Abstract

Following the present scale of fiscal imbalances, governments often implement fiscal consolidation programs to restore macroeconomic stability. This paper empirically explores the connections between social expenditure, current account and fiscal consolidations using the system-GMM estimator, on a panel of 23 emerging and middle-income countries for the 2009–2018 period. Our results confirm that government social expenditure decreases once fiscal austerity measures are implemented, practically when they are spending-driven. Fiscal consolidation may hurt important social expenditure allocation mainly on education and health components. Furthermore, we find that fiscal consolidation improves the current account deficit, providing support for the twin deficits hypothesis. These findings indicate that fiscal consolidation will eventually contribute to medium- and long-term external debt stability through the current account improvement. However, the exclusion of key growth determinants such as human capital can lead to many inefficiencies such as weak competition in the provision of social services (Jafarov and Gunnarsson in Government spending on health care and education in Croatia: Efficiency and reform options, working paper 136, International Monetary Fund, 2008). We suggest rationalizing social spending and devoting the country’s revenue to necessary and economically productive projects. The efficient use of resources will thus ensure better quality of education and health care services. This calls for good governance, an adequate administration and effective delivery structures.

Keywords: Government expenditures, Social expenditures, Fiscal policy, Fiscal adjustment, Twin deficit hypothesis, Current account, Cyclically adjusted primary balance

Introduction

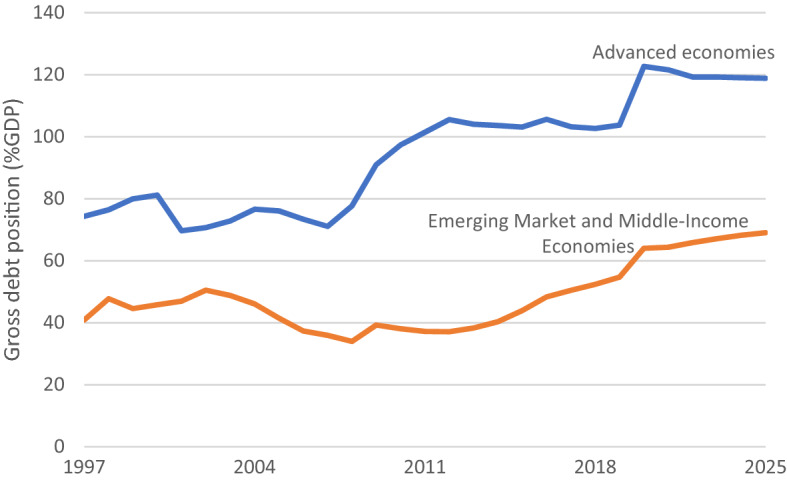

The 2009 global financial and economic great recession has struck the global economic activity. This crisis built-up historically high levels of public debt at a scale hardly ever seen before. Given the extreme severity of the crisis, many countries have been forced to adopt fiscal austerity programs. While debt ratios have generally declined in developed countries since that crisis, they still remain at very high levels in emerging countries. Recently, in early 2020, emerging market economies have faced a more dramatic economic and financial shock following the onset of the coronavirus (COVID-19) pandemic. Public debt ratio has been strongly hit by discretionary fiscal measures and has become increasingly immense. As shown in Fig. 1, public debt-to-GDP ratio across the word’s emerging market and middle-income economies rose from 40% of GDP in 2009 to 62% of GDP in 2020.

Fig. 1.

Public debt in percentage of GDP (1990–2025).

Source: Authors’ compilation from IMF Fiscal Monitor (October 2021)

Assessing the impact of public finances consolidation on output and other macroeconomic fundamentals such as consumption, investment and employment has been the main focus of the existing Fiscal consolidation literature. A large number of empirical studies have investigated the demand-side effects trying to identify the determinants, impact, timing and the length of fiscal consolidations (Alesina et al. 2008, 2019; Alesina and Ardagna 2010; Barrios et al. 2010; Cimadomo et al. 2010, 2012a, b; Sanz 2011; Agnello et al. 2013, 2015, 2016; Ball et al. 2013; Bi et al. 2013; Afonso and Jalles 2014, 2016; Agnello and Sousa 2014; Cugnasca and Rother 2015). Research has focused on several aspects of this relationship including the impact of fiscal consolidation on economic growth (Alesina et al. 2019), on income distribution (Agnello and Sousa 2014), or on governments ’chances of re-election (Hübscher 2016). Some studies show unambiguously that fiscal consolidation is costly. The cost of austerity is then amplified and the effectiveness of consolidation to achieve fiscal sustainability and economic growth is reduced. Alesina et al. (2015) confirm the absence of ‘non-Keynesian’ effects applying a seemingly unrelated regression model (SUR). The authors emphasize a milder negative effect of fiscal adjustments that are based on spending cuts rather than on revenue increases. Furthermore, Hernández de Cos and Moral-Benito (2013) employ a panel IV estimator and find a negative impact of fiscal adjustments on short-run economic growth regardless of the employed definition for fiscal adjustments. If countries had the opportunity to delay austerity measures, they would benefit from higher growth, but what would be the consequences on debt? (Blot et al. 2014).

Contrary to the conventional Keynesian wisdom which predicts negative short-run economic effects, fiscal consolidation is found to be expansionary with reference to output (Giavazzi and Pagano 1990). In literature, two types of consolidation (spending and tax-driven) have been taken into account (Alesina and Ardagna 1998, 2010; Alesina and Perotti 1995, 1997a, b, 1998; Gupta et al. 2005; McDermott and Wescott 1996; Afonso and Jalles 2012b, a; Heylen et al. 2013; Alesina and Ardagna 2013; Alesina et al. 2015, 2018). The fundamental result claims that fiscal consolidations led by spending cuts are more likely to generate growth than by tax increases. Nevertheless, using a narrative dataset of fiscal consolidation episodes in the Latin America and the Caribbean countries elaborated by David and Leight (2018), Carrière-Swallow et al. (2018) find that, contrary to the evidence obtained in advanced economies, the tax-based and spending-based fiscal multipliers are not significantly different one from another. The authors present further evidence indicating that the tax-based fiscal multiplier in Latin America and the Caribbean could be smaller in absolute value and less recessionary, than in OECD countries.

However, cutting crucial social spending on health and education should be carefully designed. By taking advantage of social expenditure allocation, it would be possible to optimize the effectiveness of fiscal consolidation, in order to avoid governments missing their fiscal targets. Indeed, it is crucial to combine the fiscal adjustment with structural reforms aimed to boost growth. Reductions in current spending in social sectors may have a larger negative effect on lower-income households and could adversely impact longer-term development prospects. It is apprehended that investment in education and health makes the labor force more productive and efficient, contributing therefore, to higher economic growth. Giving this context, a more disaggregated analysis proves that any economic reform especially linked to compression in public expenditure will adversely affect the vulnerable sections of the society. The very first question related to budgetary allocations of social sectors during the period of reforms have been widely discussed (Gupta and Sarkar 1994; Prabhu 1994; Panchamukhi 2000; Dev and Mooij. 2002; Sanz 2011). Nevertheless, one under-appreciated angle is the effect of fiscal adjustments periods which remains a widespread subject. The related literature shows that few studies have analyzed how fiscal consolidation affects expenditure composition which have given little attention to social costs during fiscal consolidation episodes (Castro 2017; Bamba et al. 2019). This has brought to the forefront the issue of transitional social costs during fiscal consolidation episodes.

H1

Social expenditures are negatively affected by fiscal consolidation.

The basic theoretical Ricardian equivalence hypothesis states that an increase in taxes leads to a reduction in budget deficit and subsequently not affect current accounts. This is because a decline in government savings does not affect consumption due to the fact that people tend to prefer hoarding, thus, private savings increase (Barro 1989). However, several studies have proven that fiscal consolidation through cutting expenditure or increasing taxes would be accompanied by an improvement in the current account (Bluedorn and Leigh 2011; Breuer and Nam 2020). Such predictions are in line with the so-called twin deficits hypothesis, which posits that fiscal consolidation can reduce external imbalances (Marinheiro 2008).

Governments emphasize the importance of fiscal consolidations as a requirement for two purposes. The first is to boot economic growth through its main determinants such as human capital. The second is to stabilize and bring down the debt-to-GDP ratio via current account increase. Given the large impact of the connection between social expenditure and current account on the economy, the contribution of this paper is threefold. First, to our knowledge, this paper is one of the first to empirically estimate the social expenditure effect of fiscal consolidations for emerging and middle-income countries. Our study attempts to specifically focus on the government expenditure and particularly social expenditure during fiscal consolidation episodes, a subject that has indeed received little attention in Castro (2017) and Bamba et al. (2019).

H2

Total expenditures are negatively affected by fiscal consolidation.

Beyond the fact that, conceptually, the distinction between education and health sectors is actually needed, this is a notable innovation compared to most previous studies on the effect of fiscal consolidation. Second, in case of fiscal consolidation episodes, we employ Alesina and Ardagna (2013)’s novel measure which has the advantage of considering the size and persistence of fiscal adjustment instead of a dummy variable (De Haan et al. 1996). Then, we use panel data techniques and apply modern system-GMM estimations of Blundell and Bond (1998) due to the inherent limitation of the fixed-effect model. This rigorous approach properly takes into account the observed and unobserved heterogeneity of countries and tackles endogeneity problems of some variables. Appreciably, compared with Castro (2017) and Bamba et al. (2019), we cover a longer sample size for the conventional method to the observations of fiscal adjustment periods that goes beyond 2010–2011, as we are able to include data on the global crisis years 2010–2013. Covering a more extensive time period is vital, since that fiscal consolidation measures have been a central feature of the global crisis management in several emerging countries in order to cut fiscal deficits and bring down public debt. Finally, there is little available evidence analyzing how social expenditure and current account are both affected by fiscal consolidations. This paper attempts to fill in this gap and link insights from the literature on the effects of fiscal consolidations on social expenditure with the evolution of the current account. Therefore, we conduct an empirical analysis of fiscal adjustment effect on the current account.

H3

Current account deficit is positively affected by fiscal consolidation.

The paper employs evidence from a sample of 23 emerging and middle-income countries over the period 2009–2018. Our findings reveal that fiscal consolidation strongly reduces social expenditure and simultaneously improves the current account. The effect also remains robust and relevant when taking into account alternative instruments and data restrictions. The remainder of the paper is organized as follows. “Literature Review” section reviews the theoretical and empirical literature on the effects of fiscal adjustments. “Data and Methodology” section introduces the data and empirical methodology. “Empirical Results” section discusses the empirical findings. “Robustness Check” section reports a robustness check of the results. Finally, “Conclusion” section concludes and presents useful policy recommendations.

Literature Review

Our paper builds on two strands of literature: the literature on the contractionary effect of fiscal consolidations on government expenditure and the literature on its effect on the current account.

The State of Social Expenditure During Fiscal Consolidation Episodes

In a typical Keynesian model with sticky nominal wages and prices, fiscal contraction is said to draw output reduction (Barro and Grossman 1971). Contrary to what is stated in the literature related to the Keynesian view, a large number of studies argue that there is a higher probability of fiscal policy being non-Keynesian in certain circumstances. According to this theory, episodes of fiscal consolidation contribute substantially to the acceleration of both aggregate demand and output even in the short term (Alesina and Ardagna 1998, 2010, 2012; Blanchard 1990; Alesina and Perotti 1995, 1997a, b; Giudice et al. 2007; McDermott and Wescott 1996; Lambertini and Tavares 2005; Afonso et al. 2006; Alesina et al. 2019). These researches have focused on several aspects of this relationship including the composition of fiscal consolidation. The main result reveals that fiscal consolidation via spending cuts is more likely to stimulate growth than a tax increase.

Relatively, little is known about the impact of fiscal consolidation on expenditure components in emerging and middle-income countries. In particular, the existing Fiscal consolidation literature does not provide clear guidance on whether social expenditures are protected during fiscal adjustment episodes in emerging economies. The basic underlying idea of social sectors’ budgetary allocations during the period of reforms has been widely discussed (Gupta and Sarkar 1994; Prabhu 1994; Panchamukhi 2000; Dev and Mooij. 2002; Sanz 2011). Yet, none of the aforementioned studies considers the available cyclical correction methods to identify the period of fiscal adjustment. For example, Sanz (2011) seeks to explain the link between the components of government expenditure and the government size, but does not identify fiscal consolidation episodes using the cyclically adjusted primary balance. Actually, the overall/general budget balance was the most common variable used in the literature to analyze fiscal adjustment effects. However, the general fiscal balance or the narrow balance approach assumes that changes in the budget balance are due to government’s discretionary fiscal policies (the internal factors), and so neglect cyclical fluctuations. Indeed, by definition, the actual budget balance has a pro-cyclical nature, which means that a reduction in public revenue must be necessarily accompanied by a reduction in public expenditures; thus, it does not allow fiscal policies to counteract recessionary periods as instead invoked by the classical stabilization function of the public sector (Musgrave 1959). As economic fluctuations subject government budget balance to subsequent rise and fall, it is important that laws of fiscal surveillance account for the impact of economic cycle on public finance. This broader approach adjusts for changes caused by internal, external and financial factors so as to remove the cyclical fluctuations which are beyond the direct control of the authorities. In fact, looking solely at changes in the fiscal balance can thus be misleading: these movements may lead to think of expansionary (or contractionary) discretionary policy actions, even though the changes are driven by cyclical factors. Furthermore, the structural budget balance allows to better define expansionary or contractionary fiscal policy, as it is a budgetary indicator independent of the economic cycle (Blanchard 1990; Chouraqui et al. 1990; Larch and Turrini 2010). This is why cyclical adjustment is applied, to filter the impact of cyclical movements on fiscal variables and assess the “underlying” fiscal stance”.

Some analysis explored these components but unfortunately, they were limited to a political perspective only (Potrafke 2010; Katsimi and Sarantides 2012; Enkelmann and Leibrecht 2013; Morozumi et al. 2014; Castro and Martins 2016). They analyze whether and how electoral motives, government ideology and political support affect the components of public expenditures, but they are silent regarding the fiscal consolidation’s aftermath. A few other papers have also evaluated the effect of fiscal consolidation on expenditure components. For example, Castro (2017) checked out the different components of government expenditure in 15 EU countries during the period 1990–2012. Using fixed effects estimator, he proves that spending on public services increases during fiscal consolidations, while spending on defense, public order, health, education and social protection is significantly cut. Also, Bamba et al. (2019) employed system-GMM estimations on a sample of 53 developed and emerging countries over 1980–2011 and assumes that fiscal consolidations significantly reduce the government investment-to-consumption ratio.

It is noteworthy to mention that incorporating evidence from emerging countries has a particular importance. In fact, developed countries tend to value the health and education sectors in the national expenditure plans compared to emerging countries.

Figure 2 depicts government expenditure by main components in advanced, emerging and developing economies. Social spending is significantly higher in developed economies. During 2005–2018, advanced economies allocated around 35% of their total spending on the social sector against only 25% in the case of emerging and developing countries (Fig. 2). Taking stock of these indications, it appears that analyzing how fiscal consolidations affect social spending, mainly education and health, is highly important for an adequate design of fiscal consolidation programs. This analysis represents a crucial step forward relatively to the previous literature, as it allows us to identify and understand which items inside the social components of public expenditure are being more significantly affected by the fiscal consolidation processes and, as so, infer about the social consequences in emerging countries.

Fig. 2.

Government Expenditure by main components (percent of GDP).

Source: Authors’ compilation from IMF, World Economic Outlook Database

H4

Health expenditures are negatively affected by fiscal consolidation.

H5

Education expenditures are negatively affected by fiscal consolidation.

The Twin Deficit Hypothesis: Fiscal Consolidation Versus Current Account

The determinants and the dynamics of the current account and fiscal deficit have been a topic of interest in open economy macroeconomics. Economic theory stipulate that the investigation of the budget and trade balance deficits nexus revolve around three different contradicting approaches, that is, twin deficit hypothesis, twin divergence phenomena and Ricardian Equivalence hypothesis. Studies in favor of the twin deficits, such as those by Roubini (1988), Miller and Russek (1989), Normandin (1999), Salvatore (2006), Daly and Siddiki (2009) explain the probability of an increase in budget deficit to cause an upsurge in current account deficit. The twin deficits hypothesis was first tested in the USA in the 1980s because trade deficit and budget deficit were experienced by the economy in question (Akbostanc and Tunc 2015).

Conversely, there are also studies supporting the twin divergence, such as those by Dewald and Ulan (1990), Erceg et al. (2005), Corsetti and Muller (2006), and Kim and Roubini (2008). They reveal the existence of an inverse relationship, where a cut in the budget deficit raising the current account deficit. Nevertheless, in between both theorems, there is the Ricardian's equivalence that occurs when an increase in budget deficit has no effect on trade deficit (Azgün 2012; Sakyi and Opoku 2016).

The Standard Keynesian macroeconomics theory introduces the expenditure approach as a method to measure the national income through the following equation:

| 1 |

We denote government purchases of goods and services by (G), consumption (C), investment (I), and net export value (NX). The twin deficit hypothesis supposes that if a country suffers a budget deficit (G > T), then it has to suffer a trade deficit as well (M > X), assuming S and I are constant. As showed by the Mundell–Fleming model, a large budget deficit will lead to a rise in interest rates and therefore to an increase in demand on the domestic currency; the resulting increased exchange rate will ultimately lead to a fall in exports and a rise in imports or in other words a current account deficit (Fleming 1962; Mundell 1963; Ball and Mankiw 1995; Dudley and McKelvey 2004). Emerging countries have run current account deficits for some years during the last decade. As evidenced in Fig. 1, the current account deficit has permanently increased from −3.12% of GDP in 2009 to −1.25% of GDP in 2018. Results support that current account deficits will affect the amount of net factor incomes. This clearly shows the equivalence between net exports (X-M) and current account balance (CA).

To illustrate the twin deficit hypothesis, note that T is taxes, we decompose total national savings (S) into public savings () and private savings () as follows:

| 2 |

| 3 |

Therefore,

| 4 |

From equation (4) we obtain:

| 5 |

According to equation (5), the current account is directly related to the government savings (T−G) which is defined as the difference between tax revenue collected from households and businesses and public expenditure. If domestic investment is entirely financed by private savings (SP ≈ I), all increase in the budget deficit (and in particular an increase in public expenditure over tax revenue) will positively affect the current account. Consequently, the current account and government balance must move together (twin deficits). Keynes’s absorption theory explains the positive relationship between budget and current account deficit. According to this theory, an increase in budget deficit may causes an upsurge in aggregate demand, thus, further encouraging imports, and current account deficit (Marinheiro 2008). The pattern of this relationship is also explained through Mundell–Fleming's concept. His model emphases changes in terms of trade and interest rates. It asserts that an increase in budget deficit will cause an upward shift in interest rate and exchange rate, which drives up domestic savings, therefore, deteriorates the balance of the trade balance.

One part of the literature on fiscal consolidation effect sheds light on the relationship between fiscal policy changes and current account. Most studies predominantly seek to test empirical validity of the twin deficit nexus. Summers (1986), Alesina et al. (1991), Abbas et al. (2010), and Gagnon (2011) reveal that such a twin deficit link is rather negligible or even non-existent. They show that the relationship between fiscal consolidation expressed in terms of GDP and the reduction of the current account deficit-to-GDP ratio reach only 1 percent to 0.1 and 0.3 percentage points. Moreover, Bluedorn and Leigh (2011) use the narrative approach from Devries et al. (2011), to identify consolidations. They find that a 1 percent of GDP fiscal consolidation reduces the current account deficit-to-GDP ratio by about 0.6 percentage points. Breuer (2019) focuses on the incomplete cyclical adjustment problem and proposes a new version of the “Blanchard measure” for cyclical adjustment of budget data (refer to Blanchard 1990) or using Girouard and André (2005) methods.

Data and Methodology

Data

Annual data for the cyclically adjusted primary balance1 (CAPB) are collected from the IMF World Economic Outlook (WEO) database (April 2020). CAPB data are not available for a number of countries in 2009–2018 period. Therefore, missing data were obtained from the WEO database (April 2014)2 for 6 countries (Kenya, Lithuania, Bulgaria, Jordan, Romania, South Africa).

It must be recognized that several possibilities are available to define a fiscal consolidation episode. According to Feldstein (1986) and Blanchard (1990), it is inappropriate to use the current budget deficit. Indeed, several components of government budget are influenced by the macroeconomic stance in ways that operate to smooth the business cycle, acting as automatic stabilizers. For example, the unemployment benefit system: in a recession the growing payment of unemployment benefits supports demand and the other way around occurs in an upswing. If governments allow an automatic fiscal stabilizer to work fully in a recession period, the stabilizers may lead to a bias toward weak underlying budget positions. In fact, when economic activity slows down, revenues are negatively affected and spending may increase automatically, such as unemployment benefits, which results in a deterioration of the fiscal balance. Looking solely at changes in the fiscal balance can thus be misleading: these movements may give an impression of expansionary (or contractionary) discretionary policy actions, even though the changes are driven by cyclical factors. This is why cyclical adjustment is applied, to filter the impact of cyclical movements on fiscal variables and assess the “underlying” fiscal stance (IMF 2009).

Hagemann (1999) defines the structural fiscal balance as the residual balance after removing the balance of the estimated budgetary consequences of the business cycle. The purpose of cyclical adjustment is to make a correction for the influence of the economic cycle on the public finances and leads to a measure that better reflects the underlying, or structural, budgetary position. In particular, the structural budget balance allows to better define expansionary or contractionary fiscal policy, as it is a budgetary indicator independent of the economic cycle (Blanchard 1990; Chouraqui et al. 1990; Larch and Turrini 2010). Estimating the cyclical component of the budget generally involves trying to measure: (i) where the economy stands in relation to its potential or trend level; and (ii) how different components of the budget normally respond to fluctuations in economic activity.

Therefore, the calculation of the CAPB is advantages, as it provides a clearer picture of the underlying fiscal situation by removing the influence of cyclical fluctuations. As a result, it can be used to guide fiscal policy analysis. Finally, the CAPB becomes the most common variable used in the literature as the corrected measure to show the underlying fiscal position when cyclical or automatic movements are removed.

The basic empirical studies (such as Alesina and Ardagna 1998; Ardagna 2004; Giudice et al. 2007) exploring the effect of fiscal adjustments adopt a regression with a dummy variable of changes in CAPB. In fact, we follow Alesina and Ardagna (2013)’s novel measure of fiscal consolidations that links the amplitude and the persistence of the CAPB/GDP change to the size of the adjustment. They define a fiscal consolidation as a two-year period in which the cyclically adjusted primary balance-to-GDP ratio improves each year and the cumulative improvement is at least 2 percentage points of GDP.

This method apparently does not select all instances of fiscal consolidation existing within the 48 Emerging and middle-income countries dataset provided by the WEO database (April 2020) for the CAPB over the 2009–2018 period. In limited cases, a number of countries do not actually implement any consolidation, or they implement a fiscal adjustment that notably fall short of Alesina and Ardagna (2013)’s council recommendation. Hence, we keep only countries that possess at least one identified fiscal consolidation episode. Subsequently, the impact of fiscal consolidation on social expenditure is estimated using annual data of 23 countries with 32 episodes. Table 6 in appendix reports the number of fiscal adjustment episodes and their occurrence dates for each country in our sample.

Table 6.

Episodes of fiscal consolidations

| Countries | Adjustment periods | Number |

|---|---|---|

| Algeria | 2011; 2013; 2017–2018 | 3 |

| Argentina | 2018 | 1 |

| Chile | 2011 | 1 |

| Colombia | 2012 | 1 |

| Croatia | 2009; 2013; 2015–2017 | 3 |

| Dominican Republic | 2014 | 1 |

| Ecuador | 2017–2018 | 1 |

| Egypt | 2017–2018 | 1 |

| Hungary | 2009–2010; 2012–2013 | 2 |

| India | 2004–2007; 2013 | 2 |

| Malaysia | 2011 | 1 |

| Mexico | 2017–2018 | 1 |

| Morocco | 2014 | 1 |

| Peru | 2011 | 1 |

| Philippines | 2012 | 1 |

| Russian fed | 2012–2013; 2017–2018 | 2 |

| Ukraine | 2009; 2014–2016 | 2 |

| Poland | 2012 | 1 |

| Bulgaria | 2012 | 1 |

| Jordan | 2011; 2013–2015 | 2 |

| Romania | 2010–2013 | 1 |

| South Africa | 2009 | 1 |

| Lithuania | 2010–2013 | 1 |

| Total | 32 |

The analysis developed in this study is based on government expenditure as variable of interest while accounting for the effect of a set of control variables namely debt (debt), real growth (gdpg) and corruption (corrp). Besides, to inspect the impact of the structure of the population (demographic issues) on government expenditure, two additional variables are considered: population aging 65 years and more (eldy) and population between 0 and 14 years of age (young). Table 7 reports the sources and definitions of control variables. Table 8 in the Appendix reports the descriptive statistics of control variables. The results reveal that the dispersion of our data variables ranges from 0.6366 for corrup to 9.0819 for Texp. Descriptive statistics also indicate that the average level ranges from −1.7296 for CA to 32.1907 for Texp. It is negative for CA and positive for other variables. Pearson correlation coefficients are summarized in Table 9 in the appendix. The results show that the highest correlation coefficient, in absolute value, between young and eldy (0.7694). According to Kennedy (2008), the multicollinearity is a serious problem if correlation coefficient between two independent variables is above 0.8. Consequently, the computed correlation coefficients in our setting imply that there is enough statistical evidence to support no multicollinearity between all variables involved.

Table 7.

Description of the variables

| Variables | Descriptions | Sources |

|---|---|---|

| Texp | Total government expenditure in % of GDP | WDI database |

| Sexp | Social government expenditure in % of GDP | Authors’ estimations based on WDI database |

| CA | Current account in % of GDP | WDI database |

| G_health | Government expenditure on health in % of GDP | WDI database |

| G_educ | Government expenditure on education in % of GDP | WDI database |

| Fa | Change in CAPB in fiscal consolidation stance and zero otherwise | Authors’ estimations based on WEO dataset: IMF fiscal monitor (October 2020; April 2014) |

| growth | Real GDP growth rate | WDI database |

| eldy | Population with 65 or more years of age in % of total population | WDI database |

| young | Population between 0 and 14 years of age in % of total population | WDI database |

| debt | Total debt in % of GDP | WDI database |

| corrup | Corruption index | ICRG Database |

(i) WDI: World Development Indicators; (ii) WEO: World economic outlook; (iii) ICRG: International Country Risk Guide

Table 8.

Summary statistics

| Obs | Mean. | Std.Dev. | Min. | Max. | |

|---|---|---|---|---|---|

| Texp | 229 | 32.1907 | 9.0819 | 15.7988 | 50.6404 |

| Sexp | 229 | 7.93386 | 2.0567 | 1.8565 | 12.6005 |

| CA | 229 | −1.7296 | 4.2452 | −16.3780 | 15.7230 |

| health | 229 | 3.7142 | 1.4007 | 0.8565 | 6.8244 |

| educ | 229 | 4.2492 | 1.1114 | 1 | 7.3180 |

| growth | 228 | 5.3845 | 8.4186 | −14.8386 | 48.1109 |

| Corrupt | 207 | 2.4546 | 0.6366 | 1.5 | 4.5 |

| Fa | 229 | 0.3594 | 1.0872 | 0 | 11.5071 |

| Eldy | 229 | 10.0664 | 5.2911 | 3.40229 | 21.0219 |

| Young | 229 | 23.9882 | 7.1856 | 13.4963 | 37.62320 |

Table 9.

The matrix of Pearson correlation coefficients

| Texp | Sexp | CA | Health | Education | fa | |

|---|---|---|---|---|---|---|

| Texp | 1.0000 | |||||

| Sexp | 0.5429* | 1.0000 | ||||

| CA | 0.0372 | −0.1142 | 1.0000 | |||

| health | 0.4284* | 0.8291* | −0.1858* | 1.0000 | ||

| education | 0.4339* | 0.7174* | 0.0061 | 0.2264* | 1.0000 | |

| fa | 0.1704* | 0.0400 | 0.0708 | 0.0606 | −0.0135 | 1.0000 |

| debt | 0.3119* | 0.0660 | −0.0995 | −0.0091 | 0.1225 | 0.0187 |

| gdpg | −0.2938* | −0.1539* | 0.0698 | −0.0914 | −0.1683* | −0.1290 |

| corrupt | −0.0310 | 0.1115 | 0.0098 | 0.1262 | 0.1000 | −0.0766 |

| young | −0.4859* | −0.3300* | −0.2683* | −0.3659* | −0.1395* | −0.0927 |

| eldy | 0.2639* | 0.2327* | 0.3077* | 0.2316* | 0.1256 | 0.0112 |

| debt | gdpg | corrupt | young | eldy | ||

|---|---|---|---|---|---|---|

| debt | 1.0000 | |||||

| gdpg | −0.1764* | 1.0000 | ||||

| corrupt | 0.0150 | −0.0294 | 1.0000 | |||

| young | 0.0951 | −0.1535* | −0.1186 | 1.0000 | ||

| eldy | 0.0853 | 0.2822* | 0.1299 | −0.7694* | 1.0000 |

*Indicates statistical significance at the 5% level. Source: Stata: authors’ calculations

The choice of control variables is dictated by their ability to provide information regarding the shift in social allocation budget in response to fiscal adjustments. Except for real growth, all variables are in ratio of GDP. For an additional robustness check, we carry out further analysis in splitting social government (Sexp) expenditure into two components: (i) health expenditure (G_health) and (ii) education (G_educ) expenditure. In this study, we take a narrow definition of social spending that includes social government expenditure in education and health only. In fact, compared to other social expenditures, it is proven that these sectors are key growth indicators. The total general government expenditures (Texp), current account (CA), social expenditure, and each of the two components are used as dependent variables in separate regressions.

Methodology

Consider the following baseline dynamic panel econometric model:

| 6 |

with denotes the dependent variable of country at time point . It refers to either total, social, education, or health expenditure or current account. represents the variable of interest, fiscal consolidation episodes. is the vector of control variables as explained in the previous section. Finally, accounts for country-specific effects, and is the idiosyncratic error term.

As described above, to investigate the link between the government expenditure and fiscal consolidation episodes, we evaluate the coefficients of our variables using adequate econometric techniques. In the first stage, we estimate the panel data model using the pooled ordinary least square (POLS) and panel fixed effects (FE) approaches. The Hausman test is performed beforehand to determine the suitability of either fixed- or random-effects. The relevance of FE is established in both regressions (Table 1). However, the POLS and FE approaches have several shortcomings. There are a number of sources of biases that can cause inconsistent estimates of the coefficients in panel regressions. The first is the omitted-variables bias (so-called heterogeneity bias) resulting from possible correlation between country-specific fixed effects and the regressors, affecting the consistency of pooled OLS estimates. The second is the endogeneity problem due to potential correlation between the regressors and the error term, which would affect the consistency of pooled OLS and FE estimates (Woo and Kumar 2015). In the context of dynamic panels, there is a dynamic panel bias which will make FE estimates inconsistent. The third is classical measurement errors (errors in variables) in the independent variables, which affects the consistency of pooled OLS and FE estimator, although the bias tends to be exacerbated in FE. Specifically, the FE addresses the problem of the omitted-variables bias via controlling for fixed effects, but tends to exacerbate the measurement error problem, relative to OLS estimator. This measurement error bias under FE tends to get even worse when the explanatory variables are more time-persistent than the errors in the measurement (Hauk and Wacziarg 2009).

Table 1.

The effect of fiscal consolidation on total and social expenditure (POLS and FE)

| POLS | FE | |||

|---|---|---|---|---|

| (1) | (2) | (1) | (2) | |

| Total expenditure | Social expenditure | Total expenditure | Social expenditure | |

|

0.969*** (0.013) |

0.929*** (0.042) |

0.507*** (0.089) |

0.506*** (0.091) |

|

|

−0.464*** (0.135) |

−0.147*** (0.051) |

−0.459*** (0.104) |

−0.128*** (0.049) |

|

|

−0.041* (0.025) |

−0.002 (0.004) |

−0.411** (0.052) |

−0.037** (0.016) |

|

|

−0.126 (0.166) |

−0.020 (0.066) |

−1.449** (0.536) |

−0.217 (0.203) |

|

|

−0.010* (0.006) |

−0.004** (0.001) |

−0.049* (0.027) |

−0.013* (0.008) |

|

|

−0.027 (0.031) |

0.012 (0.010) |

−0.112 (0.278) |

0.123 (0.121) |

|

| −0.041* | −0.011 | 0.076 | 0.059 | |

| (0.023) | (0.007) | (0.154) | (0.074) | |

| constant |

3.317*** (1.191) |

1.234** (0.482) |

21.627*** (5.261) |

2.619* (2.434) |

| N | 207 | 207 | 207 | 207 |

| R-squared | 0.959 | 0.867 | 0.448 | 0.340 |

| groups | 23 | 23 | 23 | 23 |

| Hausman | 15.04** | 16.84*** | ||

Robust standard errors are in parentheses Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***. The dependent variable is total government spending in model (1) and social spending in model (2)

Furthermore, in the dynamic panel setting, the within-transformation in the estimation process of FE introduces a correlation between transformed lagged dependent variable and transformed error, which also makes FE inconsistent. Consequently, we extend our approach and estimate a dynamic panel data model by applying the SGMM (System Generalized Method of Moment) approach of Blundell and Bond (1998) for the following reasons. First, in the presence of country-fixed effects, OLS leads to biased and inconsistent estimates, since they do not account for country-unobserved heterogeneity (for example influence of economic specificities and environmental policies, etc.). However, the GMM estimations in first difference and in system deal with the above-mentioned potential source of correlation. Second, due to measurement errors,3 the main concern that needs to be addressed in POLS and FE methods is the endogeneity problem. The difference GMM method may be useful in dealing with such issues. However, it tends to produce unsatisfactory results if correlations between differenced lagged dependent variables and their instrumental variables are weak (Mairesse, and Hall 1996). To reduce this problem, the use of instrumental variables is highly recommended. Arellano and Bover (1995) and Blundell and Bond (1998) suggest including lagged levels as instruments for equations in first differences. This system of equations is estimated simultaneously by the SGMM. Finally, the SGMM remains more consistent and efficient compared to the difference GMM estimator which has poor finite sample properties in the presence of highly persistent variables over time (Blundell and Bond 1998; Blundell et al. 2001).

Empirical Results

The Fiscal Consolidation Impact on Total and Social Expenditure

This section presents the baseline regression results using both POLS and panel FE estimations. The results of our estimation approaches are reported, respectively, in Tables 1, 2 and 3. We estimate two main sets of equations pertaining to each government expenditure measure (total and social expenditure). Knowing that, while POLS and FE estimates are inconsistent due to the presence of a lagged dependent variable as an explanatory variable, they can be helpful when specifying the SGMM estimator. Bond (2002) emphasizes that allowing for dynamics may be crucial to identify the stability of the SGMM.

Table 2.

The effect of fiscal consolidation on total expenditure

| Dynamic Panel Estimation SGMM | ||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

|

0.613*** (0.201) |

0.462*** (0.134) |

0.479*** (0.181) |

0.769*** (0.086) |

0.701*** (0.107) |

0.725*** (0.117) |

|

|

−0.485*** (0.124) |

−0.548*** (0.104) |

−0.517*** (0.075) |

−0.626*** (0.077) |

−0.595*** (0.090) |

−0.622*** (0.106) |

|

|

−0.165** (0.076) |

−0.149** (0.067) |

−0.210*** (0.050) |

−0.230*** (0.056) |

−0.233*** (0.062) |

||

|

−0.695 (1.558) |

−1.566* (0.927) |

−2.656** (0.994) |

−2.868*** (1.016) |

|||

|

0.016 (0.022) |

−0.024 (0.028) |

−0.025 (0.041) |

||||

|

0.373** (0.161) |

0.134 (0.314) |

|||||

|

−0.214 (0.269) |

||||||

| N | 230 | 229 | 207 | 207 | 207 | 207 |

| groups | 23 | 23 | 23 | 23 | 23 | 23 |

| N-instr | 10 | 15 | 17 | 19 | 21 | 23 |

| AR(1) | 0.003 | 0.013 | 0.009 | 0.002 | 0.002 | 0.002 |

| AR(2) | 0.322 | 0.360 | 0.419 | 0.442 | 0.387 | 0.405 |

| Hansen | 0.764 | 0.737 | 0.606 | 0.111 | 0.232 | 0.393 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. Starting from the most parsimonious specification (column 1), we progressively introduce GDP growth, corruption, public debt, eldy and young population in columns (2)–(6) Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***

Table 3.

The effect of fiscal consolidation on social expenditure

| Dynamic Panel Estimation SGMM | ||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

|

0.800*** (0.180) |

0.756*** (0.189) |

0.843*** (0.136) |

0.897*** (0.079) |

0.881** (0.094) |

0.882*** (0.086) |

|

|

−0.13*** (0.048) |

−0.160*** (0.043) |

−0.152*** (0.041) |

−0.156*** (0.047) |

−0.158*** (0.047) |

−0.158*** (0.047) |

|

|

−0.046** (0.022) |

−0.043* (0.023) |

−0.041* (0.023) |

−0.043** (0.020) |

−0.045** (0.021) |

||

|

−0.028 (0.271) |

−0.041 (0.267) |

−0.160 (0.220) |

−0.169 (0.230) |

|||

|

−0.011* (0.006) |

−0.015** (0.007) |

−0.015** (0.007) |

||||

|

0.031 (0.026) |

0.043 (0.035) |

|||||

|

0.011 (0.022) |

||||||

| N | 230 | 229 | 207 | 207 | 207 | 207 |

| groups | 23 | 23 | 23 | 23 | 23 | 23 |

| N-instr | 6 | 11 | 15 | 19 | 15 | 21 |

| AR(1) | 0.050 | 0.048 | 0.047 | 0.031 | 0.035 | 0.034 |

| AR(2) | 0.128 | 0.103 | 0.159 | 0.133 | 0.135 | 0.134 |

| Hansen | 0.2016 | 0.146 | 0.296 | 0.473 | 0.432 | 0.442 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. Starting from the most parsimonious specification (column 1), we progressively introduce GDP growth, corruption, public debt, eldy and young population in columns (2)–(6). Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***

It is well known that the OLS and FE estimators are likely to be biased in the opposite direction in the context of lagged dependent variables in short panels, with OLS biased upwards, and FE downwards. The SGMM autoregressive coefficients should lie between the two (Bond 2002). Consistent with this reasoning, in both SGMM specifications, the estimated autoregressive coefficients are, respectively, 0.725 and 0.882 (Tables 2 and 3). They are between the POLS coefficients of total and social expenditure (0.969 and 0.929) and the FE coefficients (0.507 and 0.506) (Table 1). Consequently, the reported SGMM estimate in Tables 2 and 3 are likely to be consistent parameter estimates of the convergence rate.

As noted by Roodman (2009), the implementation of the difference and SGMM generates a large number of instruments, which weakens the Hansen test. To overcome the proliferation of instruments, following Roodman (2009) recommendation, we collapse the instrument matrix to limit the number of instruments compared to countries. The SGMM model is useful for estimations in small samples (Baltagi 2008). Thus, we confirm the validity of SGMM by ensuring that the number of cases (N) is greater than the time dimensions (T). In addition, the use of the SGMM estimator is equally supported by usual diagnostic tests, namely valid instruments using the Hansen test, and the presence (absence) of first-order (second-order) autocorrelation in the dependent variable using the AR(1) (AR(2)) test. These diagnostic tests are equally valid (Tables 2, 3 and 4).

Table 4.

The effect of fiscal consolidation on current account

| Dynamic Panel Estimation SGMM | ||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

|

1.136*** (0.238) |

0.750*** (0.222) |

0.808*** (0.214) |

0.785*** (0.198) |

0.797** (0.094) |

0.772*** (0.208) |

|

|

0.760** (0.324) |

0.774*** (0.284) |

7757** (0.322) |

0.797 ** (0.327) |

0.812** (0.333) |

0.793** (0.323) |

|

|

−0.183* (0.101) |

0.147* (0.085) |

0.190** (0.097) |

0.219** (0.112) |

0.164** (0.084) |

||

|

−0.131 (0.233) |

−0.132 (0.359) |

−0.906 (0.431) |

−0.161 (0.338) |

|||

|

0.026 (0.178) |

0.030 (0.025) |

0.029 (0.023) |

||||

|

−0.036 (0.108) |

−0.118 (0.147) |

|||||

|

−0.111* (0.064) |

||||||

| N | 207 | 206 | 184 | 184 | 184 | 184 |

| groups | 23 | 23 | 23 | 23 | 23 | 23 |

| N-instr | 6 | 8 | 9 | 10 | 11 | 12 |

| AR(1) | 0.019 | 0.054 | 0.044 | 0.039 | 0.049 | 0.048 |

| AR(2) | 0.570 | 0.606 | 0.561 | 0.544 | 0.545 | 0.525 |

| Hansen | 0.157 | 0.538 | 0.479 | 0.511 | 0.527 | 0.525 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. Starting from the most parsimonious specification (column 1), we progressively introduce GDP growth, corruption, public debt, eldy and young population in columns (2)–(6). Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***

As expected, the results reported in Tables 1 and 2 indicate that, in all panel data estimations, fiscal consolidations significantly decrease the total government expending. Actually, fiscal adjustment strategy is based on expenditure cuts targets which is not a surprising result. Nevertheless, our analyses aim mainly at estimating public spending components and particularly social expenditure. A primary interest regarding these results is to check how social spending may be affected when total expenditure is reduced. Interestingly, using the social expenditure as dependent variable, the coefficient of the fiscal consolidation variable does not show any systematic changes when we introduce control variables to the model as reported in Table 3. They are still negative and highly statistically significant, confirming a long-run negative relationship between fiscal consolidations and government social expenditure. It is clear that despite the imperative need to enhance allocations to social sectors, there has been a deceleration of social expenditure across the considered 23 emerging and middle-income states. Findings highlight those social expenditures are more sensitive to debt shocks than other expenditures, mainly because they are more severely affected by fiscal consolidation. The current finding, therefore, lends support to the popular belief that the structural adjustment programs are more likely to reduce spending in the social sectors, particularly education and health. As a result, social expenditure in emerging countries has remained relatively flat at around 6.33% and 8.12% of GDP during the period 2005–2018. It has registered a slight decline from 8.12% of GDP in 2013 to 7.08% of GDP in 2018 (Fig. 3).

Fig. 3.

Emerging Economies: General Government Expenditures, 2005–2018 (Percent of GDP).

Source: Authors’ compilation from IMF, World Economic Outlook Database

This is also consistent with the argument that an important part of public expenditures is generally financed through public debts. Once governments incur a high public debt due to an economic recession, they usually resort to reduce social expenditures (Fosu 2007; Lora and Olivera 2007). In contrast, our findings contradict the results from Alun (2006), who showed that debt relief can boost social expenditures in Heavily Indebted Poor Countries. According to Alun (2006), low-income countries have managed to fully protect social expenditures from the effects of budgetary consolidation over the past two decades, while middle-income countries have shown a strong inverse relationship with social expenditures.

The IMF (2013) shows that most of emerging countries create more public jobs for education and health care sectors which are relatively less productive. The use of such measures to pursue social goals is considered misguided as it may lead to overstaffing problem and unnecessarily high costs. This is the answer to simultaneously explain the need for social spending cuts in emerging counties. A further argument is that the category of public expenditure itself may produce pressure on budgetary allocation shifts. Indeed, compared to education and health spending, social security and military government expenditure, by their very nature, are often seen as quite inflexible aggregates during fiscal adjustments. These findings are broadly in line with Castro (2017) confirming that education and health spending are the bigger and more ‘visible’ categories on which governments tend to spend more in proportion to the total expenditure during elections.

With respect to our extended set of control variables, we examine the effects of the fiscal adjustment on social expenditure obtained using SGMM. The results show that GDP growth rate (growth) has a negative and significant impact on social spending (Sexp). Meanwhile, governments tend to decrease social public expenditures during economic expansion. Following Guseh (1997) and Abu-Bader and Abu-Qarn (2003), it is possible that this behavior is an outcome of the crowding out effect. This scenario occurs when higher government spending leads to an undesirable or negative impact on growth, which shows that the desired stimulus on economic growth could be created through social expenditure decrease. Similar effect is observed in what concerns the public debt variables, indebtedness is also found to have significant decrease in social expenditure. Moreover, these results confirm Lora and Olivera (2006) conclusions that higher debt ratios do reduce social expenditures when using an unbalanced panel of around 50 countries over the period 1985–2003. In particular, they show evidence that this effect comes mostly from the stock of debt rather than from debt service payments. Finally, corruption, elderly and young population do not seem to matter much for the evolution of public social spending. This might be the case because corruption problem is only a form of wrong economic relations violating the fundamental laws of economic development but it does not produce a damaging effect on social expenditure. Besides, additional political and economic reasons, other than the structure of population, may play a more important role in the fluctuations of social public spending components.

The Impact of Fiscal Consolidation on Current Account

In an attempt to shed some light on the foreign debt crisis in emerging countries, it seems appropriate to analyze budget deficit and the current account deficit which are together called the twin deficits. This relationship is equally investigated using the SGMM. Results reported in Table 4 show that the effect of fiscal consolidations significantly improves the CA on average, even in the presence of different control variables. As already mentioned, a decrease in fiscal deficit tends to create a current account expansion, thus providing support for the twin deficits hypothesis. This result is in line with Breuer and Nam (2020) findings as they show that most of the twin deficit linkage is driven by cases of fiscal consolidation rather than expansionary policies. They find empirical evidence supporting the twin deficit hypothesis using “new” strategy to adjust for cyclical effects. In particular, these authors distinguish between revenue- and spending-based adjustments and argues that the twin deficit link is especially pronounced for expenditure-based consolidations.

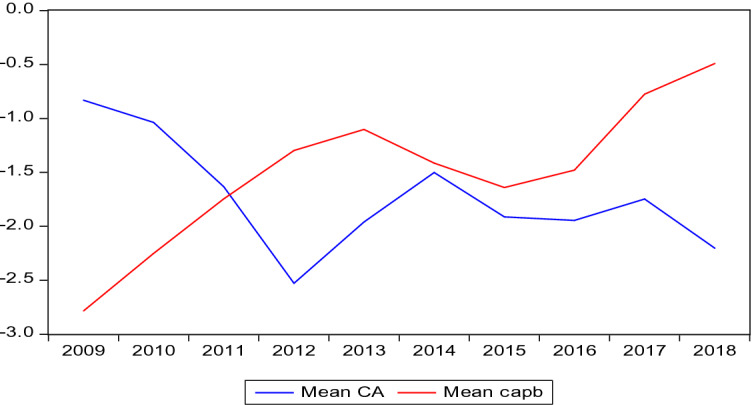

As reported in Fig. 4, this condition occurs simultaneously with budget deficit, which was experienced within 2011–2017. Actually, the change in the CAPB may reflect an explicit policy response to the current account balance. Note that the CAPB deteriorates during economic expansions and improves during downturns. According to Fig. 4, the current account increases with a value of −2.5% to −2.2% of GDP on instances where the CAPB improves as means to decrease the fiscal deficit.

Fig. 4.

Conditions of Cyclically Adjusted primary balance and Current Account Deficit in emerging countries over 2009–2018.

Source: Authors’ compilation from WDI database

The underlying reason to explain this fact is that government tend to sacrifice its government savings, particularly social spending, and increase in taxes to obtain a grow level of current account increase. From a theoretical viewpoint, the current account deficit is financed by foreign borrowing in order to cover the budget deficit and the excess of domestic investment over domestic saving (Gordon 2003). This is usually associated with public finances improvement. In view of this effect, we therefore infer that in spite of the human capital decrease, fiscal consolidation consents to assess the likelihood of future external debt distress.

Robustness Check

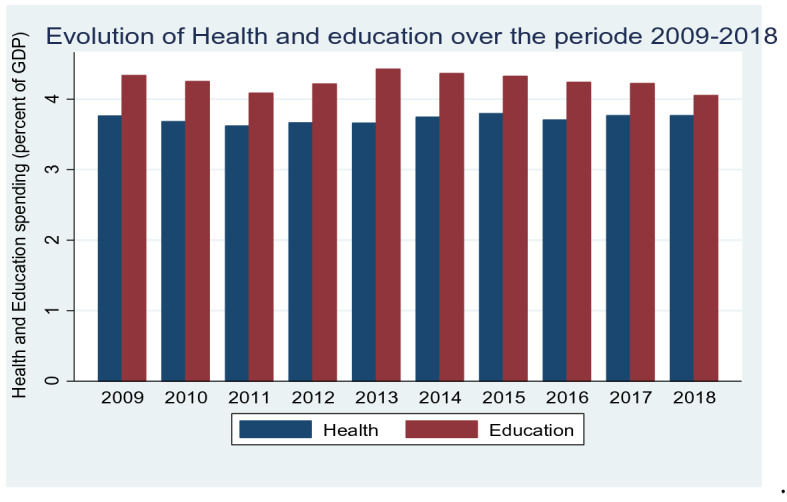

In this section, a variety of robustness checks were conducted to check there are significant changes in the estimated coefficients. A first concern is to examine the effect of fiscal adjustment on social expenditure incurred on education and health sectors. To this purpose, we re-estimate our specification with the additional depending variables. It is obvious from Table 5 that the declining trend in the expenditures can be significantly noticed during fiscal consolidation episodes. Meanwhile, fiscal adjustment program hurt government social expenditure allocations mainly in education and health components. By the same token, estimation results show that the decline in education expenditures is found to be stronger than the contraction of health expenditures (Table 5). According to Fig. 5, health spending has stagnated over the period 2009–2018 in emerging countries. It did not exceed 3.8% of GDP (Fig. 5). Additionally, Fig. 5 shows that education expenditure recorded a significant decline during the last decade reaching a level of 4% in 2018. This amounts to a fall of 0.5 percentage points from the level of 4.5% achieved in 2009.

Table 5.

The effect of fiscal consolidations on social expenditure components

| (1) G_health |

(2) G_educ |

|

|---|---|---|

| 0.880*** (0.073) | 0.899*** (0.147) | |

| −0.052*** (0.017) | −0.107** (0.047) | |

| −0.035*** (0.005) | −0.002 (0.020) | |

| −0.018 (0.115) | −0.262* (0.145) | |

| −0.009*** (0.003) | 0.002* (0.008) | |

| 0.029 (0.029) | 0.017 (0.027) | |

| 0.005 (0.017) | 0.009 (0.017) | |

| N | 207 | 204 |

| groups | 23 | 23 |

| N-instr | 21 | 23 |

| AR(1) | 0.038 | 0.015 |

| AR(2) | 0.214 | 0.116 |

| Hansen | 0.552 | 0.649 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. G_health and G_educ are predetermined, GDP growth. Eldy and young population are exogenous, and the remaining covariates are endogenous. Significance level at which the null hypothesis is rejected p < 0.1*; p < 0.05**; p < 0.01***

Fig. 5.

Health and Education spending in emerging countries (Percent of GDP)

Our results contradict those of Sanz (2011) arguing that fiscal adjustments protect functions that have both a social and productive character. Consequently, we confirm that debt sustainability incurred by the government is at the cost of lower allocations devoted the total government budget to education and health sectors. Subsequent work has emphasized the importance of investments in human capital such as expenditures in education and health (Krueger and Lindahl 2001; Baldacci et al. 2004). It is obvious that the exclusion of such key growth determinants can lead to many inefficiencies such as weak competition in the provision of social services (Jafarov and Gunnarsson 2008). Indeed, rationalizing social spending is a crucial step for enhancing the flexibility of fiscal policies and coping with debt shocks.

The second robustness check exercise examines whether our previous results are affected by the IMF forecasted data. In fact, the dataset was chosen based on data availability. Our estimation technique is the system-GMM dynamic panel estimator. This estimator is appropriate for large N and small T (Roodman 2009). Thus, incorporating 6 countries that have undertaken fiscal consolidation between 2014 and 2018 was adopted to avoid biased and inconsistent estimates. To explore the robustness of our baseline results, we restricted the sample period to the 2009–2014 by excluding all the IMF forecasted data. Estimations reported in Tables 10, 11, 12, 13 and 14 show that the effect of fiscal consolidation on social expenditure (health and education) along with the current account, remain robust and relevant after removing the forecasted data. In particular, fiscal consolidation significantly decreases social expenditure and increases current account for the 2009–2014 period, corroborating our previous results based on IMF data incorporating IMF forecasts.

Table 10.

The effect of fiscal consolidation on total and social expenditure (POLS and FE) for the 2009–2014 period

| POLS | FE | |||

|---|---|---|---|---|

| (1) | (2) | (1) | (2) | |

| Total expenditure | Social expenditure | Total expenditure | Social expenditure | |

|

0.986*** (0.027) |

0.916*** (0.047) |

0.401*** (0.097) |

0.649* (0.257) |

|

|

−0.572*** (0.166) |

−0.225*** (0.077) |

−0.479*** (0.079) |

−0.455*** (0.173) |

|

|

−0.006 (0.024) |

−0.005 (0.011) |

−0.072 (0.077) |

−0.038 (0.083) |

|

|

−0.021 (0.295) |

−0.097 (0.138) |

−1.424* (0.867) |

−2.087** (0.923) |

|

|

−0.001 (0.010) |

−0.005 (0.004) |

−0.028 (0.043) |

0.001 (0.045) |

|

|

−0.016 (0.071) |

−0.010 (0.033) |

0.755 (0.685) |

−0.010 (0.702) |

|

| 0.002 | −0.009 | 0.207 | −0.007 | |

| (0.052) | (0.021) | (0.433) | (0.074) | |

| Constant |

0.823 (2.370) |

1.565* (0.902) |

12.111** (16.111) |

38.054** (15.518) |

| N | 110 | 110 | 114 | 114 |

| R-squared | 0.963 | 0.865 | 0.654 | 0.402 |

| Groups | 23 | 23 | 23 | 23 |

| Hausman | 37.04** | 35.18*** |

Robust standard errors are in parentheses Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***. The dependent variable is total government spending in model (1) and social spending in model (2)

Table 11.

The effect of fiscal consolidation on total expenditure for the 2009–2014 period

| Dynamic Panel Estimation SGMM | ||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

|

0.710*** (0.230) |

0.768*** (0.377) |

0.618*** (0.147) |

0.616*** (0.132) |

0.689*** (0.088) |

0.637*** (0.129) |

|

|

−0.546** (0.109) |

−0.777*** (0.202) |

−0.703** (0.174) |

−0.816*** (0.175) |

−0.847*** (0.199) |

−0.694*** (0.193) |

|

|

−3.082 (2.033) |

−0.696 (1.002) |

−0.321 (0.283) |

−0.617* (0.344) |

−0.376 (0.297) |

||

|

0.047** (0.023) |

0.0381 (0.017) |

−0.023 (0.045) |

−0.066** (0.027) |

|||

|

−0.095*** (0.036) |

−0.345*** (0.120) |

−0.071** (0.033) |

||||

|

0.388*** (0.139) |

−0.494*** (0.189) |

|||||

|

−0.554*** (0.195) |

||||||

| N | 115 | 115 | 115 | 114 | 114 | 114 |

| Groups | 23 | 23 | 23 | 23 | 23 | 23 |

| N-instr | 7 | 7 | 10 | 13 | 15 | 13 |

| AR(1) | 0.069 | 0.061 | 0.055 | 0.002 | 0.011 | 0.008 |

| AR(2) | 0.124 | 0.220 | 0.270 | 0.290 | 0.436 | 0.320 |

| Hansen | 0.311 | 0.568 | 0.650 | 0.479 | 0.391 | 0.368 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. Starting from the most parsimonious specification (column 1), we progressively introduce GDP growth, corruption, public debt, eldy and young population in columns (2)–(6). Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***

Table 12.

The effect of fiscal consolidation on social expenditure for the 2009–2014 period

| Dynamic Panel Estimation SGMM | ||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

|

0.789*** (0.173) |

0.732** (0.188) |

0.797*** (0.115) |

0.384*** (0.128) |

0.395*** (0.133) |

0.648*** (0.238) |

|

|

−0.456** (0.187) |

−0.221*** (0.072) |

−0.301** (0.122) |

−0.214** (0.086) |

−0.210** (0.086) |

−0.222*** (0.073) |

|

|

−1.527* (0.886) |

−1.728* (1.558) |

−0.910** (0.412) |

−1.177** (0.504) |

−0.722* (0.407) |

||

|

0.077* (0.115) |

0.025** (0.012) |

−0.001 (0.019) |

−0.012 (0.021) |

|||

|

−0.011 (0.011) |

−0.049** (0.025) |

−0.038* (0.021) |

||||

|

0.128** (0.060) |

0.081 (0.105) |

|||||

|

−0.007 (0.074) |

||||||

| N | 207 | 115 | 114 | 114 | 114 | 114 |

| Groups | 23 | 23 | 23 | 23 | 23 | 23 |

| N-instr | 7 | 13 | 14 | 21 | 21 | 20 |

| AR(1) | 0.002 | 0.003 | 0.003 | 0.001 | 0.001 | 0.002 |

| AR(2) | 0.337 | 0.370 | 0.268 | 0.386 | 0.414 | 0.361 |

| Hansen | 0.559 | 0.881 | 0.200 | 0.484 | 0.360 | 0.744 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. Starting from the most parsimonious specification (column 1), we progressively introduce GDP growth, corruption, public debt, eldy and young population in columns (2)–(6). Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***

Table 13.

The effect of fiscal consolidation on current account for the 2009–2014 period

| Dynamic Panel Estimation SGMM | ||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

|

0.603*** (0.188) |

0.509*** (0.101) |

0.951*** (0.166) |

0.735*** (0.133) |

0.720*** (0.103) |

0.715*** (0.128) |

|

|

0.858** (0.365) |

0.288* (0.173) |

0.312** (0.144) |

0.377* (0.221) |

0.380* (0.214) |

0.377** (0.207) |

|

|

2.253*** (0.835) |

−0.326 (0.746) |

4.323** (1.688) |

0.410 (0.923) |

−0.242 (0.324) |

||

|

0.081* (0.042) |

0.143*** (0.040) |

0.032** (0.016) |

0.068** (0.033) |

|||

|

0.174** (0.080) |

0.225** (0.093) |

0.146** (0.080) |

||||

|

−0.126 (0.114) |

−0.152 (0.092) |

|||||

|

−0.133** (0.054) |

||||||

| N | 115 | 115 | 115 | 114 | 114 | 114 |

| groups | 23 | 23 | 23 | 23 | 23 | 23 |

| N-instr | 9 | 16 | 16 | 12 | 22 | 14 |

| AR(1) | 0.079 | 0.223 | 0.047 | 0.015 | 0.084 | 0.025 |

| AR(2) | 0.469 | 0.521 | 0.662 | 0.665 | 0.689 | 0.621 |

| Hansen | 0.234 | 0.201 | 0.145 | 0.542 | 0.467 | 0.365 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. Starting from the most parsimonious specification (column 1), we progressively introduce GDP growth, corruption, public debt, eldy and young population in columns (2)–(6). Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***

Table 14.

The effect of fiscal consolidations on social expenditure components for the 2009–2014 period

| (1) G_health |

(2) G_educ |

|

|---|---|---|

| 0.675*** (0.131) | 0.651* (0.376) | |

| −0.096*** (0.019) | −0.252*** (0.083) | |

| −0.052** (0.023) | −0.006 (0.053) | |

| −0.092 (0.287) | −0.667* (0.342) | |

| −0.009 (0.007) | −0.001 (0.011) | |

| 0.036 (0.051) | 0.001 (0.979) | |

| −0.012 (0.029) | −0.009 (0.021) | |

| N | 114 | 112 |

| groups | 23 | 23 |

| N-instr | 20 | 18 |

| AR(1) | 0.025 | 0.109 |

| AR(2) | 0.519 | 0.834 |

| Hansen | 0.801 | 0.775 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. G_health and G_educ are predetermined, GDP growth. Eldy and young population are exogenous, and the remaining covariates are endogenous. Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***

As a final and complementary exercise, we account for the heterogeneity that could be present in the sample of countries used in this analysis. Thus, we figured out that excluding 5 countries (Chile, Croatia, Hungary, Lithuania and Poland) which correspond to high-income countries allows us to come out with a more homogenous group that includes 18 middle-income countries.4 Tables 15, 16, 17, 18 and 19 in the Appendix report the robustness of our baseline results to the exclusion of high-income countries. Estimates clearly indicate that coefficients of the fiscal adjustment are statistically significant and relevant for all different specifications. These results confirm again the negative effect of fiscal consolidations on the social expenditure and additionally the positive effect on the current account even after excluding high-income countries from our sample.

Table 15.

The effect of fiscal consolidation on total and social expenditure (POLS and FE) for middle-income countries

| POLS | FE | |||

|---|---|---|---|---|

| (1) | (2) | (1) | (2) | |

| Total expenditure | Social expenditure | Total expenditure | Social expenditure | |

|

0.975*** (0.023) |

0.962*** (0.028) |

0.481*** (0.069) |

0.595*** (0.073) |

|

|

−0.451*** (0.135) |

−0.163*** (0.048) |

−0.452*** (0.127) |

−0.143*** (0.051) |

|

|

−0.012 (0.020) |

−0.003 (0.007) |

−0.053 (0.059) |

−0.007 (0.024) |

|

|

−0.037 (0.440) |

−0.306 (0.161) |

−1.314** (0.625) |

−0.489** (0.247) |

|

|

−0.012 (0.009) |

−0.006* (0.003) |

−0.069*** (0.023) |

−0.012 (0.009) |

|

|

−0.021 (0.071) |

−0.002 (0.019) |

0.475 (0.407) |

0.143 (0.163) |

|

| −0.005 | 0.010 | 0.338* | 0.051 | |

| (0.046) | (0.021) | (0.203) | (0.081) | |

| constant |

1.558 (1.804) |

0.990* (0.545) |

8.711 (7.525) |

2.151 (2.968) |

| N | 144 | 144 | 144 | 144 |

| R-squared | 0.946 | 0.904 | 0.799 | 0.766 |

| Groups | 18 | 18 | 18 | 18 |

| Hausman | 14.86** | 17.28 *** |

Robust standard errors are in parentheses Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***. The dependent variable is total government spending in model (1) and social spending in model (2)

Table 16.

The effect of fiscal consolidation on total expenditure for middle-income countries

| Dynamic Panel Estimation SGMM | ||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

|

0.592* (0.350) |

0.599** (0.281) |

0.736** (0.297) |

0.997*** (0.090) |

0.682** (0.318) |

0.637*** (0.129) |

|

|

−0.449*** (0.155) |

−0.561** (0.210) |

−0.689*** (0.097) |

−0.738*** (0.166) |

−0.664*** (0.119) |

−0.694*** (0.193) |

|

|

−0.176 (0.219) |

0.095 (1.556) |

0.254 (1.103) |

−1.095 (1.551) |

−0.376 (0.297) |

||

|

0.0* (0.023) |

−0.054* (0.032) |

−0.036 (0.031) |

−0.066** (0.027) |

|||

|

−0.172** (0.064) |

−0.328* (0.160) |

−0.071** (0.033) |

||||

|

0.169 (0.139) |

−0.494*** (0.189) |

|||||

|

−0.554*** (0.195) |

||||||

| N | 162 | 161 | 115 | 144 | 144 | 114 |

| groups | 18 | 18 | 23 | 18 | 18 | 23 |

| N-instr | 7 | 9 | 10 | 14 | 14 | 13 |

| AR(1) | 0.065 | 0.037 | 0.055 | 0.032 | 0.091 | 0.008 |

| AR(2) | 0.130 | 0.123 | 0.270 | 0.153 | 0.140 | 0.320 |

| Hansen | 0.303 | 0.529 | 0.650 | 0.144 | 0.996 | 0.368 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. Starting from the most parsimonious specification (column 1), we progressively introduce GDP growth, corruption, public debt, eldy and young population in columns (2)–(6). Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***

Table 17.

The effect of fiscal consolidation on social expenditure for middle-income countries

| Dynamic Panel Estimation SGMM | ||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

|

0.757*** (0.231) |

0.648*** (0.195) |

0.656*** (0.183) |

0.799*** (0.195) |

0.791*** (0.137) |

0.789*** (0.135) |

|

|

−0.104** (0.040) |

−0.129*** (0.027) |

−0.140** (0.028) |

−0.211*** (0.060) |

−0.176*** (0.054) |

−0.176*** (0.054) |

|

|

−1.053*** (0.359) |

−1.043*** (0.325) |

−0.016 (0.322) |

−0.662** (0.284) |

−0.646** (0.270) |

||

|

0.006 (0.009) |

−0.016* (0.008) |

−0.007 (0.007) |

−0.006 (0.007) |

|||

|

−0.107* (0.055) |

−0.037* (0.019) |

−0.039* (0.022) |

||||

|

0.032 (0.028) |

0.044 (0.045) |

|||||

|

0.011 (0.035) |

||||||

| N | 162 | 115 | 114 | 114 | 114 | 114 |

| groups | 18 | 18 | 18 | 18 | 18 | 18 |

| N-instr | 9 | 13 | 17 | 12 | 16 | 17 |

| AR(1) | 0.008 | 0.003 | 0.017 | 0.055 | 0.032 | 0.031 |

| AR(2) | 0.104 | 0.370 | 0.432 | 0.502 | 0.423 | 0.423 |

| Hansen | 0.888 | 0.881 | 0.601 | 0.380 | 0.373 | 0.382 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. Starting from the most parsimonious specification (column 1), we progressively introduce GDP growth, corruption, public debt, eldy and young population in columns (2)–(6). Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***

Table 18.

The effect of fiscal consolidation on current account for middle-income countries

| Dynamic Panel Estimation SGMM | ||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

|

1.216*** (0.299) |

1.073*** (0.119) |

0.996*** (0.176) |

0.865*** (0.181) |

0.720*** (0.103) |

0.851*** (0.165) |

|

|

0.865** (0.376) |

0.839** (0.405) |

0.823** (0.381) |

0.915** (0.361) |

0.900** (0.372) |

0.895** (0.372) |

|

|

−0.588 (0.205) |

−0.976 (0.798) |

−1.106* (0.554) |

−1.185* (0.609) |

−0.853 (0.511) |

||

|

0.056 (0.058) |

0.025 (0.027) |

0.027 (0.032) |

0.068** (0.033) |

|||

|

0.145** (0.067) |

0.160* (0.092) |

0.146* (0.075) |

||||

|

−0.088 (0.137) |

−0.142 (0.195) |

|||||

|

−0.079 (0.097) |

||||||

| N | 162 | 145 | 145 | 144 | 144 | 144 |

| groups | 18 | 18 | 18 | 18 | 18 | 18 |

| N-instr | 6 | 11 | 11 | 13 | 14 | 15 |

| AR(1) | 0.049 | 0.028 | 0.043 | 0.063 | 0.064 | 0.057 |

| AR(2) | 0.486 | 0.468 | 0.410 | 0.418 | 0.424 | 0.425 |

| Hansen | 0.242 | 0.102 | 0.333 | 0.479 | 0.486 | 0.512 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. Starting from the most parsimonious specification (column 1), we progressively introduce GDP growth, corruption, public debt, eldy and young population in columns (2)–(6). Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***

Table 19.

The effect of fiscal consolidations on social expenditure components for middle-income countries

| (1) G_health |

(2) G_educ |

|

|---|---|---|

| 0.796*** (0.073) | 0.649*** (0.212) | |

| −0.045** (0.025) | −0.128*** (0.039) | |

| −0.007 (0.015) | −0.049** (0.019) | |

| −0.316** (0.151) | −0.333 (0.252) | |

| 0.001 (0.004) | −0.007 (0.262) | |

| 0.003 (0.029) | 0.066* (0.036) | |

| −0.007 (0.025) | 0.019 (0.026) | |

| N | 144 | 143 |

| groups | 18 | 18 |

| N-instr | 18 | 18 |

| AR(1) | 0.055 | 0101 |

| AR(2) | 0.467 | 0.490 |

| Hansen | 0.439 | 0.273 |

Robust standard errors are in parentheses. Regressions are based on the Blundell-Bond estimator. G_health and G_educ are predetermined, GDP growth. Eldy and young population are exogenous, and the remaining covariates are endogenous. Significance level at which the null hypothesis is rejected: p < 0.1*; p < 0.05**; p < 0.01***

Conclusion

Although the effects of economic reforms on social expenditures and current account is a subject of interest for politicians, social activists and the public at large, few studies have been conducted to examine this issue. Given the importance of the social sector in emerging and middle-income countries’ context, it is very relevant and useful to examine the impact of fiscal consolidations on social sector expenditures. In this paper, we investigate the effect of fiscal adjustment on social expenditure by performing System-GMM estimations on a sample of 23 countries during the 2009–2018 period.

We first quest whether the budgetary allocations to the social sector as a whole have been affected during fiscal consolidation episodes. This analysis has very strong policy implications. We demonstrate that higher priority is assigned to education and health care budgetary allocation cuts. In particular, we have found that, in response to increasing debt paths, emerging and middle-income countries tend to favor social expenditures cuts during fiscal consolidation episodes. This finding reveals that governments decrease social spending in order to address the overstaffing problem in public sector. A further argument is that education and health care spending are proven to be more flexible compared to the rest of public spending categories. We also find that fiscal consolidation leads to a rise in the external current account balance, in line with a strong “twin deficits” link.

While there are benefits to having a relatively large current account, caution should be at work particularly during fiscal consolidations. Our findings suggest rationalizing social spending. Consequently, government spending on health and education could be reduced without undue sacrifices in the quality of these services. If these qualifications are kept in mind, it seems useful to announce credible plans and take more convenient measures. In fact, keeping budget execution under control requires effective management system. Governments should devote the country’s revenue to necessary and economically productive projects (Omrane and Gabsi 2019). This behavior enhances the likelihood of successful fiscal adjustment. Besides, improving education and health care sectors usually creates better levels of socio-economic development. Thus, decent work is fundamental to ensure effective education and health care systems, to achieve public debt sustainability and long-run growth at the same time. Policymakers should, however, recognize that the role of human capital can be appropriately evaluated at the macroeconomic level through the reallocation of social expenditures. Taking the efficiency of public expenditures into consideration, there are still strong opportunities to avoid the transitional social costs during fiscal consolidation episodes. This calls for good governance, an efficient administration and effective delivery structures.

Acknowledgments

The authors would like to thank the Editor in Chief Dr. Nauro F Campos and the four anonymous referees for their comments that helped to improve considerably this paper.

Appendix

See Tables 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18 and 19

Footnotes

Cyclically adjusted primary balance during the consolidation episode is the size of the fiscal consolidation, expressed as a share of potential GDP.

Projections for the CAPB are provided through 2019 in the WEO database (April 2014).

The empirical problem in applying OLS and FE models is the presence of omitted variable bias and correlation between the lagged dependent variable and the error term. It is not also efficient to use the Within Groups estimator because it does not eliminate dynamic panel bias (Nickell 1981; Judson and Owen 1999; Bond 2002).

Argentina, Bulgaria, Colombia, Dominican Rep, Ecuador, Egypt, India, Jordan, Malaysia, Mexico, Romania, Algeria, Morocco, Peru, Philippines, Russian Fed, South Africa and Ukraine.

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Contributor Information

Amine Lahiani, Email: amine.lahiani@univ-orleans.fr.