Supplemental Digital Content is available in the text.

Key Words: mental health, insurance parity, policy effectiveness

Background:

Mental health insurance laws are intended to improve access to needed treatments and prevent discrimination in coverage for mental health conditions and other medical conditions.

Objectives:

The aim was to estimate the impact of these policies on mental health treatment utilization in a nationally representative longitudinal sample of youth followed through adulthood.

Methods:

We used data from the 1997 National Longitudinal Survey of Youth and the Mental Health Insurance Laws data set. We specified a zero-inflated negative binomial regression model to estimate the relationship between mental health treatment utilization and law exposure while controlling for other explanatory variables.

Results:

We found that the number of mental health treatment visits declined as cumulative exposure to mental health insurance legislation increased; a 10 unit (or 10.3%) increase in the law exposure strength resulted in a 4% decline in the number of mental health visits. We also found that state mental health insurance laws are associated with reducing mental health treatments and disparities within at-risk subgroups.

Conclusions:

Prolonged exposure to comprehensive mental health laws across a person’s childhood and adolescence may reduce the demand for mental health visitations in adulthood, hence, reducing the burden on the payors and consumers. Further, as the exposure to the mental health law strengthened, the gap between at-risk subgroups was narrowed or eliminated at the highest policy exposure levels.

It is estimated that about half of the US population is diagnosed with a mental illness at some point in their life; in 2015, ∼20% of all adults had a mental illness and 4% had serious mental illness and over one-fifth of children had a serious mental illness.1 Mental illnesses are identified as the third most common cause of hospitalizations among 18–44 years old adults2 and lead to a shorter life expectancy.3 In the United States, mental illness accounts for the second largest disease burden, and severe mental health disorders account for about a quarter of hospital admissions and disability payments.4 About half of these chronic illnesses begin by age 14 and 75% begin by age 24.1 If detected early in childhood or adolescence, many mental health conditions can be managed effectively or occasionally prevented entirely in adulthood, which will substantially reduce the economic and psychological burden.4 Despite evidence that early detection and treatment can ease the impact on outcomes and reduce the prevalence of mental illnesses, ∼70% of children and adolescents do not receive needed mental health treatment services.4,5 Inadequate insurance coverage for mental illness is reported as one of the primary reasons for such insufficient access.4,6,7

Public health laws and policies aim to disrupt the status quo by shifting resources and mandating certain actions to improve the underlying health outcomes. Mental health insurance laws are intended to improve access to needed treatment and to prevent discrimination in insurance coverage by requiring equal coverage for mental health treatment and treatment for other medical conditions.4,8,9 Lack of such parity imposed substantial financial burden on families, especially for those with private health insurance that lacked adequate mental health provisions.8 This problem has been addressed in the past decades by adopting parity laws at both federal and state levels.

Although research has shown that these laws improve insurance coverage for mental health care,10,11 there is mixed evidence on the effectiveness of these policies at changing utilization or health outcomes. Studies from the early 2000s reported that parity laws increased mental health treatment utilization by adults with mild symptoms and low-income individuals. However, only a small effect was reported among children.9,12–14 Results from more recent studies were not conclusive. McGinty et al15 found increased utilization of substance use disorder treatment, while others reported no changes in these rates.16–20 Li and Ma4 identified that state mental health insurance laws resulted in modest increases in mental health care utilization among children from middle-income families. Sipe et al21 found that although mental health legislation broadly appeared to improve mental health outcomes for US populations, generally, few studies examine high-risk populations who experience access problems (p. 763).21

Prior studies simplified the legal intervention through use of presence or absence variables8,9,22 and characterized the strength or comprehensiveness of the state laws by their parity provisions23–26 and/or mandated coverage provisions.24,27 To date, no studies have explored the role that laws using specific mental health definitions or enforcement/compliance have had on outcomes. In addition, no known studies have explored longer term or cumulative effects of such legislation on mental health access and utilization, even though it is hypothesized that length of exposure to better legislation could improve access, resulting in better mental health outcomes.

This study estimates the association of mental health insurance laws with mental health treatment utilization in a nationally representative longitudinal sample of youth followed through adulthood. We hypothesize that cumulative exposure over time to stronger mental health insurance laws will be associated with utilization of mental health treatment in adulthood. This analysis uniquely considers life course risk and protective factors that alter adolescent trajectories of mental health and allows for evaluation of the law in future measurement periods after their adoption to determine whether such laws affect mental health treatment. Our study includes detailed nuances of the laws and their changes over a 14-year period using granular variables of state mental health insurance laws. This approach will further clarify the effect of mental health insurance legislation on improving mental health treatment access.

METHODS

We performed retrospective analysis of mental health treatment utilization in a longitudinal sample of adolescents through their adulthood. Data were obtained from the National Longitudinal Survey of Youth 1997 Cohort (NLSY97)28 and the State Mental Health Insurance Laws (SMHIL) data set.29

National Longitudinal Survey of Youth 1997

Data on mental health treatment, as well as individual and environmental characteristics, were obtained from NLSY97 Rounds 1–15, which consists of a nationally representative sample of 8984 youths born during 1980 and 1984. At Round 1, respondents were 12–18 years of age and they continued to be interviewed on an annual basis. By Round 15, 83% of the original sample was retained (for details see Technical Appendix, Supplemental Digital Content 1, http://links.lww.com/MLR/C309). We selected individual and environmental variables that were measured at baseline (1997), adolescence (2001–2005), and adulthood (2009–2011, rounds 13–15) associated with our research question and hypothesis, and available in the survey data. Not all variables were measured at every NLSY97 round.

State Mental Health Insurance Laws Data Set

SMHIL coded state mental health insurance laws across 6 legal provisions using a scientifically rigorous policy surveillance methodology.29 For each year between 1997 and 2020, state mental health insurance laws were evaluated on 6 characteristics: parity (does a state statute require that coverage for mental health services is equal to coverage for other medical conditions); coverage (does a state statute mandate insurance coverage of mental health conditions); definition (does a state statute define mental illness); all conditions defined (does a state statute define mental health conditions as all conditions listed in the Diagnosis and Statistical Manual of Mental Disorders); enforcement (is a state agency required to enforce existing state and/or federal mental health parity laws); and compliance (are insurers required to submit reports demonstrating compliance with state and/or federal parity legislation). All 6 characteristics except parity were scored yes (1 point) or no (0 points), and parity was scored as full parity (2 points), partial parity (1 point), or no parity (0 points). The total score for each state for each year ranged from 0 to 7.

The outcome variable, asked at Rounds 13–15 (2009–2011), was the number of self-reported mental health treatments that the respondent had when they were 24–30 years old. Respondents were asked “How many times have you been treated by a mental health professional?” Responses were coded as “0,” “1,” “2,” “3,” or “4 or more” visits in a year. We created a new variable that measured the number of times the respondent has visited a mental health provider over the 3-year period. The count variable was right censored and the total number of mental health visits in this 3-year period ranged from 0 to 12 visits.

The mental health insurance law variable (Law) is the strength of the respondents’ cumulative exposure to the state mental health insurance laws over time during their adolescence and young adulthood. The Law was constructed using the SMHIL data set.29 For this study, we used data between 1997 and 2011 (beginning and ending period for our outcome variable). The effective dates of insurance laws adopted by states ranged throughout the calendar year, but for our analysis, we chose to adjust the actual effective date to January 1 of the following year, which typically aligns with the insurance plan’s effective date. We assigned each survey respondent a Law strength score based on the state they resided in for each year of the survey (1997–2011). State of residence was obtained from the Bureau of Labor Statistics (BLS) to link NLSY97 and SMHIL data. We aggregated individual mental health insurance law strength scores across all years to create a single value for each respondent that described the amount of exposure they had to mental health insurance laws over the 1997–2011 period. The Law could range between 0 and 97, where a higher value indicated exposure to stronger mental health insurance laws.

Other Variables

In our model, we also accounted for individual [age, sex, race, ethnicity, education, marital status, number of children in the household, adult general health, employment status, exposure to adverse childhood experiences (ACEs)], receiving government assistance measured during respondents’ adolescent period in 2005–2009, household federal poverty level (FPL) and health insurance status at adulthood, whether they live in a rural area, and having had emotional problems in childhood) and environmental factors (state unemployment rate, percent uninsured in the state) that are likely to affect individual’s access to mental health care or outcomes over the life course (The Technical Appendix, Supplemental Digital Content 1, http://links.lww.com/MLR/C309 discusses the construction of ACEs variable).

Analysis

We used NLSY97 Custom Weighting program30 to create custom sampling weights based on the design features and years used in this study. Respondents missing any predictor variable for any reason were retained as a separate category (labeled as “unknown”) and were included in our analyses. Only those missing the outcome variable [n=1031 (11.5%)], were dropped. Per NLSY97, weights were applied when generating descriptive statistics, but not when running complex regressions.30 All analyses were done using Stata 16.31

We specified a regression model to estimate the relationship between mental health treatment utilization and law exposure while controlling for other explanatory variables. Our dependent variable is a count ranging between 0 and 12 with a heavy concentration of zero values (ie, no mental health visits). Given the nature of our dependent variable, we used a zero-inflated negative binomial regression model to account for concentration of large number of zeros and possible overdispersion. For ease of interpretation, Table 2 reports the incidence rate ratio (IRR), which is the ratio of the rate of mental health visit counts (incidents) for those experiencing any mental health visit and shows the percent change in the mean outcome, mental health visits, when Law is increased by 1 unit. In auxiliary regressions (not reported), we also examined law exposure interactions with race, employment, and health insurance status as well as an alternative specification for the inflation model (Technical Appendix, Supplemental Digital Content 1, http://links.lww.com/MLR/C309). None of the interactions were statistically significant. The final model was chosen based on the best fit by the Akaike (AIC) and Bayesian (BIC) information criteria.

TABLE 2.

Mental Health Policy Impact on the Mental Health Treatment Visit

| Count Model | Inflation Model | |||

|---|---|---|---|---|

| Variables | IRR† | 95% CI | IRR | 95% CI |

| Mental Health Policy Exposure Strength | 0.9968** | 0.9937–0.9998 | ||

| Age | 1.059*** | 1.016–1.104 | ||

| Sex (ref. male) | ||||

| Female | 0.904 | 0.785–1.042 | 0.447*** | 0.374–0.535 |

| Race (ref. White) | ||||

| Black | 0.811** | 0.680–0.966 | 2.484*** | 1.995–3.092 |

| Other | 0.869 | 0.680–1.110 | 0.983 | 0.746–1.296 |

| Unknown | 1.197 | 0.489–2.929 | 1.327 | 0.459–3.841 |

| Hispanic ethnicity | 1.012 | 0.807–1.269 | 1.692*** | 1.304–2.196 |

| General health (ref. excellent) | ||||

| Good | 1.084 | 0.931–1.262 | 0.609*** | 0.505–0.736 |

| Fair/poor | 1.103 | 0.927–1.312 | 0.369*** | 0.290–0.469 |

| Unknown | 0.323*** | 0.166–0.630 | 0.313 | 0.028–3.490 |

| Employment (ref. full-time) | ||||

| none | 1.392*** | 1.154–1.678 | 0.464*** | 0.376–0.573 |

| part-time | 1.224** | 1.040–1.441 | 0.606*** | 0.497–0.739 |

| Unknown | 1.131 | 0.765–1.671 | 0.771 | 0.463–1.283 |

| State unemployment (ref. <7.5%) | ||||

| Over 7.5% | 0.864** | 0.747–1.000 | ||

| Unknown | 0.681* | 0.448–1.034 | ||

| Gov assistance recipient (ref. no assistance) | ||||

| Any welfare during 2005–2009 | 0.988 | 0.839–1.163 | 0.562*** | 0.454–0.694 |

| Adverse childhood events (ref. none) | ||||

| 1 ACE | 1.112 | 0.917–1.347 | 0.735** | 0.574–0.939 |

| 2 ACEs | 1.121 | 0.909–1.381 | 0.695*** | 0.538–0.896 |

| 3+ ACEs | 1.236* | 0.995–1.537 | 0.615*** | 0.467–0.811 |

| Living in rural area (ref. rural) | ||||

| Urban | 0.979 | 0.815–1.178 | 0.655*** | 0.516–0.830 |

| Unknown | 0.914 | 0.696–1.199 | 0.725* | 0.501–1.049 |

| Poverty level (ref. 3.00+) | ||||

| 0–0.99 | 0.994 | 0.805–1.227 | ||

| 1.00–1.99 | 0.845* | 0.692–1.031 | ||

| 2.00–2.99 | 0.773** | 0.618–0.965 | ||

| Unknown | 1.051 | 0.877–1.260 | ||

| Health insurance (ref. uninsured) | ||||

| Insured | 1.363*** | 1.158–1.604 | 0.610*** | 0.501–0.742 |

| Depression status (ref. none of the time) | ||||

| Some or all the time | 1.453*** | 1.248–1.693 | ||

| Unknown | 1.300 | 0.950–1.779 | ||

| Highest education completed (ref. less than HS/HS/GED) | ||||

| Associate/Junior college | 0.980 | 0.749–1.281 | ||

| College and above | 1.127 | 0.940–1.351 | ||

| Unknown | 1.189 | 0.654–2.161 | ||

| Marital status (ref. never married) | ||||

| Married | 0.923 | 0.778–1.096 | ||

| Separated | 0.780 | 0.504–1.208 | ||

| Divorced | 0.974 | 0.773–1.227 | ||

| Widowed | 0.171 | 0.014–2.059 | ||

| Unknown | 4.409* | 0.976–19.914 | ||

| Children in the household (ref. none) | ||||

| 1–2 | 0.859 | 0.713–1.034 | 1.852*** | 1.480–2.316 |

| 3+ | 0.978 | 0.749–1.276 | 2.769*** | 1.937–3.959 |

| Unknown | 0.840 | 0.463–1.526 | 3.883 | 0.341–44.221 |

| Percent of state population uninsured (ref. below nat. average) | ||||

| Above average | 1.000 | 0.871–1.148 | 1.148 | 0.964–1.367 |

| Unknown | 0.500*** | 0.341–0.734 | 2.524*** | 1.517–4.197 |

| Having emotional problems at childhood (ref. no) | ||||

| Yes | 0.719*** | 0.564–0.916 | ||

| Unknown | 1.175 | 0.906–1.524 | ||

| Intercept | 0.598 | 0.180–1.985 | 36.917*** | 25.215–54.049 |

| Alpha | 0.447*** | 0.334–0.598 | ||

| N | 7953 | 7953 | ||

IRR is the ratio of the rate of counts (incidents), which is calculated as IRR=exp(β)=e β, where β is the coefficient estimate from the negative binomial regression; (exp(β)–1)×100 shows the percent change in the mean outcome when model input parameter (ie, independent variable) is increased by 1 unit. In our model, IRR for the policy variable is 0.996 and implies that if policy strength were to increase by 10 units (or 10.3%) then we would expect number of mental health visits to decrease by 4%.

ACE indicates adverse childhood experience; CI, confidence interval; GED, graduate equivalency degree; HS, high school; IRR, incidence rate ratio.

P<0.10.

P<0.01.

P<0.001.

Source: Authors’ analysis of data from the NLSY97.

Adjusted Predictions

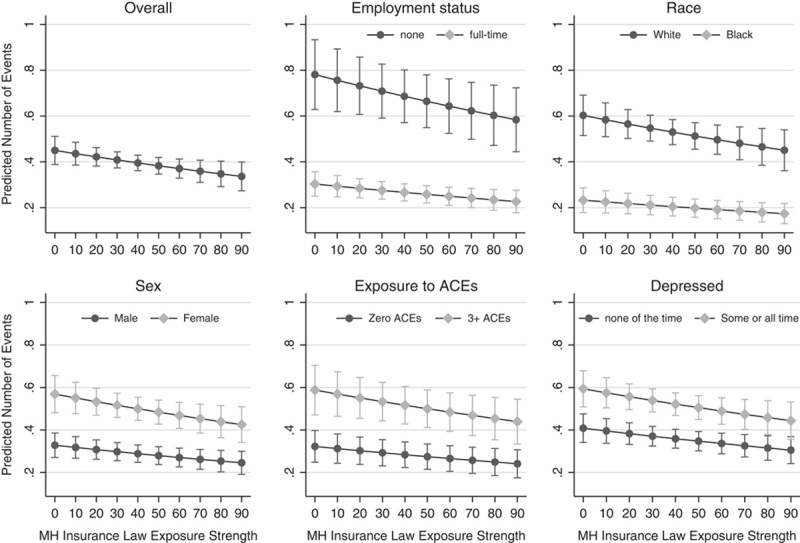

Regression results generate conditional mean estimate of the effect of the Law on the mental health outcome. Adjusted predictions, calculated from the regression estimates, allow us to predict rates of mental health utilization at various levels of Law exposure for specific subgroups, while holding other variables constant. Figure 1 illustrates the predicted number of mental health visits at each level of Law for the overall model as well as by select major factors that play a key role in determining mental health outcomes (race, exposure to ACEs, employment status, depression status, and sex).

FIGURE 1.

Association between Mental Health Insurance Law Exposure Strength and Utilization of Mental Health Services. This figure reports the predicted number of mental health visitations associated with exposure to the Law variable, quantified by a range of 0–97 in increments of 10. These predictions are reported for the overall sample and across subgroups by employment status, race, sex, exposures to adverse childhood experiences, and depression status. For example, upper left graph illustrates the overall predicted number of visits at values of Law that range from 0 to 97 in increments of 10. Similarly, the lower left graph illustrates the predicted number of visits for men and women at values of Law that range from 0 to 97 in increments of 10. This figure shows that the predicted number of mental health visits declined as exposure to the Law increased. However, the group-wise declines were not uniform. At low levels of exposure to mental health insurance laws over the time period, the differences in mental health treatment are wide for specific subgroups after holding other variables constant; however, as exposure to stronger laws increases, the differences in mental health treatment for subgroup variables (eg, employment, race, sex, adverse childhood experiences) are lessened. Dotes denote to point estimates and vertical bars denote to the 95% confidence interval. Source: Authors’ analysis of data from the National Longitudinal Survey of Youth 1997 (NLSY97) and the Mental Health Insurance Parity Statutes data sets.

Limitations

Our study is limited to using secondary data. The NLSY97 lacks more specific mental health outcome variables, such as a diagnosis of mental illness, that we would have desired. However, this is the first study to explore: (1) the cumulative effect of insurance coverage over a 14-year period using longitudinal data; and (2) the comprehensiveness of behavioral health insurance coverage, including granular policy variables. Many previous studies use a preapproach/postapproach to study policy impact and cross-sectional data, which also have significant limitations for interpretation. We believe that this study provides a foundation for further exploration. Also, our outcome variable is censored in the top category where “4 and more” visits are coded as 4. Only 3% of the respondents experienced this, and therefore we believe that this limitation did not significantly alter the results and their interpretation.

The mental health visitation variables were only measured in NLYS97 rounds 13–15 (2009–2011). By this time, all participants were at least 24 years of age. Unfortunately, mental health visits cannot be studied during youth or adolescence. Therefore, our study solely examines self-reported and parent-reported variables from these periods and their effect on later (adult) reported mental health visits. Given the secondary nature of our data set, the results can only apply to the underlying population that they represent, specifically individuals who were born between 1980 and 1984. While we may hypothesize that the mental health insurance laws may produce similar outcomes for the other population age groups, this hypothesis is best addressed in the future research that includes data on other population subgroups. Given that laws change over time, and that exposure to different laws is hypothesized to affect outcomes, these findings should be replicated in other longitudinal cohorts of different ages.

The SMHIL data set did not include data from administrative regulations or statutes contained outside of the insurance code. These laws do not directly influence Medicare, Medicaid, or military-related health plan insured individuals. Because of the heterogeneity of state mental health insurance laws, the data set does not assess all variation contained in state statutes, but adds important nuance of legal provisions that have previously gone unstudied.

RESULTS

As reported in Table 1, in our (weighted) study population, females comprised 49% of the population. White and Black participants were 58% and 26%, respectively, and 21% were Hispanic. In 2009, respondent age ranged from 24 to 30, 63% had high school or lower education, 29% had college education, 59% were never married, 34% were married, majority (61%) had no biological children, and 59% lived in states with below average uninsured rates. During 2009–2011, about 12% of respondents reported having at least 1 visit for a mental health treatment and majority (75%) reported being in good or excellent health. In 2009, 47% of respondents had full-time employment and 18% were unemployed, 19% lived in rural areas, 26% reported being depressed some or all the time, 31% received governmental assistance during this period, the majority had experienced at least one ACE (33% one ACE, 29% two ACEs, and 19% more than 3 ACEs), and 56% had either public or private insurance.

TABLE 1.

Weighted Descriptive Summary of the NLSY97 Sample Used in This Study (N=7953)

| Variable | N | Mean | SD | Minimum | Maximum |

|---|---|---|---|---|---|

| Mental Health Policy Exposure Strength | 7953 | 32.36 | 19.73 | 0 | 97 |

| Age (in 2009) | 7953 | 26.75 | 1.47 | 24 | 30 |

| MH visits during 2009–11 (mean) | 7953 | 0.43 | 1.79 | 0 | 12 |

| n (%) | |||||

| MH visits during 2009–2011 | |||||

| None | 7161 (88.07) | ||||

| 1–12 | 792 (11.93) | ||||

| Sex | |||||

| Male | 4041 (51.19) | ||||

| Female | 3912 (48.81) | ||||

| Race | |||||

| White | 4548 (58.24) | ||||

| Black | 2197 (26.58) | ||||

| Other | 1139 (14.29) | ||||

| Unknown | 69 (0.89) | ||||

| Hispanic ethnicity | 1725 (21.16) | ||||

| General health status | |||||

| Excellent/very good | 4589 (51.08) | ||||

| Good | 2189 (24.37) | ||||

| Fair/poor | 778 (8.66) | ||||

| Unknown | 397 (15.89) | ||||

| Employment | |||||

| None | 1544 (17.82) | ||||

| Part-time | 2037 (23.22) | ||||

| Full-time | 4145 (47.27) | ||||

| Unknown | 227 (11.69) | ||||

| State unemployment | |||||

| 4.0–7.5% | 1506 (16.77) | ||||

| Over 7.5% | 6264 (69.75) | ||||

| Missing | 183 (13.48) | ||||

| Government assistance recipient | |||||

| None | 5186 (68.63) | ||||

| Any welfare during 2005–2009 | 2776 (31.37) | ||||

| Exposure to adverse events | |||||

| 0 ACEs | 1573 (19.10) | ||||

| 1 ACE | 2793 (33.37) | ||||

| 2 ACEs | 2143 (28.94) | ||||

| 3+ ACEs | 1444 (18.59) | ||||

| State poverty level | |||||

| 0–0.99 | 1270 (14.14) | ||||

| 1.00–1.99 | 1244 (13.85) | ||||

| 2.00–2.99 | 1142 (12.71) | ||||

| 3.00 and over | 2984 (33.21) | ||||

| Missing | 1313 (26.09) | ||||

| Insured | 4990 (55.54) | ||||

| Rurality | |||||

| Rural | 1193 (18.52) | ||||

| Urban | 5705 (72.80) | ||||

| Unknown | 1055 (8.68) | ||||

| Depressed | |||||

| None of the time | 5300 (72.23) | ||||

| Some or all the time | 1988 (25.79) | ||||

| Unknown | 665 (1.98) | ||||

| Education | |||||

| Less than HS/HS/GED | 5219 (63.44) | ||||

| Associate/junior college | 484 (7.02) | ||||

| College and above | 1795 (28.86) | ||||

| Unknown | 455 (0.68) | ||||

| Marital status | |||||

| Never married | 4718 (58.87) | ||||

| Married | 2327 (34.18) | ||||

| Separated | 99 (1.23) | ||||

| Divorced | 391 (5.50) | ||||

| Widowed | 10 (0.09) | ||||

| Unknown | 408 (0.13) | ||||

| Children in the household | |||||

| None | 4428 (61.41) | ||||

| 1–2 | 2511 (32.10) | ||||

| 3+ | 609 (6.44) | ||||

| Unknown | 405 (0.058) | ||||

| Percent state uninsured population | |||||

| Below average | 3999 (58.53) | ||||

| Above average | 3421 (40.73) | ||||

| Unknown | 533 (0.74) | ||||

Data presented are weighted using NLSY97 custom sampling weights.

ACE indicates adverse childhood experience; GED, graduate equivalency degree; HS, high school; MH, mental health; NLSY97, National Longitudinal Survey of Youth 1997 Cohort.

Source: Authors’ analysis of data from the NLSY97.

Table 2 reports regression results estimating the relationship between Law and number of mental health visits, while controlling for other covariates. As hypothesized, the mental health Law (IRR=0.996) was statistically significant (P<0.05) and implies that if Law is increased by 10 units (or 10.3%) then we would expect number of mental health visits in adulthood to decrease by 4%. Our results also showed that Black respondents, compared with White respondents, reported lower levels of mental health treatment visits (IRR=0.806, P<0.05). Those with part-time (IRR=1.404, P<0.001) or no employment (IRR=1.680, P<0.001), reported higher mental health visits than those who were employed full time. Mental health visits increased with age at about 6% for each year (IRR=1.058, P<0.05). Those who had 1–2 children at home, had 25% less mental health visits than those without children (IRR=0.749, P<0.001) and those having reported being depressed some or all the time had 58% higher mental health visits (IRR=1.583, P<0.001).

As the state-level unemployment increased, the number of mental health visits declined (IRR=0.836, P<0.05). Respondents who were exposed to higher levels of ACEs (more than 3) reported significantly more mental health visits compared with the respondents without any ACE (IRR=1.259, P<0.10). Individuals living in a household with income at >300% FPL had 22% higher mental health visits compared with those in the 200%–299% FPL level (IRR=0.784, P<0.05). Insured respondents had 42% more mental health visits (IRR=1.415, P<0.001) compared with uninsured respondents. Other variables were not statistically associated with the outcome.

Figure 1 reports adjusted predictions and shows that the predicted number of mental health visits declined as exposure to the Law increased. However, the group-wise declines were not uniform. The marginal effects illustrate that at low levels of exposure to mental health insurance laws over the time period, that differences in mental health treatment are wide for specific subgroups after holding other variables constant; however, as exposure to stronger laws increases, the differences in mental health treatment for subgroup variables (eg, employment, race, sex, ACEs) are lessened.

DISCUSSION

We found that cumulative exposure to more comprehensive mental health insurance laws across the lifespan was associated with fewer mental health visits in young adulthood. To our knowledge, this is the first population-based evaluation of cumulative exposure to mental health insurance laws over a period of 14 years. Previous studies show that mental health diagnoses and visits32 as well as mental health spending33 have been increasing in the United States, particularly for those with existing mental illness. Our results indicate that prolonged exposure to stronger mental health insurance laws was associated with fewer mental health visits among adults who reported any mental health treatment visits during the study period. These results are important because they demonstrate that stronger state mental health insurance laws may contribute toward reducing the need for mental health treatment over time, hence, reducing the burden on the health system.

Our results make a significant contribution to the existing literature by exploring novel aspects of mental health insurance laws. Our study is unique in that we incorporated the comprehensiveness and complexity of mental health insurance laws, such as factors defining mental health conditions, enforcement, and compliance with state laws. The granularity of our coding scheme incorporates important nuances of state mental health insurance laws and may inform future legislative proposals.

We characterize reduced utilization of mental health treatment in adulthood as a positive outcome in this study. In cross-sectional studies, increased utilization of treatment is often indicative of improved access to needed treatment. However, in this longitudinal study, we hypothesize that exposure to more comprehensive and stronger legislation throughout the life course may have provided respondents with needed mental health treatment in childhood and adolescence, therefore reducing the need for treatment in adulthood. Several studies have found that childhood social and emotional problems and exposure to ACEs result in negative mental health outcomes.34,35 Insurance coverage is associated with fewer structural barriers to mental health treatment.36 However, evidence is limited on the effect that insurance coverage for mental health treatment in childhood has on adult outcomes. The survey data set used in this study limits our ability to further test this hypothesis and highlights a need for future research.

Our findings also showed that mental health visits declined in different ways among population subgroups as exposure to strong mental health insurance laws increased. Greater exposure to stronger laws appears to narrow differences in subgroups who tend to be different in demographics (eg, race) or socioeconomic indicators (eg, employment). Insurance laws are intended to improve access; for marginalized groups or groups who may experience greater access barriers, the stronger laws may be contributing to fewer treatment disparities. This is an important finding given what we know about the salience of multilevel factors that influence mental health treatment utilization, particularly among populations with significant barriers to care.37 Barriers to mental health help-seeking among African American adults includes perceived discrimination and racism,38 distrust of the mental health care system,39 poorer quality health care plans,39 and limited access to culturally competent mental health care services.40 Increasing access to mental health care in childhood through exposure to strong mental health insurance laws may help those experiencing population-level, system-level, and provider-level biases avoid these barriers in adulthood and reduce mental health inequities.

It is important to note the broader context of mental health legislation and insurance reform that was occurring simultaneously with the adult outcome measurement in 2009–2011. The MHPAEA was passed in 2008 and became effective in 2009, and the ACA was passed in 2010 and became effective in 2014. Both of these federal laws had significant impacts on insurance coverage for mental health treatment and were also the impetus for state-level efforts to improve mental health insurance coverage. While the state insurance laws studied here were limited to the commercial insurance market, the federal laws affected both the commercial and public insurance markets. It is possible that the changes in state mental health insurance laws after 2008 are indicative of these national and broader state-level efforts and that our findings reflect these policies. We were unable to control for many of these factors, but the closure in utilization gaps between employed and unemployed respondents, despite only studying commercial insurance, supports this possibility.

Research has established a link between ACEs and problems in adulthood, including mental health problems, substance misuse, and underemployment.41 Our study suggests that stronger mental health insurance laws are associated with a significantly lower number of visits as an adult reported by those with 3+ ACEs in childhood as compared with those with 3+ ACES who were exposed to weak mental health laws. Taken in the context of the mental health care needs of those experiencing ACEs, our study implies that mental health insurance laws are likely important for improving adult outcomes for those experiencing a greater need as a child. While additional research is needed to further establish these linkages and pathways, our results suggest that strong mental health insurance laws are an important moderator. These findings are very promising and may guide policymakers and mental health advocates on improving access and utilization of mental health services in the future.

Mental health insurance legislation is generally less visible to the public and is more difficult to enforce than other laws intended to improve health. For example, tobacco control policies, tend to be visible, easily enforceable, and there are clear disincentives to disobeying the law. In contrast, the immediate effects of mental health insurance legislation are not always clear to the public or even to policymakers. Inclusion of enforcement and compliance variables in the legal data set we used allowed us to explore how these previously unstudied factors may contribute to decreased utilization of treatment in adulthood. Our findings support the need for stronger mental health parity legislation, which uses clear, unambiguous definitions of mental health conditions, and which is enforceable at the state-level.

In summary, our results highlight that prolonged exposure to strong mental health laws across a person’s childhood and adolescence may reduce the demand for mental health visitations in adulthood, hence, reducing the burden on the payors and consumers. The context of our study in the Great Recession and the corresponding expansion of mental health insurance laws during this time period, provide a ripe area for future inquiry to better understand the long-term effects of state mental health insurance laws during individuals’ childhood, adolescence, and adulthood.

Supplementary Material

Supplemental Digital Content is available for this article. Direct URL citations appear in the printed text and are provided in the HTML and PDF versions of this article on the journal's website, www.lww-medicalcare.com.

Footnotes

This study was funded by the US Department of Health and Human Services, Health Resources and Services Administration, Maternal and Child Health Field Initiated Research Program through award R40MC32878.

The authors declare no conflict of interest.

Contributor Information

Vahé Heboyan, Email: vheboyan@augusta.edu.

Megan D. Douglas, Email: mdouglas@msm.edu.

Brian McGregor, Email: bmcgregor@msm.edu.

Teal W. Benevides, Email: TBENEVIDES@augusta.edu.

REFERENCES

- 1.CDC. Learn About Mental Health. Centers for Disease Control and Prevention. 2020. Available at:https://www.cdc.gov/mentalhealth/learn/index.htm. Accessed August 27, 2020.

- 2.CDC. Data and Publications. Centers for Disease Control and Prevention. 2020. Available at:https://www.cdc.gov/mentalhealth/data_publications/index.htm. Accessed August 27, 2020.

- 3.Parks J, Svendsen D, Singer P, et al. Morbidity and Mortality in People With Serious Mental Illness. Alexandria, VA: National Association of State Mental Health Program Directors (NASMHPD) Medical Directors Council; 2006. [Google Scholar]

- 4.Li X, Ma J. Does mental health parity encourage mental health utilization among children and adolescents? Evidence from the 2008 Mental Health Parity and Addiction Equity Act (MHPAEA). J Behav Health Serv Res. 2020;47:38–53. [DOI] [PubMed] [Google Scholar]

- 5.American Academy of Child and Adolescent Psychiatry. Improving mental health services in primary care: reducing administrative and financial barriers to access and collaboration. Pediatrics. 2009;123:1248–1251. [DOI] [PubMed] [Google Scholar]

- 6.Haffajee RL, Mello MM, Zhang F, et al. Association of Federal Mental Health Parity Legislation with health care use and spending among high utilizers of services. Med Care. 2019;57:245–255. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Bose J, Hedden SL, Lipari RN, et al. Key Substance Use and Mental Health Indicators in the United States: Results From the 2017 National Survey on Drug Use and Health. Rockville, MD: US Department of Health and Human Services, Substance Abuse and Mental Health Services Administration, Center for Behavioral Health Statistics and Quality; 2018. [Google Scholar]

- 8.Barry CL, Busch SH. Do state parity laws reduce the financial burden on families of children with mental health care needs? Health Serv Res. 2007;42 (pt 1):1061–1084. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9.Harris KM, Carpenter C, Bao Y. The effects of state parity laws on the use of mental health care. Med Care. 2006;44:499–505. [DOI] [PubMed] [Google Scholar]

- 10.Thalmayer AG, Friedman SA, Azocar F, et al. The Mental Health Parity and Addiction Equity Act (MHPAEA) evaluation study: impact on quantitative treatment limits. Psychiatr Serv. 2017;68:435–442. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11.Horgan CM, Hodgkin D, Stewart MT, et al. Health plans’ early response to Federal Parity Legislation for Mental Health and Addiction Services. Psychiatr Serv. 2016;67:162–168. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12.Busch SH, Barry CL. New evidence on the effects of State Mental Health Mandates. Inquiry. 2008;45:308–322. [DOI] [PubMed] [Google Scholar]

- 13.Azrin ST, Huskamp HA, Azzone V, et al. Impact of full mental health and substance abuse parity for children in the Federal Employees Health Benefits Program. Pediatrics. 2007;119:e452–e459. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 14.Sturm R. State parity legislation and changes in health insurance and perceived access to care among individuals with mental illness: 1996–1998. J Ment Health Policy Econ. 2000;3:209–213. [DOI] [PubMed] [Google Scholar]

- 15.McGinty EE, Busch SH, Stuart EA, et al. Federal parity law associated with increased probability of using out-of-network substance use disorder treatment services. Health Aff (Millwood). 2015;34:1331–1339. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 16.Busch SH, Epstein AJ, Harhay MO, et al. The effects of federal parity on substance use disorder treatment. Am J Manag Care. 2014;20:76–82. [PMC free article] [PubMed] [Google Scholar]

- 17.Busch AB, Yoon F, Barry CL, et al. The effects of mental health parity on spending and utilization for bipolar, major depression, and adjustment disorders. Am J Psychiatry. 2013;170:180–187. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 18.Friedman S, Xu H, Harwood JM, et al. The Mental Health Parity and Addiction Equity Act evaluation study: impact on specialty behavioral healthcare utilization and spending among enrollees with substance use disorders. J Subst Abuse Treat. 2017;80:67–78. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19.Huskamp HA, Samples H, Hadland SE, et al. Mental health spending and intensity of service use among individuals with diagnoses of eating disorders following federal parity. Psychiatr Serv. 2018;69:217–223. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.Ettner SL, J MH, Thalmayer A, et al. The Mental Health Parity and Addiction Equity Act evaluation study: impact on specialty behavioral health utilization and expenditures among “carve-out” enrollees. J Health Econ. 2016;50:131–143. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21.Sipe TA, Finnie RKC, Knopf JA, et al. Effects of mental health benefits legislation: a community guide systematic review. Am J Prev Med. 2015;48:755–766. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 22.McGuire TG, Montgomery JT. Mandated mental health benefits in private health insurance. J Health Polit Policy Law. 1982;7:380–406. [DOI] [PubMed] [Google Scholar]

- 23.Klick J, Markowitz S. Are mental health insurance mandates effective? Evidence from suicides. Health Econ. 2006;15:83–97. [DOI] [PubMed] [Google Scholar]

- 24.Lang M. The impact of mental health insurance laws on state suicide rates. Health Econ. 2013;22:73–88. [DOI] [PubMed] [Google Scholar]

- 25.Wen H, Cummings JR, Hockenberry JM, et al. State parity laws and access to treatment for substance use disorder in the United States: implications for federal parity legislation. JAMA Psychiatry. 2013;70:1355–1362. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 26.Dave D, Mukerjee S. Mental health parity legislation, cost-sharing and substance-abuse treatment admissions. Health Econ. 2011;20:161–183. [DOI] [PubMed] [Google Scholar]

- 27.Bao Y, Sturm R. The effects of state mental health parity legislation on perceived quality of insurance coverage, perceived access to care, and use of mental health specialty care. Health Serv Res. 2004;39:1361–1377. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 28.Bureau of Labor Statistics U.S. Department of Labor. National Longitudinal Survey of Youth 1997 cohort, 1997-2017 (rounds 1-18). In: Produced and distributed by the Center for Human Resource Research (CHRR). Columbus, OH: The Ohio State University; 2019.

- 29.Douglas M Weber S Bass C, et al. Creation of a longitudinal legal dataset to support legal epidemiology studies of mental health insurance legislation. Psychiatr Serv. 2021. [DOI] [PubMed]

- 30.Bureau of Labor Statistics. National Longitudinal Survey of Youth 1997, Documentation on using and understanding the data, sample weights and design effects. Available at: https://www.nlsinfo.org/content/cohorts/nlsy97/using-and-understanding-the-data/sample-weights-design-effects. Accessed Februrary 14, 2021.

- 31.StataCorp. Stata Statistical Software: Release 16. College Station, TX: StataCorp LLC;; 2019. [Google Scholar]

- 32.Glied SA, Frank RG. Better but not best: recent trends in the well-being of the mentally ill. Health Aff (Millwood). 2009;28:637–648. [DOI] [PubMed] [Google Scholar]

- 33.Mark TL, Levit KR, Vandivort-Warren R, et al. Changes In US spending on Mental Health And Substance Abuse Treatment, 1986-2005, and implications for policy. Health Aff (Millwood). 2011;30:284–292. [DOI] [PubMed] [Google Scholar]

- 34.Merrick MT, Ports KA, Ford DC, et al. Unpacking the impact of adverse childhood experiences on adult mental health. Child Abuse Negl. 2017;69:10–19. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 35.Brown DW, Anda RF, Tiemeier H, et al. Adverse childhood experiences and the risk of premature mortality. Am J Prev Med. 2009;37:389–396. [DOI] [PubMed] [Google Scholar]

- 36.Walker ER, Cummings JR, Hockenberry JM, et al. Insurance status, use of Mental Health Services, and unmet need for Mental Health Care in the United States. Psychiatr Serv. 2015;66:578–584. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 37.Langheim FJ, Shim RS, Druss BG.Compton MT, Shim RS. Poor access to health care. The Social Determinants of Mental Health. Arlington, VA: American Psychiatric Publishing; 2015:213–234. [Google Scholar]

- 38.Townes DL, Chavez-Korell S, Cunningham NJ. Reexamining the relationships between racial identity, cultural mistrust, help-seeking attitudes, and preference for a Black counselor. J Couns Psychol. 2009;56:330–336. [Google Scholar]

- 39.Whaley AL. Cultural mistrust and mental health services for African Americans: a review and meta-analysis. Couns Psychol. 2001;29:513–531. [Google Scholar]

- 40.Hogan MF. The President’s New Freedom Commission: recommendations to transform mental health care in America. Psychiatr Serv. 2003;54:1467–1474. [DOI] [PubMed] [Google Scholar]

- 41.CDC. The ACE Study Survey Data [Unpublished Data] Atlanta, GA: US Department of Health and Human Services, Centers for Disease Control and Prevention; 2016. [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Supplemental Digital Content is available for this article. Direct URL citations appear in the printed text and are provided in the HTML and PDF versions of this article on the journal's website, www.lww-medicalcare.com.