Background:

Despite improved insurance coverage for gender confirmation surgeries in the United States, coverage for facial feminization surgery (FFS) continues to be difficult. Here, we describe our institutional experience on navigation, time, and costs of the FFS insurance authorization process.

Methods:

FFS consults (n = 40) at the University of California, Los Angeles (2018–2020) were reviewed for time and cost to definitive insurance authorization decision. Patients were stratified into 3 groups based on authorization process: Group A (standard approval, n = 26, 65.0%) including public and private insurances; Group B (extended approval, n = 10, 25.0%) consisting of private insurance plans that initially denied and required multi-level appeals for denial overturn; and Group C (denial, n = 4, 10.0%), including private insurance plans that denied even after multi-level appeals.

Results:

An estimated 90% of all patient consults were approved for FFS under insurance. Group A averaged 1.1 months for approval, requiring 1.4 hours of administrative time translating to $38.18 per patient. The addition of multi-level appeals in Groups B and C increased the total time for a definitive decision (7.0 and 5.1 months, respectively) and required both surgeon and administrative time to navigate the process (10.8 and 12.0 hours, respectively). The time spent on the presurgical authorization process for Groups B and C translated to an over 20-fold increase in cost ($855.00 and $988.38, respectively) compared with Group A.

Conclusion:

Navigation of the insurance process for FFS is challenging and time-consuming; however, coverage is a reality in California provided that multi-level appeals are exhausted.

INTRODUCTION

One of the major barriers for transgender patients is accessibility to gender-affirming surgeries due to the lack of insurance coverage or inability to afford surgery as a self-pay patient.1 In an analysis of the National Inpatient Sample, Canner and colleagues noted that between 2000 and 2014, 56.3% of patients undergoing gender-affirming surgery were not covered by any health insurance plan.2 Over the course of this period, particularly between 2012 and 2014, an increase in patients covered by private insurance and Medicare and Medicaid was noted. In addition to legislative changes, the rationale for increasing coverage may be related to calculations on the cost-effectiveness of coverage. Modeling performed by Padula and colleagues for employer-based insurance plans in Massachusetts indicated that, over the course of 5 years, coverage for transition-related services would lead to societal costs of $0.016 per month per member.3 The authors concluded that the relatively low societal cost, combined with the increase in quality-adjusted life years for transgender patients, supported coverage of transition-related services in employer-based plans. Despite these reports, coverage continues to be variable from state to state, physician to physician, as well as depending on anatomical region.

Among the various gender-affirming procedures, facial feminization surgery (FFS) is arguably the most commonly denied surgery, as insurance companies often deem the involved procedures as cosmetic and not medically necessary. Yet, a number of studies have demonstrated that FFS is not only associated with improvement in quality of life for transfeminine patients, but also, for some patients, the most important aspect of transition.4–7 Although significant barriers exist, an improvement in insurance coverage for FFS has occurred over time, albeit navigation of the process is both laborious and confusing. In this work, we report the methods, time consumption, costs, challenges, and successes of our institutional experience on obtaining insurance coverage for FFS.

METHODS

Participants

We identified all patients with gender dysphoria consulted for FFS under a single surgeon (JCL) at the University of California Los Angeles between January 2018 and February 2020 (n = 55). Only patients with insurance authorization decisions were included in this study (n = 40). Demographic, clinical, and administrative data were retrospectively collected (UCLA IRB #19-001482).

Insurance Groups

Patients were stratified into 3 groups by authorization process. Group A (standard approval) included patients who were approved after undergoing a standard authorization process, such as those with Medi-Cal, Medicare, and private insurance. Medi-Cal, the California state equivalent of Medicaid, authorizes all gender-affirming surgeries including FFS and Medicare does not require prior authorization. Private insurances included health maintenance organizations and preferred provider organization. Group B (extended approval) primarily encompassed all patients who were initially denied but, after undergoing a multi-level appeal process, was ultimately approved. The multi-level appeal process included physician-initiated appeal, patient-initiated appeal, and independent medical review (IMR). Denial overturn was either mandated by the California Department of Managed Healthcare for California-insured plans or by the respective insurance companies for self-insured, employer-based plans under the Employee Retirement Income Security Act of 1974 (ERISA). Finally, Group C (denial) included private insurance plans under ERISA that resulted in denial despite multi-level appeals and IMR requested from the plan.

Time and Cost Analysis

We performed a cost analysis of the pre-surgical insurance process for patients seeking FFS. The analysis was done by identifying individual steps involved in the insurance process (Fig. 1) and surveying administrative personnel and physicians to determine the approximate time spent on each step. The administrator hourly compensation set at our institution was used for the cost analysis. Because the plastic surgeon is not paid on an hourly or salary basis, the national average salary was used.8,9 The estimated cost of the insurance process per patient was calculated by combining the hours spent per step and compensation rates.

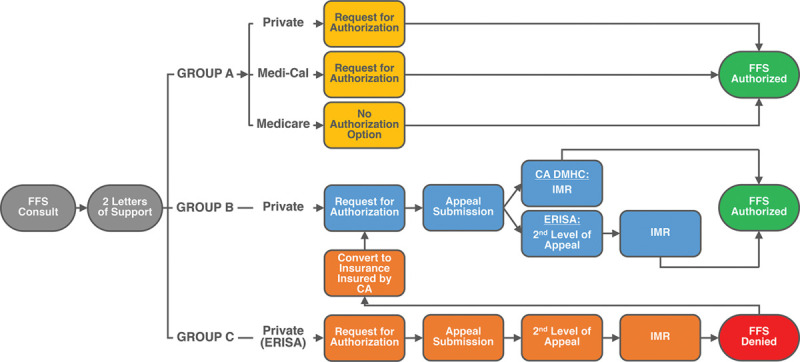

Fig. 1.

Insurance authorization process for FFS.The insurance authorization process for FFS begins with submission of two letters of support from a mental health provider and primary care physician following surgical consult. Subsequently, the process typically follows one of three paths: Group A (standard approval), Group B (extended approval), and Group C (denial). Group A is similar to other medically necessary reconstructive procedures where authorization is requested and procedures are authorized. Plans that fall into this group include Medi-Cal, Medicare, and some private insurance plans. Group B, consisting only of private insurance plans, are processes that initially resulted in denial, thereby requiring multi-level appeals. Such multi-level appeals begin with a surgeon-initiated appeal, which is then also denied. Subsequently, in California-insured plans, an IMR is then requested from the California Department of Managed Healthcare (CA DMHC). Due to the gender non-discrimination laws of the state, the denial is typically overturned and the procedures are authorized. Unlike California-insured plans, job-based plans which are self-insured, also called Employee Retirement Income Security Act (ERISA)-plans, a second-level, patient-initiated appeal is typically required. Upon denial, an IMR is requested directly from the insurance plan. Unlike California plans, self-insured plans are not under the CA DMHC and, thus, the final outcome is more variable. Some will result in eventual approval (Group B) and others will result in eventual denial (Group C). Patients who are definitively denied (Group C) may then exit their employer-based plan and switch to a plan under California jurisdiction on the health insurance exchange.

Statistical Analyses

All data were analyzed using SPSS software, version 25 (IBM, Chicago, Ill.). Descriptive statistics were performed for demographic variables. Analyses of variance with posthoc comparisons under the Tukey criterion were used to compare time from consultation to approval or denial, time spent obtaining insurance authorization, and cost. P < 0.05 was considered significant.

RESULTS

Patient Population

A total of 40 transfeminine patients were identified (mean age 35.6 ± 2.2 years) (Table 1). Among the total cohort, most patients had private insurance (n = 23, 57.5%), followed by Medi-Cal (n = 13, 32.5%), and Medicare (n = 4, 10.0%). A total of 36 patients (90.0%) have been approved by insurance. Specific surgical procedures were requested based on patient desires and clinical assessment, with the goal of completing FFS in a one-stage surgery. Procedures requested for facial feminization insurance authorization are detailed in Table 2. Requested CPT codes are detailed in Supplemental Digital Content 1. (See table 1, Supplemental Digital Content 1, which displays requested CPT codes and associated terminology for facial feminization surgery. http://links.lww.com/PRSGO/B647.)

Table 1.

Insurance Information of FFS Patients

| Total (n = 40) | |

|---|---|

| Age, y (Mean ± SE) | 35.6 ± 2.2 |

| Insurance type, n (%) | |

| PPO (private) | 20 (50.0) |

| HMO (private) | 3 (7.5) |

| Medi-Cal/Medicaid | 13 (32.5) |

| Medicare | 4 (10.0) |

| Insurance groups, n (%) | |

| Group A | 26 (65.0) |

| Group B | 10 (25.0) |

| Group C | 4 (10.0) |

Table 2.

Procedures Requested for Facial Feminization Surgery

| Procedures | Total (n = 40),n (%) |

|---|---|

| Brow lift | 40 (100.0) |

| Forehead (frontal bone recontouring, recontouring of superior orbital rim, hairline lowering) | 38 (95.0) |

| Fat graft | 37 (92.5) |

| Rhinoplasty with osteotomies | 36 (90.0) |

| Two-piece osseous genioplasty | 33 (82.5) |

| Reduction of mandibular angles | 29 (72.5) |

| Tracheal shave | 22 (55.0) |

| Upper lip lift | 22 (55.0) |

| Canthopexy | 2 (5.0) |

| Zygoma reduction | 1 (2.5) |

Stratification of Insurance Authorization Process

From the cohort, 3 subgroups were delineated. All patients with public insurance (Medi-Cal or Medicare) as well as a small subset of private insurance plans were approved after initial submission of authorization request or did not require approval before surgery (Medicare) (Fig. 1). These patients underwent a standard approval process no different from other reconstructive procedures (Group A). A second subgroup of patients (Group B), all of whom had private insurance, were approved for surgery but required multi-level appeals, peer-to-peer discussions, and, ultimately, an IMR. These IMRs are often requested through the California Department of Managed Healthcare resulting in state-mandated overturn of the insurance decision, or less commonly, through the insurance company for ERISA or self-insured plans which do not fall under state jurisdiction. Lastly, a third subgroup of patients (Group C), all with private insurance, were denied for surgery despite multi-level appeals, peer-to-peer discussions, and IMR. Unlike Group B, patients within Group C only had plans that were self-insured under ERISA.

Group A: Standard Approval

Among the 26 patients (65.0%) who underwent the standard approval process, 13 patients had Medi-Cal, 4 patients had Medicare, and 9 patients had private insurance.

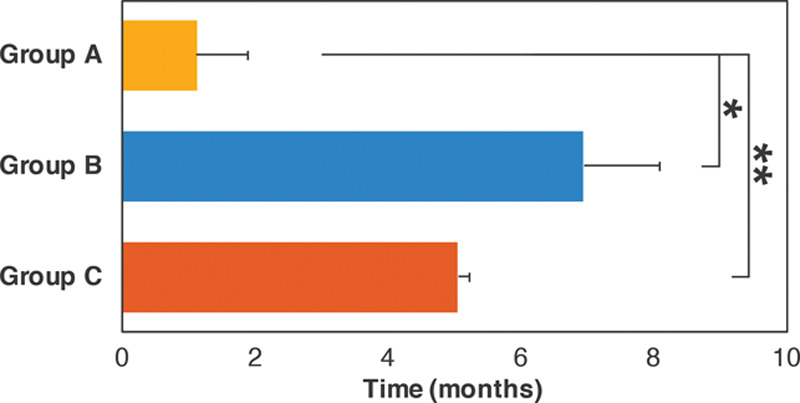

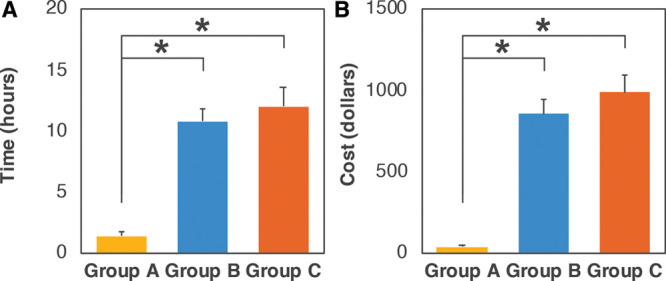

The total time from initial consultation to definitive authorization decision for Group A was 1.1 ± 0.2 months (Fig. 2). Because Medicare patients (n = 4) do not need prior authorization, they were excluded from the time and cost analysis of the insurance appeal process for Group A. Administrative time in this cohort included obtaining initial authorizations, which resulted in an average of 1.4 ± 0.4 hours spent per patient at an estimated cost of $38.18 ± 10.18 per patient (Fig. 3). (See table 2, Supplemental Digital Content 2, which displays the total time and cost of the insurance approval process per group. http://links.lww.com/PRSGO/B648.)

Fig. 2.

Months required for definitive insurance authorization decisions for FFS. Average months spent from initial facial feminization consultation to final insurance authorization decision. Error bars denote standard error. *P < 0.001; **P = 0.003.

Fig. 3.

Time and cost of the insurance approval process for FFS. Average time spent from administrator and surgeon in obtaining insurance approval for FFS (A). Estimated costs of obtaining insurance approval for FFS (B). Error bars denote standard error. *P < 0.001.

Group B: Extended Approval

An estimated 10 patients (25.0%), all with private insurance, underwent an extended approval process requiring multi-level appeals and denial overturn after IMR and frequently, state intervention.

The total time from initial consultation to authorization approval in Group B required 7.0 ± 1.1 months, a 6-fold longer process compared with Group A patients (P < 0.001) (Fig. 2). Administrative time, including obtaining initial authorizations, appeals, IMRs, and additional phone calls, averaged to 7.2 ± 1.0 hours spent per patient. (See table 2, Supplemental Digital Content 2, which displays the total time and cost of the insurance approval process per group. http://links.lww.com/PRSGO/B648.)

In addition to administrative time, multi-level appeals required time from the attending craniofacial surgeon for peer-to-peer reviews, writing appeal letters, and patient counseling over the 6-month period, in total averaging 3.6 ± 0.5 hours per patient. In total, the time and cost estimate of the insurance appeal process was 10.8 ± 1.0 hours and $855.00 ± 91.53 per patient, respectively. Compared with Group A, the amount of time spent acquiring the authorization was 8-fold higher (P < 0.001), with a 22-fold higher cost (P < 0.001) for the Group B authorization process (Fig. 3).

Group C: Denial

In total, 4 patients (10.0%) were ultimately denied despite multi-level appeals and IMR requests. As stated above, all patients within this group were covered by private insurance plans that were not within the purview of the State of California and, thus, were not eligible for state intervention. The time from initial consultation to final insurance denial required 5.1 ± 0.7 months, nearly 5-fold higher than Group A (P = 0.003) (Fig. 2). Coordinating presurgical authorization required an average of 7.8 ± 1.5 hours per patient for the administrator and 4.3 ± 0.5 hours per patient for the attending craniofacial surgeon to navigate multi-level appeals. (See table 2, Supplemental Digital Content 2, which displays the total time and cost of the insurance approval process per group. http://links.lww.com/PRSGO/B648.) In total, the time consumption of the insurance process was 12.0 ± 1.6 hours and cost $988.38 ± 101.76 per patient. The Group C authorization process, which resulted in denial of services, consumed a 9-fold higher amount of time (P < 0.001) and 26-fold higher cost (P < 0.001) when compared with Group A (Fig. 3).

DISCUSSION

In this work, we detailed our institutional experience on obtaining insurance coverage for FFS. We identified 3 subsets of authorization processes, which partially correlated to the types of insurance plans of the respective patients. In the standard approval process (Group A), patients were under both public and certain private insurance plans (39% of all privately insured patients in the cohort). On average, the authorization process required approximately 1 month to complete and cost on average $38 worth of time to coordinate administratively. In contrast to Group A, patients who required significant efforts in the form of multi-level appeals, peer-to-peer reviews, and IMRs were designated Groups B and C, depending on ultimate approval versus denial as the outcomes, respectively. For both Groups B and C, the authorization process averaged approximately 6 months, a 6-fold increase compared with Group A. The cost of the administrative and attending craniofacial surgeon effort for Groups B and C averaged approximately $900, over 20-fold more than Group A. The major difference between approval (Group B) versus denial (Group C) was that the former primarily consisted of plans insured by California and, thus, under the jurisdiction of California law, whereas Group C plans were entirely self-insured employer (ERISA) plans, which are exempt from state regulation. Despite the time, effort, and costs incurred, 90.0% of patients were approved for FFS under insurance. The remaining 10.0% of patients who were ultimately denied were counseled and in the process of exiting their job-based insurance plan and enrolling for coverage through plans under the health insurance exchange established by the Affordable Care Act, which fall under state jurisdiction. Our current work highlights the high likelihood of success in FFS coverage under insurance in California, but also details the challenges that plastic surgeons and plastic surgery practices incur for coverage to occur.

Insurance coverage for FFS is an important issue for a number of reasons for both patients and surgeons. First, one of the most significant barriers to FFS for patients is the ability to pay for surgery, which ranges from $40,000 upwards for full-face, one-stage surgery. Thus, coverage significantly increases accessibility. Second, while complications are not high in FFS, they may occur. Furthermore, revisions may be indicated in some patients over time. In these circumstances, both complications and revisions are covered as reconstructive procedures, whereas self-pay patients may be responsible for secondary surgical costs. Third, full-face, one-stage FFS is a highly time-consuming surgery due to the multiple anatomical areas addressed at once (averaging 8.5 hours in the senior author’s experience). For self-pay patients, cost will frequently dictate the operative and postoperative setting such that patients may be preferentially or solely performed in an outpatient setting. This may influence the decision-making of surgeons with respect to the complexity of procedures to perform. For example, some may be reluctant to perform an osteotomy of the anterior table of the frontal bone for setback in an outpatient surgery center and, thus, default to a less aggressive method of frontal bone recontouring, which may be an undercorrection for certain patients. In contrast, FFS under insurance coverage allows for inpatient care, which may be important, particularly to surgeon decision-making as well as patients who may have other medical conditions, pain control issues, or those who travel from long distances. Lastly, FFS coverage also allows for inclusion of technologies, such as virtual modeling and surgical planning, which may be cost prohibitive in self-pay patients despite evidence that accuracy is improved.10,11

One of the major issues among surgeons and patients with regard to insurance coverage for FFS is the lack of understanding of the process as coverage for gender healthcare is highly variable depending on state law and plan variabilities (Table 3).

Table 3.

State Laws on Coverage for Transition-related CARE12

| Explicitly Covers (Year) | Explicitly Excludes (Year) | Does Not State or Uncertain |

|---|---|---|

| California (2013) | Alaska (2010) | Alabama |

| Colorado (2017) | Arizona (2004) | Arkansas |

| Connecticut (2015) | Georgia (1992) | Delaware |

| District of Columbia (2014) | Hawaii (1993) | Florida |

| Illinois (2019) | Iowa (1994, 2019) | Idaho |

| Maine (2019) | Missouri (2017) | Indiana |

| Maryland (2016) | Nebraska (1990) | Kansas |

| Massachusetts (2015) | Ohio (2015) | Kentucky |

| Michigan (2019) | Tennessee (2006) | Louisiana |

| Minnesota (2017) | Texas (2019) | Mississippi |

| Montana (2017) | West Virginia (2005) | New Mexico |

| Nevada (2018) | Wyoming (1992) | North Carolina |

| New Hampshire* (2019) | North Dakota | |

| New Jersey (2017) | Oklahoma | |

| New York (2016) | South Carolina | |

| Oregon (2014) | South Dakota | |

| Pennsylvania (2016) | Utah | |

| Rhode Island (2015) | Virginia | |

| Vermont (2008) | ||

| Washington (2015) | ||

| Wisconsin* (2019) |

*Previously excluded.

Additionally, the timeline for authorization is relatively opaque, thereby causing more uncertainty in patients and surgeons. As an example, the typical timeline for our Group B and C patients is as follows: 1. Submission and review of initial authorization request (1 month); 2. Submission and review of physician-initiated appeal (1 month); 3. Submission and review of second level, patient-initiated appeal (1 month); 4. Submission and review of IMR (1 month). The pre-surgical authorization process for patients in Groups B and C, constituting 60.8% of all private insurance patients in our cohort, is highly time-consuming due to the individual review periods required for each level. In the Group A patients, FFS under Medi-Cal still requires preauthorization, just like private insurances. However, California state law stipulates gender non-discrimination in health insurance, thus, Medi-Cal covers all procedures performed specifically for the purposes of gender affirmation. As gender dysphoria is highly individual, such procedures will vary by anatomical areas associated with dysphoria for each individual patient as well as decision-making from the treating surgeon. It is of great importance to note that there is no “one-size-fits-all” solution for facial gender affirmation with respect to determining medical necessity of procedures. One patient may have severe dysphoria over their forehead, while one may have dysphoria over their upper lip. Thus, specifying any one procedure as medically necessary while excluding other facial procedures reflects a lack of understanding of the nature of the diagnosis.

The time and costs necessary to achieve approval from insurance plans for FFS are not trivial. Administrative costs have been estimated to account for 31% of health care expenditures in the United States.13 At the level of individual academic surgical practices, contemporary estimations of processing time and total costs for billing and insurance-related activities were 100 minutes and $215.10 for an inpatient surgical procedure in 2017.14 Time and costs for activities carried out by physicians were estimated at a median of 15 minutes or $51.20 for an inpatient surgical procedure.14 In plastic surgery, Braun and colleagues have performed a similar study evaluating the time and cost burden of insurance denials for pediatric patients with congenital breast anomalies.15 Their work estimated that the average pre-surgery insurance process to cost $445.36 and require 7.4 hours of institutional time. Compared with the published literature, patients within Groups B and C are multi-fold greater than the reported standard estimates in the former study without even taking into account time and costs of post-surgical billing activities. Furthermore, even in the challenging scenario for insurance authorization reported by Braun and colleagues, Groups B and C also exceed reported estimates. In total, attempting and succeeding at obtaining insurance coverage for FFS is a significant time and cost burden that may be difficult to overcome for a number of plastic surgical practices, suggesting ramifications for patient accessibility. One potential consideration for reducing time and costs is to centralize administrative staff for gender health insurance authorizations. Especially with the establishment of multi-disciplinary gender health teams across the United States, coordination of care through a consistent group of trained administrative staff knowledgeable in the process and appeals process for gender health procedures would potentially reduce the burden on individual offices and surgeons.

There are a few limitations in this study that deserve mention. The generalizability of the findings presented here is limited by state laws. Secondly, the current study does not take into account the postsurgical administrative and billing time consumption and costs. For example, a number of state-mandated denial overturns in Group B patients resulted in billing challenges postsurgery. Similarly, while Medicare does not require an authorization process to move forward with surgery, we have experienced significant billing challenges postsurgery. These are difficult to quantify as our institutional billing activities are centralized and carried out by multiple administrators. Thirdly, it is likely that the current work underestimated the total cost of the insurance approval process, as we could not quantify the cost of surgery cancelations, additional clinic visits, and unquantifiable administrative time. Lastly, the time consumption, costs, and difficulties to the patient were not assessed. A number of patients had multiple consultations, some consulted legal assistance, and, particularly patients in Groups B and C, some experienced significant distress over the repetitive denials and lack of clarity in the end result of the process. Additionally, the patients who exited their employer-based plans to buy health insurance on the exchange paid more for health insurance by foregoing employer contributions.

CONCLUSIONS

This study highlighted the successes and burdens associated with obtaining insurance authorization for FFS. We detail our institutional experience to provide a roadmap for craniofacial surgeons to navigate the process in an effort to provide higher accessibility to transgender patients seeking facial reconstruction.

ACKNOWLEDGEMENTS

This work was supported by the Bernard G. Sarnat Endowment for Craniofacial Biology (JCL) and the Jean Perkins Foundation (JCL). JCL is additionally supported by the US Department of Veterans Affairs under award number IK2 BX002442 and the National Institutes of Health/NIDCR R01 DE0289098.

Supplementary Material

Footnotes

Published online 18 May 2021.

Disclosure: All the authors have no financial interest to declare in relation to the content of this article.

Related Digital Media are available in the full-text version of the article on www.PRSGlobalOpen.com.

REFERENCES

- 1.James S, Herman J, Rankin S, et al. The report of the 2015 U.S. transgender survey. 2016. Available at: https://www.transequality.org/sites/default/files/docs/USTS-Full-Report-FINAL.PDF. Accessed April 21, 2021.

- 2.Canner JK, Harfouch O, Kodadek LM, et al. Temporal trends in gender-affirming surgery among transgender patients in the United States. JAMA Surg. 2018; 153:609–616. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 3.Padula WV, Heru S, Campbell JD. Societal implications of health insurance coverage for medically necessary services in the U.S. Transgender population: a cost-effectiveness analysis. J Gen Intern Med. 2016; 31:394–401. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Ainsworth TA, Spiegel JH. Quality of life of individuals with and without facial feminization surgery or gender reassignment surgery. Qual Life Res. 2010; 19:1019–1024. [DOI] [PubMed] [Google Scholar]

- 5.Raffaini M, Magri AS, Agostini T. Full facial feminization surgery: patient satisfaction assessment based on 180 procedures involving 33 consecutive patients. Plast Reconstr Surg. 2016; 137:438–448. [DOI] [PubMed] [Google Scholar]

- 6.Ousterhout DK. Facial feminization surgery: the forehead. surgical techniques and analysis of results. Plast Reconstr Surg. 2015; 136:560e–561e. [DOI] [PubMed] [Google Scholar]

- 7.Capitán L, Simon D, Kaye K, et al. Facial feminization surgery: the forehead. Surgical techniques and analysis of results. Plast Reconstr Surg. 2014; 134:609–619. [DOI] [PubMed] [Google Scholar]

- 8.Doximity. 2018 Physician Compensation Report. 2018. Available at: https://blog.doximity.com/articles/doximity-2018-physician-compensation-report. Accessed August 1, 2019.

- 9.Leigh JP, Tancredi D, Jerant A, et al. Physician wages across specialties: informing the physician reimbursement debate. Arch Intern Med. 2010; 170:1728–1734. [DOI] [PubMed] [Google Scholar]

- 10.Hoang H, Bertrand AA, Hu AC, et al. Simplifying facial feminization surgery using virtual modeling on the female skull. Plast Reconstr Surg Glob Open. 2020; 8:e2618. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11.Gray R, Nguyen K, Lee JC, et al. Osseous transformation with facial feminization surgery: improved anatomical accuracy with virtual planning. Plast Reconstr Surg. 2019; 144:1159–1168. [DOI] [PubMed] [Google Scholar]

- 12.Mallory C, Tentindo W. Medicaid coverage for gender-affirming care. Research that Matters. Los Angeles, CA: University of California, Los Angeles School of Law; 2019. [Google Scholar]

- 13.Woolhandler S, Campbell T, Himmelstein DU. Costs of health care administration in the United States and Canada. N Engl J Med. 2003; 349:768–775. [DOI] [PubMed] [Google Scholar]

- 14.Tseng P, Kaplan RS, Richman BD, et al. Administrative costs associated with physician billing and insurance-related activities at an academic health care system. JAMA. 2018; 319:691–697. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15.Braun TL, Braun JL, Hernandez C, et al. insurance appeals for pediatric reconstructive surgery: a micro cost analysis and how-to guide. Ann Plast Surg. 2018; 80:198–204. [DOI] [PubMed] [Google Scholar]

- 16.AAPC Coder. Available at: https://coder.aapc.com/. Accessed July 1, 2020.

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.