities, often referred to as ‘fluid’ or ‘executive’ control processes, include mental flexibility, inhibition, working memory, as well as episodic memory, prospection and future planning (Park, Polk, Mikels, Taylor and Marshuetz, 2001; Schacter, Addis, Hassabis, Martin, Spreng and Szpunar, 2012). In the context of exploitation risk, age-related declines in executive control and episodic memory have been associated with more risky decision-making style, and declines in financial capacity – a critical risk factor for financial fraud and exploitation (Boyle et al., 2012, James et al., 2014). Poor executive control functioning has also been linked to risky decision-making on a gambling task following ventral medial frontal lobe damage (Bechara Damasio, Tranel and Damasio, 2000) and in normal aging (Denburg, Cole, Hernandez, Yamada, Tranel et al., 2007). Reduced executive control capacity has also been associated with poor decision-making, problem-solving and planning for one’s financial future (Griffith, Belue, Sicola, Krzywanski, Zamrini et al., 2013; Sherod, Griffith, Copeland, Beleu, Krzywanski et al., 2009).

Several studies have specifically investigated loss of financial skills as potential markers of functional decline and potential exploitation risk in aging and brain disease (e.g. Griffith et al., 2003; Marson et al., 2000; Sherod et al., 2009). Specific measures of cognitive skills that have been investigated in the context of financial abilities include conceptual, pragmatic, and judgment abilities, ranging from basic (e.g. numericity) to more complex cognitive skills (e.g. financial reasoning). These abilities are necessary to enumerate, allocate and monitor personal finances in the service of current and future financial goals (Marson et al., 2000). Indeed, assessments of financial capacity have become important markers of functional independence in neurodegenerative disease (Griffith et al., 2003; Marson et al., 2000).

However, not all cognitive processes decline with advancing age. Knowledge of oneself and the world, often referred to as ‘crystallized’, conceptual, or semantic knowledge, continues to increase across the adult lifespan and remains comparatively stable into older age (Park et al., 2001). Older adults may be able to draw upon this repertoire of semantic knowledge to identify potentially fraudulent behavior or avoid exploitative situations (Ross et al., 2014, and reviewed in Samenz-Larkin and Knutson, 2015). In the context of financial decision-making, Li and colleagues (2013) tested this possibility and reported that crystallized cognitive abilities in older adults directly offset losses in fluid abilities, and supported more adaptive financial decision-making (Li, Baldassi, Johnson, Weber, 2013). During a financial ultimatum game, older adults reject more ‘unfair’ offers than their younger counterparts (Beadle, Paradiso, Kovach, Polgreen, Denburg and Tranel, 2012). The authors speculated that younger adults demonstrated more empathic responding. In contrast, the older cohort, although equally high in self-reported empathy, appeared to tap into more lived experience (e.g. ‘money doesn’t buy friends’), countering their high empathy, and resulting in more rational decisions.

These divergent trajectories of age-related cognitive decline have been suggested as a possible explanation for the findings in a recent economic report that identified a mid-life ‘sweet-spot’ for optimal financial decision-making (Agarwal, Driscoll, Gabaix, and Laibson, 2014). The report’s authors argued that while younger adults may possess the executive control skills necessary to respond flexibly and adaptively to rapidly shifting environmental contingencies, they lack the experiential knowledge to identify longer-term patterns and anticipate future consequences. In contrast, older adults have lower fluid cognitive abilities, and reduced financial skills, to flexibly adapt to novel and shifting contingencies. Yet, they are able to bring lived experience to decisions to better identify and potentially avoid longer-term risk. Middle adulthood provides the optimal balance of executive control and experiential knowledge to maximize financial decision in both the near and far term.

It is clear, both from the experimental research reviewed above, and the population studies discussed in the opening section of the paper (e.g. James et al., 2014) that cognitive changes impact decision-making capacity across the lifespan, and that these changes have a direct impact on financial competence and exploitation risk for older adults. Understanding how the dual trajectory of age-related cognitive decline exacerbate, or protect against, elder financial abuse in specific contexts will be an important area of future research.

(ii). Socio-emotional changes.

Exploitation, by definition, involves both victim and perpetrator. Avoiding fraudulent or deceptive behaviors depends on the ability to successfully navigate complex, potentially conflict-ridden, social dynamics. In this context, reduced socio-emotional capacity would be associated with heightened risk, both for inter-personal exploitation (the grandson who continuously ‘borrows’ money) and for more impersonal, albeit relational, forms of exploitation such as telemarketing fraud (Pinsker, McFarland, & Pachana, 2010). Personal familiarity between victim and perpetrator almost certainly increases the social complexity of potentially exploitative situations. This may be a contributing factor for the overwhelming prevalence of within-family financial abuse (Acierno et al., 2010; Peterson et al., 2014) and may be further compounded by diminishing social support and need for sociality, loneliness and a reduced sense of well-being (James et al., 2014; Lichtenberg et al., 2013).

There is growing evidence that socio-emotional factors have difference influences on decision-making in older versus younger adults, and that these changes reflect specific patterns of age-related brain change. Older adults show reduced negative arousal to anticipated losses (Samanez-Larkin, Gibbs, Khanna, Nielsen, Carstensen and Knutson, 2007). These differences in value expectation have been linked to alterations in an affective-integrative-motivational brain circuit, including ventral striatum, anterior insula, medial temporal lobe and prefrontal cortex (PFC) regions, as well as motor-planning areas (Samanez-Larkin and Knutsen, 2015). This absence of negative expectation to anticipated losses suggests that older adults may engage in more risky financial decision-making, and indeed, this has been shown to be the case. Older adults make more sub-optimal decisions during risk-seeking, but not risk-avoidant financial decisions (Samanez-Larkin et al., 2007). On a decision-making task design to mimic real-world shifts in gain and loss contingencies (Denburg et al., 2007), more than one-third of older adults did not identify altered contingencies and continued to make high-risk decisions. These older participants also failed to show anticipatory physiological arousal during risky choices, suggesting that a significant proportion of older adults may experience a disruption in a biologically-based, deception-detection system. Critically, those older adults who exhibited high-risk decisions were more susceptible to false and misleading advertising (Denburg et al., 2007). In a follow-up study, the authors reported that patients with specific damage to ventral-medial prefrontal cortex (vmPFC) regions were impaired on the false advertising task (Asp et al., 2012), providing more direct evidence that age-related changes in this brain region may be a neural marker of exploitation risk.

Older adults also demonstrate less reactivity to negatively-valenced social stimuli (see Carstensen, Turan, Scheibe, Ram, Ersner-Hershfield, et al., 2011, for a review). This reduction in arousal has been associated with lower activation of the anterior insula, a region associated with interoceptive awareness, potentially disrupting that ‘gut-feeling’ associated with a pending risky decision (Samanez-Larkin et al., 2007). Poor physiological responsiveness to negative stimuli is also consistent with the well documented ‘positivity bias’ in older adulthood. Older adults show selective attention to, and greater recall of, more positively-valenced information than younger adults (see Charles and Carstensen, 2009, for a review). In the context of declining episodic memory, and less detailed representations of the future (Addis, Wong and Schacter, 2008), it has been suggested that older adults may make decisions on the basis of a ‘bright but blurry’ future (Weierich, Kensinger, Munnell, Sass, Dickerson et al., 2011).

These affective changes also influence decision-making in a social context, potentially increasing vulnerability to interpersonal exploitation. In a recent study of trust-worthiness, older adults labeled more pictures of faces as ‘trustworthy’ than did younger subjects (Castle et al., 2012). Older adults also exhibit a ‘positivity bias’ during impression formation of others. This is associated with increased involvement, or conscription, of medial prefrontal cortical regions engaged during negative impression formation in young (Cassidy, Leshikar, Shih, Aizenman and Gutchess, 2013).

Taken together, studies investigating affective influences on decision-making suggest that older adults may adopt a more risky decision-making style in anticipation of a more positively imagined, albeit less detailed, future. Critically, these deficits also impact social functioning, broadening the specter of vulnerability from maladaptive personal choices to inter-personal exploitation and fraud. Further, age-related changes in affective and cognitive processes likely interact to influence decision-making behavior. These interactions may be positive in some contexts. Access to a larger repertoire of representational knowledge has been shown to mitigate impulsive decision-making and reduce temporal discounting during financial decision-making tasks (Li et al., 2013). However, these changes may also compound deficits in more cognitively demanding contexts: older-adult decision-making is particularly impaired on tasks that require rule-learning or shifting contingencies, or involve more abstract or context-dependent reasoning (see Samanez-Larkin and Knutsen, 2015).

(iii). Neural changes.

As suggested in the opening section, age-related changes in decision-making ability are likely associated with specific patterns of structural and functional brain change. Performance on a comprehensive measure of financial capacity – the Financial Capacity Instrument (Marson et al., 2000) is associated with cortical volume in the angular gyrus in amnestic mild cognitive impairment (Griffith et al., 2010). Performance on this measure has also been associated with dorsal medial prefrontal volume in early AD (Stoeckel et al., 2013). Together these regions have been implicated in conceptual thinking and mentalizing about one’s future actions (Andrews-Hanna, Smallwood, & Spreng, 2014; Spreng et al., 2015) and may be critical for fact-based financial planning, reasoning and decision-making about monetary allocations.

Appraisal of socially-conveyed information in domains relevant to financial exploitation such as deceptive advertising (Asp et al., 2012; Denburg et al., 2007), trustworthiness judgments (Castle et al., 2012), impression formation (Cassidy et al., 2013), self-other judgments (Ochsner et al., 2005) or risky decision-making in novel contexts (Samanez-Larkin & Knutsen, 2014) has been consistently associated with medial prefrontal cortex structure and function. As reviewed briefly above, appraisal of information with high personal significance, or involving social inferences about the actions or intentions of others, is represented more ventrally in medial prefrontal regions, where the affective meaning of these contingencies is represented (Roy, Shohamy, & Wager, 2012). These regions, which are core nodes in an assembly of functionally-connected brain regions known as the default network are closely coupled with limbic structures and ventral striatum, known to mediate affective responses and emotional regulation during decision-making tasks (Samnez-Larkin and Knutsen, 2015, and see next section for a more detailed discussion of default network changes and financial exploitation risk). The integrity of these ventral frontal brain regions, and their connections to other brain systems, may be essential for navigating complex social dynamics in situations of high personal relevance, such as potential fraud or exploitation, particularly if the perpetrator is known.

(iv). Default network and exploitation risk.

Dorsal and ventral medial aspects of prefrontal cortex are core nodes in a network of brain regions collectively referred to as the default network (Andrews-Hanna et al., 2014; Buckner, Andrews-Hanna, & Schacter, 2008; Raichle, MacLeod, Snyder, Powers, Gusnard and Shulman, 2001). Regions associated with the default network include medial prefrontal cortex (PFC; dorsal, anterior and ventral aspects, as well as rostral anterior cingulate), the lateral frontal cortex (superior and inferior frontal gyri), as well as medial and lateral aspects of parietal and temporal cortices (Andrews-Hanna et al., 2014). While originally considered a ‘task-negative’ network (Spreng, 2012), recent evidence has demonstrated convincingly that this assembly of functionally-connected brain regions is engaged by self-generated thought, and is active across multiple functional domains including memory, future thinking, autobiographical planning, and social cognition (Andrews-Hanna et al., 2014). The majority of financial exploitation incidents occur in a social context (Acierno et al., 2010; Peterson et al., 2014). Thus age-related brain changes to anterior and ventral medial PFC aspects of the default network, which are implicated in social appraisal of personally-relevant information, and mentalizing about the thoughts and intentions of others, may predict exploitation risk. Further, reductions in the functional and structural integrity of the default network is associated with age-related cognitive decline (Buckner, 2004; Spreng & Turner, 2013) and reduced financial competence is a hallmark of age-related brain disease (e.g. Han et al., 2015; Marson et al., 2000; Lai and Karlawish, 2007). Changes in the default network have also been directly implicated in financial skills loss in older adulthood (Griffith et al., 2010). Taken together, evidence suggests that age-related changes in the default network, specifically ventral medial PFC, may be a marker of vulnerability to financial exploitation in older adulthood.

More recently, age-related changes in complex cognitive functions, such as problem-solving and planning for one’s personal future, have been associated with altered connectivity between default network brain regions and other functional brain networks (Spreng and Schacter, 2012; Turner and Spreng, 2015). Consistent with this idea, in a recent pilot study, older adults who had experienced financial exploitation showed reduced anterior insula volume and increased functional connectivity between this region and the default network (Spreng et al., forthcoming). The anterior insula is a node in a network of brain regions implicated in salience detection (Seeley, Menon, Schatzberg, Keller, Glover et al., 2007; Uddin, 2015). As we noted earlier, this region is also part of the affective-integrative-motivational brain circuit associated with decision-making capacity (Samanez-Larkin and Knutsen, 2015). Increased connectivity between salience and default network brain regions may signal greater reliance on social processing during decision-making in older adulthood. Reduced salience of social information, combined with altered social processing secondary to default network changes (e.g. positive impression formation, Cassidy et al., 2013), may leave older adults more vulnerable to undue social influences and exploitation. Changes in functional connectivity between large-scale brain networks implicated in social decision-making may be an important neural marker of exploitation risk. We explore this idea further in our social cognitive neuroscience model of exploitation risk described in the next section.

In this section, we briefly reviewed the evidence linking age-related changes in cognitive, affective, social and neural function to decision-making ability and financial exploitation risk. Changes in each of these domains, and their interactions, directly influence exploitation risk in older adults. Accurately measuring these changes, and identifying clinically-relevant markers of exploitation risk, represents an important next step in early detection and intervention. In the next section, we review two approaches to the assessment of financial risk in older adulthood developed in our laboratories. We also offer an extension of these approaches, a novel integrated assessment tool, based on our neurobehavioral framework for assessing financial vulnerability in older adulthood (described below).

III. Assessing financial competence and exploitation risk

In this section we review two clinically-validated, performance-based measures of financial competence: the Financial Capacity Instrument (FCI, Marson et al., 2000) and the Assessment of Competence for Everyday Decision-Making (ACED, Lai and Karlawish, 2007; Lai, Cooney, Gill, Bradley, Hawkins et al., 2008). These measures assess two broad domains of financial competence: cognitive and financial skills (FCI) and decision-making capacity (ACED). Both have been adopted broadly in clinical and research settings. We have chosen to focus on these assessments here as they provide the foundation for a novel assessment approach we describe later in the paper. An exhaustive review of financial capacity assessments is beyond the scope of this paper. However, a vast array of measures and assessment strategies have been developed to assess financial capacity, and vulnerability, in older adults. These include self-report scales (e.g. the Financial Industry Regulatory Authority Risk Meter, AARP, 1999 and the related Susceptibility to Scams Survey, James et al., 2014; the Age Associated Financial Vulnerability Survey, Lachs and Han, 2015), financial literacy, numericity and capacity questionnaires (e.g. Independent Living Questionnaire, Loeb, 1997; Financial literacy assessments, Lusardi, & Mitchell, 2007; Lusardi and Tufano, 2009) and performance-based assessments (e.g. Decision-Making Competence Assessment Tool, Finucane, Mertz, Slovic and Schmidt, 2005; Lichtenberg Financial Decision Making Rating Scale, Lichtenberg, Ficker and Rahman-Filipak, 2016).

While many of the published measures have been developed for population-based incidence and prevalence research, increasingly researchers, clinicians, regulatory and advocacy agencies are focusing on performance-based measures to better assess financial competence, and exploitation risk, in real-world settings. Below we provide a detailed review of two performance-based tools, the FCI and ACED, that provide the foundation for a novel assessment approach that we present at the end of this section.

(i). Financial Capacity Instrument.

The FCI, published in its original form in 2000 (Marson et al., 2000) was updated based on a clinically-based, conceptual model of decision-making and financial capacity in older adults (Griffith et al 2003). This model forms the basis of the Financial Capacity Instrument (FCI) and related studies of financial capacity in MCI, Alzheimer’s disease (AD), and other clinical populations. The financial capacity model has three levels (Griffith et al., 2003): (1) specific financial abilities or tasks, each of which is relevant to a particular domain of financial activity; (2) general domains of financial activity, which are relevant to the independent functioning of community dwelling older adults; and (3) overall financial capacity, which reflects a global measure of capacity based on the summation of domain- and task-level performance.

Building from this model, the Financial Capacity Instrument (FCI) (Marson, et al, 2000) was developed as a standardized, performance-based measure to assess everyday financial skills and abilities in adult populations. The FCI directly assesses financial abilities across 18 tasks, 9 domains and two global scores. Trained technicians administer and score the FCI. Administration time for the FCI is approximately 60 minutes, depending on the cognitive level of the examinee.

The FCI has been used to investigate loss of financial skills in patients with Alzheimer’s disease. In an initial study, a sample of 23 older controls and 53 AD patients (30 with mild dementia, and 23 with moderate dementia), were administered an early version of the FCI (Marson et al., 2000). Mild AD patients performed equivalently with control subjects on basic monetary skills, but significantly below controls on all other domains of financial capacity. Moderate AD patients performed significantly below controls and mild AD patients on all domains. On FCI tasks, mild AD patients performed equivalently with controls on simple tasks such as naming coins/currency, counting coins/currency, understanding parts of a checkbook, and detecting risk of mail fraud. Mild AD patients performed significantly below controls on more complex tasks such as defining and applying financial concepts, obtaining change for vending machine use, using a checkbook, understanding and using a bank statement, and making an investment decision. Moderate AD patients performed significantly below controls and mild AD patients on all tasks (Marson et al. 2000). This study represented the first empirical effort to investigate loss of financial capacity in patients with AD. The findings suggest that significant impairment of financial capacity occurs in AD, even in the early stages of the disease. Mild AD patients appear to experience deficits in complex financial abilities, and some level of impairment in almost all financial activities (domains). Moderate AD patients appear to experience loss of both simple and complex financial abilities, and severe impairment across all financial activities.

A follow-up study showed that financial capacity declines rapidly in mild AD over the course of one year (Martin et al., 2008). In a sample of 55 individuals with mild AD and 63 healthy older adults, Marson and colleagues examined financial capacity on two occasions with an expanded FCI. Results replicated prior cross-sectional findings and indicated that patients with mild AD exhibit global financial capacity deficits relative to same aged cognitively intact peers at baseline. At one-year follow up, participants in the mild AD group exhibited marked declines in overall financial capacity and on the majority of financial capacity domains. In contrast, the healthy older adults exhibited stable financial capacity over the course of the study. Overall, the AD group exhibited relatively rapid change, with an overall 10% decline over the course of one year--from approximately 80% of the control group’s performance level at the baseline assessment to 70% of the control group’s performance level at follow up (Martin et al., 2008).

The FCI has also been used to investigate financial capacity in patients with mild cognitive impairment. MCI represents a transitional phase between normal cognitive aging and dementia, with less functional impairment than is characteristic of dementia but nevertheless with clear declines in instrumental activities of daily living (Petersen et al., 2001; Ritchie et al., 2001). Using the FCI, Griffith and colleagues examined financial capacity in a cross-sectional sample of 21 older controls, 21 patients with amnestic MCI, and 22 patients with mild AD (Griffith et al., 2003). They found that, at the domain level, controls performed significantly better than mild AD subjects on all domains with the exception of Knowledge of Assets/Estate. Controls performed significantly better than the MCI group on Financial Concepts, Checkbook Management, Bank Statement Management, Financial Judgment, and Bill Payment. There were no domains on which the MCI group performed better than controls. In turn, the MCI group performed significantly better than mild AD patients on all domains except Financial Judgment and Knowledge of Assets/Estate. For overall financial capacity, control participants performed significantly better than MCI and AD participants, and MCI participants performed significantly better than AD participants. This study represented one of the first published reports of performance based evidence for functional decline and diminished capacity in MCI (Griffith et al., 2003). Importantly, the results suggested that initial declines in financial capacity are already present in MCI prior to development of a frank dementia.

This excerpt of the FCI line of research supports the value of performance-based assessment of financial capacity in older adults with dementias of aging. The FCI represents an advance in functional assessment in dementia (Moye, 2003). It is specific to the construct of financial capacity, and is based on a model conceptualizing financial capacity as a series of discrete spheres of activity (domains) linked to independent community functioning. The FCI has demonstrated construct validity by discriminating the financial performance of controls, mild AD patients, and moderate AD patients (Marson et al., 2000), and the performance of controls, amnestic MCI patients, and mild AD patients (Griffith et al., 2003).

While the FCI has demonstrated efficacy in detecting loss of financial capacity in older adults with dementia, even early in the disease course, another aspect of financial competence involves the application of these financial skills to across an array of decision-making contexts. As we will see below, the ACED is a performance-based assessment tool developed to measure decision-making competence across a range of functional domains including financial management.

(ii). Assessment of Competency in Everyday Decisions (ACED).

A unifying consequence of the many diseases of aging is the loss of functional status, either in the instrumental activities of daily living such as managing money, medications or preparing a meal, or in the basic activities of daily living such as the abilities to bath, dress, or groom. These functional losses, whether from physical or cognitive causes, require care, such as having someone pay the bills or dress a person.

In many cases, the decision about how to provide this care is relatively straightforward, but in some cases, older adults have difficulty deciding whether to accept that assistance, or refuse it. These are common themes in cases of self-neglect or abuse, and they are of particular clinical and ethical concern, particularly when the decision involves social and ethical tradeoffs that engage costs, autonomy or privacy.

Clinicians facing such cases need to assess if the person has sufficient capacity to make the decision. This assessment not only has substantial implications on the course of clinical interventions, but it may also initiate legal actions that may ultimately lead to partial or complete guardianship. At the same time, however, persons who demonstrate sufficient capacity to refuse assistance have the right to do so, even when such choices conflict with their clinicians’ recommendations.

Thus far in the review we have described cognitive, social and neural correlates of financial decision-making skills. However, in this section we shift focus to decision-making capacity, conceptualized along at least one of four decisional abilities: understanding, appreciation, reasoning and stating a choice. The Assessment of Capacity for Everyday Decision- making, or ACED, was developed to assist in deciding whether an older adult is able to solve a specific functional problem (Lai and Karlawish 2007; Lai et al 2008). The ACED uses a semi-structured interview that assesses each of the four decisional abilities in order to produce a metric measure of how well a person performs on each of the abilities. Studies have examined how an older adult who has a functional deficit, such as problems managing money, understands and appreciates this problem, understands and appreciates the risks and benefits of solutions to that problem and can reason though choices about how to solve the problem (Lai et al 2007; Liu, Lam, Chau, Fung, Wong et al., 2013).

As an example of one of these studies, Lai and colleagues examined the capacity of 39 community-dwelling persons aged 65 or greater with mild to moderate stage dementia to solve one of the following documented functional problems: managing medications, managing finances, and preparing meals. The order of the ACED interview was as follows: understanding the problem, appreciating the problem, understanding the options to solving the problem, understanding the benefits of the options, understanding the harms of the options, appreciating the benefits of the options, appreciating the harms of the options, comparative reasoning, consequential reasoning, expressing a choice, and the logical consistency of that choice.

Patients were evenly divided into three stages of dementia severity: very mild (n=13); mild (n=13); and moderate (n=13). A comparison group of 13 family members, who were caregivers for the patients, provided a measure of divergent validity. Although both groups were equally capable of articulating a choice, they differed in their abilities to understand, appreciate, and reason. Caregiver performance on all ACED items was skewed towards the higher ranges with all but one person scoring within one point of the highest score.

In contrast, patient performance was distributed across the score ranges. Only 15 patients (38%) achieved an understanding score above the lowest score observed in the caregiver group. Only six patients (15%) scored in the highest category (7–8) of appreciation, whereas, all caregivers scored within the highest category. The majority of patients, 29 of the 39, scored between one and four. Contributing to the lower scores was notably poor performance on the appreciation item asking patients whether they believed that they had functional problem. Specifically, 22/39 (56%) demonstrated inadequate (score=0) recognition of proxy reported functional problems.

Performance on the ‘ability to reason’ was similar to appreciation. Only six patients (15%) were able to achieve scores of 9 or 10, the range of scores found in caregiver group for this ability. However, total scores above five points in this ability were observed for 30 patients (77%), reflecting the relatively strong performance on the two comparative reasoning questions and the one logical consistency question where ≤ 3% of patients scored less than one on each item. A moderate to strong correlation between performance on the ACED and the MacCAT-T, a measure of the capacity to make a treatment decision, in each of the four decision-making abilities further supported the ACED’s convergent validity.

These data show that it is possible to measure a patient’s ability to solve his or her everyday functional problems using an instrument tailored to fit each patient’s specific functional deficits, (i.e., my husband has left the stove on and bounced two checks). This person and problem specific interview can be of substantial value to deciding whether an older adult retains the capacity to decide how best to manage their disabilities, an issue of substantial concern in cases of elder abuse or neglect.

Thus far, we have shown that assessments of financial skills (e.g. FCI) and decision-making competence (e.g. ACED) are important for understanding vulnerability to financial risk in aging and brain disease. However, as we reviewed above, financial exploitation is inherently a social transaction. As we have seen above, older adults process, and integrate social information into decision-making processes differently from younger adults. This suggests that assessing financial decision-making in social contexts may be an important avenue for identifying exploitation risk, especially at the hands of a known other – a sphere where the vast majority of exploitation occurs (Acierno et al., 2010).

(iii). Social cognitive neuroscience model of financial exploitation.

Older adults experience changes in both cognitive and socio-emotional functioning that can lead to poor decision making ability and ultimately exploitation risk. As discussed above, functional and structural brain changes in older adulthood lead to reduced fluid intellectual abilities, including reasoning and problem-solving, as well as social-emotional changes such as a positivity bias, reduced sensitivity to future financial loss, reduced deception detection and poor trust-worthiness judgments. Age-related changes in both domains, their interaction, may leave older adults increasingly vulnerable to exploitation.

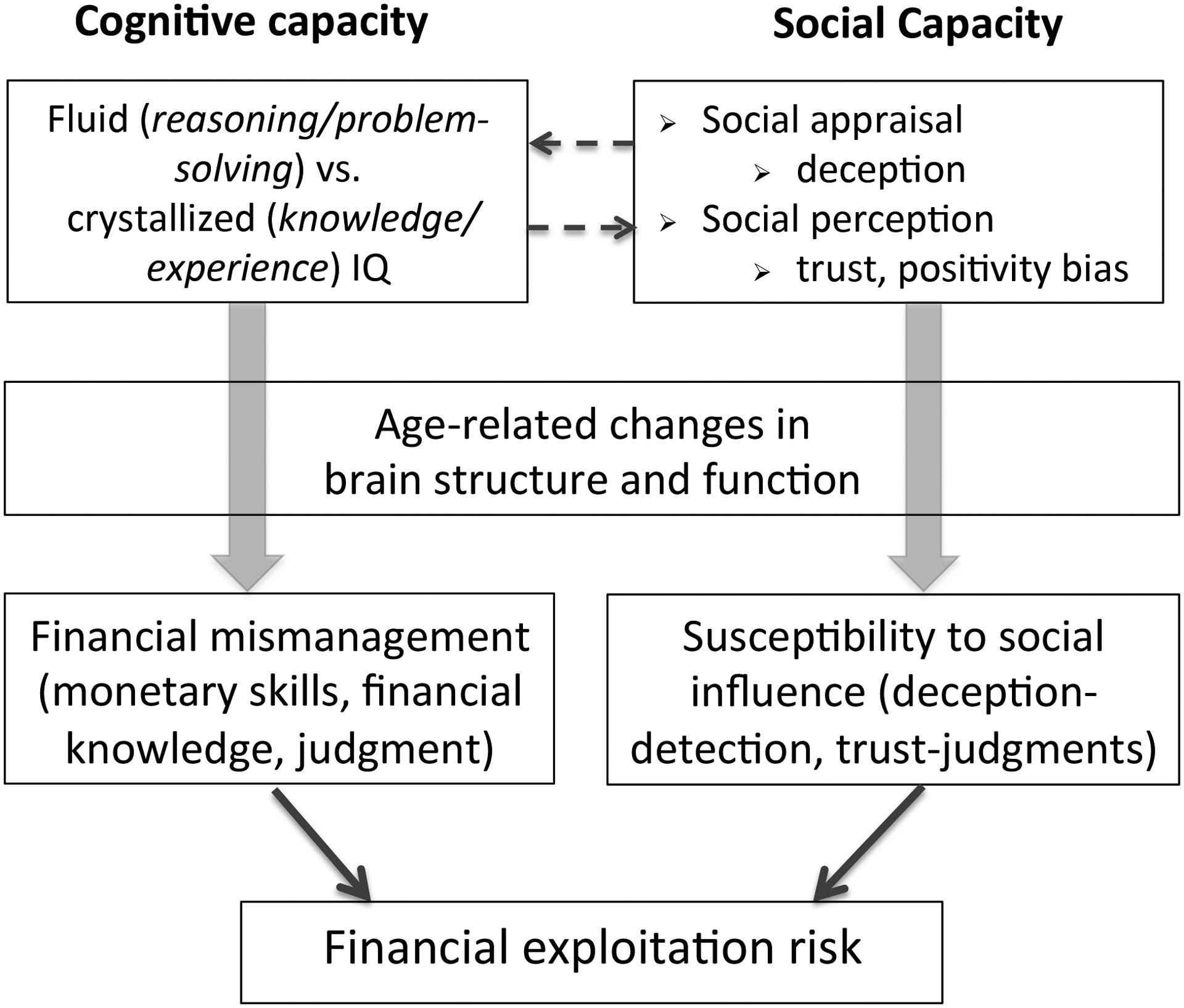

Recognizing that age-related change occurs in brain, cognition and social functioning, we have developed a novel framework for assessing financial exploitation risk in older adulthood (Figure 1). As we reviewed in the first two sections, there are myriad determinants of financial exploitation risk. These include non-modifiable factors, such as demographics, socioeconomic status, geographical location or race, as well as contextual factors such as financial regulatory regimes, availability of community and social support, or access to educational and informational resources. As with a recently proposed model of decision-making ability (Lichtenberg, 2016), our model focuses primarily on person-centered factors, such as neuropsychological and functional capacities, as mediated by age-related changes in brain structure and function. Based on the research reviewed earlier, we argue that there are two behaviorally and neurally distinct pathways to increased exploitation risk.

Figure 1. Social cognitive neuroscience model for assessing financial exploitation risk.

Two interacting pathways can lead to increased exploitation risk in older adulthood. Cognitive changes are associated with reduced financial skills, and increased risk of exploitation through financial mismanagement. Changes in social cognition are associated with increased exploitation risk through undue social influence, coercion or deception at the hands of others. Both pathways are associated with dissociable patterns of structural and functional brain change (see text for details).

The first pathway originates from age-related changes in the balance between fluid intelligence abilities (which decline) and crystallized intelligence (which are preserved or increase) (see section 2.3 above). Loss of fluid relative to crystallized capacities can result in poor attentional capacity, poor goal direction, planning, and loss of cognitive ability necessary to adapt to shifting contingencies. These changes can ultimately result in financial mismanagement, consistent with recent research (e.g. James et al., 2014; Han et al., 2015; Marson et al., 2000).

The second pathway originates from reduced social capacity (specified in our model as social appraisal and perception) in older adulthood. Older adults show reduced ability to appraise and detect potentially deceptive information (Denburg et al., 2007). They also demonstrate difficulty perceiving social cues necessary to make appropriate trust-worthiness judgments (Asp et al., 2012), or display increased attention to more positively-valenced information (Charles and Carstensen, 2011). These changes in social cognition may leave older adults more vulnerable to undue social influences, resulting ultimately in increased risk of exploitation at the hands of others, although research directly addressing this relationship remains in it’s infancy.

Critically, both pathways are associated with dissociable patterns of brain changes in older adults. Functional and structural changes in lateral frontal and parietal brain regions have been implicated in age-related decline in fluid reasoning ability such as working memory, inhibition and mental flexibility (Turner and Spreng, 2012). In contrast changes in socio-emotional functioning have been associated with alterations in the affective-integrative-motivational brain circuit (Samanez-Larkin and Knutsen, 2015), default network brain regions (Asp et al., 2012; Cassidy et al., 2013; Griffith et al., 2010), or their interaction. In developing this social cognitive neuroscience model of exploitation risk, we put forth the idea that recognizing and appreciating these dissociable patterns of behavioral and brain change will help in the development of more context-specific indicators of financial exploitation risk in older adulthood (e.g. heightened vulnerability to exploitation in situations of high versus low social complexity).

As depicted in Figure 1, declines in cognitive capacity, associated with changes in lateral PFC would predict increased difficulty with financial management tasks such as problem-solving, planning or reallocation of resources. In contrast, declines in social capacity, associated with changes in default network brain regions, or their interactions with subcortical brain regions involved in affect processing, would lead to increased social vulnerability and exploitation at the hands of others. This dual-path model is not meant to imply that cognitive and social capacities are entirely dissociable. These undoubtedly interact (represented by the reciprocal arrows in the top row of Figure 1). For example, declines in working memory have been associated reduced capacity to mentalize about the thoughts or intentions of others (i.e. theory of mind, McKinnon and Moscovitch, 2007).

The intent of the model is to highlight both the cognitive and social changes that occur in older adulthood, and how these may lead to different patterns of vulnerability for older adults. As our review here has shown, assessments of cognitive and social function, as well as brain structure and function, are well established. However, there is not, as yet, a single tool for the assessment of both cognitive and social capacity in the context of everyday financial decision-making. In the next section we proposed a novel assessment tool designed to fill this gap and identify older adults at risk for financial exploitation, whether through financial mismanagement or undue social influence or coercion.

(iv). Financial Competence in Everyday Decision-making (FCED).

Based on the social cognitive neuroscience model of financial exploitation described above (and represented in Figure 1), the ACED (Lai and Karlawish, 2007, Lai et al., 2008) was adapted to include financial scenarios with varying levels of social complexity. During administration of the FCED, two scenarios are presented, one involving high social complexity (exploitation of an older adult by a grandson) and another with low social complexity (telemarketing credit card fraud). These vignettes are drawn from known cases of older adult financial exploitation, and vetted by community agencies serving at-risk adults (e.g. Adult Protective Services). Recognizing the importance of both cognitive social determinants of exploitation risk, the FCED includes scenarios involving potential exploitation by an unknown (telemarketer) as well as a known other (grandson). These scenarios reflect actual reported cases of financial exploitation (Peterson et al., 2014).

As with the ACED, the FCED is designed to measure understanding, appreciation, and reasoning in financially-risky situations. Within the appreciation and reasoning sections, the adapted protocol includes separate qualitative and quantitative performance ratings for social (“I didn’t want to harm my relationship with my grandson”) and non-social (“I can’t afford to lose money”) responses.

The protocol follows a structured interview format, with a trained administrator guiding the subject through each phase of the assessment. The protocol begins with the presentation of the scenario and then proceeds through open-ended questioning of the subject’s understanding of the facts of the situation, appreciation of the possible options, and reasoning about the advantages and disadvantages of those options. Each stage of the assessment (understanding, appreciation and reasoning) includes two levels of probing. The first involves an open-ended response period with minimal prompting. The second involves specific probing by the examiner about various aspects of the scenario or options under consideration. This extra probing allows the evaluators to determine whether the subject was able to generate information and solutions independently, or whether their performance could be aided by additional supports. Administration time is approximately 30 minutes, although there is some variability depending on subject response styles. Interviews are scored following a detailed protocol that includes exemplar responses for each score level and each rating criterion. Once examiners are trained on the scoring protocol, the assessment may be scored in real time using a standard scoring template. Scores are derived for overall financial competence with individual cognitive and social capacity scores.

The FCED is currently undergoing validation as a putative measure of financial exploitation risk. Few studies have investigated neurobehavioral differences between exploited and non-exploited older adults. This has left a significant gap in the literature and is a core recommendation in our proposed research agenda described in section IV. To partially address this research gap, the FCED is currently being administered to older adults who have, and have not, been victims of financial exploitation since aged 60.

In this section we reviewed decision-making capacity assessments developed to identify financial exploitation risk in normal aging and brain disease. A full review of the broad range of self-report and performance-based measures is beyond the scope of this paper. However, these approaches, and the broader literature reviewed throughout the paper, suggest that while financial exploitation risk is associated with broad demographic and socio-economic factors, individual differences in vulnerability to financial exploitation make the search for better assessment approaches an imperative for future research. In the concluding section we turn to recommendations for a research agenda to rapidly advance progress towards this urgent objective.

IV. Bridging the gap: An integrated research approach for early detection of financial exploitation risk in community-dwelling older adults

As revealed in this brief review, age-related changes in decision-making capacity can directly influence financial competence and financial exploitation risk in older adulthood. Rapid advances in our understanding of the cognitive, affective and social determinants of decision-making, and their neural basis, are opening new avenues for identifying person-specific predictors of exploitation risk. However, researchers need to narrow the gap between investigations of neural mechanisms underlying decision-making deficits, and assessments of financial competence in the real-world. As the recent review by Samanez and Knutsen (2015) clearly demonstrates, the neural mechanisms associated with decision-making in older adulthood are becomingly increasingly well-defined, providing opportunities for the development of more targeted decision-making aids. The social cognitive neuroscience framework proposed here (Figure 1) is an important advance in this regard, guiding the development of brain and behavioral markers to detect both the extent of exploitation risk as well as the context in which exploitation is most likely to occur.

However, there remains a significant gap between laboratory measures and real-world decision-making, specifically in the context of an at-risk older adult population where economic, health, and social pressures are likely the primary drivers of financial decisions. Efforts to bridge this gap are also proceeding in the opposite direction, from the clinic to research laboratory, with the development of ecologically valid assessment tools to measure decision-making and financial competence in vulnerable older adults (e.g. Lai and Karlawish, 2007, Lai et al., 2008; Marson et al., 2000). These instruments are now being incorporated into a neuroimaging environment to characterize the cognitive and neural basis of performance on these tasks (e.g. Sherod et al., 2009; Stoeckel et al., 2013).

While advances in each direction are essential to mapping the neural and neurocognitive basis of financial exploitation risk, a critical missing link remains access to community-dwelling seniors who have been, or continue to be, financially exploited. This is a challenging yet urgently necessary research need, to assess the discriminative validity of measures and markers of exploitation risk. To this end, greater collaboration between the research community and point of care service providers is necessary, to identify older adults who may have experienced exploitation for participation in research projects, to vet and validate translational opportunities arising from the research, and ultimately to reinforce this first line-of-defense by providing community and financial services workers with the information necessary to identify and prevent abuse before it occurs.

A recent White House Council on Aging report urged that much more research be conducted to improve surveillance and early detection of elder abuse (Pillemer et al., 2015). This will require large and diverse samples of older adults who have and have not been victims of exploitation to identify sensitive, specific, and generalizable behavioral and neural biomarkers of exploitation risk that will ultimately be translatable and useful for point of service providers. This will require large-scale, multi-site, and broadly-defined investigations of the neurobehavioral determinants of financial exploitation risk across the late adult lifespan – from normal aging to neurodegenerative disease. As we have shown here, much of this work is well underway. However efforts need to be scaled up to match the rapidly expanding scope of the problem in our aging population.

Funding

This work was supported in part by the Alzheimer’s Association (NIRG-14-320049) and a grant from the Elder Justice Foundation to R.N.S, grants from the NIA (P30: AG01024) and CDC (HBRN: U48 DP 005006, 005002, 005053, 005000, and 005013) to J.K. and a grant from NIA (R01 AG21927) to D.C.M.

References

- Acierno R, Hernandez MA, Amstadter AB, Resnick HS, Steve K, Muzzy W, et al. (2010). Prevalence and Correlates of Emotional, Physical, Sexual, and Financial Abuse and Potential Neglect in the United States: The National Elder Mistreatment Study. American Journal of Public Health, 100(2), 292–297. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Addis DA, Wong AT, Schacter DL (2008). Age-related changes in the episodic simulation of future events. Psych Sci. 2008, 19, 33–41. [DOI] [PubMed] [Google Scholar]

- Agarwal S, Driscoll J, Gabaix X, & Laibson D (2009). The age of reason: Financial decisions over the lifecycle and implications for regulation. Brookings Papers on Economic Activity, 2, 51–117. [Google Scholar]

- Amstadter AB, Zajac K, Strachan M, Hernandez MA, Kilpatrick DG, & Acierno R (2011). Prevalence and Correlates of Elder Mistreatment in South Carolina: The South Carolina Elder Mistreatment Study. Journal of Interpersonal Violence, 26(15), 2947–2972. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Andrews-Hanna JR, Smallwood J, & Spreng RN (2014). The default network and self-generated thought: component processes, dynamic control, and clinical relevance. Ann N Y Acad Sci, 1316(1), 29–52. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Asp E, Manzel K, Koestner B, Cole CA, Denburg NL, & Tranel D (2012). A neuropsychological test of belief and doubt: damage to ventromedial prefrontal cortex increases credulity for misleading advertising. Front Neurosci, 6, 100. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Beach SR, Schulz R, Castle NG, & Rosen J (2010). Financial exploitation and psychological mistreatment among older adults: Differences between African Americans and non-African Americans in a population-based survey. The Gerontologist, 50, 744–757. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Beadle JN, Paradiso S, Kovach C, Polgreen L, Denburg NL, & Tranel D (2012). Effects of age-related differences in empathy on social and economic decision-making. Int Psychogeriat, 24(5), 822–833. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Bechara A, Damasio H, Tranel D, Damasio AR. The Iowa Gambling Task and the somatic marker hypothesis: some questions and answers. Trends Cog Sci, 9(4), 159–62. [DOI] [PubMed] [Google Scholar]

- Boyle PA, Yu L, Wilson RS, Gamble K, Buchman AS, Bennet DA (2012). Poor decision making is a consequence of cognitive decline among older persons without Alzheimer’s disease or mild cognitive impairment. PLoS One, 7, e43647. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Buckner RL (2004). Memory and executive function in aging and AD: multiple factors that cause decline and reserve factors that compensate. Neuron, 44(1), 195–208. [DOI] [PubMed] [Google Scholar]

- Buckner RL, Andrews-Hanna JR, & Schacter DL (2008). The brain’s default network: anatomy, function, and relevance to disease. Ann N Y Acad Sci, 1124, 1–38. [DOI] [PubMed] [Google Scholar]

- Cassidy BS, Leshikar ED, Shih JY, Aizenman A, & Gutchess AH (2013). Valence-based age differences in medial prefrontal activity during impression formation. Soc Neurosci, 8(5), 462–473. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Carstensen L, Turan B, Scheibe S, Ram N, Ersner-Hershfield H, Samanez-Larkin GR, Brooks KP, & Nesselroade JR (2011). Emotional experience improves with age: evidence based on over 10 years of experience sampling. Psychol. Aging 26, 21–33. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Cassidy BS, Leshikar ED, Shih JY, Aizenman A, & Gutchess AH (2013). Valence-based age differences in medial prefrontal activity during impression formation. Soc Neuro, 8(5), 462–473. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Castle E, Eisenberger NI, Seeman TE, Moons WG, Boggero IA, Grinblatt MS, et al. (2012). Neural and behavioral bases of age differences in perceptions of trust. Proc Natl Acad Sci U S A, 109(51), 20848–20852. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Charles S, and Carstensen LL (2009). Social and emotional aging. Annu Rev Psychol, 61, 383–409. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Deem DL (2000). Notes from the field: Observations in working with the forgotten victims of personal financial crimes. Journal of Elder Abuse & Neglect, 12(2), 33–48. [Google Scholar]

- Denburg NL, Cole CA, Hernandez M, Yamada TH, Tranel D, Bechara A, et al. (2007). The orbitofrontal cortex, real-world decision making, and normal aging. Ann N Y Acad Sci, 1121, 480–498. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Dong X, & Simon MA (2013a). Association between reported elder abuse and rates of admission to skilled nursing facilities: findings from a longitudinal population-based cohort study. Gerontology, 59(5), 464–472. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Dong X, & Simon MA (2013b). Elder abuse as a risk factor for hospitalization in older persons. JAMA Intern Med, 173(10), 911–917. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Financial Industry Regulatory Authority [FINRA]. (2013). Financial Industry Regulatory

- Authority risk meter. Retrieved from http://apps.finra.org/meters/1/riskmeter.aspx

- Finucane ML, Mertz CK, Slovic P, Schmidt ES (2005). Task complexity and older adults’ decision-making competence. Psychol Aging, 20, 71–84. [DOI] [PubMed] [Google Scholar]

- Griffith HR, Belue K, Sicola A, Krzywanski S, Zamrini E, Harrell L, et al. (2003). Impaired financial abilities in mild cognitive impairment: a direct assessment approach. Neurology, 60(3), 449–457. [DOI] [PubMed] [Google Scholar]

- Griffith HR, Stewart CC, Stoeckel LE, Okonkwo OC, den Hollander JA, Martin RC, et al. (2010). Magnetic resonance imaging volume of the angular gyri predicts financial skill deficits in people with amnestic mild cognitive impairment. J Am Geriatr Soc, 58(2), 265–274. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Han D, Boyle PA, James BD, Yu L, & Bennett JS (2015). Mild Cognitive Impairment Is Associated with Poorer Decision-Making in Community-Based Older Persons. J Am Geriatr Soc, 63, 676–683. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Jackson SL, & Hafemeister TL (2011). Financial abuse of elderly people vs. other forms of elder abuse: Assessing their dynamics, risk factors, and society’s response. Final Report Presented to the National Institute of Justice. [Google Scholar]

- James BD, Boyle PA, Bennett JS (2014). Correlates of Susceptibility to Scams in Older Adults Without Dementia. J. Elder Abuse & Neglect, 26, 107–122. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Lachs MS, & Han SD (2015). Age associated financial vulnerability: An emerging public health issue. Ann Int Med, 163(11), 877–878. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Lai JM, & Karlawish J (2007). Assessing the capacity to make everyday decisions: a guide for clinicians and an agenda for future research. Am J Geriatr Psychiatry, 15(2), 101–111. [DOI] [PubMed] [Google Scholar]

- Lai JM, Cooney LM, Gill TM, Bradley EH, Hawkins KA, Karlawish JH Evaluating the Ability of Older Persons with Cognitive Deficits to Solve Problems in Performing their Activities of Daily Living. Journal of the American Geriatrics Society 2007; 55:D55. [Google Scholar]

- Lam LC, Lui VW, Chiu HF, Leung KF, Appelbaum PS, Karlawish J: Assessing mental capacity for everyday decision-making in the Chinese older population. Hong Kong Medical Journal 19(Supplement 9): 17–20, December 2013. [PubMed] [Google Scholar]

- Lantz PM, House JS, Mero RP, & Williams DR (2005). Stress, life events, and socioeconomic disparities in health: results from the Americans’ Changing Lives Study. J Health Soc Behav, 46(3), 274–288. [DOI] [PubMed] [Google Scholar]

- Laumann EO, Leitsch SA, & Waite LJ (2008). Elder mistreatment in the United States: Prevalence estimates from a nationally representative study. The Journals of Gerontology: Series B, Psychological Sciences and Social Sciences, 63, S248–S254. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Li Y, Baldassi M, Johnson EJ, Weber EU (2013). Complementary cognitive capabilities, economic decision making, and aging. Psych Aging, 28(3), 595–613. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Lichtenberg PA, Stickney L, & Paulson D (2013). Is psychological vulnerability related to the experience of fraud in older adults? Clin Geron: J. Aging Mental Health, 36, 132–146. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Lichtenberg PA, Ficker LJ, & Rahman-Filipiak A (2016). Financial decision-making abilities and financial exploitation in older African Americans: Preliminary validity evidence for the Lichtenberg Financial Decision Rating Scale (LFDRS). J Elder Abuse & Neglect, 28(1):14–33. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Lichtenberg PA (2016). Financial exploitation, financial capacity, and Alzheimer’s disease. Am. Psychol, 71(4), 312–320. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Liu V, Lam L, Chau R, Fung A, Wong B, Leung G, Leung KF, Chiu H, Karlawish J, Applebaum P: Structured Assessment of Mental Capacity to Make Financial Decisions in Chinese Older Persons with Mild Cognitive Impairment and Mild Alzheimer Disease. Journal of Geriatric Psychiatry and Neurology 26: 69–77, June 2013. [DOI] [PubMed] [Google Scholar]

- Loeb PA: ILS: Independent LivingScales Manual. San Antonio, Tex, Psycho-logical Corp, Harcourt Brace Jovanovich, 1996. [Google Scholar]

- Lusardi A, & Mitchell O (2006). Financial literacy and planning: Implication for retirement wellbeing. Business economics, 2007 (Jan), 35–44. [Google Scholar]

- Lusardi A, & Tufano P (2009). Debt literacy, financial experiences, and overindebtness. National Bureau of Economic Research. NBER Working Paper No. 14808. [Google Scholar]

- Marson DC, Sawrie SM, Snyder S, McInturff B, Stalvey T, Boothe A, et al. (2000). Assessing financial capacity in patients with Alzheimer disease: A conceptual model and prototype instrument. Arch Neurol, 57(6), 877–884. [DOI] [PubMed] [Google Scholar]

- Marson DC, Martin RC, Wadley V, Griffith HR, Snyder S, Goode PS, … Harrell LE (2009). Clinical interview assessment of financial capacity in older adults with mild cognitive impairment and Alzheimer’s disease. J Am Geriatr Soc, 57, 806–814. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Martin R, Griffith HR, Belue K, Harrell L, Zamrini E, Anderson B, et al. (2008a). Declining financial capacity in patients with mild Alzheimer disease: a one-year longitudinal study. Am J Geriatr Psychiatry, 16(3), 209–219. [DOI] [PubMed] [Google Scholar]

- McKinnon M & Moscovitch M (2007). Domain-general contributions to social reasoning: theory of mind and deontic reasoning re-explored. Cognition, 102(2), 179–218. [DOI] [PubMed] [Google Scholar]

- Moye J (2003). Guardianship and conservatorship. In Grisso T (Ed.), Evaluating Competencies: Forensic Assessments and Instruments (2nd ed., pp. 309–390). New York, NY: Plenum Press. [Google Scholar]

- The metlife study of elder financial abuse: Crimes of occasion, desperation and predation against america’s elders. National Committee for the Prevention of Elder Abuse (2011). Wesport, CT: Virginia Tech Metlife Mature Market Institute. [Google Scholar]

- Ochsner KN, Beer JS, Robertson ER, Cooper JC, Gabrieli JD, Kihsltrom JF, et al. (2005). The neural correlates of direct and reflected self-knowledge. Neuroimage, 28(4), 797–814. [DOI] [PubMed] [Google Scholar]

- Pak K, & Shadel D (2011). AARP Foundation national fraud victim study. Washington DC: AARP. [Google Scholar]

- Park DC, Polk TA, Mikels JA, Taylor SF, Marshuetz C. (2001). Cerebral aging: integration of brain and behavioral models of cognitive function. Dialogues in clinical neuroscience, 3(3), 151–65. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Peterson JC, Burnes DP, Caccamise PL, Mason A, Henderson CR Jr., Wells MT, et al. (2014). Financial exploitation of older adults: a population-based prevalence study. J Gen Intern Med, 29(12), 1615–1623. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Petersen RC, Doody R, Kurz A, Mohs RC, Morris JC, Rabins PV, et al. (2001). Current concepts in mild cognitive impairment. Arch Neurol, 58(12), 1985–1992. [DOI] [PubMed] [Google Scholar]

- Pillemer K, Connolly MT, Breckman R, Spreng RN & Lachs MS (2015). Elder mistreatment: Priorities for consideration by the White House conference on aging. The Gerontologist, 55, 320–327. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Pinsker DM, McFarland K, & Pachana NA (2010). Exploitation in older adults: Social vulnerability and personal competence factors. . The Journal of Applied Gerontology, 20(6), 740–761. [Google Scholar]

- Raichle ME, MacLeod AM, Snyder AZ, Powers WJ, Gusnard DA, & Shulman GL (2001). A default mode of brain function. Proc Natl Acad Sci U S A, 98(2), 676–682. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Ritchie K, Artero S, & Touchon J (2001). Classification criteria for mild cognitive impairment: A population based validation study. Neurology, 56, 37–42. [DOI] [PubMed] [Google Scholar]

- Ross M, Grossmann I, Schryer E (2012). Perspectives on Psychological Science, 9(4), 427–442. [DOI] [PubMed] [Google Scholar]

- Roy M, Shohamy D, & Wager TD (2012). Ventromedial prefrontal-subcortical systems and the generation of affective meaning. Trends Cogn Sci, 16(3), 147–156. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Samanez-Larkin GR, Gibbs SEB, Khanna K, Nielsen L, Carstensen LL, Knutson B (2007). Anticipation of monetary gain but not loss in healthy older adults. Nat Neuroscience 10, 787–791. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Samanez-Larkin GR (2013). Financial Decision Making and the Aging Brain. APS Obs, 26(5), 30–33. [PMC free article] [PubMed] [Google Scholar]

- Samanez-Larkin, & Knutsen A (2014). Reward processing and risky decision making in the aging brain. In Reyna V & Zayas V (Eds.), The Neuroscience of Risky Decision Making. Washington, D.C.: American Psychological Association. [Google Scholar]

- Samanez-Larkin GR, & Knutson B (2015). Decision making in the ageing brain: changes in affective and motivational circuits. Nat Rev Neurosci, 16(5), 278–289. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Schacter DL, Addis DR, Hassabis D, Martin VC, Spreng RN, Szpunar KK. (2012). The future of memory: Remembering, imagining, and the brain. Neuron. 76: 677–694. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Schafer MH, & Koltai J (2014). Does embeddedness protect? personal network density and vulnerability to mistreatment among older american adults. J Gerontology, Series B: Psychological Sciences and Social Sciences, 70(4), 597–606. [DOI] [PubMed] [Google Scholar]

- Seeley WW, Menon V, Schatzberg AF, Keller J, Glover GH, Kenna H, et al. (2007). Dissociable intrinsic connectivity networks for salience processing and executive control. J Neurosci, 27(9), 2349–2356. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Sherod MG, Griffith HR, Copeland J, Belue K, Krzywanski S, Zamrini EY, et al. (2009). Neurocognitive predictors of financial capacity across the dementia spectrum: Normal aging, mild cognitive impairment, and Alzheimer’s disease. J Int Neuropsychol Soc, 15(2), 258–267. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Spreng RN (2012). The fallacy of a “task-negative” network. Front Psychol, 3, 145. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Spreng RN, Gerlach KD, Turner GR & Schacter DL (2015). Autobiographical planning and the brain: Activation and its modulation by qualitative features. J Cognit Neurosci, 27, 2147–2157. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Spreng RN, Schacter DL (2012). Default network modulation and large-scale network interactivity in healthy young and old adults. Cereb Cortex, 22, 2610–2621. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Spreng RN, & Turner GR (2013). Structural covariance of the default network in healthy and pathological aging. J Neurosci, 33(38), 15226–15234. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Stoeckel LE, Stewart CC, Griffith HR, Triebel K, Okonkwo OC, den Hollander JA, et al. (2013). MRI volume of the medial frontal cortex predicts financial capacity in patients with mild Alzheimer’s disease. Brain Imaging Behav, 7(3), 282–292. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Turner GR, & Spreng RN (2012). Executive functions and neurocognitive aging: dissociable patterns of brain activity. Neurobiol Aging, 33(4), 826 e821–813. [DOI] [PubMed] [Google Scholar]

- Turner GR, & Spreng RN (2015). Prefrontal Engagement and Reduced Default Network Suppression Co-occur and Are Dynamically Coupled in Older Adults: The Default-Executive Coupling Hypothesis of Aging. J Cogn Neurosci., 27(12), 2462–2476. [DOI] [PubMed] [Google Scholar]

- Uddin LQ (2015). Salience processing and insular cortical function and dysfunction. Nat Rev Neurosci, 16(1), 55–61. [DOI] [PubMed] [Google Scholar]

- Weierich MR, Kensinger EA, Munnell AH, Sass SA, Dickerson BA, Wright CI, & Feldman Barrett L (2011). Older and wiser? An affective science perspective on age-related challenges in financial decision making. Soc Cog Affect Neuro, 6, 195–206. [DOI] [PMC free article] [PubMed] [Google Scholar]