Insurance coverage has lagged behind improvements in gynecologic cancer care, with one third of women never seeing a gynecologic oncologist and half experiencing financial toxicity during cancer treatment.

Abstract

With 102,000 new cases of gynecologic cancer, 30,000 associated deaths annually, and increasing rates of endometrial cancer, gynecologic cancer is a growing problem. Although gynecologic cancer care has advanced significantly in the past decade owing to new therapeutics and specialized training in radical surgery, even insured women face major barriers to accessing and affording quality gynecologic cancer care. This commentary reviews current literature on insurance-mediated disparities in gynecologic cancer and provides education to clinicians on barriers to care. One third of women with a gynecologic cancer never see a gynecologic oncologist. Up to 40% of Medicare Advantage plans lack an in-network gynecologic oncologist, and 33% of private insurance plans do not include an in-network National Cancer Institute-accredited cancer center, limiting access to surgical advances and clinical trials. Women with Medicaid insurance and gynecologic cancer are 25% less likely to receive guideline-concordant care. Among insured women, 50% experience financial toxicity during gynecologic cancer treatment, and costs may be even higher for certain Medicare enrollees. Addressing these insurance-mediated disparities will be important to help our patients fully benefit from the scientific advances in our field and thrive after a gynecologic cancer diagnosis.

Having insurance is not a panacea to quality gynecologic cancer care. Endometrial cancer rates are increasing, and there are 102,000 new cases of gynecologic cancer and 30,000 associated deaths annually. Yet even insured women face major barriers to accessing and affording quality gynecologic cancer care.1 In endometrial cancer, new therapies, such as Jemperli (dostarlimab), an immunotherapy recently approved by the U.S. Food and Drug Administration for the treatment of advanced or recurrent endometrial cancer for the one third with mismatch repair deficiency, are estimated to cost $104,000 in the first 6 months of treatment alone.2,3 This amount does not include physician visit fees, infusion center costs, imaging, and support services—and assumes a patient's insurance will cover the drug. Drug costs are just one area of concern: patients with inadequate public or private insurance face significant barriers in receiving health care. Underinsurance is when a patient's insurance does not adequately cover necessary treatment, which can occur through exclusion of benefits (eg, their insurance does not cover genetic testing) or high out-of-pockets costs (eg, their medical care expenses are beyond what they can afford). Underinsurance often translates into lower rates of cancer screening and surveillance, delayed follow-up after abnormal results, later stage diagnosis, and delays in receipt of quality cancer care.4 Underinsurance—and its effect on clinical care—differs by insurance type, such as between private or employer-sponsored insurance and Medicare. In this article, we review existing evidence on the effect of insurance type on the screening to treatment continuum in gynecologic cancers.

SCREENING AND TIME TO CANCER CARE INITIATION BASED ON INSURANCE TYPE

Uninsured

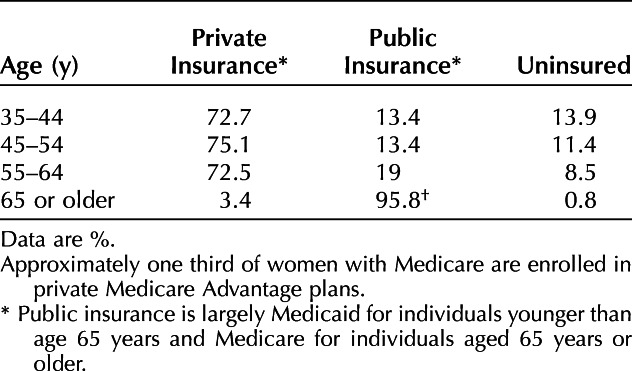

Under the 2010 Patient Protection and Affordable Care Act (ACA), 20 million Americans gained insurance coverage by 2016.5 Yet, despite coverage expansions, there remained 30 million uninsured Americans in 2019 (Table 1). Lacking health insurance leads to lower screening rates for cervical, breast, and colorectal cancers, putting women at risk for late-stage cancer diagnosis.6

Table 1.

Insurance Coverage by Age, 201954

Because cervical cancer is preventable and has a screening test, the National Breast and Cervical Cancer Early Detection Program was enacted in 1990 as a state block grant program to alleviate many of the expenses associated with cancer screening and treatment for low-income uninsured and underinsured women. The National Breast and Cervical Cancer Early Detection Program covers 100% of treatment and short-term follow-up costs; however, this applies only to cervical cancer and cervical cancer–related treatment, and how screening is delivered (eg, through community health centers, screening drives, or private practices) differs between states.

Although any woman earning less than 250% of the federal poverty level is eligible for cervical cancer screening through the National Breast and Cervical Cancer Early Detection Program, one third of the 5.3 million women who qualify are not regularly screened.7 Screening disparities were exacerbated by the COVID-19 pandemic with an 84% reduction in National Breast and Cervical Cancer Early Detection Program–funded cervical cancer screening in 2020.8

Medicaid

Under the ACA, Medicaid coverage has expanded to individuals up to 138% federal poverty level in the 37 states and Washington, DC, that expanded coverage.5 The ACA's Medicaid expansion has been associated with improvements in cervical cancer screening, earlier diagnosis of gynecologic cancers, timely receipt of cancer care, and improved 1-year survival.9,10 Nonetheless, Medicaid-insured patients are still screened 10% less than privately insured patients.11 Improving cervical cancer screening among Medicaid patients through patient or clinician interventions, such as covering travel costs or screening reminders, is a key component to preventing cervical cancer.

Medicare

Medicare is the primary and often only insurer of American adults 65 years and older. Although enrollment for Medicare Part A (hospital care) is automatic and covers 80% of costs, Medicare12 Part B (outpatient services) requires individual enrollment and premiums are administered based on income levels and can range anywhere from $150 to $500 monthly. This facet of Medicare, known as traditional Medicare or Medicare fee-for-service, is essential because it provides coverage for physician services, outpatient hospital services, and diagnostic examinations (Table 2).13 Low-income elderly patients may have inadequate coverage owing to their inability to cover these extra premiums for Medicare Part B or co-insurance for hospitalizations under Part A, but these individuals will often qualify for Medicaid, which can alleviate the financial burden of health care expenses. However, Medicaid enrollment is not automatic, and the 20% of elderly patients who are dual-eligible may face logistic barriers to enrollment.14 Individuals have the option of enrolling in Medicare Part C, aka “Medicare Advantage,” as an alternative to Parts A and B. In Medicare Advantage, a private payer contracts with the Centers for Medicare & Medicaid Services to provide hospital and outpatient coverage and additional services, such as dental care, through a premium, adding up to $200 monthly. In contrast to traditional Medicare, private payer–lead Medicare Advantage plans can implement health care professional networks and additional coverage restrictions, such as prior authorization, like private insurance. This design allows Medicare Advantage plans to innovate, but it also leads to variable coverage and out-of-pocket costs (ie, co-pays, deductibles, co-insurance) based on an individual's chosen Medicare Advantage plan. For example, patients with ovarian cancer and Medicare may pay between $1 and $1,234 annually for PARP inhibitor maintenance therapy, depending on their Medicare plan.15

Table 2.

Medicare Plans in the United States

Differences in Medicare type (Medicaid-Medicare, Medicare fee-for-service, Medicare Advantage) affect cancer screening rates. Patients with Medicare fee-for-service had screening rates seven times higher than Medicare–Medicaid patients in one recent study.16 Patients with Medicare Advantage usually have higher screening rates than Medicare fee-for-service, given physician pay-for-performance metrics used in Medicare Advantage plans.17

Private Insurance

The majority (70%) of working adults younger than age 65 years have employer-sponsored private insurance. The ACA standardized plan coverage and cost-sharing for preventive health services by requiring coverage and eliminating co-pays (ie, fee charged at the time of visit) for preventive services with a U.S. Preventive Services Task Force “A” or “B” rating, including cervical, breast, colorectal, and lung cancer screening.18

Although cervical cancer screening may no longer be financially burdensome for privately insured individuals, there is no mandate requiring insurers to cover follow-up testing after abnormal screening results.19 If follow-up diagnostic examinations, such as colposcopy and biopsies, are cost or time-prohibitive to patients through co-pays or missed work, care is likely to be delayed, making regular screening ineffective in ensuring optimal cancer prevention. Moreover, woman may have trouble finding an available, in-network gynecologist for colposcopy: only 60% of women received a colposcopy within 6 months of an abnormal Pap test result in a recent analysis.20 Some low-income privately insured women may qualify free follow-up of abnormal cervical cancer screening results under the National Breast and Cervical Cancer Early Detection Program.

Factors Affecting Time to Care Initiation

The first step to any diagnosis is visiting your primary care physician, but this may not be accessible to those uninsured, underinsured, or insured by Medicaid or Medicare programs. A national survey evaluating physician's willingness to accept new patients found that, although 96% of primary care practitioner had clinical capacity, 40% were not accepting uninsured individuals, 26% were not accepting Medicaid patients, and 14% were not accepting Medicare enrollees.13 Obstetrician–gynecologists (ob-gyns) may be the de facto primary care practitioner for many younger gynecologic oncology patients and are more likely to accept Medicaid than other specialties.21 Higher Medicaid reimbursement would likely increase health systems' willingness to accept Medicaid and facilitate more clinicians seeing Medicaid patients. Moreover, under some insurance plans, patients may not be able to get a specialty referral to gynecology without first seeing a primary care practitioner. Lack of a primary care practitioner during cancer treatment also complicates treatment of common complications, such as hypertension, contributing to the 17% of patients with cancer seeking emergency care annually for nonemergent symptoms.22

Even when patients have access to a primary care practitioner, physician knowledge of gynecologic cancer symptoms may delay work-up and diagnosis. A common symptom of endometrial cancer is postmenopausal bleeding, with 90% of patients experiencing bleeding before diagnosis. Yet postmenopausal bleeding, bloating, or vaginal itching—all symptoms of gynecologic cancers—may be dismissed by primary care practitioner as attributable to more common, benign symptoms. Issues in work-up are known contributors to racial disparities with Black women more likely to face diagnostic delays—and twice as likely to die of endometrial cancer.23,24

INEQUITABLE CARE QUALITY AND SPECIALTY ACCESS

Community Health Centers

Twenty-five million Americans, the majority of whom are uninsured or have Medicaid, receive their care from community health centers, which provide comprehensive primary health care regardless of ability to pay.25 Although the ACA increased funding for community health centers, these centers remain limited in their ability to provide adequate cancer screening and access to specialty care.26 Between 69% and 79% of community health centers do not have affiliations with hospitals for specialty referrals.19 Affiliated centers report easier access to follow-up treatment and more timely communication.27 Development of referral networks and navigator programs from community health centers to cancer centers may help bridge this gap from primary to cancer care.28

Gynecologic Oncologist Specialty Access

The Society of Gynecologic Oncology and the American Society of Clinical Oncology recognize evaluation by a gynecologic oncologist as the standard of care for gynecologic cancer, owing to specialized surgical skills, higher rates of guideline-adherent care, and improved survival outcomes.29,30

Yet one third of women never see a gynecologic oncologist during their cancer care.31 Although access to a general ob-gyn is included in network adequacy standards, access to a subspecialist gynecologic oncologist is not included in the network adequacy standard for Centers for Medicare & Medicaid Services' Medicare Advantage (Part C) plans. In contrast, the subspecialities of surgical and medical oncology and urology are included in these standards.32 In a survey of Medicare Advantage plans, 27% of silver plans and 44% of bronze plans did not include a gynecologic oncologist in-network.30 Private insurers and Medicaid are similarly not under any legal requirement to provide access to a gynecologic oncologist. The trend towards narrow network plans offered under the ACA's health insurance exchanges (a venue for individuals to purchase private insurance) led to updated standards in 2015 to ensure “adequate provider networks.” However, the classification and evaluation of network adequacy is left to individual states.33 And state-mandated coverage requirements are not applicable to self-insured plans, which represent two thirds of employer-sponsored insurance plans.34

Despite no requirement for in-network gynecologic oncologist coverage for any insurance type, higher clinician reimbursement rates under private insurance plans generally facilitate access to gynecologic cancer care. Although the occurrence of a cancer diagnosis should not differ by insurance type, one study analyzing the insurance distribution of a public, academic gynecologic oncology clinic in Virginia found that privately insured patients made up 44% of their referrals, compared with 31% Medicare and only 6% Medicaid (remainder were uninsured).35 Uninsured or underinsured women with cervical cancer benefiting from the National Breast and Cervical Cancer Early Detection Program are likely to face similar obstacles in finding a gynecologic oncologist, given the fact that this program's payments for clinical services cannot exceed Medicare reimbursement rates.

Disparities in Standard-of-Care Treatment

Even when patients are able to access a gynecologic oncologist, publicly insured women are less likely to receive standard-of-care treatment, surgery by a high-volume surgeon, and timely chemotherapy initiation than privately insured women. Further, Medicare–Medicaid coverage is associated with less guideline-concordant care with 44% of dually eligible beneficiaries receiving chemotherapy compared with 60% of exclusively Medicare-covered or privately insured individuals.36 In ovarian cancer, having private insurance was associated with a 6-month longer survival compared with having public insurance after controlling for sociodemographic, cancer, and treatment factors, a survival gain similar to those seen in recent chemotherapy advances. (Frost A, Smith AJ, Wethington S, and Fader A. Factors associated with long-term (≥10 year) ovarian cancer survival in the National Cancer Database. Gyn Oncol 2020;156:e24. doi:10.1016/j.ygyno.2019.11.080)

Insurance barriers to care are increasingly common in private insurance. 95% of Medicare Advantage plans—and many private insurance plans—have implemented prior authorization, a process that may delay or deny patients' access to chemotherapy, imaging, or surgery. Although 90% of appealed prior authorization claims are ultimately approved by insurers, 80% of patients and clinicians do not challenge these insurance denials owing to time and staff resources. In other cancers, prior authorization has been associated with 2-week or greater delays in treatment start as well as significant patient stress.37,38

Another factor affecting the quality of cancer care received is oncologist volume and ability to get in-network care at Commission on Cancer accredited hospitals and National Cancer Institute designated cancer centers. Most private insurance plans (95%) available on the federal exchanges had at least one Commission on Cancer accredited hospital in their network, but only 41% of networks included National Cancer Institute-designated cancer centers, which limits availability of high-volume, specialized care and clinical trial opportunities (Table 3).39

Table 3.

Anticipated Effect of Insurance-Mediated Disparities in Gynecologic Oncology

Financial Toxicity

Fifty percent of patients with gynecologic cancer experience financial toxicity while undergoing treatment, often resulting in acquisition of debt and treatment delays.40,41 Where patients with cancer declare bankruptcy, their risk of mortality is increased by 80% compared with patients who do not declare bankruptcy.42 Patients who identify as Black or Hispanic, have Medicaid or Medicare insurance, or lower incomes are significantly more likely to experience financial toxicity with a sevenfold higher risk delaying or avoiding care as a cost-coping strategy.42

A large portion of financial toxicity comes from drug costs. New therapies, such as Jemperli (dostarlimab) and Zejula (niraparib), U.S. Food and Drug Administration–approved oral chemotherapies for treatment of endometrial and ovarian cancer respectively, have price tags upwards of $100,000 for a year's supply.2 Among privately insured patients with ovarian cancer on PARP inhibitors, such as Zejula (niraparib), 83% face out-of-pocket costs with mean monthly expenses of $305, and these medications—and cost—may be continued for up to 3 years.43 If patients forgo purchasing Medicare D coverage, which nearly a quarter of Medicare enrollees do, they face covering the entire cost of oral chemotherapies, an average $12,422 monthly, for PARP inhibitors alone.44,45 Patient assistance programs are available to patients with high co-pays, but cannot provide assistance to all patients who need them.

Aside from oral medication costs, Medicare fee-for-service (Part B) has a coinsurance rate of 20% for services covered, such as physician visits, imaging, and IV chemotherapy. Nearly one third of patients on Medicare fee-for-service report out-of-pocket spending of $5,000 or more, and 7% spend more than $10,000 annually.13 Even among privately insured patients, an increasing number—43% in 2017—are covered by high deductible health plans. Plans have minimum deductibles, ranging from $1,655 to $4,779 on average, that patients are required to spend on medical care before any cost coverage becomes effective.46 Although Medicaid traditionally has minimal cost-sharing, it did not cover clinical trial enrollment until 2021, leading to cost-exclusion of Medicaid patients from clinical trials, the standard of care in recurrent gynecologic cancer.

The costs of cancer care continue to accumulate long after completion of primary treatment. In ovarian cancer, the median total medical expenditures 1 year after surgery for privately insured patients was $93,632, of which patients bear, on average, 3% as out-of-pocket costs (approximately $2,800).47 Patients experiencing financial toxicity spend less on leisure activities, borrow money, and may fail to adhere to cancer treatment and surveillance.40 Without intervention, these cost-coping strategies jeopardize the health of patients who potentially could have recovered from a cancer diagnosis with recommended care, and the financial well-being of their families.

Genetic Testing

Genetic testing is now the standard of care in ovarian cancer and will likely be recommended for all cancer diagnoses, given the 8% rate of germline mutations in patients with cancer.48 In recurrent ovarian cancer, patients with a BRCA1 or BRCA2 mutation had a 70% reduction in cancer progression or death and 13-month gain in overall survival with PARP inhibitors as maintenance therapy after chemotherapy.49 Identifying at-risk individuals before cancer diagnosis is equally important with screening recommended based on family history or after diagnosis of a relative with a genetic cancer syndrome.

Although Medicaid, Medicare, and private insurance cover genetic testing after an ovarian cancer diagnosis, testing after other cancer diagnoses or based on family history is highly variable. Although most Medicaid programs cover BRCA and Lynch syndrome testing for individuals who have a known familial mutation, testing for other ovarian cancer-causing genes, such as RAD51C, may not be covered, even when there is a known pathogenic mutation in a first-degree relative.50 Medicare has stricter guidelines, limiting genetic testing for individuals who have received a cancer diagnosis and meet additional criteria, making family history-based genetic testing inaccessible to many patients, even those with a known BRCA mutation in the family.51 For private insurance, although the ACA mandated that BRCA testing for women with a personal or family history of cancer be covered without cost-sharing, individuals may face similar barriers in obtaining genetic testing. Before qualifying for ACA-mandated coverage, patients with a BRCA ancestry are required to undergo assessment by a familial risk assessment tool, and coverage may not be available to those with a smaller pedigree or a non-BRCA pathogenic mutation.52 After this screening, coverage is limited exclusively to in-network practitioners and genetic testing companies; this may limit which genes are tested.50

CONCLUSION

Gynecologic cancer survival has improved significantly in the past decade owing to new therapeutics, specialized training in radical surgery, and ongoing research efforts. Yet insurance coverage of these services lags behind. One third of women never see a gynecologic oncologist, and 50% of insured women experience financial toxicity, with greater disparities seen for Medicaid and Medicare patients. Interventions are needed at the ob-gyn, gynecologic oncologist, insurer, and national level. At the practice level, generalists can audit screening practices to ensure adequate screening across insurance types, build partnerships with community health centers, and streamline referrals to gynecologic oncologists. Gynecologic oncologists and cancer centers can work with local insurers to ensure network inclusion, partner with community health centers, and provide financial navigation to patients. At the national level, gynecologic oncology should be added to network adequacy standards, and low-cost coverage for follow-up of abnormal cervical cancer screening results and genetic testing should be expanded. Addressing these insurance-mediated disparities will be important to help our patients fully benefit from the scientific advances in our field and thrive after a gynecologic cancer diagnosis.

Footnotes

Dr. Smith's and Daniella Pena's work was funded by grants from the National Cancer Institute's Geographic Management of Cancer Health Disparities Program, the American College of Obstetricians and Gynecologists, and the University of Pennsylvania's Basser Center for BRCA.

Financial Disclosure: Emily M. Ko disclosed that money was paid to her institution from Tesaro. Money was paid to her from the University of Massachusetts Medical School. The other authors did not report any potential conflicts of interest.

Each author has confirmed compliance with the journal's requirements for authorship.

Peer reviews and author correspondence are available at http://links.lww.com/AOG/C541.

Figure.

No available caption

REFERENCES

- 1.Centers for Disease Control and Prevention. Gynecologic cancer incidence, United States—2012–2016. Accessed September 9, 2021. https://www.cdc.gov/cancer/uscs/about/data-briefs/no11-gynecologic-cancer-incidence-UnitedStates-2012-2016.htm [Google Scholar]

- 2.Gershman J, PharmD Cp. New developments for gynecologic cancers. Pharm Times 2021;3:30. [Google Scholar]

- 3.Pagliarulo N. GSK immunotherapy wins FDA approval, joining crowded cancer drug class. Accessed August 8, 2021. https://www.biopharmadive.com/news/gsk-jemperli-immunotherapy-fda-approval/598962/ [Google Scholar]

- 4.Goss E, Lopez AM, Brown CL, Wollins DS, Brawley OW, Raghavan D. American Society of Clinical Oncology policy statement: disparities in cancer care. 2009;27:2881–5. doi: 10.1200/JCO.2008.21.1680 [DOI] [PubMed] [Google Scholar]

- 5.Tolbert J, Orega K. Key facts about the uninsured population. Accessed August 8, 2021. https://www.kff.org/uninsured/issue-brief/key-facts-about-the-uninsured-population/ [Google Scholar]

- 6.Institute of Medicine (US) Committee on the Consequences of Uninsurance. Care without coverage: too little, too late. National Academies Press (US); 2002. [PubMed] [Google Scholar]

- 7.Howard DH, Tangka FKL, Royalty J, Dalzell LP, Miller J, O’Hara B, et al. Breast cancer screening of underserved women in the USA: results from the national breast and cervical cancer early detection program, 1998–2012. Cancer Causes Control 2015;26:657–68. doi: 10.1007/S10552-015-0553-0 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.DeGroff A, Miller J, Sharma K, Sun J, Helsel W, Kammerer W, et al. COVID-19 impact on screening test volume through the National Breast and Cervical Cancer Early Detection Program, January–June 2020, in the United States. Prev Med (Baltim) 2021;151:106559. doi: 10.1016/J.YPMED.2021.106559 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9.Smith AJB, Fader AN. Association of the Affordable Care Act with ovarian cancer care. Obstet Gynecol 2020;135:257–65. doi: 10.1097/AOG.0000000000003630 [DOI] [PubMed] [Google Scholar]

- 10.Albright BB, Nasioudis D, Craig S, Moss HA, Latif NA, Ko EM, et al. Impact of Medicaid expansion on women with gynecologic cancer: a difference-in-difference analysis. Am J Obstet Gynecol 2020;224:195.e1–17. doi: 10.1016/j.ajog.2020.08.007 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11.Sabatino SA, Thompson TD, White MC, Shapiro JA, de Moor J, Doria-Rose VP, et al. Cancer screening test receipt — United States, 2018. Morb Mortal Wkly Rep 2021;70:29–35. doi: 10.15585/MMWR.MM7002A1 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12.Medicare.gov. Part B costs. Accessed August 30, 2021. https://www.medicare.gov/your-medicare-costs/part-b-costs [Google Scholar]

- 13.Ward E, Halpern M, Schrag N, Cokkinides V, DeSantis C, Bandi P, et al. Association of insurance with cancer care utilization and outcomes. CA Cancer J Clin 2008;58:9–31. doi: 10.3322/CA.2007.0011 [DOI] [PubMed] [Google Scholar]

- 14.Coughlin SS, Caplan L, Young L. A review of cancer outcomes among persons dually enrolled in Medicare and Medicaid. J Hosp Manag Heal Policy 2018;2:36.. doi: 10.1200/JCO.2008.21.1680 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15.Liang MI, Chen L, Hershman DL, Hillyer GC, Huh WK, Guyton A, et al. Total and out-of-pocket costs for PARP inhibitors among insured ovarian cancer patients. Gynecol Oncol 2020;160:793–9. doi: 10.1016/j.ygyno.2020.12.015 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 16.Zhao G, Okoro C, Li J, Town M. Health insurance status and clinical cancer screenings among U.S. adults. Am J Prev Med 2018;54:e11–9. doi: 10.1016/J.AMEPRE.2017.08.024 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 17.Rosenkrantz AB, Fleming M, Duszak R. Variation in screening mammography rates among Medicare advantage plans. J Am Coll Radiol 2017;14:1013–9. doi: 10.1016/J.JACR.2017.01.056 [DOI] [PubMed] [Google Scholar]

- 18.Health Resources & Services Administration. Women's preventive services initiative. Accessed August 10, 2021. https://www.hrsa.gov/grants/find-funding/hrsa-21-045 [Google Scholar]

- 19.Moy B, Polite BN, Halpern MT, Stranne SK, Winer EP, Wollins DS, et al. American society of clinical oncology policy statement: opportunities in the patient protection and Affordable Care Act to reduce cancer care disparities. J Clin Oncol 2011;29:3816–24. doi: 10.1200/JCO.2011.35.8903 [DOI] [PubMed] [Google Scholar]

- 20.Sivashanker K, Bell G, Khorasani R, Lacson R, Lipsitz S, Neville B, et al. Electronic health record transition and impact on screening test follow-up. Jt Comm J Qual Patient Saf 2021;47:422–30. doi: 10.1016/J.JCJQ.2021.03.010 [DOI] [PubMed] [Google Scholar]

- 21.Medicaid and CHIP Payment and Access Commission, Holgash K, Heberlein M. Physician acceptance of new Medicaid patients. Accessed October 19, 2021. https://www.macpac.gov/publication/physician-acceptance-of-new-medicaid-patients-findings-from-the-national-electronic-health-records-survey/#:~:text=Similar%20to%20findings%20from%20MACPAC%E2%80%99s%20prior%20analysis%2C%20physicians,although%20acceptance%20varied%20by%20specialty%20and%20by%20state

- 22.Albright B, Delgado M, Latif N, Giuntoli R, Ko E, Haggerty A. Treat-and-Release emergency department utilization by patients with gynecologic cancers. J Oncol Pract 2019;15:E428–38. doi: 10.1200/JOP.18.00639 [DOI] [PubMed] [Google Scholar]

- 23.Doll KM, Khor S, Odem-Davis K, He H, Wolff EM, Flum DR, et al. Role of bleeding recognition and evaluation in Black-White disparities in endometrial cancer. Am J Obstet Gynecol 2018;219:593.e1–14. doi: 10.1016/j.ajog.2018.09.040 [DOI] [PubMed] [Google Scholar]

- 24.Doll KM, Hempstead B, Alson J, Sage L, Lavallee D. Assessment of prediagnostic experiences of Black women with endometrial cancer in the United States. JAMA Netw Open 2020;3:e204954. doi: 10.1001/jamanetworkopen.2020.4954 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 25.Evans L, Charns MP, Cabral HJ, Fabian MP. Change in geographic access to community health centers after Health Center Program expansion. Health Serv Res 2019;54:860–9. doi: 10.1111/1475-6773.13149 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 26.Chuang E, Pourat N, Chen X, Lee C, Zhou W, Daniel M, et al. Organizational factors associated with disparities in cervical and colorectal cancer screening rates in community health centers. J Health Care Poor Underserved 2019;30:161–81. doi: 10.1353/HPU.2019.0014 [DOI] [PubMed] [Google Scholar]

- 27.Doty MM, Abrams MK, Hernandez SE, Stremikis K, Beal A. Enhancing the capacity of community health centers to achieve high performance: findings from the 2009 Commonwealth Fund National Survey of Federally Qualified Health Centers. Commonwealth Fund; 2010. [Google Scholar]

- 28.Haggstrom D, Taplin S, Monahan P, Clauser S. Chronic Care Model implementation for cancer screening and follow-up in community health centers. J Health Care Poor Underserved 2012;23:49–66. doi: 10.1353/HPU.2012.0131 [DOI] [PubMed] [Google Scholar]

- 29.Minig L, Padilla-Iserte P, Zorrero C. The relevance of gynecologic oncologists to provide high-quality of care to women with gynecological cancer. Front Oncol 2015;5:308. doi: 10.3389/FONC.2015.00308 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 30.Shalowitz DI, Huh WK. Access to gynecologic oncology care and the network adequacy standard. Cancer 2018;124:2677–9. doi: 10.1002/cncr.31392 [DOI] [PubMed] [Google Scholar]

- 31.Weeks K, Lynch CF, West M, Carnahan R, O’Rorke M, Oleson J, et al. Rural disparities in surgical care from gynecologic oncologists among Midwestern ovarian cancer patients. Gynecol Oncol 2021;160:477–84. doi: 10.1016/j.ygyno.2020.11.006 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32.Centers for Medicare & Medicaid Services. Medicare-Medicaid plan (MMP) application & annual requirements. Accessed September 9, 2021. https://www.cms.gov/Medicare-Medicaid-Coordination/Medicare-and-Medicaid-Coordination/Medicare-Medicaid-Coordination-Office/FinancialAlignmentInitiative/MMPInformationandGuidance/MMPApplicationandAnnualRequirements [Google Scholar]

- 33.National Association of Insurance Commissioners. Network adequacy. Accessed August 8, 2021. https://content.naic.org/cipr_topics/topic_network_adequacy.htm [Google Scholar]

- 34.National Conference of State Legislatures. State insurance mandates and the ACA essential benefits provisions. Accessed August 8, 2021. https://www.ncsl.org/research/health/state-ins-mandates-and-aca-essential-benefits.aspx

- 35.Courtney-Brooks M, Pelkofski EB, Engelhard CL, Duska LR. The Patient Protection and Affordable Care Act: impact on the care of gynecologic oncology patients in the absence of Medicaid expansion in central Virginia. Gynecol Oncol 2013;130:346–9. doi: 10.1016/j.ygyno.2013.04.468 [DOI] [PubMed] [Google Scholar]

- 36.Warren JL, Butler EN, Stevens J, Lathan CS, Noone AM, Ward KC, et al. Receipt of chemotherapy among Medicare patients with cancer by type of supplemental insurance. J Clin Oncol 2014;33:312–8. doi: 10.1200/JCO.2014.55.3107 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 37.Gupta A, Khan AJ, Goyal S, Millevoi R, Elsebai N, Jabbour SK, et al. Insurance approval for proton beam therapy and its impact on delays in treatment. Int J Radiat Oncol Biol Phys 2019;104:714–23. doi: 10.1016/j.ijrobp.2018.12.021 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 38.Kelly MJ, Sung L, Dickens DS. Barriers to medication access in pediatric oncology in the United States. J Pediatr Hematol Oncol 2019;41:286–8. [DOI] [PubMed] [Google Scholar]

- 39.Kehl KL, Liao K-P, Krause TM, Giordano SH. Access to accredited cancer hospitals within federal exchange plans under the Affordable Care Act. J Clin Oncol 2017;35:645–51. doi: 10.1200/JCO.2016.69.9835 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 40.Esselen KM, Gompers A, Hacker MR, Bouberhan S, Shea M, Summerlin SS, et al. Evaluating meaningful levels of financial toxicity in gynecologic cancers. Int J Gynecol Cancer 2021;31:801–6. doi: 10.1136/IJGC-2021-002475 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 41.Wright J. Financial toxicity: a severe but underrecognized side effect for cancer patients. Gynecol Oncol 2019;154:1–2. doi: 10.1016/J.YGYNO.2019.06.005 [DOI] [PubMed] [Google Scholar]

- 42.Bouberhan S, Shea M, Kennedy A, Erlinger A, Stack-Dunnbier H, Buss MK, et al. Financial toxicity in gynecologic oncology. Gynecol Oncol 2019;154:8–12. doi: 10.1016/j.ygyno.2019.04.003 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 43.Harrison R, Fu S, Sun C, Zhao H, Lu KH, Giordano SH, et al. Patient cost sharing during poly(adenosine diphosphate-ribose) polymerase inhibitor treatment in ovarian cancer. Am J Obstet Gynecol 2021;225:68.e1–11. doi: 10.1016/J.AJOG.2021.01.029 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 44.Kaiser Family Foundation. An overview of the Medicare Part D prescription drug benefit. Accessed August 8, 2021. https://www.kff.org/medicare/fact-sheet/an-overview-of-the-medicare-part-d-prescription-drug-benefit/ [Google Scholar]

- 45.Goldsberry WN, Summerlin SS, Guyton A, Caddell B, Huh WK, Kim KH, et al. The financial burden of PARP inhibitors on patients, payors, and financial assistance programs: who bears the cost? Gynecol Oncol 2021;160:800–4. doi: 10.1016/J.YGYNO.2020.12.039 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 46.Yabroff KR, Valdez S, Jacobson M, Han X, Fendrick AM. The changing health insurance coverage landscape in the United States. Am Soc Clin Oncol Educ Book 2020:e264–74. doi: 10.1200/EDBK_279951 [DOI] [PubMed] [Google Scholar]

- 47.Bercow AS, Chen L, Chatterjee S, Tergas AI, Hou JY, Burke WM, et al. Cost of care for the initial management of ovarian cancer. Obstet Gynecol 2017;130:1269–75. doi: 10.1097/AOG.0000000000002317 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 48.Mandelker D, Zhang L, Kemel Y, Stadler ZK, Joseph V, Zehir A, et al. Mutation detection in patients with advanced cancer by universal sequencing of cancer-related genes in tumor and normal DNA vs guideline-based germline testing [published erratum appears in JAM 2018;320:2381]. JAMA 2017;318:825–35. doi: 10.1001/JAMA.2017.11137 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 49.Norquist BM. Challenges in the identification of inherited risk of ovarian cancer: where should we go from here? Gynecol Oncol 2019;152:3–6. doi: 10.1016/J.YGYNO.2018.12.003 [DOI] [PubMed] [Google Scholar]

- 50.American Society of Clinical Oncology. Genetic testing coverage & reimbursement. Accessed August 10, 2021. https://www.asco.org/news-initiatives/current-initiatives/genetics-toolkit/genetic-testing-coverage-reimbursement [Google Scholar]

- 51.FORCE. Medicare and Medicaid cover genetic testing for some people. Accessed March 1, 2021. https://www.facingourrisk.org/support/insurance-paying-for-care/genetic-services/medicare-medicaid

- 52.Moyer VA; U.S. Preventive Services Task Force. Risk assessment, genetic counseling, and genetic testing for BRCA-related cancer in women: U.S. Preventive Services Task Force recommendation statement. Ann Intern Med 2014;160:271–81. doi: 10.7326/M13-2747 [DOI] [PubMed] [Google Scholar]

- 53.State Health Access Data Assistance Center. SHADAC analysis of American Community Survey (ACS) public use microdata sample (PUMS) files. Accessed August 10, 2021. https://www.shadac.org/our-focus-areas/american-community-survey [Google Scholar]

- 54.Department of Health and Human Services. 2021 Medicare Parts A & B premiums and deductibles. Accessed December 13, 2021. https://www.cms.gov/newsroom/fact-sheets/2021-medicare-parts-b-premiums-and-deductibles [Google Scholar]