Abstract

We assess the impact of the coronavirus disease 2019 (COVID‐19) pandemic on the labour markets and economies of 16 SADC member states using a qualitative risk assessment on the basis of high‐frequency Google Mobility data, monthly commodity price data, annual national accounts, and households survey labour market data. Our work highlights the ways in which these complementary datasets can be used by economists to conduct near real‐time macroeconomic surveillance work covering labour market responses to macroeconomic shocks, including for seemingly information scarce African economies. We find that Angola, South Africa and Zimbabwe are at greatest risk across several labour market dimensions from the COVID‐19 shock, followed by a second group of countries consisting of Comoros, DRC, Madagascar and Mauritius. Angola faces relatively less general employment risk than South Africa and Zimbabwe due to more muted decreases in mobility, though faces large pressure in its primary sector. These countries all face high risk in their youth populations, with Angola and Zimbabwe seeing high risks for women. South Africa faces more sector‐specific risks in their secondary and tertiary sectors, as does Mauritius. Comoros, DRC and Madagascar all face high risks of employment loss for women and youth, with Comoros and Mauritius facing severe general employment risks.

1. INTRODUCTION

Southern African Development Community (SADC) countries have been hard hit by the economic fallout associated with the coronavirus disease 2019 (COVID‐19) pandemic. The global economic impact of COVID‐19 has been transmitted to SADC economies due to their strong external integration, in particular their reliance on global demand (World Bank, 2020a). Significant local economic contractions are projected with the African Development Bank's (AfDB's) July Southern Africa Economic Outlook (African Development Bank, 2020) estimating the region's baseline growth to be −4.9%, with a worst‐case scenario of −6.6%.

This paper uses innovative 'high‐frequency' data sources and techniques to offer a novel analysis of labour employment vulnerability to COVID‐19‐induced economic changes. This employment vulnerability is given by sector (primary, secondary, tertiary) across all 16 SADC countries (data permitting). In addition, we provide risk assessments for women and youth based on an occupational approach. Women face added vulnerabilities (Anyanwu & Augustine, 2013) given their over‐representation in poverty and precarious employment (United Nations Women, 2018), and under‐representation in training and highly skilled occupations (United Nations Women, 2020). Their position in the household often means that they stay behind in rural areas to work in subsistence, unremunerated labour, with a reliance on volatile remittances, government support or seasonal conditions. Young workers are also often particularly vulnerable in the face of a crisis, as they lack job experience and have low levels of savings, and suffer from the closure of traineeships (International Labour Organization, 2020a). These groups are well documented as being less resilient to labour market shocks, and the disproportionate impacts are already showing to be substantial (Chen, 2020).

A plethora of research on the impact of COVID‐19 has emerged. This includes both studies projecting the impact of COVID‐19 and those assessing economic changes that have already occurred (International Monetary Fund, 2020a; Southern African Development Community, 2020). These includes African countries (African Development Bank, 2020; Boukar et al., 2021; Djoumessi, 2021; Ibukun & Adebayo, 2021; Morsy et al., 2020; Wonyra et al., 2021). They paint a bleak picture of the impact of COVID‐19 on these economies, showing, in Southern Africa, real gross domestic product (GDP) contractions of 6.6%, weakening current account balances of up to −7.4%, weakening fiscal balances, increasing external debt, lower revenue collection volumes, lower investment rates and an additional 40 million or more people projected to be pushed into extreme poverty, amongst an array of other measures.

Despite these important contributions, at the time of writing no study had either assessed the expected region‐wide pandemic‐induced impact on employment, disaggregating this by worker demographics, nor made extensive use of high‐frequency datasets in the region. In both these respects, this paper is a novel contribution.

Generally, existing studies on the employment and socioeconomic impacts of COVID‐19 are focused on individual countries using household surveys, such as Jain et al. (2020) in South Africa, The Gambia Bureau of Statistics (2020) in The Gambia, telephonic Living Standards Measurement Study1 surveys ongoing in Ethiopia, Malawi, Nigeria, Tanzania and Uganda (World Bank, 2020b), and Razani and Cheung Kai Suet (2020) in Mauritius. Labour market impacts of COVID‐19 have been relatively mixed across African economies (Weber et al., 2020), with the extent of trade integration and lockdown measures factoring into these results (International Monetary Fund, 2020b). The Southern African Development Community (2020) highlights the main areas of employment loss will be in trade, tourism, transport, hospitality, and wholesale and retail trade sectors, though no specific figures are given.

Morsy et al. (2020), using a DSGE model, are the only authors, at the time of writing, that model employment impacts. This is done on a continent‐wide basis. They anticipate reductions in employment in Africa of 43.2% in the informal sector, 51.1% in the formal non‐tradable sector, and 32.3% in the formal tradable sector. Our study differs in its geographic scope, disaggregated nature, estimation techniques, and underlying theoretical approaches.

High‐frequency datasets, such as unemployment insurance claims data, mobility data, household surveys, online job‐posting volumes, and night‐time luminosity data, have been widely used to gauge the effects of COVID‐19 on employment and economic activity (Baek et al., 2020; Dalton et al., 2020; Ghosh et al., 2020; Sampi & Jooste, 2020; Scott & Finamor, 2020). Their near‐immediate availability and standardized nature has made them particularly useful due to issues with standard data collection measures (International Labour Organization, 2020b). Naturally, the use of high‐frequency data is not without contention, even when in abundance, as evidenced in Cajner et al. (2020).

To date, this data has rarely been applied in Africa, even though increasing use of cell phones on the continent now means that Google Mobility data is available for many countries. This paper makes use of this high‐frequency data and combines it with new IMF monthly datasets on commodity prices, annual national accounts data, and International Labour Organization (ILO) employment data from various household surveys and questionnaires. Commodity prices and national accounts data are useful due to the heavy external reliance of many—but not all—of SADC economies. Together this helps provide a holistic and largely real‐time qualitative impact assessment of the COVID‐19 shock to SADC's economies. This provides an important basis to inform other macroeconomic and labour market surveillance work for SADC country economists going forward.

This paper takes the theoretical position of SADC countries as experiencing demand‐side crises, with falling employment being a consequence. This differs from the supply‐side shock modelled in Morsy et al. (2020). As with other advanced economies, SADC countries were—at times—forced to reduce supply in the economy through various forms of lockdowns. However, the binding economic constraint on economic activity and employment in these countries has been falling local and international demand for the products produced. This is evidenced by studies mapping local consumption spending and exports (Gondwa, 2020; Wu & Thomasberger, 2020).

The rest of the paper is as follows. Section 2 details the data and methodology employed in generating the employment risk indicators of Table 1. Section 3 provides an overview of the qualitative risk assessment (low, medium, high) of the impact of COVID‐19 on each SADC member's labour markets for 2020, by sector, for women, and for youth. Section 4 discusses policy implications and concludes.

Table 1.

2020 Employment risk and vulnerability analysis for SADC countries from COVID‐19 shock

| General | Primary | Secondary | Tertiary | Women | Youth | |

|---|---|---|---|---|---|---|

| Angola | High | High | Low | Medium | High | High |

| Botswana | High | Low | Low | Medium | Low | ND |

| Comoros | High+ | Low | Medium | ND | High | High |

| DRC | High | Medium | Low | Low | High | High |

| Eswatini | High | Low | ND | High | Low | High |

| Lesotho | High | Low | High | Medium | Low | ND |

| Madagascar | High | Low | Medium | Low | High | High |

| Malawi | Medium | Low | ND | Medium | High | High |

| Mauritius | High+ | Low | High | High | Low | Low |

| Mozambique | Medium | Low | Medium | Low | High | High |

| Namibia | High | Low | Medium | Medium | Low | ND |

| Seychelles | High+ | Low | Medium | High | ND | Low |

| South Africa | High+ | Low | High | High | Low | High |

| Tanzania | Medium | Low | Low | Low | High | High |

| Zambia | Medium | Low | Medium | Low | High | High |

| Zimbabwe | High+ | Low | Medium | Medium | High | High |

Note: Risk level is relative to each country as risk cannot be standardized. Where information is insufficient, risk level is left blank with ‘ND’ indicating no data. Employment risk indications are informed by quantitative and secondary qualitative literature where necessary. Estimates do not account for planned or implemented mitigation strategies.

Abbreviations: COVID‐19, coronavirus disease 2019; SADC, Southern African Development Community.

Sources: Google COVID‐19 Community Mobility Reports for cumulative workplace and residential mobility changes from January baseline volumes and duration, International Monetary Fund (IMF) for real GDP per capita growth forecast for 2020 (Column 1 on general employment risk); data from the IMF used for commodity net export price index terms of trade changes (Column 2 on primary sector employment risk); manufacturing share of employment data from ILOstat (Column 3 on secondary sector employment risk); Google COVID‐19 Community Mobility Reports for cumulative retail and recreation and grocery and pharmacy mobility changes from January baseline volumes, Google Search Trends for changes in online travel search popularity (Column 4 on tertiary sector employment risk); ILOstat used for vulnerable occupation share of employment by gender (Column 5 on women's employment risk); ILOstat used for vulnerable occupation share of employment for youth (Column 6 on youth employment risk).

This article is being made freely available through PubMed Central as part of the COVID-19 public health emergency response. It can be used for unrestricted research re-use and analysis in any form or by any means with acknowledgement of the original source, for the duration of the public health emergency.

2. DATA AND METHODOLOGY

This paper makes use of high‐frequency data sources and select national accounts data. This allows for the extrapolation of employment risk estimates to be made in the absence of traditional household surveys.

Community Mobility Reports data from Google is used to measure changes in total daily visitors to different locations, specifically retail and recreation, supermarket and pharmacy, workplaces, and residential locations. This data is collected by Google from those who have not opted out of providing location history on their electronic devices. For all locations besides residential, the data shows the percentage change in the total number of visitors to those locations, measured against a median ‘baseline’ period of 5 weeks before the crisis—3 January 2020–6 February 2020. The changes in visitor frequency for each day is relative to the corresponding day of the week in the baseline period. Residential data, however, is measured in change in duration of time spent at an individual's place of residence.2

For general risk employment, we use the sum of the total workplace visits (excluding weekends) over the period 15 February 2020–4 August 2020, less the sum of changes in time spent in residential locations. This allows us to gauge the effects of lockdown conditions and the extent to which people are not going to workplaces. The results are summarized in Table 1, with high+ risk being measured as a total greater than −6000, high risk between −6000 and −3000, and medium employment risk less than −3000. For countries where Google data is unavailable, we use a cruder measure of forecasted changes in GDP per capita as a proxy for general employment risk, with high+ risk being changes greater than −8%, high indicating changes between −8 and −3%, and medium risk indicated by changes less than −3%. We do not believe any SADC economy faces low unemployment risk and adjust our risk scale accordingly.

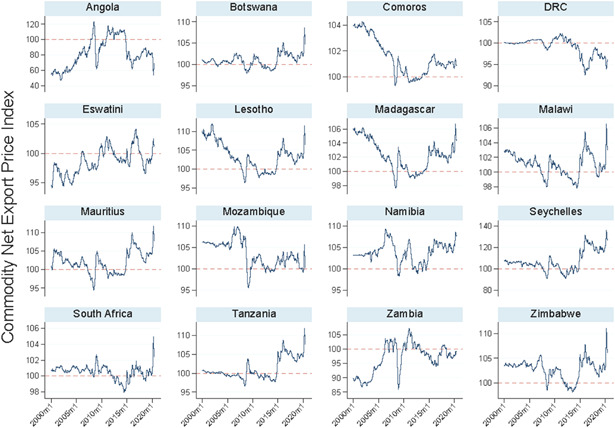

Primary sector risk is assessed by the use of monthly commodity net export price indices from the IMF, whereby prices of the top 45 export commodities, weighted by their ratio of net exports to GDP using rolling weights, is employed. This gives us an indication of the stress imposed on primary sectors via their export prices. Those with moves greater than −10 point changes since January 2020 are considered high risk, medium risk representing changes between −10 and −5 points, and low risk being a move of less than −5 points. We analyse changes from January 2020 to July 2020, but also consider the recent changes relative to trends since 2000 to assess whether a country's terms‐of‐trade trajectory has significantly changed path.

Secondary sector risk is based on the share of manufacturing jobs in total employment, using data from the ILO (latest date available). High risk is assigned to those with shares of manufacturing in total employment of over 10%, medium risk to countries with shares between 10% and 4%, and low risk for those with shares less than 4%.

Tertiary sector risk again uses daily Google Mobility data, with the sum of total retail and recreation location visits (excluding weekends) from 15 February to 4 August 2020 added to the sum of total grocery and pharmacy visits over the same period. Countries with totals greater than −8000 face high risk, totals between −8000 and −4000 denote medium risk, and totals less than −4000 are deemed as low risk. Where Google Mobility data is unavailable, we use data from the ILO to look at the economic sector structure in employment. Those countries with shares of employment in services larger than 50% face high risk, between 50% and 30% are regarded as medium risk, and less than 30% are considered as low risk. Further, we look at weekly Google Search Trend Popularity Indices to indicate travel intentions for countries with large tourism industries.

Employment risk for women is based on pre‐existing occupational data from the ILO. We calculate the share of women and men in at‐risk occupations. At‐risk occupations include clerical support workers, service and sales workers, craft and related trades workers, plant and machine operators and assemblers, and elementary occupations and skilled agricultural, forestry and fishery workers (those occupations that are generally lower paid with fewer protections, and more outward facing). This is taken as a share of all employment, which also includes occupations deemed more resilient to labour market shocks and better able to work from home (managers, professionals, and technicians and associate professionals). Where this share is higher for women than for men, we deem this high risk, and low risk where women's share in at‐risk occupations is lower than that of men.

Employment risk for youth (ages 15–24) is derived in a similar manner. At‐risk occupations include clerical support workers, service and sales workers, skilled agricultural, forestry and fishery workers, craft and related trades workers, plant and machine operators, assemblers, elementary occupations and occupations not elsewhere classified. This is taken as a share of all employment, which also includes occupations deemed more resilient to labour market shocks (managers, professionals, technicians and associate professionals, and armed forces). High risk for youth employment is for those countries where the share is larger than 85%, and low where the share is below 85%.

3. RESULTS

3.1. Overview

Using the coding description given above, Table 1 summarizes the employment risks for SADC countries as a whole, and for the three sectors and two demographic groups. We see that five countries fall into the highest general risk category of high+, seven are considered high, and only four medium, indicating significant employment risk across the region. The primary sector is not considered as the epicentre of the risk, with all but one country categorized as facing a low risk in this sector. Higher risked is faced in the secondary and tertiary sector, with the latter being more at risk overall. Women and youth are more at risk then the population as whole for the majority of SADC countries. These findings are expanded upon below.

3.2. General employment risk

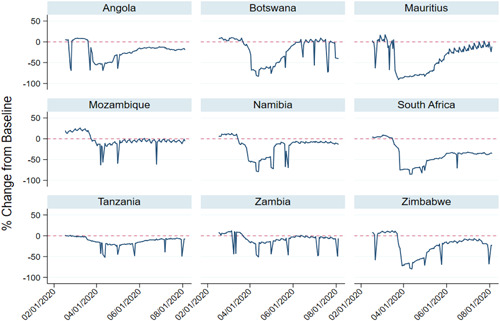

High frequency data from Google's Community Mobility Reports data on workplace and residential trends are analysed since February 2020 to proxy for general loss‐of‐employment risk. This is shown for nine SADC countries in Figures 1 and 2.

Figure 1.

Workplace number of visits relative to January baseline, February–August 2020, excluding Saturday and Sunday. Source: Using Google COVID‐19 Community Mobility Reports, change in total visits

Figure 2.

Change in duration spent at place of residence relative to January baseline, February–August 2020, excluding Saturday and Sunday. Source: Using Google COVID‐19 Community Mobility Reports, change in duration of visit

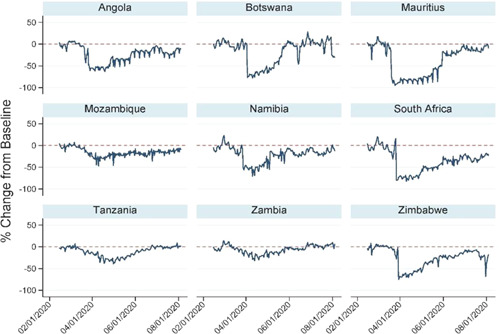

SADC countries with the largest decreases in returning to work are Angola, Botswana, Mauritius, Namibia, South Africa and Zimbabwe, all of whom experience a reduction in workplace visitation of more than 50% compared to their ‘normal’ baseline. Botswana and Namibia have the fastest return to work figures, with Mauritius and Zimbabwe returning to ‘near‐normal’ levels slightly later. Angola and South Africa have not returned to previous averages for workplace visits, with South Africa plateauing near a −35% decline relative to ‘normal’ levels for some months. Mozambique, Tanzania and Zambia have not seen material decreases in workplace visits, which is promising in terms of a less severe general employment risk. This seems in part due to less stringent lockdowns.

Similar risk profiles are captured in Figure 2. Figure 2 shows the change in total time people spend in their homes relative to normal periods (the baseline). This differs from the other mobility trends which measure changes in total visitors (‘volume’). The two trends generally align: those not visiting their workplaces spend more time at home,3 common among the unemployed in countries with a lower ability to undertake remote work. Given that some workers may reasonably be working remotely in countries with more developed information and communication technologies infrastructure, this is only indicative of employment risk.

As with declines in mobility to work, SADC countries with the largest increases in residential durations (reflecting we assume less time spent in the workplace), include Botswana, Mauritius, South Africa and Zimbabwe, all with increases of 40% at some point. Moderate increases of between 20% and 40% include Angola and Namibia, and relatively low increases of between 0% and 20% for Mozambique, Tanzania and Zambia.

Risk profiles for countries are largely consistent across the two metrics used. This is shown in Table 2, which summarizes the changes in mobility over the first two quarters of 2020 and provides an aggregate across the two metrics. South Africa and Mauritius show the largest risk, followed closely by Zimbabwe; and then Botswana, Angola and Namibia (high risk), and finally Zambia, Tanzania and Mozambique (medium risk).

Table 2.

Workplace and residential mobility changes during Q1 and Q2 2020

| Country | Workplace | Residential | General total |

|---|---|---|---|

| Angola | −2840 | 2411 | −5251 |

| Botswana | −2662 | 2730 | −5392 |

| Mauritius | −5520 | 2772 | −8292 |

| Mozambique | −319 | 1229 | −1548 |

| Namibia | −2529 | 1719 | −4248 |

| South Africa | −5426 | 3085 | −8511 |

| Tanzania | −1972 | 815 | −2787 |

| Zambia | −749 | 1482 | −2231 |

| Zimbabwe | −3203 | 3710 | −6913 |

Note: Column General Total (Column 3) subtracts Residential Total (Column 2) from cumulative workplace total (column 1). Measured from 15 February to 4 August 2020.

Source: Using Google COVID‐19 Community Mobility Reports.

This article is being made freely available through PubMed Central as part of the COVID-19 public health emergency response. It can be used for unrestricted research re-use and analysis in any form or by any means with acknowledgement of the original source, for the duration of the public health emergency.

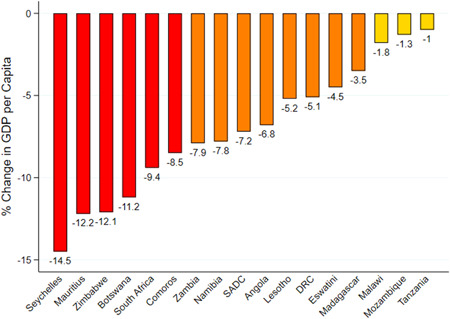

GDP per capita is used instead where no Google Mobility data exists for the SADC country. We anticipate larger general employment risks for those countries with higher forecasted reductions in GDP per capita for 2020. This is informed by Okun's law. As a result, we anticipate severe general employment risks with forecasted GDP per capita contractions in excess of −8% for Seychelles and Comoros, moderate risk with contractions between −8% and −3% for Lesotho and the DRC, and low risk with contractions of less than −3% for Eswatini, Madagascar and Malawi. This is shown in Figure 3.

Figure 3.

GDP per capita change, 2020 forecast. Note: Dark grey shading represents GDP per capita change estimates for 2020 of more than −8% (high+ risk), medium grey representing changes between −8% and −3% (high risk), and light grey represents changes of less than −3% (medium risk). Source: International Monetary Fund, Sub‐Saharan Africa Regional Economic Outlook Update, June 2020

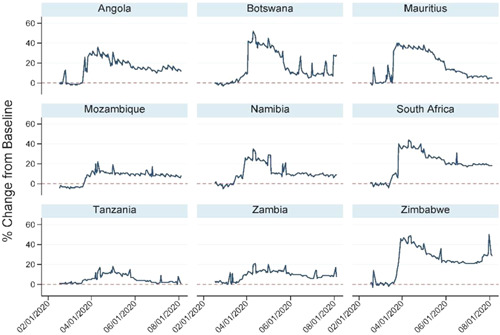

3.3. Primary sector employment risk

Employment risk in the primary sectors of SADC members states is analysed using high frequency data with regard to each country's terms of trade. Due to relatively low manufacturing shares of employment in most SADC member states, most exports are in the form of raw materials making this measure particularly important.

As shown in Figure 4, we observe positive increases in the terms of trade for almost all countries since early 2020. Angola and the DRC stand out as outliers, with substantial declines, though remained elevated. Angola's terms of trade in particular have collapsed due to depressed oil prices, relative to the prices of imports. As a result, we expect much larger employment risks for Angola's primary sector relative to other SADC member countries, with low risks for all other SADC member countries, apart from the DRC, which sees moderate risk.

Figure 4.

Terms of trade—commodity net export price index, January 2019–July 2020. Note: Index base is June 2012; 45 individual commodities weighted by ratio of net exports to GDP, recent rolling weights; monthly data from January 2019 to July 2020. Source: International Monetary Fund, 2020

The ILO's warning of employment risks in the agricultural sector is salient here too, as well as the importance of the sector's continued output in mitigating food insecurity risk (International Labour Organization, 2020c). Disruptions in local and international demand, transport routes, and value chains may aggravate food insecurity, as well as lead to higher employment risk in the primary sector.

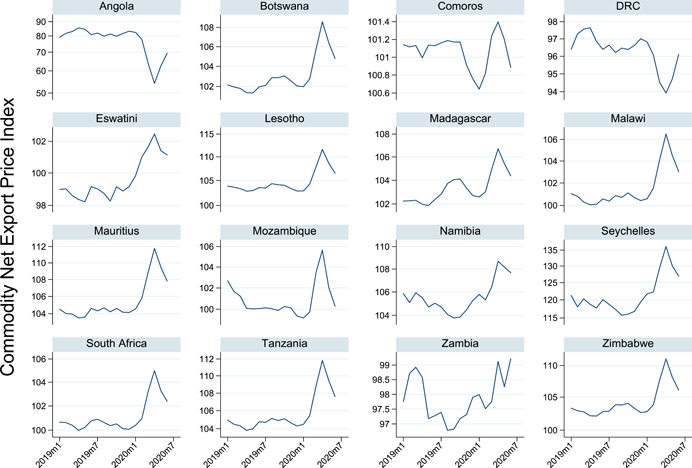

A second caveat is that the above changes are not always large in the broader scheme of commodity price movements since 2000. This is the case for around half the SADC countries (Figure 5). For the other half, however, the movements since 2000 remain highly significant. Angola in particular is currently at levels not experienced since the early 2000s, indicating a large regression in its primary sector's strength, with a high employment risk factor as a result. The DRC has more or less continued on its trend of deteriorating terms of trade, with a recent dip and subsequent recovery in line with the downward trend emerging in 2017/18. Other SADC member states are trading above or near to their June 2012 levels, with notable trade term improvements since the start of 2020 for Botswana, Eswatini, Lesotho, Madagascar, Malawi, Mauritius, Namibia, Seychelles, South Africa, Tanzania, Zambia and Zimbabwe. These improvements serve to mitigate potential employment risk in the primary sector, and subsequently we classify these risks as relatively low.

Figure 5.

SADC member terms of trade, January 2000–July 2020. Note: Index base is June 2012; 45 individual commodities weighted by ratio of net exports to GDP, recent rolling weights; monthly data from January 2000 to July 2020. Reference line indicates index base of 100. Source: International Monetary Fund, 2020

3.4. Secondary sector employment risk

We use two metrics to assess risks to secondary sector employment risk.

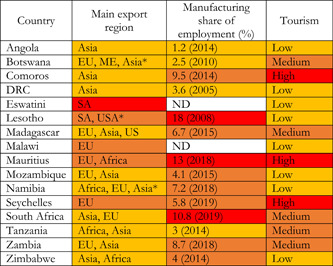

First, based on employment in export‐facing sectors, Eswatini, Lesotho, Malawi, Mauritius and the Seychelles face the highest risk. Secondary sector employment risk (and primary and tertiary to some extent) is difficult to differentiate from export employment risk, because most secondary sector production on the continent is exported. In this respect, Table 3, Column 1, which considers countries’ main export destinations (in general) indicates high risk for Eswatini because its main export market is South Africa, which is experiencing a large contraction in GDP. Lesotho, Malawi, Mauritius and the Seychelles are facing moderate risk in this regard due to their moderately risky main export destination partners (i.e., slower recoveries and/or deeper contractions), which we define as Africa or the USA, and Europe to a lesser extent.

Table 3.

Export and secondary sector risk assessment for 2020

|

Note: Export region risk indication is based on main export partner region by value, with Asia representing lower risk, EU medium risk, USA and Africa highest risk. Where more than one export region is specified, this is deemed as lower risk where Asia is one of the main regions. Share of employment in manufacturing (latest available date) shading in dark grey represents share more than 10%, medium grey between 4% and 10%, light grey less than 4%. Tourism risk indication is termed high, medium or low risk as per the IMF's Regional Economic Outlook for sub‐Saharan Africa (April 2020). Economic structure dependency risk indication is also based on the IMF's Regional Economic Outlook for SSA (April 2020), where non‐resource dependency is lower risk, resource intensive countries medium risk, and oil (Angola) high risk.

Source: Main export region: The Observatory of Economic Complexity, *World Integrated Trade System; Manufacturing Share of Employment: ILOstat; Tourism: International Monetary Fund; Dependency: International Monetary Fund.

This article is being made freely available through PubMed Central as part of the COVID-19 public health emergency response. It can be used for unrestricted research re-use and analysis in any form or by any means with acknowledgement of the original source, for the duration of the public health emergency.

A wider range of countries are shown to face medium and high secondary sector employment risks when this is measured based on a country's manufacturing share of employment. This is shown in Column 2 of Table 3. This is the preferred measure of secondary sector risk, due to the employment risks which the sector poses for the wider economy as a result of strong linkages. By this measure Lesotho, Mauritius and South Africa face larger risks due to their secondary employment shares being in excess of 10% of total employment. In the summary table, Table 1 above, secondary sector employment risk is estimated based on this second metric. Interestingly, manufacturing exports are forecast to have a quicker recovery than oil or other export dependencies, such as tourism (Column 3). Recent manufacturing surveys from advanced economies bears this out (Sparshott, 2020).

3.5. Tertiary sector employment risk

Employment risk factors in the tertiary sector are proxied using Google Mobility data. This analysis focuses on visits to retail and recreation destinations, as well as grocery and pharmacy destinations. These measures comprise the bulk of tertiary sector activity and are well suited as an indication of employment risk. We compose an analysis similar to that of the general employment risk section.

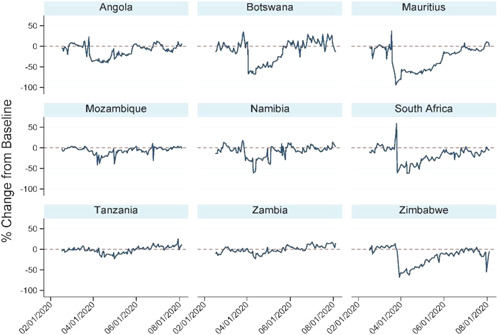

All countries for which there is data show a meaningful dip in visit to retail and recreation sites as the pandemic hits in early 2020, although less so for Mozambique, Tanzania and Zambia. These retail and recreation mobility trends, illustrated in Figure 6, give us a good indication of the extent of consumption changes in the tertiary sector. In some cases, the bulk of employment in the tertiary sector is in retail and wholesale trade, and so decreased revenues are likely to result in business closures, working‐hour and wage reductions, and job losses. The trends above show Angola, Botswana, Mauritius, Namibia, South Africa and Zimbabwe having substantial decreases in retail and recreation foot traffic. All of the aforementioned have subsequently returned to near‐baseline figures, except from South Africa, which remains 20% below its January averages. As noted, Mozambique, Tanzania and Zambia all saw relatively smaller reductions in retail and recreation traffic, and have mostly recovered to January levels, with Mozambique having recovered consistently and is almost back to its baseline.

Figure 6.

Retail and recreation number of visits relative to January baseline, February–August 2020. Note: Retail and recreation mobility trends are relative to a median baseline reference period measured between 3 January and 6 February 2020. Comparisons are relative to corresponding day of the week. Measured from 15 February to 4 August 2020. Source: Google COVID‐19 Community Mobility Reports

These findings are confirmed by a second metric—changes in foot traffic to grocery and pharmacy outlets shown in Figure 7. Mozambique, Tanzania and Zambia, with less stringent lockdowns, saw more activity. As with visits to retail and recreation, Mauritius, South Africa and Zimbabwe saw large reductions in foot traffic to grocery and pharmacy locations.

Figure 7.

Grocery and pharmacy number of visits relative to January Baseline, February–August 2020, Saturday and Sunday excluded. Note: Retail and recreation mobility trends are relative to a median baseline reference period measured between 3 January and 6 February 2020. Comparisons are relative to corresponding day of the week. Measured from 15 February to 4 August 2020. Source: Google COVID‐19 Community Mobility Reports

Quantification and aggregation of these metrics—shown in Table 4, using the same approach as Table 2 previously—show that Mauritius and South Africa have the highest tertiary sector employment risks (with totals greater than −8000); Angola, Botswana, Namibia and Zimbabwe have moderate risks (with totals between −8000 and −4000); and Mozambique, Tanzania and Zambia have relatively low tertiary sector employment risk (with totals greater than −4000).

Table 4.

Cumulative retail and residential and grocery and pharmacy mobility changes, during Q1 and Q2 2020

| Country | Retail and recreation | Grocery and pharmacy | Tertiary total |

|---|---|---|---|

| Angola | −4138 | −1698 | −5836 |

| Botswana | −3015 | −1739 | −4754 |

| Mauritius | −6619 | −5173 | −11792 |

| Mozambique | −2756 | −961 | −3717 |

| Namibia | −3572 | −1484 | −5056 |

| South Africa | −6231 | −2985 | −9216 |

| Tanzania | −1932 | −263 | −2195 |

| Zambia | −1057 | −33 | −1090 |

| Zimbabwe | −4371 | −2526 | −6897 |

Note: Authors’ construction. Tertiary total adds cumulative grocery and pharmacy figures to cumulative retail and recreation figures. Measured from 15 February to 4 August 2020.

Source: Google COVID‐19 Community Mobility Reports.

This article is being made freely available through PubMed Central as part of the COVID-19 public health emergency response. It can be used for unrestricted research re-use and analysis in any form or by any means with acknowledgement of the original source, for the duration of the public health emergency.

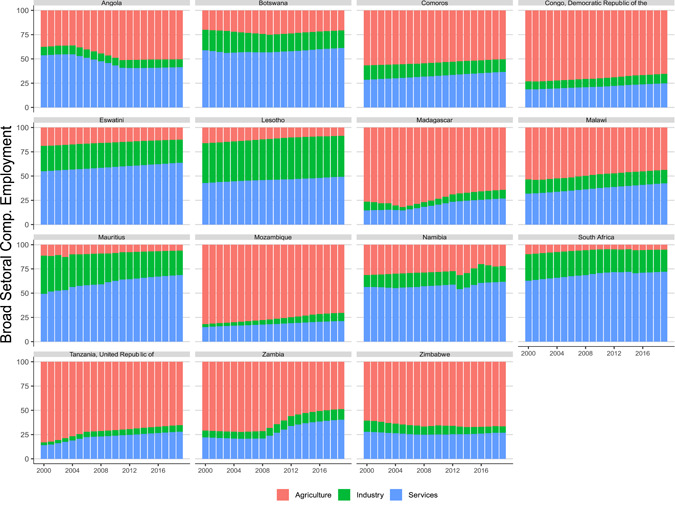

We once again complement this Google Mobility data with the sectoral composition of employment shown in Figure 8. This shows us the concertation of employment in the tertiary sector. It is particularly important where Google Mobility data is unavailable, although it remains a weaker proxy of assessing tertiary sector employment risk. However, it is useful in determining employment risks in the tertiary sector in the context of the wider economy.

Figure 8.

Broad employment composition as a proportion of total for SADC countries, 2000–2019. Source: ILOStat

By this metric, Eswatini is added to the high‐risk category as its tertiary sector employment share is over 50% of total employment. Comoros, Lesotho and Malawi face moderate tertiary sector employment risk, with shares between 30% and 50%, and the DRC and Madagascar face relatively low risk with shares less than 30% of total employment.

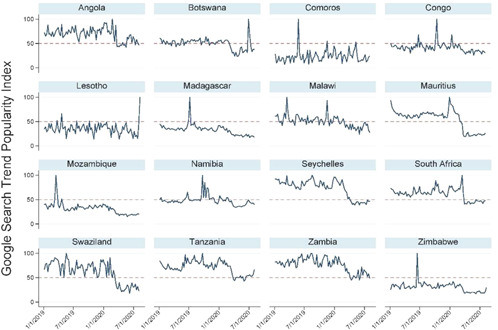

The tourism industry is another measure of tertiary sector employment risk as some SADC economies, especially the island countries of Comoros, Mauritius, Madagascar and Seychelles, have a relatively larger reliance on, and income generation from, the tourism sector. Figure 9 highlights changes in Google search trend popularity, which can be used to proxy for tourism activity (Bokelmann & Lessman, 2019; Onder, 2017).

Figure 9.

Google tourism searches for each country, January 2019–July 2020. Note: Google Trends weekly search data. ‘Travel’ filter applied. Search input is as they are in the figure, showing highest relevant search volumes. ‘Congo’ is used, which does not accurately identify the DRC, which had very low search volumes in any iteration of search input. The index is base 100, with a value of 50 representing half as much search interest during that week as opposed to the highest week. Source: Google Search Trend Popularity Index

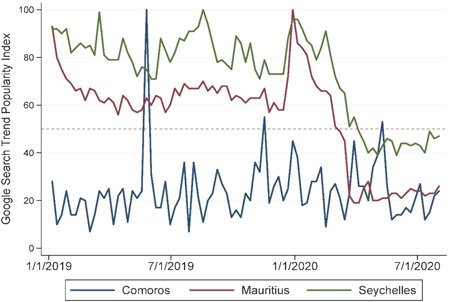

Over the course of 2020, we see weekly search term popularity decreasing for all countries relative to their week of maximum popularity. In some cases, highest popularity has been during 2020, which is likely due to the citizen repatriations undertaken by various governments. This aside, all SADC member states see relative decreases in travel search popularity, with the exception of Comoros, which has relatively low search volumes and thus higher volatility in their index. Countries with higher vulnerability to decreases in tourism activity include Comoros, Mauritius and Seychelles. This can have strong knock‐on effects on employment in connecting industries, which in these economies are vast. We zoom in on these three countries in Figure 10. We see that changes to searchers for the Comoros is more muted than the other two countries, reflecting a much smaller tourism sector compared to its regional neighbours (and in turn more shallow, volatile search data), though we assume high risk as well.

Figure 10.

Google tourism searches for tourism dependent countries, January 2019–July 2020. Note: Trends for tourism intensive countries as defined by the IMF. Comoros data has more volatility due to relatively lower search volumes. Source: Google Search Trend Popularity Index

3.6. Women employment risk

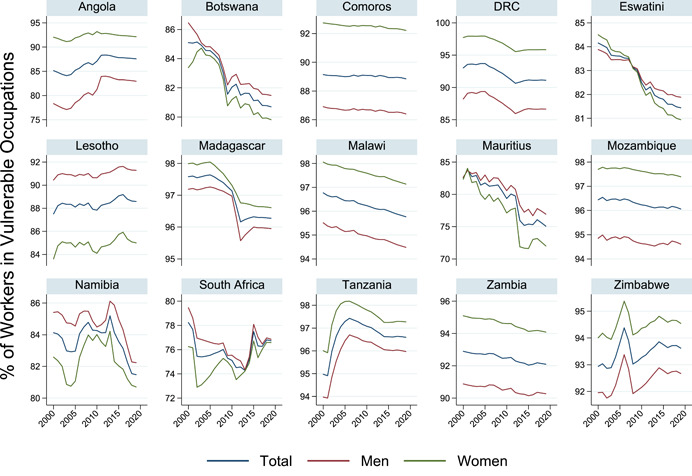

Employment risk for women is an important subject to interrogate due to their relative precarity in employment, as well as the traditionally higher burden of responsibility for home and care work. We focus on the relative ‘vulnerability’ of women versus that of men, which we define by which occupations women work in (relative to men) and the approximate degree of risk of these occupations to loss of employment as a result of the pandemic (see Section 2 for a list of these occupations).

Countries where women have higher proportions of at‐risk employment (relative to men) include Angola, Comoros, the DRC, Madagascar, Malawi, Mozambique, Tanzania, Zambia and Zimbabwe (Figure 11), as shown by the green line being above the blue line. In general, SADC member states have high proportions of both men and women in vulnerable occupations, with totals often exceeding 85%. Botswana, Eswatini, Mauritius, Namibia and South Africa have slightly lower levels.

Figure 11.

At‐risk occupation share of employment by gender. At‐risk occupational share is authors’ construction. Source: ILOStat

3.7. Youth employment risk

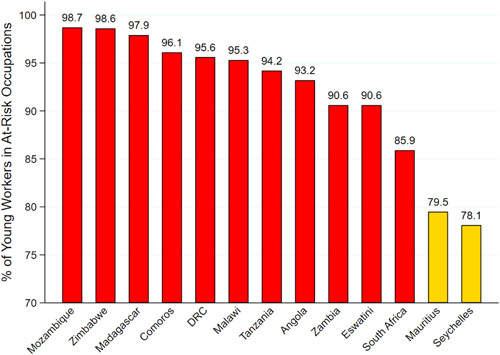

In most all SADC countries youth face significant employment risk. This is shown in Figure 12, where the proportion of youth in at‐risk occupations is shown. Countries facing at‐risk shares of youth employment of over 90% are at very high risk of severe youth employment risk, including (in descending order of severity): Mozambique, Zimbabwe, Madagascar, Comoros, DRC, Malawi, Tanzania, Angola, Zambia and Eswatini. This partly reflects demographic differences between countries, different labour force participation rates of youth (with young people having entered the workforce more in these economies), larger informal sector markets with opportunities for youth work, and weaker training and education systems. Mauritius and Seychelles face relatively low risk by this measure with shares of at‐risk youth employment at less than 80%.

Figure 12.

At‐risk employment share for youth as a percentage of total youth occupations. Note: Latest available year shown. Youth defined as ages between 15 and 24. Dark grey shading represents a share of vulnerable occupations in youth employment of over 85%, light grey represents under 85%. Occupational data availability varies by country, increasing the uncertainty of these figures. Source: ILOStat and Quarterly Labour Force Survey 2020:Q2 for South Africa

4. CONCLUSION AND POLICY IMPLICATIONS

Using high frequency data from Q1 and Q2 2020, as well as 2019 annual data, this paper provided risk estimates of the impact of COVID‐19 on SADC member states’ labour markets. These risk estimates ranged from low to high, and include analyses on key labour market demographics including differentiating by sector and worker type.

Methodologically, this analysis highlights how, in seemingly information scarce environments, qualitative near real‐time employment risk assessments can be provided for countries on the basis of macroeconomic surveillance, which incorporates daily, weekly, monthly and annual data. As use of cell phones with GPS technology increases in Africa so too will more Google Mobility data become available. Although this paper did not use finer‐grained changes in mobility patterns, or changes in mobility within countries by province or region, future papers and country‐specific surveillance can easily do so. Incorporating such data into regression analysis is a plausible extension of this study and is recommended at the monthly level, so long as measures of employment or output can be found at this frequency too.

We find that Angola, South Africa and Zimbabwe are at greatest risk across several labour market dimensions from the COVID‐19 shock.4 This is followed by a second group of countries consisting of Comoros, the DRC, Madagascar and Mauritius. Angola faces relatively less general employment risk than South Africa and Zimbabwe, due to more muted decreases in mobility, though faces large pressure in its primary sector as oil production remains depressed. These countries all face high risk to their youth populations, with Angola and Zimbabwe seeing high risks for women. South Africa faces more sector‐specific risks in their secondary and tertiary sectors, as does Mauritius. Comoros, the DRC and Madagascar face high risks of employment loss for women and youth, with Comoros and Mauritius facing severe general employment risks.

Namibia and Botswana's labour markets are likely to be least affected by COVID‐19 according to our analysis. Although they face moderate general employment risk, their specific employment risks owing to the nature of their production structures and the occupations occupied by women and youth dampen the negative labour market impact. Both countries' export partners are expected to recover faster than other regions too. This does not mean that their economies will be unaffected, only that the impact will be less severe relative to other SADC economies along the dimensions analysed here.

Appropriately addressing the labour sectors at highest risk is important when SADC countries consider how to design inclusive policies to support a broad‐based recovery from COVID‐19. A range of such policy options are available.

First, general economy‐wide measures will support all at‐risk groups. Wage‐support measures have been widely used internationally (Gentilini et al., 2020), where governments provide businesses with funds necessary to pay salaries (or a share thereof) to prevent retrenchments. However, these may not be as appropriate for countries with large informal sectors or own‐account workers, as in many SADC countries. In this case, universal social security would help these workers weather the storm (International Labour Organization, 2020d; Oxfam, 2020). Not only does this protect people against the virus, but acts as a useful mechanism to increase consumer demand and thus promote a more rapid recovery in output and employment. In the context of constrained fiscal space, additional taxes may prove beneficial to revenue collection volumes. Special ‘luxury good’ taxes, one‐off taxes on those with extremely high wealth, budget reprioritizations, and increased income taxes on high‐income earners are some obvious avenues in this regard.

Second, sector‐specific policies should aim to support sectors that are at relatively higher risk of contraction than others, according to specific output and employment structures, as well as those facing greater difficulties in mobility to and from those workplaces. Sectors that remain relatively intact should be stabilized, and the value produced used to supplement the losses in other vital sectors to prevent long‐term capacity loss. Such strategies include business subsidies, low‐cost flexible‐term loans, and tax breaks or deferments. Further, facilitating the safe mobility to and from workplaces is important, especially with regard to public transport, as decreases in mobility contribute to the fall in local supply and demand in local economies. Governments should work to create, strengthen and monitor health and safety protocols in workplaces, retail and recreational, grocery and pharmacy locations to protect workers and consumers and slow the spread of contraction of the virus.

Third, as some employment loss is to be expected, governments should consider bolstering occupational training centres aimed at retraining and upskilling those who have lost their jobs, with a focus on giving people skills to work in higher value‐adding occupations (those in industry and service sectors). This can be encouraged by the extension of unemployment insurance benefits to those retrenched and can specifically target youth. Lastly, female employment protection should be a specific feature of all government programmes. In addition, alleviating women's care responsibilities can support them remaining in the workforce. This can be done through targeted social transfers, child‐care provision, and improving basic services.

ACKNOWLEDGEMENTS

Thank you to feedback from ILO and SADC members on earlier drafts. All errors are our own.

Rosenberg, J. , Strauss, I. , & Isaacs, G. (2021). COVID‐19 impact on SADC labour markets: Evidence from high‐frequency data and other sources. Afr Dev Rev, 33, S177–S193. 10.1111/afdr.12528

This paper draws on an impact assessment written for SADC and the ILO by the authors as expert external consultants.

ENDNOTES

Living Standards Measurement Study.

More info available at https://support.google.com/covid19-mobility/answer/9825414?hl=en&ref_topic=9822927.

It may, however, also reflect less time spent consuming in person.

Angola, South Africa and Zimbabwe have three or more high‐risk portions of their labour market, with at least two portions at medium risk. Other countries have at least three high‐risk portions, or two high‐risk portions and at least two medium‐risk portions.

REFERENCES

- African Development Bank (2020). Southern Africa Economic Outlook 2020—coping with the COVID‐19 pandemic. African Development Bank Group. https://www.afdb.org/en/documents/southern-africa-economic-outlook-2020-coping-covid-19-pandemic

- Anyanwu, J. C. , & Augustine, D. (2013). Gender equality in employment in Africa: Empirical analysis and policy implications. African Development Review, 25(4), 400–420. [Google Scholar]

- Baek, C. , McCrory, P. B. , Messer, T. , & Mui, P. (2020). Unemployment effects of stay‐at‐home orders: Evidence from high frequency claims data. The Review of Economics and Statistics, 1–72. https://www.mitpressjournals.org/doi/abs/10.1162/rest_a_00996 [Google Scholar]

- Bokelmann, B. , & Lessman, S. (2019). Spurious patterns in Google Trends data—an analysis of the effects on tourism demand forecasting in Germany. Tourism Management, 75, 1–12. https://www.researchgate.net/publication/318832909_Forecasting_tourism_demand_with_Google_trends_Accuracy_comparison_of_countries_versus_cities [Google Scholar]

- Boukar, A. M. , Mbock, O. , & Kilolo, J. M. (2021). The impacts of the Covid‐19 pandemic on employment in Cameroon: A general equilibrium analysis. African Development Review 1–14. https://onlinelibrary.wiley.com/doi/full/10.1111/1467-8268.12512 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Cajner, T. , Figura, A. , Price, B. M. , Ratner, D. & Weingarden, A. E. (2020). Reconciling unemployment claims with job losses in the first months of the COVID‐19 crisis (Finance and Economics Discussion Series Working Paper No. 2020‐055). https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3655846

- Chen, W. (2020). Disparities in real time: Online job posting analysis shows the extent of the pandemic's damage, especially to women and youth. IMF Finance & Development. https://www.imf.org/external/pubs/ft/fandd/2020/12/pdf/value-of-real-time-data-in-covid-crisis-chen.pdf

- Dalton, M. , Weber Handwerker, E. , & Loewenstein, M. A. (2020). Employment changes by employer size during the COVID‐19 pandemic. Monthly Labor Review, 1–17. https://www.bls.gov/opub/mlr/2020/article/employment-changes-by-employer-size-during-the-covid-19-pandemic-a-look-at-the-current-employment-statistics-survey-microdata.htm [Google Scholar]

- Djoumessi, Y. F. (2021). The adverse impact of the Covid‐19 pandemic on the labour market in Cameroon. African Development Review, 1–14. https://onlinelibrary.wiley.com/doi/full/10.1111/1467-8268.12508 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Gentilini, U. , Almenfi, M. , Dale, P. , Lopez, A. V. , & Zafar, U. (2020). Social protection and jobs responses to COVID‐19: A real‐time review of country measures (Living paper, version 12). https://openknowledge.worldbank.org/bitstream/handle/10986/33635/Social-Protection-and-Jobs-Responses-to-COVID-19-A-Real-Time-Review-of-Country-Measures.pdf?sequence=17

- Ghosh, T. , Elvidge, C. D. , Hsu, F.‐C. , Zhizhin, M. , & Bazilian, M. (2020), The dimming of lights in India during the COVID‐19 pandemic, Remote Sensing, 12, 3289. https://www.mdpi.com/2072-4292/12/20/3289/pdf [Google Scholar]

- Gondwa, G. (2020). Assessing the impact of COVID‐19 on Africa's economic development., United Nations Conference on Trade and Development. https://unctad.org/system/files/official-document/aldcmisc2020d3_en.pdf

- Ibukun, C. O. , & Adebayo, A. A. (2021). Household food security and the COVID‐19 pandemic in Nigeria, African Development Review, 1–13. https://onlinelibrary.wiley.com/doi/10.1111/1467-8268.12515 [DOI] [PMC free article] [PubMed] [Google Scholar]

- International Labour Organization (2020a). Global employment trends for youth 2020: Technology and the future of jobs. International Labour Office. https://www.ilo.org/wcmsp5/groups/public/---dgreports/---dcomm/---publ/documents/publication/wcms_737648.pdf

- International Labour Organization (2020b). COVID‐19 impact on the collection of labour market statistics. https://ilostat.ilo.org/topics/covid-19/covid-19-impact-on-labour-market-statistics/

- International Labour Organization (2020c). COVID‐19 and the impact on agriculture and food security. https://www.ilo.org/wcmsp5/groups/public/---ed_dialogue/---sector/documents/briefingnote/wcms_742023.pdf

- International Labour Organization (2020d). Social protection responses to the COVID‐19 pandemic in developing countries: Strengthening resilience by building universal social protection. https://www.ilo.org/wcmsp5/groups/public/---ed_protect/---soc_sec/documents/publication/wcms_744612.pdf

- International Monetary Fund (2020a). World Economic Outlook update, June 2020. https://www.imf.org/en/Publications/WEO/Issues/2020/06/24/WEOUpdateJune2020

- International Monetary Fund (2020b). World Economic Outlook: A long and difficult ascent. https://www.imf.org/en/Publications/WEO/Issues/2020/09/30/world-economic-outlook-october-2020

- Jain, R. , Budlender, J. , Zizzamia, R. , & Bassier, I. (2020). The labour market and poverty impacts of COVID‐19 in South Africa. NIDS‐CRAM https://cramsurvey.org/wp-content/uploads/2020/07/Jain-The-labour-market-and-poverty-impacts.pdf

- Morsy, H. , Balma, L. , & Mukasa, A. , (2020, June). ‘Not a Good Time’: Economic impact of COVID‐19 in Africa (Working Paper Series No 338). African Development Bank. https://www.afdb.org/en/documents/working-paper-338-not-good-time-economic-impact-covid-19-africa [DOI] [PMC free article] [PubMed]

- Onder, I. (2017). Forecasting tourism demand with Google Trends: Accuracy comparison of countries versus cities. International Journal of Tourism Research, 19(4) 648–660. https://www.researchgate.net/publication/318832909_Forecasting_tourism_demand_with_Google_trends_Accuracy_comparison_of_countries_versus_cities [Google Scholar]

- Oxfam (2020). Shelter from the storm: The global need for universal social protection in times of COVID‐19: https://reliefweb.int/sites/reliefweb.int/files/resources/bp-social-protection-covid-19-151220-en.pdf

- Razani, M. , & Cheung Kai Suet, L. (2020). The labor market impact of the COVID‐19 pandemic in Mauritius: Evidence from three rounds of high‐frequency surveys [World Bank Blogs]. https://blogs.worldbank.org/africacan/labor-market-impact-covid-19-pandemic-mauritius-evidence-three-rounds-high-frequency

- Scott, D. , & Finamor, L. (2020). Employment effects of unemployment insurance generosity during the pandemic. Yale University. https://tobin.yale.edu/sites/default/files/files/C-19%20Articles/CARES-UI_identification_vF(1).pdf [Google Scholar]

- Sampi, J. , & Jooste, C. (2020). Nowcasting economic activity in times of COVID‐19: An approximation from the Google community mobility report (Policy Research Working Paper 9247). World Bank Group. http://documents1.worldbank.org/curated/en/619261589478136374/pdf/Nowcasting-Economic-Activity-in-Times-of-COVID-19-An-Approximation-from-the-Google-Community-Mobility-Report.pdf

- Southern African Development Community (2020). SADC regional response to COVID‐19 pandemic (Bulletin No. 9). SADC Secretariat. https://www.sadc.int/files/4515/9562/4051/COVID-19_9th_Report_EN.pdf

- Sparshott, J. (2020). Newsletter: More factory output, fewer factory workers [Realtime Economics, Wall Street Journal]. https://blogs.wsj.com/economics/2020/09/02/newsletter-more-factory-output-fewer-factory-workers/

- The Gambia Bureau of Statistics . (2020). COVID‐19 impact on household wellbeing monitoring. World Bank Group. https://www.gbosdata.org/downloads-file/the-gambia-high-frequency-survey-report-wave-1 [Google Scholar]

- United Nations Women . (2018). Gender differences in poverty and household composition through the life cycle. World Bank Group. https://www.unwomen.org/-/media/headquarters/attachments/sections/library/publications/2018/sdg-report-spotlight-01-gender-differences-in-poverty-and-household-composition-en.pdf?la=en%26vs=4813 [Google Scholar]

- United Nations Women (2020). From insights to action: Gender equality in the wake of COVID‐19. https://www.unwomen.org/-/media/headquarters/attachments/sections/library/publications/2020/gender-equality-in-the-wake-of-covid-19-en.pdf?la=en%26vs=5142

- Weber, M. , Palacios‐Lopez, A. , & Contreras‐Gonzalez, I. M. (2020). Labor market impacts of COVID‐19 in four African countries [World Bank Blogs]. https://blogs.worldbank.org/opendata/labor-market-impacts-covid-19-four-african-countries

- Wonyra, K. O. , Lanie, T. , & Sanoussi, Y. (2021). Potential short‐term effects of the COVID‐19 pandemic on poverty in the countries of the West African Economic and Monetary Union (UEMOA). African Development Review. https://onlinelibrary.wiley.com/doi/full/10.1111/1467-8268.12509 [Google Scholar]

- World Bank (2020a). Global economic prospects. pandemic, recession: The global economy in crisis. www.worldbank.org/en/publication/global-economic-prospects

- World Bank (2020b). LSMS‐supported high‐frequency phone surveys on COVID‐19. https://www.worldbank.org/en/programs/lsms/brief/lsms-launches-high-frequency-phone-surveys-on-covid-19

- Wu, K. , & Thomasberger, M. (2020). When will the global consumer class recover? https://www.brookings.edu/blog/future-development/2020/11/25/when-will-the-global-consumer-class-recover/