Abstract

Coronavirus 2019 (COVID‐19) has caused ongoing disruptions to U.S. meat markets via demand and supply‐side shocks. Abnormally high prices have been reported at retail outlets and meat packers have been accused of unfair business practices because of widening price spreads. Processing facilities have experienced COVID‐19 outbreaks resulting in shutdowns. Using weekly data on wholesale and retail prices of beef, pork, and poultry, we characterize the time series behavior and dynamic linkages of U.S. meat prices before the COVID‐19 pandemic. We model vertical price transmission using both linear and threshold autoregressive (AR) models and vector error correction (VEC) models. With the estimated models, we then compare price movements under COVID‐19 to model predictions. All three meat markets are well‐integrated and we observe unexpected, large price movements in April and May of 2020. Early COVID‐19 related shocks appear to be transitory with prices returning to expected levels at a pace consistent with the speed of transmission prior to the pandemic. This well‐functioning market process suggests a degree of resilience in U.S. meat supply chains.

Keywords: beef, COVID‐19, pork, poultry, price transmission

1. INTRODUCTION

Coronavirus‐2019 (COVID‐19) has had major economic impacts in the United States and worldwide (Baker, Bloom et al., 2020; Jinjarak et al., 2020; Laborde et al., 2020). COVID‐19 is a disease caused by infection with the novel coronavirus SARS‐CoV‐2. The virus is thought to have originated in Wuhan, China in late 2019 but has since spread across the globe (Zhou et al., 2020). Respiratory effects of COVID‐19 can be acute and the disease usually appears clinically in the form of a cough, nasal congestion, fever, and other signs of upper respiratory infection. These symptoms can progress to viral pneumonia and in severe cases may result in a wide range of serious health impacts which can lead to death (Velavan & Meyer, 2020). As of August 14, 2020, the U.S. had experienced over 5.2 million cases and 168 thousand deaths (World Health Organization, 2020). While estimated infection and death rates are being updated daily by the Centers for Disease Control and Prevention, SARS‐CoV‐2 is widely regarded as highly infectious.

The COVID‐19 pandemic has affected the U.S. agricultural sector through a variety of channels. Impacts have been particularly pronounced in the U.S. meat sector where policymakers have brought increased attention to price transmission, marketing margins, and the continued supply of meat. In a March 31, 2020 letter to Attorney General William Barr and Secretary of Agriculture Sonny Perdue, Senator Chuck Grassley of Iowa asked for Justice Department and Department of Agriculture (USDA) investigations into “potential market manipulation and unfair practices” in the cattle industry following the COVID‐19 outbreak in the U.S. (Grassley, 2020). This call was echoed by legislators in the largest farm states and precipitated by an increase in the farm‐retail price spread for beef over the month of March (Comer, 2020; Rounds et al., 2020). On April 8, 2020, Secretary Perdue announced that USDA's Packers and Stockyards Division would extend investigations of beef price spreads to cover the COVID‐19 epidemic.

Shortly after the USDA announced expanded investigations of beef packers, outbreaks of COVID‐19 began to impact processing facility operations. On April 12, 2020, Smithfield Foods announced that it would idle a Sioux Falls Plant for an indefinite period of time (Bunge, 2020a). By April 15, the plant had become the largest single source of COVID‐19 cases in the U.S. Several other meat processing facilities closed or moved to limited operations (Bunge, 2020b). USDA food safety inspectors working in the plants also contracted the virus (Bagenstose et al., 2020). Plant closures affect prices up and down the supply chain with the press reporting possible meat shortages at retail outlets (Almeida & Dayy, 2020). In response to possible food shortages, President Trump issued an executive order under authority of the Defense Production Act to ensure continued supply of beef, pork, and poultry (Trump, 2020).

In addition to changes to supply conditions, there is growing evidence that COVID‐19 has caused a shift in demand both across and within different types of meat (Cavallo, 2020; Cranfield, 2020). Closures of restaurants and other food service businesses clearly cause a decline in expenditures on food away from home. As far as various types of meat tend to be consumed away from—instead of at—home, there are likely to be differential demand effects by type or cut of meat (Weersink et al., 2020). As well, consumers are responding to changes in income due to macroeconomic effects of the pandemic (Gay et al., 2020). Given the length of the pandemic, it remains to be seen whether consumers will revert back to previous consumption habits or if COVID‐19 has resulted in a permanent change in food and meat consumption behavior.

Price adjustments to COVID‐19 occur simultaneously in a complex system of price discovery; these adjustments are bellwethers of market efficiency and resilience. They also provide a means of measuring the magnitude of exogenous shocks to a system. In lieu of measurement of the underlying fundamentals of agricultural markets, price analysis provides a reduced‐form approach for understanding how markets react to shocks. For markets with multiple levels, reactions to disequilibria involve price transmission. Price transmission refers to the process by which prices integrate markets both vertically, across space, and across time.

Price linkages between markets are important indicators of market performance. In markets with vertical relationships, price transmission is typically characterized in terms of the size and speed of price adjustments to shocks at different levels of the market. If economic agents are subject to constraints on their adjustments to shocks, adjustments may occur with low speed and significant lag. The presence of transaction costs can increase the size of the shock required for price transmission to occur. In contrast to spatial price transmission, studies of vertical price transmission are complicated by the fundamental changes that occur to commodities as they move through the supply chain.

Imperfect price transmission, whether the result of the exercise of market power or for other reasons, implies that price changes at farm, wholesale, or retail levels are only slowly or partially transmitted to other levels of the supply chain, if at all. Asymmetries in price transmission, whereby positive and negative shocks exhibit different patterns of adjustment or when there are different adjustments going up or down the supply chain, play an important role in welfare evaluation in agricultural markets. Therefore, modeling of asymmetric adjustment has assumed a central role in modern studies of price transmission. Linear and nonlinear time‐series models that are capable of incorporating asymmetries have enabled empirical study of asymmetric responses to shocks. These increasingly flexible methods allow for tests of the underlying economic theory of price transmission and a richer assessment of price behavior.

Ultimately, price movements result from changes to both supply and demand; COVID‐19 has caused shocks to both sides of meat markets. The shocks of greatest impact in the near term appear to be related to supply issues arising from the labor intensive nature of meatpacking. In the long term, COVID‐19 may result in changes to diets and thus in changes to demand for meat. Several recent articles have examined the impacts of COVID‐19 on meat markets in particular. Lusk et al. (2021) examine beef and pork marketing margins (farm to wholesale) and document the effects of plants running at reduced capacity. They present evidence that packers are not operating in a non‐competitive manner and note that changes in marketing margins can occur under competitive markets with large supply shocks. Martinez et al. (2021) and Maples et al. (2021) examine changes to U.S. cattle and poultry markets, respectively, as a result of COVID‐19. In addition to changes in slaughter resulting from COVID‐19 infections at processing facilities, Martinez et al. (2021) note that a decline in food purchased away‐from‐home resulted in a major decline in demand for live cattle from the food service industry. Maples et al. (2021) cite a similar decline in demand in poultry.

Analogous concerns are voiced in articles by McEwan et al. (2020), Weersink et al. (2020), and Rude (2020) on the Canadian pork, poultry, and beef industries, respectively. All three articles devote some attention to supply shocks caused by infections at processing facilities, with Weersink et al. (2020) and Rude (2020) suggesting that the impacts of such shocks are likely to be short‐lived. On the other hand, they suggest that longer term changes may result from demand side shocks. Cranfield (2020) provides an overarching discussion of food demand response, while Goddard (2020) contains some statistics for food demand in Canada at the beginning of the pandemic. Concerns surrounding demand for meat relate primarily to lower household incomes, shifts from food away from home to food at home, and food delivery as opposed to in‐store purchase,

Baker, Bloom, et al. (2020) and Goddard (2020) document sharp decreases in restaurant spending at the beginning of the pandemic. Baker, Farrokhnia, et al. (2020) additionally show that grocery spending initially increased but then declined. Interestingly, food delivery spending was mostly flat through the end of March 2020. Chang and Meyerhoefer (2021) found that demand for online food shopping services increased with COVID‐19 prevalence in Taiwan. Most of the published articles mentioned above make use of data going through March or April of 2020 and are informative with respect to COVID‐19 impacts at early stages of the pandemic.

A recent article by Cavallo (2020) uses credit card and debit card transactional data to construct consumer price index baskets for the U.S. through early June, 2020; while macroeconomic in focus, there are several interesting findings in terms of demand for food products. Grocery spending peaked in late March but remained flat from April onwards. Restaurant and hotel spending declined by over 50% but has continued to rise since April. Although Cavallo (2020) is concerned with constructing a COVID‐19 consistent CPI, he provides some embedded insights for food markets. As part of total consumer expenditures, and with reference to the weights of the normal CPI, the weight on food at home increased by nearly fifty percent, the weight on grocery spending decreased by nearly fifty percent, and the weight on alcoholic beverages increased by about fifty percent. The impact of COVID‐19 on meat markets can then be summarized as a series of (ongoing) shocks to both meat supply and demand. Even without measurement of exogenous factors affecting supply and demand, price movements are readily available and can be assessed through application of time series statistical methods.

Motivated by the significant effect of COVID‐19 on U.S. meat markets, we empirically assess price transmission between levels of the beef, pork, and chicken sectors using linear and threshold vector error correction (VEC) models and linear and threshold autoregressive (AR) models. We also implement a VEC model of all six price series that accounts for cross‐price effects. These models recognize nonstationarity in the underlying price data and allow for asymmetric responses in price transmission. The models are estimated using a unique set of data on weekly prices for meat composites at wholesale and retail levels. The data run through early July of 2020, allowing price movements under COVID‐19 to be compared to predicted prices through an event study (Campbell et al., 1997). The event study provides measures of the impact of COVID‐19 and illustrates how shocks from the pandemic cause prices to deviate from modeled behavior.

We find that beef, pork, and poultry markets were well‐integrated prior to the incidence of COVID‐19. The pandemic coincided with severe, historically large changes in prices for beef and pork. Chicken prices did not see major fluctuation. However, prices appear to be at, or returning to, previously forecasted levels, suggesting that some COVID‐19 shocks may only be transitory. We suggest that these major transitory shocks likely relate to supply bottlenecks caused by reduced plant operating capacity. In any event, sustained gaps in meat supply failed to occur as equilibrating price movements provided an incentive for packers to keep plants operating. The full effect of the pandemic is likely to be revealed only after it has fully abated and markets return to normal conditions. Nonetheless, evidence thus far indicates that the U.S. livestock sector is capable of managing and responding to the disequilibria arising from COVID‐19.

2. PRICE TRANSMISSION IN AGRICULTURAL MARKETS

An extensive body of research has investigated issues associated with linkages among markets that are spatially, temporally, and vertically distinct. These studies are usually concerned with measurements of market efficiency (however defined) or market responses to extreme shocks. Much of this research has addressed market interrelationships among geographically separated markets for a homogeneous commodity. This work is often characterized as evaluations of spatial market integration. A survey of this research can be found in Fackler and Goodwin (2001) with specific applications in Adbulai (2000), Tostão and Brorsen (2005), Serra et al. (2006), Myers and Jayne (2012), Chen and Saghaian (2016), and Lence et al. (2018). Ongoing concerns regarding geographic market segmentation and disruptions in transportation and marketing channels as a result of COVID‐19 highlight spatial price transmission as an important concern in this context.

A separate but related line of research, that includes this study, has examined price transmission across th supply chain. In agricultural contexts, studies of vertical price transmission concentrate on relationships among farm, wholesale, and retail prices. Early work in this area used structural models to describe price behavior in agricultural markets (Gardner, 1975). A central concern in such studies is the response of markets to shocks that can occur at one or all levels of the market. The speed with which prices are transmitted, the magnitudes of transmission, and nonlinear behavior in price transmission, can be important indicators of market inefficiency. Moreover, they can imply differences in the welfare impacts of shocks on market participants.

An extensive survey of the vertical price transmission literature was undertaken by Meyer and von Cramon‐Taubadel (2004) and many conceptual issues in price transmission were discussed by Lloyd (2017). Some examples—in a variety of agricultural settings—include Boyd and Brorsen (1988), Griffith and Piggott (1994), Cramon‐Taubadel (1998), Azzam (1999), Franken et al. (2011), Ben‐Kaabia and Gil (2007), Ahn and Lee (2015), and Hahn et al. (2016). Examinations of the transmission of shocks among farm, wholesale, and retail markets for beef and/or pork were presented by Goodwin and Holt (1999) and Goodwin and Harper (2000). Their research found that important asymmetries characterized the transmission of shocks among different levels of the marketing chain, with farm prices often realizing negative shocks from other markets but finding much less response to price increases.

A number of theoretical explanations are consistent with observed asymmetries and imperfect price pass‐through. These include cost of adjustment (Bailey & Brorsen, 1989), inventory behavior (Wohlgenant & Mullen, 1987), and policy interventions (Serra & Goodwin, 2003). Non‐competitive behavior can also result in asymmetric price transmission (Abdulai, 2002; Acharya et al., 2011). Market power is often forwarded as an explanation for imperfect price transmission; monopsony power has attracted increased attention as livestock industries have become increasingly concentrated (Kuiper & Lansink, 2013; McCorriston et al., 1998). However, imperfect price transmission is only suggestive of the exercise of market power by market participants (Weldegebriel, 2004). The ultimate cause of imperfect transmission cannot be ascertained without a structural model which itself would rest on maintained assumptions or without careful comprehension of the institutional details of the markets being studied.1

Studies of vertical price transmission, and the assignment of asymmetric adjustment to any single cause, are complicated by the conceptual framework of vertical markets. Unlike spatially differentiated markets, for which the underlying commodity is relatively homogeneous, commodities undergo transformation as they move from the farm to retail level. In many cases, the underlying commodity is a single input to the production process which may include other commodities, labor, and the use of capital equipment; these other inputs are rarely observed. Because of this difference, the exact causes of imperfect price transmission in vertical markets are difficult to identify solely on the basis of model results. The study of vertical price transmission thus requires greater attention to the specific details of the markets under consideration.

3. ECONOMETRIC METHODS

We first consider the time series properties of the price data and then estimate models capable of capturing linear and nonlinear behavior in the transmission of prices. Stationarity and cointegration (and their alternatives) are statistical features that characterize time series processes. Many time series are nonstationary and must be differenced to be made stationary; a time series which is differenced d times to be made stationary is referred to as integrated of order d. Because the concept of cointegration is defined for variables with certain stationarity properties, most price transmission studies begin with an assessment of stationarity in the individual price series. Nonstationary behavior being confirmed, attention is then directed to cointegration.

We use standard augmented Dickey‐Fuller (ADF) tests to test for the presence of a unit root (i.e., whether the time series exhibit nonstationary behavior) (Dickey & Fuller, 1979; Said & Dickey, 1984). Studies have shown that the ADF test can suffer from low power and size distortions (Schwert, 2002). Test results also depend on lag selection; rules of thumb are often used to select the number of lags. Recognizing these drawbacks of the traditional ADF test, we also implement an efficient unit root test of Ng and Perron (2001). The optimal lag length for the test is selected as in Ng and Perron (2001) and we use the same chosen optimal lag length in the ADF test.

Engle and Granger (1987) introduced the concept of cointegration which occurs when two or more variables are nonstationary but a linear combination of the variables is stationary. Consider two nonstationary economic variables which are linked by a long‐run, stable relationship such that

| (1) |

with yt and xt representing prices at different levels of the meat supply chain. Equation (1) shows a standard cointegration relationship where vt = φvt− 1 + is referred to as the error correction term. The behavior of vt determines whether the variables are cointegrated. Cointegration implies that the price variables move together in the long run but may diverge in the short run.

Engle and Granger (1987) suggest a cointegration testing procedure whereby Equation (1) is estimated and the residuals are tested for stationarity. We implement the augmented Dickey‐Fuller test for a unit root in the residuals. We also test for cointegration using the trace‐based test of Johansen (1991). Engle and Granger (1987) show that if two variables are cointegrated, as in Equation 1, they can be represented as a VEC model. The Johansen test is based on the vector error correction (VEC) representation of the cointegrated variables. It does not require the two‐step procedure of the test of residuals.

Once stationarity and cointegration tests are complete, and with confirmation of cointegration, a natural question is whether price transmission and correction of short run disequilibria are characterized by nonlinear, asymmetric behavior. Balke and Fomby (1997) implemented a threshold model to evaluate possible departures from equilibrium in a cointegrated system. Nonlinearity tests can be applied to the residuals of equation 1 to test whether consideration of threshold cointegration is warranted. If the tests fail to reject linearity, we can model the residuals using an autoregressive (AR) model and model the cointegrated system as a VEC model.

We implement a total of four tests for nonlinear behavior (linearity) in the analysis that follows. The first two tests are based on the theory of neural networks. Neural network models can approximate any nonlinear function to an arbitrary degree. The test of Tera¨svirta et al. (1993) relies on Taylor series expansions of the neural network model. The second neural network‐based test was introduced by White (1989). It was subsequently compared with several other tests for nonlinear behavior by Lee et al. (1993) and found to have favorable statistical properties. The third test of Tsay (1986) is a Tukey nonadditivity type test. Lastly, we implement the likelihood ratio test of Chan (1991). This test compares the null hypothesis of a normal autoregressive process with the alternative of a threshold autoregression.

Nonlinear behavior in the error correction terms suggests that they do not follow a linear AR process. In particular, they may be more appropriately characterized by a self‐exciting threshold autoregression (SETAR) model, as applied in Balke and Fomby (1997). The SETAR approach allows for asymmetric adjustment to shocks with the error correction term now following

| (2) |

where T is the threshold value for the two‐regime case with regimes L and H. Asymmetric adjustment occurs when φL is not equal to φH .

Let the VEC model be given by

| (3) |

This representation can also be extended to include threshold behavior in the fashion of Cramon‐ Taubadel (1998) and Goodwin and Holt (1999). The threshold vector error correction model (TVECM) is

| (4) |

with two regimes L and H. Note that vL and vH denote the error correction terms in each of two regimes. Threshold behavior in cointegration can thus be described by either a SETAR model of the residuals from the cointegrating regression or a TVECM.

We use both AR and SETAR models and VEC and TVEC models to evaluate the dynamic patterns of price adjustment. Standard and generalized impulse response functions are used to evaluate price behavior. The nature of the impulse responses depends on the timing, size, and direction of the shocks. The generalized impulse is given by

| (5) |

Time series models can be described by a number of different generalizations of impulse responses (Koop et al., 1996). We consider regime‐specific standard impulse responses which use parameters from each regime for the threshold models. Generalized impulse responses are also shown where large numbers of shocks are applied to the univariate distributions at different points in the data and replicated to determine overall patterns for the entire analysis. This provides inference for the impact of market‐wide shocks.

Lastly, we conduct an event study by comparing predictions from the econometric models to price behavior observed under COVID‐19. Discussions of the event study methodology are provided by Campbell et al. (1997) and Gürkaynak and Wright (2013). Briefly, the approach is to estimate a model over an estimation window preceding an event and compare the results of this model to the outcome variable after the event occurs. In this case, we are interested in anomalous or abnormal price movements. An abnormal price is defined as one that is higher or lower than the price expected under the model: in other words, the forecasted price. In the absence of a sufficient amount of data following an event, or for an event that has recently occurred, the event study approach provides a method for assessing the impact of the event on the price system.

The event study requires selection of an estimation window and event period through event definition. Event definition may be difficult for a worldwide pandemic such as COVID‐19. COVID‐ 19 first appeared in late November 2019, but the first case in the United States was not reported until 2020. Moreover, there appears to have been a significant lag between the first reported case in the U.S. and any major economic effects in livestock markets. The two most immediate COVID‐19 related shocks appear to be found in an increased demand for food at retail and decreased demand for food away from home in late March and meat processing plant shutdowns which started to occur in the middle of April. The second shock appears to have had the largest effect on prices, possibly because it revealed labor vulnerabilities in meatpacking operations.

Based on the evolution of the pandemic, and observed price movements in meats, we take any date before April 1, 2020 as the estimation window. The last data reporting date in the estimation window is March 28, 2020, several days before Senator Grassley's letter on the meatpacking industry. This is also several weeks before plant shutdowns were reported. Inclusion of the event period in the estimation window has the potential to bias the estimated models. The event period cutoff date was robust to the choice of earlier dates with similar models and results being implied.

An important qualification of the event study implemented here is that the forecasted price is not the price that would have prevailed, ceteris paribus, without COVID‐19. In fact, it is the price that would have prevailed without COVID‐19 and any other shocks that have occurred during the event period. The pandemic has had effects in a number of markets related to meat retail markets, such as markets for animal feed. As well, shocks unrelated to COVID‐19 have directly affected meat demand and supply since April 1, 2020. The event study would only provide an estimate of the impact of COVID‐19 on these markets, all else equal, if all other shocks could be assumed away or accounted for in the model. Such concerns are likely to affect other studies that may seek to use COVID‐19 as a natural experiment. In spite of this limitation in terms of the counterfactual, the event study still provides insight into the nature of market adjustments during the COVID‐19 pandemic.

4. DATA

We collected weekly data on wholesale and retail prices of beef, pork, and chicken. Wholesale prices for beef and pork composites were provided by the Economic Research Service (ERS) and Agricultural Marketing Service (AMS). The wholesale chicken price was obtained from the Livestock Marketing Information Center and the National Whole Broiler/Fryer Report conducted by AMS. We do not analyze pork and poultry farm prices as most production in these markets is contracted, making quoted cash prices misleading or impossible to find. While the majority of beef cattle are still sold on the open market, the use of production contracts in this sector has increased as well.

Retail prices were taken from National Weekly Retail Activity Reports provided by AMS. These retail reports consist of advertised retail pricing in major supermarkets. Prices underlying the reported price are mostly from retailer websites. The retail price used in our analysis is the average price per pound for a beef or pork composite. The retail price for chicken is the price for a bagged fryer reported in the AMS National Weekly Retail Activity Reports. The composite retail prices for beef and pork are constructed using item level or cut prices. To create the composites, we used the same approach as implemented by the ERS in constructing monthly retail composites from Bureau of Labor Statistics price data.

Reported prices were combined by week; for example, a Friday wholesale report is matched with the Saturday retail report of the same week. Prices at different levels were missing for a small number of dates. In these situations, we used cubic spline interpolation to construct the full set of weekly prices. Even in the most extreme cases, less than 5% of observations required interpolation. In the analysis that follows, we consider the beef, pork, and poultry datasets to be distinct and all analyses focus on linkages across market levels for a specific type of meat.

Previous studies have shown that cross‐sectional data aggregation, incorporation of temporary sales prices, and temporal aggregation can have important impacts on the results of price transmission studies and their interpretation. On the last point, temporal aggregation is unlikely to result in major inconsistencies here because the report times differ only by a day and measure the same week. However, we are aggregating across stores and regions and the data at the retail level include sales prices. The implications of cross‐sectional aggregation are discussed in von Cramon‐Taubadel et al. (2006). Briefly, they show that aggregation leads to price transmission dynamics with slower response than on average at the store level. However, estimates of long‐run equilibria are not affected. In contrast, incorporation of sales prices will cause price transmission to appear faster, at least in disaggregated data (Tifaoui & Von Cramon‐Taubadel, 2017). Some additional discussion and implications of the use of scanner data versus data collected from the Bureau of Labor Statistics at different frequencies are provided in Pozo et al. (2021). Our price transmission dynamics therefore do not correspond to specific items at the retail level, but to aggregate composites (and a national aggregate for a whole fryer) which are statistical constructs.

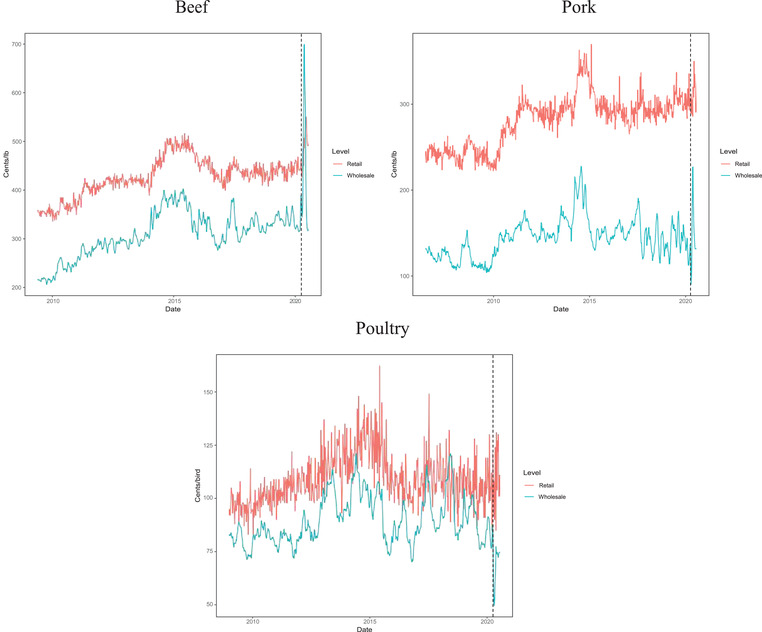

Summary statistics for the price series are shown in Table 1 with plots of the weekly prices shown in Figure 1. Note that, although each series has a different number of observations as determined by data availability, each series ends on July 4, 2020. To reiterate, we consider the COVID‐19 period to be all dates after and including April 1, 2020. As expected, retail prices are on average higher than wholesale prices indicating the presence of a consistently positive marketing margin. The wholesale to retail margin, as measured using the mean prices in the series, is 28% of mean retail price for beef, 49% for pork, and 18% for chicken in the pre‐COVID period. Wholesale prices are more variable than retail prices relative to their mean price levels.

TABLE 1.

Summary statistics for meat price series estimation

| Period | Event Period | |||||||

|---|---|---|---|---|---|---|---|---|

| Series | Mean | St. Dev. | Min. | Max. | Mean | St. Dev. | Min. | Max. |

| Beef (N = 565) | ||||||||

| Retail price | 427 | 38.7 | 336 | 516 | 492 | 39.9 | 427 | 550 |

| Wholesale price | 309 | 45.6 | 208 | 402 | 454 | 136 | 316 | 698 |

| Pork (N = 718) | ||||||||

| Retail price | 281 | 29.4 | 222 | 369 | 311 | 18.8 | 285 | 350 |

| Wholesale price | 144 | 22.1 | 104 | 228 | 150 | 42.4 | 91.2 | 227 |

Note: Beef and pork prices are quoted in cents per pound. Chicken price is quoted in cents per whole fryer.

This article is being made freely available through PubMed Central as part of the COVID-19 public health emergency response. It can be used for unrestricted research re-use and analysis in any form or by any means with acknowledgement of the original source, for the duration of the public health emergency.

FIGURE 1.

Weekly meat prices [Color figure can be viewed at wileyonlinelibrary.com]

Mean prices during the pandemic are higher across all series except in wholesale chicken. Likewise, standard deviations are larger in all series except retail pork and wholesale chicken. As the maximum prices in the beef series are observed during COVID‐19, this may indicate a comparatively larger shock to beef markets. In contrast to beef, chicken prices have been historically low at the wholesale level. The summary statistics indicate general shocks to all meat prices from COVID‐19, but with differential impacts across and within markets.

Figure 1 shows several general trends in the prices over time. Prices for all meats, and at all levels of the supply chain, increased from 2010 to 2015. A large spike in prices occurred from late 2014 to early 2015. After this increase, prices moved sideways. There were strong, but short‐lived, spikes in wholesale prices in the COVID‐19 period that do not appear to have been passed through fully to retail prices. Surprisingly, the wholesale‐retail price spread for beef inverted for most of the month of May, 2020. The plots provide suggestive evidence of stable price relationships and market integration prior to COVID‐19 with sizeable shocks occurring in beef and pork as a result of the pandemic.

Although we do not observe wholesale prices that are spatially differentiated, the datasets used to construct the retail price series contain regional prices for different meat items of different qualities. While we do not statistically model price behavior for individual items or regions, the data permit an exploratory analysis of differences in price behavior across regions. Beef items are reported as branded, choice, or other, while there are no quality differences for the pork items or bagged fryers. As one moves to lower levels of aggregation, the price series tend to be more volatile and many of the beef items do not have a reported price for certain regions and qualities.

Figures A1 and A2 of the Appendix show weekly beef prices by region and item and weekly pork and chicken prices by region and item respectively over 2020. Certain items lack data for some dates and regions (for instance, choice boneless sirloin steak). It is important to note that these item‐specific regional prices are not panel data. Nonetheless, the plots show that prices generally move together at the item level and show a similar pattern of movement to the beef and pork composites. Although there are differences in prices across regions, there is little discernible visual evidence that COVID‐19 had differential impacts across regions.

There are some differences in price movements across cuts that could be related to changes in demand due to the pandemic. In pork, boneless ham prices have remained flat while prices for assorted chops and sliced bacon increased over the period. In beef, ground beef prices returned to levels observed in January, but prices for choice chuck/shoulder/arm roasts remain elevated. Such price movements could result from decreased demand for premium cuts in food service but increased demand for cuts typically used in home consumption. A useful extension of this research would be a more detailed assessment of item‐level price movements, which might be conducted using scanner data to circumvent the limitations of AMS Weekly Retail Activity reports.

5. EMPIRICAL ANALYSIS

Using the data series for beef, pork, and chicken in the estimation window, we first test for stationarity of the individual level price series and of first‐differenced prices. All econometric tests and estimation are conducted using log prices. As evident from Table A1 of the Appendix, the individual price series are nonstationary in all cases. There is some disagreement between the ADF and NP tests in wholesale pork. Although not reported here, the first‐difference prices are all stationary, indicating that the individual price series are integrated of order 1. We also report tests of the contemporaneous log‐price differential between different levels of the market. These differentials are also stationary; stationarity should be expected, otherwise the prices at different levels of the supply chain would be free to wander arbitrarily far apart. In this sense, stationarity of the price differentials suggests at least some degree of vertical integration in all three markets and a constant relative marketing margin.

Table 2 shows the results of the pairwise cointegration regression in each market and the Johansen trace cointegration test. In each case, the logarithmic wholesale price is regressed on the logarithmic retail price. All of the ADF tests of the residuals are significant at the 5% level. The Johansen tests indicate a single cointegrating vector. The results indicate cointegration in all markets implying that VEC models are appropriate for modeling these price series. All three markets have relatively strong relationships between wholesale and retail prices with high R‐squared values. The price transmission elasticity for beef in Table 2 is greater than 1. This is indicative of overshooting in adjustments to price shocks at the wholesale level. In contrast, the price transmission elasticity in the pork market is near unity while that of the chicken market is inelastic.

TABLE 2.

Pairwise Cointegration Regression, ADF Test, and Johansen Test

| Intercept | Slope | R Squared | ADF Test | Johansen | |||||

|---|---|---|---|---|---|---|---|---|---|

| Market | Estimate | Std Error | Estimate | Std Error | Stat | p Value | r = 0 | r < = 1 | |

| Beef | |||||||||

| Wholesale—Retail | −3.40 | .18 | 1.51 | .03 | .82 | .99 | .01 | 79.38 | 5.88 |

| Pork | |||||||||

| Wholesale—Retail | −.71 | .21 | 1.01 | .04 | .51 | .68 | .02 | 66.06 | 6.05 |

| Chicken | |||||||||

| Wholesale—Retail | 1.62 | .19 | .61 | .04 | .28 | .70 | .01 | 69.45 | 12.98 |

This article is being made freely available through PubMed Central as part of the COVID-19 public health emergency response. It can be used for unrestricted research re-use and analysis in any form or by any means with acknowledgement of the original source, for the duration of the public health emergency.

A key insight in Gardner (1975) is that the elasticity of price transmission depends on changes in demand and supply at different levels of the market. The sign and magnitude of the price transmission elasticity can be related to different underlying economic forces. These ideas are further developed in an insightful article by Kinnucan and Zhang (2015). Although Gardner (1975) and Kinnucan and Zhang (2015) work in the space of the farm‐retail price spread, many of their arguments are applicable to the wholesale‐retail price spread, particularly in pork and chicken where contracting causes the farm price to be less meaningful. Two major points raised are that (1) perfect price transmission does not generally imply that the elasticity of price transmission is one and (2) an elasticity of price transmission near zero is not sufficient to imply noncompetitive pricing. Gardner (1975) found that no simple markup pricing rule can accurately depict the relationship between the farm and retail price. Weldegebriel (2004) concludes “it is not generally possible to attribute low (or high) values of the price transmission coefficient to market power”.

Recent research has noted that price transmission along different levels of the production and marketing chain may be influenced by the degree of competition that exists in markets, although the nature of these influences remains unclear. Increasing market power in meat markets has drawn considerable attention in recent years, both from researchers and from legislators. Concentration concerns may exist at the processing level or at the retail level and both aspects of market power have been noted in an extensive literature. A consistent result that emerges from this large body of research is that market power, returns to scale, and the degree of input substitution, concepts which are often intertwined, can influence vertical price transmission (see, for example, Weldegebriel (2004), Lloyd et al. (2009), and McCorriston et al. (2001)).

Kinnucan and Zhang (2015) further note that the often‐assumed transmission elasticity of 1.0 between absolute (in levels) farm and retail prices requires perfect competition as well as other rigid assumptions, including a lack of technical change and constant costs of marketing inputs. They also note that these implications for the absolute farm‐retail price margin do not carry over to proportional price comparisons, as is the case in our analysis. Thus, we do not attempt to interpret our empirical estimates as reflecting competition (or the lack thereof) or industry structure but rather use them to predict prices in the COVID‐19 period. These predictions, when compared with price movements during the pandemic, speak to the adjustment of the meat industry to shocks and resilience to economic disequilibria regardless of the underlying market structure. Our empirical approach can be viewed as a reduced form that utilizes lagged prices and price changes over time to characterize the relationships among wholesale and retail prices.

Bearing in mind that the elasticity estimated here is that of the wholesale price with respect to the retail price (i.e., for a price transmitted down the supply chain), the elasticities share some similarities with those estimated in previous literature. Regressing the logarithmic retail price on both logarithmic wholesale and farm prices, Goodwin and Holt (1999) found beef price transmission elasticities to be inelastic, while Goodwin and Harper (2000) found pork elasticities near unity. These are largely consistent with our results. Similarly, Fousekis et al. (2016) find inelastic price transmission from wholesale to retail in U.S. beef. Employing several structural break tests for different regimes in U.S. beef and pork, Boetel and Liu (2010) also find inelastic price transmission elasticities for beef when regressing retail on wholesale and farm prices. The elasticities for pork are slightly larger and closer to unity. The long run elasticity for broilers is quite different from previous findings by Bernard and Willett (1996) who found wholesale to retail price transmission to be inelastic.

Having confirmed cointegration in all markets, we then test for nonlinear behavior in the error correction term. Tests of the residuals from the cointegrating regressions are in Table A2 of the Appendix. Linearity cannot be rejected at any conventional level of significance for beef and pork. The evidence in chicken is mixed with three of four tests failing to reject symmetry and a fourth rejecting symmetry at the 1% level. Nonlinearity conditions have implications for the models considered below, namely differences in transmission and adjustment across the different regimes indicated by thresholds. Based on results in Table A2, and in the interest of parsimony unless indicated otherwise, we use linear models for the beef and pork markets and a nonlinear model in the chicken market.2

For the threshold model in the chicken market, it is necessary to test for the number of thresholds. This is a particularly difficult problem in the VEC framework if one wishes to consider more than two or three regimes (Hansen & Seo, 2002). Table A3 of the Appendix gives the results of specification tests for the number of thresholds in the SETAR model of the cointegration equation residuals. The tests are—respectively—tests of the null of no threshold vs. one threshold, no threshold vs. two thresholds, and one threshold vs. two thresholds. The results of the tests weakly favor a single threshold in chicken.

We selected the lag order of each model by comparing the Bayesian information criterion for up to four lags. The final specifications are AR(2) and VEC(2) for beef, AR(2) and VEC(2) for pork, and SETAR(2) and TVEC(1) for chicken. The qualitative results did not appear to be sensitive to the choice of lag order. Market integration is supported when shocks to the price differential are temporary and eventually return to zero and shocks to individual prices cause equilibrating responses at other levels of the supply chain. Evidence for the degree of market integration is contained in the estimated time series models.

Estimated parameters of the AR and SETAR models are given in Table 3. The autoregressive parameters are of interest; the larger is the estimated AR parameter, the slower will be the adjustment to shocks in the price differential equilibrium. The AR(1) terms are larger in pork compared to both beef and chicken. All AR parameters are statistically significant indicating statistically significant temporal relationships among the prices. Likewise, the coefficients are all statistically different from 1, which would represent a total lack of adjustment to deviations from the long run relationship. In the SETAR model for chicken, the regimes are distinguished by the speed of adjustment over the two periods. In the low regime, the AR(1) term is smaller compared to the high regime while the AR(2) term is larger. We observe relatively quicker adjustment in the low regime.

TABLE 3.

AR and SETAR Estimates

| Intercept | AR(1) | AR(2) | |||||

|---|---|---|---|---|---|---|---|

| Series | Estimate | Std Error | Estimate | Std Error | Estimate | Std Error | |

| Beef | |||||||

| Wholesale—Retail | .0002 | .0077 | .5781 | .0414 | .1719 | .0416 | |

| Pork | |||||||

| Wholesale—Retail | −.0011 | .0165 | .7896 | .0371 | .0965 | .0372 | |

| Chicken | |||||||

| Wholesale—Retail | Low regime | −.0042 | .0030 | .4618 | .0496 | .3397 | .0438 |

| High regime | .01423 | .01872 | .6341 | .1346 | .1730 | .0919 | |

Note: Chicken threshold is .1075.

This article is being made freely available through PubMed Central as part of the COVID-19 public health emergency response. It can be used for unrestricted research re-use and analysis in any form or by any means with acknowledgement of the original source, for the duration of the public health emergency.

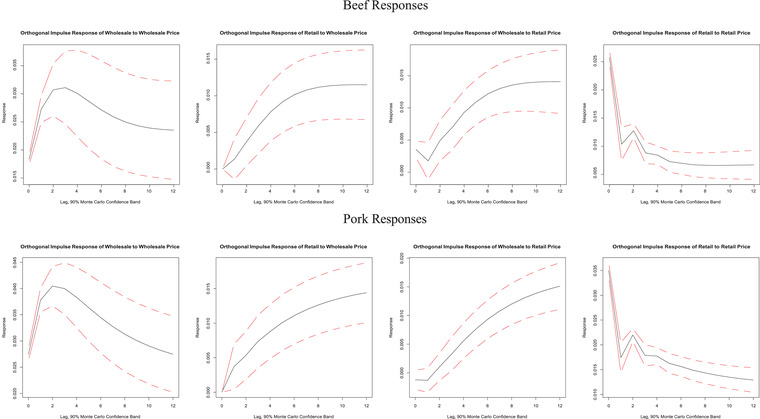

The VECM and TVECM estimates are shown in Table A4 of the Appendix and indicate significant dynamic relationships among the price series. The coefficients on the error correction terms are generally much larger at the retail level than at wholesale. Orthogonalized impulse response functions for the beef, pork, and chicken models are shown, respectively, in Figures 2 and 3. The impulse responses for beef and pork are quite similar. Shocks to wholesale prices tend to take longer to die out. Likewise, the beef market reacts more quickly compared to the pork market. Although the shocks bring about permanent changes in price levels, certainly possible with nonstationary prices, shocks to beef and pork mostly die out within a period of 8–12 weeks. In contrast to earlier work by Goodwin and Holt (1999), shocks at the retail level trigger price adjustments at wholesale, and vice versa.

FIGURE 2.

Beef and pork VECM orthogonalized impulse response functions [Color figure can be viewed at wileyonlinelibrary.com]

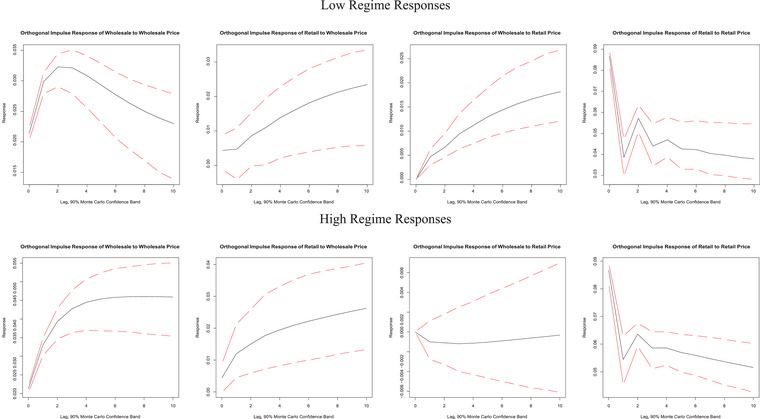

FIGURE 3.

Chicken TVECM orthogonalized impulse response functions [Color figure can be viewed at wileyonlinelibrary.com]

The TVECM for chicken shown in Figure 3 shows impulse responses where the threshold model admits nonlinear adjustment. Major differences in the two regimes are evident. In both regimes, shocks to the wholesale price trigger movements in both wholesale and retail prices. Shocks to wholesale prices, however, do not generally pass‐through to retail prices. While they respond to some degree in the low regime, there is no response in the high regime. Responses to shocks are mostly faster than responses in pork and beef, possibly reflecting the time required to bring a fryer to market as compared to cattle and hogs. Responses to retail shocks conclude around 2–5 weeks. The regimes delineate very different response times to wholesale shocks. Adjustment in the high regime takes anywhere from 2–5 weeks, while adjustment in the low regime is much slower and estimated with a high degree of uncertainty.

We also considered generalized impulse response functions (GIRF) for the TVECM model of chicken wholesale and retail markets. The GIRFs are illustrated in Figure A3 of the Appendix. The GIRFs were determined using 100 replications over 250 different histories and 500 different shocks drawn from the residuals. We considered ‘economy‐wide’ shocks, meaning that both markets were shocked using contemporaneous draws from the residuals. The impulses indicate that both retail and wholesale markets take several weeks to fully respond to economy‐wide shocks, with the wholesale market responding slightly faster than is the case for retail markets. Densities of the replicated GIRFs (Figure A3) do not show convergence as the periods after the shocks are increased. The distributions of shocks for 1, 5, and 10 weeks show a similar degree of volatility, suggesting that the prices do not tend to settle to similar long‐run equilibria for the different histories and shocks.

The parameter estimates from both models and the impulse responses indicate wholesale‐retail markets that are well‐integrated. Shocks to both retail and wholesale prices elicit price responses at other levels of the supply chain. Although the speed of adjustment depends on where in the price system an impulse occurs, almost all adjustments are completed within a period of 3 months. Assuming that COVID‐19 does not induce changes in the degree of market integration, we might expect COVID‐19 related shocks to generate large responses in both retail and wholesale prices regardless of the originating level of the market.

In addition to the bivariate models, we also estimated a joint system containing wholesale and retail prices for each of the three meat products. This allows for the spillover of shocks across different commodity markets. We also used the joint system of six prices to forecast post‐COVID prices using pre‐COVID data. Following the approach used with the three commodity‐specific systems of wholesale and retail prices, we utilized a vector error correction model with two lags. Johansen tests of cointegration revealed multiple (3 to 5) cointegrating relationships among the six prices. In light of the relatively weak support for nonlinearities in the bivariate chicken model, and likewise a failure to reject linearity using residuals from a regression of wholesale chicken prices on all the other prices, we utilize a standard linear VEC model.

Orthogonalized impulse responses were generated to evaluate the dynamic paths of price adjustments. These are presented in the Appendix in Figures A5, A6, A7, A8, A9, and A10 and we discuss the results here. Shocks in the chicken wholesale market evoke responses in wholesale markets for beef and pork, thus indicating a degree of spillover across commodities. Retail markets for beef and pork do not respond to wholesale chicken price shocks. An exogenous shock to retail chicken prices evokes a modest effect on retail beef prices and a negative but small effect on beef wholesale prices.

Exogenous shocks to beef wholesale prices evoke responses in chicken and beef retail markets, but do not affect wholesale prices for chicken and pork. A shock to retail beef prices evokes a permanent increase in chicken and beef retail prices but does not affect any of the wholesale prices. A shock to wholesale pork prices does not affect any of the other markets. A shock to pork retail prices causes a small but permanent increase in chicken retail prices and a larger increase in pork retail prices. The results are generally similar to those revealed for the individual commodity markets, though a modest degree of spillover of shocks exists in some cases.

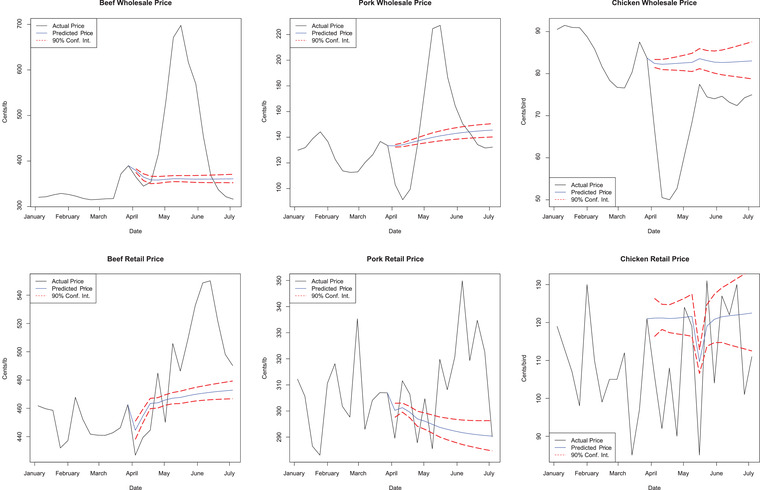

Based on the estimated VEC and TVEC models, we next conduct an event study of the impact of COVID‐19. After obtaining the parameter estimates for the models, we forecast changes to the price series from April 1, 2020. The results of the event study are shown in Figure 4. Clearly, prices observed during COVID‐19 are far outside of their forecasted levels. Most large movements in beef and pork occurred in May, and to some extent June, while movements in chicken are mostly confined to April. Price increases in the COVID‐19 period appear to occur in the wholesale market prior to changes in the retail market. Similar results are obtained for the multivariate VEC model shown in Figure A4 of the Appendix, although the forecast for chicken increases slightly instead of remaining flat as in the bivariate models.

FIGURE 4.

Expected price movements and actual price movements under COVID‐19 from bivariate models [Color figure can be viewed at wileyonlinelibrary.com]

The beef market, particularly at the wholesale level, had the largest increase in prices over the period. In May, the normal price relationship inverted and the wholesale price exceeded retail for 5 weeks. The largest difference occurred in the week ending May 15, 2020 when the wholesale beef price was 93% larger than its expectation. There is a decrease in prices in early April, possibly from decreased demand due to declining consumption through restaurants and other outlets. A second major shock occurs in the middle of April when widespread plant closures occurred.

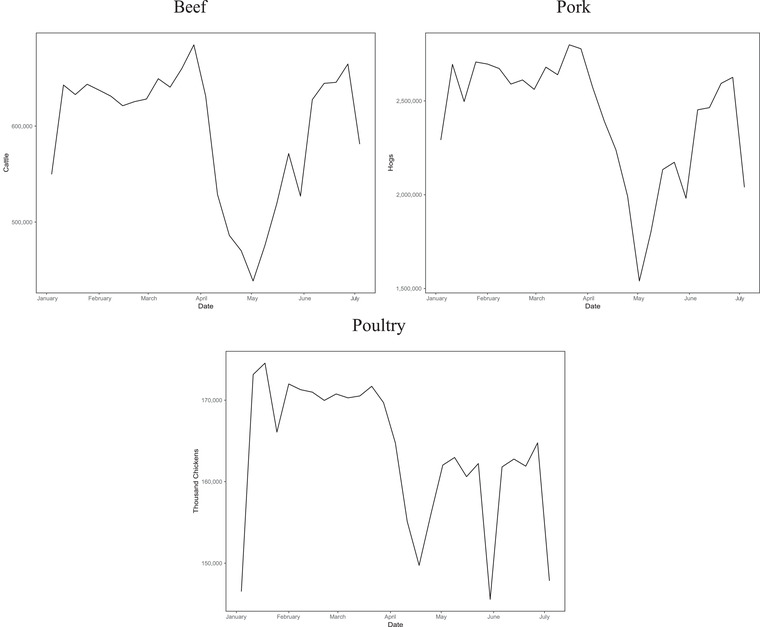

The major increases in values in beef and pork coincide with sharply decreased meat production reported by USDA and ERS. Weekly slaughter values of beef, pork, and poultry are shown in Figure 5. Federally inspected cattle and hog slaughter was up in March 2020, compared to earlier in the year. April saw a decline in slaughter of about 24% in beef and 21% in hogs. By June, beef slaughter had recovered to levels earlier in the year. Pork slaughter continued to decline into May, but increased in June. The coincidence of decreased slaughter with abnormal price movements indicates that the second, April shock from COVID‐19 was largely a supply‐side shock. However, we cannot rule out the possibility that it may also have partially arisen from increased purchasing of meat from consumers in response to news of possible shortages.

FIGURE 5.

Weekly livestock slaughter

Chicken appears to be an exception to the trend of increasing prices observed in the beef and pork markets. Wholesale prices for chicken fell throughout April and May at the same time that chicken slaughter was down. Retail prices also fell in April and May, enough to trigger a shift in regime in the TVEC model, but were close to forecasted levels by June. Moreover, the price movements observed in chicken throughout the period are well within previous trading ranges.

To put the price changes into perspective, at their highest levels, beef and pork retail prices exceeded the predicted values by $3.36 per pound and $3.23 per pound, respectively. Figure 4 illustrates these extreme price movements. In contrast, retail chicken prices fell, but by a much more modest amount that at its greatest was $0.31 per pound. Using weekly meat production statistics from the AMS, this suggests an increase of $6.8 billion in beef expenditures and $5.6 billion in pork expenditures and a decrease of $11.4 million in chicken expenditures over the post‐COVID outbreak period evaluated here (April 4–July 4, 2020) in the U.S.3 Thus, consumer outlays for these meat commodities increased significantly after the COVID outbreak, but returned to normal levels by late August.

Prices have largely returned to, or are returning to, expected levels. All wholesale prices are below forecasts as of July, with chicken lower throughout the event period. Moreover, the speed with which the supply shocks were transmitted through the markets is consistent with the speed of price transmission observed in the estimated models. In beef and pork, the early COVID‐19 shocks lasted roughly 1 to 2 months while the estimated models show shocks dying out within 2 to 3 months. This suggests that immediate shocks of COVID‐19—likely arising through supply channels—are transitory. The U.S. meat system appears to be resilient given the quick recovery of prices in the face of an unprecedented pandemic. Resilience in the face of supply disruptions is a key part of the overall resilience of the food system as defined by Orden (2020). Our findings contrast with other studies that have suggested that the COVID‐19 pandemic has exposed weaknesses throughout the U.S. food supply chain (Chenarides et al., 2021).

6. CONCLUSION

We assess the impact of COVID‐19 and model price transmission in U.S. beef, pork, and poultry markets. Our analysis is based on weekly price data at wholesale and retail levels. The frequency of the data permits an event study of the impact of COVID‐19 that compares realized prices to prices predicted by the time series models. We use linear and threshold autoregressions (AR) and vector error correction (VEC) models to characterize the behavior of prices. These models allow for nonlinear price adjustments if warranted.

Meat prices at all levels of the supply chain are nonstationary in levels but are cointegrated within each market. The beef and pork series are modeled with AR and VEC models, while the chicken market is described with SETAR and TVEC models. Model parameters indicate well‐integrated beef, pork, and poultry markets across the retail and wholesale levels. We find abnormally large price movements as a result of COVID‐19. However, the timing and direction of these movements differs by market. The largest discrepancies occur in May and June for beef and pork and April and May for chicken. In general, wholesale prices appear to have reacted more quickly to COVID shocks. Prices returned to forecasted levels by June and July indicating that the supply shocks to meat markets from COVID‐19 are largely transitory.

As time passes and more data on prices during and after the COVID‐19 pandemic become available, attention may be turned to testing for structural change in the time series. Likewise, the nonlinear models in this analysis could be extended in several directions. These include smooth transition models of the type discussed in Tera¨svirta (1994). The Bayesian paradigm may also offer some conceptual advantages. Bayesian error correction and threshold models are developed and applied in Balcombe (2006), Greb et al. (2013), and Balcombe and Rapsomanikis (2008). It may be possible to incorporate measures of COVID‐ 19 prevalence into the econometric models instead of using event dates specified by the analyst. All of these extensions could involve modeling the entire time series inclusive of the COVID‐19 period. Measurements of supply and demand could be incorporated in structural models to provide explanations for some of the questions raised in this analysis. For instance, why were chicken prices mostly immune to labor related price increases when chicken processing plants were affected by COVID‐19?

The results of this study suggest a resilient U.S. livestock sector. The COVID‐19 pandemic has had significant effects on many aspects of the American economy. Baker, Bloom, et al. (2020) show that no infectious disease outbreak of the 20th and 21st centuries had as large an impact on the U.S. stock market as COVID‐19. Making some simple assumptions about the nature of the infection, Alfaro et al. (2020) report that a doubling of predicted infections is associated with a market value decline in equities of between four and eleven percent. In spite of the unprecedented magnitude of COVID‐19 shocks, price adjustments by livestock retailers and wholesalers have prevented widespread meat shortages and high prices at retail do not appear to be sustained.

The question for policymakers is whether intervention is necessary in light of observed COVID‐ 19 impacts. As noted by Orden (2020), there is potential for detrimental changes in policy based on the fragility inherent in a highly integrated global economy. Laborde et al. (2020) suggest that food security might be preserved worldwide if governments act alongside market participants to provide institutional frameworks for markets to work. Policies should facilitate the market process and avoid disrupting the functioning of markets. There are many innovations being adopted, and largely driven by market participants, that can improve supply‐chain resilience even further (Reardon, Swinnen, et al., 2020). This study paints a picture of a U.S. meat processing and retailing industry that is both efficient and resilient in times of crisis. We therefore conclude that any actions taken with respect to U.S. meat markets should be carefully considered.

Supporting information

Figure A1: Weekly Beef Retail Prices by Region and Item

Figure A2: Weekly Pork and Chicken Retail Prices by Region and Item

Figure A3: Chicken TVECM Generalized Impulse Response Functions and Densities

Figure A4: Expected Price Movements and Actual Price Movements Under COVID‐19 from Multivariate Model

Table A1: Augmented Dickey‐Fuller and Ng‐Perron Unit Root Tests of Weekly Prices and Differential

Table A2: Linearity Tests of Price Differences

Table A3: SETAR Specification Tests

Table A4: VECM and TVECM Estimates

ACKNOWLEDGMENTS

This research was supported by USDA‐NIFA Project: COVID‐19 Rapid Response: Coronavirus Disease 2019, Price Transmission, and the Farm‐Retail Price Spread in U.S. Livestock. The views expressed here are those of the authors and cannot be attributed to the Economic Research Service or the U.S. Department of Agriculture.

Ramsey AF, Goodwin BK, Hahn WF, Holt MT. Impacts of COVID‐19 and Price Transmission in U.S. Meat Markets. Agricultural Economics. 2021;52:441–458. 10.1111/agec.12628

Footnotes

For example, the increasing relevance of captive supplies—cattle owned or contracted by a processor significantly in advance of processing—has been alluded to as an institutional factor that may inhibit price transmission (Chin & Weaver, 2002). Ward et al. (1996) found that captive supplies exhibited a small but negative impact on fed cattle transactions prices.

Note that the threshold‐based linearity tests involve a consideration of the similarity of estimated parameters across the regimes delineated by the thresholds. Applying a threshold model to a linear case will cause a loss of statistical efficiency, but the estimates and predictions remain consistent.

Unpublished data taken from weekly reports of the AMS indicated that 3234 loads of beef and 6284 loads of pork, with each load corresponding to 40,000 lb, were produced during the second week of August 2020. During the same week, 41.8 million lb of broilers and fryers were produced.

REFERENCES

- Abdulai, A. (2000). Spatial price transmission and asymmetry in the Ghanaian maize market. Journal of Development Economics, 63(2), 327–349. 10.1016/S0304-3878(00)00115-2 [DOI] [Google Scholar]

- Abdulai, A. (2002). Using threshold cointegration to estimate asymmetric price transmission in the Swiss pork market. Applied Economics, 34(6), 679–687. 10.1080/00036840110054035 [DOI] [Google Scholar]

- Acharya, R. N. , Kinnucan, H. W. , & Caudill, S. B. (2011). Asymmetric farm–retail price transmission and market power: A new test. Applied Economics, 43(30), 4759–4768. 10.1080/00036846.2010.498355 [DOI] [Google Scholar]

- Ahn, B.‐I. , & Lee, H. (2015). Vertical price transmission of perishable products: The case of fresh fruits in the western united states. Journal of Agricultural and Resource Economics, 40(3), 405–424. [Google Scholar]

- Alfaro, L. , Chari, A. , Greenland, A. N. , & Schott, P. K. (2020). Aggregate and firm‐level stock returns during pandemics, in real time (Working Paper No. 26950). National Bureau of Economic Research. Retrieved from http://www.nber.org/papers/w26950 10.3386/w26950 [DOI] [Google Scholar]

- Almeida, I. , & Dayy, M. (April 12, 2020). Top pork producer shuts key plant and warns of meat shortfall. Bloomberg, Retrieved from https://www.bloomberg.com/news/articles/2020‐04‐12/smithfield‐foods‐idles‐sioux‐falls‐plant‐amid‐virus‐concerns [Google Scholar]

- Azzam, A. M. (1999). Asymmetry and rigidity in farm‐retail price transmission. American Journal of Agricultural Economics, 81(3), 525–533. 10.2307/1244012 [DOI] [Google Scholar]

- Bagenstose, K. , Hauk, G. , & Chadde, S. (April 23, 2020). USDA inspector dies as coronavirus spreads in meat packing plants. USA Today, Retrieved from https://www.usatoday.com/story/news/2020/04/23/usda‐inspector‐dies‐coronavirus‐spreads‐meat‐packing‐plants/3014597001/ [Google Scholar]

- Bailey, D. , & Brorsen, B. W. (1989). Price asymmetry in spatial fed cattle markets. Western Journal of Agricultural Economics, 14(2), 246–252. [Google Scholar]

- Baker, S. R. , Bloom, N. , Davis, S. J. , Kost, K. J. , Sammon, M. C. , & Viratyosin, T. (2020). The unprecedented stock market impact of Covid‐19 (Working Paper No. 26945). National Bureau of Economic Research. 10.3386/w26945 [DOI] [Google Scholar]

- Baker, S. R. , Farrokhnia, R. A. , Meyer, S. , Pagel, M. , & Yannelis, C. (2020). How does household spending respond to an epidemic? Consumption during the 2020 covid‐19 pandemic (Working Paper No. 26949). National Bureau of Economic Research. 10.3386/w26949 [DOI] [Google Scholar]

- Balcombe, K. (2006). Bayesian estimation of cointegrating thresholds in the term structure of interest rates. Empirical Economics, 31(2), 277–289. 10.1007/s00181-005-0011-z [DOI] [Google Scholar]

- Balcombe, K. , & Rapsomanikis, G. (2008). Bayesian estimation and selection of nonlinear vector error correction models: The case of the sugar‐ethanol‐oil nexus in Brazil. American Journal of Agricultural Economics, 90(3), 658–668. 10.1111/j.1467-8276.2008.01136.x [DOI] [Google Scholar]

- Balke, N. S. , & Fomby, T. B. (1997). Threshold cointegration. International Economic Review, 38(3), 627–645. [Google Scholar]

- Ben‐Kaabia, M. , & Gil, J. M. (2007). Asymmetric price transmission in the Spanish lamb sector. European Review of Agricultural Economics, 34(1), 53–80. 10.1093/erae/jbm009 [DOI] [Google Scholar]

- Bernard, J. C. , & Willett, L. S. (1996). Asymmetric price relationships in the US broiler industry. Journal of Agricultural and Applied Economics, 28(2), 279–289. [Google Scholar]

- Boetel, B. L. , & Liu, D. J. (2010). Estimating structural changes in the vertical price relationships in us beef and pork markets. Journal of Agricultural and Resource Economics, 35(2), 228–244. [Google Scholar]

- Boyd, M. S. , & Brorsen, B. W. (1988). Price asymmetry in the US pork marketing channel. Applied Economic Perspectives and Policy, 10(1), 103–109. 10.1093/aepp/10.1.103 [DOI] [Google Scholar]

- Bunge, J. (April 12, 2020a). Smithfield CEO Warns of Risks to Pork Supply. Wall Street Journal. [Google Scholar]

- Bunge, J. (April 15, 2020b). Smithfield to close more pork plants over coronavirus pandemic. Wall Street Journal, Retrieved from https://www.wsj.com/articles/smithfield‐to‐close‐more‐pork‐plants‐deepening‐coronavirus‐farm‐crisis‐11586990622 [Google Scholar]

- Campbell, J. Y. , Lo, A. W. , & MacKinlay, A. C. (1997). The econometrics of financial markets. Princeton, NJ: Princeton University Press. [Google Scholar]

- Cavallo, A. (2020). Inflation with Covid consumption baskets . (Working Paper No. 27352) National Bureau of Economic Research. 10.3386/w27352 [DOI]

- Chan, K. S. (1991). Percentage points of likelihood ratio tests for threshold autoregression. Journal of the Royal Statistical Society: Series B (Methodological), 53(3), 691–696. 10.1111/j.2517-6161.1991.tb01858.x [DOI] [Google Scholar]

- Chang, H.‐H. , & Meyerhoefer, C. D. (2021). Covid‐19 and the demand for online food shopping services: Empirical evidence from Taiwan. American Journal of Agricultural Economics, 103(2), 448–465. 10.1111/ajae.12170 [DOI] [Google Scholar]

- Chen, B. , & Saghaian, S. (2016). Market integration and price transmission in the world rice export markets. Journal of Agricultural and Resource Economics, 41(3), 444–457. [Google Scholar]

- Chenarides, L. , Manfredo, M. , & Richards, T. J. (2021). Covid‐19 and food supply chains. Applied Economic Perspectives and Policy. 43(1), 270–279. 10.1002/aepp.13085 [DOI] [Google Scholar]

- Chin, M.‐C. , & Weaver, R. D. (2002). Contracting, captive supplies, and price behavior (Tech.Rep.).

- Comer. (2020). Congressman comer applauds USDA plan to expand beef price fixing in vestigation to COVID‐19 impacts on cattle prices . https://comer.house.gov/media/press‐releases/congressman‐comer‐applauds‐usda‐plan‐expand‐beef‐price‐fixing‐investigation.

- Cramon‐Taubadel, S. V. (1998). Estimating asymmetric price transmission with the error correction representation: An application to the german pork market. European Review of Agricultural Economics, 25(1), 1–18. 10.1093/erae/25.1.1 [DOI] [Google Scholar]

- Cranfield, J. A. (2020). Framing consumer food demand responses in a viral pandemic. Canadian Journal of Agricultural Economics/Revue canadienne d'agroeconomie. 68(2), 151–156. 10.1111/cjag.12246 [DOI] [Google Scholar]

- Dickey, D. A. , & Fuller, W. A. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association, 74(366), 427–431. 10.1080/01621459.1979.10482531 [DOI] [Google Scholar]

- Engle, R. F. , & Granger, C. (1987). Cointegration and error correction: Representation, estimation, and testing. Econometrica, 55(2), 143–159. [Google Scholar]

- Fackler, P. L. , & Goodwin, B. K. (2001). Spatial price analysis. Marketing, Distribution, and Consumers, Handbook of Agricultural Economics, 1, 971–1024.Elsevier. [Google Scholar]

- Fousekis, P. , Katrakilidis, C. , & Trachanas, E. (2016). Vertical price transmission in the US beef sector: Evidence from the nonlinear ARDL model. Economic Modelling, 52, 499–506. 10.1016/j.econmod.2015.09.030 [DOI] [Google Scholar]

- Franken, J. R. , Parcell, J. L. , & Tonsor, G. T. (2011). Impact of mandatory price reporting on hog market integration. Journal of Agricultural and Applied Economics, 43(2), 229–241. [Google Scholar]

- Gardner, B. L. (1975). The farm‐retail price spread in a competitive food industry. American Journal of Agricultural Economics, 57(3), 399–409. 10.2307/1238402 [DOI] [Google Scholar]

- Gay, S. , Adena¨uer, M. , & Frezal, C. (2020). Potential macroeconomic impact of the covid‐19 pandemic on food demand. Eurochoices. 19(3), 40–41. 10.1111/1746-692X.12271 [DOI] [Google Scholar]

- Goddard, E. (2020). The impact of covid‐19 on food retail and food service in Canada: Preliminary assessment. Canadian Journal of Agricultural Economics/Revue canadienne d'agroeconomie. 68(2), 157–161. 10.1111/cjag.12243 [DOI] [Google Scholar]

- Goodwin, B. K. , & Harper, D. C. (2000). Price transmission, threshold behavior, and asymmetric adjustment in the US pork sector. Journal of Agricultural and Applied Economics, 32(3), 543–553. 10.1017/S1074070800020630 [DOI] [Google Scholar]

- Goodwin, B. K. , & Holt, M. T. (1999). Price transmission and asymmetric adjustment in the US beef sector. American Journal of Agricultural Economics, 81(3), 630–637. 10.2307/1244026 [DOI] [Google Scholar]

- Grassley, C. (2020). Meat packers market manipulation . https://www.grassley.senate.gov/news/news‐releases/grassley‐seeks‐federal‐investigations‐potential‐market‐manipulation‐and‐other.

- Greb, F. , von Cramon‐Taubadel, S. , Krivobokova, T. , & Munk, A. (2013). The estimation of threshold models in price transmission analysis. American Journal of Agricultural Economics, 95(4), 900–916. 10.1093/ajae/aat006 [DOI] [Google Scholar]

- Griffith, G. R. , & Piggott, N. (1994). Asymmetry in beef, lamb and pork farm‐retail price transmission in Australia. Agricultural Economics, 10(3), 307–316. [Google Scholar]

- Gurkaynak, R. S. , & Wright, J. H. (2013). Identification and inference using event studies. The Manchester School, 81, 48–65. [Google Scholar]

- Hahn, W. , Stewart, H. , Blayney, D. P. , & Davis, C. G. (2016). Modeling price transmission between farm and retail prices: A soft switches approach. Agricultural Economics, 47(2), 193–203. 10.1111/agec.12222 [DOI] [Google Scholar]

- Hansen, B. E. , & Seo, B. (2002). Testing for two‐regime threshold cointegration in vector error‐correction models. Journal of Econometrics, 110(2), 293–318. [Google Scholar]

- Jinjarak, Y. , Ahmed, R. , Nair‐Desai, S. , Xin, W. , & Aizenman, J. (June, 2020). Pandemic shocks and fiscal‐monetary policies in the Eurozone: Covid‐19 dominance during January‐June 2020 (Working Paper No. 27451). National Bureau of Economic Research. 10.3386/w27451 [DOI] [Google Scholar]

- Johansen, S. (1991). Estimation and hypothesis testing of cointegration vectors in Gaussian vector autoregressive models. Econometrica, 59(6), 1551–1580. [Google Scholar]

- Kinnucan, H. W. , & Zhang, D. (2015). Notes on farm‐retail price transmission and marketing margin behavior. Agricultural Economics, 46(6), 729–737. 10.1111/agec.12188 [DOI] [Google Scholar]

- Koop, G. , Pesaran, M. H. , & Potter, S. M. (1996). Impulse response analysis in nonlinear multivariate models. Journal of Econometrics, 74(1), 119–147. 10.1016/0304-4076(95)01753-4 [DOI] [Google Scholar]

- Kuiper, W. E. , & Lansink, A. G. O. (2013). Asymmetric price transmission in food supply chains: Impulse response analysis by local projections applied to us broiler and pork prices. Agribusiness, 29(3), 325–343. 10.1002/agr.21338 [DOI] [Google Scholar]

- Laborde, D. , Martin, W. , Swinnen, J. , & Vos, R. (2020). Covid‐19 risks to global food security. Science, 369(6503), 500–502. 10.1126/science.abc4765 [DOI] [PubMed] [Google Scholar]

- Lee, T.‐H. , White, H. , & Granger, C. W. (1993). Testing for neglected nonlinearity in time series models: A comparison of neural network methods and alternative tests. Journal of Econometrics, 56(3), 269–290. 10.1016/0304-4076(93)90122-L [DOI] [Google Scholar]

- Lence, S. H. , Moschini, G. , & Santeramo, F. G. (2018). Threshold cointegration and spatial price transmission when expectations matter. Agricultural Economics, 49(1), 25–39. 10.1111/agec.12393 [DOI] [Google Scholar]

- Lloyd, T. (2017). Forty years of price transmission research in the food industry: Insights, challenges and prospects. Journal of Agricultural Economics, 68(1), 3–21. [Google Scholar]

- Lloyd, T. , McCorriston, S. , Morgan, W. , Rayner, A. , & Weldegebriel, H. (May, 2009). Buyer power in U.K. food retailing: A ’first‐pass’ test. Journal of Agricultural & Food Industrial Organization, 7(1). 10.2202/1542-0485.1253 [DOI] [Google Scholar]

- Lusk, J. L. , Tonsor, G. T. , & Schulz, L. L. (2021). Beef and pork marketing margins and price spreads during COVID‐19. Applied Economic Perspectives and Policy. 43(1), 4–23. 10.1002/aepp.13101 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Maples, J. G. , Thompson, J. M. , Anderson, J. D. , & Anderson, D. P. (2021). Estimating covid‐19 impacts on the broiler industry. Applied Economic Perspectives and Policy. 43(1), 315–328. 10.1002/aepp.13089 [DOI] [Google Scholar]

- Martinez, C. C. , Maples, J. G. , & Benavidez, J. (2021). Beef cattle markets and covid‐19. Applied Economic Perspectives and Policy. 43(1), 304–314. 10.1002/aepp.13080 [DOI] [Google Scholar]

- McCorriston, S. , Morgan, C. , & Rayner, A. J. (1998). Processing technology, market power and price transmission. Journal of Agricultural Economics, 49(2), 185–201. 10.1111/j.1477-9552.1998.tb01263.x [DOI] [Google Scholar]

- McCorriston, S. , Morgan, W. , & Rayner, J. (Jan). (2001). Price transmission, market power, marketing chain, returns to scale, food industry. European Review of Agricultural Economics, 28(2), 143–159. 10.1093/erae/28.2.143 [DOI] [Google Scholar]

- McEwan, K. , Marchand, L. , Shang, M. , & Bucknell, D. (2020). Potential implications of covid‐19 on the Canadian pork industry. Canadian Journal of Agricultural Economics/Revue canadienne d'agroeconomie. 68(2), 201–206. 10.1111/cjag.12236 [DOI] [Google Scholar]

- Meyer, J. , & von Cramon‐Taubadel, S. (2004). Asymmetric price transmission: A survey. Journal of Agricultural Economics, 55(3), 581–611. 10.1111/j.1477-9552.2004.tb00116.x [DOI] [Google Scholar]

- Myers, R. J. , & Jayne, T. (2012). Multiple‐regime spatial price transmission with an application to maize markets in southern africa. American Journal of Agricultural Economics, 94(1), 174–188. 10.1093/ajae/aar123 [DOI] [Google Scholar]

- Ng, S. , & Perron, P. (2001). Lag length selection and the construction of unit root tests with good size and power. Econometrica, 69(6), 1519–1554. 10.1111/1468-0262.00256 [DOI] [Google Scholar]

- Orden, D. (2020). Resilience test of the north American food system. Canadian Journal of Agricultural Economics/Revue canadienne d'agroeconomie. 68(2), 215–217. 10.1111/cjag.12238 [DOI] [Google Scholar]

- Pozo, V. F. , Bachmeier, L. J. , & Schroeder, T. C. (2021). Are there price asymmetries in the US beef market? Journal of Commodity Markets, 21. 100–127. 10.1016/j.jcomm.2020.100127 [DOI] [Google Scholar]

- Reardon, T. , Swinnen, J. , et al. (2020). Covid‐19 and resilience innovations in food supply chains. IFPRI book chapters, 132–136.

- Rounds, M. , Cramer, K. , Daines, S. , & Hoeven, J. (2020). Letter to department of justice regarding cattle prices . https://www.rounds.senate.gov/imo/media/doc/Letter%20to%20Department%20of%20Justice%20Regarding%20Cattle%20Prices.pdf.

- Rude, J. (2020). Covid‐19 and the Canadian cattle/beef sector: Some preliminary analysis. Canadian Journal of Agricultural Economics/Revue canadienne d'agroeconomie. 10.1111/cjag.12228 [DOI] [Google Scholar]

- Said, S. E. , & Dickey, D. A. (1984). Testing for unit roots in autoregressive‐moving average models of unknown order. Biometrika, 71(3), 599–607. [Google Scholar]

- Schwert, G. W. (2002). Tests for unit roots: A Monte Carlo investigation. Journal of Business & Economic Statistics, 20(1), 5–17. 10.1198/073500102753410354 [DOI] [Google Scholar]

- Serra, T. , Gil, J. M. , & Goodwin, B. K. (2006). Local polynomial fitting and spatial price relationships: Price transmission in EU pork markets. European Review of Agricultural Economics, 33(3), 415–436. 10.1093/erae/jbl013 [DOI] [Google Scholar]

- Serra, T. , & Goodwin, B. K. (2003). Price transmission and asymmetric adjustment in the Spanish dairy sector. Applied Economics, 35(18), 1889–1899. 10.1080/00036840310001628774 [DOI] [Google Scholar]