Abstract

Objective

To observe trends in practice consolidation within otolaryngology by analyzing changes in size and geographic distribution of practices within the United States from 2014 to 2021.

Study Design

Retrospective analysis based on the Physician Compare National Database from the US Centers for Medicare and Medicaid Services.

Setting

United States.

Methods

Annual files from the Physician Compare National Database between 2014 and 2021 were filtered for all providers that listed “otolaryngology” as their primary specialty. Organization affiliations were sorted by size of practice and categorized into quantiles (1 or 2 providers, 3-9, 10-24, 25-49, and ≥50). Both the number of practices and the number of surgeons within a practice were collected annually for each quantile. Providers were also stratified geographically within the 9 US Census Bureau divisions. Chi-square analysis was conducted to test significance for the change in surgeon and practice distributions between 2014 and 2021.

Results

Over the study period, the number of active otolaryngology providers increased from 7763 to 9150, while the number of practices fell from 3584 to 3152 in that time span. Practices with just 1 or 2 otolaryngology providers accounted for 80.2% of all practices in 2014 and fell to 73.1% in 2021. Similar trends were observed at the individual provider level. Regional analysis revealed that New England had the largest percentage decrease in otolaryngologists employed by practices of 1 or 2 active providers at 45.7% and the Mountain region had the lowest percentage decrease at 17.4%.

Conclusion

The otolaryngology practice marketplace has demonstrated a global trend toward practice consolidation.

Keywords: practice consolidation, health care economics, health care market, otolaryngology

Recent changes to the health care system at the federal level have affected the relationship between hospitals and physicians across the country with a shift in the focus from pay for performance to population health.1-3 The Patient Protection and Affordability Act and the Children’s Health Insurance Program have placed an emphasis on increasing quality of care while reducing health care costs. 4 These policies constrain the health markets, which govern the behavior of physician practices, with some variation at the state level due to differences in local legislation.3,5 Given these constraints, smaller physician practices are incentivized to consolidate with larger health care corporations to maximize collective bargaining with insurance companies, decrease overhead by creating economies of scale, and shift a portion of the malpractice risk and cost to a system. 6 A senior government official at the time stated that this legislation will “lead to vertical organization of providers and accelerate physician employment by hospitals and aggregation into larger physician groups.” 7 According to several studies, there has been an observable increase in the numbers of medical groups owned by hospitals in the United States,8,9 in addition to trends toward other forms of integration in recent years, such as financial integration between providers and hospitals and mergers of smaller practices. 10 To ensure the future success of physician practices in attaining quality improvement measures and cost-effectiveness in the setting of changing market constraints, ongoing analysis of market trends is paramount.

Practice consolidation is a trending topic in the medical literature in general and within various subspecialties.11-13 However, there is a paucity of research regarding the specific effect of this phenomenon in otolaryngology, which historically has a strong foundation in the private practice model composed of smaller physician groups. 14 Prior analysis of the otolaryngology workforce has demonstrated that nearly one-third of practicing otolaryngologists participated in some form of solo practice in 2001. 15 Some argue that smaller, often private, practices in otolaryngology are specifically equipped to adapt to the constraints of an ever-changing health care market, as these practices often offer same-day services that improve efficiency, reduce costs, and improve patient service and satisfaction.14,16 Yet, the survival of small practices within otolaryngology may be increasingly threatened by pressures to join larger organizations. 16 Therefore, the aim of this study was to analyze the quarterly trends in size and geographic distribution of otolaryngology practices within the United States from 2014 to 2021 to observe current trends in practice consolidation.

Methods

The study was exempted from the University Hospitals Cleveland Medical Center’s Institutional Review Board (20210811) as all of the data utilized are publicly available. The Centers for Medicare and Medicaid Services (CMS) publishes bimonthly updates of a Physician Compare National Downloadable File. This file provides a list of all active providers registered within the CMS, with additional demographic details such as primary and secondary specialties, current organization affiliations, and associated geographic locations. This database has been used for other specialties and has been considered representative of the current state of the physician workforce across other literature.12,13

Annual files between 2014 and 2021 were accessed and filtered for all providers that listed “otolaryngology” as their primary specialty. Providers were aggregated by their organizational affiliation. For providers with >1 organizational affiliation, the duplicates were removed, and the organization with the fewest members for each provider was selected, in accordance with previous literature. Additionally, providers with no organization listed were deemed to operate within a single-provider practice model.12,13

Organization affiliations were sorted by size of practice and categorized into quantiles in accordance with previous literature (1 or 2 providers, 3-9, 10-24, 25-49, and ≥50). 13 Both the number of practices and the number of surgeons within a practice were collected for each quantile. This was conducted each year for a temporal trend analysis. Providers were also stratified geographically within the 9 US Census Bureau divisions. Chi-square analysis was conducted with SPSS version 27.0 (IBM) to test significance for the change in surgeon and practice distributions between March 2014 and April 2021, nationally and within each geographic region. P < .05 was determined to be statistically significant.

Results

Over our study period from 2014 to 2021, the number of active otolaryngology providers increased from 7763 to 9150. These providers were distributed across 3584 practices in 2014 and 3152 practices in 2021. Of the current providers, 18.9% are female. The South was the region with the greatest number of individual providers (3287) and unique practices (1129).

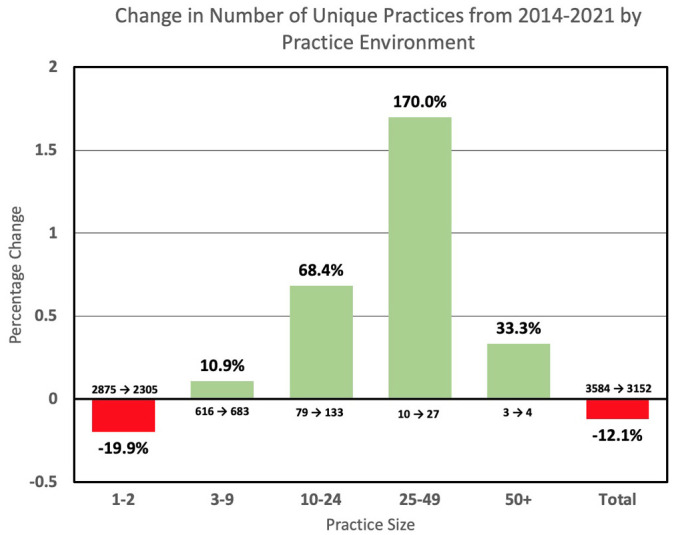

The number of practices consisting of 1 or 2 active otolaryngologists decreased from 2876 to 2305 (–19.9%; Figure 1 ). Yet, the number of practices consisting of 3 to 9 active otolaryngologists increased from 616 to 683 (10.9%); 10 to 24 active otolaryngologists, from 79 to 133 (68.4%); 25 to 49 active otolaryngologists, from 10 to 27 (170.0%); and ≥50 active otolaryngologists, from 3 to 4 (33.3%). Meanwhile, there was a decline in the number of unique otolaryngology practices in total from 3584 to 3152 (–12.1%). One or 2 provider practices accounted for 80.2% of practices in 2014 and just 73.1% of practices in 2021. In contrast, the market share of larger practices all significantly increased during the study period.

Figure 1.

Percentage change in the number of unique otolaryngology practices by practice size from 2014 to 2021 (absolute numbers labeled above each bar).

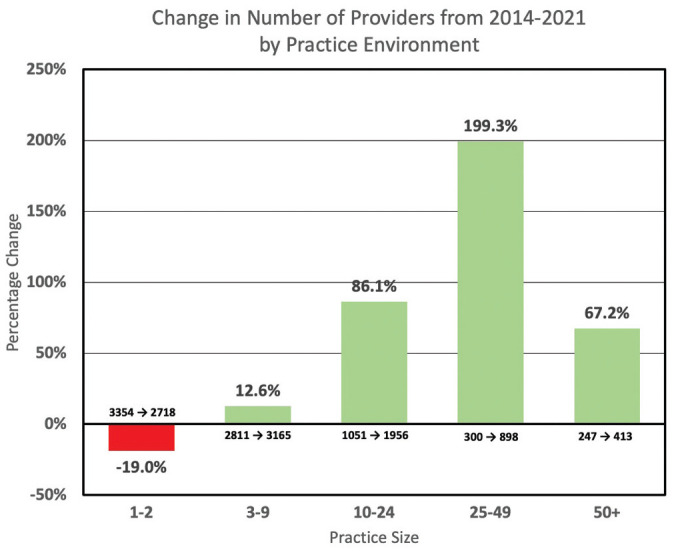

Very similar trends were observed at the individual provider level (P < .001). The number of otolaryngologists working within a 1- or 2-provider practice decreased from 3354 to 2718 (–19.0%) within the study period ( Figure 2 ). Yet, the number of otolaryngologists employed within practices consisting of 3 to 9 active members increased from 2811 to 3165 (12.6%); 10 to 24 active members, from 1051 to 1956 (86.1%); 25 to 49 active members, from 300 to 898 (199.3%); and ≥50 active members, from 247 to 413 (67.2%).

Figure 2.

Percentage change in the number of otolaryngologists within varying practice sizes from 2014 to 2021 (absolute numbers labeled above each bar).

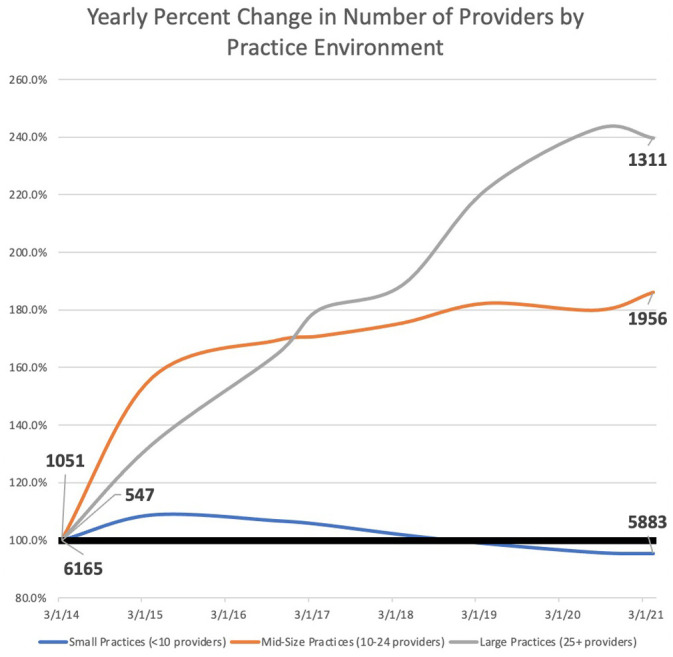

While the number of otolaryngologists employed within practices consisting of 1 or 2 active members has steadily declined since 2015, the numbers of otolaryngologists within midsized and larger practices have skyrocketed over the last decade ( Figure 3 ).

Figure 3.

Percentage change in the number of otolaryngologists within various practice sizes annually from 2014 to 2021 (absolute numbers labeled at the beginning and end of each line).

Our analysis observed similar regional trends toward practice consolidation across the country. Analysis of the 4 US Census Bureau regions (Northeast, Midwest, South, and West) was performed initially. Across the Northeast, there was a 38.0% decrease in the percentage of otolaryngologists employed by practices with 1 or 2 active providers. In contrast, the West had only a 26.2% decrease. Further analysis by US Census divisions revealed that New England specifically had the largest percentage decrease in otolaryngologists employed by practices of 1 or 2 active providers at 45.7% and the Mountain region had the lowest percentage decrease at 17.4% ( Figure 4 ). The average decrease in percentage of small practice providers from 2014 to 2021 across 9 divisions was 31.6% (P < .001). The regions with the greatest observed decrease in small practice otolaryngologists were New England, the Mid-Atlantic, and the South Atlantic.

Figure 4.

Percentage change in the percentage of providers within practices consisting of 1 or 2 active members by US Census Bureau division since 2014.

Discussion

A trend toward practice consolidation has been demonstrated in several medical specialties across the United States within the last decade.12,13,17 However, trends in practice consolidation within the field of otolaryngology have not previously been described. We found a significant trend toward consolidation within the otolaryngology workforce between 2014 and 2021 (P < .001). This trend was present at the practice and individual levels. Our analysis also provided interesting insights into the regional trends in practice consolidation. While trends of practice consolidation were consistent nationally, certain regions seemed to be affected more than others.

Studies similar to ours have shown that these findings are not unique to otolaryngology. For example, physicians in specialties such as radiology and neurosurgery are also transitioning from smaller practice environments to larger health care organizations.12,13 In addition, similar regional trends toward practice consolidation have been found, with the northeast commonly being identified as one of the top regions with the highest concentration of physicians at large institutions. 13

Whether these trends represent a shift in provider preference for employment at a large academic institution over employment within a small private practice in the field of otolaryngology is difficult to assess. It has been a commitment of the American Academy of Otolaryngology–Head and Neck Surgery to preserve the integrity of the small practice setting within our specialty. 18 Given the high prevalence of in-office procedures and increasing reliance on advanced practice providers, otolaryngology has the potential to be particularly appealing for medical students seeking careers that allow for independence and personalization, with less dependence on academic environments, research, and administrative responsibilities.16,19

Conversely, medical students may appreciate the flexibility to work within a larger organization, whether academic or private, which offers a number of short- and long-term career advantages, given an individual’s personal and professional priorities. For example, with the increasing prevalence of high research productivity in academic otolaryngology, new providers seeking careers with clinical and research responsibilities can find ample resources and funding at larger health care institutions. 20 Similarly, providers with interests in teaching residents and medical students are likely to find these opportunities within larger organizations affiliated with academic centers. Finally, alternative explanations for the decline in small practices could be the increased bureaucratic costs of running a smaller private practice as well as the appeal of a decreased call burden that is often offered at larger academic institutions.

The broad scope of practice environments within the specialty appears to be rapidly dwindling. Shifting health care policy within the United States has stunted the sustainability of smaller practices. For example, the administrative overhead associated with purchasing real estate and equipment, optimizing billing practices, and managing other day-to-day business operations within a health care practice has the potential to overwhelm providers in smaller or solo practices. Furthermore, coupled with the financial incentive, there is an increased regulatory burden associated with recent legislation that includes mandatory outcome reporting, which has similarly overwhelmed small practices. 7 Accordingly, newly minted physicians are beginning to prioritize lifestyle considerations and the avoidance of this administrative burden over the autonomy of practice ownership. 8 Such market effects are reducing the variability in career options in otolaryngology that attracted a number of these providers into the specialty in the first place.

There are potential benefits to large-scale acquisition of smaller practices. Adherence to population-based care standards and participation in value-based reimbursement programs are more likely within a larger health care organization, where integration of medical records and access to resources are commonplace. In addition, coordination of patient care and quality improvement is more likely to thrive within larger organizations, where standardized care pathways are more heavily implemented. 21 Small private practices may be subject to different financial pressures than larger practices, potentially due to fewer economies of scale, reduced negotiating power in the marketplace with insurers, or a lack of eligibility for reimbursement relating to provision of care for underinsured or uninsured patients. These differences could have ramifications for patient access to care, as small practices may be compelled to favor patients based on profitability to ensure sustainability of their practices in the setting of an evolving health care landscape. 22

There is evidence to suggest that practice consolidation, especially at a large scale, does not necessarily improve the cost of care for the patient or improve the quality or access to care.8,11 Specifically, some have suggested that larger health care organizations may prioritize profitability and other institutional goals over improving quality of care. 12 Most notably, given the greater market power of larger organizations, larger practices may be more able to negotiate higher compensation, ultimately raising the cost of care for the consumer.23-25 Yet, smaller provider practices may yield tangible cost benefits for their patients. Ho and Aloia found that high surgeon procedural volume, rather than hospital group procedural volume, correlates more strongly with lower surgical and treatment costs, reflecting the value of provider-specific referral programs. In other words, providers that prioritize clinical productivity above extraclinical endeavors, such as those in small practice environments, may yield higher-quality outcomes for their patients. 26 Finally, large-scale practices, in a world with increased consolidation, may trend toward urbanization and ultimately widen health care disparities by limiting access to care in rural areas.12,27

Given these concerns, further research is necessary to assess the influence of practice consolidation on health care costs, access, and quality of care in the field of otolaryngology. A continued trend toward large-scale practice consolidation could lead to the demise of the solo provider practice in otolaryngology, and given the potential implications on the delivery of quality health care services, the American Academy of Otolaryngology–Head and Neck Surgery and other national specialty societies should monitor these trends closely.

The present study had several limitations. First, the data that we present were obtained from the Physician Compare National Database, which captures only active physicians who bill to CMS. Therefore, the results in this study may not represent the true extent of practice consolidation in the field of otolaryngology in the United States, particularly regarding the subspecialty of pediatric otolaryngology due to its relative lack of representation among the Medicare population. This data set also includes files dating back to 2014, which unfortunately limits the scope of our consolidation analysis. In addition, the data source does not provide any details pertaining to the prevalence of physician providers of other specialties and advanced practice providers within each practice, such as audiologists and speech-language pathologists, which are commonplace in otolaryngology practices. 28 Given the recent increase in the prevalence of advanced practice providers in otolaryngology practices, particularly nurse practitioners and physician assistants, the trend in consolidation of services may be even more pronounced than what our study suggests, as the overall volume of care being delivered per site is consolidated.29,30 Last, it is important to note that our results and analysis compare the trends of size of practice, and in this way, we are unable to conclude anything on the trends relating to private vs academic practices. While many small practices are private ventures, further research is needed to assess whether these changes are being similarly seen with regard to private practice consolidation.

Conclusion

From 2014 to 2021, the otolaryngology workforce within the United States has demonstrated a widespread trend toward practice consolidation, with a considerable decline in the number of single-provider practices. Further research is necessary to explore the impact of this trend on the delivery of quality patient care, access to care, and costs incurred by the patient.

Author Contributions

Humzah A. Quereshy, conception or design of the work, data collection, data analysis and/or interpretation, drafting the article, final approval of the version to be published; Brooke A. Quinton, data collection, data analysis and/or interpretation, drafting the article, final approval of the version to be published; Jeremy S. Ruthberg, data collection, data analysis and/or interpretation, drafting the article, final approval of the version to be published; Nicole C. Maronian, final approval of the version to be published, critical revision of the article; Todd D. Otteson, final approval of the version to be published, critical revision of the article.

Disclosures

Competing interests: None.

Sponsorships: None.

Funding source: None.

Footnotes

ORCID iDs: Humzah A. Quereshy  https://orcid.org/0000-0001-7849-4774

https://orcid.org/0000-0001-7849-4774

Brooke A. Quinton

https://orcid.org/0000-0003-4524-612X

References

- 1. Kim DH, Duco B, Wolterman D, et al. A review and survey of neurosurgeon-hospital relationships: evolution and options. Neurosurgery. 2017;80(4S):S10-S18. [DOI] [PubMed] [Google Scholar]

- 2. Kim DH, Forcht-Dagi T, Bean JR. Neurosurgical practice in transition: a review. Neurosurgery. 2017;80(4):S4-S9. [DOI] [PubMed] [Google Scholar]

- 3. Caughman S, Jordan J, Johnston J, et al. Health Reform and the Decline of Private Physician Practice. Physicians Foundation; 2010. [Google Scholar]

- 4. Manchikanti L, Helm S, II, Benyamin RM, et al. A critical analysis of Obamacare: affordable care or insurance for many and coverage for few? Pain Phys. 2017;20:111-138. [PubMed] [Google Scholar]

- 5. Spetzler RF, Kick SA. The status of neurosurgery in the United States: 2010 and beyond. World Neurosurg. 2010;74(1):32-40. [DOI] [PubMed] [Google Scholar]

- 6. O’Hanlon CE, Whaley CM, Freund D. Medical practice consolidation and physician shared patient network size, strength, and stability. MedCare. 2019;57:680-687. [DOI] [PubMed] [Google Scholar]

- 7. Wilson R. Why private practice is dying. Forbes Magazine. Published September 2016. Accessed April 23, 2021. http://www.forbes.com/sites/realspin/2016/09/07/why-private-practice-is-dying/?sh=205a096d27c8

- 8. Kirchhoff SM. Physician practices: background, organization, and market consolidation. Published 2013. Accessed April 26, 2021. https://www.fas.org/sgp/crs/misc/R42880.pdf

- 9. Payton B. Physician-hospital relationships: from historical failures to successful “new kids on the block.” J Med Pract Manage. 2012;27(6):359-364. [PubMed] [Google Scholar]

- 10. Neprash HT, Chernew ME, Hicks AL, et al. Association of financial integration between physicians and hospitals with commercial health care prices. JAMA Intern Med. 2015;175(12):1932-1939. [DOI] [PubMed] [Google Scholar]

- 11. Muhlestein DB, Smith NJ. Physician consolidation: rapid movement from small to large group practices, 2013-15. Health Aff (Millwood). 2016;35:1638-1642. [DOI] [PubMed] [Google Scholar]

- 12. Rosenkrantz AB, Fleishon HB, Silva E, III, et al. Radiology practice consolidation: fewer but bigger groups over time. J Am Coll Radiol. 2020;17:340-348. [DOI] [PubMed] [Google Scholar]

- 13. Singh R, Richter KR, Pollock JR, et al. Trends in neurosurgical practice size: increased consolidation 2014-2019. World Neurosurg. 2021;149:e714-e720. [DOI] [PubMed] [Google Scholar]

- 14. Brown E. Private practice otolaryngology 2018. American Academy of Otolaryngology–Head and Neck Surgery. Published August 2018. Accessed April 23, 2021. https://bulletin.entnet.org/home/article/21247363/private-practice-otolaryngology-2018 [Google Scholar]

- 15. Hughes CA, McMenamin P, Mehta V, et al. Otolaryngology workforce analysis. Laryngoscope. 2016;126(suppl 9):S5-S11. [DOI] [PubMed] [Google Scholar]

- 16. Setzen G. Practice in an era of healthcare disruption. American Academy of Otolaryngology–Head and Neck Surgery. Published June 2018. Accessed April 23, 2021. https://bulletin.entnet.org/home/article/21247281/practice-in-an-era-of-healthcare-disruption [Google Scholar]

- 17. Konda S, Francis J, Motaparthi K, et al. Future considerations for clinical dermatology in the setting of 21st century American policy reform: corporatization and the rise of private equity in dermatology. J Am Acad Dermatol. 2019;81(1):287-296.e8. [DOI] [PubMed] [Google Scholar]

- 18. Setzen G. Private practice otolaryngology is not a dying concept. American Academy of Otolaryngology–Head and Neck Surgery. Published August 2018. Accessed November 7, 2021. https://bulletin.entnet.org/home/article/21247362/private-practice-otolaryngology-is-not-a-dying-concept [Google Scholar]

- 19. Cohen D. A day in the life of a private practitioner. American Academy of Otolaryngology–Head and Neck Surgery. Published January 2019. Accessed April 23, 2021. https://www.entnet.org/content/day-life-private-practitioner [Google Scholar]

- 20. Thangamathesvaran L, Patel N, Siddiqui SH, et al. The otolaryngology match: a bibliometric analysis of 222 first-year residents. Laryngoscope. 2019;129(7):1561-1566. doi: 10.1002/lary.27460 [DOI] [PubMed] [Google Scholar]

- 21. Jabbour M, Newton AS, Johnson D, et al. Defining barriers and enablers for clinical pathway implementation in complex clinical settings. Implementation Sci. 2018;13(1):139. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 22. Friesner DL, Rosenman R. Do hospitals practice cream skimming? Health Serv Manage Res. 2009;22(1):39-49. doi: 10.1258/hsmr.2008.008003 [DOI] [PubMed] [Google Scholar]

- 23. Baker LC, Bundorf MK, Kessler DP. Vertical integration: hospital ownership of physician practices is associated with higher prices and spending. Health Aff (Millwood). 2014;33(5):756-763. [DOI] [PubMed] [Google Scholar]

- 24. Baker LC, Bundorf MK, Royalty AB, et al. Physician practice competition and prices paid by private insurers for office visits. JAMA. 2014;312(16):1653-1662. [DOI] [PubMed] [Google Scholar]

- 25. Austin DR, Baker LC. Less physician practice competition is associated with higher prices paid for common procedures. Health Aff (Millwood). 2015;34(10):1753-1760. [DOI] [PubMed] [Google Scholar]

- 26. Ho V, Aloia T. Hospital volume, surgeon volume, and patient costs for cancer surgery. Med Care. 2008;46(7):718-725. [DOI] [PubMed] [Google Scholar]

- 27. Urban MJ, Wojcik C, Eggerstedt M, et al. Rural-urban disparities in otolaryngology: the state of Illinois. Laryngoscope. 2021;131(1):E70-E75. [DOI] [PubMed] [Google Scholar]

- 28. Norris B, Harris T, Stringer S. Effective use of physician extenders in an outpatient otolaryngology setting. Laryngoscope. 2011;121(11):2317-2321. [DOI] [PubMed] [Google Scholar]

- 29. Ge M, Kim JH, Smith SS, et al. Advanced practice providers utilization trends in otolaryngology from 2012 to 2017 in the Medicare population. Otolaryngol Head Neck Surg. 2021;165(1):69-75. [DOI] [PubMed] [Google Scholar]

- 30. Patel RA, Torabi SJ, Kasle DA, Pivirotto A, Manes RP. Role and growth of independent Medicare-billing otolaryngologic advanced practice providers. Otolaryngol Head Neck Surg. 2021;165(6):809-815. [DOI] [PubMed] [Google Scholar]