Abstract

The dynamics of racial/ethnic wealth inequality among U.S. families with resident children (child households) have been understudied, a major oversight because of wealth’s impact on child development and intergenerational mobility. Using data from the Survey of Consumer Finances (2004–2016), the authors find that wealth gaps between black and white households are larger in, and have grown faster for, child households relative to the general population. In contrast, black-white income gaps for child households have remained largely unchanged. Wealth trends for black and Hispanic child households have diverged, and by 2016, Hispanic child households had more net worth than black child households. Between 2004 and 2016, home ownership rates and home equity levels for black child households decreased, while educational debt increased. In 2016, black child households had just one cent for every dollar held by non-Hispanic white child households. These findings depict the extreme wealth fragility of black child households.

Keywords: wealth, inequality, race, children

The United States is in the midst of an ongoing conversation about how to redress the consequences of slavery and discrimination and ameliorate current racial/ethnic inequalities across many domains, including household wealth. Wealth, a household’s asset’s minus its debts, is more unequally distributed in the United States than income and exhibits greater levels of racial/ethnic inequality (Wolff 2017). The Great Recession, from 2007 to 2009, led to a sharp uptick in racial/ethnic wealth inequality, and the economic recovery has been uneven, further hardening racial/ethnic disparities in wealth (Bricker et al. 2017; Wolff 2018).

In this article, we argue that racial gaps in wealth are larger than is realized for a key population of sociological and public policy interest: households with children. Wealth is critical to the life chances of children, as parental wealth operates throughout a child’s life course to shape future educational, employment, and family choices and opportunities (Killewald, Pfeffer, and Schachner 2017; Yellen 2016). Moreover, intergenerational wealth mobility is low, suggesting that children who come from low-wealth households have an increased likelihood of having children (and grandchildren) whose net worth is also low (Pfeffer and Killewald 2017).

Yet to date, studies of racial/ethnic differences in wealth have not focused specifically on households with resident children (hereafter child households) even though wealth inequality is rising faster among child households than among other household types (Gibson-Davis and Percheski 2018). Recent trends in child household wealth also show a sharp decline in wealth levels for those at the very bottom (Gibson-Davis and Percheski 2018), and many of these households are likely to be headed by parents of color. It therefore seems plausible, and even likely, that racial/ethnic disparities in wealth among children are larger than among the general population.

In this study, we provide the first analyses of racial/ethnic disparities in wealth focused on child households (defined as households with at least one resident child under the age 19). Households with minor children constituted 35 percent of U.S. households in 2016. Data come from five waves of the Survey of Consumer Finances (SCF), the premier source of wealth data in the United States. Focusing on child households with non-Hispanic white, black, or Hispanic household heads, we describe recent trends in racial/ethnic disparities in wealth. We examine racial/ethnic differences at multiple points in the wealth distribution, illuminating how wealth gaps among families at the bottom, middle, and top of the distribution changed between 2004 and 2016. We also consider how racial/ethnic gaps vary over time by home ownership and whether a family holds educational debt, the most common type of household asset and debt (Ratcliffe and McKernan 2013; Wolff 2017). We estimate models of both income and wealth to compare racial/ethnic gaps in each.

Our work makes several contributions to the literature. First, our analysis provides the first estimates of the extreme racial/ethnic wealth inequality that characterizes child households and documents that black-white wealth disparities are larger for child households than for the rest of the population at every point in the wealth distribution. Between 2004 and 2016, increases in black-white wealth disparities for child households also outpaced those of the general population. Second, we show that although black-white wealth gaps for child households have increased dramatically over our study period, black-white income gaps have remained stable, and that demographic changes among child households do not account for the growing racial wealth gaps. Third, our findings underscore the importance of considering Hispanic and black child households as distinct groups. Black child households now have lower wealth levels than Hispanic child households, a reversal of pre–Great Recession trends. Fourth, our description of patterns of debts and assets suggests that changes in home ownership rates and educational debt holdings have contributed to, but cannot fully explain, the decline in wealth among black child households. When considered together, our findings underscore the necessity of considering child households separately from other household types and call attention to the extreme level of racial/ethnic inequality in children’s resources in the United States.

Background

Most previous research focuses on racial/ethnic disparities in wealth for all households, irrespective of life stage or demographic composition. We argue, though, that for both theoretical and empirical reasons, child households merit their own analyses and that the lack of focus on families with children obscures important knowledge about the contours of racial/ethnic inequality in the United States.

A focus on wealth disparities among households with children, rather than on wealth disparities across the whole population, is warranted because of the centrality of wealth for child well-being, particularly human capital (education and skills) acquisition (Conley 2001; Elliott, Destin, and Friedline 2011; Yellen 2016). For children born in the 1980s, Pfeffer (2018) found that the college graduation rate for children whose parents are in the bottom quintile of wealth is 49 percentage points lower than that of children whose parents are in the top quintile for wealth (11 percent vs. 60 percent). In turn, having a four-year college degree leads to higher earnings and better adult health (Card 1999; Lochner 2011) and has been associated with the formation of more stable romantic unions (Isen and Stevenson 2011). Moreover, children’s levels of wealth in their families of origin influence the wealth level of their children (and that of their children’s children) (Pfeffer and Killewald 2017), suggesting that contemporaneous wealth disparities will only exacerbate future disparities in educational attainment.

Because there is a rich body of research on racial/ethnic wealth inequalities among the total population (inclusive of child households and childless households), we start with an overview of what is known about racial/ethnic differences in household wealth for the total population and the mechanisms that produce these inequalities. We then discuss how racial/ethnic inequalities and mechanisms may differ for child households and state the hypotheses that we test in this study.

Racial/Ethnic Differences in Household Wealth

In the United States, gaps in household wealth by race/ethnicity are extremely large and have not narrowed over time (Oliver and Shapiro 1995; Thompson and Suarez 2015). In 1983, the black-white median net worth ratio was .07 (indicating that black households had seven cents for every dollar of wealth that white households had); the Hispanic-white median net worth ratio was .04. In 2016 (the latest year available), the Hispanic-white ratio remained at .04, whereas the black-white ratio had fallen to .02 (Wolff 2017).

These statistics, however, belie the dynamic changes in relative wealth levels experienced by minority families. In the 1980s and 1990s, black and Hispanic households saw small but measurable improvements in their wealth levels relative to whites. The black-white wealth ratio peaked in 1992 at .17, and the Hispanic-white ratio peaked in 1995 at .08 (Wolff 2017). Beginning in the late 1990s and early 2000s, however, the wealth levels of minority households began to erode and then fell cataclysmically with the onset of the Great Recession in 2007 (McKernan et al. 2014). Between 2007 and 2013, white median wealth declined by 38 percent, whereas black median wealth declined by 529 percent and Hispanic wealth by 425 percent (authors’ calculations on the basis of estimates reported in Wolff 2017).

In the aftermath of the Great Recession, the wealth levels of black and Hispanic households have diverged. Median Hispanic wealth, though lower in 2016 than in 2004, has increased since the Great Recession ended. Hispanic-white disparities in wealth in 2016 were similar to what they were in 2004 and were roughly comparable to what they were in 1983 (Wolff 2018). Black households, in contrast, lost wealth during the Great Recession and have seen continued declines since it ended. As a result, black-white inequalities in wealth were larger in 2016 than in 2004 and were just as large as they were in the early 1980s (Wolff 2018).

Because black and Hispanic households have diverged in their post–Great Recession levels of wealth, the relative wealth standing of black and Hispanic households has been reversed (Wolff 2018). In the 1980s, 1990s, and early 2000s, Hispanic households had median wealth levels that were between one third and one half as high as those of black households. The wealth advantage of black households over Hispanic households, however, disappeared in the aftermath of the Great Recession. Since 2010, Hispanic household median wealth has doubled, whereas black household median wealth has been cut in half. As a result, black households in 2016 had median wealth levels that were one half as high as those of Hispanic households (Wolff 2018).

Racial/ethnic differences in wealth far exceed racial/ethnic differences in income. In 2016, black and Hispanic households had median household incomes that were 58 percent and 65 percent as high, respectively, relative to white median incomes. For median household wealth, those same figures were 2 percent for blacks and 4 percent for Hispanics (Wolff 2017). And whereas the net effect of the past few decades has been a worsening of black/white disparities in wealth, racial/ethnic disparities in income over the past few decades have remained relatively constant (Wolff 2017).

Factors Contributing to Racial and Ethnic Differences in Wealth

Beginning with the seminal work of Oliver and Shapiro (1995), scholars have identified a number of factors that contribute to large racial/ethnic gaps in wealth (Darity and Nicholson 2005; Pfeffer and Killewald 2019). First, different life trajectories—lower levels of human capital, weaker attachment to the labor market, poorer health, and less stable family structures—can lead to differences in income, which in turn affect asset accumulation (Shapiro, Meschede, and Osoro 2014). Notably, though, these demographic differences cannot fully explain wealth disparities. Holding such factors as age, education, and marital status constant, black and Hispanic households still have lower levels of wealth than white households (Altonji and Doraszelski 2005; Darity and Nicholson 2005; Oliver and Shapiro 1995). Second, racial discrimination impedes asset accumulation, as minority households historically and currently face bias in obtaining credit, purchasing homes, and securing loans (Shapiro et al. 2014; Thurston 2018). Third, many black and Hispanic adults come from families of origin with lower levels of wealth (Pfeffer and Killewald 2019). Black and Hispanic adults also receive less wealth from in vivo transfers and inheritances than do white adults (Oliver and Shapiro 1995; Rauscher 2016). Low levels of intergenerational wealth mobility in the United States mean that minority adults are unlikely to obtain a higher wealth class than they experienced as children (Killewald and Bryan 2018; Pfeffer and Killewald 2017). Fourth, high rates of incarceration, particularly among black men, impede wealth by lowering family incomes, imposing legal costs, and incurring debts (Sykes and Maroto 2016).

Racial/ethnic differences in wealth are exacerbated by home ownership patterns and policies (Killewald and Bryan 2016). Residential segregation results in black and Hispanic families’ occupying neighborhoods that have lower housing values and higher rates of vacancy and foreclosure (Massey 2015). Redlining—the designation of minority neighborhoods as financially risky areas, which mortgage lenders and insurance companies often used as grounds for rejecting mortgage applications (Thurston 2018)—has been replaced by “reverse redlining,” in which lenders target minority households for subprime loans and other predatory loan practices (Rugh and Massey 2010). Racially biased housing policies have contributed to minority families, relative to white families, being less likely to own a home, having homes of lower value, and receiving less return on their home ownership investments (Killewald 2013; Killewald and Bryan 2016; Shapiro et al. 2014). Notably, since the Great Recession ended, home ownership rates and home equity levels have increased for Hispanic households, but not for black households. Differences in home ownership patterns can partially explain why the wealth of Hispanic households, but not black households, has increased since 2010 (Wolff 2018).

Beyond home ownership, education debt is arguably the most important factor in racial/ethnic inequalities in wealth (Addo, Houle, and Simon 2016; Killewald and Bryan 2018). Since the 2000s, the level and amount of education debt has exploded, and it now lags behind only mortgage debt as the most common type of consumer loan (Ratcliffe and McKernan 2013). Black students, in part because their parents provide less tuition money, have taken on disproportionately more educational debt than have white students (Addo et al. 2016; Rauscher 2016). Moreover, black adults also receive lower returns on their educational investments. Repaying education debt often hampers wealth accumulation among black households and thus exacerbates the black-white disparity in wealth (Houle and Addo 2018; Killewald 2013; Zhan, Xiang, and Elliott 2016). Among young adults, education debt explains nearly one quarter of the black-white wealth gap (Houle and Addo 2018). The prevalence of education debt is more similar between Hispanic and (non-Hispanic) white working-age adults (Braga 2016) and may contribute relatively less to the Hispanic-white wealth gap.

Racial/Ethnic Differences in Wealth for Families with Children

Analyses that include all households may not reflect the levels of racial/ethnic wealth inequality among children, but whether the gaps between groups will be larger or smaller for child households is empirically unclear. The life-cycle hypothesis—that households save and spend at different rates on the basis of the age of the household head (Ando and Modigliani 1963)—suggests that levels of wealth for child households will be lower than for non–child households, insofar as child households are likely to be headed by younger individuals than non–child households.

How the life cycle translates into racial/ethnic wealth gaps is not as straightforward, however. If younger adults have low levels of assets, and if wealth trajectories diverge as people age (Killewald and Bryan 2018), then racial/ethnic wealth gaps may be smaller among parents with minor children who are typically in their twenties, thirties, and forties, than for households without children, which include older adults. Similarly, the birth cohorts under consideration here (those with resident children from 2004 to 2016) are more racially and ethnically diverse and exhibit more marital status heterogeneity relative to older cohorts. Higher proportions of racial minority households and fewer married household heads will decrease aggregate wealth levels for younger cohorts and will likely increase population-level wealth variability. Yet increased variability does not necessarily translate to an increased gap between racial/ethnic groups.

Children can affect wealth-building behaviors, including savings and investment strategies, employment choices, and home ownership (Maroto 2018). Households headed by parents have slightly higher levels of wealth than households headed by childless adults, but this wealth advantage of parenthood only holds for married couples (Percheski and Gibson-Davis 2019). Parental and marital status differ by race and ethnicity; non-Hispanic white adults, relative to black or Hispanic adults, are less likely to have children, but non-Hispanic white parents are more likely to be married than black or Hispanic parents (Umberson, Pudrovska, and Reczek 2010; Wang and Parker 2014). Thus, combining all households together—those with children and those without children—likely obscures racial/ethnic inequalities within population subgroups defined by parental status or family characteristics.

Previous research finds that wealth inequality among child households is rising faster than among other household types, with an increasing wealth polarization at the very top and bottom of the net worth distribution (Gibson-Davis and Percheski 2018). Between 1989 and 2013, wealth levels for child households in the top 1 percent of the wealth distribution increased by 156 percent, whereas wealth levels for child households in the bottom half of the wealth distribution decreased by 260 percent. In contrast, over the same time period, wealth levels for all households (including households with and without children), increased by 82 percent for the top 1 percent and decreased by 87 percent for the bottom half of the wealth distribution (Gibson-Davis and Percheski 2018). It seems plausible that this increasing wealth polarization among child households is correlated with the race/ethnicity of the household head. Thus, we hypothesize as follows:

Hypothesis 1: Wealth gaps are larger for child households than for households without resident children.

Additionally, on the basis of trends seen in the general population (Wolff 2018), we expect that black child households have experienced large declines in wealth and that black-white disparities in wealth have increased. Hispanic child households are likely to have lost wealth during the Great Recession, but disparities between Hispanic and white child households are unlikely to have grown.

Hypothesis 2: Black-white and black-Hispanic gaps in wealth among child households increased between 2004 and 2016.

Finally, given previous research finding that home ownership and educational debt are key predictors of wealth and also vary by race and ethnicity (Houle and Addo 2018; Killewald and Bryan 2018), we hypothesize as follows:

Hypothesis 3: Changes in rates of home ownership and holding educational debt partially account for increases in racial/ethnic wealth gaps among child households.

Data and Methods

Data

Our data are from the SCF, a cross-sectional study of U.S. households conducted by the Federal Reserve approximately every three years. The SCF is nationally representative of U.S. households when weighted and includes an oversample of high-income households. It is considered the best source of data on wealth at the household level for the United States (Keister 2014; Kennickell 2008; Wolff 2016). Data come from five waves of the SCF, collected in 2004, 2007, 2010, 2013, and 2016.1 All monetary estimates are presented in 2016 dollars.

The primary sample consisted of households in which the household (1) contained at least one member under the age of 18 and (2) had a household head who self-identified as non-Hispanic white, non-Hispanic black, or Hispanic. In some analyses, we compare this primary sample with households without minor children in residence. (Note that this category of “households without minor resident children” includes households with children under the age of 18 who live elsewhere as well as households with children who are older than 18 either living in the household or residing elsewhere.) Between 2004 and 2016, the fraction of households with minor resident children who were headed by a non-Hispanic white parent decreased (from 65 percent in 2004 to 55 percent in 2016), and the fraction of such households with black and Hispanic household heads increased from 14 percent (each) in 2004 to 17 percent (black) and 16 percent (Hispanic), respectively, in 2016.2

Measures

Net worth is defined as the sum total of a family’s fungible assets minus debts. Assets consisted of the value of the following 10 categories: the primary residence; other owned real estate; savings deposits, certificates of deposit, and money market accounts; checking accounts; government bonds and other financial securities; stocks and mutual funds; pension plans, including individual retirement accounts and 401(k) plans; surrender value of life insurance plans; equity in trust funds; and other miscellaneous assets not classified elsewhere. Six categories of debt were assessed, covering amount owed on primary residence, residential and building debt for other properties, credit card debt, educational debt, installment debt, and debt not classified elsewhere. (Medical debt was not specifically assessed but was classified into installment or the “other debt” category, depending on how it was paid.) Following Wolff (2011), we excluded the value of vehicles (whose resale value is far less than their consumption value) as well as the value of future pension and Social Security income (an asset that the household may realize in the future but does not currently possess). By including only assets that are readily convertible to cash, our measure of net worth reflects a household’s current holdings.

To account for economies of scale, we adjusted net worth (measured in 2016 dollars) by the square root of household size. On average, Hispanic households had slightly more household members (4.4) than did white (4.0) and black households (3.7) (see Appendix Table A1). Household size remained virtually constant over our time period for all three racial/ethnic groups; thus, changes in household size cannot explain our results.

Following Pfeffer and Killewald (2017), we measured levels of household wealth using their percentile rank in a weighted net worth distribution. Using the percentile rank of wealth, rather than a log of wealth, means that all households, even if they have negative wealth, can be included in one model (23 percent of households in our sample had negative net worth). Percentile net worth was calculated relative to all SCF households for each survey year.

For covariates in our regression models, we included the household head’s age (linear and squared terms), education, marital or partnership status, number of children, age of youngest child, presence of elderly adults, and income. Education consisted of five categories: no high school diploma, high school diploma (omitted category), some college, bachelor’s degree, and graduate degree. Marital or partnership status was a combination of marital or partnership status and gender of the household head, with five categories: married couple, cohabiting couple, never married mother, divorced mother, and single father.3 The number of children in the household was measured using a set of dichotomous indicators: one (the omitted category), two, and three or more. Another dichotomous variable indicated whether the oldest child in the household was younger than 6. The presence of at least one person older than 65 in the household was measured dichotomously.

Household income (measured in 2016 dollars) includes earnings, rents, alimony or child support, and all other types of income. It is divided by the square root of family size. Those without any household income were coded as 0.

Descriptive statistics of the sample (see Appendix Table A1) are as expected on the basis of past research, insofar as white household heads, relative to black and Hispanic household heads, were more likely to be married, had higher levels of education, and were slightly older. Racial/ethnic differences in household size and number of children were minimal, though Hispanic child households were slightly larger than the other two groups. Black child households were more likely than white and Hispanic child households to have an adult older than 64 in the household. Over time, within each racial/ethnic group, average educational levels increased, and a larger fraction of child households included elderly adults in the household. White child households (but not black and Hispanic child households) also became less likely to be headed by married individuals. Racial/ethnic differences in other demographic characteristics show little or no change over time.

Method

In the first part of the analysis, we produce a set of detailed descriptive statistics. For each racial/ethnic group and year, we calculate median income and net worth as well as median net worth for selected points in the wealth distribution (25th, 75th, and 90th percentiles). We graph trends in wealth ratios (using median net worth) between black and non-Hispanic white households and between Hispanic and non-Hispanic white households for households with resident children (our primary sample) as well as for all other households for the period of 2004 to 2016. We also show how changes over time in median wealth compare with changes in median income by racial/ethnic group, scaling changes to 2004.

In the second part of the analysis, we investigate how much of the racial/ethnic gaps in net worth and income can be explained by differences across groups in demographic and household characteristics. Specifically, we estimate the following ordinary least squares regression model as a baseline specification:

where PCTftr is an ordinal variable that corresponds to the position (1–99) that family f in time period t, rep r holds in the respective distribution (income or net worth). BLACKftr is a binary variable equal to 1 if the head of household for family f in time period t, rep r identifies as black and 0 otherwise, and HISPftr is a binary variable equal to 1 if the head of household for family f in time period t, rep r identifies as Hispanic and 0 otherwise. Xftr is a vector of family and household head characteristics. σt represents time period fixed effects, and εftr is a mean-zero random error term.

In the third part of the analysis, we examine asset and debt portfolios, including home ownership and education debt, by race/ethnicity and year to better understand racial differences in net worth. For each racial/ethnic group, we examine the holding of and total amount of assets and debts and then, for home ownership and education debt, the median amount of home equity or education debt. We also estimate models of percentile net worth separately for 2004 and 2016, using the same set of demographic covariates as in the previous models. For each year, we estimate models that include interactions between race/ethnicity and home ownership and models that include interactions between race/ethnicity and holding educational debt.

To account for the complex sampling and weighting design, we use the scfcombo command in Stata for all analyses. This command adjusts the standard errors appropriately.

Results

Wealth and Income Gaps by Household Type

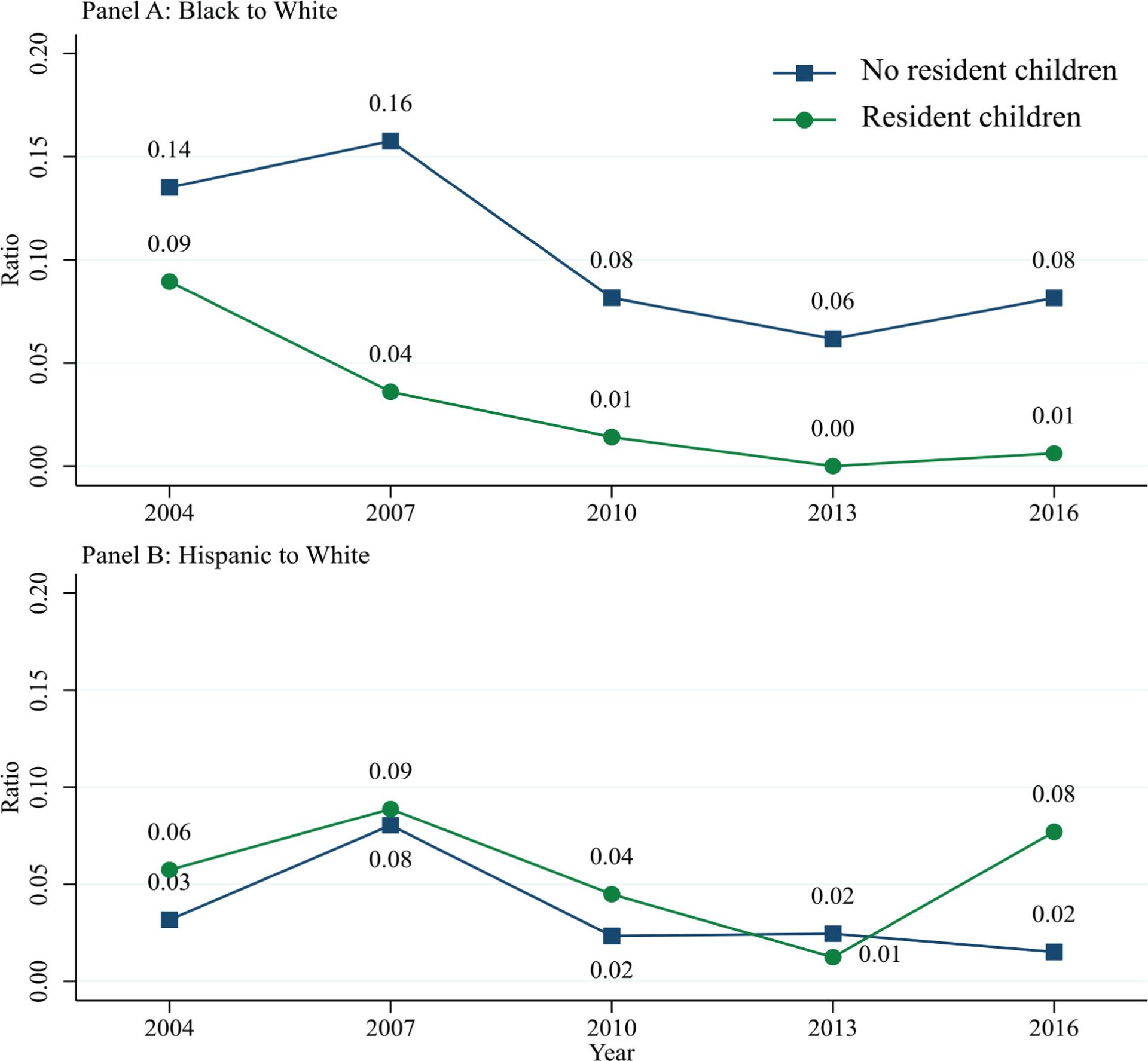

Consistent with hypothesis 1, the black-white wealth gap was larger for child households than for households without minor children for the entire period of 2004 to 2016 (Figure 1A). (We calculate the wealth gap between groups as the ratio of the median net worth for one group to the median net worth of another group.) In 2016, the median black household without children had just eight cents in wealth for every dollar in wealth held by non-Hispanic white households. Households with children had an even bigger racial wealth gap, as black child households had just one cent of wealth for every dollar of wealth for non-Hispanic white child households. Although the Great Recession and its aftermath exacerbated racial wealth inequality for both types of households, inequality among child households was increasing before 2007. Between 2004 and 2007, the black-white wealth ratio for child households fell from .09 to .04, whereas the black-white wealth ratio for households without resident children rose modestly from .14 to .16.

Figure 1.

Median wealth ratios, by presence of resident children.

Note: Ratios represent the ratio of median black (Hispanic) wealth to median white wealth for households of the same type.

The Hispanic-white wealth ratio, in contrast, showed smaller wealth gaps among child households than among other households. For four of the five survey years, child households had a slightly higher Hispanic-white wealth ratio (i.e., a smaller wealth gap) than did households without resident children. Hispanic households of both compositions had very little wealth compared with non-Hispanic white households; in 2016, Hispanic child households had eight cents for every dollar held by white child households, and Hispanic households without children had two cents for every dollar of wealth held by white households without children. For most years, the presence of children in the household did not differentiate wealth gaps as sharply for Hispanic households as it did for black households, and the Hispanic-white wealth ratio was extremely low, irrespective of whether the household had a resident child.

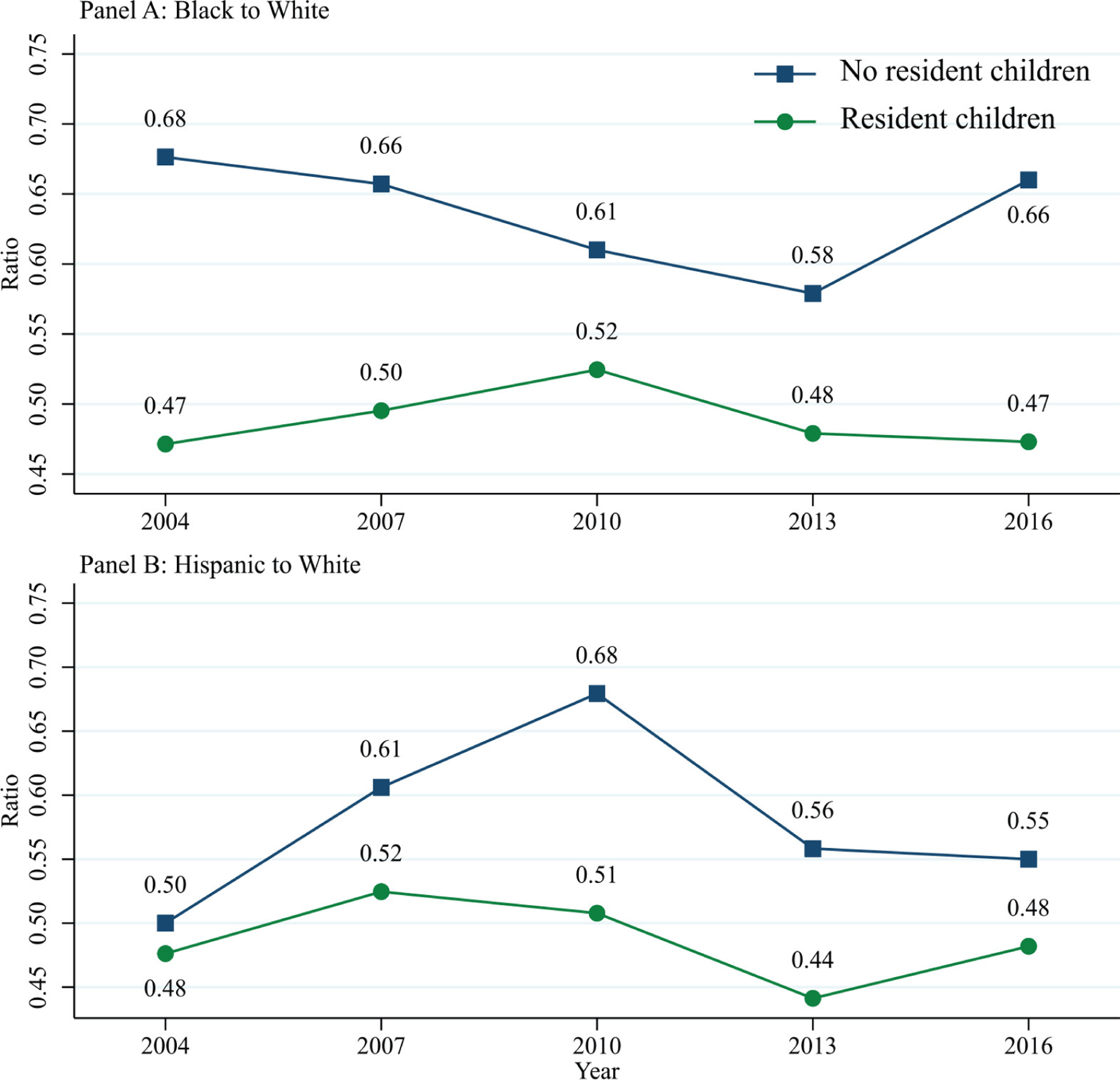

In additional analyses, we examined these same ratios for median income, rather than median wealth (see Appendix Figure A1). As with wealth, black-white income gaps were greater for child households than for households without children. In 2016, the black-white income ratio was .47 for child households and .66 for households without resident children. These ratios were virtually unchanged from 2004. Compared with the black-white wealth ratios (.01 and .08, respectively), these income ratios underscore how racial gaps in wealth are substantially larger than racial gaps in income.

In contrast to wealth gaps, Hispanic-white gaps in income were larger for child households than for households without children at every time point examined. In 2016, the Hispanic-white ratios were .48 and .55, respectively, for households with and without children; in 2004, the ratios were .48 and .50. The relatively small difference between the two ratios indicates that, as was found for wealth, Hispanic-white income gaps did not vary substantially by the presence of a child in the household.

Thus far, results show that black-white gaps in median wealth are larger for child households than for non–child households and that black-white wealth gaps have widened faster for child households than for households without a resident child. In contrast, Hispanic-white wealth gaps were similar across household types for most of the period examined, but in 2016 Hispanic-white wealth gaps for child households were smaller than for non–child households. For both black and Hispanic child households, gaps in wealth are far larger than gaps in income.

Race/Ethnicity Gaps for Child Households by Position in the Wealth Distribution

Because racial/ethnic gaps in wealth may exhibit a different pattern of change over time at different points in the distribution, we next examine racial/ethnic wealth disparities for child households among the least and most wealthy households (Table 1). We present wealth holdings by race/ethnicity for child households for 2004 (pre–Great Recession), 2010 (during the Great Recession), and 2016 (post–Great Recession) for the 25th percentile, median, and 75th and 90th percentiles of the wealth distribution. We include black-white, Hispanic-white, and black-Hispanic wealth gaps.

Table 1.

Household Wealth by Race/Ethnicity and Distributional Position for 2004, 2010, and 2016, Child Households.

| Level | Ratio | |||||

|---|---|---|---|---|---|---|

| Black | Hispanic | White | Black-White | Hispanic-White | Black-Hispanic | |

| 25th percentile | ||||||

| 2004 | 0 | 0 | 6,378 | — | — | — |

| 2010 | −1,914 | −393 | 191 | — | — | — |

| 2016 | −5,236 | −40 | 3,205 | — | — | — |

| 50th percentile | ||||||

| 2004 | 4,856 | 3,115 | 54,262 | .09 | .06 | 1.56 |

| 2010 | 420 | 1,335 | 29,496 | .01 | .05 | .31 |

| 2016 | 294 | 3,637 | 47,250 | .01 | .08 | .08 |

| 75th percentile | ||||||

| 2004 | 39,743 | 38,897 | 189,567 | .21 | .21 | 1.02 |

| 2010 | 26,792 | 30,712 | 145,185 | .18 | .21 | .87 |

| 2016 | 23,264 | 32,007 | 178,438 | .13 | .18 | .73 |

| 90th percentile | ||||||

| 2004 | 126,323 | 169,515 | 513,793 | .25 | .33 | .75 |

| 2010 | 72,399 | 71,914 | 486,819 | .15 | .15 | 1.01 |

| 2016 | 69,773 | 100,130 | 565,700 | .12 | .18 | .70 |

Note: Wealth has been adjusted for household size. All estimates weighted and in 2016 dollars. Child households are defined as those with residents younger than 19.

We find that racial/ethnic disparities in median wealth exist throughout the distribution. The black-white and Hispanic-white net worth ratios are smallest (indicating the biggest relative gaps) at the bottom of the wealth distribution, but the largest gaps in absolute dollars are at the 90th percentile. For example, in 2016 the black-white relative gap as indicated by the ratio was larger (.01) at the median than at the 90th percentile (.12), but the absolute gap in dollars was much smaller at the median ($46,956) than at the 90th percentile ($495,927).

The pattern of change over time in wealth gaps vis-à-vis white child households by position in the wealth distribution differs between Hispanic and black child households. During the Great Recession, Hispanic child households at the top of the wealth distribution lost the most wealth relative to white child households and regained less of their lost wealth than white families at the top of the distribution. Thus, wealth gaps between Hispanic and white families at the 75th and 90th percentiles were bigger in 2016 than in 2004. In contrast, Hispanic child households in the bottom and middle of the distribution had regained most of their lost wealth by 2016, whereas white families at the 25th percentile had recovered much less of their lost wealth. Thus, gaps between Hispanic and white families at the 25th and 50th percentile were smaller in 2016 than 2004. The story for black child households was less complex: between 2004 and 2016, black families lost wealth relative to white families at every percentile examined. Moreover, black child households did not recoup their pre–Great Recession levels of wealth.

Across the wealth distribution, the wealth gap between black child households and Hispanic child households has widened. In 2004, black families had similar or greater levels of wealth than Hispanics at the 25th, 50th, and 75th percentiles. By 2016, black child households had substantially lower levels of wealth than Hispanics at each of these points. Declines in black wealth vis-à-vis Hispanic wealth were substantial. In 2004, at the median, black child households had $1.56 in wealth for every $1 in wealth for Hispanic child households; by 2016, black child households had 8 cents. These disparities manifested themselves during the Great Recession, when black families lost proportionately more wealth than did Hispanic families. Disparities continued to grow after the recession as black families have continued to lose wealth, whereas Hispanic families have regained much of their lost wealth.

Finally, we note the bleak wealth holdings of black and Hispanic child households at the 25th percentile of the distribution. These families had $0 in wealth before the Great Recession and had negative net worth following the Great Recession. In 2016, black child households at the 25th percentile had a net worth of −$5,236.

Changes in Wealth versus Income for Child Households

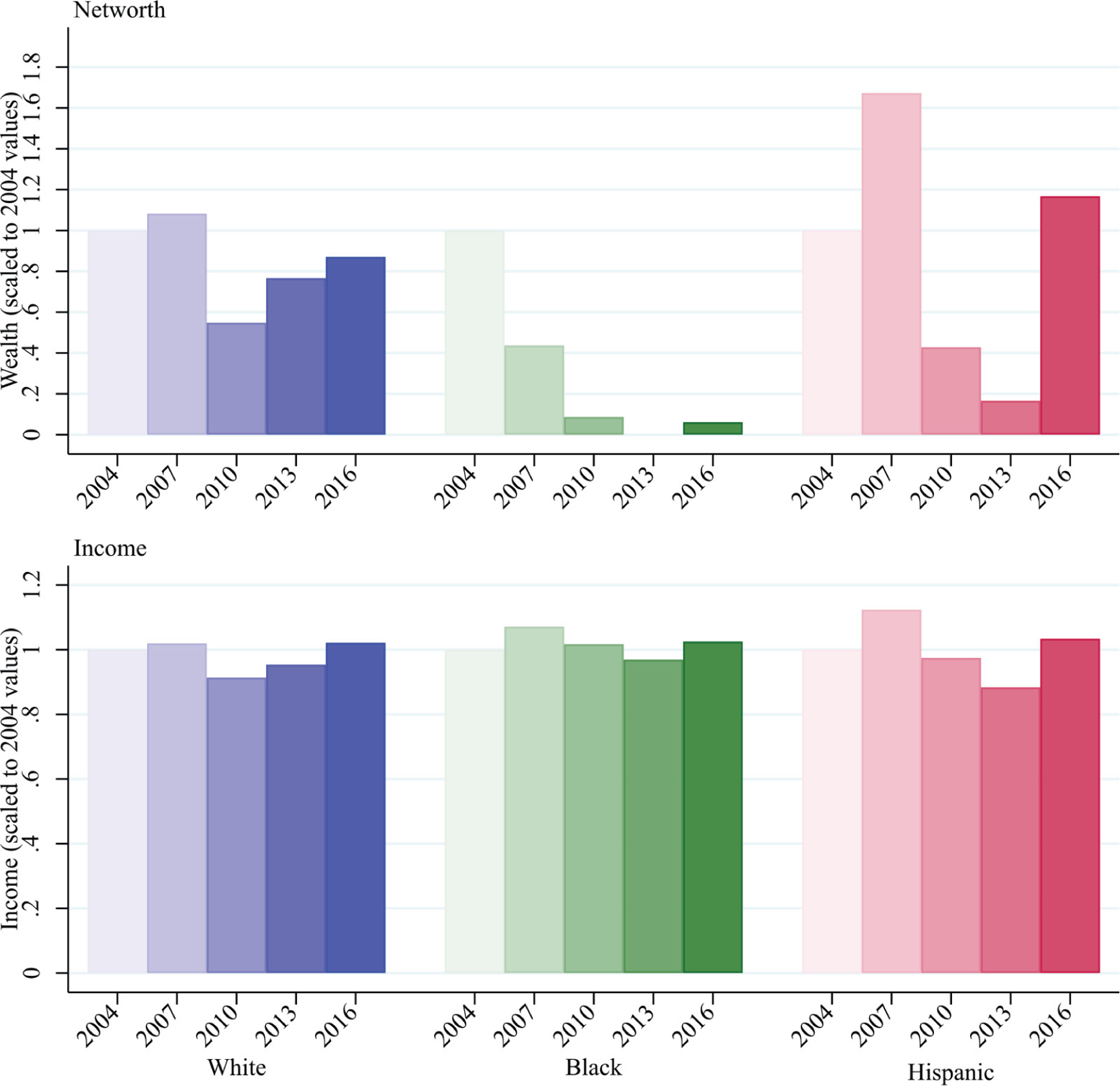

Our next set of analyses compares relative changes in wealth for child households by race and ethnicity between 2004 and 2016 to relative changes in income for child households. In the first set of results, we show a comparison of changes in wealth and income by race/ethnicity, with each variable measured in dollars and scaled to their 2004 values (Figure 2).

Figure 2.

Scaled changes in median household wealth and income, by race/ethnicity and year.

Note: These figures are for child households.

Changes in income for child households were quite modest and were dwarfed by changes in wealth. Each racial/ethnic group had about the same relative level of income in 2016 as it did in 2004 (Figure 2B), indicating that racial/ethnic disparities in income neither grew nor shrank over this time period. In contrast, changes in wealth for child households were quite large (Figure 2A). White and Hispanic families followed a similar pattern for median wealth: gains in 2007 relative to 2004, losses during the Great Recession years, and partial recovery in the post–Great Recession period. Black families, on the other hand, lost wealth even before the Great Recession began, suffered large losses during the Great Recession, and their wealth levels have yet to recover. The 2016 wealth levels of black child households are a fraction (approximately 1/15th) of what they were in 2004.

Descriptive statistics for the average over-time rank position of black, Hispanic, and non-Hispanic white child households in wealth and income are shown in Appendix Table A2. We examine rank positions in percentile wealth and income in a regression framework (Table 2). Each outcome variable was modeled as a function of race/ethnicity, year, and year-race/ethnicity interactions.4 Demographic characteristics, as described above, were included as covariates; their coefficients are available in Appendix Table A3. (Net worth models also include linear and squared terms for logged income).

Table 2.

Regressions on Percentile Net Worth and Percentile Income for Child Households, Including Interaction Terms between Year and Race/Ethnicity (n = 9,889).

| Percentile Net Worth | Percentile Income | |

|---|---|---|

| Race/ethnicity | ||

| White (reference) | ||

| Black | −5.91 (1.02)*** | −7.87 (1.39)*** |

| Hispanic | −4.01 (1.09)*** | −6.93 (1.35)*** |

| Other race | −1.69 (.54)** | −5.71 (.61)*** |

| Year | ||

| 2004 (reference) | ||

| 2007 | −1.33 (.67)* | .48 (.68) |

| 2010 | −1.25 (.75) | −1.30 (.64)* |

| 2013 | .20 (.84) | −.19 (.69) |

| 2016 | −.91 (.71) | −.26 (.72) |

| Interaction terms | ||

| Black × 2007 | 2.81 (1.70) | −1.68 (1.91) |

| Black × 2010 | .29 (1.52) | 1.53 (1.73) |

| Black × 2013 | −2.64 (1.33)* | −1.47 (1.61) |

| Black × 2016 | −3.39 (1.31)* | .68 (1.81) |

| Hispanic × 2007 | 2.29 (1.54) | −.28 (1.78) |

| Hispanic × 2010 | 1.60 (1.31) | −.52 (1.57) |

| Hispanic × 2013 | .64 (1.48) | −2.80 (1.49) |

| Hispanic × 2016 | −.21 (1.48) | −1.66 (1.57) |

Note: All estimates are weighted. Standard errors are in parentheses. Models control for relationship status, age, square of age, education of head, number of children in the household, whether the youngest child is younger than 6, and the presence of an elderly person in household. The model for percentile net worth controls for income (logged and squared).

p < .05.

p < .01.

p < .001.

Consistent with previous findings, black child households, compared with demographically similar non-Hispanic white child households, experienced over-time declines in wealth. At baseline in 2004, child households with black household heads were, on average, 5.91 percentiles lower in the net worth distribution than similar child households headed by non-Hispanic white household heads (p < .001). However, as indicated by the interaction terms, those wealth gaps substantially grew in 2013 and 2016 (B = −2.64 in 2013, B = −3.39 in 2016; p < .05 for both). By 2016, the wealth gap between black and white household heads with similar characteristics and incomes was 9.3 percentiles. Black-white disparities in income, however, were relatively static over time. In 2004, black child households were, on average, almost 8 percentiles lower on the income distribution than demographically similar white child households (p < .001). However, none of the black-by-year interaction terms approached statistical significance (and in two of the years, 2010 and 2016, the coefficient was signed positively, not negatively). Thus, results indicate no statistically significant or substantively large over-time change in black-white income gaps between households headed by demographically similar individuals.

Results for Hispanic child households suggest that their average position, relative to non-Hispanic white child households, in both the wealth and income distribution neither substantially worsened nor improved. Relative to demographically similar white child households, Hispanic child households in 2004 were 4.01 percentiles lower on the net worth distribution and 6.93 percentiles lower on the income distribution (p < .001 for both). These differences remained relatively constant over the time period, as the interaction terms between year and Hispanic identity for both wealth and income failed to reach conventional levels of statistical significance.

Asset and Debt Patterns for Child Households

To understand if growing racial gaps in wealth reflect changes in debts or assets (or both), we examined how debts and assets, including home ownership and educational debt, have changed over time. In the results we present, we concentrate on home ownership and education debt because they represent the most common and largest categories of assets and debts (excluding home-related debt) for child households. In additional analyses, we examined over-time changes in other mechanisms that might affect net worth, including the receipt of inheritances, savings behaviors, attitudes toward financial risk taking, ownership of other types of assets (e.g., retirement accounts), and holding other types of debts (e.g., credit card debt). We found that none of these exhibited substantial change over time or had an association with percentile net worth that differed substantially by race/ethnicity.

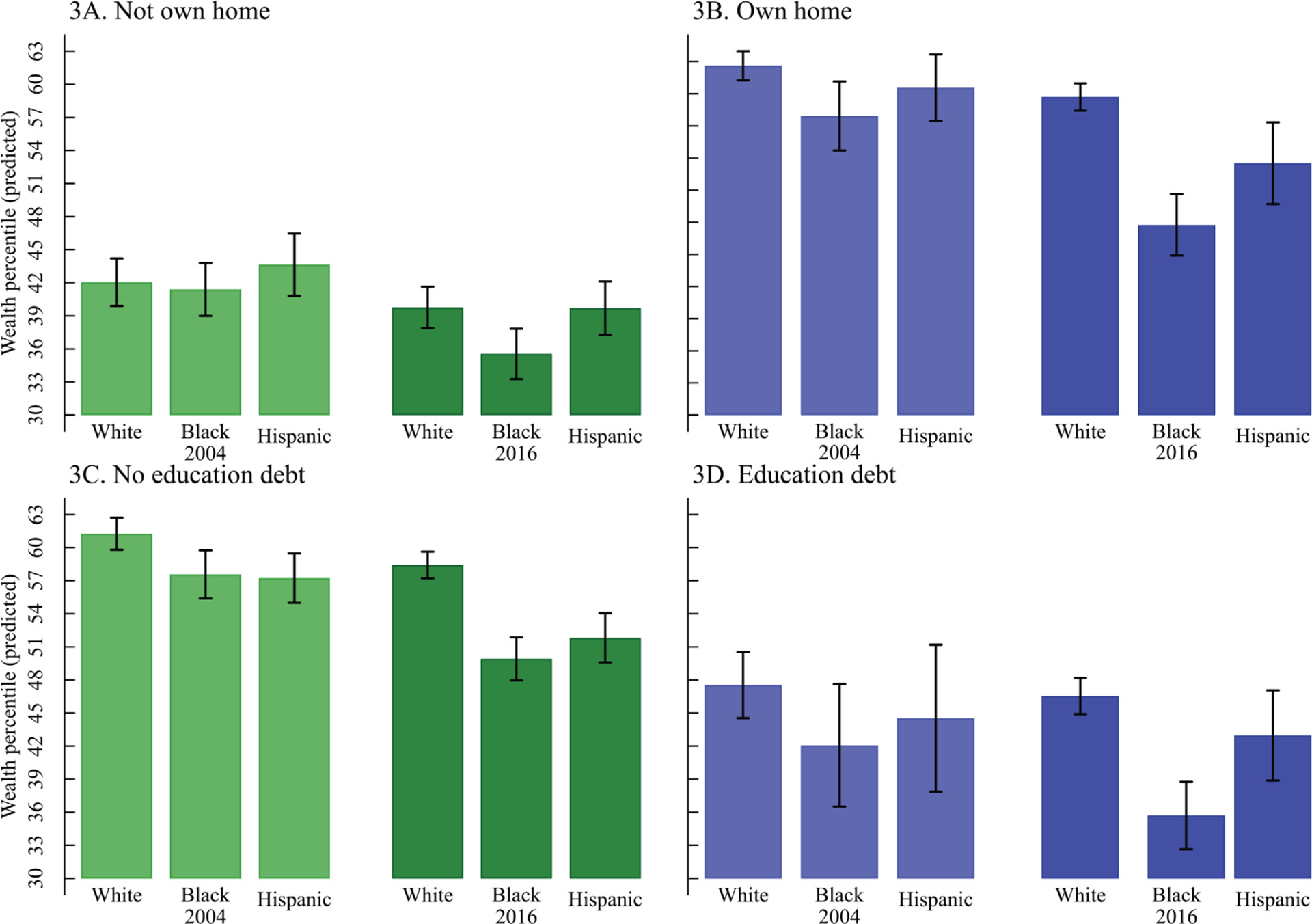

We begin with descriptive statistics on median assets and debts (Table 3) and then present predicted percentiles of net worth for whites, blacks, and Hispanics in models that include indicators of home ownership and educational debt (Figure 3). Models include interaction terms between race/ethnicity and either home ownership (Figures 3A and 3B) or having educational debt (Figures 3C and 3D). Model coefficients are available in Appendix Table A4.

Table 3.

Description of Assets and Debts for Child Households, by Race and Ethnicity, Select Years.

| Asset to Debt Ratio | Assets | Debt | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Any | Amount | Home Ownership | Any | Amount | Education | |||||

| Owns home | Equitya | Any | Amountb | |||||||

| White | 2004 | 1.90 | .97 | 254,102 | .78 | 85,209 | .92 | 133,537 | .19 | 13,990 |

| 2010 | 1.71 | .98 | 221,397 | .76 | 56,372 | .90 | 129,766 | .29 | 13,817 | |

| 2016 | 1.91 | .99 | 230,190 | .73 | 80,000 | .91 | 120,400 | .33 | 17,000 | |

| Black | 2004 | .75 | .87 | 32,456 | .48 | 40,697 | .74 | 43,241 | .19 | 9,538 |

| 2010 | .50 | .88 | 19,896 | .44 | 38,687 | .74 | 39,792 | .36 | 13,817 | |

| 2016 | .26 | .97 | 10,250 | .38 | 42,000 | .80 | 39,000 | .43 | 20,000 | |

| Hispanic | 2004 | .60 | .85 | 32,685 | .50 | 64,861 | .75 | 54,687 | .06 | 6,359 |

| 2010 | .85 | .90 | 28,042 | .50 | 40,897 | .75 | 33,160 | .14 | 8,953 | |

| 2016 | 1.15 | .98 | 40,000 | .47 | 54,000 | .78 | 34,800 | .19 | 16,000 | |

Note: Amounts represent medians. Estimates are weighted.

Among households that own the home.

For households with education (or credit card) debt.

Figure 3.

Predicted percentile net worth by home ownership and educational debt status among child households.

Note: Models control for relationship status, age, square of age, education of head, number of children in the household, whether the youngest child is younger than 6, the presence of an elderly person in the household, and income (logged and squared). Bars represent 95 percent confidence intervals.

From descriptive statistics (Table 3), we highlight the diverging asset and debt patterns of black child households compared with other child households in two respects.5 First, black child households differ from white and Hispanic child households insofar as they were the only racial/ethnic subgroup whose asset-to-debt ratio declined. Driven by a large decrease in assets, the asset-to-debt ratio for black child households fell from $0.75 in 2004 to $0.26 in 2016. In contrast, the asset-to-debt ratio for white child households remained relatively constant, and the asset-to-debt ratio for Hispanic child households increased over time, $0.60 in 2004 to $1.15 in 2016. The increase in the asset-to-debt ratio for Hispanic child households was the result of increases in assets (from $32,685 in 2004 to $40,000 in 2016) as well as declines in debt ($54,687 in 2004 and $34,800 in 2016). Second, black child households, in contrast to white and Hispanic child households, had larger changes in both home ownership and education debt. Between 2004 and 2016, all racial/ethnic subgroups experienced declines in the share of child households that owned homes and increases in the share of child households with education debt. However, black child households experienced more substantial changes in each. In 2016, black child households were still the least likely to own a home (38 percent), still had the lowest levels of home equity ($42,000), now had the highest share that held education debt (43 percent), and now had the largest amount owed on that debt ($20,000).

Declines in black home ownership rates and increases in the share of black child households holding educational debt, however, cannot by themselves account for increasing racial gaps in wealth. In Figure 3, we show predicted percentiles net worth from regression models run separately by year (for 2004 and 2016) with interactions between race/ethnicity and home ownership (Figures 3A and 3B) and race/ethnicity and educational debt (Figures 3C and 3D). As expected, child households who rented their homes and had education debt had lower wealth. Black child households that did not own homes or that had educational debt had the lowest predicted percentile net worth. Notably, though, we find that there were larger black-white gaps in percentile net worth in 2016 than in 2004 across the board: among homeowners and among renters, among child households with educational debt and those with no educational debt. Black-Hispanic gaps for child households across all comparison groups were also larger in 2016 than in 2004. Interestingly, the largest decrease in predicted wealth between 2004 and 2016 across the 12 subgroups (3 racial/ethnic categories × home ownership × educational debt) were for black homeowners: a decline of 10 percentiles. In sum, gaps in wealth for black child households, relative to white child households and to Hispanic child households, increased regardless of changes in home ownership or education debt.

Our study is descriptive, and our estimates are not causal. Moreover, though our regression models included a rich set of demographic covariates, estimates are likely biased by unobserved and omitted variables. The SCF oversampled high-income households and may not have as accurately captured the wealth levels for lower income households. Given differences in the income distribution by race/ethnicity, this suggests that our estimates likely understate the true racial/ethnic wealth gap.

Conclusions

Amid an ongoing debate about how to reduce racial/ethnic disparities in economic resources, this study focuses on wealth among households with children, a household type of policy interest that has largely been overlooked in the wealth inequality literature. Having sufficient levels of wealth is widely regarded as critical to the flourishing of children (Yellen 2016), but studies to date on racial/ethnic gaps in wealth have combined all household types together, likely understating the extent of racial/ethnic inequalities in children’s resources.

Consistent with hypothesis 1, our results indicate that black-white wealth gaps are larger for child households (households with resident children) than for other household types. Black households without resident children still have wealth levels far below those of similarly configured white households: at the median, about 8 cents on the dollar relative to non-Hispanic white wealth. But this racial wealth gap for households without children is far surpassed by the staggering size of the racial wealth gap among child households. In 2016, non-Hispanic white child households had a median wealth of $47,250, whereas black child households had a median wealth of $294. Expressed as a ratio, black child households had 1 cent of median wealth for every dollar of wealth held by non-Hispanic white child households.

Our findings show, however, that Hispanic-white wealth gaps were similar for households with resident children and for households without children for most of the period between 2004 and 2016. Moreover, in most years observed, there was a smaller Hispanic-white wealth gap for child households than for non–child households.

Why are black-white wealth gaps so much larger for child households, relative to households without children, whereas the same does not hold for Hispanic-white wealth gaps?

We cannot fully answer this question, but our analysis reveals a few pieces of the puzzle. First, differences in wealth by household type (i.e., between child households and households without children) are less stark for Hispanic households than for white and black households. Second, Hispanic households without children had extremely low levels of wealth, lower than black households without children. We suspect that the immigration status of Hispanic household heads may differ between child households and childless households and that immigrant Hispanic households without resident children may be remitting wealth to children or relatives in their country of origin (Flippen forthcoming). Additionally, households headed by Hispanic immigrants may have different patterns of investments and risk taking than households with U.S.-born household heads. Unfortunately, the SCF lacks information on immigration status, parental nativity, and immigration dates, so we cannot investigate how much of the low average wealth of Hispanic households without children is explained by immigration-related factors.

Our results also show that black-white gaps in wealth among child households have increased over time, consistent with hypothesis 2. Throughout the wealth distribution, Black child households saw declines in wealth vis-à-vis the relative wealth position of white child households. White child households (as well as Hispanic child households) lost wealth during the Great Recession (2007–2009) and its immediate aftermath (2010–2013). However, between 2013 and 2016, white child households increased their wealth, whereas black child households lost wealth, leading to larger racial gaps in wealth in 2016 than in 2004.

Hispanic-white wealth gaps among child households show a different pattern. Wealth gaps (measured as a ratio or in absolute dollars) at the median and 25th percentile were slightly smaller in 2016 than in 2004. Hispanic-white wealth gaps at the 90th percentile, however, were larger in 2016 than in 2004.

As for the general population (Wolff 2018), the relative wealth position of black and Hispanic child households has reversed since 2004. In 2016, black child households throughout the wealth distribution had substantially lower levels of wealth than did Hispanic child households. At the median, for example, black child households had wealth levels in 2016 that were 94 percent lower than their 2004 levels, while Hispanic child household wealth levels were 17 percent higher in 2016 than in 2004.

Part of the reversal in the wealth position of black and Hispanic child households may stem from changes in home ownership (Wolff 2018). In the Great Recession and its aftermath, the share of Hispanic child households that owned homes remained relatively constant, whereas the share of black child households that owned homes declined by nearly one fifth. Hispanic child households also had higher levels of home equity than did black child households. We also document large increases in education debt for black child households.

Changes in the rates of home ownership rates and holding educational debt were not enough to completely explain why black-Hispanic and black-white wealth disparities for child households grew over time, however. We also found large declines in predicted wealth among black homeowners, consistent with recent work indicating declining returns on home ownership for black households (Killewald and Bryan 2016). Nevertheless, wealth gaps increased between black child households and white and Hispanic child households with the same home ownership status and educational debt status.

Black child households did not experience similar declines in income, and racial gaps in income remained large but relatively constant between 2004 and 2016. (Hispanic-white disparities in income also did not change.) The stability in racial/ethnic income gaps alongside growth in black-white wealth gaps underscores the distinctiveness of wealth inequality and suggests the need for policy solutions that specifically target wealth. For example, policy makers should consider targeting discrimination in housing and mortgage markets, reducing racial residential segregation, and addressing inequalities in financing higher education.

Racial/ethnic gaps in wealth are extremely large. Gaps between black children and both white and Hispanic children are growing. Given low levels of intergenerational wealth mobility and the importance of wealth in human capital acquisition (Pfeffer 2018; Pfeffer and Killewald 2017), the wealth fragility of today’s black families with children will likely impede social mobility for generations to come.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Science Foundation (award 1459631).

Author Biographies

Christine Percheski, PhD, is an associate professor of sociology and faculty fellow at the Institute for Policy Research at Northwestern University. Her research investigates how changes in family demography are intertwined with economic inequality in the United States, with a focus on women and children.

Christina Gibson-Davis, PhD, is a professor of public policy and sociology at Duke University and a faculty affiliate of the Center for Child and Family Policy. Her recent work centers on describing the contours of wealth inequality among families with children and identifying the likely repercussions of wealth scarcity for child well-being.

Appendix

Figure A1.

Income ratios, by presence of resident children.

Table A1.

Descriptive Statistics of Demographic and Social Characteristics for Child Households, by Race and Ethnicity.

| All Years | 2004 | 2016 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| White | Black | Hispanic | White | Black | Hispanic | White | Black | Hispanic | |

| Marital status | |||||||||

| Married | .72 | .33 | .60 | .76 | .30 | .57 | .69 | .29 | .57 |

| Cohabiting | .08 | .11 | .16 | .06 | .09 | .17 | .10 | .14 | .18 |

| Divorced/widowed | .12 | .22 | .12 | .11 | .26 | .14 | .12 | .21 | .12 |

| Never married | .03 | .29 | .09 | .04 | .30 | .07 | .04 | .32 | .09 |

| Single father | .04 | .04 | .03 | .03 | .05 | .04 | .04 | .04 | .04 |

| Education | |||||||||

| No high school | .06 | .11 | .39 | .07 | .17 | .42 | .06 | .15 | .42 |

| High school | .31 | .37 | .34 | .31 | .38 | .36 | .25 | .32 | .27 |

| Some college | .26 | .32 | .16 | .27 | .27 | .13 | .27 | .30 | .15 |

| Bachelor’s | .23 | .12 | .07 | .21 | .12 | .06 | .27 | .14 | .12 |

| Graduate degree | .14 | .08 | .03 | .14 | .08 | .03 | .15 | .09 | .04 |

| Age (y) | 41.5 (10.4) | 40.4 (12.5) | 39.1 (10.3) | 40.1 (9.5) | 40.3 (11.9) | 37.8 (9.3) | 42.1 (11.2) | 41.2 (13.4) | 41.1 (10.5) |

| Household size | 4.0 (1.2) | 3.7 (1.4) | 4.4 (1.1) | 3.9 (1.1) | 3.7 (1.3) | 4.3 (1.4) | 3.9 (1.2) | 3.7 (1.2) | 4.3 (1.3) |

| Number of children | 1.9 (1.0) | 1.9 (1.1) | 2.0 (1.0) | 1.8 (.9) | 1.9 (1.1) | 2.1 (1.0) | 1.9 (.9) | 1.9 (.9) | 2.0 (1.0) |

| Oldest child <6 y | .28 | .24 | .26 | .27 | .21 | .28 | .30 | .22 | .22 |

| Adult >64 y in household | .04 | .07 | .06 | .03 | .05 | .06 | .06 | .11 | .08 |

| Sample sizes | 6,334 | 1,293 | 1,263 | 1,156 | 190 | 199 | 1,252 | 299 | 288 |

Note: Estimates are weighted. Standard deviations are in parentheses.

Table A2.

Percentile Net Worth and Percentile Income for Child Households by Year and Race/Ethnicity.

| Wealth | Income | |||||

|---|---|---|---|---|---|---|

| White | Black | Hispanic | White | Black | Hispanic | |

| 2004 | 48.1 (27.1) | 30.6 (20.0) | 31.9 (22.0) | 54.7 (27.1) | 30.7 (20.0) | 31.9 (22.0) |

| 2007 | 47.4 (27.8) | 32.1 (23.4) | 33.3 (23.0) | 53.9 (27.3) | 31.9 (23.4) | 33.8 (23.0) |

| 2010 | 47.2 (27.2) | 30.5 (19.7) | 32.7 (18.8) | 53.0 (27.8) | 34.1 (19.7) | 31.5 (27.8) |

| 2013 | 49.2 (27.7) | 28.2 (20.1) | 31.8 (18.8) | 55.4 (27.7) | 32.3 (20.1) | 30.3 (18.8) |

| 2016 | 49.7 (27.2) | 28.6 (20.2) | 33.4 (19.6) | 55.2 (27.2) | 33.2 (20.2) | 33.0 (19.6) |

| Across years | 48.3 (27.4) | 29.9 (20.8) | 32.6 (20.4) | 54.4 (27.4) | 32.5 (24.7) | 32.1 (22.7) |

| Sample size | 6,334 | 1,293 | 1,263 | 6,334 | 1,293 | 1,263 |

Note: Standard deviations are in parentheses.

Table A3.

Coefficients for Wealth Interaction Models (n = 9,889).

| Percentile Net Worth | Percentile Income | |

|---|---|---|

| Marital status | ||

| Married (reference) | ||

| Cohabiting | −3.63 (.54)*** | −6.80 (.67)*** |

| Divorced | −3.47 (.54)*** | −21.35 (.48)*** |

| Never married | .03 (.62) | −21.74 (.62)*** |

| Single father | −.69 (.96) | −13.73 (1.21)*** |

| Age | .63 (.02)*** | .44 (.03)*** |

| Age squared | .00 (.00)* | −.02 (.00)*** |

| Education | ||

| No high school | −.36 (.45) | −11.45 (.54)*** |

| High school (reference) | ||

| Some college | −.93 (.46)* | 7.98 (.43)*** |

| BA | 5.53 (.60)*** | 21.22 (.64)*** |

| More than BA | 6.72 (.65)*** | 29.09 (.65)*** |

| Number of children | ||

| 1 (reference) | ||

| 2 | 1.07 (.37)** | −3.10 (.35)*** |

| ≥3 | 1.87 (.43)*** | −10.33 (.51)*** |

| Oldest child <6 y | −.79 (.41) | −1.40 (.53)** |

| Adult >64 y in household | 1.58 (.82) | −1.34 (1.12) |

| Income (logged) | −17.41 (.88)*** | |

| Squared income (logged) | 1.49 (.04)*** |

Note: All estimates are weighted. Standard errors are in parentheses.

p < .05.

p < .01.

p < .001.

Table A4.

Coefficients for Figure 3 Models.

| Home Ownership: 2004 | Home Ownership: 2016 | Education Debt: 2004 | Education Debt: 2016 | |

|---|---|---|---|---|

| Home ownership | 20.6 (1.18)*** | 19.9 (.93)*** | ||

| Home ownership × black | −4.03 (2.39) | −7.71 (1.76)*** | ||

| Home ownership × Hispanic | −3.63 (1.99) | −6.11 (2.42)* | ||

| Education debt | −13.72 (1.58)*** | −11.88 (.97)*** | ||

| Education debt × black | −1.78 (3.30) | −2.33 (1.90) | ||

| Education debt × Hispanic | 1.00 (3.98) | 3.03 (2.31) | ||

| Race/ethnicity | ||||

| White (reference) | ||||

| Black | −.66 (1.21) | −4.22 (1.10)*** | −3.69 (1.25)** | −8.51 (1.03)*** |

| Hispanic | 1.59 (1.34) | −.06 (1.17) | −4.02 (1.04)*** | −6.60 (1.12)*** |

| Other race | 4.16 (1.61)* | .48 (1.11) | .14 (1.85) | −2.43 (1.20)* |

| Marital status | ||||

| Married (reference) | ||||

| Cohabiting | 2.23 (1.45) | .30 (1.13) | −1.92 (1.58) | −3.47 (1.06)** |

| Divorced | −1.21 (1.06) | .17 (.80) | −4.92 (1.21)*** | −3.49 (1.01)** |

| Never married | 6.53 (1.45)*** | 7.20 (1.08)*** | −.30 (1.58) | 3.14 (1.18)** |

| Single father | −2.98 (1.89) | 4.71 (1.52)** | −3.27 (2.09) | .05 (1.62) |

| Age | .58 (.06)*** | .43 (.04)*** | .71 (.06)*** | .49 (.04)*** |

| Age squared | .00 (.00) | .00 (.00) | −.01 (.00)*** | .00 (.00) |

| Education | ||||

| No high school | −.89 (1.19) | .74 (.89) | −2.34 (1.12)* | −2.40 (.95)* |

| High school (reference) | ||||

| Some college | −1.14 (.93) | −3.31 (.91)*** | 1.04 (1.04) | −1.30 (.92) |

| BA | 3.20 (1.26)* | 4.09 (1.12)*** | 7.22 (1.19)*** | 7.28 (1.13)*** |

| More than BA | 3.51 (1.72)* | 3.80 (1.30)** | 7.22 (1.67)*** | 7.50 (1.34)*** |

| Number of children | ||||

| 1 (reference) | ||||

| 2 | .83 (1.03) | 1.87 (.68)** | .52 (.95) | 1.84 (.69)** |

| ≥3 | 1.53 (1.06) | 1.91 (.76)* | 1.92 (1.04) | 2.01 (.86)* |

| Adult >64 y in household | .95 (2.33) | 1.60 (1.37) | 5.09 (2.37)* | 1.27 (1.52) |

| Oldest child <6 y | 1.70 (1.10) | −.53 (.88) | 2.57 (1.02)* | −1.64 (.86) |

| Income (logged) | −18.0 (2.82)*** | −12.7 (5.39)* | −17.3 (2.78)*** | −14.4 (3.99)*** |

| Squared income (logged) | 1.47 (.14)*** | 1.15 (.25)*** | 1.50 (.14)*** | 1.29 (.19)*** |

| Sample size | 1,646 | 2,102 | 1,646 | 2,102 |

Note: All estimates are weighted. Standard errors are in parentheses.

p < .05.

p < .01.

p < .001.

Footnotes

We chose 2004 as the base year it because it was the SCF wave that was closest to, but did not overlap with, the onset of the Great Recession (which occurred between 2007 and 2009). As the Great Recession exacerbated racial wealth disparities for the total population (Pfeffer, Danziger, and Schoeni 2013; Wolff 2018), we chose a baseline year for our analyses of child households that was prior to the Great Recession’s onset. Using waves prior to the 2004 (e.g., 2001 or 1998) as the baseline does not substantially change our results.

Households headed by persons of “other” race/ethnicity increased from 7 percent in 2004 to 13 percent in 2016.

Widowed heads were included with divorced mother households. Married and cohabiting couples include both different-sex and same-sex couples.

In a robustness check, we substituted logged income for percentile income and used the same model as described earlier. The pattern of results for race/ethnicity variables did not change.

The increase in the share of black and Hispanic households that reported assets between 2010 and 2016 is driven by an increase in the share of households with money in checking accounts.

References

- Addo Fenaba R., Houle Jason N., and Simon Daniel. 2016. “Young, Black, and (Still) in the Red: Parental Wealth, Race, and Student Loan Debt.” Race and Social Problems 8(1):64–76. [PMC free article] [PubMed] [Google Scholar]

- Altonji Joseph G., and Doraszelski Ulrich. 2005. “The Role of Permanent Income and Demographics in Black/White Differences in Wealth.” Journal of Human Resources 40(1):1–30. [Google Scholar]

- Ando Albert, and Modigliani Franco. 1963. “The ‘Life Cycle’ Hypothesis of Saving: Aggregate Implications and Tests.” American Economic Review 53(1):55–84. [Google Scholar]

- Braga Breno. 2016. “Racial and Ethnic Differences in Family Student Loan Debt.” Retrieved March 22, 2020. https://www.urban.org/sites/default/files/publication/82896/2000876-Racial-and-Ethnic-Differences-in-Family-Student-Loan-Debt.pdf.

- Bricker Jesse, Dettling Lisa J., Henriques Alice, Hsu Joanne W., Jacobs Lindsay, Moore Kevin B., Sabelhaus John, Thompson Jeffrey, and Windle Richard A.. 2017. “Changes in U.S. Family Finances from 2013 to 2016: Evidence from the Survey of Consumer Finances.” Federal Reserve Bulletin 100(3):1–42. [Google Scholar]

- Card David. 1999. “The Causal Effect of Education on Earnings.” Pp. 1801–1863 in Handbook of Labor Economics (Vol. 3). New York: Elsevier. [Google Scholar]

- Conley Dalton. 2001. “Capital for College: Parental Assets and Postsecondary Schooling.” Sociology of Education 74(1):59–72. [Google Scholar]

- Darity William A. Jr., and Nicholson Melba J.. 2005. “Racial Wealth Inequality and the Black Family.” Pp. 78–85 in African American Family Life: Ecological and Cultural Diversity), edited by McLoyd VC, Hill NE, and Dodge KA. New York: Guilford. [Google Scholar]

- Elliott William III, Mesmin Destin, and Terri Friedline. 2011. “Taking Stock of Ten Years of Research on the Relationship between Assets and Children’s Educational Outcomes: Implications for Theory, Policy and Intervention.” Children and Youth Services Review 33(11):2312–28. [Google Scholar]

- Flippen CA Forthcoming. “The Uphill Climb: A Transnational Perspective on Wealth Accumulation among Latino Immigrants in Durham, NC.” Journal of Ethnic and Migration Studies. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Gibson-Davis, Christina M, and Christine Percheski. 2018. “Children and the Elderly: Wealth Inequality among America’s Dependents.” Demography 55(3):1009–32. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Houle Jason N., and Addo Fenaba R.. 2018. “Racial Disparities in Student Debt and the Reproduction of the Fragile Black Middle Class.” Sociology of Race and Ethnicity 5(4):562–77. [Google Scholar]

- Isen Adam, and Stevenson Betsey. 2011. “Women’s Education and Family Behavior: Trends in Marriage, Divorce and Fertility.” Pp. 107–142 in Demography and the Economy), edited by Shoven JB. Chicago: University of Chicago Press. [Google Scholar]

- Keister Lisa A. 2014. “The One Percent.” Annual Review of Sociology 40:347–67. [Google Scholar]

- Kennickell Arthur B. 2008. “The Role of Over-sampling of the Wealthy in the Survey of Consumer Finances.” Irving Fisher Committee Bulletin 28:403–408. [Google Scholar]

- Killewald Alexandra. 2013. “Return to Being Black, Living in the Red: A Race Gap in Wealth That Goes beyond Social Origins.” Demography 50(4):1177–95. [DOI] [PubMed] [Google Scholar]

- Killewald Alexandra, and Bryan Brielle. 2016. “Does Your Home Make You Wealthy?” RSF: The Russell Sage Foundation Journal of the Social Sciences 2(6):110–28. [Google Scholar]

- Killewald Alexandra, and Bryan Brielle. 2018. “Falling Behind: The Role of Inter-and Intragenerational Processes in Widening Racial and Ethnic Wealth Gaps through Early and Middle Adulthood.” Social Forces 97(2):705–40. [Google Scholar]

- Killewald Alexandra, Pfeffer Fabian T., and Schachner Jared N.. 2017. “Wealth Inequality and Accumulation.” Annual Review of Sociology 43:379–404. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Lochner Lance. 2011. “Non-Production Benefits of Education: Crime, Health, and Good Citizenship.” NBER Working Paper No. 16722. Retrieved March 22, 2020. https://www.nber.org/papers/w16722.pdf. [Google Scholar]

- Maroto Michelle. 2018. “Saving, Sharing, or Spending? The Wealth Consequences of Raising Children.” Demography 55(6):2257–82. [DOI] [PubMed] [Google Scholar]

- Massey Douglas S. 2015. “The Legacy of the 1968 Fair Housing Act.” Sociological Forum 30(S1):571–88. [DOI] [PMC free article] [PubMed] [Google Scholar]

- McKernan Signe-Mary, Ratcliffe Caroline, Steuerle Eugene, and Zhang Sisi. 2014. “Disparities in Wealth Accumulation and Loss from the Great Recession and Beyond.” American Economic Review 104(5):240–44. [Google Scholar]

- Oliver Melvin L., and Shapiro Thomas M.. 1995. Black Wealth, White Wealth: A New Perspective on Racial Inequality. New York: Routledge. [Google Scholar]

- Percheski Christine, and Christina Gibson-Davis. 2019. “Marriage, Kids, and the Picket Fence? Parenthood and Wealth among U.S. Households.” Unpublished manuscript. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Pfeffer Fabian T. 2018. “Growing Wealth Gaps in Education.” Demography 55(3):1033–68. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Pfeffer Fabian T., Danziger Sheldon, and Schoeni Robert F.. 2013. “Wealth Disparities before and after the Great Recession.” Annals of the American Academy of Political and Social Science 650(1):98–123. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Pfeffer Fabian T., and Killewald Alexandra. 2017. “Generations of Advantage: Multigenerational Correlations in Family Wealth.” Social Forces 96(4):1411–42. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Pfeffer Fabian T., and Killewald Alexandra. 2019. “Intergenerational Wealth Mobility and Racial Inequality.” Socius 5:1–2. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Ratcliffe Caroline, and Signe-Mary McKernan. 2013. “Forever in Your Debt: Who Has Student Loan Debt, and Who’s Worried.” Washington, DC: Urban Institute. [Google Scholar]

- Rauscher Emily. 2016. “Passing It On: Parent-to-Adult Child Financial Transfers for School and Socioeconomic Attainment.” RSF: The Russell Sage Foundation Journal of the Social Sciences 2(6):172–96. [Google Scholar]

- Rugh Jacob S., and Massey Douglas S.. 2010. “Racial Segregation and the American Foreclosure Crisis.” American Sociological Review 75(5):629–51. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Shapiro Thomas, Meschede Tatjana, and Osoro Sam. 2014. “The Widening Racial Wealth Gap: Why Wealth Is Not Color Blind.” Pp. 99–122 in The Assets Perspective, edited by Cramer R and Shanks TRW. New York: Palgrave Macmillan. [Google Scholar]

- Sykes Bryan L., and Maroto Michelle. 2016. “A Wealth of Inequalities: Mass Incarceration, Employment, and Racial Disparities in U.S. Household Wealth, 1996 to 2011.” RSF: The Russell Sage Foundation Journal of the Social Sciences 2(6):129–52. [Google Scholar]

- Thompson Jeffrey P., and Suarez Gustavo A.. 2015. “Exploring the Racial Wealth Gap Using the Survey of Consumer Finances.” Retrieved March 22, 2020. https://www.federalreserve.gov/econresdata/feds/2015/files/2015076pap.pdf.

- Thurston Chloe. 2018. At the Boundaries of Homeownership: Credit, Discrimination, and the American State. New York: Cambridge University Press. [Google Scholar]

- Umberson Debra, Pudrovska Tetyana, and Reczek Corinne. 2010. “Parenthood, Childlessness, and Well-Being: A Life Course Perspective.” Journal of Marriage and Family 72(3):612–29. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Wang Wendy, and Parker Kim. 2014. “Record Share of Americans Have Never Married.” Pew Research Center. Retrieved March 22, 2020. https://www.pewsocialtrends.org/2014/09/24/record-share-of-americans-have-never-married/. [Google Scholar]

- Wolff Edward. 2011. “Recent Trends in Household Wealth, 1983–2009: The Irresistible Rise of Household Debt.” Review of Economics and Institutions (1):1–31. [Google Scholar]

- Wolff Edward N. 2016. “Household Wealth Trends in the United States, 1962 to 2013: What Happened over the Great Recession?” RSF: The Russell Sage Foundation Journal of the Social Sciences 2(6):24–43. [Google Scholar]

- Wolff Edward N. 2017. “Household Wealth Trends in the United States, 1962 to 2016: Has Middle Class Wealth Recovered?” NBER Working Paper No. 24085. Retrieved March 22, 2020. https://www.nber.org/papers/w24085.pdf. [Google Scholar]

- Wolff Edward N. 2018. “The Decline of African-American and Hispanic Wealth Since the Great Recession.” NBER Working Paper No. 25198. Retrieved March 22, 2020. https://www.nber.org/papers/w25198. [Google Scholar]

- Yellen Janet L. 2016. “Perspectives on Inequality and Opportunity from the Survey of Consumer Finances.” RSF: The Russell Sage Foundation Journal of the Social Sciences 2(2):44–59.30123834 [Google Scholar]

- Zhan Min, Xiang Xiaoling, and Elliott William III,. 2016. “Education Loans and Wealth Building among Young Adults.” Children and Youth Services Review 66:67–75. [Google Scholar]